Plenty to consider in Inland Revenue’s latest Interpretation Statement on tax avoidance

Working from home allowances updated

GST and Donation Tax Credit fraudsters convicted

Last year, I covered the Supreme Court decision in Frucor Suntory New Zealand Ltd v Commissioner of Inland Revenue. To recap, Frucor had entered into a series of arrangements mainly for the benefit of its overseas parent. However, in the eyes of the Commissioner these arrangements represented tax avoidance. By a majority of 4 to 1, the Supreme Court ruled that the arrangements did indeed represent tax avoidance, and they also met the threshold for the imposition of shortfall penalties totalling $3.8 million. What was also of particular note here was the very strong dissenting judgement from Justice Glazebrook, which was completely at odds with the majority opinion.

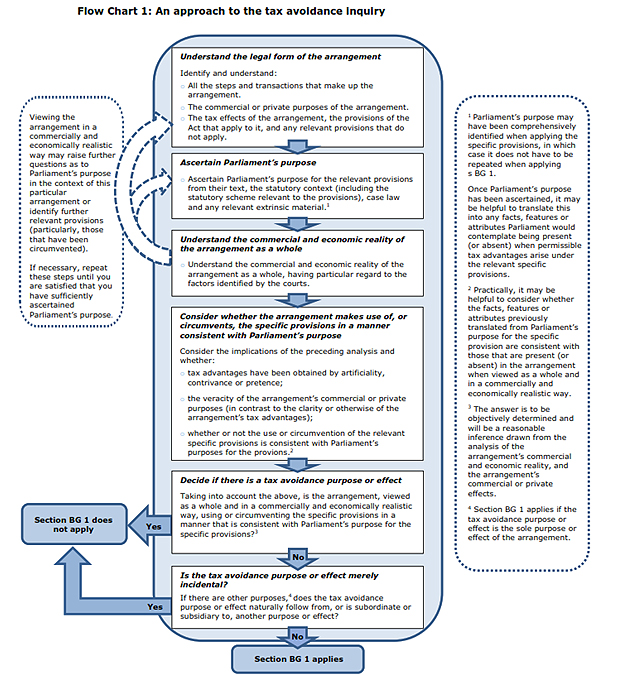

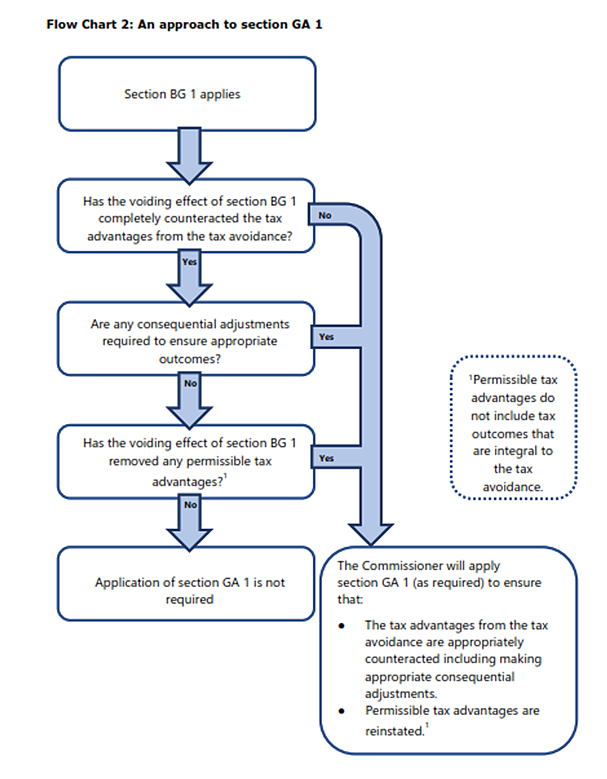

Following the Supreme Court decision, Inland Revenue have now released an updated Interpretation Statement IS23/01 Tax avoidance and the interpretation of the general anti avoidance provisions of sections BG 1 and GA 1 of the Income Tax Act 2007. This 138-page Interpretation Statement is accompanied by a nine-page fact sheet and two Questions We’ve Been Asked covering income tax scenarios on tax avoidance, which amount to another 50 pages or so. A fair amount of material to work through.

The statement sets out the Commissioner’s approach to the application of Section BG 1 and then explains how under the related section J1 the Commissioner may act to counter it. And counter any tax advantage that a person has obtained from a tax avoidance arrangement. This Interpretation Statement is also relevant to the general anti-avoidance provisions in section 76 of the Goods and Services Tax Act 1985. This Interpretation Statement also replaces the previous Interpretation Statement is 13 zero one issued on 13 2nd June 2013.

The statement sets out the Commissioner’s approach to applying section BG1 and then explains how under the related section GA1 the Commissioner may act to counteract any tax advantage that a person a obtains from a tax avoidance arrangement. The Statement is also relevant for the general anti avoidance provision in Section 76 of the Goods and Services Tax Act 1985. It replaces the Commissioners previous Interpretation Statement IS13/01 issued on 13th June 2013

For those unfamiliar with these provisions, section BG1 is the main anti avoidance provision in the Income Tax Act. If applicable it will void a tax avoidance arrangement for income tax purposes. The related section GA1 then enables the Commissioner to make adjustments where an arrangement voided under section BG1 has not “appropriately counteracted” any tax advantages arising under the tax avoidance arrangement.

The key case relating to these anti avoidance provisions is the Supreme Court decision in Ben Nevis Forestry Ventures Limited in 2008. In that decision the Supreme Court adopted the principle of Parliamentary Contemplation in determining how the anti-avoidance provisions were to be applied. In brief Parliamentary Contemplation requires deciding whether the arrangement when viewed as a whole and in a commercially and economically realistic way makes use of or circumvents specific provisions in a manner consistent with parliament’s purpose. If not, the arrangement will have a tax avoidance purpose or effect. Subsequent to the Ben Nevis decision this principle of Parliamentary Contemplation was applied in the well-known Penny and Hooper case, and again in the Frucor decision.

It would be foolish to think these tax avoidance provisions only apply to major corporates. as I’ve just mentioned the principles were relevant in the Penny Hooper decisions and at last week ATAINZ conference the point was made that section BG1 could be applied in circumstances where a person’s lifestyle appears to rely on payments and distributions from a trust because it is in excess of that person’s reported salary.

Just as an aside, apparently in March 2021, almost $11 billion in dividends were paid prior to the increase in the top personal tax rate to 39%, with effect from 1st of April 2021. Now, that is more than four times greater than the usual amount of dividends paid at that time of year. I understand Inland Revenue is discussing the pattern of distributions with some tax agents.

