This week the ninth edition of the OECD’s Tax Policy Reforms was released. This is an annual publication that provides comparative information on tax reforms across countries and tracks policy developments over time. This edition covers tax reforms in 2023 for the 90 member jurisdictions of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

Reversing the trend

It’s a fascinating document which tracks trends of what’s happening around the tax world at both a macro and micro level. The report has three parts: a macroeconomic background, then a tax revenue context, and then part three is the guts of the report with details of tax policy reforms around the world.

There is an enormous amount in here to consider and the executive summary lays out the ‘balancing act’ issues pretty clearly.

“Policymakers are tasked with raising additional domestic resources while simultaneously extending or enhancing tax relief to alleviate the cost-of-living crisis… On the one hand, governments further protected and broadened their domestic tax bases, increased rates, or phased out existing tax relief. On the other hand, reforms also kept or expanded personal income tax relief to households, temporary VAT [GST] reductions, or cuts to environmentally related excise taxes.”

A key observation for 2023 was a trend towards reversing the responses to the COVID-19 pandemic. Instead, as the report notes “2023 has seen a relative decrease in rate cuts and base narrowing measures in in favour of rate increases and base broadening initiatives across most tax types.”

“A notable shift”

This includes “A notable shift occurred in the taxation of business, where the trend in corporate income tax rate cuts seems to have halted with far more jurisdictions implementing rate increases than decreases for the first time since the first edition of the Tax Policy Reforms report in 2015.”

This is a pretty significant change. I think actually when you consider last week’s speech by Dominick Stephens of Treasury, it was setting out the context for why having got over the crisis of responding to the pandemic, countries are realising they’ve got to deal with the demographic issues of ageing populations and funding superannuation.

Climate considerations

Beyond these concerns, there is the immediate impact of climate change and its growing effects. The executive summary picks up on this issue:

“Climate considerations are also increasingly influencing the design and use of tax incentives, with more jurisdictions implementing generous base narrowing measures to promote clean investments and facilitate the transition towards less carbon intensive capital.”

And on that point, I hope all the listeners and readers down in Dunedin and Otago are safe and well at the moment.

Paying for superannuation

The other thing picked up is that in referencing that point I made a few minutes ago about population ageing. There has been a growing trend amongst countries to increase Social Security contribution taxes. Alongside Australia, and to a lesser extent Denmark, we are unique in that we don’t have social security contributions. However, elsewhere in the OECD social security contributions raise increasingly significant amounts of revenue.

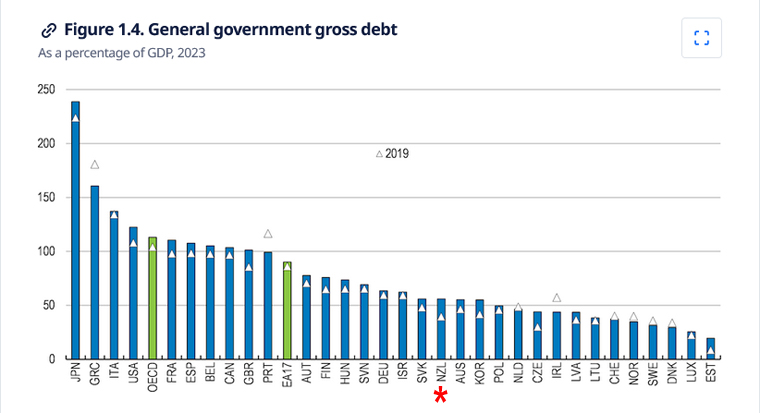

The report begins with a macroeconomic background. It notes that for the OECD as a whole in 2023 government debt rose by about nine percentage points, reaching 113% of GDP. For context, New Zealand’s debt-to-GDP ratio is just over 50%.

As the macroeconomic summary notes after generally decreasing in 2022 Government deficits increased again in 2023 following the energy crisis triggered by the war in Ukraine. Consequently,

“As debts and interest rates increased, interest payments have started to rise as a share of GDP. Even so, in 2023 they mostly remained below the average over 2010 to 2019, except notably for Australia, Hungary, New Zealand, the United Kingdom, and the United States.”

In short, we definitely have issues to deal with in terms of debt management and rising costs.

Responding to growing deficits

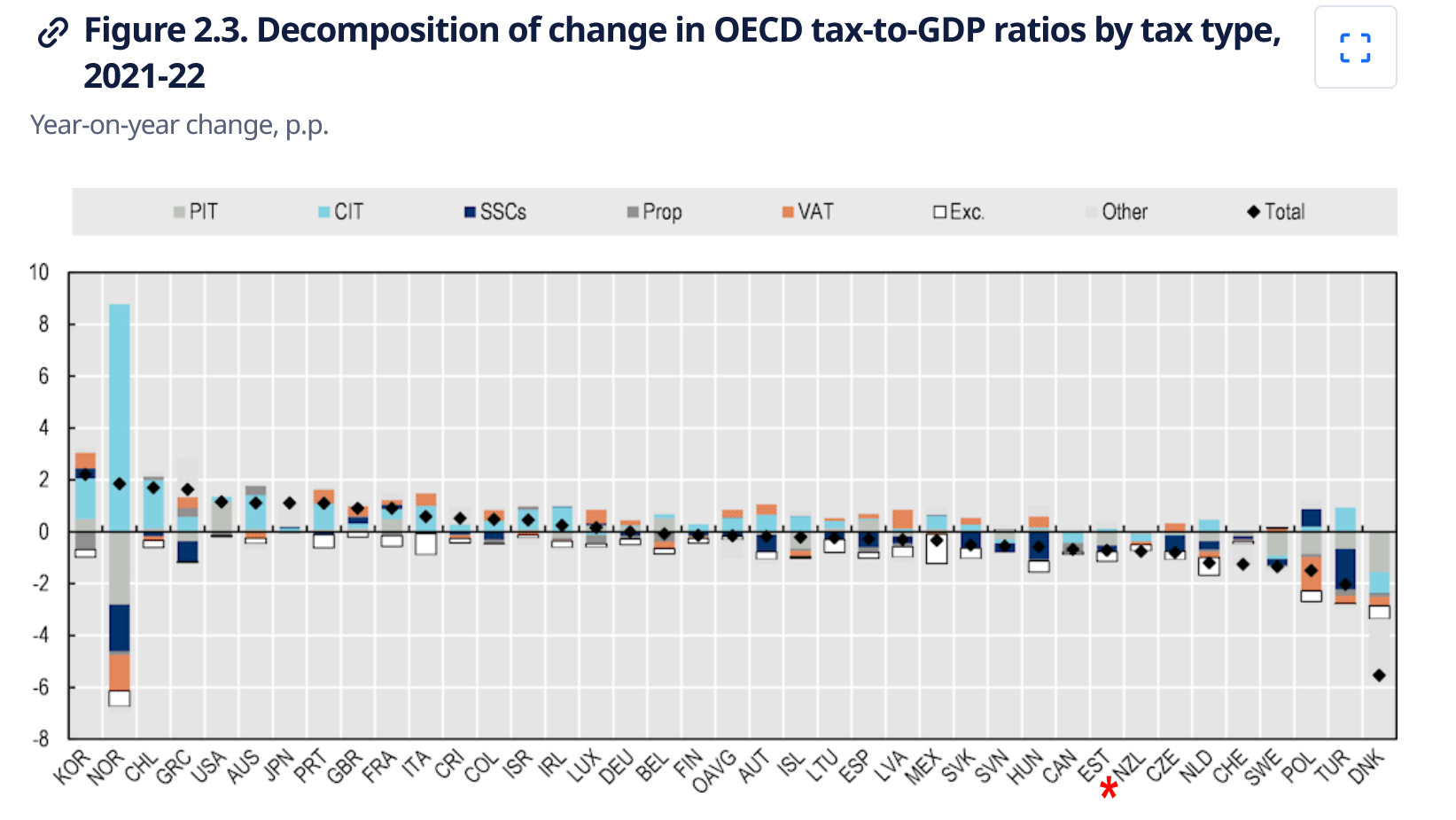

The report then notes that responses to growing deficits have been to start at increasing taxes. In general tax revenue terms,

“From 2020 to 2021, the tax-to-GDP ratio rose in 85 economies with available data for 2021, fell in 38, and stayed the same in one. In more than half of these economies, the change in the tax-to-GDP ratio was under one percentage point, whereas 22 economies saw shifts greater than two percentage points in their tax-to-GDP ratio.”

Denmark saw the most significant drop of 5.5 percentage points, with New Zealand’s tax-to-GDP ratio falling by three-quarters of a percentage point, well above the OECD average fall of .147 percentage points. (Norway’s dramatic corporate income tax take increase of 8.775% is the result of “extraordinary profits in the energy sector”.)

