2 May, 2022 | The Week in Tax

- Minister of Revenue philosophises on tax and proposes a Tax Principles Act

- The IRS drops the ball

Transcript

Ministers of Revenue typically deliver several speeches during the year, mostly to business audiences or at the start of tax conferences.

On Tuesday, however, the Minister of Revenue, David Parker, delivered a speech at Victoria University Wellington entitled Shining a Light on Fairness in the Tax System, which is without doubt one of the most interesting speeches made by any Minister of Revenue in many years.

After some scene setting about the purpose of tax and how the Government has been able to use tax revenues to fund its COVID 19 response, Parker then pivoted to talk about beginning what he called a fact-based discussion. He started by challenging the assumption that our tax system is progressive overall.

“What’s hidden that the effective marginal tax rate for middle income Kiwis is generally higher than it is for their wealthiest citizens. Indeed, some of their wealthier Kiwi compatriots pay very low rates of tax on most of their income.”

The Minister then dived into the question of the lack of data on the distribution of wealth and capital income in New Zealand. He highlighted the fact that according to the Household Economic Survey, the highest net worth ever reported was $20 million.

This was, he said, ridiculous, given that we know there are billionaires in the country. As he pointed out, that meant the National Business Review’s annual rich list is a better set of data than the official statistics. In fact, that’s quite common around the world as statistics on capital wealth are rare and rich lists are often used to help revenue authorities gather data in this area.

So this lack of data, Parker explained, was the rationale behind the powers granted to Inland Revenue for the purposes of conducting research into high wealth individuals. As listeners will know, this is a somewhat controversial project, even though the Minister repeatedly stated that the intent was to gather better data for research and not as had been accused, so Inland Revenue could secretly work on new taxes.

“Until we have a much more accurate picture about how much tax the very wealthy pay relative to their full “economic income”, we can’t really we can’t honestly say that our tax system is fair.” And this led on to the most surprising part of the speech his proposal for a Tax Principles Act.

He referenced four principles of taxation that Adam Smith set out in Wealth of Nations back in 1776. And he noted that the many tax working groups and other reports that New Zealand has had over the past 40 years, such as the McCaw Review in 1982, the MacLeod Review in 2001, the most recent tax working group, and the all the work that went on during the Rogernomics period all basically followed these four principles set out by Adam Smith.

“They all endorse the same principles, based in that most core value of New Zealand – fairness. The main settled principles are:

Horizontal equity, so that those in equivalent economic positions should pay the same amount of tax

Vertical equity, including some degree of overall progressivity in the rate of tax paid

Administrative efficiency, for both taxpayers and Inland Revenue

The minimisation of tax induced distortions to investment and the economy.”

He also noted that recent reviews in the UK and in Australia both adopted similar approaches. Incidentally and perhaps not coincidentally here, Deborah Russell and I adopted the same principles when we wrote Tax and Fairness back in 2017.

And as you know, Deborah is now the Parliamentary Under-Secretary for Revenue and David Parker’s number two. The proposal is that officials should periodically report to ministers on the operation of the tax system using the principles as the basis for the reporting.

The Tax Principles Act would sit alongside existing legislation, such as the Public Finance and Child Poverty Reductions Acts, which also require the Government and officials to report on specific issues. This is quite revolutionary, but in a way sits within the philosophy of open tax policy that New Zealand has adopted through what we call our generic tax policy process.

This open approach to developing tax policy is widely regarded as world leading by other jurisdictions. The proposed Tax Principles Act is not inconsistent with the existing approach. The intention is there will be consultation later this year and following that a bill would be introduced once the principles had been agreed and the reporting requirements had been established.

The resulting bill would be enacted before the end of the current parliamentary term, i.e. just in time for next year’s election. The proposal caused quite a stir and there’s plenty of good reading on it. Bernard Hickey has a very good summary of the matter.

It’s also quite rare certainly to see Ministers of Revenue philosophise in quite a public way. David Parker referenced Thomas Piketty’s seminal work, Capital in the 21st Century. He also acknowledged the very regressive nature of GST. Somewhat controversially he noted that because GST in transactions between GST registered businesses essentially zeros out and is a final tax for those who are not GST registered, it many ways it falls on labour earners.

As he put it, “GST is really paid out of our earnings when we spend it. In economic terms, GST is mainly a tax on labour income. Who pays that cost?”

The Minister noted we have limited data on the overall rate of GST paid by New Zealanders, either by income or wealth decile. So he’s asked Inland Revenue to gather data and to provide feedback on this. I suppose from a political viewpoint this hints that potentially if there are changes to a tax mix at a later date, something may be done in relation to GST as it impacts lower income earners.

All this kicked up quite a stir. When I appeared on Radio New Zealand’s the Panel following the speech, the panellists expressed some shock about the fact that we don’t really have data about how wealthy people are. I think the reason for this, which wasn’t discussed by Minister Parker, is that it’s probably largely the unintended consequences of the abolition of stamp duties, estate and gift duties, and the absence of a general capital gains tax.

In other jurisdictions which have some or all of those taxes, this gives a reference point when a transaction occurs as to what wealth is held and by whom. Incidentally, the disclosure requirements regarding trusts I discussed last week although they are primarily an integrity measure, they also represent, in part, an attempt to gather some data about wealth held in trusts and help fill the gaps in Inland Revenue knowledge.

With National and Act already putting out their tax proposals, it looks like tax will feature quite heavily in next year’s election. So it’s very much a case of let’s watch this space.

Moving on, today is the due date for submissions on Inland Revenue’s discussion document, Dividend Integrity and Personal Services Income Attribution. This contains a couple of controversial proposals.

Firstly, that sales and share of shares in a company with undistributed retained earnings would trigger a deemed dividend.

And secondly, changes to the personal services income attribution rules, which would mean more income would be attributed to a primary income earner.

Now, neither of these proposals have gone down particularly well and to describe them as controversial would be a bit of an understatement. The personal services attribution rules, in fact, may well have a very much wider effect politically than the Government might want to see.

