The debate over international taxation and the so-called Two Pillar proposals has been driven largely by the G20 and the Organisation for Economic Cooperation and Development, (the OECD). But in recent years the United Nations has started to flex its muscles in this space. This is unsurprising, because the UN represents the wider world view outside the 40-odd countries which make up the G20/OECD.

All of this is behind the story that RNZ ran at the start of the week about the United Nations Committee on Economic, Social and Cultural Rights statement on tax policy. The RNZ ran this statement under the banner headline “UN Report questions fairness of GST”, in which it pointed out that GST can be regressive for low-income earners.

In fact, the UN Committee statement went much further than GST. It noted the terms of reference to the United Nations Framework Convention on International Tax Cooperation, which had been adopted by the General Assembly,

“This development represents an important opportunity to create global tax governance that enables state parties to adopt fair, inclusive and effective tax systems and combat related illicit financial flows.”

“regressive and ineffective tax policies”

The key paragraph to the UN Committee statement is paragraph 4, which refers to “regressive and ineffective tax policies”, having

“…a disproportionate impact on low-income households, women, and disadvantaged groups. One such example is a tax policy that maintains low personal and corporate income taxes without adequately addressing high income inequalities. In addition, consumption taxes such as value added tax can have adverse effects on disadvantaged groups such as low-income families and single parent households, which typically spend a higher percentage of their income on everyday goods and services. In this context, the Committee has called upon States Parties to design and implement tax policies that are effective, adequate, progressive and socially just.”

It’s the reference to consumption taxes that was picked up by RNZ. The regressivity of GST is well known and was noted by the last Tax Working Group. The general approach we’ve taken here to that issue is to try and ameliorate the impact by benefits or transfer payments such as Working for Families and Accommodation Supplement to lower income families.

The thing is though, as Alan Bullôt, of Deloitte noted in the RNZ story, GST is a very effective tool for the government to raise a large amount of money relatively easy. In fact, GST represents about 25% of all tax revenue a point I repeated when I discussed the whole story on RNZ’s The Panel last Monday.

Principles of a well-designed tax system

But the Committee statement is interesting beyond the GST issue because it goes on in paragraph 6 to set out what it regards as the principles of a well-designed tax system. It suggests, for example,

“…ensuring that those with higher income and wealth, in particular those at the top of the income and wealth spectrums, are subject to a proportionate and appropriate tax burden.”

That can be clearly interpreted as a call for a capital gains tax or some form of capital taxation, a point I made to The Panel.

The Committee also fires a few shots over international tax, stating

“The Committee has observed situations in some States where low effective corporate tax rates, wasteful tax incentives, weak oversight and enforcement against illicit financial flows, tax evasion and tax avoidance, and the permitting of tax havens and financial secrecy drive a race to the bottom, depriving other States of significant resources for public services such as health, education and housing and for social security and environmental policies.”

That clearly targets tax havens, but it’s also a shot across the likes of Ireland, for example, with its low corporate tax rate.

A global minimum tax

The Committee also calls for a “global minimum tax on the profits of large multinational enterprises across all jurisdictions where they operate and to explore the possibility of taxing those enterprises as single firms based on the total global profits, with the tax then apportioned fairly among all the countries in which they undertake their activities.”

That’s quite the statement even if probably forlorn given the Trump administration’s recent declarations. It’s probably what the less developed world is after, because they’re quite concerned they’re losers under the current system. This is going to lead to wider clashes over the G20/ OECD proposal, which I think to be frank, is probably dead. In any case, I thought it was always noteworthy that Pakistan, the World’s fifth most populous country and Nigeria, the sixth most populus country and also Africa’s largest economy, both refused to sign up for Two Pillars.

Now economically, that was not highly significant because the economies are small relative to the giant economies of the developed world. However, I think this refusal points to existing issues and this statement underlines there’s global tensions ahead on this question of international tax.

As I said, the Trump administration basically is saying no go. But I think you will see countries attempting to find ways of taxing what they regard as their part of the international multinationals’ income. So, plenty ahead in this space.

Rising GST debt

Now moving on, another RNZ report picked up that there had been a substantial growth in GST debt. Allan Bullôt, of Deloitte raised a concern this could be creating zombie companies. In particular he noted the amount of GST collected but not paid to the Government, has risen from $1.9 billion in March 2023 to $2.6 billion by March 2024.

As mentioned earlier, GST represents 25% of tax revenue. It also represents just under 40% of all tax debt and has been rising sharply. That’s a reflection of the economic slowdown and the cash flow crunch that’s happening to a lot of businesses.

Even so, this is a matter where Inland Revenue has a number of resources it can deploy, and one Alan mentioned is the power to notify credit reporting agencies about tax debt. According to the Inland Revenue, it only did that three times in the year ended 20 June 2024 and not at all during the June 2023 year.

This means that people were trading and doing business with companies without realising the potential risk. What that might mean is that you provide services to a company which is struggling with GST debt, and lo and behold, you suddenly find you’ve got a bad debt on your hand.

Creating zombie companies?

This is a major issue and as Allan put it,

“That’s grown and grown. I get very nervous we’re creating zombie companies … if you’re three or four GST returns behind, it’s incredibly unlikely if you’re a retail or service business that you’ll ever come back. If you’re three of four GST payments behind, it’s incredibly unlikely that your retail or service business will ever come back.

Maybe if you’re a property developer who’s got big assets that you sell and settle your debt. But if you’re a normal business, a restaurant or something like that, you go belly up.”

This is an area where Inland Revenue has information which is not available to the general public and maybe it should be making that more widely available. There’s a question here to my mind, of what proportion of debt you would report. The Inland Revenue I think has every right to say this person owes X amount of GST, or is behind on GST, but bear in mind in some cases the debt is inflated by interest and penalties. Or in some cases there may have been estimated assessments.

Notwithstanding this Allan is right to raise concerns and I expect we will see more money being granted to Inland Revenue in this year’s Budget to chase this debt.

Meanwhile, jam tomorrow in the Australian Budget

It was the Australian budget on Tuesday night our time in which the ruling Australian Labor Party promised modest tax cuts starting in July 2026, with a further round in July 2027. Under the proposed cuts, a worker on average earnings of A$79,000 per year (about NZ$86,800) will receive A$268 in the first year and that will rise to A$536 in the second year. In addition, there will be a A$150 energy rebate payable in A$75 instalments.

