Facebook New Zealand’s 2023 results show the scale of the advertising revenue going offshore.

Treasury’s blunt warning ahead of the Coalition Government’s December Mini-Budget.

The Australian budget was announced last Tuesday evening and although comparisons with Australia are not always constructive, there are several points of interest, not just in terms of how the tax systems operate, but also about initiatives which could replicated here.

The Treasurer is predicting a surplus for the period to June 2025, but after that, apparently things get a bit tougher. A little bit like Aotearoa-New Zealand in that regard. The key point with an election coming up, is the “Stage Three” tax cuts take effect from 1 July. As is well known and has been the subject of some commentary over time, Australia has a tax-free threshold of A$18,200. That threshold isn’t changing, but what is happening is that the tax rate for the next bracket between $18,200 and $45,000 is dropping from 19% to 16%. The big change is in the next tax bracket where the rate drops from 32.5% to 30% for income from A$45,000 all the way up to A$135,000 Australian. Quite apart from the rate change the bracket has been extended from A$120,000 to A$135,000. The 37% bracket remains in place and applies for income between A$135,000 and A$190,000. Over $190,000 the top rate of 45% kicks in.

We had record migration last year and a lot of those people are heading to Australia and no doubt these tax measures will make it more attractive. I’m in the camp that you can’t ever compete on tax cuts because there’s always someone better able to reduce tax rates further. Right now that’s Australia.

One of the interesting comments I’ve heard about the Australian budget, is that the Australian Treasury forecasts, are frequently incorrect sometimes resulting in unexpected surpluses. Apparently, the Australian Treasury consistently under-estimates forecast inflation and the iron ore price, which since Australia is such a huge minerals exporter, is quite critical. Generally, the Australian economy tends to perform better than Australian Treasury predictions.

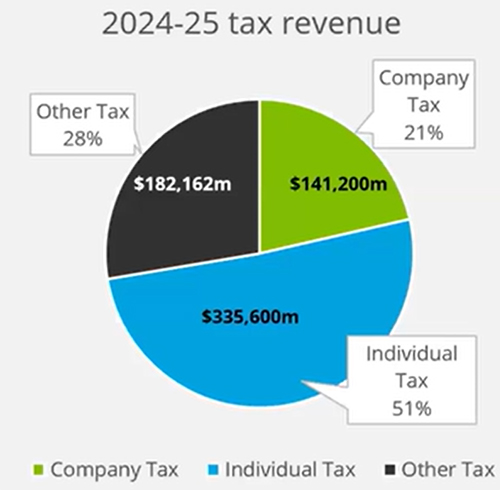

Another strong Australian corporate tax result

Furthermore, as the Australian economy is performing so well, the Australian company tax take is now a significant proportion of the total tax revenue. For the coming year to June 2025 it’s predicted to be A$141.2. billion or just over 21%.

(Deloitte Australia)

That’s a substantial sum by world standards. For comparison, in the UK (a near comparatively sized economy) the proportion of the tax take that comes from companies is usually between 7% and 10%. We are also a country with a fairly high corporate tax take. In the year to June 2023, it was 16.1% of total tax revenue. However, one of the reasons the Government’s books are deteriorating is the decline in the company tax take which is expected to fall to 15.6% of the total tax revenue this year.

Australian cost of living initiatives

There were also a number of other direct cost of living initiatives, including a $300 energy bill rebate to all Australian households. Eligible small businesses will get a $325 rebate during the coming year to June 2025. The Australian Government will also provide A$1.9 billion Australian over five years to increase the Commonwealth Rent Assistance maximum rates by 10%. (This would appear to be the Australian equivalent of the Accommodation Supplement).

Over here we don’t know whether the Budget in two weeks’ time will contain specific cost of living responses similar to these Australian initiatives but that appears highly unlikely. Based on what we’ve heard so far, the Government is relying on the individual tax threshold adjustments to sort of deliver cost of living relief.

