Inland Revenue’s clampdown on the horticultural sector.

Earlier this year Inland Revenue released an issues paper consulting on fringe benefit tax changes. This originated from a 2022 stewardship review of FBT. The issues paper noted it has been 40 years since FBT was introduced and it was therefore opportune to reconsider certain areas of the tax.

One of the key areas the Government is consulting on is in relation to the FBT treatment of motor vehicles. The issues paper noted that there may be some concerns and misconceptions around the work-related vehicle exemption as it applied for twin or double cab utes. There appears to be a widespread perception that twin cab utes are exempt from FBT because they represent work related vehicles.

On Tuesday, Inland Revenue Deputy Commissioner for policy David Carrigan stated in a press release that it is a myth that utes have always been free from FBT.

“When it comes to double cab utes, these are treated no differently to any other vehicle unless the use of the vehicle meets all requirements for an exemption from FBT, then a double cab ute is and always has been subject to FBT. That is the current law.”

He added that work related vehicles are only exempt from FBT if they meet specific requirements. But there is no blanket exemption for twin cab utes.

The press release goes on to explain the way the rules work and how the exemption might work. The basic position being that it is only exempt on days when it is used for essential work purposes as defined by Inland Revenue. Where vehicles are used partly for business and partly privately, they’ve always been subject to FBT on the days those vehicles are used for private purposes.

Simplifying FBT

According to the press release the purpose of the proposals out for consultation, if implemented, is to simplify FBT and reduce compliance costs, not create additional obligations. If a business, including a farm, is not currently liable for FBT on a vehicle, then it’s unlikely that that business would become liable for FBT on any proposals taken forward.

The press release then concludes by reminding that government still hasn’t made any final decisions in relation to any potential changes for FBT as it’s still considering the feedback it received on the issues paper released in April consultation which closed on 5th May.

My expectation is that if we’re going to see anything happen, we’ll see any changes included in this year’s tax bill, which we can expect to see in late August/early September based on previous years.

In the meantime, it is interesting to see Inland Revenue feels compelled to come out and remind people of the rules. Clearly, the perceived status of twin cab utes was something of a sore point for some people who felt that the work-related vehicle exemption was being abused.

Inland Revenue targets the horticulture sector.

Moving on, we’ve frequently discussed Inland Revenue initiatives on compliance and debt enforcement. As we noted last week, the Budget allocated close to $90 million this year in additional funding to Inland Revenue for investigation and general compliance work and debt management. The expectation is that Inland Revenue will get a return of $8 for every dollar put into such activity.

And then on Wednesday, the latest update on Inland Revenue’s progress in these areas was in relation to the horticultural sector where the press release noted

“Inland Revenue is seeing a few concerning practises in the horticultural sector, including people being paid under the table.”

In the past ten months, Inland Revenue has found $45 million of undeclared tax in the horticultural industry from under the table cash sales not being reported correctly, withholding tax either not being deducted on schedular payments made or deducted at the wrong rates. In some cases, the payments were not even reported to Inland Revenue.

Convoluted structures

According to the press release, many of the issues Inland Revenue has seen arise are in relation to labour hire firms, who frequently pay the labourers in cash. Some of those firms then use convoluted business structures to try and hide those payments and avoid the withholding tax obligations that come with them.

The problem Inland Revenue has with this behaviour is the withholding tax it’s obviously missing out on. But it also means that because the labourers’ incomes have been understated, they could possibly get benefit payments they’re not entitled to and in some cases avoid their child support and student loan payments.

Unsurprisingly, Inland Revenue is cracking down on this .

“…by requiring many contracting firms to withhold tax from their labour repayments and pay that directly to Inland Revenue, where Inland Revenue identifies growers and other payments not correctly deducting or accounting for their tax. We’re also following these up with interviews.”

It’s also pursuing the contracting firms through audits and prosecutions, and apparently there are nearly 100 such audits active at the moment.

“High use of cash and migrant labour”

The press release concludes by noting that there’s a high use of cash and migrant labour. The horticultural industry is therefore a sector open to abusing workers so Inland Revenue will work with other New Zealand government agencies to address these issues.

Cash payments are always a target for Inland Revenue, but it’s interesting to see a sector singled out and certain types of firms identified as the risky part of the equation. The initiative is another sign of how Inland Revenue is using its increased funding and the ongoing issues it encounters in the sector. It will be interesting to see the results of the prosecutions.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

Budget Day lockup is a mad frenzy of activity as you basically have three and half hours to sift through a massive information dump, determine the key points and write something for release at 2PM when the Budget is officially released.

Surprisingly, in the midst of all the information provided, you don’t get copies of any accompanying legislation, bill commentary and Regulatory Impact Statements that will be also released at 2PM. Therefore, those of us who are in the Budget Lockup are a still little bit blind as to the full details of the Budget initiatives. Because of this I increasingly view the Budget Lockup as an interesting experience, a good opportunity to interact with Treasury officials, because you can actually ask for specific information and an opportunity to perhaps quiz the Minister of Finance on some points.

Budget Day – just a government showpiece?

On the other hand, it is increasingly clear from the run up to Budget Day that the budget itself is very much a set piece for the government of the day to boost specific Budget initiatives and narratives. Any detailed analysis on the day is swamped by all the good or bad news about the state of the economy or who’s getting extra or reduced funding. It’s not really until the week following the Budget that you start to get some detailed analysis of what is in the budget and the potential implications.

Investment Boost – a real boost to productivity or just meh?

On Budget Day the Investment Boost proposal was well received, but as people looked into the detail some concerns have emerged. What the measure does is essentially accelerate the depreciation which would have been claimed on these assets. This is done by way of an immediate 20% deduction with the remaining 80% of the asset expenditure depreciated as normal. My initial reaction was to recall the First Year Allowances I used to deal with when I was working in the UK and which operated in a similar fashion.

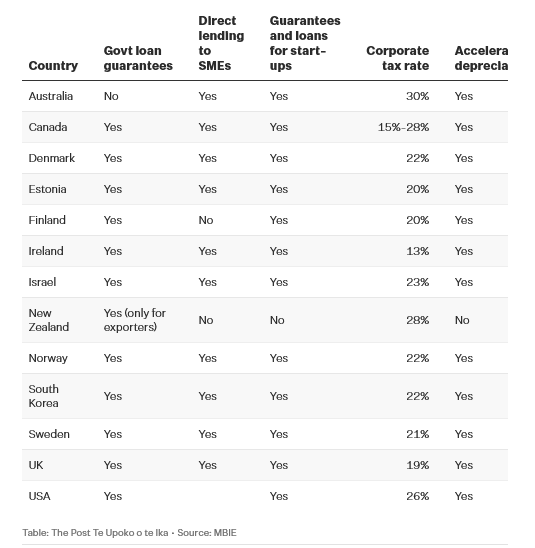

The twist is last year the Government removed depreciation on commercial buildings, including factories, to pay for its tax cuts. But this year commercial buildings are included in those groups of assets that are able to qualify for the Investment Boost. This about-face has prompted Andrea Black the former independent advisor to the last Tax Working Group, and a previous a guest on the podcast to write an op-ed in The Post about the Investment Boost initiative. In summary, she argues if we are trying to boost productivity, then Investment Boost is a step in the right direction but is not the productivity game changer that is being promoted.

