Earlier this year, Inland Revenue ran a consultation on the not-for-profit sector. In the course of that consultation it raised the treatment of the taxation of mutual associations, including clubs and societies. Inland Revenue indicated that mutual transactions between clubs and members, such as subscriptions, which were previously thought to be exempt from tax, were in fact taxable. It transpired Inland Revenue had actually been sitting on a draft operational statement on this matter for some time.

Inland Revenue has now released a draft operational statement (“OS”) on the taxation of mutual transactions of associations, clubs and societies.

This OS takes into account submissions Inland Revenue received on the not for profits consultation. One of the issues this draft OS considers is whether the principle of mutuality applies. As the draft OS notes, under the common law principle of mutuality, an association of people such as a club or society, cannot derive taxable income from transactions within the circle of membership of the association. Mutual transactions do not generate profits for the association, because the amounts received by the association come from members transacting with themselves.

This primarily refers to subscriptions, but as the draft OS also notes, the principle does not apply where legislation provides otherwise. And what Inland Revenue has highlighted in this consultation is that it wants to give greater clarification about the scope of these potentially mutual transactions.

The basic position is supplying stock or services to members is taxable. That’s not a new position, but as the draft OS comments

“…this has not been communicated clearly or consistently, and Inland Revenue is aware affected customers take different approaches. We are hoping to increase awareness of the correct treatment and achieve certainty and consistency by finalising a statement on this aspect following consultation.”

A change of tack

The key point the draft OS proposes is that member subscriptions may be subject to tax, which does represent a change in practice. Therefore, “an object of this consultation is to test whether the reasoning for that conclusion is sound.”

To be frank, this has caused a bit of a stir amongst the potentially affected clubs and societies. There are exemptions given for specific charities and sports clubs, but a large number of organisations would previously have thought and filed tax returns on the basis that transactions involving member subscriptions were exempt. This does work both ways. If the subscription is treated as exempt, then costs relating to subscriptions are not deductible.

The paper contains 7 examples setting out various scenarios and how transactions might be treated. As noted, Inland Revenue’s position is that in some cases membership fees and levies are not mutual in nature but represent income and are taxable. A key point in this approach is if the associations constitution allows distributions to be made to members. If distributions are prohibited, then membership fees and levies are income. The following examples taken from the draft OS illustrate the issues under consideration.

One for legislative reform?

The sector has been taken a bit by surprise by this consultation. In my view it represents such a change of interpretation it should be legislated if Inland Revenue wants to achieve that clarity. To be fair, Inland Revenue is saying that any changes made after consultation is finalised would be prospective and it would not generally seek to reopen prior years. I recommend all potentially affected groups to submit on this draft OS, consultation on which is open until 25th of June.

Inland Revenue gets tough on student loan debts

Moving on, Inland Revenue has been regularly providing updates on the progress of its debt collection and general enforcement in the wake of the additional funding of $116 million over 4 years it got in last year’s Budget for this purpose. Last week, we discussed the extra $153 million Inland Revenue has recovered in the year to date from the property sector alone.

Its latest update this week is about its progress on recovering student loan debt and included the news that “One person was arrested at the border last month and they have since paid off their debt.” According to Inland Revenue at the end of April, there were 113,733 people with student loans believed to be based overseas. More than 70% of those people were in default of their loans and in total they owe $2.3 billion. This includes 150 overseas based borrowers with a combined default debt of $15 million. It is therefore understandable why Inland Revenue is a tougher line on student loan debt.

Information sharing with New Zealand Customs…and airlines

Inland Revenue gets notified by New Zealand Customs about any border crossings into New Zealand by overseas based borrowers. According to the RNZ report apparently airlines are also providing similar information to Inland Revenue. This is an interesting, and previously unknown, detail.

Once notified Inland Revenue will then apply to the District Court and the police can make an actual arrest, which, as noted, happened last month. Since 1st January 2024, 89 people have been advised they could be arrested at the border. This has prompted 11 of them to take action, either by making acceptable repayments or entering into repayment plans and applying for hardship. So far during the current financial year to 30th June, this programme has collected $207 million in repayments from overseas borrowers. This is up 43% on the same period in the previous year. So yes, it’s making progress.

Progress, but…

On the other hand, some of the reported numbers are quite concerning to me, and I consider also highlight why student loan debt has become such a problem. As noted above those 113,733 overseas based borrowers owe over $2.3 billion, but more than a billion dollars represents penalties and interest. What happens is that as the interest and penalties pile up, many debtors get to a point where they feel it can’t be repaid, and they simply freeze hoping the issue will somehow go away. This phenomenon is well understood by Inland Revenue because it happens with other tax debt.

Therefore, the question arises about the efficacy of the current penalty and interest rate regime. Interest and penalties accumulate swamping repayments, so little progress in repaying debt is made even where repayments are being made. The overall amount of debt on Inland Revenue’s books then just blows out.

Debt more than 15 years old? How did that happen?

One particular point really concerns me about Inland Revenue’s latest update. Apparently for over 24,000 of the overseas based borrowers, the debt is more than 15 years old. In many cases, it’s highly likely that people in that category are not going to return to the country, so the threats of arrest at the border are probably not going to be effective.

But then the question also arises is it really very realistic to expect people to repay debt which has been allowed to accumulate for 15 years? And a really big question here is what was Inland Revenue doing during that time?

It’s all well and good to say Inland Revenue is clamping down now. But it seems to me to be against natural justice that it can target debtors where the debt has been allowed to accumulate, and insufficient action was taken early enough to control the debt and prompt earlier repayment.

Inland Revenue, as we repeatedly mention on this podcast, has enormous information sharing and gathering powers. The question really arises as to whether sufficient resources were made available in the first instance to keep control of the student loan debt. And now we’ve reached a situation where, to borrow an old saying, “You owe the bank $100,000, it’s your problem. You owe the bank $1 million; it becomes their problem.” It seems to me that’s where we’ve reached with overdue student loan debt.

Are the rules fit for purpose?

It should also be noted that looking into the legislation applying to student loan debt it appears it’s quite difficult for Inland Revenue to write off debt and interest as part of reaching a settlement. The rules are very prescriptive in such instances, apparently deliberately so.

As a consequence, I wonder if this holds people back about making attempts to settle outstanding debt. There’s also the question of debt over 15 years old and what records are available to prove outstanding amounts. Inland Revenue has the luxury of having the upper hand here where the age of the debt means debtors may not be able to provide any contradictory evidence about lost payments or incorrect adjustments. Although it’s good to see Inland Revenue is making progress on the overall collection, I don’t think that means that it should avoid scrutiny for how the debt book has been handled in the past.

Pre-Budget teasers

The Budget is next Thursday and ahead of it, there’s always plenty of speculation as to its contents. Things have got spicier because of the pay equity issue: depending on who you want to believe this has either “saved the Budget” or just happens to be a coincidence.

As usual there’s been a steady stream of announcements from the Government about particular items which will be in the Budget. A very interesting and quite significant one relates to future drawdowns from the New Zealand Superannuation Fund (“the NZSF”), established by the late Sir Michael Cullen in 2002.

