Inland Revenue releases three special reports regarding the changes to the platform economy rules, the 39% trustee tax rate and the new 12% offshore gambling duty

Under the banner “Cut your excuses and sort your tax” Inland Revenue last Monday issued what it called a “last chance warning to the construction sector” to do the right thing and get on top of their tax obligations. The release advises that if people do the right thing, then Inland Revenue will help them. If they don’t, Inland Revenue will find them and start follow up action.

Richard Philp, a spokesperson for Inland Revenue, commented;

“Most people and businesses in New Zealand pay tax in full and on time but there is a core group who don’t. … we also know that while some are struggling just to keep up with the everyday grind, others are actively avoiding their tax obligations.”

Tax evading tradies?

Apparently, tax debt is high in the construction sector and there’s also a fair amount of cash jobs apparently happening in the sector. The Inland Revenue release commented that across all sectors, it gets about nearly 7,000 anonymous tip offs about cash jobs and the like each year noting “Construction is the industry most anonymously reported to Inland Revenue”.

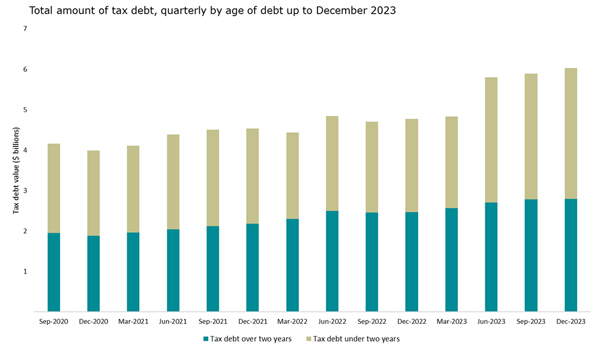

The media release is silent about the extent of the debt within the sector, but we do know from the latest statistics as of 31st December 2023, that tax debt over two years old has increased to from $2.5 billion in December 2022 to $2.8 billion in December 2023.

ADVERTISING

Understandably, with the Government’s books under pressure, Inland Revenue is keen to collect as much of this overdue debt as quickly as possible. This is probably the first of many such campaigns where we will see Inland Revenue taking additional action. And remember, under the Coalition agreement, additional resources have been promised to Inland Revenue for investigation work.

In this particular campaign, Inland Revenue is saying it’s going to issue emails and letters to 40,000 taxpayers in the construction industry who have either outstanding tax debt or tax returns, or both. It then specifies that 2,500 of those will be contacted by text message, asking if they would like to support to get their outstanding tax sorted. There will be a follow up call if the taxpayers they respond that they do want help. Inland Revenue will also be carrying out site visits to key locations across the country.

As I said, this is likely to be the first of several initiatives we’re going to see from Inland Revenue. I would be interested in seeing some specific stats around the proportion of debt and the composition of debt and get an understanding of what sort of businesses are struggling here. It will also be interesting to see how successful this campaign turns out to be.

More on the new GST rules for online marketplaces

Last week I discussed the confusion that seems to have arisen following the introduction of new GST rules from 1st April. These rules affect people who are not GST registered but provide services through such apps as Airbnb, Bookabach and Uber.

This week, Inland Revenue released three special reports relating to the new legislation and one of these is on accommodation and transportation services supplied through online marketplaces. In fact, this is an updated version of a report previously issued in June last year. The report has been updated to include the changes that took effect as of the start of this month and in particular how the flat-rate credit scheme operates.

Changes to online marketplace operators

Under the new rules, so-called online marketplace operators such as Airbnb, Uber and Bookabach will charge GST on all bookings made through them. However, the person who actually provides the ride or the accommodation may not be GST registered. This is where the flat-rate credit scheme comes into effect as the following example illustrates:

The full report is 68 pages so there’s plenty more to dive into.

