The Organisation for Economic Co-operation and Development (OECD) recently released its 2026 Economic Survey of New Zealand. The OECD, like the International Monetary Fund (IMF), carry out regular reviews and this is a fairly detailed report running to over 140 pages, which you would expect, given the OECD has a significant economic database to work with.

The OECD was cautiously optimistic about the state of the NZ economy but noted that GDP growth was slower than in many OECD countries. Ongoing fiscal consolidation was needed, but the Middle East conflict may require more “targeted support”. It recommended ensuring “strong accountability through transparency of the [RBNZ’s] Monetary Policy Committee decision making”. Other recommendations included harnessing digital tools to improve health system performance and for a more affordable, secure and sustainable electricity system (which, in the long term, does not include LNG in the OECD’s view).

Not all recommendations made by the OECD or the IMF are greeted with enthusiasm by the government of the day. The Prime Minister reacted very strongly to warnings about the Government’s LNG proposals, calling the OECD’s report “a load of rubbish”.

Unlocking capital markets to drive growth

It’s Chapter 4 of the survey, which I found most interesting and relevant, as it included a discussion of our tax settings relating to the taxation of savings. This section was written by Dr David Haugh, the head of the New Zealand (and Finland) desk, together with his colleagues Kyongjun Kwak and Carl Magnus Magnusson. Dr Haugh is actually a New Zealander who started his career with the Treasury before joining the OECD. That means he has a good background knowledge of New Zealand and our challenges.

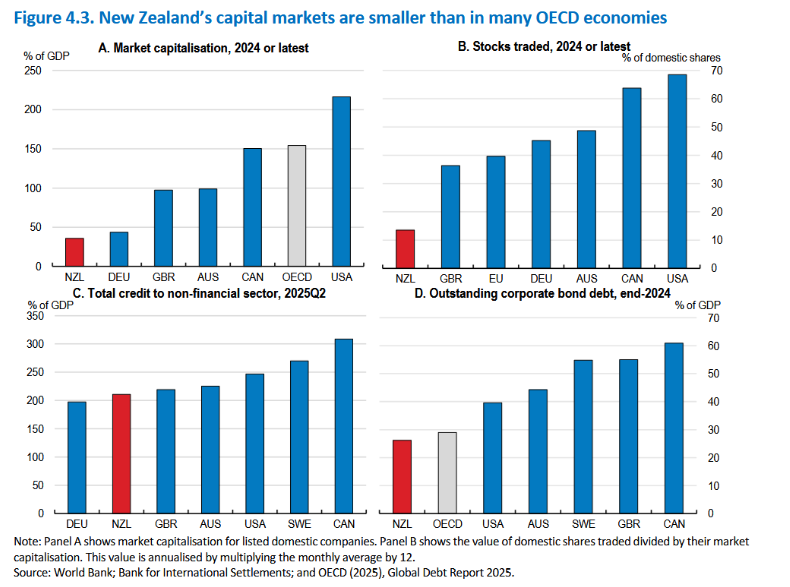

The background summary is that our capital markets remain “shallow by international standards, constraining long-term investment, innovation and productivity growth”. The survey notes that the NZX has seen no major domestic initial public offerings since 2021. That’s apparently part of a worldwide trend, as many firms that might otherwise have gone to market have instead opted for a private or trade sale. A classic example would be Fonterra’s recent sale of its global consumer and associated businesses, Mainland Group, to Lactalis.

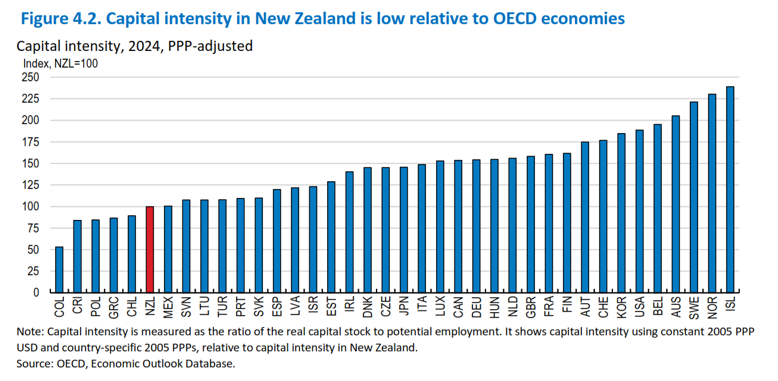

There are some pretty damning graphs illustrating the scale of the problem. Quite apart from smaller-than-average capital markets, ‘capital intensity’ or the ratio of real capital stock to potential employment is low relative to other OECD economies. In 2024, New Zealand’s capital intensity was just about 100%, whereas if you look at Israel, Norway and Australia, they’re all over 200%.

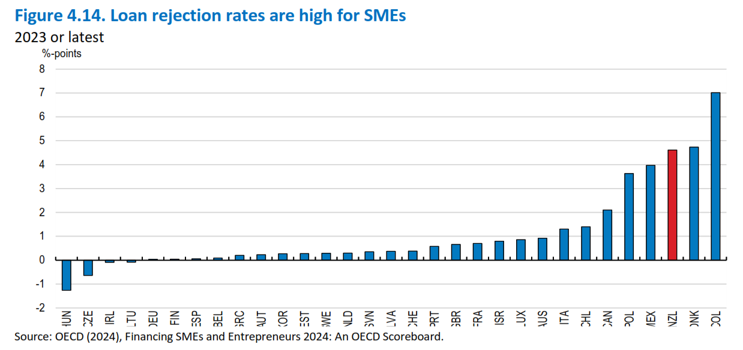

There’s also a sideswipe for the Australian banks, with the OECD saying “costly bank lending dominates, with OECD analysis of lending margins showing they’re about twice the international norm”. With the main banks preferring mortgage lending, SME loan rejection rates are high.

There’s a fairly blunt assessment of why our capital markets are underdeveloped – the decision in 1975 to cancel the Third Labour Government’s compulsory superannuation scheme:

“The decision to abolish the private pension saving schemes in 1975 and replaced it with a publicly funded universal pension at age 60, significantly hampered the development of New Zealand’s capital markets by reducing households’ incentives to accumulate private pensions, depriving capital markets of a key source of long-term domestic funding.” [page 98]

Developing public equity markets – the Swedish example

There’s a very interesting discussion about how Sweden “has developed one of the most dynamic and inclusive equity markets relative to its economic size in Europe and across the OECD.” A key element of this is the Investment Savings Account, or an ISK account. There are over 4 million ISK accounts, with half the adult population having an ISK. These have helped channel household investments into listed equities. Britain’s Individual Savings Account is a slightly similar product. The recommendation is that we consider introducing a non-retirement New Zealand Equity Savings Account.

Raising household savings through changes to KiwiSaver

The report notes our retirement savings are fairly inadequate by world standards. In September 2025, the value of funds under management in KiwiSaver was $141 billion or 32% of GDP. By comparison, in Australia, the assets under management exceeded A$3.6 trillion or 133% of GDP. Furthermore, the average Australian retirement pension plan value is NZ$130,000 or nearly five times greater than the average NZ$28,000 in New Zealand.