The country’s biggest taxpayer

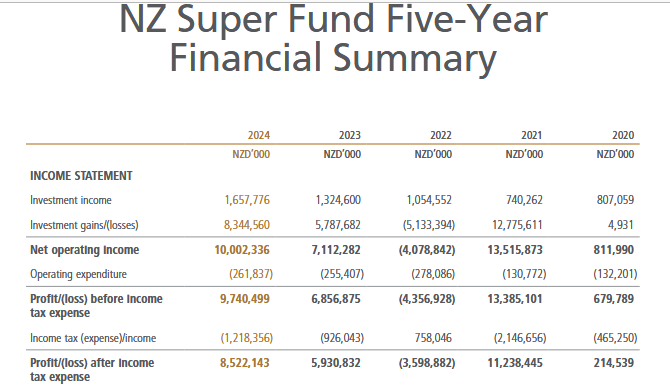

Ahead of the Budget the Finance Minister announced that the Government will start drawing down on the NZSF with effect from 2028, five years ahead of first forecast. It is just worth keeping in mind that since inception the NZSF has been paying tax. In fact, it is the only sovereign wealth fund in the world which is taxed. For the year ended 30th June 2024, its tax bill was $1.2 billion. It’s usually the largest single taxpayer in the country, meaning it’s already contributing to the funding of New Zealand Superannuation.

Changes ahead for KiwiSaver? National’s record would indicate so

Elsewhere there’s been speculation about what’s going to happen with KiwiSaver. The Finance Minister has alluded to some changes leading to speculation that the Government’s contribution could be increased for lower income earners or might be means tested for higher income earners.

It’s worth noting that previous National-led governments have a pattern of playing around with KiwiSaver. The maximum Government contribution each year used to be $1,043 a year until that was halved by Sir Bill English with effect from 1 July 2012. He also scrapped in 2009 a $40 annual fee subsidy. English also removed the $1,000 kick start payment from 21st May 2015.

The biggest KiwiSaver change English made was introducing employer superannuation contribution tax (“ESCT”) on employer contributions to KiwiSaver funds from 1 April 2012. To illustrate how important that change was, the amount of ESCT collected annually was $1.982 billion for the year to 30th June 2024 or about 1.7% of the Government’s total tax take for the year. Consequently, ESCT is too big for it to be changed in any way. But I do think we might see some tweaking of the Government’s KiwiSaver contribution settings.

A potential corporate tax cut or accelerated depreciation?

There’s also been talk about a potential corporate income tax cut, but I’m with Robin Oliver who said that if they’re going to do it, they’d have to go big. In other words, from probably 28% down to 18%, and that’s simply not going to happen because it would be unaffordable. On the other hand I do think we might see some more targeted investments around increased or accelerated depreciation allowances, which I, and the business sector, would certainly welcome.

The Green alternative

The Greens took the opportunity also to publish their alternative budget on Wednesday. Looking past the predictable scoffing from opponents a few initiatives stand out. They’re proposing a higher top rate of 45%, which is the same top rate as Australia and the UK just for reference, it should kick in at income over $180,000 with the 39% rate starting at $120,000. The trade-off is that every person will get $10,000 a year tax free exemption. The 45% top rate is comparable to other jurisdictions, notably Australia and the UK. I’m not so sure about the thresholds though as the level they kick in seem on the low side.

Think 45% is high? Try Austria

As an aside and about high tax rates I was very surprised to find out this week that Austrian Government, which is a centre right coalition, has kept in place for the next four years a top income tax rate of 55% applicable to income above €1,000,000. Food for thought therefore claiming the Greens’ suggestions are excessive. (As a sidebar and follow on from my comments last week about mandatory indexation of thresholds, Austria is actually reducing part of the inflation adjustment for the tax rate thresholds. In Austria income tax thresholds are automatically adjusted annually by 2/3 of the inflation rate unless the government legislates otherwise).

A Capital Acquisitions Tax?

The Greens are also proposing a 2.5% wealth tax on net assets over an individual’s threshold of $2,000,000 with a 1.5% tax applying to net assets held in “private trusts,” The press has talked about the Greens introducing an inheritance tax, but that’s not actually correct. In fact, and I think this is probably the most interesting revenue raising idea from the Greens, what they are actually proposing is a variation of the Irish Capital Acquisitions Tax. Why this is interesting is Capital Acquisitions Tax is a donee based tax. In other words, it is the person who receives the gift who is taxed. By contrast a typical inheritance tax or estate duty work on the principle of any taxes being paid by the donor (the person, or their estate making the gift.

Under the Greens proposal a 33% wealth transfer tax will apply to significant gifts and inheritances received, over an accumulated lifetime threshold of $1,000,000. The 33% rate is the same as the Irish Capital Acquisitions Tax. This is an interesting proposal and it’s the first time I’ve seen a New Zealand party raise it as an option.

Elsewhere the Greens want to increase the corporate tax rate to 33% and also restore a 10-year bright-line test, as well as reintroducing interest deductibility restrictions. All of the tax increases are to pay for a huge social. Investment programme, including free dental care. It would also include a major increase in the threshold for Working for Families from the current $42,700, which has not changed since June 2018, to $61,000. The current 27% abatement rate would also be reduced.

Wealth taxes and capital flight

On wealth taxes, a reason why tax practitioners including myself are sceptical about the revenue projections for a wealth tax are the issues of valuation and capital flight. Valuation issues are always a key objection to wealth taxes, but I think the question of capital flight is one that we perhaps have to think hard about when considering the impact of a wealth tax. That’s because I think we are very vulnerable to capital flight to Australia.

Australia has always been a huge land of opportunity for many Kiwis but it’s also very attractive for those Kiwis moving there who qualify for the Australian Temporary Resident exemption. This exempts non Australian sourced income and capital gains from Australian tax. It’s similar to our Transitional Resident exemption, but unlike that which is generally only available for 48 months, the Australian Temporary Resident exemption, is more or less indefinite or until the point you either become an Australian citizen or marry or cohabit with an Australian citizen.

A bewildering brouhaha

In the run up to the Budget, there’s been a quite bewildering to me brouhaha over who can or cannot attend the Budget Lockup. It’s really surprising that Treasury would get itself dragged into such a controversy with its unpleasant tones of attempting to silence critics. I do think as a result of that, together with the pay equity issue, Thursday’s Budget Lockup could get a little fractious. I certainly think the Parliamentary ‘debate’ will be particularly rowdy.

What does happen in the Budget Lockup?

Thursday should be my 15th Budget Lockiup. I’ve attended every single one since 2010 other than the COVID affected 2020 Budget. The routine is that we get access to the Budget documents at 10:30 and then we have about 90 minutes to analyse them before the Minister of Finance (and several colleagues) comes in to give a speech and answer questions. After that Q&A session Treasury provides lunch, and everyone finalises their analysis for release at 2 o’clock when the Finance Minister starts delivering the Budget to Parliament.

To be honest, I don’t know why the Finance Minister bothers with a speech to analysts. We’ve all read the material and frankly it’s much more interesting to ask questions about particular details. Obviously, finance ministers all want to sell the big picture, but for most in the Lockup, including myself, we’re very much more interested in the detail.

This is why the Lockup matters; it’s one of those few opportunities where experts can directly ask questions of the Minister of Finance and other attending ministers. The first few questions will go to the Press Gallery after which economists and other experts chime in.

It’s quite interesting to see who attends the Lockup. I’ve sat next to next to overseas economists, analysts from the British Embassy as well as plenty of other colleagues from the Big Four and other various accounting and advisory firms. But the best part of the Lockup is the question and answer with the Finance Minister which I’m looking forward to as I think it could be a bit spicy this year.

Budget predictions?

