Lessons from the largest known GST fraudster – could it happen again?

Corporate tax cuts – who benefits and what does the public think?

The tax year-end of 31st of March is fast approaching and at this time of year tax agents are busy with the last year’s tax returns and also giving a heads up to clients about what actions they need to take ahead of 31st March. It’s always an incredibly busy period and it’s often easy to overlook some important matters amidst the rush and the mayhem. So, here’s a quick reminder of key issues that that you should be considering as the tax year ends.

GST and Airbnb

First up, a GST election is running out in respect of being able to take assets out of the GST net. We discussed this a few weeks back. To quickly recap, this could particularly affect Airbnb operators that may have bought a residential property, rented it out and then realised that Airbnb produces a better return. They’ve therefore signed up to Airbnb or other apps and then registered for GST either voluntarily or because they’ve exceeded the $60,000 registration threshold.

Subsequently, the taxpayer may have claimed an input tax credit on the property but now realise that they could be liable for a substantial GST bill on any subsequent sale of the property. That obviously is a big shock.

To address this issue, a transitional rule was introduced under section 91 of the Goods and Services Tax Act with effect from 1st April 2023. The rule enables a person to elect to take an asset out of the GST if the following four criteria are met:

the asset was acquired before 1st of April 2023; and

it was not acquired for the principal purpose of making taxable supplies; and

it was not used for the principal purpose of making taxable supplies; and

a GST input tax credit was previously claimed, or the asset was acquired as part of a zero-rated supply.

If all those criteria apply, then the person can elect to take the asset out of the GST net and pay back the GST that was claimed on the original input tax. In other words, they don’t pay GST on the increase in value. A good example here would be a bach or family holiday home which was subsequently rented out for short stay accommodation.

The key thing is this election expires as of 1st April 2025, by which time you must have notified Inland Revenue of your election. You don’t necessarily have to pay the GST; you can do so as part of your GST return to 31st March, but you must have notified Inland Revenue in a satisfactory manner. I would recommend using the MyIR message service to do so.

Other year-end matters

There are a number of elections relating to whether or not a taxpayer wants to adopt or leave a tax regime. A classic example would be companies entering or leaving the look-through company regime. Another, lesser known one would be entry or exit into the little known, and apparently little used, Consolidation regime.

Another matter that pops up regularly around year-end is checking your bad debts ledger. Bad debts are only deductible for income tax purposes if they are fully written off by 31st March so make sure this happens. Then there is the year-end fringe benefit tax returns where taxpayers should check to see whether they are making full use of any available exemptions.

A very important one for companies is to ensure their imputation credit account, either is in credit or has a nil balance. If there’s a debit (negative) balance on 31st March, that will result in a 10% penalty. It may be possible in some cases to make use of tax pooling to rectify some of these issues.

Finally, if you’re registered with a tax agent, your tax return for the 2024 income year must be filed by 31st March otherwise late filing penalties may apply. Possibly more critically, the so-called “time-bar” period during which Inland Revenue may review and amend already filed tax returns is extended by another year.

Lessons from the country’s biggest known GST fraud

Moving on, an interesting story has popped up in relation to what was then the largest known GST fraud. Gisborne farmer John Bracken was jailed in May 2021 after he was found guilty of 39 charges of GST fraud. He had run a scam through his company, creating false invoices totalling more than $133 million between August 2014 and July 2018 which resulted in receiving GST refunds totalling $17.4 million to which he wasn’t entitled. He was jailed and is currently out on parole.

At the time he was sentenced Inland Revenue and the police issued restraining orders and are trying to make an application for an asset forfeiture. In other words, assets subject to the forfeiture order were acquired through fraud and should be forfeited and handed to the Crown.

Now naturally Mr. Bracken and his family, including his wife and his parents and his son, are all fighting back on this because they stand potentially to lose assets that may be subject to the restraining order and subsequent forfeiture. The interesting part of this is the sheer scale of what went on and how it went undetected for four years before an employee got suspicious, notified the Serious Fraud Office, who then tipped off Inland Revenue.

At the time the frauds were committed, Inland Revenue was at the start of its Business Transformation project, upgrading all its systems. Until it got tipped off It had no idea of the extent of the fraud. Mr. Bracken appeared to have covered his tracks reasonably well, although once uncovered it was a fairly simple GST fraud. He just submitted fraudulent GST invoices, but he was careful to get them from actual companies with whom he had established some form of trading relationship.

Obviously the concern is now twofold. The Crown will be wanting to recover as many assets as possible to the value of the $17 million that it was defrauded, but also, can this happen again?

I’d like to think “No”. Certainly, Inland Revenue feels that its new systems have enhanced its capabilities greatly and that would appear anecdotally to be the case. There was a GST fraud scheme spread by TikTok influencers which caught the Australian Tax Office completely off guard and was worth tens of millions of dollars. Inland Revenue feels that that sort of fraud could not happen here. Mr Bracken’s release on parole and the ongoing forfeiture case is a reminder that Inland Revenue has to be vigilant all the time.

But sometimes it comes down to a conscientious person, an employee usually, tipping off the authorities. But it shouldn’t always come down to that. Inland Revenue and other authorities should be able to pick up signs of these frauds. As I said, I have confidence they do, but I would also hope that confidence is not tested too much.

Corporate tax cuts – a possibility or just flying a kite?

In recent weeks there’s been some chatter or hints from the Government and Finance Minister Nicola Willis about a potential corporate tax cut. She made the not unreasonable point that our corporate tax rate is high by world standards. This prompted comments from the former Deputy Commissioner of Inland Revenue Robin Oliver that tinkering around the edges by reducing it from 28% to 25% might not achieve much. If the Government wanted to attract investment, they’d have to go big, maybe nine or ten percentage points cut. Robin was sceptical the Government could afford to do so because of the loss of revenue. And I agreed with that assessment.

I do wonder whether this idea might be something of a bit of a red herring. Some comments I’ve heard seemed to suggest that maybe the Government was just flying a kite to see the reaction.

