Could the US retaliate against a digital services tax?

Last week, in a series of interviews with the press, notably with Newstalk ZB, Finance Minister Nicola Willis dropped several hints about what might be in the forthcoming May 22nd Budget. In particular, she talked about the corporate tax rate, and the possibility of cuts to that as part of promoting the Government’s growth agenda.

Corporate tax rate above OECD average

Speaking with Heather Du Plessis-Allan, Ms Willis commented:

“Well, if you compare New Zealand with the rest of the world, we’re not as competitive as we used to be. Which is to say that our corporate tax level is reasonably high when you compare it to the rest of the developed world.”

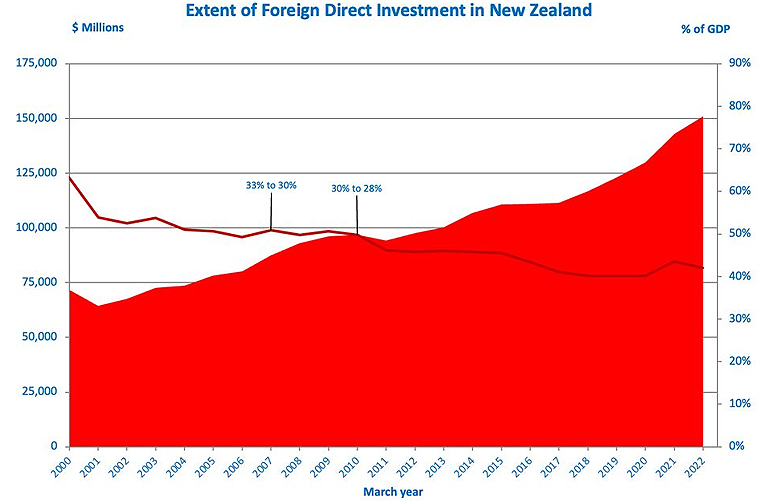

This is a very valid point which comes up frequently in discussions. Our current company tax rate at 28% is well above the OECD average of 24% and has been out of alignment for some time.

New Zealand back in the late 80s under the Fourth Labour Government was actually at the forefront of cutting company tax rates. A particularly interesting action was to align the company tax rate with the top individual and trust rates of 33%. The three basically stayed in line until the election of the Fifth Labour Government and the increase in the top personal tax rate to 39% in 2000.

There have been a couple of corporate tax cuts over the past 15 years or so. In 2007, the rate was cut from 33% to 30% and then in 2010, as part of the rebalancing that took place under Bill English with the increase of GST from 12.5%, the corporate tax rate was cut to 28% where it remained since.

As I’ve discussed previously, there has been a long running global trend towards lower corporate tax rates. But that has slowed in recent years, first because of the effect of the Global Financial Crisis and secondly, the fiscal shock to government finances because of the COVID-19 pandemic. As a result, according to the OECD in 2023, corporate tax rates rose generally across the board. Nevertheless, we are out of sync at the headline rate level.

More to investment than the corporate tax rate and will it work?

A lower corporate tax is undoubtedly attractive. However, the tax rate needs to be seen in context with what other incentives are available. Overseas companies and investors are very focused on what else might be on the table. A lower company tax rate would certainly be attractive, so the suggestion has been met with enthusiasm by some. Others are a bit more sceptical. Economist Ed Miller noted that when the effect of the corporate tax cuts in 2007 and 2010 are considered there does not seem to be any significant increase in foreign direct investment as a result.

The last tax working group didn’t see overwhelming evidence to support the theory that lower tax cuts at lower corporate tax rate would attract investment.

Problems and an alternative

There’s a flip side to this though, and it’s tied into the Government’s intention of restoring a surplus. Our corporate tax rate is not only above the OECD average, but our corporate tax take is also high by world standards. According to OECD statistics, 14% of the total tax receipts in New Zealand for 2022 came from company tax, whereas around the OECD the average is 12%.

So, if the Government, in an attempt to boost economic growth, is going to cut the corporate tax rate, it must then look at other alternatives to replace the lost revenue. One of the things it did back in 2010 and which it has already repeated, was to remove depreciation on all buildings. Depreciation for commercial buildings was restored under Labour but then removed again from the start of the current tax year on 1st April 2024.

A counter argument to the Government’s proposal for corporate tax cuts would be that enhanced depreciation allowances, including restoration of commercial building depreciation, which would include factories, might be a more effective approach than across the board tax cut.

How to replace lost tax revenue?

But if the Government is thinking of a corporate tax cut, and that does seem to be the case, what counter measures could they take to ensure that it is not fiscally too draining on the resources? One option might be that the availability of imputation credits may be restricted. For example, it might be that you can elect to have a lower corporate tax rate, but you imputation credits are no longer available to for shareholders.

As an aside, imputation (sometimes called franking) credit regimes were very popular during the 1980s, but gradually fell out of favour over time, mainly because, or in part because the European Court ruled that imputation credits or franking credits have to be available to all shareholders resident in the EU. After the German government lost this case its response was to heavily restrict the use of franking credits.

Change the tax treatment of Portfolio Investment Entities?

Another option might be to review the taxation of portfolio investment entities held by persons with effective marginal tax rates above the 28%. To quickly recap, Portfolio Investment Entities (PIEs) have a tax rate of 28%, equal to the company tax rate, which is also the maximum prescribed investor rate for individuals. So, there is actually a tax saving opportunity for individuals whose other income is taxed above the 28% rate for PIEs.

The Government might look at this, decide that will no longer apply and instead income from PIEs will be taxed at the person’s marginal rate. That could raise sufficient sums to partially offset the effect of a lower corporate tax rate.

The Finance Minister also mentioned reforming the Foreign Investment Fund regime, which is currently being considered by Inland Revenue and made some encouraging sounds about that potentially being an option.

We shall see. No doubt there’s a lot of work going on in Treasury and Inland Revenue looking at these options. All will be revealed in the Budget on 22nd May.

A threat to our Digital Services Tax

As covered in our first podcast of the year, one of President Trump’s initial executive orders withdrew the United States from the OECD Two-Pillar international tax deal. I drew attention to the second paragraph of that Executive Order, which directed the US Treasury to consider taking actions against other jurisdictions for tax actions which are potentially prejudicial to American interests.

Vernon Small, who was an advisor to the former Minister of Revenue, David Parker, now writes a weekly column in the Sunday Star-Times has picked up on this point noting that “Treasury has budgeted to rake in $479 million between January 2026 and June 2029 from a 3% Digital Services Tax (DST) on tech giants like Google and Meta.”

This, according to Small, “is an heroic piece of forecasting given current uncertainties and the provision for delaying collections until 2030 if progress is made on a multilateral approach through the OECD.”

And then the crunch point:

“Trump has bosom buddies in high places in the industry with Elon Musk first amongst them, and Mark Zuckerberg making a play for the new US administration’s affections.

Trump has promised to retaliate against discriminatory or extra-territorial taxes aimed at US interests. So the DST could be a prime target.”

Vernon Small is underlining the potential threat to our revenue base and our sovereign right to tax. If the OECD deal does fall over there are a number of countries including Canada, no longer America’s best friend, it seems, with DSTs ready to go. So there’s a whole potential for a tax war.

The Trump threat to tax administration

But equally worryingly, coming out of the United States is something about the question of bureaucratic independence from the executive. This might sound an arcane issue but it’s actually quite important to the independence of tax authorities.

One of the first actions of the Trump administration was to sack 17 Federal Inspectors-general. There’s also a move to put all Federal Government employees on the basis that they serve at the pleasure of the President. This would mean that an employee could be fired without the need for cause as the American terminology puts it.

Project 2025’s Schedule F

The implications of this have been picked up by Francis Fukuyama, the author of the famous The End of History essay written in the wake of the collapse of the Soviet Union and the end of the Cold War.

Writing for the Persuasion Substack under the title Schedule F is Here (and it’s much worse than you thought) Fukuyama wrote:

‘ “For cause” protection means that the official cannot be removed except under specific and severe conditions, like committing a crime or behaving corruptly. And now many individuals have been moved, in effect, to Schedule F because they are said to serve at the pleasure of the President.