Composition of tax base

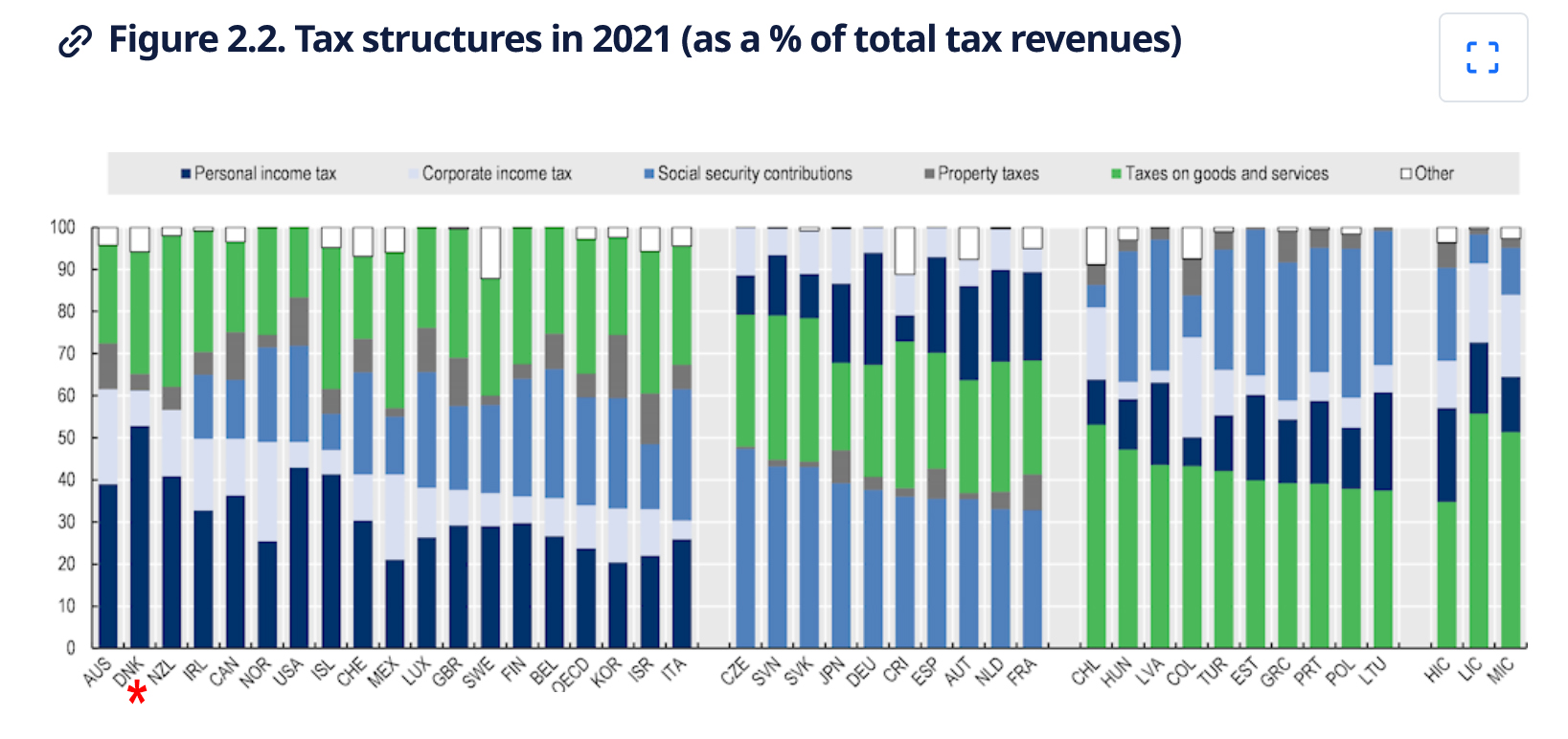

With regards to the composition of tax, 18 OECD countries (including New Zealand) primarily generate their revenues from income taxes, including both corporate and personal taxes. Ten OECD countries relied most heavily on Social Security contributions, and another 10 derived the majority of the revenues from consumption taxes, including VAT, (GST). Notably, taxes on property and payroll taxes contributed less significantly to the overall tax revenue mix in OECD countries during 2021.

Drilling into the detail

Part 3, of the report looks at the detail of the tax policy reforms adopted during 2023. This part has an introduction, then looks at five separate categories of taxes beginning with personal income tax and Social Security contributions, followed by corporate income tax and other corporate taxes, taxes on goods and services, environmentally related taxes and finally taxes on property.

As I mentioned previously, there was “a marked increase in the number of jurisdictions that broadened their Social Security contribution bases and raised rates”. Generally speaking, for high income countries personal income tax and social security contributions represent 49% of total tax revenue. Across the OECD personal income tax represented 24% and social security contributions 26% on average.

Here about 40% of all tax revenue comes from personal income tax. That’s one of the higher proportions around. Around the globe there was a bit of tinkering around personal income tax reforms mainly targeting lower income earners. This is an area where I think we need to focus any future reforms.

We have just (partly) adjusted thresholds for inflation and interestingly, I see that during 2023 quite a few jurisdictions did increase thresholds for inflation. For example, Austria updated its automatic inflation adjustment mechanism to counteract inflation, pushing workers into higher brackets. Meanwhile Australia increased its threshold for its Medicare levy to ensure low income households continue to be exempt, given that inflation has led to higher normal wages.

Corporate income tax rates are on the rise

Substantially more corporate income tax rate increases and decreases were announced or legislated by jurisdictions in 2023. Six jurisdictions increased their corporate tax,four of those did so by at least two percentage points. Türkiye increased all its corporate tax rates by five percentage points.

Whenever there are discussions about reforming our tax system, the issue of reducing our corporate tax rates will come up. With a 28% rate we are at the higher end of the corporate tax rate scale. There is potentially some scope, but as economist Cameron Bagrie has noted any such decrease needs to be part of a broader range of changes.

An example of such a change was the introduction of a general capital gains tax by Malaysia for all companies, limited liability partnerships, cooperatives and trusts from 2024.

Picking out of the details something which I know businesses here would look at with a certain amount of envy is more generous depreciation allowances. The UK, for example, has permanent full expensing for main rate capital assets as it’s called and a 50% first year allowance for special rate assets. Australia has also increased its thresholds for effectively fully expensing items for small businesses. Around the world there’s a whole range of incentives for R&D and environmental initiatives.

We have just limited the limits for residential interest deductions but it’s interesting to see that Italy abolished its allowance for corporate equity provision. Meantime Canada has new restrictions on net interest and financing expenditure claimed by companies and trusts.

Taxes on goods and services (VAT/GST)

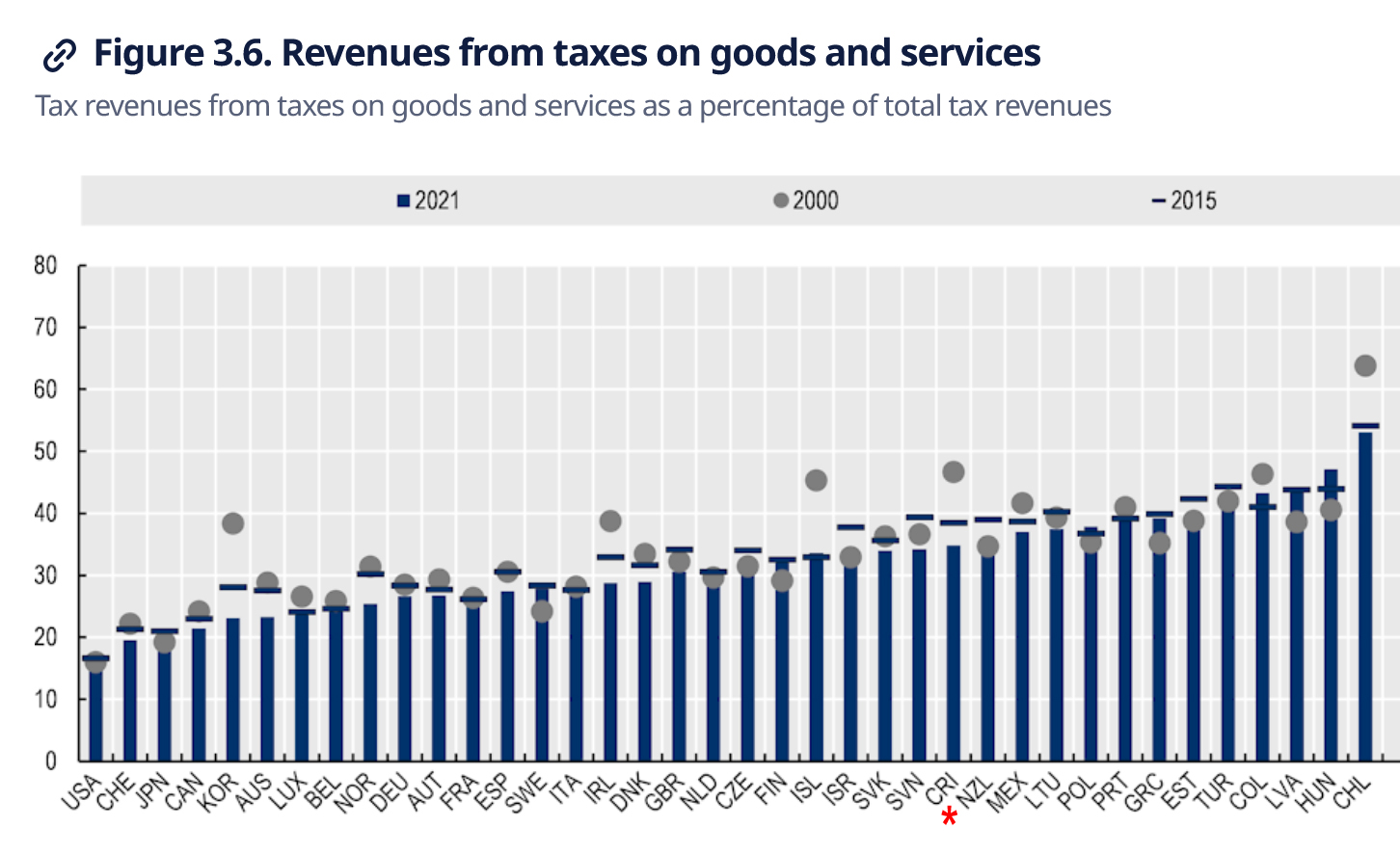

In the VAT/GST space, in terms of revenue from taxes on goods, although we have one of the most comprehensive GST systems in the world, New Zealand was only twelfth in the OECD for the percentage of tax revenue from goods and services as a percentage of total tax revenues. GST raises just over 30% of total tax revenue here, whereas Chile raises over 50%. This is quite interesting given how comprehensive our GST system is. It might mean that there is scope to expand the the rates of GST further. (Six countries including Estonia, Switzerland and Türkiye did so in 2023). But any government doing so should do so as part of a total tax switch package.

We discussed GST registration thresholds a couple of weeks back. During 2023 seven countries increased or planned to increase their VAT registration threshold. I was very interested to discover that Ireland has a split VAT registration threshold treatment: the registration threshold for the sale of goods is €80,000. But for the provision of services, it’s €40,000. I’ve not seen this split before. Meanwhile Brazil is undertaking the introduction of VAT/GST, which is a huge step forward.