I don’t actually think that we’ll see a lot of tax measures in the Budget other than possible accelerated depreciation changes. We might get more details about those changes previously announced in relation to the Foreign Investment Fund regime. As I said, I think the Lockup could be a little bit more entertaining this year and I do expect the Parliamentary debate to be more raucous than usual.

Tax Freedom Day

16th May was Tax Freedom Day according to business accounting firm Baker Tilly Staples Rodway. From this day onwards, workers will have paid their tax bill for the year and are now working for themselves for the rest of the year. Interestingly, according to Bake Tilly Staples Rodway the overall tax paid has increased by 4.66% on last year. That’s despite the tax cuts announced in last year’s budget.

Happy Anniversary…to me 😊

May 16th was also the 32nd anniversary of my arrival in New Zealand, and for those who don’t know my back story, I arrived on this day in 1993 as a backpacker, to follow that year’s Lions tour. The All Blacks finished up winning that series 2-1. Despite that result, I had a great time, and I decided I rather liked New Zealand so I explored opportunities about how I could stay. The rest, as they say, is history. One of the key changes is these days I’m very much an All Blacks fan. Anyway, happy anniversary to me and many thanks to many, many people not least of all my wife Tina for what’s been a fantastic 32 years.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

The debate over international taxation and the so-called Two Pillar proposals has been driven largely by the G20 and the Organisation for Economic Cooperation and Development, (the OECD). But in recent years the United Nations has started to flex its muscles in this space. This is unsurprising, because the UN represents the wider world view outside the 40-odd countries which make up the G20/OECD.

All of this is behind the story that RNZ ran at the start of the week about the United Nations Committee on Economic, Social and Cultural Rights statement on tax policy. The RNZ ran this statement under the banner headline “UN Report questions fairness of GST”, in which it pointed out that GST can be regressive for low-income earners.

In fact, the UN Committee statement went much further than GST. It noted the terms of reference to the United Nations Framework Convention on International Tax Cooperation, which had been adopted by the General Assembly,

“This development represents an important opportunity to create global tax governance that enables state parties to adopt fair, inclusive and effective tax systems and combat related illicit financial flows.”

“regressive and ineffective tax policies”

The key paragraph to the UN Committee statement is paragraph 4, which refers to “regressive and ineffective tax policies”, having

“…a disproportionate impact on low-income households, women, and disadvantaged groups. One such example is a tax policy that maintains low personal and corporate income taxes without adequately addressing high income inequalities. In addition, consumption taxes such as value added tax can have adverse effects on disadvantaged groups such as low-income families and single parent households, which typically spend a higher percentage of their income on everyday goods and services. In this context, the Committee has called upon States Parties to design and implement tax policies that are effective, adequate, progressive and socially just.”

It’s the reference to consumption taxes that was picked up by RNZ. The regressivity of GST is well known and was noted by the last Tax Working Group. The general approach we’ve taken here to that issue is to try and ameliorate the impact by benefits or transfer payments such as Working for Families and Accommodation Supplement to lower income families.

The thing is though, as Alan Bullôt, of Deloitte noted in the RNZ story, GST is a very effective tool for the government to raise a large amount of money relatively easy. In fact, GST represents about 25% of all tax revenue a point I repeated when I discussed the whole story on RNZ’s The Panel last Monday.

Principles of a well-designed tax system

But the Committee statement is interesting beyond the GST issue because it goes on in paragraph 6 to set out what it regards as the principles of a well-designed tax system. It suggests, for example,

“…ensuring that those with higher income and wealth, in particular those at the top of the income and wealth spectrums, are subject to a proportionate and appropriate tax burden.”

That can be clearly interpreted as a call for a capital gains tax or some form of capital taxation, a point I made to The Panel.

The Committee also fires a few shots over international tax, stating

“The Committee has observed situations in some States where low effective corporate tax rates, wasteful tax incentives, weak oversight and enforcement against illicit financial flows, tax evasion and tax avoidance, and the permitting of tax havens and financial secrecy drive a race to the bottom, depriving other States of significant resources for public services such as health, education and housing and for social security and environmental policies.”

That clearly targets tax havens, but it’s also a shot across the likes of Ireland, for example, with its low corporate tax rate.

A global minimum tax

The Committee also calls for a “global minimum tax on the profits of large multinational enterprises across all jurisdictions where they operate and to explore the possibility of taxing those enterprises as single firms based on the total global profits, with the tax then apportioned fairly among all the countries in which they undertake their activities.”

That’s quite the statement even if probably forlorn given the Trump administration’s recent declarations. It’s probably what the less developed world is after, because they’re quite concerned they’re losers under the current system. This is going to lead to wider clashes over the G20/ OECD proposal, which I think to be frank, is probably dead. In any case, I thought it was always noteworthy that Pakistan, the World’s fifth most populous country and Nigeria, the sixth most populus country and also Africa’s largest economy, both refused to sign up for Two Pillars.

Now economically, that was not highly significant because the economies are small relative to the giant economies of the developed world. However, I think this refusal points to existing issues and this statement underlines there’s global tensions ahead on this question of international tax.

As I said, the Trump administration basically is saying no go. But I think you will see countries attempting to find ways of taxing what they regard as their part of the international multinationals’ income. So, plenty ahead in this space.

Rising GST debt

Now moving on, another RNZ report picked up that there had been a substantial growth in GST debt. Allan Bullôt, of Deloitte raised a concern this could be creating zombie companies. In particular he noted the amount of GST collected but not paid to the Government, has risen from $1.9 billion in March 2023 to $2.6 billion by March 2024.

As mentioned earlier, GST represents 25% of tax revenue. It also represents just under 40% of all tax debt and has been rising sharply. That’s a reflection of the economic slowdown and the cash flow crunch that’s happening to a lot of businesses.

Even so, this is a matter where Inland Revenue has a number of resources it can deploy, and one Alan mentioned is the power to notify credit reporting agencies about tax debt. According to the Inland Revenue, it only did that three times in the year ended 20 June 2024 and not at all during the June 2023 year.

This means that people were trading and doing business with companies without realising the potential risk. What that might mean is that you provide services to a company which is struggling with GST debt, and lo and behold, you suddenly find you’ve got a bad debt on your hand.

Creating zombie companies?

This is a major issue and as Allan put it,

“That’s grown and grown. I get very nervous we’re creating zombie companies … if you’re three or four GST returns behind, it’s incredibly unlikely if you’re a retail or service business that you’ll ever come back. If you’re three of four GST payments behind, it’s incredibly unlikely that your retail or service business will ever come back.

Maybe if you’re a property developer who’s got big assets that you sell and settle your debt. But if you’re a normal business, a restaurant or something like that, you go belly up.”

This is an area where Inland Revenue has information which is not available to the general public and maybe it should be making that more widely available. There’s a question here to my mind, of what proportion of debt you would report. The Inland Revenue I think has every right to say this person owes X amount of GST, or is behind on GST, but bear in mind in some cases the debt is inflated by interest and penalties. Or in some cases there may have been estimated assessments.

Notwithstanding this Allan is right to raise concerns and I expect we will see more money being granted to Inland Revenue in this year’s Budget to chase this debt.

Meanwhile, jam tomorrow in the Australian Budget

It was the Australian budget on Tuesday night our time in which the ruling Australian Labor Party promised modest tax cuts starting in July 2026, with a further round in July 2027. Under the proposed cuts, a worker on average earnings of A$79,000 per year (about NZ$86,800) will receive A$268 in the first year and that will rise to A$536 in the second year. In addition, there will be a A$150 energy rebate payable in A$75 instalments.

