It has, to put it mildly, been a rather dramatic week in the geopolitical arena, with the United States appearing to basically abandon the security arrangements it established in Europe after World War 2, particularly the foundation of NATO.

Coupled with the US opening direct negotiations with Russia about the war in Ukraine, without the involvement of either Ukraine or NATO, it is now clear that a radical reshaping of the world order is underway after only a month of President Trump’s second term. It’s also clear that this is very much America First.

The OECD Two-Pillar deal is dead

The same is true in the tax world. In my first podcast of the year, I discussed one of President Trump’s initial executive orders, which in my view, pretty much meant the end of the Organisation for Economic Cooperation and Development’s (OECD) two pillar deal on international tax. My view was confirmed in a fairly bleak summary of the state of international tax by a Washington based presenter at this year’s International Fiscal Association (IFA) conference.

More on the IFA conference later. But as our presenter noted, it now appears that Value Added Tax (GST) is in the Trump administration’s crosses. On 13th February he issued another Executive Order on Reciprocal Trade and Tariffs. The issue here is protectionism which is very much part of President Trump’ economic policy agenda. He is particularly concerned about the decline in manufacturing and in particular about trade imbalances which he views as a consequence of the decline in manufacturing. Accordingly, many of the Executive Orders he has issued in this area are to redress these imbalances particularly those with Canada and Mexico. Hence the imposition of tariffs against both countries even if some are temporarily suspended. In the meantime, arguments continue.

In this vein Section 2 of the 13th February order noted

“It is the policy of the United States to reduce our large and persistent annual trade deficit in goods and to address other unfair and unbalanced aspects of our trade with foreign trading partners. In pursuit of this policy, I will introduce the ‘“Fair and Reciprocal Plan” (Plan). Under the Plan, my Administration will work strenuously to counter non-reciprocal trading arrangements with trading partners by determining the equivalent of a reciprocal tariff with respect to each foreign trading partner. This approach will be of comprehensive scope, examining non-reciprocal trade relationships with all United States trading partners, including any:

tariffs imposed on United States products;

unfair, discriminatory, or extraterritorial taxes imposed by our trading partners on United States businesses, workers, and consumers, including a value-added tax;”

A new and dangerous approach?

Note the word “each”. Value added tax is what we call GST. This is somewhat new and it’s frankly quite alarming because as you can imagine the impact of VAT is separate to that of tariffs. This is obviously quite concerning and causing consternation around the world. Because, as I said, this goes further than simply saying we’re going to impose retaliatory tariffs on you, because there is no equivalent to GST in the United States. There is no national sales tax. Every state imposes its own sales taxes at varying levels and sometimes local counties have separate sales taxes. It would actually take a constitutional amendment to introduce the equivalent of GST in the United States.

Another point that has been made in discussions around this, is that even if you added up the various state sales taxes that might be imposed, they’re nowhere near the same level of VAT that is often charged. And so, the question is, when a US firm has VAT applied to exports it now appears that this would open the door for retaliatory action by the US.

What about Netflix?

This led to quite an interesting debate at the presentation around the question of whether our “Netflix tax” might be within the scope of these retaliatory actions now. Potentially no, because the Netflix tax is a tax on services – in GST/VAT terminology a “reverse charge”. It’s imposed because otherwise no VAT or GST would be payable because the supply of services is outside the jurisdiction of the country providing the services. As Netflix is providing services from outside New Zealand to New Zealand residents, we’ve decided GST applies.

So, in fact it could be in scope. We really don’t know. One of the recurring themes of the assessment we got from the Washington based presenter at IFA was we have no idea what’s going on here, and we don’t know whether this is just rattling the cage for the sake of hopefully obtaining better terms on a deal. President Trump is very much transactional in his approach because that’s what he’s been about all through his life and he is applying that approach on a global scale now.

Maybe that’s the end of it, but it could also be that there is a genuine threat to impose tariffs where the US feels that GST has been unfairly imposed. We will have to wait and see.

What about a Digital Services Tax?

What I would say is that any hopes of a Pillar Two deal which has been moved forward (painstakingly slowly) by the OECD is probably dead in the water for now. This would probably extend to any digital services tax that we might consider introducing.

Remember that in President Trump’s Executive Order which withdrew the United States from of the OECD deal, there was also an instruction for the U.S. Treasury Department to investigate all potentially discriminatory taxes, and that would include a digital services tax. It would seem to me that our ability to impose that is quite restricted. So, we’re now into completely unknown territory here. The risk of retaliation might be lower at our end, but you never know.

Higher defence spending?

One of the issues that has been pushed on President Trump’s agenda (and it’s actually not an unreasonable point) is that America had borne much of the cost of defence throughout the Cold War, and even after the end of the Cold War it still continues to have a very large military establishment.

President Trump therefore demanded NATO nations needed to increase their defence spending to at least 2% of GDP. That is happening rather rapidly. This week, for example, Denmark announced further increases to its defence budget.

Our defence budget will come under examination, and this week the Prime Minister commented “We will be getting as close to 2 percent [of defence spending on GDP] as we possibly can, we know that’s the pathway we want to get to.” That’s probably not something Finance Minister Nicola Willis wanted to hear, but that’s the way of the world at the moment.

Could the sackings at the Internal Revenue Service have implications here?

The other thing of concern is what’s going on at the US Internal Revenue Service (the IRS)? Apparently some 6000 workers were sacked the other day, and we have reports that Elon Musk’s Department of Government Efficiency, DOGE, has been trying to gain access to records held by the IRS.

What I hadn’t been aware of is that the Commissioner of the IRS had resigned and will be replaced by a Trump appointee. I’ve previously commented about the risks that these actions represent to other tax jurisdictions. One would be in relation to all the information sharing agreements that exist, particularly FATCA.

I have no doubt whatsoever that IRS officials will do everything within their power to ensure the security of information shared under FATCA and other agreements is maintained. But if as is suggested, DOGE personnel are able to gain access to that information what will that mean for our international agreements? Will we and other nations be willing to continue to share information with the United States if we have concerns that it may no longer be secure? That’s a huge matter that there’s probably no answer to at the moment. I imagine quite a few tax authorities, including our own, are probably considering this very point right.

