And I reflect on 40 years in tax – what’s changed or not changed.

The Finance Minister Nicola Willis made the first of what is going to be a series of pre-Budget speeches to the Hutt Valley Chamber of Commerce, and in it she dropped a few clues as to the likely contents of the Budget.

In particular, she announced that the Budget’s “tax relief package will increase the take home pay of 83% of New Zealanders over the age of 15 and 94% of households.”

In case you’re wondering who is in the unlucky 17%, these are taxpayers with annual income currently below $14,000 or with no income at all. They therefore would not benefit from any increase in tax thresholds. According to Inland Revenue in the year to March 2022, there were over 800,000 taxpayers whose income is been between $1.00 and $14,000. There were another 210,000 or so who had no income at all during the 2022 tax year.

14 long years?

In her speech Nicola Willis noted that New Zealanders have not seen any changes to personal income tax rates and thresholds for 14 years. “Unlike most developed countries, New Zealand has made no adjustments to tax brackets to compensate for rampant inflation.” However, having highlighted this point, there wasn’t a commitment in her speech to regular indexation of thresholds, which is how we got 14 years without changes. I’ll have more commentary on that a little later.

The Finance Minister talked about “tax relief aimed at middle and lower-income workers” which is interesting because it hints that maybe threshold adjustments might be focused most on those earning below $70,000. The threshold which I think is most problematic, and Geof Nightingale, Sir Rob McLeod and Robin Oliver all agreed with this, is at $48,000 where the tax rate goes from 17.5% to 30%. There doesn’t appear to be any plans to adjust the tax rates there, but whether there is a bigger proportional increase around that threshold relative to the other thresholds, we’ll have to wait and see. We know by the way that the $180,0000 threshold at which the 39% tax rate kicks in is not likely to be increased.

The OECD joins the call for a capital gains tax

The Finance Minister’s speech came hot on the heels of the latest Organisation for Economic Cooperation and Development (OECD) Economic Survey on New Zealand, released on Monday. The big headline here from a tax perspective that the OECD joined the IMF in recommending a capital gains tax. What was interesting here is that when the IMF made this suggestion, Nicola Willis, dismissed it with a snippy comment following in the footsteps of her predecessor Sir Michael Cullen. This time around, there was no such snippy dismissal.

The report actually is quite sobering reading, not just around the tax side of it, but just generally about what it has to say about certain aspects of the New Zealand economy. Education was specifically mentioned as a point where attention needs to be focused on improving standards and therefore flowing through to greater productivity across the economy.

The OECD agreed with the Government’s proposed fiscal approach trying to squeeze spending and keep it under control. It had some criticisms about how budget operating allowances have been allowed to increase in recent years without any real explanation.

The OECD supports the broad-base, low rate approach, a capital gains tax, and tax reliefs for pension saving

But it also made the point that “any tax cuts should be fully funded by offsetting revenue or expenditure measures”, before going on to add “raising revenues should first be achieved through broadening the tax base and reducing distortions before raising rates of existing taxes.” That very much endorses the broad-base, low-rate approach Sir Rob MacLeod in particular espoused in a recent podcast.

No surprises there, but the report continues:

“There is a need to reduce distortions to household choice of asset allocation. Shares, land and owner-occupied residential property are tax favoured. Most capital gains from shares, owner-occupied residential property and land are not taxed. To ensure the tax system is not overly distorting, saving and supporting broader growth, capital gains taxation reform should be done as part of a wider review of tax settings for saving. New Zealand’s tax settings remain an outlier in some respects in international comparison, and notably in offering no tax deduction for contributions and in taxing the returns pensions funds earned while they’re invested and prior to withdrawal at progressive rates, this likely distorts saving away from private pension saving.”

Robin Oliver made the point about over-investment in housing, but as mentioned last week Dr Andrew Coleman picked up on how our taxations of savings is unusual by world standards,

There’s a lot to digest in this 150-page report which is only available online. It’s probably no surprise that expanding the capital gains tax base is not likely to be very high on the agenda of the Coalition Government at the moment. But there’s plenty of food for thought in the report.

One of the other points of interest, and there has been some commentary about this, is the suggestion for an Independent Fiscal Institution, basically, a policy costing unit. The OECD picked up that there had been no independent costings of policies in the run up to last year’s election. This is something that could be done by an Independent Fiscal Institution. Some work was done on this under the last government and Nicola Willis seems open to revisiting the issue.

Following the Irish example?

The OECD survey suggested the Irish Fiscal Advisory Council (IFAC) https://www.fiscalcouncil.ie/as a model that could could be followed. Given Ireland has a similar population this seems a good idea. Personally, I think we ought to look very closely at countries of comparable size to ourselves. The IFAC has been mandated to independently assess the government’s fiscal stance and budgetary forecasts and monitor compliance with budgetary rules. As I mentioned earlier the OECD thinks that we need to review our budget rules.

According to the OECD survey about 80% of OECD have some form of Independent Fiscal Institution. The Congressional Budget Office in the United States which has 270 staff is a very well-known example. Over in Australia, the Parliamentary Budget Office, with 45 staff has this role. The Canadians have a similar Parliamentary Budget Office and over in the UK they have the Office for Budget Responsibility. There’s plenty of examples around the world to consider and it would be encouraging if we heard something in the Budget about this.

Small businesses and statistics

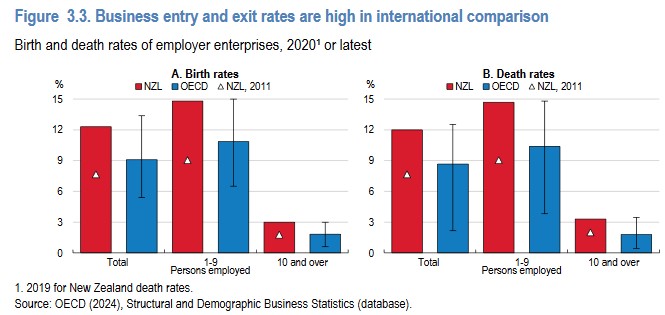

The OECD survey, noted that the business entry and exit rates are higher in international comparison although this means “business dynamism is vibrant” the OECE also noted that the “high share of the population working in micro, small and medium enterprises…hints at a difficulty for these firms to grow into larger businesses.”

One other thing I thought was very interesting was commentary around improving the timeliness of New Zealand’s macroeconomic statistics. I’ve long thought it was a weakness that we don’t see monthly GDP or inflation data, but I wasn’t aware we were, like Australia, very much in the minority within the OECD in not producing a monthly CPI index. As the OECD noted “Older and less frequent statistics increase the risk of costly policy mistakes”. I wonder what the OECD would have made of the news that all Stats NZ staff were offered voluntary redundancy?

Don’t look back in anger? Forty years in tax

This week, it is 40 years since I started working in tax. They say the past is a different country, we did things differently there and that’s true, but one thing that hasn’t changed over my time in the past 40 years is the behavioural impact of tax. When I started working in the UK, the top rate of income tax was 60% and I saw people very incentivised to make sure that they’re claiming all the possible deductions, maximising pension deductions and the like. The top rate in the UK now is 45%, but you still see the same behavioural impact.

For comparison in 1984 the top rate in New Zealand was officially 60% but a further 10% surcharge had been introduced in 1982 by Sir Robert Muldoon, the Prime Minister and Finance Minister at the time. The top rate was therefore 66% which applied to income above $64,000. Based on CPI since then that’s the equivalent of roughly $260,000 now. According to the Inland Revenue date for the March 2022 income year, just over 42,400 taxpayers earned more than $260,000. That’s a little bit under 1% of all taxpayers. But they had a substantial amount of income between them, close to $20 billion and therefore paid a sizeable amount of tax nearly $7 billion in total.

The effects of forty years of inflation – how New Zealand taxpayers appear to have lost out compared to their UK counterparts

In terms of inflation, it’s quite interesting to look back at the tax rates and the income bands which applied. In 1984 the lowest rate was 20% on the first $6,000 of income. That $6,000 in 1984 dollars would now be $24,350 so in terms of inflation adjustments, even when we see the current 10.5% tax threshold move from $14,000 to maybe $16,000 in the Budget you can see that maybe New Zealanders have been losing out. Consequently, because we aren’t adjusting thresholds regularly, fiscal drag means that inflation has affected the ordinary working New Zealanders quite substantially.

That becomes clearer when you swap notes with what’s gone on in the UK with the tax thresholds there over the same period. The UK has a tax-free personal allowance which Was £2,005 back in 1984 when I started working. It’s now £12,570, but if it had just kept in place in place with inflation, it would be only £6,300. In other words, the value of the tax-free personal allowance has doubled in the past 40 years.

Interestingly, the tax threshold after which the higher tax rates kick in was £15,400 back in 1984. Inflation adjusted that would £48,300 compared with the £50,000 where it actually takes effect. There is an additional rate of 45% in the UK on income over £100,000. Back in 1984 the highest 60% tax rate kicked in at £38,100 inflation adjusted that would be £120,000 now.

