Earlier last year, Inland Revenue conducted a policy consultation on tax matters relating to charities and not-for-profit sector. At the time, there was a fair bit of speculation that there would be changes announced in the May budget in relation to the taxation of charities and in particular what was seen perceived to be the unfair tax advantage given to charities which owned businesses.

That actually didn’t play out, but instead Inland Revenue pushed forward with consultation on the taxation of mutual transactions of associations or not-for-profits, including clubs and societies. Behind the scenes it began targeted consultation in November with around 50 persons and organisations who had provided feedback on the previous consultations. This consultation covered donor-controlled charities, membership subscriptions, and other matters.

A Christmas surprise?

On 15th December, just before Christmas, Inland Revenue then released what it called a ‘Targeted policy consultation’. This explained what had happened in November and that it was now seeking more feedback because of wider public interest in the issue. The thing was, though, the initial deadline for submissions was 24th December. However, Inland Revenue added it would be prepared to extend this submission deadline on request, but it plans to review all submissions by late January.

The surprise part of the consultation is in relation to membership subscriptions and related matters. The consultation makes clear that membership subscriptions charged by tax-exempt not-for-profits, such as the 29,000 registered charities and 19,000 amateur sports clubs, are not taxable currently and will not be taxed under the proposals out for consultation.

Are membership subscriptions taxable?

But the question under consideration is around membership subscriptions for most not-for-profit organisations. Currently, the accepted treatment is that trading with members, such as conferences and sales of merchandise, are considered taxable income, but membership subscriptions were not as they were covered by the ‘mutuality principle’. However, Inland Revenue has drafted an operational statement “…indicating that it is likely to formally change its view and state that under current law many membership subscriptions would be taxable.” Needless to say, this would be an unwelcome surprise for quite a lot of groups. Although there may be a trade-off in that some other expenses which are currently not deductible may become deductible.

The consultation also suggests the current annual tax-free threshold of $1000 could be raised to $10,000. There are also suggestions to simplify the income tax filing requirements for taxable not-for-profits, but Inland Revenue also wants to require banks and other financial institutions to provide it with financial information for those not-for-profits who use the tax-free threshold.

This is a surprising and for many organisations unwelcome development estimated to raise perhaps $50 million annually. From what I’ve seen there’s no clear explanation given as to why Inland Revenue thinks the mutuality principle no longer applies in relation to the subscriptions. I imagine there will be quite some pushback on the membership subscription issue. It will be interesting to see how this plays out and what changes are announced in the 2026 Budget.

“Don’t look back in anger” – 2025 in review

Talking of Budgets, the 2025 budget on 22nd May contained a pleasant surprise with the announcement of the Investment Boost allowance. This enables businesses of any size to fully deduct 20% of the value of any new assets in the year of purchase. Interestingly, it also includes new commercial and industrial buildings and would also cover earthquake strengthening in some cases. Perhaps surprisingly, there was no cap put on the amount which could be claimed by a business.

The Investment Boost initiative is designed to boost investment and productivity, a theme in common with other tax initiatives, for example, proposals for digital nomads and changes to the Foreign Investment Fund regime included in the Taxation (Annual Rates for 2025−26, Compliance Simplification, and Remedial Measures) Bill currently before Parliament. It’s actually a on long-standing principle of our tax policy to enable investment in New Zealand and remove barriers to doing so.

The investment boost was a big surprise. Whether it’s had the hoped for impact is not clear yet. As everyone is well aware, economic activity was bumpy in 2025, but it could be that the groundwork has been laid for a stronger recovery this year.

Boosting Inland Revenue’s compliance activities

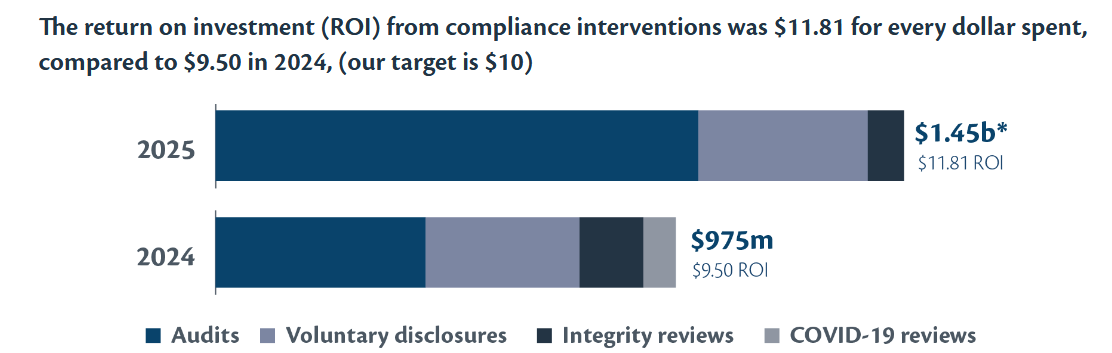

Another constant theme for the year, was more money in the 2025 Budget for Inland Revenue to boost its compliance activities. On top of the $116 million it was given over 4 years in the 2024 Budget it got another $35 million in the 2025 Budget. Consequently, 2025 saw great degree of investigative work by Inland Revenue. According to Inland Revenue’s 2025 Annual Report, it has achieved great returns from its increased compliance activities.

