calls for capital gains tax to help solve housing affordability.

Earlier this year, the popular Auckland Cafe chain Little and Friday closed its final store in Ponsonby. That was a great personal disappointment for me as its food was wonderful, although my waistline is probably all the better for its closure.

It has now emerged that at the time of its closure, the owners owed $640,000 in tax and the company has now been put into liquidation owing creditors over $1.4 million.

This obviously puts a different complexion on the closure, and it also prompted an interesting debate amongst my tax agent colleagues, with quite a few pointing out the inconsistencies that they see in Inland Revenue’s debt management. One took particular exception to the news, commenting how he had been grilled over a relatively small adjustment, less than three figures, and yet somehow Little and Friday had been allowed to build up unpaid GST and PAYE totalling $640,000.

Focusing on the wrong target?

Another tax agent noted that he had received a call regarding a client being overdue in making their small business cashflow scheme repayments. The amount outstanding was $18,000, but as the tax agent pointed out, the client also owed several hundred thousand dollars in relation to unpaid GST and income tax. The agent was therefore rather puzzled as to why Inland Revenue seemed to prioritise the small business cashflow scheme arrears. Several other tax agents weighed in with similar points about such inconsistencies.

Now, debt management is a core role for Inland Revenue. That goes without saying. But it is also an issue where there are clearly strains emerging. We’ve talked previously about what’s been going on with the student loan scheme, where substantial amounts of debt are allowed to build up over enormously long periods of time.

My attention has been drawn to a case where the student loan borrower left more than 20 years ago and was eventually contacted by Inland Revenue demanding over $200,000 of accumulated interest and penalties. Like Little and Friday, and other cases noted above, the unanswered question is “How did Inland Revenue manage to let it get to that stage?”

Earlier intervention needed?

When looking at Inland Revenue’s management of its debt portfolio two concerns arise – its approach seems inconsistent and it doesn’t intervene soon enough.

Inland Revenue has enormous tools at its disposal. It can put companies into liquidation and that’s actually what happened with Little and Friday. But it doesn’t want to do that all the time. It will sometimes hesitate before doing anything, for perfectly reasonable circumstances. But there does come a point where it is probably better for all concerned that the Inland Revenue moves sooner and doesn’t allow the debt to build up.