Otherwise, there weren’t many other tax measures to report. That was hardly surprising because two days later, Prime Minister Anthony Albanese announced that the Federal Election would be held on 3rd May. The Budget was therefore what you might call a typical pre-election budget, promising jam tomorrow if you vote for the ALP.

One tax measure of note was that the Australian Tax Office is getting further funding for dealing with tax avoidance and tax evasion. I think that’s a pretty standard pattern we’re seeing around the world. The British had what they call their Spring Statement this week, the half yearly report by the Chancellor of the Exchequer or Finance Minister.

No new tax measures were announced. But like the ATO, HM Revenue and Customs was allocated more money to target tax evasion, with the expectation that it would achieve about a billion pounds a year in additional revenue, which seems very light given the scale of the UK economy.

Mega Marshmallows food or confectionery?

Finally, this week, a couple of years back, we discussed the Mega Marshmallows Value Added Tax (VAT) case from the United Kingdom. Basically, it involved the VAT treatment of large marshmallows. If deemed to be food they would be zero-rated for VAT purposes, but if they were confectionery, they would be standard rated which at 20% means quite a significant sum is at stake.

I will cite this and its very well-known predecessor the ‘Max Jaffa’ case involving Jaffa Cakes from the 1990s, when people make suggestions about maybe reducing the GST on food to help with the cost of living, particularly for lower-income families. It’s a well-meant policy except the practical issues you run across lead to absurdities at the margins. My view on this topic is if you want to assist people at the lower end of the income scale, it’s better give them income rather than try and fiddle with the GST system because there are unintended consequences, and this mega marshmallow case is a classic example.

The case involves unusually large marshmallows. The recommendation by the manufacturer is that they should be roasted as they’re marketed as part of the North American tradition of roasting marshmallows over an open fire. Except it’s not clear in fact, if that actually happens.

The story so far is that after HM Revenue and Customs lost in the First-Tier Tribunal, it appealed to the Upper-Tier Tribunal which basically said, “Nope, we’re not hearing it.” So HMRC appealed again to the Court of Appeal which has now issued its ruling. The Court of Appeals determined it was not absolutely clear whether in fact these marshmallows can only be eaten if they are cooked, in which case they must be food, or they can be eaten with the fingers, in which case they are confectionery.

Accordingly, the key issue is whether they are normally eaten with the fingers. This is a question of fact about which the first-tier tribunal has not made a finding. In some cases, it will be obvious from the nature of the product whether it is normally eaten with the fingers or in some other way. But that is not clear with this particular product.

The Court of Appeals therefore sent the case back to the First-Tier Tribunal to decide on this question of fact. Are these mega marshmallows mostly eaten with the fingers? If so they’re confectionery and subject to VAT at 20%. Alternatively, are they mostly cooked as supposedly intended, and therefore zero-rated food.

Time for the UK to apply VAT to food?

This case came to my attention through the UK tax thinktank Tax Policy Associates which is run by the estimable Dan Neidle, a former tax partner at the mega law firm Clifford Chance. Commenting on the Court of Appeal’s decision, he pointed out the sheer absurdity and costs involved and questioned why this was so. “Why do we have a horribly complicated set of rules that mostly benefit people on high incomes (because they spend more on food)? “

His solution – scrap zero-rating on food, in other words, adopt the approach we have here in New Zealand and tax everything. He estimates that would raise about £25 billion which could be used to reduce the standard rate of VAT from 20% to 17%.

Warming to his theme Dan thinks a better idea would be “Cut the rate to 18% and use the remaining [money] in benefit increases and tax cuts targeting those on low incomes, so they’re not out of pocket from the loss of the 0% rate.”

It’s the first time I can recall a British commentator suggest this. I doubt it will happen, but it’s just a reminder that although our GST is highly comprehensive, we don’t have these absurd but entertaining cases involving marshmallows of unusual size.

But a comprehensive GST is regressive, and I think a better approach is to address that by means of transfers to lower incomes rather than tinkering with exemptions. You never know, there may be something in this space in the Budget, we’ll find out next month.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

It has, to put it mildly, been a rather dramatic week in the geopolitical arena, with the United States appearing to basically abandon the security arrangements it established in Europe after World War 2, particularly the foundation of NATO.

Coupled with the US opening direct negotiations with Russia about the war in Ukraine, without the involvement of either Ukraine or NATO, it is now clear that a radical reshaping of the world order is underway after only a month of President Trump’s second term. It’s also clear that this is very much America First.

The OECD Two-Pillar deal is dead

The same is true in the tax world. In my first podcast of the year, I discussed one of President Trump’s initial executive orders, which in my view, pretty much meant the end of the Organisation for Economic Cooperation and Development’s (OECD) two pillar deal on international tax. My view was confirmed in a fairly bleak summary of the state of international tax by a Washington based presenter at this year’s International Fiscal Association (IFA) conference.

More on the IFA conference later. But as our presenter noted, it now appears that Value Added Tax (GST) is in the Trump administration’s crosses. On 13th February he issued another Executive Order on Reciprocal Trade and Tariffs. The issue here is protectionism which is very much part of President Trump’ economic policy agenda. He is particularly concerned about the decline in manufacturing and in particular about trade imbalances which he views as a consequence of the decline in manufacturing. Accordingly, many of the Executive Orders he has issued in this area are to redress these imbalances particularly those with Canada and Mexico. Hence the imposition of tariffs against both countries even if some are temporarily suspended. In the meantime, arguments continue.

In this vein Section 2 of the 13th February order noted

“It is the policy of the United States to reduce our large and persistent annual trade deficit in goods and to address other unfair and unbalanced aspects of our trade with foreign trading partners. In pursuit of this policy, I will introduce the ‘“Fair and Reciprocal Plan” (Plan). Under the Plan, my Administration will work strenuously to counter non-reciprocal trading arrangements with trading partners by determining the equivalent of a reciprocal tariff with respect to each foreign trading partner. This approach will be of comprehensive scope, examining non-reciprocal trade relationships with all United States trading partners, including any:

tariffs imposed on United States products;

unfair, discriminatory, or extraterritorial taxes imposed by our trading partners on United States businesses, workers, and consumers, including a value-added tax;”

A new and dangerous approach?

Note the word “each”. Value added tax is what we call GST. This is somewhat new and it’s frankly quite alarming because as you can imagine the impact of VAT is separate to that of tariffs. This is obviously quite concerning and causing consternation around the world. Because, as I said, this goes further than simply saying we’re going to impose retaliatory tariffs on you, because there is no equivalent to GST in the United States. There is no national sales tax. Every state imposes its own sales taxes at varying levels and sometimes local counties have separate sales taxes. It would actually take a constitutional amendment to introduce the equivalent of GST in the United States.