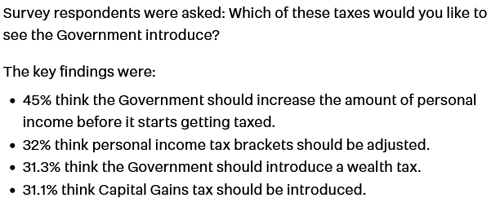

Anyway, this week a poll run by Stuff which suggested that very few would support a corporate tax cut, or rather that the population was pretty lukewarm about the idea. The poll carried out by Horizon Research, found only 9% of adults supported lowering the corporate tax rate, while 25% actually wanted it increased. There were a few other interesting results:

Who would benefit from a corporate tax cut?

Craig Renney (the chief economist for the Council of Trade Unions) and researcher Edward Miller also looked at who would benefit from a drop in the New Zealand company tax rate. They concluded the main beneficiaries of a corporate tax cut would probably be overseas shareholders. In terms of attracting greater foreign direct investment, they saw little evidence that corporate tax cuts would be likely to achieve that.

As they noted,

“…company taxation is only one aspect of a decision by a company or fund to invest in New Zealand. In addition to the company tax rate, there is the R&D tax incentive, the lack of a capital gains tax, and the lack of substantial payroll taxes. These taxes affect the actual tax paid by corporates in comparison with other countries when considering investing in New Zealand.”

Renney and Miller’s modelling suggested that a tax cut would not result in further investment but would just simply increase the funds flowing offshore. In particular they saw the Big Four Australian banks as being prime beneficiaries. The pair estimated that a cut from 28% to 20% would have increased the annual income to offshore shore shareholders by up to $1.3 billion.

There’s always a lot of debate around the benefit of corporate tax cuts, whether they do drive investment, or they simply put money into the back pockets of the shareholders. That debate has gone on for a long time and continues again. But it’s interesting to marry that along with the public’s general lack of enthusiasm for such a cut.

Yeah, but what about the IMF?

I think it was also noticeable that the International Monetary Fund in its recent Concluding Statement for its 2025 Article IV Mission suggested “judicious adjustments to the corporate income tax regime.” So maybe it too isn’t entirely sold on corporate tax cuts as a key driver for investment.

No doubt more will be revealed in May’s Budget. And until that time speculation will mount, but we will find out on the day and as always, we will bring you the news when it emerges.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

This week our guest is Tracey Lloyd, Service Leader Compliance Strategy and Innovation at Inland Revenue. We discuss how Inland Revenue’s new START system enables it to detect fraud.

TB: My guest this week is Tracey Lloyd, Service Leader, Compliance Strategy and Innovation at Inland Revenue. Kia ora Tracey, thanks for coming along.

Tracey Lloyd: Thank you for asking me.

TB: What’s your role within Inland Revenue? What does Compliance Strategy and Innovation mean?

TL: OK, so I’m the service leader of a relatively new unit in Inland Revenue called Compliance Strategy and Innovation or CSI for short. During Inland Revenue’s Business Transformation, we introduced our brand-new computer solution called START (Simplified Taxation and Revenue Technology). I oversaw the team that was responsible for utilising the analytical tools of that system once Business Transformation was finished. CSI was designed to take over and expand the work that we had been doing. It’s been in existence for about 20 months now and there’s 25 of us, including me.

TB: CSI Inland Revenue sounds very ominous but joking aside you’ve got these new tools that Business Transformation has provided and other Inland Revenue officials have told me that it has greatly enhanced your capabilities. How have you deployed those capabilities? What does CSI do in this case?

TL: We’re basically using intelligence to lead our approach to compliance. We combine insights from our customer segments, what our customers are saying, what our people are seeing, our systems, the tax and social policy products that we administer and analytics. We then connect the dots between all those different challenges to help the leadership teams make decisions about how to prioritise compliance initiatives.

It’s not just proactive compliance activities. It’s such things as sending out query letters, following up overdue debt overdue returns, but also working on educating our customers through tailored communications marketing campaigns and of course audit work.

Basically, we look at problems where our compliance is not good or where customers are confused. And we think how we can help; how can we help our customers and how can we improve compliance with the amazing tools that we now have available?

CSI – connecting the dots and checking COVID payments

TB: Where is an initiative that you’ve been able to deploy some of these tools, which has helped clear up confusion?

TL: Probably one which we should probably touch on is how CSI interacted with the Ministry of Social Development (MSD) and some of the various COVID products that Inland Revenue administered.

MSD had the wage subsidy, and I won’t cover our interactions with them over that. I just want to clarify that if someone was in business and eligible for the wage subsidy which was administered by MSD, then that wage subsidy had to be in their income tax return.

What we found within one week of the 2021 tax returns being able to be filed was that 80% of people who’d received the wage subsidy were not returning it.

TB: 80%? Wow!

TL: Yes, 80% and obviously we can identify that but then every single one of them needs some manual action and a contact for us to ask whether people are happy for us to include it because there was the odd one where the data wasn’t quite right, but only very rarely.

What we did is we worked with MSD who were super helpful, and we were able to upload those Wage Subsidy files and pre-populate that information within 10 days into everyone’s tax returns. That meant that we went from an 80% fail rate of people including it to a 20% fail rate where it was pre-populated, but people were perhaps changing that figure or deleting that figure out of their return before they submitted it.

TB: What happened then if they deleted or amended those numbers?

TL: The return would be stopped for manual review. We would contact the person and ask if there was a reason for the change, maybe they had paid some of it back to MSD. And so we would liaise over that to check that they returned the right amount.

TB: This group of people would be self-employed or shareholder employees because everyone’s else wage subsidies should have gone through PAYE?

TL: Yes, that’s right. If you were an employee, then there was no impact to you.

TB: The other COVID support payments, those were directly Inland Revenue’s responsibility?

TL: They were, so we had Covid Support and Resurgence Support Payments and the Small Business Cashflow Scheme.

CSI in action – detecting COVID fraud early

TB: I see today there’s a report about a Waikato sharemilker who was sentenced to home detention for fraudulently claiming Covid Support Payments and the Small Business Cashflow Scheme. https://www.ird.govt.nz/media-releases/2023/waikato-sharemilker-sentenc… How might you have picked this up?

TL: Well, a lot of the work that we did was at front end based on the application rather than letting the money out the door because it’s very difficult to recover once the money’s gone out.

We are obviously doing that audit activity because we’re starting to see prosecutions following on from those reviews. We will contact people and determine whether they fraudulently applied for it or applied in error.

But what we were able to use START for was to proactively stop those applications in the system based on running them across a whole lot of rules and then stop suspicious ones for manual review.

