Inland Revenue guidance on the new 39% trustee rate

Briefing the Minister

Tax credits or threshold adjustments?

The Finance Minister signed off 2023 rather like a Shortland Street season finale, leaving us all guessing as to the exact extent of the proposed tax cut package and when it might apply. We were told at the Half Year Economic Fiscal Update Mini-Budget on 20th December we could expect more details shortly. But now it’s February and we’re no wiser. It now appears likely we’ll have to wait until the Budget in May for full details.

A 39% trustee tax rate?

On the other hand, the business of government carries on and we will know early next month whether the coalition government will proceed with increasing the trustee tax rate to 39%. That’s when the Finance and Expenditure Committee reports back on the Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill. This is the annual tax bill currently before Parliament which proposed the increase to 39%. It must be passed by 31st March.

The FEC heard oral submissions last week, and I note that (previous podcast guest) John Cantin thinks it’s most likely that the tax rate will go ahead. This is even though such evidence as we’ve seen suggests that a 39% tax rate for trusts probably represents over taxation of many trusts once the wider family context is considered.

I tend to agree with John that the rate increase will go ahead, in part because it is a base protection measure as it aligns the trustee rate with the top individual tax rate. But also, the Government will probably be grateful for some additional revenue to counterbalance the lost revenue from the proposed tax threshold adjustments. That said, I know a number of submissions proposed that some sort of de minimis threshold is introduced, and the rate of 39% will only apply on the excess.

Inland Revenue’s view on tax planning for the new 39% rate

Meantime, and rather helpfully, Inland Revenue released last Friday some high-level guidance about how it might perceive taxpayer transactions and structural changes ahead of a rate change. General Article GA 24/01 proposed increase in the trustee tax rate to 39% has been released in response to requests since the rate was proposed for guidance on how Inland Revenue might perceive some transactions.

GA 24/01 contains several examples of possible transactions and how Inland Revenue would view the transaction. The first example is a company owned by a trust which changes its dividend paying policy. Inland Revenue considers a company is entitled to change its dividend paying policy and while taking into account the funding needs of shareholders and applicable tax rates, it “is unlikely without more (such as artificial or contrived features) to be tax avoidance.”

The example then notes Inland Revenue might have concerns if the company could pay a dividend by crediting shareholder current accounts, but “objectively has no real ability to pay those credit balances if it was to be liquidated.” In other words, the company tries to pay a dividend ahead of the trustee rate increase but doesn’t have the funds to pay the dividends in cash in full.

Another example is of a trustee choosing to wind up a trust. Again, GA 24/01 suggests such a step is “unlikely without more (such as artificial or contrived features) to be tax avoidance.” GA 24/01 also looks at the question of trustees investing in Portfolio Investment Entities instead of other available investment options. The advantage here is that the maximum rate applicable to Portfolio Investment Entities is 28% Again, Inland Revenue concludes such a step is unlikely without artificial or contrived features to be tax avoidance.

That said, Inland Revenue is going to continue to gather information on trusts and something it has said would be of concern to it is where income is allocated to a beneficiary taxed at a lower rate, and then instead of actually being paid out or being fully available to the beneficiary, is resettled back on the trust. In effect, the beneficiary has not benefited from the distribution.

The allocation of income to a beneficiary, where the beneficiary actually doesn’t know of an allocation or has no expectation of receiving the income together with replacing dividend income with loans “in an artificial manner”, are other alternatives which would concern Inland Revenue if there’s no real commercial reality behind the arrangement. And then artificially altering the timing, ie: bringing forward or deferring any taxable deductible payment, particularly it’s linked to existing contractual terms or practise for the date of payment.

These are just a number of scenarios which might play out. And clearly Inland Revenue’s watching. As I said, we really won’t know what the state of play will be until early next month when the FEC reports back, and when it does, we’ll let you know. But as I said, the expectation I have is we should see that tax rate increase.

The Tax Principles Act may be gone but its first draft report lives on

Moving on, one of the first things the coalition government did was repeal the controversial Tax Principles Act. Nevertheless, the draft report that was due to be produced under the Tax Principles Act has been proactively released and it makes for some interesting reading.

The report gives a background as to why it’s being prepared, its reporting obligations, and it explains what are the tax principles that were measured. These were included in the Act – efficiency, horizontal equity, vertical equity, revenue integrity, compliance and administration costs, flexibility and adaptability and certainty and predictability. Incidentally, a lack of certainty and predictability was one of the objections that was made about the Tax Principles Act because didn’t go through the full generic tax policy process.

Inland Revenue was required to assess the principles, against four measurements:

Income distribution and income tax paid;

Distribution of exemptions from tax and of lower rates of taxation;

Perceptions of integrity of the tax system, and

Compliance with the law by taxpayers.

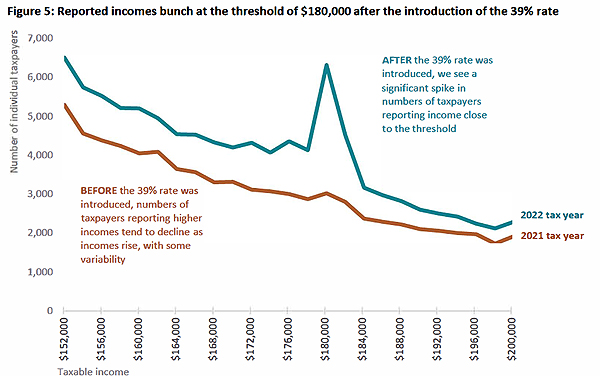

The report has lots of interesting graphs including the taxable income distribution for individuals for the 2022 tax year which shows a wee spike around the $180,000 mark.

I think that’s rather revealing even if there are apparently only 4,000 individuals involved. But still for those taxpayers you may need to have a good explanation of what’s going on.

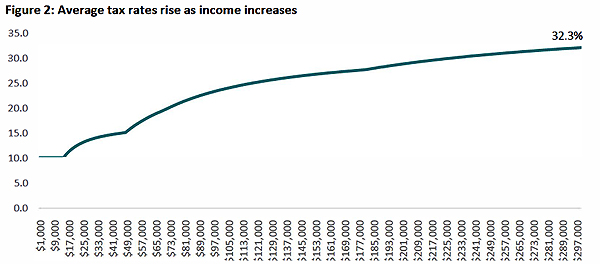

There’s a graph showing how average tax rates rise as income rises. This graph tops out at $300,000, by which point the average tax rate has risen to 32.3% for someone of that income.