Another point that has been made in discussions around this, is that even if you added up the various state sales taxes that might be imposed, they’re nowhere near the same level of VAT that is often charged. And so, the question is, when a US firm has VAT applied to exports it now appears that this would open the door for retaliatory action by the US.

What about Netflix?

This led to quite an interesting debate at the presentation around the question of whether our “Netflix tax” might be within the scope of these retaliatory actions now. Potentially no, because the Netflix tax is a tax on services – in GST/VAT terminology a “reverse charge”. It’s imposed because otherwise no VAT or GST would be payable because the supply of services is outside the jurisdiction of the country providing the services. As Netflix is providing services from outside New Zealand to New Zealand residents, we’ve decided GST applies.

So, in fact it could be in scope. We really don’t know. One of the recurring themes of the assessment we got from the Washington based presenter at IFA was we have no idea what’s going on here, and we don’t know whether this is just rattling the cage for the sake of hopefully obtaining better terms on a deal. President Trump is very much transactional in his approach because that’s what he’s been about all through his life and he is applying that approach on a global scale now.

Maybe that’s the end of it, but it could also be that there is a genuine threat to impose tariffs where the US feels that GST has been unfairly imposed. We will have to wait and see.

What about a Digital Services Tax?

What I would say is that any hopes of a Pillar Two deal which has been moved forward (painstakingly slowly) by the OECD is probably dead in the water for now. This would probably extend to any digital services tax that we might consider introducing.

Remember that in President Trump’s Executive Order which withdrew the United States from of the OECD deal, there was also an instruction for the U.S. Treasury Department to investigate all potentially discriminatory taxes, and that would include a digital services tax. It would seem to me that our ability to impose that is quite restricted. So, we’re now into completely unknown territory here. The risk of retaliation might be lower at our end, but you never know.

Higher defence spending?

One of the issues that has been pushed on President Trump’s agenda (and it’s actually not an unreasonable point) is that America had borne much of the cost of defence throughout the Cold War, and even after the end of the Cold War it still continues to have a very large military establishment.

President Trump therefore demanded NATO nations needed to increase their defence spending to at least 2% of GDP. That is happening rather rapidly. This week, for example, Denmark announced further increases to its defence budget.

Our defence budget will come under examination, and this week the Prime Minister commented “We will be getting as close to 2 percent [of defence spending on GDP] as we possibly can, we know that’s the pathway we want to get to.” That’s probably not something Finance Minister Nicola Willis wanted to hear, but that’s the way of the world at the moment.

Could the sackings at the Internal Revenue Service have implications here?

The other thing of concern is what’s going on at the US Internal Revenue Service (the IRS)? Apparently some 6000 workers were sacked the other day, and we have reports that Elon Musk’s Department of Government Efficiency, DOGE, has been trying to gain access to records held by the IRS.

What I hadn’t been aware of is that the Commissioner of the IRS had resigned and will be replaced by a Trump appointee. I’ve previously commented about the risks that these actions represent to other tax jurisdictions. One would be in relation to all the information sharing agreements that exist, particularly FATCA.

I have no doubt whatsoever that IRS officials will do everything within their power to ensure the security of information shared under FATCA and other agreements is maintained. But if as is suggested, DOGE personnel are able to gain access to that information what will that mean for our international agreements? Will we and other nations be willing to continue to share information with the United States if we have concerns that it may no longer be secure? That’s a huge matter that there’s probably no answer to at the moment. I imagine quite a few tax authorities, including our own, are probably considering this very point right.

Time running out for an important GST election

One of the issues we deal with on an increasing basis is the treatment of Airbnb properties. In particular the implications when the GST threshold of $60,000 is crossed. In some instances, the taxpayer has claimed GST input tax on the purchase of the property involved, only to find out that they face significant GST liability if they decide to sell at a later point. This is something which obviously comes as a shock.

It so happens that two years ago, with effect from 1st April 2023, a transitional rule was introduced in section 91 of the Goods and Services Tax Act, which enables a person to elect to take that asset out of the GST net if certain criteria are met. The four requirements are:

if the asset was acquired before 1st April 2023, and

it must not have been acquired for the principal purpose of making taxable supplies, and

the asset was not used for the principal purpose of making taxable supplies, and

a GST input tax credit has been previously claimed, or the asset was acquired of as a zero-rated supply.

Note that ALL the above criteria must be met.

A good example would be a property which was acquired as a bach or holiday home but then rented out for short stay accommodation during the peak holiday period via Airbnb. Another example might be a business that has a residential property which was acquired as part of a larger land purchase.

Although primarily acquired for GST-exempt purposes the properties have been used to make GST supplies. Consequently, GST will be payable on sale. However, if you apply this transitional rule, you must make the election to take the asset out of the GST net before 1st April. If the election isn’t made in time, then the sale of any asset with business use, where GST was claimed on purchase, will be subject to GST on sale.

Basically, people have now just under five weeks to review their GST position and consider whether to make this transitional election and potentially bypass a large GST bill on a future sale.

Obviously in the run up to the end of the tax year on 31st March, there will be a number of other income tax and GST elections for people to consider if action is required.

An interesting conference

And finally, as I mentioned earlier, this year’s International Fiscal Association Conference was held on Thursday and Friday, hence why this podcast been delayed. It’s a policy-focused conference whose attendees are mainly partners from the large accounting and law firms, together with the heads of tax in major companies and very senior Inland Revenue officials.

This conference is subject to Chatham House rules, so while I can’t say much about what specifically was discussed, I can say it was an extremely interesting conference as always, and my thanks to the organisers.

As I mentioned earlier, we had a very interesting and thought-provoking presentation on the state of international tax as viewed from America. Inland Revenue has been very busy working on a number of topics, so we ought to see some very interesting legislation coming through this year, around either the time of the Budget, or more likely, when the annual tax bill is released in August.

Growing problems with double tax agreements

In relation to international tax, we had an interesting presentation on the impact of very specific anti avoidance rules on double tax agreements. Now double tax agreements generally override domestic law. In other words, we might have legislation where we might say we’re going to tax this. But then the double tax agreement says actually the taxing rights go to another country.

