- Tax cuts delivered, but watch out student loan borrowers.

After what seems to have been an interminable dance of the seven veils, all has been revealed and we now know the final shape of the Government’s tax package. Nicola Willis has delivered on National’s manifesto and increased thresholds as promised.

That was unsurprising, although there’s a twist in that these changes will take effect from 31 July, four weeks later than expected. The delay is to enable payroll providers to update their systems.

The big surprise for me is the decision to increase the threshold for the Independent Earner Tax Credit (IETC) to $70,000. As I said in my Budget preview, I expected this to be cut to help pay for, or even increase, the threshold adjustments. Speaking on Breakfast TV, I expressed the hope that any threshold adjustments would focus on the group around the threshold where the tax rate jumps from 17.5% to 30%. The lift in that threshold to $53,500 together with the extension of the IETC will help, but more needs to be done in my view.

Giving with one hand, taking with the other…

The Government has also increased the in-work tax credit (IWTC) by $50 per fortnight, which is welcome. However, its effect will be mitigated by the fact that the $42,700 annual family income threshold above which the IWTC will be abated at a rate of 27 cents per dollar remains unchanged. The threshold has not been increased since 1 July 2018 which means that families with income above the threshold face an effective marginal tax rate of at least 46.1% (17.5% plus 27% abatement plus 1.6% ACC Earner Levy) which is higher than that of the Minister of Finance. It remains remarkable to me that this issue has been allowed to continue for so long, but when I raised the issue with the Minister of Finance her response was “I utterly reject the question”. (There were quite a few other questions also rejected with varying degrees of utterly).

Increased Inland Revenue funding

As also promised by New Zealand First in its manifesto, the Budget proposes an additional $29 million annually for increased compliance activities. Interestingly, the specific appropriation for investigation, audit and litigation activities will be increased from $106.2 million to $165.4 million. The Appropriation for Services to manage debt and unfiled returns will also rise from $83.5 million for the June 2024 year to $105.7 million in the coming year. Both increases indicate we should expect to see a significant rise in Inland Revenue investigation and debt management activity.

Student loans

Unlike my prediction about the IETC, my speculation that there would be some increases here was correct. The Government proposes increasing the interest rate on student loan debt payable by overseas based borrowers from 3.9% to 4.9% from 1 April 2025. Furthermore, the late payment interest for both overseas AND New Zealand based borrowers will increase by 1 percentage point.

However, as previously discussed, the amount of student loan debt has steadily increased and only 26% of overseas-based borrowers are making repayments. The Budget Appropriations include a provision for debt impairment of $633 million (up from $539 million) for the coming year.

As noted above Inland Revenue is boosting its compliance activities for student loan overseas-based borrowers, “including those returning to or visiting New Zealand”. We can therefore expect to see a few defaulters being detained at airports. It will be interesting to see if such moves result in significantly increased repayments.

Waste disposal levy changes

Elsewhere, the Government proposes increasing the level of Waste Disposal Levy but at a lower rate than initiated by the previous Government. It’s anticipated the Levy will raise a total of $1.195 billion over four years to 2027/28 which is split 50:50 with local government. The Government proposes amending the Waste Minimisation Act 2008 to expand the range of activities the levy can be used for, such as restoring freshwater catchments. This sort of recycling of environmental levies is to be supported but perhaps the split between local and central government should be shifted in favour of local government.

Calling Inland Revenue?

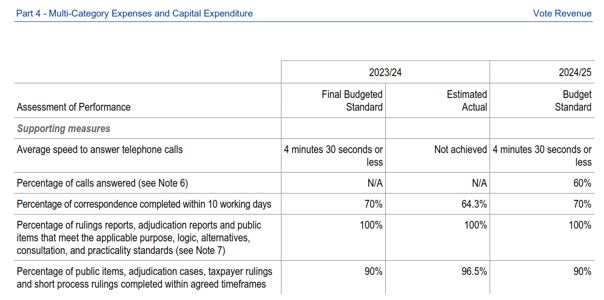

Wading through the detail of the Appropriation Estimates often reveals some interesting nuggets. The Vote Revenue Estimates included the following details about Inland Revenue’s expected performance when answering calls and responding to correspondence. It will be no surprise to many to note that the standard of answering calls within 4 ½ minutes was not met. Going forward Inland Revenue expects to answer 60% of all calls so I will check in next year to see how it performed.

Now what?

Having delivered on its campaign promises what next for the Government’s tax policy? The Finance Minister referenced the ACT Party’s proposals to flatten the tax scale but made no commitment as to when that might happen.

Willis also acknowledged Treasury’s advice of a structural deficit of about 1.5% of GDP (roughly $6 billion). This can only be addressed by spending cuts or tax increases and the expectation at present is for spending cuts to meet that gap. That means any future threshold adjustments are off the table, including the possibility of automatic indexation at some point. For the moment the Finance Minister will be happy to take the credit for the changes announced today. Let’s just hope it doesn’t take another 14 years for the next revisions.