New Zealand is an outlier, again

Andrea is critical that the Investment Boost initiative does include commercial property and notes that our labour productivity is poor and that direct assistance in terms of accelerated depreciation – which she strongly supports – doesn’t really exist for many New Zealand manufacturers. She includes a very telling graph put together based on information obtained under the Official Information Act from the Ministry of Business, Innovation and Employment about how other countries subsidise business, including through tax breaks and government loan guarantees.

As can be seen we only grant government loan guarantees for exporters, in contrast to most other countries in the OECD. Similarly, we and Finland are the only countries which do not provide direct government lending support to small and medium enterprises. The United States, for example, has the Small Business Administration, and this initiative was something we looked at when I was on the Small Business Council back in 2018-2019. I thought then, and still do, that the lack of government financial support for our SME sector is something we really need to address.

A step in the right direction but…

As Andrea notes until Investment Boost New Zealand had no accelerated depreciation which meant we were very much out of line with other jurisdictions. So the Investment Boost initiative is a step in the right direction even if it perhaps could have gone further. I have little doubt Investment Boost will have an effect on investment, like Andrea whether it will have the effect the government is hoping for in boosting productivity, I’m not so sure.

I’m particularly concerned wearing my devious tax planner cap that the opportunity now exists for some clever financiers to put some property related deals together to accelerate the building of some commercial properties to obtain the 20% upfront deduction. I saw something similar happen in the UK with the former Business Enterprise Scheme, which was designed to boost startups but quickly saw property backed schemes emerge to claim the generous deductions. Anyway we shall see how this plays out over time.

Investment Boost, Fringe Benefit Tax and skewing the composition of our vehicle fleet

Incidental to this issue Newsroom published an interesting article talking about the impact of proposed changes to the Fringe Benefit Tax (FBT) regime treatment of motor vehicles. The article suggested that the Investment Boost proposal, which applies to vehicles as well, might mean that we might see a shift away from the use of double cab utes.

There’s a number of reasons that they are now so prevalent on our streets and a growing component of the vehicle fleet. One reason is that there was a perception that double cab utes qualify for the work-related vehicles exemption from FBT. The other was that manufacturers were promoting these vehicles with some highly favourable deals.

The increase in the number of double cab utes prompted Angela Hodges, from NZ Tax Desk to comment the combination of those two factors and particularly the perceived exemption has

“skewed the composition of New Zealand’s vehicle fleet over time, with tax settings influencing business-purchasing decisions in ways that probably weren’t intended”.

The Newsroom article suggests that the coming FBT changes together with the Investment Boost initiative may encourage a switch away from double cab utes to alternative vehicles. It will be interesting to see how this develops.

Inland Revenue’s “significant funding boost”– what can we expect?

Moving on and in as big a surprise as the sun will rise tomorrow, Inland Revenue was given additional permanent funding of $35 million per year to invest in tax compliance and collection activities. As the Commissioner of Inland Revenue, Peter Mersi, pointed out, “This is a significant funding boost and is recognition of what we do and the excellent results we’ve had so far this year.”

These results include for the year to 31st March 2025 assessing additional tax of $880 million from audit activity and improved debt collection activities, with just under $3 billion collected in the year to date compared with $2.7 billion for the previous year. There’s also been a doubling in the number of prosecutions and a big increase in the collection of overseas student loan repayments. In my view this is a scheme that really needs a lot of re-thinking about how it’s managed.

In addition to that $35 million Inland Revenue also got an additional $29 million per year last year for compliance and debt collection. Furthermore, the Government has also agreed to continue $26.5 million of funding set to end this year. All up Inland Revenue is getting close to $90 million of funding for investigation and debt collection activities.

This should have a significant impact given the rate of return of between seven and eight dollars for each dollar invested, which has been achieved in the past. The total return from increased compliance and collection activities is therefore potentially as high as $700 million per year.

A warning and a reminder

Against this backdrop people should keep two things in mind. Firstly, as I’ve said on many previous occasions, Inland Revenue has vast resources. It receives data from many sources, and it is increasingly efficient at absorbing, analysing and acting on that data. The basic proposition you should operate on is; if you have put anything in writing anywhere, Inland Revenue will have access to that information at some point. In particular, Inland Revenue has become increasingly efficient in tracking property transactions.

The other point is in relation to tax debt. If you are behind, take action and front up to Inland Revenue. It’s much better doing so than hoping you won’t be on their radar. Being proactive will get a better result for you in the long term.

The Digital Services Tax is dead – now what?

Now at last, in the run up to the budget, the Minister of Revenue, Simon Watts, announced that the Government had decided to discharge the Digital Services Tax bill from the legislative programme. This had been introduced in 2023 by the previous Labour Government. It was really intended as a backstop to OECD’s Two-Pillar international tax initiative.

According to Mr. Watts, “we’ve been monitoring international developments and decided not to progress the Digital Services Tax bill at this time. A global solution has always been our preferred option and we have been encouraged by the recent commitment of countries to the OECD work in this area.”

The consequence of the decision is that the forecast revenues from the introduction of the Digital Services Tax will no longer be included in the Crown accounts. This represents a $476 million reduction in tax revenue over a four-year period. The question therefore arises as to what replaces this lost revenue.

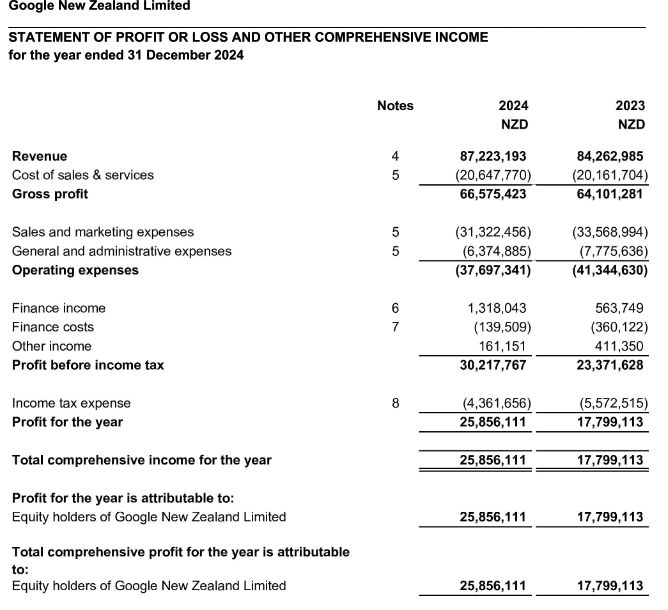

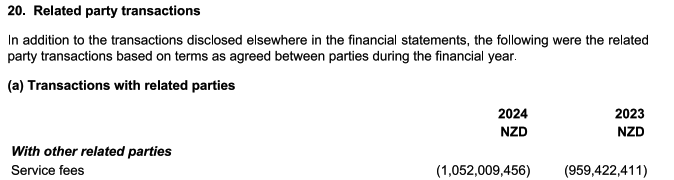

Google New Zealand’s billion-dollar service fees are not unique

In the same week as the Budget and the announcement about the Digital Services Tax, Google New Zealand released its results for the year ended 31 December 2024.

During the year Google NZ paid $1.05 billion in service fees to related parties, almost $100 million more than in 2023.

A week or so later, Facebook New Zealand announced its December 2024 results and the amount of fees it paid to associated entities was over $150 million, roughly the same as for 2023.

Jonathan Milne of Newsroom wrote an interesting article looking at the question of the payments that were being made by all the tech companies. Taking into consideration the fees paid by Apple, Amazon, Microsoft together with Google and Facebook he estimated the annual amount of service fees being paid to associated entities was close to $4 billion. Assuming all are deductible then at the corporate income tax rate of 28% that represents over $1.1 billion of lost tax revenue.