What is happening is there’s been a steady growth of what’s been called the general anti-avoidance rules, where it appears that companies have made what’s seen as abusive use of these double tax rules to claim tax relief. Countries are increasingly updating their tax treaties to include this general anti avoidance provision overriding the double tax agreement.

For example if you look at how Netflix, Visa and MasterCard seem to have substantial income from New Zealand without apparently paying much income tax, the question arises are the double tax agreement rules being abused and should this be dealt with by way of a general anti avoidance rule overriding the tax treaties?

Or you could also see these issues as being part of what we discussed at the top of the podcast is that the changes to the international tax order means more friction as basically tax authorities get more willing to get down and dirty and fight with each other over who has the taxing rights over income. We certainly live in interesting times.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Inland Revenue consults on treatment of repairs to newly acquired assets

Last week I discussed the suggestion from the Minister of Finance, Nicola Willis, that a cut in the corporate tax rate from 28% was under consideration.

Subsequently, on last Sunday’s Q+A, Robin Oliver was interviewed by Jack Tame on the topic. Robin is a former Deputy Commissioner of Policy at Inland Revenue and was also a member of the last Tax Working Group. In his role as a Deputy Commissioner at Inland Revenue he would have been involved in most of the major tax reforms of the last 30 years, so he really is one of the Titans of tax and always worth listening to.

Go big or go home…

In discussing the question of a corporate tax cut he made a very important point – go big or don’t bother. In his view dropping it from 28% to 25% simply wouldn’t make much difference. Instead, he suggested a bolder approach would be to cut it to say 18%. Because if you really are wanting to attract investment then you have to show something significantly different.

He raised the point that Singapore, which is often raised as a comparable, has a 17% corporate tax rate. Ireland, another comparable country has a 12.5% rate. Against these countries we would need to cut our tax rate substantially in order to attract investment.

But Robin Oliver also raised the question as to the consequences of such a cut and whether there might be other opportunities for improvement. He mentioned the problems which we’ve previously discussed about the Foreign Investment Fund regime. He also floated the alternative of accelerated depreciation for plant and machinery, which in his view was more fiscally realistic. Personally, I think this would be a more worthwhile move.

Reshaping our tax system – higher GST?

If he was given the opportunity for complete freedom of action over the tax system, Robin Oliver would be bold and go for a higher GST rate and taking the emphasis away from income tax. But he pointed out that although this might be nice in theory, the GST rate might have to rise to 28%, which would be pretty near unacceptable to the broader public. His key point was there are trade-offs to be to be made and it’s not simply a matter of a corporate tax cut will attract investment. Other considerations have to come into play.

I agree with Robin that if you are going to go with a corporate tax cut, you probably have to be bold about it. The question then is how do you recover that lost revenue? Robin’s response was that some hard choices would have to be made. He was a bit gloomy on those options, I thought.

What about a capital gains tax?

As I said Robin is a vastly experienced tax practitioner and he would have considered many options during his time supporting the work of various tax working groups and then as part of the last tax working group. He made a passing comment suggesting people stop whinging about capital gains tax. Robin was one of the three dissenters to the general capital gains tax proposal made by the last Tax Working Group but remember that the whole group was unanimously supportive of increasing the taxation of residential investment property.

Overall, very interesting to hear Robin’s take and I recommend watching the interview. It may be a corporate tax cut needed to be really attractive is probably beyond the Government’s fiscal capabilities at this point and therefore other alternatives might be more cost effective.

Further clues about tax changes?

Incidentally Iain Rennie, Secretary to the Treasury, made a speech to the 2025 New Zealand Economics Forum Bending two curves: New Zealand’s intertwined economic and fiscal challenges which supported a speech made by Finance Minister Nicola Willis, yesterday about the Government’s Going for Growth economic plan. Both mentioned tax with Iain Rennie noting

Our taxation of investment is also uneven, which distorts investment choices. Such economic settings can discourage the acquisition of productivity-enhancing assets like machinery and equipment.

This suggests that the policy responses are likely to include those that create an environment more conducive to firms making these investments. This could be through the structure of business taxation, savings policy, and regulatory frameworks that keep pace with business changes and create certainty for investment in emerging sectors.

These speeches provide a few more that a corporate tax cut could be perhaps a possibility. But there are, as Robin Oliver pointed out, other opportunities. Anyway, we’re obviously going to see a lot more speculation in the run up to the Budget on 22nd May.

Netflix’s tax reporting under investigation in France

An interesting story popped up this week involved Netflix’s tax activities. It appears Netflix’s offices in both Paris and Amsterdam had been raided late last year by French fraud investigators. European Union investigators started looking into the matter after France’s National Financial Prosecutor’s Office raised suspicions about the company “covering up serious tax fraud and off-the-books work”.

It transpires Netflix’s French subsidiary reported turnover “at odds with paying user numbers in the country.” Between 2019 and 2020, Netflix France paid less than €1,000,000 in corporate taxes, despite having more than 10 million customers.

What about Netflix New Zealand?

This is an ongoing investigation which after it came to the attention of Edward Miller the researcher at the Centre for International Corporate Tax and Accountability and Research, piqued his interest about Netflix’s activities here. When he went looking, he found out Netflix does not file any financial statements in New Zealand. This is actually acceptable under our low compliance approach to corporate filings. At present under the Companies Act 1993 public financial statements of a foreign-owned company must be filed if either the total assets are more than $22 million or the total revenue exceeds $11 million.

Now, surprise, surprise, Netflix New Zealand Ltd is apparently falls below that threshold, which as Edward Miller pointed out, seems odd given that there’s about 1.3 million users in New Zealand paying at least $18.49 a month to access its service. We’re therefore looking at another example of how multinationals are apparently able to shift profits offshore. Simultaneously, this is also an example of how tax authorities are increasingly taking a look at these activities and saying, ‘well, this is no longer really acceptable in our view.’

What do Netflix and Uber have in common?

