How to deal with recipients of paid parental leave with tax underpayments

A bizarre tax avoidance case from the UK involving snails

In line with other government agencies, Inland Revenue is required to produce a long-term insight briefing once every three years. These briefings are intended to

“…help us collectively as a country think about and plan for the future. They do this by identifying and exploring long-term issues that matter for our future wellbeing. Specifically, [briefings] are required to make publicly available:

information about medium- and long-term trends, risks and opportunities that affect or may affect New Zealand society, and

information and impartial analysis, including policy options for responding to the trends, risks and opportunities that have been identified.”

This is Inland Revenue’s second long-term insight briefing, its first one released in 2022 was on tax, foreign investment and productivity and that was a fairly chunky topic. But this time around it’s proposing to take on a bigger topic “what broad structure of the tax system would be suitable for the future.” What it would do is look at this topic by reviewing our tax system through the lenses of what is the tax base and what regimes apply.

As part of the initial stage of consultation for this topic Inland Revenue has released a 50 page briefing document giving a background on the whole process. The briefing summarises the current state of the New Zealand tax system and the options for consideration. Chapter one gives a complete overview of the current system. Chapter two then gives options for a future tax system and looks at international perspective. The final chapter summarises the topic and the approach to be taken by the briefing.

A mini-tax working group review

There are a lot of interesting insights in this paper, because in essence it’s similar to the scoping paper usually prepared by a tax working group at the start of a review before the group gets into detailed analysis of particular aspects of the tax system. The briefing is a therefore a handy high level summary of the current state of the New Zealand tax system.