Consider what this may mean if Trump hand picks a new Internal Revenue Service chief, that individual can be pressured by the Government to order audits of journalists, CEOs, NGOs and NGO leaders. Removal of Inspectors General will cripple the public’s ability to hold his administration accountable.’

Trump’s decision to move all Federal employees to Schedule F status is a step towards autocracy. What perhaps we all need to keep in mind is that the separation between the Commissioner of Inland Revenue and the Minister of Revenue is actually incredibly important. Yes, at times the Inland Revenue might do something which probably might embarrass the Minister of Revenue, but he cannot directly intervene in Inland Revenue’s operations.

A key part of a well-functioning democracy is that civil servants can act independently from their nominally political superiors. Fukuyama is right to say we should therefore have some concern coming at what’s happening in, in the United States because it does seem to be centralising power very rapidly around the President. The .potential for mischief is therefore enhanced as a result, and don’t think that such a step ultimately doesn’t have tax consequences.

Latest on the changes to the United Kingdom ‘non-dom’ regime

On a more positive note, last year I discussed the changes to the so-called ‘non-dom’ regime in the United Kingdom. This is where persons who are not domiciled in the UK have a special basis of taxation. Basically, they’re not taxed on income and gains which are not remitted to the UK.

This is a significant concession which is ending with effect from 5th April this year when it will be replaced by something which is more akin to our transitional resident’s exemption. This is pretty important for the approximately 300,000 Britons like me who’ve migrated here, plus the significant number of Kiwis who have assets in the UK or family going to the UK but have retained assets here. All of this group are potentially within the scope of these reforms.

There’s been a fair amount of push back on the reforms together with concerns that there will be a flight effect as wealthy, ‘Non-doms’ leave the UK. The UK Labour Government has been under pressure to make some changes to the proposals.

In response, the Chancellor of the Exchequer (Finance Minister) Rachel Reeves announced a concession (ironically at the gathering of the super-wealth at Davos) which will increase what’s called the temporary repatriation concession.

This concession will allow non-doms a three year window to pay a temporary repatriation charge on designated foreign income and capital gains so that they can subsequently be remitted to the UK without any further tax. The temporary repatriation charge will initially be 12% before rising eventually to 15% in the year ended 5th April 2028. For comparison, without the concession remitted income would be taxed at rates up to 45% and remitted capital gains would be subject to capital gains tax at 24%.

There’s a lot of opportunity here for potential tax savings for those who could be affected or will be affected by the proposed change to the non-dom regime. We’re still working through all of the implications but we will be updating our clients and bringing you developments as they arise.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Potential big change for US citizens living abroad

Latest IR consultation

Last week, with immediate effect, the Government announced changes in visa conditions, which will allow visitors to work remotely for an overseas employer/client during a visit to New Zealand. This change will affect all applications received from 27th January. It includes tourists, people visiting families together with partners and guardians on longer term visitor visas.

A faster growth track

Basically, the changes are designed to encourage digital nomads to come here and enable them to carry on working for their overseas employer without breaching their visa conditions. As Nicola Willis in her role as Minister for Economic Growth explained in the accompanying press release “The change is part of the Government’s plan to unlock New Zealand’s potential by shifting the country onto a faster growth track.”

These new visitor visas are subject to the following conditions: the visa holder cannot work for a New Zealand employer, nor can they provide goods or services to people or businesses in New Zealand, nor can they do work that requires them to be physically present at a workplace in New Zealand.

What about income tax?

What difference, though, does the new visa make from a New Zealand income tax perspective? The short answer is ‘not an awful lot.’ Much of this possible digital nomad activity is already within section CW19 of the Income Tax Act 2007.

Under that provision the income that a non-resident person derives from performing personal or professional services in New Zealand is exempt if the visit is for 92 or fewer days, the services are performed for a person who’s not resident in New Zealand and that income is taxable in the jurisdiction in which the person is resident. This would typically capture most of activity of a digital nomad.

Section CW 19 is a long standing provision and, as the New Zealand Immigration announcement noted, the 92 day exempt period can be increased to 183 days if the visitor is tax resident in a tax country with which we have a double tax agreement.

As the Immigration Minister Erica Stanford noted, updating these visitor visas reflects the realities of current modern flexible working environment. It’s probably a good move to bring the visas up to date and make clear that it’s generally not a major issue if you are working remotely when visiting and are not in breach of any tax obligations.

Keep in mind the 92-day exemption in section CW 19 is for employees only, it does not apply to any self-employed person who might provide goods or services to people or businesses in New Zealand.

Yes, but what about Taylor Swift?

The other group of people who aren’t covered by the section CW 19 exemption are ‘public entertainers.’ Which means that if we ever did manage to get Taylor Swift here, theoretically the earnings that she made from any concert would be taxable in New Zealand. As an aside there are all sorts of very interesting and complex tax rules around entertainers.

Overall, it’s an interesting move which seems to now bring our visa practices in line with what’s happening globally. It reflects that, because of the greater interconnectivity available now people have quietly been working remotely, effectively acting as digital nomads without actually realising that they may have been in breach of their visa conditions.

In any case, if the person has been here for under 92 days, then generally speaking, they shouldn’t be in breach of any of their tax obligations. As I said an interesting move and no harm clarifying the visa situation. What the economic impact will be, who knows.

An end to citizenship based taxation for US citizens?

In our last podcast of 2024, we discussed Inland Revenue’s paper on changing the Foreign Investment Fund (FIF) regime to make it more attractive for migrants. One of the issues the paper discussed was how the FIF regime created headaches for American citizens and Green Card holders tax resident in New Zealand but who still have to file U.S. Federal tax returns. The paper was proposing changes that might help deal with the essential double taxation issue for these taxpayers.

It so happens an Illinois Republican Congressman, Darren LaHood, has introduced the Residence-Based Taxation for Americans Abroad Act, which would implement a residence based taxation system for U.S. citizens currently living overseas.

LaHood’s press release doesn’t mention it, but I’d be very curious to know exactly how much tax these expat American citizens pay in the US.

The preamble in the press release notes that the United States is the only major country that uses citizenship based taxation. According to recent estimates, there are about 5 million U.S. citizens currently living aboard. Based on the last census there are over 30,000 US born persons here in New Zealand.

LaHood is also a member of the highly influential House Committee on Ways and Means, (their equivalent of the Finance and Expenditure Select Committee) so perhaps this is a serious move. This bill could also gain from the general tax cutting mood of the new Trump administration. We’ll be interested to see how much further this goes.

In the meantime we’ll also be watching for progress on Inland Revenue’s proposals to try and deal with the anomalies the FIF regime creates for U.S. citizens resident here.

New Inland Revenue guidance on depreciation

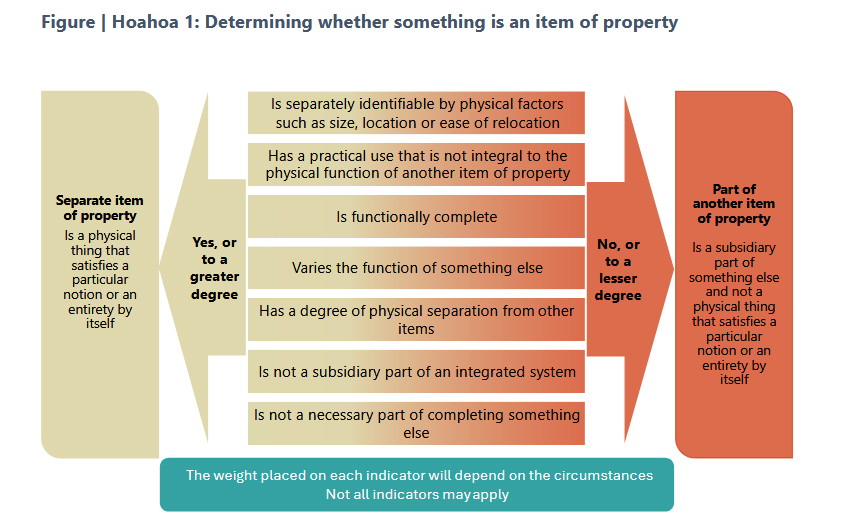

Finally, Inland Revenue as always has been busy pushing out guidance and draft consultations on issues. One which caught my eye and will be worth perhaps thinking further about is Interpretation Statement IS25/03Income tax. Identifying the relevant item of property for depreciation purposes. There’s also an accompanying fact sheet which is always very helpful.