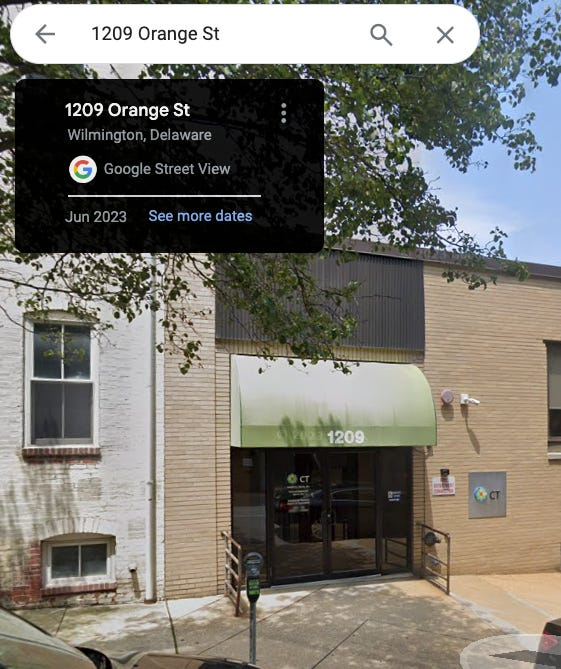

Where it becomes quite entertaining is that ultimately the head office for Netflix appears to be an address in a very unassuming building at 1209 Orange St, . Wilmington, Delaware in the United States. Delaware is a very tax favourable jurisdiction within the United States, and this particular address is so favourable that it is registered address of no fewer than 285,000 U.S. companies, including Uber.

That somewhere so modest is the home to so many companies is entertaining but also points to the serious issue of highly sophisticated tax planning where apparently income is earned in a jurisdiction but little or no income tax is paid.

In fairness to Netflix, notwithstanding its income tax position, it’s highly likely that it will be paying a substantial amount of GST. That’s because its customer base is individuals who will not be GST registered and therefore will not be able to recover the GST paid.

Incidentally, Visa and Mastercard are two other companies that we know very little about but have a significant effect here. Neither company have published financial statements for almost 10 years now. The revenue they earn on fees probably runs to hundreds of millions of dollars, but we just don’t know what portion is being taxed here. What Netflix is doing is a bigger issue than perhaps is generally appreciated.

Time to rethink our reporting requirements?

Given how opaque these transactions are, perhaps we need to rethink our rather relaxed approach to reporting and filing of a company’s financial statements, particularly in relation to multinationals. Interestingly, Australia now requires large multinational groups with an Australian presence to submit data on their global financial and tax footprint to the Australian Taxation Office (ATO), which will give more disclosure where around international profits are being booked. The Post approached the Minister of Revenue, Simon Watts, for comment and said that a similar proposal was not under consideration. (Note that the Australian proposal goes beyond country-by-country reporting https://www.ird.govt.nz/international-tax/exchange-of-information/count… which applies to a small number of multinationals).

What next?

The French investigation of Netflix is just another example of how many tax authorities around the world are looking at this question of where’s that income being really taxed and wanting justification for enormous fees that seem to end up in tax havens. But then, as I said last week, we now have the potential threat of the United States under the new Trump administration not favouring such investigation activities. It will be interesting to see how this plays out.

Are repairs to a newly acquired asset deductible?

As always, Inland Revenue is busy producing guidance on a number of matters and this week it was an exposure draft (ED) on a very interesting point – are expenses incurred on repairing a recently acquired capital asset deductible.

This draft is part of a series on repairs and maintenance expenditure which will eventually replace the current Interpretation Statement IS 12/03 – Deductibility of repairs and maintenance expenditure – general principles.

This exposure draft is potentially pretty significant – it reaches a different conclusion from IS 12/03 on the relevance of whether the price of the asset was discounted. Consequently, Inland Revenue is “particularly interested in comments on the relevance of the assets price in the context of initial repairs, as it appears there may be differences in opinion and practice.”

The ED guidance centres on what happens if you buy an asset that’s pretty run down, and then you carry out repairs to it to get it up and running? Are you able to claim those costs as repairs or should they be capitalised? For example, if you buy machinery that’s pretty run down and carry out repairs. If you can’t show that the repairs are genuine repairs – that they reflect wear and tear – Inland Revenue’s view is you must capitalise those costs. As such those costs are probably going to be depreciable.

What about repairs to buildings?

However, it’s a much, much bigger issue in relation to buildings. Because with the withdrawal of depreciation allowances for all buildings (not just residential buildings) the question of whether expenditure represents repairs and maintenance becomes an all or nothing issue. In other words, if it’s a repair, it’s deductible. If not, no deduction, whether in the form of depreciation or any other form, is available. I see a real pressure point emerging on this matter.

As always there’s lots of useful examples, but there’s also one or two matters we’d like to see clarified. For example, the ED refers to “normal wear and tear.” But what does that mean? If you’re talking about an asset that’s depreciated over, say, five years economically are Inland Revenue saying that repairs in excess of what the normal depreciation would be on that asset must be capitalised?

What about buildings?

It’s something I think needs more certainty, particularly in relation to buildings. The ED has an example on the treatment of repairs to a newly acquired building and I’m not so sure I’d agree with Inland Revenue’s conclusions. In summary, a 100-year-old tenanted residential property has been inherited by James. It’s in a poor state of repair and its condition was such that it could only be rented on a short-term basis with a high turnover of tenants and poor rental returns.

Because the property is in a good location James therefore decides if he restores the property to good condition the rental return can be increased by attracting different tenants for longer term letting. So, he carries out repairs to the property while it remains tenanted, including repairing the leaking roof, replacing some of the guttering down pipes, repainting portions of the exterior proper, and a number of other matters, including a repair to the main water supply pipe to the property.

The conclusion is that the expenditure incurred was necessary to restore and maintain the functionality of the property to the level required for its intended use of letting it on a longer-term basis. And for that reason, it’s capital in nature. No deduction will be available, and as I mentioned earlier, because it’s a building, no depreciation is available.

I’m not sure that would stand up in court if tested, because James is still deriving gross income. Yes, there’s an improvement to enhance it, but court cases have accepted that all repairs involve some form of improvement because you’re replacing old materials with new materials.

I’m intrigued to see what the response is to this and what comes out in the finalised guidance. Certainly, as I saw Robyn Walker of Deloitte point out, buying a car without wheels and then claiming a repair by sticking wheels on is clearly something that is not appropriate. But then in that case there should be a depreciation deduction available. It’s much more tricky in relation to repairs carried out to newly acquired properties. Again, watch this space.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Could the US retaliate against a digital services tax?

Last week, in a series of interviews with the press, notably with Newstalk ZB, Finance Minister Nicola Willis dropped several hints about what might be in the forthcoming May 22nd Budget. In particular, she talked about the corporate tax rate, and the possibility of cuts to that as part of promoting the Government’s growth agenda.

