The Government introduces a surprise fringe benefit tax exemption

The potential implications for New Zealanders from the UK’s Spring Budget

Inland Revenue has now formally launched its campaign to improve tax compliance in the construction industry, which I first mentioned a couple of weeks back. Under the heading, “Take the stress out of tax” it is promoting a tax toolbox for tradies.

This is intended to provide the rules, resources and tools to enable people to get their tax position correct. Proclaiming “We’re here to help”, there’s a series of pre-recorded online seminars covering the most common topics, such as an introduction to business, a GST workshop and employers’ responsibilities. There’s also offers for more direct contact, such as a business advisory or social policy visit. And then there’s a reminder that people can also talk to tax agents or use accounting software to, “take the pressure off.”

The background notes released comment that 42% of construction industry taxpayers who are behind either in tax payments or in filings have a tax agent. So, the role of tax agents is seen as important and obviously Inland Revenue is hoping that the role of agents will expand.

There’s also a reminder that Inland Revenue has access to data, which, as it puts it, means “We have a good handle on what happens in the construction industry”, adding it’s never too late to do the right thing. And it goes on to suggest people should come forward if they’ve forgotten some income of past tax returns or maybe have overinflated their expenses.

This is a welcome initiative by Inland Revenue. The phrasing of the campaign “Take the stress out of tax” is a classic example of speaking softly but carrying a very big stick. My view is that too many people either underestimate or are unaware of just how much data is available to Inland Revenue. This campaign phrasing also touches on something of a paradox I’ve experienced when dealing with clients with tax arrears. They’re often relieved to discover after discussing the matter the position is nowhere near as bad as they had feared, and they can now sleep easier. And I expect I’m not the only tax agent to have observed that.

It will be interesting to see the outcomes from the campaign. And as always, we’ll keep you updated with developments.

Exemption from FBT for bicycles, e-bikes, e-scooters … and mobility scooters

Now, two weeks back, I discussed the so-called apps tax. This is part of the Finance and Expenditure Committee report back on the Taxation Annual Rates for 2022-2023 (Platform Economy and Remedial Matters) Bill (No.2). The updated bill included some provisions around the proposals to charge GST on services supplied by the likes of Uber and Airbnb. The bill also included clarifications to a proposed fringe benefit tax exemption for the use of public transport.

As part of the bill, over 400 submitters, including myself, made submissions proposing some form of FBT exemption for e-bikes and e-scooters. The officials report declined the submissions commenting,

“Our overall conclusion is that a specific FBT exemption for bicycles would increase the distortion between the taxation of transport benefits and other fringe benefits, reducing the overall fairness and coherence of the tax system and giving rise to integrity risks, impacting on the fiscal cost.

If Parliament wanted to increase the uptake of cycling to help achieve improved health outcomes and assist New Zealand to achieve emissions reductions, it would instead recommend a more transparent and potentially targeted subsidy specifically designed to achieve considered policy outcomes.”

This is Inland Revenue’s boilerplate for “Nah, go away. We don’t like subsidies and special tax exemptions.”

That was then. But in what has become something of a pattern following Chris Hipkins’ elevation to Prime Minister, this week the Government has released a Supplementary Order Paper for the bill, which now introduces an exemption from FBT for bicycles, e-bikes, e-scooters and mobility scooters.

According to Revenue Minister David Parker the Government “considers that there is a public good to be gained from encouraging low emission transport” and “This measure will support New Zealand’s shift to more sustainable transport options and encourage employers to provide further sustainable and climate-friendly transport options for their staff.”

The bill includes a regulation making power which would specify the maximum cost of the exemption and the specifications to qualify. When I made my submission, I suggested a cap of about $4,000 should apply. It will be interesting to see what will be the maximum available under the exemption and how many employers make use of it, which will come into force on 1st April.

An English Budget and why it’s interesting here

On Wednesday night, the British Government unveiled its Spring Budget. This is a far less dramatic affair than the Autumn Statement last September, just after the Queen died, which led to the downfall of Liz Truss. This time the Chancellor of the Exchequer (Finance Minister) Jeremy Hunt has gone for something rather more cautious in its approach with one or two twists.

I was actually surprised there weren’t any moves around restricting the availability of non-residents to make use of the Personal Allowances exemption, or just generally increase the taxation of non-residents. That’s something I’ve seen other countries do. Australia is a very good example of where that happens. A cynic might say that’s because some of those non-residents are Conservative Party donors. But cynicism aside, given the financial pressures that the British government faces, not kicking over the stone and looking, is a bit surprising,

For example, there weren’t any changes to the controversial non domiciled or “Non-dom” scheme which gives a tax advantage on foreign income for people who are not tax-domiciled in the UK (including Prime Minister Rishi Sunak’s wife). (Most New Zealanders would qualify for this exemption).

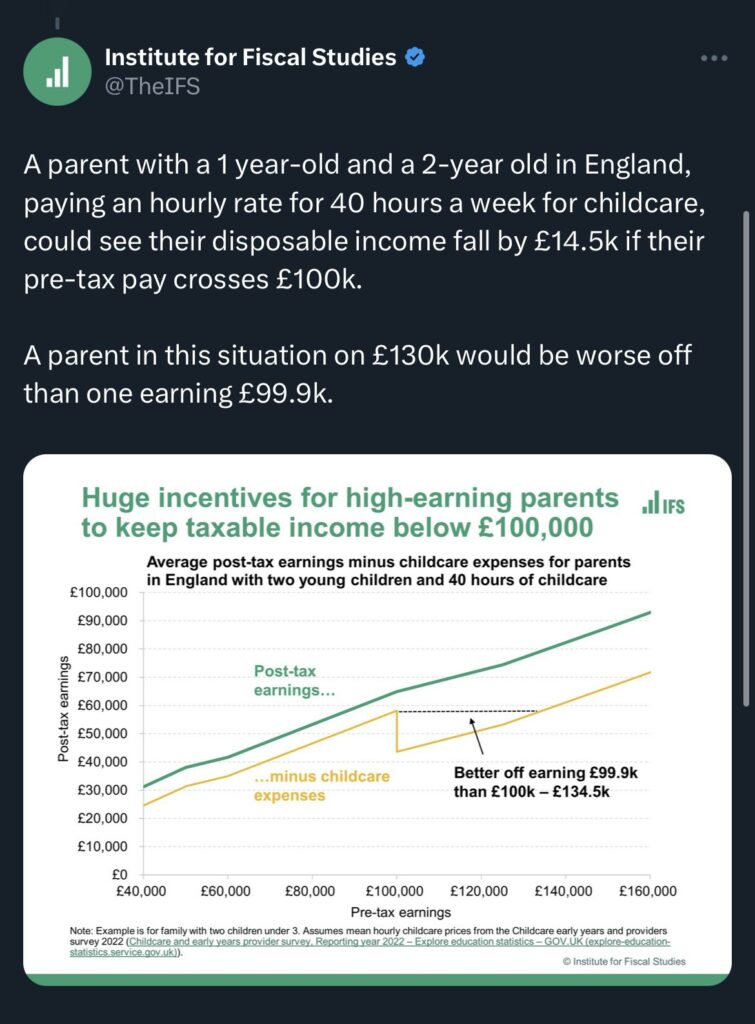

But what has perhaps attracted a fair bit of interest here was an excellent proposal, to provide and support up to 30 hours each week of free childcare support for working parents with children now aged between nine months and three years. Basically, free childcare will be available from between the ages of nine months and when children go to school. The National Party has recently announced proposals boosting childcare access.