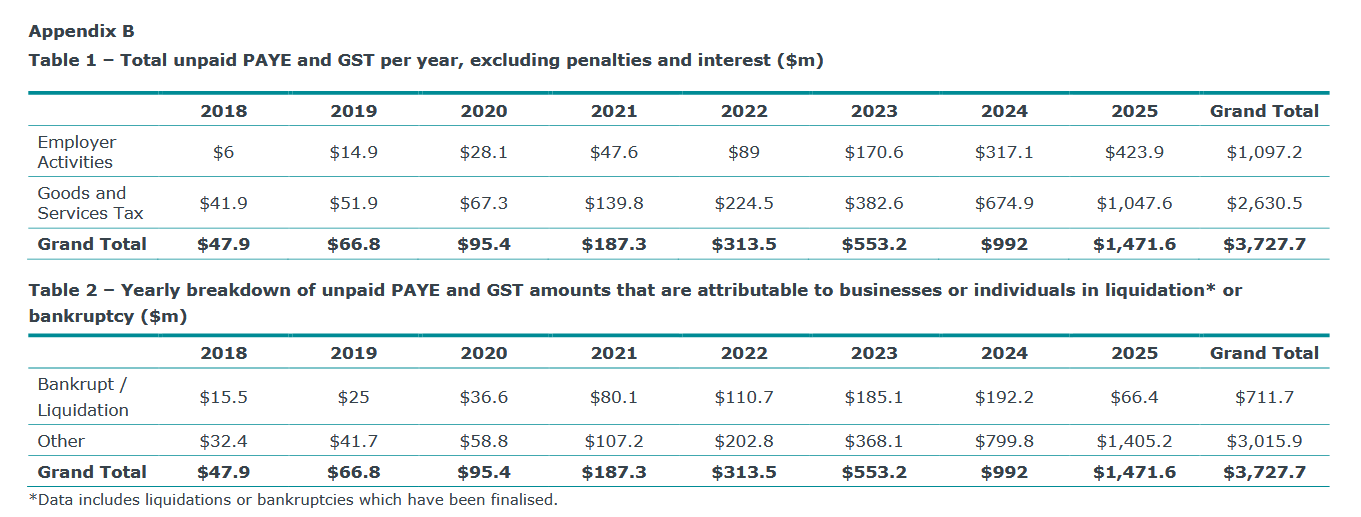

Now Little and Friday is not an unusual circumstance. While preparing for this podcast I came across an Official Information Act request about debt dating from June this year, and the number being reported was frankly horrifying. According to this report, as of 31st of March 2025, the total amount of unpaid PAYE and GST, excluding penalties and interest, stands at $3.727 billion.

As can be seen $711.7 million of that $3.7 billion represents businesses or individuals going into liquidation. The rest is simply outstanding debt which Inland Revenue is hoping to obviously try and recover. But the amount of debt it is writing off is starting to increase, as is the amount of debt that it deems non-collectible. According to this OIA report the non-collectible amount as of 31st of March 2025 is expected to be $1.1 billion dollars.