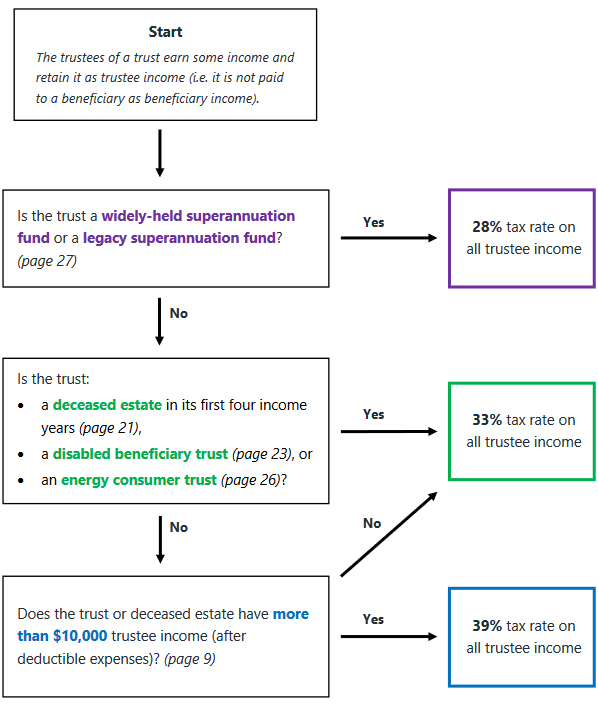

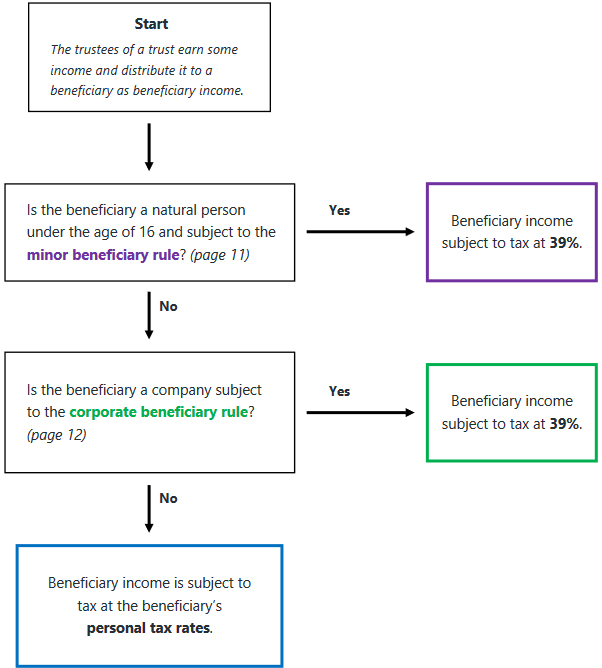

Special report on 39% trustee rate

One of the other reports that was issued is on the application of the trustee rate of 39%. Basically, trustee income is the net income of the trust, which has not been distributed to beneficiaries. The 30-page report explains the basic provisions about “beneficiary income” and “trustee income” together with a couple of useful flow charts.

Trustee income flowchart

Beneficiary income flowchart

The report references the minor beneficiary rule which applies where the beneficiary is a natural person under the age of 16. In such a case only $1,000 of income per year can be distributed to that person as beneficiary income and be taxed at that person’s marginal tax rate, presumably below 39%. Under the new rules, any beneficiary income in excess of $1,000 paid to a minor would be taxed at 39%.

Overall, this is useful guidance. Just remember the $10,000 threshold is all or nothing: if trustee income is $10,000 or less, the trustee tax rate that applies is 33%, but if it’s $10,001 then it’s 39% on everything.

The third report is on the proposed offshore gambling duty, which takes effect from 1st of July and will apply to online gambling provided by offshore operators to New Zealand residents.

The bright-line test and tax evasion – a couple of useful real-life case studies

Finally, this week a couple of interesting Technical Decision Summaries from Inland Revenue. Technical Decision Summaries are anonymised summaries of some interesting cases that Inland Revenue’s Tax Counsel Office has encountered either through tax disputes and investigations or applications for binding rulings.

