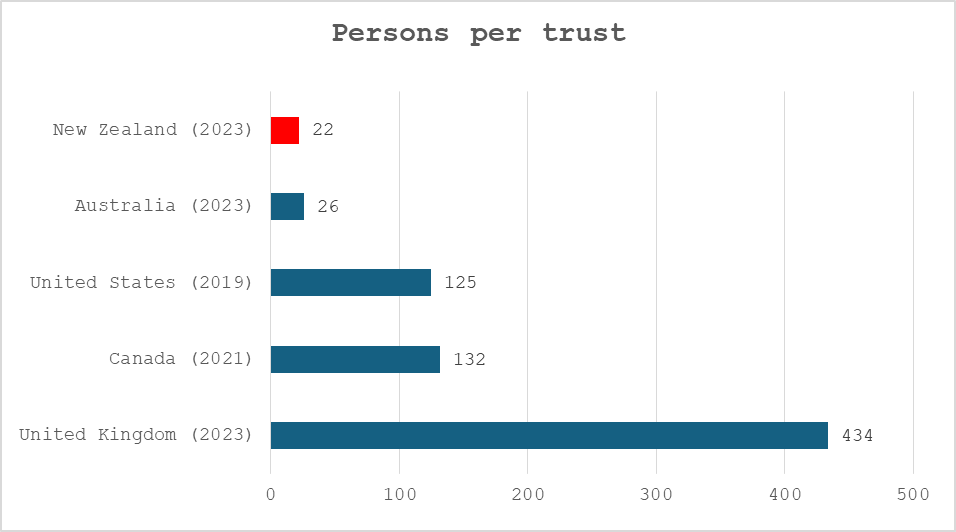

New Zealand has an extraordinarily high number of trusts relative to its population. We don’t actually have official numbers on the number of trusts in the country but estimates range as high as 600,000. Inland Revenue’s recent trust disclosures data notes that as of 31st March 2023 it had 412,000 trusts with IRD numbers. Not all of them have to file tax returns but to put it in context that number of 412,000 represents one trust for every 12 people in the country. By comparison, based on UK tax return filing statistics filed for the same period, there is one trust in the UK for every 434 people.

(Prepared by author using latest available official tax return statistics)

So, there are a significant number of trusts in New Zealand. And that means unintended consequences are lurking for the settlors, trustees and beneficiaries of these trusts. One I would consider is a well-known issue is that for Australian tax purposes, a trust is deemed resident if any trustee is tax resident in Australia. A common pre-migration planning tactic for people moving from here to Australia is to ensure that they resign any trusteeships.

Watch out for Australian resident executors

By the way, this trust residency rule also applies to executors. I’ve frequently advised clients that they need to update their wills and if they have an Australian executor, they need to remove that person or consider alternatives.

Got an Australian resident trustee? Get ready to pay Australian capital gains tax even if it is your main home.

The implications of having an Australian resident trustee are frankly messy, to put it mildly. For Australian tax purposes a trust is deemed tax resident in Australia if ANY trustee is tax resident in Australia. This potentially makes the trust subject to Australian capital gains tax with the Australian resident trustee responsible for collecting the tax on any capital gain derived by the trust.

As an Australian resident trust any capital gain will be calculated under Australian tax law. This applies regardless of the fact that we don’t have a general capital gains tax. The issue that’s emerged in several cases that I’m dealing with relates to property has been sold by a trust and the disposal was not taxable for New Zealand because either the bright-line test didn’t apply or in some cases the property was actually the main home of one of the trust beneficiaries.

Australia has an exemption from capital gains tax for the main home, but and this is a huge but, this exemption does NOT apply to main homes held in trust.

The danger scenario

The danger scenario is a typical New Zealand complying trust with an Australian resident trustee. The trust sells a New Zealand situated property and then looks to distribute the gain. Even if that gain is distributed only to New Zealand resident beneficiaries, under Australian legislation, the Australian trustee is liable for the tax on that gain. Conceptually, it seems inconceivable that the sale of a New Zealand property distributed to New Zealand residents is taxable in Australia but it’s the interpretation the Australian Tax Office has adopted because at least one trustee is an Australian tax resident.

Well, what about the double tax agreement?

What can be done about this? Well in some cases, if there are only Australian resident trustees, then to use a technical term you are frankly stuffed. But more often than not, the majority of trustees are New Zealand tax residents. In this case you might be able to apply the clauses within the double tax agreement between Australia and New Zealand (the DTA) dealing with residency.

The problem is that the current DTA following the modifications made in 2017 to adopt the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS (the MLI), doesn’t have an easy process for resolving this matter. Generally, you can apply the relevant double tax agreement to determine the place of effective management for non-individuals.

For example, a trust might have five trustees with only one in Australia and the remaining four trustees plus the settlor and this is the group which carries out the management of the trust. Accordingly, the place of effective management is in New Zealand. Australia therefore gets no taxing rights in relation to any disposals of non-Australian situated property. (Keep in mind that even if this scenario plays out, if a distribution is made to an Australian resident beneficiary who does not qualify for the Australian temporary resident exemption, the distribution is still taxable in Australia).

However, at present under the modified DTA, trustees wanting certainly will actually have to make an application to Inland Revenue through the mutual agreement process to ask them to consult with the Australian Tax Office and resolve the matter of residency.

A helpful United Kingdom court case?

Coincidentally, Howarth v HMRC [2025] EWCA Civ 822 an interesting UK Court of Appeal decision on the issue of place of effective management for a trust has just been released. The case involved a widely marketed tax avoidance scheme known as a “round the world” scheme, which was designed to avoid UK capital gains tax (CGT).

Under the scheme the trust’s Jersey based trustees held shares in a UK incorporated company. The Jersey trustees resigned in favour of a Mauritius resident trustee company who then sold the shares. Following the sale the Mauritian trustees resigned in favour of UK resident trustees. At the time the shares were sold, the trust would be deemed tax resident in Mauritius, a jurisdiction which, very conveniently, does not tax capital gains.

When the Court of Appeal considered the issue of the trust’s place of effective management it concluded the trustees in Mauritius were following a predetermined single plan set out by the UK settlors of the trust. The Mauritian trustees were “playing their parts in a script which had been written by others”. The Court of Appeal therefore upheld two lower court decisions (the equivalents of the Taxation Review Authority) that the place of effective management of the corporate trustee was in the UK.

It’s quite useful to see courts talking about the residency of trusts because double tax agreements don’t specifically refer to trusts but “non-individuals”. As a UK Court of Appeal decision, it represents a good precedent. Incidentally it’s expected if the case goes up to the UK Supreme Court, it will probably still rule the same way.

I think Haworth v HMRC could be useful for any trustees who find themselves dealing with the complications of an Australian resident trustee and they wish to ensure any Australian tax is limited only to gains actually distributed to an Australian resident.

