the first ever sentencing for possession of tax evasion tools.

Inland Revenue’s draft long-term insights briefing currently out for consultation has generated quite a bit of debate. The paper discusses the future shape of the system and how to fund the rising cost of superannuation and related health costs.

Sir Roger Douglas has now entered the chat as he, together with Professor Robert MacCulloch of Auckland University, have released a paper titled How to change the welfare state from a taxation to a savings-based model. In some typically bold thinking from Sir Roger, the proposal is to dramatically change the tax system, and instead of trying to raise additional tax to meet these costs, take a completely different approach.

A tax cut or something else?

Sir Roger and Professor MacCulloch suggestion is for the first $60,000 of income to be tax free. Based on current tax rates, that’s at least a $10,000 tax cut for everyone with income of at least $60,000. Instead, those taxes would be directed into mandatory savings accounts for health, pensions and other risk cover. These would then be supplemented by employer contributions (effectively a social security tax, although not specifically described as such) with the trade-off for these contributions being a cut to the corporate income tax rate.

They’ve released a short paper outlining their proposal (there’s also a more detailed paper that Sir Roger and Professor MacCulloch produced in 2020). The paper starts with an analysis of the forthcoming rise in health and superannuation costs and the need to take a long-term view on addressing this issue. Sir Roger and Professor MacCulloch take the view that the conventional approach, raising taxes to meet these costs isn’t going to cut it. Something more dramatic is needed.

Taking the axe to corporate welfare

In addition to the proposed mandatory savings accounts, Sir Roger and Professor MacCulloch propose cuts to what they call corporate welfare and grants to high earners. The cuts include the removal of screen production grants, ending accelerated depreciation allowances for industries such as forestry, fishing and bloodstock, withdrawing winter energy payments to wealthy households and KiwiSaver subsidies to higher earners. They also propose ending the “favourable tax treatment to owners of rental housing” but this isn’t defined. I’d be very intrigued to know more about what exactly they’re driving at there. All up Sir Roger and Professor MacCulloch suggest these could save over $12 billion annually.

Yeah, but…

This is quite a radical proposal which would be quite a shock to the system, and I’d be very interested to see what other economists think of it. One hurdle I see is with the proposals aimed at introducing competition into the provision of health services. This is a perennial problem for our economy. We are just 5.2 million people and 2,000 kilometres away from the nearest neighbour. Competition in that context is always going to be difficult but it’s an issue we need to address, not just in this context but across the economy as a whole, because I think it’s a major problem for our economy.

Overall, you can never say that Sir Roger Douglas would die wondering. As a RNZ report noted it’s a bold plan and I recommend reading the summary paper. Bear in mind some of what it proposes in terms of removing subsidies such as the Government’s KiwiSaver contribution for high-income employees are now actually happening.

What about increasing GST?

On a more conventional approach Inland Revenue’s briefing paper includes a discussion about the implications of raising GST from 15% to 18%. Last Thursday I spoke with Wallace Chapman of RNZ’s The Panel about this proposal.

The Inland Revenue briefing paper notes the suggested GST increase could raise $5.5 billion of tax annually. This is because, as I explained to Wallace and his panellists, GST is an enormously efficient tax. It does meet the classic broad based low-rate approach. You broaden the basis as widely as possible so you can have as low rate as possible. Furthermore, because we have no exemptions, our GST is enormously efficient. So really if you were thinking of increasing taxes your first point of call would be to raise GST.

A regressive tax

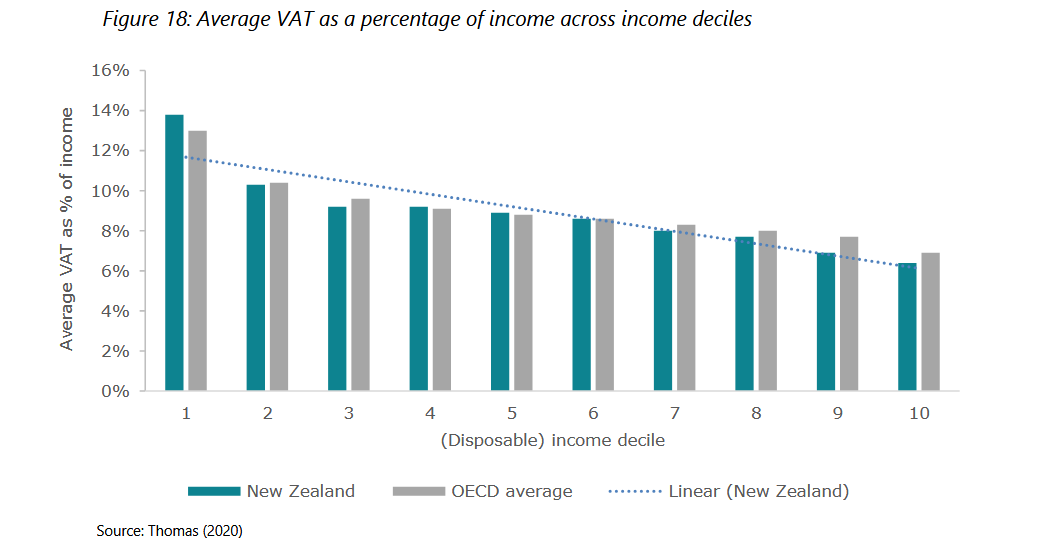

The problem is though, as Inland Revenue pointed out and as Holly Bennett, one of Wallace’s guests immediately jumped on, GST is a regressive tax. There’s quite an interesting analysis of this in the Inland Revenue briefing paper. The paper notes that GST or VAT (value added tax) is regressive relative to income.

According to the organisation of Economic Cooperation and Development (the OECD), the average GST to income ratio declines from 10.4% in Decile 2 to 6.9% in Decile 10. We follow a similar profile with our GST to income ratio declining from 10.3% in Decile 2 to 6.4% in Decile 10.

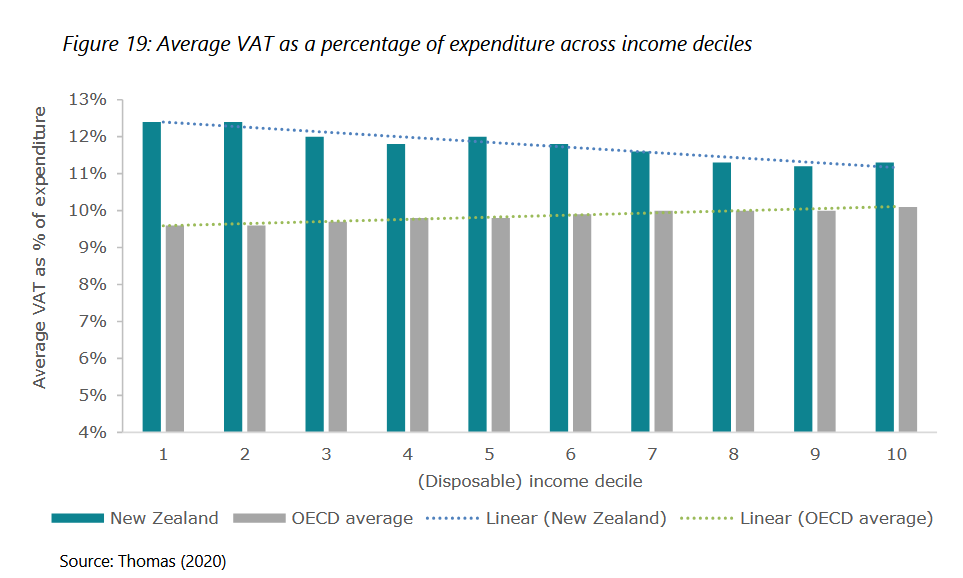

The Inland Revenue paper also considers the effect of GST relative to expenditure. In this instance GST or VAT is slightly progressive for most OECD countries because of the exemption of tax of necessities such as food and some sanitary products and various other Items which make up a very large proportion of the consumption basket of lower income households. However, our GST, because we don’t have any such exemptions, is mildly regressive.

Increasing poverty?