The issue tax agents, advisers and clients should be aware of is where there is no regular pattern of distributions, even though profits were available, but suddenly there’s a very big distribution in this particular year. You could be vulnerable to Inland Revenue looking at that and saying, “Well, you paid a big dividend in March 2021, but you haven’t paid similar dividends in March 22 or March 23. Why is that? Nothing to do with the new 39% personal tax rate?” So just to reinforce these tax avoidance provisions, the case law may generally involve large corporates, but they are very relevant to small and medium enterprises.

Fortunately, there’s some good examples accompanying the Interpretation Statement and give you guidance as to where the Inland Revenue think the boundary might apply. For example, and this is a very common scenario, a company is wholly owned by a family trust. Over some years the trust has advanced $1 million to the company as shareholder advances on an interest free repayment on demand basis. The company has then used these funds to finance its business operations for the purpose of deriving assessable income.

The trustees decide to demand repayment of the full amount of the loan. In order to make that repayment the company borrows $1 million from a third-party lender at market interest rates secured over the assets of the trust. The $1 million loan is then used to repay the shareholder advances. The company deducts the cost of borrowing from its income. Meanwhile, the trustees have used the funds to purchase a holiday home for the trust’s beneficiaries.

As I said, this is a not uncommon scenario. But does it represent tax avoidance? No, according to the Commissioner. Which is a relief but be careful of relying on that particular set of circumstances, there may be a little twist in your tale, which may interest the Commissioner.

Another example is where a taxpayer with a marginal rate of 39% invests in a portfolio investment entity where the maximum prescribed investor rate is 28%. This would not constitute tax avoidance because the tax advantage of the maximum prescribed investor rate of 28% is within Parliament’s contemplation.

On the other hand, an example is given of an investor whose tax rate is 39%. He borrows funds from a bank to invest in a Portfolio Investment Entity (PIE) sponsored by the same bank. The policy of this PIE is to invest all funds in New Zealand dollar interest-bearing two-year deposits with the bank.

In this situation, this arrangement would represent tax avoidance. The key facts being the somewhat circular nature of the investment, but critically the fact the return is less than the cost of borrowing, resulting in a pre-tax negative, i.e. a loss position, but a post-tax positive net return. Once you look at the interest earned and the tax rate 28% tax rate, there’s a deduction available to the investor at 39% effectively. But the PIE income is only taxed at 28%.

This got me thinking because it suggests the well-known practice of negative gearing to purchase investment properties might in some circumstances represent tax avoidance. Now, this is less likely following the introduction of the loss ring-fencing rules and interest limitation rules in 2019 and 2021, respectively. But it’s another case where you ought to think carefully about how Inland Revenue might view a particular transaction.

As you can see, there’s a considerable amount of material and reading to work through including some useful flow charts (see below). At a minimum, I would suggest reading the Fact Sheet and the two Questions We’ve Been Asked which accompanied the Interpretation Statement.

You can also find some excellent commentary by the Big Four accounting firms. They’re always worth reading on these matters as they’ve got the resources to really go in and consider what these Interpretation Statements might mean. (And no doubt it’s particularly relevant for their clients).

Like some, I have my reservations about the Parliamentary Contemplation test. I think it was Rodney Hide who remarked about the principle “When I was in Parliament, most of the time I was contemplating what I was going to have for dinner”. Joking aside, I feel we should be approaching the test with some caution. I also think Justice Glazebrook’s dissent in Frucor raised valid concerns about how these provisions would apply. As I mentioned at the time, she comes from a very experienced commercial and tax background which is one reason why her dissent was raised a few eyebrows in the tax world.

Notwithstanding all of that, the Frucor and Ben Nevis cases are the law. And with the release of this Interpretation Statement and related material, taxpayers now should have a clearer idea where the boundaries lie. More examples from Inland Revenue around where they see the boundaries applying would be a great help in continuing to clarify the position. As always, we’ll bring you developments as they emerge.

Reimbursement for working from home

Now, moving on, we’ve discussed in the past how the impact of the pandemic and the resulting shift to more people working from home meant Inland Revenue had to quickly reconsider the treatment of reimbursing payments made to employees who work from home and for using their own phones and other electronic devices as part of their employment. Inland Revenue released a series of determinations giving some guidance as to the appropriate level of reimbursement.

Inland Revenue has just issued an updated determination which will, once it’s gone through consultation, apply from 1st April. It basically updates these previous determinations and gives a little bit more leeway in terms of the amounts allowed. The reimbursement allowance for employees working from home has increased from $15 per week to $20 per week. The previous limit of $5 per week for person use of telecommunications tools is now $7 a week. I feel these amounts are on the low side, but at least Inland Revenue is revisiting the matter and updating them to take account of inflation. So that’s welcome.

Jail for tax fraud

And finally this week news about convictions involving tax fraud. Firstly, a former developer who apparently lived in Manhattan before he migrated here in 2016 on an entrepreneur residency visa, has just been jailed for tax fraud relating to $1.5 million in fraudulent GST refunds. He had bought a vineyard in Canterbury and then filed fraudulent GST returns between April 2017 and April 2021 in relation to the purchase and operation of this vineyard. He received over $1.3 million in GST refunds, but a further $175,000 was withheld once Inland Revenue realised what was happening in April 2021.

He’s been jailed for a total of three years and seven months. One other thing of note is Inland Revenue has taken court action to recover what was fraudulently obtained. Unusually it also took a high court freezing order out and had a receiver appointed over the assets of the vineyard owning company. So good move from Inland Revenue. That’s what we expect them to be doing.

The case does raise an issue though, because it was four years before Inland Revenue detected this fraud. And so, again, you just wonder that hopefully this was because during this period it was going through its Business Transformation program. So, you would hope that now Inland Revenue, with its enhanced capabilities, is picking up on these frauds much quicker.

In a related release, five members of the Samoan Assembly of God Church in Manukau have been sentenced to community detention and ordered to repay the money they received after they made false donation tax credit claims worth almost $170,000. They apparently used not only false donation credits for themselves, but also asked other individuals, usually members of their own congregation for personal information, including their IRD numbers. They then using these details issued a series of false donation receipts. The fraud was detected by Inland Revenue and the five were charged. All have pleaded guilty and received various sentences mostly involving community detention but also reparations and repayment of the funds claimed.

I often see a lot of feedback around the charitable exemption particularly in relation to businesses. It’s a touchy point. One of the areas where the Tax Working Group had concerns was about whether the donations once received were actually being applied for charitable purposes.

Now, I don’t know whether this particular case is just one of those scenarios where Inland Revenue came across it and acted or it’s part of a general operation where it’s looking more closely at what’s happening with charitable donations and whether in fact, they’re being applied to charitable purposes. We’ll find out in due course.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Change on the way for GST recordkeeping requirements

A clear-eyed dissent by a Supreme Court justice

Tax revenue exceeds $100 billion for the first time

Over the next few months, GST registered businesses will receive a stream of information from Inland Revenue explaining new recordkeeping requirements for GST purposes, which will take effect from the 1st April next year. These changes relate to what information needs to be shared or retained to support GST input tax claims.

