Tax continues to feature heavily in the Election with the ongoing debate over the validity or otherwise of National’s proposed foreign buyer tax. But away from the election, it has been a busy week in the tax world. By far the most interesting story, partly because of its source, but also how it speaks to the structure of our tax system, is the commentary from Matt Whineray, the outgoing chief executive of the New Zealand Superannuation Fund (NZSF), about the fund’s tax status.

In an interview with the New Zealand Herald’s Markets with Madison, he remarked on the NZSF’s tax status, noting that since the fund began investing in 2003, it had paid nearly $10 billion in tax, including $2.2 billion for the year to June 2022.

This makes it by far and away the largest single taxpayer in the country. He thought this was rather nonsensical and that the fund really should have tax immunity status in line with many other sovereign wealth funds around the world, (including ACC and the Reserve Bank of New Zealand, both quite substantial investment funds). “My wish would be that we didn’t pay tax because I think that would solve a few issues.”

A nonsensical money-go-round?

He questioned the practice of the NZSF returning money to the Crown in tax, and the Crown in return contributes to the fund annually. “If I take my wallet out of this pocket and put it into this pocket, I haven’t got richer.” The problem, in his view, was exacerbated when the Crown stopped contributing to the fund completely, as it did for almost a decade between 2009 and 2017.

It’s interesting to hear such commentary from Matt Whineray, which highlights an anomaly about the NZSF, in that it is a sovereign wealth fund, but it pays tax, which is highly unusual around the world. In fact, I’m not sure there are any other sovereign wealth funds which do pay tax. (It’s an issue Whineray’s predecessor Adrian Orr also raised, ashas Whineray previously).

Now when the NZSF was set up 20 years ago, the rationale behind it paying tax was this would help it make sound investment decisions based on investment principles and not by tax considerations. And in a broader sense, that’s not unreasonable. I always tell my clients, don’t let the tax tail wag the investment dog. Think in the longer-term investment and returns rather than the short, potentially shorter-term tax implications.

A “Fair” Dividend Rate?

Someone else this week commenting on this question of the tax status of savings was financial planner Rachelle Blanch speaking to Susan Edmonds of Stuff.

Rachelle thought it was time for a review of the Foreign Investment Fund (FIF) regime, particularly in relation to how it applies to portfolio investment entities such as KiwiSaver funds. Now, the FIF regime and the Financial Arrangement regime are the two main reasons the NZSF pays so much tax. That’s because both regimes tax unrealised gains and there will be substantial unrealised gains in investment funds.

As the story in Stuff noted, under the FIF regime KiwiSaver funds and the NZSF must use what’s called the fair dividend rate in respect of their overseas shareholdings. This deems 5% of the opening market value of the investments held at the start of the tax year to be taxable income. Now obviously as KiwiSaver funds grow in size, and they diversify out of the New Zealand market as the NZSF has done, then the amount of tax payable as a consequence of the FIF regime will increase. However, unlike individuals or trusts, who can switch methods to mitigate the impact of a drop in values of some of investment funds by adopting what we call the comparative value method, KiwiSaver funds and the NZSF can’t do that.

How much tax is payable under the FIF regime is not at all clear. The NZSF is probably the only entity which can give a pretty accurate gauge on that. But to give you some idea of the total tax that might be payable – the Financial Markets Authority produces an annual report each year on KiwiSaver funds, and it notes that for the year to June 2022, KiwiSaver funds paid over $256 million in tax for that year. Remember in the same period, the NZSF paid over $2.2 billion.

Rachelle Bland has raised a very good question as to whether, in fact, this is an appropriate tax policy response where people have long term savings. She describes it as effectively a capital gains tax. Another way of looking at this, and it’s how I describe it whenever explaining the regime to overseas clients, is that it operates as a quasi-wealth tax.

As I said, there’s no mitigation for significant falls in stock markets. Unlike a capital gains tax regime which taxes on a realisation basis you can decide to realise capital losses and offset them against capital gains. You can’t do that under a FIF regime. Therefore you have this situation where the value of investments are falling but you’re still paying tax on the value of those investments. And that’s been the scenario for quite a few funds over the past 12 to 18 months.

What about a tax exemption then?

It’s not surprising then that quite apart from this anomalous washing – as Matt Whineray referred to the process of cycling funds from the Crown to the NZSF and then back in the form of tax – there’s also calls for some form of tax exemptions for KiwiSaver funds. You see such tax exemptions around the world for other pension schemes. New Zealand is yet again, a bit of an outlier here. The reason such exemptions were taken away in the late 1980s is they are costly. However, in overseas jurisdictions where tax exemptions apply to pension schemes withdrawals are taxed, whereas in our system we apply what we call a tax-tax-exempt approach where the contributions are made out of after-tax income, the schemes are subject to the ordinary taxation rules, but any withdrawals are exempt.