What you see looking at these numbers is broadly speaking average earners in the UK have been less affected by fiscal drag and inflation than New Zealand workers have been. And that is something that I think I’d like to see changed here for the better and we should be having regular inflationary adjustments as is required by the UK tax law. I think such a move would tie into the better fiscal discipline suggested by the OECD.

The behavioural impact of no capital gains tax

I’ve now worked for over 30 years in New Zealand, but I still remember my shock when I realised there wasn’t a general capital gains tax here. When I consider the behavioural impact of taxation, that’s where you see it apply most where people will be looking to turn something that could be taxable at 39% into a non-taxable gain. And so, there’s a distortionary effect there.

And just to circle back to discussions we’ve had previously on the podcast and what the OECD have just said, there is a tremendous amount of value in the broad-based low-rate approach. It’s not perfect, but one of the things it does deal with is this question of behavioural impact and distorting behaviour chasing tax benefits. My personal view is the absence of a general capital gains tax has had an effect on our productivity. If it’s better in investment returns to invest in residential property in which the returns are largely tax free, than investing in a business or in shares that are taxed, such as overseas shares under the Foreign Investment Fund regime, then that diverts investment into less productive assets. Whether that’s for the benefit of the wider economy as a whole, well, that is a matter for ongoing debate. My view is it’s not.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A quiet week in the tax world – but is this the calm before the storm of this year’s Budget?

The latest OECD report on taxing wages shows the tax wedge rising in most countries including New Zealand.

It’s been a quiet week in the tax world, which, to be honest, is quite welcome. But there’s also a growing sense of a calm before the storm, that being the Coalition government’s first Budget on 30th May, I’ll offer up some speculation as to what I think will be in the budget closer to the time, but one thing we do know will be expected to happen, is adjustments to the flat tax thresholds, which as listeners will well be aware of, have not actually been adjusted since October 2010.

It so happened last week the Organisation for Economic Cooperation and Development (the OECD) released Taxing Wages 2024, its annual Taxing Wages report. This is a fascinating document which looks across the composition of wages and provides details of taxes paid on wages. This year, it’s also focusing on fiscal incentives for second earners in the OECD and how tax policy might contribute to gender outcome gaps and labour out market outcomes. It’s a big report which runs to 679 pages and is only available online.

Taxes are increasing thanks to inflation

One of the things that comes out of the Executive Summary was that in the words of the report tax systems in the OECD are not fully adjusting to inflation. Consequently,

“The average tax wedge for all eight household types covered in this report increased in the majority of countries between 2022. And 2023 driven in most cases by higher income tax. For the second consecutive year, more post tax incomes at the average wage level declined across the majority of all OECD countries now.”

The tax wedge is described as the difference between the labour costs to an employer and the corresponding net take home pay of the employee. It represents the sum of the total personal income tax and Social Security contributions paid by employees and employers. Less any cash benefits that the employee might receive.

New Zealand has consistently scored well in this measure because we don’t have Social Security taxes and we’ll talk a little bit more about that later. But notwithstanding that, the average take home wage for New Zealand employees has been declining over the past few years.

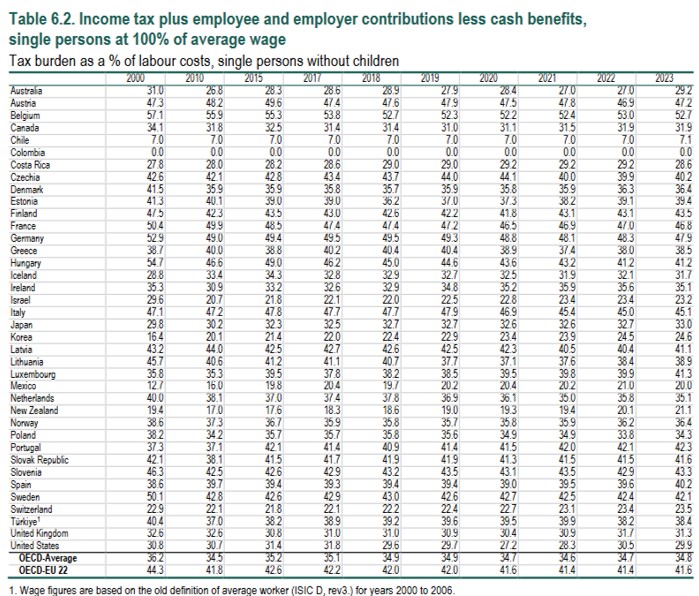

The report has an appendix showing the evolution of effective tax rates on labour since 2000 with a number of separate measurements based on single persons, single parents, or married couple with two children. It looks at what the tax wedge for each group is based on 67% of average wage, 100% of average wage and 167% of the average wage.

Now, whatever measure you take, you can see that the tax burden for New Zealand employees has been rising steadily since 2010, but you can see it start to accelerate in the last three to four years. So, for a single person at 167% of the average wage, their tax burden has gone from 23.9% in 2017 to 25.8% in 2024. Now you might think 2 percentage points isn’t much, but it becomes more noticeable as it accumulates over time. For a single person at 100% of the average wage the tax burden has gone from 18.3% to 21.1% over the same period.

This OECD report reinforces what we’ve been saying for some time that tax adjustments to the thresholds are long overdue. Now those who listened in to last week’s podcast with Sir Rob, Rob McLeod, Robin Oliver and Geof Nightingale will have noted pretty much everyone was of the view that the threshold where the 30% tax rate kicks in, that’s $48,000 was a major problem in our tax system. Geof was particularly insistent on this point. This OECD data reinforces that point. So, it will be interesting to see what moves are made in that space in the Budget at the end of the month.

Social security taxes – time for a rethink?

Moving on, thanks to everyone who’s commented or given feedback here and across the various social media platforms about last week’s podcast. It’s always great to have some engagement. I do read all the comments even if I don’t always respond.

There were some particularly interesting comments from Dr Andrew Coleman of the University of Otago about Social Security taxes and the absence of them in New Zealand. As he noted, New Zealand is an outlier in world terms in this respect.

Now, as I mentioned in the podcast, Social Security contributions were once quite a significant factor of the New Zealand tax system from the 1930s until the 1960s. But what happened over time was that the contributions weren’t hypothecated and applied only to Social Security payments, but in fact just became treated as part of taxation generally until in April 1964, the Social Security Fund was merged into the Consolidated Fund

Ultimately, the then Finance Minister Robert Muldoon decided in 1968 that separate Social Security contributions were no longer required and merged everything formally into income tax. Since then period, income tax has used to pay for Social Security such as welfare and superannuation.

That’s more than 50 years ago, but as Doctor Coleman pointed out many other countries have Social Security taxes. So, is that something we should consider in more detail? Well, I hope to explore that point in a separate podcast.

Sir Rob McLeod, Robin Oliver and Geof Nightingale on expanding the tax base

[In this part of the podcast I asked Sir Rob, Robin and Geof about the strains New Zealand’s Broad Base Low-Rate approach is experiencing and if a government wanted to raise how would it do so- through a wealth tax, capital gains tax, stamp duties or estate duties, whatever].

Sir Rob Mcleod (RM) Well, if I can kick off, I’m a huge fan of Broad Base Low-Rate (BBLR). I think it’s got a very simple thrust. It’s as much about pragmatism as it is about technical. I think we need to be careful in my experience with the debate and understanding that a Broad Base Low-Rate system is not one characterised by a myriad of taxes. Some people interpret a myriad of taxes as achieving breadth and therefore fitting with Broad Base Low-Rate. No, my definition of Broad Base Low-Rate is a few taxes with a broad reach. That’s where you get the simplicity. And the income tax and the GST covers most of GDP in the nation.

What does it not touch is the question to ask. You can talk about wealth tax and CGT, capital gains tax, but they’re actually part of the income tax. There’s an overlap between wealth tax, capital gains tax and the income tax. I don’t believe that that gap justifies the kind of emphasis that’s being given to wealth tax and CGT.

Sure, we’ve got some capital gains not taxed, most of them actually are taxed already in the system. The comprehensive capital gains tax I think in that sense is a bit of a misnomer because we do not have comprehensive taxation in the New Zealand system. And if you go and then put wealth taxes on, whether it be land or wealth in general, you are actually doubling up on the income tax. You’ve got an element of double tax in doing that and that takes us back to the starting point, that Broad Base Low-Rate is about identifying the gaps. And there’s bugger all gaps actually left by a broadly designed GST and income tax such as New Zealand has.

And when we go into the debates on specifics around the margins of that base, there are good reasons for arguing about why we shouldn’t have them. So that’s why I think BBLR is there. If you want to get more out of what we’ve got than the broad base of income tax and GST, you’ve got to justify it and you’ve got to start with what percentage of the GDP should be taxed in the first place. With balanced budgets, government spending equals taxation. With a balanced budget, which is kind of where the world wants to be these days.

So, I think recognise that the tax rate for the nation is government spending divided by GDP. And there’s a hell of a lot of benefit from there. So, if you want a tax cut, you’ve got to cut the government spending. It’s the only way to do it. Those various elements I think are very interconnected in the debate around Broad Base Low-Rates.

