This week the ninth edition of the OECD’s Tax Policy Reforms was released. This is an annual publication that provides comparative information on tax reforms across countries and tracks policy developments over time. This edition covers tax reforms in 2023 for the 90 member jurisdictions of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

Reversing the trend

It’s a fascinating document which tracks trends of what’s happening around the tax world at both a macro and micro level. The report has three parts: a macroeconomic background, then a tax revenue context, and then part three is the guts of the report with details of tax policy reforms around the world.

There is an enormous amount in here to consider and the executive summary lays out the ‘balancing act’ issues pretty clearly.

“Policymakers are tasked with raising additional domestic resources while simultaneously extending or enhancing tax relief to alleviate the cost-of-living crisis… On the one hand, governments further protected and broadened their domestic tax bases, increased rates, or phased out existing tax relief. On the other hand, reforms also kept or expanded personal income tax relief to households, temporary VAT [GST] reductions, or cuts to environmentally related excise taxes.”

A key observation for 2023 was a trend towards reversing the responses to the COVID-19 pandemic. Instead, as the report notes “2023 has seen a relative decrease in rate cuts and base narrowing measures in in favour of rate increases and base broadening initiatives across most tax types.”

“A notable shift”

This includes “A notable shift occurred in the taxation of business, where the trend in corporate income tax rate cuts seems to have halted with far more jurisdictions implementing rate increases than decreases for the first time since the first edition of the Tax Policy Reforms report in 2015.”

This is a pretty significant change. I think actually when you consider last week’s speech by Dominick Stephens of Treasury, it was setting out the context for why having got over the crisis of responding to the pandemic, countries are realising they’ve got to deal with the demographic issues of ageing populations and funding superannuation.

Climate considerations

Beyond these concerns, there is the immediate impact of climate change and its growing effects. The executive summary picks up on this issue:

“Climate considerations are also increasingly influencing the design and use of tax incentives, with more jurisdictions implementing generous base narrowing measures to promote clean investments and facilitate the transition towards less carbon intensive capital.”

And on that point, I hope all the listeners and readers down in Dunedin and Otago are safe and well at the moment.

Paying for superannuation

The other thing picked up is that in referencing that point I made a few minutes ago about population ageing. There has been a growing trend amongst countries to increase Social Security contribution taxes. Alongside Australia, and to a lesser extent Denmark, we are unique in that we don’t have social security contributions. However, elsewhere in the OECD social security contributions raise increasingly significant amounts of revenue.

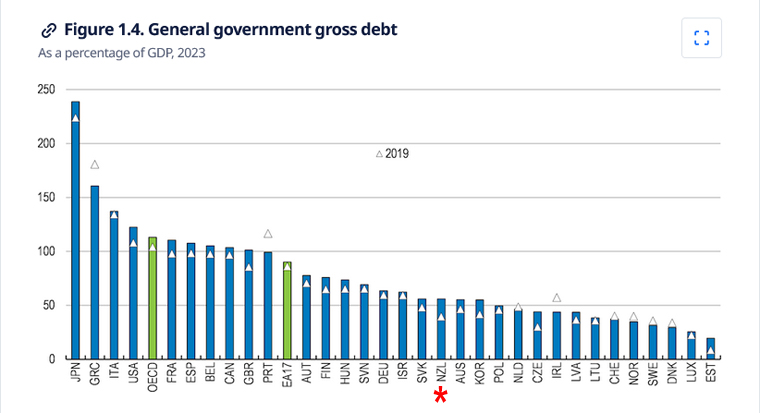

The report begins with a macroeconomic background. It notes that for the OECD as a whole in 2023 government debt rose by about nine percentage points, reaching 113% of GDP. For context, New Zealand’s debt-to-GDP ratio is just over 50%.

As the macroeconomic summary notes after generally decreasing in 2022 Government deficits increased again in 2023 following the energy crisis triggered by the war in Ukraine. Consequently,

“As debts and interest rates increased, interest payments have started to rise as a share of GDP. Even so, in 2023 they mostly remained below the average over 2010 to 2019, except notably for Australia, Hungary, New Zealand, the United Kingdom, and the United States.”

In short, we definitely have issues to deal with in terms of debt management and rising costs.