Our very detailed tax depreciation rules system rules have numerous depreciation rates available so it’s often a worthwhile exercise identifying what assets are involved and maximising the available depreciation.

The Interpretation Statement therefore provides general guidance on how to identify the relevant item of property when applying the depreciation rules. The key issue is determining whether the item is physically distinct from a wider asset of which it might from a part.

In determining this you would first consider its location or size, whether it’s integral to the physical functioning of a wider asset and the degree of physical attachment to other related assets.

Secondly, is the item largely functionally complete, in other words, can it function on its own? That doesn’t necessarily mean that it has to be self-contained or used separately, but could it function on its own??

Thirdly, does the item vary the function of another item? What this means is two items will remain separate items where one varies the function of another item, enabling it to perform more specialised function.

The Interpretation Statement provides a few examples together with a useful flow chart.

A key part of the analysis is it always comes down to a question of fact and that means that there will be different outcomes for apparently similar situations.

The Interpretation Statement contains links to other Inland Revenue guidance on depreciation related issues. All this is very useful because in the run up to the end of the tax year on 31st March, we often have situations where clients are looking at investments and wanting to maximise depreciation.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

President Trump was inaugurated for his second term last week, and he swiftly set about implementing his agenda. In his inauguration speech he remarked “America will no longer be beholden to foreign organisations for our national tax policy, which punishes American businesses.” This prompted me to ask on LinkedIn what the potential implications could be for the OECD Two Pillar agreement?

Repudiating the OECD Two-Pillar proposal

Well, President Trump didn’t wait long to take further action. In fact, pretty much almost immediately he issued a Whitehouse Executive Order railing against the “Global Tax Deal” which “limits our Nation’s ability to enact tax policies that serve the interests of American businesses and workers.” Instead, the Executive Order “recaptures our Nation’s sovereignty and economic competitiveness by clarifying that the Global Tax Deal has no force or effect in the United States.”

The Executive Order goes on to direct the Secretary of the Treasury (the equivalent of our Finance Ministerand the Permanent Representative of the United States to the OECD) to

“…notify the OECD that any commitments made by the prior administration on behalf of the United States with respect to the Global Tax Deal have no force or effect within the United States absent an act by Congress adopting the relevant provisions of the Global Tax Deal.”

So “Shots fired” would be the quick response to that. But it’s Section Two of the memorandum which caught my eye when I looked at it. The Order doesn’t have the technical and legal language you might expect, but it’s written with very much the voice of Trump.

Getting your retaliation in first

Section Two of the Order discusses options for protection from discriminatory and extraterritorial tax measures. It directs the Secretary of Treasury in consultation with the United States Trade Representative, to

“…investigate whether any foreign countries are not in compliance with any tax treaty with the United States or have any tax rules in place, or are likely to put tax rules in place, that are extraterritorial or disproportionately affect American companies, and develop and present to the President, through the Assistant to the President for Economic Policy, a list of options for protective measures or other actions that the United States should adopt or take in response to such non-compliance or tax rules.”

Now that is something that I don’t think many people have yet noted. Basically, it’s a pre-emptive strike at other governments responding to what appears like an almost certain collapse of the OECD’s Two Pillar solution by adopting digital services taxes (DSTs). We’ve introduced (but not yet enacted) that legislation. Several countries such as Canada and France do have DSTs in place as a backstop in case the OECD’s Two Pillar solution fell over.

So now we’re in very interesting times. And the issue is that the large tech companies in particular are the target of the Two Pillar solution. Mark Zuckerberg, the head of Meta, together with the head of Google, as well as Elon Musk, owner of the site formerly known as Twitter, all had prime seats at President Trump’s inauguration. Musk in addition, heavily financed President Trump’s campaign. All now have the President’s ear which will maybe enable retaliatory actions by the US against attempts by other governments to say, ‘Well, wait a minute, without the Two Pillar deal we’re losing revenue ourselves here.” The collapse of the Two Pillar solution could provoke the 2020’s tax equivalent of the notorious Smoot Hawley Tariff Act of 1930, which is often credited with triggering the Great Depression of the 1930s.

What could be the impact in New Zealand?

We are a small player, but from our perspective it’s quite relevant how we tackle the taxation of the tech companies. According to Google and Facebook’s financial statements for the December 2023 year, the two companies probably captured about $1.1 billion in advertising all of which was sent offshore. However, the reported taxable income for those two companies for the 2023 year was just under $28 million before tax.

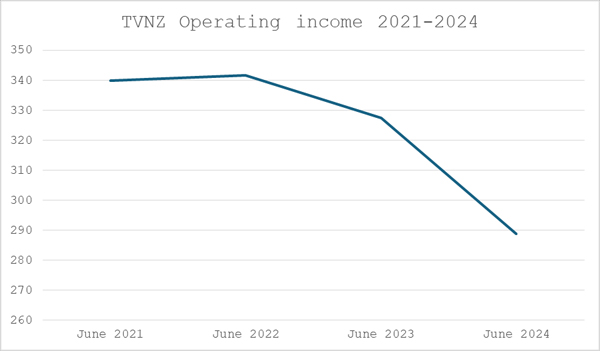

I’m bringing this up because this week NZME announced that it was cutting its newsroom staff by 40, and the financial woes of the media are well documented. Media is struggling as its advertising revenue has essentially collapsed because large chunks of it are now being paid offshore.

If you want to put it in some context of just how bad the problems are for our media, TVNZ’s pretax 10 years ago for the year to June 2015 was $333.9 million.

You’d expect with inflation those numbers would have risen. In fact, for the last three years, TVNZ’s revenue has plateaued at $339.9 million for 2021, $341.7 million for 2022 and $327.6 million for 2023 before falling by $39 million to just under $289 million for the year to June 2024.

The media is in desperate financial states and that has the knock on effect for the Government, because sooner or later it will be called on for some sort of financial support. An option the Government might consider is whether a levy of some sort could be directed at advertising, which is paid offshore.

Sooner or later a New Zealand government will be put in the position where it may have to make an uncomfortable call. Meanwhile, we have the United States making it very clear that it is not going to accept the Two Pillar solution – and would take retaliatory action if it felt its companies’ business interests were threatened by a DST or other levy. It’s not a great scenario and makes for a pretty rocky start to the year.

Raising taxes on the quiet?

Moving on, an interesting story came out over the holiday break in relation to the International Visitor Levy (IVL). Now this was quite controversially increased from $35 per head to $100 from 1st October last year. This move is expected to raise $149 million. The increase to $100 was way above what the tourism industry wanted or what ministry officials recommended. The IVL must be spent on tourism and conservation, essentially, it’s what we term hypothecated – ring fenced for those particular areas.

It turns out that there’s some digging been done by Derek Cheng at The New Zealand Herald, who found out under the Official Information Act that there was quite a bit of ministerial wrangling over how it might be possible to divert or repurpose the IVL income to improve the Government’s overall finances.

Essentially, the dramatic increase in the IVL enabled central government funding which would have gone to the Department of Conservation to be frozen. According to the Herald report this move gave the Government approximately $307 million of ‘fiscal headroom’.

Now there’s nothing wrong with this move although stakeholders in the sector are unhappy with the result. Apparently, the Minister of Finance Nicola Willis wanted to have the IVL funds become part of the Government’s Consolidated Fund where it could be spent as she directed. That was rejected as it would require a change of law.

I think this attempt indicates we’re going to see more of this tactic from the Government. Nicola Willis made a passing comment at a briefing that she’d like to make more use of fees and levies to raise revenue. Looking ahead, the budget in May will give us a really good indicator of how increased fees and levies might be used to basically shore up the Government’s books.

It’s a sleight of hand way of finding additional revenue without explicitly raising taxes directly. Fee increases such as those for the IVL means although the rates of personal income tax and GST remain the same, the Government is managing to extract additional revenue.

So, watch this space. Governments all around the world are trying to do this. In some cases, it’s appropriate, it’s a bit like user pays. But in other cases, you wonder if it’s just a little bit too much financial wizardry for the sake of it.