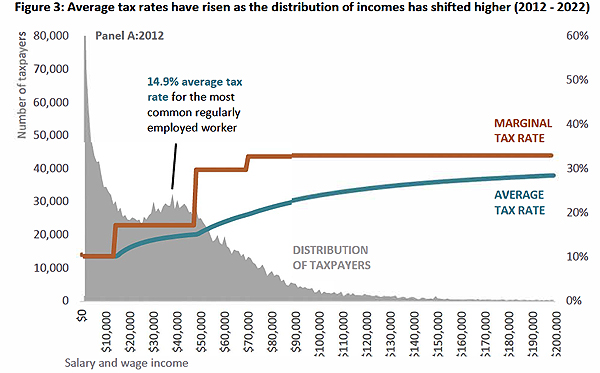

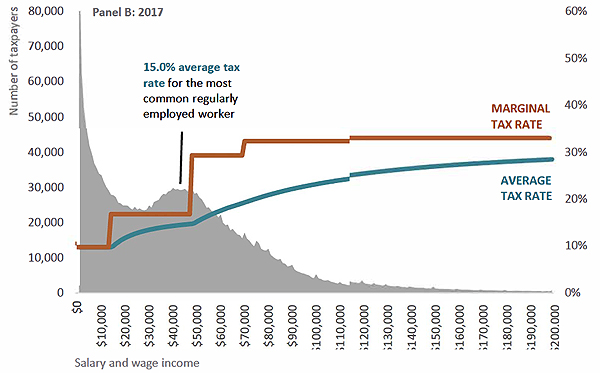

But what I thought was quite interesting were the graphs looking at the average tax rates from 2012 to 2022. In particular the graphs illustrated the effect of inflation combined with the non-adjustment of thresholds. That’s an issue I’ve talked about frequently and threshold adjustments we think will be at the core of the Government’s proposed tax relief package expected to be rolled out later this year.

The report notes between 2012 and 2017, the average tax rate for the most common regularly employed worker increased by 0.1 percentage points. Not too bad. But from 2017 to 2022 it increased by 1.2 percentage points. That’s quite a more significant example. Overall, in the period between 2012 and 2017 it rises from 14.9% to 15% and then rose between 2017 and 2022 to 16.2%.

This is the fiscal drag (or bracket creep) I discussed with Susan Edmunds of Stuff. It’s been an issue for quite some time. As wages rise faster, they drag persons on average incomes into a higher tax bracket. It will be interesting to see how the Government addresses it, and I’ll talk about that in a few minutes.

There’s plenty of other material to consider. There’s an interesting stat that the top decile of taxable income earners paid 44% of personal income tax. The report notes that the same group earned 33% of total income and suggests this is a better indicator of progressivity in the tax system than the fact that 44% of tax is paid by the top decile.

The arguments will rage around the progressivity and fairness, David Seymour of the Act Party for one has been talking about this area. Overall, there’s a lot to consider in the report. Interestingly, in the note to Cabinet regarding the repeal of the Tax Principles Act, the new Minister of Revenue Simon Watts suggested that much of this data could be made separately available, perhaps as part of Inland Revenue’s annual report. I hope we do see that, because for some time I’ve felt that the discussion around bracket creep, fiscal drag and thresholds has been sort of sidelined because governments have been not too keen to discuss it in great detail.

Briefing the Minister

Mentioning the new Minister of Revenue Simon Watts, another report released last Friday was the Briefing to the Incoming Minister. I think some of the data that’s been included in this draft report under the Tax Principles Act, would normally go into the Briefing for Incoming Minister.

What I found interesting in the Briefing was Inland Revenue’s discussion around where it’s at and the effect of the completion of the Business Transformation Programme which has allowed it to “deliver significant cost savings”. For example, the Briefing notes the amount of revenue collected for the year ended 30 June 2023 grew by 62.5% compared with the year ended 30 June 2016, the last full year before transformation began. Over the same period, the number of Inland Revenue full-time equivalents reduced by 29%.

There’s been a lot of talk about government cuts for the public sector, but I think the Briefing subtly, or not too subtly, you might say, raises a good question – if an organisation has managed to reduce its headcount by 29% and its funding is not tracked with inflation since 2017, which appears to be the measure for the basis of these public spending cuts, why would you add further cuts?

My view would be, and I think I wouldn’t be alone in thinking this amongst tax practitioners, is that Inland Revenue is under a bit of strain. We know it probably needs to boost its investigations efforts. So why it should be on the chopping block when it’s already done much of what any government would want it to do – more with less. But we’ll see how that plays out.

I thought the amount of commentary in the Briefing around the question of funding this point was quite interesting. It notes that for the year, to June 2024, the department gets about $800 million a year. And at October 31st 2023 its workforce was 4,231. Whereas back in June 2016 it was 5,662. And by the way, the report also notes the department has planned for taking a $13.9 million reduction for the year to June 2025, which was announced by the previous government in August 2023.

According to the Briefing funding would be running around about $700 million going forward, but then adds something the government should probably pay attention to.

“Our primary cost pressures in out years will be remuneration and inflationary cost pressures on technology as a service contracts, accommodation, leases and other operating costs. We are currently developing options for meeting these costs and we’ll report back to you on these matters.”

I know speaking as an employer and along with other colleagues, finding staff is difficult at the moment, so that puts pressure on salaries, obviously. And Inland Revenue is not immune to that because it needs to pay near market rates to attract good quality people, because as the gamekeeper, so to speak, it needs to match the poachers on the other side. Like so much in the year ahead it will be interesting to see how the Minister settles in and what happens with Inland Revenue’s funding.

The shape of things to come – tax credits or threshold adjustments?

And finally, coming back to what lies ahead, as I mentioned at the start, the Half Year Economic Forecast Update left us none the wiser as to the nature of the threshold adjustments, which we think are going to happen. In that gap. David Seymour of ACT has come forward and talked about the ACT policy, which is to simplify the tax rate structure down from the current five rates down to three, with a top rate of 33%. This is moving back to the rate structure which applied from 1989 through to 2008. Basically, until 1 April 2000 (when the 39% rate was introduced) there were two main rates with a tax credit adjustment for low-income earners.

David Seymour talked about tax credits similar to the existing Independent Earner Tax Credit. But as I told RNZ while the concept’s not uncommon, there’s still the issue we discussed earlier. What about adjustments for inflation and keeping the true value of that, otherwise lower rate/ lower income earners will face higher effective marginal tax rates.

There’s also a certain complexity with tax credits. The thing about applying thresholds across the board to everybody, it’s pretty straightforward. Whereas with tax credits, if there’s a claim process that’s involved, not everybody will claim that. It introduces a bit of complexity at the bottom end, which Inland Revenue’s Business Transformation was determined to do the opposite in order to try and make it as easier for most taxpayers to comply.

As mentioned, we have the independent earned tax credit, but it starts cutting out at $44,000 and then drops out at $48,000 once income crosses that threshold. We’ll have to wait to see what happens and in the meantime there will be plenty of debate ahead. We will bring all of those developments to you as usual.

In the meantime, that’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

With effect from 1st July this year, there was a change in the Child Support system so that from that date whenever a liable parent makes a child support payment, it will be passed on to receiving carers on a sole parent rate of benefit.

Previously, any such payment was used to pay the cost of providing the benefit. This change is designed to put more money in the pockets of carers.

The change begins with child support payments due for the month of July 2023 onwards. Child support payments are paid by Inland Revenue in the month following deduction. The first payment that receiving carers receive under the new system would have been made by Inland Revenue on 22nd August “as long as the liable payment parent makes their payment on time.”