What’s the most effective approach? Well, that’s still a matter for debate. But one thing to keep in mind is that tax does have an impact on the long-term return of funds. Now, whether anyone is going to do anything about this is very questionable. The FIF regime in its current iteration has been in place now since 1st April 2007, and it generally works pretty well. The rules were very controversial when they were first proposed. There was an absolute storm of protest when they were first proposed, with Parliament’s Finance and Expenditure select committee receiving 3,400 submissions against the introduction of what is now the FIF regime, and only two in favour. In the face of this criticism, they were actually reshaped and now everyone has got used to working with the regime.

And this perhaps is the critical point. Governments appreciate the tax paid by the NZSF and KiwiSaver funds. The total tax for the year ended 30th June 2022 from those two sources probably represents just about 2% of the total tax take for that year. Therefore, changing the tax treatment for the NZSF and for KiwiSaver Funds would be an expensive move even if as a trade-off the Government might not then need to make any more contributions to the NZSF.

Wrong sort of investment signals?

Given the short-term pressures at the moment on the Government’s books, I think any move in this area is not going to happen. But I also consider it underlines a scenario where we’re prepared to tax savings under the current tax system, but generally whole asset classes, such as property, the bright line test excepted, are outside the tax net. This treatment sends an investment signal which politicians aren’t prepared to address.

Where does investment get directed? The evidence we have points to it being directed into relatively unproductive residential property investment as opposed to the likes of KiwiSaver funds, which will invest in productive businesses.

The discussion we’re not having

Now, this is a discussion we’re not having at the moment about how the tax system and investment interacts. As I’ve said in previous podcasts when you consider National is proposing removing commercial property depreciation on non-residential property again, (as is Labour for its part) in both cases to fund some form of tax cuts this to me sends the wrong signals. We’re basically directing funds away from investment in our economy into consumption.

But this is not a discussion we’re going to have because although politicians quietly recognise that whatever we the electorate might say about the impact of tax in the back pockets – and we’ll happily all take tax relief, tax cuts, how you phrase them – we also like the services tax provides. So, this dichotomy exists. We’ve got to maintain services as far as possible but not want to pay for them. But as I’ve said repeatedly, I think the under taxation of capital is an unsustainable position long term.

Donations tax credit review announced

Moving on, Inland Revenue just carries on carrying on regardless of whether the Government is out campaigning. It has been busy churning out quite a lot of interesting material. But two particular initiatives happened this week.

Firstly, on Friday, it announced it is going to undertake a review of the rules relating to the donations rebate rule. This review is part of the Regulatory Stewardship programme required of all state agencies in respect of the rules they administer. In this case, a review is going to assess whether the donations tax credit regime is operating effectively, is achieving its policy intent, and how it compares internationally.

Inland Revenue will open up consultation with an aim of undertaking this review and completing a report, setting out its findings as well as any recommendations by mid-2024. Interested parties will be contacted on this. I imagine you can expect the Charities Commission, some more major charities, would be approached. I think the main accounting bodies, together with the New Zealand Law Society will also be approached for comment on the matter.

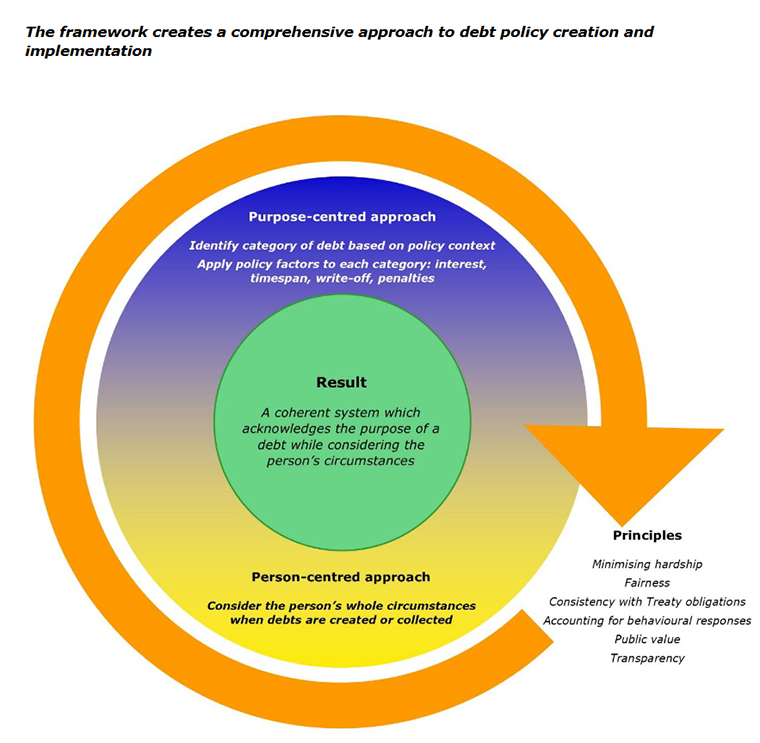

A fairer Government debt policy framework?