As Holly Bennet (one of Wallace’s panelists) was quick to also point out, an effect of GST increases is to increase the poverty headcount. According to Inland Revenue, based on the 2015/2016 Household Expenditure Survey GST “increased the imposition of GST in New Zealand increased the poverty headcount by 4.7%, the poverty gap by 1.7%, and the squared poverty gap by 0.8.” What’s worse is that the effect of those increases is higher than the OECD averages of 3.1%, 0.7%, and 0.3% respectively, again, because we have no exemptions.

The GST dilemma

So, raising GST results in the dilemma that it would raise a lot of revenue very quickly but hit lower income families harder. The suggestion in Inland Revenue’s paper is that there should be a compensation increase in welfare benefits for low-income families. They suggest that would probably cost maybe $440 million a year in total.

Readers and listeners may recall that last year a guest was Andrew Paynter, one of the Tax Policy Charitable Trusts co-winners. We discussed his proposal of raising GST to 17.5 % and introducing a GST refund tax credit for low- and middle-income earners.

Coincidentally or not, Andrew works for Inland Revenue, but there’s a worldwide trend looking at this particular issue. For example, the International Monetary Fund released a paper last year Designing a Progressive VAT which suggested a point of sale credit for low-income families. As the Inland Revenue paper notes Canada and Thailand have point of sales/refund credits for low-income earners.

Some form of capital taxation also needed

If you were adopting a conventional approach to addressing the rising expenditure gap, then raising GST is the most likely approach. My personal view is we also need to have some form of capital taxation because as I explained to the Panel, not only do we have rising health and superannuation costs, the cost of dealing with the impact of climate change, is rapidly accelerating.

This week Forsyths Barr and the Insurance Council released data that showed that over 40 years, the average annual cost of dealing with weather related events was $203 million. However, in the latest 10 years those costs had risen to $606 million annually and the five-year average is now $952 million per annum. Currently Tasman is spending $500,000 a day repairing its roads in the wake of the recent floods.

So climate change is having a huge impact now and there are a huge number of properties – 220,000 in total – presently worth over $180 billion, which are located within coastal inundation and inland flood zones. More than a quarter of those are in the Canterbury, Tasman, Gisborne, West Coast and Nelson regions. Those last four of which have all had severe weather events in the last year.

A quid pro quo

Protection against climate events will be another growing demand, particularly since for most people their property is their principal capital asset. This is where I think some form of capital taxation/capital gains tax is perhaps appropriate because if the Government and local councils are expected to spend more to protect capital assets, the quid pro quo must be that those capital assets become taxable.

Working for Families – a correction

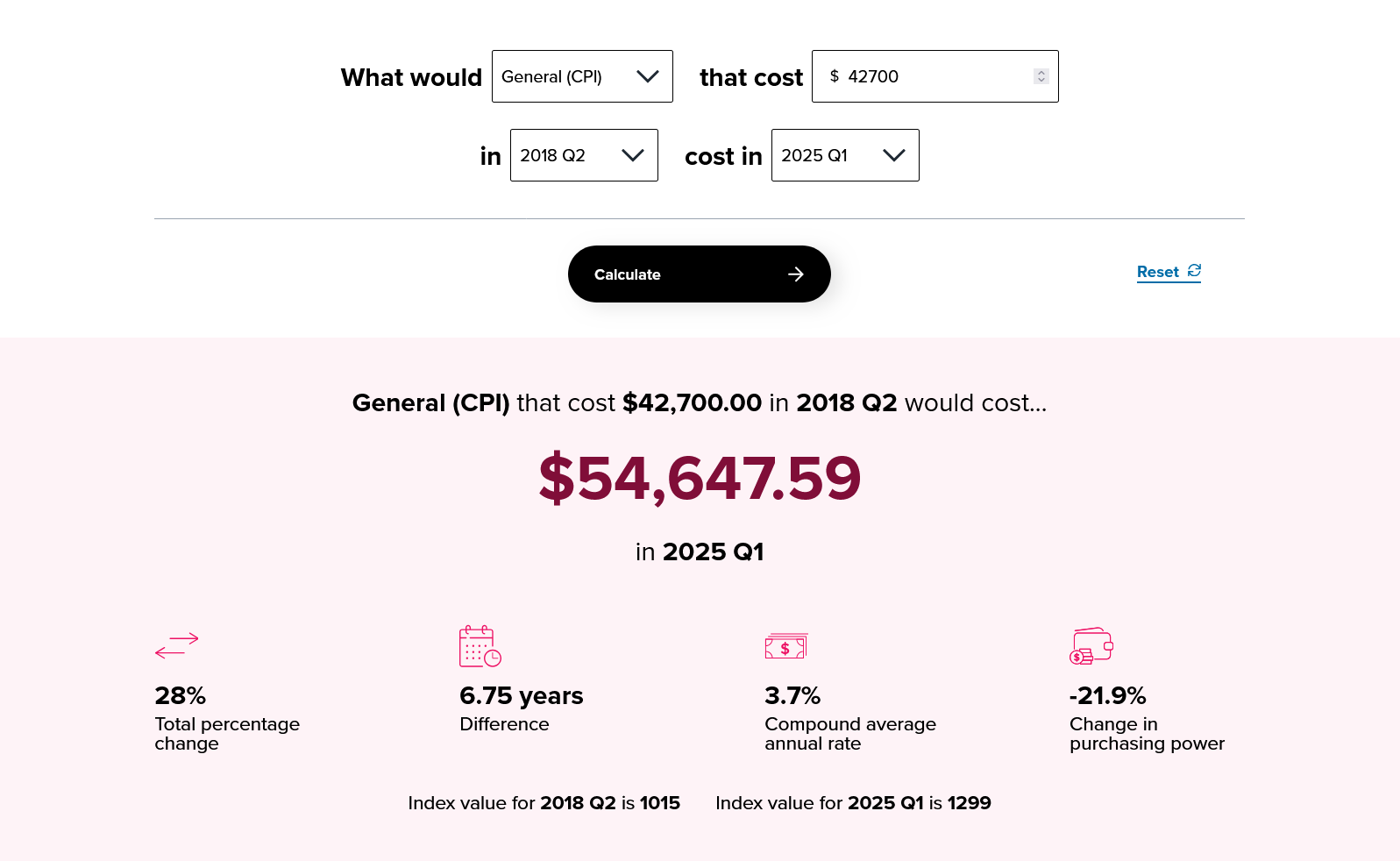

Moving on, last week I talked about the changes to FamilyBoost and I noted that there had been no change to the threshold for Working for Families. That was actually incorrect. A kind reader from Inland Revenue pointed out that the Working for Families threshold will increase to $44,900 with effect from 1st of April next year its first increase since July 2018. Thanks for getting in touch and apologies for my error.

I’ll just simply add that on an inflation adjusted basis, that threshold should have gone up to something like $54,650 so it’s still way short of where it should be.

In any case the effect of the increase in the threshold from$42,700 to $44,900, which remember is for a family’s income, is mitigated by the increase in the abatement rate went up from 27.5 cents per $100 to 28 cents per $100.

Furthermore, the other point I made last week was about the focus of the FamilyBoost towards higher income families. That point doesn’t change just because the threshold for Working for Families has been (slightly) increased.

A New Zealand first

A recurrent theme this year is how Inland Revenue has increased its focus on chasing non-compliance. The latest example is the Auckland man who has become the first person in New Zealand to be convicted and sentenced for aiding and abetting his company’s possession of the electronic sales suppression tools.

Now these sales suppressions tools basically alter the Eftpos record so they’re very much about suppressing income and basically trying to defraud the taxpayer. In this case, Gurwinder Singh has been sentenced to seven months home detention on tax evasion charges, including the charge of aiding and abetting this company for possessing electronic sales suppression tools for the purpose of evading the assessment and payment of tax.

All up, Singh’s tax evasion amounted to $198,500. Apparently one of the things he was also doing was although he had four employees, including himself, he was only reporting PAYE returns for two staff. So, some obvious and not so obvious tax evasion was going on here. Anyway, this is the first time the new law in relation to electronic sales suppression tools has been applied. Would-be fraudsters have been warned.