To give you an example of some of the rules that we ran such as duplicate bank accounts, or if someone had a few entities using the same bank account, that was usually a a trigger for us that there was some sort of identity theft potentially going on. We also had examples where we had no record of that particular customer being in business at all. We stopped applications completed from offshore, as you had to be a New Zealand based business.

TB: You would have identified those offshore applications through the domain and the IP address.

TL: That’s right. All that information was available to us. We also had people putting deceased persons on their employee schedule or the number of employees over lockdown were going up, that generated some questions from us. We found employees that were either children or very, very elderly.

Sometimes the same employee was on a large number of schedules, which also raises a number of questions. Currently one of my team is preparing for a prosecution relating to a Resurgence Support Payment claim.

Just on Resurgence Support Payments, applications used to open at 8:00 AM in the morning and there five or six different iterations over time. One time, something like four out of the first five applications that arrived within a couple of minutes after 8:00 AM were fraudulent. A lot of those claims were from offshore, but our systems were able to stop all of those.

In relation to Covid Support Payments we stopped 9% of all applications for manual review. That’s actually quite low if you think about it. 91% went automatically out the door overnight and people got the money that they desperately needed.

Of the 9% that we did stop, we declined 66% which is a very high percentage. Generally speaking, the ones that we did pay out after stopping for a manual review were people who had recently started in business. So we asked them for some proof of business and that type of stuff and then the application was fine. I know that’s no help to customers who had to wait, but did get the money in the end. But we did decline about 33,032 applications and we stopped $147 million from being erroneously issued to people who weren’t entitled.

With the Small Business Cashflow Scheme loan, we declined 67% of the applications we stopped and this amounted to $550 million.

TB: I mean the Small Business Cashflow Scheme was in many ways bigger than the various Covid support payments, I think it ran to over $1.5 billion. [$2.3 billion per Inland Revenue’s Annual Report for 30 June 2022] So people attempted to borrow $550 million on top of what was already lent?

TL: Yes, that’s correct. It’s testament to the people that we had working on it and the new system that we were able to do it proactively instead of coming along afterwards and saying hey, you shouldn’t have got that money, can you pay it back because that’s very, very difficult.

TB: I mean the wage subsidy is a good example of a high trust environment. It was money out the door because we’re in the midst of the COVID crisis.

TL: That’s right, the wage subsidies were the first COVID product that was paid out.

Lessons from the Australian Tax Office TikTok GST scandal

TB: To give a comparison with another overseas tax agency that didn’t quite get it so right, there’s this ongoing scandal over the Australian Tax Office where these TikTok influencers basically said, “Here’s how to scam the ATO out of GST”. I think it’s over a billion dollars and counting. The ATO has admitted it really isn’t sure how big this scandal is, and that’s quite staggering.

I mean, what do you do about that? Could TikTok influencers do that here?

TL: We’re going to talk about Integrity Manager a little later but we’ve definitely had people send us snips of social media marketing along the lines of “Hey, give me your IRD number and I’ll get you a refund” but nothing quite to the extent of Australia.

We keep a very, very close eye on our own GST to ensure that nothing like that will happen in in New Zealand. We’ve spoken to our senior execs about it and we’re very comfortable that we would be able to react immediately if we saw any of that behaviour. But I mean that the numbers are just staggering over in Australia.

TB: To repeat a point I made earlier, conversations I’ve had with other Revenue officials is that if START hadn’t been available when COVID turned up, it would have been very difficult for Inland Revenue to have run any of these COVID support programmes. They probably would have all had to have been run out of MSD with a higher risk of fraud, perhaps.

TL: Yes. Or even just high trust model with payouts from Inland Revenue with no checking beforehand.

START and auto-assessment

TB: One of the great things that START did was to bring in the year-end auto-assessment routine. https://www.ird.govt.nz/income-tax/income-tax-for-individuals/what-happ… People no longer had to either go through a tax agent or the tax intermediaries and instead the majority of taxpayers who are salary-earners with all their income having tax withheld either through pay as you earn or through resident withholding tax are now on auto assessment.

You just mentioned Integrity Manager this is something that is part of this auto-assessment routing. How does it operate? Because you’re dealing with 2,000,000 taxpayers in six or seven weeks.

TL: I think our last auto-assessments had 3.2 million individual income tax returns were sent to customers and 88% of those required a customer to do absolutely nothing. I was one of those, I didn’t have to do absolutely anything.

We’ve discussed Decision Support Manager which we used for the COVID products and Integrity Manager is another amazing tool that we now have which stops returns with potential errors and fraud in them.

Every single tax return goes through Integrity Manager before it’s processed. We screened 10 million tax returns in the last year.

TB:Tax returns would not only be individual tax returns, but also GST returns which would be a big group and particularly the Pay As You Earn filings.

TL: The only one that doesn’t have rules through Integrity Manager are the PAYE employer schedules. That’s because we need to make sure that the deductions and entitlements get paid out as soon as possible. You know, Child Support and Student Loan, etcetera. But we will do some back work on that on those.

Basically, we review Non Resident Withholding Tax, Approved Issuer Levy, GST returns and donations. That’s another big group where we also run rules over returns. And so, while we had 10 million tax returns in the past year, over 200,000 were looked at to be manually reviewed because they hit a rule which raised some concern from us.

TB: That’s what 2% of all returns?

TL: Yes, a pretty small group. So, some of the main areas we look at are GST, income tax and donations. They’re our big ones and examples of some of the things that we review are changing pre-populated figures. You know, why are you changing them? Because we have already got that data. Another is making up figures even though we can check that against other data we hold. I think you could describe that as a frequent flyer, shall we say. Every year people just making up figures.

Snapshotting to prevent incorrect tax returns

TB: You gave an example at a recent ATAINZ conference where one person was constantly changing the online return until they got the right number and by that stage they had amended it 50 or 60 times.

TL: We call that Snapshot and it’s another tool in the new START system. It’s the ability for us to view activity in myIR. We also use it just as much internally. For example, every time I’m in the system it’s all recorded and for training purposes. So when we’ve got someone on the phone, I can hear the people sitting behind me saying, “OK, you’re in the wrong part of the return. You need to go to this particular tab to do what you’re trying to do”. We’re able to track where a person is and help them through the system.