Corporate tax rate above OECD average

Speaking with Heather Du Plessis-Allan, Ms Willis commented:

“Well, if you compare New Zealand with the rest of the world, we’re not as competitive as we used to be. Which is to say that our corporate tax level is reasonably high when you compare it to the rest of the developed world.”

This is a very valid point which comes up frequently in discussions. Our current company tax rate at 28% is well above the OECD average of 24% and has been out of alignment for some time.

New Zealand back in the late 80s under the Fourth Labour Government was actually at the forefront of cutting company tax rates. A particularly interesting action was to align the company tax rate with the top individual and trust rates of 33%. The three basically stayed in line until the election of the Fifth Labour Government and the increase in the top personal tax rate to 39% in 2000.

There have been a couple of corporate tax cuts over the past 15 years or so. In 2007, the rate was cut from 33% to 30% and then in 2010, as part of the rebalancing that took place under Bill English with the increase of GST from 12.5%, the corporate tax rate was cut to 28% where it remained since.

As I’ve discussed previously, there has been a long running global trend towards lower corporate tax rates. But that has slowed in recent years, first because of the effect of the Global Financial Crisis and secondly, the fiscal shock to government finances because of the COVID-19 pandemic. As a result, according to the OECD in 2023, corporate tax rates rose generally across the board. Nevertheless, we are out of sync at the headline rate level.

More to investment than the corporate tax rate and will it work?

A lower corporate tax is undoubtedly attractive. However, the tax rate needs to be seen in context with what other incentives are available. Overseas companies and investors are very focused on what else might be on the table. A lower company tax rate would certainly be attractive, so the suggestion has been met with enthusiasm by some. Others are a bit more sceptical. Economist Ed Miller noted that when the effect of the corporate tax cuts in 2007 and 2010 are considered there does not seem to be any significant increase in foreign direct investment as a result.

The last tax working group didn’t see overwhelming evidence to support the theory that lower tax cuts at lower corporate tax rate would attract investment.

Problems and an alternative

There’s a flip side to this though, and it’s tied into the Government’s intention of restoring a surplus. Our corporate tax rate is not only above the OECD average, but our corporate tax take is also high by world standards. According to OECD statistics, 14% of the total tax receipts in New Zealand for 2022 came from company tax, whereas around the OECD the average is 12%.

So, if the Government, in an attempt to boost economic growth, is going to cut the corporate tax rate, it must then look at other alternatives to replace the lost revenue. One of the things it did back in 2010 and which it has already repeated, was to remove depreciation on all buildings. Depreciation for commercial buildings was restored under Labour but then removed again from the start of the current tax year on 1st April 2024.

A counter argument to the Government’s proposal for corporate tax cuts would be that enhanced depreciation allowances, including restoration of commercial building depreciation, which would include factories, might be a more effective approach than across the board tax cut.

How to replace lost tax revenue?

But if the Government is thinking of a corporate tax cut, and that does seem to be the case, what counter measures could they take to ensure that it is not fiscally too draining on the resources? One option might be that the availability of imputation credits may be restricted. For example, it might be that you can elect to have a lower corporate tax rate, but you imputation credits are no longer available to for shareholders.

As an aside, imputation (sometimes called franking) credit regimes were very popular during the 1980s, but gradually fell out of favour over time, mainly because, or in part because the European Court ruled that imputation credits or franking credits have to be available to all shareholders resident in the EU. After the German government lost this case its response was to heavily restrict the use of franking credits.

Change the tax treatment of Portfolio Investment Entities?

Another option might be to review the taxation of portfolio investment entities held by persons with effective marginal tax rates above the 28%. To quickly recap, Portfolio Investment Entities (PIEs) have a tax rate of 28%, equal to the company tax rate, which is also the maximum prescribed investor rate for individuals. So, there is actually a tax saving opportunity for individuals whose other income is taxed above the 28% rate for PIEs.

The Government might look at this, decide that will no longer apply and instead income from PIEs will be taxed at the person’s marginal rate. That could raise sufficient sums to partially offset the effect of a lower corporate tax rate.

The Finance Minister also mentioned reforming the Foreign Investment Fund regime, which is currently being considered by Inland Revenue and made some encouraging sounds about that potentially being an option.

We shall see. No doubt there’s a lot of work going on in Treasury and Inland Revenue looking at these options. All will be revealed in the Budget on 22nd May.

A threat to our Digital Services Tax

As covered in our first podcast of the year, one of President Trump’s initial executive orders withdrew the United States from the OECD Two-Pillar international tax deal. I drew attention to the second paragraph of that Executive Order, which directed the US Treasury to consider taking actions against other jurisdictions for tax actions which are potentially prejudicial to American interests.

Vernon Small, who was an advisor to the former Minister of Revenue, David Parker, now writes a weekly column in the Sunday Star-Times has picked up on this point noting that “Treasury has budgeted to rake in $479 million between January 2026 and June 2029 from a 3% Digital Services Tax (DST) on tech giants like Google and Meta.”

This, according to Small, “is an heroic piece of forecasting given current uncertainties and the provision for delaying collections until 2030 if progress is made on a multilateral approach through the OECD.”

And then the crunch point:

“Trump has bosom buddies in high places in the industry with Elon Musk first amongst them, and Mark Zuckerberg making a play for the new US administration’s affections.

Trump has promised to retaliate against discriminatory or extra-territorial taxes aimed at US interests. So the DST could be a prime target.”

Vernon Small is underlining the potential threat to our revenue base and our sovereign right to tax. If the OECD deal does fall over there are a number of countries including Canada, no longer America’s best friend, it seems, with DSTs ready to go. So there’s a whole potential for a tax war.

The Trump threat to tax administration

But equally worryingly, coming out of the United States is something about the question of bureaucratic independence from the executive. This might sound an arcane issue but it’s actually quite important to the independence of tax authorities.

One of the first actions of the Trump administration was to sack 17 Federal Inspectors-general. There’s also a move to put all Federal Government employees on the basis that they serve at the pleasure of the President. This would mean that an employee could be fired without the need for cause as the American terminology puts it.

Project 2025’s Schedule F

The implications of this have been picked up by Francis Fukuyama, the author of the famous The End of History essay written in the wake of the collapse of the Soviet Union and the end of the Cold War.

Writing for the Persuasion Substack under the title Schedule F is Here (and it’s much worse than you thought) Fukuyama wrote:

‘ “For cause” protection means that the official cannot be removed except under specific and severe conditions, like committing a crime or behaving corruptly. And now many individuals have been moved, in effect, to Schedule F because they are said to serve at the pleasure of the President.