These changes are permissive in nature, and existing invoicing practises and systems which are compliant with the previous GST rules will still remain compliant with the new information rules. The new rules are less prescriptive about the information required to support a GST input tax claim.

The key purposes of these changes are to try and reduce compliance costs for businesses and facilitate the introduction of e-invoicing. The changes will be done by way of requiring the supplier and recipient of a taxable supply to retain a minimum set of information relating to that supply. The current rules, which required formal documents such as tax invoice, credit notes, debit notes etc. to support input and output tax will be repealed.

One of the most noticeable changes will be that there will no longer be a requirement for an invoice to have the words ‘Tax Invoice’ in a prominent place. Tax invoices will now be caught termed ‘taxable supply information’ and the former debit and credit notes which had to be issued when a correction was made, will now be termed ‘supply correction information’, which is better terminology as it actually reflects what’s going on.

There are also changes to the buyer credit created tax invoice regime which are now called ‘buyer created taxable supply information’. And these changes have already come into effect and actually are pretty helpful because you now no longer need to get Inland Revenues permission to operate the buyer created taxable supply information.

There will be a minimum set of information required to be retained in business records under the new rules for a taxable supply. According to Inland Revenue these rules are generally consistent with the requirements of commercial contract law relating to invoicing and recordkeeping. The requirement to hold a tax invoice in order to claim an input tax deduction is now replaced with the requirement to have business records showing that GST has been borne on the supply.

Now key information for both a supplier and a recipient of a supply of goods or services is that of, ‘supply information’. This includes, at a minimum, all the following information:

– the name and registration number of the supplier,

– the date of supply,

– a description of the goods or services, and

– the amount of consideration for the supply.

Helpfully, the low value transaction threshold for taxable supplies has been increased from $50 to $200. And that is part of a drive to simplify recordkeeping requirements for a large number of low value transactions.

There are now three value thresholds for the general meaning of taxable supply information and the information requirements for each of these are mutually exclusive. The thresholds are:

– Supplies exceeding $1,000,

– Supplies between $200 and $1,000,

– and then those for supplies not exceeding $200.

All these changes come into effect from 1st April next year, although, as I mentioned, the changes to the buyer created taxable supply information have already taken effect. As noted, existing systems will still remain compliant. So, there’s no need to dramatically go out and change everything to meet the new requirements. Inland Revenue will continue to release information about the changes over the coming months.

Supreme Court justices display worrying lack of tax knowledge in key decision

Last Friday, the Supreme Court released its decision in the case of Frucor Suntory New Zealand Ltd v Commissioner of Inland Revenue. This case has been watched with some keen interest by tax professionals. It relates to a series of transactions that took place in 2003, as a result of which DHNZ, a predecessor to Frucor Suntory, claimed interest deductions totalling $66 million in respect of an advance made by Deutsche Bank.

Inland Revenue sought to restrict the interest deductions totalling just over $22 million dollars claimed for the 2006 and 2007 income years on the grounds the funding arrangements constituted tax avoidance. Just for good measure, they also levied shortfall penalties totalling $3.8 million for the two years because they considered the tax avoidance was abusive.

The case reached the High Court in 2018, which ruled in favour of Frucor which was something of a surprise at first sight for those not familiar with the facts. Inland Revenue unsurprisingly appealed the decision and in 2020 the Court of Appeal held that the deductions did represent tax avoidance. However, the Court of Appeal did not accept the criteria for shortfall penalties had been met, so both parties were unhappy with their decision and naturally both appealed to the Supreme Court.

Last Friday it ruled by a 4 to 1 majority that the arrangement did represent tax avoidance and the shortfall penalties were correct as the tax position adopted by DHNZ (Frucor) was unacceptable and abusive as DHNZ acted with the dominant purpose of obtaining tax advantages.

Now, in some ways, the Supreme Court’s ruling is unsurprising. New Zealand courts have taken a fairly hard line on what is perceived as tax avoidance for the last 15 years or so. But there’s still a number of points of interest here. Firstly, you will note the length of time involved: the transaction happened in 2003. The assessments, which are the subject of the appeal, were for the 2006 and 2007 tax years. And there’s nothing I’ve seen yet explaining why it took nearly so long to reach the High Court. Under the principle of justice delayed is justice denied it’s concerning to see the amount of time involved.

Then there is the imposition of shortfall penalties, which seems harsh. If you are taking something all the way to the Supreme Court, you know you’re arguing on the margins. Nine judges looked at the matter and five said no shortfall penalties were appropriate. The only four that did think they were appropriate were the ones that mattered most because they were all on the Supreme Court. And you often see this in in court cases, the lower courts rule one way and then the Supreme Court says, nope, it’s the other way, and that’s the end of it.

But most interesting of all is the strong dissent by Justice Glazebrook in the Supreme Court now. Dissenting justice judgements are often very interesting reads, and I suspect Justice Glazebrook’s will be read and examined in quite considerable detail, given what she rebutted completely the principles adopted by the other four justices. Just for the record it’s worth noting that before she became a judge back in 2000, Justice Glazebrook was a tax partner in a law firm. She’s actually one of the co-authors of a book on the financial arrangements regime. In fact, the first edition, published back in 1999, is still had not yet been updated. So she’s got a good background in tax.

But the paragraph, I think is going to raise a few eyebrows is the penultimate one of her judgement.

[247] “The majority say that the dominant purpose of the arrangement in this case was to reduce the tax liabilities of Frucor. This despite the fact that the whole reason for the restructuring was to ensure that Danone Asia did not incur tax liabilities in Singapore, unlike the position before the refinancing where direct debt funding was provided by Danone Finance. Given that, before the refinancing, Frucor was deducting interest payments roughly equivalent to the amounts it claimed deductions for under the current arrangement, it is difficult to see how its purpose could have been to achieve a result it was already receiving (deductibility of interest) and thus difficult to see its dominant purpose as being to reduce its tax liabilities or to achieve an illegitimate tax advantage in New Zealand.”

Now that’s quite some paragraph, I have to say I don’t think I’ve seen for a while a judgement where you’ve got such completely opposite views on between the judges.

You often see differences in interpretation, but here there’s a very marked difference on the core of the case. Justice Glazebrook has questioned how it is tax avoidance in New Zealand when you consider that the real purpose of the restructure was to resolve a tax problem for the offshore parent.

It will be interesting to see feedback from other, more experienced legal practitioners and tax specialists who work in this space about this decision. As I said, I find Justice Glazebrooks dissent there quite strong, and I suspect it will generate quite a bit of commentary.