Inland Revenue targeting collection of tax debt

Unsurprisingly Inland Revenue is continuing its actions we saw last year of increased activity in collecting debt. Stories have emerged since the start of this year relating to its pursuing families for overpaid Working for Families credits.

RNZ ran a story on 20th January about a parent who had incorrectly recorded her relationship status for Working for Families only for Inland Revenue to advise her she now owes $47,000. This was the third such report this year with the other two stories involving tax bills of $9,000 and $24,000 respectively. Inland Revenue’s response is that these are the rules, and it has to carry on and collect the overpaid credits. However, I am aware that there have been issues with parents registering new-born children through the Department of Internal Affairs website resulting in overpayments.

Don’t look at me, I’m only the Minister

When RNZ asked the Minister of Revenue Simon Watts for comment, he responded it was an operational matter for Inland Revenue.

“I’m advised that this issue affects a small number of taxpayers who have received an overpayment due to not providing IRD with the most recent information on their circumstances.”

To be fair to Inland Revenue, as Susan St John, an economist and Child Poverty Action Group member said, the problems were not with Inland Revenue’s application of Working for Families, but with the system itself.

This touches on a point I’ve made repeatedly in the past. Working for Families tax credits begin to be clawed back (abated) where family income is at $42,700 per annum. Above that threshold, Working for Families is abated at a rate of 27 cents for every dollar earned above that threshold. Now that threshold has not been changed since June 2018, and I had a somewhat testy exchange with the Minister of Finance at the Budget Lockup in 2024 over the fact the threshold was left unchanged.

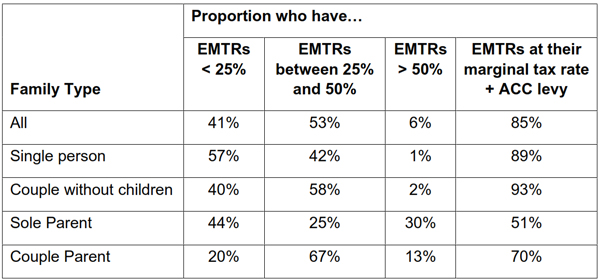

Who suffers the highest Effective Marginal Tax Rates? It’s not who you might think

As a consequence, families on relatively low incomes face very high effective marginal tax rates. Coincidentally this week Treasury released a paper The Cost of Working More: Understanding Effective Marginal Tax Rates in New Zealand’s Tax and Transfer Systems which analyses the impact of effective marginal tax rates on work incentives. The paper examines what happens to a person’s effective marginal tax rate, when their income rises resulting in higher tax rates or the abatement of benefits such as Working for Families.

The paper notes that for most persons their effective marginal tax rate (EMTR) is equal to their top tax rate. For example, someone earning over $180,000, with no other benefits, their EMTR would be 39%. In other words, for every dollar they earn above that threshold it is taxed at 39%. Overall, most New Zealanders’ EMTRs are below 50%, with only 6% experiencing EMTRs of over 50%.

But the distribution of high EMTR varies significantly across different family types. Families without children generally experience low EMTRs.

Therefore, they have higher work incentives because they are less likely to be receiving government support payments that would be reduced by increases to income. Around 90% of such families have EMTRs equal to their marginal tax rate.

“The Iron Triangle”

The paper notes the issue of what it calls “the Iron Triangle”. This is the inherent trade-off between three competing objectives – providing adequate income support, maintaining reasonable government costs and preserving work incentives. Whatever you do, you’re never going to hit the sweet spot on any of that. It’s therefore a question of continual adjustment.

The paper is very interesting as it breaks down the various family types, the composition of their income and the benefits they receive. People might be receiving Best Start, Working for Families, Accommodation Supplement, all of which are subject to some form of abatement and at differing rates. The paper then analyses what happens when people start earning additional income and the numbers are really quite astonishing. The paper concludes parents are the group that most likely face financial disincentives to work because of the impact of high effective marginal tax rates.

Where it gets really problematical as these abatements start kicking in is for families with children. 13% of couple parent families have EMTRs greater than 50%. 30% of all single parent families have effective marginal tax rates greater than 50%. And there are a number of families with children that have EMTRs higher than 100%. The stats don’t reveal just how many people that might be affecting, but it’s certainly 20,000 to 50,000 it would seem. Which is a substantial number of people.

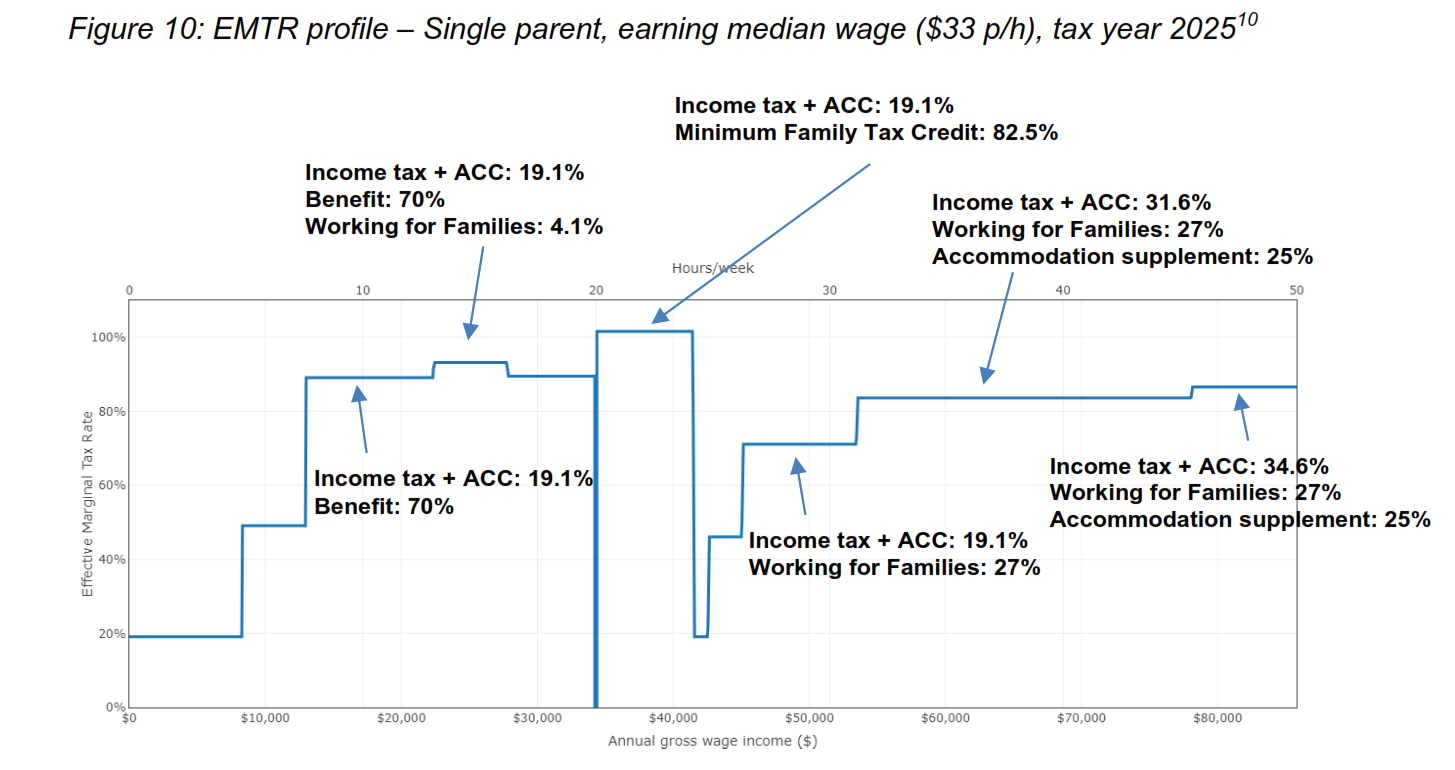

Figure 10 in the paper shows the EMTR profile for a sole parent family earning the media wage of $33 per hour. As the paper notes regardless of weekly working hours the parent faces high EMTRs almost consistently:

1. When working between 8 to 20 hours per week, they keep only around 10 cents of each additional dollar earned due to income tax and reductions in benefits and Working for Families tax credits.

