Treasury Analytical Note examines the effects of taxes and benefits for the 2018-19 tax year

The Australian Tax Office gets heavy with the Exclusive Brethren – will Inland Revenue follow suit?

Understandably the start of the new tax year on 1st April and the increase in interest deductibility for residential investment property to 80% was generally greeted by residential property investors with enthusiasm. Users of apps such as Airbnb and Uber, on the other hand, were less enthusiastic because the provisions relating to GST on listed services also took effect on 1st April. It has become clear that this change has caused some confusion and led indirectly to price rises.

Now GST on listed services refers to online marketplace operators who “facilitate the sale of listed service”. This is the so-called “Apps Tax”, which National promised to repeal when it was campaigning in last year’s election but then decided to keep it because it needed the money to make up for the loss of its overseas buyers tax.

These rules apply to the likes of Airbnb, Uber, Ola, and Bookabach which facilitate the sale of related the services. They now have to collect and return GST when the relevant service is performed, provided or received in New Zealand. It doesn’t matter whether or not the seller, the actual person doing the providing of the Uber or Airbnb, is GST registered. (For those already GST registered the change will have little effect).

Confusion and an unnecessary price increase?

However, a significant number of those providing the Uber or Airbnb, are not GST registered because the total services they provide annually are below the GST registration threshold of $60,000. But the introduction of the apps tax has prompted some of these non-registered persons to effectively increase their prices 15% to take account of the GST charge. However, this overlooks that though as part of the changes those non-GST registered persons can expect a 8.5% rebate under the flat-rate credit regime scheme.

What happens here is the offshore marketplace (Uber or Airbnb) will collect 15% GST on the booking but then pass 8.5% of that to the persons actually providing the Uber or Airbnb. But as an article in The Press notes, it appears many people now think they are GST registered and have effectively increased their prices by 15%. As Robyn Walker of Deloitte said, there definitely appears to be some confusion around hosts about this law change, and probably many don’t fully appreciate that they’re getting this 8.5% rebate.

As GST specialist Allan Bullot of Deloitte, noted there is a lot of confusion with Airbnb. It’s a complicated area, and something Airbnb providers are very careful about is registering for GST because of the fear they might have to pay GST if they sell the property to someone who’s not GST registered. In which case they effectively had to pay GST on the capital gain.

It appears what we’re seeing here is that those who have been brought into the new flat rate credit scheme haven’t yet quite worked out how the new rules will work for them. I would expect things to settle down in time and maybe Inland Revenue might put out more guidance. But it would appear that some providers are getting an accidental windfall at this point, although the increase is taxable for income tax purposes. Anyway, watch this space to see how this plays out and whether there’s some tweaking to the rules as this scheme beds in.

Treasury analyses the effects of tax and income

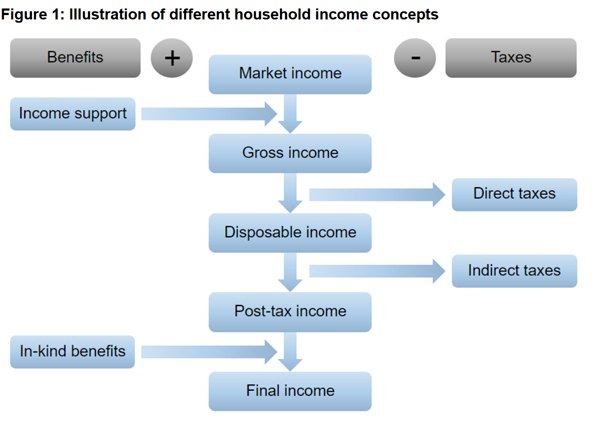

Moving on, just before the end of the tax year, Treasury produced an interesting Analytical Note on the effects of taxes and benefits on household incomes in tax year 2018 – 2019. This is interesting in a number of ways because frequently when people are talking about the effective tax burden, they look at the impact of direct taxation on a person’s pre-tax income.

Some have pointed out this is not really a true measure of a person’s net tax burden. They’re referring to the effect of transfers that people might receive from government in the form of Working for Families or New Zealand Super, but also the indirect transfers such as education and healthcare.

This paper tries to examine that for the 2018-19 tax year and what it does is calculate a household’s “final income” which represents net income after direct and indirect taxes and then adds an estimate of the government spending on health and education services received in kind.