And that is a very big ‘but’. As an article at the start of the week in Stuff by Susan Edmunds notes, as of the end of August over $1 billion of child support was due. slightly down from the amount owed in August 2022. But of that amount owing $488 million represents penalties charged.

Inland Revenue acts as the intermediary in the system. It calculates the amount due and then payments by liable parents to receiving carers are made through Inland Revenue. This is done when parties after a relationship breakdown can’t agree how financial support is to be provided. Under the Child Support Act 1991 Inland Revenue manage this whole process by collecting payments from liable parents and passing them on to the receiving carers.

To encourage prompt payment, late payment penalties are payable. Those penalties have been adjusted recently, but the basic charge is an initial 2% penalty of the amount not paid, and then another 8% is added to that 28 days later, if it still hasn’t been paid. These penalties arise for each payment. So, if you keep missing payments, debt piles up, which is what we’ve seen.

I’ve been a long standing critic of this penalty regime. It leads to large amounts of debt building up, a very high proportion of which represents penalties. As Susan Edmunds pointed out, for the June 2021 year, Inland Revenue wrote off nearly a billion dollars of debt and then wrote off another $181 million in the June 2022 year. The system has been like this for years, basically it’s never worked as well as people thought it would.

Somehow, we have ended up with a system where the penalties for not paying your child support on time are greater than those for not paying your tax on time. Remember Inland Revenue is just acting as an intermediary. As I told Susan, the current penalty system is outrageous. Really, we need to have a harder think about it.

Can pay, won’t pay?

This is always going to be a difficult matter because relationship breakdowns can get very toxic. Resentment builds up and without some form of compulsion/penalty, the system would probably be even more dysfunctional. Still, we’ve got to find a middle way.

Incidentally Inland Revenue also has a right to issue deduction notices which I’ve discussed before. It can issue these to an employer on the grounds that this person owes X and you are to take an extra 10% of their salary when you are applying PAYE. I understand quite a substantial number of the deduction notices are that are issued each year relate to arrears of child support.

But even so, it’s a question, I think, for all of us to think about – why is the system like this and what can we do to make it better? There’s been some tinkering around the edges but really, whoever forms the Government after the Election, this is something I’d like to see them think longer and harder about improving.

FBT interest rates to rise

The prescribed rate of interest applies when someone has taken a loan from a company or is a shareholder/director with an overdrawn current account balance. In such situations interest is calculated using the prescribed rate of interest on that overdrawn balance or loan to determine the FBT payable by the company. This interest rate is to increase on 1st October from 7.89% to 8.41%. As recently as 30th June last year the rate was 4.50% so you can see there’s been a very rapid increase in the rate payable.

The downsides of holding property in trust

A few weeks back Tammy McLeod of Davenports Law was a guest and we discussed the new landscape for trusts in the wake of the Trusts Act 2019. One of the areas we discussed was whether in fact so much property should be held in trust. Are there in fact too many trusts? The reason people set up trusts are manyfold, some tying back to the story at the start of this week’s podcast about relationship breakdowns.

But trusts come with downsides. And one has been illustrated in a story that emerged this week regarding people applying for government assistance following the floods in January and February. It turns out that the assistance package provides up to $160 a week to help with the cost of renting a house because your home has been red or yellow stickered.

However, according to this story from 1News the package only covers displaced homeowners. Those people who have property held in trusts are not covered. And this has come as a quite understandably unpleasant shock for a number of affected people.

The story is also interesting in that you can see a number of common misconceptions about trusts pop up, such as one affected homeowner saying, “I own the trust I have that owns my house. I’ve had it for 20, 30 years”. That’s not the case. You may be a trustee, but you don’t own the trust. And then a representative from Ministry of Social Development who’s handling these claims saying “a trust is a separate legal entity.” No, that’s not the case either, the property is registered in the name of the trustees of the trust but a trust does not have any separate legal status, whatsoever.

This misrepresentation might actually be hopefully a window of opportunity for the affected homeowners. Someone looked at this and think, well, if there are trust beneficiaries who are also trustees living in that house, then technically they are homeowners and they then may qualify for support.

I’ll keep an eye on this story and see how it pans out. But it’s another example of what Tammy and I discussed, at the time a trust was set up, it served a very specific purpose. But over time, life changes and maybe those original purposes are no longer valid. It may therefore be time to rethink and perhaps wind up the trust.

Just on the other hand, like I said at the top of the podcast, you may have gone through a relationship breakdown. You’re going into a new relationship and you may wish to protect your assets from the impact of another relationship breakdown through settling a trust. There are other mechanisms that might apply there, but the use of trusts by parties to second or third marriages is not uncommon.

A public mood for change?

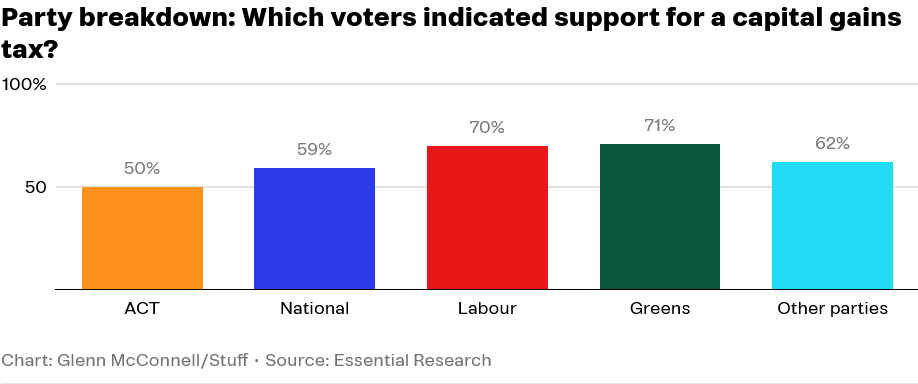

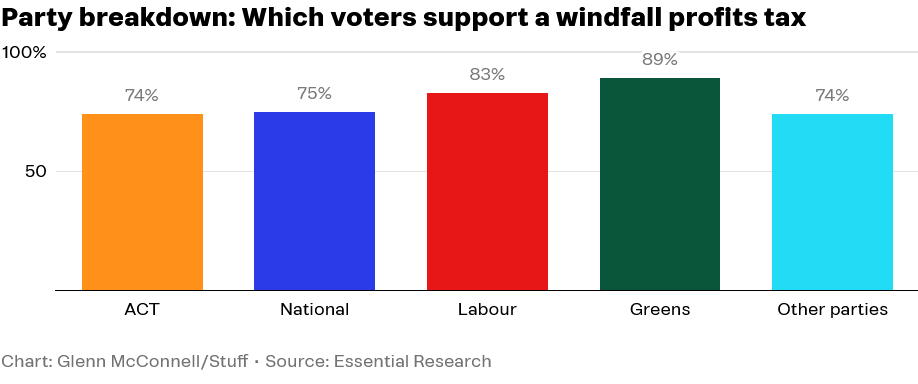

The Election campaign is still rumbling on with just two weeks to go. This week a survey run for Tova O’Brien’s podcast Tova indicates widespread support for taxes on excess profits and capital gains.