Responding to growing deficits

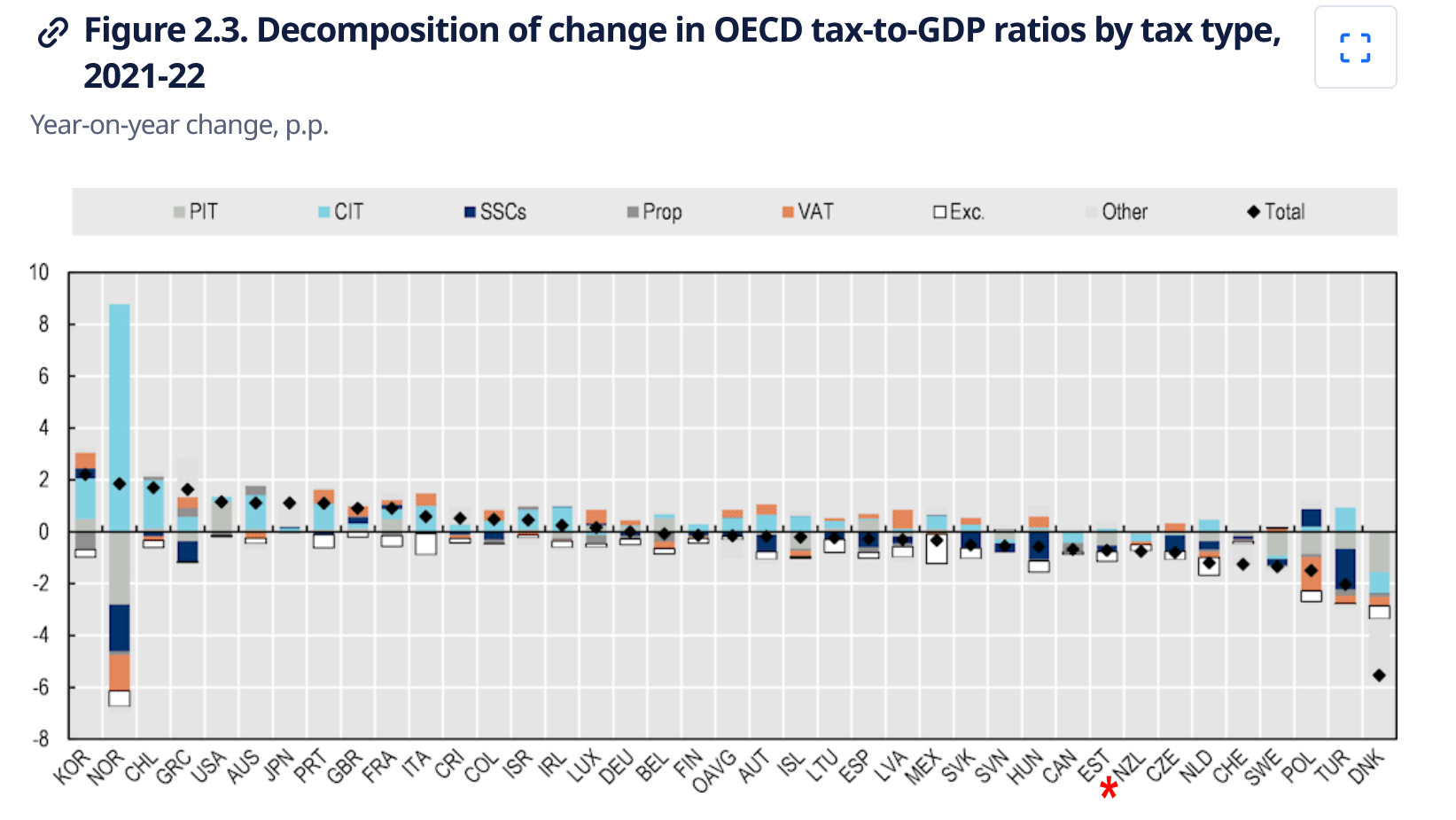

The report then notes that responses to growing deficits have been to start at increasing taxes. In general tax revenue terms,

“From 2020 to 2021, the tax-to-GDP ratio rose in 85 economies with available data for 2021, fell in 38, and stayed the same in one. In more than half of these economies, the change in the tax-to-GDP ratio was under one percentage point, whereas 22 economies saw shifts greater than two percentage points in their tax-to-GDP ratio.”

Denmark saw the most significant drop of 5.5 percentage points, with New Zealand’s tax-to-GDP ratio falling by three-quarters of a percentage point, well above the OECD average fall of .147 percentage points. (Norway’s dramatic corporate income tax take increase of 8.775% is the result of “extraordinary profits in the energy sector”.)