Hiding the effect of fiscal drag

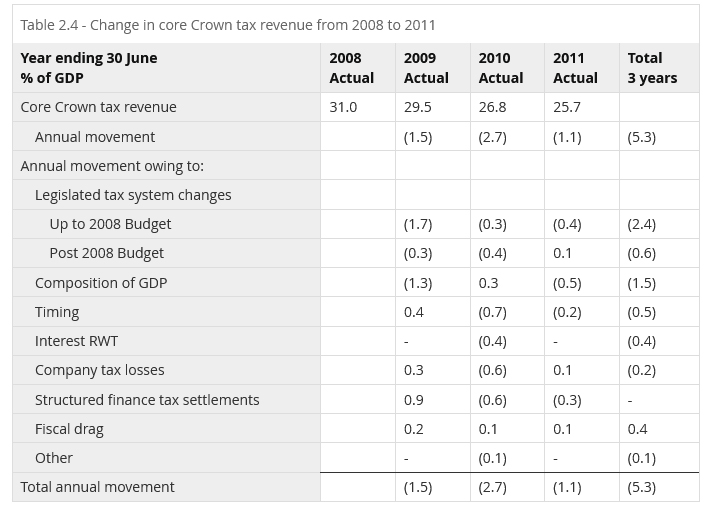

Moving on, the Government published its financial statements for the year ended 30th June 2022 on Wednesday. As you no doubt are aware by now these turned out to be better than expected and have generated quite a bit of chatter around the overall tax burden and the implications for next year’s election.

From a tax perspective, what’s interesting to see is the strong rebound in company income tax. The forecast in the 2021 Budget was that corporate tax would be just over $13 billion. By the time of this year’s budget in May the estimate had risen to $17.25 billion. In fact the total for the year was just under $19.9 billion.

For individuals the tax source deduction payments (PAYE) are up. Two factors are at play here: the well-known one of fiscal drag or bracket creep which means as people’s wages rise, they cross tax thresholds and their tax increases. On top of that, you’ve got the introduction of the new 39% tax rate. Those two combined, according to the commentary to the financial statements, represented about $1 billion of extra tax.

You have to dig very hard to find out what is the effect of bracket creep or fiscal drag, because that’s not being reported in the budget statements. You can draw your own conclusions as to why that is so. But we do know that when it was included in the 2012 Budget the effect was between 0.1 and 0.2% of GDP.

At a rough guess the current effect of fiscal drag would be somewhere around $500 Million a year.

The GST take rose to $43 billion gross with the net GST for the year being $26 billion through. Overall, as I mentioned at the top of the podcast, tax revenue, including indirect taxation, exceeded $100 billion for the first time at just under $107.9 billion.

So, lots of excitable chatter about what that means politically for tax cuts and other changes. Speaking on RNZ’s The Panel yesterday afternoon, (about 12 minutes in) I reiterated what I have said elsewhere that we need to do more about the tax brackets at the bottom end because that’s where the effects of fiscal drag are the hardest. The non-indexation of income tax and Working for Families thresholds means there are people on say $50,000 a year & receiving Working for Families who are on an effective marginal tax rate of 57%.

Roasting the idea of GST exemptions

Obviously what went on over in the UK has also attracted attention. This week the UK Government abandoned its higher rate tax cuts in the face of extreme political pressure from all sides, including Conservative MPs. It’s been very interesting and entertaining to watch a really classic example of the “Order, Counter-order, Disorder” maxim. And I do wonder how Prime Minister Liz Truss and her [Finance Minister] Kwasi Kwarteng are going to survive.

And finally, speaking of the UK, one of the things that comes up in discussions about how do we help with the cost of living is a not unreasonable suggestion on the face of it, to remove GST on certain foods. Now I’m in the GST purist camp here. I don’t believe we should do that. To repeat a point I’ve made several times, if you are trying to help people who have not enough income, give them more income. Any changes to the GST system such as zero-rating food benefits everybody and therefore are also more expensive as a consequence. And that idea of targeted assistance is consistently noted by the Tax Working Group and also the Welfare Expert Advisory Group.

But there’s another reason why you wouldn’t want to do it unless you wanted some inadvertent laughs. And that is the absurdity of the distinction which happens at the point where you are trying to determine whether a particular product is zero rated or standard rated. Now, Britain, with its VAT (value added tax) regime, has produced a number of very entertaining cases on this. I think people may be aware of the Max Jaffa case, which involves the distinction between a biscuit (standard rated) and a cake (zero-rated).

But this week I was alerted to one which is even more spectacularly hilarious, and it involved marshmallows of unusual size, which really sounds like something a line from The Princess Bride. A VAT tribunal case ruled that marshmallows of an unusual size are 0%, but standard sized marshmallows were standard rated at 20%. As one commentator noted, it’s sometimes very difficult to decide whether a VAT case is indistinguishable from satire.

This case involved a £470,000 dispute between Innovative Bites Ltd and H.M. Revenue Customs about the product “Mega marshmallows”. The VAT tribunal ruled that mega marshmallows were zero rated because they have to be roasted before they could be consumed and therefore not a standard rated snack.

On that bombshell, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Last week I mentioned that Inland Revenue had released a discussion document, Dividend Integrity and Personal Services Income Attribution, which set out its proposals for measures to limit the ability of individuals to avoid the 39% or 33% personal income tax rate through use of a company structure. This is what we call integrity measures designed to support the integrity of the tax system. In this case, the proposals are to support the objective of the increase in the top tax rate to 39% and to counter attempts to avoid that rate by diverting income through to entities taxed at a lower rate.

Now this paper is pretty detailed and runs to 54 pages. There’s a lot in here which will get tax agents and consultants sitting upright and reading the fine print as in some cases they will be affected directly. It’s actually the first of potentially three tranches in this area. Tranches two and three will consider the question of trust, integrity and company income retention issues, and finally integrity issues with the taxation of portfolio investment income. And the reason for the last one is that portfolio investment entity income is taxed at the maximum prescribed investor rate of 28%, which is undoubtedly attractive to taxpayers with income which is now taxed at the maximum tax rate of 39%.

The Inland Revenue discussion document has three proposals. Firstly, that any sale of shares in the company by the controlling shareholder be treated as giving rise to a dividend for that shareholder to the extent the company and its subsidiaries has retained earnings.

Secondly, companies should be required on a prospective basis, i.e. from a future date, to maintain a record of their available subscribed capital and net capital gains. These can then be more easily and accurately calculated at the time of any share cancellation or liquidation. That’s a relatively uncontroversial proposal.

And thirdly, the so-called “80% one buyer test” for the personal services attribution rule be removed. This one will probably cause a bit of a stir.

The document begins by explaining these measures are required to support the 39% tax rate. There’s a lot of very interesting detail in this discussion, for example it notes that with the top tax rate of 39%, the gap between this and the company tax rate of 28% at 11 percentage points is actually smaller than the gap in most OECD countries.

But then, as the document says, “However, New Zealand is particularly vulnerable to a gap between the company tax rate and the top personal tax rate because of the absence of a general tax on capital gains.”

And so to repeat a long running theme of these podcasts, this lack of coverage of the capital gains has unintended consequences throughout the tax system. And this question of dealing with this arbitrage opportunity between differing tax rates is, in essence, a by-product of that.