In addition to investigation and review work, Inland Revenue is also trying to close off what it considers loopholes and areas where there appears to be seepage in the tax system. The not-for-profits consultation we discussed earlier is one such example. However, arguably the biggest single example, and which was such a bolt from the blue, I called it a bombshell, was the recently announced consultation on the taxation of shareholder advances. It’s one of the most significant changes to the taxation of small businesses in recent years, potentially worth several hundred million of additional tax revenue annually. We’re therefore going to see a fair bit of lobbying and feedback about the proposals which are almost certain to be as part of the 2026 Budget and the annual tax bill. Watch that space.

Targeting crypto-assets

The taxation of crypt-assets is one specific area where Inland Revenue is currently very active. In November I discussed Technical Decision Summary TDS 25/23 where investors in crypto-assets lost the argument that gains were on capital account and therefore non-taxable. This case is probably the tip of the iceberg as according to Inland Revenue’s 2025 Annual Report “As at 30 June 2025, more than 150 customers were under review, with total tax at risk in the tens of millions.”

We’ll also see ongoing activity from Inland Revenue reviewing property transactions. Everyone tends to underestimate how much access to data Inland Revenue has and the information sharing which goes on with other Government agencies and tax authorities around the world. I’m sure I’m not the only tax agent seeing increasing numbers of inquiries from clients and Inland Revenue relating to investigations or reviews covering overseas income which may or may not have been declared properly.

Tax debt – a $9.3 billion problem

The other big area for Inland Revenue is managing the debt book, in late November I had a very interesting discussion with Tony Morris from Inland Revenue about how it is approaching the management of its debt book, which is over $9.3 billion and what steps are being taken to reduce this.

I’m seeing a much more forceful attitude from Inland Revenue around earlier interventions and debt collection. In some cases, that’s well merited. Other cases, I think it’s been a little ham-fisted. There’s also work to be done in managing companies which fall behind on GST and PAYE. Much earlier intervention is needed there. But one hopes that the extra money that Inland Revenue has received from the government will aid that. Getting the debt book under control is obviously very important for Inland Revenue and for the Government.

One area I think actually needs a fundamental redesign, is the question of student loans where only 30% of overseas-based debtors are making repayments at this point. Now, Inland Revenue does have the power in many double tax agreements to ask overseas authorities to intervene on its behalf, but it seems to have been a bit reluctant to do so. 2026 may see a change in this approach.

Overall, we can expect to see Inland Revenue gathering using all its available tools to collect the maximum amount of overdue debt and bring the debt book under control. That’s been a big theme in 2025 and it’s going to be a continuing theme this year.

The Trump effect

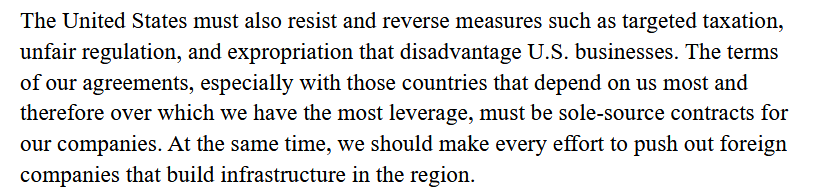

Internationally, the second Trump administration has caused all sorts of upheaval across the world order geopolitically, but also in the tax space where progress on the already grindingly slow Organisation for Economic Cooperation and Development/G20 multilateral tax proposals, the so-called Pillar 1 and Pillar 2 proposals, has basically ground to a halt.

The Trump administration made it clear early on it is hostile to what it considers unfair taxation and regulation. Its National Security Strategy released in November spelled it out bluntly.

(National Security Strategy of the United States of America, page 19)

Against this background it’s hardly surprising the Government in May decided to withdraw (“discharge”) the Digital Services Tax Bill.

Big Tech, Little Tax

The multilateral Pillar 1 and Pillar 2 deals seem dead in the water, but as the Tax Justice Aotearoa noted in their report, Big Tech, Little Tax that still leaves the problem of the tech companies’ apparently extensive use of transfer pricing methodologies to minimise their tax bills.

One of the examples the Tax Justice Aotearoa report considered was Oracle New Zealand, which according to its 2024 financials, earned revenue of $172.7 million, but paid licensing fees of $105.3 million to an Irish-related party company. It ultimately finished up with taxable income of just $5.3 million. It’s apparently paid royalties representing between one third and three-fifths of its total revenue. Oracle, incidentally, is currently undergoing an audit in Australia and there’s a related tax case going through the courts, which I expect Inland Revenue will be watching very closely.

And then there’s Microsoft, which earned revenue of $1.32 billion, but then paid over a billion dollars in purchases to another Irish located related party company.