The survey notes that withdrawals are allowed to buy a first farm or first house, which, together with increasing withdrawals for hardship (these have doubled from $100 million a month in 2023 to $200 million a month in 2025), slows the accumulation of funds. The OECD questions the purpose of withdrawals for first farms or houses. It suggests that if the policy objective is to support low-income people into house ownership, then a separate instrument would be more effective. The OECD also recommends not creating any further exemptions.

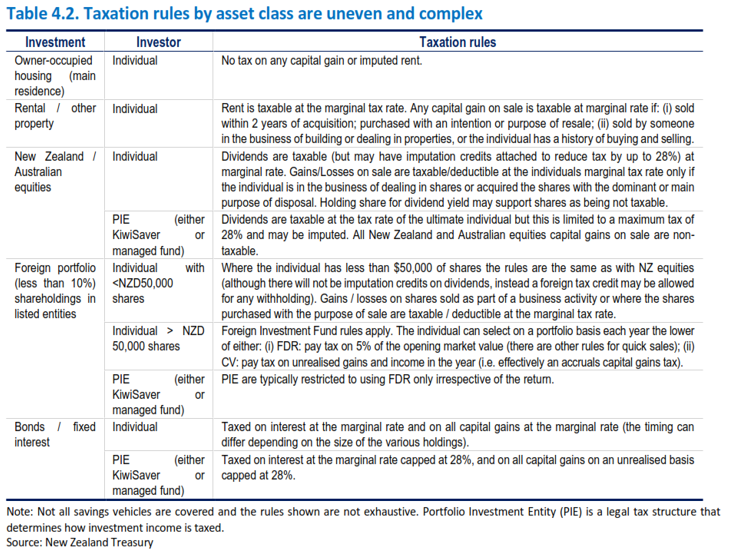

‘New Zealand’s taxation of capital income and savings is complex and uneven’

The survey then discusses the taxation of capital income and savings, which it describes as “complex and uneven, with housing taxed lightly relative to financial assets and especially pensions”. Our corporate income tax at 28% is noted to be amongst the highest in the OECD. Taken together, these settings:

“…distort household and firm investment decisions and suppress the accumulation of private pensions and other long-term financial savings, which is a critical issue not only for capital market developments but also for retirement income adequacy.”

In short, the way our tax system has distorted savings has had long-run consequences. This is something I’ve been saying for a long time and it’s also the view of the International Monetary Fund.

Increasing the accumulation of pension savings by reforming the taxation of savings

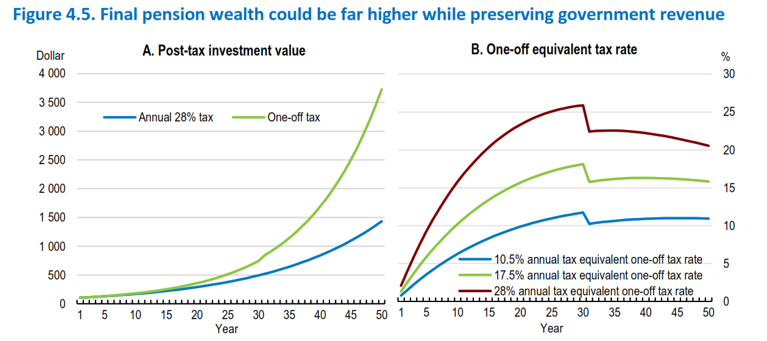

The OECD’s view is that the taxation of savings needs reform to allow greater accumulation of pension savings. The survey notes only seven of 38 OECD countries tax the investment income pension and only three, New Zealand, Australia and Türkiye, have a tax-tax exempt system (TTE). The most common system operated in about 17 out of 38 countries is an exempt tax, which is what you see in the UK and America, which allows the accumulation of more funds within the fund that eventually gets taxed as a pension.

The critical disadvantage of our TTE system is that it penalises the accumulation of long-term financial retirement assets, sharply reducing compounding returns relative to the exempt-exempt-tax systems used by many other countries, such as the UK and the United States.

The OECD bluntly concludes:

“The TTE system for financial savings combined with light taxation of housing in New Zealand… makes the overall system one of the most housing-biased tax systems in the OECD. This bias has been capitalised into higher house prices, larger new dwellings, lower ownership rates amongst younger cohorts, and a worsening of New Zealand’s net international asset position, reflecting reduced domestic financial capital available for firms.”

The OECD notes that because pension savings compound over 40 years or so, lowering the tax burden on returns “substantially increases long-run private wealth accumulation”. So, does that mean switching to the common exempt-exempt-tax approach? Not quite. An argument against such tax incentives, and one I share, is that the benefit of such savings is mostly captured by the wealthy who would be saving anyway, and tax incentives don’t lead to significantly increased savings. Another issue with tax incentives is, as Finance Minister Nicola Willis pointed out, they are extremely expensive.

Auto-enrolment and KiwiSaver

According to the OECD, many of these concerns are indirectly addressed by an auto-enrolment system, i.e. everyone would be in KiwiSaver and therefore automatically contributing and saving. UK evidence is that within such auto-enrolment schemes, savings do not fall or rise in response to tax incentives and other private savings are not reduced to offset the diversion into tax-preferred schemes. Furthermore, the strongest benefit of such a change would be for low and middle-income households, who have limited discretionary savings anyway.

Removing or reducing tax on KiwiSaver returns would operate primarily by allowing greater compounding and unchanged contribution patterns, generating substantial increases in total retirement wealth. In other words, directing the incentives there towards the lower-income earner is an approach I fully support.

The survey includes an example illustrating that if this approach is adopted and coupled with a withdrawal tax, the post-tax pension value is twice as large by age 65 compared with the current annual taxation approach.

Overall, there’s plenty of food for thought in this survey. We’ve had a long period of stable policy settings in relation to savings, but we have problems with productivity and access to capital for start-up companies. New Zealand actually has a fairly vibrant tech sector, but as this paper notes, a lot of small tech companies go overseas to get funding because they can’t get it here. I’ve advised on a few such situations, and I’m always surprised the investment capital isn’t readily available here. This OECD survey should therefore provoke plenty of debate amongst politicians and analysts alike, but I fear it will get drowned out by the noise around the coming general election.

The latest National Climate Change Risk Assessment is not a pretty read

More or less simultaneously with the OECD report release, the Climate Change Commission released its National Climate Change Risk Assessment (NCCRA) for 2026. This is the first one that’s been produced since 2020 and is not pretty reading. It identifies the 10 significant risk areas “where focused action would make the biggest difference.” In short, this means increased infrastructure spending, particularly in relation to water infrastructure. The NCCRA warns that without immediate action, water infrastructure could be the “first climate risk to reach an extreme severity level within the next 25 years”.

The regularity of natural disasters has been increasing. According to the NCCRA stat, about 97% of the estimated $33 billion of government expenditure on natural hazards since 2010 was spent on responding to and recovering from disasters, with only 3%, i.e. a billion dollars, spent on risk reduction.

What happens when the insurers withdraw cover?