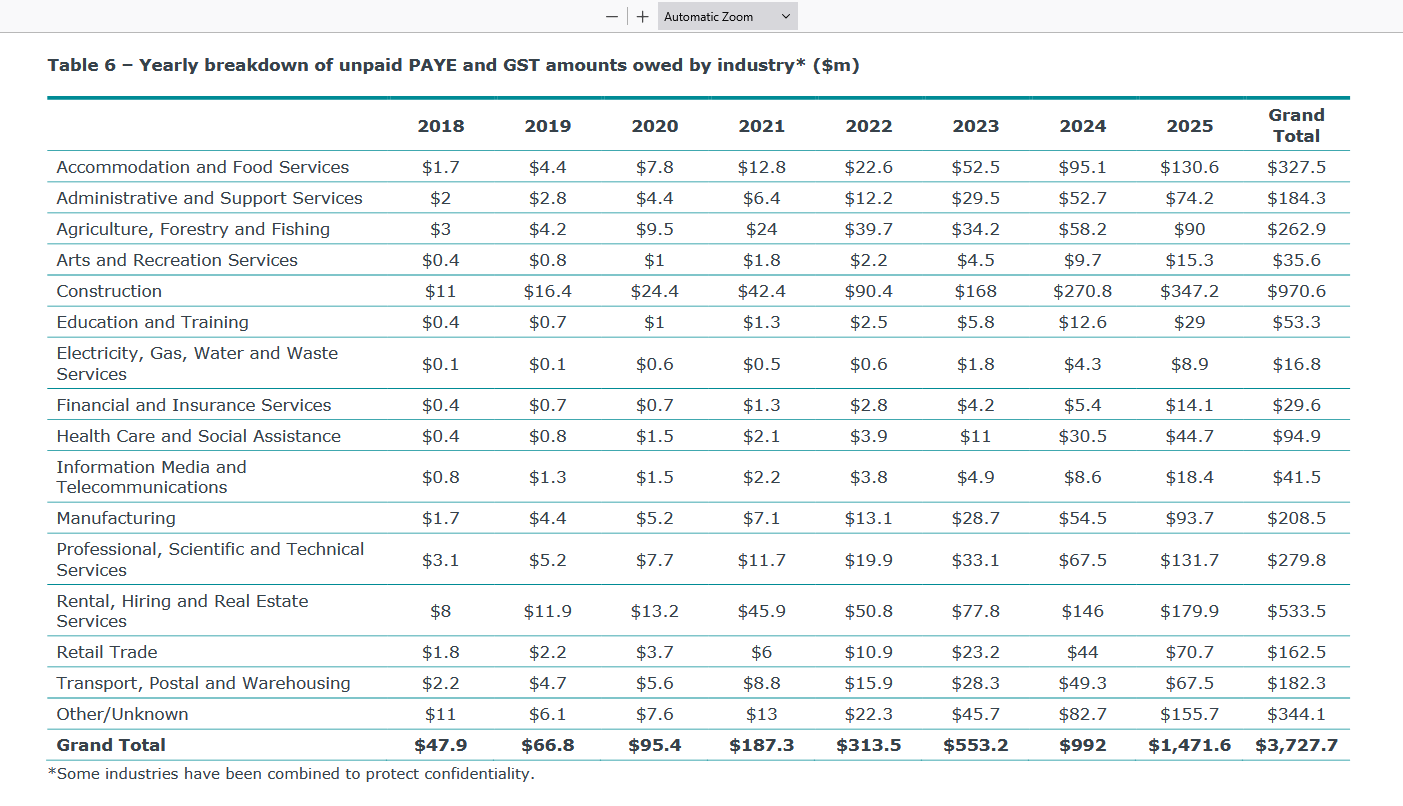

Then there’s a very interesting industry breakdown of how that amount of debt has accumulated.

The sectors hardest hit in that are our construction which has $347.2 million of unpaid debt as of March 2025. accommodation and food services, i.e. cafes like Little and Friday owe $130.6 million, manufacturing $93.7 million and professional, scientific and technical services have also accelerated remarkably $131.7 million. Even rental hiring and real estate services, which you would regard as relatively strong industries, has unpaid GST and PAYE of $179.9 million as of 31st March this year.

Across the whole of the economy, these numbers are piling up and it presents a huge problem for Inland Revenue, and by extension for the Government as to how is it going to manage this issue.

Unfairly targeting student loan defaulters?

A very real threat for people owing student loans who are not meeting their obligations is being arrested at the border. But none owe $600,000 of tax. In theory, someone owing that amount of unpaid GST and PAYE could be freely entering and leaving the country without customs making a move against them.

On the other hand, someone owing $100,000 of student loan debt, which is sizeable, yes, could enter the country and be arrested. I wonder why such an inconsistent approach applies.

To be fair Inland Revenue is working through the overdue debt issue and taking enforcement action. This week it reported how an accountant, Luke Daniel Rivers, also known as Mai Qu was jailed for six years over a $1.7 million COVID-19 fraud. He made false claims over wage subsidies in the small business cash flow scheme.

Now quite correctly Inland Revenue and the Ministry of Social Development have pursued that. But at the same time, we have these other businesses falling over, owing very substantial sums of money, and it appears almost as if the defaulters are able to walk away without consequences, to the frustration of myself and other tax agents.

What about MBIE?

One other thing of note in this area are the potential breaches under the Companies Act 1993. In some cases, you’d have to say there there’s a strong argument that businesses racking up hundreds of thousands of dollars of tax debt are in breach of their Companies Act obligations, which could lead to action by the Ministry of Business, Innovation and Employment.

The economy is under strain and tax debt is rising. Sometimes really bad luck hits a business or person. Small businesses can get hit particularly hard if a key person falls ill. Tax debt may just be down to sheer bad luck, the wrong thing happening at the wrong time.

But overall, Inland Revenue looks to be struggling, for want of a better word, managing the portfolio. Even allowing for maybe getting better resources to manage this, there’s still the question of an inconsistent approach that I and other tax agents have noted. So, there’s a lot of going on in this space.

I expect the Commissioner of Inland Revenue is reporting very frequently to the Minister of Revenue on this issue and any new initiatives to address these concerns. The most important thing would be to get the economy going again and hopefully some of these businesses are able to trade their way out. But we’ll have to wait and see.

Capital gains tax to deal with housing affordability?

Now, in recent weeks, there’s been quite a lot of chatter around Inland Revenue’s long-term insights briefing, which has talked about the need to perhaps expand the tax base. Last week we discussed how CPA Australia called for a capital gains tax.

This week at the Government’s Building Nations 2025 Infrastructure Summit on Wednesday 6 August, Group Chief Economist and Head of Research for ANZ Richard Yetsenga discussed the question of what he described as runaway house prices in Auckland, Australia and New Zealand. He said that we should look seriously at introducing a capital gains tax as a means of addressing house price affordability. In his view, if this issue is not resolved, “I think it’s going to eat us alive. It’s our biggest intergenerational issue.”