Beefing up the ATO

Australia has a capital gains tax and some changes are proposed around the application of capital gains tax to non-residents. These are intended to ensure from 1 July 2025 that foreign residents are caught within the rules in relation to disposals of land. That’s something people tend to forget, that non-residents are taxable on disposals of Australian property and these proposed rules are intended to strengthen that compliance.

Another thing of note, which I think we will see something similar in our budget, is increased funding for various Australian Tax Office (the ATO) compliance programmes. The ATO has currently got three such programmes on the go, covering personal income tax, the shadow economy and tax avoidance (Tax Avoidance Taskforce). The Budget announced a new initiative countering fraud. In terms of dollar returns on these programmes, they range between four to one for the funding of the personal income tax down to a little two to one for the Tax Avoidance Taskforce.

Small businesses and ABUMS

The other thing that I think people would love to see here is the Instant Asset Write Off. This is where small businesses can purchase an asset up to $20,000 in value and claim an instant write off. This programme has been extended for another year. Apparently one of the reasons it has been extended is that the legislation which would have terminated that programme hasn’t yet been passed. Australian governments have a habit of announcing measures and then not getting around to passing the relevant legislation resulting in something with the delightful acronym ABUMS – Announced But Unacted Measures.

Overall, there was some interesting stuff in the Australian Budget including another measure I’m going to talk about next, which I also wonder whether we might see applied here.

Facebook’s results

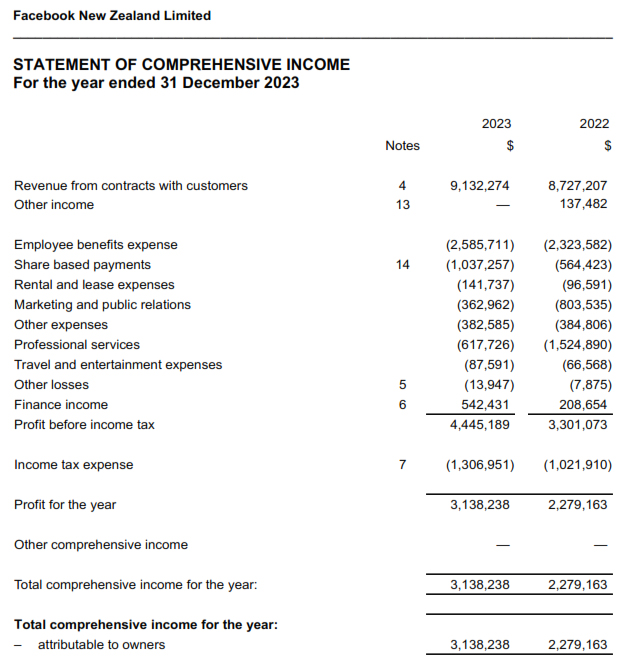

Moving on, Facebook has now released its New Zealand financial statements for the year to 31 December 2023, and these are bound to generate some controversy. The official income reported for the year was $9.1 million and the profit before tax was $4.4 million, resulting in income tax of $1.3 million.