Otherwise, there weren’t many other tax measures to report. That was hardly surprising because two days later, Prime Minister Anthony Albanese announced that the Federal Election would be held on 3rd May. The Budget was therefore what you might call a typical pre-election budget, promising jam tomorrow if you vote for the ALP.

One tax measure of note was that the Australian Tax Office is getting further funding for dealing with tax avoidance and tax evasion. I think that’s a pretty standard pattern we’re seeing around the world. The British had what they call their Spring Statement this week, the half yearly report by the Chancellor of the Exchequer or Finance Minister.

No new tax measures were announced. But like the ATO, HM Revenue and Customs was allocated more money to target tax evasion, with the expectation that it would achieve about a billion pounds a year in additional revenue, which seems very light given the scale of the UK economy.

Mega Marshmallows food or confectionery?

Finally, this week, a couple of years back, we discussed the Mega Marshmallows Value Added Tax (VAT) case from the United Kingdom. Basically, it involved the VAT treatment of large marshmallows. If deemed to be food they would be zero-rated for VAT purposes, but if they were confectionery, they would be standard rated which at 20% means quite a significant sum is at stake.

I will cite this and its very well-known predecessor the ‘Max Jaffa’ case involving Jaffa Cakes from the 1990s, when people make suggestions about maybe reducing the GST on food to help with the cost of living, particularly for lower-income families. It’s a well-meant policy except the practical issues you run across lead to absurdities at the margins. My view on this topic is if you want to assist people at the lower end of the income scale, it’s better give them income rather than try and fiddle with the GST system because there are unintended consequences, and this mega marshmallow case is a classic example.

The case involves unusually large marshmallows. The recommendation by the manufacturer is that they should be roasted as they’re marketed as part of the North American tradition of roasting marshmallows over an open fire. Except it’s not clear in fact, if that actually happens.

The story so far is that after HM Revenue and Customs lost in the First-Tier Tribunal, it appealed to the Upper-Tier Tribunal which basically said, “Nope, we’re not hearing it.” So HMRC appealed again to the Court of Appeal which has now issued its ruling. The Court of Appeals determined it was not absolutely clear whether in fact these marshmallows can only be eaten if they are cooked, in which case they must be food, or they can be eaten with the fingers, in which case they are confectionery.

Accordingly, the key issue is whether they are normally eaten with the fingers. This is a question of fact about which the first-tier tribunal has not made a finding. In some cases, it will be obvious from the nature of the product whether it is normally eaten with the fingers or in some other way. But that is not clear with this particular product.

The Court of Appeals therefore sent the case back to the First-Tier Tribunal to decide on this question of fact. Are these mega marshmallows mostly eaten with the fingers? If so they’re confectionery and subject to VAT at 20%. Alternatively, are they mostly cooked as supposedly intended, and therefore zero-rated food.

Time for the UK to apply VAT to food?

This case came to my attention through the UK tax thinktank Tax Policy Associates which is run by the estimable Dan Neidle, a former tax partner at the mega law firm Clifford Chance. Commenting on the Court of Appeal’s decision, he pointed out the sheer absurdity and costs involved and questioned why this was so. “Why do we have a horribly complicated set of rules that mostly benefit people on high incomes (because they spend more on food)? “

His solution – scrap zero-rating on food, in other words, adopt the approach we have here in New Zealand and tax everything. He estimates that would raise about £25 billion which could be used to reduce the standard rate of VAT from 20% to 17%.

Warming to his theme Dan thinks a better idea would be “Cut the rate to 18% and use the remaining [money] in benefit increases and tax cuts targeting those on low incomes, so they’re not out of pocket from the loss of the 0% rate.”

It’s the first time I can recall a British commentator suggest this. I doubt it will happen, but it’s just a reminder that although our GST is highly comprehensive, we don’t have these absurd but entertaining cases involving marshmallows of unusual size.

But a comprehensive GST is regressive, and I think a better approach is to address that by means of transfers to lower incomes rather than tinkering with exemptions. You never know, there may be something in this space in the Budget, we’ll find out next month.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Lessons from the largest known GST fraudster – could it happen again?

Corporate tax cuts – who benefits and what does the public think?

The tax year-end of 31st of March is fast approaching and at this time of year tax agents are busy with the last year’s tax returns and also giving a heads up to clients about what actions they need to take ahead of 31st March. It’s always an incredibly busy period and it’s often easy to overlook some important matters amidst the rush and the mayhem. So, here’s a quick reminder of key issues that that you should be considering as the tax year ends.

GST and Airbnb

First up, a GST election is running out in respect of being able to take assets out of the GST net. We discussed this a few weeks back. To quickly recap, this could particularly affect Airbnb operators that may have bought a residential property, rented it out and then realised that Airbnb produces a better return. They’ve therefore signed up to Airbnb or other apps and then registered for GST either voluntarily or because they’ve exceeded the $60,000 registration threshold.

Subsequently, the taxpayer may have claimed an input tax credit on the property but now realise that they could be liable for a substantial GST bill on any subsequent sale of the property. That obviously is a big shock.

To address this issue, a transitional rule was introduced under section 91 of the Goods and Services Tax Act with effect from 1st April 2023. The rule enables a person to elect to take an asset out of the GST if the following four criteria are met:

the asset was acquired before 1st of April 2023; and

it was not acquired for the principal purpose of making taxable supplies; and

it was not used for the principal purpose of making taxable supplies; and

a GST input tax credit was previously claimed, or the asset was acquired as part of a zero-rated supply.

If all those criteria apply, then the person can elect to take the asset out of the GST net and pay back the GST that was claimed on the original input tax. In other words, they don’t pay GST on the increase in value. A good example here would be a bach or family holiday home which was subsequently rented out for short stay accommodation.

The key thing is this election expires as of 1st April 2025, by which time you must have notified Inland Revenue of your election. You don’t necessarily have to pay the GST; you can do so as part of your GST return to 31st March, but you must have notified Inland Revenue in a satisfactory manner. I would recommend using the MyIR message service to do so.

Other year-end matters

There are a number of elections relating to whether or not a taxpayer wants to adopt or leave a tax regime. A classic example would be companies entering or leaving the look-through company regime. Another, lesser known one would be entry or exit into the little known, and apparently little used, Consolidation regime.

Another matter that pops up regularly around year-end is checking your bad debts ledger. Bad debts are only deductible for income tax purposes if they are fully written off by 31st March so make sure this happens. Then there is the year-end fringe benefit tax returns where taxpayers should check to see whether they are making full use of any available exemptions.

A very important one for companies is to ensure their imputation credit account, either is in credit or has a nil balance. If there’s a debit (negative) balance on 31st March, that will result in a 10% penalty. It may be possible in some cases to make use of tax pooling to rectify some of these issues.

Finally, if you’re registered with a tax agent, your tax return for the 2024 income year must be filed by 31st March otherwise late filing penalties may apply. Possibly more critically, the so-called “time-bar” period during which Inland Revenue may review and amend already filed tax returns is extended by another year.

Lessons from the country’s biggest known GST fraud

Moving on, an interesting story has popped up in relation to what was then the largest known GST fraud. Gisborne farmer John Bracken was jailed in May 2021 after he was found guilty of 39 charges of GST fraud. He had run a scam through his company, creating false invoices totalling more than $133 million between August 2014 and July 2018 which resulted in receiving GST refunds totalling $17.4 million to which he wasn’t entitled. He was jailed and is currently out on parole.