Geof Nightingale (GN) I think your question was where would you go to for another 1% of GDP? And I would agree with Rob that it feels to me that 30% of GDP or Government expenditure to GDP at roughly 30% has (that’s our long-run average, it spikes up and down for pandemics and earthquakes and recessions and things) that’s a constraint that I would be quite personally happy for our economy to operate against.

The question is then how you raise that revenue. And I totally support Broad Base Low-Rate. I think it’s effective in practise and 30 years of experience. I think the missing bit still there is our income tax is not as Broad Based as it should be, and I think we do need to extend it into further realised capital gains. So, whether you do that as a separate comprehensive capital gains tax like other countries, or you just change the definition of income, that’s a design feature.

Philosophically, it’s the same thing. It’s just how you get there. Taxing more income through realised capital gains, and then I would recycle that revenue into tax cuts, reductions, initially in the lower marginal rates because that’s where our problems come with high effective marginal tax rates in conjunction with welfare, which leads to productivity and incentives to work and all of that. So I would extend the taxation of capital, recycle the revenue and like Rob aim for 30% government expenditure over GDP.

TB Robin, you were part of the tax working group, you were one of the three dissenters in 2019. I that still your opinion?

Robin Oliver (RO) As Rob said and Geof echoed, it’s not a black and white issue. Do you tax capital gains or not? I mean, Michael Cullen kept on trying to make the point, talking about taxing capital income, not capital gains. Everybody ignored it, but he had a point that we do tax capital gains in certain cases and it’s all part of our income tax system and GST anyway. Are there holes in the system where you can efficiently raise more money at low cost? And the big hole, the gap in our system, it came out in the tax working group and all other reports is land.

We are a growing economy, growing population, land rises/increases systematically in value and that produces a lot of income and overall, we don’t tax it. You look at all the data, you know, higher wealth people, predominantly own land. Not all, but predominantly. So OK, should we be taxing land in one form or another? And I’ve got sympathy for that, but you’re going down to the workability. No government will ever tax home ownership. If it does, it will cease to be a government pretty quickly and someone sensible will come in and abolish that tax. So that’s a big hole in any land base. And then you’ve got issues about iwi and their relationship with land. You’ve got farmers.

We used to have a land tax. We had a comprehensive tax in the 1890s and we ended up with a tax just on Queen St commercial property. Everybody else got exemptions over time. I have some sympathy for taxing the increase in the value of land or land in some form which is not taxed now, but the housing, the home ownership stuff. You know, David Caygill, he proposed taxing homeowners. And he got told to back off.

I was working with him on capital gains tax proposal and we officials recommended including home ownership. And we were gobsmacked, totally bewildered when he accepted our recommendation. We expected him not to. And he went off to lose that next election, but probably not for that reason.

Workability matters. Home ownership is off the table. Our problem as a country is we take our savings, we invest it in land, we borrow from Australia, we invest in more land, bid up the price of land. We end up with the same amount of land as we began with – because that doesn’t increase – and heavily in debt to Australian banks. Solving that problem is not easy.

The problem with overinvestment in housing

TB Yes, it’s a behavioural impact. I had this conversation with an American client yesterday, who because of the fact they have to file U.S. tax returns, they’re subject to capital gains tax. But the FIF regime, he looked at that, and said, well, I can’t invest in stocks so I’m going to look at residential investment property here. That’s really a case of an unintended consequence of a tax.

On the family home, I fully grasp all of that, but is there an argument for saying that there is a limit? Because we build some of the biggest houses in the world. New Zealand houses – new houses, were until quite recently – are the third largest in the OECD. They were nearly getting on for close to 200 square metres.

RO We like our houses.

TB So could you say above two and a half million dollars or $5 million, the gain above that – some pro rata, we’re getting into technical details, but there is this thing that you’ve just espoused it perfectly, Robin. That at present we’re encouraged to invest in land and more land and borrow. So, there’s a loss of productivity, that 20% dead weight. There’s got to be a lot of lost productivity because capital is diverted into land rather than elsewhere.

RO The current group did look at something like that, although it was outside our terms of reference. We were not allowed to even consider the home or the land underneath the home or the sky above the. In terms of reference that we did look at that. The trouble is, a $2,000,000 house is not all that much in Auckland, as Michael Cullen kept on putting out, it was a hell of a lot in Whakatane.

TB There are 77,000 homes in Auckland worth more than $2,000,000, according to an OIA I got.

RO Probably one in Whakatane.

GN There’s a technical solution. If you were going to put all realised capital gains into the tax pot, you give every New Zealander a lifetime exemption, regardless of asset class or description, and that might be $5,000,000 or more, less but and that then shouldn’t distort behaviour. It’s arguably equitable and from a compliance and administration perspective, it would take probably 95% of us out of the of the loop.

RO And with that 95% of revenue.

GN Yes, well, maybe not because the assets are weighted towards the top. But anyway, the argument against that was always administrative. It’s very difficult to administer. But with current digitisation and things, I’m not sure those administration and compliance arguments – the integration of the land registers and share registers and things – as strong as it used to be. So, there are theoretical solutions there, but they’re hard to get to the public.

RO The idea of taxing the person with over $5 million has got a lot of appeal, but it’s not realistic. I always give the example of the idea you can freely tax all these very high wealth individual/ medium wealth individual people. Well, some of those are your medical specialists, your surgeon, your oncologist. And they can go to Australia.

You whack this $5,000,000 tax on their income over a lifetime and off they go to Sydney. So you’re sitting here in New Zealand, you’ve got cancer or something like that, and we’ve got a more equal society, but we have no treatment for cancer. Off to a hospice you go.

GN That might be the case with a wealth tax, but with an income tax I’m not convinced, Robin. I mean, Rob might be able to comment with direct experience of working in Australia. But labour and consumption taxes in Australia on high earners, medical professionals, they’re pretty tough compared to New Zealand. (TB 45% top rate plus 2% Medicare).I would have thought, but I don’t know what your experience is Rob.

RM it’s not just Australia, we’re becoming more global, aren’t we? So almost every country is a neighbour of one sort or another these days. The other thing is these people are incentivised to find these loopholes. And having lived, having operated and worked in Australia for six years, they’ve seen wealthy people find loopholes there too. So that that won’t go away.

TB It’s our job to find them, to be frank.

RM Yes.

RO The government legislates for them. You get tax free superannuation in Australia, or 15%. We’ve got to get away from this idea we can tax our wealth. Our problem is, as we’re next to Australia, is Australia becoming wealthier than we are. It’s attracting our nurses, our doctors, our policemen, our police persons and what have you through higher wages. We’ve got to increase our wage level and our productivity, and we don’t do that by sitting around and inventing new taxes.

TB But do we change the incidence of tax, so that capital gets diverted into more productive areas?

RO I give you the example of houses. I agree with that.

GN Our effective marginal tax rates, in those doctors, nurses and policemen, if you go across to Australia and look at those, yes, the incomes are definitely higher 30 or 40%. But I think there’s a tax dynamic in there as well for those people. Because we’re sweating our labour incomes, particularly in those low ends.

Robin has often said this, the worst tax rate we’ve got in New Zealand is the 30% rate at $48,000. Which is huge, it kicks in below the median income. So, I think there’s a tax dynamic in those migrations of doctors, nurses and police as well.

What about inheritance taxes?

TB The $48,000 threshold is a shocker. A final point on this housing. I think you’re right, politically a capital gains that incorporates the family home is impossible. You’re not even a one term government with that. But does that perhaps point to the need – and this is where the IMF come in – is that maybe that’s picked up through an inheritance tax at a separate point. Inheritance taxes, estate duty used to be quite significant. It was 5% of government revenue way back when in 1949, and they were one of the first taxes we introduced here. But they’ve declined over time around the world, but now there seems to be particularly with this, the wealthiest generation in history – and I think all of us are members of the Boomers – are starting to pass away, and there’s a huge transfer of wealth about to happen. And governments are looking at that.

RM Can I bring the conversation back to where I was about what percentage of GDP should tax be.

Because we are straight into, in essence, the tapestry of taxes. And what lurks underneath the motive for that conversation is really redistribution. Because a lot of the motive in the conversation that we’re having is about getting feathers off particular geese, and about certain thresholds and the rest of it.

The starting point ultimately is what does the country need by way of revenue as a percentage of GDP now? Now, if you’re arguing that actually New Zealand’s got a big problem of injustice or inequity because the rich are basically getting away with it, is a bit of a different to back from where we came from and earlier on in our conversation. Geof, to be fair, has identified redistribution as a goal. So he’s been consistent in that regard.

But I think this demonstrates why it’s so important to first of all ask yourself what you’re trying to do with your tax system, and if it is about revenue and getting a particular percentage of the GDP, then I think that these debates about estate duty and wealth tax and land tax are red herrings.