Mr Yetsenga was speaking after addresses from the Finance Minister, Nicola Willis, and Transport Minister and Housing Minister Chris Bishop. In response he suggested looking at both the supply and demand issues of the tax system, which in his view, was one of most effective ways available to influence economic activity.

That’s something I would agree with. What we don’t tax is as important as what we do tax. I think the fact that we don’t have a capital gains tax has resulted in major distortions for our economy. This was something which the recent International Monetary Fund report on our poor productivity mentioned. It’s very interesting to see all the constant chatter on the topic of capital gains taxation.

How many people return overseas income?

Finally, Inland Revenue proactively publishes any Official Information Act (OIA) requests that it receives. These often include some very interesting data such as the breakdown of debt I discussed earlier.

The question was rather oddly phrased because the requester asked “Do you know if/believe there high compliance with NZ tax rules for NZers working overseas?” Inland Revenue’s response was basically this is actually not a request for information, it’s more for an opinion so we aren’t answering that.

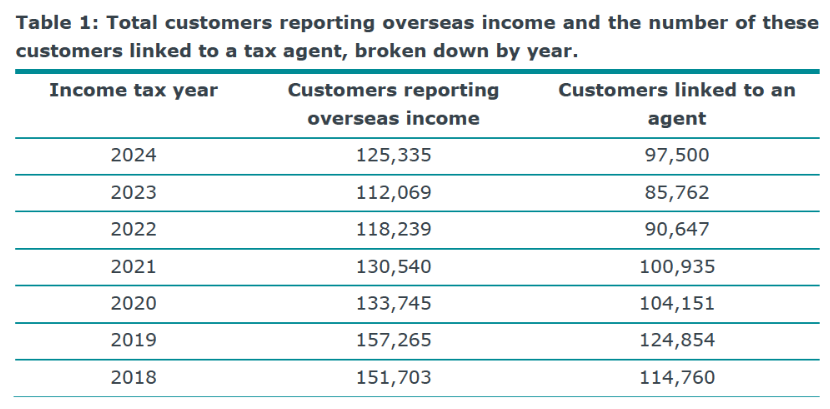

The request then asked for specific data about taxpayers reporting overseas income, and also the split between taxpayers who reported it and those taxpayers with tax agents who report it. Inland Revenue provided the following breakdown for the 2018 to 2024 tax years. (The final due date for filing tax returns for the 2024 tax year is 31st March 2025 so 2024 is the latest year for which complete details are available).

What caught my eye about this data is that the numbers have fallen since the 2019 year. In 2018, 151,703 taxpayers reported overseas income, of which 114,760 were linked to a tax agent. After an increase in the 2019 year the numbers reporting income decline each year until the 2024 year when it rises from 112,069 to 125,335.

I find it quite surprising, given the international mobility of our labour, that fewer people appear to be reporting overseas income when we have a lot more migrants arriving.

I suspect it’s possibly piqued Inland Revenue’s interest, because I’ve had some clients requesting assistance after they have been contacted by Inland Revenue which has received information under the Common Reporting Standards of Automatic Exchange of Information. It will be interesting to see how that number of taxpayers reporting overseas income tracks.

By the way, this OIA also references the Common Reporting Standard, confirming in response to a question it “receives financial account information automatically from the Australian Tax Office under the Common Reporting Standard. This information is matched to taxpayer accounts and risk assessments.”

This ought to be well known and, as noted above, maybe we might see an increase in the numbers reporting overseas income.

Happy Twenty-first!

Now finally this week, according to LinkedIn, Baucher Consulting is 21 years old today. So Happy Birthday to me. It’s been and continues to be an amazing journey and who knows what the future will bring. In the meantime, thank you all for all the messages of support.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

the winners of this year’s Tax Policy Charitable Trust Scholarship are announced.

A preview of next week’s United Kingdom Budget.