At the time he was sentenced Inland Revenue and the police issued restraining orders and are trying to make an application for an asset forfeiture. In other words, assets subject to the forfeiture order were acquired through fraud and should be forfeited and handed to the Crown.

Now naturally Mr. Bracken and his family, including his wife and his parents and his son, are all fighting back on this because they stand potentially to lose assets that may be subject to the restraining order and subsequent forfeiture. The interesting part of this is the sheer scale of what went on and how it went undetected for four years before an employee got suspicious, notified the Serious Fraud Office, who then tipped off Inland Revenue.

At the time the frauds were committed, Inland Revenue was at the start of its Business Transformation project, upgrading all its systems. Until it got tipped off It had no idea of the extent of the fraud. Mr. Bracken appeared to have covered his tracks reasonably well, although once uncovered it was a fairly simple GST fraud. He just submitted fraudulent GST invoices, but he was careful to get them from actual companies with whom he had established some form of trading relationship.

Obviously the concern is now twofold. The Crown will be wanting to recover as many assets as possible to the value of the $17 million that it was defrauded, but also, can this happen again?

I’d like to think “No”. Certainly, Inland Revenue feels that its new systems have enhanced its capabilities greatly and that would appear anecdotally to be the case. There was a GST fraud scheme spread by TikTok influencers which caught the Australian Tax Office completely off guard and was worth tens of millions of dollars. Inland Revenue feels that that sort of fraud could not happen here. Mr Bracken’s release on parole and the ongoing forfeiture case is a reminder that Inland Revenue has to be vigilant all the time.

But sometimes it comes down to a conscientious person, an employee usually, tipping off the authorities. But it shouldn’t always come down to that. Inland Revenue and other authorities should be able to pick up signs of these frauds. As I said, I have confidence they do, but I would also hope that confidence is not tested too much.

Corporate tax cuts – a possibility or just flying a kite?

In recent weeks there’s been some chatter or hints from the Government and Finance Minister Nicola Willis about a potential corporate tax cut. She made the not unreasonable point that our corporate tax rate is high by world standards. This prompted comments from the former Deputy Commissioner of Inland Revenue Robin Oliver that tinkering around the edges by reducing it from 28% to 25% might not achieve much. If the Government wanted to attract investment, they’d have to go big, maybe nine or ten percentage points cut. Robin was sceptical the Government could afford to do so because of the loss of revenue. And I agreed with that assessment.

I do wonder whether this idea might be something of a bit of a red herring. Some comments I’ve heard seemed to suggest that maybe the Government was just flying a kite to see the reaction.

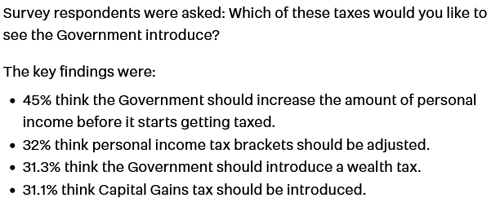

Anyway, this week a poll run by Stuff which suggested that very few would support a corporate tax cut, or rather that the population was pretty lukewarm about the idea. The poll carried out by Horizon Research, found only 9% of adults supported lowering the corporate tax rate, while 25% actually wanted it increased. There were a few other interesting results:

Who would benefit from a corporate tax cut?

Craig Renney (the chief economist for the Council of Trade Unions) and researcher Edward Miller also looked at who would benefit from a drop in the New Zealand company tax rate. They concluded the main beneficiaries of a corporate tax cut would probably be overseas shareholders. In terms of attracting greater foreign direct investment, they saw little evidence that corporate tax cuts would be likely to achieve that.

As they noted,

“…company taxation is only one aspect of a decision by a company or fund to invest in New Zealand. In addition to the company tax rate, there is the R&D tax incentive, the lack of a capital gains tax, and the lack of substantial payroll taxes. These taxes affect the actual tax paid by corporates in comparison with other countries when considering investing in New Zealand.”

Renney and Miller’s modelling suggested that a tax cut would not result in further investment but would just simply increase the funds flowing offshore. In particular they saw the Big Four Australian banks as being prime beneficiaries. The pair estimated that a cut from 28% to 20% would have increased the annual income to offshore shore shareholders by up to $1.3 billion.

There’s always a lot of debate around the benefit of corporate tax cuts, whether they do drive investment, or they simply put money into the back pockets of the shareholders. That debate has gone on for a long time and continues again. But it’s interesting to marry that along with the public’s general lack of enthusiasm for such a cut.

Yeah, but what about the IMF?

I think it was also noticeable that the International Monetary Fund in its recent Concluding Statement for its 2025 Article IV Mission suggested “judicious adjustments to the corporate income tax regime.” So maybe it too isn’t entirely sold on corporate tax cuts as a key driver for investment.

No doubt more will be revealed in May’s Budget. And until that time speculation will mount, but we will find out on the day and as always, we will bring you the news when it emerges.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Every year, the International Monetary Fund (IMF) undertake an official staff visit or mission to New Zealand as part of regular consultations under Article IV of the IMF Articles of Association. Each IMF mission speak with the Minister of Finance, Treasury officials and other persons – economists, academics and the like about the state of New Zealand’s economy and related issues. At the end of the visit the Mission then issues a short concluding statement of its preliminary findings.

The IMF will then prepare a lengthier report setting out its findings in more detail which we can expect to see in a couple of months time.

“A window of opportunity”

After noting it expects real GDP growth to rise to 1.4% for this year and then to 2.7% in 2026 the Mission noted:

“The macroeconomic environment provides a window of opportunity for New Zealand to consider broad based reforms needed to address medium- and long-term challenges, including to secure fiscal sustainability, boost productivity, address persistent infrastructure and housing supply gaps, and initiate early dialogue on population aging.”

“A comprehensive capital gains tax”

My understanding of the IMF submission is that each Mission has a different focus. This year, I understand the Mission was looking at the question of funding the future cost of New Zealand Superannuation and therefore the tax policies required. This led the Mission to call for some tax policy reforms

“Tax policy can support a more growth-friendly fiscal consolidation, and reforms aimed at improving the tax mix can help increase the efficiency of the income tax system while reducing the cost of capital to incentivize investment and foster productivity growth. Options include a comprehensive capital gains tax, a land value tax, and judicious adjustments to the corporate income tax regime.”

I expect we’ll hear a lot more about this when we see the final report.

“Initiate early dialogue”

It’s not the first time the IMF have suggested a comprehensive capital gains tax, and the Organisation for Economic Cooperation and Development has also frequently made a similar suggestion. Generally speaking, the government of the day just responds, “Yeah, but, nah”. However, the issues prompting the suggestion still don’t go away. In this particular case, the IMF suggests we need to start transitioning into a new system to cope with the rising cost of New Zealand superannuation.

“It is essential to initiate early dialogue among all stakeholders regarding comprehensive reform options that can help mitigate these challenges and other long term spending pressures from healthcare and aged care care needs with a fair burden sharing across generations. This can be further supported by KiwiSaver reforms aimed at achieving greater private savings retirement savings.”

The IMF is echoing comments myself and others have repeatedly made. We have rising costs in relation to aged healthcare and superannuation and we need to start thinking seriously about how we’re going to address those. This is a multi-generational impact. One of the unusual points about New Zealand Superannuation is it is a fully funded universal pay as you go system.