The 1% of GDP, for example, Geof, that you’ve mentioned in the question we’re asked to consider through a new tax, does not undermine my general principle of the broad reach and impact of GST and income tax. In fact, you guys (Robin and Geof) were both on the Cullen Review and you actually, in the report that came out, compared a 1% increase in GST with the capital gains tax and it kind of blew it away. That demonstrates my point that the Broad Base reach of GST and income tax can do everything that you’re trying to get out of these, peripheral and miscellaneous taxes. The only thing that’s left standing as to why you want to do it, is redistribution.

RO I’m OK with that, obviously. But getting on to death duties, estate duties, they have an interesting history. Other countries have them. People have different ideas about bequests and motivation. You know, how important it is to give money to the children. You’ve got Warren Buffett, who honestly gave each of his children 10 million and that’s it. Well, 10 million seems like a nice little nest egg, but in Warren Buffett’s terms, that’s just rounding. Bugger all in bequest terms, Other people will die for it. Literally, they will fight. It is enormously powerful. They will do anything to avoid death duties.

When we used to have them, that was the area of massive tax planning. It was the beginning of it all – avoiding death duties was a massive industry. And you think it’d be easy to do. Well, you’ve got to have gift duties as well, otherwise people just give it away to the kids. And you end up with Inland Revenue, as it used to do, roaring around, stamping every gift that’s made in the country, every Christmas and what have you, and determining they’re not subject to gift duty.

Massive amounts of bureaucracy involved. They are not easy taxes and I’ll just finish with the history of the end of death duties in New Zealand.

It started off with Australia. Death duties were limited to the state governments. When Queensland got rid of its death duties Victoria and New South Wales and the rest of Australia followed suit. We followed thereafter. Because anybody was going to go to the country which didn’t have it.

Death duties have got some appeal to people, I understand the issues. It’s very appealing when people don’t have any bequest, motive to actually tax a windfall gain. The only reason they are working, building their business is for the children and grandchildren. These people will react massively to its reintroduction.

[This is an edited part of the full podcast which readers are encouraged to download and listen to at the link at the top of this page.]

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

What makes a good tax system and where does New Zealand presently sit?

The current broad-base, low rate approach is under strain. How do we address that? What can we do to keep/ preserve that as far as possible? And more.

Terry Baucher: It is my very great privilege this week to be joined by three of the titans of tax in New Zealand, Rob McLeod, Robin Oliver and Geof Nightingale.

Rob, or more correctly Sir Robert McLeod, KNZM is one of THE gurus of New Zealand tax, has been involved in tax policy at the highest levels since the 1980s. A former chair of EY, he was chair of the 2001 McLeod Tax Review and was also a member of the 2010 Victoria University of Wellington Tax Working Group. He’s currently a consultant, although still very much involved in the tax policy world. He was knighted in 2019 for services to business and Māori. Kia Ora, thank you for joining us.

Robin Oliver, another of the gurus of New Zealand tax, until he retired from Inland Revenue, was Deputy Commissioner of Inland Revenue and head of Tax Policy where he advised the 2001 and 2010 tax working groups. He is now a partner in tax consultancy Oliver Shaw and was a member of the last Tax Working Group. Robin was made a member of the New Zealand Order of Merit in 2009.

Geof Nightingale recently retired from PwC, and when he’s not cycling the length of the South Island, is an independent tax consultant. He was a member of both the 2010 and 2019 tax working groups. Thank you again to all of you for joining us.

What makes a good tax system and where does New Zealand presently sit?

We’ll begin with what was asked at this year’s International Fiscal Association Conference. The three of you spoke on the topic of what makes a good tax system. What does make a good tax system and where does New Zealand presently sit? Rob, would you like to lead off?

Rob Mcleod (RM) Thanks, Terry. Well, I think at its core tax is mainly about raising revenue to finance government programmes. It’s true that tax has peripheral tasks as well, like you know, correcting for market failure. If we think about carbon taxes, the primary purpose of that kind of tax is really to moderate adverse behaviour in the economy, which is not is not really a revenue raising objective. Some would also argue that taxes are there to achieve redistribution goals, transfer income to those that are in need. That too is not so much a revenue raising goal.

“At its core tax is mainly about raising revenue to finance government programmes”

But if you go to the real reason why income tax exists in countries, it’s actually to raise revenue for governments. If governments didn’t need revenue, you wouldn’t have taxes. And chances are you wouldn’t have such a major regime doing these other two things, like corrective taxation, like carbon taxes, or trying to redistribute income without the agenda of raising revenue. I would argue that we wouldn’t have tax systems on the scale that we have them doing those other things. So, I believe that raising revenue is the primary goal of a good tax system and doing it at least cost would be my formulation.

Robin Oliver (RO) I agree with Rob, even more so, that a good tax system is one that works. It raises money for the government. That may seem obvious to people, but you can’t have taxes which fail to raise money. Margaret Thatcher’s poll tax failed to raise money. It was a failure.

“You’ve got to really focus on raising money at least cost”

So it has to raise money at least cost to society and that’s admin costs, compliance costs, but overall economic costs. The cost of disincentivising people from work and savings and so forth. People think that’s “blah blah blah blah” but the estimates in New Zealand and Australia, and used by the Australian Treasury, is that twenty cents in every dollar of tax is lost in economic costs. In other words, not quite, but basically lost output, lost wealth for the country. So, you’ve got to really focus on raising money at least cost.

Rob mentioned redistribution. I think redistribution’s got nothing to do with a good tax system. Government raises money to do good things – health, education, welfare. We’ve lost focus on what tax is about. We’ve got diverted into all sorts of ideas that it could be used for. No, it’s about raising money, at least cost. Every tax proposal should be looked at “Is this the way we could raise some money, effectively, at least the cost to society.”

TB Thanks, Robin. Geof, I think you have a slightly different take on the redistribution issue and I note that the IMF was talking about redistribution in one of its papers recently

Geof Nightingale (GN) Well, Terry, I’d largely, and violently agree with Rob and Robin that the primary function of a good tax system is to raise the revenue that government needs. But it’s how it goes about that where I might differ.

There’s a couple of backgrounds, opening points I’d like to make, and the first is I think it seems, really uncontroversial that our modern democratic states with tax systems and, you know, rule of law-based things. They’ve done more than anything that’s ever been tried to lift living standards. So, broadly, I think they are a good thing that the tax status policy people might call it is a good thing.

“You can only tax by consent”

The second point is, that in those democracies, it’s really important for tax policy people to acknowledge that you can only tax by consent. I mean we impose taxation through the rule of law and through enforcement. But in the end people vote on taxes and people vote governments in and out and tax is often a key election thing. So you can really only tax by consent.

So, whatever the theory may tell you, you have to – I’ve learned over many years now – bring the public with you. That’s the job of the politicians, not the policy people. The policy people have to accept. That general consent point is really important when you start talking about the future of tax in New Zealand.

And then the third thing is there’s no such thing as a perfect tax system and as Robin pointed out, we navigate it, every tax policy choice is a bunch of trade-offs, and we navigate those trade-offs with some well-established principles. You know, equity efficiency, administration etcetera. And those principles can never be applied scientifically. In the end, they come down to, in my view anyway, value judgments at the margin, and that’s where the politics comes into the tax system as it as it should be.

So what is a good tax system? Well as Rob and Robin said, primarily one that raises revenue with the least cost to society. And there are secondary objectives, and those are the distributional impacts. I think those are important for policymakers to take into account. And I think they feedback around into the consent of citizens to be taxed and and the fundamental democratic process actually. and. Most OECD countries, in fact all I think, have progressive tax systems by and large and general voting patterns suggest that that’s the majority view of life across OECD democracies.

The problem with behavioural taxes

Other secondary objectives that Rob and Robin mentioned with behavioural changes, carbon taxes and things and those are very specific instruments of public policy, and they might raise some short term revenues. But they shouldn’t be relied on for long term revenues and it’s almost a different category of taxation to the general tax system because if they work – those behavioural taxes – the revenues will often dry up, will be reallocated into the areas that they’re trying to change.

TB That’s something we’re actually seeing with the tobacco excise duty. It worked and now revenues are falling and now that’s sort of a hole in the finances.

RO But if that works, yeah, it’s the same as environmental taxes. You know you have taxes on degradation of the environment. And if you don’t degrade the environment, you get no money. And it’s perfectly fine. They work, but back to Geof’s point. I totally disagree that redistributions got anything about it. You clearly have to have a democracy; in a democracy you have to have consent. I agree with that. You have to have consent to make the tax system work because of voluntary compliance and all that.

Poll taxes – efficient but unworkable?

But the purpose of tax is to raise the money in the most cost-effective way. And I give the example of that is the poll tax, Margaret Thatcher’s poll tax. I mean poll taxes are loved by economists because it’s thought of as being efficient. But it doesn’t work. I mean if you want to raise New Zealand’s government revenue by poll tax you’ve got to raise about $30,000 per individual. You’re not going to go out to people in South Auckland, a family household, and demand $100,000 from them please. I mean, they don’t have it. And there’s no point in demanding money, which people just don’t have.