The pitfalls of schedular payments

As often mentioned, Inland Revenue turns out vast amounts of very interesting and helpful material. Once such source are its Technical Decision Summaries about issues or rulings that Inland Revenue has encountered.

One TDS released this week is a private ruling in relation to the application of the schedular payment rules.

This involved a company wanting to make use of offshore personnel to act as directors in New Zealand. The question of interest here is a reminder that if you are making payments to overseas persons, they may, even if they are contractors, be subject to non-resident withholding taxes/schedular payments.

That’s why this one is useful. This ruling explained why those provisions would not apply. But typically, if they do apply then 15% withholding tax can be deducted which can come as a shock to some overseas persons. This is a useful ruling on a point which we often encounter but is one of those cases where I suspect the compliance isn’t always as diligent as it could be.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Lessons from the largest known GST fraudster – could it happen again?

Corporate tax cuts – who benefits and what does the public think?

The tax year-end of 31st of March is fast approaching and at this time of year tax agents are busy with the last year’s tax returns and also giving a heads up to clients about what actions they need to take ahead of 31st March. It’s always an incredibly busy period and it’s often easy to overlook some important matters amidst the rush and the mayhem. So, here’s a quick reminder of key issues that that you should be considering as the tax year ends.

GST and Airbnb

First up, a GST election is running out in respect of being able to take assets out of the GST net. We discussed this a few weeks back. To quickly recap, this could particularly affect Airbnb operators that may have bought a residential property, rented it out and then realised that Airbnb produces a better return. They’ve therefore signed up to Airbnb or other apps and then registered for GST either voluntarily or because they’ve exceeded the $60,000 registration threshold.

Subsequently, the taxpayer may have claimed an input tax credit on the property but now realise that they could be liable for a substantial GST bill on any subsequent sale of the property. That obviously is a big shock.

To address this issue, a transitional rule was introduced under section 91 of the Goods and Services Tax Act with effect from 1st April 2023. The rule enables a person to elect to take an asset out of the GST if the following four criteria are met:

the asset was acquired before 1st of April 2023; and

it was not acquired for the principal purpose of making taxable supplies; and

it was not used for the principal purpose of making taxable supplies; and

a GST input tax credit was previously claimed, or the asset was acquired as part of a zero-rated supply.

If all those criteria apply, then the person can elect to take the asset out of the GST net and pay back the GST that was claimed on the original input tax. In other words, they don’t pay GST on the increase in value. A good example here would be a bach or family holiday home which was subsequently rented out for short stay accommodation.

The key thing is this election expires as of 1st April 2025, by which time you must have notified Inland Revenue of your election. You don’t necessarily have to pay the GST; you can do so as part of your GST return to 31st March, but you must have notified Inland Revenue in a satisfactory manner. I would recommend using the MyIR message service to do so.

Other year-end matters

There are a number of elections relating to whether or not a taxpayer wants to adopt or leave a tax regime. A classic example would be companies entering or leaving the look-through company regime. Another, lesser known one would be entry or exit into the little known, and apparently little used, Consolidation regime.

Another matter that pops up regularly around year-end is checking your bad debts ledger. Bad debts are only deductible for income tax purposes if they are fully written off by 31st March so make sure this happens. Then there is the year-end fringe benefit tax returns where taxpayers should check to see whether they are making full use of any available exemptions.

A very important one for companies is to ensure their imputation credit account, either is in credit or has a nil balance. If there’s a debit (negative) balance on 31st March, that will result in a 10% penalty. It may be possible in some cases to make use of tax pooling to rectify some of these issues.

Finally, if you’re registered with a tax agent, your tax return for the 2024 income year must be filed by 31st March otherwise late filing penalties may apply. Possibly more critically, the so-called “time-bar” period during which Inland Revenue may review and amend already filed tax returns is extended by another year.

Lessons from the country’s biggest known GST fraud

Moving on, an interesting story has popped up in relation to what was then the largest known GST fraud. Gisborne farmer John Bracken was jailed in May 2021 after he was found guilty of 39 charges of GST fraud. He had run a scam through his company, creating false invoices totalling more than $133 million between August 2014 and July 2018 which resulted in receiving GST refunds totalling $17.4 million to which he wasn’t entitled. He was jailed and is currently out on parole.

At the time he was sentenced Inland Revenue and the police issued restraining orders and are trying to make an application for an asset forfeiture. In other words, assets subject to the forfeiture order were acquired through fraud and should be forfeited and handed to the Crown.

Now naturally Mr. Bracken and his family, including his wife and his parents and his son, are all fighting back on this because they stand potentially to lose assets that may be subject to the restraining order and subsequent forfeiture. The interesting part of this is the sheer scale of what went on and how it went undetected for four years before an employee got suspicious, notified the Serious Fraud Office, who then tipped off Inland Revenue.

At the time the frauds were committed, Inland Revenue was at the start of its Business Transformation project, upgrading all its systems. Until it got tipped off It had no idea of the extent of the fraud. Mr. Bracken appeared to have covered his tracks reasonably well, although once uncovered it was a fairly simple GST fraud. He just submitted fraudulent GST invoices, but he was careful to get them from actual companies with whom he had established some form of trading relationship.

Obviously the concern is now twofold. The Crown will be wanting to recover as many assets as possible to the value of the $17 million that it was defrauded, but also, can this happen again?

I’d like to think “No”. Certainly, Inland Revenue feels that its new systems have enhanced its capabilities greatly and that would appear anecdotally to be the case. There was a GST fraud scheme spread by TikTok influencers which caught the Australian Tax Office completely off guard and was worth tens of millions of dollars. Inland Revenue feels that that sort of fraud could not happen here. Mr Bracken’s release on parole and the ongoing forfeiture case is a reminder that Inland Revenue has to be vigilant all the time.

But sometimes it comes down to a conscientious person, an employee usually, tipping off the authorities. But it shouldn’t always come down to that. Inland Revenue and other authorities should be able to pick up signs of these frauds. As I said, I have confidence they do, but I would also hope that confidence is not tested too much.

Corporate tax cuts – a possibility or just flying a kite?

In recent weeks there’s been some chatter or hints from the Government and Finance Minister Nicola Willis about a potential corporate tax cut. She made the not unreasonable point that our corporate tax rate is high by world standards. This prompted comments from the former Deputy Commissioner of Inland Revenue Robin Oliver that tinkering around the edges by reducing it from 28% to 25% might not achieve much. If the Government wanted to attract investment, they’d have to go big, maybe nine or ten percentage points cut. Robin was sceptical the Government could afford to do so because of the loss of revenue. And I agreed with that assessment.

I do wonder whether this idea might be something of a bit of a red herring. Some comments I’ve heard seemed to suggest that maybe the Government was just flying a kite to see the reaction.

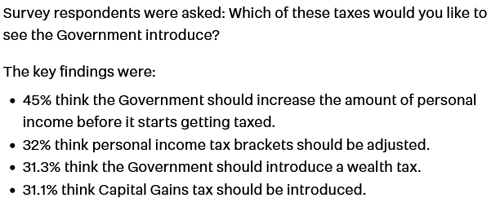

Anyway, this week a poll run by Stuff which suggested that very few would support a corporate tax cut, or rather that the population was pretty lukewarm about the idea. The poll carried out by Horizon Research, found only 9% of adults supported lowering the corporate tax rate, while 25% actually wanted it increased. There were a few other interesting results:

Who would benefit from a corporate tax cut?

Craig Renney (the chief economist for the Council of Trade Unions) and researcher Edward Miller also looked at who would benefit from a drop in the New Zealand company tax rate. They concluded the main beneficiaries of a corporate tax cut would probably be overseas shareholders. In terms of attracting greater foreign direct investment, they saw little evidence that corporate tax cuts would be likely to achieve that.