An intergenerational issue

In other words, it’s available to everyone, but it’s funded out of current taxation. I think there’s a widespread perception that some part of your tax pays for your future superannuation. It doesn’t. Tax paid by working people below the age of retirement is used to fund the current superannuation of those who have retired. The funding of superannuation is therefore a major intergenerational issue but one rarely discussed. Hence the IMF’s call to initiate early dialogue. I’ll have more on this when the IMF releases its final report.

In the meantime, whenever the IMF or OECD calls for tax reforms, the Minister of Finance of the day usually responds, sometimes in quite snippy terms. Sir Michael Cullen was wont to do so as did Nicola Willis last year. This year the Finance Minister hasn’t publicly responded to the IMF concluding statement, possibly because her attention was on this week’s Infrastructure Investment Summit in Auckland.

Foreign Investment Fund changes announced

As part of the summit, the Minister of Revenue Simon Watts has announced that there will be changes to the current Foreign Investment Fund, or FIF regime. The Government has very heavily signalled that it would do something in this space, so this is no surprise.

The proposed changes to the FIF rules include the addition of a new method to calculate a person’s taxable FIF income, the revenue account method, in other words taxing capital gains. According to the Minister;

“This will allow new migrants to be taxed on the realisation basis for their FIF interests that are not easily disposable and acquired before they came to New Zealand. For migrants who risk being double taxed due to their continuing citizenship tax obligations, this method can apply to all their FIF interests.”

This last point is of particular interest to United States citizens who face this double taxation issue, and which is turning people away. Furthermore, these changes will apply to migrants who became New Zealand tax residents on or after 1st April 2024.

More detail needed and further changes ahead?

This is a very good move but there’s a bit more detail still required. Does the reference to new residents arriving on or after 1st April 2024 mean those new residents are able to make use of this provision in the current tax year? One of the other key issues is if you do opt to be taxed on the revenue account method, what tax rate would apply? From discussions with Inland Revenue policy officials, they seem to be intending that it should be at the person’s marginal rate. Which for those on the 39% bracket would not be terribly welcome. So that’s a key design point.

The other thing of note is that Mr Watts added the Government will also be looking at how the rules impact New Zealand residents and will have more to say later in 2025. That’s interesting, because for me, the rules are quite a compliance burden in terms of calculations and have huge impact for everyone who has a KiwiSaver with overseas investments.

How to pay for New Zealand Superannuation

As noted above the IMF are looking very closely at the question of the fiscal cost of superannuation and aged healthcare which they suggest mean reforms to the tax system are needed to address those growing costs.

Coincidentally, Assistant Professor Susan St John of Auckland Business School’s Economic Policy Centre Pensions and Intergenerational Equity Hub released a working paper on New Zealand Superannuation as a basic income. This is an interesting proposal, which I know Susan has been working on for some time with the assistance of Treasury modelling.

The idea is that New Zealand Superannuation is changed into a universal basic income and treated as a grant. This allows an effective claw back mechanism to operate through the tax system. The proposal is that this claw back would generate additional revenue to help meet the cost of pensions and aged care.

The paper begins by setting out the background to the issue, the increasing demographic strains that we’re seeing. It notes that Treasury has been raising this issue for some time now, such as in its 2021 Long Term Fiscal Statement, He Tirohanga Mokopuna and speeches last year by Dominic Stephens of Treasury on the fiscal projections and costs.

Demography and migration

One of the interesting points the paper makes is although we face some financial strains ahead, because of our demographics the cost of New Zealand Superannuation will not be as high as what some nations are currently dealing with.

Incidentally, as part of their concluding statement, the IMF made a number of presentations illustrating certain areas they’re examining in more depth. One was the question of demographic pressures of superannuation, and it made the point that migration is not going to be the magic bullet some policymakers seem to think.

What about means testing?

After setting out the background Susan St John discusses the option of using means testing as a means of addressing costs. The paper looks at what happens in Australia and our own experience when New Zealand Superannuation was means tested for a while – right up until Winston Peters and New Zealand First became part of the first MMP Parliament in 1996. One of the conditions of that coalition agreement was the abolition of the New Zealand Superannuation Surcharge.

Australia tests income and assets but it’s highly complex and achieves a fiscal objective of managing the cost. On the other hand, Australia has a much more well developed long running compulsory private saving scheme, which makes what they call the Age Pension (the equivalent of New Zealand Superannuation) more of a backstop. The paper also notes that the private pension savings in Australia are more generously state subsidised than KiwiSaver.

The Australian means testing approach is very comprehensive and frankly a nightmare. The paper notes our surcharge which operated between 1985 and 1998 was highly unpopular, but it did deliver useful savings. In short, surcharges or means testing helps mitigate superannuation costs. But they are unpopular and like the Australian approach complicated to run. Furthermore, they encourage attempts to mitigate their effect.

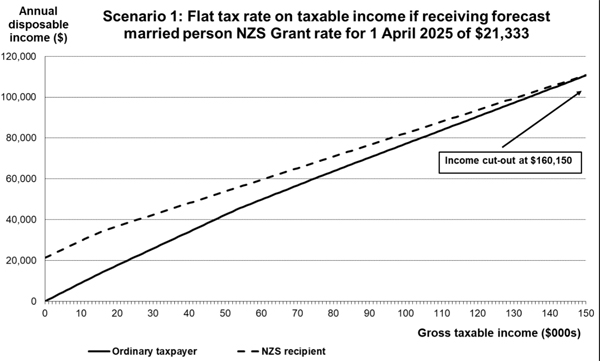

Making New Zealand Superannuation a universal basic income

Instead, Susan proposes turning New Zealand Superannuation into a basic income, the New Zealand Superannuation Grant (the NZSG). She also suggests equalising the current different rates which currently apply depending on whether a person is in a relationship or living together, so it becomes a universal basic income for those who’ve reached the superannuation age.

As a basic income the NZSG would no longer be taxable. Instead, when a recipient earns additional income, it’s taxed under a progressive tax regime, so the tax system does the work of providing a claw back of the universal grant for high income people. The effect would be that above a certain point a person decides it’s simply not worth their while taking the NZSG.

For example with a flat tax of 40% on all other income, above $160,150 it would not be worthwhile taking the NZSG.

Another alternative would be a two-tiered rate of 17.5% for the first $15,000 of other income, and 43% on each dollar above. In this case the breakeven point becomes $151,885. A third scenario has a two-tiered rate, 20% for the first $20,000 earned and then 45% above that level. Under this scenario, the income cut out point drops to $135,000. Treasury has helped Susan with the modelling for this paper and its methodology is explained in the appendices to the paper.

15-20% savings possible?

Under Susan’s approach up to 5% of all eligible super annuitants will not apply for the NZSG because there’s no gain in it. She estimates savings could be between $2.8 billion and $3.8 billion or between 15% and 20%.

This is an interesting proposal which seems preferable to reintroducing the New Zealand Superannuation Surcharge or adopting the Australian means testing approach. I think it’s worth considering but the key thing is, as the IMF said, this is an issue we really need to start discussing now because these costs are starting to accelerate as baby boomers age.

It also seems fairer than raising the age of eligibility, which is unfair on Māori and Pasifika. There’s already a seven-year life expectancy gap between Māori and non-Māori so raising the age of eligibility for superannuation is politically difficult particularly as the proportion of the Māori population grows because of those changing demographics.

This is a worthwhile proposal which merits serious consideration as part of the ongoing debate.