Consider what this may mean if Trump hand picks a new Internal Revenue Service chief, that individual can be pressured by the Government to order audits of journalists, CEOs, NGOs and NGO leaders. Removal of Inspectors General will cripple the public’s ability to hold his administration accountable.’

Trump’s decision to move all Federal employees to Schedule F status is a step towards autocracy. What perhaps we all need to keep in mind is that the separation between the Commissioner of Inland Revenue and the Minister of Revenue is actually incredibly important. Yes, at times the Inland Revenue might do something which probably might embarrass the Minister of Revenue, but he cannot directly intervene in Inland Revenue’s operations.

A key part of a well-functioning democracy is that civil servants can act independently from their nominally political superiors. Fukuyama is right to say we should therefore have some concern coming at what’s happening in, in the United States because it does seem to be centralising power very rapidly around the President. The .potential for mischief is therefore enhanced as a result, and don’t think that such a step ultimately doesn’t have tax consequences.

Latest on the changes to the United Kingdom ‘non-dom’ regime

On a more positive note, last year I discussed the changes to the so-called ‘non-dom’ regime in the United Kingdom. This is where persons who are not domiciled in the UK have a special basis of taxation. Basically, they’re not taxed on income and gains which are not remitted to the UK.

This is a significant concession which is ending with effect from 5th April this year when it will be replaced by something which is more akin to our transitional resident’s exemption. This is pretty important for the approximately 300,000 Britons like me who’ve migrated here, plus the significant number of Kiwis who have assets in the UK or family going to the UK but have retained assets here. All of this group are potentially within the scope of these reforms.

There’s been a fair amount of push back on the reforms together with concerns that there will be a flight effect as wealthy, ‘Non-doms’ leave the UK. The UK Labour Government has been under pressure to make some changes to the proposals.

In response, the Chancellor of the Exchequer (Finance Minister) Rachel Reeves announced a concession (ironically at the gathering of the super-wealth at Davos) which will increase what’s called the temporary repatriation concession.

This concession will allow non-doms a three year window to pay a temporary repatriation charge on designated foreign income and capital gains so that they can subsequently be remitted to the UK without any further tax. The temporary repatriation charge will initially be 12% before rising eventually to 15% in the year ended 5th April 2028. For comparison, without the concession remitted income would be taxed at rates up to 45% and remitted capital gains would be subject to capital gains tax at 24%.

There’s a lot of opportunity here for potential tax savings for those who could be affected or will be affected by the proposed change to the non-dom regime. We’re still working through all of the implications but we will be updating our clients and bringing you developments as they arise.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

One of the unseen revolutions in international tax over the last decade has been the adoption of the automatic exchange of financial account information. Also known as the Common Reporting Standards https://www.ird.govt.nz/crs this was developed by the Organisation of Economic Cooperation and Development, the OECD, in conjunction with G20 countries. It requires the automatic exchange of information on financial accounts – which is bank accounts, other investments held by taxpayers outside their jurisdiction. Financial institutions are required to provide information on such accounts to their respective tax authority which then sends that information to the jurisdiction in which that taxpayer is resident.

This project began in 2017. For the latest year, the tax authorities from 111 jurisdictions have automatically been exchanging information on financial accounts. And as I said, it’s a very broad range of investments, not just bank accounts. It’s all forms of investments. By and large, the public is pretty unaware of what’s happening here even though the numbers are significant.

€130 billion in tax interest and penalties so far

According to the latest peer reviewfrom the OECD, information from over 134 million financial accounts was exchanged automatically in 2023, and that covered total assets of almost €12 trillion. As a result, over €130 billion in tax interest and penalties have been raised by the jurisdictions through various voluntary disclosure programmes and other offshore compliance programmes.

Now the interesting thing here is that as a consequence of the introduction of the CRS, financial investments held in international finance centres or tax havens have decreased by 20% since the introduction of CRS in 2017. That’s a significant change. It means investments are moving into jurisdictions where they will be taxed. Over the long term that’s going to be quite significant for increased tax revenue around the world.

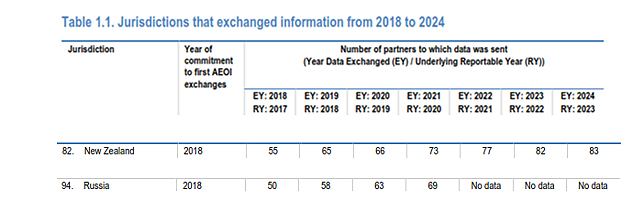

The full OECD report, which also discusses methodologies, runs to 248 pages, but the bulk of what people will be interested in is covered in the first chapter. Table 1.1. gives a summary of how many jurisdictions have been exchanging information, starting in 2018. According to the latest report the time of this report, 118 jurisdictions including New Zealand have started exchanging information.

Now the interesting thing to notice is the steady growth in the number of partners to which data has been sent. For example, the tax haven Anguilla in 2017 sent data to four countries but by 2023, it’s up to 67. The Cayman Islands, another key tax have sent data to 83 jurisdictions.

CRS and New Zealand

New Zealand began swapping data in 2018 when it sent information to 55 partners. For the latest year that’s grown to 83. Based on the early data exchanges Inland Revenue began a review programme in late 2019 which was then interrupted by COVID. However, it has now resumed its review programme, and I have one case at the moment which involves the taxpayer making the relevant disclosures after Inland Revenue enquiries based on data received through CRS. They won’t be the only one.

I was rather amused to see that Russia began exchanging data in 2018 when it sent data to 50 jurisdictions. But for the last three years no data is available. Wonder what’s happened there.

By the way the United States is not part of the CRS. That’s because it has something called the Foreign Account Tax Compliance Act, which basically was the model on which the current global CRS was built, and so it reports data separately.

How much data is Inland Revenue sharing?

I’ve tried unsuccessfully to obtain more detailed information on the data exchanges using the Official Information Act (the data exchanges are outside the OIA because of international treaty obligations which is fair enough). Notwithstanding this the impression I have is there are some huge numbers involved.

You have been warned…

What people should be aware of is that there’s a massive amount of data being circulated by tax authorities around the world right now. Many people may be oblivious to what’s going on. The likelihood is if you have an overseas financial account and you haven’t declared it for whatever reason, then it is quite likely that you will soon be asked a few questions about that by Inland Revenue.