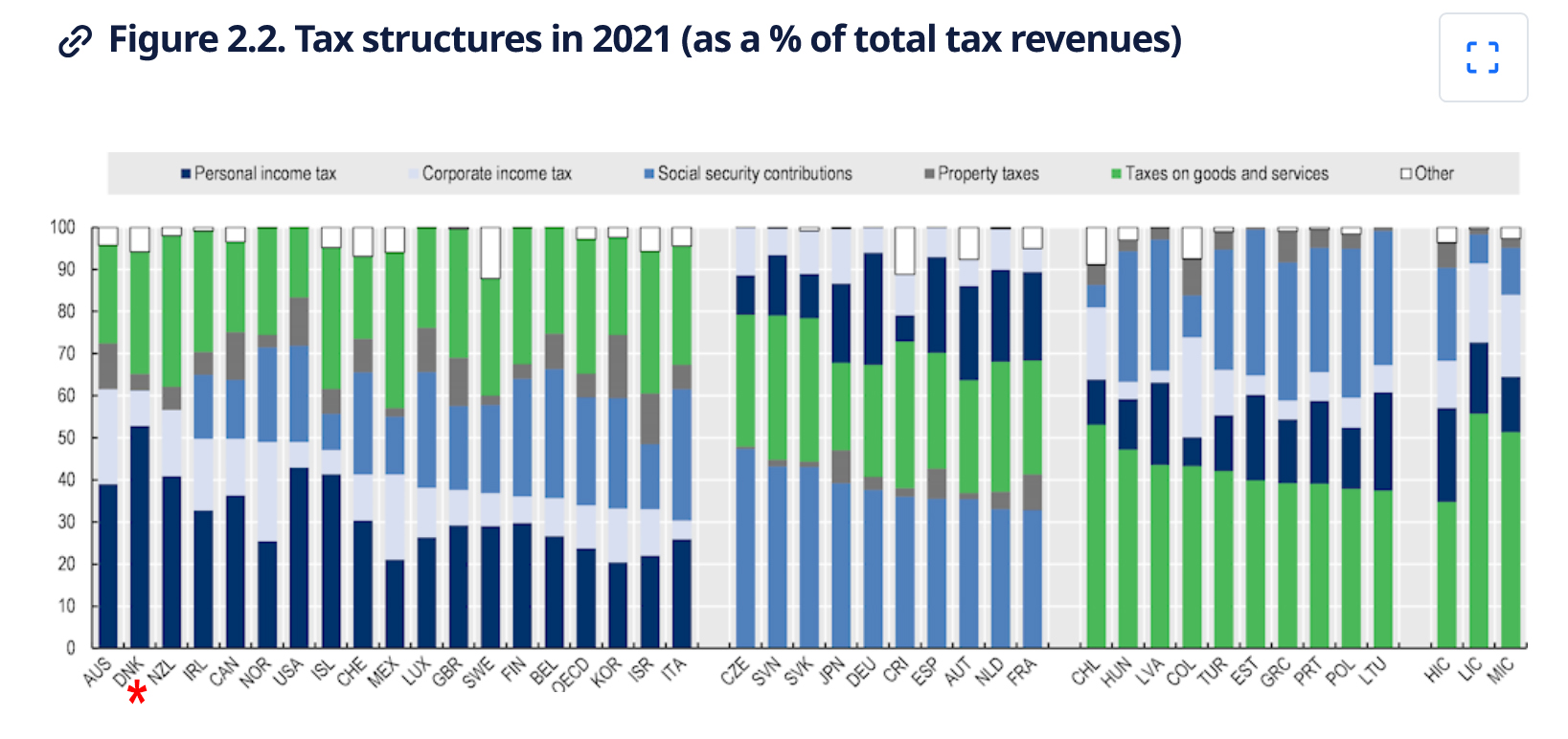

Composition of tax base

With regards to the composition of tax, 18 OECD countries (including New Zealand) primarily generate their revenues from income taxes, including both corporate and personal taxes. Ten OECD countries relied most heavily on Social Security contributions, and another 10 derived the majority of the revenues from consumption taxes, including VAT, (GST). Notably, taxes on property and payroll taxes contributed less significantly to the overall tax revenue mix in OECD countries during 2021.

Drilling into the detail

Part 3, of the report looks at the detail of the tax policy reforms adopted during 2023. This part has an introduction, then looks at five separate categories of taxes beginning with personal income tax and Social Security contributions, followed by corporate income tax and other corporate taxes, taxes on goods and services, environmentally related taxes and finally taxes on property.

As I mentioned previously, there was “a marked increase in the number of jurisdictions that broadened their Social Security contribution bases and raised rates”. Generally speaking, for high income countries personal income tax and social security contributions represent 49% of total tax revenue. Across the OECD personal income tax represented 24% and social security contributions 26% on average.

Here about 40% of all tax revenue comes from personal income tax. That’s one of the higher proportions around. Around the globe there was a bit of tinkering around personal income tax reforms mainly targeting lower income earners. This is an area where I think we need to focus any future reforms.

We have just (partly) adjusted thresholds for inflation and interestingly, I see that during 2023 quite a few jurisdictions did increase thresholds for inflation. For example, Austria updated its automatic inflation adjustment mechanism to counteract inflation, pushing workers into higher brackets. Meanwhile Australia increased its threshold for its Medicare levy to ensure low income households continue to be exempt, given that inflation has led to higher normal wages.

Corporate income tax rates are on the rise

Substantially more corporate income tax rate increases and decreases were announced or legislated by jurisdictions in 2023. Six jurisdictions increased their corporate tax,four of those did so by at least two percentage points. Türkiye increased all its corporate tax rates by five percentage points.

Whenever there are discussions about reforming our tax system, the issue of reducing our corporate tax rates will come up. With a 28% rate we are at the higher end of the corporate tax rate scale. There is potentially some scope, but as economist Cameron Bagrie has noted any such decrease needs to be part of a broader range of changes.

An example of such a change was the introduction of a general capital gains tax by Malaysia for all companies, limited liability partnerships, cooperatives and trusts from 2024.

Picking out of the details something which I know businesses here would look at with a certain amount of envy is more generous depreciation allowances. The UK, for example, has permanent full expensing for main rate capital assets as it’s called and a 50% first year allowance for special rate assets. Australia has also increased its thresholds for effectively fully expensing items for small businesses. Around the world there’s a whole range of incentives for R&D and environmental initiatives.