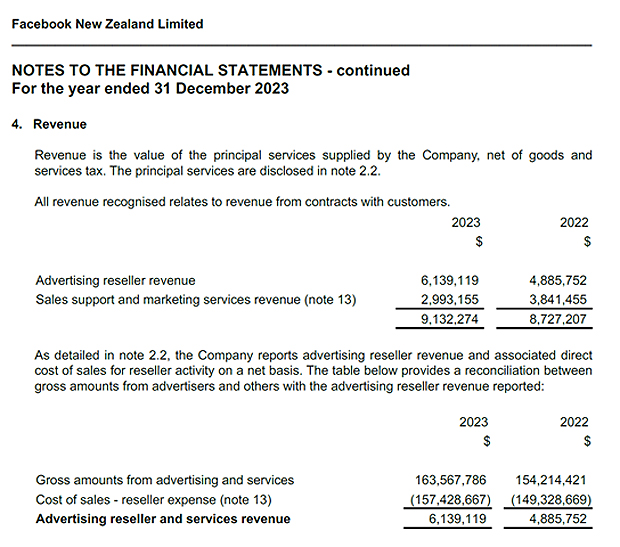

Like Google New Zealand details of the payments to related parties is the very interesting section to look at, together with the statement of cash flows because these give you a better clue of what the scale of Facebook’s activities within New Zealand are. Note 4 to the financial statements, which explains the revenue, sets out what is happening. “The company reports advertising reseller revenue and associated direct cost of sales for reseller activity on a net basis” This note explains that the gross amounts it received in the year to December 2023 from advertising and services was $163,567,786 and then a reseller expense was $157,428,667.

So, although Facebook is reporting income for income tax purposes of $9.1 million, the real scenario is that the revenue that’s passing through it, is substantially higher.

Another Australian example to follow?

Now it so happens there’s a case going through Australia at the moment involving what they call an embedded royalty. Basically the Australian Tax Office took a case against drinks company Coca-Cola in relation to what it perceived as an embedded royalty (and therefore subject to withholding tax) in payments for the right to brew Coca-Cola in Australia.

The Australian budget has a number of what’s termed Intangibles Integrity Measures. One of those it appears is a new provision, effective from 1 July 2026, where it applies a penalty to taxpayers who are part of a group with more than $1 billion in global turnover annually, that are found to have mischaracterised or undervalued royalty payments to which royalty withholding tax would otherwise fly.

Now that’s two years away from implementation, but it’s clearly a shot across the bow of companies such as Facebook or Meta, and Alphabet, the owner of Google, about these reseller services expense. So that’s something to watch how this develops.

And I just wonder whether we might see something similar here, because significant sums of money coming from advertising, are going overseas, and, as I’ve mentioned before, that has had a detrimental impact on our media landscape that it’s basically been starved of cash as a consequence. So, watch this space.

Treasury’s warning on structural reform

Finally, this week there was a budget information release from Treasury of papers relating to the Government’s mini budget in December. And one of the papers titled Implementing the fiscal strategy has attracted quite a great bit of interest.

In the paper Treasury sets out in fairly blunt terms that there is a requirement or need for structural reform of the tax system. The key paragraphs are 24,25 and 26. Paragraph 24 notes

“Structural reform of the tax system is the most effective way to ensure it is flexible and capable of raising additional revenue sustainably… Such reform would need to recognise that while revenue raising is the primary purpose of the tax system, its distributional and economic objectives are also important.”

Plenty of wry smiles here for those who listened to the Titans of Tax expand on this very point.

The problem with fiscal drag

Paragraph 25 then discusses the importance of fiscal drag

“Since 2010, fiscal drag…has played an important role in enabling successive governments to use the tax system to meet their revenue objectives. This has placed increased pressure on the tax system’s other objectives. If you wish to offset or end fiscal drag, through adjustment of personal income tax rates and thresholds the fiscal headroom which needs to be created will further increase”.

In other words, if you want to end fiscal drag, you really do need to rebalance and reshape the tax system,

I’ve seen some commentary that this was blunter advice than was provided to the previous government. I don’t actually subscribe to that view because in my view Treasury’s 2021 long-term fiscal insights briefing He Tirohanga Mokopuna was pretty clear that a fiscal crunch was coming. I just think that because there’s been a change in government, what Treasury has done here is taken the rather softly, softly approach in He Tirohanga Mokopuna and just made it very blunt so the new Government knows from the offset that there are challenges ahead. And to be fair to Finance Minister Nicola Willis and the Prime Minister, they have not denied that. But what they propose to do about it, of course, we’ll have to wait and see.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

New Zealand Budgets are usually exercises in political grandstanding and are the duller for it. While political grandstanding around Budgets isn’t confined to New Zealand, Budgets overseas often have some interesting new tax measures.

