Podcast special with Shamubeel Eaqub analysing Inland Revenue’s high wealth individuals report

- This week I’m joined by Shamubeel Eaqub, a partner at the boutique economic consultancy Sense Partners.

Shamubeel is a regular commentator on economics and is the author of several books including Generation Rent.

Terry Baucher (TB): Kia ora Shamubeel, welcome to the podcast. It’s been an interesting week, we’ve had three major reports on the true tax rate paid by the wealthy on their economic income. What have you made of all this? Are we any the wiser after these three reports?

Shamubeel Eaqub (SE): I think we are much wiser. I think we’ve all always suspected that the rich were not required to pay tax on a lot of their incomes. But we didn’t know how much income or how much wealth there was. So, the report by IRD in particular, I think was really useful to get a much better understanding of the survey of high wealth individuals and families. Just how rich they were and just how much income they were earning from wealth alone. The report that came out the previous week from Sapere and OliverShaw Consulting I think was really poor.

I think the official report laid bare those conjectures and I think fairly largely lobbying efforts that was done in the Sapere report.

(TB): Yes, the Sapere report was something, I’ve described it elsewhere as fairly indigestible. You had the complete difference in the conclusions the Sapere report reached that broadly speaking the wealthy were paying a fair amount of tax in line with middle income New Zealand. By contrast the reports from Treasury and Inland Revenue which show a completely different picture, with Inland Revenue concluding the median income tax rate on economic income was 8.9%, I think that raised a lot of eyebrows.

SE: It did. I mean the reports from Inland Revenue and Treasury didn’t show that the rich are not paying tax on the income that is taxable. What it showed was our tax system simply does not ask rich people to pay tax on the income that they earn. Most of the income earned, of course, is from capital. Wealth begets wealth and that huge amount of income, almost all of the income comes from that. You know, the wealthy becoming wealthier and they’re not paying tax on it because we don’t ask them to.

I think there was a sort of misconception that somehow the wealthy are sneaking around and not paying tax on what’s required of them. Although we suspect that they might do that as well. This report wasn’t really about that. But, you know, tax minimisation is a thing. There’s a whole profession that’s out there to help rich people do it very well, people like you, Terry. And then there was the other bit, which is, I think, a bigger and more pertinent question, which is “What counts as taxable income, and should that be taxed?”

TB: Yes, and that’s at the heart of this whole thing. It’s not controversial to be looking at the question of the distinction between economic income and taxable income, because I’ve seen other jurisdictions consider the same issues. On Wednesday, I was on Radio New Zealand’s The Panel. A panelist argued bringing in economic income into the equation isn’t right, because it’s not taxed and we’re also talking about gains not realised. But as you know, we do tax certain instruments on an unrealised basis. But broadly speaking, there is no controversy about looking at the economic value to determine what is a fair or what is a true rate of tax.

SE: There isn’t. And I think the norms will change over time as well. And at a particular point in time, income taxes were thought to be ridiculous, but they’re now the norm. There is nothing to say that there is no one form of income or wealth or a taxable base that we can’t tax. To me, it feels a little bit strange to think that just because we’ve got a system now, which defines taxable income as a particular way, that’s the only thing that we can possibly tax. That’s not true, as you know, when it comes to, for example, things like foreign shares, we have a foreign shares deemed rate of return regime, and that actually works pretty well because it takes a lot of the complexity away and you pay tax on the return that you’re likely to make on the asset that you have invested overseas.

We do tax [unrealised gains] already, it’s not like we don’t. We also do it on things like rates, which is calculated by reference to the value of our houses. So, it’s not like there is any reason why we should think that there can be no connection between wealth or the income earned and wealth. This whole thing that somehow it’s terrible we’re taxing unrealised wealth. As if these are poor people and they can’t afford to pay a tiny amount of that wealth by selling some of those assets or borrowing money or deferring it to a future point. There are so many ways we could design a system that would work quite well.

But to me, these [arguments] are just distractions. But these distractions are going to be really coordinated and very powerful because you know what? There’s a lot of money on the line.

TB: Were there any surprises for you in the numbers that came out?

SE: No, it wasn’t surprising. I think for most New Zealanders, the surprise would be just how rich the rich are.

TB: Yes. I figured that we might see something around the 10% mark because we knew other overseas jurisdictions had seen that. There’s that White House report from America where they actually have a capital gains tax and an estate tax and a gift tax. And they still think that the true tax rate on the economic income of the top 400 families in America is 8.2%, which is quite astonishing, really. Again, it illustrates the effect of what we tax and what we don’t tax although, the American system is riddled with particular exemptions. I do think you’re right, the scale of the wealth at the top end of these 300 odd families being collectively worth about $85 billion, I think that did take a few by surprise.