What about the OECD Two-Pillar deal?

Now, of course, it’s more complicated than this simple calculation. But the withdrawal of the Digital Services Tax should be seen alongside what can only be described as regulatory capture in Washington by the tech giants. That in turn has led to these trade threats made by President Trump against digital services taxes and other attempts to tax the tech giants. This all means that the international Pillar One and Pillar Two proposals in which Minister of Revenue Simon Watts places great faith are practically dead in the water.

The Government therefore has a problem. Having accepted it’s not going get $476 million of revenue from the Digital Services Tax, how does it replace that lost revenue. What about the potential $4 billion of service fees going in affiliate fees, should these be subject to some questions under the transfer pricing rules? What is going to happen in that space? Will some of the roughly additional funding of $90 million discussed earlier be deployed in boosting Inland Revenue’s reviews of the transfer pricing practices of the tech companies? We don’t know, but this is an area other jurisdictions around the world are also grappling with.

In Australia at the moment some of these transfer pricing issues are involved in the PepsiCo case. The case revolves around an embedded royalties issue, basically: do some of the payments made for concentrate include some form of royalty which should be subject to non-resident withholding tax? Typically, non-resident withholding taxes for royalties are between 5% and 10% of the payment. Increased focus here may be a means of recovering some of the lost revenue from the digital services tax.

This issue of the treatment of service fees is in my view probably one of the most interesting challenges in the international tax space right now. All around the world there’s great interest in addressing this issue of transfer pricing. We’re therefore watching to see how Inland Revenue moves and, as always, we will report on developments as and when they arise.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

And reveals results of increased audit activities.

Is GST really a tariff?

It’s been a busy week in tax. Right at the start of the tax year, Inland Revenue has launched a public consultation on a review of the fringe benefit tax regime which is now 40 years old. The 75 page issues paper titled Fringe benefit tax – options for change reviews the current status of FBT, focusing on issues Inland Revenue has identified. It puts forward a number of proposals aimed at simplification of these rules and a reduction in compliance costs, a long standing issue with major employers. There’s plenty to digest here but there’s a summary of the proposals on pages 6-8 of the paper if you want to get a quick handle on the proposals.

Reimagining FBT

The paper also addresses the separate issue of general compliance with the regime. A particular source of grief amongst compliant taxpayers is the treatment of the ubiquitous twin cab ute and the application of the work related vehicle exemption. Overall, the purpose of the paper is to

“…to review how FBT is assessed now, highlight current issues we are aware of with FBT and then outline some new concepts for how we could think about a reimagined FBT regime that is less complex and more targeted…”

The paper has 12 chapters, beginning with an introductory chapter, with Chapter 2 setting out the aims of the review. Chapter 3 explains how FBT is currently assessed. Chapter 4 picks up the FBT regulatory stewardship review from August 2022 which is really one of the initiators of this project. Chapter 5 then provides some comparisons with international FBT regimes.

Chapter 6 has an interesting discussion about FBT’s connection with remuneration. We tend to forget FBT was mainly introduced to ensure that all types of remuneration were brought into scope. Back in the 1980s, before FBT was introduced and the top personal tax rate was 66% it was common practice to give employees non-cash benefits such as company vehicles. Countering this was a key driver behind the introduction of the FBT rules in 1985.

Chapters 7 and 8 look at FBT and motor vehicles and considers options for change. Chapter 9 considers one of the areas of complexity, the treatment unclassified benefits. Chapter 10 discusses the option of applying FBT on entertainment expenditure, a proposal which will probably surprise a few people. The paper notes that entertainment regime also attracts a great deal of controversy and complaints about the compliance costs involved. Finally, chapter 11 looks at miscellaneous issues before Chapter 12 looks at data filing and integrity.

Why such a tight submission deadline?

There’s a lot to consider in this paper but submissions are due by 5th May, which means between Easter and Anzac Day there’s barely 4 weeks in total to review the paper and make submissions. The Minister of Revenue, Simon Watts, has repeatedly expressed a wish to simplify the FBT rules so he is keen to get this moving. My understanding the reason for the tight timeline is a desire to have the relevant legislation ready to be part of this year’s main tax bill, which will be introduced around late August or early September.

Proposed changes to FBT on motor vehicles

I expect many will focus on the proposals for motor vehicles. An interesting proposal is to increase the weight limit for vehicles subject to FBT from 3,500 kg to 4,500. Given the weight limit for a person with a full individual drivers’ license is 6,000 kg, my view is the FBT limit should tie into that threshold. Another proposal is to exempt vehicles that are used for providing emergency services.

A key change is removing the tax book value based option for calculating the fringe benefit value of a vehicle. Something worth considering is the suggestion for an optional valuation basis based on the fuel source for the vehicle i.e. electric, hybrid or petrol and diesel.

As part of re-connecting FBT with remuneration the paper suggests the FBT value of the motor vehicle could be calculated by reference to external sources such as remuneration consultations or maybe the AA calculations of vehicle running costs. The paper suggests regular revaluations, maybe every four years. One of the reasons why the tax book value option was introduced was that if people are not changing their vehicles regularly, then there’s an issue that the vehicle may be overvalued for FBT purposes. The proposal would address this issue.

However, the Lord giveth, and the Lord taketh. The paper proposes the following new rates for calculating the fringe benefit value of a vehicle based on its cost:

standard rate: 26% annual or 6.5% quarterly

hybrid vehicles: 22.4% annual or 5.6% quarterly, and

electric vehicles: 19.4% annual or 4.8% quarterly.

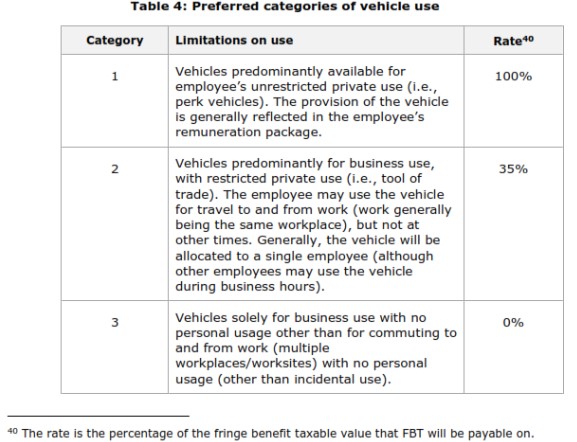

Availability vs actual use

As part of the intention to simplify FBT, the suggestion is to no longer require taxpayers to maintain logbooks to determine the days the vehicle is available for private use. Instead, the focus will shift towards the actual extent of private use the vehicle is available for (for example, is it limited to home to work travel?).

The paper suggests the following categories of vehicle use:

As part of this change, the paper proposes excluding “incidental travel” to ensure that one-off private use of a vehicle can be ignored for FBT purposes. Behind this idea is a “close enough is good enough” approach.

A key proposal is to remove the current work-related vehicle exemption which as the paper says, is a “most misunderstood” exemption. The changes should address the issue of double-cab utes supposedly qualifying for the work related vehicle exemption and avoiding FBT entirely.

Changes to the entertainment regime

The other major proposal of note is integrating the entertainment regime into the FBT regime. Again, the idea behind this is to simplify quite a number of issues that currently exist in relation to the entertainment rules which have never been very popular and compliance is also a problem. As the paper notes many employers are taking a close enough is good enough approach to entertainment expenditure.