This is an edited transcript of the podcast episode recorded on 14th March – it has been edited for clarity and length.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Inland Revenue consults on not-for-profit sector and more.

It’s been an extremely busy week in tax – just as we were planning to go to air, Parliament’s Finance and Expenditure Select Committee (“the FEC”) released its report on the Taxation, Annual Rates for 2024-25 Emergency Response and Remedial Measures Bill initially introduced last August.

We covered the bill’s main initiatives when it was initially released, and now the FEC is reporting back on submissions it received, what’s been amended and why, together with Inland Revenue’s accompanying report on submissions. There’s also a supporting report from the independent adviser to the Select Committee, John Cantin, a former guest of this podcast. Overall, there are no major real changes to the legislation. There are minor amendments resulting from issues brought to the attention of the FEC which is how the submission and Select Committee process is meant to operate.

Tax relief for future emergency events

The Officials’ Report on submissions had some interesting submissions on the issue of procedures to manage tax relief for any future emergency events.

The measure was uniformly supported but several submissions proposed making ready to go after a trigger event some of the measures that were brought in and employed relatively successfully during the initial COVID response in 2020, such as carry back of losses, accelerated depreciation, or cashing out of losses. In most cases the submissions were noted or declined.

I thought it was interesting to see that the main submitters involved the Big Four accounting firms, Chartered Accountants of Australia and New Zealand, and the Corporate Taxpayers’ Group. I think these submissions were prompted by our experience during COVID in 2020, where a lot of policy had to be devised and implemented on the hoof, with frantic consultation going on between Inland Revenue and various parties.

I was involved in some of those consultations, and I think it’s not unreasonable to have these measures ready to go if needed. On the other hand, I can see why Inland Revenue and the Government might be a little reluctant to have the ambit of the bill expanded.

Transferring UK pensions to New Zealand

Moving on, one of the measures I was interested in was the proposal for what they call a scheme pays measure in relation to Qualifying Recognised Overseas Pension Schemes or QROPS. These are schemes that are able to receive transfers of pensions from the United Kingdom.

There’s been some debate around this, as under our rules those transfers are taxable, and it has been a long-standing issue that in many cases this triggered a tax bill which taxpayers could not pay as the funds were locked up in the transferred funds.

One suggestion that had been made was this scheme pays proposal, where transfers are made into a scheme. The scheme may make a payment on behalf of the transferring taxpayer and that will be done at a flat rate of 28%, a “transfer scheme withholding tax”. There’s been a bit of tinkering with the proposal mainly about reporting requirements. Otherwise, the regime looks all set to go ahead with effect from 1st April 2026.

It’s a measure I feel ambivalent about. I was part of a group which lobbied for this change so it’s good to see it finally in place. On the other hand, as I’ve said previously, I do think that we ought to be thinking harder about why we’re taxed. (I also think taxing people years ahead of when they could access the funds is technically questionable – what if they died before reaching the required age?)

Crypto-Asset Reporting Framework

The other thing of note is that this Bill also introduced the legislation for the Crypto-Asset Reporting Framework. No amendments have been made to that regime. So that will be coming into force with effect from 1st April 2026. From that date New Zealand-based reporting crypto-asset service providers would be required to collect information on the transactions of reportable users that operate through them and report it to Inland Revenue by 30 June 2027. Inland Revenue would exchange this information with other tax authorities (to the extent it related to reportable persons resident in that other jurisdiction) by 30 September 2027.

Taxation and the not-for-profit sector

Moving on Inland Revenue has now released for consultation an Officials Issues Paper Taxation and the not-for-profit sector. This consultation is something that has been telegraphed for some time, there’s what might be termed unease around the exemption for the charitable sector and the merits of some entities apparently making use of the exemption. For example, the involvement of Destiny Church in the recent events at the Te Atatu library prompted calls for its charitable status being withdrawn.

Quite surprisingly, given the scale of the topic, the Issues Paper is a reasonably short paper running to just 24 pages in all. It covers three main topics. Firstly, a review of the issues involved in the charity business income tax exemption including the rationale for providing such an exemption, and then what potential policy design issues would need to be considered if that exemption was to be removed.

The second topic is donor-controlled charities, which is probably where the most controversy is emerging. It considers the integrity issues that arise from the absence of specific rules for donor-controlled charities in New Zealand, and again looks at possible design issues, including how other countries treat such entities.

And finally, the paper considers a number of integrity and simplification issues to protect against tax avoidance.

The charity business income tax exemption

Apparently, there are over 29,000 charities registered under the Charities Act. Many raise funds through business activities ranging from small op-shops to significant commercial enterprises. There’s been long-standing grumbling about how charities which run a business and have an exemption have an unfair advantage. So, it’s interesting to read the background behind this exemption which has been in place since 1940.

Para 2.3 of the Paper sets out the scope of the review:

“Some tax-exempt business activities directly relate to charitable purposes, such as a charity school or charity hospital. Other tax-exempt business activities are unrelated to charitable purposes, such as a dairy farm or food and beverage manufacturer. It is the unrelated business activities that are the focus of this review.”

“…an international outlier”

According to the Paper “The current tax policy settings make New Zealand an international outlier”. According to a 2020 OECD study Taxation and Philanthropy most countries have either restricted the commercial activities that charitable entity can engage in, or they tax charity business income if the business income is unrelated to charitable purpose activities. As the Paper notes

“These countries have typically been concerned with a loss of tax revenue from businesses if a broader tax exemption was applied, unfair competition claims, a desire to separate risk from a charity’s assets, and a desire to encourage charities to direct profits to their specified charitable purpose.”

New Zealand’s exemption is based on the “destination of income approach.” This means that income earned by registered charities is exempt because it would ultimately be destined for a charitable purpose. But, and this is again one of the key concerns that’s emerged over time, this approach allows income to be accumulated tax free for many years within a charity’s registered business subsidiaries before the public receives any benefit.

What competitive advantage?

Paras 2.7 to 2.14 of the paper look at the question of the exemption providing a competitive advantage because they don’t pay tax. This is an allegation I’ve seen repeatedly raised. As the Paper notes not paying tax means

“One element of a firm’s normal cost structure, income tax, is not present in the case of charity run trading operation. It is argued that this “lower” cost could be used by a large-scale entity to undercut its competitors, to improve its market share, or to deter new entrants.”

The Paper does not accept this argument stating:

“Although the exemption does provide a tax advantage, it does not provide a competitive advantage. Any one type of cost can be looked at in isolation.”

The reasoning for this conclusion is:

[2.9] “Because the tax-exempt entity can generally earn tax free returns from all forms of investment, the “after tax” return it expects from a trading activity is correspondingly higher than that of its tax competitors. Therefore, an income tax exempt entity cannot rationally afford to lower its profit margins on a trading activity because alternative forms of investments would then become relatively more attractive.

[2.10] On this basis, the tax exempt entity will charge the same price as its competitors. The tax exemption merely translates to higher profits and hence higher potential distributions to the relevant charitable purpose. Consequently, funding the charitable activity from trading activities is no more distortion than sourcing it from passive investments such as interest on bank deposits or from direct fund raising.”

What about predatory pricing?

The Paper also discusses whether a charity has a greater ability to use predatory pricing to gain an advantage. Again, that’s dismissed because “the value of tax losses for taxable businesses mitigates this advantage. Taxable businesses can carry forward losses to offset future profits.” That said, if the taxable company goes bust then it has no use for those losses so maybe that is an actual advantage.