Both suggestions have been ruled out by National and Labour but what’s interesting is the apparent cross-party support amongst voters for the proposals.

What makes this poll a bit more interesting is the fact that when it was broken down across the various parties, there was still fairly widespread support for a capital gains tax even amongst National and ACT supporters.

Cross-party support for a windfall profits tax was also surprisingly strong with 74% of ACT supporters and 75% of National supporters in favour.

This is interesting to see and whether any party follows through on any of this is of course a matter which we will only find out after the Election. But even so, the survey perhaps indicates the electorate in some ways thinks there may need to be changes. But on the other hand, as some people rightly pointed out, the Labour Party ran on introducing a capital gains tax in both 2011 and 2014 and got nowhere. Subsequently both Jacinda Ardern and Chris Hipkins ruled out capital gains tax on their watch. The question remains where exactly does the political will amongst the electorate really lie on this issue?

Haere ra Geof Nightingale

Finally this week, haere ra to Geof Nightingale who retired yesterday as a partner from PWC after what can only be described as an distinguished career. Amongst his many accomplishments Geof was a member of the last two tax working groups and has been one of the leading tax professionals in the country for many years. As the many comments on his LinkedIn post announcing his retirement attests, I am one of many he has given sage advice and guidance and it was a delight to have him as an early guest of this podcast. I’m sure this won’t be the last we hear from Geof on tax but for now thank you Geof and go well in your new direction.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

My guest this week is Tammy McLeod, Managing Director of North Shore based firm Davenports Law. Tammy is a trust and asset structuring specialist with over 25 years’ legal experience, specialising in the areas of personal asset planning, trust law and Property Relationships Act. Tammy leads the Davenports trust team and has been a principal in the firm since 2006. Kia ora Tammy. Welcome to the podcast. Thank you for joining us.

Tammy McLeod

Thank you so much for having me, Terry. It’s a pleasure.

TB

Not at all. The Trust Act 2019 came into force on 30th January 2021, and it’s caused quite a big upheaval in the trusts ecosystem. What have you seen as the main changes coming out of the implementation of the act?

Tammy McLeod

A couple of things. The first one is that there’s been a major shift towards the rights of beneficiaries and knowledge of beneficiaries regarding trusts. So, I guess if you think about the shift that we’ve seen over the last ten, 15 years from employer to employee, employees have more rights, landlords/tenants. Now there seems to be a shift from trustees to beneficiaries, to the beneficiaries being entitled to ask for more information and holding trustees to account has really shifted the whole landscape. That’s the first thing.

The second thing is I think that a lot of people are actually deciding whether they actually need a trust anymore. So particularly through the 2000s, we used to set trusts up left, right and centre because their accountant might see the need for a trust, or the neighbours had a trust and it just seems to be the thing to do.

And a lot of people are now taking stock and seeing whether they still actually need a trust or whether it’s something that they don’t need any more given the extra compliance costs that have come about, in particular because of new changes to the law, not just the Trust Act, but also changes to the Income Tax Act and the way trusts report to the IRD.

TB

Yes, that’s a good point, that last one. I’ve seen quite a bit of rethinking about what role the trust has in relation to income tax purposes with the increased disclosure requirements Inland Revenue asked for in the March 2022 and March 2023 years. And now we have, as you may be aware, the bill going through Parliament, which proposes increasing the trustee tax rate to 39%.

A lot of interesting commentary is going around. Many trusts, the majority in fact, rarely distribute their income and have minimal income. Once you aggregate that trusts income with those of the principal settlors, they’re well short of the $180,000 threshold where the 39% tax rate kicks in. So, there’s quite a rethinking going on in that. And that’s certainly what I’ve been seeing.

A lot went on in the nineties and early noughties, as you say, in terms of trust setting up. But right now, as that generation of business owners passes through into retirement, they’re thinking about winding up trusts.

And then there’s the other area where I get asked to help quite a bit. And that’s where you’ve got beneficiaries or trustees overseas. People think of trusts and think of tax. That’s not really why we use trusts, is it? What’s the real purpose of trusts?

Tammy McLeod

No, and in fact what I was taught early on was to never mention tax in the first three things that you talked about the benefits of trusts, simply because that shouldn’t be the only reason.

From a lawyer’s perspective, or from a legal perspective, I think asset protection to asset protection, still should be the number one driver. So, if you are in a position of risk, say the director of a company, own your own business and you could be at risk for because of your actions, then very, very simplistically put, because if your assets are in a trust, that could actually help protect in the event that you were sued for whatever reason, or something went wrong with your business.

And it does date back to the days of the Crusades when the knight would ride off to the Crusades and leave his estate in the hands of the neighbours to look after for his wife and family. Because if he didn’t have someone holding that in trust, then it’s likely that it could have been taken for taxes or just taken. So asset protection is still a big driver.

With relationship property, a trust is not the panacea to all ills when it comes to relationship property. But they certainly help with segmenting estates and ring-fencing assets that people might receive by way of inheritance from relationship property pools. And it’s a really good way of protecting those assets.

Another reason is often people may want to treat their children differently. Under a trust, you can’t claim against a trust in the same way that you can make a claim against an estate. So this is a really good way of estate planning, sort of outside the normal rules around will making and estates and how they’re distributed.

And then lastly, people that have assets might just want to keep it in trust for future generations. So think of a family holiday home as an example, or a family business that’s wanting to be kept for future generations. There’s a number of reasons why trusts can be very, very helpful with asset structuring.

TB

Yes, I’ve come across all of those scenarios and in some sad cases you actually have to ringfence the assets because either the beneficiary is incapable or is an addict sometimes.

On trusts and the government’s proposed 39% trustee tax rate rise, one of the points of debate that I saw raised in submissions to Parliament, it’s a question of will trusts. Because they initially were saying, oh well, they will be taxed at 33% for the first 12 months, but that’s way too short a period in my view. What in your view will be more likely period? More realistic?

Tammy McLeod

Well, I think that probably flagging the 12 months because in estate matters, usually everything’s distributed within 12 months on the grounds of probate. But obviously there’s often times where assets are held on trust under an estate for a much longer period of time, you’ve got minor beneficiaries is the usual rule.

But I would say that probably 85 to 90% of estates are distributed within the first 12 months. So, I think that’s where they’ve got it from.

And another one of those perhaps tax rules where you wind up paying your advisors a whole lot more to sort out what should be something that is quite simple and quite straightforward. But it doesn’t seem fair if you like, for assets or money that’s being held on trust for a minor beneficiary to be taxed at 39 cents, it’s highly unlikely a minor beneficiary would be paying 39 cents on the dollar.

TB

And then as I’ve occasionally come across, there’s disputes over who’s to get what which will delay winding up. Whenever these erupt the only people, in my view, who ever win are the lawyers and accountants.

Tammy McLeod

Without a doubt. Lawyers in particular.