As Inland Revenue notes, one answer would be to align the company, personal and trust tax rates. This was the case until 1999, when the rate was 33% for companies, individuals and for trusts. But this ended on 1 April 2000 when the individual top rate went up to 39%. And since then, the company income tax rate has fallen to 28%.

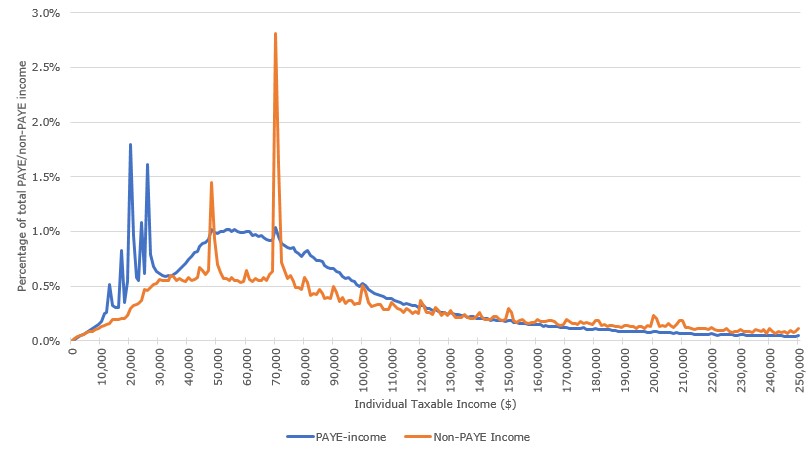

So this is a matter which needs to be addressed. There’s a really interesting graph illustrating the distribution of taxable income and noting there’s a huge spike at around $70,000, where the tax rate rises to 33%.

Taxable income distribution: PAYE and non-PAYE income (year ended 31 March 2020)

There’s also some interesting data around what high wealth individuals pay in tax. For the 2018 income year, Inland Revenue calculated the 350 richest individuals in New Zealand paid $26 million in tax. Meanwhile the 8,468 companies and 1,867 trusts they controlled, paid a further $639 million and $102 million in tax respectively, indicating a significant amount of income earned through lower rate entities.

It appears to Inland Revenue that tax is being deferred through retention of dividends in companies.

The opportunity in New Zealand is that a sale of the shares under current legislation would bypass the potential liability on distribution. The shareholder is basically able to convert what would be income if it was distributed to him or her, to a capital gain. And clearly, the Government wants to put an end to that, but can’t because it doesn’t have a capital gains tax. The discussion document therefore proposes that any sale of shares in the company will be deemed to give rise to a dividend. This will trigger a tax liability for the shareholder.

The paper goes into detail around this particular issue, and I think this is going to be quite controversial. Because although I could see a measure where a controlling shareholder sells shares to a related party such as, for example, someone holding shares personally sells them to a trust or to a holding company, which they control. You could see straight away that Inland Revenue could counter this by arguing it’s tax avoidance.

But the matter gets more complicated where third parties are involved. And this is where I think the rules are going to cause some consternation because it proposes transactions involving third parties would also be subject to this rule. That, I think is where most pushback will come in on this position. Without getting into a lot of detail on this there could be genuine commercial transactions resulting in some might say is a de facto capital gains tax.

The proposal is not all bad. If a dividend is triggered, then the company will receive a credit to what is called its available subscribed capital, ie, its share capital, which can later be distributed essentially tax free.

In making its proposals, the paper looks at what happens in Australia, the Netherlands and Japan and draws on some ideas from there. It’s interesting to see Inland Revenue looking at overseas examples. All three of those jurisdictions, to my knowledge, have capital gains tax as well, but they still have these integrity measures.

But the key point is this question that any sale, will trigger a dividend. There’s no de-minimis proposed. This could disadvantage a company trying to expand by bringing in new shareholders. It might have to use cash reserves it wants to keep to pay the withholding tax on the deemed dividend. The potentially adverse tax consequences for its shareholders might hinder that expansion. I expect there will be a fair degree of pushback as a lot of thought will go into responding to this proposal. It will be interesting to see exactly what comes back.

Cleaning up tracking accounts

Less controversial and something probably overdue, is the proposal for what they call tracking accounts to cover the question of a company’s available subscribed capital, and the available capital distribution amounts realised from capital gains. Both of these may be distributed tax free either on liquidation or in a share cancellation in the case of available subscribed capital. But the requirement for companies to track this is rather limited, and these are very complicated transactions.

As the paper points out, the definition of ‘available subscribed capital’ runs to 40 subsections and 2820 words. So, there’s a lot of detail to work through, and if companies haven’t kept up their records on this, then confusion may arise if, say, 10 years down the track they’re looking to either liquidate or make a share cancellation.

I don’t see this proposal causing much controversy. I think Inland Revenue’s proposals here are fair and probably something that should have been done a long time ago. They will apply on a prospective basis, as I mentioned earlier on.

Personal services income attribution – a 50% rule?

And then finally, the third part deals with personal services income attribution. And what this part does is picking up the principles from the Penny and Hooper decision. This was the tax case involving two orthopaedic surgeons, which ruled on the tax avoidance issues arising from the last time the tax rate was increased to 39%.

The discussion document is basically trying to codify that decision. The intention is to put an end to people attempting to use what you might call interposed entities, lower rate entities, to avoid paying tax personally. The particular issue it’s driving at is when an individual, referred to as a working person, performs personal services and is associated with an entity, a company usually, that provides those personal services to a third person, the buyer.

Inland Revenue is now looking at a fundamental redesign of this personal service attribution rule, which was designed to capture employment like situations. It was really designed where contractors might be providing services to basically one customer (the ‘80% one buyer rule’) and in effect, they were employees. However, they could potentially avoid tax obligations by making use of an interposed entity with a lower tax rate.

Inland Revenue thinks that 80% rule is too narrow. The proposal is to broaden its application and by doing so it can at the same time deal with the issue that arose with the Penny and Hooper case.

Under current legislation, Bill is an accountant who is the sole employee and shareholder of his company A-plus Accounting Limited. The company pays tax at 28% on income from accounting services provided to clients and pays Bill a salary of $70,000, just below the 33% threshold. Any residual profits are either retained in the company or made available to Bill as loans.

The proposal is to remove that 80% one buyer rule and so that now Bill’s net income for the year, if it exceeds $70,000 will all be attributed to him where 80% of the services sold by that company are provided by Bill. Sole practitioners and smaller accounting firms and tax agents will find themselves in the gun. In fact, the discussion document suggests maybe this threshold of 80% should be lowered to 50%.

Now, you might think that the bigger issue is not the 33% threshold at $70,000, but the $180,000 threshold, so why do we want such a low threshold for this rule to apply? The discussion document points to the evidence that shows that there is income deferral going on. It appears to be at the $70,000 threshold (see the graph above) and wants to put an end to that.