A stable tax policy or just less tax activism?

There’s a lot to consider in this report more than can be easily covered here. Overall, it’s incredibly interesting to see what’s going on around the world. Many of the reforms discussed here involve threshold adjustments but there are plenty of new exemptions and incentives introduced. We generally don’t get into this space, that’s possibly a reflection of a very stable tax policy environment, but also perhaps a less activist philosophy by New Zealand governments which hope market incentives will work. Whatever, the approaches it’s interesting to see what’s going on around the world and I recommend having a look at this very interesting report.

ACC crackdown

Moving on, ACC has been in the news when it emerged that it has been chasing thousands of New Zealanders for levies on income they earned while working overseas.

According to the RNZ report, ACC sent 4,300 Levy invoices for the 2023 tax year to New Zealand tax residents who had declared foreign employment or service income in their tax return. The issue is that the person was often overseas at the time the income was earned and in some cases the the person has probably incorrectly reported the income in their return.

It’s an interesting issue and coincidentally, it so happens that I’ve just come across a couple of similar instances. My initial view is there seems to a bit of a mismatch between the relevant income tax legislation and the legislation within the Accident Compensation Act 2001. Watch this space on this one because I’m not sure the matter is entirely as cut and dried as ACC considers.

Inland Revenue responds to social media criticisms

A couple of weeks back, we covered criticism of Inland Revenue for providing the details of hundreds and thousands of taxpayers to social media platforms. It had done so as part of various marketing campaigns targeting people who owed taxes and Student Loan debt in particular.

Inland Revenue has now responded by putting up a dedicated page on its website, referring to customer audience lists.

In its words “social media is just one channel we use to reach customers. It is very effective at reaching people where they are.” As I said in the podcast Inland Revenue’s dilemma is it has to go to where the people are which is on the social media websites. In order to reach out to them it’s going to have to provide certain data. To reassure people the new page explains how it uses custom audience lists and what data is provided.

They do upload a list of identifiers such as name and e-mail addresses, which is then ‘hashed’ within Inland Revenue’s browser before being uploaded to the social media platform. This is where I think the tech specialists have raised concerns that the hash technique is not as secure as Inland Revenue thinks.

Australia – the Lucky Country again

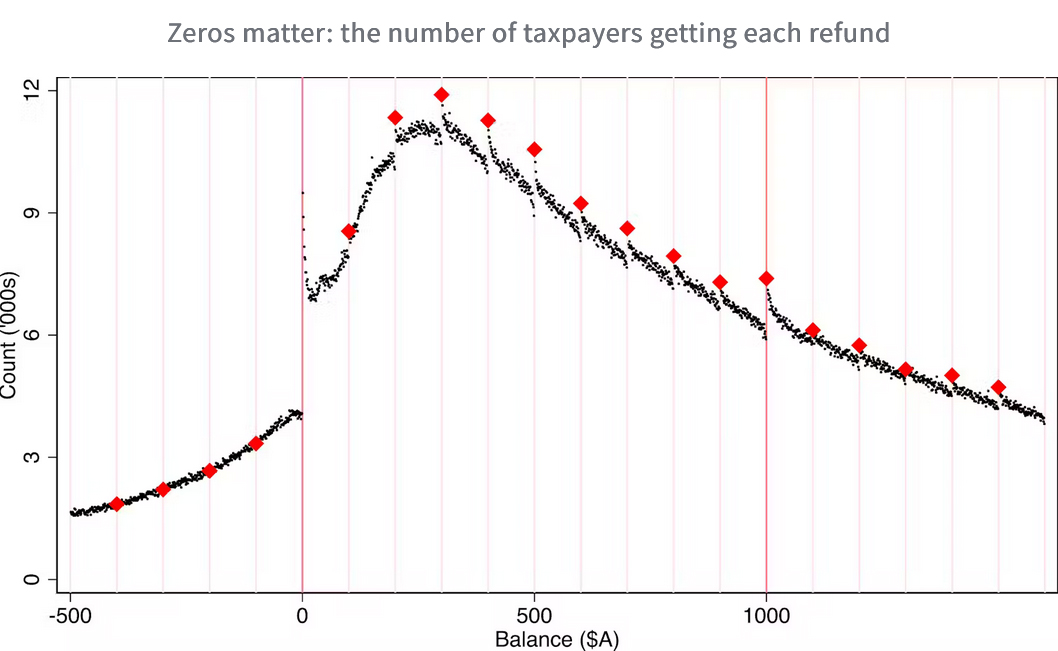

And finally, an interesting story from Australia about tax refunds. A research team at the Australian National University’s Tax and Transfer Policy Institute discovered a “striking” number of returns generating round number refunds (basically any digit ending in zero). The unit examined 27 years of de-identified individual tax files and found far more refunds of exactly $1,000 than of $999 or $995.

The unit concluded these returns are more likely to be driven by efforts to evade and minimise tax and are costly for the Australian Tax Office to audit such as work related expense deductions. Unlike New Zealanders, Australians can claim deductions on their tax returns. Somewhat concerning to me as a professional is that zeros in tax returns prepared by agents were twice as common as those prepared by taxpayers.

What this article is driving at is that some of the complexity of the Australian system results in the system getting gamed. Back in February you may recall Tracey Lloyd, Service Leader, Compliance Strategy and Innovation at Inland Revenue was a guest on the podcast. Based on our discussion and my own observation I would have confidence that Inland Revenue would not get caught out the same way thanks to the Business Transformation programme. As Tracy recounted, Inland Revenue can track live changes and they can see people just trying to square the return off to what they regard as an acceptable number.

Anyway, it’s an interesting story. It shows the differences between our tax system and that of Australia, but it does seem a little rich that not only can you earn more in Australia, but you get bigger refunds.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

In the same week as Public Service Minister Nicola Willis directed department bosses to tighten up on working from home arrangements, it’s a little ironic to see Inland Revenue release a draft consultation on the topics of deductions for expenditure and travel by motor vehicle between home and work and when an employer provided motor vehicle is subject to fringe benefit tax (FBT) for travel between home and work.

These were released alongside some interesting commentary from Inland Revenue that it is currently reviewing FBT, so what is set out in the draft consultations may change, but as Inland Revenue note, it gets a lot of questions on the topic. With regard to this FBT review my understanding is we may see something relatively soon. I think given the outcome of the Inland Revenue’s regulatory stewardship review of FBT and what the Minister of Revenue has said previously, it’s likely this review with look at simplification measures.

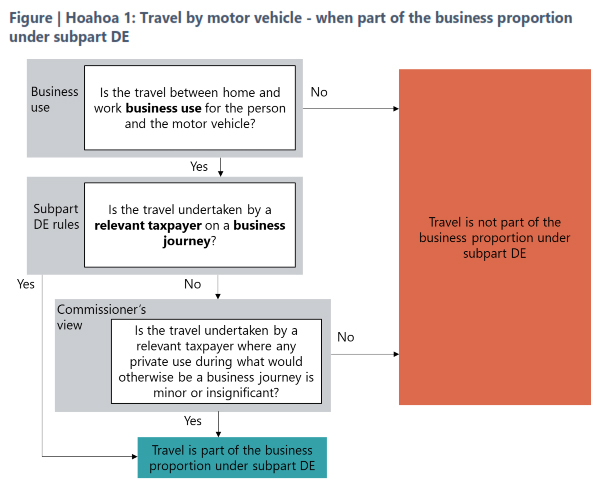

There are actually two consultations which will replace the previous interpretation statement IS3448. The topic is quite involved, because the two draft consultations run to 111 pages of commentary and examples. Fortunately, as is now the common practise, each draft consultation is accompanied by fact sheets, each containing a very useful flow chart to help people work their way through the maze.

The deductibility of motor-vehicle travel between home and work

The first draft interpretation statement deals with the question of deductibility of travel by motor vehicle between home and work which is set out in Subpart DE of the Income Tax Act 2007. What that subpart does is limit deductions for motor vehicle expenditure to the business proportion of the expenditure. It generally applies to self-employed taxpayers and partners in partnerships, but it can also apply in some circumstances to close companies and look through companies.

The basic position is that a journey is deductible if it’s a business journey, but to be a business journey and deductible, the whole journey must be undertaken for the purpose of deriving income. This is actually slightly different from the general deductibility provision for tax, which allow deductions quote to the extent to which they are incurred in deriving gross income. By contrast, this the provisions in Subpart DE are very specific it’s got to be a business journey if it is to be deductible.

Four exceptions

Generally speaking, and it’s probably no surprise here, travel between home and work is viewed as private. But there are four exceptions as a result of case law. Firstly, where the vehicle is necessary for the taxpayer to transport goods and equipment that are essential for their work between their home and workplace and for use both at home and in their workplace.

Now secondly, the taxpayers work is itinerant, which means that the taxpayer works at different locations during the workday and the sequence of where they work and how much time they spend is unpredictable and varies. It’s therefore not practicable for them to carry out their work without the use of a vehicle.

The third case is where a taxpayer is responding to emergency call outs and does so from home. And finally, and this is increasingly relevant, the taxpayer’s home is a workplace or base of operations for the purposes of travel to and from work.

This latter point is where we’ll probably see a lot of discussions and arguments. In order for a home to be treated as a workplace or base of operations the role requires a significant proportion of a person’s work to be spent working at home. I think it’s most likely to apply to owners of businesses who may be working between two places, but senior employees who might be required to make international calls in the evening, they may will be covered.

What’s a business journey?

A business journey is one primarily carried out for business purposes. Case law allows an overall journey to be treated as two journeys if there is a stop in between. It’s possible that one part represents a business journey, and the other part is private.

Furthermore, case law also said that some incidental private use does not mean a journey is prevented from being a business journey. Under the draft Inland Revenue consider that insignificant private use can’t exceed either approximately 5% of the total journey and approximately two kilometres.