SE: Yes. I mean, it’s an extraordinary sum of money. And, you know, that is well beyond the conception of what any normal New Zealander could hope to have. And I think quite often when you think about the proposition to people when it comes to tax policy, particularly any taxes on wealth, they think that one, their wealth is going to be targeted or two, they might one day become wealthy.

But we’re not talking about that. We’re talking about, you know, a scale of wealth that there is very little chance that any normal New Zealander will ever achieve that kind of wealth.

TB: Yes, you’d have to have bought thousands of Bitcoin back in 2010 to match some of the numbers we’ve seen here. What do you think about the fact the median age of the respondents was 67? I think that was a little older than I was expecting to see. What can we read into that?

SE: I think it shows people who have made it, who worked hard, got lucky because luck and hard work are the two things that are the key ingredients for becoming quite wealthy. And sometimes intergenerational as well. I think it shows there was a bunch of people who came through that period of the economic reforms which made some big winners and losers, and some of them did spectacularly well.

And we see that, right. We know we know some of these individuals who are out there in that kind of age group. They’re quite visible and well known. It doesn’t detract from all the work they might have done. It’s more that I think they lived through a period of time which created opportunities that were quite unusual.

TB: Is that a moral, do you think, then, going forward for all of us, just come back to your point a few minutes ago, that people say “Well, so-and-so has made X and we can as well.” Or are we different economy, different times?

SE: Well, I think we will mint new billionaires and multimillionaires over time. They will be the Rod Drurys, and the Peter Becks, as well as the Stephen Tindalls and other people.

So there are different ways and some people are at the right point at the right time with the right skills and all those bits that make that magic. But the reality is, in a country of five million people, not all five million of us will have that magic.

TB: Indeed.

SE: A vanishingly small number of us will ever have that. So, I don’t think it’s a model that’s replicable, per se. It’s, of course, nice to have that aspiration that we should try and improve ourselves. We should start businesses; we should try and do well. We should create jobs. But actually, for most of us, we’re not going to achieve and attain those kinds of numbers, that kind of wealth.

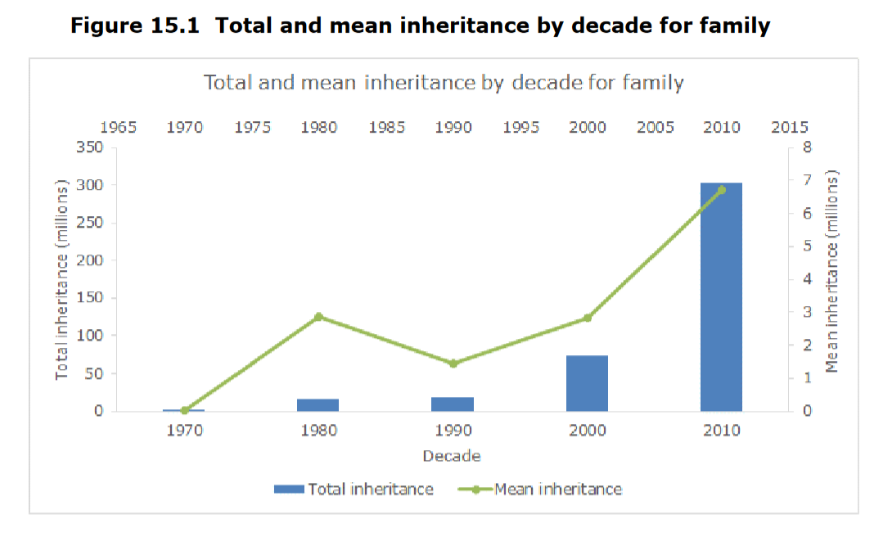

TB: Actually on wealth one of the things that I was intrigued to see Inland Revenue had looked at was the impact of inheritances. And this saw $411 million that had been transferred in what they call sizeable gifts, which is more than $25,000. But that was over a 50-year period, which isn’t terribly significant. I think that if memory serves right, half of that happened in the decade between 2010 and 2020.

What do you make of that? We’re not talking about old money being passed down from generation to generation, are we? Or maybe the money is still locked up in trusts. Did that surprise you? Because it was a surprise to me. I was expecting to see bigger numbers than actually popped up.

SE: Yes, I think there are now a lot of family offices for the truly wealthy families. It doesn’t make sense to give the money away. It’s much easier to keep it locked up because you get the economies of scale from running a family office, which gives you the ability to create even more wealth for future generations.