As they noted,

“…company taxation is only one aspect of a decision by a company or fund to invest in New Zealand. In addition to the company tax rate, there is the R&D tax incentive, the lack of a capital gains tax, and the lack of substantial payroll taxes. These taxes affect the actual tax paid by corporates in comparison with other countries when considering investing in New Zealand.”

Renney and Miller’s modelling suggested that a tax cut would not result in further investment but would just simply increase the funds flowing offshore. In particular they saw the Big Four Australian banks as being prime beneficiaries. The pair estimated that a cut from 28% to 20% would have increased the annual income to offshore shore shareholders by up to $1.3 billion.

There’s always a lot of debate around the benefit of corporate tax cuts, whether they do drive investment, or they simply put money into the back pockets of the shareholders. That debate has gone on for a long time and continues again. But it’s interesting to marry that along with the public’s general lack of enthusiasm for such a cut.

Yeah, but what about the IMF?

I think it was also noticeable that the International Monetary Fund in its recent Concluding Statement for its 2025 Article IV Mission suggested “judicious adjustments to the corporate income tax regime.” So maybe it too isn’t entirely sold on corporate tax cuts as a key driver for investment.

No doubt more will be revealed in May’s Budget. And until that time speculation will mount, but we will find out on the day and as always, we will bring you the news when it emerges.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Rachel Reeves, the first ever female Chancellor of the Exchequer delivers a UK Autumn Budget with potentially significant implications for many Kiwis and Britons who have migrated to New Zealand.

Meanwhile Inland Revenue’s crackdown on tax evasion continues.

The UK finance minister is officially called the Chancellor of the Exchequer, a post which is more than 800 years old, and until this year it had never been held by a woman. So, when Rachel Reeves, the Labour Chancellor of the Exchequer delivered her maiden budget speech last Wednesday night, she made history as the first woman Chancellor in British history.

There was quite a lot to consider in this UK Budget, as people were watching to see how the new government would respond to the challenges it inherited. British budgets, unlike ours, coincide with the release of a Finance Bill and tax measures there’s always a lot of tax matters to consider beyond the headline measures.

The headline measures

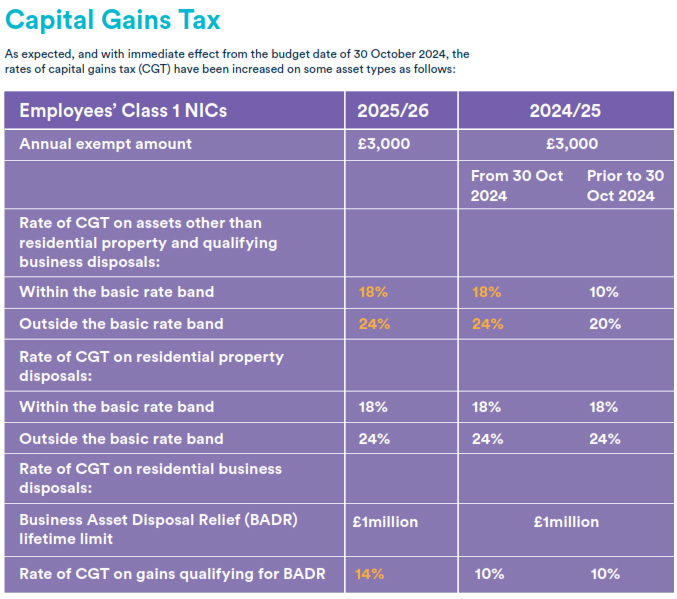

Most notably, there was an increase in Employer National Insurance Contributions (a Social Security tax) by 1.2 percentage points to 15% with immediate effect. There are also immediate tax rises for capital gains tax, but the top rate for capital gains tax still was capped at 24% for both property and non-property assets. Which as some commentators said is still lower than countries with which the UK compares itself. It’s quite interesting to see that comment about 24%, because one of the key points of our discussion around capital gains taxes here is what rate would apply? It’s therefore interesting to have an international comparison.

Beyond the headlines

It’s always interesting to dig around in other countries’ budgets and see what they do in certain areas. For example, the UK doesn’t have an imputation credit system, but there are lower rates of tax applied to dividends, even for those on the highest income. There’s also a savings allowance, which exempts certain amounts of investment income. It’s currently £1,000 for basic rate taxpayers (taxable income up to £37,700) and £500 for the higher rate taxpayers. The UK basic rate of tax is 20% and we have two rates lower than that so this savings allowance is not necessarily a measure we might want to copy here.

Twin cab utes and fringe benefits – an example to follow?

There’s apparently some uncertainty around the fringe benefit taxation treatment of twin cab utes which the Budget clarified. Where they have a payload of one tonne or more such vehicles are not there to be treated as cars for benefit in kind purposes unless they were acquired prior to 6th April 2025.

On Fringe Benefit Tax, the benefit value is calculated as a percentage of the vehicle’s list price when the car was first registered which is similar to our treatment. However, the percentage used is determined by the vehicle’s carbon dioxide emissions, or its range if it’s an electric vehicle. These percentages are set to increase steadily over the next three years as part of the range of tax increases announced. Inland Revenue is presently reviewing FBT and as is well known tax can act as a disincentive. If we want to incentivise a transition to a lower emissions economy, maybe we should be looking at how the UK applies FBT to vehicles.

UK pension tax free lump sum unchanged

There’s always lots of rumours before a Budget which I’ve seen sometimes used as a means to get people to buy new products or make tax driven decisions in fear of change. One of the rumours before this budget was that there were going to be changes to the taxation of pensions and in particular to the 25% tax free lump sum. That hasn’t happened, but remember, our rules are completely different. Just because 25% of the pension can be withdrawn tax free in the UK, that doesn’t mean the same rules apply here.

The big changes

But the main reason I was paying particular attention to this UK budget was because we finally got more detail around the two announcements made in the March Budget – the new foreign and income gains regime and the end of the non-domicile regime and the changes to inheritance tax. These are both measures which have significant impact for New Zealanders, who are either going to the UK or have returned to the UK, but also for UK expats who have migrated here.

New foreign income and gains regime

The foreign income gains (FIGS) regime is very similar to our transitional resident’s exemption in that a new tax resident’s foreign income and capital gains will be tax exempt for the first four UK tax years that they are resident in the UK. It’s not like our 48-month exemption period, it is tied to the UK tax year, which remember runs from 6th April to 5th April. (Perhaps reflecting that some of this stuff does date back 800 years or more, there’s no intention to change that tax year end).

What has also been clarified is that individuals who have previously elected to be taxed on the remittance basis, which meant their non-UK sourced income investment income was not taxable, can now be allowed to take advantage of a so-called temporary repatriation facility. This will last for three years, and they will be able to nominate and remit their non-UK income and gains from years when they were within the remittance basis and take advantage of lower tax rates. Initially 12% for the first two years ending 5th April 2026 and 2027, and then 15% for the year ended 5th April 2028.

As part of the FIGS regime there are also changes to what’s called the Overseas Workday Relief. This will allow UK tax resident employees who perform all or some of their duties outside of the UK to claim tax relief on the remuneration relating to their non-UK duties determined on “a just and reasonable basis”. This is quite a significant one for expats and for companies that have very highly paid and skilled employees and has been greeted with general enthusiasm by by those impacted.

Inheritance Tax

Potentially the biggest change though, is in relation to inheritance tax (IHT). This applies to all assets situated in the UK or all assets situated anywhere, if the person is domiciled within the UK. There’s a nil rate band of £325,000, above which 40% will apply (these rates and thresholds have been frozen until 2030). IHT has a potentially significant impact because under the present rules, someone tax resident outside the UK could still be within the IHT net because they are still deemed to be domiciled in the UK. I’ve had to deal with one or two of these instances.

There’s also a pretty nasty trap for someone like me who might have left the UK a long time ago and adopted a new domicile of choice outside the UK. At present if I ever became tax resident again in the UK, our domicile would immediately revert to the UK. Therefore, working or living for prolonged periods of time in the UK was actually potentially highly tax disadvantageous from an IHT perspective.