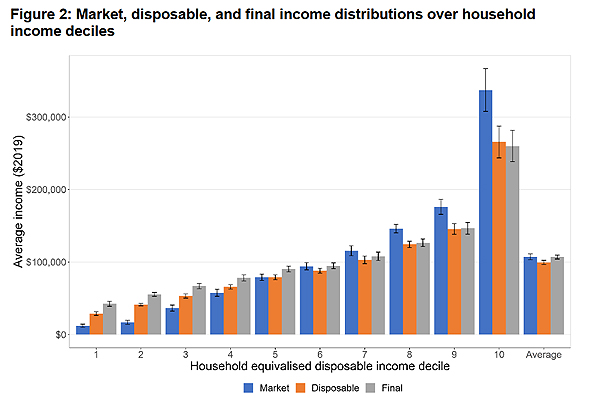

As the paper notes basically when you just look at disposable income, that is market income plus transfers, such as Working for Families credits or New Zealand Super, these are incomes are generally lower than market incomes on average over the population of New Zealand, and fairly unequally distributed. However, once you bring in indirect taxes and in kind benefit payments to get final incomes as defined, these are significantly more equally distributed than disposable incomes and close to market incomes when averaged over all households.

Yes, but what about Gini?

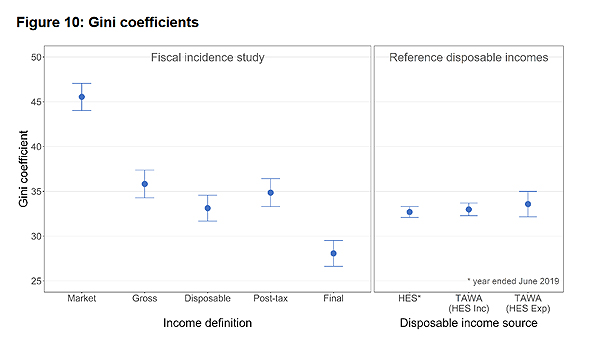

The Note also considers the Gini coefficient. This is the measure of inequality, where the higher the number, the more inequality society is. The Gini coefficient starts at 45.6 ± 1.5, and that drops to 35.8 once you bring in income support payments. Once you include consumption taxes and the benefits in kind such as health and education you end up with a Gini coefficient of 28.1 which is considerably lower and indicative of a much more equal society.

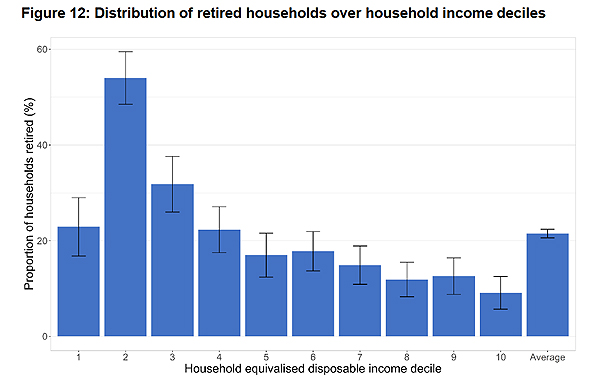

What the Treasury analysis did was to take 66% of all core Crown tax revenue and 68% of core Crown expenditure and allocated that to New Zealand households. Although the effect is approximately neutral as the note describes the effect is unevenly distributed. Households in the bottom five “equivalised disposable income deciles” received on average more in government services than they paid in taxes, whereas the opposite is true for houses in the top four deciles.

The second decile is the one where there’s a large amount of support happening. This is because there’s a fairly high concentration of New Zealand super recipients in that second docile.

The Note also considers “retired households”, where one of the people in the household is receiving New Zealand super.

“Drink yourself more bliss”