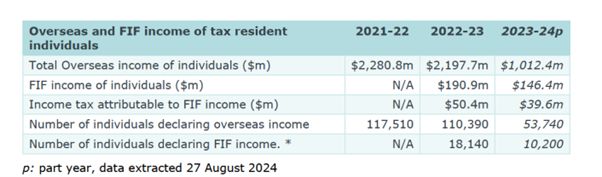

Inland Revenue regularly releases Official Information Act requests that it has answered. One from last month was in relation to the amount of overseas income reported by individuals. My attention was first drawn to this OIA by Robyn Walker of Deloitte (thanks Robyn) who like me, and many other professionals were quite surprised when we saw the number of people reporting Foreign Investment Fund (FIF) income.

Is there under-reporting?

According to Inland Revenue, which only really started gathering exact data on this in the 2023 income year, 18,140 individuals reported a total of $190.9 million of FIF income for that year.

When you consider that based on the latest Census 28% of the population of New Zealand were born outside the country, it seems to me that the amount of overseas income being reported, and in particular in relation to FIF income, is probably below what we would expect to see. And that’s what caught Robyn’s eye. One or two other advisors have made the same comment.

It could be because we deal in this space, there’s a bit of an echo chamber effect because we will regularly advise on these matters. If we’re dealing with a fairly high proportion of overseas migrants, and our practise Baucher Consulting does, then it’s natural we might think there is a broader scale of overseas investments generally.

But the number seems incredibly low in relation to the FIF income being reported, and also generally speaking, when you think about the number of overseas persons declaring overseas income.

A question of non-compliance

The issue therefore arises as to whether in fact we have non-compliance happening. I raised my concerns about this with Jenny Ruth of Good Returns. In our practice we regularly encounter clients coming to us who have realised that they have not been compliant with the Foreign Investment Fund regime. In some cases, they’ve come to us on another matter and in the course of discussions, it’s emerged that they have not been compliant. At any one time we are usually filing disclosures and bringing tax returns up to date.

Complexity and non-compliance

In my view this possible level of non-compliance speaks to the complexity of the Foreign Investment Fund regime. It’s not a capital gains tax, it operates as a quasi-wealth tax. That’s how I describe it to taxpayers and whenever I’m speaking to overseas advisors on the matter.

Old habits die hard

The FIF regime is not intuitive and I’m often dealing with people who come from overseas jurisdictions which have capital gains tax. They’re aware that where there’s a disposal there is a tax point that’s triggered. This may seem strange to say, but I’ve found in my practise that people’s tax habits developed in their country of origin take long to die even after many years in New Zealand.

Now, coincidentally, just to give some idea of the complexities involved in the FIF regime, Inland Revenue has just released a draft interpretation statement for consultation on the income tax issues involved in using the cost method to determine FIF income.

The Cost Method and the FIF regime

Those who have investments within the regime will be familiar that a fair dividend rate of 5% will apply to the value of your Foreign Investment Fund interest as of the start of the tax year. The alternative is to look at the total realised and unrealised gains of your portfolio including dividends over the year and report that instead, if that’s the lower amount. Incidentally that option way is not available for KiwiSaver funds or for the New Zealand Super Fund which is why it’s regularly one of the largest taxpayers in the country.

But what happens if your FIF interest is unlisted? The cost method generally applies when an investor is holding shares in an unlisted overseas company. And so this interpretation statement explains when that cost method may be applied and how it operates. As is now common, there are lots of examples and flow charts which explain the process. But the fact that there’s an interpretation statement on this matter which has set out and explains when you can or cannot use it the methodology, speaks to the complexity of the regime, and also the compliance costs involved in this.

The cost regime is generally to be used when the values of shares are not readily available. As part of that it will require the taxpayers to find and obtain an initial market value of the overseas stock, so they have a base cost for the purposes of the FIF calculations. It’s possible in some circumstances to use the net asset value of the accounts, usually if those accounts are audited.

Practical problems with the FIF regime

But as can be seen when people are required to obtain independent valuations this means additional compliance costs in what is already quite an involved regime. The other reason why the FIF regime causes consternation amongst taxpayers is the tax liability is not based on cash flows. A tax liability arises under the FIF regime even if the company in question is a growth company and not paying any dividends. Earlier this year I discussed a reportThe place where talent does not want to live, about the issues the FIF regime creates for startup companies and New Zealand resident investors.