The second Inland Revenue initiative and probably something that’s going to have more immediate impact ties into the rather strange case we talked about last week involving the Nelson woman who got herself into a whole heap of trouble with Inland Revenue and decided the best way out of avoiding a $365,000 tax debt was to sell her property worth $845,000 to a UK company. The Official Assignee took a dim view of the idea and obtained a court order striking the sale down.

Leaving aside the oddities involved the case is relevant for the important question of tax debt and other debt that’s owed to the Government. According to the New Zealand Herald story reported last week, as of 30th June 2023 Inland Revenue is owed nearly $5 billion.

Now, both the Tax Working Group and the Welfare Expert Advisory Group took a look at the question of debt owed to the Government as part of their reviews, and they recommended there should be some form of all of government approach to debt. Firstly trying to prevent debt arising with the Government, but also how each relevant government agency responds and manages that issue.

Consequently, a policy framework for debts the Government is owed has now been developed and has been signed off by the Cabinet. Inland Revenue this week released its report and background details on this framework.

There’s quite a bit to consider in here, not just the $5 billion Inland Revenue is owed but the other debts built up, primarily with the Ministry of Social Development and also with the Ministry of Justice.

According to this report, at present 762,460 New Zealand residents collectively owe $4.68 billion of debt to these three agencies – Ministry of Social Development, Inland Revenue and the Ministry of Justice. More than a quarter of these persons owe debt to two or more agencies and 6% that’s over 45,000 people owe a debt to all three. Furthermore, around three quarters of this debt, so that’s well over $3 billion, is owed by low-income individuals, many of whom rely on government benefits as well. 13% or just over 99,000 people owe more than $10,000 to the Government.

More than 85% of those who do owe a debt have owed it for more than a year and about 45% cent, an incredible number, have owed debt for at least four years. Finally, Māori and Pacific people are overrepresented in almost all categories of debt a sadly quite typical issue.

The debt policy framework is trying to ensure is that debt recovery is fair and effective and avoids exacerbating hardship. And above all, it aims to prevent debt occurring in the first place and not exacerbate issues.

There are three main parts to the framework. Firstly, a set of overarching principles for creating and managing debt. Then secondly, a purpose centred approach which classifies debt into different groups according to the policy purpose and discusses how different settings might be appropriate for some purpose and others. And then finally, what’s called term to person centred approach, which takes into consideration the personal circumstances, with focus on consideration of financial hardships, as I said.

These debt issues tend to exacerbate and build on each other leading to a circle of despair. $10,000 of debt doesn’t sound like a lot, but for very low-income people it seems like an insurmountable mountain.

Anyway, this framework has been signed off by the Government after feedback from quite a number of interested agencies. For example, the Citizens Advice Bureau, the Methodist Alliance, the New Zealand Council of Christian Social Services, the Salvation Army, and a whole range of other non-governmental organisations. Hopefully this feedback will build a better framework for the practice of managing this debt.

Good but Inland Revenue also needs to do its part

I welcome this initiative, but I also think that as part of it, Inland Revenue needs to be also considering its approach to debt management, such as the effectiveness of the late penalty regime, and how efficiently it is on top of managing debts, because if the debts get away from people, they just give up. That’s what my experience has shown time and again and it’s also what Inland Revenue has experienced.

I think it’s still a good step forward, particularly, in trying to bring a coordinated approach because there’s nothing more infuriating to someone who might be unlucky enough to find ourselves in a position of debt with two or three agencies, and finding that the approach taken by each of those agencies is different.

The Tax Working Group recommended a single Crown agency to manage current debt should be established to deal with this issue. That does not seem to have been part of these recommendations at the moment, maybe it might be picked up at a later stage. Nevertheless, it’s a step forward in the right direction and we’ll hope that it starts to address these issues of managing the debt fairly and efficiently for people.

The $5 billion PREFU hole no-one is worried about

And finally, this week, back to the Election. We’re still hearing plenty about tax in the election campaign. Politicians are all out on the trail telling us everything that’s going to happen or not happen. This week the formal opening of the government books happened with the release of the Pre-election Economic and Fiscal Update (PREFU). There was plenty of differing interpretation about the state of the government’s finances going forward.