Brian Fallow, writing in a very good column in last week’s New Zealand Herald, pointed out that the attribution rules, if enacted, would affect very large numbers of small businesses quoting former Inland Revenue Commissioner Robin Oliver “It is likely to catch tradies — a plumber, say, or a landscape contractor — with a van and some equipment and just themselves or one employee doing the work,”

And Oliver raised the question, is this really appropriate? I expect a lot of submissions on this paper, and I urge you to do so because as you can gather from comments made by Oliver, it could have a quite potentially significant impact for the SME sector.

I personally think the proposals go too far. And incidentally, one of the reasons that the proposals have been made comes back to a longstanding topic in this podcast and something that wasn’t directly referenced by Minister Parker in his speech, the absence of a general capital gains tax.

Inland Revenue proposes any transfer of shares by a controlling shareholder to trigger a dividend where the company has retained earnings. In jurisdictions which have capital gains tax, that transaction is normally picked up as a capital gain. But as we don’t have a capital gains tax Inland Revenue is proposing a workaround which I don’t think is appropriate one.

I think there are other alternatives they might want to consider. The proposals on the personal services attribution rules are an integrity measure. They build on the Penny Hooper decision relating to surgeons from ten years ago.

They are understandable, but I believe go too far and are probably targeting the wrong group of people. Moving on Inland Revenue has a useful draft interpretation statement out considering what is the meaning of building for the purpose of being able to claim depreciation.

This has actually become quite relevant because back in 2011 the depreciation rate on buildings was reduced to zero. But in 2020, in the wake of the pandemic, the depreciation rate for long life non-residential buildings was increased from 0% to 2% if you use a diminishing value basis or 1.5% if you’re using straight line method.

What this draft interpretation statement explains is the critical difference between residential and non-residential buildings. it replaces a previous interpretation statement released in 2010 which has had to be updated following an important tax case in 2019 involving Mercury Energy.

A building owner will be able to claim depreciation for a ‘non-residential building’ and that can in some cases have some residential purposes. Generally, it’s aimed at commercial industrial buildings and certain buildings such as hotels, motels that could provide residential commercial accommodation on a commercial scale. It’s a useful explanation and comments on the draft close on 2nd May.

Chump change for FATCA

And finally, a quite extraordinary story from the United States, where it has emerged that a very important tax act, the Foreign Account Tax Compliance Act, better known as FATCA, hasn’t generated as much income as was expected when it was introduced in 2010.

The projection was that over the ten years to 2020, it would raise about US$8.7 billion US. The US equivalent of Inland Revenue, the Internal Revenue Service, (the IRS) spent US$574 million implementing FATCA. But according to a report just released, all the IRS can show for all that money invested are penalties totalling just US$14 million.

Now, that’s quite extraordinary. And this is important from a New Zealand perspective, because FATCA represents a huge compliance burden for all US citizens who are required to file tax returns, even if they may be tax resident in another jurisdiction.

FATCA was the template for what became the Global Common Reporting Standards on the Automatic Exchange of Information. The rest of the world looked at FATCA and thought, “That’s a good idea. We’d like to have some information about what overseas accounts our taxpayers have”. And so, the CRS, as it’s known, was introduced and has been in force now for about four years.

I would hazard a guess that Inland Revenue probably gathered well in excess of US$14 million as a result of the introduction of CRS. But to come back to a point that David Parker made about politics and tax being inseparable. One of the reasons that the IRS has done so badly is that the Republican controlled Congress won’t give it the money to do its job. And that situation doesn’t look likely to change.

As David Parker said, politics and tax are inseparable. And we’re going to hear plenty more about the two in coming months.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

26 Apr, 2022 | The Week in Tax

- Higher interest rates on unpaid tax

- Extended reporting requirements for trusts

- The potential New Zealand tax implications of a British political scandal

The Official Cash Rate was increased last week, but Inland Revenue seems to have pre-empted the effects of an increase as two weeks ago it announced that the interest rate for use of money interest on unpaid tax and for the prescribed rate of interest for fringe benefit tax purposes would increase from 10th May.

The use of money interest rate on unpaid tax will rise from 7% to 7.28%, and the prescribed rate of interest for fringe benefit tax purposes will rise from 4.5% to 4.7%, with effect from the quarter beginning 1st July 2022. The use of money interest rate for overpaid tax remains at zero.

With the final provisional tax payment for the March 2022 income year coming up on 9th May, it’s a good time to ensure that your Provisional Tax payments are as accurate as possible to minimise the effect of this use of money interest. That’s particularly true where a taxpayer’s residual income tax for the year is expected to exceed $60,000. So right now, advisers like myself are looking at this situation and making sure clients are getting ready to make the payments they need to minimise any potential interest charge.

As we’ve discussed previously tax pooling is a useful tool in dealing with tax payments. And right now, people are making use of tax pooling not only to get ready for the Provisional Tax payment coming up, but we’re also wrapping up the final tax payments due for the year ended 31 March 2021. There will be people who haven’t paid sufficient tax for the year and could be looking at substantial use of money interest and maybe even related late payment penalties.

This is therefore a good time to make use of tax pooling intermediaries. Typically, the deadline for making a request to use tax pooling is 76 days after the terminal tax date for the relevant taxpayer. If the taxpayer has a 31 March balance date and is linked to a tax agent, that is typically 7th of April, which means that sometime in mid-June is the final date for payment. If they’re not linked to a tax agent the terminal tax due date was on 7th February and therefore they’ve only got a few days left to make that payment using tax pooling.

What’s happened is that in the wake of the Omicron wave, Inland Revenue have used the discretion that was given to them when the pandemic broke out to extend the deadline for the time in which a request for making tax pooling can be made.

That time has now been extended to the earlier of 183 days after a terminal tax date or 30th September this year.

There are a few conditions. The contract must be put in place with the tax pooling intermediary on or before 21st June. Furthermore in the period between July 2021 and February 2022, the so-called affected period, the taxpayer’s business must have experienced a significant decline in actual predicted revenue as a result of the pandemic. This meant they were unable to either satisfy their existing commercial contract with tax pooling intermediary or weren’t able to enter into one, or they’ve had difficulties finding the tax return because either they or their tax advisor was sick with COVID.