Whether or not you accept what’s driving climate change, it is happening. The NCCRA notes that 556,000 buildings with a combined replacement value of $235 billion are currently exposed to inland flooding. Insurance premiums are rapidly rising, leading the OECD’s economic survey to note “climate-change-induced rises in insurance premiums make inflation control more difficult”.

Quite apart from rising insurance premiums, my concern is that at some point, the insurers are going to dictate what happens with such properties. If the insurers start withdrawing cover, and that’s now coming into general discussion, people will look to the government to help because if they can’t get insurance on their properties, the banks won’t lend against that. This also ties into what the OECD was saying about the high dependency on property ownership for savings.

The NCCRA notes that if we keep allowing the current pattern to continue, of simply accepting damage will happen and then repairing it afterwards, this will drain funds away from core services such as health and education. Over the past 15 years, we’ve spent on average $2 billion a year, or roughly 0.5% of GDP, on climate mitigation and recovery, and things are only getting worse.

All this comes back to a long-standing argument I’ve been making here on the podcast and elsewhere: that climate change is going to drive changes in our tax system by way of having to increase revenue to fund these changes. There’s been plenty of debate about the long-term fiscal sustainability of New Zealand superannuation, but the impact of climate change is an immediate and growing problem.

This is a long-term issue where you really do hope that all the major parties in Parliament accept the need to address this and move accordingly. But as we’ve seen with the superannuation debate, that’s not likely to happen.

The Australian Budget

Finally, across the ditch, the Australian Budget was handed down on Tuesday, 12th May. There had been a lot of speculation beforehand that there would be changes to ‘negative gearing’ and the taxation of capital gains. This speculation was correct, but the extent of the changes has taken people by surprise.

Negative gearing is what the Australians call the ability to offset losses from residential property investment against other income. With immediate effect, any new investors will now only be able to offset losses from purchases of ‘new builds’. (Rather like our previous interest limitation rules.) Taxpayers with existing rental properties will still be able to offset their losses against other income. In other words, they will not be subject to what we term ‘loss ring fencing’.

The capital gains tax surprise

Presently, Australia grants a 50% discount on the amount of a capital gain for individuals, trusts and partnerships if the asset in question has been owned for more than 12 months.

This 50% discount will no longer apply for any gains realised on or after 1st July 2027. Instead, there will be a cost-based indexation, i.e. based on retail price, which was the rule between 1985 (when Australia introduced capital gains tax) and 1999. There will also be a minimum 30% tax rate on capital gains.

This is a significant change, and it’s expected to result in a rise in payable capital gains tax. Pre-Budget speculation focused on gains from residential property investment, but this change will apply to all asset classes.

A potential silver lining?

Now, the interesting thing if you’re a New Zealand resident and you’ve got a property investment in Australia, this change may be beneficial. At present, New Zealand tax residents are subject to Australian capital gains tax on disposals of Australian-situated property, but because they are not Australian tax residents, they do not get the 50% discount. (Australia is frequently quite sneaky in how it taxes non-residents.)

This change may mean that New Zealand investors subject to Australian capital gains tax on Australian properties may actually be better off. We’ll need to see the details on that, but it’s perhaps a silver lining for everyone.

On that note, that’s it for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and tell you and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

[This is the transcript of the episode recorded on Friday 15th May – it has been edited for brevity and clarity]

Tax continues to feature heavily in the Election with the ongoing debate over the validity or otherwise of National’s proposed foreign buyer tax. But away from the election, it has been a busy week in the tax world. By far the most interesting story, partly because of its source, but also how it speaks to the structure of our tax system, is the commentary from Matt Whineray, the outgoing chief executive of the New Zealand Superannuation Fund (NZSF), about the fund’s tax status.

In an interview with the New Zealand Herald’s Markets with Madison, he remarked on the NZSF’s tax status, noting that since the fund began investing in 2003, it had paid nearly $10 billion in tax, including $2.2 billion for the year to June 2022.

This makes it by far and away the largest single taxpayer in the country. He thought this was rather nonsensical and that the fund really should have tax immunity status in line with many other sovereign wealth funds around the world, (including ACC and the Reserve Bank of New Zealand, both quite substantial investment funds). “My wish would be that we didn’t pay tax because I think that would solve a few issues.”

A nonsensical money-go-round?

He questioned the practice of the NZSF returning money to the Crown in tax, and the Crown in return contributes to the fund annually. “If I take my wallet out of this pocket and put it into this pocket, I haven’t got richer.” The problem, in his view, was exacerbated when the Crown stopped contributing to the fund completely, as it did for almost a decade between 2009 and 2017.

It’s interesting to hear such commentary from Matt Whineray, which highlights an anomaly about the NZSF, in that it is a sovereign wealth fund, but it pays tax, which is highly unusual around the world. In fact, I’m not sure there are any other sovereign wealth funds which do pay tax. (It’s an issue Whineray’s predecessor Adrian Orr also raised, ashas Whineray previously).

Now when the NZSF was set up 20 years ago, the rationale behind it paying tax was this would help it make sound investment decisions based on investment principles and not by tax considerations. And in a broader sense, that’s not unreasonable. I always tell my clients, don’t let the tax tail wag the investment dog. Think in the longer-term investment and returns rather than the short, potentially shorter-term tax implications.

A “Fair” Dividend Rate?

Someone else this week commenting on this question of the tax status of savings was financial planner Rachelle Blanch speaking to Susan Edmonds of Stuff.

Rachelle thought it was time for a review of the Foreign Investment Fund (FIF) regime, particularly in relation to how it applies to portfolio investment entities such as KiwiSaver funds. Now, the FIF regime and the Financial Arrangement regime are the two main reasons the NZSF pays so much tax. That’s because both regimes tax unrealised gains and there will be substantial unrealised gains in investment funds.

As the story in Stuff noted, under the FIF regime KiwiSaver funds and the NZSF must use what’s called the fair dividend rate in respect of their overseas shareholdings. This deems 5% of the opening market value of the investments held at the start of the tax year to be taxable income. Now obviously as KiwiSaver funds grow in size, and they diversify out of the New Zealand market as the NZSF has done, then the amount of tax payable as a consequence of the FIF regime will increase. However, unlike individuals or trusts, who can switch methods to mitigate the impact of a drop in values of some of investment funds by adopting what we call the comparative value method, KiwiSaver funds and the NZSF can’t do that.

How much tax is payable under the FIF regime is not at all clear. The NZSF is probably the only entity which can give a pretty accurate gauge on that. But to give you some idea of the total tax that might be payable – the Financial Markets Authority produces an annual report each year on KiwiSaver funds, and it notes that for the year to June 2022, KiwiSaver funds paid over $256 million in tax for that year. Remember in the same period, the NZSF paid over $2.2 billion.

Rachelle Bland has raised a very good question as to whether, in fact, this is an appropriate tax policy response where people have long term savings. She describes it as effectively a capital gains tax. Another way of looking at this, and it’s how I describe it whenever explaining the regime to overseas clients, is that it operates as a quasi-wealth tax.