2. When working between 20 to 24 hours, they keep none of the additional dollar earned due to reductions in the Minimum Family Tax Credit, income tax, and the ACC levy. In this case, they actually lose nearly 2 cents by earning an extra dollar.

3. When working between 26 to 31 hours, they keep slightly less than 30 cents of each additional dollar earned due to income tax and reductions in Working for Families tax credits and Accommodation Supplement.

4. When working between 31 hours and full-time11, they keep less than 20 cents of each additional dollar earned due to a higher income tax rate and reductions in Working for Families tax credits and Accommodation Supplement.

A long-standing issue no-one seems to want to fix

Compounding the matter, the paper notes that parents may be limited by childcare costs when choosing to increase their work, as there are fewer adults within the household supervising care for children. Overall it concludes:

“While the system generally preserves work incentives for most of the population, certain family types, particularly single parents, face significant financial disincentives to increasing work hours. This suggests that future policy development may need to focus on whether current abatement thresholds and rates are optimally placed.”

My response is that current abatement thresholds and rates are not “optimally placed”’ which was something the Welfare Expert Advisory Group was saying back in 2019. As I previously mentioned, the $42,700 abatement threshold for Working for Families (which is the limit of family income, not individual income) has not been increased since 2018, so there’s a real issue here. The Minister of Finance, who is now the Minister for Economic Growth, is keen on getting people into productive work as part of that. But people are not going to take up additional work if they realise that between the abatements and the additional childcare costs they’re going backwards.

It’s a long running issue and it will be very interesting to see what response the government makes to that. As always, we’ll bring you developments.

On that note, that’s all for this week. I’m Terry Baucher, and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

There have been several constant themes throughout this year. A surprising one has been the question of how we tax capital and whether we should have a capital gains tax. Throughout the year there have been a steady stream of stories on the topic. Meanwhile the Labour Party is currently reviewing its tax policy, and whether it’s going to go with a wealth tax or a capital gains tax.

A place where talent does not want to live

Intriguingly, Inland Revenue has added to this mix right at the end of the year with the release of an issues paper on the effect of the Foreign Investment Fund (FIF) rules on immigration.

Earlier this year I discussed a New Zealand Institute of Economic Research report called The place where talent does not want to live, which looked at the impact of the FIF rules on migrants to New Zealand. The NZIER report concluded that the FIF rules were acting as a hindrance to investors, particularly those migrants coming here who have previously invested in offshore startup companies.

The report also discussed an issue I’ve encountered fairly regularly of the impact of the FIF rules for American citizens. Even though they may have been resident in New Zealand for many years, because they are American citizens they still have to file U.S. tax returns. As a result, a mismatch arises for them between the FIF rules, which basically act as a quasi-wealth tax, and the realisation basis of capital gains tax that applies in America.

Inland Revenue policy officials have been aware of this issue for some time. In fact, I spoke to several officials earlier this year about the issues and potential options. The topic was highlighted as an option for review and was included in the Government’s tax and social work policy programme released last month. This report has therefore come out quicker than I expected which is a pleasant surprise.

The problem with the FIF rules

The problem is set out very clearly in paragraph 1.5 of the issues paper.

“Migrants will generally have made their investments without awareness of the FIF rules and may not be organised so that they can fund the tax on deemed rather than actual income. This is particularly a problem for illiquid investments acquired pre migration…. Because the FIF tax is imposed in years before realisation and on deemed rather than actual income, FIF taxes paid may not be creditable against foreign taxes charged on the sale of the investment.“

This highlights a key point about the FIF rules – they’re highly unique by world standards. When I’m discussing them with overseas clients and advisers, to make them more understandable I tend to explain them from the viewpoint that they’re a quasi-wealth tax. As the quote above notes problems also emerge whether the tax paid under the FIF rules can be fully utilised in the United States, for example.

Fixing the problem – taxing the capital gains?

The paper canvasses several options for reform, including one of simply increasing the current $50,000 threshold above which the FIF rules automatically apply. A key proposal is that maybe the investments subject to the FIF rules should be taxed on what is called revenue account. That is only dividends received and any gain in the value of those investments attributed to New Zealand on disposal would be taxed. In other words, an investor would be taxed on dividends and then when the investment was disposed of, a capital gains would be become payable.

Now to buttress this option the paper proposes that there should be an exit tax. In other words, if someone elects to use the revenue account method, but then decides no, actually New Zealand isn’t working out for us for whatever reasons, and they become a non-tax resident, this migration would trigger an exit charge. I’ve seen this in other jurisdictions and current FIF rules do have a provision covering it. This approach should be pretty understandable to investors coming here.

Maybe a deferral basis?

Another alternative is a so-called deferral basis, is where the FIF rules would apply on a realisation basis. This would be achieved in a way similar to how withdrawals on foreign superannuation schemes are currently taxed when the tax charge arises on withdrawal or transfer into a New Zealand based Qualifying Recognised Overseas Pension Scheme.

The taxable amount would be based on a deemed 5% per annum income from the date of their migration, with an interest charge for deferral. Again, this would be buttressed by an exit tax.

What happens overseas?

Picking up on what I was saying at the start about the question of taxation of capital, most other jurisdictions don’t encounter this issue to the same extent as we do because they usually have a capital gains tax regime that applies to comprehensive capital gains. Actually, in paragraphs 2.3 and 2.4 I find there’s some intriguing commentary from Inland Revenue on this issue.

“Because New Zealand does not tax capital gains without the FIF rules, no New Zealand tax would ever be paid on an investment in a foreign company that paid no dividends and was sold for a capital gain.”

This is an interesting insight to the issues caused by non-taxation. In effect without the FIF rules the Government is forsaking potential revenue. I always thought the expansion of the FIF rules in 2006 was really a sidestep around the difficult issue of taxing capital. And of course, despite having kicked the capital gains tax can down the road back in 2006, it’s still there.

Tax driven behaviour, or just a rational investment choice?

The issues paper goes on, quite controversially in my view, to argue that without the FIF rules in New Zealand, residents have a tax driven incentive to invest in foreign companies that enjoy low effective tax rates and do not pay significant dividends. Speaking with 40 years of tax experience, yes taxes do drive investment behaviour.

But this argument sidesteps a huge criticism, which is still valid, of the current FIF rules. When they were introduced in 2006, many of the submissions against them argued that the New Zealand stock market is so small in global terms that investors would be unwise to be fully invested here, and therefore should be spreading their risk by diversification and investing in offshore markets.

That is as valid a criticism of the FIF rules now as it was back in 2006. And of course, memories of the 1987 stock market crash, which was actually quite catastrophic by world standards, still run deep in many areas. We now have this scenario here where the FIF rules were designed because the Government wanted some revenue. It saw tax driven behaviour happening offshore, but it ignored a key fact, the importance of diversification. And if you don’t tax the capital but you want the revenue, where do you go from there?

Backdating the introduction of the changes?

Anyway, the whole paper is a very worthwhile read. It has one further highly interesting suggestion that changes could be back dated to take effect from 1st April 2025 and the start of the next tax year. Such a swift law change doesn’t happen with issues papers. Normally there’s usually another year or so before legislation is introduced and then comes into effect.

This option is actually very encouraging for migrants. I have had a number of inquiries on this issue, and I know of clients who have backed away from New Zealand because of the FIF rules. So, they will be looking at the proposals with great interest.

The paper also canvasses whether it should apply to new migrants or to existing New Zealand tax residents. That’s a good question it should certainly apply to migrants who can reorganise their affairs in anticipation, but I believe it should also apply to U.S. citizens who still have to file U.S. tax returns and are very disadvantaged by the current FIF rules.

Worth noting that although this is largely a tax measure it’s important to the Government because the existing FIF rules are seen (as the NZIER report noted) as a hindrance to attracting high quality migrants. Changing the law is seen as a priority as part of the Government’s general economic programme,

Submissions are open now and continue until 27th of January. I urge everyone interested in this topic to submit. We will be submitting a paper on this ourselves. We will also be contacting clients on this matter as it’s quite a welcome Christmas present.

The year in review

Moving on, its been a very busy year in tax. And I guess the biggest story in many ways was the Budget on 30th May, with the promised increase in tax thresholds finally being enacted with effect from 31st July. That was certainly the most eagerly anticipated one, and according to my data reads, it was the most read transcript over the year.