And that’s why even an efficient tax system, inevitably given the level of government expenditure we have, will need to be progressive. Because you know the lower income earners just don’t have money to pay the tax that the government needs. But again, the point is, you’re really trying to raise money to spend on health, education and welfare and you want to do it at least cost. And forget about trying to have a secondary objective of redistributing income, that just leads you into bad taxes. And that’s led us from having a good tax system to one which is now pretty awful or going that way.

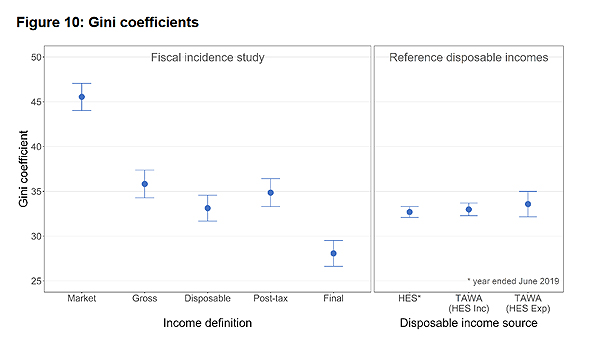

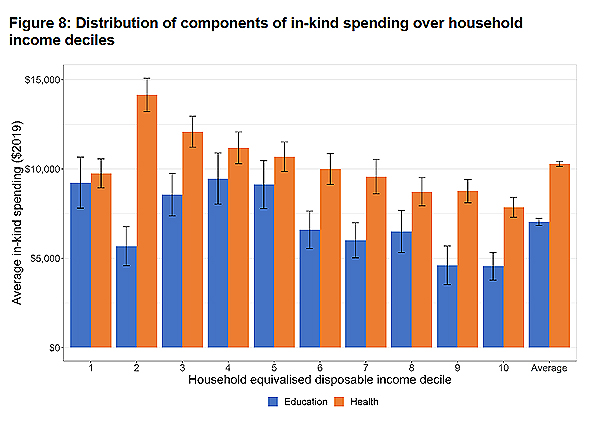

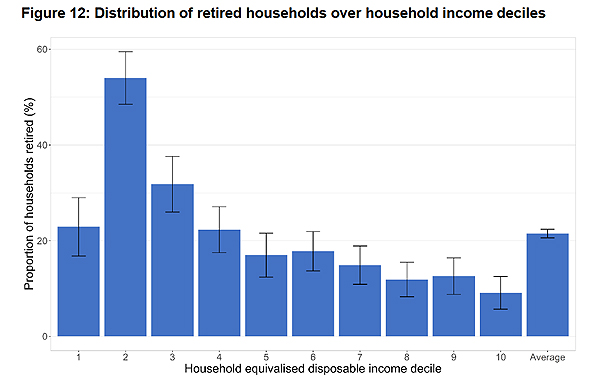

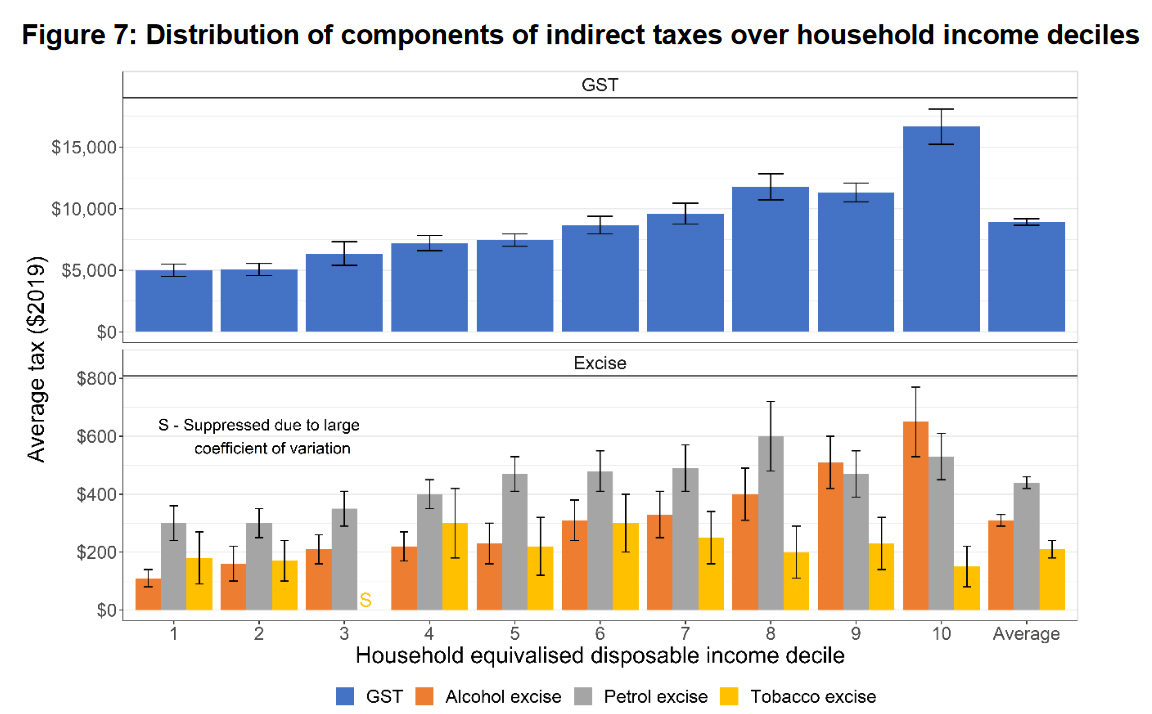

TB It’s a hell of a topic that. I mean, there is always a redistributive effect of tax, and the recent Treasury paper on the fiscal incidence of taxation was quite interesting in that regard.

RO Yes, good paper.

What about ring-fencing taxes for certain objectives?

TB The Treasury paper showed health and education benefits going to different deciles. They’re essentially redistributed within the system. So just a quick thought about these behavioural taxes Do you actually see much of a role for ring fencing? Tax takes such as, for example, environmental taxation that we raise these, we’re trying to encourage better behaviour, but the funds don’t go into the general pool but are used to mitigate the impact of climate change. Is there a role for that Rob?

RM Yes, I think I think there is. We call this hypothecation and we’ve had hypothecation in the area of fuel taxes for example, which are put on road users and then reinvested back on to roads at various times. But over time, you know, I think that money was ultimately then sent to the consolidated fund.

RO I mean, money is fungible. And therefore, putting it in one pot versus many pots, you can have an argument about whether that’s effective. I think ultimately if governments ensure there is a correlation between how they apply the funds and the taxes they raise, and hypothecation is a solid principle to get that correlation. But I think that the more recent view of governments has been that they can be relied on to effectively finance it all out of a consolidated pot. So yes, hypothecation is certainly there, and we’ve got examples of it.

Economists hate hypothecated taxes, because it ends up government spending money wastefully and low priority areas, because that’s where the money is. But it does serve a purpose, it provides the right incentives. There’s a case for it you know road user charges, Rob said was a good case in point. And you can make other cases like how do we control the level of health expenditure? Well, you could hypothecate GST to health and if people want to spend more on health, GST goes up and everybody has to pay it, so you can end up with arguments for hypothecated taxes. But the economists really hate them.

GN At the risk bringing distributional effects back onto the table, hypothecated taxes can also be highly regressive, so yes, I’ll just leave that there.

TB Yes, a common hypothecated tax around the world, which we don’t now have but once did, was Social Security. You see that many other jurisdictions had that and we’d had that until the late 60s. I think it was Rob Muldoon who decided stuff this we’ll just get rid of it because it was, as Rob described, was just going into the consolidated fund. But looking way back, it was a quite significant part of tax revenues if you look track the history of tax.

The problem with social security taxes

RO And very important in Europe in particular, and the United States of America. And we are very lucky not to have them. Australia and New Zealand, one of the few OECD type countries not to have Social Security payroll taxes, which are linked with the benefits. The reason for that is it results in peoples’ old age pensions, or whatever you call them – New Zealand super being linked with past earnings.

And that means that the poor are really poor, when they are elderly. And that’s the case in the UK. Everybody gets the same in New Zealand which in my view is absolutely a much better system than using your tax system to provide benefits linked with wages. Which means particularly women who are not always in the workforce, but child rearing, skills get really done over. I think we’ve got a much more equitable system of expenditure on welfare because we don’t have that.

The incidence of tax – who is actually bearing the tax burden?

RM Terry, can I just perhaps take us back to redistribution, I think there’s one important point about redistribution which unfortunately is a bit of a technical point. But it’s one that is overlooked not only by lay persons, you know, people not familiar with technical stuff, but also the tax profession itself. Which is the issue of incidence.

So if you just start with the GST as an example, most New Zealanders wouldn’t accept, and rightly, that the GST is not imposed on them. And yet, if you have a look at who pays the GST, they don’t pay it. The consumers do not send cheques to Inland Revenue. The tax is actually imposed on businesses. As a matter of imposition. When we talk about redistribution, we’re inclined to assume that the tax impact is where the law imposes it, but the key principle that’s demonstrated by the GST example is the market actually takes that tax and spreads it around, arguably like margarine, to all of the stakeholders and sometimes non stakeholders, and the and the contract to be affected.