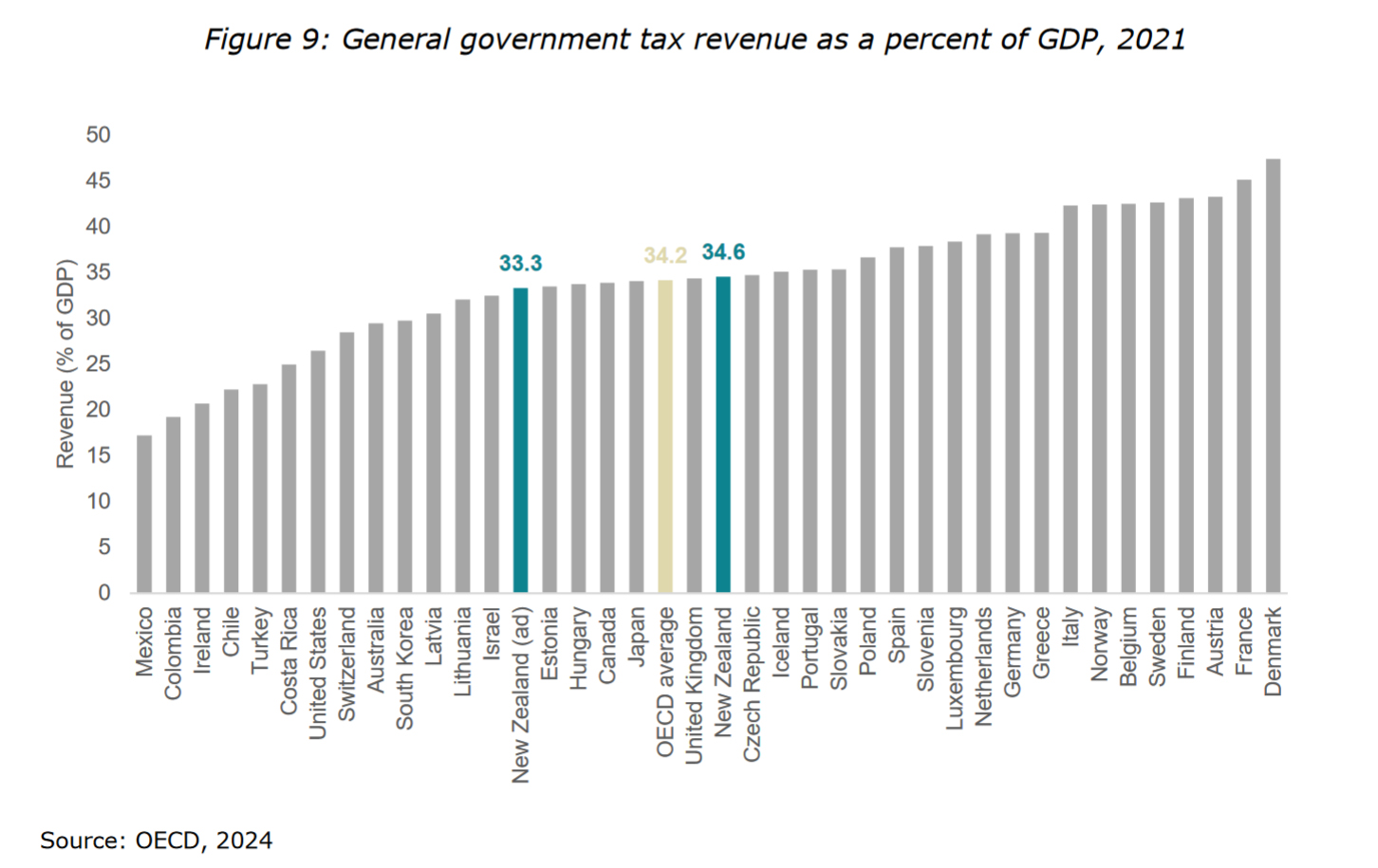

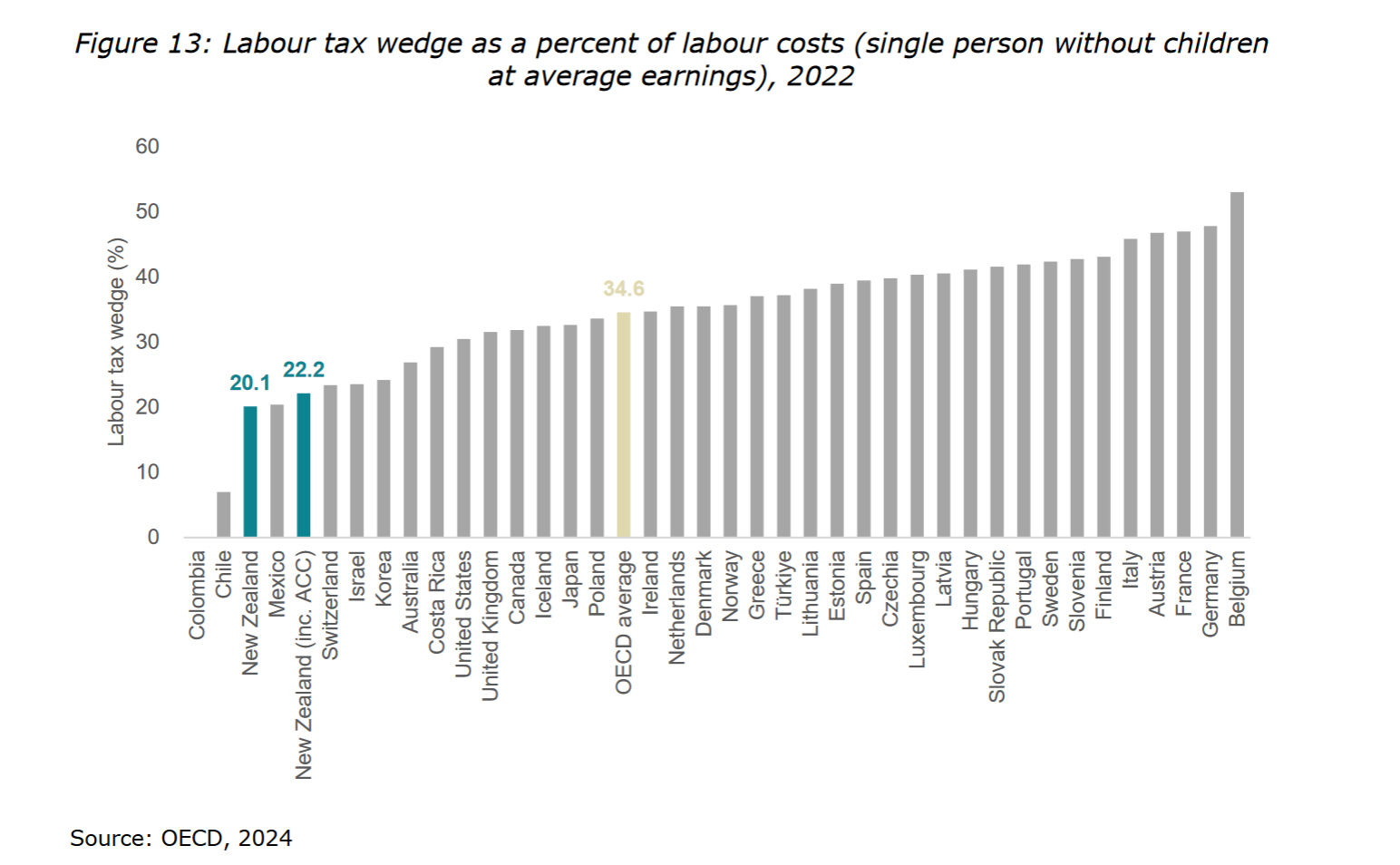

In summary, the level of tax revenue we currently raise relative to the size of our economy is pretty close to the OECD average. It’s in the composition of tax revenue. It’s where it gets interesting. We are almost unique in the OECD in not having any significant specific taxes on labour income such as social security contributions or payroll taxes.

Taxing labour…lightly?

Furthermore, quite a few of other OECD tax systems have what they call a schedular tax system, which means in some cases they tax capital income such as dividend, and in some cases capital gains at lower rates than taxes on labour. As a result, many OECD countries have a higher tax burden on employee labour than New Zealand.

To give an example, the UK has a 20% basic tax rate, but employees also pay National Insurance Contributions above a certain threshold (8% on income between £242 and £967 per week and 2% above £967 per week). Employers pay 13.8% on all earnings over £175 per week. By contrast we have no such taxes which means we have one of the lowest tax wedges in the OECD.