Now this is a good use of the discretion available to Inland Revenue. But remember, it is COVID 19 related. So if you just happen to have been caught off guard and didn’t make your payments on time, you’re not going to get this additional extension of time. Tax pooling is a very useful tool which you should make use if you can.

But if you can’t, talk to Inland Revenue and make them aware that you have issues. You’ll find that they are more approachable in this than people might expect and can be quite fair so long as you come to the table with a reasonable offer.

Trust compliance just got more expensive

Moving on, we’re now starting to prepare tax returns for the year ended 31 March 2022. And for this year, the required reporting requirements for domestic trusts have been greatly increased following a legislative change last year.

In connection with that, Inland Revenue has released Operational Statement OS22/02, setting out the new reporting requirements for domestic trusts. These reporting requirements were introduced to gather further information from trustees so Inland Revenue can “gain an insight into whether the top personal tax rate of 39% is working effectively and to provide better information and understand and monitor the use of trust structures and entities by trustees”. It’s what we call an integrity measure.

There is a hook in that the legislation is also retrospective as it enables Inland Revenue to request information going back as far as the start of the 2014-15 income year.

The Operational Statement is a pretty detailed document, setting out over 48 pages the obligations involved. There’s a very useful flow chart on page 6 setting out what trusts will be caught under the provision and required to make the relevant disclosure disclosures. The basic rule is that all trustees of a trust, other than a non-active complying trust, who derive assessable income for tax year must file a tax return and therefore will be subject to the reporting requirements.

Non-active complying trusts are not required to file tax returns. These are trusts receiving minimal income under $200 a year in interest, no deductions other than reasonable professional fees to administer the trust and minimal administration costs, such as bank fees totalling less than $200 for the year. Such trusts are not required to file tax return.

The trustees also need to file a declaration that it is a non-active complying trust, it’s not enough to be not required to file a tax return, it must also file this declaration. The types of trusts covered by this exemption are ones which may hold a bank account earning some interest. More generally, their principal asset is the family home and the beneficiaries are living in that place and are responsible for meeting the ongoing expenses.

For those trusts required to comply there’s a fair bit of detail involved. But fortunately, there is an option for what they call Simplified Reporting Trusts. These are trusts which derive assessable income of less than $100,000 or deductible expenditure, which is also less than $100,000 and the total assets within the trust at the end of the income year are under $5 million. Such trusts can use cash basis accounting and aren’t subject to the full accrual reporting requirements set out by the Operational Statement.

In addition to preparing detailed financial statements, there are several other requirements that the trustees are expected to provide to Inland Revenue. These include details of each settlor of the trust and each settlement made on the trust together with details of beneficiaries and distributions made to beneficiaries. The trustees must also provide details of who holds the power of appointment within the trust.

All this expands greatly the amount of reporting that trusts have to do now. And although typically you do see financial statements prepared for most trusts that do have to file tax returns, these requirements extend those reporting obligations. And I daresay many trustees aren’t going to be too happy about the increased costs that will come out of that.

And of course, we have this potential issue now, that Inland Revenue may request information going back as far as the start of the year ended 31 March 2015. There’s a fair bit of controversy around this measure which would certainly mean a lot more work for advisors and trustees.

A very British scandal that risks Kiwis

Now, over in the UK, the Chancellor of the Exchequer Rishi Sunak, the equivalent of Finance Minister Grant Robertson, is embroiled in a political scandal after it emerged that his wife, Akshata Murty, has been claiming non-domiciled status for UK tax purposes.

Non-domicile status means that a person’s foreign income and capital gains are generally not subject to UK income tax and capital gains tax unless they happen to be remitted to the UK. It so happens that Ms Murty’s father is the billionaire owner of an Indian IT company, and it’s estimated that she may have saved up to £20 million of UK income tax on dividends from her father’s company. Needless to say, it’s not a great look for Mr Sunak as the person responsible for managing the finances of the UK to find himself in that position.

But Ms Murty’s status as what is called a non-dom is actually quite common. Most New Zealanders living and working in the UK would qualify as non-doms and may be able to make use of this special status. The exemption is pretty generous. In fact, according to a University of Warwick research study, more than one in five top earning bankers in the UK has benefited from claiming non-dom status. Apparently a sizeable share of those earning more than £125,000 per annum have non-dom status. For example, one in six top earning sports and film stars living in the UK have claimed non-dom status. As these persons have got an average income of more than £2 million pounds per year it’s a pretty significant benefit.

Now what New Zealand advisers need to be watching out for is misunderstanding the complexity of these rules. It used to be the general rule that a non-dom’s income was not taxed in the UK if it wasn’t remitted to the UK. The opportunity was for New Zealand trusts to make distributions of income to UK resident beneficiaries, but never actually remit that income to the UK. Instead it stayed in a New Zealand bank account or some other non UK bank account and therefore wasn’t subject to UK tax rates, which could be as high as 45%. It also meant that the income distributed wasn’t taxed at the trustee rate of 33%, so it was a very nice, tax-efficient system.

However, the rules have been subject to a number of changes in past years, as political pressure has built on the question of whether these non-doms should get such generous tax treatment. I’ve seen a number of cases where advisers have continued to apply what they think the rules are, unaware that there have been significant changes to the use of non-dom rules and the remittance basis. They have therefore inadvertently created tax liabilities for not only for the UK resident beneficiary, but potentially also for the trust.

The UK has introduced a register of trusts and in some cases, New Zealand trusts may be required to be part of that register. Along with UK inheritance tax this is one of these ticking time bombs where there is a lot of people who don’t know what they don’t know and could be in for an unpleasant shock.

It’s also fairly highly likely in the wake of this political scandal that there may be more changes to come to the non-dom exemption so trustees with beneficiaries resident in the UK, should be very careful about making distributions to such beneficiaries in the mistaken belief they are trying to exploit a rule which has been amended. Generally speaking, the use of trusts in the UK and in particular distributions from foreign trusts to UK tax residents is a real minefield and great care is required to avoid potentially serious tax consequences.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time, kia kaha, stay strong.