Tuesday’s Australian Budget was no exception. As Bernard Hickey pointed out supposedly conservatives the Liberal-National coalition government unveiled a AU$107 billion deficit spending plan for 2021/22 and expects to run deficits for the rest of the decade, building up a debt load of AU$1 trillion by 2024/25 or around 50% of GDP. This is at a time when the Labour Government here is concerned about a net debt to GDP ratio of 32% and has picked a fight with the public sector in the name of restraint. We live in strange times.

Other than splashing a lot of cash, the Australian Budget had a number of tax initiatives which would be viewed with envy from this side of the Tasman.

For starters, they included an additional AU$7.8 billion in tax cuts by retaining the low and middle income tax offset, and that’s been extended for another year. Now, remember, our personal tax thresholds have not been changed since 1st of October 2008. And the tax rates themselves haven’t been changed, with the exception of the new 39% rate, since 1st October 2010.

For businesses, the measures included extending the temporary full expensing of depreciable assets until 30 June 2023. Now remember, a similar measure here only increased the depreciable assets threshold for a write off or full expensing to $5,000 dollars, and that expired on 17th March.

The temporary loss carryback regime will also be extended by another year to 30 June 2023. And that enables businesses to offset losses against profits as far back as the year ended 30 June 2019. We have only allowed the temporary loss carryback regime for the March 2020 and March 2021. So, again, big difference in the approach.

There’s something else which is a bit of a worldwide trend called a patent box regime, which taxes income derived from Australian medical and biotech patents at 17% effective concessional corporate tax rate. The ordinary corporate tax rate in Australia is 30% (or 25% cent for SMEs). This new regime, which will start from 1st July 2022, is intended to encourage businesses to undertake the research and development in Australia and keep patents in Australia. And Australia is now one of over 20 countries, including the UK and France with this sort of regime,

There’s changes to employee share schemes and a Digital Tax Gains Tax Offset to promote the growth of the digital games development industry in Australia. And if you think gaming has little value, think again. The Kumeu based gaming company Ninja Kiwi was recently sold for over NZ$200 million.

Tax residency

However, probably the most significant change from a New Zealand perspective and one which will impact people here is the change in the tax residency tests.

From 1st July the primary test for individuals will be what is described as a simple bright-line test. A person who is physically present in Australia for 183 days or more in any tax year will be an Australian tax resident. Now, if the individual doesn’t meet that primary test, there’s a number of secondary tests that will depend on a combination of physical presence and what are described as a measurable, objective criteria.

As I said, this rule applies from 1st July, and so people who are making regular and frequent trips to Australia will need to keep in mind the impact of the new rules. Furthermore, the Australian Government is going to consult on expanding the newly revised residency test for corporates to include trusts and corporate limited partnerships. There’ll be consultation going forward on that. Watch this space.

So, a lot to unpick there and frankly, a lot more interesting than what I expect to see in next week’s New Zealand Budget. The key thing is I noted for New Zealanders is the residency test. So start tracking your days carefully and if in any doubt see an expert. It’s arguable that the terms of the double tax agreement between Australia and New Zealand may get you out of Australian tax residency because of what we call a tie break provisions which take you back to New Zealand. But still, there could be a few pitfalls in there which can be avoided with proper consideration.

Moving on, as everyone is aware, the top income tax rate increased to 39% for income over $180,000 with effect from 1st April 2021. An article in Stuff on Wednesday pointed out that a number of people were getting quite concerned about the impact of this on disposals of what may be capital gains – investment properties in particular – because we have a new Bright-line test as well, extended to 10 years.

Currently the position is, income or gains that arise from the sale of a property subject to the bright-line test is added to a person’s annual income and taxed at the marginal rate. That’s the rule New Zealand has always applied. And if you recall when John Cantin and I discussed whether in fact that was perhaps appropriate for taxing lump sums. The view of Inland Revenue was, as John summarised it, if there was no tax paid during the time the gains were accruing, it seems only fair to apply the rate at the time of disposal.