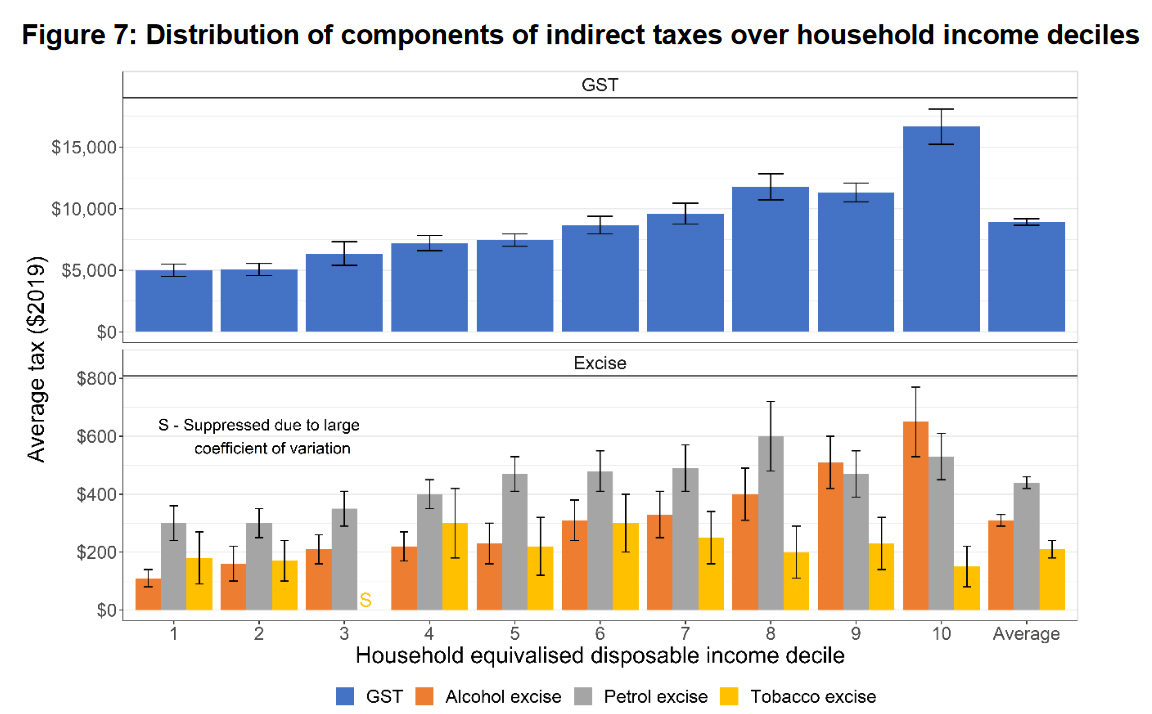

I was amused to see in the analysis of indirect taxes a comment about the average alcohol excise amounts increasing reasonably steady with each decile household equivalent. In other words, the richer the decile, the more they drink. That is a crude summary but it did amuse me.

As I noted, the Treasury analysis covers GST and the effect of economic benefits in kind. There was some commentary at the time of last year’s High Wealth Individual report that it wasn’t really quite fair because it didn’t take into account what the impact of GST and government benefits in kind. This is interesting to see, and I definitely recommend having a read of the note which is a reasonably easy read.

The Australian Tax Office raids the Exclusive Brethren’s business operations

And finally this week, a story coming out of Australia caught my eye about the Australian Tax Office (“the ATO”) raiding multiple premises associated with the global headquarters of Universal Business Team (UBT) on March 19th. UBT is a Sydney registered company that provides services and advicee to about 3000 exclusive Brethren owned businesses in 19 countries.

ATO investigators also apparently raided the head offices of a number of Brethren run companies, including OneSchool Global. In what would also be the standard procedure here, they confiscated phones, computers, documents and other materials. This was done as part of what the ATO call a “no notice raid”. Inland Revenue can do such raids as well, but the point is, it’s not done very often, and the fact that this has happened is extremely intriguing to see.

One of the things that I see frequently pop up in the comments of these transcripts, are questions/ pushback about charities having an exemption from tax on their business profits. It’s more complicated than that, but it’s there’s an obvious tension there. (Again thank you to all those who contribute, your comments are read even if I don’t always respond).

On this point I recall a discussion I had with the late Michael Cullen when he was chairing the last tax working group. During a roadshow event I asked him if there was anything which had surprised him during his role. He replied that he had been surprised by the scale of the charitable sector. He and the group had some concerns about whether in fact, all the charitable donations were being used for charity. In particular whether donations made under an exemption to an exempt business were in fact being used for a charitable purpose. The Tax Working Group’s final report noted:

“80. …the income tax exemption for charitable entities’ trading operations was perceived by some submitters to provide an unfair advantage over commercial entities’ trading operations.

81. notes, however, that the underlying issue is the extent to which charitable entities are accumulating surpluses rather than distributing or applying those surpluses for the benefit of their charitable activities.”

The Sunday Star Times asked Inland Revenue to comment on the ATO’s action but Inland Revenue just dropped a dead bat on it. But I would think, as the Sunday Star Times said, any information relating to New Zealand businesses that came into the ATO’s hands would proactively be passed on under the Convention on Mutual Administration Assistance and Tax Matters, part of the double tax agreement between Australia and New Zealand.

The scale of information exchange which goes on between tax authorities is very largely unknown, but it’s probably one of the most revolutionary changes to the tax landscape which has happened in the last five to 10 years. I don’t think we’ve yet seen anything like the impact that it will have.

Will Inland Revenue follow suit?

In summary the ATO clearly feels that it’s justified in launching a “No notice raid”. The question is whether Inland Revenue is considering something similar or is it just going to sit back and watch carefully? We don’t know, it won’t say, but you can be sure that it will be watching very closely to see what findings that come out of the ATO raid. If it does get anything interesting from the ATO, expect to see something similar happen here.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Australian Tax Office ruling on residency – time for a clearer statutory definition?

Applying for Australian citizenship? Watch out for the sting in the tail.