So, I wasn’t super surprised because there was no great incentive to dilute your wealth and to give that money away. I’m not really clear on what the definitions were in terms of those inheritances. Was it really money being gifted or was it the returns that are given to family members? There are lots of different ways that you could think about that. But my sense is that there is no great tax incentive for [the wealthy] to give the money away. There is no kind of reason for why you shouldn’t have the trusts and structures going on in perpetuity.

So was Thomas Piketty right?

TB: I see that Thomas Piketty has been quoted on Newshub about the report.

We know that Piketty is David Parker’s favourite economist or one of his favourites. Do you think this vindicates what Piketty has been saying?

SE: But I think it confirms what we know to be true, wealth begets wealth. To be very rich, it’s very helpful to begin by being very rich. And we also know that because of the way that our tax system is designed, it is designed for the many rather than for the few.

So, you know, inevitably you’re going to see the critique that this is the politics of envy and all that kind of stuff. But actually, when you jump back and ask the question ‘What is income and what should be taxed?’ it does take you away from that idea of envy. And actually, your income is very large and you’re not paying the same share as everybody else. Why is it that because you are wealthy, you are exempt from this income that you earning?

I think this was the core fundamental of the kinds of things that Piketty has been arguing for, why is this unearned income, this accident of birth? Why is it that you have some God given right to keep that protected from the rest of society? Why is it that that wealth, that income is not part of the wider taxation system in a society that you choose to participate in?

TB: I guess a response to that would be, well, we pay most of the tax anyway. It’s a small group, the numbers being pushed say the top 2% or 3% pay 26% of the tax. So the probable counter might be, ‘Well, we are paying enough anyway. We are paying our share.’ What would you say to that? Again, I guess it’s a question of how we define income, isn’t it?

SE: I think so. And I think, it’s also entirely possible to counter that with saying, ‘Well, if you also pay 20% like the rest of us, then, in fact, that future reality might be that all of us pay 15%.’

TB: The broad base, low-rate approach, broadening the base and lowering the rate. Yes.

SE Exactly. So, the alternative features are not just that they pay more. It might be that they pay more and the rest of us pay less. And again, this still goes back to the fundamental question of what is income and what we choose to define as taxable income.

And I think that’s really what came through that entire work. It wasn’t really about wealth. I mean, for me, it was really about asking the question of what do we actually consider to be income? And why is it that our tax system deliberately and specifically excludes some forms of income? Just because they happen to be the domain of the rich.

A ground-breaking report

TB: The report has been described as groundbreaking and not because of its methodologies, because those are fairly common. We were talking earlier that there seem to be three different methodologies and Treasury got down to nine different calculations of effective average tax rate, which I think was testing the patience of even the most dedicated of us.

What marks this report out as groundbreaking in my view, is we’ve actually got really good hard data, to work on for a change. And so it’ll be interesting to see how this plays out around the world.

SE: As you know, Terry, this is not new in the sense that there’s been other countries, particularly the US, where they’ve really kicked this off trying to find out what’s going on, because, you know, the domain of the very rich is quite opaque.

They can keep things opaque because they’re very rich and they have very good lawyers and very good accountants. And also, people are private because they don’t want people to know how much money they’ve got. But the groundbreaking nature of this study was very much that now we have real data based on an extraordinarily high rate of response.

TB: I think it was 93%. And, you know, fair’s fair, to be honest when the project was announced, there was a lot of immediate pushback on this. But 93% compliance, I think, is something I would expect that’s actually better than Inland Revenue were hoping for at the start of the project.

SE: I think it’s excellent. I mean, we know that there is a large enough population to give us a really good understanding of what this group of people look like. But I think it also speaks to something about it’s not like these people are necessarily trying to hide things, right?

When you see these kinds of numbers come out, there’s always a tension that all the rich are trying to hide things or they’re not trying to pay their fair share.

My sense is that that’s not really what the high rate of participation shows. I think what it shows is that people are relatively open. I mean, of course, there’s always a risk of not complying with Inland Revenue’s requests. But to me, it shows that even the very rich families, they do feel there’s a civic responsibility participating in society, that they want to be part of New Zealand and a tax system that is fair and transparent.

At least for me, the signals were very positive that these very high net worth individuals and families, they wanted to share that information so that we could have an open conversation about what is it that we want to do. Because the reality is that if we make changes on things like capital gains or wealth taxes, it’s not going to be just those families that will be affected, it will be a wider group of people. And having that transparency and openness does make it easier for us to have those conversations.

I think the study is really helpful because those studies give us real data and also just showed us the distribution of New Zealand. You know, the 99% of New Zealanders will live very different lives to that top 1%.

So how did the rich get rich?