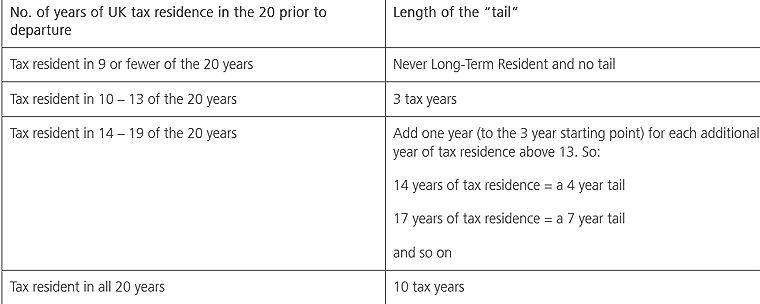

All this will be replaced now by a residence-based regime. The tests for whether non-UK assets are subject to IHT will now be whether the individual has been tax resident in the UK for at least 10 out of the last 20 tax years immediately preceding the tax year in which the chargeable event, most typically death, but can also be a lifetime transfer into a trust, happens.

There’s also a tail on how long a person is in scope if they’ve been non-resident during a period. For example, if someone had been UK tax resident for between 10 and 13 years, they remain in scope for IHT for three years post departure.

(Courtesy Burges Salmon)

Implications for New Zealand residents

What this change means for a lot of British expats resident here is they’ve got to think again about what their IHT obligations could be. By the way, our double tax agreement with the UK does not cover IHT. The UK has the right to charge IHT on assets situated in the UK, that’s not surprising. However, it potentially also has got a long reach if HM Revenue & Customs determine someone resident here is subject to IHT.

IHT and trusts

One of the other IHT changes is to the taxation of trusts used to hold assets outside the scope of IHT, so-called excluded property trusts. If I understand it right, starting from 6th April 2025, if a settlor dies and they’re within the scope of IHT, assets settled by them into what was previously an excluded property trust are now within IHT. This is a major change and I’m investigating it further given we make very extensive use of trusts. I’ve been dealing with quite a few clients who have UK connections year and it’s been really revealing to see how complex the taxation of trusts is from the UK perspective. It’s good to see some clarity around the new rules, but as I say, it’s a significant budget in many ways, and there could be quite major consequences for more people based here than they might anticipate.

Meanwhile, Inland Revenue’s crackdown continues

Moving on, Inland Revenue continues its crackdown when it announced on Thursday that it’s making unannounced visits to hundreds of businesses who it believes are not meeting all their tax obligations as employers.

According to Inland Revenue, they receive about 7000 anonymous tip offs each year. It has said “the volume of tip offs has grown over previous years indicating an increased sense of frustration by the community in general, businesses who are not doing the right thing.”

Inland Revenue’s analysis shows that the tax risks overwhelmingly relate to taking cash for personal use without reporting sales and or paying employees in cash.

Based on this Inland Revenue is making unannounced visits to over 300 employers whose practices it will closely examine. I’ve seen this happen with a few clients under investigation. Inland Revenue staff will go to a café or business and just watch to see what’s happening. They may buy something, but they will certainly sit and observe and see who uses the till, how everything is recorded and from there they will draw the relevant conclusions.

The consequences of being investigated

As an example of what happens to taxpayers who have not been compliant, the director of an asbestos removal and labour hire company has been jailed for three years in what the judge called serious offending and the worst of its kind to come before the Christchurch District Court in the last 20 years. The director, Melanie Jill Tatana, also known as Melanie Jill Smith, was jailed for three years for what was described as wilful diversion of funds.

Her company employed around 60 people, and between April 2019 and September 2022 had been required to deduct PAYE on 63 occasions but failed to pay the full amounts totalling $1.6 million. Tatana was therefore charged with 63 counts of aiding and abetting to knowingly take PAYE from workers’ wages and not pay it on to Inland Revenue. Instead, more than $800,000 had been diverted for her personal use.

One of the more encouraging things from my perspective about this case is that this offending has all been pretty recent and Inland Revenue tracked it down within a couple of years. I’ve seen cases where the offending has been four or five years.

I still think 63 occasions of nonpayment is a little generous, but bear in mind that Inland Revenue did take the the foot off the throttle around pushing hard on on companies and businesses because of COVID. That amnesty or less stringent approach is now over and it’s back to business. And Tatana won’t be the first to find out about Inland Revenue’s hardline approach.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The aim is to develop a corporate tax database which is going to be available to tax policy researchers and policy makers about corporate tax rates, effective tax rates, tax incentives for research and development and other topics such as withholding taxes. Increasingly, the amount of information includes anonymised and aggregated country by country reporting data, which provides an overview of the global tax and economic activities of thousands of large multinational enterprises operating worldwide. This year’s report covers 8000 such enterprises.

The detailed statistics in the report are mostly from the 2021 calendar year although some 2022 data is included. The report does take into account the statutory tax rates currently in force.

Increased country by country reporting and more reporting generally is part of the 15 actions within BEPS. The report sets out why this is important:

“Action 11 noted the lack of available and high-quality data on corporate taxation is a major limitation to the measurement and monitoring of the scale of BEPS and the impact of the measures agreed to be implemented under the OECD/G20 BEPS Project.”

Corporate tax rates are stabilising

The headline summary is that corporate tax revenues remain important, but statutory corporate tax rates as the report are now showing signs of having stabilised after pretty near two decades of decline. During the period between 2000 and 2024 the average statutory tax rate declined from about 28% in 2000 to 21.7% in 2019. However, between 2019 and through to 2024, it has remained relatively stable at a rate of 21.7% in 2019 and 21.1% in 2024. I think stabilisation is a trend that’s going to continue.

Who knows, though, if the possible re-election of Donald Trump may change this. But I think governments balance sheets worldwide have been weakened considerably by the double whammy of the Global Financial Crisis and then the pandemic. I therefore think the opportunities to actually cut corporate tax rates further are quite limited, but we shall see.

Just to put New Zealand in context, back in 2000, our corporate tax rate was 33%. With effect from 1st April 2008, it was reduced to 30% and then on 1st April 2011 it was reduced to its current level of 28%. Across the ditch Australia has had a 30% corporate tax rate since 2001.

There’s interesting data about the importance of the corporate tax take. On average for the 2021 year, which was also a pandemic affected year, corporate tax revenue represented 16% of all tax revenues. New Zealand is in line with that average, but as a percentage of GDP, the OECD average was 3.3% whereas here it was considerably higher at 5.7%.

The report also considers effective average tax rates (EATRs) and examines the effect of tax incentives such as more generous tax depreciation compared with true economic deprecation. Again, according to the report effective average tax rates have remained relatively stable falling slightly from 20.9% in 2019 to 20.2% in 2023. Median effective average tax rates were 22.8% in 2019 and practically unchanged at 22.7% in 2023. Meanwhile, New Zealand’s effective marginal effective average tax rate is still relatively close to our statutory tax rate of 28%.

But…a narrowing tax base?

Chapter 4 of the report discusses effective and marginal tax rates and has some interesting commentary around declines of effective marginal tax rates (EMTRs). The report notes

“The stability of EATRs combined with declines in EMTRs suggests a narrowing of tax bases in the sample, notably through an increase in the generosity of depreciation provisions. Examining the asset breakdown shows these trends have been driven by increased generosity of depreciation of tangible and intangible assets, as opposed to buildings and inventories.”

I think some of this might be part of the response to the pandemic. New Zealand is noted being alongside Argentina, Japan, Papua New Guinea and Peru as having a higher effective marginal tax rate because we’ve got less generous depreciation rules. (This has become more so with the imminent withdrawal of building depreciation).

Research and development incentives

Chapter 5 looks at tax incentives for research and development, noting that they’ve become more generous over the past 20 years or so. 33 out of 38 OECD jurisdictions offer tax relief from R&D expenditures in 2023, compared with 19 in 2000. New Zealand is one of the new jurisdictions now offering R&D incentives. These are becoming more generous over time.

