The debate over international taxation and the so-called Two Pillar proposals has been driven largely by the G20 and the Organisation for Economic Cooperation and Development, (the OECD). But in recent years the United Nations has started to flex its muscles in this space. This is unsurprising, because the UN represents the wider world view outside the 40-odd countries which make up the G20/OECD.

All of this is behind the story that RNZ ran at the start of the week about the United Nations Committee on Economic, Social and Cultural Rights statement on tax policy. The RNZ ran this statement under the banner headline “UN Report questions fairness of GST”, in which it pointed out that GST can be regressive for low-income earners.

In fact, the UN Committee statement went much further than GST. It noted the terms of reference to the United Nations Framework Convention on International Tax Cooperation, which had been adopted by the General Assembly,

“This development represents an important opportunity to create global tax governance that enables state parties to adopt fair, inclusive and effective tax systems and combat related illicit financial flows.”

“regressive and ineffective tax policies”

The key paragraph to the UN Committee statement is paragraph 4, which refers to “regressive and ineffective tax policies”, having

“…a disproportionate impact on low-income households, women, and disadvantaged groups. One such example is a tax policy that maintains low personal and corporate income taxes without adequately addressing high income inequalities. In addition, consumption taxes such as value added tax can have adverse effects on disadvantaged groups such as low-income families and single parent households, which typically spend a higher percentage of their income on everyday goods and services. In this context, the Committee has called upon States Parties to design and implement tax policies that are effective, adequate, progressive and socially just.”

It’s the reference to consumption taxes that was picked up by RNZ. The regressivity of GST is well known and was noted by the last Tax Working Group. The general approach we’ve taken here to that issue is to try and ameliorate the impact by benefits or transfer payments such as Working for Families and Accommodation Supplement to lower income families.

The thing is though, as Alan Bullôt, of Deloitte noted in the RNZ story, GST is a very effective tool for the government to raise a large amount of money relatively easy. In fact, GST represents about 25% of all tax revenue a point I repeated when I discussed the whole story on RNZ’s The Panel last Monday.

Principles of a well-designed tax system

But the Committee statement is interesting beyond the GST issue because it goes on in paragraph 6 to set out what it regards as the principles of a well-designed tax system. It suggests, for example,

“…ensuring that those with higher income and wealth, in particular those at the top of the income and wealth spectrums, are subject to a proportionate and appropriate tax burden.”

That can be clearly interpreted as a call for a capital gains tax or some form of capital taxation, a point I made to The Panel.

The Committee also fires a few shots over international tax, stating

“The Committee has observed situations in some States where low effective corporate tax rates, wasteful tax incentives, weak oversight and enforcement against illicit financial flows, tax evasion and tax avoidance, and the permitting of tax havens and financial secrecy drive a race to the bottom, depriving other States of significant resources for public services such as health, education and housing and for social security and environmental policies.”

That clearly targets tax havens, but it’s also a shot across the likes of Ireland, for example, with its low corporate tax rate.

A global minimum tax

The Committee also calls for a “global minimum tax on the profits of large multinational enterprises across all jurisdictions where they operate and to explore the possibility of taxing those enterprises as single firms based on the total global profits, with the tax then apportioned fairly among all the countries in which they undertake their activities.”

That’s quite the statement even if probably forlorn given the Trump administration’s recent declarations. It’s probably what the less developed world is after, because they’re quite concerned they’re losers under the current system. This is going to lead to wider clashes over the G20/ OECD proposal, which I think to be frank, is probably dead. In any case, I thought it was always noteworthy that Pakistan, the World’s fifth most populous country and Nigeria, the sixth most populus country and also Africa’s largest economy, both refused to sign up for Two Pillars.

Now economically, that was not highly significant because the economies are small relative to the giant economies of the developed world. However, I think this refusal points to existing issues and this statement underlines there’s global tensions ahead on this question of international tax.

As I said, the Trump administration basically is saying no go. But I think you will see countries attempting to find ways of taxing what they regard as their part of the international multinationals’ income. So, plenty ahead in this space.

Rising GST debt

Now moving on, another RNZ report picked up that there had been a substantial growth in GST debt. Allan Bullôt, of Deloitte raised a concern this could be creating zombie companies. In particular he noted the amount of GST collected but not paid to the Government, has risen from $1.9 billion in March 2023 to $2.6 billion by March 2024.

As mentioned earlier, GST represents 25% of tax revenue. It also represents just under 40% of all tax debt and has been rising sharply. That’s a reflection of the economic slowdown and the cash flow crunch that’s happening to a lot of businesses.

Even so, this is a matter where Inland Revenue has a number of resources it can deploy, and one Alan mentioned is the power to notify credit reporting agencies about tax debt. According to the Inland Revenue, it only did that three times in the year ended 20 June 2024 and not at all during the June 2023 year.

This means that people were trading and doing business with companies without realising the potential risk. What that might mean is that you provide services to a company which is struggling with GST debt, and lo and behold, you suddenly find you’ve got a bad debt on your hand.

Creating zombie companies?

This is a major issue and as Allan put it,

“That’s grown and grown. I get very nervous we’re creating zombie companies … if you’re three or four GST returns behind, it’s incredibly unlikely if you’re a retail or service business that you’ll ever come back. If you’re three of four GST payments behind, it’s incredibly unlikely that your retail or service business will ever come back.

Maybe if you’re a property developer who’s got big assets that you sell and settle your debt. But if you’re a normal business, a restaurant or something like that, you go belly up.”

This is an area where Inland Revenue has information which is not available to the general public and maybe it should be making that more widely available. There’s a question here to my mind, of what proportion of debt you would report. The Inland Revenue I think has every right to say this person owes X amount of GST, or is behind on GST, but bear in mind in some cases the debt is inflated by interest and penalties. Or in some cases there may have been estimated assessments.

Notwithstanding this Allan is right to raise concerns and I expect we will see more money being granted to Inland Revenue in this year’s Budget to chase this debt.