The first one, TDS 24/06, is an application for a ruling regarding whether the bright-line test or section CB 14 of the Income Tax Act would apply. The facts are complicated but involve three sections of land currently owned by the ruling applicant.

The applicant had initially acquired one section outright before his spouse and another co-owner acquired interests as tenants in common. Over time, the applicants proportion of the ownership changed until at the time his spouse died the property was held 50% as tenants in common with his late spouse. The second section was owned 50% each as tenants in common with his late spouse. After her death her 50% interest had passed to him under her will. The third section was owned by the applicant and his late spouse as joint tenants. Following her death, her interest was automatically transmitted to him.

The ruling applicant was concerned about the treatment of future sales. Would the bright-line test apply or failing that, would section CB 14? This section is a little used provision and applies where there’s been a disposal within 10 years of acquisition and during that time there’s been a 20% more increase in value of the land thanks to a change in zoning, or removal of restrictions.

The Tax Counsel Office concluded neither the bright-line test nor section CB 14 would apply. This is obviously a good result for the taxpayer but it’s actually also a good example, of how you can apply for a ruling to get Inland Revenue’s interpretation on a tax issue. You don’t necessarily have to follow it, but if you don’t, you better have good reasons for not doing so.

Fiddling the books and getting found out

On the other hand, TDS 24/07 involved suppressed cash sales, GST and income tax evasion and shortfall penalties. The taxpayer carried on a restaurant business which was registered for income tax and GST. Inland Revenue’s Customer Compliance Services (CCS) investigated the company and formed the view that there was fraudulent activity going on. There was suppression of cash sales, and the taxpayer was under returning GST and income tax.

CCS reassessed the taxpayer’s GST and income tax returns for the relevant periods and they increased the taxable revenue for suppressed cash sales based on analysis of point of sale data, the taxpayer’s bank statements and industry benchmarking.

Industry benchmarking – an underused tool?

Just on industry benchmarking, I think Inland Revenue ought to be much more public about its data here and warn taxpayers there are benchmarks against which it will measure your business. It has done so in the past, but I think the combination of Business Transformation and then the pandemic interrupted progress in this space.

What people should remember is, Inland Revenue has some of the best data available anywhere about measuring industry benchmarking. I believe it should be making this much more public so that it can serve as an early warning shot for businesses that think they can suppress income. Everyone loses when this happens. Gresham’s law about bad money driving out the good is very applicable here, because businesses which are not tax compliant are undercutting those businesses which are following the rules. This is not a healthy situation as it leads to considerable frustration and anger and if not dealt with, will just simply encourage more of the same behaviour.

Tax evasion? Have a 150% shortfall penalty

In this particular case, the taxpayer’s fraud was identified, and GST and income tax reassessments followed. In addition, Inland Revenue also imposed tax evasion shortfall penalties, which are 150% of the tax involved. These evasion shortfall penalties were reduced by 50% for previous good behaviour, but that’s still represents a penalty of 75% of the tax and GST evaded.

Unsurprisingly, the taxpayer counter-filed a Notice of Proposed Adjustment under the formal dispute process, and the dispute ended up with the Adjudication Unit, which is run by the Tax Counsel Office as part of the formal dispute process. The Adjudication Unit did not accept the taxpayer’s counter arguments, including an attempt to claim an income tax and GST input tax deduction for the cost of fresh produce purchased with cash. The problem was there was no supporting evidence for this claim, so the Adjudication Unit probably found it easy to reject it. The Adjudication Unit ruled not only was the tax due, but the penalties were also correctly imposed.