The tax cuts which weren’t

These tax cuts as they were called (which they’re not because they’re only inflation adjustments) also highlighted a big and continuing problem with our tax system, which the politicians apparently don’t want to address. The threshold adjustments only factored in inflation from 2018. They therefore effectively locked in the inflationary effect of the non-adjustment between 1st October 2010 (the last time the thresholds were adjusted) and the 2018 baseline.

On the other hand, in order to help pay for these adjustments which will reduce government revenue, the threshold on Working for Families which has been at $42,700 since 1st July 2018, was not increased. This means that families with income above that threshold have their Working for Families credits abated at 27.5%. Consequently, they face some of the highest effective marginal tax rates in the country.

And as I have repeatedly said in past podcasts, our politicians are very much less than transparent about the impact of what’s called fiscal drag. That is, as wages increase with inflation, they pull taxpayers up into higher tax brackets. We have a particularly big problem around the now $53,500 threshold where the tax rate jumps from 17.5% to 30%, the biggest single jump in the whole tax scale.

To bang a drum already beat repeatedly, this hinders a discussion around what is happening with our tax system? How much revenue have we really raised because politicians have been happy to use fiscal drag to quietly increase the tax take.

But the main effect is that the burden of tax falls on low to middle income earners who face significantly higher marginal tax rates because of the effect of abatements on people receiving social support, such as Working for Families.

So overall, those tax threshold adjustments were welcome. They were overdue, but they were one step forward and two steps sideways and half a step back because there’s no comprehensive commitment to ensuring that we have regular threshold adjustments.

If America can do it, why not here?

Just as an aside, in America all thresholds are automatically index-linked. Countries vary on their treatment of inflation and thresholds. And in low inflation periods, you can get away with not needing to do it every year, but you can’t leave such adjustments for 14 years without finally having to do something.

A year of anniversaries

2024 was quite a big year for me personally. I started working in tax 40 years ago in Britain and it so happened that the British budget on 30th October had several announcements which have huge significance not just for UK migrants who have moved here but also for many Kiwis. So, I find myself, somewhat ironically, still doing a lot of work on the impact of British taxation.

It’s also been 20 years since I started Baucher Consulting and as I said in the podcast much has changed, and yet in some ways little has changed. One constant which hasn’t really changed is the behavioural impact of tax- this week’s discussion of the FIF regime is the latest example. I’d like to thank everyone who’s supported me over the these past 20 years.

Our fantastic guests

Looking at some other highlights of the year in terms of the podcast, we had a lot of great guests this year and my thanks again to all of them. My particular favourite episode was the Titans of Tax with Sir Rob McLeod, Robin Oliver and Geof Nightingale. Many thanks to Sir Rob, Robin and Geof for giving up their time. It was a fantastic discussion and very, very enjoyable. It was extremely well received all around. It was fascinating to just sit back and listen and to three experts who’ve been very heavily involved in the last three major tax working groups.

My thanks also to all my other guests this year, including the four finalists for this year’s Tax Policy Charitable Trusts Scholarship. Again, thank you so much for your input. Very interesting to talk to you, and the future of tax policy is in good hands.

Inland Revenue goes full throttle on compliance work

One of the big themes for the year, and less of a surprise, was Inland Revenue’s ramping up its enforcement approach. One of our guests very early in the year (and thanks again) was Tracy Lloyd, service leader of Compliance Strategy and Innovation at Inland Revenue. Tracy’s podcast was a really interesting one looking at what tools Inland Revenue is using and how it’s ramping up its investigative activities.

We’ve seen Inland Revenue’s more aggressive approach constantly through throughout the year. It has made announcements about cracking down on the construction sector, looking at liquor stores. Pretty much every week there’s a media release that another tax fraudster has been jailed or received substantial fines or home detention. In addition Inland Revenue is making use of information received through the Common Reporting Standards on the Automatic Exchange of Information.

These things will continue to come through. Inland Revenue got $116 million over four years to beef up its investigation activities and to improve its tax collection. As part of this we’re seeing a crackdown on student loan debt, which is a much more problematical issue mainly because the biggest portion of debt is held by persons overseas. It’s therefore not so easy to collect.

Inland Revenue’s activities will continue to ramp up but I think it may start to find there’s increasing push back as it clamps down. I think it’s previously been slow in responding, and during the COVID pandemic that was understandable. But right now, the faster it responds to debt issues developing, the better for all of us. Zombie businesses which linger on are no good to anyone.

The surprising continuing debate over capital gains

But the other big thing this year has been a surprising one. It’s the question of the shape of the tax system and persistent media stories about whether we should have a wealth tax or capital gains tax. This is a topic I don’t see going away. I see the pressure mounting on it because as, the Government’s main agency, Treasury, is pointing out we have ongoing demographic pressures in relation to superannuation and funding health.

And as I keep pointing out, we also have the question of climate change. We have insurers withdrawing cover and I think that means the Government will be expected to step in. And that means sharing the burden, which means ultimately some form of tax increases. All this means the composition of the tax base will continue to be a matter of debate.

Of course, we have options like capital gains tax, wealth taxes, or as Dr. Andrew Coleman suggested (another one of the fascinating podcasts this year) maybe we should rethink our issue of Social Security taxes, where again we’re a unique jurisdiction in that we don’t have them. We used to have such taxes way back from the early 1930s through until late 60s, before they were finally abolished,

So overall lots to discuss this year. I’d like to thank all my guests again, and all the listeners, readers and all those who chip in and comment away. Your comments are read and always welcome. And on that note, everyone have a very happy festive season. We’ll be back with what’s new in the tax world in January 2025.

more feedback on Inland Revenue’s long-term insights briefing

an interesting Technical Decision Summary on cryptoassets

A fairly regular topic in podcasts and public domain generally, has been the tax treatment of charities. When the Government announced its tax and social policy work programme last month it included a review of the tax treatment of charities.

Last Tuesday, the Finance Minister Nicola Willis revealed more details around what was happening, explaining that there would be announcements in next year’s budget, to be delivered in May 2025.

“What essentially we’re doing is looking to see if there are any loopholes that are being exploited that would allow entities that are structured as charities to avoid tax they should otherwise pay”

More tolls on the way

Ms Willis commented it would not be right to rule out any new tax revenue streams or levies in this current Parliamentary term, adding “The truth is, I will be looking at revenue from tolls, and there could be tweaks to the charity tax regime. You can expect me to make announcements at the Budget” On the theme of toll revenue on Friday, the Government announced three new highways being built in the North Island would all be tolled.

Sir Michael Cullen’s biggest surprise

I recall discussing the role of charities with the late Sir Michael Cullen, when he was Chair of the last Tax Working Group. When I asked him what the biggest surprise of his time on the TWG had been, he replied it was been the extent of the charitable sector and its relative importance. The Finance Minister picked up on this commenting “what we’re weighing up here is on the one hand, in reality, New Zealand Charities play a massive role in our communities and many of them fundraise, contribute significantly to their communities and they face a lower tax burden because we all appreciate that.” She then went on to add.

On the other hand, wherever you have omissions from the tax regime, there will be some who structure their affairs to limit their liability. Who might, for example, be building up funds that aren’t going to charitable purposes, that are building up their own coffers. That’s one of the issues we’re looking at. There are a number of details here. What I want to work through carefully is not punishing the good while going trying to go after the bad.

Apparently the Finance Minister specifically mentioned Best Start and Sanitarium as examples of trading entities that are structured as charities which could impacted by the changes.

What did the last Tax Working Group say?

It’s worth looking back at what the last Tax Working Group said in its section on charities. It recommended the Government periodically review the charitable sectors use of what would otherwise be tax revenue, and to verify that intended social outcomes are being achieved.

In relation to the likes of Best Start and Sanitarium, the TWG noted “the income tax exemption for charitable entities’ trading operations was perceived by some submitters to provide an unfair advantage over commercial entities trading operations”. That is a common analysis that I see.

But the Tax Working Group hit the nail on the head when it went on to say “the underlying issue is the extent to which charitable entities are accumulating surpluses rather than distributing or applying those surpluses for the benefit of their charitable activities.”