All of this just underlines the complexities of the FIF regime. As I told Jenny Ruth of Good Returns, whenever I hear someone arguing “Oh well, capital gains tax is very complicated” I immediately think, ‘Well, they’ve clearly never dealt with the Foreign Investment Fund or financial arrangements regimes.’

Complexity leads to non-compliance?

Anyway, the upshot of all of this is there’s probably a considerable amount of non-compliance happening in in relation to reporting of FIF income. And Inland Revenue are now cracking down on this by making use of the information now available to them under the Common Reporting Standards on the Automatic Exchange of Information.

Now this is an OECD information sharing initiative which started in 2017. Inland Revenue which started a compliance project in late 2019 using this data. But then Covid turned up so that project had to be parked but it has now been reinitiated. As a result, I’ve recently taken on clients contacted by Inland Revenue advising it has received information under the Common Reporting Standards. The clients have been asked for an explanation about their apparent non-disclosure of overseas income and ‘invited’ to make the relevant income disclosures.

Keep in mind also that in the May Budget Inland Revenue was given $116 million over the next four years for investigation activity. The upshot is we’re probably going to see a lot more disclosures about FIF income when we’re looking at the numbers for the 2025 year.

In the meantime, I urge readers and listeners to consider their position and check with their tax advisor if they think they may have investments within the Foreign Investment Fund regime and have not made the disclosures they should have.

And the winners are…

Now moving on, the winners of this year’s Tax Policy Charitable Scholarship were announced in Wellington on Tuesday night. The Tax Policy Charitable Trust was established by Tax Management New Zealand and its founder Ian Kuperus to encourage future tax policy leaders and support leading tax policy thinking in Aotearoa New Zealand. Three of this year’s finalists, Matthew Handford, Claudia Siriwardena and Matthew Seddon have appeared on the podcast over the past few months discussing their proposals.

The format for Tuesday night was that the four finalists, having already prepared a 4000-word final submission, would then present their proposals to a judging panel and the audience, as part of a Q&A.

The judging panel consisted of Joanne Hodge, who’s a former tax partner at Bell Gully and a member of the last Tax Working group. Professor Craig Elliffe Professor of Law at the University of Auckland and another member of the last Tax Working Group. Nick Clark, Senior Fellow of Economics and Advocacy at the New Zealand Initiative and Chris Cunniffe, Strategic Advisor of Tax Management New Zealand. A pretty daunting panel to be frank.

According to Chris Cunniffe “the quality of the presentations on Tuesday night was exceptionally good” and in the end the judges were unable to separate Matthew Seddon and Andrew Paynter.

Winners Andrew Paynter (left) and Matthew Seddon (right) with the judging panel

Matthew’s proposal, is to extend withholding taxes to payments received by independent contractors.

Andrew works as a policy adviser in Inland Revenue. His proposal is to increase the GST rate to 17.5% and introduce a GST refund tax credit for lower and middle income individuals. This would be a means tested individualised credit and would be paid at a flat rate to all qualifying tax resident individuals under a particular income threshold. It’s a fascinating proposal and I’ve reached out to Andrew about appearing on the podcast in the near future.

In the meantime, congratulations to the winners Andrew and Matthew and also to the runners up Claudia and Matthew Handford. Don’t be surprised if you see something popping up in legislation in the near future involving one or more of these proposals. They were all of a very high standard this year, so well done everyone.

UK Budget preview

And finally this week, a brief preview of next week’s UK budget. The new Labour government has been in office now for three months and it’s finally getting around to announcing its first budget. That is part of what they call the Autumn budget statement.

The UK has two budget statements a year, but this one is going to be quite significant because there’s a lot of noise and chatter around tax changes. A quite significant part of my practice at the moment is advising New Zealanders going to the UK, and migrants coming here, and the tax implications involved.

