Could the US retaliate against a digital services tax?

Last week, in a series of interviews with the press, notably with Newstalk ZB, Finance Minister Nicola Willis dropped several hints about what might be in the forthcoming May 22nd Budget. In particular, she talked about the corporate tax rate, and the possibility of cuts to that as part of promoting the Government’s growth agenda.

Corporate tax rate above OECD average

Speaking with Heather Du Plessis-Allan, Ms Willis commented:

“Well, if you compare New Zealand with the rest of the world, we’re not as competitive as we used to be. Which is to say that our corporate tax level is reasonably high when you compare it to the rest of the developed world.”

This is a very valid point which comes up frequently in discussions. Our current company tax rate at 28% is well above the OECD average of 24% and has been out of alignment for some time.

New Zealand back in the late 80s under the Fourth Labour Government was actually at the forefront of cutting company tax rates. A particularly interesting action was to align the company tax rate with the top individual and trust rates of 33%. The three basically stayed in line until the election of the Fifth Labour Government and the increase in the top personal tax rate to 39% in 2000.

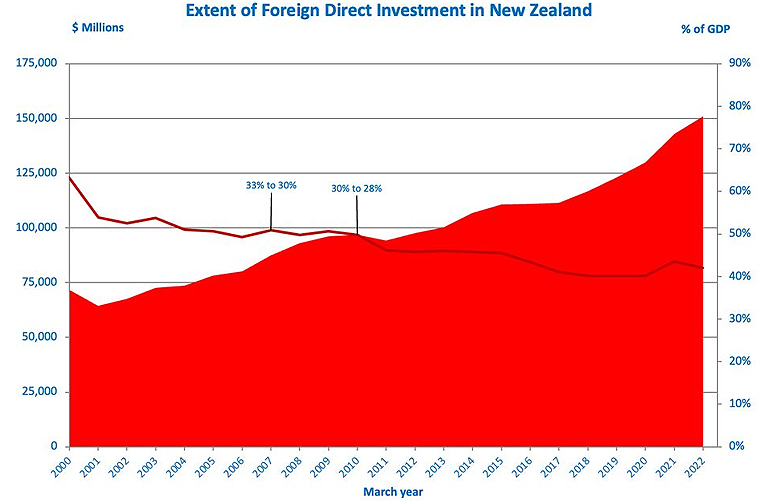

There have been a couple of corporate tax cuts over the past 15 years or so. In 2007, the rate was cut from 33% to 30% and then in 2010, as part of the rebalancing that took place under Bill English with the increase of GST from 12.5%, the corporate tax rate was cut to 28% where it remained since.

As I’ve discussed previously, there has been a long running global trend towards lower corporate tax rates. But that has slowed in recent years, first because of the effect of the Global Financial Crisis and secondly, the fiscal shock to government finances because of the COVID-19 pandemic. As a result, according to the OECD in 2023, corporate tax rates rose generally across the board. Nevertheless, we are out of sync at the headline rate level.

More to investment than the corporate tax rate and will it work?

A lower corporate tax is undoubtedly attractive. However, the tax rate needs to be seen in context with what other incentives are available. Overseas companies and investors are very focused on what else might be on the table. A lower company tax rate would certainly be attractive, so the suggestion has been met with enthusiasm by some. Others are a bit more sceptical. Economist Ed Miller noted that when the effect of the corporate tax cuts in 2007 and 2010 are considered there does not seem to be any significant increase in foreign direct investment as a result.

The last tax working group didn’t see overwhelming evidence to support the theory that lower tax cuts at lower corporate tax rate would attract investment.

Problems and an alternative

There’s a flip side to this though, and it’s tied into the Government’s intention of restoring a surplus. Our corporate tax rate is not only above the OECD average, but our corporate tax take is also high by world standards. According to OECD statistics, 14% of the total tax receipts in New Zealand for 2022 came from company tax, whereas around the OECD the average is 12%.

So, if the Government, in an attempt to boost economic growth, is going to cut the corporate tax rate, it must then look at other alternatives to replace the lost revenue. One of the things it did back in 2010 and which it has already repeated, was to remove depreciation on all buildings. Depreciation for commercial buildings was restored under Labour but then removed again from the start of the current tax year on 1st April 2024.

A counter argument to the Government’s proposal for corporate tax cuts would be that enhanced depreciation allowances, including restoration of commercial building depreciation, which would include factories, might be a more effective approach than across the board tax cut.

How to replace lost tax revenue?

But if the Government is thinking of a corporate tax cut, and that does seem to be the case, what counter measures could they take to ensure that it is not fiscally too draining on the resources? One option might be that the availability of imputation credits may be restricted. For example, it might be that you can elect to have a lower corporate tax rate, but you imputation credits are no longer available to for shareholders.