But one of the sides things that’s come from that is that we’re actually able to look at what someone’s done while they’ve been filing their return. For example, we can see when people are adjusting figures, to see how big or small the refund is now and then going back and changing the figures. Doing this backwards and forwards and backwards and forwards countless times.

Now if you’re doing that type of behaviour, even either you’re really confused and you need some help from us, or you’re just making up figures. And so, we have the ability to see that and we’re also able to stop such returns.

Some of the other rules we can run identify an IP address which has been used to commit fraud in the past so we can red list that. Identity theft is an ongoing issue for us unfortunately.

Overclaimed donations and other “creative” deductions

TL: Other rules that we have include one for large school donations, which may possibly be private and therefore not allowed. Or large donations compared with total income. It may be totally legit, but let’s just ask a question about it and see how you how you go.

I mean in the past we’ve had people just making up figures and putting them in the return such as made-up employee share scheme figures. We’ve seen interest and resident withholding tax entries that are the same amount – $10,000 and $10,000. What we also see is that when people are making up figures to put in their return, they quite often make them all zeros. Nothing quite like a round number.

Over the last year to June 2023 year Integrity Manager reviews stopped $145 million of incorrect or fraudulent refunds dollars. $56 million of this was voluntarily disclosed by customers. Another $89 million of refunds were stopped after we engaged with the customer and asked them some questions.

With regards to some examples of non-business expenses, these have been a continual source of frustration for us. Under the auto-assessments system there are only four or five things that you can claim for. The one that most people claim for is for loss of income insurance. the main. But we get everything, literally everything coming through there.

One example I’ve got is someone had claimed just over $15,000 of non-business expenses and when we called to ask what it was, he said that he’d paid quite a lot of tax and his father-in-law suggested he claimed some of it back.

TB: Nothing like being honest.

TL: We did sort of point out that the amount of tax you pay is relevant to the amount of income that you and this person had earned a significant amount of income. We had another one where this person was only on salary and wages but had claimed $20,800 of non-business expenses. When we asked what they were, she said her son was at Auckland University and she was still supporting him. She thought she should be allowed to claim his expenses and added up his rent and groceries because he eats quite a lot. She did ask if we could put it in another box if that would help. But we said there was no other box that we could put that in.

But an example of a more deliberate fraud, shall we say we had someone who was receiving Working for Families but had no income at all. And then when we did some deep diving into their searches, we found fifteen other customers were linked to the same bank account. And a majority of those customers were overseas because we can do Customs checks.

TB: Yes, because you share information fairly frequently.

TL: We do very regularly.

TB: In my role we’re often determining when someone became tax-resident. We’ll tell a client go to Immigration and they’ll come back to you with the dates you arrived and left the country. Clients are often incredibly impressed how efficient Immigration is with providing those details. And I’ve been in a meeting where the file of information which had been shared from Customs and Immigration was literally about a foot high and I thought “We’re in a bit of trouble here.” Unsurprisingly, we didn’t win that case.

So, yes, a lot of information sharing regularly goes on. It’s a common theme in the podcast, but I think people do not understand just how much information is shared and how much information you can access.

TL: That was definitely something that we saw with the wage subsidy when we pre-populated returns. And you know people deleted the entry and we asked “Why?” and they actually admitted to us straight off the bat that they weren’t actually eligible for it.

And we’re just like “Well, we’re not sure what you want us to do about that because you did actually receive the money.” They didn’t obviously think that we would talk to MSD and get that information. While the pre-population was a second step, we were always getting that file with the income information.

Running information campaigns and engaging with migrant communities

TB: Inland Revenue sometimes runs campaigns based around this misinformation. Talking about expenses are I recall recently there was a campaign advising real estate agents about what they could claim. https://www.ird.govt.nz/pages/campaigns/realestateagents This arose because it had come to your attention that there seemed to be a lot of expenses being claimed. And I think the result of that campaign was the following tax year the amount of expenses claimed declined, is that right?

TL: That’s right. Integrity Manager was used because obviously we have BIC codes which tell us who’s a real estate agent. Yeah. And we’re able to look at the level of income compared with the level of expenditure. And it doesn’t necessarily always prove that there’s anything wrong, but it does beg a question and the number of very imaginative expenses that people claimed was huge.

And that’s why on our website now it’s very easy to find the real estate agents form which details what expenses you’re able to claim and what you cannot.

I think we also did that in a few different languages as well to hopefully help people understand the rules a little bit better because it can be different in other countries.

TB: Just to talk about other languages in there, there was a little snippet that came out of the report that was released in connection with the repealed Tax Principles Act. One of the comments about trust and Inland Revenue was that it was extremely high amongst migrant communities, and highest amongst Asian migrant communities. That’s credit to Inland Revenue for being able to build a level of trust there.

TL: Oh, thank you. Yes, our community compliance folks spend a lot of time working with our migrant communities and speaking to them in their own languages and going to trade fairs and community halls and so on. Helping people understand because they’re also entitled to social policy, which we need to make sure they get as well.

TB: That’s right. Inland Revenue is not just about taking tax off people. It also redistributes because it’s the key agency for distributing KiwiSaver, Working for Families, which is $2 billion and Child Support.

Inland Revenue and tax agents

TB: How important are tax agents to your role? Because we work with you on campaigns and we’ve seen increased engagement recently.

TL: Absolutely that’s certainly how it feels like to us. I mean, tax agents represent about 1.8 million customers to Inland Revenue. It’s a massive way for us to contact a huge customer group by using tax agents.

Many of the rules we’ve discussed when checking returns we don’t enable for tax agents because we just don’t see the same type of erroneous and fraudulent behaviour that we do with customers who aren’t represented by tax agents. You know, there’s always the odd one, but they’re very rare.

Tax can be really complex and tax agents are a critical part of making sure that people get it right. And as you know, we have regular meetings with Chartered Accountants Australia New Zealand and also with ATAINZ, which is how we met after I did a presentation at an ATAINZ workshop.

We share about what we’re doing with compliance, and you know how we can help. Quite often when we’re planning to do some sort of compliance campaign, the tax agents will be the first people that we contact to say, “Hey, this is what we’re gearing up to do, we’re just letting you know so that you can think about it in terms of your client base.”

Forthcoming campaigns on the shared economy and overdue Student Loan debt

TB: Speaking of which, any new compliance campaigns on the horizon?