CPA Australia calls for a capital gains tax

Still in relation to capital gains tax, as previously discussed Inland Revenue has a long-term insights briefing currently out for consultation. (Submissions are open until 1st September). The briefing discusses how we need to look at ways we could expand the base tax base to meet coming financial demands mostly around superannuation, health and in my view, climate change.

This week CPA Australia, the accountancy body which represents over 3000 accountants here in New Zealand, has called for a rethink of the tax system, including consideration of an introduction of capital gains tax (CGT). The organisation agreed with Inland Revenue; there are many pressures on the New Zealand tax system particularly around ageing demographics. CPA Australia felt the absence of a capital gains tax puts pressure on other taxes. I agree with that analysis, and I also think that’s tied to the question of productivity and diversion of our scarce capital into lower return assets, mainly residential property investment.

It’s interesting to see the CPA Australia come out in favour of a CGT. It suggests that a CGT should only apply to assets acquired after a certain date. In other words, assets held prior to the introduction of that date would be exempt. This is what Australia did when it introduced CGT, coming up 40 years ago next month.

Follow Australia? “Yeah, nah.”

Interestingly, when the last Tax Working Group considered CGT, it got advice from Australia which recommended not to follow the Australian approach and instead go for what’s sometimes known as the valuation day approach. This would base CGT on the valuation of assets on the date of introduction. CPA Australia rightly point out there are compliance problems with that approach but like so much of the stuff we encounter in the tax world, other countries have met and dealt with these issues, so they are not unique or insurmountable.

More on the abatement web

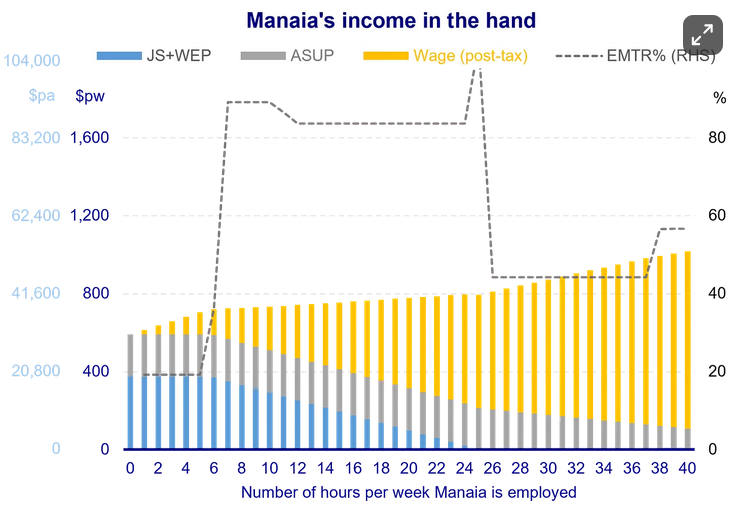

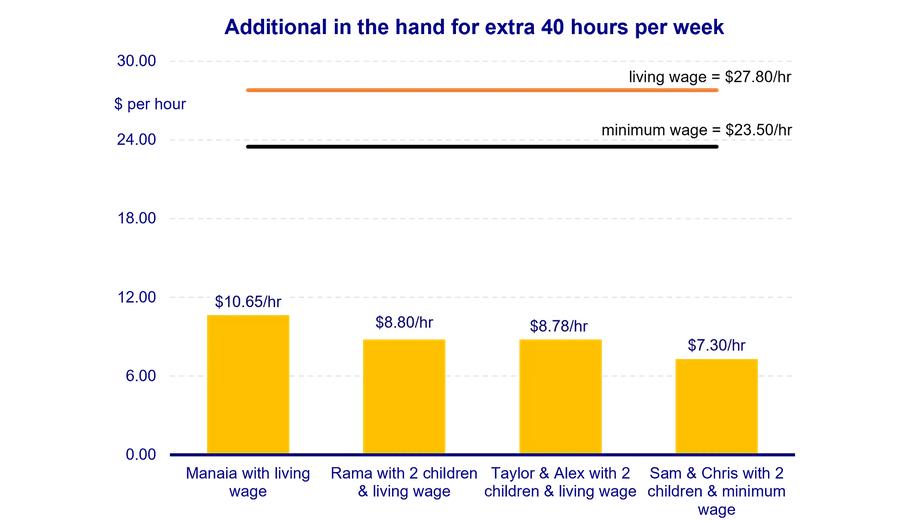

Last week I discussed a substack from Ganesh Ahirao, former head of the Productivity Commission analysing what I called The Dirty Secret of the New Zealand tax system – that very high effective marginal tax rates apply, sometimes over 70%, to people on very modest incomes.

Ganesh has written a follow up this week providing further examples illustrating how people trapped on low-income or benefits, who are trying to work their way out of the system, as they are encouraged to do so, are hit very quickly by very high marginal tax rates.

For example, Manaia is single with no children, no student loan, paying immediate rent of $415 a week for a one-bedroom flat. Manaia is eligible for Jobseeker Support alongside the Winter Energy Payment and Accommodation supplement for a total of $592 per week before tax. Six hours employment at the living wage will raise her weekly pre-tax income to $700 but above that threshold, she starts losing her Jobseeker Support at a rate of $0.70 on the dollar. Her effective marginal tax rate jumps above 80% plus.

As Ganesh details, many low-income earners seeking support even one as widespread as Working for Families face similar situations.

These graphs illustrate Ganesh’s argument which I fully endorse, is we have allowed a huge problem to develop over the last 30-40 years through constant tinkering with the benefits system and swapping universality for a more “targeted” approach. The result is a horrendously complex position which really needs cut through and reform.

I support that and make no apologies for bringing the story up. It is something we should be discussing more frequently and asking our politicians to fix. We can’t be saying to people we need you to work if you’re a beneficiary and then promptly hitting them with 80% marginal tax rates. That is unrealistic and unfair.

The meaning of ‘payment’ for GST purposes

And finally, this week, Inland Revenue has released a valuable draft interpretation statement for consultation on the meaning of payment for GST purposes. When a payment is made is crucial for determining the GST time of supply, the tax period for which you may return output tax. It’s also relevant when an input tax deduction can be claimed and particularly in relation to secondhand goods input tax deductions which are only available when a payment is made.

This draft interpretation statement (only 22 pages) will replace a couple of previous Inland Revenue guidance items, which are actually over 30 years old. The principles involved haven’t changed, but it’s still useful to see the advice consolidated in an updated interpretation statement.

The draft considers typical examples of what constitutes payment. Obviously, cash or bank transfers are payments, but what about if there is an offset or some vendor finance. For example, payment could be made by setting off against an existing debt owed by the supplier to the recipient. Accounting entries can count, but you have to have the evidence to support them, and obviously payment of a deposit represents a payment (and can trigger some GST time of supply issues in relation to the sale and purchase of a property), Overall a very useful guidance.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Rachel Reeves, the first ever female Chancellor of the Exchequer delivers a UK Autumn Budget with potentially significant implications for many Kiwis and Britons who have migrated to New Zealand.