As I said, there’s no mitigation for significant falls in stock markets. Unlike a capital gains tax regime which taxes on a realisation basis you can decide to realise capital losses and offset them against capital gains. You can’t do that under a FIF regime. Therefore you have this situation where the value of investments are falling but you’re still paying tax on the value of those investments. And that’s been the scenario for quite a few funds over the past 12 to 18 months.

What about a tax exemption then?

It’s not surprising then that quite apart from this anomalous washing – as Matt Whineray referred to the process of cycling funds from the Crown to the NZSF and then back in the form of tax – there’s also calls for some form of tax exemptions for KiwiSaver funds. You see such tax exemptions around the world for other pension schemes. New Zealand is yet again, a bit of an outlier here. The reason such exemptions were taken away in the late 1980s is they are costly. However, in overseas jurisdictions where tax exemptions apply to pension schemes withdrawals are taxed, whereas in our system we apply what we call a tax-tax-exempt approach where the contributions are made out of after-tax income, the schemes are subject to the ordinary taxation rules, but any withdrawals are exempt.

What’s the most effective approach? Well, that’s still a matter for debate. But one thing to keep in mind is that tax does have an impact on the long-term return of funds. Now, whether anyone is going to do anything about this is very questionable. The FIF regime in its current iteration has been in place now since 1st April 2007, and it generally works pretty well. The rules were very controversial when they were first proposed. There was an absolute storm of protest when they were first proposed, with Parliament’s Finance and Expenditure select committee receiving 3,400 submissions against the introduction of what is now the FIF regime, and only two in favour. In the face of this criticism, they were actually reshaped and now everyone has got used to working with the regime.

And this perhaps is the critical point. Governments appreciate the tax paid by the NZSF and KiwiSaver funds. The total tax for the year ended 30th June 2022 from those two sources probably represents just about 2% of the total tax take for that year. Therefore, changing the tax treatment for the NZSF and for KiwiSaver Funds would be an expensive move even if as a trade-off the Government might not then need to make any more contributions to the NZSF.

Wrong sort of investment signals?

Given the short-term pressures at the moment on the Government’s books, I think any move in this area is not going to happen. But I also consider it underlines a scenario where we’re prepared to tax savings under the current tax system, but generally whole asset classes, such as property, the bright line test excepted, are outside the tax net. This treatment sends an investment signal which politicians aren’t prepared to address.

Where does investment get directed? The evidence we have points to it being directed into relatively unproductive residential property investment as opposed to the likes of KiwiSaver funds, which will invest in productive businesses.

The discussion we’re not having

Now, this is a discussion we’re not having at the moment about how the tax system and investment interacts. As I’ve said in previous podcasts when you consider National is proposing removing commercial property depreciation on non-residential property again, (as is Labour for its part) in both cases to fund some form of tax cuts this to me sends the wrong signals. We’re basically directing funds away from investment in our economy into consumption.

But this is not a discussion we’re going to have because although politicians quietly recognise that whatever we the electorate might say about the impact of tax in the back pockets – and we’ll happily all take tax relief, tax cuts, how you phrase them – we also like the services tax provides. So, this dichotomy exists. We’ve got to maintain services as far as possible but not want to pay for them. But as I’ve said repeatedly, I think the under taxation of capital is an unsustainable position long term.

Donations tax credit review announced

Moving on, Inland Revenue just carries on carrying on regardless of whether the Government is out campaigning. It has been busy churning out quite a lot of interesting material. But two particular initiatives happened this week.

Firstly, on Friday, it announced it is going to undertake a review of the rules relating to the donations rebate rule. This review is part of the Regulatory Stewardship programme required of all state agencies in respect of the rules they administer. In this case, a review is going to assess whether the donations tax credit regime is operating effectively, is achieving its policy intent, and how it compares internationally.

Inland Revenue will open up consultation with an aim of undertaking this review and completing a report, setting out its findings as well as any recommendations by mid-2024. Interested parties will be contacted on this. I imagine you can expect the Charities Commission, some more major charities, would be approached. I think the main accounting bodies, together with the New Zealand Law Society will also be approached for comment on the matter.

A fairer Government debt policy framework?

The second Inland Revenue initiative and probably something that’s going to have more immediate impact ties into the rather strange case we talked about last week involving the Nelson woman who got herself into a whole heap of trouble with Inland Revenue and decided the best way out of avoiding a $365,000 tax debt was to sell her property worth $845,000 to a UK company. The Official Assignee took a dim view of the idea and obtained a court order striking the sale down.

Leaving aside the oddities involved the case is relevant for the important question of tax debt and other debt that’s owed to the Government. According to the New Zealand Herald story reported last week, as of 30th June 2023 Inland Revenue is owed nearly $5 billion.

Now, both the Tax Working Group and the Welfare Expert Advisory Group took a look at the question of debt owed to the Government as part of their reviews, and they recommended there should be some form of all of government approach to debt. Firstly trying to prevent debt arising with the Government, but also how each relevant government agency responds and manages that issue.

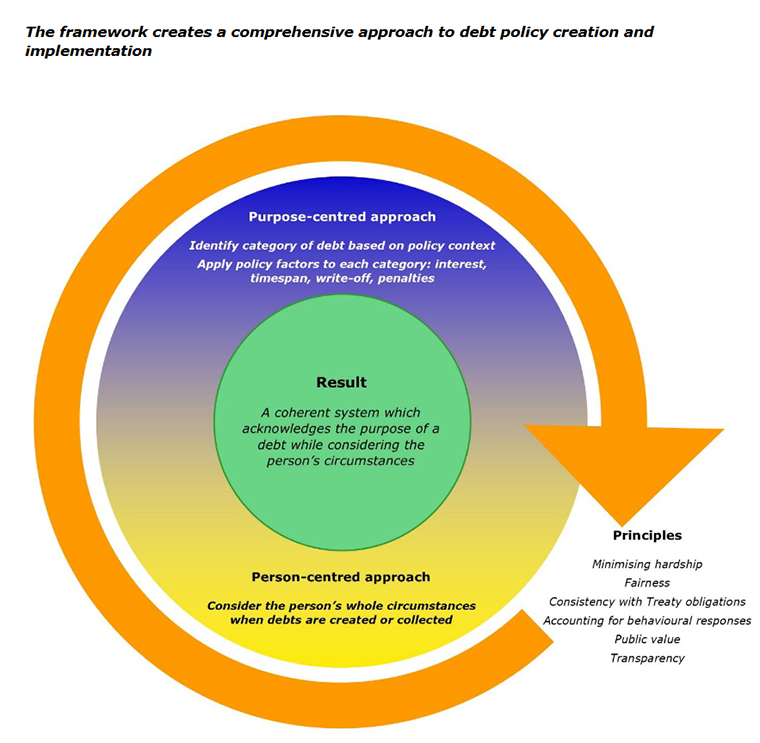

Consequently, a policy framework for debts the Government is owed has now been developed and has been signed off by the Cabinet. Inland Revenue this week released its report and background details on this framework.

There’s quite a bit to consider in here, not just the $5 billion Inland Revenue is owed but the other debts built up, primarily with the Ministry of Social Development and also with the Ministry of Justice.