From a New Zealand perspective, we discuss the importance of R&D in boosting our productivity and we still could do more in that space. I’m inclined to the view I heard recently expressed that it’s better to give a tax incentive for it rather than get involved in the grant process. Because with a grant process, the companies can be restrained in what they have to spend because of the application process. Also, there’s a lot of effort involved with applying grants, less so with an R&D tax incentive, subject to Inland Revenue monitoring.

According to the report the level of direct government funding and tax support for business R&D in 2021 was about .12% of GDP, well below the OECD average of .2 of GDP. So, there’s still room for improvement although that’s something that’s been acknowledged across the board.

Chapter 6 looks at BEPS actions and notes that there’s a large number of controlled foreign corporation or control foreign company rules with apparently 53 jurisdictions having it in place in 2024. There’s also growth in the use of interest limitation rules. This is part of a growing trend in tax policy around the world to consider imposing restrictions on the deductibility of interest. Apparently, there are now over 100 interest limitation rules in place up from 67 jurisdictions back in 2019.

The dangers of following Ireland’s example

Chapter 7 has a breakdown of country by country reporting statistics with 52 jurisdictions out of a possible 101 submitting statistics to the OECD. As I mentioned earlier, this report includes the activities of over 8000 multinationals so there’s a lot of detail in here.

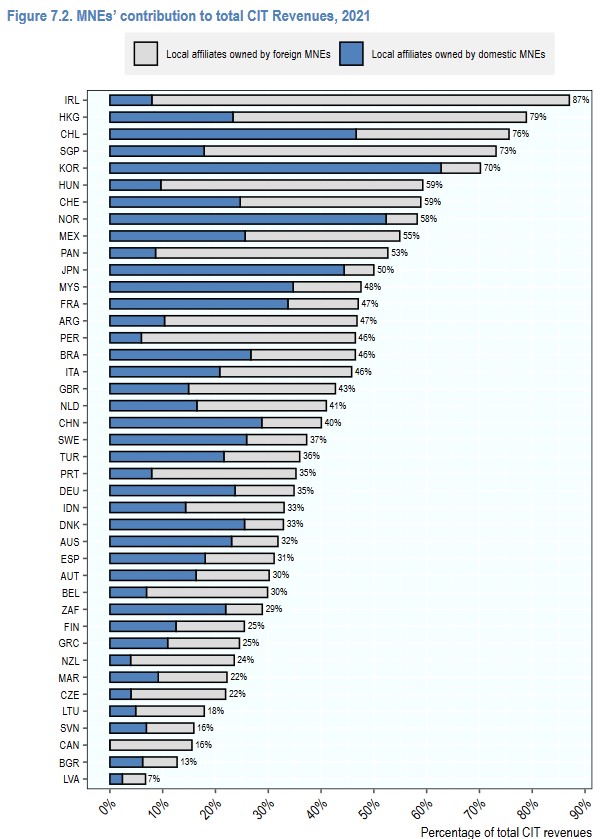

Several commentators including the New Zealand Initiative have recently mentioned Ireland as a potential model to follow. As is well known, Ireland has a very low corporate tax rate. I was therefore very intrigued by figure 7.2 on page 81 of the report, which illustrates the multinational enterprises contribution to local corporate income tax revenues in 2020.

As can be seen, 87% of Ireland’s corporate tax came from multinationals, and the vast majority of those multinationals were local affiliates owned by foreign multinationals. In fact, the Irish Treasury and the European Commission have expressed concern about the sustainability of Ireland’s corporate tax revenue because of the dependency on a few large multinationals.

New Zealand is near the opposite end of the scale with only 24% of corporate tax revenue coming from multinationals, probably three-quarters of which look to be from overseas owned. I think this is an extremely interesting stat which makes me wonder about whether New Zealand is attracting enough investment and whether we should have more multinationals of our own based overseas.

Yes, but is BEPS working?

In summarising key insights on BEPS from the Country by Country Report data the report makes this observation”

“There is evidence of misalignment between the location where profits are reported and the location where economic activities occur. The data show continuing differences in the distribution across jurisdiction groups of employees, tangible assets, and profits.” [page 87]

In other words, the report is basically saying there appears to be some profit shifting going on, but we don’t quite know enough about it. This gets to the heart of the idea behind the BEPS initiative, find out more about what’s happening and then fix it.

As I said the OECD’s corporate database is constantly being expanded so if you’re a bit of a stats guru there’s plenty to dive into and research. Overall, another interesting report highlighting how New Zealand’s corporate tax rate is at the higher end, but noting it also raises a lot of revenue relative to other jurisdictions.

Is that asset depreciable?

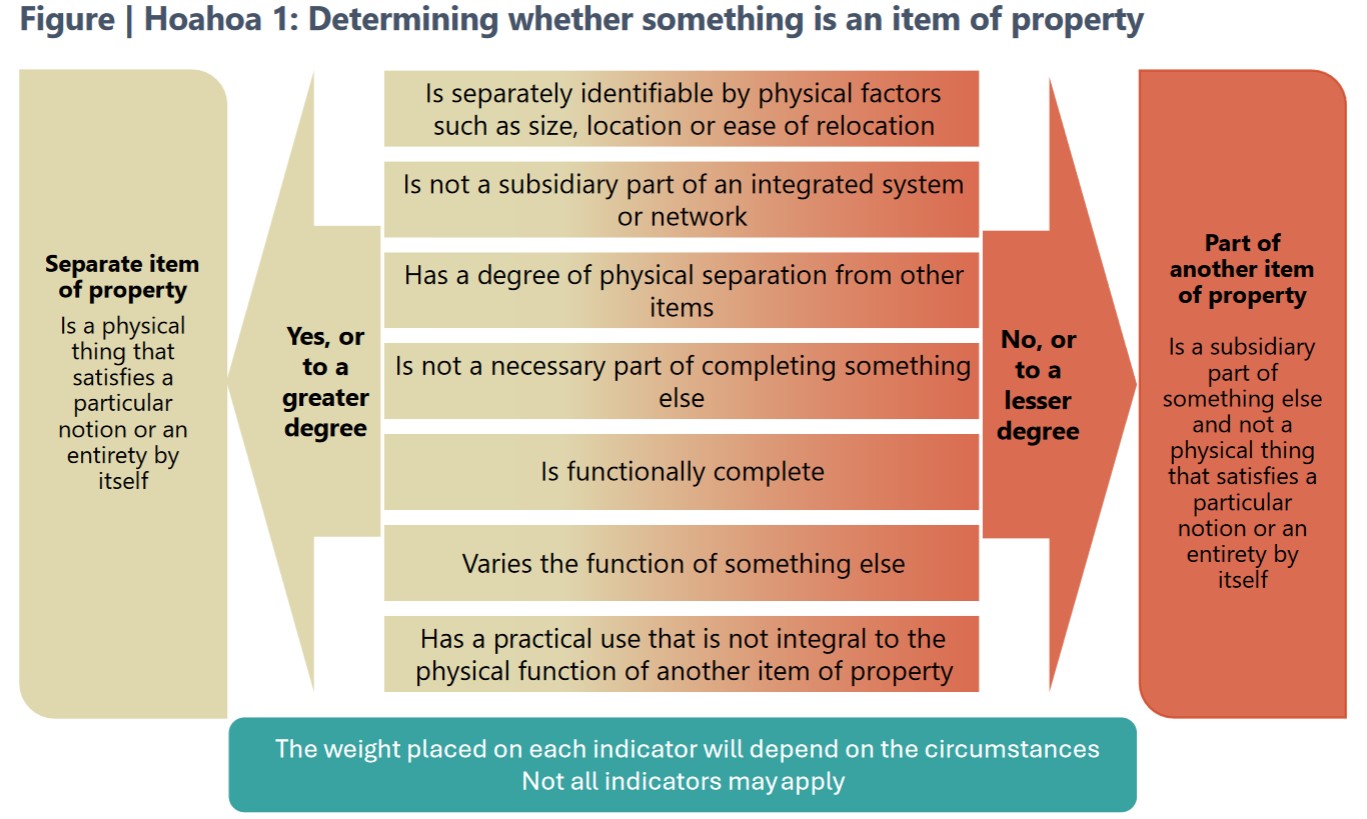

Moving on and picking up on depreciation one of the issues covered by the OECD stats, Inland Revenue has just released a draft interpretation statement for comment on identifying the relative relevant item or property for depreciation purposes. This is quite important because our depreciation regime is extremely detailed with a myriad of available rates across several categories.