Time running out for an important GST election

One of the issues we deal with on an increasing basis is the treatment of Airbnb properties. In particular the implications when the GST threshold of $60,000 is crossed. In some instances, the taxpayer has claimed GST input tax on the purchase of the property involved, only to find out that they face significant GST liability if they decide to sell at a later point. This is something which obviously comes as a shock.

It so happens that two years ago, with effect from 1st April 2023, a transitional rule was introduced in section 91 of the Goods and Services Tax Act, which enables a person to elect to take that asset out of the GST net if certain criteria are met. The four requirements are:

if the asset was acquired before 1st April 2023, and

it must not have been acquired for the principal purpose of making taxable supplies, and

the asset was not used for the principal purpose of making taxable supplies, and

a GST input tax credit has been previously claimed, or the asset was acquired of as a zero-rated supply.

Note that ALL the above criteria must be met.

A good example would be a property which was acquired as a bach or holiday home but then rented out for short stay accommodation during the peak holiday period via Airbnb. Another example might be a business that has a residential property which was acquired as part of a larger land purchase.

Although primarily acquired for GST-exempt purposes the properties have been used to make GST supplies. Consequently, GST will be payable on sale. However, if you apply this transitional rule, you must make the election to take the asset out of the GST net before 1st April. If the election isn’t made in time, then the sale of any asset with business use, where GST was claimed on purchase, will be subject to GST on sale.

Basically, people have now just under five weeks to review their GST position and consider whether to make this transitional election and potentially bypass a large GST bill on a future sale.

Obviously in the run up to the end of the tax year on 31st March, there will be a number of other income tax and GST elections for people to consider if action is required.

An interesting conference

And finally, as I mentioned earlier, this year’s International Fiscal Association Conference was held on Thursday and Friday, hence why this podcast been delayed. It’s a policy-focused conference whose attendees are mainly partners from the large accounting and law firms, together with the heads of tax in major companies and very senior Inland Revenue officials.

This conference is subject to Chatham House rules, so while I can’t say much about what specifically was discussed, I can say it was an extremely interesting conference as always, and my thanks to the organisers.

As I mentioned earlier, we had a very interesting and thought-provoking presentation on the state of international tax as viewed from America. Inland Revenue has been very busy working on a number of topics, so we ought to see some very interesting legislation coming through this year, around either the time of the Budget, or more likely, when the annual tax bill is released in August.

Growing problems with double tax agreements

In relation to international tax, we had an interesting presentation on the impact of very specific anti avoidance rules on double tax agreements. Now double tax agreements generally override domestic law. In other words, we might have legislation where we might say we’re going to tax this. But then the double tax agreement says actually the taxing rights go to another country.

What is happening is there’s been a steady growth of what’s been called the general anti-avoidance rules, where it appears that companies have made what’s seen as abusive use of these double tax rules to claim tax relief. Countries are increasingly updating their tax treaties to include this general anti avoidance provision overriding the double tax agreement.

For example if you look at how Netflix, Visa and MasterCard seem to have substantial income from New Zealand without apparently paying much income tax, the question arises are the double tax agreement rules being abused and should this be dealt with by way of a general anti avoidance rule overriding the tax treaties?

Or you could also see these issues as being part of what we discussed at the top of the podcast is that the changes to the international tax order means more friction as basically tax authorities get more willing to get down and dirty and fight with each other over who has the taxing rights over income. We certainly live in interesting times.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Inland Revenue consults on treatment of repairs to newly acquired assets

Last week I discussed the suggestion from the Minister of Finance, Nicola Willis, that a cut in the corporate tax rate from 28% was under consideration.

Subsequently, on last Sunday’s Q+A, Robin Oliver was interviewed by Jack Tame on the topic. Robin is a former Deputy Commissioner of Policy at Inland Revenue and was also a member of the last Tax Working Group. In his role as a Deputy Commissioner at Inland Revenue he would have been involved in most of the major tax reforms of the last 30 years, so he really is one of the Titans of tax and always worth listening to.

Go big or go home…

In discussing the question of a corporate tax cut he made a very important point – go big or don’t bother. In his view dropping it from 28% to 25% simply wouldn’t make much difference. Instead, he suggested a bolder approach would be to cut it to say 18%. Because if you really are wanting to attract investment then you have to show something significantly different.

He raised the point that Singapore, which is often raised as a comparable, has a 17% corporate tax rate. Ireland, another comparable country has a 12.5% rate. Against these countries we would need to cut our tax rate substantially in order to attract investment.

But Robin Oliver also raised the question as to the consequences of such a cut and whether there might be other opportunities for improvement. He mentioned the problems which we’ve previously discussed about the Foreign Investment Fund regime. He also floated the alternative of accelerated depreciation for plant and machinery, which in his view was more fiscally realistic. Personally, I think this would be a more worthwhile move.

Reshaping our tax system – higher GST?

If he was given the opportunity for complete freedom of action over the tax system, Robin Oliver would be bold and go for a higher GST rate and taking the emphasis away from income tax. But he pointed out that although this might be nice in theory, the GST rate might have to rise to 28%, which would be pretty near unacceptable to the broader public. His key point was there are trade-offs to be to be made and it’s not simply a matter of a corporate tax cut will attract investment. Other considerations have to come into play.

I agree with Robin that if you are going to go with a corporate tax cut, you probably have to be bold about it. The question then is how do you recover that lost revenue? Robin’s response was that some hard choices would have to be made. He was a bit gloomy on those options, I thought.

What about a capital gains tax?

As I said Robin is a vastly experienced tax practitioner and he would have considered many options during his time supporting the work of various tax working groups and then as part of the last tax working group. He made a passing comment suggesting people stop whinging about capital gains tax. Robin was one of the three dissenters to the general capital gains tax proposal made by the last Tax Working Group but remember that the whole group was unanimously supportive of increasing the taxation of residential investment property.

Overall, very interesting to hear Robin’s take and I recommend watching the interview. It may be a corporate tax cut needed to be really attractive is probably beyond the Government’s fiscal capabilities at this point and therefore other alternatives might be more cost effective.

Further clues about tax changes?

Incidentally Iain Rennie, Secretary to the Treasury, made a speech to the 2025 New Zealand Economics Forum Bending two curves: New Zealand’s intertwined economic and fiscal challenges which supported a speech made by Finance Minister Nicola Willis, yesterday about the Government’s Going for Growth economic plan. Both mentioned tax with Iain Rennie noting

Our taxation of investment is also uneven, which distorts investment choices. Such economic settings can discourage the acquisition of productivity-enhancing assets like machinery and equipment.