TL: Well, there there’s a few that are sort of in the planning stages. Obviously, you would have heard about payment service providers with the new legislation. We’re getting that data and once we have that, obviously we will definitely kick off some campaigns around that.

We’ll be running a targeted campaign, focusing on raising awareness, educating and so on about ride sharing, food and beverage delivery and short stay accommodation. Trying to raise customers awareness and understanding as it applies from 1st April and some people might get caught out. We’ll soon start our next campaign on auto-assessments around just letting people know that’s coming soon.

The other big one that we’ve got on the go is about student loans. This targeted campaign is mostly focusing on overseas based borrowers who are in default. Only 26% of overseas borrowers are making the required repayments that they should be making on their loans whereas 94% of New Zealand based borrowers do.

The purpose of the campaign is to increase the overall compliance of student loan borrowing customers so that they understand their obligations when they leave New Zealand to perhaps go do their big OE and stuff that they’re still obligated to make repayments.

This particular campaign we’re slicing into nine specific segments to try and make our awareness campaigns a little bit more targeted and hopefully a little bit better at getting through to people. You might see some information on the sharing economy via LinkedIn, but you probably won’t see targeted paid advertising unless you’ve got a student loan debt or you’re doing a Uber side hustle.

TB: Quite a lot to ponder there about what CSI Inland Revenue is up to, but to wrap up what sort of message would you like to send Tracey. Like Liam Neeson in Taken we have the tools and we will find you?

TL: Pretty much. I mean obviously our first step is to make it as easy for people to get it right in the first place and we spend a lot of time reviewing how customers behave in the system so that we can help and maybe change the system to make it more intuitive for people. But you’re right, we’ve got these amazing tools and we’re using and utilising them all the time and we’re learning more and more about them. It’s a great system and it’s good for All New Zealanders.

TB: Computer projects are controversial but START has been an enormous project which was delivered on time and under budget. Just to put some numbers in context. You mentioned earlier about identifying $145 million of fraud. Inland Revenue’s annual operating budget is about $700 million so you pretty much pay for yourself very, very quickly.

On that note, Tracey, thank you so much for joining us. It’s been a pleasure having you on the Podcast.

TL: Thank you for inviting me.

TB: That’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A few weeks back, an issue emerged over in the East Coast and here in Auckland about the potential application of the bright-line test to homeowners who had been forced to move out following Cyclone Gabrielle and the January and February flooding events. The issue was if they had to leave the property for more than 12 months while it was being repaired or because they could no longer live there, the bright-line test could apply if they were forced to sell within the relevant bright-line test period.

The Government this week announced that it is adding a Supplementary Order Paper (SOP) to a tax bill that’s going through Parliament at the moment (and which will be enacted after the election).

The SOP contains proposals to ensure that the main home exclusion from the bright-line test is not affected by a property owner needing to vacate their North Island flood or cyclone damaged home for more than 12 months so it can be remediated or repaired. It also ensures the bright-line and other land-based timing tests, because we have a number of them, are not triggered when local authorities or the crown buyout properties impacted by the 2023 Auckland flood events and or Cyclone Gabrielle. You’ll recall that last month Auckland Council and the Government agreed to a $2 billion package which will be used to buy out homes that were rendered unliveable following Cyclone Gabrielle or the Auckland Anniversary weekend floods.

So, this is a good result. That’s the problem with tests, they can have some harsh results. But as the Government said, by picking up examples from what happened following the Canterbury earthquakes, it will devise tests to ensure that those harsh treatments do not follow.

Fooling around and finding out…

And speaking of harsh treatments, some harsh lessons were learned by a couple of taxpayers about tangling with Inland Revenue. In the first, an Auckland second hand car dealer has been sentenced to six months community detention for tax fraud. The offender Mr Levada created a false identity and then as a director and shareholder set up two companies. The companies were then used to obtain GST refunds totaling $309,000 even though neither company traded. There was a bit of a hard story behind this in that he wanted to help his wife’s family in Ukraine. But he admitted that he knew he was stealing and he has repaid the full amount owing.

Apparently, this got picked up by the Ministry of Business, Innovation and Employment in April 2021. And then obviously from there Inland Revenue realised what was happening. To me this is another example of why we really ought to think hard about GST compulsory zero rating between GST registered businesses. It reduces the opportunity for people to try and defraud the system. They don’t always get away with it, as we’ve just seen here. But maybe remove the temptation in the first place is where I would go with my suggestion.

Avoiding tax by forgoing all income?

But that story is really quite tame compared with a story from Nelson in the New Zealand Herald. As I told the reporter this is an “absolutely wild story”. Mila Amber had run into trouble with Inland Revenue and at the end of 2017 she was told she owed at least $110,000 in taxes, penalties and overpaid Working for Families tax credits. (In fact, the final figure was amended to nearly $365,000).

Amber decided to devise a scheme in cooperation with a UK based company under which she sold her property in Nelson to this company for $847,000. The buyer didn’t have to pay a deposit or any interest and just would simply pay off the property over 25 annual payments with the first payment due a year after settlement. The deal meant that the property was out of the reaches of Inland Revenue if they were going to try and seize the property or force a sale to pay off the debts. Amber was made bankrupt, and the Official Assignee took the case to court to try and overturn the sale. Which is how all these details emerged.

It’s just quite staggering what was attempted and what people thought was going to happen here. This seems to have been one of those cases where the taxpayer got really enraged by Inland Revenue’s actions. She changed the name of her trading company to Abbey Services (Killed by Tax Maladministration) Ltd which as the judge in the decision, called it rather unsubtle and refused to acknowledge the name basically in the judgement. The judge overturned the sale effectively transferring the property to the Official Assignee.

The judgement includes this rather jaw dropping line “It’s hard to see how it is beneficial to avoid tax by forgoing all income” which may be true but didn’t work out for Ms Amber. As I told the Herald, as the property seems to have been mortgage free she basically did herself out of half a million dollars. She’d have done better to have sold the property, pay the tax and move on.

I use this case to repeat something I’ve said many times previously. When you run into trouble with your taxes, talk to Inland Revenue. Go forward and initiate action and in most cases, if you are making reasonable offers and reasonable attempts to meet your liabilities and Inland Revenue can see that you’re being reasonable in your approaches, it will be prepared to find a way forward for everyone. In this particular case going around renaming your company Killed by Tax Maladministration and entering into a quite scandalously scheme to avoid those liabilities got the taxpayer nowhere.