The consultation also deals with the issue of what if vehicles are taken home for security purposes or, as is now more common, it’s an electric vehicle taken home to be recharged. Either of those circumstances are not sufficient in themselves to make the relevant journey between home and work a business journey. There have to be other factors at play, such as the exceptions we’ve previously mentioned or that home represents a workplace.

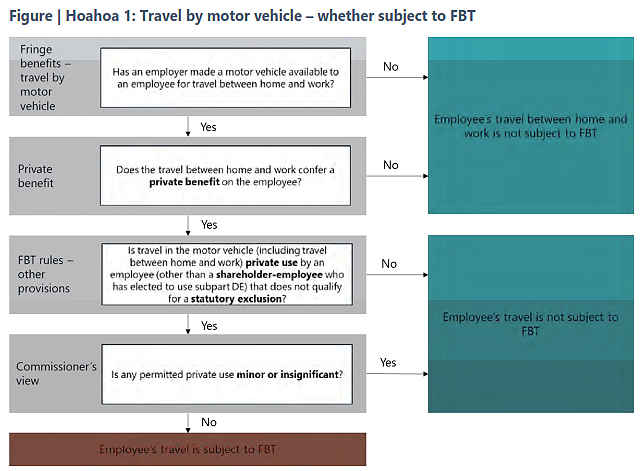

When does a fringe benefit arise?

The second interpretation statement and supporting fact sheet considers the question of when a fringe benefit arises when an employer provided motor vehicle is used for travel between home and work. The position is pretty straightforward: if a vehicle has been provided for private use, FBT will apply. In this context private use would include the use of the vehicle for travel between work and home and work. If a employee has a employer provided vehicle and travels to between home and work in that, then fringe benefit will apply.

There are three statutory exclusions from FBT which would cover travel between home would work. These exclusions apply to work related vehicles (a topic the subject of a whole another interpretation statement;

Emergency calls affecting health, life or the operation of essential machinery and services; and

business trips of more than 24 hours.

If any of these exclusions apply the whole day is excluded from the calculation of FBT.

As noted above Inland Revenue is in the course of reviewing FBT, so maybe some of this might change within the next couple of years or so. In the meantime, it’s good to have this draft guidance. Consultation on this is open until 6th November.

Meanwhile progress on the international tax deal continues

Moving on, we’ve talked regularly about the G20/OECD international tax agreements on base erosion and profit sharing. This week, several jurisdictions signed a multilateral treaty which will to help the Pillar Two subject to tax rule. But the other thing that’s important which was concluded in the last few days, was a Model Competent Authority Agreement on the Application of the Simplified and Streamlined Approach to Amount B of Pillar One. This agreement will provide a framework to enable jurisdictions to comply with what’s expected to be the final format of the rule of the Pillar One and Pillar Two agreements.

However, progress has slowed right down since October 2021 when 135 jurisdictions announced that they were accepting the two-pillar solution. With tax, the devil is in the detail and there is a lot of detail and devil to work through.

I think the other thing that should be kept in mind is that the US Presidential and Congressional elections happening in November will determine how much further progress will happen. As previously noted, the likes of Meta and Alphabet are none too keen on what’s proposed here and their lobbyists have the ears of plenty within Congress. We’ll just have to wait and see. But in the meantime, the deal seems to be inching forward.

“The time has arrived for a capital gains tax”

Last week I covered the report from Victoria University of Wellington about comparing tax rates between New Zealanders and taxpayers in nine other jurisdictions. This week things got spicier than I would expect in this sort of debate after the CEO of ANZ Bank Antonia Watson said in the course of her RNZ interview with Guyon Espiner “the time has arrived for a capital gains tax.” This in turn provoked a strong response from both the Prime Minister and the Minister of Finance. I found this a little surprising. I would have thought they’d just let Ms Watson make her comments and move on, but it certainly adds to the headlines.

CGT the most likely option

Following on from Antonia Watson’s remarks, I spoke to RNZ’s The Panel on Wednesday evening about the question of a capital gains tax. Put on the spot I said I could see it happening. To expand on my answer, it seems to me that a CGT is the most likely option if we do expand the tax base, because CGTs are common in other jurisdictions and the concepts are broadly well understood. And as Antonia Watson also noted, wealth taxes on unrealised gains are deeply unpopular with those that would be affected.

The interview with Antonia Watson is well worth listening to. One of the things I found quite interesting was that a couple of times she mentioned the impact of adverse weather effects. This wasn’t anything to do with tax, but she was explaining that our vulnerability to such events was a factor in why we have higher interest rates than Australia.

This circles back to the point that I made last week and again on The Panel, that the discussion around the question of capital gains tax or expanding the taxation of capital base is really around the question of how do we pay for the forthcoming costs of climate change and an ageing population? Are we raising enough tax revenue right now? If not, what are the options on the table?

What does Inland Revenue think?

Inland Revenue currently have their proposed long-term insights briefing for next year out for consultation. Susan Edmunds of RNZ picked up on this in a story on Thursday. The consultation finishes Friday 4th October, and I really do recommend reading and submitting on it.

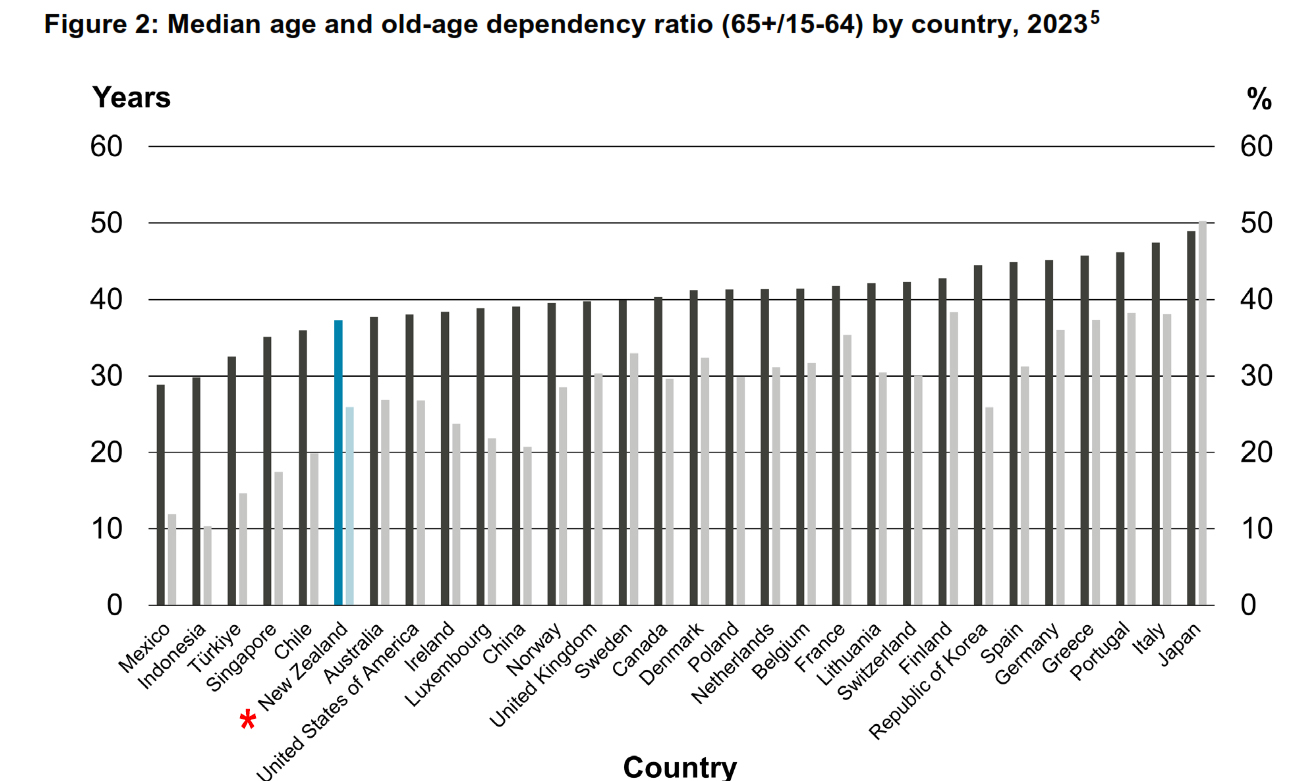

On the question of the forthcoming actual fiscal pressures, Dominick Stephens, the chief economic adviser for the New Zealand Treasury (and former chief economist for Westpac), delivered a speech on Wednesday titled Longevity and the Public Purse, which I’d recommend reading. It includes plenty of graphs illustrating the difficulty that we are facing. Our population is ageing, which is well known and the median old age dependency ratio is rising, although as the speech notes thanks to strong population growth it’s not as bad as other jurisdictions which means we are at the lower end of that range.

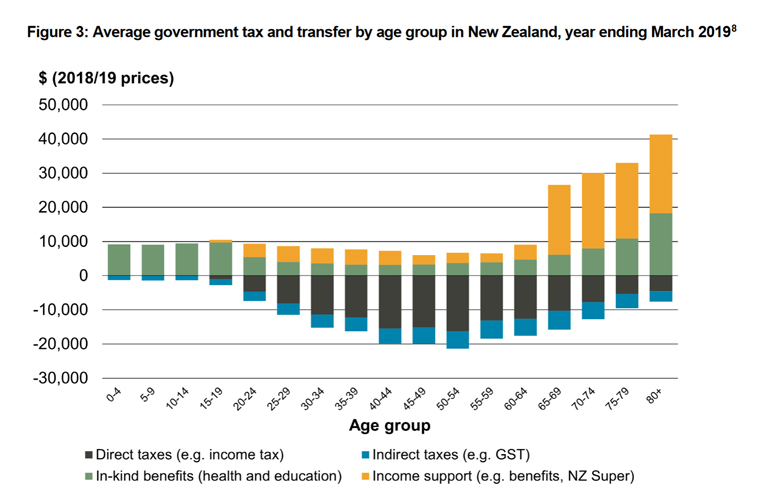

There’s a particularly telling graph about the average government tax and transfer by age group in New Zealand, for the year ended 31 March 2019

As can be seen above for the 65 and over age groups the transfers from Government rise significantly. These are the age groups which is where the debate about sustainability arise, as Dominick Stephens comments:

“Since 2006, the Treasury’s Long-term Fiscal Statements have repeated the message that our fiscal settings are not sustainable over the long run given the impact of population ageing.”