There is a kicker to this in that it’s not available to anyone whose adjusted income is above £100,000. Basically, if someone earns more than £100,000, then all of those childcare costs they might have received are clawed back. Essentially, they don’t get back into the same net position until their income rises to £191,000. A 100% effective marginal tax rate will apply.

Now, you might well say, and I have to agree with you, that income of over £100,000 is a nice problem to have. However, it highlights a similar issue we have in our tax system in relation to clawback of Working for Families tax credits that effectively people on what modest incomes face higher than expected marginal tax rates. The clawback kicks in at a rate of 27 cents per dollar of income above $42,700.

I would hope whoever’s in Government will look seriously at this question of the clawback, the amount applicable and the threshold.

Of more direct interest to some New Zealanders is a change to what is known as the Lifetime Allowance Charge. Now, this is a controversial move that was brought in some years back because Britain has generous tax exemptions for pensions contributions. Consequently, some had accumulated very substantial pension pots tax free. To counter this, the Lifetime Allowance Charge was introduced, which imposed a charge which could be as high as 55% where the accumulated funds were above a threshold (£1,073,100).

The Lifetime Allowance Charge will be removed from 6th April and will be abolished in a future finance bill. Apparently up to 1.4 million people were caught by this. I know of several clients within this group. So they were considering their options about when and how to withdraw funds from their UK pensions. The removal of the charge means they may wish to reconsider their options.

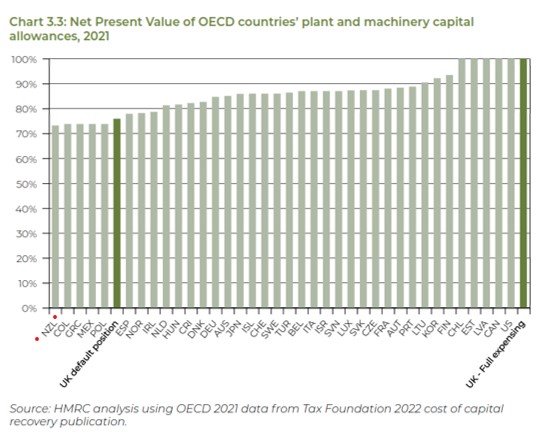

But the other thing that was particularly interesting to me is, and I think for our economy at wide was the decision to allow full expensing for capital assets acquired up to £1 million per year. Under this “Investment Allowance”, a first year allowance of 100% will be available up to the £1 million threshold. The idea is to encourage investment.

This is a topic that comes up in discussions down here. But what caught my eye was a graph produced as part of the background papers showing the net present value of all OECD countries plant and machinery capital allowances as of 2021.

As you can see under the present previous tax treatment, the UK would have been 33rd in the OECD. By going to full expensing, it moves up to be jointly top of the OECD. However, what caught my eye is that New Zealand is bottom of the OECD.

The question therefore arises whether we ought to be looking at our capital allowances regime. A similar type of initiative would be expensive, there’s no doubt about that. That’s one of the main reasons cited against such initiatives. But on the other hand, Britain has made this move because it wants to boost productivity and we know we’ve got problems with productivity.

So, here’s another challenge for the Finance Minister, Grant Robertson, to be considering right now. How do you boost our productivity? Is something similar to the UK investment allowance worth considering? We will see how that plays out in the UK. I see speculation about what might be in our budget in May is already emerging. Increasing capital allowance deductions is something I’m sure is under consideration. However, I’m also, to be honest, sceptical that we’ll see anything in the Budget.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Plenty to consider in Inland Revenue’s latest Interpretation Statement on tax avoidance

Working from home allowances updated

GST and Donation Tax Credit fraudsters convicted

Last year, I covered the Supreme Court decision in Frucor Suntory New Zealand Ltd v Commissioner of Inland Revenue. To recap, Frucor had entered into a series of arrangements mainly for the benefit of its overseas parent. However, in the eyes of the Commissioner these arrangements represented tax avoidance. By a majority of 4 to 1, the Supreme Court ruled that the arrangements did indeed represent tax avoidance, and they also met the threshold for the imposition of shortfall penalties totalling $3.8 million. What was also of particular note here was the very strong dissenting judgement from Justice Glazebrook, which was completely at odds with the majority opinion.

Following the Supreme Court decision, Inland Revenue have now released an updated Interpretation Statement IS23/01 Tax avoidance and the interpretation of the general anti avoidance provisions of sections BG 1 and GA 1 of the Income Tax Act 2007. This 138-page Interpretation Statement is accompanied by a nine-page fact sheet and two Questions We’ve Been Asked covering income tax scenarios on tax avoidance, which amount to another 50 pages or so. A fair amount of material to work through.