11 Apr, 2022 | The Week in Tax

- Comparing New Zealand’s taxation of property with other countries

- OECD heralds a clampdown on crypto assets

- Another warning from Inland Revenue about attempts to manipulate income to avoid the 39% tax rate

Transcript

In last week’s Sunday Star Times, Miriam Bell looked at the question of how New Zealand’s taxation of property compares with other jurisdictions.

In doing so, she spoke to myself, Robyn Walker of Deloitte, and John Cuthbertson, the tax director for Chartered Accountants Australia and New Zealand. We all gave differing takes on the position.

According to the OECD statistics, we are near the bottom end of the range as a percentage of GDP. Including local government rates, New Zealand’s taxes on property for 2020 was approximately 1.9% of GDP and the total tax take for the year of 32.18% of GDP. By comparison, Australia’s taxes on property was 2.718% of GDP (2019 numbers), the UK was 3.855% and Canada 4.15% of GDP (both 2020 numbers).

As you can see, Canada and the UK are significantly above New Zealand. One of the reasons for this, as Robyn and John pointed out, is that they have a range of stamp duties that may apply. But also, as we all pointed out, all three jurisdictions, Australia, Canada and the UK, also have capital gains tax and in the case of the UK, inheritance tax may also apply on some properties on transfer.

The article provoked a fairly lively debate, as you would expect. The range of views across the board is that, yes, it looks like we’re under taxed. But the bright-line test is in place which is problematic in that although it looks like a capital gains tax, it doesn’t apply comprehensively, unlike in the other three jurisdictions.

Robyn Walker then made a very good point following through that the design of the bright-line test is basically all or nothing. If you hold property for more than 10 years, you’re outside the test, which means that you’re likely not to be taxed on it. So you get this wide variance in the tax effect of sales or property, which you don’t see to the same extent in other jurisdictions.

Robyn subsequently did a nice little post on LinkedIn, in which she looked at what would be the tax consequences in Australia, Canada, the UK, and New Zealand for the sale of a property which realised a $100,000 gain. Because we treat it as income, we’ll tax the full gain at the relevant marginal rate and for the purpose of the example that was 33%. Canada and Australia will tax only half the gain at the relevant marginal rate, although non-residents in Australia will be taxed on the full gain. And although the UK will tax the full gain the top rate applicable is 28%.

The end result was that if the bright-line test applied, then the tax payable in New Zealand would be highest relative to the other three jurisdictions. But if the bright-line test didn’t apply, then it was the lowest. In fact, it would be nil. And this reinforces Robyn’s point that it is a poorly designed test which can be very unfair in its application. You hold a property for nine years and 363 days, you’re taxed. Hold it for 10 years and one day you’re probably not.

The point I stressed in the article is that we want to look at broadening the range of taxation, and it’s fair if we do so because we start to get round these arbitrary distinctions. As I’ve previously said, my preferred methodology for expanding the taxation of capital is that promoted by Associate Professor Susan St John and myself the fair economic return, not a transactional based capital gains tax.

Anyway, this debate will continue to run and run. Miriam Bell’s article provoked a fierce reaction on Stuff, unsurprisingly, and there’s been an interesting debate around Robyn’s LinkedIn article. I urge you to take a look at that.

I think we really do need to address the issue of taxing property particularly when you consider what the Infrastructure Commission said earlier this week about property owners benefiting to the extent of house prices being 69% higher than they would have been without actions being taken to restrict the supply of housing. Housing and the taxation of property is a touchpoint now and will be in next year’s election. We’re going to see plenty more of this debate

Taxes on crypto assets are coming

Moving on to another controversial asset class – crypto assets. Now the value of crypto assets has just simply exploded in the last 10 years. Because of the explosion of the value, it has forced its way onto the tax agenda and tax authorities all around the world are looking to see how this new asset class fits in with their existing rules. New Zealand is no different from other jurisdictions which are all struggling with this. The recent tax bill that was passed last week, by the way, had provisions relating to the application of GST on crypto-assets.

A couple of weeks back, the OECD released a public consultation document proposing a new tax transparency framework for crypto assets. What it has identified is that crypto assets can be transferred and held without going through the normal financial intermediaries, such as banks, and fund managers. And from a tax perspective, there’s no central administrator having what the OECD calls full visibility on either the transactions carried out or on the location of crypto asset holdings.

It also appears that malware attacks and ransomware attacks, payments are increasingly demanded in crypto-assets, which are largely untraceable. So that’s obviously a matter of concern to not just tax authorities.

The OECD paper also points out that some new paid payment products. Such as digital money products and central bank digital currencies, which also provide electronically storage and payment functions similar to money held in traditional bank accounts.

But at the moment, none of these are covered by the Common Reporting Standard on the Automatic Exchange of Information. A reminder the Common Reporting Standard is an agreement between almost 100 jurisdictions where they agree to swap information on financial accounts held in their country by citizens or tax residents of another jurisdiction. It’s been a huge step forward in tackling adn improving tax transparency and tackling tax evasion.

And what the OECD is proposing is, it wants to develop a new global tax transparency framework, which will involve the same reporting for transactions related to crypto assets as for financial assets covered by the Common Reporting Standard. And it’s calling this the Crypto Asset Reporting Framework, or CARF. The paper proposes that the following types of transactions involving crypto assets will be reportable under the CARF:

- exchanges between crypto assets and fiat currencies;

- exchanges between one or more forms of crypto assets;

- reportable retail payment transactions; and

- transfers of crypto assets.

This would bring about a very significant change in the crypto asset world as a result. It will basically be bringing the whole crypto asset world in line with other reportable transactions under the existing Common Reporting Standard framework. I doubt that will be very popular with investors in the crypto world, but it certainly will be for tax authorities and other authorities, such as financial regulators and police, as they deal with the implications of the arrival of this asset class. Consultation is now open on the document through until 29th April.