Meanwhile, jam tomorrow in the Australian Budget

It was the Australian budget on Tuesday night our time in which the ruling Australian Labor Party promised modest tax cuts starting in July 2026, with a further round in July 2027. Under the proposed cuts, a worker on average earnings of A$79,000 per year (about NZ$86,800) will receive A$268 in the first year and that will rise to A$536 in the second year. In addition, there will be a A$150 energy rebate payable in A$75 instalments.

Otherwise, there weren’t many other tax measures to report. That was hardly surprising because two days later, Prime Minister Anthony Albanese announced that the Federal Election would be held on 3rd May. The Budget was therefore what you might call a typical pre-election budget, promising jam tomorrow if you vote for the ALP.

One tax measure of note was that the Australian Tax Office is getting further funding for dealing with tax avoidance and tax evasion. I think that’s a pretty standard pattern we’re seeing around the world. The British had what they call their Spring Statement this week, the half yearly report by the Chancellor of the Exchequer or Finance Minister.

No new tax measures were announced. But like the ATO, HM Revenue and Customs was allocated more money to target tax evasion, with the expectation that it would achieve about a billion pounds a year in additional revenue, which seems very light given the scale of the UK economy.

Mega Marshmallows food or confectionery?

Finally, this week, a couple of years back, we discussed the Mega Marshmallows Value Added Tax (VAT) case from the United Kingdom. Basically, it involved the VAT treatment of large marshmallows. If deemed to be food they would be zero-rated for VAT purposes, but if they were confectionery, they would be standard rated which at 20% means quite a significant sum is at stake.

I will cite this and its very well-known predecessor the ‘Max Jaffa’ case involving Jaffa Cakes from the 1990s, when people make suggestions about maybe reducing the GST on food to help with the cost of living, particularly for lower-income families. It’s a well-meant policy except the practical issues you run across lead to absurdities at the margins. My view on this topic is if you want to assist people at the lower end of the income scale, it’s better give them income rather than try and fiddle with the GST system because there are unintended consequences, and this mega marshmallow case is a classic example.

The case involves unusually large marshmallows. The recommendation by the manufacturer is that they should be roasted as they’re marketed as part of the North American tradition of roasting marshmallows over an open fire. Except it’s not clear in fact, if that actually happens.

The story so far is that after HM Revenue and Customs lost in the First-Tier Tribunal, it appealed to the Upper-Tier Tribunal which basically said, “Nope, we’re not hearing it.” So HMRC appealed again to the Court of Appeal which has now issued its ruling. The Court of Appeals determined it was not absolutely clear whether in fact these marshmallows can only be eaten if they are cooked, in which case they must be food, or they can be eaten with the fingers, in which case they are confectionery.

Accordingly, the key issue is whether they are normally eaten with the fingers. This is a question of fact about which the first-tier tribunal has not made a finding. In some cases, it will be obvious from the nature of the product whether it is normally eaten with the fingers or in some other way. But that is not clear with this particular product.

The Court of Appeals therefore sent the case back to the First-Tier Tribunal to decide on this question of fact. Are these mega marshmallows mostly eaten with the fingers? If so they’re confectionery and subject to VAT at 20%. Alternatively, are they mostly cooked as supposedly intended, and therefore zero-rated food.

Time for the UK to apply VAT to food?

This case came to my attention through the UK tax thinktank Tax Policy Associates which is run by the estimable Dan Neidle, a former tax partner at the mega law firm Clifford Chance. Commenting on the Court of Appeal’s decision, he pointed out the sheer absurdity and costs involved and questioned why this was so. “Why do we have a horribly complicated set of rules that mostly benefit people on high incomes (because they spend more on food)? “

His solution – scrap zero-rating on food, in other words, adopt the approach we have here in New Zealand and tax everything. He estimates that would raise about £25 billion which could be used to reduce the standard rate of VAT from 20% to 17%.

Warming to his theme Dan thinks a better idea would be “Cut the rate to 18% and use the remaining [money] in benefit increases and tax cuts targeting those on low incomes, so they’re not out of pocket from the loss of the 0% rate.”

It’s the first time I can recall a British commentator suggest this. I doubt it will happen, but it’s just a reminder that although our GST is highly comprehensive, we don’t have these absurd but entertaining cases involving marshmallows of unusual size.

But a comprehensive GST is regressive, and I think a better approach is to address that by means of transfers to lower incomes rather than tinkering with exemptions. You never know, there may be something in this space in the Budget, we’ll find out next month.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Facebook New Zealand’s 2023 results show the scale of the advertising revenue going offshore.

Treasury’s blunt warning ahead of the Coalition Government’s December Mini-Budget.

The Australian budget was announced last Tuesday evening and although comparisons with Australia are not always constructive, there are several points of interest, not just in terms of how the tax systems operate, but also about initiatives which could replicated here.

The Treasurer is predicting a surplus for the period to June 2025, but after that, apparently things get a bit tougher. A little bit like Aotearoa-New Zealand in that regard. The key point with an election coming up, is the “Stage Three” tax cuts take effect from 1 July. As is well known and has been the subject of some commentary over time, Australia has a tax-free threshold of A$18,200. That threshold isn’t changing, but what is happening is that the tax rate for the next bracket between $18,200 and $45,000 is dropping from 19% to 16%. The big change is in the next tax bracket where the rate drops from 32.5% to 30% for income from A$45,000 all the way up to A$135,000 Australian. Quite apart from the rate change the bracket has been extended from A$120,000 to A$135,000. The 37% bracket remains in place and applies for income between A$135,000 and A$190,000. Over $190,000 the top rate of 45% kicks in.

We had record migration last year and a lot of those people are heading to Australia and no doubt these tax measures will make it more attractive. I’m in the camp that you can’t ever compete on tax cuts because there’s always someone better able to reduce tax rates further. Right now that’s Australia.

One of the interesting comments I’ve heard about the Australian budget, is that the Australian Treasury forecasts, are frequently incorrect sometimes resulting in unexpected surpluses. Apparently, the Australian Treasury consistently under-estimates forecast inflation and the iron ore price, which since Australia is such a huge minerals exporter, is quite critical. Generally, the Australian economy tends to perform better than Australian Treasury predictions.