Submissions closed Friday on the Tax Principles Reporting Bill. Now for a bill that doesn’t actually increase the tax rates this has been a surprisingly controversial bill, mainly because it’s actually perceived as being highly political in its ambit in introducing reporting on tax principles. The speed with which with which it has been rushed through is also controversial because normally tax legislation is developed through what we call the generic tax policy process (GTPP). The GTPP is very well regarded around the world.

But every so often, for whatever reason, the process is bypassed. Sometimes as during the COVID emergency because things need to be done immediately. It’s a framework through which New Zealand tax policy has operated for the better part of nearly 30 years. And it means changes of tax policy and of the particular tax treatment of certain items are developed over time through consultation.

Controversy around the Tax Principles Reporting Bill

In this case, the Tax Principles Reporting Bill came out of left field. There’s been very little consultation about it. In fact, we’ve only had barely three weeks between its introduction alongside the Budget and today. So that’s part of the controversy around it.

The other question is what it really is setting out to do. I think most objections will centre around this question of why is this here? The idea of setting out some ideas about what tax principles might be is not unreasonable in itself. But criticism of the Bill is focusing on whether it’s very clear about what it’s trying to do. For example, Inland Revenue is required to report on certain effective principles and whether there are inconsistencies in the tax system with these principles. But then, as several tax advisors have asked, what action will be taken at that point. There is also no acknowledgement that tax policy ultimately involves trade-offs between principles and politics. To be frank, tax is politics.

I’ve seen one or two interesting comments about which agency should be reporting under the Bill. Inland Revenue or maybe Treasury? There are a whole heap of things to consider about the Bill. Although it comes into effect on 1st July, if there is a change of government, it will almost certainly be repealed.

It’s an interesting Bill because it’s attempting to clarify the basis on which we design and operate a tax system. But it’s also flawed because I don’t think it’s has actually achieved that. We’ll see plenty of pushback and I’ll be interested to read the submissions on the bill. (Shortly after the podcast was recorded, John Cantin published his submission).

Australian tax residency

Moving on, I frequently deal with issues of tax residency. It’s a core part of what I do because tax residency determines what sources of income will be taxed in Aoteaora-New Zealand. There are also rules set out in double tax agreements, and one pretty basic principle wherever you go in the world is that if you have property situated in the country, that country gets what we call the primary taxing rights to it.

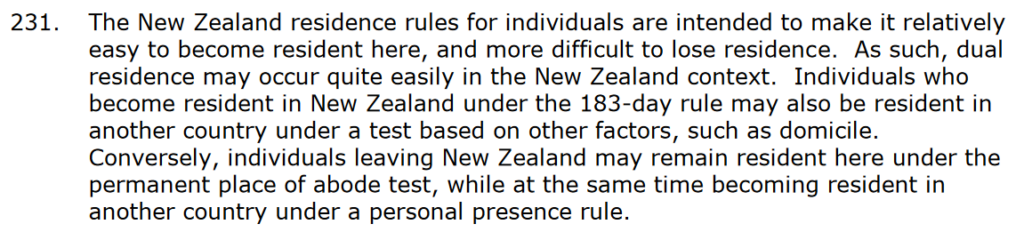

But individual tax residency is a matter of great practical importance. If a person is resident in the country, then that country can tax them on their world-wide income, and that can have quite significant implications.

The Australian Tax Office (ATO) has just updated and released a tax ruling TR 2023/1, on income tax residency tests for individuals. Australia deems a person to be tax resident in Australia if they reside in Australia under what they call the ‘ordinary concepts’ test, and that includes a person whose domicile in Australia, unless they’re satisfied that they have a permanent place of abode outside Australia.

A person is also resident if they have actually been in Australia continuously or intermittently during more than half of the year of income, unless they’re satisfied that they have a usual place of abode outside Australia and they do not intend to take up residency in Australia. There’s also another series of tests, which I’ve not come across, relating whether or not they’re a member of a superannuation scheme or are covered under the Commonwealth Fund.

When you look at these tests you can see there are quite a few value judgements involved. And so there have been calls for the Australian tax residency test to be put on a more statutorily defined basis, most notably by the Australian Board of Taxation. “The Board’s core finding is that the current individual tax residency rules are no longer appropriate and require modernisation and simplification.”

Now it’s of interest here obviously for people going across to Australia, but also because our own residency test is twofold. The primary test, and this is often forgotten, is a person is tax resident in New Zealand if they have a permanent place of abode in New Zealand. You’ll note that phrase, “permanent place of abode” is actually also used in Australia.

Failing that, there’s the days present test where a person is deemed to be resident in New Zealand if they are physically present in New Zealand for more than 183 days in any 12-month period. There’s a subtle difference there between our days present test and many other jurisdictions in that it is based on a rolling 12-month period rather than a tax year. On the other hand, when you get down to defining a permanent place of abode, that involves quite a number of value judgements.