Same old problem returns

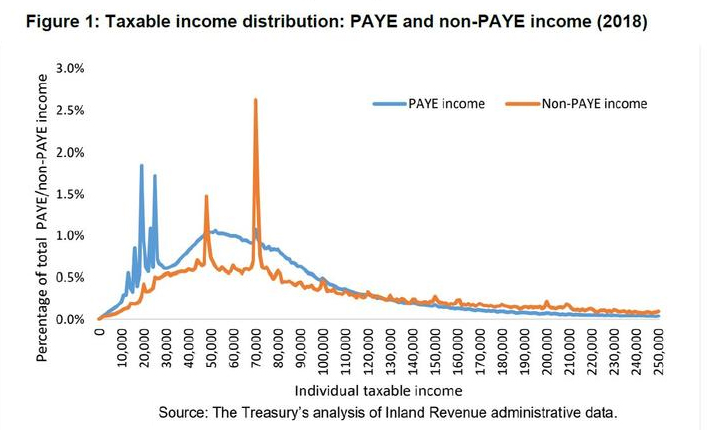

And finally, this week, a couple of weeks ago I discussed the new Inland Revenue consultation paper on countering attempted top tax rate avoidance. It so happens that yesterday RNZ had a story on the paper and Inland Revenue’s concerns that “structures may be being used to reduce incomes below $180,000.”

Inland Revenue has provisionally estimated that income from these high earners will be down $2.88 billion, or about 14% from the year prior. This is on the basis that the average self-employed person – who has the most control over their income – might declare 13% less income than they did the year before, to drop from $191,000 to $166,000 (and by happy coincidence below the $180,000 threshold). The number of PAYE earners is expected to reduce, and also declare lower incomes, from an average of $228,000 to $217,000.

If that is happening then I would expect Inland Revenue to react aggressively. On the other hand, Inland Revenue has known for some time that self-employed income spikes around the $48,000 mark (the threshold when the tax rate increases from 17.5% to 30% and $70,000 dollars when the threshold tax rate increases to 33%). I’m not yet aware of increased Inland Revenue investigation activity into such apparent income manipulation. It seems to me that although Inland Revenue has concerns about manipulation involving the new 39% tax rate, what appears to be happening around the $48,000 and $70,000 thresholds seems very blatant.

The RNZ report included a chart from Inland Revenue of the taxable income distribution for the 2018 income year which illustrated these spikes occurring at the $48,000 and $70,000 thresholds.

The graph mirrors one produced in 2008 (when the top tax rate was 39%). You can see exactly the same pattern of income spikes around $38,000, the threshold at which the tax rate increased from 19.5% to 33% and then at $60,000 when the tax rate rose from 33% to 39%.

In other words this is a very longstanding problem and the question arises why that issue has been allowed to continue? Does Inland Revenue have the resources to address it? They most certainly will say they do, and they would also probably say that they have had a lot to deal with managing the COVID-19 response over the last two together with finalising the Business Transformation project. Either way you should expect action on this from Inland Revenue.

Incidentally on the question of high tax rates, another news report covered the effect of increases for working for families tax credits. It pointed out that the effective marginal tax rate for recipients of working for families can in some cases be 57%. This is the combination of 30% tax rate on incomes over $48,000 and the 27 cents in the dollar abatement, which applies above a threshold of $42,700.

So before people start complaining about 39% being a very high tax rate, think about what’s going on with working for families, accommodation supplement and other social welfare payments. It’s quite conceivable that someone on $60,000 per annum, receiving working for families with a student loan could have a marginal tax rate on every dollar earned of 69%. This represents 30% income tax, 27 cents on the dollar abatement on their working for families and 12% student loan repayments.

By the way, the $42,700 threshold when the working for families’ abatement kicks in is now, by my calculations, less than the annual income of someone working 40 hours a week on the current minimum wage would earn. It’s another case of where governments have allowed inflation to quietly increase the tax take with worse consequences for people at the lower end of the scale. Yet another issue we’ve talked about repeatedly.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time, kia kaha, stay strong.

28 Mar, 2022 | The Week in Tax

- Inland Revenue’s proposal for a big stick to counter top tax rate avoidance

- Potential tax changes make a difference to the cost of living

- What you should do to get ready for tax year end

Transcript

Last week I mentioned that Inland Revenue had released a discussion document, Dividend Integrity and Personal Services Income Attribution, which set out its proposals for measures to limit the ability of individuals to avoid the 39% or 33% personal income tax rate through use of a company structure. This is what we call integrity measures designed to support the integrity of the tax system. In this case, the proposals are to support the objective of the increase in the top tax rate to 39% and to counter attempts to avoid that rate by diverting income through to entities taxed at a lower rate.

Now this paper is pretty detailed and runs to 54 pages. There’s a lot in here which will get tax agents and consultants sitting upright and reading the fine print as in some cases they will be affected directly. It’s actually the first of potentially three tranches in this area. Tranches two and three will consider the question of trust, integrity and company income retention issues, and finally integrity issues with the taxation of portfolio investment income. And the reason for the last one is that portfolio investment entity income is taxed at the maximum prescribed investor rate of 28%, which is undoubtedly attractive to taxpayers with income which is now taxed at the maximum tax rate of 39%.

The Inland Revenue discussion document has three proposals. Firstly, that any sale of shares in the company by the controlling shareholder be treated as giving rise to a dividend for that shareholder to the extent the company and its subsidiaries has retained earnings.

Secondly, companies should be required on a prospective basis, i.e. from a future date, to maintain a record of their available subscribed capital and net capital gains. These can then be more easily and accurately calculated at the time of any share cancellation or liquidation. That’s a relatively uncontroversial proposal.

And thirdly, the so-called “80% one buyer test” for the personal services attribution rule be removed. This one will probably cause a bit of a stir.

The document begins by explaining these measures are required to support the 39% tax rate. There’s a lot of very interesting detail in this discussion, for example it notes that with the top tax rate of 39%, the gap between this and the company tax rate of 28% at 11 percentage points is actually smaller than the gap in most OECD countries.