Another strong Australian corporate tax result

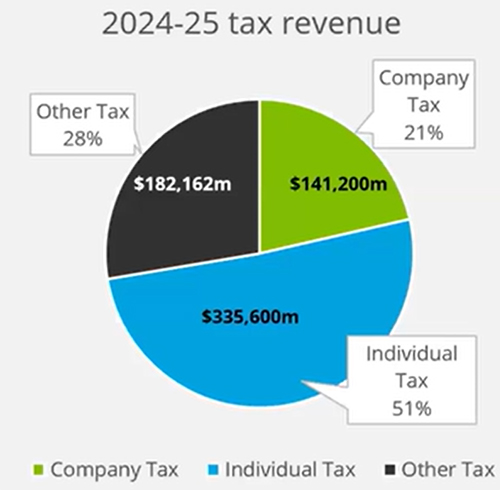

Furthermore, as the Australian economy is performing so well, the Australian company tax take is now a significant proportion of the total tax revenue. For the coming year to June 2025 it’s predicted to be A$141.2. billion or just over 21%.

(Deloitte Australia)

That’s a substantial sum by world standards. For comparison, in the UK (a near comparatively sized economy) the proportion of the tax take that comes from companies is usually between 7% and 10%. We are also a country with a fairly high corporate tax take. In the year to June 2023, it was 16.1% of total tax revenue. However, one of the reasons the Government’s books are deteriorating is the decline in the company tax take which is expected to fall to 15.6% of the total tax revenue this year.

Australian cost of living initiatives

There were also a number of other direct cost of living initiatives, including a $300 energy bill rebate to all Australian households. Eligible small businesses will get a $325 rebate during the coming year to June 2025. The Australian Government will also provide A$1.9 billion Australian over five years to increase the Commonwealth Rent Assistance maximum rates by 10%. (This would appear to be the Australian equivalent of the Accommodation Supplement).

Over here we don’t know whether the Budget in two weeks’ time will contain specific cost of living responses similar to these Australian initiatives but that appears highly unlikely. Based on what we’ve heard so far, the Government is relying on the individual tax threshold adjustments to sort of deliver cost of living relief.

Beefing up the ATO

Australia has a capital gains tax and some changes are proposed around the application of capital gains tax to non-residents. These are intended to ensure from 1 July 2025 that foreign residents are caught within the rules in relation to disposals of land. That’s something people tend to forget, that non-residents are taxable on disposals of Australian property and these proposed rules are intended to strengthen that compliance.

Another thing of note, which I think we will see something similar in our budget, is increased funding for various Australian Tax Office (the ATO) compliance programmes. The ATO has currently got three such programmes on the go, covering personal income tax, the shadow economy and tax avoidance (Tax Avoidance Taskforce). The Budget announced a new initiative countering fraud. In terms of dollar returns on these programmes, they range between four to one for the funding of the personal income tax down to a little two to one for the Tax Avoidance Taskforce.

Small businesses and ABUMS

The other thing that I think people would love to see here is the Instant Asset Write Off. This is where small businesses can purchase an asset up to $20,000 in value and claim an instant write off. This programme has been extended for another year. Apparently one of the reasons it has been extended is that the legislation which would have terminated that programme hasn’t yet been passed. Australian governments have a habit of announcing measures and then not getting around to passing the relevant legislation resulting in something with the delightful acronym ABUMS – Announced But Unacted Measures.

Overall, there was some interesting stuff in the Australian Budget including another measure I’m going to talk about next, which I also wonder whether we might see applied here.

Facebook’s results

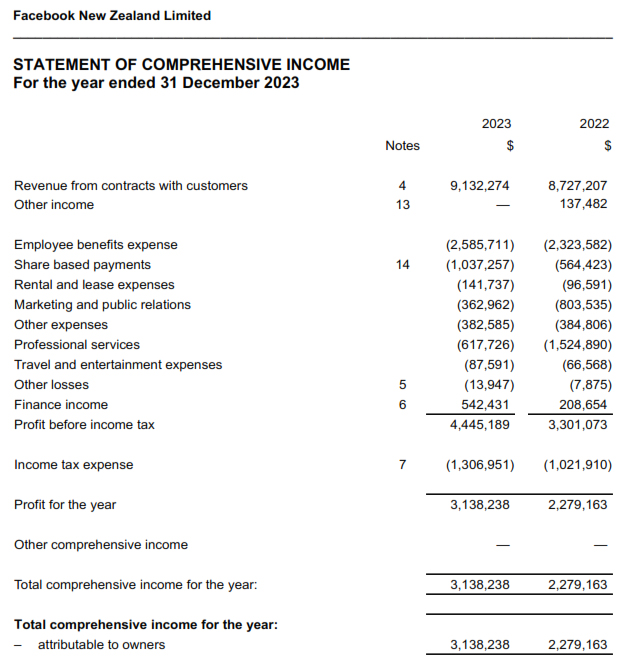

Moving on, Facebook has now released its New Zealand financial statements for the year to 31 December 2023, and these are bound to generate some controversy. The official income reported for the year was $9.1 million and the profit before tax was $4.4 million, resulting in income tax of $1.3 million.

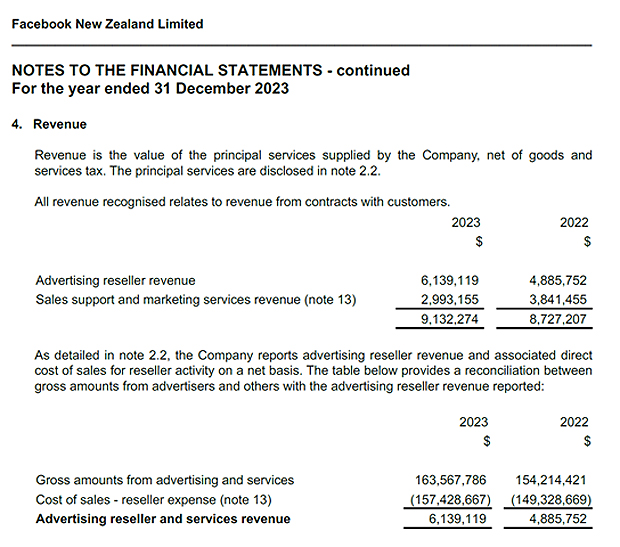

Like Google New Zealand details of the payments to related parties is the very interesting section to look at, together with the statement of cash flows because these give you a better clue of what the scale of Facebook’s activities within New Zealand are. Note 4 to the financial statements, which explains the revenue, sets out what is happening. “The company reports advertising reseller revenue and associated direct cost of sales for reseller activity on a net basis” This note explains that the gross amounts it received in the year to December 2023 from advertising and services was $163,567,786 and then a reseller expense was $157,428,667.