So that’s a more detailed look at what is a very important paper. It’s likely to generate quite a lot of controversy and feedback from accountants and other tax specialists. It’s also another part in the long running tale of the implications of not having a capital gains tax. But certainly, this one will run and run. Submissions are now open and will run through until 29th April. I expect all the major accounting bodies and firms will be responding.

Using tax to mitigate cost of living impacts

Moving on briefly, there’s been a lot to talk about what tax changes could be done to help the increased cost of living. And Daniel Dunkley ran through some of the proposals.

One idea that pops up regularly is the question of removing GST from food. My view, which I expressed to Daniel and is also probably that of most tax specialists, is that this would undermine the integrity of GST, because we don’t have any exemptions on that.

I also don’t think it would achieve the objective that is hoped for. There is, regardless of what people might say, an administrative cost to splitting out tax rates, having zero rate for food and standard rate for other household goods in your shopping trolley. And that differential, that cost involved, will be passed on to customers.

So the full effect of the GST decrease will never flow through to customers. To be perfectly frank; supermarkets and operators will play the margins around this. I suggest you have a look at what’s happened with the fuel excise cut. It was 25 cents, but in every case did the pump price fall by 25 cents? And how could you tell because prices move around so much?

As I said to Daniel, and has been a longstanding view of mine, if the issue is getting money to people who have not enough money, give them more money. The Welfare Expert Advisory Group was staunch when it said that there was a desperate need to raise benefits. We also saw how the temporary JobSeeker rate was increased when COVID first hit. So, this issue of increasing benefits hasn’t gone away.

The best position would not be to tinker with the tax system. You could perhaps look at tax thresholds, definitely, but they still would not be as effective as giving people an extra $30-40 or more cash in hand.

End of year preparations

And finally, the end of the tax year is fast approaching, so there’s plenty of tax issues that you might want to get done before 31st March. A key one to think about is if you’re going to enter the look through company regime, you need to get the election in before the start of the tax year. In some situations you might have more of a bit of a grace period for dropping out of the regime, as part of the Government’s response to the Omicron variant. But it you are electing to join the regime, I suggest you file the election on or before 31st March.

Coming back to companies and shareholders another important issue is the current accounts of the shareholders. You should check to see if any shareholder has an overdrawn current account (that is more drawings than earnings). If so, then either see about paying a dividend or a salary to clear that negative balance, although of course, you’re up against the issue of the higher tax rate I discussed earlier. If that’s not possible, charge interest at the prescribed fringe benefit tax rate of 4.5%.

Companies may have made loan advances to other companies, look at those carefully because you may need to charge interest there to avoid what we call a deemed dividend.

Another very important matter is if there are any bad debts. If so, then consider writing them off before 31st March in order to claim a deduction. And then if you’re thinking about bringing forward expenditure to claim deductions such on depreciation, then do so.

Companies should check their imputation credit accounts balances and make sure these are positive. There are mechanisms through tax pooling to manage this problem if you miss a negative balance.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax tax or wherever you get your podcasts. Thank you for listening, and please send me your feedback and tell your friends and clients. Until next time, ka pai te wiki, have a great week.

The background facts are complicated, but basically the case involved an advance of $204 million dollars to Frucor in exchange for a fee and some convertible notes issued by Frucor to Deutsche Bank. There was a related party payment from Frucor’s then Singapore based parent for the purchase of the shares from Deutsche Bank.

Over a five year period Frucor paid Deutsche Bank $66 million dollars on an interest only basis. Inland Revenue argued to this was a tax avoidance arrangement and for the 2006 and 2007 income years disallowed deductions to the extent of $10.8 million and $11.6 million respectively.

Frucor won this case in the High Court in 2018, a decision which actually raised a few eyebrows in the tax advisor industry because it seemed similar to the arrangement struck down involving the big Australian banks about 10 years ago.

Unsurprisingly, Inland Revenue appealed and have now won in the Court of Appeal. Under the arrangement, Frucor had apparently achieved interest deductions totalling $66 million. But in the court’s view, it had not incurred a corresponding economic cost for which Parliament intended deductions would be available. $55 million as a matter of commercial and economic reality of the claimed interest was in fact a repayment of principal borrowed and not an interest cost. The Court concluded that the funding arrangement had tax avoidance as one of its purposes or effects and was this was not merely incidental to some other purpose. The overall purpose of the funding was provision of tax efficient funding to Frucor.

The only bright spot in this decision for Frucor is that the Court of Appeal agreed the High Court was reasonable to find that the shortfall penalties for a tax avoidance arrangement (which can be up to 100% of the tax avoided) should not have been imposed by Inland Revenue.

The key lesson here – and it’s going to be of importance looking forward if Labour forms the next government, given its announcement for a higher personal tax rate – is that the courts are still very much onside with striking down tax avoidance cases where they consider the arrangements are not seen to be in line with Parliament’s intention. And Inland Revenue has made aggressive use of tax avoidance provisions in section BG 1 of the Income Tax Act, and until Frucor’s High Court victory, it had not lost a case involving a tax avoidance matter for something like 10 years.

So aggressive tax planning is very much still under the gun for Inland Revenue and the courts are supportive of that approach, even though it might look as if all the necessary legal form has been satisfactorily met. So that’s just a warning for the times ahead. I think we’re going to see Inland Revenue make more use of anti-avoidance provisions in other areas as it returns to normal after its attention was diverted responding to the COVID-19 pandemic in the early part of this year.

Taxing crypto assets

Moving on, Inland Revenue has issued some updated guidance on the tax treatment of crypto assets. There’s nothing especially new here. It is confirming that crypto assets are to be treated as a form of property and that in each case it will look carefully at what are the circumstances behind the acquisition and disposal of the relevant crypto asset.

The guidance does expand a little bit more on what we’ve seen previously in this area.

Inland Revenue has said very clearly that it will look at the purpose for acquiring the crypto assets. And it is pretty straightforward in saying that if your purpose when acquiring crypto assets was to sell or exchange them, you will need to pay tax when you do so.

Inland Revenue will look very carefully at your purpose at the time you acquire crypto assets. The guidance repeats the key point, which is often overlooked, that it is the purpose at the time of acquisition that matters. If that purpose changes later on, that is not relevant. If you plan on selling or exchanging your crypto assets at some time in the future, then you have a purpose of disposal. It doesn’t matter how long you plan to hold onto them before doing so. Your main purpose can be to sell or exchange them even if it takes a few years. Then, of course, you’ve got to have supporting evidence of what your intention was at the time of acquisition.

And one of the things the guidance points out is the nature of the crypto assets being acquired. And in particular, does it provide an income stream or any other benefits while being held? (By the way, benefits isn’t clearly defined). Now, Inland Revenue’s view is that if you have crypto assets that do not provide an income stream or any other benefits, this strongly suggests you acquired them for the purpose of selling or exchanging them. This is because the only benefit you get is when you sell or exchange those crypto assets. And that, by the way, is similar to Inland Revenue’s position on gold bullion.