The current residency test is now over 30 years old. As noted above the Australian Board of Taxation suggested that really the Australian test perhaps should be more clearly defined in statutory legislation. And I’m coming around to the view that maybe that’s what we need to do in New Zealand as well. I’ve seen at least one academic article in the past year that’s picked up on this point.

“You can check out any time, but you can never leave”

Now, why we don’t do that is explained in the Inland Revenue Interpretation Statement on residency. Right now the permanent place of abode test does make it easy for someone to be defined as tax resident, but difficult to lose that.

Notably, the Interpretation Statement does not have an example of a time period of how many years must a person be overseas before Inland Revenue would consider that someone has lost their permanent place of abode.

So, this makes residency a very open-ended issue, which is not terribly good in terms of certainty for taxpayers. It’s become more of an issue in the past 30 years since we introduced the permanent place of abode test in 1989 because as we have seen in the last three or four years, the world’s got a lot more mobile with people moving and working around the world.

This issue of being tax resident here, perhaps inadvertently, is actually something that individuals are concerned about. They obviously want to minimise their tax obligations as far as legally possible. On the other hand, governments know that if you set out very specific tests then people will play to the letter of those rules by watching carefully the number of days present in a country.

A British alternative?

The British residency test, the statutory residence test, actually deals with this day count issue pretty well by specifying what it calls “ties”. Depending on how many ties to the UK you have, whether you’ve been tax resident beforehand and how many days you spent in the previous tax years, then the number of days you can spend in a in the UK in a tax year before you become resident drops.

It’s therefore not as simple as you can spend 182 days and then you’re okay. Each year it drops off quite dramatically and basically at its tightest definition you can only spend 16 days in the UK. Obviously, people will still try and manipulate their timing within these limits but the UK test is much more specific and it gives a great deal of clarity.

And I think in our case, just as the Australian Board of Taxation considers, it’s not an unreasonable objective to be looking at a statutory definition of residency which addresses the concerns Inland Revenue rightly has about people trying to game the system, but it provides certainty for people.

Becoming an Australian citizen – beware the potential tax trap

Still on Australia, there was good news recently that there’s now a pathway for Australia and New Zealanders who live in Australia to become citizens. This is very important for the huge numbers of New Zealanders over there, well over half a million. There is, however, a potential sting in the tail.

People will be aware that New Zealand has what we call a transitional residents exemption, which applies to new migrants or people who have returned to here and have not been tax resident for ten years. Under this exemption their non-New Zealand sourced investment income for the first 48 months is generally not taxable here.

Australia has a similar test if it applies to what they call temporary residents and it applies to most New Zealanders living in Australia. The sting in the tail is that if you apply for citizenship in Australia, you are no longer a temporary resident. What that means in particular is your New Zealand assets here become subject to Australian tax, including capital gains tax. The impact of Australian capital gains tax on New Zealand assets is often overlooked. It’s an issue I deal with regularly.

So that’s the trade off on Australian citizenship. Overall, it’s a good news and it puts people who have contributed significantly to the Australian economy on a level footing. But there is a wee sting in the tail for some. So, approach with caution.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Green Party quotes Margaret Thatcher with approval

The Australian Tax Office’s latest corporate tax transparency report

The latest from the OECD on the carbon pricing of greenhouse gas emissions

Last week, the Green Party released a discussion document on what it’s called an excess profits tax. This is part of its “commitment to a progressive and fair taxation system.” What it is saying is that an excess profits tax or windfall tax is required to level the playing field so that, “big businesses are not able to profit to excess when so many people are struggling”.

The proposal comes on the back of data showing that in the 2021 financial year, corporate profits reached $103 billion, up $24.5 billion on the previous year. And you’ll recall that the corporate tax take for the year to June 2022 was almost $20 billion. The Green Party are saying we’ve got several matters going on at the moment. It believes there are excess profits being earned at a time of hardship. There’s also a need to address the impact of the unprecedented transfer of wealth that happened in response to the COVID 19 pandemic.

The discussion document points out that windfall taxes are common in other countries. It notes that the EU is implementing an excess profit tax in the energy sector. Spain has an excess profit tax on the energy sector and banks. Interestingly, the paper then uses the example of Britain under Margaret Thatcher in 1981, when the Conservative government introduced a windfall tax on banks. This was raised the equivalent of about £3 billion in today’s money and represented about a fifth of the profits banks were pocketing at the time.

That obviously attracted quite a lot of controversy back in 1981. The 1981 British budget is one of the most controversial I can recall in my time. But Thatcher was unrepentant about what she did. In her memoirs The Downing Street Years, she responded

“Naturally, the banks strongly opposed this, but the fact remained that they had made their large profits as a result of our policy of high interest rates rather than because of increased efficiency or better service to the customer.”