This suggests that the policy responses are likely to include those that create an environment more conducive to firms making these investments. This could be through the structure of business taxation, savings policy, and regulatory frameworks that keep pace with business changes and create certainty for investment in emerging sectors.

These speeches provide a few more that a corporate tax cut could be perhaps a possibility. But there are, as Robin Oliver pointed out, other opportunities. Anyway, we’re obviously going to see a lot more speculation in the run up to the Budget on 22nd May.

Netflix’s tax reporting under investigation in France

An interesting story popped up this week involved Netflix’s tax activities. It appears Netflix’s offices in both Paris and Amsterdam had been raided late last year by French fraud investigators. European Union investigators started looking into the matter after France’s National Financial Prosecutor’s Office raised suspicions about the company “covering up serious tax fraud and off-the-books work”.

It transpires Netflix’s French subsidiary reported turnover “at odds with paying user numbers in the country.” Between 2019 and 2020, Netflix France paid less than €1,000,000 in corporate taxes, despite having more than 10 million customers.

What about Netflix New Zealand?

This is an ongoing investigation which after it came to the attention of Edward Miller the researcher at the Centre for International Corporate Tax and Accountability and Research, piqued his interest about Netflix’s activities here. When he went looking, he found out Netflix does not file any financial statements in New Zealand. This is actually acceptable under our low compliance approach to corporate filings. At present under the Companies Act 1993 public financial statements of a foreign-owned company must be filed if either the total assets are more than $22 million or the total revenue exceeds $11 million.

Now, surprise, surprise, Netflix New Zealand Ltd is apparently falls below that threshold, which as Edward Miller pointed out, seems odd given that there’s about 1.3 million users in New Zealand paying at least $18.49 a month to access its service. We’re therefore looking at another example of how multinationals are apparently able to shift profits offshore. Simultaneously, this is also an example of how tax authorities are increasingly taking a look at these activities and saying, ‘well, this is no longer really acceptable in our view.’

What do Netflix and Uber have in common?

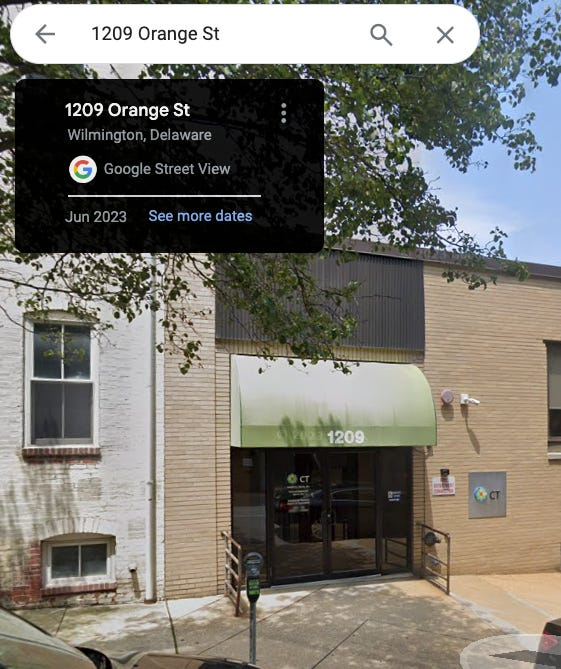

Where it becomes quite entertaining is that ultimately the head office for Netflix appears to be an address in a very unassuming building at 1209 Orange St, . Wilmington, Delaware in the United States. Delaware is a very tax favourable jurisdiction within the United States, and this particular address is so favourable that it is registered address of no fewer than 285,000 U.S. companies, including Uber.

That somewhere so modest is the home to so many companies is entertaining but also points to the serious issue of highly sophisticated tax planning where apparently income is earned in a jurisdiction but little or no income tax is paid.

In fairness to Netflix, notwithstanding its income tax position, it’s highly likely that it will be paying a substantial amount of GST. That’s because its customer base is individuals who will not be GST registered and therefore will not be able to recover the GST paid.

Incidentally, Visa and Mastercard are two other companies that we know very little about but have a significant effect here. Neither company have published financial statements for almost 10 years now. The revenue they earn on fees probably runs to hundreds of millions of dollars, but we just don’t know what portion is being taxed here. What Netflix is doing is a bigger issue than perhaps is generally appreciated.

Time to rethink our reporting requirements?

Given how opaque these transactions are, perhaps we need to rethink our rather relaxed approach to reporting and filing of a company’s financial statements, particularly in relation to multinationals. Interestingly, Australia now requires large multinational groups with an Australian presence to submit data on their global financial and tax footprint to the Australian Taxation Office (ATO), which will give more disclosure where around international profits are being booked. The Post approached the Minister of Revenue, Simon Watts, for comment and said that a similar proposal was not under consideration. (Note that the Australian proposal goes beyond country-by-country reporting https://www.ird.govt.nz/international-tax/exchange-of-information/count… which applies to a small number of multinationals).

What next?

The French investigation of Netflix is just another example of how many tax authorities around the world are looking at this question of where’s that income being really taxed and wanting justification for enormous fees that seem to end up in tax havens. But then, as I said last week, we now have the potential threat of the United States under the new Trump administration not favouring such investigation activities. It will be interesting to see how this plays out.

Are repairs to a newly acquired asset deductible?

As always, Inland Revenue is busy producing guidance on a number of matters and this week it was an exposure draft (ED) on a very interesting point – are expenses incurred on repairing a recently acquired capital asset deductible.

This draft is part of a series on repairs and maintenance expenditure which will eventually replace the current Interpretation Statement IS 12/03 – Deductibility of repairs and maintenance expenditure – general principles.

This exposure draft is potentially pretty significant – it reaches a different conclusion from IS 12/03 on the relevance of whether the price of the asset was discounted. Consequently, Inland Revenue is “particularly interested in comments on the relevance of the assets price in the context of initial repairs, as it appears there may be differences in opinion and practice.”