We have just limited the limits for residential interest deductions but it’s interesting to see that Italy abolished its allowance for corporate equity provision. Meantime Canada has new restrictions on net interest and financing expenditure claimed by companies and trusts.

Taxes on goods and services (VAT/GST)

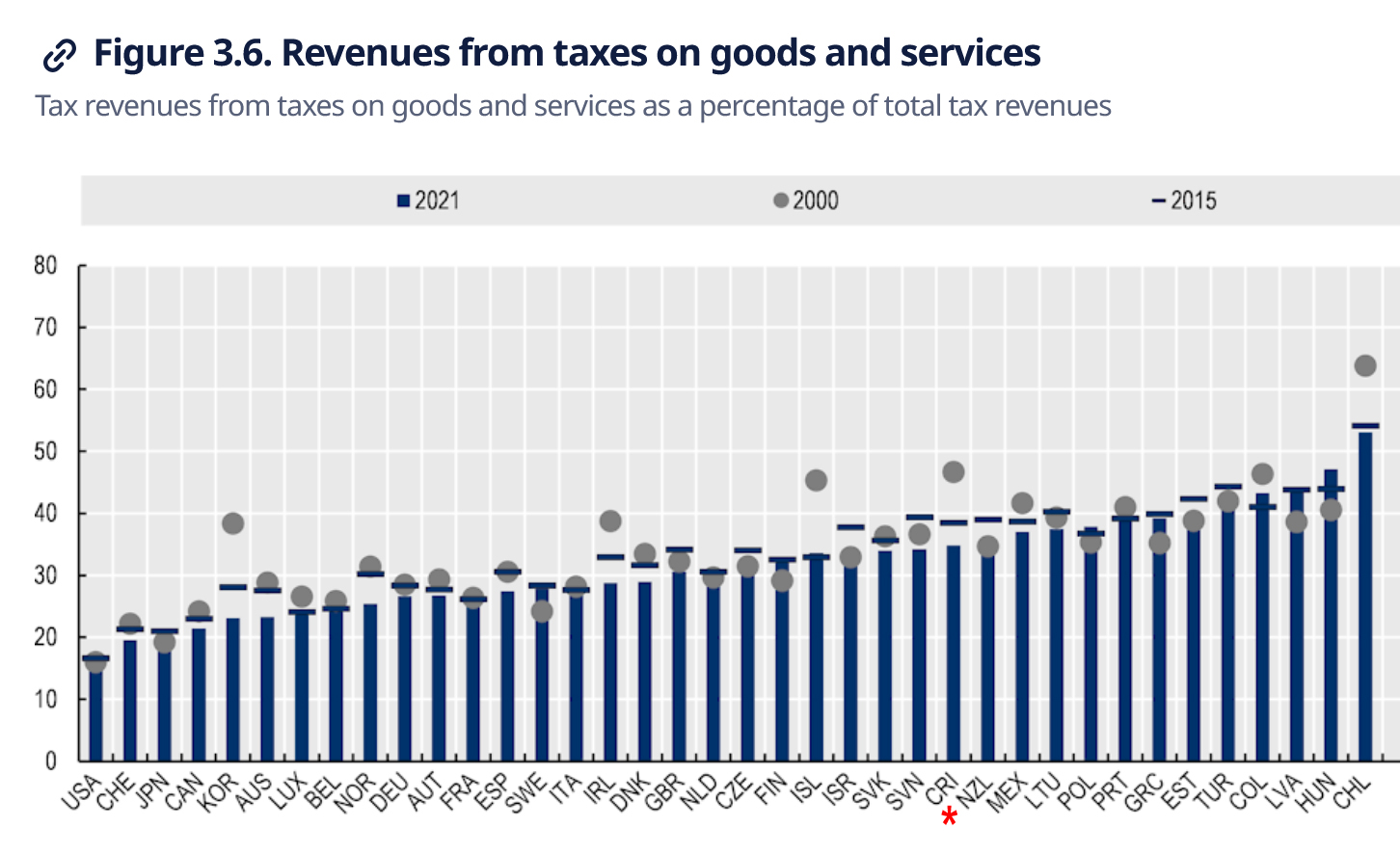

In the VAT/GST space, in terms of revenue from taxes on goods, although we have one of the most comprehensive GST systems in the world, New Zealand was only twelfth in the OECD for the percentage of tax revenue from goods and services as a percentage of total tax revenues. GST raises just over 30% of total tax revenue here, whereas Chile raises over 50%. This is quite interesting given how comprehensive our GST system is. It might mean that there is scope to expand the the rates of GST further. (Six countries including Estonia, Switzerland and Türkiye did so in 2023). But any government doing so should do so as part of a total tax switch package.