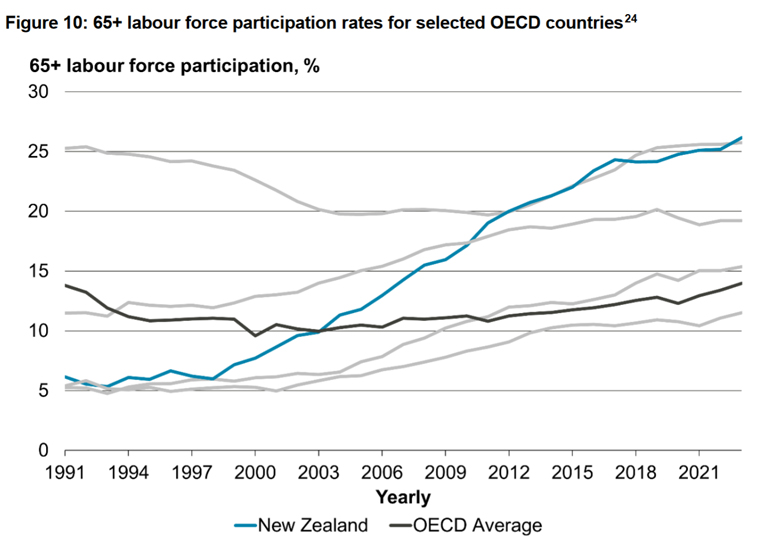

Over the period since 2006 some interesting developments have somewhat ameliorated the potential impact. Interest rates, for example, have been lower than were predicted in 2006, while population growth has been higher.

One of the more extraordinary developments since 2006 is labour force participation for 65 plus age groups has dramatically increased. Consequently, we’ve gone from being amongst the lower labour force participation rates to one of the highest.

All things being considered, there are difficult choices to be made and the question of whether more revenue is necessary is a question which isn’t going to go away.

“There is no silver bullet: none of the policy options we modelled in 2021 was large enough to stabilise debt on its own. This means that governments will need to likely draw on multiple expenditure and revenue changes to close the fiscal gap.

Some savings can be made from a greater preventative focus and reducing inefficiencies but making substantive savings is likely to require some tough choices around entitlements. This would have come with trade-offs, particularly for groups of the population who already face challenges accessing health services.”

Governments could also choose to raise additional revenue, in fact as Dominick remarked “successive increases in taxes over time would be required unless actions were also taken to manage demographic expenditure pressures.”

So tough fiscal choices ahead. I note in the comments on last week’s transcript some noted ‘well, wait a minute, why don’t we try and reduce expenditure?’ That’s certainly a driver for the current Government. But I think what Dominick Stephens and Treasury are saying, addressing the fiscal pressures will be a two-part process. We will need to both reduce costs and raise revenue. So, this debate over capital taxation isn’t going to go away soon and will continue. I expect I’ll be asked plenty more times to comment.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week, as part of its continuing drive to increase compliance, Inland Revenue released an updated property tax decision tool.

What this does is help people work out when a property might be taxable under any of the land taxing rules, including the bright-line test. It’s been updated to take account of the bright-line test changes which took effect on 1st July this year.

The growing issue of helping families into housing – what are the tax implications?

Generally speaking, since 1st July, the bright-line test only applies where the end date for sale as determined under the rules is within two years of when the property was deemed to have been acquired. The aim of the tool is to work through all the various scenarios that might apply. So that’s something worthwhile, and I think we’re going to see more of people wanting to make more use of this because of a developing trend around shared home ownership where people who are not necessarily couples are coming together to purchase properties. There are also families wanting to help elderly parents.

We’re seeing some very interesting scenarios develop as a result. One of those scenarios was the subject of last week’s Mary Holm’s column for the New Zealand Herald.

“We’ve bought my wife’s parents’ house. They had a small mortgage on it, with no income, just super, coming in. They didn’t have enough money to keep paying the mortgage, hence they were going to start a reverse mortgage to keep things afloat.

If they sold the house they would’ve struggled to get into a retirement village and stay near family etc. So we bought the house so they don’t ever have to leave – so let’s say they will be there for at least another 10 years.

They pay us $750 rent per week. We took out a 30-year $800,000 mortgage, with just the interest on it at $1977 a fortnight, so we are topping up mortgage payments as the rent does not cover it. We also pay the rates, insurance and any maintenance costs.

How do we treat this in terms of any possible tax or claims as such?”

Mary asked Inland Revenue and me for comment. Notwithstanding that a net loss was foreseeable, my advice was you never always know what the full story is as there may be a detail which for whatever reason, the correspondent has overlooked. The basic approach I took was you should report it. Inland Revenue were much of the same view but noted that any excess deductions would be ring fenced.

As I mentioned to Mary, I think we’re going to see a lot more of this. Because they’re coming from both ends of the generational spectrum. In this case we’ve got the elderly parents wanting to stay near family and then at the other end, young people trying to get on the housing ladder.

Is shared home ownership an answer to housing affordability?

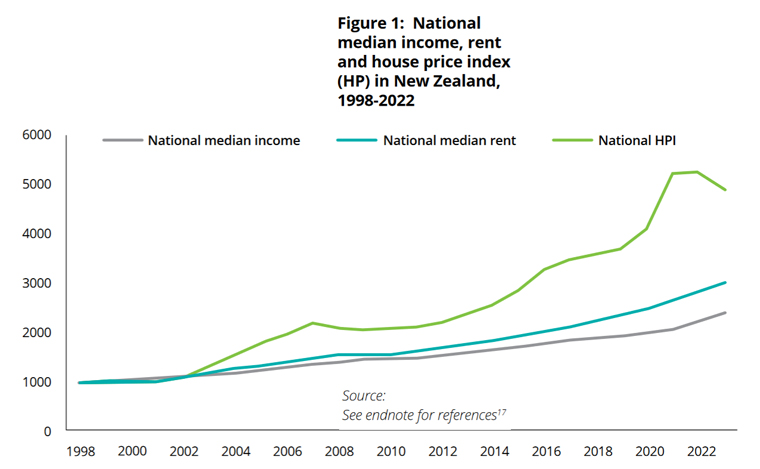

Over the last 20 years or so I’ve seen the practice develop quite rapidly of parents, grandparents and other relatives helping their children or grandchildren get their foot on the property ladder. This was the subject of an interesting report on shared home ownership released by Westpac called Next Step Forward. The report notes that the housing market is increasingly difficult, and “the home ownership dream is increasingly out of reach for some New Zealanders”. The report’s analysis is that shared home ownership will become increasingly common and how might that develop.

The report describes the housing market as “distorted”. To give you some idea of the scale of the problem, the report notes “As of February 2024, the median house price was 6.8 times the median income compared to 5.4 times in 2004 and roughly 2.3 times in 1984.” So over 40 years, the median house price relative to median income has practically trebled.

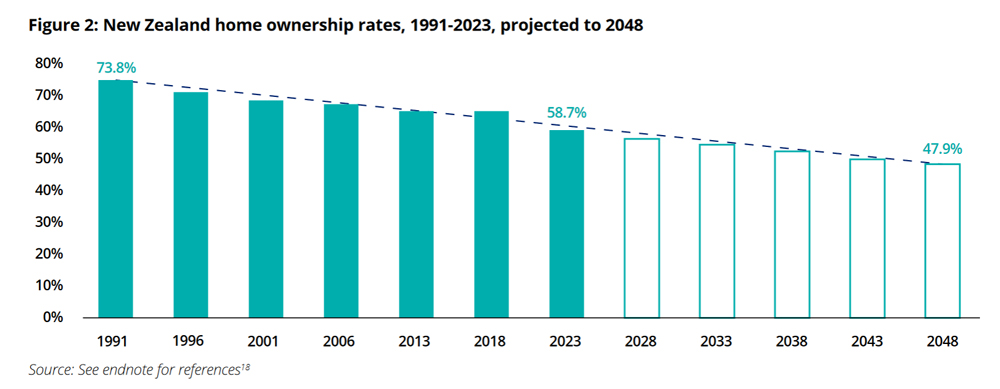

The report also notes that home ownership rates in New Zealand have been declining steadily since peaking in 1991 at 73.8%. They’re down to 58.7%, so a 15 percentage point drop over 30 years is pretty substantial. But the report projects that within 25 years, the proportion of homeowners will have dropped to 47.9%. (The report notes the outlook is even worse for Māori and Pacific peoples, where the home ownership rate is lower, at 47% and 35%, respectively, as of 2023).

What are we going to do about this? Well, as the report suggests shared home ownership is going to become more common. This in turn is going to trigger all sorts of tax issues. Which is why something like Inland Revenue’s property tax tool is handy. The report, incidentally, doesn’t really discuss tax other than mentioning tax free capital gains do play a part in people’s investment decisions and may have an impact on the housing market

There’s no real short answer to this issue. Raising incomes would be one thing, freezing or slowing the rate of house prices would be another, and building more homes would be a vital third factor. Pulling all this together is a huge problem and each solution comes with secondary effects.

International tax deal in trouble?

Moving on, an equally complicated scenario and one we’ve been covering for several years, is the question of the taxation of multinationals. Back in 2021, the OCED/G20 declared a breakthrough international tax deal over the taxation of the largest multinationals in the world. The deal proposed a Two-Pillar solution over the question of taxing rights. Ultimately this is where the idea of a minimum corporate tax rate of 15% emerged.

Agreeing in principle was one thing, but the negotiations have been going on since then and increasingly it seems to be that they’re running into difficulty. A key 30th June deadline has now passed, and it appears that some governments are starting to lose patience with the whole process.