TB: Yes, indeed. Just on the distribution in the report was there anything of interest to you about the range of the sources of that wealth? There’s some property, new technologies. Anything stood out for you in that data?

SE: Well, I mean, to me it was more that there was such a variety. I think that’s cool, right? It shows that to be filthy rich, there isn’t a common formula. There’s lots of different ways people have become filthy rich. Some of it because of, you know, like just being at the right time, at the right place in the right industry or having the right whatever. But it wasn’t all property. It wasn’t all one thing.

TB: Now the property thing is really interesting. I think on average each of the 311 families held 22 properties. But the analysis and modelling by Inland Revenue showed the capital gains weren’t all from property, they represented a range of things, portfolio investments, but mainly their own businesses that they had built up.

And that actually was something I thought was quite encouraging because you take that and the fact that we did not see a lot of inheritances being passed down and you got the impression that there were people who could come in and start at the bottom and have huge success. You mentioned Peter Beck earlier. Rod Drury of Xero would be another example of that. Stephen Tindall with The Warehouse, three different types of industries there. None of those are traditional industries, by the way. They’re not farming, or forestry related, but they’re all very wealthy people as a result of that. I guess people might say it shows a more diverse economy and the opportunity existing in that. So, I was encouraged by that.

SE: I think so. I think for most New Zealanders, the story of wealth creation kind of goes to a housing type story, right? Actually, there are a lot of people who’ve made a lot of money by starting businesses, selling businesses, or keeping businesses and growing them. And that to me is what creates economic vitality. That’s what creates a better New Zealand, right? That’s what creates more jobs.

I mean, of course we need homes. But you know what? It’s such a passive way to create wealth. Businesses are exciting because you’re creating jobs and changing lives through providing livelihoods. That, to me, is enormously more satisfying and exciting. Seeing a lot of that in the very high net worth individuals tax statistics, I think was very encouraging.

But it’s also true that not only do they make money by being in business, they continue to invest in businesses. So, it’s not like, there are these rich families that are sitting there with all this money sitting idle. We know they’re using that money all the time. They’re always looking for the next big opportunity. Of course, they don’t get it always right. But the reality is that, you know, I’ve been involved with businesses startups with these high net worth individuals, and they are the ones who back people. They’ll say ‘Here is a cheque for $1,000,000. I’m going to back you.’ And that is hugely powerful.

TB: That was something I came across when I was on the Small Business Council, the access to venture capital in New Zealand is surprisingly good. There is a fair amount available, and it is these wealthy people reinvesting in businesses. They go looking for the next Xero, the next Rocket Lab. And again, that’s encouraging.

What next?

So, what next? If you’re the Finance Minister or the Prime Minister, you’ve got this report and you say, ‘Right, here’s what we’re going to do.’ What would be the three things you would say to address the issues these reports have thrown up and improve our tax system?

SE: Well, if I were truly a politician in New Zealand, you know that I would have already sent out a poll asking a small group of people what they think about more taxes because we do politics by polling in New Zealand. And the polls will show that nobody, no New Zealander wants more taxes because they’re afraid that they might one day be rich, and they might be asked to pay tax on it.

So, you know that that the self-interest, that greed, that fear of missing out of a potential future, which is I think almost impossible, I think that would motivate most polls and they would show that people don’t want more taxes. And as Finance Minister, if I were truly in Cabinet today, I would see those polls and say ‘Bugger it, I’m not going to do anything. Bury this thing.’

That is the sad reality, it’s heartbreaking that we have seen very little action when it comes to tax policy in New Zealand for decades. Because you know what? We just don’t have the steel and the political consensus across the community to do anything different.

TB: Yes, I think that’s it in a nutshell. I mean, I think Jim Bolger’s ‘Bugger the pollsters’ is something that should be adopted when it comes to tax. Because the politicians, and it’s interesting, doesn’t matter which side, they run away from the issue.

I know I’m a broken record on this. I’m looking at what’s coming down the track, what the Tax Working Group saw was coming down the track. We’ve got demographics working against us with ageing, higher superannuation costs, greater health care demands and now climate change.

The Climate Change Commission in its report released yesterday basically said ‘We can’t buy our way out of reducing our emissions, we need to diversify.’ And that report, when it talked about tax, made repeated mentions of tax incentives for better investment to address these issues.

So, it seems to me that like it or not, politicians are going to have to address these facts or simply say, well, ‘You can’t have anything because we need to protect these unrealised gains.’

SE: You know, I was probably being overly pessimistic. But I think the thing is, in the current moment in time, the crisis still feels like it’s two or three or four or five political cycles away.