This draft ties into several other related items of guidance such as residential rental properties depreciation, the question of deductibility of repairs and maintenance – if expenses are not deductible are they depreciable instead? There’s also QB 20/01 – can owners of existing residential parental properties claim deductions for costs incurred to meet healthy home standards? And finally, Interpretation Statement IS 22/04 relating to claiming depreciation on buildings. The imminent withdrawal (again) of building depreciation makes it very important now to maximise depreciation and to identify whether in fact that asset is part of the building or can be claimed separately. This draft is therefore pretty relevant.

The draft runs to 40 pages the last 15 or so pages of which are examples. There’s also a useful 6 page fact sheet accompanying it. Submissions are open until 29th August.

A post-hibernation bear is hungry…

Finally, as we discussed last week, one of the things that came out of Inland Revenue’s recent performance improvement review was for it to be more prominent in promoting what actions it has taken against non-compliant taxpayers. We’re seeing more of that this week when Inland Revenue was announced that an Auckland couple have been sentenced to three years in prison on tax evasion charges. The pair committed 69 tax related offences involving income tax and GST evasion amounting to about $750,000, together with another $80,000 in unaccounted for PAYE. The judge described it as very deliberate offending including deliberate under reporting of business income filing false returns, and even failing to file false returns once under investigation. The couple withheld information from their accountants and concealed the existence of what were described as “highly relevant bank accounts.” So pretty clear case here of tax evasion.

One thing of note that does slightly concern me is this offending occurred over a six year period between 2010 and 2015. That’s quite some time ago and I think Inland Revenue is much more on the case now. Even so you would hope that it doesn’t take 7-8 years or more to bring people to justice on this in the future.

The taxman cometh…

For an idea of how Inland Revenue’s increased activities might play out for your average person, this week’s episode of RNZ’s podcast The Detail discussed how Inland Revenue plans to utilise its additional funding. The episode focuses on the construction industry because of the sector’s long association with the proliferation of the “cashie”. Inland Revenue apparently gets 7,000 anonymous tip offs a year, many of which relate to tradies.

There’s some very interesting commentary from Malcolm Fleming, the New Zealand Certified Builders Association chief executive. He rightly points the finger back at the public for this issue. As he notes, nobody asks their accountant or lawyer ‘Well, how much is it for cash?’ On the other hand, the public seems to be happy to try this tactic with builders and others in the construction industry. On the question of tax evasion and cashies, maybe quite a few people should be looking in the mirror about that rather than pointing the finger elsewhere. It’s a very valid point.

The episode is well worth a listen; it highlights more of what Inland Revenue is currently doing. It’s now doing unannounced site visits to construction sites, for example, which I’m sure would alarm some businesses. But to be fair it also points out most small businesses are run on the straight and narrow. They are perhaps poorly capitalised with overworked owners who are also the main administrator. In many cases the question of tax arrears is more one of poor administration rather than in the case of the couple who were jailed, deliberate malfeasance.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue releases three special reports regarding the changes to the platform economy rules, the 39% trustee tax rate and the new 12% offshore gambling duty

Under the banner “Cut your excuses and sort your tax” Inland Revenue last Monday issued what it called a “last chance warning to the construction sector” to do the right thing and get on top of their tax obligations. The release advises that if people do the right thing, then Inland Revenue will help them. If they don’t, Inland Revenue will find them and start follow up action.

Richard Philp, a spokesperson for Inland Revenue, commented;

“Most people and businesses in New Zealand pay tax in full and on time but there is a core group who don’t. … we also know that while some are struggling just to keep up with the everyday grind, others are actively avoiding their tax obligations.”

Tax evading tradies?

Apparently, tax debt is high in the construction sector and there’s also a fair amount of cash jobs apparently happening in the sector. The Inland Revenue release commented that across all sectors, it gets about nearly 7,000 anonymous tip offs about cash jobs and the like each year noting “Construction is the industry most anonymously reported to Inland Revenue”.

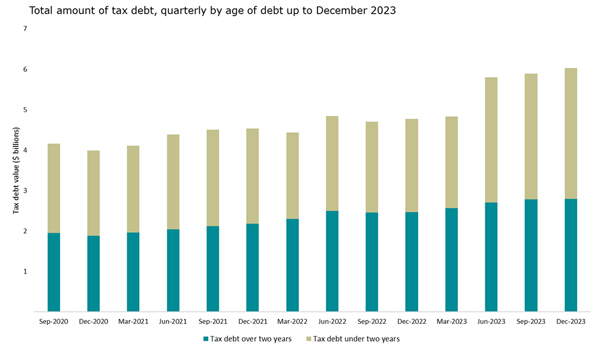

The media release is silent about the extent of the debt within the sector, but we do know from the latest statistics as of 31st December 2023, that tax debt over two years old has increased to from $2.5 billion in December 2022 to $2.8 billion in December 2023.

ADVERTISING

Understandably, with the Government’s books under pressure, Inland Revenue is keen to collect as much of this overdue debt as quickly as possible. This is probably the first of many such campaigns where we will see Inland Revenue taking additional action. And remember, under the Coalition agreement, additional resources have been promised to Inland Revenue for investigation work.

In this particular campaign, Inland Revenue is saying it’s going to issue emails and letters to 40,000 taxpayers in the construction industry who have either outstanding tax debt or tax returns, or both. It then specifies that 2,500 of those will be contacted by text message, asking if they would like to support to get their outstanding tax sorted. There will be a follow up call if the taxpayers they respond that they do want help. Inland Revenue will also be carrying out site visits to key locations across the country.

As I said, this is likely to be the first of several initiatives we’re going to see from Inland Revenue. I would be interested in seeing some specific stats around the proportion of debt and the composition of debt and get an understanding of what sort of businesses are struggling here. It will also be interesting to see how successful this campaign turns out to be.

More on the new GST rules for online marketplaces

Last week I discussed the confusion that seems to have arisen following the introduction of new GST rules from 1st April. These rules affect people who are not GST registered but provide services through such apps as Airbnb, Bookabach and Uber.

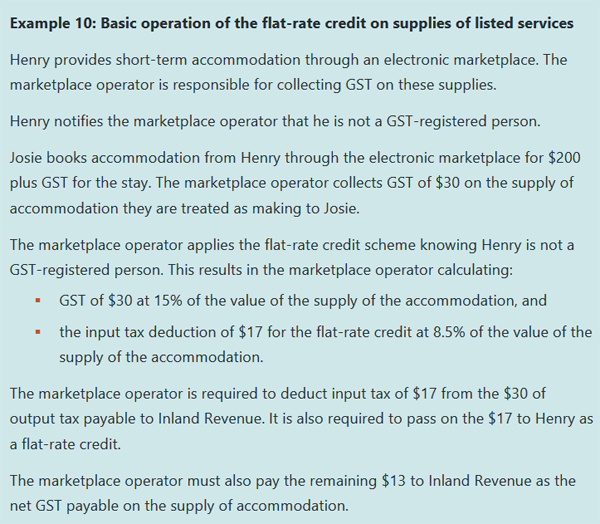

This week, Inland Revenue released three special reports relating to the new legislation and one of these is on accommodation and transportation services supplied through online marketplaces. In fact, this is an updated version of a report previously issued in June last year. The report has been updated to include the changes that took effect as of the start of this month and in particular how the flat-rate credit scheme operates.

Changes to online marketplace operators

Under the new rules, so-called online marketplace operators such as Airbnb, Uber and Bookabach will charge GST on all bookings made through them. However, the person who actually provides the ride or the accommodation may not be GST registered. This is where the flat-rate credit scheme comes into effect as the following example illustrates:

The full report is 68 pages so there’s plenty more to dive into.