We discussed GST registration thresholds a couple of weeks back. During 2023 seven countries increased or planned to increase their VAT registration threshold. I was very interested to discover that Ireland has a split VAT registration threshold treatment: the registration threshold for the sale of goods is €80,000. But for the provision of services, it’s €40,000. I’ve not seen this split before. Meanwhile Brazil is undertaking the introduction of VAT/GST, which is a huge step forward.

A stable tax policy or just less tax activism?

There’s a lot to consider in this report more than can be easily covered here. Overall, it’s incredibly interesting to see what’s going on around the world. Many of the reforms discussed here involve threshold adjustments but there are plenty of new exemptions and incentives introduced. We generally don’t get into this space, that’s possibly a reflection of a very stable tax policy environment, but also perhaps a less activist philosophy by New Zealand governments which hope market incentives will work. Whatever, the approaches it’s interesting to see what’s going on around the world and I recommend having a look at this very interesting report.

ACC crackdown

Moving on, ACC has been in the news when it emerged that it has been chasing thousands of New Zealanders for levies on income they earned while working overseas.

According to the RNZ report, ACC sent 4,300 Levy invoices for the 2023 tax year to New Zealand tax residents who had declared foreign employment or service income in their tax return. The issue is that the person was often overseas at the time the income was earned and in some cases the the person has probably incorrectly reported the income in their return.

It’s an interesting issue and coincidentally, it so happens that I’ve just come across a couple of similar instances. My initial view is there seems to a bit of a mismatch between the relevant income tax legislation and the legislation within the Accident Compensation Act 2001. Watch this space on this one because I’m not sure the matter is entirely as cut and dried as ACC considers.

Inland Revenue responds to social media criticisms

A couple of weeks back, we covered criticism of Inland Revenue for providing the details of hundreds and thousands of taxpayers to social media platforms. It had done so as part of various marketing campaigns targeting people who owed taxes and Student Loan debt in particular.

Inland Revenue has now responded by putting up a dedicated page on its website, referring to customer audience lists.

In its words “social media is just one channel we use to reach customers. It is very effective at reaching people where they are.” As I said in the podcast Inland Revenue’s dilemma is it has to go to where the people are which is on the social media websites. In order to reach out to them it’s going to have to provide certain data. To reassure people the new page explains how it uses custom audience lists and what data is provided.

They do upload a list of identifiers such as name and e-mail addresses, which is then ‘hashed’ within Inland Revenue’s browser before being uploaded to the social media platform. This is where I think the tech specialists have raised concerns that the hash technique is not as secure as Inland Revenue thinks.

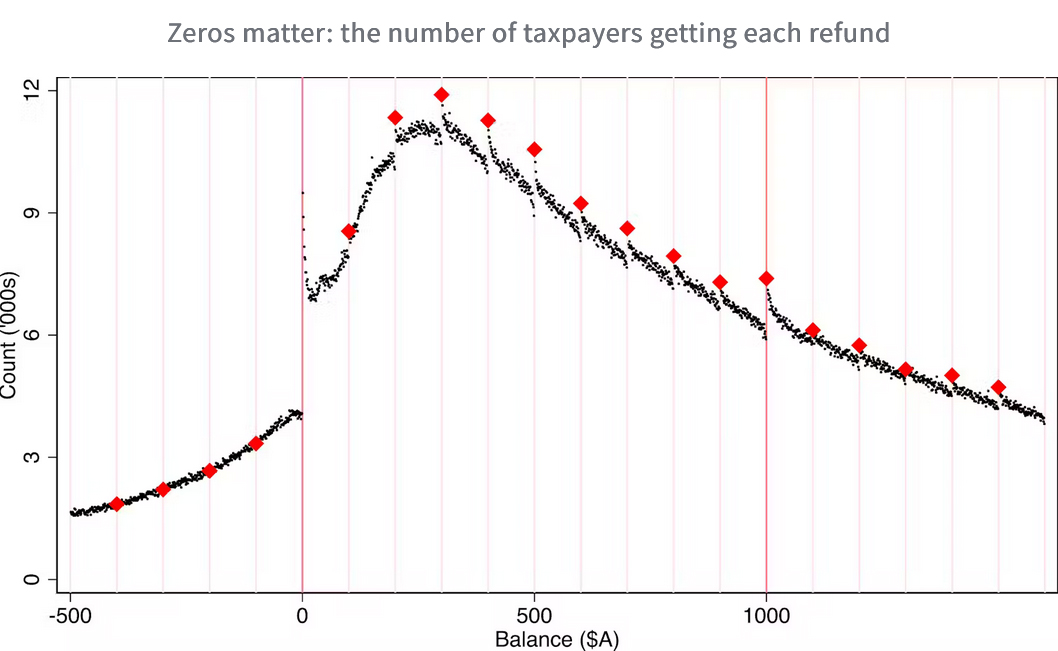

Australia – the Lucky Country again

And finally, an interesting story from Australia about tax refunds. A research team at the Australian National University’s Tax and Transfer Policy Institute discovered a “striking” number of returns generating round number refunds (basically any digit ending in zero). The unit examined 27 years of de-identified individual tax files and found far more refunds of exactly $1,000 than of $999 or $995.