If you make changes on tax policy today, inevitably you will see whoever’s in power next undo them. So there will be no enduring tax policy because we don’t have consensus in New Zealand. Do we have a pressing need to shift our tax policy? Of course, we do because of demographics and because of climate change, because of large infrastructure deficits, we know that we need to change things. But we also know that New Zealand has an extraordinary reactionary political system. There is no leadership, it is reactionary. And so, unless there is a crisis, until something really breaks, we’re not going to change.

TB: So you don’t think Cyclone Gabrielle, or the Auckland floods are a breaking point?

SE: Not at all. I mean, they might cost the government, you know, a maximum of $15 billion in the scheme of things. That’s nothing spread over three or four years.

You know, the Government’s tax take per year is $100 billion. Those costs are at the margins. So that’s not enough. It’s when you’ve got Cyclone Gabrielle happening every year or every other year when people can’t get access to insurance, when we’ve got coastal properties that are being inundated, when we’ve got erosion that’s taking away what we’ve previously valued as multi-million-dollar bachs. That’s when you’re going to start to really strike those pressure points, because we haven’t actually planned for any of this stuff.

TB: Those are all happening right now, actually. I mean, Tairawhiti East Coast region, I think Cyclone Gabrielle was the fourth major event that warrants special tax treatment inside 12 months. But as just said, it’s now receding into the background. Maybe it’s not so much our politicians, it’s also our media cycle just isn’t adapted to that.

SE: I think it’s less about the media cycle, it’s also what we want to hear as citizens, as engaged people in politics, people who are engaged in the civics of the country. Are we actually engaged in grappling with these big structural issues? And the answer is no. And I think the conversations that we have on public policy in New Zealand are, by and large infantile.

You know, they are by and large led by people who are lobbyists and people who are actually biased with a huge amount of self-interest because it is a small group of people who do everything. There’ll be the tax experts who are providing expert advice to people to minimise their taxes and the same people who are going there to try and design a business tax system. Well, I don’t know, man can you really trust them?

TB: Well, reputational risk here, but yes, I think self-interest is a problem. But let’s just be bold, let’s say you’ve decided ‘Bugger the pollsters’ what would you do?

What tweaks would you do if you were looking at something that might take the population around along with you? What would be the first thing to do.

A tax switch?

SE: You know, I think one would be relatively easy in that you would do a tax switch. You would implement a land tax and you reduce something like GST. That switch would be quite immediate and it would create a much better balance in New Zealand. It wouldn’t capture the very high net worth because it’s not about that, but it would create the introduction of a wealth tax. We already have the mechanisms for that with things like the rating tools.

But, you remember with the Tax Working Group, the land tax was one of those things that was identified as a good tax to have, because we know that not only would it incentivise better use of our land that we have, but it’s also that one asset that can’t run away, like unlike many of the other types of assets that people hold. So that would be the big thing.

But fundamentally for me, it’s really around if you really want to change tax policy, you’re going to have to create consensus. And you know, we can’t do that until we have some kind of bipartisan agreement about, one, what the issues are, and two, that we fundamentally either need to have higher taxes or we simply cannot have all the services that we have promised ourselves.

Now, that’s a really hard conversation to have. You know, you look at the quality of our political leaders. They’re not engaged in any of that debate. You know, most of our political leadership is engaged in the politics of who’s going to do the least.

TB: It’s a very small target strategy.

SE: It’s sort of, if you ask me what needs to change, I think the change that needs to happen is not that you need to jump in and make lots of changes, because the reality is that the knee jerk reaction will be to reverse those through a change of government. I think the change that requires us to have is actually creating something like the Climate Change Commission that creates this conversation. Some of those public policy issues that take the politics out of it.

TB: So, are you saying there should be the equivalent of the Climate Change Commission, a Tax Policy Commission that alongside David Parker’s Tax Principles Act, but sits there and pushes out the reports and saying, ‘This is it, guys, this is what we can do.’ In other words, a semi-permanent tax working group.

SE: Except of course it must have powers and it must have the ability to hold the politicians to account. Quite often what we do with things like the Climate Change Commission is we give them the power to design, but we don’t give them the power to actually fund or hold the powerful to account.

It’s not going to be very hard, right, because no politicians want to give the power away to somebody else. There will be no independent body that they’re going to give the powers away. The only one that they’ve really done that with is the Reserve Bank, and I think they’ve been regretting it ever since.

TB: Yes, I was thinking of the Reserve Bank too. I think that’s probably as good a point as any to leave it there.

Shamubeel, thank you so much for being on the show. Really appreciate your insights on this. I hope I don’t feel so pessimistic, but to be frank, we probably have good reasons for people to be sceptical about what will change anyway.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week, kia pai to rā.

Have a great day.