This has been a long-standing issue and a sore point for some commercial operators which has been on Inland Revenue’s radar for some time. It will be interesting to see what comes out of this review and whether in fact there are some very targeted measures restricting the ability to qualify for the charitable exemption. But I suspect what it will come down to is how exactly the funds are being applied.

How much is at stake?

Another news report estimated that perhaps up to $2 billion of profit in the charitable sector may not be subject to tax. This estimated was based on the Charity Services latest annual report which noted charities had for the year ended 30 June 2024 total income of $27.34 billion with expenditure of $25.28 billion, leaving a difference of approximately $2 billion unaccounted for. Theoretically that income could have been taxed at 28% or $560 million. Which is not to be sniffed at, given the Finance Mnister’s repeated concerns about the state of the books. What counter-action comes out of the Inland Revenue review will be revealed in next year’s Budget.

Inland Revenue’s proposed long-term insight briefing under fire

Moving on, last week I covered Inland Revenue’s feedback and summary of submissions it received on its proposed long-term insights briefing (LTIB). Inland Revenue was proposing to explore what the structure of the tax system would be suitable for the future, and it published the submissions that it had received on the matter. This included, as I said, a rather entertaining but bold (as you might expect) submission by Sir Roger Douglas,

Subsequently Business Desk published a story on Monday under the rather excitable headline “Corporate tax group tells Inland Revenue to stay in its lane over the long-term briefing” (paywalled) .The gist of the story was that Inland Revenue was under fire from the Corporate Taxpayers Group for having suggested that it should undertake such a review without a proper mandate. According to the CTG’s submission Inland Revenue “could be viewed as suggesting this next LTIB process would be a review of the “broad structure” of the New Zealand tax system and its future suitability. That seems to require a general review of all aspects of the tax system along the lines of the 2019 (Cullen) Tax Working Group Report.”

Such reviews are often undertaken specifically at the request of a government, often after a change of government such as the 2001 MacLeod tax review, the 2010 Victoria University Wellington review and in 2019, the last Tax Working Group.

Inland Revenue’s unique role

The truth is always a little bit more nuanced than what the CTG were apparently saying. A point that hasn’t been picked up is that this actually shows one of the problems around Inland Revenue not only being the Government’s main revenue gathering agency and responsible for the administration of the tax system, but it also is the lead policy advisor on tax. Treasury has a tax policy group, but it’s significantly smaller in scale. This is unusual by global standards because typically tax policy sits within the equivalent of treasury.

In my view it’s unfair to be singling out Inland Revenue for undertaking a periodic review. It’s been five years since the last Tax Working Group, and a lot has happened since then. Let’s remember we’ve had a pandemic, and we’ve also got a major war going on in Ukraine. The global environment has changed dramatically since 2019, and I would actually expect government agencies like Treasury to be looking periodically at the shape of the tax system. This is a key purpose of long term insights briefings.

Treasury has its own long-term insights briefing on the fiscal position, which I’ve referred to repeatedly, which has implications for tax policy. I think the criticisms are slightly unfair, and the headline probably a bit excitable, although the Business Desk notes that Deloitte were also slightly critical of the proposal.

Corporate Taxpayers Group’s suggestions

When you actually look at the CTG’s submission, it’s more nuanced. The CTG suggests

“a more focused approach than attempting another general tax review. The environmental scan seems to suggest that the officials’ concern with the existing tax system is its possible inflexibility.”

The CTG submissions makes the very worthwhile comment that an official exercise here should be taking a sort of lead role in educating the public, and to some extent politicians, about the issues that are ahead and the options available for change. The suggestion is the focus should be on future revenue flexibility and then a question as to how governments might wish to apply the tax system to meet redistribution objectives (distributional flexibility). Against this background:

“Officials have an important role to play in such political processes. They should provide the best possible advice and objective manner matters. What are the best economic estimated economic costs of different tax bases? How would any proposal to meet distribution objectives increase these costs? The political process can then trade off measures to meet distributional objectives with the economic costs this would incur.”

The CTG suggests Inland Revenue’s proposed long-term insight briefing should consider at what is known from New Zealand and overseas studies of the dead weight costs or tax revenue generally on a particular tax basis.

I think this is a perfectly reasonable response by the CTG. You might say well of course they would say that because they represent some of the largest taxpayers in the country. So perhaps they’ve got a bit of self-interest on the matter. But the point is there are economic costs of taxing or not taxing particular sources of income and those costs need to be considered in the scope of any stand-alone review.

An interesting tax issue involving crypto assets

Finally, this week, there was an interesting issue raised in one of Inland Revenue’s latest Technical Decision Summaries. These are anonymised issues that Inland Revenue’ Tax Counsel Office (TCO) has come across either as a result of a dispute that’s between the taxpayer and Inland Revenue, or as here involving a taxpayer who has made an application for a ruling as to the correct treatment of a transaction.

Technical Decision Summaries can provide useful guidance, but they are always highly fact specific. In this case the taxpayer was a natural person who qualified to be a transitional resident because he was looking to return to New Zealand after more than 10 years of non-residency.

The question he asked was would he be a transitional resident in relation to crypto assets held in overseas centralised exchanges as well as decentralised exchanges.

Would the sale of those crypto assets therefore be exempt under the transitional residence exempt?

As I said, these are very highly fact specific, and the ruling that came back was he would qualify as a transitional resident so long as he met various conditions and yes, the amounts derived from the sale of crypto assets during the transitional residence exemption, which typically lasts at least 48 months, would not be deemed to have a source in New Zealand.

As part of the analysis, the technical decision summary looked at what we call the source rules in section YD 4 of the Income Tax Act 2007. Would this be income from a business wholly or partly carried on in New Zealand? Are the contracts wholly or partly performed in New Zealand, or is this disposal of property situated in New Zealand?

The TCO concluded that none of those would apply and therefore because the crypto assets being traded or sold through the offshore centralised exchanges and decentralised exchanges, any gains would qualify for the transitional residence exemption. This is an issue I’ve seen discussed previously, although I’ve not directly advised on it, so it’s interesting to get some Inland Revenue commentary. But as I said, although Technical Decision Summaries are useful, bear in mind these are always highly fact specific, so be very careful in deciding if one might apply to your circumstances.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

One of the unseen revolutions in international tax over the last decade has been the adoption of the automatic exchange of financial account information. Also known as the Common Reporting Standards https://www.ird.govt.nz/crs this was developed by the Organisation of Economic Cooperation and Development, the OECD, in conjunction with G20 countries. It requires the automatic exchange of information on financial accounts – which is bank accounts, other investments held by taxpayers outside their jurisdiction. Financial institutions are required to provide information on such accounts to their respective tax authority which then sends that information to the jurisdiction in which that taxpayer is resident.

This project began in 2017. For the latest year, the tax authorities from 111 jurisdictions have automatically been exchanging information on financial accounts. And as I said, it’s a very broad range of investments, not just bank accounts. It’s all forms of investments. By and large, the public is pretty unaware of what’s happening here even though the numbers are significant.

€130 billion in tax interest and penalties so far

According to the latest peer reviewfrom the OECD, information from over 134 million financial accounts was exchanged automatically in 2023, and that covered total assets of almost €12 trillion. As a result, over €130 billion in tax interest and penalties have been raised by the jurisdictions through various voluntary disclosure programmes and other offshore compliance programmes.

Now the interesting thing here is that as a consequence of the introduction of the CRS, financial investments held in international finance centres or tax havens have decreased by 20% since the introduction of CRS in 2017. That’s a significant change. It means investments are moving into jurisdictions where they will be taxed. Over the long term that’s going to be quite significant for increased tax revenue around the world.

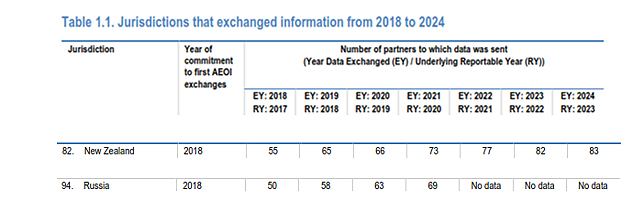

The full OECD report, which also discusses methodologies, runs to 248 pages, but the bulk of what people will be interested in is covered in the first chapter. Table 1.1. gives a summary of how many jurisdictions have been exchanging information, starting in 2018. According to the latest report the time of this report, 118 jurisdictions including New Zealand have started exchanging information.