But then, as the document says, “However, New Zealand is particularly vulnerable to a gap between the company tax rate and the top personal tax rate because of the absence of a general tax on capital gains.”

And so to repeat a long running theme of these podcasts, this lack of coverage of the capital gains has unintended consequences throughout the tax system. And this question of dealing with this arbitrage opportunity between differing tax rates is, in essence, a by-product of that.

As Inland Revenue notes, one answer would be to align the company, personal and trust tax rates. This was the case until 1999, when the rate was 33% for companies, individuals and for trusts. But this ended on 1 April 2000 when the individual top rate went up to 39%. And since then, the company income tax rate has fallen to 28%.

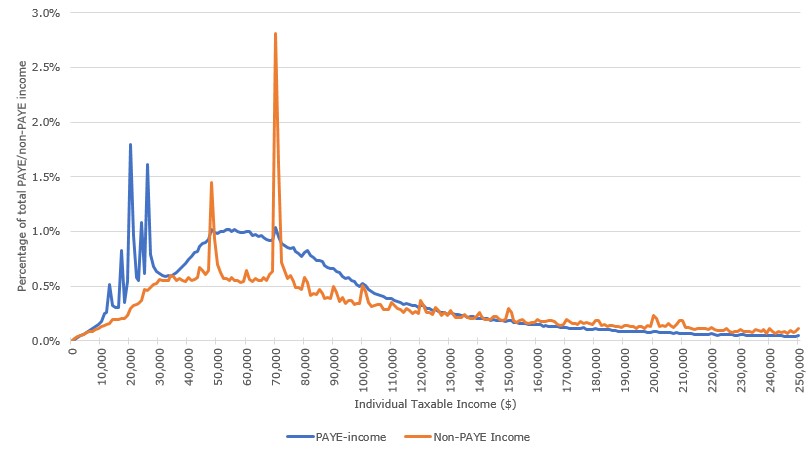

So this is a matter which needs to be addressed. There’s a really interesting graph illustrating the distribution of taxable income and noting there’s a huge spike at around $70,000, where the tax rate rises to 33%.

Taxable income distribution: PAYE and non-PAYE income

(year ended 31 March 2020)

There’s also some interesting data around what high wealth individuals pay in tax. For the 2018 income year, Inland Revenue calculated the 350 richest individuals in New Zealand paid $26 million in tax. Meanwhile the 8,468 companies and 1,867 trusts they controlled, paid a further $639 million and $102 million in tax respectively, indicating a significant amount of income earned through lower rate entities.

It appears to Inland Revenue that tax is being deferred through retention of dividends in companies.

The opportunity in New Zealand is that a sale of the shares under current legislation would bypass the potential liability on distribution. The shareholder is basically able to convert what would be income if it was distributed to him or her, to a capital gain. And clearly, the Government wants to put an end to that, but can’t because it doesn’t have a capital gains tax. The discussion document therefore proposes that any sale of shares in the company will be deemed to give rise to a dividend. This will trigger a tax liability for the shareholder.

The paper goes into detail around this particular issue, and I think this is going to be quite controversial. Because although I could see a measure where a controlling shareholder sells shares to a related party such as, for example, someone holding shares personally sells them to a trust or to a holding company, which they control. You could see straight away that Inland Revenue could counter this by arguing it’s tax avoidance.

But the matter gets more complicated where third parties are involved. And this is where I think the rules are going to cause some consternation because it proposes transactions involving third parties would also be subject to this rule. That, I think is where most pushback will come in on this position. Without getting into a lot of detail on this there could be genuine commercial transactions resulting in some might say is a de facto capital gains tax.

The proposal is not all bad. If a dividend is triggered, then the company will receive a credit to what is called its available subscribed capital, ie, its share capital, which can later be distributed essentially tax free.

In making its proposals, the paper looks at what happens in Australia, the Netherlands and Japan and draws on some ideas from there. It’s interesting to see Inland Revenue looking at overseas examples. All three of those jurisdictions, to my knowledge, have capital gains tax as well, but they still have these integrity measures.

But the key point is this question that any sale, will trigger a dividend. There’s no de-minimis proposed. This could disadvantage a company trying to expand by bringing in new shareholders. It might have to use cash reserves it wants to keep to pay the withholding tax on the deemed dividend. The potentially adverse tax consequences for its shareholders might hinder that expansion. I expect there will be a fair degree of pushback as a lot of thought will go into responding to this proposal. It will be interesting to see exactly what comes back.

Cleaning up tracking accounts

Less controversial and something probably overdue, is the proposal for what they call tracking accounts to cover the question of a company’s available subscribed capital, and the available capital distribution amounts realised from capital gains. Both of these may be distributed tax free either on liquidation or in a share cancellation in the case of available subscribed capital. But the requirement for companies to track this is rather limited, and these are very complicated transactions.

As the paper points out, the definition of ‘available subscribed capital’ runs to 40 subsections and 2820 words. So, there’s a lot of detail to work through, and if companies haven’t kept up their records on this, then confusion may arise if, say, 10 years down the track they’re looking to either liquidate or make a share cancellation.

I don’t see this proposal causing much controversy. I think Inland Revenue’s proposals here are fair and probably something that should have been done a long time ago. They will apply on a prospective basis, as I mentioned earlier on.

Personal services income attribution – a 50% rule?

And then finally, the third part deals with personal services income attribution. And what this part does is picking up the principles from the Penny and Hooper decision. This was the tax case involving two orthopaedic surgeons, which ruled on the tax avoidance issues arising from the last time the tax rate was increased to 39%.

The discussion document is basically trying to codify that decision. The intention is to put an end to people attempting to use what you might call interposed entities, lower rate entities, to avoid paying tax personally. The particular issue it’s driving at is when an individual, referred to as a working person, performs personal services and is associated with an entity, a company usually, that provides those personal services to a third person, the buyer.