As an aside, imputation (sometimes called franking) credit regimes were very popular during the 1980s, but gradually fell out of favour over time, mainly because, or in part because the European Court ruled that imputation credits or franking credits have to be available to all shareholders resident in the EU. After the German government lost this case its response was to heavily restrict the use of franking credits.

Change the tax treatment of Portfolio Investment Entities?

Another option might be to review the taxation of portfolio investment entities held by persons with effective marginal tax rates above the 28%. To quickly recap, Portfolio Investment Entities (PIEs) have a tax rate of 28%, equal to the company tax rate, which is also the maximum prescribed investor rate for individuals. So, there is actually a tax saving opportunity for individuals whose other income is taxed above the 28% rate for PIEs.

The Government might look at this, decide that will no longer apply and instead income from PIEs will be taxed at the person’s marginal rate. That could raise sufficient sums to partially offset the effect of a lower corporate tax rate.

The Finance Minister also mentioned reforming the Foreign Investment Fund regime, which is currently being considered by Inland Revenue and made some encouraging sounds about that potentially being an option.

We shall see. No doubt there’s a lot of work going on in Treasury and Inland Revenue looking at these options. All will be revealed in the Budget on 22nd May.

A threat to our Digital Services Tax

As covered in our first podcast of the year, one of President Trump’s initial executive orders withdrew the United States from the OECD Two-Pillar international tax deal. I drew attention to the second paragraph of that Executive Order, which directed the US Treasury to consider taking actions against other jurisdictions for tax actions which are potentially prejudicial to American interests.

Vernon Small, who was an advisor to the former Minister of Revenue, David Parker, now writes a weekly column in the Sunday Star-Times has picked up on this point noting that “Treasury has budgeted to rake in $479 million between January 2026 and June 2029 from a 3% Digital Services Tax (DST) on tech giants like Google and Meta.”

This, according to Small, “is an heroic piece of forecasting given current uncertainties and the provision for delaying collections until 2030 if progress is made on a multilateral approach through the OECD.”

And then the crunch point:

“Trump has bosom buddies in high places in the industry with Elon Musk first amongst them, and Mark Zuckerberg making a play for the new US administration’s affections.

Trump has promised to retaliate against discriminatory or extra-territorial taxes aimed at US interests. So the DST could be a prime target.”

Vernon Small is underlining the potential threat to our revenue base and our sovereign right to tax. If the OECD deal does fall over there are a number of countries including Canada, no longer America’s best friend, it seems, with DSTs ready to go. So there’s a whole potential for a tax war.

The Trump threat to tax administration

But equally worryingly, coming out of the United States is something about the question of bureaucratic independence from the executive. This might sound an arcane issue but it’s actually quite important to the independence of tax authorities.

One of the first actions of the Trump administration was to sack 17 Federal Inspectors-general. There’s also a move to put all Federal Government employees on the basis that they serve at the pleasure of the President. This would mean that an employee could be fired without the need for cause as the American terminology puts it.

Project 2025’s Schedule F

The implications of this have been picked up by Francis Fukuyama, the author of the famous The End of History essay written in the wake of the collapse of the Soviet Union and the end of the Cold War.

Writing for the Persuasion Substack under the title Schedule F is Here (and it’s much worse than you thought) Fukuyama wrote:

‘ “For cause” protection means that the official cannot be removed except under specific and severe conditions, like committing a crime or behaving corruptly. And now many individuals have been moved, in effect, to Schedule F because they are said to serve at the pleasure of the President.

Consider what this may mean if Trump hand picks a new Internal Revenue Service chief, that individual can be pressured by the Government to order audits of journalists, CEOs, NGOs and NGO leaders. Removal of Inspectors General will cripple the public’s ability to hold his administration accountable.’

Trump’s decision to move all Federal employees to Schedule F status is a step towards autocracy. What perhaps we all need to keep in mind is that the separation between the Commissioner of Inland Revenue and the Minister of Revenue is actually incredibly important. Yes, at times the Inland Revenue might do something which probably might embarrass the Minister of Revenue, but he cannot directly intervene in Inland Revenue’s operations.

A key part of a well-functioning democracy is that civil servants can act independently from their nominally political superiors. Fukuyama is right to say we should therefore have some concern coming at what’s happening in, in the United States because it does seem to be centralising power very rapidly around the President. The .potential for mischief is therefore enhanced as a result, and don’t think that such a step ultimately doesn’t have tax consequences.

Latest on the changes to the United Kingdom ‘non-dom’ regime

On a more positive note, last year I discussed the changes to the so-called ‘non-dom’ regime in the United Kingdom. This is where persons who are not domiciled in the UK have a special basis of taxation. Basically, they’re not taxed on income and gains which are not remitted to the UK.

This is a significant concession which is ending with effect from 5th April this year when it will be replaced by something which is more akin to our transitional resident’s exemption. This is pretty important for the approximately 300,000 Britons like me who’ve migrated here, plus the significant number of Kiwis who have assets in the UK or family going to the UK but have retained assets here. All of this group are potentially within the scope of these reforms.