TB

As I said, one of the things I see quite a bit of is – we’ve got a very mobile population – people, beneficiaries, trustees, moving settlors, all moving around the place. What’s your experience with this? How often do you encounter those scenarios?

Tammy McLeod

At the moment, all the time, as you say, particularly after we’ve been shut down in the country, I guess for two years plus, people are just moving all over the place. A lot of people are moving to live in Australia in particular and it’s a real moving feast. There seems to be a lot of the next generation moving to Australia and other places.

And so that’s something that trustees have to be hugely aware of and I think there’s a real onus on trustees to ensure that they are aware of the movement of beneficiaries because it might have an impact on how they’re taxed in relation to the country that they’re in. So for an example, an Australian tax resident beneficiary will be taxed on a distribution from a New Zealand trust, and so proper advice needs to be taken upfront.

And I think that’s one benefit to having an independent professional trustee, is that they should be keeping on top of these issues and flagging these issues. And every time a distribution is made from a trust to a beneficiary, where that beneficiary is situated, should be considered.

Therefore, any trust that we are a trustee of, we ensure that we have regular meetings and it’s one of our agenda items, the location of some of the beneficiaries and making sure that you’re on top of that and then planning for that. Because it’s not even a distribution being made during the lifetime of the parents if they’re settlors and trustees of the trust. It’s what happens if the children are to receive as beneficiaries of the trust assets upon both parents death So it might not be in the immediate picture, but it could be something in the future, it should be planned for.

TB

That’s quite an issue. Particularly in Australia, there are two things. There are the beneficiaries who should qualify for the temporary residence exemption in some cases. That applies to exempt non-Australian sourced income so long as the beneficiary is not a citizen.

And that’s something I think trustees now need to be aware of as people become Australian citizens, then those rules where previously a distribution from New Zealand trust or New Zealand income would not be taxable in Australia. The easier ability to become an Australian citizen changes everything.

And then of course the other one, and I’m sure you’ve seen this, is when a trustee wanders across to Australia and they don’t tell you. I’m sure you’ve encountered that quite a few times.

Tammy McLeod

Many times. And I think it’s one that we’ve been more aware of and there’s been a lot more talk of. But I think the beneficiary one is really becoming an issue because as you say, the population is so mobile and one year you could be in Australia the next year, that could be in the UK, in Singapore, it’s just people are moving around. All over the show.

TB

Distributions to persons in Australia who are not Australian citizens, are manageable. But the real headaches I keep encountering are distributions to people in say Britain, particularly Britain, or America, where the rules can be quite brutal. You can be looking at a 45% tax rate because we use discretionary trusts so much, that can be really quite disadvantageous.

One of those things I see crop up, is that there is a certain proprietorial interest, “this is my trust”. Say the family set it up and were told you can self-manage this and then were sent away. A lot of those got set up during the 1990s..

How do you manage that? You come in, you find someone wants to do something, and then you find out that they’ve done a lot of things they shouldn’t have done in trust law. But what’s the process there?

Tammy McLeod

My pet peeve is how you can manage your own trust. And one thing that really frustrates me is where a lot of professionals are now saying they don’t want to be trustees, and so they’re setting up trustee companies that only mom and dad are the only directors and shareholders, often saying that’s a different entity for Mum and Dad. And I just think that’s wrong.

To me, having an independent trustee is what really makes your trust robust. And so that’s where you can put your hand on the heart and say, I can’t sell this, a trustee has to think “I can’t mortgage this property, I can’t borrow this money or buy this business without my independent trustee knowing. It’s not my decision anymore”.

And to me, that’s the first line of defence of what actually is a trust. Funnily enough, it’s not a legal requirement or one of the certainties of trusts. But from a robustness perspective, definitely having an independent trustee is important. And what has also happened over the last five years in particular, but maybe 5 to 10 years, is that the independent trustees are tending to become professional trustees.

So previously people would often use a family member, or a family friend. And I think the landscape has changed. Not only because of the risk to trustees, and so professional trustees understand the risk, know the risk and can insure against the risk.

I always say professional trustees care, but they don’t care. The numbers on the page are just numbers to us. Whereas for a friend or family member to know how much money the trust is losing, how quickly it’s paying down the debt, that can be too, too much.

So, my view is always have independent trustee, and ideally a professional independent trustee. And it also helps with the management as well. The things that we’ve just been talking about with Australian beneficiaries, if you’ve just got Ma and Pa as the only trustees, how can they keep on top of these issues without the input of a third independent person? So I’m hot on having a professional trustee.

TB

I mean, are you seeing as a result of two things – suppose that the greater rights for beneficiaries, as you mentioned in the start, but are you seeing more issues emerge from those Ma and Pa trusts set up 20, 30 years ago. Are they starting to boil over in difficult ways? What issues are those leading to?

Tammy McLeod

The major difficulty with those ones at the moment, and I’m sure there’ll be more issues that come out over time, but the big thing at the moment is if Ma or Pa dies, or in particular loses capacity, or one’s died and the others lost capacity, who are the trustees now and how are they appointed? Who are they going to be? Often children fighting between themselves. So that can be an issue. And children trying to influence aging, elderly parents. Whereas if you do have the professional in there, A you’ve got a referee, and B you’ve got a platform for how these types of issues are to be managed.

TB

That last point you made about losing capacity is one that makes me very nervous. I talk with clients on this because I’m just encountering it in tragic circumstances. If a trustee loses capacity, am I right in thinking that that means that you probably have to go to court to get things done?

Tammy McLeod

No, not anymore. So under the new Trusts Act, that’s another one of the changes, if a trustee loses capacity, then he or she is then deemed to be incapable of being a trustee going forwards and are immediately removed by virtue of the statute.

So that’s new. Previously there were no rules around who could be a trustee. The other thing the new act has also done is put in place vesting rules. Previously you had to go to court, unless the trustee had said otherwise, to enable a new trustee to be registered on titles to properties and companies, shareholding registrars and so forth.

Whereas now under the new act is an automatic deeming or vesting of the trust assets on the capable trustees. The difficulty can be assessing what capable means.

And just to give an example, I talked to a client last week and one of the settlors is verging on the early stages of dementia and he’s heavily involved in the family businesses. And the question was asked, at what point do we say that he’s not capable?

There’s this balance – is he’s capable of being a trustee? At the moment he understands what he’s doing. Can he make good decisions for the trustees going forward? How do we deem him to be incapacitated? And it might be different for him than it might be for someone else in a similar set of circumstances.

So, if you had an incapacitated, or bordering on incapacitated settlor, who doesn’t have the sophistication of understanding business, etc., that might be a different level of capacity to be a trustee.

So this is a whole minefield. And lawyers have to ask some pretty hard questions and also talk quite robustly with family, doctors, geriatricians and the like particularly with an ageing population.

If you think back about the comments that we’ve made around the lots of trusts being set up in the 1990s and early 2000s, some 20 years on we’ve got a whole raft of settlors and trustees heading towards their mid to late eighties and nineties. It’s a bubble that’s moving through which is going to create lots of issues because the other thing to remember is that enduring powers of attorney don’t fit with trusts.