The interaction of the entertainment and FBT regimes can be confusing. For example, if an employer takes an employee out to a restaurant that is subject to entertainment rules. However, if the employer gives a voucher for that restaurant to an employee to use whenever they want, then that’s subject to FBT. Another example one would be if an employer pays for employees to participate in a front run, and then then provides a BBQ for staff staff at the finish line. Is the cost of the fun run subject to FBT but the BBQ represents entertainment? Integration of the two regimes is intended to address these issues.

Overall, this is a welcome review and as previously noted pretty timely given it’s now 40 years since FBT was introduced. Just remember you’ve got to get your skates on to submit by the deadline of 5th May.

Inland Revenue ramps up its audit activities with good results

At the start of last week Inland Revenue announced some of the results of its “noticeably increased” compliance activity. For the period from 1st July to 31st December 2024, it opened 3,600 audits 50% up on the same period in 2023. According to Inland Revenue’s Segment Lead for Significant Enterprises, Tony Morris, “Inland Revenue has found $600 million of additional tax that should have been declared.”

Morris went on to add “We’ve had a strong focus on the largest businesses in New Zealand and it’s worth noting that half of that additional tax came from less than 10 audits.” In other words 10 audits yielded $300 million.

Furthermore, Inland Revenue screened over three million returns as part of its annual year-end auto-assessment process. 30,000 of those, or about 1% were selected for review which resulted in a further $859 million of tax revenue. That’s a pretty good bang for buck on the additional funding it got in last year’s Budget.

Inland Revenue has also been focusing on debt and I thought this particular comment was of interest

“We’ve been in touch with 200 business owners and told them we know they have multiple properties – some in a company name, some in trusts, some personally. We believe they should be able to refinance to pay their debts to us and told them so.

“…These 200 people had $14 million of debt between them, but within a month more than $10 million had been paid or put under arrangement.”

Inland Revenue’s data gathering around property transactions is second to none and people would be wise to not underestimate this. It has been identifying transactions in this area for quite some time. A colleague recently told me of an audit that he was involved in where the client was saying, ‘Oh well, a number of property transactions were simply renovations of my main home’. That is until Inland Revenue investigators presented a “ream sized folder” full of property transactions for this taxpayer. From that point, the question wasn’t about rebutting Inland Revenue’s proposition that he was actually a property trader but trying to mitigate the damage. You have been warned.

“This is Baycorp calling on behalf of Inland Revenue”

However, something that does concern me is Inland Revenue’s announcement on 10th April it would be “running a six month pilot program in partnership with Baycorp to improve our debt collection process.”

Inland Revenue warned taxpayers that during this pilot, “you may be collected, may be contacted by representatives from Baycorp. Please be assured that these contacts are legitimate and part of our authorised programme.”

That’s as may be, but I’m not so sure given everyone’s growing concern about scams, not too many people are going to accept calls from Baycorp saying ‘you own Inland Revenue money pay up.’ I therefore doubt the pilot is actually going to be as effective as hoped even if Baycorp show the taxpayer incontrovertible proof that they have a debt due to Inland Revenue.

This is just the latest push by Inland Revenue to improving debt collection. As we noted in our last podcast given the rise in GST debt in particular, it’s basically no surprise that Inland Revenue is putting resources into debt collection. And as I’ve said previously, I expect there will be more funding given to it in next month’s Budget.

Is GST a tariff?

Meanwhile, around the world there has been large scale turmoil in the financial markets as everyone tries to work out what exactly is happening with the tariffs proposed by President Trump’s administration. As part of this he has indicated that value added tax (VAT) is now seen as a tariff. There’s been a huge pushback against this with the basic counterargument being that tariffs are only imposed on imported goods and services, whereas GST/VAT applies regardless of source of the goods or services

If you want more a bit more detailed analysis of why GST/VAT isn’t a tariff, I suggest this interesting post by Dan Neidle of Tax Policy Associates. He considers the issue using the example of beer, which is always handy, and the implications of the policy.

Removing GST from fruit and veg – “a well-known solution to every human problem”

The American writer HL Mencken was the source of the quote “There is always a well-known solution to every human problem – neat, plausible and wrong.” This often comes to mind in relation to the frequent proposal to remove GST from fruit and vegetables. It so happened the Prime Minister was asked about this suggestion on TV1’s Breakfast Show. He responded that it was far more complex than people imagined.

I subsequently appeared on Wednesday’s show to discuss the issues involved in removing GST from fruit and veg. To be fair following Mencken’s dictum about the policy being ‘wrong’ would be a bit harsh. This is an extremely well meant suggestion based on the precept if you wanted to try and help people struggling with the cost of living then removing GST is an option or step and no doubt would provide some assistance.

But as I explained it is complex and definitional issues lead to extreme examples such as the UK Mega-Marshmallows which enabled me to sneak in a reference to The Princess Bride. Furthermore, well-meant though it is, the proposal is not perhaps the right solution for the problem you’re trying to deal with, which is people with low income who are struggling with rising costs. A targeted response is more appropriate.

The Tax Working Group’s view

This was also the analysis of the 2018-19 Tax Working Group which also addressed a key complaint about GST, that it’s seen as regressive for those on low incomes. In response to addressing regressivity by perhaps reducing the rate of GST or introducing a GST exception for food the TWG commented “there are more effective ways to increase progressivity than a reduction in the rate of GST.”

Instead, the Tax Working Group suggested

“…increases in welfare transfers would have a greater impact on low income households. Changes to personal income tax can also have a greater impact on low and middle income earners. GST exceptions are complex, poorly targeted for achieving distributional goals and generate significant compliance costs, and furthermore, it is not clear whether the benefit of specific GST exceptions are passed on to customers.”

I agree with that analysis. It’s also supported by research carried out by Tax Policy Associates on the impact of VAT(GST) changes in the UK, where VAT has been removed from several products again for very well meant reasons. Examples include a reduction in the VAT rate for tampons and other menstrual products and the zero-rating of e-books. In both cases, the analysis carried out by Tax Policy Associates identified little or no benefit going to final consumers. In fact, in the case of e-books, no benefit passed through to consumers, costing the UK £200 million.

A complex and ineffective solution

In sum removing GST from fresh fruit and veg is complex and leads to boundary definitional issues. UK cases such as Mega-Marshmallows or the older Jaffa cake case involving the UK’s zero-rating of food are very, very good examples of the sometimes absurd distinctions that arise. Even although accounting systems are much improved the fact remains there are irreducible minimum compliance costs involved. These will fall most heavily on smaller operators such as dairy owners who already have a fairly heavy compliance burden with GST.

Much as I can see why people would want to suggest zero-rating fresh fruit and vegetables, ultimately, you’d have to consider whether the benefit of such a change is actually going to flow through to those who you want to benefit? Remember, if you do apply an exception, everyone benefits from it. As the Tax Working Group noted wealthier deciles spend more on food and fresh fruit and vegetables so would probably benefit disproportionately.

This isn’t a matter that’s going to go away. My view remains in line with that of the Tax Working Group. Look at what the real issue is, and it’s some families don’t have enough income. The best approach is therefore to give them more income. But we’ve got an election coming up next year and no doubt the proposal together with other well-meaning but inefficient ideas will be put forward.

And on that note, that’s all for this week, we’ll take a short break for Easter and be back for the ANZAC Day weekend. In the meantime I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day and Happy Easter.