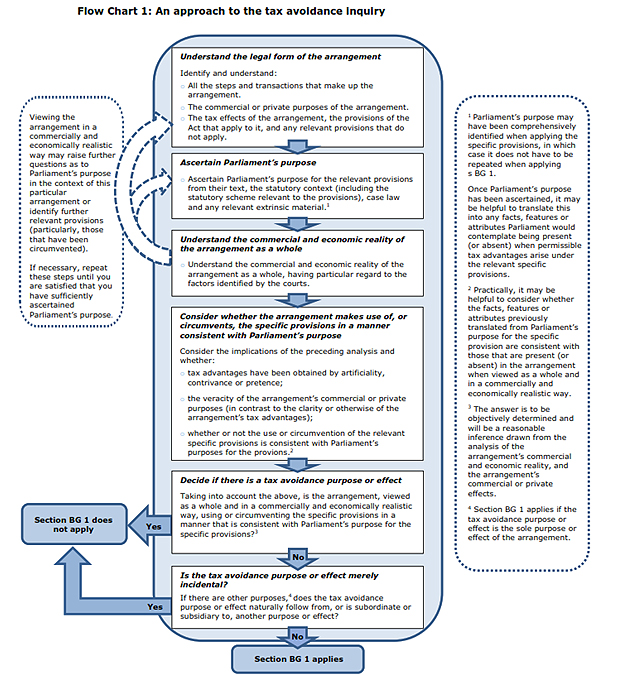

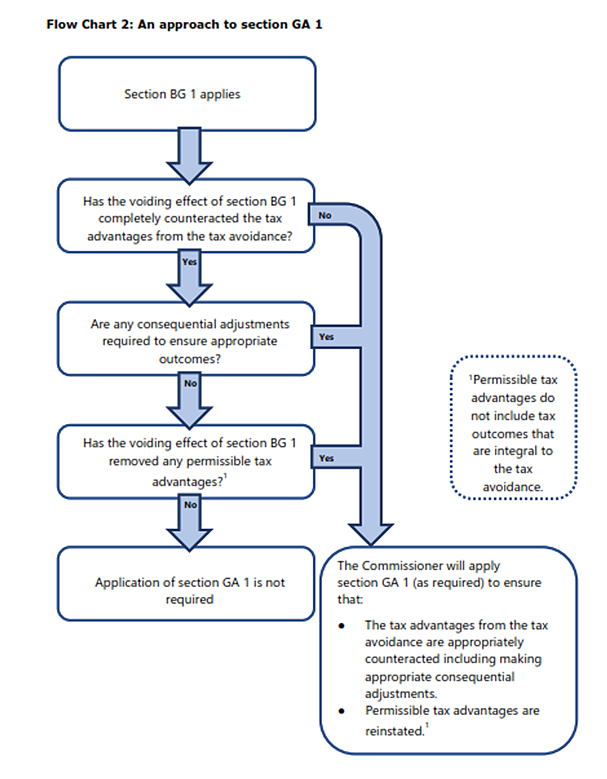

The statement sets out the Commissioner’s approach to the application of Section BG 1 and then explains how under the related section J1 the Commissioner may act to counter it. And counter any tax advantage that a person has obtained from a tax avoidance arrangement. This Interpretation Statement is also relevant to the general anti-avoidance provisions in section 76 of the Goods and Services Tax Act 1985. This Interpretation Statement also replaces the previous Interpretation Statement is 13 zero one issued on 13 2nd June 2013.

The statement sets out the Commissioner’s approach to applying section BG1 and then explains how under the related section GA1 the Commissioner may act to counteract any tax advantage that a person a obtains from a tax avoidance arrangement. The Statement is also relevant for the general anti avoidance provision in Section 76 of the Goods and Services Tax Act 1985. It replaces the Commissioners previous Interpretation Statement IS13/01 issued on 13th June 2013

For those unfamiliar with these provisions, section BG1 is the main anti avoidance provision in the Income Tax Act. If applicable it will void a tax avoidance arrangement for income tax purposes. The related section GA1 then enables the Commissioner to make adjustments where an arrangement voided under section BG1 has not “appropriately counteracted” any tax advantages arising under the tax avoidance arrangement.

The key case relating to these anti avoidance provisions is the Supreme Court decision in Ben Nevis Forestry Ventures Limited in 2008. In that decision the Supreme Court adopted the principle of Parliamentary Contemplation in determining how the anti-avoidance provisions were to be applied. In brief Parliamentary Contemplation requires deciding whether the arrangement when viewed as a whole and in a commercially and economically realistic way makes use of or circumvents specific provisions in a manner consistent with parliament’s purpose. If not, the arrangement will have a tax avoidance purpose or effect. Subsequent to the Ben Nevis decision this principle of Parliamentary Contemplation was applied in the well-known Penny and Hooper case, and again in the Frucor decision.

It would be foolish to think these tax avoidance provisions only apply to major corporates. as I’ve just mentioned the principles were relevant in the Penny Hooper decisions and at last week ATAINZ conference the point was made that section BG1 could be applied in circumstances where a person’s lifestyle appears to rely on payments and distributions from a trust because it is in excess of that person’s reported salary.

Just as an aside, apparently in March 2021, almost $11 billion in dividends were paid prior to the increase in the top personal tax rate to 39%, with effect from 1st of April 2021. Now, that is more than four times greater than the usual amount of dividends paid at that time of year. I understand Inland Revenue is discussing the pattern of distributions with some tax agents.

The issue tax agents, advisers and clients should be aware of is where there is no regular pattern of distributions, even though profits were available, but suddenly there’s a very big distribution in this particular year. You could be vulnerable to Inland Revenue looking at that and saying, “Well, you paid a big dividend in March 2021, but you haven’t paid similar dividends in March 22 or March 23. Why is that? Nothing to do with the new 39% personal tax rate?” So just to reinforce these tax avoidance provisions, the case law may generally involve large corporates, but they are very relevant to small and medium enterprises.

Fortunately, there’s some good examples accompanying the Interpretation Statement and give you guidance as to where the Inland Revenue think the boundary might apply. For example, and this is a very common scenario, a company is wholly owned by a family trust. Over some years the trust has advanced $1 million to the company as shareholder advances on an interest free repayment on demand basis. The company has then used these funds to finance its business operations for the purpose of deriving assessable income.

The trustees decide to demand repayment of the full amount of the loan. In order to make that repayment the company borrows $1 million from a third-party lender at market interest rates secured over the assets of the trust. The $1 million loan is then used to repay the shareholder advances. The company deducts the cost of borrowing from its income. Meanwhile, the trustees have used the funds to purchase a holiday home for the trust’s beneficiaries.

As I said, this is a not uncommon scenario. But does it represent tax avoidance? No, according to the Commissioner. Which is a relief but be careful of relying on that particular set of circumstances, there may be a little twist in your tale, which may interest the Commissioner.

Another example is where a taxpayer with a marginal rate of 39% invests in a portfolio investment entity where the maximum prescribed investor rate is 28%. This would not constitute tax avoidance because the tax advantage of the maximum prescribed investor rate of 28% is within Parliament’s contemplation.

On the other hand, an example is given of an investor whose tax rate is 39%. He borrows funds from a bank to invest in a Portfolio Investment Entity (PIE) sponsored by the same bank. The policy of this PIE is to invest all funds in New Zealand dollar interest-bearing two-year deposits with the bank.

In this situation, this arrangement would represent tax avoidance. The key facts being the somewhat circular nature of the investment, but critically the fact the return is less than the cost of borrowing, resulting in a pre-tax negative, i.e. a loss position, but a post-tax positive net return. Once you look at the interest earned and the tax rate 28% tax rate, there’s a deduction available to the investor at 39% effectively. But the PIE income is only taxed at 28%.

This got me thinking because it suggests the well-known practice of negative gearing to purchase investment properties might in some circumstances represent tax avoidance. Now, this is less likely following the introduction of the loss ring-fencing rules and interest limitation rules in 2019 and 2021, respectively. But it’s another case where you ought to think carefully about how Inland Revenue might view a particular transaction.

As you can see, there’s a considerable amount of material and reading to work through including some useful flow charts (see below). At a minimum, I would suggest reading the Fact Sheet and the two Questions We’ve Been Asked which accompanied the Interpretation Statement.

You can also find some excellent commentary by the Big Four accounting firms. They’re always worth reading on these matters as they’ve got the resources to really go in and consider what these Interpretation Statements might mean. (And no doubt it’s particularly relevant for their clients).

Like some, I have my reservations about the Parliamentary Contemplation test. I think it was Rodney Hide who remarked about the principle “When I was in Parliament, most of the time I was contemplating what I was going to have for dinner”. Joking aside, I feel we should be approaching the test with some caution. I also think Justice Glazebrook’s dissent in Frucor raised valid concerns about how these provisions would apply. As I mentioned at the time, she comes from a very experienced commercial and tax background which is one reason why her dissent was raised a few eyebrows in the tax world.

Notwithstanding all of that, the Frucor and Ben Nevis cases are the law. And with the release of this Interpretation Statement and related material, taxpayers now should have a clearer idea where the boundaries lie. More examples from Inland Revenue around where they see the boundaries applying would be a great help in continuing to clarify the position. As always, we’ll bring you developments as they emerge.