I also think H.M. Revenue and Customs might be very interested as to what was going with the UK company involved. And I would put good money on details of the case having been shared by Inland Revenue with HMRC. I know from experience that Inland Revenue and other authorities share information on a proactive basis. We’ve talked in other podcasts about the Common Reporting Standards for the Automatic Exchange Of Information. Tax authorities are sharing data on a vast scale now.

The cases of this Nelson lady and the second-hand car-salesman are more examples of never underestimating Inland Revenue because it may appear slow, but it will eventually catch up with you.

Having just talked about international tax agreements, it’s very interesting to see the continuing debate around National’s tax proposals, which I discussed last week and in particular the issues around the proposed foreign buyers tax. This has led to quite a debate with National confident that its numbers stack up and that it is legally possible.

The question raised last week continues to be asked ‘Well what about international tax treaties and the so-called non-discrimination clauses?’ It turns out that just after last Friday’s podcast was recorded, National went and sought advice from Robin Oliver, a former Deputy Commissioner of Inland Revenue, member of the Last Tax Working Group and a real guru of tax.

He told RNZ, this is a “very esoteric” area of tax law but it should be possible to introduce the tax.

In his view it would depend on tax residency, not nationality. In relation to the Chinese double tax treaty, it doesn’t allow discrimination on the basis of nationality. The potential argument is that a Chinese national residing in China who purchases property in New Zealand could be subject to the new law, whereas a Chinese national resident in New Zealand could not.

But even if it could be done, I’m of the view whether you should do that. Both myself and Eric Crampton the chief economist of the New Zealand Initiative think tank, told RNZ that, ‘Well, yes, it might be doable, but on the other hand, what would it do for our reputation internationally?’ We build our trade agreements around being an honest broker in this, that we follow a rules-based approach.

A point that was made at the recent International Fiscal Association trans-Tasman conference is that these tax treaties are often related to trade agreements. So, these sorts of issues would have been on the table and part of the discussions. Having signed an agreement fairly recently and then now looking to apply a workaround to tax nationals from that country doesn’t look good for our international reputation.

Just because you can doesn’t mean you should

What this comes back to is a situation myself and other tax advisers I’m sure will sometimes encounter where we’re asked to advise on something. We look at it and come back and we say, ‘Well, looking at the way the law was written we think it’s possible.’ But then sometimes the question boils down to ‘Well you could, but should you?’ Sometimes in tax just because you can doesn’t mean you should.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue has released a draft interpretation statement on the research and developments loss tax credits regime. This is a refundable tax credit available to eligible companies when they have a loss which has arisen from their eligible research and development expenditure.

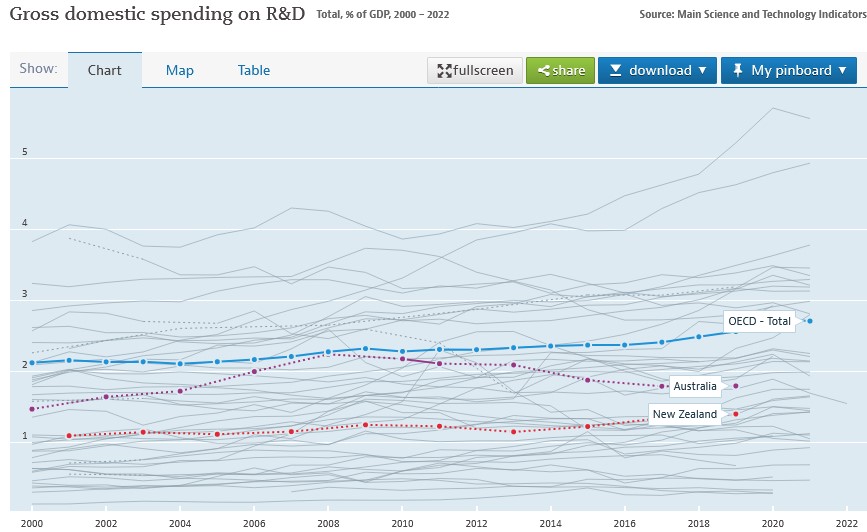

The regime was introduced in 2016 to encourage business innovation and also to address New Zealand’s poor record of R&D expenditure. According to OECD data, in 2019 New Zealand’s spending on R&D was just 1.4% of GDP, well below the OECD average of 2.56% of GDP. Over the past 20 years research and development in spending in New Zealand has been a full percentage point of GDP below the OECD average.

So given that we also have a poor record of productivity, increasing R&D expenditure is seen as critical in improving productivity and ultimately the strength of the economy.

That’s the background behind the introduction of the loss tax credits regime. It’s intended to assist the cash flow of those companies carrying out research and development. Often in the early years, these companies are running at a loss. Hopefully once the R&D matures and bears fruit, they will then have profits resulting from the expenditure.

But funding cash flow in those early years is pretty difficult. So instead of the tax losses to be used against future profits, under the regime, companies can instead receive a payment. Note, only companies can receive this R&D tax loss credit payment. That’s because losses incurred by partnerships, limited partnerships, look-through companies and sole traders can already pass those losses through to the underlying owners anyway, who will often be able to offset them against their other income. Essentially, they are already able to benefit from the ability to cash-up losses. But companies can’t do that, hence the introduction of the regime.

The Inland Revenue draft interpretation statement looks at the background to scheme, summarises the rationale for scheme and how it operates. A couple of key points about the regime: you can drop in and out of it, you can opt to choose a payment in one year but not in another year. Once you have claimed a refund by cashing up your losses, the regime operates rather like an interest free loan. You’re essentially required to repay it and it’s generally treated as being repaid when the company starts paying tax, the R&D having borne fruit.

However, there are other circumstances where the credit may have to be repaid earlier when there is, in the terminology of the regime, a loss recovery event. Now, that typically will happen if there’s a disposal or transfer of the intangible property, core technology, intellectual property, etc., which is done for either less than market value or the amount sold is a non-assessable capital gain.

Another situation, and this is actually one where I’ve been involved, is where the company is no longer tax resident in New Zealand. Some very interesting issues arise in that case. Then there’s the worst-case scenario, where a company goes into liquidation although what exactly can be recovered at that point is a moot point. But that’s still a loss recovery event.