There’s been a fair amount of push back on the reforms together with concerns that there will be a flight effect as wealthy, ‘Non-doms’ leave the UK. The UK Labour Government has been under pressure to make some changes to the proposals.

In response, the Chancellor of the Exchequer (Finance Minister) Rachel Reeves announced a concession (ironically at the gathering of the super-wealth at Davos) which will increase what’s called the temporary repatriation concession.

This concession will allow non-doms a three year window to pay a temporary repatriation charge on designated foreign income and capital gains so that they can subsequently be remitted to the UK without any further tax. The temporary repatriation charge will initially be 12% before rising eventually to 15% in the year ended 5th April 2028. For comparison, without the concession remitted income would be taxed at rates up to 45% and remitted capital gains would be subject to capital gains tax at 24%.

There’s a lot of opportunity here for potential tax savings for those who could be affected or will be affected by the proposed change to the non-dom regime. We’re still working through all of the implications but we will be updating our clients and bringing you developments as they arise.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

More on UK trust filings, and why are there so many trusts in New Zealand?

Financing local government, time for change?

I’ll be honest, even after 30 years in New Zealand, I miss British budgets. There’s a building sense of anticipation beforehand, as rumours circulate about bold tax plans and the abolition/introduction of new measures. Then on the day itself, we have to deal with the myriad of tax measures introduced, usually always without any warning beforehand, other than leaks to selected media. Being perfectly cynical, they are handy work-creation events, much more so than their New Zealand counterparts. (That said this year’s May Budget here is looking like it will be the exception, which proves the rule).

This year’s UK Spring Budget, which was released on Wednesday night, did not disappoint. There were a whole raft of measures, some of which, to borrow the phrase the 1974 Lions adopted in South Africa against the Springboks involved “Getting your retaliation in first”. These measures were done simply to hamper what’s expected to be the next Labour government after Britain has its General Election sometime this year.

Ending the Remittance Basis of taxation

So, there’s a lot to consider, but there were two that are of particular interest to New Zealanders, and these are to do with the so-called non-dom rules. The UK has a special set of rules called The Remittance Basis of Taxation for non-domiciled persons. That is people, generally speaking, born outside the UK, and they are able to basically exempt their non-UK sourced income from UK taxation, if they don’t remit it to the UK.

These rules have been around for a long time and there has been a lot of amendments in recent years. And I suspect there is a fair bit of non-compliance going on from people here in New Zealand, who’ve not kept up with those changes.

The UK Labour Party had indicated it would remove the regime as a fundraising measure. Instead, the Conservative Chancellor of the Exchequer, (Finance Minister), Jeremy Hunt, has gone ahead and decided to pre-empt that by abolishing the regime with effect from 6th April 2025. It will be replaced by a regime which looks very similar to the transitional residence exemption we have here. That is, individuals will not pay UK tax on foreign income and capital gains for the first four years of UK tax residence.

There will be some transitional rules which will apply to existing individuals who are claiming the remittance basis. You can claim remittance basis for up to 15 years, but after a period of ten years you have to start paying a Remittance Basis Charge of £50,000. And then after 15 years of tax residency in the UK, you’re deemed to be domiciled in the UK and the exemption no longer applies. It’s long been a very controversial measure. The wife of the present Prime Minister, Rishi Sunak, is apparently a non-dom and questions have always been asked about whether she made use of that exemption as she comes from an incredibly wealthy family.

I’ve got a number of clients moving across to the UK, or who are all already there, and we’re looking at the question of how to manage the implications of becoming UK tax residents. So, this proposal is interesting to see. More details will emerge, obviously over time, but it is significant in that it will perhaps make it a little easier for people to migrate to the UK without triggering huge tax liabilities or having to manage them extremely carefully under the remittance basis regime.

Domicile and Inheritance Tax – good news for Kiwis & UK migrants?

Related to the end of the remittance basis regime and arguably even more important, are changes to the UK’s Inheritance Tax (IHT) regime. IHT is a unified estate and gift duties, and probably should be still what it was originally called Capital Transfer Tax. At present, IHT applies to all assets situated in the UK or all assets worldwide if the person is domiciled in the UK.

The proposal is that those current rules will also be replaced from 6th April 2025 with a residency-based set of rules which will probably involve a ten-year exemption period for new arrivals and then a ten-year tail provision for those who leave the UK and become non-resident. What that tail provision may mean is that someone who’s been resident or domiciled meets the test for IHT, may have to be non-resident for ten years to escape the full effect of it.