Get ready for more Inland Revenue action

Circling back to our first story, this TDS illustrates what lies ahead for those in the construction industry who have been suppressing income. As I said, I do think Inland Revenue should make everyone more aware of its benchmarking data which would be a warning for would be tax evaders. It’s pretty clear from the announcement about the construction industry that Inland Revenue is gearing up for many campaigns targeting debt arrears and clamping down on tax evasion in particular industries. As always, we will keep you updated as to developments in those areas as they happen.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Treasury Analytical Note examines the effects of taxes and benefits for the 2018-19 tax year

The Australian Tax Office gets heavy with the Exclusive Brethren – will Inland Revenue follow suit?

Understandably the start of the new tax year on 1st April and the increase in interest deductibility for residential investment property to 80% was generally greeted by residential property investors with enthusiasm. Users of apps such as Airbnb and Uber, on the other hand, were less enthusiastic because the provisions relating to GST on listed services also took effect on 1st April. It has become clear that this change has caused some confusion and led indirectly to price rises.

Now GST on listed services refers to online marketplace operators who “facilitate the sale of listed service”. This is the so-called “Apps Tax”, which National promised to repeal when it was campaigning in last year’s election but then decided to keep it because it needed the money to make up for the loss of its overseas buyers tax.

These rules apply to the likes of Airbnb, Uber, Ola, and Bookabach which facilitate the sale of related the services. They now have to collect and return GST when the relevant service is performed, provided or received in New Zealand. It doesn’t matter whether or not the seller, the actual person doing the providing of the Uber or Airbnb, is GST registered. (For those already GST registered the change will have little effect).

Confusion and an unnecessary price increase?

However, a significant number of those providing the Uber or Airbnb, are not GST registered because the total services they provide annually are below the GST registration threshold of $60,000. But the introduction of the apps tax has prompted some of these non-registered persons to effectively increase their prices 15% to take account of the GST charge. However, this overlooks that though as part of the changes those non-GST registered persons can expect a 8.5% rebate under the flat-rate credit regime scheme.

What happens here is the offshore marketplace (Uber or Airbnb) will collect 15% GST on the booking but then pass 8.5% of that to the persons actually providing the Uber or Airbnb. But as an article in The Press notes, it appears many people now think they are GST registered and have effectively increased their prices by 15%. As Robyn Walker of Deloitte said, there definitely appears to be some confusion around hosts about this law change, and probably many don’t fully appreciate that they’re getting this 8.5% rebate.

As GST specialist Allan Bullot of Deloitte, noted there is a lot of confusion with Airbnb. It’s a complicated area, and something Airbnb providers are very careful about is registering for GST because of the fear they might have to pay GST if they sell the property to someone who’s not GST registered. In which case they effectively had to pay GST on the capital gain.

It appears what we’re seeing here is that those who have been brought into the new flat rate credit scheme haven’t yet quite worked out how the new rules will work for them. I would expect things to settle down in time and maybe Inland Revenue might put out more guidance. But it would appear that some providers are getting an accidental windfall at this point, although the increase is taxable for income tax purposes. Anyway, watch this space to see how this plays out and whether there’s some tweaking to the rules as this scheme beds in.