But there was a wonderfully interesting little snippet which Newsroom picked up on, and that was the impact of next year’s Matariki public holiday. Matariki always falls on a Friday, and next year it falls on 28th June, which is the last working day of the fiscal year to 30th June 2024. And because of that, the cash that would come in on that day, which represents about $5 billion of GST and provisional tax won’t actually hit the Government’s coffers until the following Monday, which is 1st July and the start of the following tax year. So, on the face of it, the Government’s going to be $5 billion short of cash for the current year ending 30th June 2024.

As a Treasury spokesperson said, “This public holiday effect is expected to affect the Crown’s tax receipts but not tax revenue, since Inland Revenue will calculate accrued tax revenue as at 30 June 2024 as it normally would at any other year end.”

And for the record, this won’t really affect individuals because we file tax returns to 31st March each year. Furthermore, Inland Revenue won’t penalise people for making a payment on 1st July, the first working day after it was due because Inland Revenue hasn’t switched over to a seven-day banking. So nice quirky little story to end the week.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A few weeks back, an issue emerged over in the East Coast and here in Auckland about the potential application of the bright-line test to homeowners who had been forced to move out following Cyclone Gabrielle and the January and February flooding events. The issue was if they had to leave the property for more than 12 months while it was being repaired or because they could no longer live there, the bright-line test could apply if they were forced to sell within the relevant bright-line test period.

The Government this week announced that it is adding a Supplementary Order Paper (SOP) to a tax bill that’s going through Parliament at the moment (and which will be enacted after the election).

The SOP contains proposals to ensure that the main home exclusion from the bright-line test is not affected by a property owner needing to vacate their North Island flood or cyclone damaged home for more than 12 months so it can be remediated or repaired. It also ensures the bright-line and other land-based timing tests, because we have a number of them, are not triggered when local authorities or the crown buyout properties impacted by the 2023 Auckland flood events and or Cyclone Gabrielle. You’ll recall that last month Auckland Council and the Government agreed to a $2 billion package which will be used to buy out homes that were rendered unliveable following Cyclone Gabrielle or the Auckland Anniversary weekend floods.

So, this is a good result. That’s the problem with tests, they can have some harsh results. But as the Government said, by picking up examples from what happened following the Canterbury earthquakes, it will devise tests to ensure that those harsh treatments do not follow.

Fooling around and finding out…

And speaking of harsh treatments, some harsh lessons were learned by a couple of taxpayers about tangling with Inland Revenue. In the first, an Auckland second hand car dealer has been sentenced to six months community detention for tax fraud. The offender Mr Levada created a false identity and then as a director and shareholder set up two companies. The companies were then used to obtain GST refunds totaling $309,000 even though neither company traded. There was a bit of a hard story behind this in that he wanted to help his wife’s family in Ukraine. But he admitted that he knew he was stealing and he has repaid the full amount owing.

Apparently, this got picked up by the Ministry of Business, Innovation and Employment in April 2021. And then obviously from there Inland Revenue realised what was happening. To me this is another example of why we really ought to think hard about GST compulsory zero rating between GST registered businesses. It reduces the opportunity for people to try and defraud the system. They don’t always get away with it, as we’ve just seen here. But maybe remove the temptation in the first place is where I would go with my suggestion.

Avoiding tax by forgoing all income?

But that story is really quite tame compared with a story from Nelson in the New Zealand Herald. As I told the reporter this is an “absolutely wild story”. Mila Amber had run into trouble with Inland Revenue and at the end of 2017 she was told she owed at least $110,000 in taxes, penalties and overpaid Working for Families tax credits. (In fact, the final figure was amended to nearly $365,000).

Amber decided to devise a scheme in cooperation with a UK based company under which she sold her property in Nelson to this company for $847,000. The buyer didn’t have to pay a deposit or any interest and just would simply pay off the property over 25 annual payments with the first payment due a year after settlement. The deal meant that the property was out of the reaches of Inland Revenue if they were going to try and seize the property or force a sale to pay off the debts. Amber was made bankrupt, and the Official Assignee took the case to court to try and overturn the sale. Which is how all these details emerged.

It’s just quite staggering what was attempted and what people thought was going to happen here. This seems to have been one of those cases where the taxpayer got really enraged by Inland Revenue’s actions. She changed the name of her trading company to Abbey Services (Killed by Tax Maladministration) Ltd which as the judge in the decision, called it rather unsubtle and refused to acknowledge the name basically in the judgement. The judge overturned the sale effectively transferring the property to the Official Assignee.

The judgement includes this rather jaw dropping line “It’s hard to see how it is beneficial to avoid tax by forgoing all income” which may be true but didn’t work out for Ms Amber. As I told the Herald, as the property seems to have been mortgage free she basically did herself out of half a million dollars. She’d have done better to have sold the property, pay the tax and move on.