Reimbursement for working from home

Now, moving on, we’ve discussed in the past how the impact of the pandemic and the resulting shift to more people working from home meant Inland Revenue had to quickly reconsider the treatment of reimbursing payments made to employees who work from home and for using their own phones and other electronic devices as part of their employment. Inland Revenue released a series of determinations giving some guidance as to the appropriate level of reimbursement.

Inland Revenue has just issued an updated determination which will, once it’s gone through consultation, apply from 1st April. It basically updates these previous determinations and gives a little bit more leeway in terms of the amounts allowed. The reimbursement allowance for employees working from home has increased from $15 per week to $20 per week. The previous limit of $5 per week for person use of telecommunications tools is now $7 a week. I feel these amounts are on the low side, but at least Inland Revenue is revisiting the matter and updating them to take account of inflation. So that’s welcome.

Jail for tax fraud

And finally this week news about convictions involving tax fraud. Firstly, a former developer who apparently lived in Manhattan before he migrated here in 2016 on an entrepreneur residency visa, has just been jailed for tax fraud relating to $1.5 million in fraudulent GST refunds. He had bought a vineyard in Canterbury and then filed fraudulent GST returns between April 2017 and April 2021 in relation to the purchase and operation of this vineyard. He received over $1.3 million in GST refunds, but a further $175,000 was withheld once Inland Revenue realised what was happening in April 2021.

He’s been jailed for a total of three years and seven months. One other thing of note is Inland Revenue has taken court action to recover what was fraudulently obtained. Unusually it also took a high court freezing order out and had a receiver appointed over the assets of the vineyard owning company. So good move from Inland Revenue. That’s what we expect them to be doing.

The case does raise an issue though, because it was four years before Inland Revenue detected this fraud. And so, again, you just wonder that hopefully this was because during this period it was going through its Business Transformation program. So, you would hope that now Inland Revenue, with its enhanced capabilities, is picking up on these frauds much quicker.

In a related release, five members of the Samoan Assembly of God Church in Manukau have been sentenced to community detention and ordered to repay the money they received after they made false donation tax credit claims worth almost $170,000. They apparently used not only false donation credits for themselves, but also asked other individuals, usually members of their own congregation for personal information, including their IRD numbers. They then using these details issued a series of false donation receipts. The fraud was detected by Inland Revenue and the five were charged. All have pleaded guilty and received various sentences mostly involving community detention but also reparations and repayment of the funds claimed.

I often see a lot of feedback around the charitable exemption particularly in relation to businesses. It’s a touchy point. One of the areas where the Tax Working Group had concerns was about whether the donations once received were actually being applied for charitable purposes.

Now, I don’t know whether this particular case is just one of those scenarios where Inland Revenue came across it and acted or it’s part of a general operation where it’s looking more closely at what’s happening with charitable donations and whether in fact, they’re being applied to charitable purposes. We’ll find out in due course.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Inland Revenue about to target 80,000 over incorrect Cost of Living Payments

What about a tax-free threshold?

Last week I discussed some of the submissions made on the latest tax bill and in particular the implications for persons providing accommodation through Airbnb or ride sharing via Uber or a similar app. Reading the comments to the transcript it appeared to me there is some confusion around these proposals. So, this week I thought I’d look at these proposals in a little bit more detail as I didn’t actually cover off the Taxation Annual Rates for 2022-23 Platform Economy and Remedial Matters) Bill (No 2) to give its full title at the time of its (re-)introduction.

The key part of the Bill is the platform economy sometimes also known as the digital marketplace. Now there are two parts to the proposals that are contained in the bill. The first, and what I think is relatively uncontroversial, is the implementation of an OECD Information and reporting exchange framework. This would require New Zealand based digital platforms to provide Inland Revenue with information annually about how much users of those platforms had received from relevant activities.

Inland Revenue would then use that information as part of its administration in the tax system. In other words, checking to see that people who receive payments have returned those payments. It would also share the information with foreign tax authorities where that information related to non-residents. This is intended to take effect from 1st January 2024.

Although this is still to be passed into law, earlier this week New Zealand was part of a group of 22 jurisdictions who signed a multilateral competent authority agreement for the automatic exchange of information under the OECD Model Rules for Reporting by Digital Platforms.

So that process is proceeding even as the legislation is passing through Parliament.

As I said, I think this is relatively uncontroversial. It is supported by the likes of the Chartered Accountants Australia and New Zealand. Interestingly, however, BusinessNZ was less enthusiastic about the proposals although I think it’s largely concerned about compliance costs.

It requested a delay in the introduction of the OECD based and reporting exchange framework, which isn’t going to happen because we’ve already signed the agreement to say we’re going to deliver it.

BusinessNZ also asked for Inland Revenue to undertake a quote, “clearer cost benefit analysis to ensure there was a clear understanding of the likely net benefit of the platform economy changes on the New Zealand economy”. That’s a little bit surprising but probably reflects BusinessNZ’s concerns about compliance costs.

However, it’s the second part of the proposal which generated most of the criticism and pushback from submitters that I referred to last week. The Bill proposes that the current GST rules on electronic marketplaces which apply to remote services and certain imported goods now be extended to “listed services”, which would include supplies of accommodation through Airbnb and other booking services, ride-sharing, beverage and food delivery services and services that are closely related with these services. These changes are intended to take effect from 1st April 2024. There’s a bit of lead time but it’s not that far off.

What these proposals are intended to address is an issue where some of the services provided would normally be subject to GST. But because they’re being passed through these electronic marketplaces, apps, that’s not necessarily happening. And a concern of Inland Revenue and the Government is …

“Ïf this was to continue, it could have adverse consequences for the long-term sustainability of the GST system and place traditional suppliers of these services who are charging and returning GST at a competitive disadvantage. It could also undermine New Zealand’s broad based GST system.”

You may recall that the Hospitality Association was one of those that supported the changes because of this risk.

What the bill does to address these concerns is require operators of electronic marketplaces such as Airbnb, Uber and the likes to become the deemed supplier of or for GST purposes where they authorised the charge for the supply of listed services to a recipient.

What will happen is the person who actually provides the services (what’s termed “the underlying supplier”, such as the driver or someone providing accommodation to Airbnb), would be deemed to have made a supply to the operator within the market electronic marketplace, i.e. Airbnb, Uber or other rideshare operator. That particular supply would be zero rated for GST purposes so that the underlying supplier wouldn’t be paying GST directly, but instead it would be the operator of the electronic marketplace who would be deemed to be supplier and making supplies of listed services of 15%.

Example 4: Listed services performed, provided, or received in New Zealand Charlotte is based overseas and is looking for accommodation in New Zealand for an upcoming holiday. She uses an electronic marketplace to book accommodation in a bach in Queenstown. Under the proposed amendments, as the accommodation provided through the electronic marketplace is in New Zealand, the marketplace operator would be treated as the supplier of the accommodation and would need to account for GST.

Now where the person who actually supplies the accommodation to Charlotte is registered for GST, then the transactions between them and the marketplace provider would be zero-rate for GST purposes.