In the same week as Public Service Minister Nicola Willis directed department bosses to tighten up on working from home arrangements, it’s a little ironic to see Inland Revenue release a draft consultation on the topics of deductions for expenditure and travel by motor vehicle between home and work and when an employer provided motor vehicle is subject to fringe benefit tax (FBT) for travel between home and work.

These were released alongside some interesting commentary from Inland Revenue that it is currently reviewing FBT, so what is set out in the draft consultations may change, but as Inland Revenue note, it gets a lot of questions on the topic. With regard to this FBT review my understanding is we may see something relatively soon. I think given the outcome of the Inland Revenue’s regulatory stewardship review of FBT and what the Minister of Revenue has said previously, it’s likely this review with look at simplification measures.

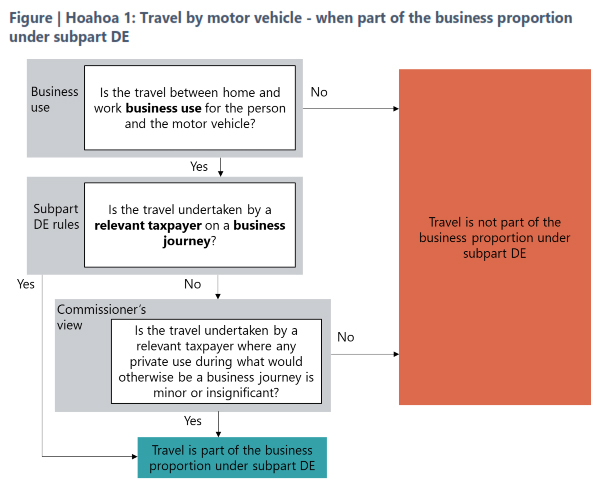

There are actually two consultations which will replace the previous interpretation statement IS3448. The topic is quite involved, because the two draft consultations run to 111 pages of commentary and examples. Fortunately, as is now the common practise, each draft consultation is accompanied by fact sheets, each containing a very useful flow chart to help people work their way through the maze.

The deductibility of motor-vehicle travel between home and work

The first draft interpretation statement deals with the question of deductibility of travel by motor vehicle between home and work which is set out in Subpart DE of the Income Tax Act 2007. What that subpart does is limit deductions for motor vehicle expenditure to the business proportion of the expenditure. It generally applies to self-employed taxpayers and partners in partnerships, but it can also apply in some circumstances to close companies and look through companies.

The basic position is that a journey is deductible if it’s a business journey, but to be a business journey and deductible, the whole journey must be undertaken for the purpose of deriving income. This is actually slightly different from the general deductibility provision for tax, which allow deductions quote to the extent to which they are incurred in deriving gross income. By contrast, this the provisions in Subpart DE are very specific it’s got to be a business journey if it is to be deductible.

Four exceptions

Generally speaking, and it’s probably no surprise here, travel between home and work is viewed as private. But there are four exceptions as a result of case law. Firstly, where the vehicle is necessary for the taxpayer to transport goods and equipment that are essential for their work between their home and workplace and for use both at home and in their workplace.

Now secondly, the taxpayers work is itinerant, which means that the taxpayer works at different locations during the workday and the sequence of where they work and how much time they spend is unpredictable and varies. It’s therefore not practicable for them to carry out their work without the use of a vehicle.

The third case is where a taxpayer is responding to emergency call outs and does so from home. And finally, and this is increasingly relevant, the taxpayer’s home is a workplace or base of operations for the purposes of travel to and from work.

This latter point is where we’ll probably see a lot of discussions and arguments. In order for a home to be treated as a workplace or base of operations the role requires a significant proportion of a person’s work to be spent working at home. I think it’s most likely to apply to owners of businesses who may be working between two places, but senior employees who might be required to make international calls in the evening, they may will be covered.

What’s a business journey?

A business journey is one primarily carried out for business purposes. Case law allows an overall journey to be treated as two journeys if there is a stop in between. It’s possible that one part represents a business journey, and the other part is private.

Furthermore, case law also said that some incidental private use does not mean a journey is prevented from being a business journey. Under the draft Inland Revenue consider that insignificant private use can’t exceed either approximately 5% of the total journey and approximately two kilometres.

The consultation also deals with the issue of what if vehicles are taken home for security purposes or, as is now more common, it’s an electric vehicle taken home to be recharged. Either of those circumstances are not sufficient in themselves to make the relevant journey between home and work a business journey. There have to be other factors at play, such as the exceptions we’ve previously mentioned or that home represents a workplace.

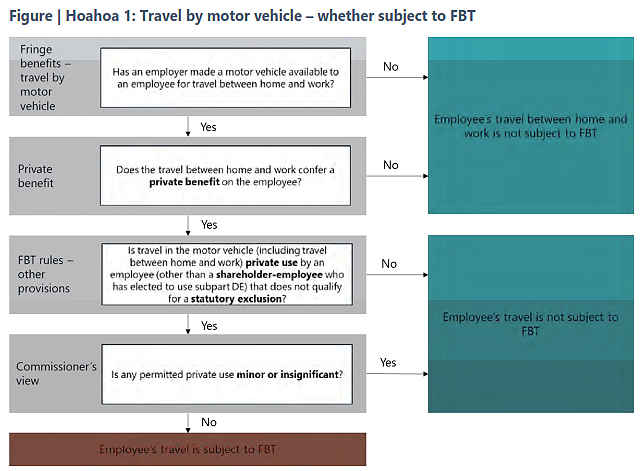

When does a fringe benefit arise?

The second interpretation statement and supporting fact sheet considers the question of when a fringe benefit arises when an employer provided motor vehicle is used for travel between home and work. The position is pretty straightforward: if a vehicle has been provided for private use, FBT will apply. In this context private use would include the use of the vehicle for travel between work and home and work. If a employee has a employer provided vehicle and travels to between home and work in that, then fringe benefit will apply.

There are three statutory exclusions from FBT which would cover travel between home would work. These exclusions apply to work related vehicles (a topic the subject of a whole another interpretation statement;

Emergency calls affecting health, life or the operation of essential machinery and services; and

business trips of more than 24 hours.

If any of these exclusions apply the whole day is excluded from the calculation of FBT.

As noted above Inland Revenue is in the course of reviewing FBT, so maybe some of this might change within the next couple of years or so. In the meantime, it’s good to have this draft guidance. Consultation on this is open until 6th November.

Meanwhile progress on the international tax deal continues

Moving on, we’ve talked regularly about the G20/OECD international tax agreements on base erosion and profit sharing. This week, several jurisdictions signed a multilateral treaty which will to help the Pillar Two subject to tax rule. But the other thing that’s important which was concluded in the last few days, was a Model Competent Authority Agreement on the Application of the Simplified and Streamlined Approach to Amount B of Pillar One. This agreement will provide a framework to enable jurisdictions to comply with what’s expected to be the final format of the rule of the Pillar One and Pillar Two agreements.

However, progress has slowed right down since October 2021 when 135 jurisdictions announced that they were accepting the two-pillar solution. With tax, the devil is in the detail and there is a lot of detail and devil to work through.

I think the other thing that should be kept in mind is that the US Presidential and Congressional elections happening in November will determine how much further progress will happen. As previously noted, the likes of Meta and Alphabet are none too keen on what’s proposed here and their lobbyists have the ears of plenty within Congress. We’ll just have to wait and see. But in the meantime, the deal seems to be inching forward.