But just because you’ve got crypto assets that do provide an income stream or other benefits, for example, staking, that doesn’t mean that you didn’t acquire them for the main purpose or sending of sale or exchange. Somewhat helpfully, there are a number of examples of how the Inland Revenue sees these rules working.

So the position to be mindful of if you’re involved in holding crypto assets, is that the default position is almost that any funds realised on a sale or exchange are going to be taxable. To counter that, you’re going to need to show good records at the time of acquisition of what your intention was and what type of assets you acquired.

This is a perennial problem that we face in our tax system because the taxation of capital gains is very much driven around a rather nebulous definition of purpose or intent. It comes back to a point I’ve said beforehand that one of the advantages of a capital gains tax is it does clear away all the uncertainty.

But this is the current position and we have to work with it. And so my advice is be very clear in recording what your intention is when you acquire crypto assets. And if you haven’t done that, it’s too late. Inland Revenue’s default position with crypto assets is that any sort of exchange is going to be taxable.

Election 2020 tax policies

And finally, Labour has now come out and announced its tax policy, the centrepiece of which is a new top income tax rate of 39% applying to income above $180,000. It’s also said that there will be a freeze on fuel tax increases, no new taxes and no further income tax increases for the entire next term of government.

The other point it’s raised is, is it going to continue to work with the OECD to find a solution on the taxation of multinationals? It’s prepared to go ahead with the implementation of a digital services tax, which present projections estimate would raise between $30 and $80 million yearly.

As can be seen there’s not a lot of tax involved with multinational taxation, but it’ll be a popular measure because it’s something that keeps coming up in conversations I have with people on the issue of taxation. People are always saying multinationals should pay more. But they’re not a bottomless well, and opportunities to tax them are limited.

The digital tax space is where there could be some movement. But that’s very much dependent on how the OECD goes. And as I’ve mentioned in the past, the Americans have pretty much brought that particular pathway to stop earlier this year by basically saying they weren’t going to cooperate or be involved

With the proposed income tax rate increase to 39%, we’ve been there before. I thought if Labour was going to raise the top tax rate, it would be to 39% percent. Crossing the 40% threshold would be a psychological barrier too far. We haven’t had an individual tax rate of more than 39% for over 30 years. 1988 was the last time the tax rate was above 40% when it was 48% as I recall. It’s expected to raise 550 million dollars.

There’s already a lot of talk going around about making use of trusts and companies to get around the increase. My understanding is they’re going to look at trusts and the trust tax rate. Conceptually, the trust tax rate should really rise to be equal to the top personal tax rate. And that’s the story in Australia, the UK and the US as well. But my understanding is trusts will be looked at to find out exactly how many trusts really would be caught by that, because there are trusts settled for minors and orphans and other charitable or semi charitable purposes.

But even if nothing happens in that space, I’ll just remind you about the first item this week, the Frucor case and the Inland Revenue’s approach to tax avoidance. Last time we had tax rates at 39% we ended up with the Penny-Hooper decision. That’s the case involving dentists who used a company to trap income at the company tax rate, which was then 33% and then then lowered to 30% instead of the personal 39% rate was struck down as tax avoidance. You can see that happening again.

So, yes, Labour seems to have opened an opportunity for tax planning. But my answer to that would be ‘Proceed with great caution’, because Inland Revenue has a big stick in the form of an anti-avoidance provision.

The other thing of note from Labour is that it’s campaigning on extending applications to the Small Business Cashflow Scheme to 31st December 2023 for ‘viable’ businesses. And it’s also promising to extend the interest free period of loans under the scheme from one year to two years, which would be very welcome for small businesses. Labour will also look at a permanent iteration of the scheme, which is something I would support.

That’s it for this week. Thank you for listening. I’m Terry Baucher and this has been The Week in Tax. Please send me your feedback and tell your friends and clients until next week. Ka kite āno.

Unsurprisingly, the price of gold has been on a rise throughout the year in the wake of the pandemic and its current price of USD 1,953 per ounce is close to its all-time high. But what are the tax implications of holding gold?

As it transpires Inland Revenue looked at this matter in a Question We’ve Been Asked (QWBA) released in September 2017. Inland Revenue’s conclusion was that a disposal of gold would be taxable under Section CB 4 of the Income Tax Act 2007 if the gold was acquired for the dominant purpose of disposal.

Actually, that was a little bit of a walk back from the draft position that was put out by Inland Revenue, which was categoric that any disposal of gold would be taxable. In the wake of submissions on its draft position, Inland Revenue walked back the position. But in general, the position remains that if the gold was acquired for dominant purpose of disposal, it will be taxable.

Now, what led Inland Revenue to conclude initially that any disposal of gold bullion would be taxable was its nature. Bullion does not provide any annual returns and it doesn’t confer any other benefits. So therefore the Commissioner of Inland Revenue’s view is that the nature of the asset is a factor that strongly indicates that generally speaking, you’re acquiring gold for a dominant purpose of ultimately disposing of it. How else are you going to realise any value from it?

However, the QWBA does recognise that in some cases people might hold bullion not so much as a means of realising funds by disposal, but perhaps as a hedge against inflation or, as we are right now, in highly uncertain times. Also, in any diversified investment portfolio perhaps there’s a role for something like bullion. So that’s why the final QWBA issued in September 2017 walked back the initial draft position.

Now, one of the problems with our lack of a formal capital gains tax regime is that section CB 4 is very subjective. What is dominant purpose? So, this is an area where people need to be very fact specific about why they’ve acquired the gold and keep records of their intentions. I would say that even though Inland Revenue have taken a view where dominant position is to be required to establish taxability, its default position will be that anyone who’s bought gold recently only did so as a means of making a quick gain.

It’s also worth noting that this bullion QWBA is actually quite an important factor in the cryptocurrency determinations that Inland Revenue subsequently released. https://www.ird.govt.nz/cryptocurrency/taxing-cryptocurrency/public-rulings-on-crypto-assets And, of course, for real tax nerds anything looking at bullion brings us back to one of my favourite tax cases, the British case of Norman Wisdom versus Chamberlain, H.M. Inspector of Taxes from the 1960s. Wisdom, was a comic, but a very shrewd investor and made a substantial gain on holding silver bullion as a hedge against devaluation which was ultimately found to be taxable. So anyway, there’s opportunities obviously with gold bullion investing, but be prepared to be taxed on your gains.

No longer deductable

Moving on. Inland Revenue has recently issued another Question We’ve Been Asked, QB 20/01, which covers the issue of whether owners of existing residential rental properties can claim deductions for costs incurred to meet healthy home standards.