And then finally, and similar to our other rules around the carry forward of losses and imputation credits, a loss recovery may occur if there is a loss of the required shareholder continuity. In the case of the tax loss credit regime, the relevant shareholding percentage is 10%. In other words, there’s no breach if at least 10% of the voting interests of the company are held by the same group of persons throughout the relevant period.

In my view this is a very important regime for improving the future productivity of the country. The scale of the spending is going on is quite interesting to see. We can get an idea of this because the Inland Revenue as part of the budget produces what is called a tax expenditure statement.

Tax expenditure statements are a summary of the cost of a particular tax preferred regime, which, like, for example, this regime, has been introduced for specific policy reasons. The OECD collects data on tax expenditures to get a global picture of what spending is going on in tax preferred regimes.

In the case of the R&D loss tax credit, the estimated value of the expenditure for the year to 30th June 2023 is $362 million, a little bit below 1% of GDP. The estimated expenditure for the year to June 2022 was $473 million. And you can see a steady rise since the regime was introduced in 2016.

Of course, the real importance of this regime is whether it has produced a boost in total R&D spending within the economy. And then ultimately, does that lead to increased productivity. It’ll be interesting to measure these once the data flows through in due course.

So, an interesting regime and good to see Inland Revenue give some guidance on this. It contains a few hooks but it’s well worth looking at if you’re thinking about trying to make use of the scheme. And as I said, we will watch with interest to see how it bears fruit.

Shuffling forward on internationalPillar One and Pillar Two proposals.

Moving on, we’ve talked fairly regularly about the OECD’s global minimum tax deal and Pillar One and Pillar Two. Last week the G20 met in India and the Secretary General of the OECD reported to the meeting that, “A historic milestone was reached at the 15th Plenary Meeting of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (Inclusive Framework) on 11 July 2023, as 138 members of the Inclusive Framework approved an Outcome Statement on the Two-Pillar Solution.”

In summary, what’s happened is that they’ve developed a text to a multilateral convention which will allow jurisdictions to exercise a domestic taxing right over the residual profits of the largest, most profitable multinationals. That’s what they call Amount A of Pillar One, and that will apply to multinationals with revenues in excess of €20 billion and profitability above 10%. What will happen is the scope of that taxing right will be 25% of the profit in excess of 10% of revenues. This €20 billion revenue threshold will gradually be lowered to €10 billion after seven years, conditional on the successful implementation of Amount A.

There’s a proposed framework for the simplified reporting application of arm’s length principle, which is key to transfer pricing and for baseline marketing and distribution activities. That’s what referred to as Amount B of Pillar One.

There’s a Subject to Tax Rule, again with an implementation framework, and this is really for developing countries to update their bilateral tax treaties to tax intra group income. This is where such income is subject to lower tax in another jurisdiction, in other words say one country has a 20% corporation tax rate. But that multinational shifts charges to another part of the multinational group in a jurisdiction where those charges are only taxed at a lower rate. This Subject to Tax Rule gives the first country more taxing rights in that income. Developing countries are very keen on this particular point because they feel that this is where the current tax regime has been almost predatory on their tax base.

There will be a comprehensive action plan developed by the OECD to “Support the swift and coordinated implementation of the Two Pillar Solution, coordinating with regional and international organisations”

On the face of it, all pretty much good news. But it’s interesting to read the views of those people who specialise in this field and there still seems to be quite a bit of uncertainty about whether in fact this whole thing will come to fruit.

In the meantime, for example, you’ve got lobbying going on in the United States. And it appears now that the US has managed to secure a further delay in the implementation of the Pillar Two global minimum tax 15% until 2026, according to a report coming out of the United States.

Pillar Two is the key proposal, because it applies to companies with annual revenues in excess of €750 million. Apparently, the US Treasury Department has managed to negotiate a delay in the implementation of this. It has got people watching all around the world as to what’s going on. It also means that the in the background, digital services taxes, for example, could still be ready to be deployed or introduced by jurisdictions if they feel that Pillar Two isn’t making enough progress and they want to secure their revenues. [Under the agreement just announced countries have agreed to hold off imposing “newly enacted” digital services taxes until after 31st December 2024.]

Overall, it’s a bit of a shuffling: one step forward, maybe half a step sideways and a quarter of a step back. In other words, progress is slow, but it’s still inching the way forward. Ultimately, it comes down to watching what happens in the United States and the lobbying goes on. If there’s a change of President next year all bets will be off at that point, I would say.

Smith, banged to rights, again. But should Companies Office be in the gun?

And finally, this week, the murderer and escapee, Philip John Smith, who’s been in jail since 1995 apart from the brief time he escaped to Brazil has now been sentenced to further two years imprisonment on tax fraud charges.

He was convicted for dishonestly using documents intending to gain pecuniary advantage, firstly, a application under the Small Business Cashflow Scheme and then for filing 17 false GST returns and a false income tax return. in total the attempted fraud was just over $66,000 of which was actually paid $53,593. He’s also been ordered to pay full reparations on that amount.

What he did was between October 2019 and March 2020, he registered five companies with the Companies Office with shareholders and directors, who were friends, associates or third parties unknown to him. He then he set up and activated myIR accounts for each company.

But Inland Revenue was quite quickly onto him, it seems, because it apparently detected the fraud involving the Small Business Cashflow Scheme in June 2020 only a few months after it started operating in April. So good quick work by Inland Revenue.

But the case also raises the point which an associate I bumped into this week mentioned, and that’s the actions (or inaction) of the Companies Office in allowing those five companies to get set up. New Zealand scores highly for ease of business in establishing companies. Many times, whenever I’m talking to overseas people, they are remarkably impressed about how quick it is to set up a company in New Zealand.

The question arises if people setting up companies by going directly through the Companies Office website, is it a little bit too easy? Was an opportunity to pick up Smith’s attempted fraud missed at that point by Companies Office? We don’t know. Accountants and lawyers are subject to the current anti-money laundering legislation, so we need to pay attention to what’s going on with company registrations and we have to obtain proof of ID. But my understanding is this process is a little less rigorous when you go directly through the Companies Office.

So good work by Inland Revenue picking it up quickly and catching Smith, again. But maybe some questions should be asked as to whether he should ever have been able to get that far along the line and that Companies Office should have picked it up sooner.