Inland Revenue is now looking at a fundamental redesign of this personal service attribution rule, which was designed to capture employment like situations. It was really designed where contractors might be providing services to basically one customer (the ‘80% one buyer rule’) and in effect, they were employees. However, they could potentially avoid tax obligations by making use of an interposed entity with a lower tax rate.

Inland Revenue thinks that 80% rule is too narrow. The proposal is to broaden its application and by doing so it can at the same time deal with the issue that arose with the Penny and Hooper case.

Under current legislation, Bill is an accountant who is the sole employee and shareholder of his company A-plus Accounting Limited. The company pays tax at 28% on income from accounting services provided to clients and pays Bill a salary of $70,000, just below the 33% threshold. Any residual profits are either retained in the company or made available to Bill as loans.

The proposal is to remove that 80% one buyer rule and so that now Bill’s net income for the year, if it exceeds $70,000 will all be attributed to him where 80% of the services sold by that company are provided by Bill. Sole practitioners and smaller accounting firms and tax agents will find themselves in the gun. In fact, the discussion document suggests maybe this threshold of 80% should be lowered to 50%.

Now, you might think that the bigger issue is not the 33% threshold at $70,000, but the $180,000 threshold, so why do we want such a low threshold for this rule to apply? The discussion document points to the evidence that shows that there is income deferral going on. It appears to be at the $70,000 threshold (see the graph above) and wants to put an end to that.

So that’s a more detailed look at what is a very important paper. It’s likely to generate quite a lot of controversy and feedback from accountants and other tax specialists. It’s also another part in the long running tale of the implications of not having a capital gains tax. But certainly, this one will run and run. Submissions are now open and will run through until 29th April. I expect all the major accounting bodies and firms will be responding.

Using tax to mitigate cost of living impacts

Moving on briefly, there’s been a lot to talk about what tax changes could be done to help the increased cost of living. And Daniel Dunkley ran through some of the proposals.

One idea that pops up regularly is the question of removing GST from food. My view, which I expressed to Daniel and is also probably that of most tax specialists, is that this would undermine the integrity of GST, because we don’t have any exemptions on that.

I also don’t think it would achieve the objective that is hoped for. There is, regardless of what people might say, an administrative cost to splitting out tax rates, having zero rate for food and standard rate for other household goods in your shopping trolley. And that differential, that cost involved, will be passed on to customers.

So the full effect of the GST decrease will never flow through to customers. To be perfectly frank; supermarkets and operators will play the margins around this. I suggest you have a look at what’s happened with the fuel excise cut. It was 25 cents, but in every case did the pump price fall by 25 cents? And how could you tell because prices move around so much?

As I said to Daniel, and has been a longstanding view of mine, if the issue is getting money to people who have not enough money, give them more money. The Welfare Expert Advisory Group was staunch when it said that there was a desperate need to raise benefits. We also saw how the temporary JobSeeker rate was increased when COVID first hit. So, this issue of increasing benefits hasn’t gone away.

The best position would not be to tinker with the tax system. You could perhaps look at tax thresholds, definitely, but they still would not be as effective as giving people an extra $30-40 or more cash in hand.

End of year preparations

And finally, the end of the tax year is fast approaching, so there’s plenty of tax issues that you might want to get done before 31st March. A key one to think about is if you’re going to enter the look through company regime, you need to get the election in before the start of the tax year. In some situations you might have more of a bit of a grace period for dropping out of the regime, as part of the Government’s response to the Omicron variant. But it you are electing to join the regime, I suggest you file the election on or before 31st March.

Coming back to companies and shareholders another important issue is the current accounts of the shareholders. You should check to see if any shareholder has an overdrawn current account (that is more drawings than earnings). If so, then either see about paying a dividend or a salary to clear that negative balance, although of course, you’re up against the issue of the higher tax rate I discussed earlier. If that’s not possible, charge interest at the prescribed fringe benefit tax rate of 4.5%.

Companies may have made loan advances to other companies, look at those carefully because you may need to charge interest there to avoid what we call a deemed dividend.

Another very important matter is if there are any bad debts. If so, then consider writing them off before 31st March in order to claim a deduction. And then if you’re thinking about bringing forward expenditure to claim deductions such on depreciation, then do so.

Companies should check their imputation credit accounts balances and make sure these are positive. There are mechanisms through tax pooling to manage this problem if you miss a negative balance.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax tax or wherever you get your podcasts. Thank you for listening, and please send me your feedback and tell your friends and clients. Until next time, ka pai te wiki, have a great week.

21 Feb, 2022 | The Week in Tax

- Inland Revenue guidance on the deductibility for income tax purposes of costs incurred due to COVID-19

- Inland Revenue releases an issues paper on the future of tax administration in a digital world

- The tax perils of not taking advice before migrating.

Transcript

We’re now in the third year of the pandemic which over the past two-and a-bit years has resulted in an enormous amount of upheaval, both socially and for businesses. Plenty of unusual situations have arisen as a result, and the tax treatment of those situations needs clarification.

Inland Revenue has therefore released some draft guidance for consultation on the tax deductibility of costs which have specifically arisen because of COVID-19. What the paper notes is that businesses have suffered significant disruption as a result of the pandemic, and many have had to incur additional costs that would normally be regarded as unusual or abnormal, which have only arisen because of the pandemic. In addition, businesses are continuing to incur holding costs such as interest and depreciation for assets which they can’t use at the moment, either because of COVID-19 restrictions or because they’ve temporarily downsized the business.

This paper is designed to give guidance around the income tax deductibility of expenditure in those circumstances. It looks at a number of particular situations that obviously Inland Revenue have seen or have been asked to advise on. For example, what about the costs of bringing employees into New Zealand or retaining teams who are unable to work? What about providing accommodation to keep teams housed together in a bubble during a particular set of COVID-19 restrictions?

Other scenarios include what’s the tax deductibility of giving employees vouchers or incentive payments? And then what about redundancy payments – are they deductible if they were a result of COVID-19? What about costs of terminating contracts and related legal fees?