I’m therefore watching this budget with some interest because we know there are going to be two proposals, the final details of which will come out, which will have an impact for quite a number of people. Firstly the so-called foreign income and gains exemption, which is the UK equivalent of our transitional resident’s exemption. This was first announced by the Conservatives in their Spring budget in March this year, but then the General Election happened so full details of the proposals were not released.

Related to that, and this is surprisingly important for a large number of people, are changes to the domicile regime also announced by the Conservatives. At present domicile is incredibly important for determining a person’s liability for UK inheritance tax, which is payable at 40% above net assets over £325,000. It appears the UK will move to a more residence-based regime, but we don’t yet know the details.

I’m therefore watching this with great interest and there are bound to be other measures which are likely to affect New Zealanders going to the UK, or the UK migrants moving here. We’ll therefore keep you abreast of developments in next week’s podcast.

Until then, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

GST is frequently touted as a simple tax, and I think that’s partly because there’s only one rate and it applies across the board on almost all goods and services consumed in New Zealand. But like any taxes, it has a number of hooks in it which frequently trip people up.

Some of these hooks shouldn’t be tripping people up because they’ve been known about for some period of time. But surprisingly, I still come across this particular issue time and again. And it’s really quite concerning that it still does happen.

The issue will almost invariably involve land. It’s where someone has purchased land from an individual and then decides that it’s perfect for a development activity or whatever, and then sells that across to a company or sometimes a trust which is registered for GST which then claims an input tax credit.

This is where things go off the rails. The issue is that the supply from the individual/another company who initially purchased the property to another party which is “associated” with it means that for GST purposes, the GST input tax claim that can be made is limited to the amount of GST paid by the first person.

Now, this provision, section 3A of the GST Act, has been in place since October 2000. It applies to transactions between “associated persons” which given the wide definition in the associated persons rules is very likely applicable when there are common shareholders/trustees/settlors.

What section 3A is designed to do is to stop someone buying a property then on selling it at an inflated price to an associated GST registered entity, which then picks up an increased input tax credit. And the rule basically says that the GST input tax is limited to the amount paid by the original purchaser. And since that purchaser often purchases it off a non-GST registered person, that amount is nil.

And I see this quite a bit. I’m surprised some lawyers and accountants haven’t really got across a measure which is now 20 years old.

The latest example I’m trying to describe is that the individual purchased the property, and then after advice from a lawyer – that for asset protection and business purposes – it would probably be better that the land be sold to a company to carry out the proposed development. That itself is not unreasonable advice. Problem was the lawyer overlooked the impact of GST and the client who is new to New Zealand didn’t get tax advice at the right time, which is another common mistake.

The company actually did get an input tax credit and refund of $450,000. You might well ask why did the Inland Revenue let a GST input tax claim of that amount go through? Fair question but it’s a complicated story.

Anyway, Inland Revenue then took a further look at it and then said, “Oh, no, you’re not entitled to that refund”. So now the client has to find $450,000 dollars and pay it back. They’re not best pleased which is understandable. And I think that is something that should provoke some fairly sharp questions between the client and their lawyer. But it is a common issue I keep seeing.

So, the golden advice here is get advice from your accountant and other advisors before you make the acquisition or get into the project. If you don’t, because you’re trying to save on professional fees, you might well find that trying to save two or three thousand dollars in advice has, like this particular client, just cost you $450,000. Get advice on any GST related transaction because GST has a lot more hooks to it than people realise.

I have a couple of other GST cases going on at the moment where people who said they were GST registered turned out to be not registered, or vice-versa and that has got lawyers at ten paces throwing writs at each other over whose client picks up the GST warranty.

NZ residents must report global tax income

Moving on, another common error I come across is people misunderstanding their income tax obligations where they have assets in more than one jurisdiction. I frequently encounter a position where a New Zealand tax resident also has property or other income source in the United Kingdom, Australia, wherever, and has been complying with that jurisdiction’s requirements to file a tax return.

This often happens involving assets in the UK. A person might have to file UK a tax return because they’ve got a rental property over there. But although they’ve complied with their UK obligations, they overlook the fact that as tax residents of New Zealand, their income is reportable taxable on a global basis. So they should be reporting the UK income here as well.