Meanwhile Inland Revenue’s crackdown on tax evasion continues.

The UK finance minister is officially called the Chancellor of the Exchequer, a post which is more than 800 years old, and until this year it had never been held by a woman. So, when Rachel Reeves, the Labour Chancellor of the Exchequer delivered her maiden budget speech last Wednesday night, she made history as the first woman Chancellor in British history.

There was quite a lot to consider in this UK Budget, as people were watching to see how the new government would respond to the challenges it inherited. British budgets, unlike ours, coincide with the release of a Finance Bill and tax measures there’s always a lot of tax matters to consider beyond the headline measures.

The headline measures

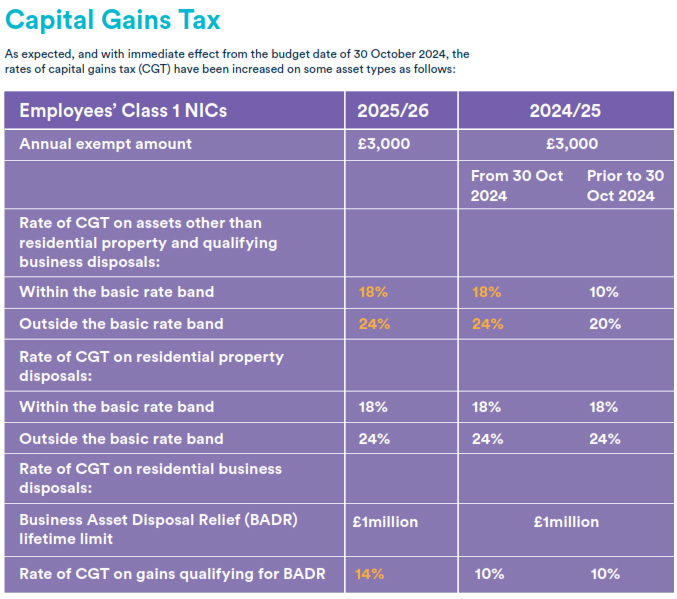

Most notably, there was an increase in Employer National Insurance Contributions (a Social Security tax) by 1.2 percentage points to 15% with immediate effect. There are also immediate tax rises for capital gains tax, but the top rate for capital gains tax still was capped at 24% for both property and non-property assets. Which as some commentators said is still lower than countries with which the UK compares itself. It’s quite interesting to see that comment about 24%, because one of the key points of our discussion around capital gains taxes here is what rate would apply? It’s therefore interesting to have an international comparison.

Beyond the headlines

It’s always interesting to dig around in other countries’ budgets and see what they do in certain areas. For example, the UK doesn’t have an imputation credit system, but there are lower rates of tax applied to dividends, even for those on the highest income. There’s also a savings allowance, which exempts certain amounts of investment income. It’s currently £1,000 for basic rate taxpayers (taxable income up to £37,700) and £500 for the higher rate taxpayers. The UK basic rate of tax is 20% and we have two rates lower than that so this savings allowance is not necessarily a measure we might want to copy here.

Twin cab utes and fringe benefits – an example to follow?

There’s apparently some uncertainty around the fringe benefit taxation treatment of twin cab utes which the Budget clarified. Where they have a payload of one tonne or more such vehicles are not there to be treated as cars for benefit in kind purposes unless they were acquired prior to 6th April 2025.

On Fringe Benefit Tax, the benefit value is calculated as a percentage of the vehicle’s list price when the car was first registered which is similar to our treatment. However, the percentage used is determined by the vehicle’s carbon dioxide emissions, or its range if it’s an electric vehicle. These percentages are set to increase steadily over the next three years as part of the range of tax increases announced. Inland Revenue is presently reviewing FBT and as is well known tax can act as a disincentive. If we want to incentivise a transition to a lower emissions economy, maybe we should be looking at how the UK applies FBT to vehicles.

UK pension tax free lump sum unchanged

There’s always lots of rumours before a Budget which I’ve seen sometimes used as a means to get people to buy new products or make tax driven decisions in fear of change. One of the rumours before this budget was that there were going to be changes to the taxation of pensions and in particular to the 25% tax free lump sum. That hasn’t happened, but remember, our rules are completely different. Just because 25% of the pension can be withdrawn tax free in the UK, that doesn’t mean the same rules apply here.

The big changes

But the main reason I was paying particular attention to this UK budget was because we finally got more detail around the two announcements made in the March Budget – the new foreign and income gains regime and the end of the non-domicile regime and the changes to inheritance tax. These are both measures which have significant impact for New Zealanders, who are either going to the UK or have returned to the UK, but also for UK expats who have migrated here.

New foreign income and gains regime

The foreign income gains (FIGS) regime is very similar to our transitional resident’s exemption in that a new tax resident’s foreign income and capital gains will be tax exempt for the first four UK tax years that they are resident in the UK. It’s not like our 48-month exemption period, it is tied to the UK tax year, which remember runs from 6th April to 5th April. (Perhaps reflecting that some of this stuff does date back 800 years or more, there’s no intention to change that tax year end).

What has also been clarified is that individuals who have previously elected to be taxed on the remittance basis, which meant their non-UK sourced income investment income was not taxable, can now be allowed to take advantage of a so-called temporary repatriation facility. This will last for three years, and they will be able to nominate and remit their non-UK income and gains from years when they were within the remittance basis and take advantage of lower tax rates. Initially 12% for the first two years ending 5th April 2026 and 2027, and then 15% for the year ended 5th April 2028.

As part of the FIGS regime there are also changes to what’s called the Overseas Workday Relief. This will allow UK tax resident employees who perform all or some of their duties outside of the UK to claim tax relief on the remuneration relating to their non-UK duties determined on “a just and reasonable basis”. This is quite a significant one for expats and for companies that have very highly paid and skilled employees and has been greeted with general enthusiasm by by those impacted.

Inheritance Tax

Potentially the biggest change though, is in relation to inheritance tax (IHT). This applies to all assets situated in the UK or all assets situated anywhere, if the person is domiciled within the UK. There’s a nil rate band of £325,000, above which 40% will apply (these rates and thresholds have been frozen until 2030). IHT has a potentially significant impact because under the present rules, someone tax resident outside the UK could still be within the IHT net because they are still deemed to be domiciled in the UK. I’ve had to deal with one or two of these instances.

There’s also a pretty nasty trap for someone like me who might have left the UK a long time ago and adopted a new domicile of choice outside the UK. At present if I ever became tax resident again in the UK, our domicile would immediately revert to the UK. Therefore, working or living for prolonged periods of time in the UK was actually potentially highly tax disadvantageous from an IHT perspective.