But if that person wasn’t GST registered, there’s going to be something termed a flat rate credit scheme which requires the app or marketplace operator to pass on as a credit, a proportion of the consideration charged for listed services.

Example 8: Basic operation of the flat-rate credit scheme for marketplace operators Henry provides taxable accommodation through an electronic marketplace where the marketplace operator is responsible for collecting and returning GST on these supplies. Henry notifies the operator of the electronic marketplace that he is not a registered person for the purposes of the GST Act. Charlotte books accommodation that Henry provides through the electronic marketplace for $200 plus GST for the stay. The marketplace operator collects GST of $30 on the supply of the taxable accommodation that they are treated as making to Charlotte. Knowing that Henry is not a registered person, under the proposed amendments, the marketplace operator applies the flat-rate credit scheme and calculates: GST of $30 at 15% of the value of the supply, and the input tax deduction of $17 for the flat-rate credit at 8.5% of the value of the supply. The marketplace operator would be required to deduct input tax of $17 from the $30 of GST payable to Inland Revenue and pass on the $17 to the underlying supplier as a flat-rate credit. The marketplace operator would pay the remaining $13 to Inland Revenue, and this would be the net GST collected on the supply of the accommodation.

This example illustrates where I think BusinessNZ and some of the other submitters have a case about the potential complexities and compliance issues.

Notwithstanding these issues the critical point from Inland Revenue and the Government’s perspective is the proposals put everyone on a level playing field as far as GST is concerned. We will probably end up with more people registering for GST.

The net effect of this, according to the accompanying Regulatory Impact Statement, was about an extra $47 million in GST annually, but I’ve seen estimates that could run as high as $100 million. There is undoubtedly some complexity coming into the system, but I am of the view that in terms of business impact I don’t believe it’s going to be quite as harmful as submitters suggested. I think other factors like the state of the world economy are more important in that case. But we’ll watch to see how what happens with the submissions process.

The expected errors emerge

Moving on, we’ve covered in the past the controversial Cost of Living payments. It emerged this week as part of the annual review of Inland Revenue by Parliament’s Finance and Expenditure Committee that it considers between 70 and 80,000 people may have been incorrectly paid some or all of that $350 Cost of Living payment.

According to the new Commissioner of Inland Revenue, Peter Mersi at least 12,000 people were incorrectly paid the first tranche of $116.67 because of a “coding error”. Apparently, all these people had a negative portfolio investment entity balance, and as it was the only income they had they weren’t actually eligible. But somehow this wasn’t picked up in time.

And then, as been previously discussed, payments were made to others who had left the country but hadn’t apparently updated their details according to Inland Revenue.

Since the first payments went out on 1st August, Inland Revenue has been checking people’s eligibility and as a result, the number of payments made has fallen as they remove what they consider ineligible persons. The first payments on 1st August were made to 1,480,000 people. The second tranche on 1st September went to 1,422,000, and the final payments on 1st October went to 1,384,000. So over the time of the payments, 96,000 fewer people received a payment for the third instalment compared with the first instalment.

So far, 177 people have returned payments and Inland Revenue is about to contact up to 80,000 about potential overpayments.

Separately, there’s another 75,000 who haven’t received any of these payments, even though they aren’t eligible. And the reason they haven’t done so is they’ve yet to supply Inland Revenue with bank account number details.

Now, as I’ve said previously, I thought mistakes were inevitable given the scale of what was happening. I was more concerned about systemic coding issues where there seem to be groups of people that shouldn’t been receiving payments were reported as having received payments. And Inland Revenue has now acknowledged that one of those groups was this group with negative portfolio investment entity income.

I was also concerned about the fact that Inland Revenue estimated it would need somewhere between 750 and 1,000 staff to process the exercise. This bears out a concern I have about Inland Revenue being under resourced. I’m hearing stories that there’s a lot of overtime being carried out by Inland Revenue staff which indicates there’s still a potential staff resourcing issue. No doubt we will hear more about these payments, and we’ll update you on future developments.

Tax-free thresholds and where bracket creep hurts most

I’ve talked previously about a tax-free threshold. And this week, I and other several other tax advisers spoke to Susan Edmunds at Stuff about the idea.

Tax free thresholds are common overseas. Australia has an exemption for the first A$18,200. Britain has a personal allowance of £12,570 and France has an exemption of €10,225. But here in New Zealand as is well known, every dollar is taxed. And partly as a result of the cost-of-living crisis questions have been raised as to whether it’s time to change.

The Tax Working Group did quite a bit of work in this space and it’s my view, as I expressed to Susan, the time’s probably come for small exemption. I was thinking of in the order of $5,000, which was also the number the Tax Working Group landed on.

But the downside is such tax-free thresholds are expensive. For example if you were to exempt the first $14,000 of income, which is currently taxed at 10.5%, would cost $4.7 billion a year. So, there’s a significant trade-off involved.

And there’s another issue that the Tax Working Group identified, which is that a significant proportion of that benefit could also go to secondary income earners in households which were above the median income. Is that something we actually want?

Deloitte partner Robyn Walker talking to Susan Edmunds made the points ‘What are we trying to address here? Is a tax-free threshold the best tool to do so?’ I entirely agree with this. For example, if we’re talking about the cost-of-living, then maybe controversial or not, it may make more sense to consider specific payments, such as happened with the Cost of Living payment.

Robyn also discussed the idea with RNZ’s The Panel. One of the things she mentioned is that there’s a tool on the Treasury website where you can do your own modelling and calculate the effect of different changes to tax rates and you can see the cost of making changes to rates and thresholds.

But discussions around a tax-free threshold and changes to thresholds aren’t going to go away. And a particular point, both Robyn, myself and others keep making is that there’s a lot of pressure on the group earning between $48,000 and $70,000 where the tax rate jumps from 17.5% to 30%. In our view this is the group that probably needs most relief and where politicians should be focused on improvements.

The politicians are undoubtedly working in the background on this issue. National’s got its plan which is to index the thresholds. What Labour has got in the works, we don’t know, but I’m pretty certain they’re planning something.

A winning idea

Finally this week, congratulations to Vivien Lei, who is this year’s winner of the Tax Policy Charitable Trust Scholarship Award. Vivien is currently Group Tax Advisor with Fisher Paykel Healthcare. Her winning proposal was how to change New Zealand’s environmental practices by introducing an impact weighted tax regime. Under this model, organisations would be taxed on their net positive or negative impact on the environment. A very interesting proposal.

Now we’ve had past winner Nigel Jemson on the podcast and I’m very pleased to say that Vivien will be joining us before the end of the year to talk about her submission.

The Green Party quotes Margaret Thatcher with approval

The Australian Tax Office’s latest corporate tax transparency report

The latest from the OECD on the carbon pricing of greenhouse gas emissions

Last week, the Green Party released a discussion document on what it’s called an excess profits tax. This is part of its “commitment to a progressive and fair taxation system.” What it is saying is that an excess profits tax or windfall tax is required to level the playing field so that, “big businesses are not able to profit to excess when so many people are struggling”.