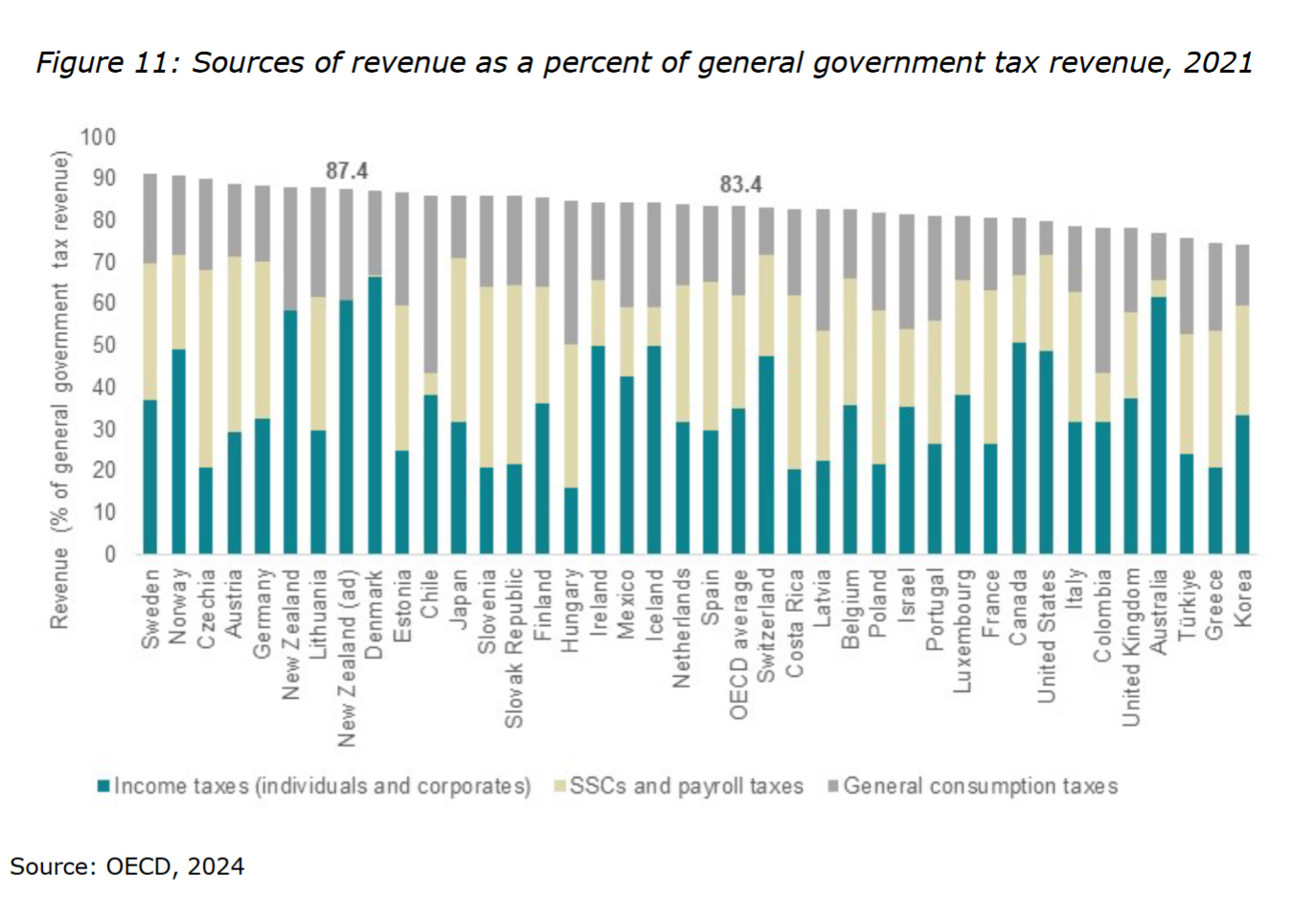

Also, where we stand out is we raise more than the OECD average on general consumptions and that’s because our GST is one of the most comprehensive in the world. We also currently have a higher company income tax rate than the OECD average.

The paper notes some concerns noted about high effective marginal tax rates on inbound investment. I have to say I do wonder whether the small size of our economy and its isolation is more of a factor than tax in attracting inbound investment.

And finally, and this is highly ironic and also relevant if, you just opened your rates bills and the comments from the Prime Minister earlier this week, New Zealand raises more than the OECD average from recurrent property taxes, mainly through local government rates.

Building fiscal pressures

As part of the background the paper explains the various fiscal pressures building up. This is something we’ve talked about before, and we’ve frequently referenced, Treasury’s He Tiro Mokopuna 2021 statement on the long-term fiscal position. The well-known pressures building in in relation of our changing demographics, rising superannuation and health costs are all mentioned again.

So too is climate change, but more in passing, although personally I think that’s the one the impact of which is going to land first for most people as we saw last year in the wake of Cyclone Gabrielle. Suddenly, climate change is not an abstract thing with targets for 2050. It’s here and now. Remember Auckland ratepayers, for example, we got a $400 million bill as a result of buying out properties rendered uninhabitable by the Anniversary Weekend floods and Cyclone Gabrielle.

A suitable tax system for the future

The paper discusses what would you do in terms of meeting these pressures. Do you expand the tax base by adding new taxes or what about increasing tax rates? The paper mentions that there are limitations about raising tax rates which is not always as straightforward as you might think. For example, we raised the rate of GST from 12.5% to 15% in October of 2010 and GST as a result is a very significant tax because our system is so comprehensive.

But GST comes at the price of being very regressive for people on lower incomes. How would you deal with that? And the paper, by the way, references an IMF Working Paper on a progressive VAT/GST which I mentioned recently.

There was also an interesting comment I’d like them to know more about in relation to company tax. The paper notes that we raise a relatively high amount of revenue from company income tax as a proportion of GDP compared with other countries.

It notes this “may be partly attributable to the level of incorporation.” I’d be interested in knowing how much more company incorporation goes on here relative to other OECD countries. I think our imputation tax system is also a factor in why we pay relatively high amounts of tax relative to other jurisdictions.