Now the interesting thing to notice is the steady growth in the number of partners to which data has been sent. For example, the tax haven Anguilla in 2017 sent data to four countries but by 2023, it’s up to 67. The Cayman Islands, another key tax have sent data to 83 jurisdictions.

CRS and New Zealand

New Zealand began swapping data in 2018 when it sent information to 55 partners. For the latest year that’s grown to 83. Based on the early data exchanges Inland Revenue began a review programme in late 2019 which was then interrupted by COVID. However, it has now resumed its review programme, and I have one case at the moment which involves the taxpayer making the relevant disclosures after Inland Revenue enquiries based on data received through CRS. They won’t be the only one.

I was rather amused to see that Russia began exchanging data in 2018 when it sent data to 50 jurisdictions. But for the last three years no data is available. Wonder what’s happened there.

By the way the United States is not part of the CRS. That’s because it has something called the Foreign Account Tax Compliance Act, which basically was the model on which the current global CRS was built, and so it reports data separately.

How much data is Inland Revenue sharing?

I’ve tried unsuccessfully to obtain more detailed information on the data exchanges using the Official Information Act (the data exchanges are outside the OIA because of international treaty obligations which is fair enough). Notwithstanding this the impression I have is there are some huge numbers involved.

You have been warned…

What people should be aware of is that there’s a massive amount of data being circulated by tax authorities around the world right now. Many people may be oblivious to what’s going on. The likelihood is if you have an overseas financial account and you haven’t declared it for whatever reason, then it is quite likely that you will soon be asked a few questions about that by Inland Revenue.

Speaking about Inland Revenue, earlier this year they asked for consultation on their proposed long-term insight briefing (LITB). To quickly recap, LITBs are

“…future focused think pieces that government departments produce every three years. They provide information on long term trends, risks and opportunities that could affect New Zealand in the future, and policy options for responding to these matters. Their purpose is to help us collectively think about and plan for the future. They are developed independently of ministers and are not current policy.”

Back in August Inland Revenue proposed that its next long term insight briefing will explore what would be a suitable structure of the tax system for the future, and invited submissions by early October.

Inland Revenue has now published a summary of those submissions. In total, there were 35 submissions from 12 groups and 23 individuals. Most submissions were generally supportive of the topic. The rest, either suggested something completely different or were either ambivalent about it or did not actually specify whether they supported the project or not.

Seven themes in feedback

Inland Revenue’s picked out seven themes that came through from those submissions. Firstly, the fiscal pressures arising from superannuation and healthcare are a key trend and that’s one of the reasons behind Inland Revenue wanting to do a long term insight briefing on this topic. Most agreed with that, but several also added the question of increasing fiscal pressures arising from climate change.

My belief is its climate change that’s going to be the trigger point around changes to the tax system because that’s happening right now. And as damage from the floods grows and costs and insurers look increasingly wary about insurance, people will be looking to the Government for support.

The second theme was keeping flexibility in the tax system. In its submission EY commented

“We agree improvements to system flexibility should be the focus for this LTIB. In particular, working through options for system integrity in the context of tax rate increases is in our view, important.”

The devil is in the detail

A third theme was the analysis needs to consider policy design details and looking at first principles. Chartered Accountants of Australia and New Zealand made the comment that “Sometimes it is the detail that can make things unworkable. The framework should consider the merits of expanded tax bases with different design parameters”.

Another theme – and this is something I think I would endorse – the analysis needs to consider the tax and transfer system interaction. There were a few submissions pushing very strongly on that point.

A fifth theme proposed considering corrective taxes. The Young International Fiscal Association Network suggested that environmental taxes would fit well with Inland Revenue’s proposed topic because of the long term environmental trends.

The impact of technology

Another theme was the question of technological change and how that will affect the sustainability of tax bases. Earlier this year an IMF report on the impact of artificial intelligence suggested changes to tax systems could be needed.

Some submitters emphasised that it was important to consider how the tax system impacts a wider range of social outcomes. These included Doctor Andrew Coleman who was broadly in support of what was in the proposed LTIB. He suggested that they need to look at a wider range of retirement savings reforms, which would be no surprise to anyone who listened to the podcast with Gareth Vaughan and myself earlier this year. Several other submissions suggested how tax system could support productivity.

Finally, there were suggestions about considering progressive consumption taxes, which hasn’t really been looked at in any detail in New Zealand.

How Inland Revenue will proceed

Following this feedback Inland Revenue has said the LTIB will discuss the arguments for lower taxes on savings and the question of the tax treatment of retirement savings as part of a discussion about social security taxes. This is an interesting development because as the consultation noted generally, most jurisdictions have social security taxes which represent somewhere around 25% of total tax revenue. Whereas we don’t have them at all. This was a point Dr Coleman made in the podcast so it’s good to see Inland Revenue will be looking at that.

No to considering financial transaction taxes

As part of managing the whole scope of the LTIB Inland Revenue believes it “could reduce the discussion of some tax bases are less likely to be subject of significant public discussion such as financial transaction taxes.” This makes sense. Financial transaction taxes or Tobin Taxes are something that pop up in discussions about tax reform. I’m ambivalent about whether in fact they will achieve what people make out for them. I think they would add complexity and they would drive all sorts of different behaviour.

They’re not going to do a full review of the interaction of the tax and transfer system. And to be fair to Inland Revenue, I think that would be an entire long-term insight briefing of itself. But their chapter on consumption taxes discussed using transfers to offset GST rate increase somewhat similar to what Andrew Paynter proposed last week. (Just to repeat Andrew’s proposal is his alone and does not reflect any Inland Revenue policy). According to Inland Revenue the tax regimes chapters “will largely focus on how to make our main tax bases more flexible to rate changes, including considering options to support system coherence and integrity.”

Providing an analytical base

In summary Inland Revenue’s intention

“…is to provide an analytical base to provide further consideration of these issues in the future. For example, our focus on tax bases is on understanding the relative costs of taxing different underlying factors and what the overlaps and differences are in those tax bases. Our focus on tax regimes is on exploring how to make our tax based main tax bases more flexible to rate changes without undermining equity or efficiency goals.”

All of this seems perfectly reasonable to me.

From here there will be a future opportunity to provide feedback when Inland Revenue releases a draft of its briefing for public consultation in early 2025. It will then be finalised and given to Parliament in mid-to-late 2025.

Sir Roger Douglas’s radical proposals

Inland Revenue have also published all the submissions, from those who gave permission to do so, adding up to 175 pages of submissions, from individuals and organisations alike. It’s interesting to dip in and see what is being suggested on the topics. Sir Roger Douglas was one of the submitters and as you might expect, the old warrior is still looking for something radical.

Part of his proposal is a tax-free threshold of $62,000. But the trade-off is most of that gets put into retirement and health accounts. With the proposed retirement account, he’s probably reflecting the thinking of Andrew Coleman about the need for the current generation to start saving in earnest because of the various pressures coming towards us. Can’t say I agree fully with Sir Roger’s proposal but full marks for boldness.

Feedback on Andrew Paynter’s proposal

And finally, this week, to pick up a little bit from last week’s podcast with Andrew Paynter and his proposal to increase GST by 2.5% points to 17.5%, but then with a rebate for low- and middle-income earners. The transcript has been very well read and generated a phenomenal number of comments, over 150 at last count, and I thank all the readers and commenters for that.

What about the self-employed?

One commenter asked a question which we didn’t cover off during the podcast; how would Andrew’s proposal apply to the self-employed? The answer is it would use something similar to the provisional tax system. A person’s income would be uplifted from last year and if you’re in the range then you qualify for the proposed payments.

Last week Tax Management New Zealand and the Young International Fiscal Association network ran a joint presentation for the two winners, Andrew and Matthew to come and present their proposals. If you recall, Matthew proposed expanding the withholding tax regime to contractors. Andrew and Matthew both made excellent presentations to a very engaged crowd, and I can see why the judges had a difficult time splitting the pair. So well done again.

Left-to-right Matthew Seddon, Terry Baucher and Andrew Paynter

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.