And that’s the bit that often gets forgotten about. Most people seem to be aware there’s a rule against double tax. And they seem to think that by filing a tax return in the country in which the property is situated, they have met their obligations and it’s only taxable in the country in which it’s situated. It’s not, it’s taxable worldwide.

Inland Revenue issued in July a very good Interpretation Statement 20/06 which sets out all the rules overseas rental properties. But I daresay this particular case won’t be the last time I’ll come encounter a situation where someone has reported income overseas, but not in New Zealand.

And it’s a good insight into always try and catch up regularly with your clients and take the opportunity to ask questions, because more often than not, if you don’t ask, you don’t find out. And then something happens after which everyone is going “Oops!” and no one is terribly happy about how that plays out.

Labour’s tax policies

And finally, last week, Labour announced their proposed income tax policy, increasing the top income tax rate to 39% for income in excess of $180,000. This has not been terribly well received, partly and very obviously from those who are likely to be affected. They’re not going to be happy about that. And that’s understandable. Who likes paying more tax? Let’s be frank about it.

But also, more importantly, leaving aside partisan issues such as Labour activists saying it’s too timid, the interesting issue to me is how other people have come out and said it really doesn’t do anything to address the issues of inequality and distortions in the tax system. It’s also been dismissed as just a drop in the ocean in terms of addressing deficits.

There’ve been two such articles in the past week that raised these issues. The first was from Jonathan Barratt a senior lecturer in taxation at Te Herenga Waka — Victoria University of Wellington. And he basically said that both Labour and National are really not doing anything to address questions of inequality. The tax base is too narrow, it benefits the wealthy and punishes the poor. And his key point was that neither major party seems to want to do anything about it.

I do have a view that the “Four legs good, two legs bad approach” to discussing taxation over the last 30 odd years hasn’t helped any constructive conversation in this matter. Also, property has become such an important asset for so many people where sometimes the untaxed growth in the value of the asset exceeds a person’s annual earnings, it’s therefore understandable people are reluctant to have that precious nest egg taxed.

Also coming out and having some fairly harsh, but fair, commentary on Labour’s tax policy was Geof Nightingale, of PWC, who’s been a previous guest of the podcast, but more importantly was a member of the last two tax working groups.

And he begins his article by calling it “Brief and predictable, but disappointing”. And he goes on to point out the 39% rate turns us back to the tax settings at the end of the 20th century when we last increased the top tax rate to 39% rate. The policy “makes the existing equity and efficiency distortions in our tax system worse and will have no significant impact on income or wealth inequality”.

Now, Geof was one of those who backed the introduction of comprehensive capital gains tax. What he’s pointed out here is that the increase in the tax rate to 39% is a progressive move but only in relation to employment and personal services income. It’s quite possible if you’ve got investment income, which is in a portfolio investment entity it’s taxed at 28% and it’s held in a trust it’s going be taxed at 33%.

I really do struggle to understand why Labour is not looking closely at the trust tax rate. It was known to be an issue the last time the top tax rate was 39%. But I suspect they may well come back to that if they get re-elected. There are anti avoidance measures in place, as Geof has said. But the whole point is that the zero percent rate on capital gains still applies and investment returns and capital gains because of the amount of money sloshing through the system now are likely to increase.

So, as he said, one solution is of course, a capital gains tax, which in his view and mine spreads the tax burden more equitably across the economy. And it could also allow lower personal tax rates. What’s often forgotten in the wake of what happened at the end of the Tax Working Group, was that lower tax rates were part of the whole package including capital gains tax. National of course will not do anything in that space. It’s saying it’s sticking to opposing capital gains tax and ruling out tax increases.

So Geof’s article was really quite swingeing in its criticism and fair enough in that regard. He concludes

“Here we are then, a government that wants a second term faced with a major fiscal crisis but backed into the dead end of a 20th century tax policy. Predictable but disappointing.”

Well, that’s it for this week. I’m Terry Baucher. And you can find his podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients. Hei konei ra!