The unit concluded these returns are more likely to be driven by efforts to evade and minimise tax and are costly for the Australian Tax Office to audit such as work related expense deductions. Unlike New Zealanders, Australians can claim deductions on their tax returns. Somewhat concerning to me as a professional is that zeros in tax returns prepared by agents were twice as common as those prepared by taxpayers.

What this article is driving at is that some of the complexity of the Australian system results in the system getting gamed. Back in February you may recall Tracey Lloyd, Service Leader, Compliance Strategy and Innovation at Inland Revenue was a guest on the podcast. Based on our discussion and my own observation I would have confidence that Inland Revenue would not get caught out the same way thanks to the Business Transformation programme. As Tracy recounted, Inland Revenue can track live changes and they can see people just trying to square the return off to what they regard as an acceptable number.

Anyway, it’s an interesting story. It shows the differences between our tax system and that of Australia, but it does seem a little rich that not only can you earn more in Australia, but you get bigger refunds.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Earlier this week, Nicola Willis, National’s finance spokesman, released information she had obtained from Inland Revenue regarding the cost-of-living payments. Included in this information was the fact that some 6,629 payments were made to individuals with overseas mailing addresses. Now it is possible that some of those persons did actually meet the criteria of being tax resident and also physically present in New Zealand at the time of the payment, however it seems more likely most of those payments were made to ineligible recipients.

This data supports anecdotal evidence I’ve heard from other tax agents who have reported examples of non-resident clients receiving the payment. And the fact that a significant number of payments were made to apparently readily identifiable non-residents is concerning is concerning and points to a potentially systemic error.

Nicola Willis also asked a number of questions regarding ineligible recipients. According to written answers provided by the Minister of Revenue currently, Inland Revenue is not aware of any recipients who were either in prison or under the age of 18, which is a bit reassuring.

It also emerged that 49,300 payments were made to persons who only declared investment income. Now that’s an interesting statistic itself, but as an Inland Revenue spokesman noted, the eligibility conditions did not prohibit payments to such persons so long as they met the three key criteria of their income being under $70,000 are tax resident and are physically present in New Zealand at the time of payment.

In the wake of the fallout from the first payment cycle in August, Inland Revenue has tightened up its processes before the second wave of payments made at the start of this month. As a result, the number of people receiving cost-of-living payments dropped by about 54,000. These types of checks apparently included Inland Revenue screening and questioning people who accessed their myIR accounts from an overseas Internet address.

MyIR is likely to be an extremely useful tool for Inland Revenue for spotting potential discrepancies. I do know one case where they noted that some numerous changes had been made to a draft return before it was finalised and when the return was subsequently investigated it turned out that the changes had been aimed at maximizing the available foreign tax credits in excess of what was allowable.

In relation to the cost-of-living payments errors were inevitable given that they would be made to an estimated 2.1 million recipients. For me, the bigger issue here is whether Inland Revenue is properly resourced. It estimated it required between 750 and 1,000 staff to deliver the payments. This is the equivalent of nearly 25% of its headcount of 4210 as of June 2021. The questions I’d be raising is why are so many additional staff required, particularly when you consider that Inland Revenue has just completed a $1.5 billion Business Transformation programme?

There’s also the question that there does seem to be a systemic error in relation to those payments made to individuals with overseas mailing addresses. In short, this is disappointing and shouldn’t really have happened. No doubt we’ll hear more about this as National is firing lots of questions on the matter at the Minister of Revenue, its MPs address on average somewhere between 80 and 100 written and oral to the Minister of Revenue each month.

Doomed, but an important point made

Moving on, last year I discussed a Taxation Review Authority (“the TRA”) case in which the taxpayer wanted assessments to be amended to reverse the effect of the over-taxation of a lump sum payment of $150,000 she had received from the Accident Compensation Corporation. This payment represented backdated compensation in respect of the previous compensation, which she should have received over the period April 2014 to September 2017. Instead, the back dated compensation was eventually paid as a single sum and subject to PAYE.

At the time, the taxpayer argued that this represented over-taxation as the payment should have been treated for tax purposes as having been derived on the accruals basis and spread over the income years to which the payment related. The Taxation Review Authority dismissed her challenge, but she has taken her case to the High Court who heard it late last month.

Her appeal was pretty much doomed from the start because currently there is no authority for the payment to be treated as she wishes, although conceptually I believe it’s a reasonable approach. And it transpired that it was a doomed appeal because the High Court declined to exercise its discretion to extend the time for her to file an appeal against the TRA decision.

But as I said, I think the point she is making is valid. Subsequent to the TRA case I obtained information from ACC under the Official Information Act about how many people had received backdated compensation.

And it turns out hundreds of people each year do receive such payments. I therefore took the matter up with Inland Revenue and Parliament’s Finance and Expenditure Committee. I understand that Inland Revenue officials are currently reviewing the treatment of lump sum payments made by ACC and the Ministry of Social Development with a view to reporting to ministers in the coming months. I’ll update you on any developments as they emerge, but that does sound hopeful.