The ED guidance centres on what happens if you buy an asset that’s pretty run down, and then you carry out repairs to it to get it up and running? Are you able to claim those costs as repairs or should they be capitalised? For example, if you buy machinery that’s pretty run down and carry out repairs. If you can’t show that the repairs are genuine repairs – that they reflect wear and tear – Inland Revenue’s view is you must capitalise those costs. As such those costs are probably going to be depreciable.

What about repairs to buildings?

However, it’s a much, much bigger issue in relation to buildings. Because with the withdrawal of depreciation allowances for all buildings (not just residential buildings) the question of whether expenditure represents repairs and maintenance becomes an all or nothing issue. In other words, if it’s a repair, it’s deductible. If not, no deduction, whether in the form of depreciation or any other form, is available. I see a real pressure point emerging on this matter.

As always there’s lots of useful examples, but there’s also one or two matters we’d like to see clarified. For example, the ED refers to “normal wear and tear.” But what does that mean? If you’re talking about an asset that’s depreciated over, say, five years economically are Inland Revenue saying that repairs in excess of what the normal depreciation would be on that asset must be capitalised?

What about buildings?

It’s something I think needs more certainty, particularly in relation to buildings. The ED has an example on the treatment of repairs to a newly acquired building and I’m not so sure I’d agree with Inland Revenue’s conclusions. In summary, a 100-year-old tenanted residential property has been inherited by James. It’s in a poor state of repair and its condition was such that it could only be rented on a short-term basis with a high turnover of tenants and poor rental returns.

Because the property is in a good location James therefore decides if he restores the property to good condition the rental return can be increased by attracting different tenants for longer term letting. So, he carries out repairs to the property while it remains tenanted, including repairing the leaking roof, replacing some of the guttering down pipes, repainting portions of the exterior proper, and a number of other matters, including a repair to the main water supply pipe to the property.

The conclusion is that the expenditure incurred was necessary to restore and maintain the functionality of the property to the level required for its intended use of letting it on a longer-term basis. And for that reason, it’s capital in nature. No deduction will be available, and as I mentioned earlier, because it’s a building, no depreciation is available.

I’m not sure that would stand up in court if tested, because James is still deriving gross income. Yes, there’s an improvement to enhance it, but court cases have accepted that all repairs involve some form of improvement because you’re replacing old materials with new materials.

I’m intrigued to see what the response is to this and what comes out in the finalised guidance. Certainly, as I saw Robyn Walker of Deloitte point out, buying a car without wheels and then claiming a repair by sticking wheels on is clearly something that is not appropriate. But then in that case there should be a depreciation deduction available. It’s much more tricky in relation to repairs carried out to newly acquired properties. Again, watch this space.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Could the US retaliate against a digital services tax?

Last week, in a series of interviews with the press, notably with Newstalk ZB, Finance Minister Nicola Willis dropped several hints about what might be in the forthcoming May 22nd Budget. In particular, she talked about the corporate tax rate, and the possibility of cuts to that as part of promoting the Government’s growth agenda.

Corporate tax rate above OECD average

Speaking with Heather Du Plessis-Allan, Ms Willis commented:

“Well, if you compare New Zealand with the rest of the world, we’re not as competitive as we used to be. Which is to say that our corporate tax level is reasonably high when you compare it to the rest of the developed world.”

This is a very valid point which comes up frequently in discussions. Our current company tax rate at 28% is well above the OECD average of 24% and has been out of alignment for some time.

New Zealand back in the late 80s under the Fourth Labour Government was actually at the forefront of cutting company tax rates. A particularly interesting action was to align the company tax rate with the top individual and trust rates of 33%. The three basically stayed in line until the election of the Fifth Labour Government and the increase in the top personal tax rate to 39% in 2000.

There have been a couple of corporate tax cuts over the past 15 years or so. In 2007, the rate was cut from 33% to 30% and then in 2010, as part of the rebalancing that took place under Bill English with the increase of GST from 12.5%, the corporate tax rate was cut to 28% where it remained since.

As I’ve discussed previously, there has been a long running global trend towards lower corporate tax rates. But that has slowed in recent years, first because of the effect of the Global Financial Crisis and secondly, the fiscal shock to government finances because of the COVID-19 pandemic. As a result, according to the OECD in 2023, corporate tax rates rose generally across the board. Nevertheless, we are out of sync at the headline rate level.

More to investment than the corporate tax rate and will it work?

A lower corporate tax is undoubtedly attractive. However, the tax rate needs to be seen in context with what other incentives are available. Overseas companies and investors are very focused on what else might be on the table. A lower company tax rate would certainly be attractive, so the suggestion has been met with enthusiasm by some. Others are a bit more sceptical. Economist Ed Miller noted that when the effect of the corporate tax cuts in 2007 and 2010 are considered there does not seem to be any significant increase in foreign direct investment as a result.

The last tax working group didn’t see overwhelming evidence to support the theory that lower tax cuts at lower corporate tax rate would attract investment.

Problems and an alternative

There’s a flip side to this though, and it’s tied into the Government’s intention of restoring a surplus. Our corporate tax rate is not only above the OECD average, but our corporate tax take is also high by world standards. According to OECD statistics, 14% of the total tax receipts in New Zealand for 2022 came from company tax, whereas around the OECD the average is 12%.

So, if the Government, in an attempt to boost economic growth, is going to cut the corporate tax rate, it must then look at other alternatives to replace the lost revenue. One of the things it did back in 2010 and which it has already repeated, was to remove depreciation on all buildings. Depreciation for commercial buildings was restored under Labour but then removed again from the start of the current tax year on 1st April 2024.

A counter argument to the Government’s proposal for corporate tax cuts would be that enhanced depreciation allowances, including restoration of commercial building depreciation, which would include factories, might be a more effective approach than across the board tax cut.

How to replace lost tax revenue?

But if the Government is thinking of a corporate tax cut, and that does seem to be the case, what counter measures could they take to ensure that it is not fiscally too draining on the resources? One option might be that the availability of imputation credits may be restricted. For example, it might be that you can elect to have a lower corporate tax rate, but you imputation credits are no longer available to for shareholders.

As an aside, imputation (sometimes called franking) credit regimes were very popular during the 1980s, but gradually fell out of favour over time, mainly because, or in part because the European Court ruled that imputation credits or franking credits have to be available to all shareholders resident in the EU. After the German government lost this case its response was to heavily restrict the use of franking credits.