The proposal comes on the back of data showing that in the 2021 financial year, corporate profits reached $103 billion, up $24.5 billion on the previous year. And you’ll recall that the corporate tax take for the year to June 2022 was almost $20 billion. The Green Party are saying we’ve got several matters going on at the moment. It believes there are excess profits being earned at a time of hardship. There’s also a need to address the impact of the unprecedented transfer of wealth that happened in response to the COVID 19 pandemic.

The discussion document points out that windfall taxes are common in other countries. It notes that the EU is implementing an excess profit tax in the energy sector. Spain has an excess profit tax on the energy sector and banks. Interestingly, the paper then uses the example of Britain under Margaret Thatcher in 1981, when the Conservative government introduced a windfall tax on banks. This was raised the equivalent of about £3 billion in today’s money and represented about a fifth of the profits banks were pocketing at the time.

That obviously attracted quite a lot of controversy back in 1981. The 1981 British budget is one of the most controversial I can recall in my time. But Thatcher was unrepentant about what she did. In her memoirs The Downing Street Years, she responded

“Naturally, the banks strongly opposed this, but the fact remained that they had made their large profits as a result of our policy of high interest rates rather than because of increased efficiency or better service to the customer.”

So, I guess we live in strange times when the Green Party is quoting Margaret Thatcher with approval, but that is a fair point. And bear in mind ANZ reported a net profit of $2 billion for the first time.

So, windfall taxes are not uncommon elsewhere in the world. They are uncommon under the New Zealand tax framework and haven’t really been used for a very long time. They were used during both world wars but apparently, they weren’t entirely successful.

It’s good to get this discussion going because sometimes I feel that the tax debate in New Zealand is very narrowly circumscribed. We’re living in unusual times so is a windfall tax something that could be done? Even if it was, in my view it would have to be a one-off, such taxes shouldn’t be part of the regular tax take. Incidentally, this is a point I’ve seen discussed elsewhere notably in Ireland following the release of a report about its tax system.

The Green’s proposal suggests a windfall tax could have some retrospective effect. This would be highly unpopular and rightly so, for companies, because it would mean there’s no certainty around their planning. Companies might budget for a 28% tax rate but then suddenly find that in fact it’s been increased to 33%. So businesses would find that hard to deal with, but if they knew there was a possibility it would be interesting to see how pricing might play out.

Overall it’s good to see this discussion going on and no doubt it’ll attract a lot of controversy and you can make your own submission on the idea to the Greens. Next year is an election year so who knows what’s going to happen afterwards? But as I said, windfall taxes are used elsewhere in the world. And if they were good enough for Margaret Thatcher, well, who knows?

Aussie ‘transparency’

Moving on, over in Australia, the Australian Tax Office, (the ATO) has just published its eighth annual report on corporate tax transparency. What this does is look at the amount of tax paid by large corporates for the year to June 2021. According to the report, the over A$68 billion paid during that year by large corporates is the highest since reporting started. It’s up A$11 billion or 19.8% on the previous, COVID-19 affected year. Apparently, rising commodity prices were a key driver for the increase in corporate tax.

The report notes that Australia has some of the highest levels of tax compliance of large businesses in the world, with 93% of tax paid voluntarily. This rises to 96% after the ATO has asked a few questions.

The ATO has been running what it calls the Tax Avoidance Taskforce for some time. According to the report since 2016, the ATO has raised tax liabilities of $29 billion and Tax Avoidance Taskforce funding being responsible for $17.2 billion of that amount. (It’s worth remembering “raised liabilities” doesn’t necessarily mean that they’ve been collected). In last week’s Australian Budget there’s an extra $200 million per annum to help expand the focus of the Tax Avoidance Taskforce. This brings the total funding for the Tax Avoidance Taskforce to A$1.1 billion over the next four years.

Now, this report covered 2,468 corporate entities, more than half of which were foreign owned with income of A$100 Million or more. 529 or about 20% were Australian owned private companies with an income of $200 million or more, which is an indication of the size and scale of the Australian economy. Interestingly, there’s a note that the percentage of entities which pay no income tax was 32%.

It’s interesting to see what other jurisdictions do with their tax data. I feel Inland Revenue should do a lot more in this space with the data it receives, but it’s very reluctant to do so at this point. It’s currently not part of its brief, but such a report and other statistics gives us a better understanding of the scale of the economy and what’s happening in it. I would like to see Inland Revenue produce something similar.

Energy, taxation and carbon pricing

Finally, this week, overnight the OECD released its latest report on pricing greenhouse gas emissions. This looks at how carbon prices, energy prices and subsidies have evolved between 2018 and 2021. This is part of a database the OECD is developing to track what’s happening on energy, taxation and carbon pricing.

This report covers 71 countries (including New Zealand) which together account for approximately 80% of global greenhouse gas emissions and energy use. There’s a summary report by country as well. Overall, more than 40% of greenhouse gas emissions in 2021 were covered by carbon prices and that’s up from 32% in 2018. And the average carbon price from emissions trading system schemes and carbon taxes more than doubled to reach €4 per tonne of CO2 equivalent.

And obviously the report goes into what’s happening across the across the globe. There’s been a rise in the amount of greenhouse gas emissions now covered, and that is as a result of the introduction or extension of explicit carbon pricing mechanisms notably in Canada, China and Germany.

What’s termed carbon net prices are rising further in 2021 as have permit prices under emission trading schemes. There’s steady changes in carbon taxes, with new carbon taxes introduced, together with increases in carbon tax rates or the phasing out of carbon tax exemptions.

As for New Zealand, 44.1% of all greenhouse gas emissions are now subject to a positive ‘Net Effective Carbon Rate’ which has not changed since 2018. The report also notes that fuel excise taxes, which are described as an implicit form of carbon pricing cover 23.8% of emissions. Again, that’s unchanged since 2018. So, looking at this, we appear to be stalling a bit on this and I do wonder whether next year’s report might show that because of the cut in fuel excise duty, we’ve gone backwards. However, other countries have also been cutting fuel taxes because of the high inflation in the wake of the war in Ukraine.

Although the level of coverage of greenhouse gases covered by carbon pricing hasn’t changed since 2018, the average carbon price has risen. For example, fuel excise taxes in 2021 amount to €19.73 per tonne of CO2 equivalent. That’s up by +9.4% relative to 2018, which is probably below inflation, though. However, once adjusted for inflation the average Net Effective Carbon Rate on greenhouse gas emissions has increased by +39% since 2018

There’s a lot to consider in this report, more than I’ve had a chance to go through right now. But again, it reflects a constant theme of this podcast about the increasing role of environmental taxation and the scope for opportunities in this space.

What we do with those funds is the other side of the equation. It’s one thing to say we need more taxation. What isn’t always debates is what we do with those taxes. I’ll repeat my longstanding view that funds coming out of environmental taxation in the form of new taxes or the existing emission trading scheme should be used to mitigate the impact of climate change.

There was a report earlier this week identifying 44 communities in great risk of environment impact from climate change which are unprepared for the flood risk. No doubt they will be looking for assistance. In the meantime, Nick Smith, Nelson’s new mayor (and former Environment Minister) has requested government assistance with dealing with the impact of the recent flooding. No doubt there will be plenty more to come on this topic.