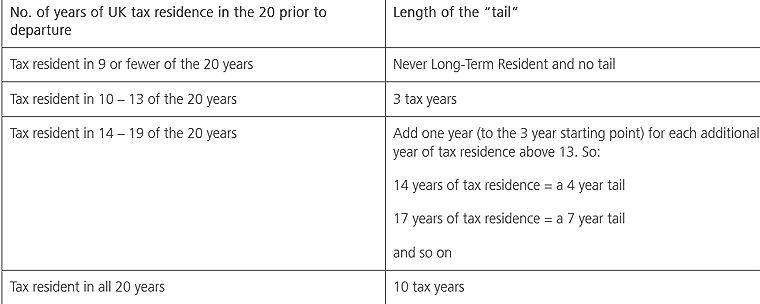

All this will be replaced now by a residence-based regime. The tests for whether non-UK assets are subject to IHT will now be whether the individual has been tax resident in the UK for at least 10 out of the last 20 tax years immediately preceding the tax year in which the chargeable event, most typically death, but can also be a lifetime transfer into a trust, happens.

There’s also a tail on how long a person is in scope if they’ve been non-resident during a period. For example, if someone had been UK tax resident for between 10 and 13 years, they remain in scope for IHT for three years post departure.

(Courtesy Burges Salmon)

Implications for New Zealand residents

What this change means for a lot of British expats resident here is they’ve got to think again about what their IHT obligations could be. By the way, our double tax agreement with the UK does not cover IHT. The UK has the right to charge IHT on assets situated in the UK, that’s not surprising. However, it potentially also has got a long reach if HM Revenue & Customs determine someone resident here is subject to IHT.

IHT and trusts

One of the other IHT changes is to the taxation of trusts used to hold assets outside the scope of IHT, so-called excluded property trusts. If I understand it right, starting from 6th April 2025, if a settlor dies and they’re within the scope of IHT, assets settled by them into what was previously an excluded property trust are now within IHT. This is a major change and I’m investigating it further given we make very extensive use of trusts. I’ve been dealing with quite a few clients who have UK connections year and it’s been really revealing to see how complex the taxation of trusts is from the UK perspective. It’s good to see some clarity around the new rules, but as I say, it’s a significant budget in many ways, and there could be quite major consequences for more people based here than they might anticipate.

Meanwhile, Inland Revenue’s crackdown continues

Moving on, Inland Revenue continues its crackdown when it announced on Thursday that it’s making unannounced visits to hundreds of businesses who it believes are not meeting all their tax obligations as employers.

According to Inland Revenue, they receive about 7000 anonymous tip offs each year. It has said “the volume of tip offs has grown over previous years indicating an increased sense of frustration by the community in general, businesses who are not doing the right thing.”

Inland Revenue’s analysis shows that the tax risks overwhelmingly relate to taking cash for personal use without reporting sales and or paying employees in cash.

Based on this Inland Revenue is making unannounced visits to over 300 employers whose practices it will closely examine. I’ve seen this happen with a few clients under investigation. Inland Revenue staff will go to a café or business and just watch to see what’s happening. They may buy something, but they will certainly sit and observe and see who uses the till, how everything is recorded and from there they will draw the relevant conclusions.

The consequences of being investigated

As an example of what happens to taxpayers who have not been compliant, the director of an asbestos removal and labour hire company has been jailed for three years in what the judge called serious offending and the worst of its kind to come before the Christchurch District Court in the last 20 years. The director, Melanie Jill Tatana, also known as Melanie Jill Smith, was jailed for three years for what was described as wilful diversion of funds.

Her company employed around 60 people, and between April 2019 and September 2022 had been required to deduct PAYE on 63 occasions but failed to pay the full amounts totalling $1.6 million. Tatana was therefore charged with 63 counts of aiding and abetting to knowingly take PAYE from workers’ wages and not pay it on to Inland Revenue. Instead, more than $800,000 had been diverted for her personal use.

One of the more encouraging things from my perspective about this case is that this offending has all been pretty recent and Inland Revenue tracked it down within a couple of years. I’ve seen cases where the offending has been four or five years.

I still think 63 occasions of nonpayment is a little generous, but bear in mind that Inland Revenue did take the the foot off the throttle around pushing hard on on companies and businesses because of COVID. That amnesty or less stringent approach is now over and it’s back to business. And Tatana won’t be the first to find out about Inland Revenue’s hardline approach.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue does not consider removal of commercial buildings depreciation “to be a fair and efficient way of raising revenue”.

New 12% online Gaming Duty still leaves $500 million gap in the Government’s tax package.

It’s been a busy week in tax, beginning on Sunday when the Associate Minister of Finance, David Seymour, announced that interest deductions for residential properties would be restored to 80% deductibility from 1st April.

There had been a proposal under the Coalition Agreement for the present 50% deductibility in in the current tax year to increase to 60% with backdated effect, but that has now been dropped. The Minister also confirmed interest on residential investment property will become fully deductible with effect from 1st April 2025, in line with the Coalition Agreement.

Interest deductibility “Yeah, Nah”

The announcement reignited a long running debate over the fairness of the measure restricting interest deductibility. The crux of the argument against it being that businesses are allowed to deduct their costs when deriving income, and the change made to restrict interest deductibility by the last government was contrary to standard business and tax practice.

But when you consider this point keep in mind that under the Income Tax Act, expenses are deductible to the extent to which they are incurred in deriving gross income or to the extent they’re incurred in the course of carrying on a business deriving accessible income.

“The extent to which” is the key phrase and the argument around non deductibility revolves around the fact that the economic return for landlords comprises of fully taxable rental income, and a capital gain which is largely tax free. But legislation generally has ignored this point of possible apportionment between what is taxable income and non-taxable capital income. This leads on to the never-ending debate as to whether we should tax capital gains. And so the argument of deductibility is just another continuation of this question.

It’s also worth noting that businesses with overseas owners are subject to the thin capitalisation regime. This also restricts interest deductions where the New Zealand company’s debt to asset ratio exceeds 60%. Now this measure also contradicts standard tax and business practice, but it’s part of many jurisdictions around the world as a means of countering the risk of excessive interest charges transfer pricing money out of the country. In other words, there are arguments for and against restricting interest deductibility.

Improving the position of renters

On Thursday, the Minister of Revenue released an Amendment Paper for the current tax bill along with five Regulatory Impact Statements two of which covered the restoration of interest deductibility and the reduction of the bright-line test period to two years. There was some interesting commentary by Treasury in both impact statements noting:

“Rental affordability is a significant issue in New Zealand. Based on Household Economic Survey data for the year ended June 2022, a quarter of renting households were spending over 40% of their disposable income on rent housing, and rents have risen faster than mortgage payments. Renters also have higher rates of reporting housing issues like dampness, mould and heating.”