According to this report, at present 762,460 New Zealand residents collectively owe $4.68 billion of debt to these three agencies – Ministry of Social Development, Inland Revenue and the Ministry of Justice. More than a quarter of these persons owe debt to two or more agencies and 6% that’s over 45,000 people owe a debt to all three. Furthermore, around three quarters of this debt, so that’s well over $3 billion, is owed by low-income individuals, many of whom rely on government benefits as well. 13% or just over 99,000 people owe more than $10,000 to the Government.

More than 85% of those who do owe a debt have owed it for more than a year and about 45% cent, an incredible number, have owed debt for at least four years. Finally, Māori and Pacific people are overrepresented in almost all categories of debt a sadly quite typical issue.

The debt policy framework is trying to ensure is that debt recovery is fair and effective and avoids exacerbating hardship. And above all, it aims to prevent debt occurring in the first place and not exacerbate issues.

There are three main parts to the framework. Firstly, a set of overarching principles for creating and managing debt. Then secondly, a purpose centred approach which classifies debt into different groups according to the policy purpose and discusses how different settings might be appropriate for some purpose and others. And then finally, what’s called term to person centred approach, which takes into consideration the personal circumstances, with focus on consideration of financial hardships, as I said.

These debt issues tend to exacerbate and build on each other leading to a circle of despair. $10,000 of debt doesn’t sound like a lot, but for very low-income people it seems like an insurmountable mountain.

Anyway, this framework has been signed off by the Government after feedback from quite a number of interested agencies. For example, the Citizens Advice Bureau, the Methodist Alliance, the New Zealand Council of Christian Social Services, the Salvation Army, and a whole range of other non-governmental organisations. Hopefully this feedback will build a better framework for the practice of managing this debt.

Good but Inland Revenue also needs to do its part

I welcome this initiative, but I also think that as part of it, Inland Revenue needs to be also considering its approach to debt management, such as the effectiveness of the late penalty regime, and how efficiently it is on top of managing debts, because if the debts get away from people, they just give up. That’s what my experience has shown time and again and it’s also what Inland Revenue has experienced.

I think it’s still a good step forward, particularly, in trying to bring a coordinated approach because there’s nothing more infuriating to someone who might be unlucky enough to find ourselves in a position of debt with two or three agencies, and finding that the approach taken by each of those agencies is different.

The Tax Working Group recommended a single Crown agency to manage current debt should be established to deal with this issue. That does not seem to have been part of these recommendations at the moment, maybe it might be picked up at a later stage. Nevertheless, it’s a step forward in the right direction and we’ll hope that it starts to address these issues of managing the debt fairly and efficiently for people.

The $5 billion PREFU hole no-one is worried about

And finally, this week, back to the Election. We’re still hearing plenty about tax in the election campaign. Politicians are all out on the trail telling us everything that’s going to happen or not happen. This week the formal opening of the government books happened with the release of the Pre-election Economic and Fiscal Update (PREFU). There was plenty of differing interpretation about the state of the government’s finances going forward.

But there was a wonderfully interesting little snippet which Newsroom picked up on, and that was the impact of next year’s Matariki public holiday. Matariki always falls on a Friday, and next year it falls on 28th June, which is the last working day of the fiscal year to 30th June 2024. And because of that, the cash that would come in on that day, which represents about $5 billion of GST and provisional tax won’t actually hit the Government’s coffers until the following Monday, which is 1st July and the start of the following tax year. So, on the face of it, the Government’s going to be $5 billion short of cash for the current year ending 30th June 2024.

As a Treasury spokesperson said, “This public holiday effect is expected to affect the Crown’s tax receipts but not tax revenue, since Inland Revenue will calculate accrued tax revenue as at 30 June 2024 as it normally would at any other year end.”

And for the record, this won’t really affect individuals because we file tax returns to 31st March each year. Furthermore, Inland Revenue won’t penalise people for making a payment on 1st July, the first working day after it was due because Inland Revenue hasn’t switched over to a seven-day banking. So nice quirky little story to end the week.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A new tax bill causes a massive storm but what happens next?

Also a brief run-through of what other tax measures are in the Taxation (Annual Rates for 2022-23, Platform Economy and Remedial Matters) Bill. (TL:DR – a lot!)

On the face of it this was a provision to address a technical issue which had developed over time where fund managers were applying different treatments to how they determined what proportion of the fees they provided were taxable supplies subject to GST and what portion represented GST exempt financial services.

The proposal determined by Inland Revenue was to standardise the approach and apply GST service and fees. This would have taken effect from the 1st of April 2026. We’re therefore talking about a measure three years in the future, but which would have netted an estimated $225 million a year in GST. That in itself probably wouldn’t have caused many issues except the Regulatory Impact Statement which accompanies the Bill, included modelling by the Financial Markets Authority which on the assumption that the increase in GST would be fully passed on to KiwiSaver fund members, KiwiSaver balances would be reduced by an estimated $103 billion by 2070.

And then the fun kicked off. There clearly was quite a bit of misunderstanding about this measure with some people thinking the Government would be charging GST on KiwiSaver balances. The Government was taken completely by surprise and the furore was such that it decided to abandon the proposal within 24 hours of announcing it, which is some form of record. It certainly made for an entertaining 24 hours in tax. You can hear more about what happened in this week’s edition of the Spinoff’s podcast When the Facts Change where Bernard Hickey and I discuss the background to the proposal and how it fits into the history of tax reform since 1984.

But it should be noted that the particular issue of an inconsistency of approach by fund managers still remains. So, what’s going to happen now? Probably Inland Revenue will have to negotiate with fund managers and come to some form of agreement over what proportion of fees it deems to be acceptable to be treated as taxable supplies. This was what happened back in 2001, but that agreement has long expired. Such an agreement is going to take some time, although maybe negotiations already started. We’ll have to wait and see how that pans out.

Ironically the GST on fund management proposal was a relatively minor part of the Bill, although it would have had the biggest single tax effect. The rest of the Bill, as its name implies, covers a whole range of matters, including the gig economy, more GST issues, cross-border workers, fringe benefit, and the bright-line test to name a few.

Addressing the Platform Economy

A number of reporting and other tax issues have arisen around economic activity facilitated by digital platforms. That is where an app connects buyers and sellers and includes accommodation services such as Airbnb and transportation services, such as the ride sharing apps, Uber and Zoomy and Ola together with other professional services provided through digital platforms.

The Bill intends to ensure Inland Revenue has better access to information about income earned by sellers using digital platforms based in New Zealand or offshore. These provisions build on proposals developed through consultation by the OECD. Inland Revenue will get greater information and it will also share that information with foreign tax authorities where it relates to non-residents.

The Bill also wants to maintain the sustainability of the GST system. Digital platforms will be required to collect GST on services provided through them in New Zealand. This will be done by extending the rules that currently apply to imported digital services and low value imported goods. These will now apply to accommodation, ride sharing and food and beverage delivery services all currently provided through digital platforms.

There is a proposed flat rate credit scheme intended to reduce the compliance costs for those accommodation hosts and drivers who are not required to register for GST because the value of the services they provide over 12 months is less than $60,000. The GST changes will come into effect from 1st April 2024 and the net impact is expected to be around $37 million per annum.