Now, in my experience, the impact of IHT on Kiwis who’ve been over in the UK or have assets in the UK, and then Brits like myself, who’ve migrated here, is not very well understood. But as the Baby Boomer and older generations are starting to pass away now, there’s a great transfer of wealth going on. The amount of IHT that the UK government is collecting is steadily rising. It’s now up to over £7 billion a year (0.3% of GDP, about $1.2 billion in New Zealand terms), steadily heading towards 0.5% of GDP. So, it’s starting to become a more significant part of the tax take.

These new rules may mean that people who have previously been caught in the regime will be out of it, but it may also mean that people who thought they were outside the regime may be caught. There’s no indication here that the rates that apply – 40% on estates worth more than £325,000 pounds or $650,000 thereabouts – have been changed. It’s a tax that people feel needs reform in that there is plenty of scope for mitigating it. It falls very heavily on relatively smaller states rather than the larger estates where they have the wealth to do some more estate planning.

More tax breaks for the film industry – a lesson for the Government?

And incidentally, just before moving on, I notice this budget also contains a number of measures to promote the UK film industry and theatre as well as the arts. These will provide over £1 billion in additional tax relief over the next five years. One of the things that’s common amongst tax systems around the world is support for the film industry, and the film industry as a whole is pretty cynical about going to where the best incentives are.

I think it’d be interesting to see just how the Coalition Government responds in the May budget about pressures mounting on the Screen Production Rebate, whether that’s going to continue in its present form. The industry here will be lobbying for it to continue because although we can’t compete with more generous exemptions that may be provided elsewhere, the rebate still provides the skills that have been built up here thanks to the likes of Weta Workshop and others which makes New Zealand skills still highly sought after. The Screen Production Rebate is the little kicker which helps get the deals across the line.

More on UK trust statistics and a warning about the perils of overseas trustees

Larger estates in the UK will undertake a fair amount of mitigation to minimise the impact of Inheritance Tax, and that invariably tends to involve the use of offshore trusts. I mentioned in last week’s podcast the extraordinary fact that in absolute terms more tax returns are filed in New Zealand for trusts than in the UK.

This provoked a lively debate in the comments section with some pointing out the UK numbers don’t really reflect trusts that have been set up to go offshore into tax havens such as the Caymans and the Isle of Man. Well yes, that’s right, the UK numbers don’t reflect this because trusts’ tax returns, for UK purposes are generally required to file tax returns based on the residency of the trustees.

That by the way, is a matter people here need to pay more attention to. If a beneficiary or trustee migrates to the UK, this may inadvertently make a New Zealand trust with New Zealand assets subject to UK taxation. Again, this is another matter which isn’t well understood, and I suspect there’s a fair bit of noncompliance going on.

The UK also has a Trusts Registration Service. This was in response to the EU’s Fifth Anti-Money Laundering Directive from 2017, which the UK went ahead and implemented despite Brexit. The UK actually went in for a tighter regime than the EU had proposed. According to the same statistics that the HMRC held about trust tax return filings in the UK, the Trust Registration Service had 633,000 trusts and estates registered as of 31st March 2023 and which remain open as of 31st August 2023. This includes 462,000 new registrations in the 12-months to 31st March.

This surge in registrations is the result of a compliance effort by HMRC to remind people around the world that if any trust has a property in the UK, or even has made loans to beneficiaries in the UK, it may have a UK tax liability, and therefore should register under the Tax Trust Registration Service. This is regardless of where the trustees are tax resident. And again, I suspect there is a fair bit of non-compliance here.

Why are there so many trusts in New Zealand?

But even if you take these greater numbers, we’re still left with the rather astonishing fact that per capita large number of trusts in New Zealand relative to the population. How did that evolve was one of the questions asked in the comments. The short answer would be that the effective abolition of Estate Duty in late 1992 removed the impediments to setting up trusts. What we saw in response was something quite unusual in trust law, where it was now quite possible for a single person to be the settlor (or the person who settles property on the trust), a trustee responsible for managing the property, and a beneficiary. This is very unusual in trust law terms around the world.

I think it has to be said that some lawyers and other practitioners took advantage of that opportunity to market themselves and trusts extremely well. Back in the early 1990s, by putting assets in trusts it was possible to mitigate against the impact of rest home charges. The income of trusts was not then taken into account when determining eligibility for the likes of Working for Families or student allowances.

All that has changed over time and my view is that a substantial number of the estimated 500,000 trusts that we have in New Zealand are no longer necessary. That’s also the view of many other practitioners in this space. So it will be interesting to see what happens over time as people realise the complexities of using trusts and the inadvertent tax issues that are created when trustees, beneficiaries or settlors move to another jurisdiction.

Since the start of the year, I’ve seen an upsurge in requests for advice in relation to trustees, beneficiaries or settlers moving to the UK or making distributions to the UK.

I don’t expect that to slow down, and I think it’s actually the tip of the iceberg.

Beware the information exchanges

I would also add that probably because of the common reporting standards and the automatic exchange of information as various tax authorities work their way through all that information that’s being accumulated and distributed around the world, they will be realising that they many trusts are non-compliant, accidentally or not, and they’ll be starting to crack down on it.