So, although Facebook is reporting income for income tax purposes of $9.1 million, the real scenario is that the revenue that’s passing through it, is substantially higher.

Another Australian example to follow?

Now it so happens there’s a case going through Australia at the moment involving what they call an embedded royalty. Basically the Australian Tax Office took a case against drinks company Coca-Cola in relation to what it perceived as an embedded royalty (and therefore subject to withholding tax) in payments for the right to brew Coca-Cola in Australia.

The Australian budget has a number of what’s termed Intangibles Integrity Measures. One of those it appears is a new provision, effective from 1 July 2026, where it applies a penalty to taxpayers who are part of a group with more than $1 billion in global turnover annually, that are found to have mischaracterised or undervalued royalty payments to which royalty withholding tax would otherwise fly.

Now that’s two years away from implementation, but it’s clearly a shot across the bow of companies such as Facebook or Meta, and Alphabet, the owner of Google, about these reseller services expense. So that’s something to watch how this develops.

And I just wonder whether we might see something similar here, because significant sums of money coming from advertising, are going overseas, and, as I’ve mentioned before, that has had a detrimental impact on our media landscape that it’s basically been starved of cash as a consequence. So, watch this space.

Treasury’s warning on structural reform

Finally, this week there was a budget information release from Treasury of papers relating to the Government’s mini budget in December. And one of the papers titled Implementing the fiscal strategy has attracted quite a great bit of interest.

In the paper Treasury sets out in fairly blunt terms that there is a requirement or need for structural reform of the tax system. The key paragraphs are 24,25 and 26. Paragraph 24 notes

“Structural reform of the tax system is the most effective way to ensure it is flexible and capable of raising additional revenue sustainably… Such reform would need to recognise that while revenue raising is the primary purpose of the tax system, its distributional and economic objectives are also important.”

Plenty of wry smiles here for those who listened to the Titans of Tax expand on this very point.

The problem with fiscal drag

Paragraph 25 then discusses the importance of fiscal drag

“Since 2010, fiscal drag…has played an important role in enabling successive governments to use the tax system to meet their revenue objectives. This has placed increased pressure on the tax system’s other objectives. If you wish to offset or end fiscal drag, through adjustment of personal income tax rates and thresholds the fiscal headroom which needs to be created will further increase”.

In other words, if you want to end fiscal drag, you really do need to rebalance and reshape the tax system,

I’ve seen some commentary that this was blunter advice than was provided to the previous government. I don’t actually subscribe to that view because in my view Treasury’s 2021 long-term fiscal insights briefing He Tirohanga Mokopuna was pretty clear that a fiscal crunch was coming. I just think that because there’s been a change in government, what Treasury has done here is taken the rather softly, softly approach in He Tirohanga Mokopuna and just made it very blunt so the new Government knows from the offset that there are challenges ahead. And to be fair to Finance Minister Nicola Willis and the Prime Minister, they have not denied that. But what they propose to do about it, of course, we’ll have to wait and see.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

About 10 years ago, myself and a group of other tax agents were on our way to a meeting with the then Minister of Revenue Peter Dunne. On the way someone mentioned whether we ought to raise the question of the law of unintended consequences in relation to a tax issue. Another replied that he’d never heard of such a thing law. So, we decided we shouldn’t say anything about that particular point.

We get into the meeting with Minister Dunne. And lo and behold in the course of our discussion, he brings up the law of unintended consequences, at which point we had to pause the meeting and explain to the Minister why we’d all cracked up.

(Incidentally, during that meeting, we raised a matter I discussed last week, the inequitable taxation of ACC lump sums. That was an issue which was supposed to be looked at by officials, and 10 years on, I guess they’re still looking).

The international impacts

I recalled this because last week I also talked about the Greensill decision in Australia, and the implications for trustees of New Zealand trusts. And on Monday, I got a new enquiry from a client where the impact of Greensill could come into play and it’s a classic example of the law of unintended consequences.

A mother had decided that she wanted all three of her children to be trustees of the family trust, and this change was made for good reasons in managing a family dynamic. Problem is, one of those children lives in Australia. As I mentioned last week under Australian tax law, if any trustee of a trust is tax resident in Australia, the trust is deemed resident in Australia. That means the Greensill decision may apply, which basically says capital gains even if realised offshore and even if distributed to a non-resident, are subject to Australian tax at the top rate of 47%.

The implications are therefore potentially quite serious for this trust. Looking into it in more detail, the trust is deemed resident from the first day a trustee is a tax resident of Australia. The trustees will have to prepare and file Australian tax returns reporting the trust’s income as calculated for Australian tax purposes.

Now, in many cases, the trusts will distribute income to beneficiaries and from an Australian perspective, if non-Australian sourced income is distributed to a non-resident, it’s not an issue. It’s just that in the law there is a technical inconsistency, which means that the Australian resident trustees are liable for Australian tax on non-Australian sourced capital gains distributed to non-residents.

This is the impact of the Greensill decision which to recap involved a capital gain of A$58 million and was held to be taxable at 47%. What’s more, with Australian trusts, the rate for retained income is 47%, and this is further complicated by rules about which beneficiaries have what is termed “present entitlement” as at the date of balance date. So overall, this is potentially quite a serious issue if substantial capital gains been raised.

Now the logical response, you’d think is, “Aha, let’s get the trustee to resign” and once the trustee resigns, that ends the connection with Australia. A logical move, except the Australian tax legislation has thought of that point. And what happens then is there’s a deemed disposal of the trust’s assets on the date of the resignation of the trustee (This is a feature of some jurisdictions with a capital gains tax). In other words the Australian Tax Office, believes in Blondie’s maxim, “One way or another we’re going to get you”.