These changes reflect the growing impact of the digital economy and the moves by tax authorities to ensure they know what’s going on and close potential gaps in loss of revenue may be arising because some of this may be happening under the table. It also reinforces something we see a lot of already and which we’ll see more of, and that is information sharing with other jurisdictions as appropriate.

We’re still working through the impact of COVID-19. And one of the areas where I’ve seen quite a bit of interesting work develop is in relation to cross-border workers. In the wake of the pandemic, we’ve seen a lot of people return to New Zealand from overseas. In many cases these returnees continue to carry on working remotely for their previous employer. This pattern of working remotely has expanded greatly as a result of the pandemic, and I don’t think that’s going to change significantly. But it was also another one of the situations where tax legislation and reporting and withholding tax obligations haven’t kept up with developments.

The Bill therefore has measures to deal with cross-border workers. The PAYE, FBT and employer superannuation contribution tax rules are very strictly applied, but they are incredibly inflexible. They really don’t take into account that employees might be working in New Zealand for non-resident employers and have very different compliance circumstances to those employees of New Zealand resident employers.

The Bill’s proposals acknowledge that such people coming in and working remotely for overseas employers justify taking a different approach to help reduce compliance costs for those cross-border workers. The key amendments are to allow more flexible application of the PAYE rules in specific circumstances. For example, it might allow PAYE to be paid annually. There’s also a repeal of a little used PAYE bond provision.

Alongside those rules are changes to the non-resident contractor rules which relate to the performance of services by non-resident contractors in New Zealand. These are essentially a withholding tax which operates to try and manage the tax risk of people coming in for a short period to perform contract work on a project and then return overseas. Without these non-resident contracting rules, no tax would be deducted. These rules have been in place for a very long time. Apparently, they were first introduced in the wake of the ‘Think Big’ projects of the late seventies and early eighties. They also apply quite extensively to the film industry as well which is where I first encountered them.

The non-resident contractor rules are being tweaked to update them and manage the compliance costs for those subject to them. Again, this reflects a trend that had been developing but has accelerated in the wake of the pandemic. The changes for the PAYE and non-resident contracting rules take effect from 1st April next year.

Notwithstanding what went on with the GST on managed funds issue, there’s quite a bit of other GST matters addressed in the Bill. These include provisions to address issues in the GST apportionment and adjustment rules. These are intended to reduce the compliance costs these rules impose and supposedly better align with current taxpayer practises.

There will be a principal purpose test for goods and services acquired for $10,000 or less GST exclusive. This would enable a registered person to claim a full GST input tax deduction. The other key change is to allow GST registered persons to elect to treat certain assets that have mainly private or exempt use, such as dwellings as if they only had a private or exempt use.

That latter change addresses an issue which has popped up from time to time in is that people may have made claimed GST as part of a home office deduction. If so, then potentially when that property is sold, is it therefore not the case that some portion of the sale will be subject to GST? This was a matter which technically existed, but probably wasn’t being addressed by many taxpayers and advisors.

This issue is generally covered by the GST apportionment and adjustment rules which are very complex and have high compliance costs. Under these rules if you have claimed an input tax deduction based on the estimated use business use of an asset, you are meant to track the business use of the asset. Where the actual use is different from the estimated business use, then you calculate and return an adjustment at the end of the tax year.

This is quite an involved process, and this measure is intended to try and simplify the matter. It’s a sensible change, in my view, which reflects the fact that although GST is a very broad-based tax, you can’t actually really describe it as a simple tax in its operation. There are all these issues around its margins regarding what represents business use, what proportions become taxable and therefore subject to GST, etc. And as we saw in relation to the GST and fund management services, the sums involved can be quite large actually. These proposed changes to try and simplify matters and will take effect from 1st April 2023.

I frequently discuss tax and environmental issues and I’m therefore pleased to see a proposal in the Bill for an exemption from fringe benefit tax (FBT) for certain public transport fares which are subsidised by an employer. This will take effect from 1st April 2023.This is a good example of tax being used as a behavioural change and comes about by looking at the bigger picture of how we address greenhouse gas emissions and what role can tax have in that. The Tax Working Group identified that the FBT treatment of parking is inconsistent and in many cases is not subject to FBT. By contrast, FBT is applied to subsidised public transport.

When you step back and take a wider environmental policy perspective about this, what’s happening is the opposite of what you really would want. The policy should be to tax parking to help reduce emissions and encourage the use of public transport. That’s what this measure is intended to do. It’s a very welcome move which is estimated to cost about $9 million a year. This would also appear to be a good example of how environmentally friendly changes can be achieved at relatively low cost.

Outside of the main policy issues we just discussed, the Bill, as is typical, contains a whole heap of provisions relating to many other issues. For example, there’s a number of changes in relation to the Bright-line test and interest limitation rules introduced last year.

Unsurprisingly, given the complexity of those rules, we are seeing a number of tweaks and clarifications about how they operate. One such example relates to when relief is available under the bright line test, when land is transferred on the death of the owner to the executor of or beneficiaries of the estate. Such a transfer is meant to be exempt, and the Bill has provisions making that clear.

There are some other provisions relating to rollover relief, that is when the bright-line test does not apply to transfers between related parties in certain circumstances. Most of those amendments will take effect the day after the Bill receives Royal Assent, which will probably be in late March next year. But some pleasingly have a retrospective effect back to when the changes to the Bright-line test and the interest limitation rule were announced on 27th March 2021. I fully expect we’ll see more such technical changes in the future, possibly even with some Supplementary Order Papers to this particular tax bill.

Another provision deals with a potential issue with the foreign trust regime and the exemption for foreign trusts whereby income from a non-New Zealand source is not taxable in New Zealand so long as it’s not distributed to a New Zealand resident. In some instances, a trust can make use of that provision but not have to comply with the foreign trust, registration and disclosure rules. The Bill therefore has provisions addressing that issue and some other minor technical matters applying to foreign trusts.

The recently announced build to rent exemption from interest limitation is also part of this bill. According to the supporting Regulatory Impact Statement this will cost $2.1 million if applied to existing build to rent assets.

Then inevitably, as in any of these tax bills, there’s a whole heap of other little remedial matters tidying up technical issues that have arisen around student loans, financial arrangements, provisional tax look-through companies, dual resident companies and more.

Ordinarily, this type of tax bill would barely get a mention in the press, so this week’s drama was quite unexpected. Now the dust has settled, it’s worth remembering that the issue around inconsistent treatment of GST on fund management services still remains. Ultimately, the Government backdown is another example of how short-term politics will nearly always trump longer-term policy.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

This week, a seemingly arcane tax change could be of major benefit to Kiwis who have Australian superannuation funds, rethinking the taxation of redundancy and Google’s 2019 results highlight the difficulties of taxing the digital giants.

Right now, New Zealand citizens or New Zealand permanent residents are the only people who can get into the country. And as the news headlines over the past couple of weeks have shown, testing at the border has become incredibly important in ensuring that COVID-19 does not gain another foothold in the country.