One of the ideas behind the agreement was to head off the implementation of digital services taxes (DSTs). As part of the process these DSTs were put on hold by several jurisdictions, including the UK, Austria, India and others. In the meantime, as negotiations have dragged on, other countries such as Canada have said “Well, we’ve had enough of this, we’re going to go ahead and impose a digital services tax.”

Meantime, the United States whose companies such as Alphabet and Meta are at the heart of the issue have threatened retaliatory tariffs on countries imposing DSTs. Nobody wants a trade war, but someone has to blink in terms of getting a deal past this impasse. So, they’re continuing to negotiate, even though the deadline theoretically has expired.

Time to go back to first principles?

On the other hand, as Will Morris, PWC’s Global Tax Leader points out in this short video. Maybe we should just go back to first principles instead of trying to hammer out a deal through the existing Pillar 1 process which some consider is not really fit for purpose.

It’s not a bad idea but it would delay further progress in the matter, and I think that’s where governments who’ve got elections to win may not be prepared to wait much longer. I think generally the public is a bit antsy about the question of corporate taxation. As I noted last week, when we looked at the OECD’s latest corporate tax statistics, statutory corporation tax rates have pretty much stabilised after 20 years of falling.

However, there are still substantial gaps in public finances as a result of first the Global Financial Crisis, then the pandemic and increasingly we’re having to deal with the impact of climate change as well. When the insurers are leaving the market, who picks up the tab? In my view, that’s going to be we the taxpayers.

There will be pressure to get some sort of deal across the line, but I also think although we may see corporate tax rates elsewhere in the world rise, I think with our 28% rate, we haven’t really got much room for manoeuvre for an increase at this point.

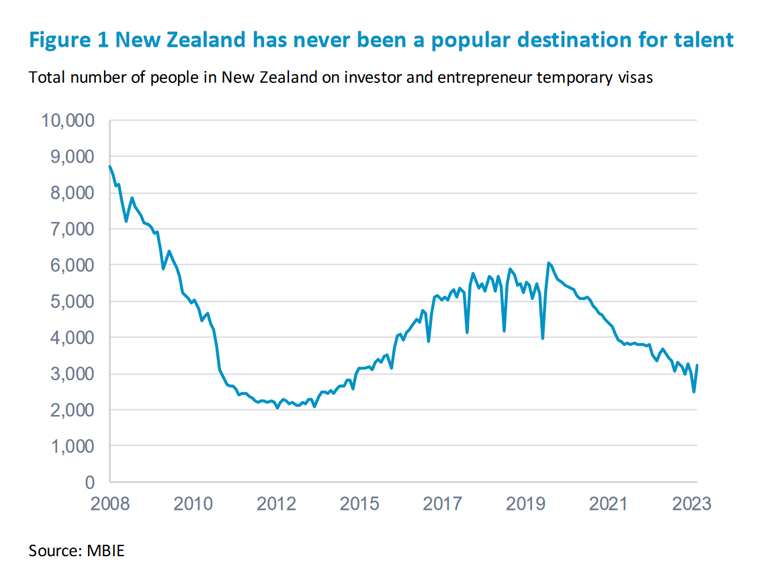

A place where talent does not want to live?

Finally, the New Zealand Institute of Economic Research released a fascinating report on Thursday. Provocatively titled The place where talent does not want to live, it looks at the question of New Zealand’s immigration policy and how that sits alongside our international tax regime.

The report was prepared for the American Chamber of Commerce in New Zealand, the Auckland Business Chamber, the Edmund Hillary Fellowship and the NZUS Council. It’s a fascinating document because it pulls together points, we don’t always hear discussed when we’re looking at immigration policy, how does our tax system interact with that policy?

The report notes that conceptually, we have developed tax rules which make sense in a tax context. However, they lead to wider issues once they start operating in a broader context. In particular the report really focuses on the Foreign Investment Fund (FIF) regime which it considers disadvantages many investors who come here hoping to use their skills and their capital to help build the economy and the tech sector in particular.

I’ve seen comments on this topic previously from entrepreneurs, and it’s easy perhaps to be cynical and say, “Well, they’re speaking out of self-interest” but 40 years of tax experience also tells me that behavioural responses to tax are very observable and policymakers should pay attention to such responses.

An in-depth examination of the Foreign Investment Fund regime

What makes this report particularly interesting are the authors, Julie Fry and Peter Wilson. Julie is a dual New Zealand and U.S. citizen who in her bio notes that “her location and financial decisions have been impacted by the tax rules covered in the report.” Peter was Manager of International Tax at the New Zealand Treasury from 1990 to 1997 and then Director of Tax Policy from 1998 to 2002. As such “He was responsible for advising the government on many of the tax issues contained in this report.” Consequently, outside of anything prepared for a tax working group, this report is one of the most in-depth examinations we’ve seen of our international tax regime and FIF regime.

The report notes that although we have a fairly open flow of migrants, “New Zealand has never been a particularly popular destination for talented people”. (Interestingly, we have no data on how long people on the various investor and entrepreneur visas stay).

As the report notes there’s a competition for global talent and New Zealand is not attracting as many as we would like. We should therefore be thinking hard about the implications of this.

The report hones in on the FIF regime as being a particular problem for many investors because of the way that it taxes unrealised gains. This creates a problem of a funding gap where an investor is expected to pay tax on an investment which very often isn’t producing cash because as a growth company cash is being reinvested. (By the way, this is often a common argument against wealth taxes).

As the report notes, “New Zealand’s tax rules were not designed with the idea of welcoming globally mobile talent in mind.” For example, as Inland Revenue’s interpretation statement on residency makes clear it’s deliberate policy to make it’s easy to be deemed tax residency in New Zealand, and hard to lose. This has long term flow implications because as the report points out, people who would perhaps want to commit to New Zealand are reluctant to do so because of the tax consequences of doing so.

Chapter Three is the very, very interesting section of the report as it explains the development of our current international tax regime and the rationale for the various FIF regimes and their design. The overall objective was to protect the tax base, but they didn’t really think about what was happening with migrants. As Ruth Richardson and Wyatt Creech then the respective Minister of Finance and Minister of Revenue explained in 1991:

“The objective of the FIF regime, where it applies, is to levy the same tax on the income earned by the FIF on behalf of the resident as would be levied if the fund were a New Zealand company. Because the FIF is resident offshore with no effective connection with New Zealand, the only way of levying the tax is on the New Zealand holder.”

This is conceptually correct from a tax perspective but as the report keeps pointing out, it doesn’t really take into account what happens with migrants who made investment decisions long before they arrived in New Zealand only to find their accumulated savings are being taxed here under the FIF regime. I have a similar problem with the taxation of foreign superannuation schemes. Although the tax treatment conceptually ties in with our system, it seems to me we are effectively taxing the importation of capital and this paper is basically saying the same thing in relation to FIF.

How much tax does the FIF regime raise?

Section 3.5.1 on page 26 of the report has an interesting analysis of how much revenue the FIF regime raises. Because our tax reporting statistics aren’t very detailed, the answer is we don’t really know. The report concludes

“The high-level finding is that the level of overseas investment is small compared to total financial assets at the national level. Portfolio foreign investment is, in some years, one-thousandth of domestic investments. This suggests that the current FIF tax base is likely only to make a minor contribution to direct revenue.”

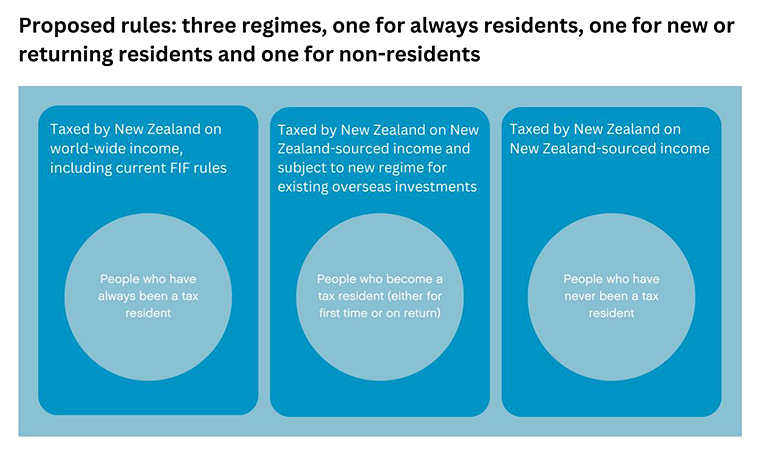

A suggested reform

The report concludes that in an international context where we were trying to attract the right talent, maybe we should be looking at the FIF regime. What it suggests is to separate the tax treatment of people who have always been tax resident from those of new and returning tax residents. The existing FIF rules would continue to be applied to those have always been New Zealand tax resident. Meantime a new regime should be designed for new and returning tax residents.

The report does touch on the question of a general capital gains tax regime (which could be an answer) but considers the development of a comprehensive CGT is a long term political consensus building project.

In discussions I’ve had with other colleagues on this matter we’ve noted how our American clients in particular are very affected by the current FIF regime. As American citizens they are required to continue to file American tax returns and are therefore subject to capital gains tax. This creates a mismatch between when they pay New Zealand income tax and the final US tax liability on realisation. Although the FIF regime creates foreign tax credits for US tax purposes, clients are frequently not able to utilise the foreign tax credits.

As people told the report authors this is extremely frustrating and there is no doubt that people are upping sticks and moving because of it. (I’ve also seen other clients switch into property investment instead).

Overall, this is a very interesting and highly recommended report considering the intersection of tax driven behaviour with wider economic issues.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last Saturday, the ACT party leader David Seymour appeared on Newshub Nation and suggested that Inland Revenue be used to deal with the gangs.

He believed the powers currently being used by Inland Revenue as part of its high wealth individual research project could equally be applied to deal with the gangs. It did make for some entertaining viewing, as interviewer Rebecca Wright was more than a little incredulous at the suggestion that gang members wearing patches would happily submit to filling out questionnaires. On the other hand, the notorious mobster Al Capone, was ultimately jailed for tax evasion so the use of Inland Revenue against organised crime is not that unreasonable a suggestion.