These are such things as gross ups, if you go and slap a tax on somebody and they’ve got market power, they’ll put the price up of what they’re supplying to others. And in so doing, they’ll pass that tax burden on to others. And this is completely ignored in my view, when people are talking about redistribution, because there’s the assumption that the taxes that are actually imposed by the government, is actually borne by the people who send cheques to Inland Revenue Department, is utterly false. And if you try and unravel that mathematically and work out who actually is bearing the tax, the best you can get to on most of it is estimates including the dead weight loss of the 20% that Robin is talking about, it’s there’s a lot of estimation going on to get to those numbers.

There’s no argument that that economic effect is real, and for me that’s a big undercut of why I don’t buy all the redistribution argument, because it tends to proceed on the assumption that the way the government’s levying the tax will ultimately shape and determine the burden of it.

RO We don’t know a lot about the incidence of tax. But what we do know, it’s almost never born entirely by the person paying it. So, you end up with these studies, like the awful IRD study on high wealth, totally ignoring this fact, just totally ignoring it.

And the classic example of economics in the United States is that you have local body bonds, the interest rate is tax free. It’s a subsidy to like City Councils or what, and the federal government doesn’t tax them.

The high wealth individual – the person on the very high rates – ends up owning all these municipal bonds. They don’t pay any tax. But they’re getting a lower interest rate because they’re bidding up the price of these bonds, which is what’s intended and the local City Council get cheap money. And then along comes a bunch of officials measuring their tax burden and finding it zero. Disastrous. Horrible. Well, in fact, they’re paying it through the lower interest rates on it.

And this happens all the time, all through the tax system. You put taxes up on foreigners, that’s a good idea. Foreigners we don’t like, they’re not voting, and we put big tax on foreigners. They just simply demand a higher rate of return or don’t invest here. We end up with lower productivity, lower wages and the economics is absolutely clear. Put your tax on your non-resident investor, it ends up coming out in lower wages. And that’s exactly Rob’s point. The incidence is always shifting and yet we totally ignore this. The political debate just assumes the world is not what it is.

TB Robin, I think we’re going to see more and more of that. Sorry, Geof, you were about to say something.

GN I totally agree with Robin and Rob on incidence, it’s critical. But it comes back to my opening point that you can only tax through consent, eventually. If incidence is not well understood, policymakers – and it’s very hard and very slippery getting your hands on the concept – but policymakers need to think about it. But if you can’t convey that to voters, then it becomes kind of irrelevant.

I remember Sir Rob’s MacLeod committee and the $1,000,000 tax cap for individuals. I thought was a was a great idea because of that sort of argument that we’d be better off with $1,000,000 than not. But that policy is too easy to attack politically from an equity and a sort of a fairness sense. And that’s what happens in the real world as we all know and that’s why we end up in political arguments around the secondary purposes of the tax system, as opposed to really discussing the primary purpose of the tax system Which is least cost revenue raising for government policy. So, I agree with their incidence comments, but it works both ways, I think.

RM Can I just jump in on that one and just observe that in the McLeod Review where we did recommend that to be honest, I think it’s politicians that say that say no to those sorts of things than not, as opposed to public sentiment. Muldoon made the famous quote that Joe Blog, the average person on the street, wouldn’t know fiscal deficit if he tripped over one. And I think that’s a long way back and things weren’t as sophisticated then as perhaps they are now.

But if you think about the complexities of tax and you think about the extent to which the public is actually engaged with that complexity, I think that you are apt to over egg that interaction. Because ultimately politicians and officials and people like ourselves, there is a leadership role we play and the public follows that leadership.

I think you can observe that in history. The differences between countries and the qualities of their tax system often reflect the differential qualities of officials, politicians, et cetera, that’s going on in those countries. So, while I agree that in the concept of democracy, there’s a public underbelly in debate and voting terms, there’s one hell of a space for leadership and tax policy. Otherwise, we might as well pack our bags and go home. And I think that that is very influential and that’s why these debates and these principles of incidence and so on are important and need to be approached in the way we’re doing it.

RO We can see that with GST. We’ve got a flat rate, a good GST system, world class.

I remember back in the 80s Sir Robert Muldoon, the proposals was put to him about that. And he said, “You mean we’re going to tax water?” And he chuckled, “No way.” We put GST on doctor’s bills. People overseas think that’s just totally astonishing. Yet there’s broad support for what we have in GST, a non-progressive tax. Bizarrely we legislated to make it regressive, but it does meet those economic principles and it’s got widespread support. I mean, politicians keep on arguing for GST on no food, but those proposals get put up and get rejected every time.

Rob McLeod’s suggested alternative to a capital gains tax

TB Rob in your review, you raised the possibility of the risk-free rate of return method (RFRM) as an alternative to a capital gains tax. And we’ve seen that in the Foreign Investment Fund regime. Are you still keen on the idea?

RM The RFRM, the McLeod Review, came largely out of the debate around taxing housing. And this was in a discussion document, by the way. It wasn’t the final recommendation; it was abandoned because of what Robin said. Michael Cullen’s switchboard was blown up by the complaints of from telephone callers and we knew that was a pretty strong signal that no government was ever going to support it.

So, we pulled the plug. But basically, the problem with taxing assets that produce, that give sort of imputed income like your motor car or your house or your washing machine, there’s no cash flow to really measure the income. It’s economic income, but it’s hard to measure. And so, the beauty of the RFRM is that you calculate it effectively as a wealth tax, which is applying a percentage, I think we had 4%, against the market value of the of the equity in the asset. It’s quite important. That’s one feature of the RFRM is you’ve got to work out what you’re going to do with debt, debt funding of the asset. And we came to the conclusion we’re best to deal with that by narrowing the tax onto the equity, which is the total value of the asset minus debt associated with it. Which brings in problems because people then start to plan with where they load their debt, right?

But it was simplicity. If we could have made the income tax work on that kind of asset that’s a superior way of going, if you can make it work. I think the only reason you go to RFRM in substitution is there’s easier compliance and administration for taxpayers and the Inland Revenue. The F|IF regime I think Terry came out of the international regime As the child of the CV, the mark-to-market option.

I think you’re thinking of the FDR [fair dividend rate] in today’s terms is probably the most relevant analogy. Fixed dividend rate which I think did come from a an RFRM logic, although it’s a bit screwy because FDR, the RFRM tax principle is you should apply it at the riskless rate of return, and not at the risky rate of return, which is the way FDR works. And also, no deductions which FDR doesn’t abide by in its various option formats. So the concept is much the same but quite different in detail.

What’s surprising in the tax world now?

TB Is there anything in the tax world that surprises you right now?

RO I would say the wealth tax coming on the table, totally unworkable. According to the papers the last government almost legislated for a wealth tax in the last budget, ??? funding and massive reductions in income tax rates. And that wealth tax was completely unworkable and would never get off the ground. It was a total nuclear bomb on our tax system. The fact that people are seriously talking about totally impractical things is a serious concern.

We’ve got to be adults here. There is no fairies at the bottom of the garden. There is no pot of gold at the end of the rainbow. Grow up. Taxes have to be pragmatic and have to be workable, and trying to measure everybody’s wealth on a comprehensive basis every year is not.

GN I remain surprised by the continued acceptance by middle New Zealand of what I consider to be really high effective tax rates on labour income through the combination of GST and [tax] rates. And I remain surprised when you look at their voting patterns, their general resistance to extending taxation into capital income to address that, so not raising taxes as a percentage of GDP, but recycling revenue, shifting the instance of where slightly where that tax is paid, and it continues to surprise me. I think that message came through the high net worth survey that came out last year, but it was obfuscated by the complexity and some of the methodology problems and the way that survey was done. That’s what I’m still surprised at.

TB I think there’s a general lack of awareness of what effective marginal tax rates are and how they interact and how high they are at relatively low incomes. The 30% rate, $48,000 is a real problem threshold.

RM I suppose I am a bit surprised that the fundamental features of what’s been great for the New Zealand tax system, reappear as controversies, in the political realm particularly. Like the high tax rate. The problem is that Europe’s got high tax rates and Australia’s got high tax rates. New Zealand trying to wave the flag in favour of the low tax rate component of the BBLR has been a challenge. And I think it’s actually been because our neighbour has high marginal rates. And Europe has been very influential on people like Robertson and so on in my opinion in the sense that they buy into the idea that we can have government spending and taxes at 50% plus of the GDP. I should say that I’m therefore not surprised by it. But I think that’s been the big disappointment, that our rates structure has been allowed to sort of get up, and in a sense it’s part of narrow base, high rate [NBHR] thinking. They don’t realise that with those high rates comes the NBHR concept.