What the briefing does reinforce is something I think is agreed within the tax community that there’s pretty much little scope for increasing company income tax rates. There’s always a lot of talk about that, but I don’t think there’s much scope for actually doing so.

“New Zealand is unusual among OECD countries in not having a general tax on income from capital gains”

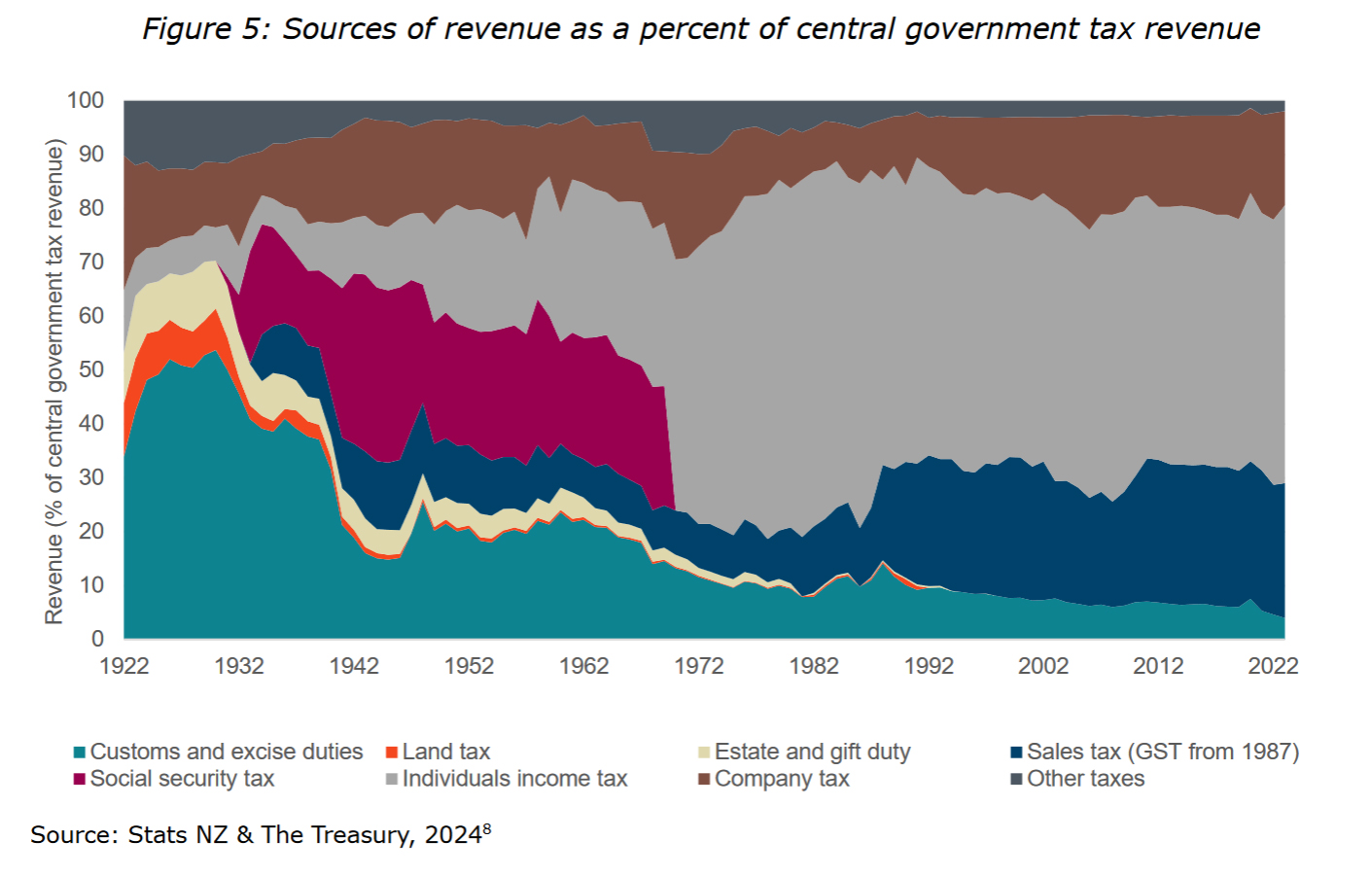

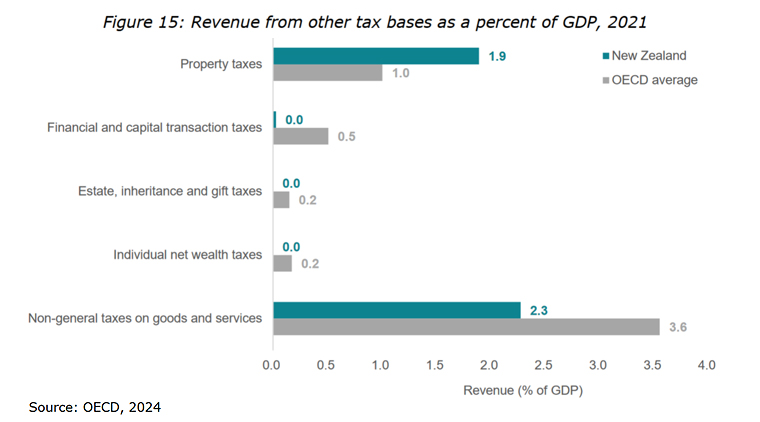

Unsurprisingly the paper considers the question of taxing capital, as part of reviewing the composition of taxes in other countries. There are a lot of interesting graphs and stats are in this section including an excellent section summarising the historical changes in the composition of the tax base over the past century.