Treasury, Inland Revenue and the Ministry of Housing and Urban Development all agreed that restoring interest deductibility should have a long-term effect of putting downward pressure on rents, but ‘should’ is doing a lot of work in this space. Other measures are going to be needed to improve rental affordability.

But restoring interest deductibility has the benefits of simplifying matters. Restricting deductibility was an imperfect measure, with a great deal of complexity and arguably went too far in the other direction of apportioning expenses relating to the split between taxable and non-taxable income.

Trustee tax rate increase to 39% confirmed subject to $10,000 exemption

The announcement on interest deductibility was followed on Monday by the Finance and Expenditure Committee (the FEC) reporting back on the Taxation (Annual Rates for 2023-24, Multinational Tax and Remedial Matters) Bill. There’s a great deal of interest around this Bill as it included the proposed increase in the trustee tax rate to 39%.

As had been hinted by Finance Minister Nicola Willis a couple of weeks back, there is going to be a de-minimis introduced for trusts with trustee income (undistributed income) of $10,000 or less. Such trusts will continue to have the 33% trustee rate apply to trustee income. However, for all trusts where the trustee income exceeds $10,000, a flat rate of 39% will apply. Therefore, if there’s $10,000 of trustee income the 33% rate applies but if it’s $10,001 the new 39% rate will apply on everything. It’s not the first $10,000 is taxed at 33% and the excess at 39%. It’s an all or nothing.

The FEC justified introducing the de-minimis exemption on the basis that the information it had received was that the compliance costs for many trusts were in the region of between $750 and $1,000 per annum. Therefore, the potential $600 benefit of a $10,000 threshold would be swallowed up by compliance costs, which is a fair point. But the reaction among my colleagues and myself is that the $10,000 threshold, although welcome is too low because, by the FEC’s own logic, something closer to $25,000 could easily have been justified.

It’s worth noting that the compliance costs for trusts have increased substantially in the last couple of years. Firstly, following the Trusts Act 2019 coming into force. And then secondly, Inland Revenue’s greater disclosure requirement for the March 2022 year onwards. By the way, we have seen nothing about those greater disclosure requirements being dialled back by Inland Revenue now there is the 39% tax rate in place. Back in 2021 part of the argument for not increasing the trustee rate to 39% at the same time as the individual tax rate went to 39% was to allow Inland Revenue to gather data on whether there was substantial amount of potential income sheltering through trusts. That theory seems to have been ditched for the moment.

Energy Consumer and deceased estates remain at 33%

Separately the FEC confirmed that the trustee rate for energy consumer trusts would remain at 33%. It also made changes to the treatment of deceased estates following submissions. A flat rate of 33%, will apply to all deceased estates rather than the deceased persons personal tax rate as originally proposed. More importantly, the trustee rate of 33% will now apply for the year of the person’s death and three subsequent income years. That was in the in the wake of many submissions pointing out that deceased estates typically don’t get wound up inside 12 months. These changes are welcome.

The Bill also covered off a number of amendments to other key topics, including the introduction of the global anti base erosion rules, the taxation of backdated lump sum payments for ACC and social welfare, rollover relief in respect of bright-line property disposals and relief under the bright-line tests for people affected by the Nelson floods.

Those global anti avoidance rules will take effect in two parts, the so-called income inclusion rule with effect from 1st January 2025 and then the ‘domestic income inclusion rule from 1st January 2026. This is a little later than the rest of the OECD and the intention is to give the affected multinational enterprise entities (those with consolidated revenue above €750 million per annum) time to get ready.

Inland Revenue recommended against removing building depreciation

On Thursday the Minister of Revenue published an Amendment Paper containing details of the proposals regarding the restoration of interest deductibility for residential investment properties, replacing the current five and ten year bright-line tests with a two year bright-line test period, removing the ability to depreciate commercial buildings and introducing a new Casino Gaming Duty. The Amendment Paper was accompanied by a detailed commentary . and, as I mentioned earlier, the relevant Regulatory Impact Statements. Now as usual, these Regulatory Impact Statements (RIS) contain some interesting reading.

The ability to depreciate commercial buildings is being removed in order to help pay for the Coalition Government’s tax package. However, in the relevant RIS Inland Revenue recommended recommends retaining the status quo and that “the Government reconsider introducing commercial and industrial building depreciation when fiscal conditions allow.”

Citing its last Long-Term Insights Briefing Inland Revenue noted that in paragraphs 19 and 20 of the RIS, that under some assumptions made by the OECD:

“…New Zealand was likely to have had the highest hurdle rate of return for investment in and industrial buildings for the 38 countries in the OECD. This was when New Zealand allowed 2% depreciation on these buildings. Denying depreciation deductions will drive up these hurdle rates of returns even higher and make New Zealand a less attractive location for investment.

This tax distortion does not only impact building owners. To the extent the additional cost is passed on and there is less investment, it also impacts any business that needs to use a building and the customers of such a business. It thereby negatively impacts productivity more generally.”

Inland Revenue conclude in paragraph 32 of the RIS:

“We do not consider the removal of building depreciation to be a fair and efficient way of raising revenue. We are particularly concerned about the efficiency impacts which will make New Zealand even more of an outlier in pushing up cost of capital for commercial and industrial buildings. We therefore recommend retention of the status quo. We note this RIS is not evaluating the merits of the Government’s tax package as a whole.”

So, why is the Coalition Government withdrawing building depreciation? Because doing so is worth $2.31 billion over four years which was understood before the election. Even so it’s fairly interesting and unusual to see such a blunt assessment.

A new Gaming Duty

National’s Election policy included a new online gaming duty which was expected to raise something like $700 million over a four-year period. I was one of the those who was a bit sceptical about the revenue forecast. And it transpires that the numbers were indeed a bit optimistic.

What is now being proposed is a new 12% gaming duty for online offshore casino websites and this is in addition to GST, which is already payable when gambling on offshore sites. This new duty would be in line with how some other countries tax offshore casino websites. It’s estimated to collect $35 million of additional tax revenue in the forthcoming year ended 30th June 2025 and expected to grow by 5% each subsequent year. This still leaves a gap of about $500 million over four-years in the original revenue forecasts.

The Budget in May is becoming more and more interesting for finding out how the Government will follow through on its commitment to increase personal income tax thresholds. Even though they won’t compensate for the effect of inflation since 2010 those threshold adjustments come at a substantial cost. I could see that further cost reductions may be imposed further down the track. Those are political matters which we’ll have to wait and see how they work out.

Foreshadowing a capital gains tax?

Some commentary in the bright-line RIS raised the prospect of a capital gains tax. Treasury, for example, proposed a 20-year bright-line test or longer as it

“…would capture more capital gains, thereby improving the fairness of the tax system and supporting more sustainable house prices.”