Local government finances, time for reform?

Finally this week, local governments are now looking to set their rates for the forthcoming 2024-25 year. The fact that no replacement for Three Waters has been found and the substantial infrastructure deficit we as a country have allowed to develop, means that rates are likely to be rising quite significantly for many of us. That’s obviously going to generate some pushback.

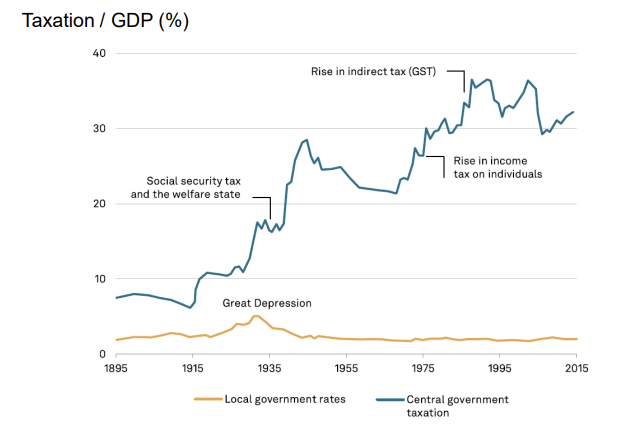

Writing on this topic Dan Brunskill noted the quite astonishing stat that local government rates have basically not increased as a percentage of the economy in the past hundred years.

Basically, local rates have stuck around about 2% of GDP overall across the country about $8 billion in rates are paid. (Not all that you pay to a Council is actually rates based on property values, there’s also the Uniform Annual General Charge together with the various services such as consent fees that councils charge).

As the graph illustrates, apart from the spike around the Great Depression period, when councils and central governments all did more to try and help alleviate the impact of that, rates as a percentage of GDP have been stable for well-nigh 90 years. I think the present rating present funding of councils is unsustainable, because, as the article notes, central governments keep giving local governments more and more to do, but restrict them in the level of income that they can raise. That’s both good and bad. We don’t want what happened with Kaipara District Council, which essentially went bankrupt because it could not fund a wastewater system in Mangawhai.

There’s scope for reform in this space. I think the crunch points around finance are arriving now and local and central government will need to think harder about how local government can be funded and what funding mechanisms are appropriate. For small councils such as Kaipara or, Waiora over near Tairawhiti East Coast, the funding issues and scope for raising funds are not the same as for Auckland a council with a rating base of over a trillion dollars. The laws need to change in my view, but we’ll have to wait and see developments.

As always, we will bring those to you when they happen. And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Thousands here could be potentially subject to UK Inheritance Tax.

Airbnb and Uber are not happy about a GST law change.

GST for all its complexities, is the best example of the Broad Base Low-Rate tax principle, a single rate of 15% applied broadly. However, one of the ongoing controversies with GST is around its application to food and other basic necessities. New Zealand’s approach is at odds with many other countries, such as Australia or the UK, where food is not subject to GST (or VAT, as the UK calls it).

Frequently we see commentary that it would be a good move to help lower income earners by removing GST on food. This has been suggested as a response to the current cost of living crisis. I am opposed to such moves and many GST specialists are also in the same camp. Firstly, I don’t think this move is effective as proponents believe, and secondly, if the issue being addressed is low income, then it is better, in my view, to give more income to that target group rather than using a tax measure which would benefit more people, including some who we probably think don’t need assistance.

A report released yesterday in the UK regarding the impact of the withdrawal of the so-called tampon tax bears out these concerns of myself and other GST specialists about introducing GST exemptions. In the UK, VAT of 5% used to apply to tampons and other menstrual products until January 2021, when it was abolished. Prior to its abolition, VAT specialists predicted that the full benefit of abolition would not be reflected in lower prices. And a report by Tax Policy Associates bears this fear out. According to the report, at least 80% of the savings from the tax savings was retained by retailers. In fact the report questions whether any of the benefit of the removal of VAT ever passed through to lower prices.

Professor Rita de la Feria the chair of tax law at the University of Leeds was one of those who warned beforehand of this likely outcome. Commenting on the report she noted this was not only predictable but predicted. In her view “we have to stop confusing policy aim with policy instrument and we also need to stop using tax policy instruments to signal we care about the policy aim.”

Those are wise words and should be kept in mind next time you hear calls for tax changes for ostensibly very sensible reasons. In tax, even with well-meaning policy, there are always unintended consequences and tax is not always the most appropriate mechanism. Sometimes direct action, such as giving payments to those affected, or supplying tampons for free is the best approach.