So, I guess we live in strange times when the Green Party is quoting Margaret Thatcher with approval, but that is a fair point. And bear in mind ANZ reported a net profit of $2 billion for the first time.

So, windfall taxes are not uncommon elsewhere in the world. They are uncommon under the New Zealand tax framework and haven’t really been used for a very long time. They were used during both world wars but apparently, they weren’t entirely successful.

It’s good to get this discussion going because sometimes I feel that the tax debate in New Zealand is very narrowly circumscribed. We’re living in unusual times so is a windfall tax something that could be done? Even if it was, in my view it would have to be a one-off, such taxes shouldn’t be part of the regular tax take. Incidentally, this is a point I’ve seen discussed elsewhere notably in Ireland following the release of a report about its tax system.

The Green’s proposal suggests a windfall tax could have some retrospective effect. This would be highly unpopular and rightly so, for companies, because it would mean there’s no certainty around their planning. Companies might budget for a 28% tax rate but then suddenly find that in fact it’s been increased to 33%. So businesses would find that hard to deal with, but if they knew there was a possibility it would be interesting to see how pricing might play out.

Overall it’s good to see this discussion going on and no doubt it’ll attract a lot of controversy and you can make your own submission on the idea to the Greens. Next year is an election year so who knows what’s going to happen afterwards? But as I said, windfall taxes are used elsewhere in the world. And if they were good enough for Margaret Thatcher, well, who knows?

Aussie ‘transparency’

Moving on, over in Australia, the Australian Tax Office, (the ATO) has just published its eighth annual report on corporate tax transparency. What this does is look at the amount of tax paid by large corporates for the year to June 2021. According to the report, the over A$68 billion paid during that year by large corporates is the highest since reporting started. It’s up A$11 billion or 19.8% on the previous, COVID-19 affected year. Apparently, rising commodity prices were a key driver for the increase in corporate tax.

The report notes that Australia has some of the highest levels of tax compliance of large businesses in the world, with 93% of tax paid voluntarily. This rises to 96% after the ATO has asked a few questions.

The ATO has been running what it calls the Tax Avoidance Taskforce for some time. According to the report since 2016, the ATO has raised tax liabilities of $29 billion and Tax Avoidance Taskforce funding being responsible for $17.2 billion of that amount. (It’s worth remembering “raised liabilities” doesn’t necessarily mean that they’ve been collected). In last week’s Australian Budget there’s an extra $200 million per annum to help expand the focus of the Tax Avoidance Taskforce. This brings the total funding for the Tax Avoidance Taskforce to A$1.1 billion over the next four years.

Now, this report covered 2,468 corporate entities, more than half of which were foreign owned with income of A$100 Million or more. 529 or about 20% were Australian owned private companies with an income of $200 million or more, which is an indication of the size and scale of the Australian economy. Interestingly, there’s a note that the percentage of entities which pay no income tax was 32%.

It’s interesting to see what other jurisdictions do with their tax data. I feel Inland Revenue should do a lot more in this space with the data it receives, but it’s very reluctant to do so at this point. It’s currently not part of its brief, but such a report and other statistics gives us a better understanding of the scale of the economy and what’s happening in it. I would like to see Inland Revenue produce something similar.

Energy, taxation and carbon pricing

Finally, this week, overnight the OECD released its latest report on pricing greenhouse gas emissions. This looks at how carbon prices, energy prices and subsidies have evolved between 2018 and 2021. This is part of a database the OECD is developing to track what’s happening on energy, taxation and carbon pricing.

This report covers 71 countries (including New Zealand) which together account for approximately 80% of global greenhouse gas emissions and energy use. There’s a summary report by country as well. Overall, more than 40% of greenhouse gas emissions in 2021 were covered by carbon prices and that’s up from 32% in 2018. And the average carbon price from emissions trading system schemes and carbon taxes more than doubled to reach €4 per tonne of CO2 equivalent.

And obviously the report goes into what’s happening across the across the globe. There’s been a rise in the amount of greenhouse gas emissions now covered, and that is as a result of the introduction or extension of explicit carbon pricing mechanisms notably in Canada, China and Germany.

What’s termed carbon net prices are rising further in 2021 as have permit prices under emission trading schemes. There’s steady changes in carbon taxes, with new carbon taxes introduced, together with increases in carbon tax rates or the phasing out of carbon tax exemptions.