Mr. Seymour does seem to have misunderstood the nature of the powers currently being used by Inland Revenue as part of its high wealth individual research project. Those powers have been deliberately limited so that the information gathered is solely for research purchase purposes. They are therefore more prescribed than the general powers available to Inland Revenue. I also think Mr. Seymour was overstating how much of a sanction non-compliance with the high worth individual research project would be.

Now Inland Revenue does indeed have some extensive powers of information request and where appropriate, search and seizure. And if you want an example of how it can apply those rules that can be found in the case of Tauber v Commissioner Inland Revenue.

In this case, Inland Revenue was investigating a former accountant who it believed was suppressing income. After its initial information requests were not satisfactorily answered in its view, Inland Revenue then decided to use the powers available to it under Section 16 of the Tax Administration Act. It carried out simultaneous search and seizure operations at six separate locations, including a boat shed.

Mr Tauber responded by making an application for judicial review, claiming that the various Section 16 warrants were too widely drawn and not specific enough. The application also questioned whether the searches were necessary for carrying out the Commissioner’s functions and if the searches were carried out in an unreasonable manner. Unfortunately for Mr Tauber and the other claimants the courts upheld Inland Revenue’s use of its powers.

The case illustrates the extensive powers available to Inland Revenue. However, what it also illustrates is that applying those powers is a very intensive operation requiring a considerable number of resources. If you’re raiding six properties simultaneously with teams of investigators, you’re talking about an operation which may have involved somewhere between 40 and 50 people. Now if you think about dealing with gang members Inland Revenue would also want to be raiding several premises simultaneously. Therefore, that would require considerable resources from it and no doubt police officers to be available in case matters escalated.

It’s therefore questionable whether Inland Revenue would actually have the resources to carry out major investigations into gangs. And although tax evasion is a criminal offence, Inland Revenue would probably be of the view that the powers available to police and other authorities under the anti-money laundering legislation, which have been strengthened this week, mean those agencies are more appropriately deployed to deal with organised crime.

This isn’t to say that Inland Revenue wouldn’t pass up the opportunity to investigate tax evasion involving gangs if it felt considerable sums were involved. But as the Tauber case shows, using its full range of investigatory powers requires considerable resources, which ultimately, I think, Inland Revenue might feel better used elsewhere. In other words, “Nice idea, but yeah nah.”

Update on OECD tax reform

Moving on, the OECD delivered its latest update on the status of the international tax reform agreement to G20 finance ministers and central bank governors a couple of weeks ago. This included a progress report on the status of Pillar One, which is the proposal to ensure that market jurisdictions can tax profits from some of the largest multinational enterprises.

The OECD Secretary-General presented a comprehensive draft of what these proposed technical model rules will be for Pillar One. These are now going to go out for public consultation between now and mid-August. The intention then is to finalise a new Multilateral Convention by mid-2023 for entry into force in 2024.

In addition to updating the status of the Multilateral Convention to implement Pillar One, the Secretary-General’s Tax Report also gave an update on how an implementation of the OECD transparency agenda (the Common Reporting Standards on The Automatic Exchange of Information). And the latest update is that information on at least 111 million financial accounts worldwide covering total assets of nearly €11 trillion was exchanged automatically between tax administrations in 2021. And later this year, the OECD will finalise a new crypto-assets reporting framework, which will be included as part of the Common Reporting Standards. So things are moving ahead even if they’re going more slowly than people had expected.

In relation to the Pillar Two work, which introduces a 15% global minimum global minimum corporate tax rate, the technical work on that is largely complete and an implementation framework is to be released later this year to facilitate the implementation and coordination between tax administrations and taxpayers. All G7 countries, the European Union and several other G20 countries, along with several other economies, have scheduled plans to introduce the global minimum tax rules. New Zealand hasn’t reached that stage but consultation on the matter has just ended, so we may see something later this year.

IRELAND’S TAX RISKS

Now one of the ideas behind the Pillar Two global minimum corporate tax rate is to try and stop tax competition driving corporate tax rates lower. Now, one of the poster child’s for lower corporate tax rates is Ireland. And last week I mentioned Ireland’s strong GDP per capita growth in recent years. This appears in part to be a by-product of multinational and multinational investment in Ireland, attracted by Ireland’s low corporate tax rate of 12.5%.

Now tax is always full of unintended consequences and this week the Irish Finance Ministry highlighted a potentially huge downside of this policy for Ireland.

Apparently just ten multinational firms pay over half of Ireland’s corporate tax receipts. These are expected to be between €18 and €19 billion this year, up from an estimated €16.9 billion forecast just three months ago. And by the way, that’s nearly a five-fold increase in the last decade.

Now, on the face of it that all sounds good. But John McCarthy, the Irish finance ministry’s economist, warned that the fact that just ten multinational firms pay more than half of honest corporate tax, represents “an incredible level of vulnerability” for the Irish economy, as a shock, which impacted on the multinational sector would have severe fiscal implications for Ireland. I understand something like one in nine Irish employees are employed by multinationals such as Facebook, Google and Pfizer. Therefore, the fallout from a shock in this sector could be huge for Ireland.

Mr. McCarthy told reporters the level of concentration in such a small number of firms is something he has never seen in any other economy. He was therefore more worried about the overreliance on these types of firms than the impact of the global overhaul of corporate tax regimes could have on Ireland’s position as a hub for multinational investment. Ireland power. The same report estimates that Ireland’s tax take would be affected negatively by about €2 billion over the medium term.

Irish Finance Minister Paschal Donohoe then chipped in saying he has long shared the concerns McCarthy outlined. He said the best way to manage the risk was to return to the pre-pandemic position where corporate tax receipts are not used to fund permanent spending. This seems an incredible admission that a low corporate tax rate is actually not sustainable over the long term. So that’s something to pause to think about when you hear talk about corporate tax cuts.

By the way, these concerns of the Irish finance minister and the Finance Ministry might explain why Ireland didn’t oppose the proposed 15% global minimum tax rate. I suspect that on the quiet this represents an opportunity for Ireland to raise its corporate tax rate without too much fuss. It would be interesting to know the level of concentration here in New Zealand. I guess the big four Australian banks and the New Zealand Superannuation Fund would represent at least 20% of the corporate income tax take.

IRD BACK LIQUIDATING DEFAULTERS

Moving on, a quick follow up from last week’s items about Inland Revenue’s enforcement and collection activity increasing. As of 30th June 2021, 140,000 taxpayers had arrangements with Inland Revenue covering $3.7 billion of tax. Now, Inland Revenue would be keen to ensure those numbers don’t continue to grow. Historically, what it’s done is taken strong enforcement action including initiating liquidations. Apparently about 70% of all high court liquidations were initiated by Inland Revenue. However, during the pandemic, as part of its more sympathetic response, that number fell to just under 30%.

However, I’ve been informed that since April that there’s been a huge escalation in Inland Revenue activity in the High Court and liquidation proceedings. So that’s the clearest sign of Inland Revenue’s increased focus on debt collection and a clear warning to all those out there that if you if you’re in trouble you need to front up and try and make arrangements with the Inland Revenue before they take it further to the liquidator.

AWARDS FINALISTS

And finally, this week, the Tax Policy Charitable Trust has just announced its four finalists in this year’s Tax Policy Scholarship competition.

This competition is designed to support tax policy, research and thinking. Entrance is limited to those under the age of 35, and the intention is that people are asked to give ideas of proposals for reforms to our current tax system, to address potential weaknesses and unintended consequences of existing laws. Now there are three topics in this year’s competition: environmental taxation, tax, administration generally, or the powers granted to the Commissioner of Inland Revenue and to investigate for research policy purposes. (These are the powers that Mr. Seymour was referring to in his interview about tackling the gangs).

The four finalists are Daniel Doughty, a senior consultant with EY in Wellington. He’s proposing a small business consolidated reporting regime to simplify tax reporting for small companies. I think this is an excellent suggestion, so look forward to finding more about this. Our tax system expects a lot of administration from small businesses without really trying to adjust the compliance burden to help them with those processes.

The second finalist is Mitchell Fraser, a tax solicitor with Mayne Wetherell in Auckland. Mitchell is worried that the new powers granted to Inland Revenue for tax policy purposes may have unintended consequences. He’s suggesting alternative means to collect the information that’s wanted, including through Statistics New Zealand.

The third finalist is Vivien Lei, a group tax advisor with Fisher Paykel Healthcare. Vivien has got another interesting proposal to change New Zealand’s environmental practises by introducing an impact weighted tax regime. Under this model, organisations will be taxed on a net positive or negative impact on the environment. Now this is an area I’m very interested in and previous readers or listeners of the podcast will know that John Lohrentz, one of the runners up in the last competition, proposed a progressive tax on bio genetic biogenic and methane emissions in the agriculture sector. It’s therefore good to see there’s plenty of focus on this area.

And finally, there’s Jordan Yates, a senior tax consultant with ASB in Auckland, and he believes the tax policy landscape has been fractured and suffocated by political roadblocks. I don’t think he’s wrong there. Jordan’s proposing an independent statutory authority that would be responsible for the independent management of fiscal policy as it relates to the tax base. It’s an idea I’ve heard floated in other places and another one I look forward to hearing more about. This fracture is one reason why the Minister of Revenue, David Parker, has proposed his Tax Principles Act.

The finalists have all been asked to develop a 5,000-word submission on their proposal. They’ll then make a final presentation and answer questions at a function later this year in October, after which the winner will be announced.

This is a great initiative by the Tax Policy, Charitable Trust, and I look forward to hearing more about these proposals. And as we did with Nigel Jemson, the winner of the last competition and runner-up John Lohrentz we will hopefully have the prize winners on the podcast.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

It’s good to see Inland Revenue have stepped up the focus in this area because we deal with quite number of clients in this space around their international tax obligations and there is a sometimes-surprising lack of knowledge. The main guide is the form IR1246 on Offshore tax transparency. It’s relatively short at 28 pages, including a glossary and as I said, is aimed clearly at the general public.