What you are also seeing is a significant rise in the number of Kiwis wanting to return to New Zealand. There are approximately one million Kiwis around the world, including nearly 600,000 in Australia. And the way the pandemic has been handled so far has made many expatriate Kiwis look at returning to New Zealand.

And a significant number of those may come from Australia. Now Australia has compulsory superannuation under which you and your employer are required to make contributions to a superannuation scheme. Unlike KiwiSaver, where you can only ever have one KiwiSaver scheme, it’s quite possible to have a number of Australian superannuation schemes. And what sometimes happens is that people lose contact with their superannuation schemes or vice versa.

Under Australian law, after a while unclaimed superannuation money is required to be repaid to the Australian Tax Office. This could affect Kiwis who have returned to New Zealand but have lost their records relating to an Australian superannuation scheme. After a while the Australian scheme must pay the funds in that scheme to the Australian Tax Office as unclaimed superannuation money.

All this sounds a little arcane, but there are absolutely billions and billions of dollars invested in these schemes (A$2.7 trillion as of the end of the March 2020 quarter), and the amount of unclaimed superannuation money can be quite significant.

Since 2013, New Zealand and Australia have had a Trans-Tasman Savings Portability Agreement in place to mainly encourage or rather remove barriers to workers freely moving across the Tasman.

The bill has a provision which is to allow the direct transfer of New Zealanders’ Australian unclaimed superannuation money from the Australian Tax Office into a KiwiSaver scheme.

This is a measure to get around the issue that once the Australian superannuation scheme deems the funds lost, it’s impossible under Australian legislation for Kiwis to get their money out.

Another handy thing to keep in mind, is that unlike the tax treatment of other foreign superannuation schemes, if you have an Australian superannuation scheme and you transfer it into a KiwiSaver scheme, you will not be taxed, even if that transfer happens more than four years after your return to New Zealand.

So, this is a measure which is favourable for those who have Australian superannuation schemes and may have forgotten what they’ve got and now want to bring the funds across. They can do so tax free into a KiwiSaver scheme. As I said this seems a little bit arcane, but it occurs to me given the numbers of returning New Zealanders we’re likely to see, this could become quite important over the next few years.

Taxing redundancy payments

Moving on, a few weeks back, I was talking to Newshub’s Madison Reidy about the taxation of redundancy payments. At present, redundancy payments are simply treated as ordinary pay and taxed at the normal rates, which means that for someone receiving a substantial redundancy payment much of it will be taxed at the top rate of 33%. I suggested this was something that needed to be looked at.

Based on an article in the Herald this week it seems that the Minister of Revenue, Stuart Nash, has received correspondence on the matter and is asking officials to look into it, which is encouraging to see.

The problem is given the circumstances we’re in right, now this sort of thing ought to be dealt with quite urgently. Maybe if we’re going to move forward with changes, it would be opportune to include some form of measure in the tax bill I mentioned earlier, which is going through Parliament right now.

One thing to think about regarding redundancy payments, is because they’re treated as ordinary pay, that means if you have a student loan 12% of the payment will be deducted. If you’re in a KiwiSaver scheme, then a further 3% at a minimum will be deducted and to your KiwiSaver scheme, fortunately, ACC does not apply.

So it could be if you’re earning above the $70,000 top rate tax threshold (which is roughly $1,350 a week) and you receive a redundancy payment, and then if you have a student loan and are also in a KiwiSaver scheme, you will lose 48% in deductions. This is why I feel it’s actually quite urgent given the circumstances we are in, that the government reconsiders the current tax treatment of redundancy.

There’s an additional bite to this for those who might receive a payment of over $30,000 before tax. This group of people are not eligible for the COVID-19 income relief payment. This is the special relief benefit for anyone who’s lost a job because of COVID-19 between 1 March and 30 October 2020. Such persons are entitled to a weekly benefit payment of $490 if they were working for more than 30 hours. The payment is untaxed and is nearly double the payment someone would normally receive who is unemployed. Fortunately, MSD has lifted its requirement for someone to spend all their redundancy before they can apply for the job seeker payment of $250 a week.

Nevertheless, the current tax treatment of redundancy needs to change urgently. But it can only be done by a statutory amendment. So, it would be good to see Inland Revenue and the Minister of Revenue moving quickly on this to make a change to help those who are going to lose their jobs or have lost their jobs in the past few months.

Taxing Google

Google New Zealand not so long ago released its financial statements for the year ended 31 December 2019. These show that its income tax bill has risen to $2.4 million.

Now, Google’s 2019 accounts were the first ones prepared as part of its more transparent country by country reporting. The accounts showed that its New Zealand revenue had increased significantly since previous years to $36 million with a pre-tax profit of just over $10.6 million.

What the accounts also show is the difficulty of taxing the digital giants and how little revenue will come through for income tax purposes. According to the accounts the pre-tax profit of $10.6 million represents the value of sales less the direct costs of sales for its advertisements and cloud services. And tucked away in the financial statements, was a note that well over $500 million was paid in service fees to related offshore parties.

And this shows the problem with the digital economy. Because so much is now driven off intellectual property, and New Zealand is at the tail end of the world in Google’s case we don’t create much intellectual property. Our right to tax is therefore quite limited.

This is not a problem unique to New Zealand. All around the globe countries are grappling with this question that Google and Facebook are piling up billions of dollars in earnings, but not much income tax is being paid in the relevant jurisdiction.

To deal with this matter the OECD has been working on a coordinated approach. The problem is, in the last week or so, that it’s hit a big hurdle with the US Treasury Secretary, Steve Mnuchin, withdrawing the US from the negotiations. Presently the United States and Europe are at pistols drawn stage, arguing over the question of digital taxation, and Mnuchin and the US pulled out of talks in the last week. This is not good for the whole global economy, and it’s not good for moves to try and get a fairer share of the enormous revenues Google and other digital companies generate.

The Tax Working Group recommended going along with the OECD approach. But it also said that we should have a digital services tax ready to go if negotiations do not go well. We’ve also been watching what the Australians are doing and for the moment they have backed off a digital services tax. But over in Europe, then Britain, which needs a trade deal with the United States, has actually introduced a digital services tax. The French have got one up and running and the Germans are talking about one, too.

So international tensions are building on this and it’ll be interesting to see what the Government decides to do over the next few months as this plays out. But as part of the general upheaval in the tax world going forward we’re going to be seeing this development with the US pulling out of the talks with Europe is not a good one. We’ll monitor developments as they happen, but for the moment it looks like tensions will continue to escalate.

Well, that’s it for this week. Next week, I’ll be joined by Josh Taylor of tax pooling company Tax Traders. We’ll be discussing how tax pooling was able to help businesses’ cash flows in the past few months.

Until then, I’m Terry Baucher, and you can find this podcast on www.baucher.tax or wherever you get your podcasts. Please send me your feedback and tell your friends and clients. And until next time, thanks for listening. Ka kite anō.

From last Tuesday, businesses and the self-employed can now apply for the Government’s Wage Subsidy Extension.