As for New Zealand, 44.1% of all greenhouse gas emissions are now subject to a positive ‘Net Effective Carbon Rate’ which has not changed since 2018. The report also notes that fuel excise taxes, which are described as an implicit form of carbon pricing cover 23.8% of emissions. Again, that’s unchanged since 2018. So, looking at this, we appear to be stalling a bit on this and I do wonder whether next year’s report might show that because of the cut in fuel excise duty, we’ve gone backwards. However, other countries have also been cutting fuel taxes because of the high inflation in the wake of the war in Ukraine.

Although the level of coverage of greenhouse gases covered by carbon pricing hasn’t changed since 2018, the average carbon price has risen. For example, fuel excise taxes in 2021 amount to €19.73 per tonne of CO2 equivalent. That’s up by +9.4% relative to 2018, which is probably below inflation, though. However, once adjusted for inflation the average Net Effective Carbon Rate on greenhouse gas emissions has increased by +39% since 2018

There’s a lot to consider in this report, more than I’ve had a chance to go through right now. But again, it reflects a constant theme of this podcast about the increasing role of environmental taxation and the scope for opportunities in this space.

What we do with those funds is the other side of the equation. It’s one thing to say we need more taxation. What isn’t always debates is what we do with those taxes. I’ll repeat my longstanding view that funds coming out of environmental taxation in the form of new taxes or the existing emission trading scheme should be used to mitigate the impact of climate change.

There was a report earlier this week identifying 44 communities in great risk of environment impact from climate change which are unprepared for the flood risk. No doubt they will be looking for assistance. In the meantime, Nick Smith, Nelson’s new mayor (and former Environment Minister) has requested government assistance with dealing with the impact of the recent flooding. No doubt there will be plenty more to come on this topic.

Inland Revenue’s new approach to tax investigations

Waste disposal levy good example of an environmental tax

How being six minutes late could cost the ATO almost $100 million

Transcript

This week, more highlights from the Chartered Accountants of Australia New Zealand Annual Tax Conference, are the proposed waste levy increases a good behavioural tax and how being six minutes late could cost the Australian Tax Office nearly 100 million dollars.

CAANZ Annual Tax Conference

Last week, I was at the Chartered Accountants of Australia New Zealand Annual Tax Conference. We heard a number of papers from Inland Revenue, including from the commissioner herself. But the one I want to focus on is on their investigations and what is the future of investigations going forward now. This was chaired by Scott Mason of Findex and Tony Morris of Inland Revenue.

Scott began by pointing out something we had noticed over the past few months – that Inland Revenue had not appeared to be very active in the investigation field and certainly wasn’t being very visible. And he raised the point that in such an environment, voluntary compliance falls and “industry practices” emerge where advisers respond to non-activity from Inland Revenue by thinking that keeping quiet is actually a valid strategy.

Tony Morris responded by acknowledging that that was an issue, but in fact, Internal Revenue after the business transformation restructure was now moving forward again. It had much more data available and understood that data better. For example, he noted that there was now potential to get the EFTPOS data for a particular industry. And then from there calculate what should be the potential cash sales for a business in that industry. The analytics were now available to determine more quickly if there were issues around non reported cash sales.

That’s something I’ve mentioned in the past. Now Inland Revenue will in some cases physically visit a business to see what’s actually going on behind the counter. So a question was then put to Tony – why not release some of this data to tax agents? This is an approach I favour. Tony replied that this can be a two-edged sword. Obviously, tax agents need to use that information proactively. But clients may not want you to know that they’re not doing that well, or that their positions are now in jeopardy, because they have been quietly salting away piles of cash unnoticed, such as the baker who got put away for nearly five years this week. He was jailed after failing to declare some six and a half million dollars in cash sales.

So Inland Revenue obviously wants to clamp down on such behaviour and identify much more quickly what’s going on. But the converse of releasing data to tax agents is that there is a risk that something might be seen as a benchmark. Therefore rather perversely it might encourage behaviour if people say “Well, if that’s the benchmark, we’ve got a bit of leeway to quietly salt away some cash”.

I think in the end the answer to this question of the cash economy is going to be what I talked about last week – the Swedish example – of fiscal control units, a centralised approach that’s already happening.

Australia and New Zealand are slightly behind the eight ball on that area of progress. But it is a matter where we could see change similar to changes we’re seeing in the rest of the world. And I would expect that Inland Revenue, with its enhanced capabilities, may decide that’s an area where it wants to move forward into.

Nudge letters

What Tony Morris talked about was Inland Revenue has developed a policy of what they call sending out “nudge” letters, which are to encourage behaviour in the right place. And these are sometimes often sent to a wide number of clients. The problem is that while that might be encouraging better behaviour at a macro level, it does cause some confusion at the micro level for individual clients who think they are already compliant. So why are they receiving notes about compliance with the automatic exchange of information, for example?