We are currently working through all these issues. This is a textbook case of whenever there’s a family trust and there is family overseas if you want one of the family to become a trustee, you have to put a big pause on that and get tax advice, particularly in relation to Australian residents.

I’ve seen some trustees who are living in the UK pop up on trusts. This is not quite as potentially catastrophic but it’s still problematic. There’s this dichotomy between New Zealand’s tax treatment, which based around the settlor and many other jurisdictions, which is based around the residence of the trustee. So, to repeat the key point, if you have any trustees that are tax resident overseas, you need to get tax advice.

Helping your children

Moving on, the second instance of unintended consequences this week involves family members such as parents, grandparents or trusts trying to help children or beneficiaries purchase property, the bank of Mum and Dad as it’s sometimes called. This has become incredibly more relevant as a by-product of the horrendous escalation in housing prices.

The issue that has to be watched out for is when the parents or whichever other entity is involved, a trust, for example, actually takes a direct ownership interest in the property to be acquired. At that point, whoever it is, is probably setting themselves up for some issues further down the track in relation to the bright-line test.

And these of course have been magnified by the fact that the bright-line test as of 27th March this year now runs for 10 years. These issues were probably manageable when the two-year bright-line test was initially introduced back in October 2015 but have now been considerably magnified with the extension of the bright-line test period to 10 years.

What is emerging in some cases is that families might say, right, well, “We’ll take a 25% interest in the property. And then as the equity and your income rises you can pay us back and gradually take over our interest”. So ultimately, the children or beneficiaries will own 100% of the property. The problem is the reduction in those minority interests in the property represent a disposal for income tax purposes and for the purposes of the bright-line test.

For example, let’s say parents co-owned a house with a child and the ownership structure was initially 50:50 between them, but change it to 75:25. In that case, there’s been change in the title in the ownership interest, and therefore there’s been a disposal by the parents of a 25% interest to their child. Therefore, this disposal would be subject to bright-line test. There would be no exemptions here because they’re not living in it and it’s not their main residence. Just bear in mind that even if that property was the main residence of the child, the parents having the interest would still have made a disposal for bright-line purposes.

There’s also a potential kicker for such a transaction if the property is sold or gifted below its market value within the bright-line period, the transaction is treated as having happened at market value. So, for example, if the market value of the property had increased from $500,000 to $1 million, then the parents reducing their interest would be taxed on whatever their share of that $1 million was, rather than what actual cash they might have received. So potentially there could be some very sticky tax bills arising.

Arguably, one potential way round this might be that the parents lend the money to the child and not take a direct ownership interest, but you know, horses for courses, individual circumstances will come into play.

So, you just have to be very careful and proceed with great care if you are taking a financial interest in your child’s property to help them on the ladder. Otherwise, it could be another example of unintended tax consequences.

Lessening inequality

And the third unintended consequences that we might see in tax relates to the recent announcements from the government about changes to working for families.

What the Government has done has announced increases to the amount payable. The family tax credit is going to be increased by $5 per child. And on average, families will be $20 a week better off. But, and there’s always a ‘but’ in this, what the Government has given with one hand it has quietly decided to take on the other by raising the abatement rate to 27%.

Now abatement is what happens when a family’s annual income exceeds $42,700 then working for families credits start to be abated. And what this means is that people on average incomes actually have the highest effective marginal tax rates in the country.

For example, a family earning $48,000, the point at which the tax rate moves from 17.5% to 30%, their effective marginal tax rate, once you add in the impact of abatement is 57%. In other words, for every dollar of extra income they earn, they will lose 30% in tax and 27% of their working for families tax credits

For family’s with income just over $70,000, the marginal tax rate rise to 60%. And if you’ve got a student loan, that’s another 12% on top of that. A person earning just above $48,000 with a student loan could be facing an effective marginal tax rate of 69%. This is the unintended consequences of the abatement rates. The theory is conceptually sound, but the problem is it traps people on low income and makes it very hard for them to break out of the need to receive social assistance.

This is one of these things that is consistently glossed over by politicians and has been one of those sneaky little tax increases that that previous finance minister Bill English did. Grant Robertson is just the latest to increase the abatement rate and so quietly claw back some of the assistance. The unintended consequence is that the step up makes it harder to get out of poverty.

There is meant to be a review of working for families going on at the moment, but that’s been paused. As we know, the Welfare Expert Advisory Group recommended significant increases in benefits and that report is now nearly over two years old.

To summarise this week’s lesson, tax is full of unintended consequences. Therefore, always proceed with caution if you’re making significant changes, such as appointing a trustee or wanting to co-invest with your children on a property purchase.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website, www.baucher.tax or wherever you get your podcasts. Thank you for listening, and please send me your feedback and tell your friends and clients. Until next week, party week, have a great week and go the Black Caps.

This week we focus on trusts, in particular new reporting requirements for trusts which have caused a stir together with a concerning court decision from Australia. Elsewhere, there is a harsh but not unexpected decision from the Taxation Review Authority regarding the taxation of arrears of weekly ACC compensation.

Last month, Inland Revenue released two papers relating to trusts, firstly, an issues paper on the reporting requirements for domestic trusts where disclosure is required under the Tax Administration Act 1994, and secondly, a detailed operational statement setting out the reporting requirements for domestic trusts.

Now, these prompted an article by Auckland barrister Anthony Grant, who specialises in trusts and estates. He was quite concerned about the papers and why this information was being gathered. His article concluded;

“The information can be wanted only because the IRD and the present government want to tax people who lend money to trusts at less than market rates, people who get benefits from trusts, people who provide services to trust assets and people who have powers in relation to trusts, as they have never been taxed before.”

That’s quite a quite a closing statement.

The source of the two Inland Revenue papers is legislation enacted when the Government increased the individual tax rate to 39%. The Government did not also increase the trustee tax rate, even though Inland Revenue recommendation was that it should, based on bitter experience of what happened between 2000 and 2010 when such a differential existed previously.

Instead, the Government made very clear statements that it would be watching the situation carefully, and if it did see what it regarded as unacceptable tax avoidance happening, it would move to increase the trust tax rate. In the meantime, it introduced a whole new set of disclosure rules to enable Inland Revenue to have a clear look at what transactions are going on involving trusts.