I use this case to repeat something I’ve said many times previously. When you run into trouble with your taxes, talk to Inland Revenue. Go forward and initiate action and in most cases, if you are making reasonable offers and reasonable attempts to meet your liabilities and Inland Revenue can see that you’re being reasonable in your approaches, it will be prepared to find a way forward for everyone. In this particular case going around renaming your company Killed by Tax Maladministration and entering into a quite scandalously scheme to avoid those liabilities got the taxpayer nowhere.

I also think H.M. Revenue and Customs might be very interested as to what was going with the UK company involved. And I would put good money on details of the case having been shared by Inland Revenue with HMRC. I know from experience that Inland Revenue and other authorities share information on a proactive basis. We’ve talked in other podcasts about the Common Reporting Standards for the Automatic Exchange Of Information. Tax authorities are sharing data on a vast scale now.

The cases of this Nelson lady and the second-hand car-salesman are more examples of never underestimating Inland Revenue because it may appear slow, but it will eventually catch up with you.

Having just talked about international tax agreements, it’s very interesting to see the continuing debate around National’s tax proposals, which I discussed last week and in particular the issues around the proposed foreign buyers tax. This has led to quite a debate with National confident that its numbers stack up and that it is legally possible.

The question raised last week continues to be asked ‘Well what about international tax treaties and the so-called non-discrimination clauses?’ It turns out that just after last Friday’s podcast was recorded, National went and sought advice from Robin Oliver, a former Deputy Commissioner of Inland Revenue, member of the Last Tax Working Group and a real guru of tax.

He told RNZ, this is a “very esoteric” area of tax law but it should be possible to introduce the tax.

In his view it would depend on tax residency, not nationality. In relation to the Chinese double tax treaty, it doesn’t allow discrimination on the basis of nationality. The potential argument is that a Chinese national residing in China who purchases property in New Zealand could be subject to the new law, whereas a Chinese national resident in New Zealand could not.

But even if it could be done, I’m of the view whether you should do that. Both myself and Eric Crampton the chief economist of the New Zealand Initiative think tank, told RNZ that, ‘Well, yes, it might be doable, but on the other hand, what would it do for our reputation internationally?’ We build our trade agreements around being an honest broker in this, that we follow a rules-based approach.

A point that was made at the recent International Fiscal Association trans-Tasman conference is that these tax treaties are often related to trade agreements. So, these sorts of issues would have been on the table and part of the discussions. Having signed an agreement fairly recently and then now looking to apply a workaround to tax nationals from that country doesn’t look good for our international reputation.

Just because you can doesn’t mean you should

What this comes back to is a situation myself and other tax advisers I’m sure will sometimes encounter where we’re asked to advise on something. We look at it and come back and we say, ‘Well, looking at the way the law was written we think it’s possible.’ But then sometimes the question boils down to ‘Well you could, but should you?’ Sometimes in tax just because you can doesn’t mean you should.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

It’s been a busy couple of weeks in the tax world. Last week, the relevant legislation for the interest limitation rules was released in a Supplementary Order Paper, and on the same day, probably not by coincidence as one or two other tax advisors have noted, Inland Revenue released a draft interpretation statement concerning whether, and if so to what extent, the land sales rules in the Income Tax Act 2007 apply to changes to co-ownership, subdivisions of land and changes of trustees. Coming out on the same day as the interest limitation legislation it certainly has given us plenty to chew on.

Furthermore, Inland Revenue has kept busy this week with an issues paper seeking feedback on a number of matters facing employers and payers of cross-border workers. The whole week kicked off with the Pandora Papers, reigniting the debate over New Zealand’s controversial foreign trust regime.

Property transfers between associated people

As we discussed last week, the Supplementary Order Paper with the relevant draft legislation for the interest limitation rules was released, and submissions are open to the Finance and Expenditure Committee until 9th November. So, you’ve got approximately five weeks to get in and make submissions on these draft rules. I expect there will be some changes as a result of submissions and certainly I encourage everyone who has an interest in this area to make submissions with the aim of trying to improve the legislation.

Included in the Supplementary Order Paper is something which begins to address an issue which has been in place since the bright-line test was introduced in October 2015. And that is when there is a transfer between associated persons. Say for example, a person holds a property and transfers it into a trust or a look through company. As the legislation presently stands, that transfer would reset the clock for the bright-line test. So, a property that might be known for many years – more than 10 years for example – which has been transferred to an associated entity and therefore economically, when you look at it, no real change of ownership has happened. But for the bright-line test purposes there has been a deemed change of ownership and therefore the clock gets reset.