But 39% is, as the article pointed out, high by world standards. But there’s a trend in the world now to look at that issue. And this is something I discussed on The Panel on Wednesday with Wallace Chapman on Radio New Zealand.

Although 39% is high by world standards, it’s not entirely exceptional. Countries are now starting to look at the question of capital taxation, and they’re also looking at the very obvious move – if you have a differential tax rate for capital gains, then the temptation is for high income earners to have income treated as capital and subject to a lower CGT rate.

And the Office of Tax Simplification in the UK looked at this in November and produced a report. It suggested to the UK government that they might want to look at changing the tax rates there where the top rate for residential property is 28%, whereas the income tax rate is 45%. But one of the things that caught my eye in the OTS report was the extent to which very large amounts of tax on capital gains are paid by a relatively small amount of people.

The OTS noted that UK£8.3 billion of capital gains tax was paid by 265,000 people in the year to April 2018. That meant their average liability was UK£32,000. By comparison, for income tax purposes, 32 million people paid UK£180 billion, which meant an average liability of UK£5,800. So, in other words, there’s a lot of concentrated wealth going on there. So the OTS said that maybe we want to look at that.

And US President Joe Biden has said the capital gains tax rate that applies for people earning more than US$1 million should be the top personal tax rate of 39%.

Now, coincidentally, or while this is going on, the OECD released a paper on inheritance taxation in the OECD countries. Its summary was that countries should be looking at inheritance tax, estate and gift taxes in general, as having the potential to play a role in the current context of recovering finances in the wake of covid. It also points out that wealth inequality is high and inheritances are unequally distributed across households.

Now, what really stood out in this OECD report was,

“the case for inheritance taxes might be strongest where the effective taxation of personal capital income and wealth tends to be low”

which would almost be as if the OECD were looking at New Zealand and saying, “Yeah, we are talking about you.” Because we don’t have a comprehensive capital gains tax, we don’t have estate taxes, we don’t have gift duties, and we don’t have stamp duties. The absence of any one of those make us unusual in world terms.

So plenty to consider in that. We won’t see any of this coming through from our Government. But I do wonder, watching the world, whether the trends that are developing there around the taxation of capital will emerge here. The OECD report really goes into how much concentrated wealth there is and the issues around that. It is saying, for example the wealthiest 10% of households own half of all household wealth on average across 27 OECD countries for which data were available.

And the wealthiest one percent, own 18% of household wealth on average. Financial wealth is particularly concentrated. The wealthiest 20% of households may own half of all real estate wealth, but they own nearly 80% of all financial wealth. So there’s a lot going on overseas looking at issues which we’re not immune to down here.

Although we’ve had the Tax Working Group report, I thought that the question of wealth taxation was something that was largely sidestepped. Obviously, they went with a capital gains tax proposal which was knocked out. And by the way, to circle back to the question of the tax rate that applies. One of the results if the capital gains tax proposal by the Tax Working Group had been implemented, by broadening the tax base it would have enabled the tax rate to stay at a 33% level.

Minimum tax rate for MNCs

And talking about tax rates elsewhere, there’s still a debate going on around international minimum corporate tax rate and progress appears to be being made on this. But one commentator has suggested that ultimately the rate that will be chosen for this minimum tax is probably going to settle very close to the Irish corporation tax rate of 12.5%. They’ve had it for decades now. And it’s why the Irish are pushing back very strongly against suggestions that this minimum tax should be 21%.

So the author somewhat cynically said, well, if we’ve got to go with a minimum tax threshold, then really, when you think about it, you’re looking at the Irish tax rate. He noted that the Treasury officials in America, when they were reporting on this to Congress, started talking in terms of a minimum tax. And he saw that as pointing to that they really were thinking in terms of a lower tax rate than initially suggested. Anyway, that’s going to be a matter of debate, but progress is being made on this point. So it could be by the end of the year, some form of minimum global corporate tax rate has been set and if it is around 12.5%, don’t be too surprised.