As I mentioned, we raise more revenue as a share of GDP from recurrent property taxes compared to the OECD. In 2021 it amounted to about 1.9% of GDP. B comparison, the average in the OECD is 1%, ranging from 0.1% of GDP in Luxembourg to 3% of GDP in Canada.

On the other hand, we don’t raise anywhere near the same level as other OECD countries from taxes on financial and capital transactions, estates and gifts. I mean, many countries have a combination of estate taxes, gift duties, capital gains, taxes and wealth taxes. According to the OECD data taxes on estates, inheritances and gifts raised an average of 0.1% of GDP in 2021. That seems a surprisingly low number, although it rose to 0.2% in 2022. This take is starting to rise as the Baby Boomers, the richest generation in history are starting to pass on. In the UK Inheritance Tax, which is a combined estate and gift tax, is now over 0.3% of GDP (£7.5 billion) and rising.

What about corrective and windfall taxes?

The paper gives a background on the possible options which might deal with future cost pressures. Its focus is going to be on revenue raising taxes. The final briefing will not examine taxes that are primarily about changing behaviours (so called “corrective taxes” such as excise duty, particularly in relation to tobacco. It will not discuss environmental taxes which are another form of corrective taxes. All taxes change behaviour in different ways and I think considering the behavioural impact of certain types of taxes would be useful

The final briefing will not consider windfall taxes, which have recently popped up in discussion in relation to supermarkets and the banks. Such taxes are one-off in nature and frankly, a reactionary tax to a set of events. If the concern, correctly in my view is about responding to the pressure of ever increasing costs, then windfall taxes are not in that context a sustainable addition to the tax base.

All in all, this is very interesting and pretty digestible reading. Consultation is now open until 4th October, so my suggestion is get reading and start submitting.

A baby and a tax bill…

Moving on, Inland Revenue has mostly completed its year-end auto assessment process for the majority of taxpayers’ income for the March 2024 tax year. Subsequently, it’s emerged that some 13,261 recipients of paid parental leave, about 27% of all such recipients have finished up with a tax bill. This is causing some concern because in some of these cases, these bills are quite substantial, amounting to several thousand dollars in some cases which have to be paid.

Paid parental leave is taxable and subject to PAYE. What seems to have happened is that people haven’t factored in the effect of their other income, for example they may have continued to work reduced hours in their main employment while also receiving paid parental leave. Consequently, because PAYE is designed around one person, one job per year the parental leave has been under taxed. But this only emerges as part of the end of tax year wash up. You can deal with this by using a secondary tax code, but that often goes the other way and leads to over taxation during the year.

Tailored tax codes

An answer to all of this, and also as a means of collecting the tax paid would be a tailored tax code. Tailored tax codes are ideal for an employee with other sources of income which aren’t subject to PAYE such as overseas pensions. What you do is advise Inland Revenue of these other sources of income and ask it to adjust your PAYE tax code taking into effect this other income. It’s then taxed during the year through PAYE. By the way, this also is a good way of bypassing the provisional tax system.

This approach is something I saw a lot of when I worked in Britain. HM Revenue and Customs adjusted tax codes for the equivalent of New Zealand Superannuation and used adjusted tax codes to collect underpayments of tax for prior years. If you underpaid one year, your PAYE code for the following year would be adjusted to collect the underpaid tax. I think this is probably an easier system than expecting lump sum payments.

My view is Inland Revenue could make a lot more use of tailored tax codes and should do so proactively. It has the information to know when someone has started a second job or starts receiving paid parental leave. It can then contact that person and ask they want to have a secondary tax code or a tailored tax code. This may already be happening but people with new babies have plenty going on, so this sort of admin detail just slips off the radar. I think it’s something where Inland Revenue systems ought to be good enough to be able to actively encourage people to make greater use of these codes.

Snail farm in city office sparks tax avoidance probe

Finally, and returning to an earlier topic, rates, there’s a story from the BBC about a quite flagrant tax avoidance scheme in the UK. The story involves a commercial building in Liverpool and what’s happened is this building has been home to a snail farm for more than a year. The firm renting the premises has told Liverpool City Council that because the building is being used for agricultural use that part of the building is exempt from business rates. Otherwise, the rates bill would be about £61,000 for the whole building.

Understandably, Liverpool Council’s not impressed, and neither are other snail farmers. (Apparently snails retail for £14 a kilo). They think the scale of the operation isn’t realistic because according to the owner there are only two snails in each crate which has been done to avoid “cannibalism, group sex and snail orgies”. (Yikes!)

This seems a fairly flagrant tax avoidance case. And it’s caught the eye of Dan Neidle of the UK tax think tank Tax Policy Associates. As he notes you’d think this sort of thing would be struck down quite easily by the courts but not so. There doesn’t appear to be a specific anti-avoidance rule in the relevant legislation, and it appears that there’s quite an industry around so-called “business rates mitigation”. Astonishingly, a recent case involved a Crown organisation Public Health England attempting to bypass rates through one of these schemes. Dan has suggested that the new Chancellor of the Exchequer, (Finance Minister) Rachel Reeves, put in place legislation to strike this sort of activity down.

An opportunity here?