Now this was a problem identified way back in 2015, and the Supplementary Order Paper begins to address it by having some new rollover relief rules, which will apply from 1st April 2022. However, the rules are very complicated, particularly in relation to the transfer for a trust. And it could be really quite problematic for trust resettlements because the transfer to the trust must be a beneficiary who is also a natural person and can qualify for the main home exclusion. There’s quite a bit of detail to unpack in there.

In fairness this is an improvement on the original proposal we saw when in consultation with Inland Revenue earlier this year, but it still has a number of complexities and traps which will make it not particularly user friendly. So, although it’s a step in the right direction, this is one area I would very definitely recommend people make submissions on.

Land sales tax rules

Now, the other thing that was released on the same day as the Supplementary Order Paper, was a draft interpretation statement – nearly 60 pages – on how the land sale rules in the Income Tax Act might apply changes to co-ownership, subdivisions and changes of trustees.

This is an extremely important paper because it addresses issues where there was some broad understanding of what the position might be, but it’s good to see Inland Revenue set out its position.

Now the starting point to bear in mind is that income tax legislation in dealing with land transactions, refers to “disposals”, not sales. And this is the issue that the draft interpretation statement is addressing – what happens if there are transfers between co-owners, for example, does that create a disposal for tax purposes?

Now, quick digression here. The paper refers to tenancy in common and joint tenancies. A tenancy in common is where each party owns a distinct share, i.e. 50% or a one third share. A joint tenancy is where the land is owned by the parties together, but there’s no specific shares, in which case each person has a notional proportional share. So, for example, if there are two joint tenants each has a notional 50% share. And if there are five joint tenants, each has a notional 20% and so on.

What the interpretation statement goes through is what happens if there’s changes to types of co-ownership. For example, instead of owning it 50-50, they go to one party owning a one third share and the other party having a two-thirds share. Or there are two people and a third person is introduced or there are three people, and then one decides to.

What the interpretation statement says if it’s the type of co-ownership and the proportional notional changes don’t change, there isn’t a disposal under the land sale rules, so that means there’s no tax implications on the transfer. So, for example, if A and B were tenants in common with 50% each and they then moved to being joint tenants with again the notional 50%, there’s no disposal.

On the other hand, if, for example, A had 25% and B had 75% under a tenancy in common and then moved to 50:50, then B has disposed of 25% interest, and this disposal, could be taxable. And here’s where the issue gets quite tricky because this sort of transaction may be done on paper and no cash may change hands. People have got to be very careful that if they are changing the proportions of how they own property, that they don’t trigger a tax charge and find themselves with a tax bill, but no cash has actually changed hands to enable payment of any tax which may become due.

To recap, if there’s a change in the form of ownership where the proportional and notional shares don’t change, that’s not a disposal. But if there is transfer, that adds a new co-owner, for example, that would be a disposal. And likewise, if there’s a transfer that removes a co-owner, that’s also a disposal. There’s a lot to consider in this paper and we’ll need to pore over it very carefully. But at least it gives us some guidance to work with. Submissions are open until 9th November.

Cross border workers

Earlier this week, Inland Revenue released another issues paper this time dealing with cross-border workers and identifying issues for reform. Work on this has probably been accelerated because of what’s happened with COVID, which has disrupted work and travel patterns. In the words of the issues paper,

“It has also highlighted the role of technology in enabling cross-border work arrangements. The pandemic has accelerated existing trends affecting how, when, and where people work and technologies such as artificial intelligence and the greater use of contracts. The supply of personal services will be increasingly important drivers in the future.”

Against that background, Inland Revenue have been looking at reviewing the tax obligations that apply to payers of cross-border workers. And this paper focuses on what happens for employers and payments to independent contractors. This is an issue I’ve encountered quite a bit recently, as people have migrated to New Zealand but continue to work remotely for their overseas employer.

The paper begins by looking at the current PAYE rules. And it concludes that these are inflexible. One of the big issues is that we have arrangements concerning our double tax agreements where a person who is deemed to be non-resident but working in New Zealand and can be paid by their overseas employer for up to 183 days without triggering PAYE.

But currently under the PAYE rules, when they cross that 183-day threshold then after the day count is breached, the employer is required to correct the tax position not just going forward but also from the first day the employee was present in New Zealand. So, it could be several months later when the position is realised. And this means employers get additional compliance costs and could also be potentially subject to shortfall penalties and use of money interest. All in all, pretty much a compliance nightmare.

Inland Revenue recognise this needs to be reviewed because it’s simply not always practical to collect PAYE from the income of cross-border employees. It’s hoping to allow greater flexibility for employees. And one of the things they’re proposing is a new period of time for correcting a situation, which is 28 days from the employer first becoming aware that this day count threshold that I mentioned earlier has been breached.