How UK tax law applies to NZ residents

Staying in the UK, next week the latest Chancellor of the Exchequer, Jeremy Hunt, Grant Robertson’s equivalent, will be presenting the Autumn Statement. He is expected to introduce a number of tax changes and tax increases in an effort to try and restore the UK’s finances. Hunt, incidentally, is the fourth chancellor this year, whereas Grant Robertson is only the fourth New Zealand finance minister this century. So that gives you a measure of just how much upheaval has been going on up there.

I regularly advise New Zealanders and migrants from the UK about UK tax matters. Frequently there are ongoing issues for them and inevitably complexities creep in.

Based on my experience, there are probably thousands of New Zealanders and family trusts who may unwittingly have UK tax obligations. There are also former residents from the UK who are now living here who misunderstand the relationship between the UK and New Zealand tax treatments of investments. So here’s a quick summary of those people who may be affected by UK tax and the differing tax rules between New Zealand and the UK.

Firstly, if you have property in the UK, then UK capital gains tax will apply to any disposals. There are strict timelines about reporting those disposals which are unrealistic in my view, but they still apply. CGT will apply even though the disposal might not be taxable for New Zealand purposes. By the way, the bright line test does apply to overseas property.

If you were renting a property out in the UK then you must report that income both in the UK and in New Zealand. However, for New Zealand purposes, any UK tax paid will be given as a credit against your New Zealand tax payable.

As should be well-known transfers of, or withdrawals from UK pension schemes are subject to New Zealand income tax. I don’t agree with that policy but it’s the law. In addition, if you are receiving a pension from the UK then the UK pension scheme should not be deducting any PAYE. You will need to apply to H.M. Revenue and Customs through Inland Revenue to get any refund of any such tax deducted. By the way, Inland Revenue will not give you a credit for any tax deducted, it wants the tax paid here. That’s the procedure under the double tax treaty and you’ll have to go and get the PAYE back off HMRC, which can be a very frustrating experience, believe me.

But potentially the most significant tax that will apply, which is also the least known, is Inheritance Tax. Inheritance Tax applies firstly to any assets situated in the UK. So, if a New Zealander who worked over in London, bought an investment property there before moving back here, that property is in the UK Inheritance Tax net.

Secondly Inheritance Tax also applies on a global basis to all assets wherever they’re situated if you are “domiciled” or deemed to be domiciled in the UK. Domicile is a complicated concept which I am not going to get into now. But basically, pretty much anyone born in the UK who’s migrated here in the last ten years or so probably still is domiciled for UK tax purposes. If you were a Kiwi and you spent more than 15 years in the UK, you may also be deemed to be domiciled in the UK. If so, Inheritance Tax applies at a rate of 40% on all assets over the first £325,000. (The price of New Zealand property means that this threshold is comfortably exceeded).

In my experience, many migrants and returning Kiwis are completely unaware of the potential impact of Inheritance Tax. For example, UK Inheritance Tax law does not recognise de facto relationships (apparently much to the relief of several politicians a partner in a London law firm once told me). I once dealt with a scenario where the New Zealand resident survivor of an unmarried couple had to pay over £50,000 of Inheritance Tax on her share of a jointly owned New Zealand property after her Scottish partner’s death.

Finally, the UK has a trust register which arrived in the wake of anti-money laundering legislation and its use has been greatly expanded. Any trust which has property in the UK must register. Furthermore, any trust which has a UK source of income such as bank interest must register if it has beneficiaries, including discretionary beneficiaries who are resident in the UK. This is a common scenario I’ve seen. It appears this registration requirement applies even if no distributions have ever been made to the UK situated beneficiaries. There’s some controversy about that particular provision because it appears New Zealand trusts may even have to file UK tax returns even if all the UK income is being distributed to New Zealand beneficiaries.

So that’s a quick summary of some of the UK tax issues which I commonly encounter. I’ll look to update this summary next week if there are any developments from the Chancellor’s Autumn Statement. Now is maybe time to have a look at your position to see if, in fact, you might potentially have a UK tax issue. And also keep in mind that Inland Revenue is currently running an initiative where it is checking on people’s potential tax obligations from their overseas investments.

“We want to remain tax-free”

Finally, this week and back to GST, Airbnb made a submission to Parliament’s Financial Expenditure Select Committee complaining about the proposal for it to charge GST on all accommodation bookings made through its platform.

In its submission, it warned this would stifle the country’s economic recovery and cost the economy up to $500 million a year.

Now this measure was introduced in the Taxation (Annual Rates for 2022-23, Platform Economy, and Remedial Matters) Bill (No 2). Airbnb along with Uber, also affected by the new proposals, unsurprisingly, think the law changes are unfair. On the other hand, the Hospitality Association was amongst those submitting in favour of the change. Chief executive Julie White said a third of its membership consists of commercial accommodation providers adding “and a consistent frustration of theirs is a lack of level playing field when it comes to services like Airbnb”.