Change the tax treatment of Portfolio Investment Entities?

Another option might be to review the taxation of portfolio investment entities held by persons with effective marginal tax rates above the 28%. To quickly recap, Portfolio Investment Entities (PIEs) have a tax rate of 28%, equal to the company tax rate, which is also the maximum prescribed investor rate for individuals. So, there is actually a tax saving opportunity for individuals whose other income is taxed above the 28% rate for PIEs.

The Government might look at this, decide that will no longer apply and instead income from PIEs will be taxed at the person’s marginal rate. That could raise sufficient sums to partially offset the effect of a lower corporate tax rate.

The Finance Minister also mentioned reforming the Foreign Investment Fund regime, which is currently being considered by Inland Revenue and made some encouraging sounds about that potentially being an option.

We shall see. No doubt there’s a lot of work going on in Treasury and Inland Revenue looking at these options. All will be revealed in the Budget on 22nd May.

A threat to our Digital Services Tax

As covered in our first podcast of the year, one of President Trump’s initial executive orders withdrew the United States from the OECD Two-Pillar international tax deal. I drew attention to the second paragraph of that Executive Order, which directed the US Treasury to consider taking actions against other jurisdictions for tax actions which are potentially prejudicial to American interests.

Vernon Small, who was an advisor to the former Minister of Revenue, David Parker, now writes a weekly column in the Sunday Star-Times has picked up on this point noting that “Treasury has budgeted to rake in $479 million between January 2026 and June 2029 from a 3% Digital Services Tax (DST) on tech giants like Google and Meta.”

This, according to Small, “is an heroic piece of forecasting given current uncertainties and the provision for delaying collections until 2030 if progress is made on a multilateral approach through the OECD.”

And then the crunch point:

“Trump has bosom buddies in high places in the industry with Elon Musk first amongst them, and Mark Zuckerberg making a play for the new US administration’s affections.

Trump has promised to retaliate against discriminatory or extra-territorial taxes aimed at US interests. So the DST could be a prime target.”

Vernon Small is underlining the potential threat to our revenue base and our sovereign right to tax. If the OECD deal does fall over there are a number of countries including Canada, no longer America’s best friend, it seems, with DSTs ready to go. So there’s a whole potential for a tax war.

The Trump threat to tax administration

But equally worryingly, coming out of the United States is something about the question of bureaucratic independence from the executive. This might sound an arcane issue but it’s actually quite important to the independence of tax authorities.

One of the first actions of the Trump administration was to sack 17 Federal Inspectors-general. There’s also a move to put all Federal Government employees on the basis that they serve at the pleasure of the President. This would mean that an employee could be fired without the need for cause as the American terminology puts it.

Project 2025’s Schedule F

The implications of this have been picked up by Francis Fukuyama, the author of the famous The End of History essay written in the wake of the collapse of the Soviet Union and the end of the Cold War.

Writing for the Persuasion Substack under the title Schedule F is Here (and it’s much worse than you thought) Fukuyama wrote:

‘ “For cause” protection means that the official cannot be removed except under specific and severe conditions, like committing a crime or behaving corruptly. And now many individuals have been moved, in effect, to Schedule F because they are said to serve at the pleasure of the President.

Consider what this may mean if Trump hand picks a new Internal Revenue Service chief, that individual can be pressured by the Government to order audits of journalists, CEOs, NGOs and NGO leaders. Removal of Inspectors General will cripple the public’s ability to hold his administration accountable.’

Trump’s decision to move all Federal employees to Schedule F status is a step towards autocracy. What perhaps we all need to keep in mind is that the separation between the Commissioner of Inland Revenue and the Minister of Revenue is actually incredibly important. Yes, at times the Inland Revenue might do something which probably might embarrass the Minister of Revenue, but he cannot directly intervene in Inland Revenue’s operations.

A key part of a well-functioning democracy is that civil servants can act independently from their nominally political superiors. Fukuyama is right to say we should therefore have some concern coming at what’s happening in, in the United States because it does seem to be centralising power very rapidly around the President. The .potential for mischief is therefore enhanced as a result, and don’t think that such a step ultimately doesn’t have tax consequences.

Latest on the changes to the United Kingdom ‘non-dom’ regime

On a more positive note, last year I discussed the changes to the so-called ‘non-dom’ regime in the United Kingdom. This is where persons who are not domiciled in the UK have a special basis of taxation. Basically, they’re not taxed on income and gains which are not remitted to the UK.

This is a significant concession which is ending with effect from 5th April this year when it will be replaced by something which is more akin to our transitional resident’s exemption. This is pretty important for the approximately 300,000 Britons like me who’ve migrated here, plus the significant number of Kiwis who have assets in the UK or family going to the UK but have retained assets here. All of this group are potentially within the scope of these reforms.

There’s been a fair amount of push back on the reforms together with concerns that there will be a flight effect as wealthy, ‘Non-doms’ leave the UK. The UK Labour Government has been under pressure to make some changes to the proposals.

In response, the Chancellor of the Exchequer (Finance Minister) Rachel Reeves announced a concession (ironically at the gathering of the super-wealth at Davos) which will increase what’s called the temporary repatriation concession.

This concession will allow non-doms a three year window to pay a temporary repatriation charge on designated foreign income and capital gains so that they can subsequently be remitted to the UK without any further tax. The temporary repatriation charge will initially be 12% before rising eventually to 15% in the year ended 5th April 2028. For comparison, without the concession remitted income would be taxed at rates up to 45% and remitted capital gains would be subject to capital gains tax at 24%.

There’s a lot of opportunity here for potential tax savings for those who could be affected or will be affected by the proposed change to the non-dom regime. We’re still working through all of the implications but we will be updating our clients and bringing you developments as they arise.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Potential big change for US citizens living abroad

Latest IR consultation

Last week, with immediate effect, the Government announced changes in visa conditions, which will allow visitors to work remotely for an overseas employer/client during a visit to New Zealand. This change will affect all applications received from 27th January. It includes tourists, people visiting families together with partners and guardians on longer term visitor visas.

A faster growth track

Basically, the changes are designed to encourage digital nomads to come here and enable them to carry on working for their overseas employer without breaching their visa conditions. As Nicola Willis in her role as Minister for Economic Growth explained in the accompanying press release “The change is part of the Government’s plan to unlock New Zealand’s potential by shifting the country onto a faster growth track.”