Treasury analyses the effects of tax and income

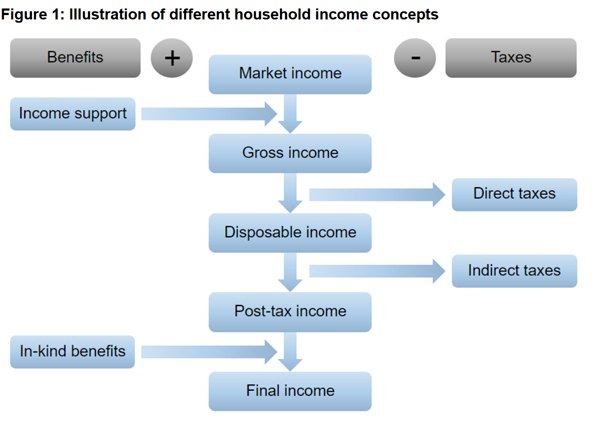

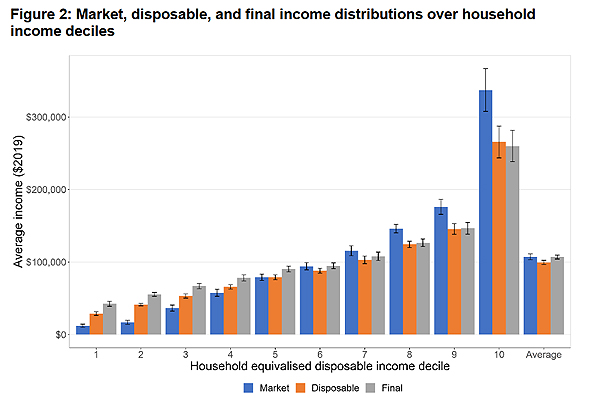

Moving on, just before the end of the tax year, Treasury produced an interesting Analytical Note on the effects of taxes and benefits on household incomes in tax year 2018 – 2019. This is interesting in a number of ways because frequently when people are talking about the effective tax burden, they look at the impact of direct taxation on a person’s pre-tax income.

Some have pointed out this is not really a true measure of a person’s net tax burden. They’re referring to the effect of transfers that people might receive from government in the form of Working for Families or New Zealand Super, but also the indirect transfers such as education and healthcare.

This paper tries to examine that for the 2018-19 tax year and what it does is calculate a household’s “final income” which represents net income after direct and indirect taxes and then adds an estimate of the government spending on health and education services received in kind.

As the paper notes basically when you just look at disposable income, that is market income plus transfers, such as Working for Families credits or New Zealand Super, these are incomes are generally lower than market incomes on average over the population of New Zealand, and fairly unequally distributed. However, once you bring in indirect taxes and in kind benefit payments to get final incomes as defined, these are significantly more equally distributed than disposable incomes and close to market incomes when averaged over all households.

Yes, but what about Gini?

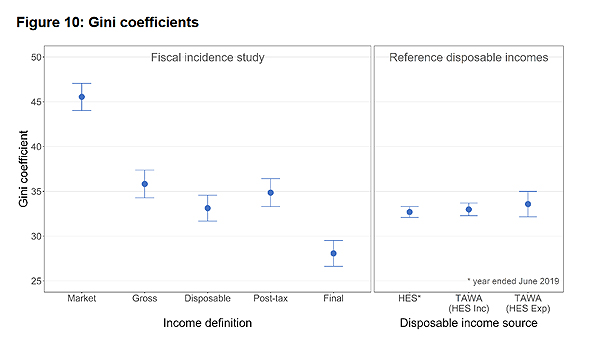

The Note also considers the Gini coefficient. This is the measure of inequality, where the higher the number, the more inequality society is. The Gini coefficient starts at 45.6 ± 1.5, and that drops to 35.8 once you bring in income support payments. Once you include consumption taxes and the benefits in kind such as health and education you end up with a Gini coefficient of 28.1 which is considerably lower and indicative of a much more equal society.

What the Treasury analysis did was to take 66% of all core Crown tax revenue and 68% of core Crown expenditure and allocated that to New Zealand households. Although the effect is approximately neutral as the note describes the effect is unevenly distributed. Households in the bottom five “equivalised disposable income deciles” received on average more in government services than they paid in taxes, whereas the opposite is true for houses in the top four deciles.

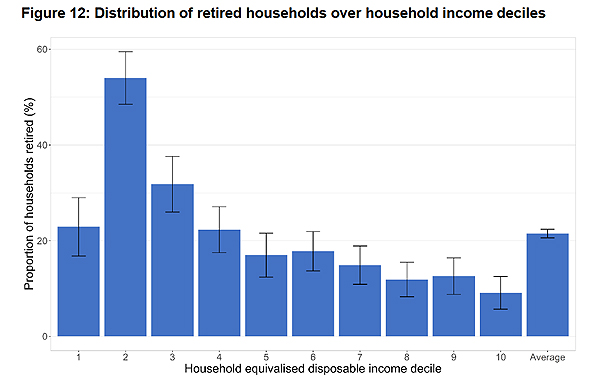

The second decile is the one where there’s a large amount of support happening. This is because there’s a fairly high concentration of New Zealand super recipients in that second docile.