Now, this was a radical departure of from previous practise. One of the weaknesses of tax administration in New Zealand, in my view, is that we don’t get to see a lot of detailed or very segmented tax statistics. If you go elsewhere in the world, tax authorities can produce very voluminous data relating to which sectors and persons are paying tax. Inland Revenue doesn’t produce those sorts of data, although if you ask for it under the Official Information Act, you should be able to obtain much of what you’re after.

That lack of tax data being made public reflects the moves made in the 1990s to ease tax administration under which most people were no longer required to file tax returns and the information to be included in most tax returns is quite limited.

The new legislation requires quite substantial amounts of information to be provided. It includes details of all settlements on a trust, which includes all transfers of value along with details identifying the entities or individuals making those settlements. Transfers of value include all things monetary and non-monetary and the provision of services below market value. Details of all distributions, whether taxable or not, are required and including again, monetary or non-monetary together with details identifying recipients. There’s a general question wanting information about details of who has the power to appoint or dismiss a trustee, add or remove a beneficiary or amend a trusted name and finally a catch all or any other information the Commissioner of Inland Revenue wishes.

This represents a large increase in compliance for trusts. It should be said that it also reflects to some extent the impact of the new Trusts Act. Trustees can now expect to have more reporting requirements because beneficiaries now have rights of access to information about the trusts.

Trustees who may previously have been a little casual, to put it mildly, about record keeping will now need to sharpen their game. Not just for tax purposes, but basically to comply with the new Trusts Act. We don’t actually know how many trusts there are in New Zealand, the best estimates are somewhere between 500 and 600,000, and it’s one of those stats where per capita New Zealand is right up there.

The Government reporting requirements come into effect with those tax returns that have to be filed for the current year ending 31 March 2022. However, the legislation contains a provision that if Inland Revenue reviews a return and finds something of concern, it can request the same information for the previous eight income years, which means the first year could be for the year ended 31st March 2015.

As noted, the legislation represents a substantial increase in compliance costs. You should also look at it in the context of the controversial high wealth individual research project, which is going on at the moment. Both these initiatives address an area where arguably New Zealand taxpayers have not been providing a lot of information, and hence the Government and Inland Revenue are in the dark as to exactly the extent of wealth in the country.

And by the way, this is a worldwide trend. Although New Zealand managed to come through the global financial crisis very well, which has enabled us to manage the COVID 19 response pretty well, for the rest of the world the double whammy of the Global Financial Crisis and now the pandemic means that governments are under enormous fiscal pressure. There’s a growing trend to request further information in relation to the wealthy and wealth taxes are being discussed elsewhere around the world. So this is actually part of a global trend here.

But that’s not to undermine the importance of the issues raised here. These represent significant compliance costs, and they are quite concerning for trustees and beneficiaries about what were apparently quite legal transactions, such as advances to beneficiaries. Details of loan advances to beneficiaries are now required together with distribution of what we call term trustee income, which is tax paid income. This is going to be particularly relevant going forward because trustee income is exempt income for a New Zealand tax resident. Therefore, for someone who’s taxed at the 39% top rate, a distribution of trustee income is a way to essentially get tax free capital distributions from a trust. And this is what one of the areas these new provisions are looking to target.

The level of detail asked in relation to beneficiaries and what is expected of trustees is incredibly high. The new rules are expected to affect about 180,000 trusts, although there’s a sort of a de minimis position for trusts which don’t have annual income exceeding $30,000 and the total value of the assets is less than $2 million. That still leaves a substantial number of trusts will required to prepare quite detailed information for submission.

For example, all interest and non-interest-bearing loans from persons associated with the trust that is the settlors, trustees and beneficiaries. Then if trust property such as a house is enjoyed by a beneficiary for less than market value, the sum is to be recorded as a drawing in favour of the beneficiary. This one in particular is going to cause a bit of a stir as it’s quite a bold step. For many trusts, properties held by the trustees are essentially let rent free to the beneficiary on the basis that the beneficiary meets the upkeep, such as rates, maintenance etc, and the interest payments relating to any mortgage over the property.

Now we see a deemed income provision in relation to assets provided by a company, but there’s no such provision for trust purposes. These particular requirements are one reason why Antony Grant sounded the alarm. It would essentially impose a deemed rental or an imputed rental on property. This is something which has been considered by several tax working groups, but not implemented by the Government.

Another matter which is going to be a headache for trustees and initially probably may not be entirely accurate, is the requirement to break down the equity of the trust between the corpus, which is the sum of all settlements that have been made on the trust less the distribution of corpus made to beneficiaries and trust capital, which is the sum of all taxable and non-taxable income retained and gains and losses made by the trust.

There’s also to be an equity item in relation to drawings, which effectively mean the total amount of assets of value withdrawn from the trust by beneficiaries during the year, and then beneficiary current accounts are to be shown. Some of these well-managed trusts will already be doing so, but the extension across the board to most trusts is going to cause increased compliance costs as I’ve said. The implications of what happens when the Inland Revenue digests all this information we’ll have to wait and see.

Now, the officials’ issue paper is open for submissions until 15th November, and submissions on the operational statement are open until 30th November. So you might want to have a quick look at these papers and then consider making submissions.

Moving on, trusts with overseas trustees, beneficiaries or settlors can cause quite a lot of confusion. It’s something I’m seeing increasingly, particularly in relation to Australia, where the latest estimate is that maybe between four and five hundred thousand Kiwis live at the moment. And one of the issues that happens is that the trust taxation law differs from country to country. But (and I see this quite a bit in relation to various jurisdictions) people mistakenly assume that the rules are similar and don’t pay attention to the fine detail.

Now, in relation to trusts and people moving to Australia, it’s been well known for some time that if there’s any trustee resident in Australia, then the trust is deemed to be resident in Australia and therefore subject to Australian tax rules. And so steps are taken to ensure that no trustees move there or resign their trusteeships before doing so. But that doesn’t always happen, and a case has just popped up in Australia, which although it involved a UK tax resident person it would have implications for New Zealanders.