Under our rating legislation here I think that a similar scheme probably wouldn’t work. Based on what I understand our rating approach seems to be a bit more comprehensive. But one of the things I know about working in tax is that where people perceive there’s an opportunity to, let’s say, push the envelope, they will do so.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

We’re now in the third year of the pandemic and one of the things that’s emerged is our working patterns have changed as many people are working remotely, not just from home, but in completely different countries.

This has prompted Inland Revenue to issue an operational statement setting out what would be the obligations for a non-resident employer in relation to pay as you earn, FBT, and employer superannuation contribution tax. This applies where the employer is based in, say, the United States, but the employees are working remotely here. A scenario that I’ve seen quite a number of times in the past couple of years.

Basically, the operational statement confirms that a non-resident employer will have an obligation to withhold PAYE on payments to an employee if the employer has made themselves subject to New Zealand tax law by having a sufficient presence in New Zealand and the services performed by the employee are properly attributable to the employer’s presence in New Zealand.

What that means is if the employer has a trading presence in New Zealand, such as carrying on operations and employing a workforce, that’s normally sufficient for it to have PAYE obligations. And that would be, for example, it has a branch or a permanent establishment. Something always to watch out for is someone is signing contracts in New Zealand and performing those contracts in New Zealand with employees based here for that purpose. But no PAYE obligation arises where the employee decides I’m going to work/ return to New Zealand because it’s safer here, and I can work remotely. That case is not covered.

The paper gives a quick example of an architecture firm based in Boston and one of its employees, George lives in Wellington. George participates in virtual meetings, complete all his work in Wellington. But because the Boston firm has no New Zealand clients, all the work is carried out relates to American work, and the company has no obligation to deduct PAYE.

But what about George’s position here? And this is something that can slip through the details here. In some cases, he is treated as self-employed and pays provisional tax. That’s not technically correct. In fact, what he should do is to register as what they call an IR 56 taxpayer, and he files the employment information and pays PAYE to Inland Revenue. So literally he accounts for his own PAYE. Alternatively, the Boston firm could register as an employer and make the deductions on his behalf.

This is a scenario we’ve seen increasingly, so it’s useful to have some guidance from Inland Revenue in the form of this Operational Statement. It’s also worth pointing out there is also sometimes a double tax agreement applies which allows someone to work in New Zealand for up to 183 days, and there would be no obligation to withhold PAYE.

In addition to PAYE an overseas employer may also find itself with FBT and employer superannuation contribution tax issues if it decides to either voluntarily enter into the PAYE regime, or it has a sufficient presence that deems it to be an employer for PAYE purposes.

The complexities of overseas income

Moving on, it’s getting towards the mad rush for filing the March 2021 tax returns before the final date for tax agents on 31st March. The more complicated income tax returns will often involve overseas income, and Inland Revenue has just issued new guidance in the form of an Interpretation Statement on how to calculate the foreign tax credits that may be involved.

Now, this Interpretation Statement is very helpful because this is a surprisingly complicated topic. There’s a lot of detail involved in this. Firstly, we have to determine is the tax paid, for example, of substantially the same nature as the income tax that we charge. That’s not always the case. Because if the foreign tax is not covered by a double tax agreement and is not of the same nature as income tax imposed under our Act, no credit would be available.

That is something I’ve seen a little bit more of in relation to charges on pension withdrawals made by the UK and Irish governments. They’ve been imposing these charges recently where people have made early withdrawals from pension schemes. The amount imposed can be quite substantial – up to 55% in the case of the UK. The way the charges have been drafted they are outside the double tax agreements we have with the UK and Ireland. And in both cases, that means that there’s no credit for the withdrawal charge. So, a person may face a large charge from either Ireland or the UK and a tax charge here and have no relief for the charges imposed by the Irish and or UK governments. It’s a complicated topic and something to watch out for.

The first booby trap you have to watch carefully where a double tax agreement is involved is what the limits are and whether New Zealand actually has any taxing rights in relation to that income. That’s not always the case. But even when you get past those two positions in terms of calculating the credit, you then have to break it down into segments. They must be divided by country and then by type.

If you’ve had tax deducted of 20% from US sourced income and 10% from UK sourced income, you cannot just aggregate those two amounts and offset them against a single amount of overseas income that you report on your return. You have to actually break it down further than that by country and by type of income. And if you’ve got an attributing interest in a foreign investment fund income, that’s a separate calculation as well.

These are surprisingly involved calculations which although people think of as reasonably commonplace, have traps for the unwary in them. So I recommend having a thorough read of this new interpretation statement. It’s about 40 pages, and it can be found in the latest Tax Information Bulletin.

The proposed Social Insurance scheme may reduce fraud?

And finally, last week I was talking about the Government’s proposed social insurance. This proposes some form of unemployment insurance will be provided, as well as for sickness and other illnesses for employees and contractors alike. As expected, it’s generated a fair amount of interest together with some pushback about costs.

This week an article from Dr Eric Crampton, the chief economist with the New Zealand Initiative caught my eye. He suggested that the new scheme would generate a whole host of rorts. He based his commentary partly on his experience of what went on when a similar scheme was operating in Canada about 30 years ago. Firstly, he suggested employers would put seasonal contractors onto permanent contracts before making them redundant before the end of the picking season. And that would be a win for the employee because they would now qualify for up to six months support. Alternatively, an employer could sack a person who about to take paternity leave. By sacking them they’d get more than the current paternity parental leave payments of $621.76 per week.