The comments from Uber and Airbnb are unsurprising to me. But what I did find of interest about the bill was there have been quite a considerable number of submissions made 820 so far, and quite a few from individuals who would be affected. To quote one, “this law change will result in fewer bookings to me and significantly impact my retirement plans. This will have the additional impact of higher costs of vacations for New Zealand families who are largely for larger families and cannot afford to stay in a hotel.”

Another submitter thought “This action will have a huge negative impact on a new form of tourism at a very personal, localised level.” I’m personally not sure that the impact will be quite as dramatic as those submitters suggest, but it is interesting to see the reaction to what might be seen as a relatively straightforward GST proposal.

As is often the case, many other submitters took the opportunity to push for other changes, such as several suggesting for the removal of FBT on the provision e-bikes to employees.

There was also criticism of the complexity of the interest,limitation and bright-line test rules. One submitter noted that the commentary to the bill had more than 28 pages devoted to remedial provisions for this legislation, and he concluded correctly, in my view, “it is simply not appropriate to expect most landlords to be able to apply the detail of tax law of this complexity.”

Incidentally, the same submitter suggested that because the interest limitation measures had been introduced partly in response to rising house prices, now house prices were falling logically the interest limitation measures should be repealed. It’s a fair point, and he wasn’t the only one to make it. But somehow I can’t see that happening. To leave off where we came in this is another situation where the policy aim and policy instruments have got confused.

What are the “Unknown unknowns” of tax? Our 3 stories from the week in tax

The financial arrangements regime and Inheritance Tax

Wage theft and missing PAYE and KiwiSaver contributions

National’s tax policy – indexing thresholds, changes to the bright-line test and loss ring-fencing

Podcast transcript

In February 2002, in the run up to the invasion of Iraq, then U S Secretary of Defense, Donald Rumsfeld, commented;

“Reports that say that something has happened are always interesting to me because as we know there are known unknowns. There are things we know we know. We also know there are known unknowns. That is to say we know there are some things we do not know, but there are also unknown unknowns. The ones we don’t know, we don’t know and if one looks throughout the history of our country and other free countries, it is the latter category that tend to be the difficult ones.“

This quote was a core theme in my presentation last week to the Financial Advice New Zealand annual conference. The unknown unknowns are also a very difficult category in tax. And what are these unknown unknowns? The ones that trip up people because they didn’t know they were there.

Well in New Zealand the biggest culprit in this would be our financial arrangement rules. These rules have been around since 1986 and yet despite their very broad application, are largely unknown. I have come across CFOs who were completely unaware how they could apply.

Financial arrangements rules apply to just about any financial instrument you can think of. Mortgages, bank term deposit accounts, swaps, bonds, gilts in the UK phrase, all those all caught within it. It’s so broad it could apply to season tickets for public transport. And in one case I dealt with we thought that electricity contracts would be caught. Actually, we were debating whether in fact they were in the stock rules or in financial arrangement rules. Welcome to the arcane world of international tax.

But the financial arrangement rules are very broadly, largely unknown to individuals and they have particular bite in the foreign exchange field. That is where exchange rate movements such as is going on right now with Brexit which is back in the news again, so the Pound will move around.

Two groups of people get caught here. Obviously, investors who have bonds or term deposits denominated in an overseas currency, the value of the New Zealand dollar falls [that is more dollars are required to buy the offshore currency], they make an exchange gain and if the value rises, they have an exchange loss.

Then there are those with, for example, a rental property in the United Kingdom, and they have a mortgage there, it works the opposite way. The Pound may become weaker against the dollar so that in dollar terms, their mortgage diminishes, then that is income. Now on an unrealised basis for most people, this largely doesn’t matter, but very abrupt movements which add up to $40,000 on an unrealised basis will pull people into the foreign financial arrangements regime and they then will have to pay tax on unrealised gains.

The classic example I encountered was a client who had substantial property interests and mortgages in the UK. In year one there was an unrealised $300,000 foreign exchange gain, on the movement on the Sterling and had to cough up $100,000 in tax. The following year, it moved back the other way and she had a $300,000 loss but she never got that tax back. Even though there’s a wash up calculation when an arrangement matures or a mortgage rolls over and so of all the unders and overs are taken into account. But if you paid tax too soon in the piece, say you paid tax two years ago and then you find out that you actually never made any gain once everything is all closed out, you’ll never get the tax back. It’s one of the harsher parts of the financial arrangements regime.

The other trap is that the arrangements regime will apply to people who have total financial arrangements of $1 million or more and that is a gross amount. What I sometimes see is people may have $500,000 of term deposits and $500,000 of mortgages overseas mortgages and they think that after netting the two off, I’m below the threshold for the regime. Economically, your net worth comes out as nil. But financial arrangements regime takes them in aggregate so therefore the two are added together so the person actually has a million dollars in financial arrangements and is therefore within the accrual part of the regime. That person will be taxed on an unrealised basis.

The financial arrangements regime just the most common trap New Zealand advisors and clients fall into in my experience.