Now, typically, distributions through a discretionary trust of current year income or capital gains are generally considered to retain those characteristics in the hands of the beneficiary. What that means for New Zealanders resident in Australian who qualify for the temporary resident’s tax exemption is if they get a distribution of foreign sourced income, that is income from outside Australia, it’s generally exempt from Australian tax. But a new decision from Australia, Greensill, makes it clear that this treatment doesn’t necessarily apply to capital gains.

Now, in this case, what happened was the trust realised A$58 million on a capital gain from the sale of a UK management company. The gains were distributed to a beneficiary living in the UK and therefore non-resident for tax purposes in Australia. The shares that were disposed of did not represent taxable Australian property for capital gains purposes.

Ordinarily, a capital gain on non-taxable Australian property made by non-residents is disregarded for Australian tax purposes. But the full Federal Court of Australia ruled that in this case, because it was distributed to a non-resident beneficiary of a discretionary trust, there was no exemption available because of the way that the legislation was drafted in relation to how trusts deal with capital gains. Therefore, the Australian trustee was required to pay income tax on behalf of the non-resident beneficiary in respect of that $58 million capital gain.

And this is where we could have problems in New Zealand. For example, a New Zealand domestic trust with three trustees, two of whom are in New Zealand, and one is in Australia. The trust is deemed an Australian tax resident and if the trust tries to distribute the capital gain, such as the realisation of the sale of a property in New Zealand then following the Greensill decision, Australian capital gains tax is payable, and it would be at 45%. So this is a major decision.

People therefore need to be very careful to be check as to the status of the trustees and settlors of the trust. Basically, what you want to try and do is minimise any link between an Australian resident and a New Zealand trust. Otherwise, you’d be looking at a substantial capital gains bill.

What wasn’t apparently argued in court was the question of whether double tax relief would be available under the double tax agreement between Australia and the UK. This is unusual because I would have thought it would have been an issue that could have been applied in the Greensill decision, but apparently it wasn’t argued.

So we may have to wait either for another tax case or for perhaps the Australian Tax Office to decide that the Greensill decision is not really what they want and change the law. I think we might be waiting a long time for that.

Now moving on from trusts, the Taxation Review Authority (TRA) has confirmed that a taxpayer who received arrears of weekly compensation from Accident Compensation Corporation relating to an injury three years earlier was correctly taxed in the year in which she received payments. This is something that pops up quite regularly and I’ve discussed it previously.

In this case, the person was injured, made a claim for weekly compensation, and for three years there was a back and forth arguing about it. And eventually ACC paid a significant lump sum of arrears total of just over $180,000. This payment was subject to pay as you earn as income in the year of receipt. The taxpayer quite reasonably objected on the basis that her regular level of earnings was always quite low. Therefore, the tax that would have been payable if she had received the payments when she was entitled to do so would have been lower.

However, the law makes no adjustment for this, and it was taxed as a lump sum at higher rates. She took her case to the to the TRA, which kicked it out on the basis the legislation provides no scope for relief. Now, this is a not uncommon problem. In fact, I wrote to ACC and asked, just how often does this happen, where arrears of ACC are paid in a subsequent income year?

And the data I got back in April said that in the year ended 30 June 2020, there were 14 166 such payments. And in each of the years ended 30 June 2017, 2018 and 2019 there were at least 1100 such cases. The average payment was around between $42,000 and $49,000 with the median pay-out around $21,000. But some very large payments were made. There’s one in the year ended 31 June 2020 of over $1.1 million.

So this is quite a significant issue which I think is something that should be amended by legislation. It seems unfair for someone who’s been injured or entitled to relief but doesn’t get it when it should happen and then has to take action to get their entitlements with more added stresses. Finally, when a person does get paid, Inland Revenue comes in and takes a big cut of it. And by the way, this is going to be a bigger problem now that we have a 39% tax rate. So, I’ve made a submission to Parliament’s Finance and Expenditure Committee on this, requesting the issue be looked at and the legislation changed.

Speaking of submissions, a reminder that submissions to the Finance and Expenditure Committee regarding the Government’s interest limitation proposals close next Tuesday, 9th November. So you’ve got until then to make submissions on that. I expect there will be quite a few submissions on the new rules. But as part of those submissions, you can actually draw the committee’s attention to other matters, which is what I am doing in relation to the ACC matter.

Well, that’s it for this week. I’m Terry Baucher and can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week kia pai te wiki, have a great week!

Inland Revenue has released five COVID-19 related variation determinations including ones covering look-through companies, bad debt write-offs and tax pooling

The tax problem of appointing an Australian resident executor

A temporary increase to the write-off threshold for tax to pay

This week, a roundup of several useful COVID-19 related variation Determinations released by Inland Revenue, a reminder to be careful about who you choose to be an executor of your will, and a temporary increase in the write off threshold for tax to pay for PAYE earners.

As part of the response to the COVID-19 pandemic, a specific discretion was introduced into the Tax Administration Act to make clear Inland Revenue’s ability to issue variations to requirements under the various Inland Revenue Acts. Basically, the conclusion was that Inland Revenue needed more discretion to be able to extend the filing date, due dates for tax returns and various other filing requirements.

This was part of one of the first earliest pieces of legislation enacted in April. Following that, Inland Revenue has now used this discretion to issue five Variation, Determinations, setting out the requirements for when it would apply its discretion in certain situations.

The first one deals with a variation to extend the time to file a look-through company election. Now normally, that must be done by the start of the relevant income tax year i.e. 31st March. This variation now extends the deadline to June 30th 2020, which is a welcome little addition.

Look-through companies are tricky elections at times. I’ve been involved in several cases where elections have gone missing or somehow weren’t filed at the right time. And that ends up with a lot of finger pointing everywhere. So under the added stress of a COVID-19 pandemic, this added flexibility from Inland Revenue is good to see.

Another variation varies the time to make an election, to spread back forestry income, and a third extends the time to make an application to change the GST taxable period. For example, you might want to switch to filing monthly GST returns from previously filing six-monthly or bi-monthly GST returns.