“Second order imperfections”

On the other hand, the Paper acknowledges that there are “various ‘second order’ imperfections in the income tax system that may need to be taken into account.” One is that charitable trading entities do not face compliance costs associated with meeting their tax obligations. This lowers their relative costs of doing business.

Another is the non-refundability of losses for taxable businesses and can result in a disadvantage for such businesses relative to tax exempt business resulting in a higher relative rate of return for non-tax paying entities when there has been a loss in one year.

A third is the costs associated with raising external capital such as negotiating with investors or banks can be significant. These costs often make retained earnings the most cost effective form of financing. Because charities retained earnings are higher, this may give them lower costs for raising capital. On the other hand, charities can’t raise equity capital because private investors cannot receive a return.

How much is ‘significant’?

Interestingly, the Paper describes the fiscal cost of not taxing charity business income unrelated to charitable purposes as “significant and is likely to increase.” But no numbers are given and I’m curious to know exactly what is the cost of this particular concession?

The Paper asks submitters to consider what are the most compelling reasons to tax or not tax charity business income before it analyses the potential implications and design issues involved. A major issue will be distinguishing between related and unrelated business activities which could prove difficult in practice without clear legislation and guidance.

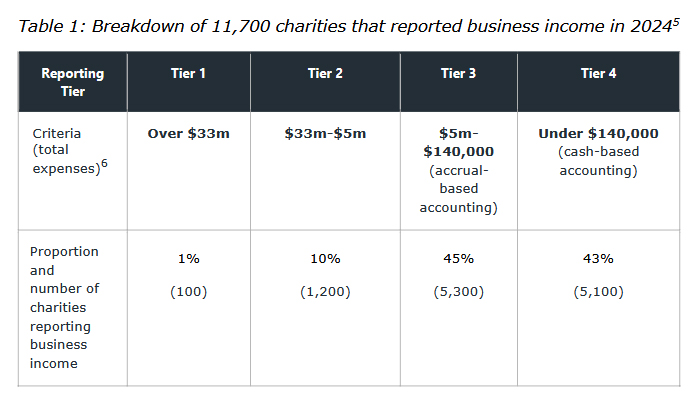

There’s more detail about the trading activities of charities. According to the Paper 11,700 of New Zealand’s 29,000 registered charities reported business income in their published 2024 financial accounts.

These four defined tiers follow the reporting requirements within the Charities Act.

A de minimis exemption?

Based on this initial analysis the Paper suggests a de minimis exemption for charities within Tiers 3 and 4. This would take 10,400 charities out of scope with only 1,300 subject to any policy change. Part of any policy change would involve the treatment of accumulated surpluses and whether there should be minimum distribution requirement.

According to the Paper a donor-controlled charity is any “charity registered under the Charities Act that is controlled by the donor, the donor’s family or their associates.” The current issue that there’s no distinction between donor-controlled charities and any other charitable organisations. The concern is growing that this can enable tax avoidance and raised compliance concerns “because of the control the donor or their associates can exercise over the use of charity funds.”

The Paper gives a few examples of potential abuse such as ‘circular arrangements’ when the donor gifts money to a charity they control, claim a donation tax credit or gift deduction, and the charity immediately invests the money back into the businesses controlled by the donor or their associates.

Also of concern with donor-controlled charities there can be a significant lag between the time of tax concessions for the donor and the charity, and the time of ultimate public benefit. This occurs because funds are accumulated and no or very minimal charitable distributions are made.

Another issue arises when donor-controlled charities purchase assets, or goods and services from the donor or their associates, at prices exceeding what would normally be paid by unrelated parties. These acquisitions are often made on terms that would not normally exist between unrelated parties.

Defining donor-controlled charities

This is the nub of the matter what criteria should be used to define a donor-controlled charity? The funds contributed and level of control a founder has. In Canada for example a charity is considered a private foundation if it is controlled by a majority (more than 50%) of directors, trustees, or like officials that do not deal with each other at arm’s length, or more than 50% of capital is contributed by a person, or a group of persons, not dealing with each other at arm’s length and who are involved with the private foundation.

The Paper suggests that transactions between donor-controlled charities and their associates could be required to be on arm’s length terms or prohibited outright noting in para 3.13:

“This approach was supported by the Tax Working Group in 2019, which found that the rules were private charitable foundations in New Zealand appeared to be unusually loose. The group recommended that the government considering removing tax concessions for private controlled foundations or trusts that do not have arm’s length, governance or distribution policies.”

Apart from citing the Canadian approach the Paper considers the approach to this issue in Australia, the United Kingdom and the United States. It suggests there should be a minimum distribution rule to deal with the question of the time lag between the charity and a donor claiming a benefit and the actual public benefit accruing from the distribution.

Taxing membership fees?

Chapter 4 considers integrity and simplification. This section has already attracted some media comment because it raises the possibility of taxing membership fees which could affect as many as 9,000 not-for-profit organisations.

At issue is the concept of mutuality and member transactions. Generally speaking, most not-for-profit organisations are treated as mutual associations. That includes many clubs, societies, trade associations, professional regulatory bodies.

Up until the early 2000s Inland Revenue’s guidance was that mutual associations were not liable for income tax from transactions with their members, including membership subscriptions and levies. Inland Revenue has withdrawn that advice and has drafted a replacement operational statement which will be released pending what feedback it receives on this Issues Paper.

The impact of Inland Revenue’s revised position would be that trading and other normally taxable transactions with members, including some subscriptions, would be deemed to be taxable income regardless of whether the common law principle of mutuality would apply. The Paper notes that most not-for-profits would not qualify for mutual treatment anyway, because their constitutions will prohibit distribution of surpluses to members including on winding up. This prevents the necessary degree of mutuality required.

Fringe Benefit Tax exemption under review

Finally, the paper touches on the FBT exemption for charities, which has been available since 1985. The paper notes “there are weak efficiency grounds for continuing this exemption” which “lacks coherence”. Inland Revenue is currently reviewing FBT generally and these comments suggest the FBT not-for-profits exemption is likely to go.

Submissions are open on the Issues Paper now, and close on the very unhelpful date it has to be said, of 31st March, when we’re all rather tied up with tax year-end issues. Notwithstanding that I expect there will be plenty of submissions particularly around the potential impact of taxing membership transactions.

Meanwhile in America…

Finally, a quick update on last week’s comments in relation to my concerns about potential leaks coming out of the US Internal Revenue Service (“the IRS”), following the Department of Government Efficiency (DOGE) trawling through the IRS and every other U.S. government agency.

The update I’ve had is that the DOGE people are looking more at IRS internal processes and nothing to do with any data that the IRS has received from Inland Revenue, or any other agency. There are a number of international obligations that the US has still to meet, but no doubt some concerns will have been raised.

But as I said at the time, which I believe is almost certainly the case, IRS officials will be highly professional in making sure that that information shared by other tax authorities is not leaked, accidentally or otherwise, to outside parties.

An interesting choice…

On the other hand, the IRS is getting a new Commissioner. The nominee is William Hollis Long II, or Billy Long, who is a former Republican House of Representatives member from Missouri.

He’s a controversial pick to say the least. He’s not a tax professional, and of particular note is that he was a co-sponsor of a bill in 2015 that would have abolished the IRS and introduced a national sales tax. He is also long-time supporter of a flat income tax for the US system. It’ll be interesting to see how this plays out, and as always, we will bring you developments as they emerge.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day