The Note also considers “retired households”, where one of the people in the household is receiving New Zealand super.

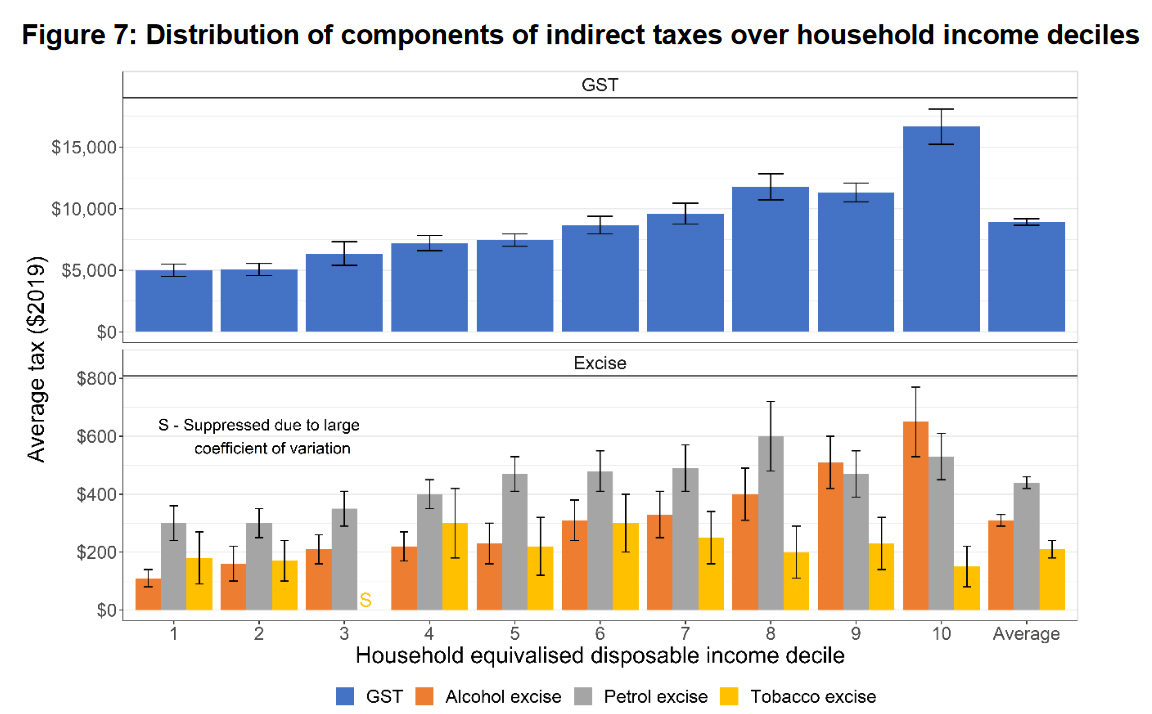

“Drink yourself more bliss”

I was amused to see in the analysis of indirect taxes a comment about the average alcohol excise amounts increasing reasonably steady with each decile household equivalent. In other words, the richer the decile, the more they drink. That is a crude summary but it did amuse me.

As I noted, the Treasury analysis covers GST and the effect of economic benefits in kind. There was some commentary at the time of last year’s High Wealth Individual report that it wasn’t really quite fair because it didn’t take into account what the impact of GST and government benefits in kind. This is interesting to see, and I definitely recommend having a read of the note which is a reasonably easy read.