To use an example from the issues paper, Estella a Brazilian tax resident, comes to New Zealand on a 10-week assignment, 70 days, to work on a construction project. It’s anticipated that the 92-day exemption, which is part of our Income Tax Act, will apply. We don’t have a double tax agreement with Brazil yet, so this 92-day exemption is only one available.

But the project gets delayed and now extends beyond the 92-day exemption to 98 days and a catch-up payment for PAYE is therefore required. And no penalties should arise so long as this is done within 28 days of identifying that there will be a breach of the 92-day threshold. That’s one of the issues Inland Revenue are looking at.

They’re also looking at non-resident contractors. There’s another set of rules that apply to independent contractors working in New Zealand. Currently, non-resident contractors’ tax is 15% and the New Zealand resident payer is required to withhold that from each contract payment made to a non-resident contractor.

The thresholds and rates haven’t been changed since 2003. Those thresholds, by the way, were adopted and in the wake of the Lord of the Rings when a large number of American productions came to New Zealand in the early 2000s and encountered this issue and work was done to mitigate those issues. It’s therefore probably time to have a look at these issues again. And it’s good to see that Inland Revenue putting some ideas out there. Submissions on this are open until 19th November.

New Zealand’s controversial foreign trust regime

As I mentioned the week kicked off with the Pandora Papers revelations. This reignited the debate over New Zealand’s foreign trust rules. Now, when the extent of the use of New Zealand based foreign trusts was revealed in 2016 in the wake of the Panama Papers, the then government moved very quickly to tighten regulations.

And as a result of that, the estimated numbers of foreign trusts registered with Inland Revenue fell from about 13,000 back in 2016 to just over 4,000 now. The Pandora Papers will reignite debate about these rules.

These foreign trusts exist as a by-product of changes made to New Zealand’s taxation regime for trusts in 1988. That’s when New Zealand switched from taxing trusts based on the residency of the trustees to taxing on the basis of the residency of the settlor (the person who established it).

Now the reason behind this was to tackle what was seen as quite substantial tax avoidance by New Zealand tax residents, and by and large, that move was highly successful. It is practically impossible now for any New Zealand tax resident to set up a trust now in a tax haven and shelter income from New Zealand tax.

But an accidental by-product of the regime was that non-New Zealand residents are able to establish such trusts. What they would do is settle a trust under New Zealand law with New Zealand trustees. Under the foreign trust regime, income from outside New Zealand would not be taxable. Which, by the way, is legal and consistent with general tax principles around the world – that is you tax residents on a global basis, or you tax income with a source in the country. So, for example, New Zealand taxes income with a New Zealand source and New Zealand residents.

If you have rules as New Zealand established, which say, “Well, we don’t deem this trust to be tax resident in New Zealand”, then offshore income becomes tax exempt in New Zealand. And so, this is quite attractive because it meant that New Zealand essentially became an onshore tax haven for sheltering income.

So, it’s quite controversial, and started to attract quite a lot of attention. In part because of growing unease with tax havens we saw the introduction of the Common Reporting Standards on the Automatic Exchange of Information. New Zealand’s current foreign trust disclosure rules are in line with those standards.

The Panama Papers gave a boost to those rules, and I’m sure the Pandora Papers will also lead to further tightening as well. Although the Minister of Revenue didn’t seem particularly enthusiastic about moving very quickly on the matter, there’s a lot going on as we have discussed. In any case, the position is that the number of trusts registered with Inland Revenue has fallen by two thirds since 2016 to just over 4,000. The argument would be that a fair amount of the more dubious entities have been weeded out.

But what’s common in moves around the world and it ties into anti-money laundering moves particularly in Europe is for establishment of trust registers which is where details of these trusts are held. Now whether they are held publicly like the Companies Office register, or privately and available only to Inland Revenue which is essentially what we are doing at the moment, needs considering.

For those who are calling to tax these trusts what needs to be kept in mind is that often these foreign trusts are established partly on grounds of secrecy but also to ensure assets held in such a trust are outside two taxes, both of which New Zealand doesn’t have. That is capital gains tax and estate duties. Now these are transactional taxes, which are triggered by death or disposal.

So, when considering calls for New Zealand to tax foreign trusts we need to think about how we would practically do that given we don’t have a general capital gains tax or estate duty. Basically, we would then be looking at a wealth tax or something akin to the foreign investment fund regime. Whatever, there’s going to be quite a bit of debate on this going forward and it’s not going to die down very quickly.