“The time has arrived for a capital gains tax”

Last week I covered the report from Victoria University of Wellington about comparing tax rates between New Zealanders and taxpayers in nine other jurisdictions. This week things got spicier than I would expect in this sort of debate after the CEO of ANZ Bank Antonia Watson said in the course of her RNZ interview with Guyon Espiner “the time has arrived for a capital gains tax.” This in turn provoked a strong response from both the Prime Minister and the Minister of Finance. I found this a little surprising. I would have thought they’d just let Ms Watson make her comments and move on, but it certainly adds to the headlines.

CGT the most likely option

Following on from Antonia Watson’s remarks, I spoke to RNZ’s The Panel on Wednesday evening about the question of a capital gains tax. Put on the spot I said I could see it happening. To expand on my answer, it seems to me that a CGT is the most likely option if we do expand the tax base, because CGTs are common in other jurisdictions and the concepts are broadly well understood. And as Antonia Watson also noted, wealth taxes on unrealised gains are deeply unpopular with those that would be affected.

The interview with Antonia Watson is well worth listening to. One of the things I found quite interesting was that a couple of times she mentioned the impact of adverse weather effects. This wasn’t anything to do with tax, but she was explaining that our vulnerability to such events was a factor in why we have higher interest rates than Australia.

This circles back to the point that I made last week and again on The Panel, that the discussion around the question of capital gains tax or expanding the taxation of capital base is really around the question of how do we pay for the forthcoming costs of climate change and an ageing population? Are we raising enough tax revenue right now? If not, what are the options on the table?

What does Inland Revenue think?

Inland Revenue currently have their proposed long-term insights briefing for next year out for consultation. Susan Edmunds of RNZ picked up on this in a story on Thursday. The consultation finishes Friday 4th October, and I really do recommend reading and submitting on it.

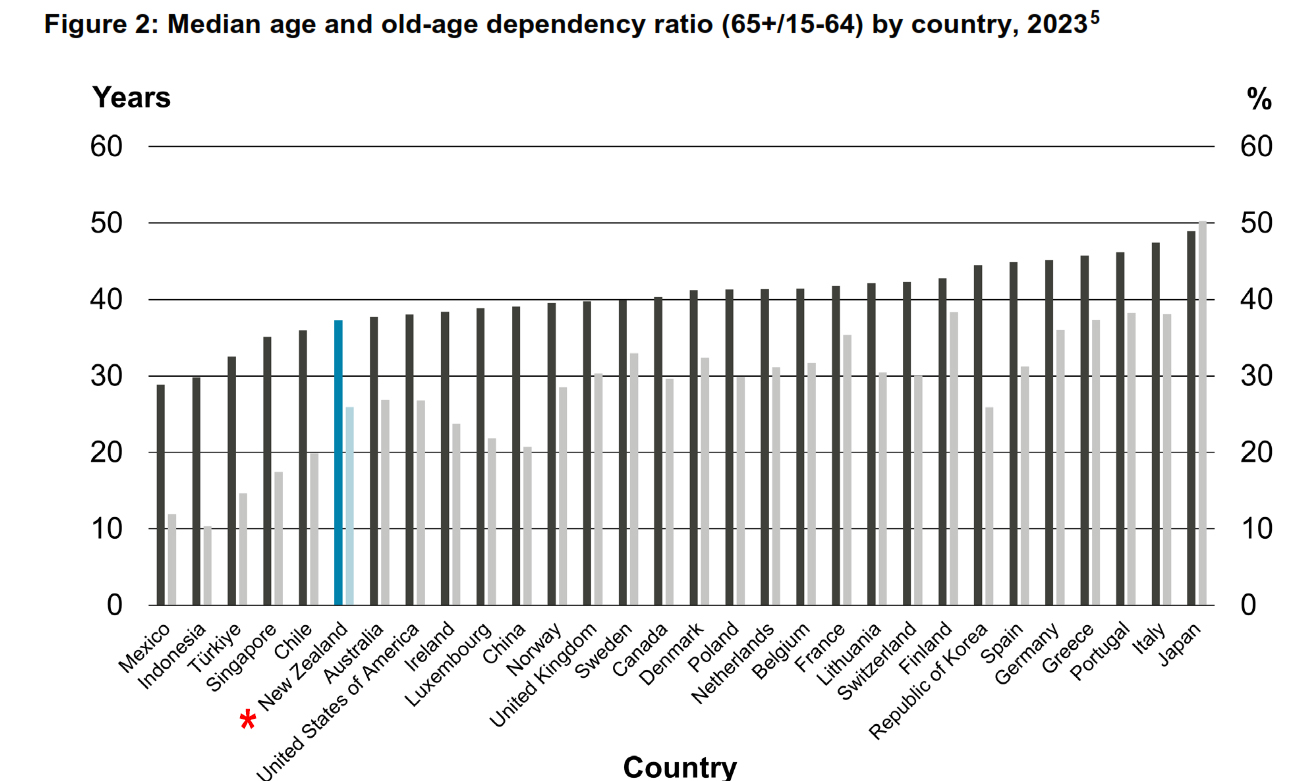

On the question of the forthcoming actual fiscal pressures, Dominick Stephens, the chief economic adviser for the New Zealand Treasury (and former chief economist for Westpac), delivered a speech on Wednesday titled Longevity and the Public Purse, which I’d recommend reading. It includes plenty of graphs illustrating the difficulty that we are facing. Our population is ageing, which is well known and the median old age dependency ratio is rising, although as the speech notes thanks to strong population growth it’s not as bad as other jurisdictions which means we are at the lower end of that range.

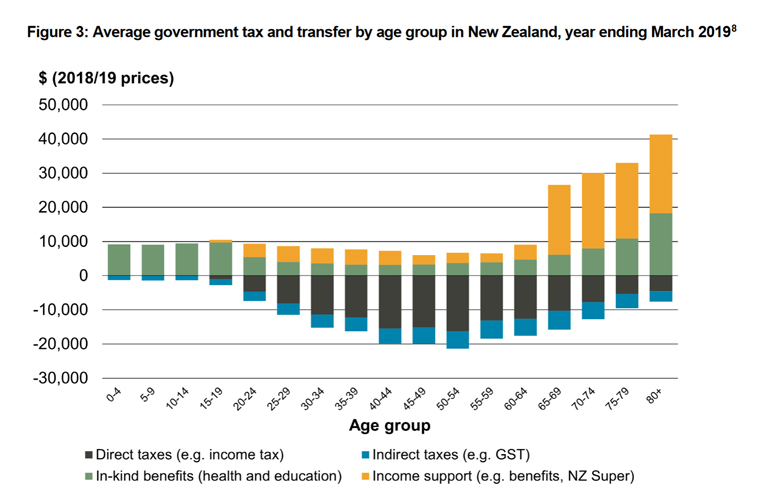

There’s a particularly telling graph about the average government tax and transfer by age group in New Zealand, for the year ended 31 March 2019

As can be seen above for the 65 and over age groups the transfers from Government rise significantly. These are the age groups which is where the debate about sustainability arise, as Dominick Stephens comments:

“Since 2006, the Treasury’s Long-term Fiscal Statements have repeated the message that our fiscal settings are not sustainable over the long run given the impact of population ageing.”

Over the period since 2006 some interesting developments have somewhat ameliorated the potential impact. Interest rates, for example, have been lower than were predicted in 2006, while population growth has been higher.