Inland Revenue meantime felt the 10-year bright-line test was not an efficient way of taxing capital income before adding “If the government wanted to tax the income, it would be preferable to have a tax on these gains, irrespective of when the assets were sold.” It’s interesting to see Treasury and Inland Revenue raising the bogeyman of a capital gains tax to address funding and fairness issues within the tax system.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

“As-salamu alaykum. Peace be upon you and peace be upon all of us.”

More on UK trust filings, and why are there so many trusts in New Zealand?

Financing local government, time for change?

I’ll be honest, even after 30 years in New Zealand, I miss British budgets. There’s a building sense of anticipation beforehand, as rumours circulate about bold tax plans and the abolition/introduction of new measures. Then on the day itself, we have to deal with the myriad of tax measures introduced, usually always without any warning beforehand, other than leaks to selected media. Being perfectly cynical, they are handy work-creation events, much more so than their New Zealand counterparts. (That said this year’s May Budget here is looking like it will be the exception, which proves the rule).

This year’s UK Spring Budget, which was released on Wednesday night, did not disappoint. There were a whole raft of measures, some of which, to borrow the phrase the 1974 Lions adopted in South Africa against the Springboks involved “Getting your retaliation in first”. These measures were done simply to hamper what’s expected to be the next Labour government after Britain has its General Election sometime this year.

Ending the Remittance Basis of taxation

So, there’s a lot to consider, but there were two that are of particular interest to New Zealanders, and these are to do with the so-called non-dom rules. The UK has a special set of rules called The Remittance Basis of Taxation for non-domiciled persons. That is people, generally speaking, born outside the UK, and they are able to basically exempt their non-UK sourced income from UK taxation, if they don’t remit it to the UK.

These rules have been around for a long time and there has been a lot of amendments in recent years. And I suspect there is a fair bit of non-compliance going on from people here in New Zealand, who’ve not kept up with those changes.

The UK Labour Party had indicated it would remove the regime as a fundraising measure. Instead, the Conservative Chancellor of the Exchequer, (Finance Minister), Jeremy Hunt, has gone ahead and decided to pre-empt that by abolishing the regime with effect from 6th April 2025. It will be replaced by a regime which looks very similar to the transitional residence exemption we have here. That is, individuals will not pay UK tax on foreign income and capital gains for the first four years of UK tax residence.

There will be some transitional rules which will apply to existing individuals who are claiming the remittance basis. You can claim remittance basis for up to 15 years, but after a period of ten years you have to start paying a Remittance Basis Charge of £50,000. And then after 15 years of tax residency in the UK, you’re deemed to be domiciled in the UK and the exemption no longer applies. It’s long been a very controversial measure. The wife of the present Prime Minister, Rishi Sunak, is apparently a non-dom and questions have always been asked about whether she made use of that exemption as she comes from an incredibly wealthy family.

I’ve got a number of clients moving across to the UK, or who are all already there, and we’re looking at the question of how to manage the implications of becoming UK tax residents. So, this proposal is interesting to see. More details will emerge, obviously over time, but it is significant in that it will perhaps make it a little easier for people to migrate to the UK without triggering huge tax liabilities or having to manage them extremely carefully under the remittance basis regime.

Domicile and Inheritance Tax – good news for Kiwis & UK migrants?

Related to the end of the remittance basis regime and arguably even more important, are changes to the UK’s Inheritance Tax (IHT) regime. IHT is a unified estate and gift duties, and probably should be still what it was originally called Capital Transfer Tax. At present, IHT applies to all assets situated in the UK or all assets worldwide if the person is domiciled in the UK.

The proposal is that those current rules will also be replaced from 6th April 2025 with a residency-based set of rules which will probably involve a ten-year exemption period for new arrivals and then a ten-year tail provision for those who leave the UK and become non-resident. What that tail provision may mean is that someone who’s been resident or domiciled meets the test for IHT, may have to be non-resident for ten years to escape the full effect of it.

Now, in my experience, the impact of IHT on Kiwis who’ve been over in the UK or have assets in the UK, and then Brits like myself, who’ve migrated here, is not very well understood. But as the Baby Boomer and older generations are starting to pass away now, there’s a great transfer of wealth going on. The amount of IHT that the UK government is collecting is steadily rising. It’s now up to over £7 billion a year (0.3% of GDP, about $1.2 billion in New Zealand terms), steadily heading towards 0.5% of GDP. So, it’s starting to become a more significant part of the tax take.

These new rules may mean that people who have previously been caught in the regime will be out of it, but it may also mean that people who thought they were outside the regime may be caught. There’s no indication here that the rates that apply – 40% on estates worth more than £325,000 pounds or $650,000 thereabouts – have been changed. It’s a tax that people feel needs reform in that there is plenty of scope for mitigating it. It falls very heavily on relatively smaller states rather than the larger estates where they have the wealth to do some more estate planning.

More tax breaks for the film industry – a lesson for the Government?

And incidentally, just before moving on, I notice this budget also contains a number of measures to promote the UK film industry and theatre as well as the arts. These will provide over £1 billion in additional tax relief over the next five years. One of the things that’s common amongst tax systems around the world is support for the film industry, and the film industry as a whole is pretty cynical about going to where the best incentives are.

I think it’d be interesting to see just how the Coalition Government responds in the May budget about pressures mounting on the Screen Production Rebate, whether that’s going to continue in its present form. The industry here will be lobbying for it to continue because although we can’t compete with more generous exemptions that may be provided elsewhere, the rebate still provides the skills that have been built up here thanks to the likes of Weta Workshop and others which makes New Zealand skills still highly sought after. The Screen Production Rebate is the little kicker which helps get the deals across the line.

More on UK trust statistics and a warning about the perils of overseas trustees

Larger estates in the UK will undertake a fair amount of mitigation to minimise the impact of Inheritance Tax, and that invariably tends to involve the use of offshore trusts. I mentioned in last week’s podcast the extraordinary fact that in absolute terms more tax returns are filed in New Zealand for trusts than in the UK.

This provoked a lively debate in the comments section with some pointing out the UK numbers don’t really reflect trusts that have been set up to go offshore into tax havens such as the Caymans and the Isle of Man. Well yes, that’s right, the UK numbers don’t reflect this because trusts’ tax returns, for UK purposes are generally required to file tax returns based on the residency of the trustees.

That by the way, is a matter people here need to pay more attention to. If a beneficiary or trustee migrates to the UK, this may inadvertently make a New Zealand trust with New Zealand assets subject to UK taxation. Again, this is another matter which isn’t well understood, and I suspect there’s a fair bit of noncompliance going on.

The UK also has a Trusts Registration Service. This was in response to the EU’s Fifth Anti-Money Laundering Directive from 2017, which the UK went ahead and implemented despite Brexit. The UK actually went in for a tighter regime than the EU had proposed. According to the same statistics that the HMRC held about trust tax return filings in the UK, the Trust Registration Service had 633,000 trusts and estates registered as of 31st March 2023 and which remain open as of 31st August 2023. This includes 462,000 new registrations in the 12-months to 31st March.