Two things stand out. There isn’t much in this for the employer because it is basically fraud. I’m not sure many employers would want to be actively engaged in that. And for that matter, neither would employees. Some of the anecdotes that Dr. Crampton suggested sounded a little bit like, “Well, my friend on Facebook’s third cousin said this.”

But he does make a key point. Fraud is a potential issue for the scheme, and I see two areas where it could be a problem. Firstly, the obvious one – trying to make claims when a person is not eligible. The second area is where a person has a valid entitlement, but the amounts claimed are fraudulent because the numbers have been manipulated to over-state the person’s income.

Under the proposal, the Accident Compensation Corporation is to be responsible for the running of the scheme. Now it has a record of managing ACC fraud. Although interestingly, its latest annual report didn’t cite any numbers as to how much fraud was detected.

But I think if you are concerned about potential for fraud, then you should draw a lot of comfort from Inland Revenue’s enhanced capabilities following the completion of its Business Transformation programme, because the new START system gives Inland Revenue far more capability to analyse data.

And another thing here, which would be different from the stories of how similar schemes may have operated in the past in other jurisdictions, is that we have now Payday filing. This means there is near real time data of salary payments flowing through to Inland Revenue. So again, attempts to manipulate numbers should be picked up very quickly.

That still leaves the self-employed, where one report suggests under-reporting of income might be as much as 20% of income. But one thing that’s going on in relation to the self-employed and especially labour-only contractors, is payments to such persons are increasingly subject to pay as you earn and go through the Payday filing system. So again, Inland Revenue is monitoring payments which gives me some comfort in the matter.

But perhaps counter-intuitively, the introduction of social insurance may mean that we see a reduction in tax evasion. And that is with the opportunity that the social insurance payments represent, people will always want to make sure that they can maximise their benefits. It may well be that persons who previously underreported their income realise that although that might reduce a tax bill it’s no good if you fall sick or your contract is terminated. So, maximising their income is in their best interests.

In answer to Dr Crampton’s concerns about fraud, yes, it could happen. But I think the reality is Inland Revenue are far more sophisticated and have the tools to manage this issue than he gives them credit for. And secondly – as an economist, I’m sure he will appreciate this – perversely, there may be an incentive for people to start reporting their correct income to ensure that they maximise the benefit in case they need to make a claim.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and send me your feedback and tell your friends and clients. Until next time, kia pai te wiki, have a great week.

What are the “Unknown unknowns” of tax? Our 3 stories from the week in tax

The financial arrangements regime and Inheritance Tax

Wage theft and missing PAYE and KiwiSaver contributions

National’s tax policy – indexing thresholds, changes to the bright-line test and loss ring-fencing

Podcast transcript

In February 2002, in the run up to the invasion of Iraq, then U S Secretary of Defense, Donald Rumsfeld, commented;

“Reports that say that something has happened are always interesting to me because as we know there are known unknowns. There are things we know we know. We also know there are known unknowns. That is to say we know there are some things we do not know, but there are also unknown unknowns. The ones we don’t know, we don’t know and if one looks throughout the history of our country and other free countries, it is the latter category that tend to be the difficult ones.“

This quote was a core theme in my presentation last week to the Financial Advice New Zealand annual conference. The unknown unknowns are also a very difficult category in tax. And what are these unknown unknowns? The ones that trip up people because they didn’t know they were there.

Well in New Zealand the biggest culprit in this would be our financial arrangement rules. These rules have been around since 1986 and yet despite their very broad application, are largely unknown. I have come across CFOs who were completely unaware how they could apply.

Financial arrangements rules apply to just about any financial instrument you can think of. Mortgages, bank term deposit accounts, swaps, bonds, gilts in the UK phrase, all those all caught within it. It’s so broad it could apply to season tickets for public transport. And in one case I dealt with we thought that electricity contracts would be caught. Actually, we were debating whether in fact they were in the stock rules or in financial arrangement rules. Welcome to the arcane world of international tax.

But the financial arrangement rules are very broadly, largely unknown to individuals and they have particular bite in the foreign exchange field. That is where exchange rate movements such as is going on right now with Brexit which is back in the news again, so the Pound will move around.

Two groups of people get caught here. Obviously, investors who have bonds or term deposits denominated in an overseas currency, the value of the New Zealand dollar falls [that is more dollars are required to buy the offshore currency], they make an exchange gain and if the value rises, they have an exchange loss.

Then there are those with, for example, a rental property in the United Kingdom, and they have a mortgage there, it works the opposite way. The Pound may become weaker against the dollar so that in dollar terms, their mortgage diminishes, then that is income. Now on an unrealised basis for most people, this largely doesn’t matter, but very abrupt movements which add up to $40,000 on an unrealised basis will pull people into the foreign financial arrangements regime and they then will have to pay tax on unrealised gains.

The classic example I encountered was a client who had substantial property interests and mortgages in the UK. In year one there was an unrealised $300,000 foreign exchange gain, on the movement on the Sterling and had to cough up $100,000 in tax. The following year, it moved back the other way and she had a $300,000 loss but she never got that tax back. Even though there’s a wash up calculation when an arrangement matures or a mortgage rolls over and so of all the unders and overs are taken into account. But if you paid tax too soon in the piece, say you paid tax two years ago and then you find out that you actually never made any gain once everything is all closed out, you’ll never get the tax back. It’s one of the harsher parts of the financial arrangements regime.