Applications open

And finally, in Covid related news you have until 11:59pm on Thursday 14 October to apply for the fourth round of the August 2021 Wage Subsidy Scheme. And applications for a third round of the Resurgence Support Payment are now open. To be eligible, your business must have experienced at least a 30% drop in revenue or a 30% decline in capital-raising ability over a 7-day period, due to an increase in Alert Levels.

You can receive $1,500 per business plus $400 per full-time employee (FTE), up to 50 FTE.

The maximum payment is $21,500.

If you’re a sole trader, you can receive a payment of up to $1,900.

If you’ve applied for previous Resurgence Support Payments and you’re eligible you can apply for this one.

Well, that’s it for today. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients. Until next week kia pai te wiki, have a great week!

The brightline test will remain at five years however for new builds. In addition, there will be changes to the main home exemption for the bright-line test and also restrictions on interest deductions for rental investment properties.

Speculation beforehand had focused on the extension of the bright-line test to 10 years. And that has been confirmed. So properties acquired on or after March 27 sold within 10 years will now be taxable.

Other tax advisors and myself were briefed beforehand by Inland Revenue and I asked a question about what additional revenue would be expected to come from the brightline test. The estimate is it will be about an extra $650 million per annum. Incidentally that’s more than the increase in the top income tax rate to 39% is expected to raise.

Separately the brightline test period will remain at five years for new builds acquired on or after 27 March. The idea here is to encourage some investment in new property.

There is another change in the brightline test rules which is potentially quite significant and that’s around the treatment of the main home exemption. Currently if 50% or more of the time a property is held, it is occupied as a main home, then it is completely exempt from taxation. If it’s 49% tough! It’s going to be fully taxable. So, it was a little bit harsh, that arbitrary treatment.

The proposal is to change that for property acquired on or after 27 March – you’ll be taxed on the period it was not occupied as your main residence. So, for example, if it was your main home for 80% of the time then only 20% of the gain will be taxed, whereas currently for properties acquired prior to 27 March the rule will be that in that case it will be fully exempt.

So on one hand it means that some gains which would have been exempt would now become taxable, on the other hand some gains, say that 49% example, which were fully taxable, now become partly taxable. So, the Lord giveth and the Lord taketh on that one.

However, the big change which has been announced that’s generating quite a bit of commentary on social media is the proposal to restrict, in fact remove entirely over time, interest deductions on residential property income. And this kicks in from October 1.

For residential investment property acquired on or after 27 March no exemption will be allowed from 1 October. However, for properties acquired before 27 March interest deductions are still claimable but will be reduced over the next four income years until it’s completely phased out by 1 April.

Starting 1 October this year, only 75% of the interest will be deductible. For the full year ending 31 March 2023, 75 % will be deductible. For the year ended 31 March 2024 it will fall to 50%, and for the year ended 31 March 2025 it falls to 25%. And then from 1 April 2025 onwards no interest deduction will be allowed.

Inland Revenue will be consulting on what happens to interest deductions in the event that the brightline test applies. In other words, if a property is sold during a period and the brightline test applies then some interest deduction could be allowed. We’ll wait to see what the proposals are around that.

Now this is obviously a significant change. I made a suggestion last year that maybe it was time to apply the thin capitalisation rules, but this has gone further than I expected. But it also reflects a measure that happens in the UK.

It will be interesting to see how this plays out. The obvious concern would be that landlords will increase rents. But on the other hand, if you are going to do a measure like this although there is never a perfect time for investors, interest rates having fallen so much means that the impact this time is probably significantly less for investors than it would have been say two/three years ago when interest rates were not 3% but 6% or even higher.

So there’s swings and roundabouts there, no doubt though the Government will be watching with some concern to see what happens about residential rental increases. And there is a measure, actually separate, which proposes to limit the number of increases in rent and it now does it per property rather than per tenant. The proposal is a landlord can only increase the rent once every 12 months per property rather than the current once per 12-month tenancy.

So, there’s a fair bit of detail and commentary going to happen around these proposals. The extension of the brightline test to 10 years was expected. It’s now getting to the point that because our land rules, as I’ve said, beforehand are very complicated, maybe it’s time for a comprehensive review. Maybe even saying that all land sales within 10 years are taxable apart from main homes, and also farms and businesses.

Possibly also in that time it might be worth thinking about whether it is appropriate that the gain gets fully taxed. But for now, those are the rules in place.

The fiscal impact of the interest rate deductions will be quite interesting because that may mean the Government has a little bit of a tax windfall, obviously because it’s now getting more income tax because there’s fewer deductions. We’ll have to wait and see.

Anyway, that’s it for now, I’ll probably have more commentary on the fallout from these proposals in our next podcast. Until then, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until Friday Ka kite ano!