The Climate Commission and COP28.

- A useful suggestion from the UK on taxing EVs

- An interesting case on staff retention payments

- Another tax case shows how not to use ChatGPT

- What’s the character of the year?

The United Nations Conference on Climate Change, COP 28, has just wrapped up in Dubai. The current Minister of Revenue, Simon Watts, is also the Minister of Climate Change so he attended the conference on behalf of the Government. There has been a lot of debate about how far COP28 has moved change forward although an agreement was finally reached on beginning a phase out of fossil fuels.

Now, coincidentally, or maybe not, as COP 28 was ongoing, the Climate Commission released its final advice to inform the Government’s plan to meet Aotearoa New Zealand’s greenhouse gas reduction goal for 2026–2030.

Briefly, the report says that the Government needs to take active steps to encourage change by removing barriers and supporting investment that cuts climate pollution. The Commission’s analysis is the country has made progress, but it is not on track to meet its climate goals for the end of this decade. In the Commission’s view, that means that we will be missing out on benefits like new jobs, a more resilient economy and healthier communities.

In all there are 27 recommendations which are focused on areas where the Commission sees there are critical gaps in action or where efforts need to be strengthened or accelerated. A couple of these are encouraging households and business to switch to electric vehicles and making it easier for more people to choose public or active transport. Key thing here which I think everybody would agree with, is sorting out the roles of the Emissions Trading Scheme and forests in achieving these objectives.

The paper, all 193 pages of it, does refer to tax being one of the tools to be used. For example,

“To support the transition to a low emissions economy, incentives need to be designed to overcome near-term capital constraints to businesses shifting their existing assets and processes to low emissions alternatives. To support this, the Government could explore amending components of the tax system (for example, adjusting depreciation schedules and rates for eligible projects).”

Overall, the Commission has no specific tax suggestions beyond such general suggestions.

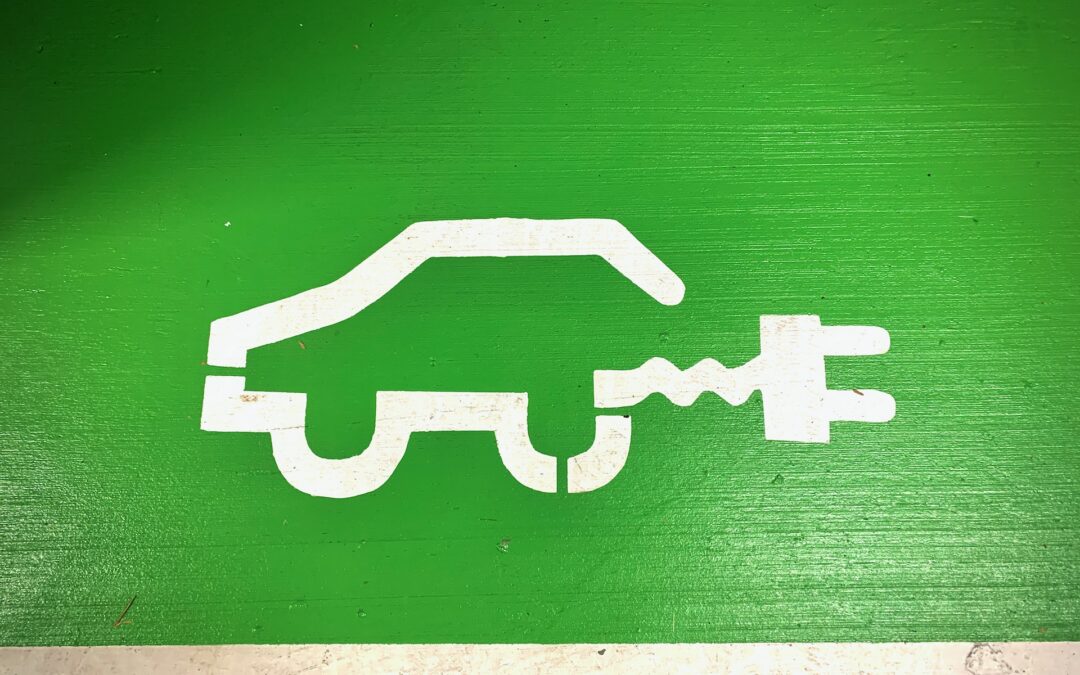

Replacing the Ute Tax – a UK suggestion

As it happens, this week the Government repealed what it called the Ute tax and with it the current clean car discount scheme, which seems at odds with the report of the Climate Commission. In the Government’s Coalition Agreements, there was a proposal from ACT for “Work to replace fuel excise taxes with electronic road user charging for all vehicles, starting with electric vehicles.”