This surge in registrations is the result of a compliance effort by HMRC to remind people around the world that if any trust has a property in the UK, or even has made loans to beneficiaries in the UK, it may have a UK tax liability, and therefore should register under the Tax Trust Registration Service. This is regardless of where the trustees are tax resident. And again, I suspect there is a fair bit of non-compliance here.

Why are there so many trusts in New Zealand?

But even if you take these greater numbers, we’re still left with the rather astonishing fact that per capita large number of trusts in New Zealand relative to the population. How did that evolve was one of the questions asked in the comments. The short answer would be that the effective abolition of Estate Duty in late 1992 removed the impediments to setting up trusts. What we saw in response was something quite unusual in trust law, where it was now quite possible for a single person to be the settlor (or the person who settles property on the trust), a trustee responsible for managing the property, and a beneficiary. This is very unusual in trust law terms around the world.

I think it has to be said that some lawyers and other practitioners took advantage of that opportunity to market themselves and trusts extremely well. Back in the early 1990s, by putting assets in trusts it was possible to mitigate against the impact of rest home charges. The income of trusts was not then taken into account when determining eligibility for the likes of Working for Families or student allowances.

All that has changed over time and my view is that a substantial number of the estimated 500,000 trusts that we have in New Zealand are no longer necessary. That’s also the view of many other practitioners in this space. So it will be interesting to see what happens over time as people realise the complexities of using trusts and the inadvertent tax issues that are created when trustees, beneficiaries or settlors move to another jurisdiction.

Since the start of the year, I’ve seen an upsurge in requests for advice in relation to trustees, beneficiaries or settlers moving to the UK or making distributions to the UK.

I don’t expect that to slow down, and I think it’s actually the tip of the iceberg.

Beware the information exchanges

I would also add that probably because of the common reporting standards and the automatic exchange of information as various tax authorities work their way through all that information that’s being accumulated and distributed around the world, they will be realising that they many trusts are non-compliant, accidentally or not, and they’ll be starting to crack down on it.

Local government finances, time for reform?

Finally this week, local governments are now looking to set their rates for the forthcoming 2024-25 year. The fact that no replacement for Three Waters has been found and the substantial infrastructure deficit we as a country have allowed to develop, means that rates are likely to be rising quite significantly for many of us. That’s obviously going to generate some pushback.

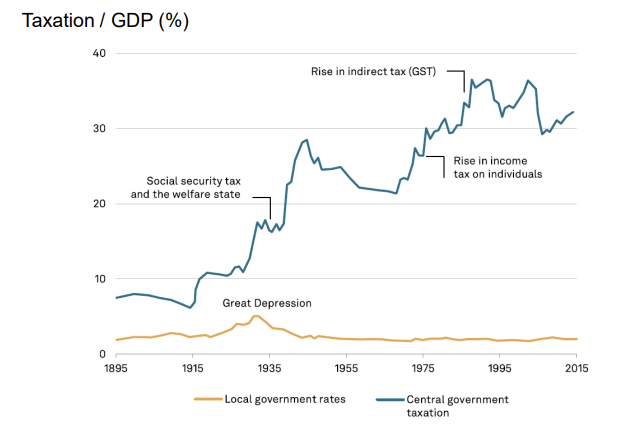

Writing on this topic Dan Brunskill noted the quite astonishing stat that local government rates have basically not increased as a percentage of the economy in the past hundred years.

Basically, local rates have stuck around about 2% of GDP overall across the country about $8 billion in rates are paid. (Not all that you pay to a Council is actually rates based on property values, there’s also the Uniform Annual General Charge together with the various services such as consent fees that councils charge).

As the graph illustrates, apart from the spike around the Great Depression period, when councils and central governments all did more to try and help alleviate the impact of that, rates as a percentage of GDP have been stable for well-nigh 90 years. I think the present rating present funding of councils is unsustainable, because, as the article notes, central governments keep giving local governments more and more to do, but restrict them in the level of income that they can raise. That’s both good and bad. We don’t want what happened with Kaipara District Council, which essentially went bankrupt because it could not fund a wastewater system in Mangawhai.

There’s scope for reform in this space. I think the crunch points around finance are arriving now and local and central government will need to think harder about how local government can be funded and what funding mechanisms are appropriate. For small councils such as Kaipara or, Waiora over near Tairawhiti East Coast, the funding issues and scope for raising funds are not the same as for Auckland a council with a rating base of over a trillion dollars. The laws need to change in my view, but we’ll have to wait and see developments.

As always, we will bring those to you when they happen. And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

What connects Pillar One and Pillar Two with the collapse of Newshub?

New draft Inland Revenue guidance on employee share schemes.

Today (Monday) I was (virtually) at the Accountants and Tax Agents Institute of New Zealand (ATAINZ) annual conference which, like last week’s International Fiscal Association, (IFA) Conference, was opened by the Minister of Revenue, the Honourable Simon Watts. The Minister repeated much of what he had said to the IFA conference about supporting the Generic Tax Policy Process, his wish for simplification in the tax system and improving compliance being a main driver. As the focus at the IFA conference is very much on tax policy his comments were very welcome.

By contrast, at the ATAINZ conference, the focus is slightly different because the audience there was comprised of tax agents, and we’re more focused on operational matters. So, when it came to Question Time, there were quite a number of questions around operational aspects of Inland Revenue. One of the first questions that was asked was what was going to happen with the trustee tax rate, which you may recall is proposed to rise to 39% under a bill presently before the Finance and Expenditure Committee.

Now we’re expecting to hear back from that fairly soon, but during the week the Minister of Finance, Nicola Willis, hinted that some form of carve-out might be happening, in that the 39% trustee tax rate might not apply to all trusts. So naturally, some questions were directed at the Minister seeking clarification on this point.

He wasn’t able to give more guidance, simply saying that we will have to wait until the Finance and Expenditure Committee reports back, which is expected next week. The Minister got told it is a rather frustrating scenario because we’ve got the run up to the end of the tax year on 31st March, and we will be wanting to plan payments for dividends and other distributions in before then. Unfortunately, the issue remains a bit of a grey area for the moment.

More trusts file tax returns in New Zealand than in the United Kingdom

There’s a couple of statistics that highlight the scale of this issue.According to Inland Revenue for the 2022 income year (typically the year ended 31st March 2022), the number of trusts and estates which filed a tax return totalled 237,226. That’s actually a decrease of more than 19,000 from the prior year.

It so happens that I came across statistics from the UK’s HM Revenue and Customs about the number of trust tax returns that are filed there. And according to the equivalent tax year to 5th April 2022, HMRC received 141,500 returns.