The other thing I just touched on is I kind of worry about the international – the OECD and the EU – devices through which large countries bully other countries. And the treaty networks and the BEPS regime and all that sort of stuff is typically a mask for powerful big countries grabbing money off other countries. And the more that happens, that’s a source of corruption and cancer for me and can ripple down and reach these national tax systems. And we’ve had more of that in the last five years than we’ve ever had before.

RO The OECD stuff is probably more two big elephants fighting, the US versus Europe and we get squashed in the middle.

TB I think that’s why the Global South is pushing back and trying to get the UN involved led by Nigeria and Pakistan which are small economies globally, but giant populations, you’re talking over 400 million people between them. They’re not buying into Pillar two. There seems to be pressure building in that area.

What one proposal from your respective tax working groups would you like to see implemented?

RM That’s a that’s a good question. Sorry to be boring, but I think I came back to the broad-based low rate. For Geof and Robin who know me well, I am a bit of a bore-a-thon drum beater on base principles, and the thing that I’ve seen is the base principle lose a bit of its grip in New Zealand in the last decade. We’ve taken our personal and our trust rate to 39%, which I do not like.

It’s the fiscal stuff that’s that this government is arguing that I don’t accept that it’s necessary for that, but that’s another big debate point about understanding how balance sheet management in government needs to be separated from profit and loss account management. I don’t think that those two aspects of the debate are properly worked through. We should take the longer road and the longer term to fix our debt issues, obviously try and avoid them from happening in the first place. But debt is not necessarily needed to be paid immediately. And not to be factored immediately into tax rate design in my opinion, which is a mistake that we’re currently going through.

GN I’ll be boringly repetitive, but I think the extension of income tax to more realised capital gains on a realisation basis and then using that revenue to recycle, I think that’s got equity efficiency benefits. And I also think it helps in some ways to resolve those high effective marginal tax rates around our productive sector of our economy, labour productivity. So that’s still what I would do if we were able to do one thing.

RO Oh, I still like Rob’s RFRM on residential rental and get rid of all these bright lines, interest deductions and ring-fencing rules. The other one Geof raised was seriously considered by the Labour government under Michael Cullen, was that you pay a million bucks worth of tax and you’ve done your bit and go away. An anathema now, times have changed. That was acceptable then it seems, but not now.

It was seriously considered by the caucus at the time. The idea is you get someone come and live in New Zealand and pay a million bucks and fund a Children’s Hospital. Doesn’t seem to me to be a bad idea.

RM Like a hypothecated tax, Robin?

RO I wouldn’t mind if it was hypothecated for good healthcare for children. I think that would be good.

TB Well, I think we’ll leave it there. I want to thank my guests this week, Sir Robert McLeod, Robin Oliver and Geof Nightingale. It’s been fantastic talking with you all. Thank you so much for being part of this.

[This is an edited part of the full podcast which readers are encouraged to download and listen to at the link at the top of this page.]

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Canada loses patience and imposes a Digital Services Tax effective 1 January 2024

Inland Revenue appears to be gearing up for a fringe benefit tax initiative.

Late last week, in response to some questions about a review the charitable exemption that religious organisations enjoy, the Prime Minister responded he was “quite open” to the idea, adding “I’ve actually been thinking through the broader dimension of our charitable taxation regimes…We will certainly be looking at things like that this term.”

The hint that a review of the exemption religious organisations and churches enjoy provoked a testy response from Brian Tamaki, among others which was in turn rebuffed by the Finance Minister, Nicola Willis.

But this is a topic which keeps popping up and obviously people have some concerns about how the exemption operates. It was also reviewed in some depth by the last Tax Working Group.

So what’s the exemption worth?

Putting some numbers around the value of the charitable exemption is a little difficult. Every Budget Treasury prepares a paper on the value what are called “Tax Expenditures” that is specific tax exemptions granted under the Income Tax Act. According to the Tax Expenditure statement prepared by Treasury for Budget 2023,

the forecast value for the year ended 31 March 2023 of charitable and other public benefit gifts given by companies was $32 million. In relation to the donations tax credit for charitable or other public benefits (including to religious organisations), value for the same period was estimated to be $315 million. (Which grossed up at 33% is ~$945 million.)

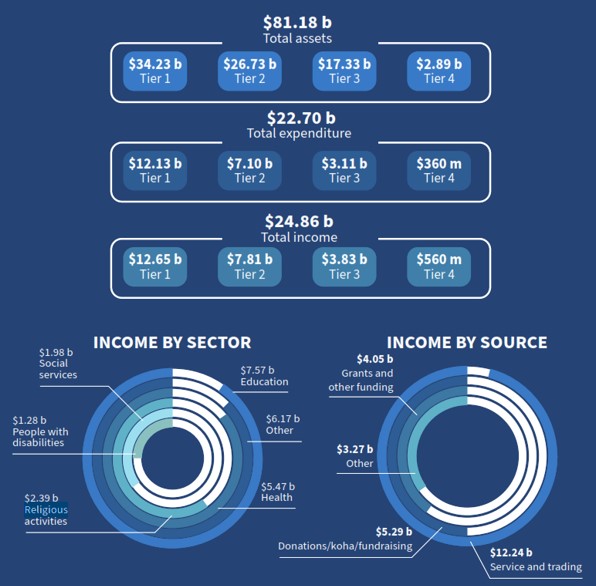

The annual report of Charities Services include a snapshot of the finances for 27,000 charities registered with it. According to the report for the year ended 30th June 2023 the income of the religious activities sector was $2.39 or just under 10% of the total income across all charities.

It’s interesting to consider charities income by source for the same period. $5.29 billion represented donations, koha and fundraising activities. Based on Treasury’s Tax Expenditures statement it appears donations tax credit or charitable donations by companies has been claimed for maybe only a billion dollars of this sum. Interestingly, about half of the total income charitable sector earns during the year comes from services and trading.

Overall Charities Services estimated that the total expenditure by charities was about $22.7 billion. In other words about $2.1 billion of the funds raised were not spent or distributed for whatever reason.

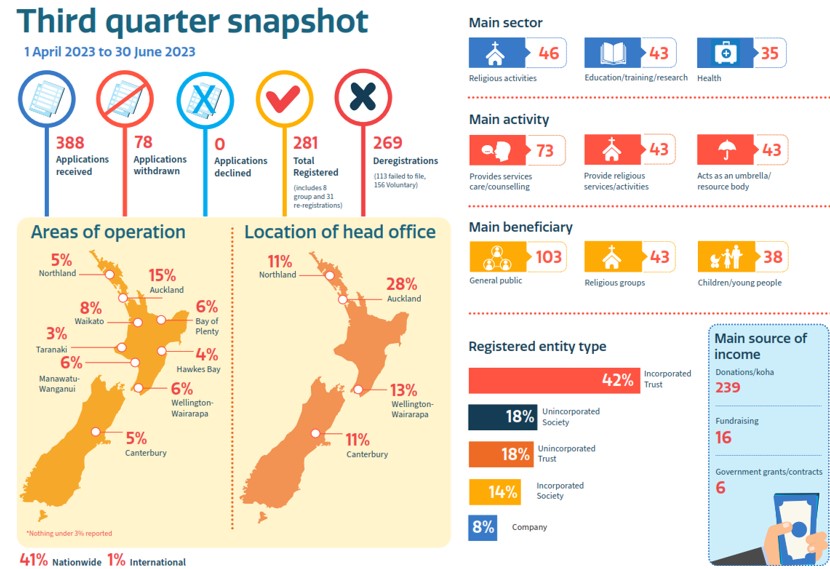

Charities Services also provides a quarterly snapshot of new registrations. The latest available is for the period to 30 June 2023 when it received 388 applications (of which 78 were subsequently withdrawn). Religious activities seem to represent a fairly substantial portion of the new registrations.

What did the Tax Working Group recommend?

The last Tax Working Group took a look at this issue and the best place to consider its views is in Chapter 16 of its interim report which sets out the issues involved.

In its final report the Tax Working Group noted it had “received many submissions regarding the treatment of business income for charities and whether the tax exemption for charitable business income confers an unfair advantage on the trading operations of charities.”

The Tax Working Group responded as follows:

“[39] It considers that the underlying issue is more about the extent to which charities are distributing or applying the surpluses from their activities for the benefit of the charitable purpose. If a charitable business regularly distributes its funds to its head charity or provides services connected with its charitable purposes, it will not accumulate capital faster than a tax paying business.

[40] The question then, is whether the broader policy tax settings for charities are encouraging appropriate levels of distribution. The Group recommends the Government periodically review the charitable sector’s use of what would otherwise be tax revenue to verify that the intended social outcomes are actually being achieved.

I think if the Government is going to review the charitable sector, and religious organisations in particular, the Tax Working Group’s recommendations will be starting point. In April 2019 when the last Government responded to the Tax Working Group’s eight recommendations on charities it noted that Inland Revenue’s Policy Division was already working on five of the recommendations. Two of the remaining three were under consideration for inclusion in Inland Revenue’s policy work programme. The other, in relation to whether New Zealand should apply a distinction between privately controlled foundations and other charitable organisations, would be undertaken by the Department of Internal Affairs, which oversees Charities Services. It’s likely the COVID pandemic disrupted this proposed work programme.