Now that also seems at first sight to be contrary to the Climate Commission’s recommendations for reducing emissions. But this week I came across a major report on the UK economy called “Ending stagnation. A new economic strategy for Britain”. This has been produced by The Economy 2030 Inquiry.

The TL:DR (too long: didn’t read) of this 293-page report is that Britain is in a far bigger mess than we might appreciate, and Brexit has done nothing to improve its position. The report has a whole heap of recommendations, including, inevitably, suggestions around changing the tax system which is what attracted my initial interest. I’m always interested to see what’s going on around the world and what goes on in Britain affects quite a large number of people here, either expat Brits or Kiwis who have family in the UK. I have several cases on the go at the moment involving UK New Zealand tax matters.

The report suggests one of the major challenges the UK economy faces is a transition to Net Zero. Which is also a challenge we face. As part of this the report makes the following suggestion:

“Our tax system also needs to keep pace with net zero transition. To ensure the burden of motoring taxes does not fall on poorer households yet to switch to electric vehicles, a 6 pence per mile charge (equivalent to fuel duty), should be introduced for [electric vehicles].”

Viewed in this context and stepping back from the emotions around the repeal of the Clean Car Discount, ACT’s proposal makes sense. Encouraging people to take up EVs is what we want to do long term. But that doesn’t mean those people should have a free pass indefinitely. EVs will soon be subject to road user charges which would be similar to this UK proposal. Therefore charging EVs some form of charge is not unreasonable.

My philosophy around environmental taxes is that the revenue from any such fund raising measures should not go into the general pool of taxation, but instead be ring fenced and applied for environmental measures. In this case my belief is those funds could be used to assist people to swap out older cars into newer cars. Those newer cars may still use fossil fuels, but they will be more fuel efficient, and that’s a worthwhile goal because it does reduce the motoring burden and emissions.

Time for a land tax and “mild increases” in tax revenues?

Incidentally the Economy2030 inquiry report specifically references our post 1984 economic transformation and how we dealt with the change involved in major economic reforms. Given Britain is pretty much in a huge hole and needs to change dramatically, the report looks at how we managed our transition post 1984. As part of that, a separate paper was prepared for the Inquiry by the former Reserve Bank of New Zealand Chair Arthur Grimes.

Incidentally, and in what’s becoming something of a trend for the new Government, Mr. Grimes’ paper makes suggestions contrary to the Government’s actions and intentions. Specifically, around tax breaks for owner-occupied rental housing, his report notes the current policies “increase wealth inequity.” He also believes a “mild increase in tax revenues will eventually be needed”. His suggestion is for “broadening the range of taxes to include a land tax, the most efficient and (vertically) equitable tax available to the Government, should be considered.” I can hear Raf Manji and the members of TOP cheering at this.

Anyway, there’s a lot to read in Arthur Grimes’ paper. I think it’s a good summary of what we went through and how our experience is relevant for other economies.

The deductibility of staff retention payments

Inland Revenue released an interesting Technical Decision Summary about payments made to retain key staff as part of a sale of a company. What happened was the company was being readied for sale and as part of this process the company entered into retention agreements with key staff. These were variations to their current employment agreements which entitled the key staff to bonus payments calculated by reference to their salaries.

And the idea was to incentivise these key employees to remain with the company to enable the ongoing smooth running of the company during the sale process. The payments were made prior to completion of the sale and were conditional on the employees remaining continuously employed by the company on the relevant payment dates.

The company in this case considered a portion of the retention payments were capital and therefore non-deductible because they were part of a capital transaction being the sale of the business. The case finished up before the Tax Counsel Office and its Adjudication Unit which decided that in fact the retention payments could be deductible in full as the capital limitation did not apply.

This is a very fact specific case which is often the case with Technical Decision Summaries. However, they do give insights into how Inland Revenue might approach a particular case. Bear in mind each is very heavily contingent on the facts. Nevertheless this is an interesting one which turned out to be a good result for the taxpayer.