These new visitor visas are subject to the following conditions: the visa holder cannot work for a New Zealand employer, nor can they provide goods or services to people or businesses in New Zealand, nor can they do work that requires them to be physically present at a workplace in New Zealand.

What about income tax?

What difference, though, does the new visa make from a New Zealand income tax perspective? The short answer is ‘not an awful lot.’ Much of this possible digital nomad activity is already within section CW19 of the Income Tax Act 2007.

Under that provision the income that a non-resident person derives from performing personal or professional services in New Zealand is exempt if the visit is for 92 or fewer days, the services are performed for a person who’s not resident in New Zealand and that income is taxable in the jurisdiction in which the person is resident. This would typically capture most of activity of a digital nomad.

Section CW 19 is a long standing provision and, as the New Zealand Immigration announcement noted, the 92 day exempt period can be increased to 183 days if the visitor is tax resident in a tax country with which we have a double tax agreement.

As the Immigration Minister Erica Stanford noted, updating these visitor visas reflects the realities of current modern flexible working environment. It’s probably a good move to bring the visas up to date and make clear that it’s generally not a major issue if you are working remotely when visiting and are not in breach of any tax obligations.

Keep in mind the 92-day exemption in section CW 19 is for employees only, it does not apply to any self-employed person who might provide goods or services to people or businesses in New Zealand.

Yes, but what about Taylor Swift?

The other group of people who aren’t covered by the section CW 19 exemption are ‘public entertainers.’ Which means that if we ever did manage to get Taylor Swift here, theoretically the earnings that she made from any concert would be taxable in New Zealand. As an aside there are all sorts of very interesting and complex tax rules around entertainers.

Overall, it’s an interesting move which seems to now bring our visa practices in line with what’s happening globally. It reflects that, because of the greater interconnectivity available now people have quietly been working remotely, effectively acting as digital nomads without actually realising that they may have been in breach of their visa conditions.

In any case, if the person has been here for under 92 days, then generally speaking, they shouldn’t be in breach of any of their tax obligations. As I said an interesting move and no harm clarifying the visa situation. What the economic impact will be, who knows.

An end to citizenship based taxation for US citizens?

In our last podcast of 2024, we discussed Inland Revenue’s paper on changing the Foreign Investment Fund (FIF) regime to make it more attractive for migrants. One of the issues the paper discussed was how the FIF regime created headaches for American citizens and Green Card holders tax resident in New Zealand but who still have to file U.S. Federal tax returns. The paper was proposing changes that might help deal with the essential double taxation issue for these taxpayers.

It so happens an Illinois Republican Congressman, Darren LaHood, has introduced the Residence-Based Taxation for Americans Abroad Act, which would implement a residence based taxation system for U.S. citizens currently living overseas.

LaHood’s press release doesn’t mention it, but I’d be very curious to know exactly how much tax these expat American citizens pay in the US.

The preamble in the press release notes that the United States is the only major country that uses citizenship based taxation. According to recent estimates, there are about 5 million U.S. citizens currently living aboard. Based on the last census there are over 30,000 US born persons here in New Zealand.

LaHood is also a member of the highly influential House Committee on Ways and Means, (their equivalent of the Finance and Expenditure Select Committee) so perhaps this is a serious move. This bill could also gain from the general tax cutting mood of the new Trump administration. We’ll be interested to see how much further this goes.

In the meantime we’ll also be watching for progress on Inland Revenue’s proposals to try and deal with the anomalies the FIF regime creates for U.S. citizens resident here.

New Inland Revenue guidance on depreciation

Finally, Inland Revenue as always has been busy pushing out guidance and draft consultations on issues. One which caught my eye and will be worth perhaps thinking further about is Interpretation Statement IS25/03Income tax. Identifying the relevant item of property for depreciation purposes. There’s also an accompanying fact sheet which is always very helpful.

Our very detailed tax depreciation rules system rules have numerous depreciation rates available so it’s often a worthwhile exercise identifying what assets are involved and maximising the available depreciation.

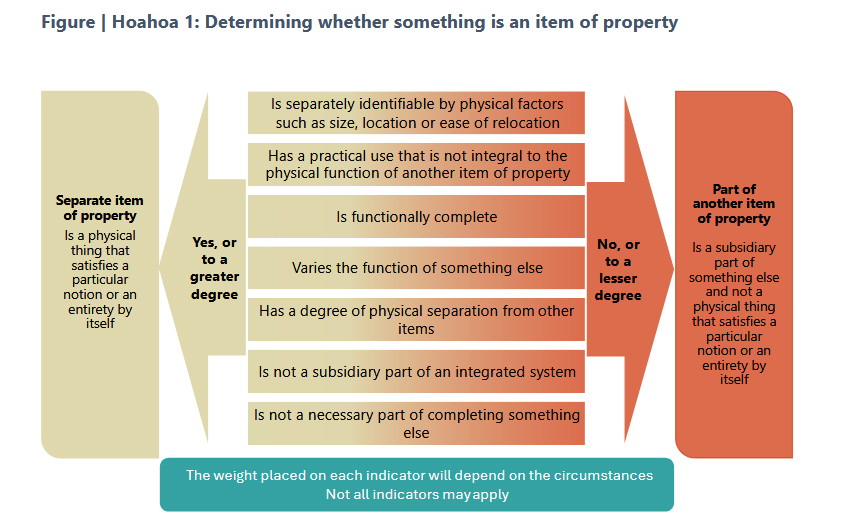

The Interpretation Statement therefore provides general guidance on how to identify the relevant item of property when applying the depreciation rules. The key issue is determining whether the item is physically distinct from a wider asset of which it might from a part.

In determining this you would first consider its location or size, whether it’s integral to the physical functioning of a wider asset and the degree of physical attachment to other related assets.

Secondly, is the item largely functionally complete, in other words, can it function on its own? That doesn’t necessarily mean that it has to be self-contained or used separately, but could it function on its own??

Thirdly, does the item vary the function of another item? What this means is two items will remain separate items where one varies the function of another item, enabling it to perform more specialised function.

The Interpretation Statement provides a few examples together with a useful flow chart.

A key part of the analysis is it always comes down to a question of fact and that means that there will be different outcomes for apparently similar situations.