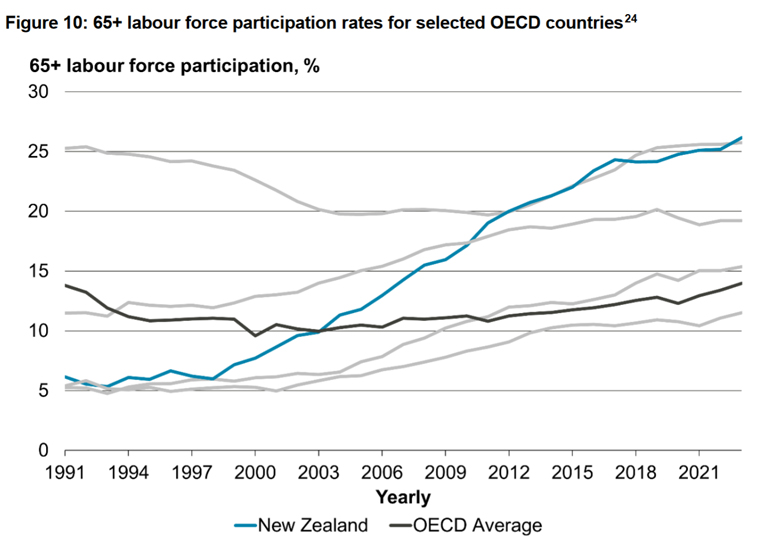

One of the more extraordinary developments since 2006 is labour force participation for 65 plus age groups has dramatically increased. Consequently, we’ve gone from being amongst the lower labour force participation rates to one of the highest.

All things being considered, there are difficult choices to be made and the question of whether more revenue is necessary is a question which isn’t going to go away.

“There is no silver bullet: none of the policy options we modelled in 2021 was large enough to stabilise debt on its own. This means that governments will need to likely draw on multiple expenditure and revenue changes to close the fiscal gap.

Some savings can be made from a greater preventative focus and reducing inefficiencies but making substantive savings is likely to require some tough choices around entitlements. This would have come with trade-offs, particularly for groups of the population who already face challenges accessing health services.”

Governments could also choose to raise additional revenue, in fact as Dominick remarked “successive increases in taxes over time would be required unless actions were also taken to manage demographic expenditure pressures.”

So tough fiscal choices ahead. I note in the comments on last week’s transcript some noted ‘well, wait a minute, why don’t we try and reduce expenditure?’ That’s certainly a driver for the current Government. But I think what Dominick Stephens and Treasury are saying, addressing the fiscal pressures will be a two-part process. We will need to both reduce costs and raise revenue. So, this debate over capital taxation isn’t going to go away soon and will continue. I expect I’ll be asked plenty more times to comment.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

It was a busy week in tax with Inland Revenue releasing guidance in relation to a couple of commonly encountered scenarios. The first is QB 24/04When is a subdivision project a taxable activity for GST purposes?

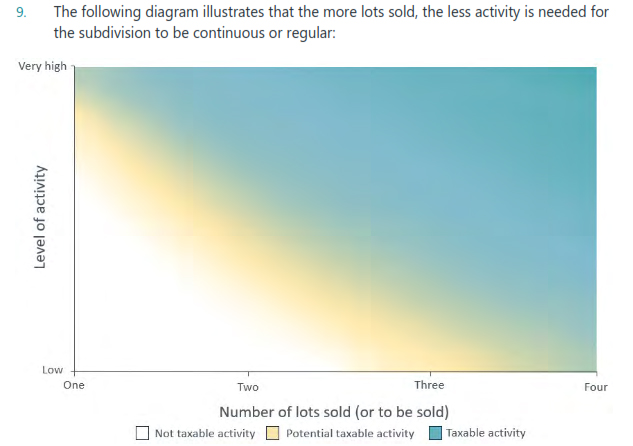

This covers the frequently discussed and very important issue of what is the GST treatment when you are subdividing land into two or more plots? The standard position about GST is that you must register if you’re carrying on a taxable activity and the value of those supplies exceeds the registration threshold of $60,000.

What’s a taxable activity?

Clearly many subdivisions will exceed that $60,000 threshold when they are sold so what represents a taxable activity? In order for a taxable activity to exist it must be carried on continuously or regularly. Therefore, it follows that for a subdivision to be continuous or regular, it usually needs to involve the sale of more than one lot. A subdivision which only involved one sale would usually be regarded as a one-off activity because it does not meet this threshold of continuous or regular.

Notwithstanding that the Inland Revenue guidance points out that some subdivisions which only led to one sale may in fact be continuous and regular. But that would only be if the level of activity involved was very high. Now, like so much of tax, it’s this comes down to the question of the facts of a particular case. Very high in this context might be something like construction and sale of a large office block, or more likely, because more often than not we’re talking about subdivisions of residential land, an apartment block.

The guidance continues the more subdivision plots are divided, the more likely it is to be deemed as being continuous or regular. Following the Newman decision way back in 1995, if a subdivision leads to the sale of four or more lots, that’s typically taken as the benchmark for determining that the continuously or regularly is happening and there is a taxable activity.

On the other hand, what happens when there are two or three lots? Then you have to consider the level of the activity relative to the number of lots being sold in order to determine whether or not this activity is continuous or regular. Therefore, you’d look at the level of development work, the time and effort involved, the level of financial investment and the level of repetition. This last point is probably most critical. If you’re repeating the process multiple times, this is more likely to fall into the continuously or regularly category. But as the guidance notes, everything is fact dependent.

On the other hand, the factors that are not so relevant are whether or not the subdivision is commercial. It doesn’t matter whether the subdivision has a “commercial” flavour or you are subdividing your own land to downsize. Anything done without an intention to sell the resulting land is not relevant. For example, if you build a house on a subdivided lot with the intention of living in it, but later change your mind and decide to sell, work done before you change your mind is not relevant.

Overall, this is useful guidance which comes with a helpful accompanying fact sheet. Keep in mind that the GST treatment is not tied to the income tax treatment. Your project might not be a GST taxable activity, but it could well be subject to the bright-line test or any of the other land taxation rules.

Another common issue – loans to shareholders

Moving on, the other topic, on which Inland Revenue has released useful guidance is a draft interpretation statement on the income tax position in relation to overdrawn shareholder loan account balances (sometimes called shareholder current accounts). Now, as anyone who works with small businesses will tell you this is actually a pretty common scenario. Despite this, the income tax position is not always as well understood as it should be.

In my experience, overdrawn shareholder current account balances typically arise in two scenarios. Firstly, where the owner or shareholder is taking out more in drawings than they’re being paid as a shareholder or employee or any other form of payment. This is a fairly common scenario.

The other instance is where the company has realised the substantial capital gain and shareholders extract the cash without waiting to consider the tax implications of doing so. Often in those situations, advisers don’t find out until maybe months afterwards. At that point it can become quite difficult to unwind the tax consequences because the numbers involved are quite substantial.

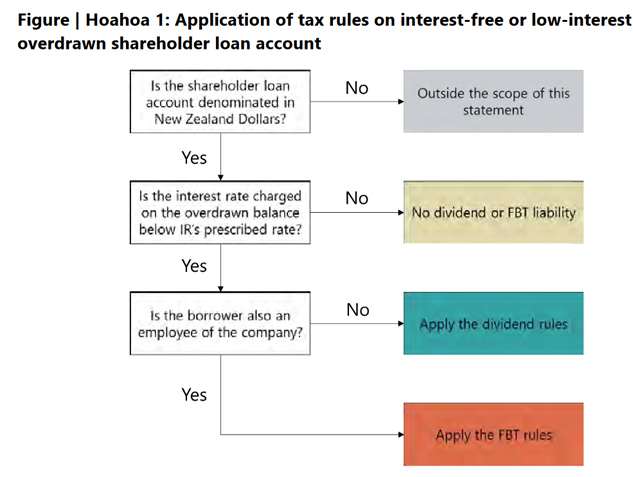

It’s therefore good to have Inland Revenue guidance and this comprehensive interpretation statement runs to 41 pages begins with the summary of the basic rules. A dividend is deemed to arise for a shareholder if they are paying little or low interest on an overdrawn shareholder loan account.