Global tax reform effort broad but it stutters

Yesterday, the OECD released its annual publication on tax policy reforms. This provides comparative information on tax reforms across countries, and this edition focuses on the tax reforms that were introduced or announced during 2021. This 2022 edition has the largest country coverage in its history. It covers the tax policy reforms made in 71 member jurisdictions of the OECD/G20 inclusive framework on the Base Erosion and Profit Shifting on international tax reform and includes all 38 OECD countries.

The report (not available as a download) breaks down into four parts. The first looks at the macroeconomic background and includes an overview of developments in the global economy. Part two presents the latest trends in tax revenues and in the composition of taxes and also identifies how these were affected by the arrival of the pandemic in 2020. Part three provides detailed description of those tax reforms that were introduced in calendar year 2021. Part four is a special feature which examines measures countries have introduced in response to rising energy prices and also has some policy recommendations.

The key policy trends identified are that personal income taxes and Social Security contributions reduced in most countries, as policymakers tried to boost economic growth and promote equity. That said, changes in personal income tax rates were less common than in previous years. Measures were targeted towards low- and middle-income households, particularly those with children aimed at promoting employment and providing in-work benefits.

Corporate income tax rates were cut in four countries. And the general convergence of corporate income tax rates across the countries continues. However, the big development last year was the agreement of 137 jurisdictions to the Two Pillar solution to reform international tax rules. Now, that seems to be stalling at the moment, but still, as I said, represents a major development.

With regard to VAT (Value Added Tax or GST), not many changes happened last year other than the reversal of most of the temporary VAT reductions introduced in the wake of the pandemic in 2020.

In the field of environment related taxes, the OECD report some progress, but at a slower pace than previously. The effect of carbon prices remains low overall because of the temporary cuts to energy taxes that started to come in with effect towards the end of 2021.

In relation to property taxes there were some measures introduced promoting progressivity and fairness. These predominantly involved tax rises either through increases in tax rates or base broadening measures. The bright-line test being extended from 5 to 10 years last year is one such example of that. The report points out that such measures are often trying to promote the efficient use of existing housing stock as well as greater fairness of property taxation, a long running theme of this podcast.

Part Four on the support measures introduced by governments to try and protect households and firms from the impacts of high energy prices is interesting reading. Here in Aoteaora New Zealand, the major energy issue has been the impact of petrol prices. Fortunately, because of our high renewable sector, we’ve been somewhat shielded from the impact of higher energy prices. But if you’ve seen reports coming out of Europe and Britain in particular, you will know that some horrific energy price rises are either on the horizon or are happening right now.

The OECD report recommends a shift towards more targeted measures aimed at helping those on lower incomes. This “may require improvements to existing transfer and social welfare systems.” So as often with a lot of the stuff we see coming out of the OECD it’s very interesting to see international trends and consider those in a New Zealand context.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Last week, on the same day as the Budget, Newsroom carried a story about Google and its taxation practises and the Minister of Revenue, David Parker’s views on that. And it was surprisingly blunt. He was, as the article put it, somewhat scathing of Google’s reticence to pay more tax.

The head of Google in New Zealand, Caroline Rainsford, had given an interview to Newsroom, which coincided with the Budget, and it outlined how Google has been pushing back against the nascent plans by the government to set in place its own digital services tax. This is conditional on whether the OECD cannot reach agreement on a unified approach to taxation.

Anyway, Rainsford said that basically, although Google is for the OECD development of a simpler and unified tax system, it’s not encouraging a unilateral approach here. In other words, please don’t tax us more, but we’ll be happy to look to see about what’s happening with this international tax initiative.

Google’s parent company Alphabet reported new net profit of equivalent of US$48 bln for the year ended 31 December 2020. And that makes it the eighth most profitable company in the world.

But the Minister of Revenue, David Parker, returned fire on this. And he noted that Google New Zealand paid $3.6 million in income tax in the year to December 2019, based on a profit of $10.6 million and revenues of $36.2 million. Apparently, similar numbers can be expected for the year ended 31 December 2020, when they’re reported shortly.

The thing which appears to have got Mr Parker’s goat is that Google’s estimated ad revenue in the country is close to $800 million, he told Newsroom;

“They could voluntarily pay some tax on the profits taken out of New Zealand already, but they’ve obviously not done that. That revenue used to be earned by media companies. Media companies would have paid tax on it. And other media companies suffer competitive disadvantage competing against Google when Google does not pay a fair amount of tax. It’s not fair and something has to change. And Google is the biggest.”

He points out the ad revenue which are being delivered in New Zealand are not being reported within the New Zealand tax net.

This is an issue we’ve talked about beforehand all around the world. And one solution that governments have put forward, pending some form of international agreement on, it is a digital services tax. That is rumoured to be in the order of maybe three percent is one number that’s been outlined. And estimates of how much it might raise, maybe between $30 and $50 million.

But I think the Minister’s point about the amount of revenue that Google is taking out the country and how that might have played in the New Zealand media companies that earned it, is a valid one. Even if it were the DST of $30 to $50 mlnn, that’s still nowhere near what would be the income tax on $800 million of revenue. So this issue is clearly one that Mr. Parker is paying particular attention to. And obviously, given Caroline Rainsford’s comments on that, Google is slightly concerned about the matter.