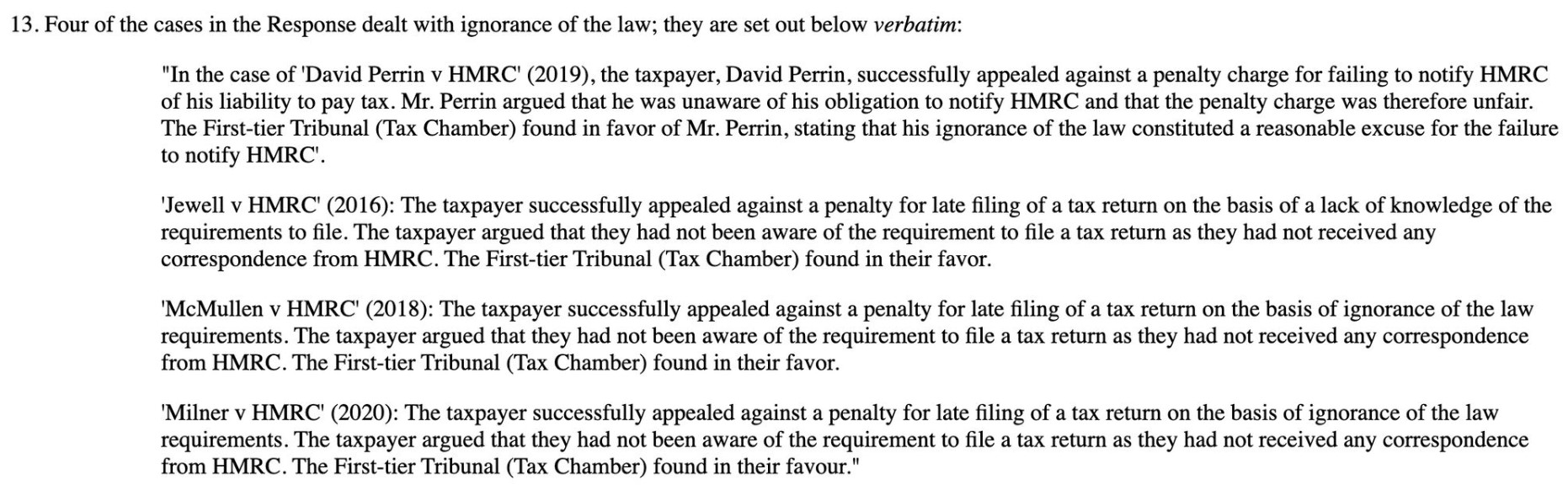

HM Revenue & Customs One – ChatGPT Nil

On the other hand, it did not go well for one Mrs Harber over in the UK who in her appeal against various HM Revenue and Customs (HMRC) assessments used ChatGPT as part of her research.

She then presented these “cases” in evidence.

Unfortunately for Mrs Harber none of these cases were real, ChatGPT in its enthusiasm had just simply dreamed them up, and Mrs. Harber hadn’t realised this.

In fact, she asked the tribunal how it could be confident that the cases relied on by HMRC were genuine. The tribunal pointed out that HMRC had provided the full copy of each of those judgments and not merely simply a summary as she had done, and the judgments were also available on publicly accessible websites. Mrs. Harber had not been aware of those websites.

She obviously lost the case, but the Tribunal generally took her approach as more of misunderstanding her obligations so did not penalise over heavily in terms of costs, awards. But it is an interesting commentary on the perils of making use of ChatGPT and the need to have discernment.

WorkRide FBT exemption update

Last week I discussed the WorkRide Product Ruling Inland Revenue had issued which would give an FBT exemption to employers providing E scooters, E bikes and the like. I originally stated there’s a cost limit of $4,000.

Subsequently a couple of people contacted me and asked if that limit was correct. It’s not. I was actually referencing a submission I’d made to the Finance and Expenditure Committee proposing a FBT exemption. In fact, the limit will be set by regulation, but that limit has not yet been passed nearly nine months after the relevant legislation was passed. It’s expected by the way the limit will be higher than the $4,000 sum I mentioned. My apologies for the confusion.

What’s the character of the year?

Finally, what is the character of this year? It turns out that in Japan it is a tradition to decide the character (kanji) of the year in mid-December. Over in England, Professor Rita de la Feria the chair of tax law at the University of Leeds, heard from a student that the kanji for 2023 has just been announced and it is 税, or “tax”.

On that bombshell, that’s all for this week. Next week in our final podcast for 2023 we’ll be reporting on the Half Year Economic and Fiscal Update and the accompanying Mini-Budget.

Until then, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.