We may get a clue as to the Government’s thinking in next month’s budget, but I think the Government’s focus will be on getting its tax relief package out of the way first so Inland Revenue’s resources will be applied there. The Government and Inland Revenue may then look at this exemption, but I imagine given the fuss and general controversy around such a move, it’s probably relatively low priority. Maybe we’ll see something in the Budget.

Canada loses patience and introduces a digital services tax

There was an interesting development in the Canadian budget, which was released earlier this week. The Canadian Government has decided to push ahead with the introduction of a digital services tax (DST) on large tech companies. Over a five-year period, this was expected to raise ~C$5.9 billion (about NZ$7.3 billion).

Canada had held off for two years to allow for the conclusion of the international negotiations on Pillar 1 and Pillar 2 to conclude, but they’ve dragged on with no clear conclusion in sight. The Canadians have therefore decided to push the button on a DST commenting:

“In view of consecutive delays internationally in implementing the multilateral treaty, Canada cannot afford to wait before taking action….The government is moving ahead with its longstanding plan to enact a Digital Services Tax.”

The tax would begin to apply for the 2024 calendar year, with the first year covering taxable revenues earned since January 1st, 2022. Understandably, this has provoked a pretty vigorous reaction from the United States, where the headquarters of all these tech companies are situated.

What does that mean for us down here? Well, again, we may find out more in the Budget. The Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill which was enacted just before 31st March included legislation for our digital services tax. The Government is therefore in a position that it can watch to see if other countries follow Canada’s lead and then decide whether it should follow suit.

The whole purpose of the digital services tax legislation is to act as a backstop in the event the Two-Pillar solution does not reach a satisfactory conclusion. At the moment negotiations are stalled thanks to vigorous push back by the the companies most affected, such as Alphabet, the owner of Google, Amazon and Meta, owner of Facebook. It’s interesting to see this Canadian move and I wonder if other countries will push ahead with their own DSTs. There are quite a number lot of digital services taxes around the world, with many on hold pending the outcome on the Two-Pillar negotiations.

Taxing Google to help New Zealand media?

Just as an aside, as is well known the media in New Zealand is in desperate financial straits and a question that keeps coming popping up is taxing the digital giants more effectively. That’s because a substantial portion of the advertising revenue that in the past went to New Zealand media companies is now going overseas in the form of (little taxed) various licence payments and fees for services to the the likes of Alphabet and Meta. Watch this space I think things are about to get very interesting.

Inland Revenue gearing up for fringe benefit tax initiatives?

This week, Inland Revenue consolidated the various advice and commentary on fringe benefit tax advice it’s published over the years under a single link. This seems to me to be further signs that Inland Revenue is gearing up to launch a fringe benefit tax initiative. It follows comments by the Minister of Revenue Simon Watts, in several speeches in which he referred to Inland Revenue’s regulatory stewardship review of FBT released in 2022. I got the clear impression that he, and therefore Inland Revenue were keen to look further at this matter and investigate what revenue raising opportunities may arise through a more through stricter enforcement of the FBT rules.

As a very good article by Robyn Walker of Deloitte noted FBT is nearly 40 years old. It’s a very strong behavioural tax. It exists to stop people converting taxable salaries into non-taxable benefits. So, it never really should be an extensive tax raise revenue raiser.

That said, I think there have been issues particularly in relation to the status of twin cab utes and the work-related vehicle exemption as to whether there is sufficient enforcement going on. My expectation therefore is Inland Revenue is gearing up to launch a number of fringe benefit tax reviews and this small step consolidating its previous commentary and advice into a single space is another sign.

Got an idea to improve our tax system? Enter the Tax Policy Charitable Trust scholarship competition

Finally, this week, the Tax Policy Charitable Trust has announced its 2024 scholarship competition. This is designed to support the continuation of leading tax policy research and thinking and to inspire future tax policy leaders. Regular listeners to the podcast will know we’ve had past winners Nigel Jemson and Vivien Lei as guests, and I’m looking forward to meeting the next batch of scholarship recipients.

Entrants may submit proposals for propose significant reform of the New Zealand tax system, analyse the potential unintended consequences from existing laws and changes, and suggest changes to address them. It’s open to young tax professionals aged 35 and under on 1st January 2024 working in New Zealand with an interest in tax policy. The winning entry this year will receive a $10,000 cash prize. The runner up will receive $4000 and two other finalists will each receive $1000 each.

I look forward to seeing what comes out of this and hopefully we will have the winners on our podcast sometime in the future. In the meantime good luck to all those who enter.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue releases three special reports regarding the changes to the platform economy rules, the 39% trustee tax rate and the new 12% offshore gambling duty

Under the banner “Cut your excuses and sort your tax” Inland Revenue last Monday issued what it called a “last chance warning to the construction sector” to do the right thing and get on top of their tax obligations. The release advises that if people do the right thing, then Inland Revenue will help them. If they don’t, Inland Revenue will find them and start follow up action.

Richard Philp, a spokesperson for Inland Revenue, commented;

“Most people and businesses in New Zealand pay tax in full and on time but there is a core group who don’t. … we also know that while some are struggling just to keep up with the everyday grind, others are actively avoiding their tax obligations.”

Tax evading tradies?

Apparently, tax debt is high in the construction sector and there’s also a fair amount of cash jobs apparently happening in the sector. The Inland Revenue release commented that across all sectors, it gets about nearly 7,000 anonymous tip offs about cash jobs and the like each year noting “Construction is the industry most anonymously reported to Inland Revenue”.

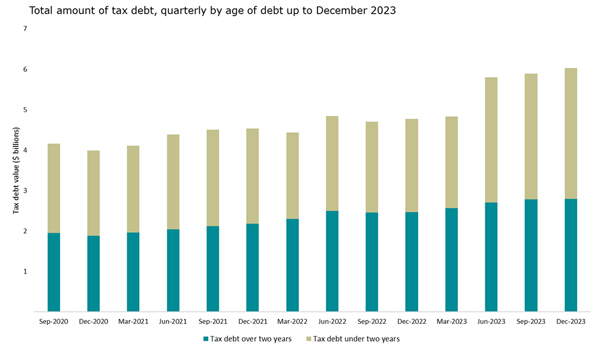

The media release is silent about the extent of the debt within the sector, but we do know from the latest statistics as of 31st December 2023, that tax debt over two years old has increased to from $2.5 billion in December 2022 to $2.8 billion in December 2023.

ADVERTISING

Understandably, with the Government’s books under pressure, Inland Revenue is keen to collect as much of this overdue debt as quickly as possible. This is probably the first of many such campaigns where we will see Inland Revenue taking additional action. And remember, under the Coalition agreement, additional resources have been promised to Inland Revenue for investigation work.

In this particular campaign, Inland Revenue is saying it’s going to issue emails and letters to 40,000 taxpayers in the construction industry who have either outstanding tax debt or tax returns, or both. It then specifies that 2,500 of those will be contacted by text message, asking if they would like to support to get their outstanding tax sorted. There will be a follow up call if the taxpayers they respond that they do want help. Inland Revenue will also be carrying out site visits to key locations across the country.

As I said, this is likely to be the first of several initiatives we’re going to see from Inland Revenue. I would be interested in seeing some specific stats around the proportion of debt and the composition of debt and get an understanding of what sort of businesses are struggling here. It will also be interesting to see how successful this campaign turns out to be.

More on the new GST rules for online marketplaces

Last week I discussed the confusion that seems to have arisen following the introduction of new GST rules from 1st April. These rules affect people who are not GST registered but provide services through such apps as Airbnb, Bookabach and Uber.

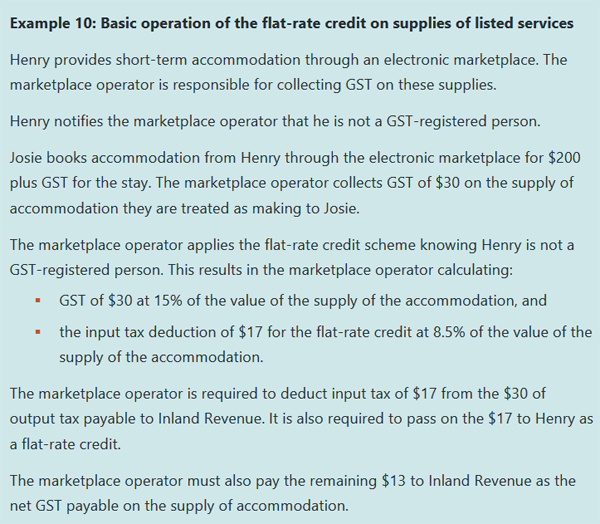

This week, Inland Revenue released three special reports relating to the new legislation and one of these is on accommodation and transportation services supplied through online marketplaces. In fact, this is an updated version of a report previously issued in June last year. The report has been updated to include the changes that took effect as of the start of this month and in particular how the flat-rate credit scheme operates.

Changes to online marketplace operators