We don’t know how much other digital companies such as Facebook, LinkedIn and Twitter take out of New Zealand through digital advertising. Google is clearly the biggest. It’s thought overall including Google’s $800 million there could be as much as one billion dollars of ad revenue going offshore. So the government will be looking at that.

It will be encouraged, no doubt, by the announcement from the US Department of Treasury this week that it is in favour of a global minimum tax rate, and it has suggested that it should be at least 15%. The US Treasury has said that 15% is a floor and discussions should be continued to be ambitious and push that rate higher – 21% is a number that’s been raised previously. But the US Treasury’s view is

“a global minimum corporate tax rate would ensure the global economy thrives based on a more level playing field in the taxation of multinational corporations and would spur innovation, growth and prosperity while improving fairness for middle class and working people”.

And no doubt Minister Parker will say amen to that.

On the other side though, the UK is the only country in the G7 which hasn’t signed up to this multilateral deal that’s being put together by the OECD. And Boris Johnson’s Government has been described as “lukewarm and evasive” on the matter. I think lukewarm and evasive is something that plenty of people have said about Boris Johnson, the latest of which being his former special adviser, Dominic Cummings, last night. But the UK also has long standing cultural or actual colonial links to many of the tax havens which are at the heart of the whole issue.

So we’ve got an interesting combination of factors going on here. Minister Parker is clearly looking at the whole Google and digital taxation matter and is obviously happy to push ahead by applying pressure and maybe push ahead with the implementation of a digital services tax. Which, by the way, the Tax Working Group said might be something to have in place if an international agreement could not be made.

On the other hand, there’s some progress on this by the US Treasury throwing its weight behind a global minimum tax. But then we have the pushback from the UK, or rather, we should say the UK not making a decision. And then there’s been pushback, as I mentioned earlier, from the likes of Ireland with its 12.5% corporate income tax. So it’s internationally the biggest thing that’s going on in tax right now. And it’s a question of just watch this space and see what develops.

Heads the IRD wins, tails the taxpayer loses

Now, moving on, a few weeks back, I discussed a case brought in the Taxation Review Authority against the Commissioner of Inland Revenue contesting the tax treatment of a lump sum paid to a claimant by ACC.

The payment was for weekly compensation for the period from the date she was injured on 22 April 2014 to 17 September 2017. And the taxpayer contended that the payment should be treated for tax purposes as having been derived on an accruals basis and spread over the income years to which the payment related, rather than being taxed in the year in which it was received. As is the current practice.

And this, as I mentioned at the time, is a longstanding issue I have been aware of. And it can mean for claimants that they receive a lump sum, and instead of being taxed at an average rate of 17.5%, they find the lump sum taxed at 33% or even potentially now at 39%. So, it’s an issue I think needs looking at.

I subsequently made an Official Information Act request to ACC about the number of such payments for backdated weekly compensation. ACC replied this week, and it made for some interesting reading. In the year to June 2017, the number of such claimants was 1,187. They received on average $42,482. The median amount, by the way, was $21,643. The maximum was $650,000.

And for 2018 similar sort of numbers – 1,172 claimants, 2019 saw 1,283, and in the year to June 2020 it was 1,466, who received on average $42,505. The median there was $21,146, but the maximum was an eye watering $1,180,000.

There’s a consistent trend there, and enough people in the system and big enough numbers for Inland Revenue Policy and the Minister of Revenue to have a look at that. We do some averaging, for example, it has been pointed out to me, in farming cases we average some of the income because of droughts. So, spreading income over several years in which it relates is not unknown to the tax system and our financial arrangements regime actually operates on that principle.

I propose to send these numbers off to Inland Revenue Policy and to the Minister of Revenue’s office. I’ll keep you posted as to how things develop from there.

Square metre rate up +4.7%

And finally this week, the square metre rate for the year ended 31 March 2021 has been set by Inland Revenue at $44.75 per square metre. That’s up from $42.75 per square metre for the year ended 31 March 2020.

Now, although this sounds quite a technical thing, it relates to the calculation of home office expenses and Inland Revenue’s square metre rate option provides a simplified process. Which means that taxpayers don’t have to keep detailed records of utility costs, contents, insurance, Internet on their private residence, and then have to apportion these costs between business and private use. Instead, they simply apply the rate to the area of the house that is used for business purposes.

It’s a nice, simplified process, something I think we should see more of in the system to try and simplify the process for clients. I think Inland Revenue would have the information or would be able to dig out some of the information for this expense, maybe by an analysis of GST returns. By the way, premises costs such as mortgage interest rates and rent, still have to be claimed based on the business proportion of the actual expenditure incurred by the taxpayer.

This is a sort of throw away measure it seems, but one that actually affects quite a lot of people. And as I said, I think we should see more of this setting rates, giving maybe a standard deduction for people, just to simplify the system.

Well, that’s it for today. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients until next week, ka kite āno.