Eligible businesses can get a lump sum payment for a further eight weeks of $585.40 per week per full time employee. The criteria for this has changed from the original wage subsidy scheme. Now a business to qualify must have had a revenue loss of at least 40% for a 30 day period in the 40 days before they apply, compared with the previous closest period last year. So, for example, you’d look at your revenue in this month, June 2020, and compare it with the revenue for June 2019.

Applications for this are open until 1st of September. And as in the case of the existing wage subsidy scheme, it will be administered by the Ministry of Social Development who will be working closely with Inland Revenue on this matter. As I understand it, what happens is the application comes in and MSD will check and then if they’ve got any enquiries, they’ll give Inland Revenue a call.

The tax treatment of this subsidy amount remains the same as previously advised. That is, it is not subject to GST, is non assessable and non-deductible for the employer, although when the payments are made to the employees, they’re taxed as regular income through PAYE.

This does lead to a rather cumbersome tax and accounting treatment and some of us are looking at this and thinking for ease of accounting and to avoid slip ups, it may be better for the employer to treat it as all taxable and deductible. The net effect is the same anyway. We’re looking at the accounting treatment of this, which can get a little awkward because of this mismatch between the wage subsidy payment being non-deductible for the employer but remaining taxable for the employees.

Speaking of ongoing government support, last Friday after I recorded last week’s podcast, the Finance Minister announced that the Small Business Cashflow Scheme would now be extended until 24th of July. This has been an extremely successful initiative for small businesses. So far, $1.33 billion dollars has been lent to well over 70,000 businesses.

And as I discussed last week, it had taken the space that the Government’s Business Finance Guarantee Scheme had not filled. And the comparison between lending under both schemes is quite stark. As I mentioned, the Small Business Cashflow Scheme has been accessed by approximately 70,000 businesses and they’ve borrowed $1.33 billion dollars.

By comparison, lending under the Business Finance Guarantee Scheme has been $86 million to just 503 businesses, according to the latest business lending numbers from the Bankers Association.

Now, it’s not like the banks are not lending. In fact, according to the Bankers Association, business lending since March 26th has been quite extensive. They’ve lent over $10 billion dollars to over 16,000 customers, as well as the separately reducing the loan payments on another $12.5 billion for 13,000 customers. In addition, they’ve deferred all loan repayments on one billion dollars owed by 3,105 customers.

So, the banks have been working in the background. It’s just that the Business Finance Guarantee Scheme, which was quite a headline project at the time, isn’t designed to do the type of lending that businesses are looking for right now. That is short-term, immediately accessible and with an uncomplicated process.

Unfortunately, the Business Finance Guarantee Scheme ticks none of those boxes and that possibly is down to the design of it and the understandable wish of Treasury to protect the Government’s risk.

As I said last week, one of the things about the benefits of the Small Business Cashflow Scheme is it deals with a matter of resourcing for small businesses. The process to borrow under the scheme is very straightforward and money is delivered quickly.

And the process small businesses go through when applying for loans to the banks, they struggle with that. They have to get a lot of material together. It costs some money to get if they bring in their accountant to assist. And there’s no guarantee they’ll get the funds.

So as I said last week, I think once we’ve gone through everything, the Government should look very carefully at how a future scheme to help small businesses could be designed. Maybe we want to have a look at what the Small Business Administration in America does. How it guarantees loans and works together with banks on lending.

A simpler process for small businesses could be very helpful for the future growth of our country. Because it’s accepted by all that, we’re going to have to grow our way out of this recession if we are to get the massive amount of debt that the Government has rightly borrowed for this emergency under control again. [Update, it appears that preliminary discussions about a permanent iteration of the Small Business Cashflow Scheme have taken place.]

Still a live public policy debate

And as part of getting the Government’s debt to GDP ratio under control again, capital gains tax has popped up on the agenda again in a couple of instances this week. Firstly, James Shaw, the co-leader of the Green Party, talking to Jenée Tibshraeny raised it as something that we should be considering. Shaw’s view was that a capital gains tax made more sense now,

“It was our policy when we entered parliament in 1999; it remains our policy today. The extent to which we’ll lead with that or with something else [at the election] is yet to be revealed,”

But I don’t think anyone should be surprised a tax is going to be on the election agenda this year. We’ve had a huge shock to the economy. The Government’s books have been shot to bits. And at some stage, tax will be a feature of how those books are rebuilt.

And talking of rebuilding and still on the tax side, PricewaterhouseCoopers (PWC) issued a report called Rebuild New Zealand, which set out seven planks, as it called them, to rebuild New Zealand.

One of these is about addressing tax reforms. And what it says about that, to pick up a theme of last year’s Tax Working Group, is that tax reform must be considered to broaden the Government’s revenue base and remove investment bias. It refers to the elephant in the room being a capital gains tax. It’s probably no coincidence that Geof Nightingale, who’s a partner at PWC, was also a member of the Tax Working Group.

The report goes on,

“In our view, there is now a greater need than ever to broaden New Zealand’s tax base so it relies less on taxing income. So is it time to look again at a simple, broad based CGT?”

The report cites the example of the introduction of a broad-based GST over 30 years ago as a model for designing a future CGT, and goes on to say,

“The debate on CGT would be very different if New Zealanders had a better understanding of the extent to which it could actually impact them during their lives and also the trade-off that there might be an eventual trade-off between CGT and income tax.”

And this is something I think should be considered: by broadening the tax base to include capital gains tax the need to increase the top rate of income tax, for example, is minimised. There is a trade-off here and I agree with PWC we should be having that discussion. I don’t think we had a great discussion last year.

We’ll probably see more discussion about this during this election. And it will be interesting to see how the parties all fence around the issue. As I said, in April in this Top Five piece, COVID-19 means we are going to need to have a look at the tax system. Whether tax rates rise or CGT comes in are all on the table for discussion.

Getting the max KiwiSaver

And finally, you have until 30th of June to make sure you have contributed a minimum of $1,042 86 to your KiwiSaver scheme in order to qualify for the maximum government top of $521.43 cents. Now, the government contribution isn’t a lot, but it’s free money, so you should take advantage of it if you can.

Incidentally, PWC’s Rebuild New Zealand report suggested the question of boosting savings should be considered in order to help address the funding of New Zealand Superannuation. It noted “While there is much to be admired with Kiwisaver, it remains a lightweight compared to the compulsory savings regimes in other countries, notably Australia”.

The report doesn’t say so but we’re still paying for the decision in 1975 by Muldoon’s third National Government to scrap the compulsory superannuation savings scheme established by the third Labour Government. In my view that decision by the Muldoon Government probably ranks as the single most economically harmful act by any New Zealand government in the past 50 years.

As I said, we’ve been paying for it for the last 50 years, particularly since the Baby Boomer generation reached retirement. And the matter will not go away. The Tax Working Group noted that structural deficits would be increasingly likely by the latter part of this decade. So the issue of addressing the cost of superannuation – how it’s funded – isn’t going to go away.

And on that bombshell, that’s it for this week. I’m Terry Baucher. And you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. Please send me your feedback and tell your friends and clients. Until next time, Kia Kaha, stay strong.