The Australian Tax Office raids the Exclusive Brethren’s business operations

And finally this week, a story coming out of Australia caught my eye about the Australian Tax Office (“the ATO”) raiding multiple premises associated with the global headquarters of Universal Business Team (UBT) on March 19th. UBT is a Sydney registered company that provides services and advicee to about 3000 exclusive Brethren owned businesses in 19 countries.

ATO investigators also apparently raided the head offices of a number of Brethren run companies, including OneSchool Global. In what would also be the standard procedure here, they confiscated phones, computers, documents and other materials. This was done as part of what the ATO call a “no notice raid”. Inland Revenue can do such raids as well, but the point is, it’s not done very often, and the fact that this has happened is extremely intriguing to see.

One of the things that I see frequently pop up in the comments of these transcripts, are questions/ pushback about charities having an exemption from tax on their business profits. It’s more complicated than that, but it’s there’s an obvious tension there. (Again thank you to all those who contribute, your comments are read even if I don’t always respond).

On this point I recall a discussion I had with the late Michael Cullen when he was chairing the last tax working group. During a roadshow event I asked him if there was anything which had surprised him during his role. He replied that he had been surprised by the scale of the charitable sector. He and the group had some concerns about whether in fact, all the charitable donations were being used for charity. In particular whether donations made under an exemption to an exempt business were in fact being used for a charitable purpose. The Tax Working Group’s final report noted:

“80. …the income tax exemption for charitable entities’ trading operations was perceived by some submitters to provide an unfair advantage over commercial entities’ trading operations.

81. notes, however, that the underlying issue is the extent to which charitable entities are accumulating surpluses rather than distributing or applying those surpluses for the benefit of their charitable activities.”

The Sunday Star Times asked Inland Revenue to comment on the ATO’s action but Inland Revenue just dropped a dead bat on it. But I would think, as the Sunday Star Times said, any information relating to New Zealand businesses that came into the ATO’s hands would proactively be passed on under the Convention on Mutual Administration Assistance and Tax Matters, part of the double tax agreement between Australia and New Zealand.

The scale of information exchange which goes on between tax authorities is very largely unknown, but it’s probably one of the most revolutionary changes to the tax landscape which has happened in the last five to 10 years. I don’t think we’ve yet seen anything like the impact that it will have.

Will Inland Revenue follow suit?

In summary the ATO clearly feels that it’s justified in launching a “No notice raid”. The question is whether Inland Revenue is considering something similar or is it just going to sit back and watch carefully? We don’t know, it won’t say, but you can be sure that it will be watching very closely to see what findings that come out of the ATO raid. If it does get anything interesting from the ATO, expect to see something similar happen here.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

In the 2010s the true extent of aggressive tax planning practices by tech giants like Apple, Google and Facebook emerged. These behemoths simultaneously piled up billions of dollars in tax havens, embedded their products ever deeper into our lives and shattered parts of the non-digital economy. It was also during this period that we personally, together with governments of both hues, willingly – if not always knowingly – gave up our sovereignty and free agency to these giants.

Uber stands as a poster child for the tech industry’s aggressive, and at worst frankly immoral business activities. It’s also the exemplar of why we cooperated in that loss of control.

Like other tech companies Uber established a network of subsidiaries in tax havens as part of its tax planning. But as the decade wore on initiatives such as the OECD’s Base Erosion and Profit Shifting (BEPS) and exchange of information work started to undermine the effectiveness of Uber’s tax structure.

In early 2019 Uber decided to fine-tune its tax planning by moving a subsidiary previously located in Bermuda to the Netherlands. This was in part in preparation for its initial public offering, but also in response to European moves cracking down on aggressive tax planning involving tax havens. As a result of the move, Uber reportedly created a US$6.1 billion Dutch tax deduction which it will be able to offset against future profits.

Uber’s transaction provoked questions in the Dutch parliament, prompting the state secretary of finance, Menno Snel (the equivalent of New Zealand’s revenue minister, Stuart Nash), to deny ever meeting any Uber representatives about the matter. Snel found out that Uber’s promises of jobs (it now has over a thousand employees in its Amsterdam office) come at a political cost.