The Interpretation Statement contains links to other Inland Revenue guidance on depreciation related issues. All this is very useful because in the run up to the end of the tax year on 31st March, we often have situations where clients are looking at investments and wanting to maximise depreciation.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

There have been several constant themes throughout this year. A surprising one has been the question of how we tax capital and whether we should have a capital gains tax. Throughout the year there have been a steady stream of stories on the topic. Meanwhile the Labour Party is currently reviewing its tax policy, and whether it’s going to go with a wealth tax or a capital gains tax.

A place where talent does not want to live

Intriguingly, Inland Revenue has added to this mix right at the end of the year with the release of an issues paper on the effect of the Foreign Investment Fund (FIF) rules on immigration.

Earlier this year I discussed a New Zealand Institute of Economic Research report called The place where talent does not want to live, which looked at the impact of the FIF rules on migrants to New Zealand. The NZIER report concluded that the FIF rules were acting as a hindrance to investors, particularly those migrants coming here who have previously invested in offshore startup companies.

The report also discussed an issue I’ve encountered fairly regularly of the impact of the FIF rules for American citizens. Even though they may have been resident in New Zealand for many years, because they are American citizens they still have to file U.S. tax returns. As a result, a mismatch arises for them between the FIF rules, which basically act as a quasi-wealth tax, and the realisation basis of capital gains tax that applies in America.

Inland Revenue policy officials have been aware of this issue for some time. In fact, I spoke to several officials earlier this year about the issues and potential options. The topic was highlighted as an option for review and was included in the Government’s tax and social work policy programme released last month. This report has therefore come out quicker than I expected which is a pleasant surprise.

The problem with the FIF rules

The problem is set out very clearly in paragraph 1.5 of the issues paper.

“Migrants will generally have made their investments without awareness of the FIF rules and may not be organised so that they can fund the tax on deemed rather than actual income. This is particularly a problem for illiquid investments acquired pre migration…. Because the FIF tax is imposed in years before realisation and on deemed rather than actual income, FIF taxes paid may not be creditable against foreign taxes charged on the sale of the investment.“

This highlights a key point about the FIF rules – they’re highly unique by world standards. When I’m discussing them with overseas clients and advisers, to make them more understandable I tend to explain them from the viewpoint that they’re a quasi-wealth tax. As the quote above notes problems also emerge whether the tax paid under the FIF rules can be fully utilised in the United States, for example.

Fixing the problem – taxing the capital gains?

The paper canvasses several options for reform, including one of simply increasing the current $50,000 threshold above which the FIF rules automatically apply. A key proposal is that maybe the investments subject to the FIF rules should be taxed on what is called revenue account. That is only dividends received and any gain in the value of those investments attributed to New Zealand on disposal would be taxed. In other words, an investor would be taxed on dividends and then when the investment was disposed of, a capital gains would be become payable.

Now to buttress this option the paper proposes that there should be an exit tax. In other words, if someone elects to use the revenue account method, but then decides no, actually New Zealand isn’t working out for us for whatever reasons, and they become a non-tax resident, this migration would trigger an exit charge. I’ve seen this in other jurisdictions and current FIF rules do have a provision covering it. This approach should be pretty understandable to investors coming here.

Maybe a deferral basis?

Another alternative is a so-called deferral basis, is where the FIF rules would apply on a realisation basis. This would be achieved in a way similar to how withdrawals on foreign superannuation schemes are currently taxed when the tax charge arises on withdrawal or transfer into a New Zealand based Qualifying Recognised Overseas Pension Scheme.

The taxable amount would be based on a deemed 5% per annum income from the date of their migration, with an interest charge for deferral. Again, this would be buttressed by an exit tax.

What happens overseas?

Picking up on what I was saying at the start about the question of taxation of capital, most other jurisdictions don’t encounter this issue to the same extent as we do because they usually have a capital gains tax regime that applies to comprehensive capital gains. Actually, in paragraphs 2.3 and 2.4 I find there’s some intriguing commentary from Inland Revenue on this issue.

“Because New Zealand does not tax capital gains without the FIF rules, no New Zealand tax would ever be paid on an investment in a foreign company that paid no dividends and was sold for a capital gain.”

This is an interesting insight to the issues caused by non-taxation. In effect without the FIF rules the Government is forsaking potential revenue. I always thought the expansion of the FIF rules in 2006 was really a sidestep around the difficult issue of taxing capital. And of course, despite having kicked the capital gains tax can down the road back in 2006, it’s still there.

Tax driven behaviour, or just a rational investment choice?

The issues paper goes on, quite controversially in my view, to argue that without the FIF rules in New Zealand, residents have a tax driven incentive to invest in foreign companies that enjoy low effective tax rates and do not pay significant dividends. Speaking with 40 years of tax experience, yes taxes do drive investment behaviour.

But this argument sidesteps a huge criticism, which is still valid, of the current FIF rules. When they were introduced in 2006, many of the submissions against them argued that the New Zealand stock market is so small in global terms that investors would be unwise to be fully invested here, and therefore should be spreading their risk by diversification and investing in offshore markets.

That is as valid a criticism of the FIF rules now as it was back in 2006. And of course, memories of the 1987 stock market crash, which was actually quite catastrophic by world standards, still run deep in many areas. We now have this scenario here where the FIF rules were designed because the Government wanted some revenue. It saw tax driven behaviour happening offshore, but it ignored a key fact, the importance of diversification. And if you don’t tax the capital but you want the revenue, where do you go from there?

Backdating the introduction of the changes?

Anyway, the whole paper is a very worthwhile read. It has one further highly interesting suggestion that changes could be back dated to take effect from 1st April 2025 and the start of the next tax year. Such a swift law change doesn’t happen with issues papers. Normally there’s usually another year or so before legislation is introduced and then comes into effect.

This option is actually very encouraging for migrants. I have had a number of inquiries on this issue, and I know of clients who have backed away from New Zealand because of the FIF rules. So, they will be looking at the proposals with great interest.

The paper also canvasses whether it should apply to new migrants or to existing New Zealand tax residents. That’s a good question it should certainly apply to migrants who can reorganise their affairs in anticipation, but I believe it should also apply to U.S. citizens who still have to file U.S. tax returns and are very disadvantaged by the current FIF rules.