TB

I was just about to ask you about that one.

Tammy McLeod

So your enduring power of attorney relates to your personal property, it doesn’t relate to your powers as a trustee. There can be mechanisms within trust deeds which help with who has the power to appoint or remove trustees or a settlor who loses capacity. But it’s not a given that the powers of attorney and the trustees have any connection at all, you need to go back to the source documents and see what’s there.

TB

What do you see going forward with trusts? Do you see much change in this area?

Tammy McLeod

I see massive change and I’m seeing it already, probably in the last three or four years, rather. We’re still setting up a lot of trusts. But we’re winding up as many, if not more probably, than what we’ve been setting up. There are still great reasons, as we talked about earlier, for people to have trusts and most people are still putting in place asset structuring.

But I see there’s a lot more dispute. A lot of the work that I’m now doing – I used to say that my legal practice is all about the good, positive things of setting up, good positive structures for people, for the future. And now a lot of it is actually how do we unwind the structure of these trustees not doing what I want them to do?

How do I make this beneficiary behave? There are disputes after Mum and Dad have died between beneficiaries as to what’s to happen with the trust assets. It’s disputes between trustees, disputes between beneficiaries.

So it’s become a lot more fraught, bordering on litigation type issues. A lot more people separating, the impact on relationship property. That’s how I sort of got more into that area was people separating, myriads of trusts which had to be unwound which were complicating factors.

What I do nowadays is more quasi litigation rather than setting up structures. And I guess that’s interesting from a purely legal perspective as well as my practice matures. So that’s interesting as well, but definitely very, very different to what it was five, ten years ago.

TB

As I said, the explosion of trusts, and we don’t actually know how many trusts we have in the country, and it’s one of those per capita starts we probably shouldn’t be too proud of.

With the administration of trusts you’ve mentioned trustees’ meetings. How critical are they in this process, particularly what you just talked about with the potential incapacity, etc., and the professional trustee?

Tammy McLeod

I think that companies, to give as an example, as opposed to trusts, are quite easy to manage in a way because the Companies Act 1993 is quite prescriptive about what you need to do to make sure that your company carries on as a company with the Annual Return and so forth.

Trusts aren’t like that. So even under the new act, there’s no real prescription there. But that’s your only evidence really, of having a trust, because trusts are this kind of ethereal being, I can’t give you something and say, here, this is a trust for your record keeping.

So having those trustee meetings are imperative to go over the kinds of things that we’ve been talking about today. Where are the beneficiaries? What’s the capacity of the trustees? Tax issues, etc.

And in fact, I’m presenting a seminar next week at the North Harbour stadium which got around 600 people registered for. And we’re going to be covering things like this. So why do you need a trust is often the first question I get asked about in trustee meetings “Remind me again why I need this trust.”

I’ll be talking about things like capacity, powers of attorney, the changes to the act, disclosure of information to beneficiaries. So, I’ll be covering all that at the seminar next week. Those are the sorts of things that we talk about at the annual trustee meetings.

TB

I’d agree trusts are quite ethereal. Sometimes you see on companies’ office documents that the ABC trust holds the shares in this. Which is not correct at all. It’s the trustees that should be named as shareholders.

So, there’s a lot of sloppy or untidy administration out there and it can lead to quite a number of issues. We’ve mentioned beneficiaries overseas. What I get very concerned about in tax is when settlors or trustees move overseas, particularly in the case of Australia if a trustee goes over there, the New Zealand property could become taxable subject to Australian capital gains tax, even if the gain is distributed to a New Zealand resident. So heaps of things going on.

I think that might be a good place to leave it there. If you’ve got this seminar coming up, I know I’ve seen you present, that will be well worth attending with 600 attendees. I’m sure you can squeeze a few more in.

My thanks very much to you, Tammy, for coming along and talking to us on this podcast. Good luck with the seminar next week.

Tammy McLeod

Fantastic. Thank you so much, Terry. I really appreciate it. We’ve been friends for a very long time, so it’s nice to get a spot on the podcast.

TB

I can very highly recommend Tammy, she’s a highly experienced veteran of the trust field. You’ll be in very good hands and the seminar will be well worth attending.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Official Cash Rate was increased last week, but Inland Revenue seems to have pre-empted the effects of an increase as two weeks ago it announced that the interest rate for use of money interest on unpaid tax and for the prescribed rate of interest for fringe benefit tax purposes would increase from 10th May.

The use of money interest rate on unpaid tax will rise from 7% to 7.28%, and the prescribed rate of interest for fringe benefit tax purposes will rise from 4.5% to 4.7%, with effect from the quarter beginning 1st July 2022. The use of money interest rate for overpaid tax remains at zero.

With the final provisional tax payment for the March 2022 income year coming up on 9th May, it’s a good time to ensure that your Provisional Tax payments are as accurate as possible to minimise the effect of this use of money interest. That’s particularly true where a taxpayer’s residual income tax for the year is expected to exceed $60,000. So right now, advisers like myself are looking at this situation and making sure clients are getting ready to make the payments they need to minimise any potential interest charge.

As we’ve discussed previously tax pooling is a useful tool in dealing with tax payments. And right now, people are making use of tax pooling not only to get ready for the Provisional Tax payment coming up, but we’re also wrapping up the final tax payments due for the year ended 31 March 2021. There will be people who haven’t paid sufficient tax for the year and could be looking at substantial use of money interest and maybe even related late payment penalties.

This is therefore a good time to make use of tax pooling intermediaries. Typically, the deadline for making a request to use tax pooling is 76 days after the terminal tax date for the relevant taxpayer. If the taxpayer has a 31 March balance date and is linked to a tax agent, that is typically 7th of April, which means that sometime in mid-June is the final date for payment. If they’re not linked to a tax agent the terminal tax due date was on 7th February and therefore they’ve only got a few days left to make that payment using tax pooling.

What’s happened is that in the wake of the Omicron wave, Inland Revenue have used the discretion that was given to them when the pandemic broke out to extend the deadline for the time in which a request for making tax pooling can be made.

That time has now been extended to the earlier of 183 days after a terminal tax date or 30th September this year.

There are a few conditions. The contract must be put in place with the tax pooling intermediary on or before 21st June. Furthermore in the period between July 2021 and February 2022, the so-called affected period, the taxpayer’s business must have experienced a significant decline in actual predicted revenue as a result of the pandemic. This meant they were unable to either satisfy their existing commercial contract with tax pooling intermediary or weren’t able to enter into one, or they’ve had difficulties finding the tax return because either they or their tax advisor was sick with COVID.

Now this is a good use of the discretion available to Inland Revenue. But remember, it is COVID 19 related. So if you just happen to have been caught off guard and didn’t make your payments on time, you’re not going to get this additional extension of time. Tax pooling is a very useful tool which you should make use if you can.

But if you can’t, talk to Inland Revenue and make them aware that you have issues. You’ll find that they are more approachable in this than people might expect and can be quite fair so long as you come to the table with a reasonable offer.