This week we take a close look at Inland Revenue’s Annual Report for the year ended 30th June 2022. It begins with an overview of how Inland Revenue “has contributed to the well-being of New Zealanders”. There’s a summary of the highlights and key results for the year including a summary graphic illustrating the composition of the $100 billion of tax revenue raised during the year and the areas in which it was spent. The highlights note that Inland Revenue exchanged financial account information with more than 70 countries and has information sharing arrangements with more than 17 agencies. This is something that people always need to keep in mind just how much information Inland Revenue has access to and how much it shares.

The overview declares “we interact with a range of customers on tax and provide payments that are critical to people’s wellbeing.” You’ll note the use of the word “customers”. In fact, “customer” or “customers” is used over 660 times in the report, compared with a mere 30 mentions of “taxpayers”.

I have great reservations about describing taxpayers as customers. I can appreciate there are some benefits from this approach in terms of helping Inland Revenue staff understand the need to provide better service to taxpayers. But the repeated use of the term customers implies a voluntary transactional relationship and ignores the power dynamic. Actually, tax is compulsion. We are compelled to pay tax and we can’t exactly say to the Inland Revenue, ‘Your service is terrible. I’m switching providers to the Australian Tax Office’.

Whatever the description, Inland Revenue considers it’s dealing with three groups of customers; individuals, families and businesses. This, however, overlooks the important role of tax agents who interact with Inland Revenue on behalf of these groups daily. However, tax agents are only mentioned nine times throughout the whole report. It’s a long-standing complaint of myself and other tax agents that the Business Transformation process underestimated the important role of tax agents in enabling the smooth running of the tax system. Accidentally or not this summary of who Inland Revenue sees as its customers rather reinforces our point.

Anyway, moving on, the next section within the report expands on Inland Revenue’s story for 2021-2022 outlining the benefits of its transformation of the tax and social policy system. After a brief look at the year ahead, we then get into the detailed analysis of how Inland Revenue performed against key measures and indicators, its organisational capability, and finally the departmental financial statements. Lots of juicy stuff here, in fact too much for one podcast.

Inland Revenue’s major achievement for the year is the completion of its Business Transformation programme, which was officially closed on 30th June this year. The project was completed on time and under budget and as a result, Inland Revenue is on track to save $100 million in administration costs annually. Furthermore, at the end of the Transformation Project, Inland Revenue handed back $458 million to the Crown. The programme was initially budgeted at $1.5 billion and came in at just over $1 billion. Given the notorious history of some I.T. projects such as Novapay, this is a significant achievement. So well done, Inland Revenue.

Business Transformation, of course, has enabled Inland Revenue to proceed with its auto-assessment process. As the report notes, previously, approximately 1.4 million people who were potentially eligible for a tax refund never applied. This year tax refunds were sent to 1.65 million taxpayers and as of 30th June, $602 million had been refunded. Apparently, it now costs on average $1.35 to process a tax return, compared with $2.33 back in 2015-2016. So that’s a significant improvement.

Business Transformation has also meant that many taxpayers now use Inland Revenue myIR portal to communicate with Inland Revenue and handle their tax affairs. There were over 60 million user sessions in the June 2022 year, and that’s a growth of 140% since 2019. Overall, 80% of taxpayers say they find it easy to deal with Inland Revenue, which is about the same as last year.

Although Inland Revenue encourages the use of its digital platform, it is aware that not everyone has ready access to computers. It’s good to see that this year it has been working with the likes of the Citizens Advice Bureau to ensure that those who are at risk of being digitally excluded always have a chance to engage with Inland Revenue. That’s something to be applauded and we hope that will continue.

There’s some interesting commentary on the impact of Business Transformation for small businesses. The report notes that approximately 90% of businesses in Aotearoa New Zealand have five or fewer employees. Inland Revenue’s hope was that this group would especially benefit from Business Transformation. However, the compliance effort for this group has not reduced as much as Inland Revenue had hoped.

According to an Inland Revenue survey in 2021, SMEs said they spend an average of 31 hours a year on meeting their tax obligations. Now, this is five hours fewer than in the survey’s baseline year of 2013. But the introduction of mandatory pay day finding from 1st April 2019 means that businesses spend as much time complying with PAYE obligations now as they did in 2013. Overall, though, 60% of small business owners felt that the time their business spends on tax matters was acceptable and that’s up from 55% in the previous survey.

The core role of Inland Revenue is the collection of tax. And this is the first year the total tax take has exceeded $100 Billion, up 7.3% on 2021. However, the overall amount of tax debt increased by 10.5% to $4.8 billion at 30th June 2022. And there are some concerning numbers in here. As of June 2022, 55,888 people who received Working for Families were in debt, which is a 27% increase on the June 2021 year.

Overdue student loan debt has also increased by 17.6% to $2 billion. This is apparently mostly due to only 24.5% of the overseas based student loan borrowers making their required repayments this year.

Inland Revenue wrote off $688 million of debt during the year. That’s down from the $812 million written off in 2021. Write offs of GST and individual income tax debt made up 58.8% of that total value.

Now the report admits that “The total amount written off is lower this year, due in part to Inland Revenue prioritising COVID-19 support work over proactive debt collection work.” The report then notes that “overdue tax debt grew at a comparable rate to tax revenue. It was 4.6% of tax revenue, compared to 4.5% in 2020–21 and 4.5% in 2018–19. This is a good result, considering how difficult the environment has been.” That’s probably fair comment. Inland Revenue has had to deal with an enormous amount of other projects such as the COVID 19 Resurgence Support Programme as well as getting ready for the cost of living payments, which happened after the end of the year.

But what action is it taking about trying to collect all this debt? Well, during the year $2.38 billion of debt was put under instalment arrangements involving approximately 120,000 taxpayers. As of 30th June, $491 million has already been repaid in full. And it’s then also started a programme in November 2021 targeting those with bigger debts. This involves around 1,350 businesses with debts totalling $356 million. And that’s apparently generated about $90 million of repayments so far.

It also pulled out the big stick and commenced the liquidation process against 759 companies, resulting in 163 companies being liquidated through the High Court. Another 592 companies went into liquidation, owing tax debt after the Inland Revenue initialised the process. Now some of these liquidations are inevitable, to be frank. Although Inland Revenue is trying to work hard in this area I definitely think there’s room for further improvement.

One of the key metrics I’m always interested in is Inland Revenue investigations activity. There’s an admission that it …

0 of 15 secondsVolume 0%

“…didn’t undertake as many interventions as usual as we didn’t want to put more pressure on customers during a difficult year. We paused some investigation activity and focused on ensuring the integrity of our COVID-19 support products.”

Consequently, Inland Revenue only met one of its four measures for investigations category. Whereas last year it achieved three out of four.

One measure is the ‘Percentage of customers whose compliance behaviour improves after receiving an audit intervention.’ The target is 85% but the actual measurement achieved this year was 69.6%. I don’t quite know how they’ve measured that, but it’s a little bit concerning because pretty much my experience is if someone from Inland Revenue turns up and there’s an audit, behaviour generally improves afterwards. I think this measurement may be a by-product of overdue debt existing.