Just pause and think about that. In absolute terms, more trust and estate tax returns are filed in New Zealand than in the UK, despite the UK, with its population of some 67,000,000 being almost 13 times greater than here. So actually, on a per capita basis, it would point to the fact, for every trust tax return that’s filed in the UK, there would appear to be close to 21 filed here. The tax rate for trusts is therefore a big issue in relative and absolute terms and that’s why the tax community and trust community are really keen to get this matter resolved as quickly as possible.

What evidence is available points to the fact that for most trusts – once you include the associated families and beneficiaries that are in there – their income would not exceed $180,000, the threshold at which the 39% top tax rate kicks in. But there is a small and significant group, about 11% according to Inland Revenue, that do receive a very large amount of income. So that’s something we’d like to see resolved soon and hope it’s in time for us to get clients advised and ready for the new tax year changes.

Interestingly, on the other comments the minister made to both the IFA and the ATAINZ conferences about Inland Revenues regulatory stewardship review of fringe Benefit Tax which it did in 2022, it’s clear that there is likely to be a focus on this issue from Inland Revenue on greater audit activity. This is something promoted under the Coalition agreement. What extra resources Inland Revenue is going to have and the full direction that it’s going to take going forward are probably only going to become clearer after the Budget on 30th May. Which, as the Minister pointed out, was not that far off in reality.

How the end of Newshub and the OCED international tax deal are connected

The news that Newshub’s operations will end with effect from 30th June was a big shock to the media community. As someone who has occasionally appeared on various Newshub programmes, my sympathies go out to all those affected. And I do hope that some means is found to keep the operation going, although it has to be said, it’s very doubtful at this point. I’ve always found in all my dealings with journalists of whichever organisation, they have always been incredibly professional, and I’ve appreciated that. And so, as I said, this is not a great day for journalism, and has also been pointed out, it’s not actually a great day for democracy as a whole.

Now one of the many excellent sessions at last week’s IFA Conference was an American perspective on Pillar One digital services tax and Pillar Two, the proposed international tax agreements, which have been under negotiation for some time. The taxation of the tech giants such as Facebook and Google is a key part of Pillar One and Pillar Two, and that’s the connection with the collapse of Newshub.

Newshub is no longer financially viable according to its owners, Warner Brothers, because of collapsing advertising revenues. A couple of days after the Newshub announcement, its competitor TVNZ reported an operating loss of $4.6 million for the six months to 31st December 2023. TVNZ noted that its advertising revenue fell from $171.3 million in the six months to December 2022 to $146.8 million in the six months to December 2023, against a background of rising costs.

So where is that advertising going? Well, most of it is going offshore. From what we can pick out from the financial statements of Google and Facebook New Zealand for the year ended 31 December 2022, it would appear that close to $1.1 billion during those years was paid to offshore affiliates in so-called service fees. Now that’s a substantial amount of money, and those transactions are entirely legitimate under the present tax rules. But it has to be said, even if 10% of that $1.1 billion were to stay in New Zealand, it would be a significant boost to the industry. And arguably the difference between Newshub’s operations continuing and being closed.

The offshore advertising and the service fees and the whole issue around the taxation of tech companies, point to the pressure building on the tech companies because New Zealand is not alone on this. Over in Australia Meta, the owner of Facebook, has said it’s no longer going to go through with the deal to pay news companies who were providing content on its websites.

The presentation at the IFA Conference kept coming back to a key point that I’ve always believed, which is tax is inherently political. The French were one of the first drivers of change in this space but obviously the American companies, which would be the most affected, pushed back by putting pressure on the American government to respond. And so even though the Generic Tax Policy Process tries to depoliticise tax policy as much as possible, ultimately governments are elected with certain political objectives, and those will often trump best tax policy, and that’s just a fact of life.

A digital services tax to help media?

The whole question of the impact on democracy and journalism of Newshub’s closure is beyond this podcast. But the pressure will now mount on the Coalition Government to consider what steps it can do to help the media. On the other hand, the Public Interest Journalism Fund was highly controversial.

Does that mean that there may need to be a change in tax policy to perhaps try and claw back some of the revenues going offshore through, for example, a digital services tax which is controversial and hated by the tech companies? Does the Government press hard for a resolution to Pillar One and Pillar Two? Or does Newshub just get shut down and we have to live with the consequences of that? Whatever, pressure will be building for the Government to take some form of action. Watch this space to see whether any such action results in amended tax policy.

Inland Revenue consultation on employee share schemes

Moving on to more routine matters, Inland Revenue has released several draft consultations on employee share schemes. The taxation of employee share schemes underwent major reforms in 2018. Subsequently, there’s been a number of questions to Inland Revenue about how the law applies in certain scenarios and how it interacts with other regimes such as PAYE and FBT.

Inland Revenue has therefore released six items – five draft interpretation statements and one draft Questions We’ve Been Asked, each focusing on a specific aspect of employee share schemes. This has been done rather than producing one single interpretation statement, so that people can more easily focus on the topic of particular interest to them. Alongside this, Inland Revenue has produced a four-page reading guide briefly summarising what each interpretation statement/QWBA addresses.

This is slightly unusual but it’s an indication of the complexity involved. Employee share schemes are used by a lot of companies and particularly small growth companies in the growth phase where they don’t have cash but want to attract and keep key employees as they expand until the ultimate goal, whether it’s ultimately a share market listing or perhaps a sale to a larger company.

The first interpretation statement is one of the more important ones, as it considers what represents an employee share scheme. The critical issue is when does the share scheme taxing date arise? That’s often a critical issue because one of the things about share schemes which causes difficulties is if there’s a mismatch between when the tax is due, but when cash might be available for the person who’s being taxed to actually pay the tax due. In fact, another of the drafts looks at the questions about an employer’s PAYE, student loan and KiwiSaver obligations where an employer wants to fund the tax cost on an ESS benefit provided in shares.

Another important draft reviews what happens with the ACC, PAYE and KiwiSaver obligations, when the employee share scheme benefit is paid in cash rather than shares. The draft concludes cash-settled ESS benefit is an “extra pay” under the general definition of extra pay and therefore a PAYE income payment, regardless of whether an employer elects to withhold PAYE in respect of the benefit.

Of the other draft consultation items, topics covered include what deductions are allowable for employers in respect of employee share schemes, and what is the treatment of dividends that are paid on shares held by a trustee for an employee share scheme.

Overall, this is very useful guidance and I do like Inland Revenue’s approach of issuing separate interpretation statements rather than consolidating all the items in a single item which would be close to 150 pages. Consultation is open until 26th April.

Thanks Chris

And finally, this week, Chris Cunniffe, CEO of Tax Management New Zealand (TMNZ) for 12 years, has just stepped down from his role. He made a brief presentation at the ATAINZ conference, explaining it coincided with the 44th anniversary of the start of his tax career at Inland Revenue. We’ve worked with Chris and his team at TMNZ for many years, helping our clients save tens of thousands of dollars. Chris has also been a past guest on the podcast. We wish him all the very best for the future.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.