Uber responded that it was “committed to openness and transparency with tax authorities around the world” and “faithful to both the letter and intent of the laws in the many jurisdictions where we operate.” Uber’s comments echo those of so many tech companies when challenged about their tax planning.

It will be no surprise to readers of Super Pumped: The Battle for Uber that Uber’s tax planning pushes the rules to breaking point. It’s the primary reason I refuse to use Uber.

I’m not alone in my distaste for such tax practices. New Zealand’s 2019 Tax Working Group in its final report commented: “The group has received many submissions about international taxation and the tax practices of multinational companies and digital firms. It is clear from the submissions that many people feel a deep sense of unfairness about the way in which the tax system deals with these firms. This is a worrying phenomenon: perceptions of unfairness have the potential to erode public support for the tax system as a whole.”

Although it’s easy to point the finger at Uber’s behaviour, at the same time it also illustrates how, despite apparently widespread public disdain for the aggressive tax planning activities of the tech sector, people continue to use their services.

For users the convenience and lower prices Uber offers outweigh any moral indignation about its tax and business practices. This is also true of other tech giants such as Apple, Amazon, Facebook and Google whose services and products are used by billions of people even as they facilitate live-streaming of mass-murder or pile up billions of dollars in tax havens. In effect, we love the sin but hate the sinner.

Exactly how much these tax practices cost New Zealanders isn’t clear. There is little public information available about the scale of the tech companies’ activities in this country let alone details of how much income tax they pay. Google, which has recently adopted “country-by-country” reporting as a means of giving more transparency to its results, did file financial statements for the year ended 31 December 2018. These show its income tax liability for the year was $398,341. (Intriguingly, the financials show the GST payable as of 31 December 2018 was $6,252,847 and that it owed over $81 million to an unnamed related party. I’ll leave you to guess where that might be located.)

By contrast, the last filed financial statements for the New Zealand subsidiaries of Facebook and Uber were for the year ended 31 December 2014. They, along with Mastercard and Visa, take advantage of Companies Office reporting requirements which only require overseas-owned subsidiaries to file financial statements if either their assets exceed $20 million or their total revenue is more than $10 million. Under the business model these companies appear to be using, the New Zealand subsidiary is usually paid a fee for “marketing” services provided to its parents. Unsurprisingly, these fees appear to be below the threshold for reporting.

The ability for the likes of Uber and Facebook to structure their affairs to minimise scrutiny is a direct result of a policy choice to put ease of business and lower compliance costs ahead of transparency. Apart from tax and a lack of transparency there are other downstream effects of that choice, namely a growing suspicion that New Zealand is a bit of an easy mark for money-launderers.

Even if the various OECD initiatives bear fruit and an international agreement is reached about the taxation of the digital economy, that will inevitably involve each government accepting a partial surrender of its sovereign taxing rights. This is particularly true of New Zealand because of our small size.

There’s a scene near the end of Danny Boyle’s Shallow Grave when Christopher Eccleston (an accountant) berates his flatmates Kerry Fox (New Zealand connection!) and Ewan McGregor (handsome journalist) for spending some of their ill-gotten gains. He warns them “That’s what you paid for it. We don’t know how much it cost.”

Similarly, although we pay little or nothing for Facebook, Google, Uber, Netflix and their ilk, the full cost to our society of a lower corporate tax take, oligopolistic business practices, a hollowed-out local media, toxic social media and the rise of fake news is still not clear.

Addressing the aggressive tax and oligopolistic practices of the tech companies requires addressing a complex set of linkages: Reversing the trend of the past 40 years towards looser regulation of businesses; determining an acceptable set of rules for international taxation which recognises the vast and relatively sudden economic changes brought by the arrival of the digital economy; and recognising our complicity in enabling this state of affairs. Over the coming decade who will demonstrate the courage to take on this challenge?