Following on from that, the other area that I’m seeing a lot more of is UK inheritance tax. Inheritance Tax is an estate and gift tax that applies to anyone domiciled in the UK or with assets in the UK.

Domicile, without getting in to too much detail, is a complicated concept, but basically, it’s where your permanent attachments are. I spoke in a previous podcast earlier about the unfortunate New Zealand woman whose Scottish partner died and because they weren’t married, she finished up paying £50,000 pounds inheritance tax on the transfer of his interest in the New Zealand property to her. So that’s not the first trap to watch for.

And I’m seeing more and more people caught by this, we have 300,000 Britons in the country. People like me, who’ve come from Britain, many more still have assets over in the UK. Maybe their children are going backwards and forwards to the UK and working there. And they’re all potentially all caught up in the inheritance tax regime.

A common thing that often gets overlooked is the implication of having assets in the UK or burial plots. Famously after Richard Burton died in 1984 the then HM Inspector of Taxes nailed his estate for inheritance tax on the basis that he had retained a burial plot in the village in Wales from which he came. So that was a very expensive burial plot as it turned out. I believe he actually is buried in Switzerland, but that’s how arcane the rules around inheritance tax are. It is the great unknown unknown. And as Donald Rumsfeld said, “These unknown unknowns tend to be the difficult ones.”

Earlier this week, Andrea Black who runs the excellent blog “Let’s Talk About Tax” went drinking with some young people. Actually, she was there to advise a group of hospitality workers who had been caught out as a result of Wagamama going into receivership. And the issue they were talking about is what’s called wage theft in the hospitality industry.

This is where the company, an employer, goes bust owing employees thousands of dollars in unpaid wages and salaries. There is often also a lot of unpaid pay as you earn floating around. There are several issues here. First and foremost, the employees have been left out of pocket and so they want to know what’s going on and when they can recover that. Then the tax man is very much often out of pocket. It often emerges that pay as you earn has been unpaid for several months an issue which I’ve seen this, and which Andrea talks about it as well.

You do wonder how quickly Inland Revenue reacts to this. Now I do hope that one of the things that will come out of Inland Revenue’s business transformation is much swifter responses to issues where pay as you earn falls into arears. My experience is Inland Revenue has let this go on for far too long. I’ve come across instances where there had been unpaid pay as you earn for going on for four years, which is just an absurd position. Someone there is either deliberately playing the system, in which case they should be hit with the full force of the law or is so hopelessly incompetent they should have been put out of their misery long ago.

Now the other thing that also comes into play for the employees is the unpaid employer KiwiSaver contribution and this adds up to quite a bit. Back in 2016 I spoke to Radio New Zealand about this matter.

At that time there was over $29 million dollars in outstanding KiwiSaver payments. In June 2015 1,663 employers had failed to pass on 15.3 million dollars in KiwiSaver payments deducted from employee’s salaries. Employees are missing out on this and on the employer contributions and it’s a real issue within the industry. Andrea asks whether the Small Business Council looked at this issue. We’ve delivered our report to the Minister and what I can say this matter did come into discussion during our deliberations.

It covers a number of matters. One is the question that we talked about previously about people with the incorrect prescribed investor rate. There’s also provisions making it easy for Inland Revenue to collect unpaid employer contributions in relation to KiwiSaver and ensuring employers pass on the employee contribution to Inland Revenue.

Hopefully employees will get the investment returns they’re missing out on because they haven’t been paid or the deductions and employer contributions haven’t yet hit their KiwiSaver account. By the way, submissions on that bill close on Monday so you’ve still got a chance to make a submission in support of that or raising other issues.

Finally, National have released their tax policy for next year. A number of things they are promising include tax cuts. Particularly they’re proposing something which I think is long overdue, and that is indexing tax thresholds. I think this is one of those quite sneaky tax increases that causes bracket creep and pushes people up into higher tax brackets gradually and it’s something which is effectively a tax increase by stealth. I think in the interest of transparency it’s a good move.

There’s a number of interesting other matters they want to deal with. That said, I’m not entirely sure if you are not a homeowner or rental investor and you’re trying to get into the investment property or to rent a property you’d appreciate what they’re proposing. They want to dial back the bright line test for residential property from five years to two years and remove loss ring fencing, which is a big break for tax investors.

That brought a fairly forthright denunciation from Jenée Tibshraeny. She also was less than impressed by the idea of removing the inflation component of interest. It’s an arcane point which has been talked about for some time which although it sounds arcane it is actually quite important.

Anyway, that will be the first shots fired in next year’s election about tax policy. All eyes will be on what the coalition will do in next year’s Budget. Given that tax thresholds haven’t been raised for more than 10 years by that time it’s hard to imagine that they wouldn’t try and do something, particularly when they’re running a surplus. I mean, cynical tax cutting budgets are not just the preserve of right wing governments. But we shall wait and see.