Well, that’s it for this week. Next week is the Budget and so we will have a special on that. In the meantime, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

The Wage Subsidy, Wage Subsidy Extension, and the Resurgence Wage Subsidy schemes are all now officially closed for further applications. And as you may well be aware, these involved some significant sums of money. In total, there were more than 750,000 applications received across the three schemes together. That includes nearly 250,000 self-employed individuals. And to date, $13.9 billion has been spent on the schemes.

By the way, the Covid-19 leave support scheme is still open to affected organisations for employees required to stay at home because of the Covid-19 risk or employees who couldn’t work at home. That was at the same level of $585.80 for those working 20 or more hours per week, and was a maximum of four weeks per employee. The scheme was repeatable, so you could apply more than once. Now hopefully that scheme will no longer be required as we’ve now all down to Lockdown Level One.

Meantime, Inland Revenue has said it will be starting to audit and review those businesses that did take the wage subsidy and applied the money as they should have done. Was all the money paid through to its employees? Were any unusual employment scenarios dealt with correctly? How did they treat it for income tax? Remember, it was non-deductible to an employer but income for a self-employed person. And it was not subject to GST. Finally, was the subsidy all paid through to employees and PAYE correctly applied?

Now there are some questions emerging as to whether it was paid to employees and PAYE applied. There have been some cases where that has been found not to be the case. So we expect that Inland Revenue will be using its new tools and casting its eye over claims. Checking to see that employers – which it knows received the wage subsidy – did also pay/meet their PAYE obligations.

Inland Revenue will probably also be checking whether in fact, the applicant did suffer a 30% drop. They may feel that the GST returns, for example, might not support that there has been a drop in income. So as always, it’s a question of just staying alert and being aware that the questions will be asked. The wage subsidy schemes were high trust regime, and it appears that that trust has been rewarded in most cases. But undoubtedly there will be a few fringe persons that didn’t follow through as they should. And they should expect to hear from Inland Revenue in due course.

Now, related to the wage subsidy scheme was the Small Business Cashflow Scheme, which is still open for applications up until 31st December. And the Labour Party has promised that it will be extended for a further two years while a permanent regime is designed. The current Revenue Minister, Stuart Nash, said in a recent debate with Andrew Bayly the National Party spokesperson for Revenue and Small Business, he was very comfortable if companies or businesses had applied for the loan and then just simply parked it in a bank account. He felt that at this stage it was important to give those businesses some comfort that they had something there because we’re not through all of this yet. Who knows how businesses are going to react post-election and particularly during the Christmas slowdown. So that’s encouraging to hear.

As I’ve said before, I’m a fan of the Small Business Cashflow Scheme, and I would like to see a permanent iteration brought in. Funding for small businesses was something we considered when I was on the Small Business Council. Funds were usually very easily available if the borrower had equity elsewhere. But for small businesses that didn’t have access to a mortgage or equity, accessing debt finance was more difficult. And access to finance is something that small businesses will need as they, as always, lead the post Covid-19 recovery. So, it’s good to know that at this stage, the government is keeping that scheme going.

Aussie tax changes

Across the ditch, the Australians had their Budget this week and there were some interesting points came out of it.

The latest estimate is that the underlying cash deficit is forecast to be A$214 billion dollars (11% of GDP) for the year to June 2021, which is some A$220 billion dollars worse than the last pre Covid-19 forecast in 2019. The Australians, like all governments around the world, have thrown a lot of money at the matter. The increase in spending is four times bigger relative to Australia’s national income than it was during the global financial crisis. Spending is expected to rise by 9.5 percentage points of income in the two years to June 2021.

Net debt is forecast to reach A$900 billion (42.8% of GDP) by June 2023. Which is some $540 billion more than the pre Covid-19 forecast. But here’s the interesting thing, and this is something that Gareth Vaughan picked up this week. The forecast payments forecast for the June 2023 year on that A$900 billion dollars are A$17.3 billion dollars, whereas it paid A$19 billion interest in the June 2019 year on, much, much lower figure debt figures, only $300 billion or so. In other words, as Gareth pointed out, the cost of borrowing has dropped so much that it is now relatively insignificant.