Speaking about Inland Revenue, earlier this year they asked for consultation on their proposed long-term insight briefing (LITB). To quickly recap, LITBs are

“…future focused think pieces that government departments produce every three years. They provide information on long term trends, risks and opportunities that could affect New Zealand in the future, and policy options for responding to these matters. Their purpose is to help us collectively think about and plan for the future. They are developed independently of ministers and are not current policy.”

Back in August Inland Revenue proposed that its next long term insight briefing will explore what would be a suitable structure of the tax system for the future, and invited submissions by early October.

Inland Revenue has now published a summary of those submissions. In total, there were 35 submissions from 12 groups and 23 individuals. Most submissions were generally supportive of the topic. The rest, either suggested something completely different or were either ambivalent about it or did not actually specify whether they supported the project or not.

Seven themes in feedback

Inland Revenue’s picked out seven themes that came through from those submissions. Firstly, the fiscal pressures arising from superannuation and healthcare are a key trend and that’s one of the reasons behind Inland Revenue wanting to do a long term insight briefing on this topic. Most agreed with that, but several also added the question of increasing fiscal pressures arising from climate change.

My belief is its climate change that’s going to be the trigger point around changes to the tax system because that’s happening right now. And as damage from the floods grows and costs and insurers look increasingly wary about insurance, people will be looking to the Government for support.

The second theme was keeping flexibility in the tax system. In its submission EY commented

“We agree improvements to system flexibility should be the focus for this LTIB. In particular, working through options for system integrity in the context of tax rate increases is in our view, important.”

The devil is in the detail

A third theme was the analysis needs to consider policy design details and looking at first principles. Chartered Accountants of Australia and New Zealand made the comment that “Sometimes it is the detail that can make things unworkable. The framework should consider the merits of expanded tax bases with different design parameters”.

Another theme – and this is something I think I would endorse – the analysis needs to consider the tax and transfer system interaction. There were a few submissions pushing very strongly on that point.

A fifth theme proposed considering corrective taxes. The Young International Fiscal Association Network suggested that environmental taxes would fit well with Inland Revenue’s proposed topic because of the long term environmental trends.

The impact of technology

Another theme was the question of technological change and how that will affect the sustainability of tax bases. Earlier this year an IMF report on the impact of artificial intelligence suggested changes to tax systems could be needed.

Some submitters emphasised that it was important to consider how the tax system impacts a wider range of social outcomes. These included Doctor Andrew Coleman who was broadly in support of what was in the proposed LTIB. He suggested that they need to look at a wider range of retirement savings reforms, which would be no surprise to anyone who listened to the podcast with Gareth Vaughan and myself earlier this year. Several other submissions suggested how tax system could support productivity.

Finally, there were suggestions about considering progressive consumption taxes, which hasn’t really been looked at in any detail in New Zealand.

How Inland Revenue will proceed

Following this feedback Inland Revenue has said the LTIB will discuss the arguments for lower taxes on savings and the question of the tax treatment of retirement savings as part of a discussion about social security taxes. This is an interesting development because as the consultation noted generally, most jurisdictions have social security taxes which represent somewhere around 25% of total tax revenue. Whereas we don’t have them at all. This was a point Dr Coleman made in the podcast so it’s good to see Inland Revenue will be looking at that.

No to considering financial transaction taxes

As part of managing the whole scope of the LTIB Inland Revenue believes it “could reduce the discussion of some tax bases are less likely to be subject of significant public discussion such as financial transaction taxes.” This makes sense. Financial transaction taxes or Tobin Taxes are something that pop up in discussions about tax reform. I’m ambivalent about whether in fact they will achieve what people make out for them. I think they would add complexity and they would drive all sorts of different behaviour.

They’re not going to do a full review of the interaction of the tax and transfer system. And to be fair to Inland Revenue, I think that would be an entire long-term insight briefing of itself. But their chapter on consumption taxes discussed using transfers to offset GST rate increase somewhat similar to what Andrew Paynter proposed last week. (Just to repeat Andrew’s proposal is his alone and does not reflect any Inland Revenue policy). According to Inland Revenue the tax regimes chapters “will largely focus on how to make our main tax bases more flexible to rate changes, including considering options to support system coherence and integrity.”

Providing an analytical base

In summary Inland Revenue’s intention

“…is to provide an analytical base to provide further consideration of these issues in the future. For example, our focus on tax bases is on understanding the relative costs of taxing different underlying factors and what the overlaps and differences are in those tax bases. Our focus on tax regimes is on exploring how to make our tax based main tax bases more flexible to rate changes without undermining equity or efficiency goals.”

All of this seems perfectly reasonable to me.

From here there will be a future opportunity to provide feedback when Inland Revenue releases a draft of its briefing for public consultation in early 2025. It will then be finalised and given to Parliament in mid-to-late 2025.

Sir Roger Douglas’s radical proposals

Inland Revenue have also published all the submissions, from those who gave permission to do so, adding up to 175 pages of submissions, from individuals and organisations alike. It’s interesting to dip in and see what is being suggested on the topics. Sir Roger Douglas was one of the submitters and as you might expect, the old warrior is still looking for something radical.

Part of his proposal is a tax-free threshold of $62,000. But the trade-off is most of that gets put into retirement and health accounts. With the proposed retirement account, he’s probably reflecting the thinking of Andrew Coleman about the need for the current generation to start saving in earnest because of the various pressures coming towards us. Can’t say I agree fully with Sir Roger’s proposal but full marks for boldness.

Feedback on Andrew Paynter’s proposal

And finally, this week, to pick up a little bit from last week’s podcast with Andrew Paynter and his proposal to increase GST by 2.5% points to 17.5%, but then with a rebate for low- and middle-income earners. The transcript has been very well read and generated a phenomenal number of comments, over 150 at last count, and I thank all the readers and commenters for that.

What about the self-employed?

One commenter asked a question which we didn’t cover off during the podcast; how would Andrew’s proposal apply to the self-employed? The answer is it would use something similar to the provisional tax system. A person’s income would be uplifted from last year and if you’re in the range then you qualify for the proposed payments.

Last week Tax Management New Zealand and the Young International Fiscal Association network ran a joint presentation for the two winners, Andrew and Matthew to come and present their proposals. If you recall, Matthew proposed expanding the withholding tax regime to contractors. Andrew and Matthew both made excellent presentations to a very engaged crowd, and I can see why the judges had a difficult time splitting the pair. So well done again.

Left-to-right Matthew Seddon, Terry Baucher and Andrew Paynter

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.