The other trap is that the arrangements regime will apply to people who have total financial arrangements of $1 million or more and that is a gross amount. What I sometimes see is people may have $500,000 of term deposits and $500,000 of mortgages overseas mortgages and they think that after netting the two off, I’m below the threshold for the regime. Economically, your net worth comes out as nil. But financial arrangements regime takes them in aggregate so therefore the two are added together so the person actually has a million dollars in financial arrangements and is therefore within the accrual part of the regime. That person will be taxed on an unrealised basis.

The financial arrangements regime just the most common trap New Zealand advisors and clients fall into in my experience.

Following on from that, the other area that I’m seeing a lot more of is UK inheritance tax. Inheritance Tax is an estate and gift tax that applies to anyone domiciled in the UK or with assets in the UK.

Domicile, without getting in to too much detail, is a complicated concept, but basically, it’s where your permanent attachments are. I spoke in a previous podcast earlier about the unfortunate New Zealand woman whose Scottish partner died and because they weren’t married, she finished up paying £50,000 pounds inheritance tax on the transfer of his interest in the New Zealand property to her. So that’s not the first trap to watch for.

And I’m seeing more and more people caught by this, we have 300,000 Britons in the country. People like me, who’ve come from Britain, many more still have assets over in the UK. Maybe their children are going backwards and forwards to the UK and working there. And they’re all potentially all caught up in the inheritance tax regime.

A common thing that often gets overlooked is the implication of having assets in the UK or burial plots. Famously after Richard Burton died in 1984 the then HM Inspector of Taxes nailed his estate for inheritance tax on the basis that he had retained a burial plot in the village in Wales from which he came. So that was a very expensive burial plot as it turned out. I believe he actually is buried in Switzerland, but that’s how arcane the rules around inheritance tax are. It is the great unknown unknown. And as Donald Rumsfeld said, “These unknown unknowns tend to be the difficult ones.”

Earlier this week, Andrea Black who runs the excellent blog “Let’s Talk About Tax” went drinking with some young people. Actually, she was there to advise a group of hospitality workers who had been caught out as a result of Wagamama going into receivership. And the issue they were talking about is what’s called wage theft in the hospitality industry.

This is where the company, an employer, goes bust owing employees thousands of dollars in unpaid wages and salaries. There is often also a lot of unpaid pay as you earn floating around. There are several issues here. First and foremost, the employees have been left out of pocket and so they want to know what’s going on and when they can recover that. Then the tax man is very much often out of pocket. It often emerges that pay as you earn has been unpaid for several months an issue which I’ve seen this, and which Andrea talks about it as well.

You do wonder how quickly Inland Revenue reacts to this. Now I do hope that one of the things that will come out of Inland Revenue’s business transformation is much swifter responses to issues where pay as you earn falls into arears. My experience is Inland Revenue has let this go on for far too long. I’ve come across instances where there had been unpaid pay as you earn for going on for four years, which is just an absurd position. Someone there is either deliberately playing the system, in which case they should be hit with the full force of the law or is so hopelessly incompetent they should have been put out of their misery long ago.

Now the other thing that also comes into play for the employees is the unpaid employer KiwiSaver contribution and this adds up to quite a bit. Back in 2016 I spoke to Radio New Zealand about this matter.

At that time there was over $29 million dollars in outstanding KiwiSaver payments. In June 2015 1,663 employers had failed to pass on 15.3 million dollars in KiwiSaver payments deducted from employee’s salaries. Employees are missing out on this and on the employer contributions and it’s a real issue within the industry. Andrea asks whether the Small Business Council looked at this issue. We’ve delivered our report to the Minister and what I can say this matter did come into discussion during our deliberations.

It covers a number of matters. One is the question that we talked about previously about people with the incorrect prescribed investor rate. There’s also provisions making it easy for Inland Revenue to collect unpaid employer contributions in relation to KiwiSaver and ensuring employers pass on the employee contribution to Inland Revenue.

Hopefully employees will get the investment returns they’re missing out on because they haven’t been paid or the deductions and employer contributions haven’t yet hit their KiwiSaver account. By the way, submissions on that bill close on Monday so you’ve still got a chance to make a submission in support of that or raising other issues.

Finally, National have released their tax policy for next year. A number of things they are promising include tax cuts. Particularly they’re proposing something which I think is long overdue, and that is indexing tax thresholds. I think this is one of those quite sneaky tax increases that causes bracket creep and pushes people up into higher tax brackets gradually and it’s something which is effectively a tax increase by stealth. I think in the interest of transparency it’s a good move.

There’s a number of interesting other matters they want to deal with. That said, I’m not entirely sure if you are not a homeowner or rental investor and you’re trying to get into the investment property or to rent a property you’d appreciate what they’re proposing. They want to dial back the bright line test for residential property from five years to two years and remove loss ring fencing, which is a big break for tax investors.

That brought a fairly forthright denunciation from Jenée Tibshraeny. She also was less than impressed by the idea of removing the inflation component of interest. It’s an arcane point which has been talked about for some time which although it sounds arcane it is actually quite important.

Anyway, that will be the first shots fired in next year’s election about tax policy. All eyes will be on what the coalition will do in next year’s Budget. Given that tax thresholds haven’t been raised for more than 10 years by that time it’s hard to imagine that they wouldn’t try and do something, particularly when they’re running a surplus. I mean, cynical tax cutting budgets are not just the preserve of right wing governments. But we shall wait and see.