On the other hand, it did meet the measure for ‘Discrepancy identified for every output dollar spent.’ Now the target is $7 per dollar but Inland Revenue achieved a return of $9.88. “We have assessed additional tax or protected the integrity of the tax system to the value of $1.12 billion. This has exceeded expectations.” Although I find the phrasing of that a little opaque.

Intriguingly, that measure has been retired and is not being used in the current year. I’m not sure why, but we will watch with interest as we won’t know what the new measure is until next year’s report is released.

As part of its usual compliance activity Inland Revenue ran a number of compliance campaigns for specific sectors and compliance issues. For example, it ran campaigns about tax residency, disclosing offshore income and basically ensuring people meet their international tax obligations. According to the report, these campaigns targeted some 7,000 taxpayers and their tax agents and resulted in voluntary disclosures totalling $100 million in omitted income in the past two years. That’s not $100 million of tax, the best-case scenario would be maybe $40 million of tax. But anyway, still a good return for Inland Revenue.

I think we can see more of this campaign. Inland Revenue, as I mentioned earlier, shares information with 70 countries. This is an area it was starting to pay attention to before the Pandemic and is now returning to this area with the launch of a new offshore tax programme in June 2022. So, watch this space.

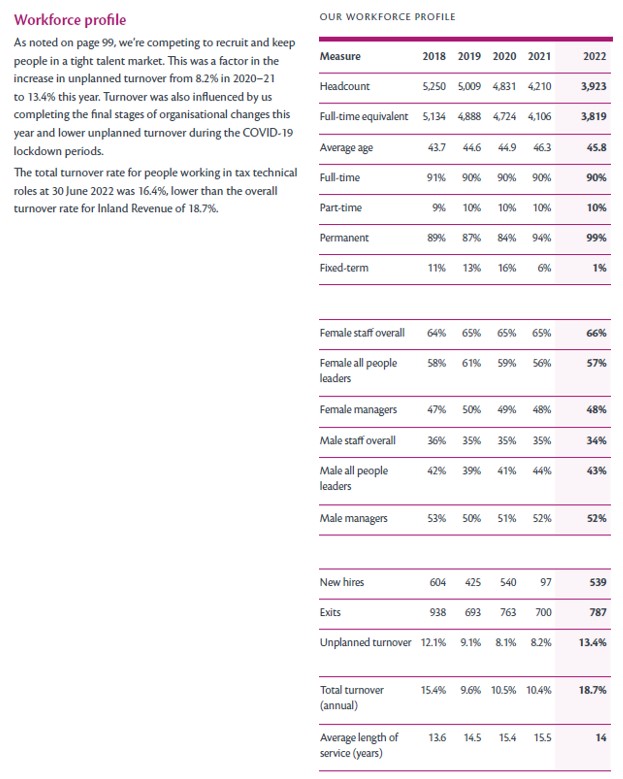

Now the key to any organisation is its people. And Inland Revenue has been through a massive amount of change in the past five years. As of 30th June, its workforce is now 3,923, which is down 1,327 or 25% since June 2018.

During the year, 787 people left Inland Revenue and it hired 539. Over the past five years, some 3,881 people have left Inland Revenue, which is 74% of the workforce as of July 2017. That is a massive churn and I have concerns about that.

The average length of service in years has dropped this year to 14, compared with last year’s 15.5 years. A lot of people have left and Inland Revenue’s staff turnover this year was 18.7%. Rather worryingly, the total turnover rate for people working in tax technical roles at 30th June 2022 was 16.4%. Although that’s lower than the 18.7% for the whole organization, it is well up on last year’s 1.3%.

Inland Revenue staff are actually very highly valued outside the public sector. My understanding is Inland Revenue is pretty competitive on wages. Seeing so many gamekeepers turning into poachers is not something we really should see. hence my concerns about what’s going on.

Page 100 onwards in the report looks at the state of morale and health in the report in Internal Revenue, and it’s very mixed. Some of the metrics are better than the public service generally. For example, 96% of staff can work remotely, which is well above what the rest of the public sector.

The report has a breakdown of employee ethnicity and the proportion of roles held by people with different ethnicities. Now, actually, Inland Revenue pretty much reflects the diversity of modern-day Aotearoa. 66% of its staff are European, compared with 70% of the population generally, 12% are Māori, which is below the 16.5% of the general population.

A bit more concerning though is looking at the proportion of leadership roles. When you get up to senior management, 96.4% are held by Europeans. Even the team leader and general management roles are all over 80%. So, there’s work to be done there.

But something which really caught my eye and is a matter that needs to be discussed more widely is a disclosure under Schedule 6 of the Public Service Act 2020. This requires Inland Revenue to report on situations where the Commissioner has delegated any of the Commissioner powers outside the public service. In other words, it said to people, ‘You can act in our capacity’.

In previous years the disclosure has involved Westpac and Callahan Innovation. But this year, for the first time, it includes Madison Recruitment Ltd. The disclosure reads

“Inland Revenue engaged Madison Recruitment Ltd to provide contingent labour to help with the introduction of the Cost of Living Payment and to provide additional support with other specific tasks due to the ongoing impact of COVID-19. The first Madison personnel began undertaking their engagement in June 2022. To enable the Madison personnel to fully undertake the engagement, the Commissioner delegated some powers to those Madison personnel. This delegation has been operating as intended in line with the contractual arrangements with Madison Recruitment.”

I have major reservations about this because it shows that Inland Revenue is perhaps under-resourced if it is taking on temporary labour. I don’t believe an organisation such as Inland Revenue with the powers available to it, should be taking on temporary contract labour. I can see there might be a business case for doing so, but as I said earlier there’s an issue with mounting overdue debt and the drop off in investigations activity.

We also have this staff churn that’s going on at Inland Revenue. Losing 75% of your workforce over five years, is not something I think is healthy for an organisation. Staff changes are inevitable and healthy. But 75%, I’m not so sure about that. So, this one of the major concerns I have coming out of this report.

Summing up the report is a mixture of the good, the not quite so good and the concerning. One of the not quite so good is a rather bumpy relationship with the tax agents, as I mentioned previously. But I understand the new commissioner Peter Mersi has been meeting with representatives of the professional bodies and no doubt this point has been discussed. In fairness, the ongoing huge challenge of dealing with a pandemic and its aftermath have not helped.

My great concern is the level of staffing and the state of morale at Inland Revenue. As I mentioned, there’s been considerable turnover of staff in the past five years, and I don’t believe the delegation of powers to Madison Recruitment is acceptable. I think it threatens Inland Revenue very well-deserved for reputation, for privacy and security of taxpayer information. It may be a temporary measure in order to help handle the Cost of Living payments, but judging by the report overall, I think Inland Revenue should be consider whether its current staffing levels are sufficient.

Overall, I would give Inland Revenue a pass mark for what has been another difficult year. The impression I have is an organisation right now in transition and under understandable stress. It could not have handled the many COVID-19 related issues it’s faced in the past two years without the benefit of Business Transformation. So, getting that project finished on time and under budget is a massive achievement. At the same time, the Pandemic and the continuing cost of living crisis has pointed to some ongoing weaknesses, which I think the new Commissioner will need to address urgently. We will be watching with interest.