Worth noting that although this is largely a tax measure it’s important to the Government because the existing FIF rules are seen (as the NZIER report noted) as a hindrance to attracting high quality migrants. Changing the law is seen as a priority as part of the Government’s general economic programme,

Submissions are open now and continue until 27th of January. I urge everyone interested in this topic to submit. We will be submitting a paper on this ourselves. We will also be contacting clients on this matter as it’s quite a welcome Christmas present.

The year in review

Moving on, its been a very busy year in tax. And I guess the biggest story in many ways was the Budget on 30th May, with the promised increase in tax thresholds finally being enacted with effect from 31st July. That was certainly the most eagerly anticipated one, and according to my data reads, it was the most read transcript over the year.

The tax cuts which weren’t

These tax cuts as they were called (which they’re not because they’re only inflation adjustments) also highlighted a big and continuing problem with our tax system, which the politicians apparently don’t want to address. The threshold adjustments only factored in inflation from 2018. They therefore effectively locked in the inflationary effect of the non-adjustment between 1st October 2010 (the last time the thresholds were adjusted) and the 2018 baseline.

On the other hand, in order to help pay for these adjustments which will reduce government revenue, the threshold on Working for Families which has been at $42,700 since 1st July 2018, was not increased. This means that families with income above that threshold have their Working for Families credits abated at 27.5%. Consequently, they face some of the highest effective marginal tax rates in the country.

And as I have repeatedly said in past podcasts, our politicians are very much less than transparent about the impact of what’s called fiscal drag. That is, as wages increase with inflation, they pull taxpayers up into higher tax brackets. We have a particularly big problem around the now $53,500 threshold where the tax rate jumps from 17.5% to 30%, the biggest single jump in the whole tax scale.

To bang a drum already beat repeatedly, this hinders a discussion around what is happening with our tax system? How much revenue have we really raised because politicians have been happy to use fiscal drag to quietly increase the tax take.

But the main effect is that the burden of tax falls on low to middle income earners who face significantly higher marginal tax rates because of the effect of abatements on people receiving social support, such as Working for Families.

So overall, those tax threshold adjustments were welcome. They were overdue, but they were one step forward and two steps sideways and half a step back because there’s no comprehensive commitment to ensuring that we have regular threshold adjustments.

If America can do it, why not here?

Just as an aside, in America all thresholds are automatically index-linked. Countries vary on their treatment of inflation and thresholds. And in low inflation periods, you can get away with not needing to do it every year, but you can’t leave such adjustments for 14 years without finally having to do something.

A year of anniversaries

2024 was quite a big year for me personally. I started working in tax 40 years ago in Britain and it so happened that the British budget on 30th October had several announcements which have huge significance not just for UK migrants who have moved here but also for many Kiwis. So, I find myself, somewhat ironically, still doing a lot of work on the impact of British taxation.

It’s also been 20 years since I started Baucher Consulting and as I said in the podcast much has changed, and yet in some ways little has changed. One constant which hasn’t really changed is the behavioural impact of tax- this week’s discussion of the FIF regime is the latest example. I’d like to thank everyone who’s supported me over the these past 20 years.

Our fantastic guests

Looking at some other highlights of the year in terms of the podcast, we had a lot of great guests this year and my thanks again to all of them. My particular favourite episode was the Titans of Tax with Sir Rob McLeod, Robin Oliver and Geof Nightingale. Many thanks to Sir Rob, Robin and Geof for giving up their time. It was a fantastic discussion and very, very enjoyable. It was extremely well received all around. It was fascinating to just sit back and listen and to three experts who’ve been very heavily involved in the last three major tax working groups.

My thanks also to all my other guests this year, including the four finalists for this year’s Tax Policy Charitable Trusts Scholarship. Again, thank you so much for your input. Very interesting to talk to you, and the future of tax policy is in good hands.

Inland Revenue goes full throttle on compliance work

One of the big themes for the year, and less of a surprise, was Inland Revenue’s ramping up its enforcement approach. One of our guests very early in the year (and thanks again) was Tracy Lloyd, service leader of Compliance Strategy and Innovation at Inland Revenue. Tracy’s podcast was a really interesting one looking at what tools Inland Revenue is using and how it’s ramping up its investigative activities.

We’ve seen Inland Revenue’s more aggressive approach constantly through throughout the year. It has made announcements about cracking down on the construction sector, looking at liquor stores. Pretty much every week there’s a media release that another tax fraudster has been jailed or received substantial fines or home detention. In addition Inland Revenue is making use of information received through the Common Reporting Standards on the Automatic Exchange of Information.

These things will continue to come through. Inland Revenue got $116 million over four years to beef up its investigation activities and to improve its tax collection. As part of this we’re seeing a crackdown on student loan debt, which is a much more problematical issue mainly because the biggest portion of debt is held by persons overseas. It’s therefore not so easy to collect.

Inland Revenue’s activities will continue to ramp up but I think it may start to find there’s increasing push back as it clamps down. I think it’s previously been slow in responding, and during the COVID pandemic that was understandable. But right now, the faster it responds to debt issues developing, the better for all of us. Zombie businesses which linger on are no good to anyone.

The surprising continuing debate over capital gains

But the other big thing this year has been a surprising one. It’s the question of the shape of the tax system and persistent media stories about whether we should have a wealth tax or capital gains tax. This is a topic I don’t see going away. I see the pressure mounting on it because as, the Government’s main agency, Treasury, is pointing out we have ongoing demographic pressures in relation to superannuation and funding health.

And as I keep pointing out, we also have the question of climate change. We have insurers withdrawing cover and I think that means the Government will be expected to step in. And that means sharing the burden, which means ultimately some form of tax increases. All this means the composition of the tax base will continue to be a matter of debate.

Of course, we have options like capital gains tax, wealth taxes, or as Dr. Andrew Coleman suggested (another one of the fascinating podcasts this year) maybe we should rethink our issue of Social Security taxes, where again we’re a unique jurisdiction in that we don’t have them. We used to have such taxes way back from the early 1930s through until late 60s, before they were finally abolished,

So overall lots to discuss this year. I’d like to thank all my guests again, and all the listeners, readers and all those who chip in and comment away. Your comments are read and always welcome. And on that note, everyone have a very happy festive season. We’ll be back with what’s new in the tax world in January 2025.