Repairs and maintenance and depreciation on assets and equipment that aren’t being used because of the pandemic – are they deductible? And then premises costs such as lease break fees and other costs such as keeping people appropriately distanced in a workplace. As you can see, there’s a lot of scenarios considered in the paper.

The general rule for deductibility is in Section DA 1 of the Income Tax Act. For a cost to be deductible there must be a nexus between the cost and the person’s income earning process. Now that’s always a matter of fact and degree and what must be kept in mind is that the cost to be deductible doesn’t need to be linked to a particular item of income and the income doesn’t need to be produced in the same year as the cost was incurred. The cost must be incurred in general terms as part of the business’s income earning operations. That means you can take longer term objectives about why you’re incurring expenditure.

The paper then matches these basic principles to the scenarios that I set out before with a series of good examples. These scenarios involve a hotel chain, a café, a construction company, a tourism business, and an office. I recommend reading the paper if you’ve encountered some of these unusual situations. Consultation, as I said, is open now and continues until 31st March.

Incidentally, talking about consultation, submissions close at the end of this month on an Inland Revenue consultation regarding charities and donee organisations. I covered this consultation in early December and the question of the charitable status of a few organisations has been in the news lately. So, here’s your opportunity to make submissions to Inland Revenue.

Tax in a digital world

Moving on, in my first podcast of the year, I suggested that Inland Revenue will be looking to move forward the process of tax administration now it’s completed its Business Transformation. And I recommended looking at a paper prepared by Business New Zealand on the future of tax administration.

Inland Revenue has now released an official issues paper on tax administration in a digital world. And this, I think, is a very important development for tax administration and for tax agents and intermediaries, or anyone involved in the tax system. As the paper outlines, businesses are moving online, and this is shaping Inland Revenue’s thinking about the future world in which the tax system will operate.

The paper runs to 25 pages and there is a lot to consider so I could rabbit on for quite some time. It picks up many of the principles or ideas that were set out by the Business New Zealand paper, but probably at a higher level. Inland Revenue believes that there are four pillars that set out the core framework for tax administration and social policy administration to function well. That is fairness and integrity, efficiency and effectiveness. And the paper discusses what is the impact of technology on all of those.

As Inland Revenue sees it, key features of the digital world are likely to be businesses operating in a digital ecosystem. That is, connected digitally to their suppliers and customers. The Administration of tax and social policy payments will be integrated to broader economic systems. That means, for example, individuals or businesses can use a common digital identity across a range of services. That is something I think that’s happened with COVID-19. The pandemic will accelerate that trend because it just makes life so much easier for everybody. You’re not having to deal with providing repeat information to different agencies.

Tax administration processes are going to become embedded into business systems that businesses are using. In other words, they’ll use systems that fit their business rather than tax obligations. And then, this is a key one, digital processes will enable data to flow in real time.

This is a point I keep coming back to – the amount of data that’s flying around and Inland Revenue’s access to that data, is increasing all the time. And the speed with which that data is being received and processed is also accelerating. Which means, as I’ve said repeatedly, there are fewer and fewer places to hide from Inland Revenue.

And so this paper looks at what that future might look like and it sets out some frameworks, and sets the scene in the shift to digital. There’s a very important chapter for tax agents, intermediaries and other people who work with Inland Revenue about how it sees these relationships developing. The paper considers the issue of data, how it’s collected, how it’s shared and what statistical data is to be made available on an anonymous basis.

You will know at the moment there’s a lot of controversy going on regarding a high wealth project where Inland Revenue is asking a group of about 400 New Zealanders for detailed information about their wealth. In my view, one of the weaknesses in the New Zealand system for some time has been that we haven’t actually collated a lot of data when we file tax returns. And so compared with other jurisdictions we don’t really have good data on many parts of economic wealth. That project, controversial as it is, addresses this issue. In the future because data can be found and supplied more easily, I think the data requests from agencies and particularly from Inland Revenue will increase.

There’s also talk about publishing debt data. In other words, if someone’s been a bad boy – and by the way, it is invariably boys in my experience – Inland Revenue may share that data and may develop a number of tools for enforcement.

Then the final chapter talks about general simplification process, how tax laws are written, simplifying the tax year end position and payments around the tax system.

The issues of data sharing and data protection are very, very important. In my view Inland Revenue does have a good reputation and processes for not leaking data, and its data is secure. But as it changes its role to interact more with intermediaries such as tax agents, there’s an obvious risk of leakage.

The paper therefore suggests the current process by which a person can become a tax agent needs to change. Actually within the tax agent industry I think there is a recognition that does need to change even if that reflects a certain amount, you might say of self-interest by the professional bodies. It is quite true and not an apocryphal story that a prisoner registered as a tax agent with Inland Revenue when he was in jail. He was able to do so because he had 10 clients who had to file tax returns.

If data is now going to be shared more freely and Inland Revenue is not directly controlling so much of the process, it needs to be certain that the people it’s granting access to its systems or data are trustworthy. So that’s a big issue to consider. As I said, the paper is a fascinating one. It’s a big topic, but it’s only 25 pages, and an easy read. Submissions are now open and continue until 31st March.

The tax consequences of emigrating

And finally, this week, according to the latest statistics New Zealand figures, more people continue to leave New Zealand on a permanent long-term basis than are arriving long term. In 2021, there was a net annual loss of three 3,915 people. Now at the risk of sounding like a broken record, one thing I regularly encounter is this issue of people migrating offshore, usually to Australia, sometimes to Britain or America, and overseas migrants from other countries coming to New Zealand.

It is quite astonishing the number of people who move overseas without looking through and considering all the tax implications of their move. In particular, if they are a trustee of a trust. As I have recounted a number of times, particularly in relation to Australia, the consequences of becoming resident in Australia can be quite disastrous. But I still keep encountering this issue. In fact, at the moment I’ve got three cases on the go involving variations on that theme.

So just a reminder to anyone who’s thinking about moving to Australia or moving overseas. Just remember to get tax advice before you go. You may be missing an opportunity. You may also be giving yourself a significant tax headache, which nobody wants.

Well that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!