It begins with a little section at the start about “What your taxes pay for”. I think we’ll see more and more of this as Inland Revenue rolls out various publications as part of its compliance programmes. It’s a reminder of how much tax revenue is raised and where does it go. In case you’re interested Social Security and Welfare is the biggest single amount at $36.8 billion in the year to June 2021 with Health coming in second at $22.8 billion and education third at $16 billion.

This is adopted from similar initiatives we’ve seen in other tax authorities around the world, emphasising your taxes are for the common good and here’s where your taxes are spent and here’s how they may benefit you. So that’s a deliberate policy aimed at reminding people that tax is part of the price we pay for a civilised society.

The guide explains Inland Revenue’s role within New Zealand and then works its way through the various international obligations and standards. Some of this is pretty boilerplate and well known to tax agents and advisors but possibly isn’t so well known to the general public.

And the key point that Inland Revenue is really stressing is that it has access to a number of international exchange or information exchange programmes such as an exchange of information on request through one of the various double tax agreements or international exchange agreements New Zealand is a signatory to.

Then there’s a section which would make anyone with property overseas sit up and pay attention:

We annually exchange land data with many of our treaty partners. The data we exchange is a combination of this information we obtained from the land transfer tax statements, received land information in New Zealand and our own internal tax data. We also receive similar information from some of our treaty partners, which serves as good initial intelligence with an option to follow up with further exchange of information requests during the course of more in-depth compliance work.

We actually experienced this with one client when Inland Revenue requested whether we had disclosed income from property in the United States as they had received information from the US regarding the property. We had, but it was still illuminating to see how much Inland Revenue knew.

And then there are the spontaneous exchanges of information under FATCA (the Foreign Account Tax Compliance Act), and the Common Reporting Standard on the Automatic Exchange of Information. Incidentally, the next exchange under the Common Reporting Standard is happening in September. There are the collection assistance agreements under several double tax agreements. This is something I don’t think people are really aware of Inland Revenue’s ability to ask overseas jurisdictions to go hunting for delinquent taxpayers and outstanding tax.

And then there’s the foreign trust regime’s reporting requirements. An interesting point here is that any information collected during the registration and annual return process of a New Zealand foreign trust is shared with the Department of Internal Affairs as the supervisor of trust and company service providers and the Financial Intelligence Unit of New Zealand Police. This information is shared because of their regulatory role in relation to anti-money laundering and countering the finance of terrorism.

The guide then runs through the various types of overseas income, and you can find more details in the Foreign Income Guide. This also includes taxpayers working remotely in New Zealand for overseas employers. This appears to be part of a new initiative.

One page in the guide has the header “Offshore is no longer off limits” and the guide explains Inland Revenue is involved with other international collaboration outside those agreements have already mentioned. These include the Joint International Taskforce on Shared Intelligence and Collaboration which apparently includes 35 of the world’s national tax administrations. There’s also the Study Group on Asia-Pacific Tax Administration and Research. I was not previously aware of these two organisations. So, you learn something every day.

Overall, this is a welcome and important initiative from Inland Revenue. People are now able to access easily understandable guidance as to their overseas income obligations. There’s an interesting comment that as a result of an initiative under the Common Reporting Standards, it received over 900 voluntary disclosures from people after they were advised Inland Revenue had received information regarding their overseas income. Voluntary disclosures happen regularly once people realise they have not complied with their obligations they come forward to rectify their errors.

“Leaving on a jet plane…”

Now, with the borders reopening and international travel resuming, Inland Revenue has decided to release for consultation a draft “Questions we’ve been asked” (QWBA) in relation to the deductibility of overseas expenses. This publication was actually delayed because of the pandemic as Inland Revenue thought it and we advisors might be busy elsewhere and really nobody was travelling.

This draft consultation covers the issue as to what extent can income tax deductions be claim for overseas travel costs other than meal costs? And basically, the answer is they can only to the extent they have a connection with deriving assessable income or carrying on a business. No deductions can be claimed for any part of the costs that are of a private or domestic nature or incurred in deriving exempt income. Now where the costs need to be impulse apportioned between deductible and deductible, then this must be done on a basis that is reasonable.

The draft QWBA doesn’t consider two issues: the treatment of a companion’s travelling costs which is covered by QB 13/05. And secondly, the deductibility of meal costs which is dealt with in Interpretation Statement IS 21/06.

This draft QWBA is a short document, 14 pages. It sets out the legislation, considers some of the current case law and then includes four practical examples covering various scenarios. The first is where there’s a both business and private purpose for travelling overseas. The second where there’s a business trip involving incidental private expenditure. Example three deals with someone is travelling overseas privately, but then realises on arrival there’s actually some business opportunities.

The final example deals with cancellation costs, which have not been refunded, something no doubt quite a few businesses experienced because of COVID 19. The example suggests that the cancellation fees are deductible because the costs were incurred in the course of, carrying on a business.

This is more useful guidance on a day-to-day issue which businesses and advisors are going to be encountering regularly now. It’s particularly opportune with borders reopening now, and international travel resuming.

Big Tech’s transfer pricing strategies

Now, last week I covered Google New Zealand’s December 2021 results. The same day Facebook also released its December 2021 results. These are the first results it’s released since December 2014. This is because Facebook has changed its model to now report on a country-by-country basis.

It’s interesting to see what’s gone on in the interim. Back in in 2014, Facebook paid $43,000 of tax on $1.2 million of revenue. This year, it’s reporting $6.5 million in revenue with a tax charge of $605,000. But the detail that’s of interest is what’s going on with its related party transactions as these give you a clue to the level of activity actually going on.

Facebook ‘s gross advertising income for the year to December 2021 was $88 million, which I have to say surprised me a bit as I thought it was higher than that. But anyway, these are the first concrete numbers we’ve seen for a while now.

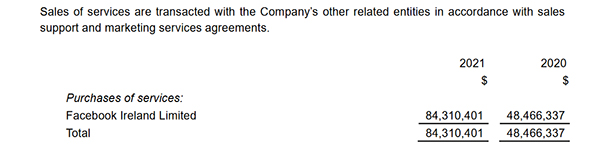

$84 million was paid to Facebook Ireland for purchases of services.

Coincidentally, Facebook Ireland’s corporate tax rate just is 12.5%. So, you can work out yourself the potential saving that could represent for Facebook.

As I said in relation to Google’s results last week, it’s possible Inland Revenue is looking at this. We know there’s a lot of review activity going on in this space. Transfer pricing, audits and investigations do take some time and we got a clue as to how long and how they might play out result when British American Tobacco released its December 2021 results.

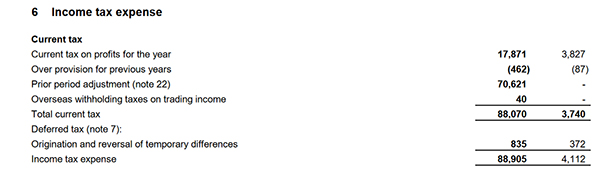

Included in these was a note that it had been engaged in an Advance Pricing Agreement (APA) process with Inland Revenue and the UK’s H.M. Revenue and Customs. This has been going on since March 2016 and it related to the combustible tobacco operations of the British American Tobacco Group. Agreement on the APA was finally reached in July 2021.

As a result, British American Tobacco New Zealand’s 2021 financial statements included a profit adjustment for prior years resulting in $70.6 million of additional tax payable for those prior years.

Now, the effect also of this agreement is that the tax payable for the December 2021 year rose from $3.8 million in the previous year to over $17.8 million. This increase illustrates the impact of the reduction in what overseas associates can charge. The turnover for New Zealand was roughly similar for both 2020 and 2021 at $247 million and $251 million respectively.

A win therefore for Inland Revenue and a little bit of a windfall as well for the Government. The case does show how long it takes to reach agreement on these issues.

Funding the road network

And finally, back in New Zealand, back in March the Government cut the fuel excise duty as a cost-of-living countermeasure. That was initially for a three-month period but is now being extended for a further two months until mid-August.

And this prompted David Chaston to take a look at the fiscal impact of this.

The National Land Transport Fund (NLTF) uses the funds from fuel excise duty and road user charges for the maintenance of country’s highway network.

The NLTF has some fairly big numbers going through it: in the year to June 2020, the total amount of fuel excise duty and road user charges amounted to just over $3.7 billion. In the June 2021 year, that total rose to just under $4.2 billion. However, as of April 2022, the total expected income from fuel excise duty and road user charges was about $23 million short of target. And obviously the longer the government keeps the fuel excise duty cut in place, the lower the income for the NLFT is going to be.

David therefore raised the issue about how are we going to fund the NLTF in the future? Remember that electric vehicles are currently exempt from those user charges, but thanks in part to the government’s clean car discount and the growing availability of electric vehicles, the number of EVs is rising. When does this exemption end? Longer term as the proportion of electric vehicles in the fleet rises, the amount of fuel excise duty will fall. This has to be an accelerating trend in order for the country to meet its emissions targets.

So, how is the NLTF to be funded in the future in order to maintain the highways? It seems to me there’s only two possible answers to that; firstly, increase road user charges, which means the exemption for electric vehicles must end, probably very soon. And secondly, and this is part of a wider decarbonisation issue, shift heavier traffic which increases wear and tear on highways to other modes of transport like local shipping and rail.

So that’s an interesting dilemma for any future government to be considering. I think any sort of environmental taxation moves in this space, are really more like behavioural taxes and therefore as the behaviour you are trying to discourage, the use of internal combustion engine vehicles declines, your revenue declines.

So longer term, some thinking has to go into how are we going to fund the maintenance of our highways? And it seems to me ultimately general taxation will need to become part of the mix. Rather than being specifically funded out of the National Land Transport Fund, the taxpayer will be paying a different way through contributions from the general tax pool.

That’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time. Ka pai te wiki, have a great week.