So, this is very important Inland Revenue guidance. What it does is going back to basics, costs of a revenue nature are generally deductible when they’re incurred. That could include, for example, repairing items that would otherwise meet the healthy home standards if they were in a reasonable condition. It also could include minor additions or alterations which do not change the character of the building, for example, meeting the draught stopping standards and those blocking unused chimneys or fireplaces, and making various ventilation systems compliant. And some, that’s the key word there, costs of meeting moisture and ingress and drainage standards around ground moisture barriers. Finally, replacing items on a like for like basis where they’ve already been treated as part of the building.

And this is the key part, which I think owners need to be very careful about – determining what is part of the building. And there are one or two surprises in here. Inland Revenue says that smoke alarms are part of the building now, even though often they’re physically separately attached and are generally of relatively low-cost. Insulation very obviously. Ducted or multi-unit heat pumps, new or replacement openable windows, new exterior doors, extractor fans and drainage systems. These items Inland Revenue view as all part of the building, which means that they would not be deductible. So, I think people need to be very careful about that.

Then there are items which Inland Revenue considers would be separately depreciable. For example, that includes electric panel heaters, some single-split heat pumps, through window extractor fans, various door opens and stops, external door draught extruders and some other devices for blocking fireplaces.

The QWBA it sets out the reasoning for why it considers items are non-deductible/capital or capital and depreciable or maybe a flat-out repair. So it’s a very important guidance for residential property investors. It won’t be welcome everywhere.

And it does touch on an issue which is probably in some ways hindering getting homes up to standard. That is if the expenditure is deemed to be part of the building, it’s not depreciable. Remember depreciation was only reintroduced for commercial buildings, not residential buildings.

This is an issue that I think isn’t going to go away. There was always something a little odd about the decision to remove depreciation on buildings back in 2010. It looked at the time to me and still does as it very much a matter of ‘We’re putting these tax cuts through and we have to balance the books somewhere and therefore we’ll remove depreciation.’ There was also an argument, by the way, that maybe these buildings weren’t actually depreciating, and this is a pretty micro detailed economic argument, that perhaps the rate of depreciation was excessive. Anyway, the guidance is there. And people will need pay attention to it. I think the smoke alarms one is one which will raise a few eyebrows. But that’s the way it plays at the moment.

If you have any involvement with a trust, you may well have been recently contacted by your lawyer about how the new Trusts Act is going to significantly change the dynamic about how trusts operate. In particular, what information trustees should be disclosing to beneficiaries. It’s now clearly set out that beneficiaries will be entitled to receive some of the financial information of the trust, as well as knowledge that they are a beneficiary. That is something that has been a matter of debate and various court cases for the past 20 years or more. So, it’s very important to finally get some statutory guidance and clear rules on the matter.

But it’s going to shake up an industry. We don’t know how many trusts there are in New Zealand. The best estimate is about 500,000. There was a surge in setting them up in the 1990s after the abolition of Estate Duty. They were incredibly flexible instruments at the time. So much so that practitioners outside New Zealand gave New Zealand trusts the side eye about what they were seeing going on. Particularly because from 1991 onward it was entirely possible for one person to be a settlor, or the person who settles funds on a trust, the trustee, or the person responsible for managing the trust and a beneficiary. And this has led to some interesting interpretations and quite a lot of legal action.

Anyway, if you’re involved with a trust you should either have been contacted or shortly will be contacted by your lawyer to discuss these changes. “Do we actually need this trust anymore?” is a question I’m going through with clients and obviously the tax consequences of winding it up. And if the purposes for holding assets in trust are still valid, what needs to change?

There’s a lot of work going to be needed to be done on this. And probably in many cases a lot of trusts will be quietly wound up and the assets distributed because they really don’t serve any purpose any longer.

Potpourri

Finally, because I wasn’t able to record last week’s episode, here’s a couple of items from the last few weeks I thought I’d mention in passing.

There will be no tears shed at the news that Eric Watson’s Cullen group has abandoned its appeal against Inland Revenue assessment for $112 million of non-resident withholding tax and interest on the basis the arrangement under which the Watson structured his exit from New Zealand to be tax avoidance.

The only thing that we should perhaps be concerned about is the timeline involved. The original transaction happened in 2003. The assessment, which led to the just abandoned case, was made in 2010 when Inland Revenue assessed Cullen Group Ltd was due to pay non-resident withholding tax at 15% instead of the 2% Approved Issuer Levy. After taking into consideration the Approved Issuer Levy paid the resulting liability was $51.5 million. The actual amount now due is $112 million. And the sixty-odd million dollars difference represents use of money interest charged on the original debt.

Now I’ve not heard many good words about Eric Watson. But I think we should be concerned that this case took so long to work its way through the system when interest is running all the time. So that basically weights everything in favour of Inland Revenue. And I think we should be asking questions to whether the processes are fair enough, whether or not you like what he did. That is a matter we should be concerned about because as the old saying goes ‘Justice delayed is justice denied”.

Another interesting case which also involves tax planning and touches on a topic which attracted a lot of commentary for the Tax Working Group, was the issue of the charitable exemption from income tax for charities with trading income.

And this point has come up in relation to Kidicorp. The redoubtable Matt Nippert of the New Zealand Herald has picked up on the fact that following a quite complex restructure in 2015, Kidicorp’s childcare centres are now owned by a charity Best Start Educare.

What happened was Kidicorp sold its whole business to a charitable foundation Best Start Educare for $332 million. The purchase was settled by way of a no-interest related party loan which is being repaid at about $20 million a year. This pretty much uses up most of the childcare operation’s surplus cashflow from its untaxed earnings.

This has raised a few eyebrows. What caught my eye about this story is that two people who were involved with the Tax Working Group, have come out and said that this is one of the matters where the group was concerned at what was going on. The Tax Working Group received a lot of submissions around the issue of the charitable exemption. Professor Craig Elliffe, who was on the Tax Working Group, commented about the Kidicorp transaction

“This is the very thing we were looking at and we were worried about. The bigger policy question is whether this is an appropriate use of charitable structures.”

Furthermore, Andrea Black, who was the independent tax adviser to the Tax Working Group, also commented that what was concerning about Best Start Educare was the small amount of donations it’s making and the fact that the business was sold rather than gifted with a loan back and therefore otherwise taxable profit is being used to pay back some of the loan. She concluded “It’s hard to see the benefit to the New Zealand community”.

We might see more on this although Inland Revenue might have already run its eyes over this and given it the tick. But this was the sort of structure the Tax Working Group was concerned about. There was a lot of public interest in the matter and a lot of the criticism involved Sanitarium and what the public saw as sometimes unfair benefits between it and its competitors who had to pay tax. The Tax Working Group took the view that if the profits in the charity were being distributed, then that was fine. However, if they weren’t or something odd was happening, then that was an issue.

Well, that’s it for this week. Thank you for listening. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you find your podcasts. Please send me your feedback and tell your friends and clients. Until next time, ka kite anō.