Now, there’s a lot of interesting tax measures in the Australian budget. They’ve brought forward some tax cuts backdated from 1st July with a one-off benefit provided to low- and middle-income earners of A$1,080. They are allowing businesses with turnover of up to A$5 billion dollars to deduct the full amount of any eligible capital assets acquired since the date of the budget on 6th October which is in use or installed prior to 30th June 2022. Now is a massive investment boost which dwarfs anything I’ve ever seen before. But we’re in unprecedented times.

There’s a loss carry back regime and that again targets companies with turn over up to A$5 billion dollars. They can elect to carry back tax losses from the 2019-20, 2020-21 or 2021-22 tax years to offset previously taxed profits in the 2018-19 or later tax years. We have a similar scheme here, as you might be aware, and understand there is work going on in the background now for a permanent iteration of that loss carry back scheme.

The Australian tax regime has a number of concessions for small businesses subject to their annual turnover. And what they’ve done is increase access to those concessions by increasing the annual turnover threshold from A$10 million to A$50 million dollars.

It’s sometimes proposed that New Zealand should have a specific tax regime targeting small businesses. However, the view of Inland Revenue and Treasury, and to be frank, myself, would be that keeping it simple is a better approach. But at the same stage I think there are things that could definitely be done for micro businesses who don’t have access to all the right support and accounting. A more flexible approach to exemptions, and maybe giving some fixed deductions, would actually be a more efficient approach.

Both National and ACT look to follow the Australian model of proposing income tax cuts to help individuals and both parties propose a temporary increase in the depreciation threshold to AUD$150,000.

Why GST cuts don’t work

ACT has also proposed a 12-month temporary cut in the GST rate from 15% to 10%. Now, cutting GST rates is something that has been tried around the world. Interestingly, the Tax Working Group, when it was putting its proposals forward last year for the capital gains tax reforms, was against GST reductions.

“This is because lowering the GST rate would not be as effective at targeting low- and middle-income families as either:

welfare transfers (for low-income households), or

personal income tax changes (for low- and middle-income earners).”

And that’s the main criticism of what’s proposed by National and ACT – that the proposals don’t put money in the pocket of lower income earners who historically do spend it. That’s where I sit on this matter. I think the tax cuts as proposed are at the wrong end of the scale and should be targeting much lower income earners because they are the ones that need the money most and would spend it.

But interestingly, the rate cut in the GST has been tried overseas before. Britain tried this in December 2008 when it temporarily reduced its rate of Value Added Tax (VAT) or GST from 17.5% to 15% for 13 months. And it turned out that this had some initial effect, according to research.But at least part of the pass-through effect of a cut was reversed after only a few months.

The main issue with GST cuts is whether, in fact, the full effect of the rate cut would flow through to customers. Between 2009 and 2012, France, Finland and Sweden each reduced their VAT rate on dining in at restaurants. But in all cases, significantly less than half the tax cut was passed through to customers.

Germany is the latest to give a GST cut a go. It introduced a temporary six months rate reduction on 1st July. Now, that’s expected to cost €20 billion, but the actual boost to German GDP is estimated to be just €6.5 billion, or basically a third of the tax shortfall.

So all the research seems to point out that although in theory a GST rate cut could work to boost spending, particularly in New Zealand, where we have one of the broadest GST systems in the world, the evidence is it may only provide a temporary uptick, but that the main beneficiaries are retailers who don’t pass on all the cut.

And again, that comes back to the point I made just now, and that is if we are wanting to boost spending, then giving money to people to spend seems to be the best approach. Not indirectly through tax cuts but targeting low- and middle-income earners.

Well, that’s it for this week. I’m Terry Baucher. And you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients. Ka kite āno.