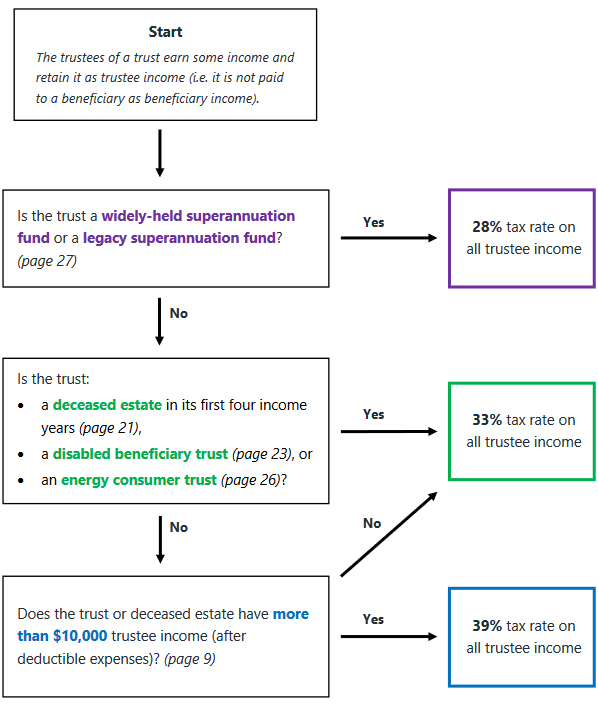

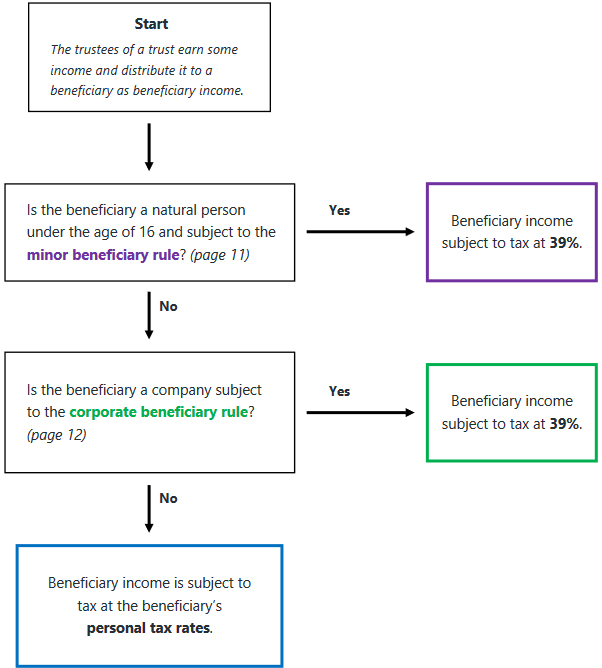

Special report on 39% trustee rate

One of the other reports that was issued is on the application of the trustee rate of 39%. Basically, trustee income is the net income of the trust, which has not been distributed to beneficiaries. The 30-page report explains the basic provisions about “beneficiary income” and “trustee income” together with a couple of useful flow charts.

Trustee income flowchart

Beneficiary income flowchart

The report references the minor beneficiary rule which applies where the beneficiary is a natural person under the age of 16. In such a case only $1,000 of income per year can be distributed to that person as beneficiary income and be taxed at that person’s marginal tax rate, presumably below 39%. Under the new rules, any beneficiary income in excess of $1,000 paid to a minor would be taxed at 39%.

Overall, this is useful guidance. Just remember the $10,000 threshold is all or nothing: if trustee income is $10,000 or less, the trustee tax rate that applies is 33%, but if it’s $10,001 then it’s 39% on everything.

The third report is on the proposed offshore gambling duty, which takes effect from 1st of July and will apply to online gambling provided by offshore operators to New Zealand residents.

The bright-line test and tax evasion – a couple of useful real-life case studies

Finally, this week a couple of interesting Technical Decision Summaries from Inland Revenue. Technical Decision Summaries are anonymised summaries of some interesting cases that Inland Revenue’s Tax Counsel Office has encountered either through tax disputes and investigations or applications for binding rulings.

The first one, TDS 24/06, is an application for a ruling regarding whether the bright-line test or section CB 14 of the Income Tax Act would apply. The facts are complicated but involve three sections of land currently owned by the ruling applicant.

The applicant had initially acquired one section outright before his spouse and another co-owner acquired interests as tenants in common. Over time, the applicants proportion of the ownership changed until at the time his spouse died the property was held 50% as tenants in common with his late spouse. The second section was owned 50% each as tenants in common with his late spouse. After her death her 50% interest had passed to him under her will. The third section was owned by the applicant and his late spouse as joint tenants. Following her death, her interest was automatically transmitted to him.

The ruling applicant was concerned about the treatment of future sales. Would the bright-line test apply or failing that, would section CB 14? This section is a little used provision and applies where there’s been a disposal within 10 years of acquisition and during that time there’s been a 20% more increase in value of the land thanks to a change in zoning, or removal of restrictions.

The Tax Counsel Office concluded neither the bright-line test nor section CB 14 would apply. This is obviously a good result for the taxpayer but it’s actually also a good example, of how you can apply for a ruling to get Inland Revenue’s interpretation on a tax issue. You don’t necessarily have to follow it, but if you don’t, you better have good reasons for not doing so.

Fiddling the books and getting found out

On the other hand, TDS 24/07 involved suppressed cash sales, GST and income tax evasion and shortfall penalties. The taxpayer carried on a restaurant business which was registered for income tax and GST. Inland Revenue’s Customer Compliance Services (CCS) investigated the company and formed the view that there was fraudulent activity going on. There was suppression of cash sales, and the taxpayer was under returning GST and income tax.

CCS reassessed the taxpayer’s GST and income tax returns for the relevant periods and they increased the taxable revenue for suppressed cash sales based on analysis of point of sale data, the taxpayer’s bank statements and industry benchmarking.

Industry benchmarking – an underused tool?

Just on industry benchmarking, I think Inland Revenue ought to be much more public about its data here and warn taxpayers there are benchmarks against which it will measure your business. It has done so in the past, but I think the combination of Business Transformation and then the pandemic interrupted progress in this space.

What people should remember is, Inland Revenue has some of the best data available anywhere about measuring industry benchmarking. I believe it should be making this much more public so that it can serve as an early warning shot for businesses that think they can suppress income. Everyone loses when this happens. Gresham’s law about bad money driving out the good is very applicable here, because businesses which are not tax compliant are undercutting those businesses which are following the rules. This is not a healthy situation as it leads to considerable frustration and anger and if not dealt with, will just simply encourage more of the same behaviour.

Tax evasion? Have a 150% shortfall penalty

In this particular case, the taxpayer’s fraud was identified, and GST and income tax reassessments followed. In addition, Inland Revenue also imposed tax evasion shortfall penalties, which are 150% of the tax involved. These evasion shortfall penalties were reduced by 50% for previous good behaviour, but that’s still represents a penalty of 75% of the tax and GST evaded.

Unsurprisingly, the taxpayer counter-filed a Notice of Proposed Adjustment under the formal dispute process, and the dispute ended up with the Adjudication Unit, which is run by the Tax Counsel Office as part of the formal dispute process. The Adjudication Unit did not accept the taxpayer’s counter arguments, including an attempt to claim an income tax and GST input tax deduction for the cost of fresh produce purchased with cash. The problem was there was no supporting evidence for this claim, so the Adjudication Unit probably found it easy to reject it. The Adjudication Unit ruled not only was the tax due, but the penalties were also correctly imposed.

Get ready for more Inland Revenue action

Circling back to our first story, this TDS illustrates what lies ahead for those in the construction industry who have been suppressing income. As I said, I do think Inland Revenue should make everyone more aware of its benchmarking data which would be a warning for would be tax evaders. It’s pretty clear from the announcement about the construction industry that Inland Revenue is gearing up for many campaigns targeting debt arrears and clamping down on tax evasion in particular industries. As always, we will keep you updated as to developments in those areas as they happen.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.