But he also revealed one or two interesting snippets. Particularly one which I think people who file their own tax returns ought to be aware of. If you’re filing your own tax return online Inland Revenue can see how you progress that filing. They will note if you are amending the expenses – this is one thing they watch very carefully. Tony Morris gave the example of someone who amended the expenses that they were claiming in their tax returns 80 times. He also noted that more often than not, early filings before the normal due dates are more likely in Inland Revenue’s experience to be fraudulent.

But he also talked about how Inland Revenue could perhaps use social media to put a message across in a very specific way. We do know Inland Revenue watches social media closely. For example, Inland Revenue might notice that a client is putting his boat into the water at Whangamata on Sunday. So the question that they might put through myIR is “how is your FBT return going?” Because FBT on twin cab utes is one of the great under-reported and probably undeclared sources of income that it might want to have a look at.

That was all very, very interesting. It gave an insight into where Inland Revenue is at, where it thinks it’s going to go, particular areas of interest to it and how it approaches these issues at a tactical level. The ability to watch what goes on in a tax return I think is fascinating and should serve as a warning for people. And how it also might possibly make more use of watching social media to then make quiet “nudges” to make sure people are compliant. Tony also made a note that the initiatives on the property area have seen the strike rate gone up astronomically since they started really looking into this area in the wake of the introduction of the Brightline test in October 2015. So that was an absolutely fascinating session from Scott and Tony.

Behavioural taxes

Another highlight of the conference was a debate about whether behavioural taxes were a good thing to have. The team arguing against included Barry Hollow of Inland Revenue. As he said, he found himself in a very unusual position for a tax policy person arguing against such taxes. His extremely witty yet insightful and funny speech carried the day and the motion was defeated. The government wasn’t listening, though, because this week it released proposals for increasing the waste disposal levy.

Now, this has caused a bit of controversy. But it is something to think about. And a point raised by the Tax Working Group is whether such a tax is a behavioural tax or just a tax grab, increasing the tax base. But the idea is to recycle funds raised. For example, half the revenue would go to councils to fund resource recovery and other waste related infrastructure. And then the remaining money would go to the Waste Minimisation Fund, which provides grants for waste reduction.

And to repeat a point I made earlier at the time of the launch of the Tax Working Group, Sir Michael Cullen talked about recycling the revenue from environmental taxes to help people transition to a lower carbon economy. Or in this case, a lower waste economy, because the amount of waste per capita New Zealand produces is extraordinary. There’s also the fact this waste disposal levy is a very good example of a behavioural tax which works.

The Tax Working Group cited the example of the U.K. They raised their waste levy tax rate from £10 pounds a tonne in 1996 to £80 a tonne by 2016. But over the same period of time, the annual waste in landfills fell from 50 million tonnes a year to 10 million tonnes a year.

So, you saw the tax increases achieving the desired result of lower waste And that’s something I think we really need to think about going forward. The reflex “All taxes bad, no tax is good” approach is understandable in political terms.

But you’ve got to look beyond the politics of this. If this tax is being recycled to reduce waste and we’re moving away from the use and disposal economy to reach “the circular economy” as it is called, then encouraging that is something we all need to be on board with. Because our environment in New Zealand is our key selling point. You know Stephen Colbert on The Late Show. He’s showing off the beauties of New Zealandand we have $46 billion of agricultural exports. They’re all dependent on our natural environment. So protecting them and making sure we make the best use of it and keep it free of pollution so we are green and clean is something we should all be behind.

The ATO stubs its toe

Finally from the “So you think you’re having a bad day” files, the Australian Tax Office has been forced to ask the Federal Court, the highest court in Australia, for special permission to appeal a decision it lost in the High Court, involving a A$92 million tax bill against mining giant Glencore. This is quite a significant transfer pricing case, by the way. And apparently the reason why the ATO had to find a special motion was it was six minutes late in meeting a critical filing deadline last month.

Now, schadenfreude aside, the case is a good, if extreme, reminder of the critical importance of filing tax returns and elections on time. Inland Revenue is reasonably flexible about late filed tax returns and can be persuaded to waive penalties in many cases. However, it is typically inflexible about other deadlines, such as those involving the disputes process, Notices of Proposed Adjustment, Notices of Response and elections to join the look through company regime. Ask any tax agent and I’m pretty sure we’ve all had situations where we’ve encountered delay in filing for the look through company or its predecessor, the qualifying companies.

These are really, really important and the big lesson is be aware of the timing of your elections and don’t leave it to the last minute. Otherwise, you too could be tripping up over a significant tax bill, although maybe not to the tune of 100 million dollars.

Next week, I’ll be joined by Chris Cunniffe of Tax Management New Zealand. We’ll be discussing the role of tax pooling and also the results of TMNZ’s recent survey of tax agents. Inland Revenue might not like that one too much.

{kind=link}