But the next two variations are probably of most relevance in these interesting times. The first one is variation COV 20/04, which extends the time for writing off bad debts. Now, basically under Section DBI 31 of the Income Tax Act, a debt must be written off as bad in that income year. So normally for the year ended 31st March 2020, if you’ve got a bad debt, you must have written it off by 31st March 2020. What this determination does is extend that write off period to 30th June. It’s a useful concession, although as always, there’s a couple of caveats here.

Firstly, that the person did not write the debt off by 31st March 2020 because of the COVID-19 impact. In other words, the disruption to their processes meant they weren’t able to process bad debt write offs as they would normally have done so. And the second one is one I think is going to cause a few headaches, because it gets down to significant interpretation. In writing off the debt, the person can only take into account information that was relevant as at the end of the 2020 income year. I’m not sure exactly what was meant by “relevant” here? You might be aware that a business was struggling but hadn’t decided to take action. Would that count? We don’t know. I suspect this is one of those caveats that’s been put in more as a protection. But we could see in a few years a significant tax case on the issue.

And the final variation, which is going to be helpful, is one that extends the time for using tax pooling transfers. Now, regular listeners will recall that I had a podcast session with Chris Cunniffe of Tax Management New Zealand late last year. Using tax pooling companies like TMNZ extends the time through which you can make payments of provisional and terminal tax, yet be deemed to have made the payment on time. So they’re a very useful mechanism for managing cash flow and minimising the impact of use of money interest.

Now, what this determination does is it extends the time for which a person can put in place a contract with a tax pooling company in order to meet the tax due for the 2019 tax year. And that time would normally have expired by now. But this variation gives an extension until July 21st 2020.

The caveat in this instance is that between January 2020 and July 2020, the business must have experienced, or for June and July 2020, be expected to experience a significant decline in actual predicted revenue. As a result, they were either unable to satisfy their existing contract for 2019 tax or they weren’t able to set up/enter into a tax pooling arrangement with a tax pooling company.

The “significant decline” in actual revenue has got to be at least 30% and must be COVID-19 related. So that last criteria is a little bit vague because it doesn’t address a position where the company was struggling to make the payment before COVID-19 turned up anyway.

The variation gives an extra month until July 21st to put a contract in place to make a tax pooling payment. And the advantages of using tax pooling are saving use of money interest and late payment penalties because the tax is deemed to have been paid when it was due. And the rate of use of money interest charged by tax pooling companies is lower than that charged by Inland Revenue.

Instalment arrangements and use of money interest

The rate of use of money interest popped up in a story on Thursday. It talked about the arrangements Inland Revenue is putting in place with taxpayers who have been struggling to meet their liabilities. And some of the taxpayers putting arrangements in place have also experienced the impact of use of money interest and late payment penalties.

Interestingly, Inland Revenue is waiving much of these interest and penalties if the delay is down to COVID-19. But again, as a caveat, only if it’s down to COVID-19. I think at some stage we may find is a hardening in the approach of Inland Revenue here.

But anyway, the numbers of taxpayers who have entered into what we call instalment arrangements with Inland Revenue rose from 16,445 in April to 26,073 in May. And on average, the debt under arrangement was just under $18,000. So that’s nearly $800 million going under arrangement. We’re going see more of this, as I’ve said this previously.

Now Inland Revenue has lowered its use of money interest rate to 7% but it’s significantly higher than the 0.25% Official Cash Rate. I suggested in the article that it was well past the time late payment penalties were abolished. These apply in addition to use of money interest and add another 1% immediately, then a further 4% if it’s not paid within seven days, and then continue at a further 1% per month thereafter. There’s no evidence late payment penalties encourage any prompter payment when compared to other jurisdictions that don’t have them.

Currently about 87% of taxes are paid on time under the current regime. There’s little evidence late payment penalties make any discernable difference to prompter payment. They just cause resentment and a 7% use of money interest rate is a very substantial deterrent in these low interest times. We’ll see when things settle down a bit if there’s finally some movement made in this area.

Beware your choice of executor

Moving on, one thing about tax that keeps me busy is the accidental tax impacts of sometimes quite apparently innocuous decisions. And one such example that I’ve come across recently is appointing an executor who is resident in Australia.

This seems fairly straightforward. You may have a parent here in New Zealand with three children, one of whom lives in Australia and the other two here. Under the will the parent appoints all three as executors. This is not an uncommon scenario.

Problem is that the Australians view a trust as being tax resident in Australia if any trustee is resident in Australia. And as I discovered recently, this also applies to personal representatives or executors of the states. You have a deceased estate of a person who died here in New Zealand. All the assets are here in New Zealand. But in the scenario I outlined earlier, one of the children who is an executor lives in Australia. This is currently sufficient for the Australians to consider the estate to be an Australian estate and therefore taxable. How exactly that is enforced is not clear, but this position is a very real risk.

So, here’s a reminder for people who may be considering wills in these uncertain times. Just be sure to cover off the tax consequences if it so happens you have someone such as a child you want to either appoint as an executor or make a beneficiary, who is living overseas.

Increase in tax write-off threshold

And finally, back to a COVID-19 related matter. The Government has temporarily increased the write off limit for unpaid tax for people on PAYE from $50 to $200. Right now, Inland Revenue is going through approximately two million people who are on PAYE and doing the automatic calculation of their liabilities for the year ended 31 March 2020.

The general rule was if they owed $50 or less, it would be written off. But above that amount, they’d have to pay. And what’s happened is they’ve decided as an interim measure to help people through this pandemic is to immediately increase the $50 threshold to $200. It only will apply for the year ended 31 March 2020.

This is only available for individuals whose year-end tax liability is calculated automatically. If you are required to file a tax return, because, for example, you’ve got a rental property, you’re not covered by this change.

And by the way, just on the automatic calculation there’s an interesting thing to note here that any amount of tax to pay for someone who is paid fortnightly and had twenty seven fortnightly pay periods during the year ended 31 March 2020 is automatically written off. (The same applies to anyone paid weekly who had 53 pay periods in the year, or someone paid four weekly who had 14 pay periods).

Well, that’s it for this week. Thank you for listening I’m Terry Baucher, and you can find this podcast on www.baucher.tax or wherever you get your podcasts. Please send me your feedback and tell your friends and clients. And until next time, Kia Kaha stay strong.