Trust compliance just got more expensive

Moving on, we’re now starting to prepare tax returns for the year ended 31 March 2022. And for this year, the required reporting requirements for domestic trusts have been greatly increased following a legislative change last year.

In connection with that, Inland Revenue has released Operational Statement OS22/02, setting out the new reporting requirements for domestic trusts. These reporting requirements were introduced to gather further information from trustees so Inland Revenue can “gain an insight into whether the top personal tax rate of 39% is working effectively and to provide better information and understand and monitor the use of trust structures and entities by trustees”. It’s what we call an integrity measure.

There is a hook in that the legislation is also retrospective as it enables Inland Revenue to request information going back as far as the start of the 2014-15 income year.

The Operational Statement is a pretty detailed document, setting out over 48 pages the obligations involved. There’s a very useful flow chart on page 6 setting out what trusts will be caught under the provision and required to make the relevant disclosure disclosures. The basic rule is that all trustees of a trust, other than a non-active complying trust, who derive assessable income for tax year must file a tax return and therefore will be subject to the reporting requirements.

Non-active complying trusts are not required to file tax returns. These are trusts receiving minimal income under $200 a year in interest, no deductions other than reasonable professional fees to administer the trust and minimal administration costs, such as bank fees totalling less than $200 for the year. Such trusts are not required to file tax return.

The trustees also need to file a declaration that it is a non-active complying trust, it’s not enough to be not required to file a tax return, it must also file this declaration. The types of trusts covered by this exemption are ones which may hold a bank account earning some interest. More generally, their principal asset is the family home and the beneficiaries are living in that place and are responsible for meeting the ongoing expenses.

For those trusts required to comply there’s a fair bit of detail involved. But fortunately, there is an option for what they call Simplified Reporting Trusts. These are trusts which derive assessable income of less than $100,000 or deductible expenditure, which is also less than $100,000 and the total assets within the trust at the end of the income year are under $5 million. Such trusts can use cash basis accounting and aren’t subject to the full accrual reporting requirements set out by the Operational Statement.

In addition to preparing detailed financial statements, there are several other requirements that the trustees are expected to provide to Inland Revenue. These include details of each settlor of the trust and each settlement made on the trust together with details of beneficiaries and distributions made to beneficiaries. The trustees must also provide details of who holds the power of appointment within the trust.

All this expands greatly the amount of reporting that trusts have to do now. And although typically you do see financial statements prepared for most trusts that do have to file tax returns, these requirements extend those reporting obligations. And I daresay many trustees aren’t going to be too happy about the increased costs that will come out of that.

And of course, we have this potential issue now, that Inland Revenue may request information going back as far as the start of the year ended 31 March 2015. There’s a fair bit of controversy around this measure which would certainly mean a lot more work for advisors and trustees.

A very British scandal that risks Kiwis

Now, over in the UK, the Chancellor of the Exchequer Rishi Sunak, the equivalent of Finance Minister Grant Robertson, is embroiled in a political scandal after it emerged that his wife, Akshata Murty, has been claiming non-domiciled status for UK tax purposes.

Non-domicile status means that a person’s foreign income and capital gains are generally not subject to UK income tax and capital gains tax unless they happen to be remitted to the UK. It so happens that Ms Murty’s father is the billionaire owner of an Indian IT company, and it’s estimated that she may have saved up to £20 million of UK income tax on dividends from her father’s company. Needless to say, it’s not a great look for Mr Sunak as the person responsible for managing the finances of the UK to find himself in that position.

But Ms Murty’s status as what is called a non-dom is actually quite common. Most New Zealanders living and working in the UK would qualify as non-doms and may be able to make use of this special status. The exemption is pretty generous. In fact, according to a University of Warwick research study, more than one in five top earning bankers in the UK has benefited from claiming non-dom status. Apparently a sizeable share of those earning more than £125,000 per annum have non-dom status. For example, one in six top earning sports and film stars living in the UK have claimed non-dom status. As these persons have got an average income of more than £2 million pounds per year it’s a pretty significant benefit.

Now what New Zealand advisers need to be watching out for is misunderstanding the complexity of these rules. It used to be the general rule that a non-dom’s income was not taxed in the UK if it wasn’t remitted to the UK. The opportunity was for New Zealand trusts to make distributions of income to UK resident beneficiaries, but never actually remit that income to the UK. Instead it stayed in a New Zealand bank account or some other non UK bank account and therefore wasn’t subject to UK tax rates, which could be as high as 45%. It also meant that the income distributed wasn’t taxed at the trustee rate of 33%, so it was a very nice, tax-efficient system.

However, the rules have been subject to a number of changes in past years, as political pressure has built on the question of whether these non-doms should get such generous tax treatment. I’ve seen a number of cases where advisers have continued to apply what they think the rules are, unaware that there have been significant changes to the use of non-dom rules and the remittance basis. They have therefore inadvertently created tax liabilities for not only for the UK resident beneficiary, but potentially also for the trust.

The UK has introduced a register of trusts and in some cases, New Zealand trusts may be required to be part of that register. Along with UK inheritance tax this is one of these ticking time bombs where there is a lot of people who don’t know what they don’t know and could be in for an unpleasant shock.

It’s also fairly highly likely in the wake of this political scandal that there may be more changes to come to the non-dom exemption so trustees with beneficiaries resident in the UK, should be very careful about making distributions to such beneficiaries in the mistaken belief they are trying to exploit a rule which has been amended. Generally speaking, the use of trusts in the UK and in particular distributions from foreign trusts to UK tax residents is a real minefield and great care is required to avoid potentially serious tax consequences.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

If a week is a long time in politics, then the three weeks since our last podcast feels like a decade. If you think I’m exaggerating, Inland Revenue’s latest Agents Answers notes that more than 100 policy and remedial changes are expected to take effect on or before 1st April.

Aside from this, there are also the ongoing COVID support measures. Applications for the second COVID support payment opened on Monday 14th and next Monday 21st of March applications open for a top up loan from the Small Business Cashflow Scheme. In addition, in the wake of the disruption caused by the ongoing Omicron wave, Inland Revenue has effectively delayed the due date for filing March 2021 income year tax returns until 31st May.

This extension also applies to certain elections, which would normally be due by 31st March, and such elections include filing controlled foreign companies and Foreign Investment Fund disclosure forms, making subvention payments relating to the 2021 tax year, and look through company elections for new companies or companies that were previously non-active. That’s all-good stuff and helpful to those tax agents who have been hit by Omicron and their schedules disrupted.

Limiting interest deductions for residential property investors

As I said, it’s been a busy period since our last podcast. The Taxation (Annual Rates for 2021-2022, GST and Remedial Matters) Bill, introduced on 8th September 2021, was reported back to Parliament on 3rd March.

Now this is the bill, which by way of a supplementary order paper, contains the controversial interest limitation and deductibility rules for residential investment property. The bill also has a number of other important measures relating to the treatment of cryptoassets, and GST in particular. It’s an important bill which must be passed by 31st March I believe, as part of the normal Parliamentary supply process.