The amount of a dividend on an interest free or low interest loan typically represents the difference between a benchmark interest rate that should be charged and the amount of actual interest rate occurring on the loan. Benchmark for this purpose is Inland Revenue’s prescribed rate of interest, which since 1 October 2023 has been 8.41%.

A dividend can also arise where the loan has been advanced to an associated person of the shareholder. This can lead to some quite involved tracing of shareholdings and related calculations about percentage of shareholdings. This is necessary to determine if there is an association and whether that associated company is part of the same 100% owned group and therefore potentially eligible for the exemption on intra-group dividends. This is another area where I’ve encountered situations where this associated person issue hasn’t been picked up.

Incidentally, it’s worth noting, by the way, that although for New Zealand tax purposes, the amount of the dividend is the amount of interest that should have been charged in Australia and the UK, the amount of the dividend is deemed to be the full amount of the advance made. This might be something we might see Inland Revenue take a look at as it’s something that has occasionally come up in discussions with officials.

Loans to shareholder-employees

Were the shareholder is also an employee of the company, then the low or interest free loan is not treated as a dividend but is instead subject to fringe benefit tax. The amount of the benefit is the difference between the interest paid and the prescribed rate of interest. Something to note here is that the shareholder-employee doesn’t solely mean someone within the provisional tax regime, but it also includes shareholders who are employees and whose salary are subject to PAYE There’s a couple of useful flow charts to help people determine who might be captured by these rules.

The draft interpretation statement also notes that typically interest paid by a shareholder on an overdrawn current account is generally not deductible. This is because usually the drawings are often applied for private or domestic purposes, and so there’s no link to an income earning process. However, in some cases the money might have been withdrawn to invest in a residential property or some other income producing asset, in which case the interest would become deductible, if all the other deductibility criteria can be met.

One other key point to note is what happens if a shareholder is no longer required to repay the overdrawn balance, because the company forgives or remits the debt in some way. In this case the full amount of the loan will be deemed to arise either as a dividend or under the financial arrangements regime. In either case the shareholder will usually be taxed on the amount that’s been remitted.

The interpretation statement also covers scenarios when resident withholding tax might need to be deducted and interest therefore be reported as investment income. This would be somewhat unusual, but the interpretation statement explains when it might happen.

Overall, this is an important and useful document setting out the rules pretty clearly on a topic which as I noted is frequently encountered amongst small businesses but isn’t always as policed or managed as effectively as it should be. It’s also accompanied by a more digestible 8 page fact sheet. Consultation is open until 2nd August.

A blueprint for taxing billionaires?

One of the interesting things going on around the world in the tax policy area now is something of a trend amongst international organisations such as the International Monetary Fund (IMF), the Organisation for Economic Cooperation and Development (OECD) for releasing papers for discussion on the taxation of capital and wealth.

The latest such paper A blueprint for a coordinated minimum effective taxation standard for ultra-high-net-worth individuals was commissioned by the Brazilian G20 presidency earlier this year. The report was written by the French economist, Gabriel Zucman, a protégé of Thomas Piketty. It proposes a framework the approximately 3,000 or so billionaires in the world to pay at least 2% of their wealth in individual income tax or wealth taxes each year.

Zucman’s report notes there been a vast improvement in international tax cooperation since the mid-2010s, particularly with the Common Reporting Standard on the Automatic Exchange of Information which commenced in 2017. He also pointed to the recent agreement hammered out by the OECD for a minimum tax of 15% on large multinationals. (It’s worth noting though that agreement has yet to be fully implemented as progress has slowed recently).

Zucman correctly points to this growing international cooperation and exchange of information as laying the baseline for further international cooperation in the form of what he terms a common minimum standard, ensuring an effective taxation of ultra-high net worth individuals. According to Zucman this “would support domestic policies to bolster tax progressivity by reducing incentives for the wealthiest individuals to engage in tax avoidance and by curtailing the forces of tax competition.” This would target the tax havens where much of this wealth is sheltered.

The paper estimates that a 2% tax on those 3,000 billionaires could realise between US$200 and US$250 billion U.S. dollars in revenue annually. If it was extended to those worth more than $100 million, that could generate another US$100 to US$140 billion per annum. These tax revenues would be collected from “economic actors who are both very wealthy and undertaxed today”. Those affected might not agree with this assessment that they’re presently under taxed.

The paper is realistic enough to note that there are real challenges with the proposals, such as how to value the wealth, ensure effective taxation if some jurisdictions don’t agree to implement it, and of course compliance by taxpayers. It’s a bold proposal which has attracted a lot of attention although I’m sceptical about the potential level of revenue which could be raised. We really don’t have a very detailed understanding of the composition of the wealth and where it is held of the very wealthy. That’s an issue which would need to be addressed. And as I mentioned, there are serious issues around valuations and informed enforcement, which Zucman acknowledges.

Starting a conversation?

But for me, the most interesting thing to me about this whole proposal, it’s the latest. As I said, it’s the latest in the line of papers coming out of the likes of the G20, the OECD, the IMF, the World Bank, all of whom are basically saying that we are not taxing wealth sufficiently and we need to do something about that to address inequality. As Zucman himself puts it in the Foreword of the report

“The goal of this blueprint is to offer a basis for political discussions – to start a conversation not to end it. It is for citizens to decide through democratic deliberation and the vote how taxation should be carried out.”

In other words, he is repeating my old precept that tax is politics.

My personal view is we need to have a broader discussion around the taxation of capital. One of the points to emerge from the current debate going on over replacing the Cook Strait ferries is that the new ferries represented just 21% of the total cost of Project iReX. The other 79% represented the cost of upgrading the supporting infrastructure not just for the larger ferries but also to make it climate change and earthquake resilient for the next 100 years.

Even if we dialled back the futureproofing to, say, 50 years, we’re still talking about significant sums of investment. We’re also still left with the key point of how will we pay for the vast amount of infrastructure that we will need to upgrade to deal with the continuing impact of climate change. In my view our politicians have not yet seriously engaged with us on this issue.

Meanwhile in the UK…

And finally, this week a quick note on the UK election which is next Thursday. The likelihood is that the opposition Labour Party is heading for a massive win. One of their key tax proposals is the abolition of the remittance basis or non-dom tax regime.

But not every voter has understood exactly what that means. As Labour candidate Karl Turner recounted to the Guardian

“We met a guy who said he was going to vote Labour but wouldn’t now because he had just heard that we were taxing condoms,”

“I said, ‘condoms?’ ‘Yeah,’ he said: ‘I just heard on that [pointing to the TV] that you are taxing condoms, and I’m not having it. You’re not getting my vote.’ It was Terence [Turner’s parliamentary assistant] here who worked it out.

“‘We’re taxing non-doms, not condoms,’ I said. ‘Oh,’ he said. ‘Like the prime minister’s wife? Ah.’ He calls out: ‘Margaret: they’re taxing non-doms, not condoms.’”

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

(Loaded to Soundcloud 30 June 2024. Appeared interest.co.nz 1 July 2024).