And finally, congratulations to the Football Ferns for their magnificent win last night at the start of the FIFA Women’s World Cup. I was lucky enough to be at Eden Park, which is why I might sound a little hoarse today! It was fantastic to experience such a great occasion even if the final nine minutes seemed like an hour. Congratulations again to everyone involved. Football definitely was the winner on the night!

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Property developers and a still too common GST mistake

EU proposes sharing credit card data to counter tax fraud

OECD proposes minimum global tax rate as part of BEPS initiative

Transcript

This week, a common and often very expensive GST mistake. The European Union ramps up its anti-fraud fight with a massive data sharing initiative, and the OECD suggests a global minimum tax.

Property developers provide a rich source of work for tax advisers and for Inland Revenue. That is because of the importance of property to the economy as a whole, but also in that they are often remarkably careless about the tax consequences of a transaction. This is probably a character flaw in that a developer sees an opportunity and knows they need to move quickly to maximise the opportunity. They therefore often go charging into a project without having someone on hand sweeping up the bits and pieces to make sure that all the i’s are dotted, and t’s are crossed.

In my experience, a key distinction between developers who fail and those who are successful is often the successful ones make sure that they have a team around them that does look after all the bits and pieces and the necessary legal frame, legal and tax frameworks to ensure the projects go ahead.

How this often manifests itself is that a developer might come across a residential property which is ripe for development and will make a bid for the property and purchase it. This is where the very common tax problem may emerge if the developers aren’t careful. If the developer purchases the property in the wrong entity, either personally or in a company or a trust which is actually used for development purposes.

At some point down the track, the developer’s lawyer or the accountant might say that property shouldn’t be in that entity and we need to get it into the proper development company. The developer often responds “Well, just deal with it. Get it into the appropriate entity”. And what will happen more frequently than it should happen is that a second transfer is made from the developer or the wrong entity to the correct entity.

And then the new entity goes and claims a GST input tax credit. For example, a residential property worth say $575,000 residential property was bought and was then transferred at a later date to the correct development company, which tries to claim an input tax credit of $75,000. Inland Revenue will turn it down.

The reason why it would turn it down is a provision in the GST Act, section 3A(3)(a). Now this provision has been in place since October 2000 and it is quite astonishing that 19 years on this issue keeps arising. Why?

What this provision exists to do is to stop people buying a property when no GST was paid. For example, a residential property bought from someone who’s not GST registered, holding it and then selling it at an inflated price to a GST registered entity, which then claims the input tax credit. This was something that was going on and was eventually put a stop to by the introduction of this provision in October 2000.

And the way it works is simply to say that if the transaction involves a sale between associated parties, the amount of the GST that can be claimed by the recipient party, the developing company in this case, is limited to the amount of GST paid by the original purchaser. So, if the purchaser buys from a non-GST registered person a residential property and then on sells it to a GST registered person no GST input tax can be claimed on the purchase because no GST was paid by the original purchaser of the property.

Now this is, as I said, a very common mistake I keep encountering. It’s a reminder to all people involved in the property industry to be careful when buying property to make sure that you have the correct entity settle on the transaction with all the necessary paperwork in place. Too often developers are keen to get something done and then buy in the wrong entity just to get the deal done. And unwinding that transaction is either impossible or proves very expensive. So that’s a word to the wise. But I still find it astonishing that this is an issue I’ve been dealing with repeatedly for 19 years.

A credit card trap

Moving on it’s been a busy week in the international tax world. I’ve spoken in past podcasts about the international efforts to address tax evasion and fraud. And this week, the European Union announced an initiative to counter e-commerce VAT(GST) fraud, which is estimated to be about costing 5 billion euros a year in the European Union.

From January 2024, credit card and direct debit providers will be obliged to provide member state tax authorities with data about certain payment details from cross-border sales. The anti-fraud Eurofisc Network will then analyse this data for potential fraud. This is another part of the massive information sharing programmes which are now common to international tax such as FATCA and the Common Reporting Standards on Automatic Exchange of Information.

Inland Revenue has been operating something similar to this for some time. The most notorious example I encountered was a family here had still kept a credit card issued by a UK bank. The mother wanted to come out and visit them and have a holiday in New Zealand. So, what she did was she put money into the credit card in the UK and they then used it for the only time to hire a camper van.

Inland Revenue found the transaction and knew that this was a credit card transaction that was made by a New Zealand tax resident. It issued a “Please explain” letter. And that turned out to be a very costly matter because in fact the son had made a pension transfer which got picked up and tax paid.

What’s notable is that Inland Revenue’s older computer system was able to track and find that credit card transaction. But following Business Transformation what will Inland Revenue’s computers be capable of tracking? It will be interesting to see. But the warning is that if you use a credit card issued by an overseas bank in New Zealand, Inland Revenue will come asking questions.

Tackling tax aribtrage

And finally, another very significant development in overseas tax. This is part of the ongoing work of the OECD/G20 Base Erosion and Profit Shifting initiative (BEPS). The OECD secretariat last Friday issued a discussion document on what’s termed the Global Anti Base Erosion proposal under Pillar Two.

I spoke on a previous podcast about the Pillar One initiative. The references to pillars, by the way, is because these proposals represent significant changes to the international tax architecture, hence the reference to pillars.

“seeks to comprehensively address the remaining BEPS challenges by ensuring that the profits internationally operating businesses are subject to a minimum rate of tax. A minimum tax rate on all income reduces the incentive for taxpayers to engage in profit shifting and establishes a floor for tax competition amongst jurisdictions.”

The press release goes on to note that

“global action is needed to stop a harmful race to the bottom on corporate taxes, which risks shifting the burden of taxes onto less mobile bases and actually may pose a particular risk for developing countries with small economies.”

And this has been something that’s been brewing for a long time now. The way that international multinationals have been using tax competition, encouraging countries to cut their tax rates and also looking to minimise their tax bills through shifting profits into low tax jurisdictions. The OECD proposals are a huge step forward and there’s a lot more to consider.

Things are now happening very rapidly in this space. The timeline for submissions on this particular Pillar 2 proposal is Monday 2nd December. There will be a public consultation meeting the following Monday 9th December in France. And the G20 is saying it wants a solution on the whole matter delivered by the end of 2020. So, stay tuned for what is a remarkably fast changing environment.

Well, that’s it for The Week in Tax. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Please send me your feedback and tell your friends and clients. And until next time have a great week. Ka kite āno.