Cryptoassets are an extremely fast-moving area. As the report of the Finance Expenditure Committee notes, there are already over 15,000 different types of crypto assets. And as a result, the Committee has recommended changes to definitions, in particular, removing the fungibility requirement for the cryptoasset definition. Its now going to add a definition for nonfungible tokens, or NFTs, which are all the rage at the moment.

There was also a recommended change to the GST apportionment rules to make it clearer the new apportionment rules do not target people who are property developers. I’ll talk a bit more about GST apportionment a bit later in the podcast.

But of course, the big and most controversial part of the bill, is in relation to the interest limitation rules. Broadly speaking, there are some changes around the fringes, but nothing significant. And that’s what I would expect with the Government’s super majority. It will push through these changes.

One of the things of note and which will be disappointing to some, is that submissions that the definition of new build should include improving, renovating or repairing existing buildings, dwellings and extensive remediation of uninhabitable dwellings, were not adopted.

The Committee did not consider these to be new builds and should not receive tax incentives by exempting the activities from interest limitation rules. However, the Committee considered the new build exemption should apply in some circumstances where “remediation of an existing dwelling prevents it from falling out of available housing supply.”

The Committee went on “In expanding the exemption, we aim to make these rules as clear and objective as possible, so would avoid using subjective terms such as ‘uninhabitable’.” A wise move there.

They therefore suggest the new build exemption would apply to existing dwellings in two specific situations. These are where a dwelling has been on the earthquake prone buildings register but remediated and removed from the register on or after 27th March 2020, or a leaky home has been substantially, at least 75%, reclad. They say there are verifiable criteria available which would allow for clear application of a new build exemption.

They also have agreed that there needs to be some changes to rollover relief provisions in relation to transfers to and from trusts and parents co-owning property with their children. The later has become particularly controversial with reports in the media about how the bright-line test has affected parents helping their children into a house.

An example given, where parents become co-owners of a property with their adult children and later sell a part share of the property to the children. The parents would be disadvantaged if the period subject to the bright-line test for any remaining share they own restarts on the date of the sale. There’s going to be an amendment to change that.

One of the other things, of course, that happened whilst I was away cycling part of the Tour Aotearoa – highly recommended by the way – is that National made its proposals around changes to the tax thresholds. There’s commentary from the National Party in the Minority Report on the lack of action in that area. And as you might expect, ACT also takes a view that these changes aren’t needed at all. So, politics will carry on as normal

Simplifying GST

Moving on, Inland Revenue has been busy kicking out a number of consultation documents. An important one was on 8th March, which relates to GST apportionment and adjustment rules, which I mentioned earlier. Inland Revenue is looking at policy options for reforming and simplifying these rules.

This is actually very important because these rules are very complex. One concern in particular, is that although GST does not tax most private assets, such as dwellings, an issue arises where some private assets may be used by a GST registered person to make taxable supplies. For example, when a person is working from a home office. Or a GST registered person may own a holiday home, which they also rent out as a taxable supply of guest accommodation.

There is an argument the use and disposal of those private assets may be in the course of furtherance of a registered person’s taxable activity. So that could lead to a GST liability when those assets are sold or an apportionment adjustment if there is a decreased percentage of taxable use.

Now what Inland Revenue have pointed out is, and what’s well known, is that many registered persons are unaware there could be such GST consequences. And what it’s suggesting is that we need to look at proposing a revision of the rules and simplification.

The proposals include a principal payment purpose test for assets purchased for less than $5000 GST exclusive. For assets above that threshold a de minimis test is proposed. If the registered person’s taxable use of the asset is less than 20%, the asset is regarded as non-taxable. No input tax deduction could be claimed on purchase, but critically no GST would be accounted for on a sale. The flipside of this is an 80% rounding up rule. Assets with 80% or more taxable use would be deemed to have 100% full taxable use. So therefore, there would be a full input tax deduction with only small amounts of non-taxable use. This is an important paper and worth reading in detail.

Taxing the gig economy

Another paper which came out two days later, was on the role of digital platforms in the taxation of the gig and sharing economy.

This paper contains proposals intended to make it easier for people earning income through digital platforms, the gig and sharing economy to comply with the tax obligations. It’s looking for feedback on how GST should apply in those rules, and whether there are opportunities to reduce compliance costs in the tax system for people earning in the income from the gig economy. As the paper notes the gig economy is now a substantial and increasing part of the modern economy.

The paper looks at what’s going on and how the current tax system deals with the gig economy. In my view the tax system currently doesn’t deal very well with the micro and small businesses. Just as an aside, in relation to this, I do wonder whether it’s time for the tax system to introduce a nil rate band for income tax purposes. This is something we see in other jurisdictions, for example across the Ditch, in Australia.

As the current legislation stands, every dollar that is earned must be taxed. And I do wonder, that might have been appropriate when inflation was low, but now seems to represent an unnecessary burden, particularly when the rate of tax in the first $14,000 is only 10.5%. The question is how much tax would it cost? How much is involved in calculating that and collecting it? Again, I recommend a good thorough read of this paper.

Minimum standards for trusts

On 7th March, an Order was made setting out the minimum standards for financial statements to be prepared by trusts in relation to new disclosure requirements.

These are actually in force for the current tax year and will be required to be complied with when we start preparing tax returns for the year ended 31st March 2022.

And there’s a special report that sets out what trusts are required to comply and what’s expected to be prepared. Basically, the minimum requirement will be to prepare a statement of profit loss and a statement of financial position. This is part of the wider information gathering that Inland Revenue wants, but also in this particular case on trusts, when you look at the new Trusts Act, which took effect earlier this last year, there’s an expectation for trustees to provide and prepare more financial information.

So again, that’s an effective increase in compliance costs, yes, but also something which is part of a wider need for transparency and full disclosure in the trust regime.

Preventing avoidance of the new top tax rate

Now, if all that wasn’t enough to be chewing over, on Wednesday Inland Revenue released a consultation document on top tax rate avoidance prevention proposals. It’s proposing some measures that limit the ability of individuals to avoid the 39 or 33% personal income tax through use of a company structure.

Now these are what we call integrity measures, there to support the integrity of the tax system. They are to be expected. But what’s interesting here and what’s going to cause some controversy, is a proposal that the sale of shares in a company by a controlling shareholder will be treated as giving rise to a dividend for that shareholder to the extent that the company and its subsidiaries have retained earnings.

This is to counteract the 11-percentage point differential between tax paid at a company level at 28%, and tax paid at the individual level at 39%. What concerns the policy advisers is that companies will not be making distributions of dividends, but by selling the shares and the shareholder usually realising what is a tax-free capital gain under present legislation, this issue of that 11-percentage point differential can be avoided.

Accordingly, one of the measures in this consultation document is to address that. There are a few other matters in the paper which I’m still digesting. So what I propose to do is talk about it at more length next week.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax tax or wherever you get your podcasts. Thank you for listening, and please send me your feedback and tell your friends and clients. Until next time, kia pai te wiki. Have a great week.