The Digital Services Tax might have had some impact on this, but a more likely tool to try and recover additional tax would be to start applying non-resident withholding tax on the royalty element of any cross-border payment. The payments should remain deductible, but subject to a (typically) 5% withholding tax. Such an approach should be acceptable under most long-standing international agreements, but it will be interesting to see what pushback emerges if Inland Revenue adopts this approach.

Tax policy highlights the rising cost of demographic change

In the tax policy space in general, it’s been an interesting year with the Inland Revenue’s long-term insights briefing somewhat controversially looking at the question of the tax base. This was alongside Treasury’s He Tirohanga Mokopuna, statement on the long-term fiscal position which took a 40-year view of the Government’s fiscal position. A common theme was the demographic pressures on pension funding. Unsurprisingly that, together with the rising costs of climate change, was also a major theme the OECD’s review of tax policy in 2024.

Capital Gains Tax – a never-ending story?

The seemingly endless debate about capital gains tax continued through 2025. The International Monetary Fund paid its regular Article IV visit and suggested it might not be the worst thing in the world. The more interesting IMF report to me was about New Zealand productivity, where it directly suggested that the lack of a capital gains tax has meant excess capital has been gone into property rather than into productive investment, and it could be a factor in our low productivity. That’s not an unreasonable conclusion in my view.

Then we had the Labour Party finally announcing its somewhat limited capital gains tax proposal, which will apply to all residential investment and commercial property. That’s a little less bold than what Labour Party members wanted, but on the other hand is in line with our practice of incremental changes. It’s also pretty much in line with what the minority group on the last tax working group suggested, a comprehensive capital gains tax wasn’t needed, but expanding it into the taxation of residential property was certainly recommended.

The Tax Policy Charitable Trust brought down former IMF Deputy Director Professor Michael (Mick) Keane for a couple of lectures, one of which was in Wellington at Treasury. He made the interesting observation that most tax jurisdictions which do have a capital gains tax, and remember we’re in the minority, approach it from the basis that everything is in unless it’s out. Presently, our approach is the flip side, everything is out unless it’s in but the problem is there’s a lot more in than people realise and so there’s seepage of potential review. In terms of conceptuality, I think his approach is to be preferred. Include everything and then carve out exemptions (such as the family home). That is what we see around the world as he noted.

Looking ahead as always, there will be a huge debate going on around what are the best tax settings for New Zealand as we head into the second half of this decade. With 2026 being an election year, we’re going to hear a lot about capital gains tax. I’m afraid non-tax geeks will probably be heartily sick of it by the end of the year.

Thank you

Finally, I’ve been very fortunate with the guests I’ve had this year, so thank you all, you’ve been most interesting and generous with your time. A special shout-out to Tony Morris of Inland Revenue for a fascinating discussion on where Inland Revenue is working in the debt space. (Transcript coming soon).

And on that note, that’s all for 2025, we’ll be back in late January to cover all the latest developments in tax as always. I’m Terry Baucher and thank you for reading and commenting. Please send me your feedback and requests for topics or guests. In the meantime, best wishes for 2026!

Inland Revenue consults on not-for-profit sector and more.

It’s been an extremely busy week in tax – just as we were planning to go to air, Parliament’s Finance and Expenditure Select Committee (“the FEC”) released its report on the Taxation, Annual Rates for 2024-25 Emergency Response and Remedial Measures Bill initially introduced last August.

We covered the bill’s main initiatives when it was initially released, and now the FEC is reporting back on submissions it received, what’s been amended and why, together with Inland Revenue’s accompanying report on submissions. There’s also a supporting report from the independent adviser to the Select Committee, John Cantin, a former guest of this podcast. Overall, there are no major real changes to the legislation. There are minor amendments resulting from issues brought to the attention of the FEC which is how the submission and Select Committee process is meant to operate.

Tax relief for future emergency events

The Officials’ Report on submissions had some interesting submissions on the issue of procedures to manage tax relief for any future emergency events.

The measure was uniformly supported but several submissions proposed making ready to go after a trigger event some of the measures that were brought in and employed relatively successfully during the initial COVID response in 2020, such as carry back of losses, accelerated depreciation, or cashing out of losses. In most cases the submissions were noted or declined.

I thought it was interesting to see that the main submitters involved the Big Four accounting firms, Chartered Accountants of Australia and New Zealand, and the Corporate Taxpayers’ Group. I think these submissions were prompted by our experience during COVID in 2020, where a lot of policy had to be devised and implemented on the hoof, with frantic consultation going on between Inland Revenue and various parties.

I was involved in some of those consultations, and I think it’s not unreasonable to have these measures ready to go if needed. On the other hand, I can see why Inland Revenue and the Government might be a little reluctant to have the ambit of the bill expanded.

Transferring UK pensions to New Zealand

Moving on, one of the measures I was interested in was the proposal for what they call a scheme pays measure in relation to Qualifying Recognised Overseas Pension Schemes or QROPS. These are schemes that are able to receive transfers of pensions from the United Kingdom.

There’s been some debate around this, as under our rules those transfers are taxable, and it has been a long-standing issue that in many cases this triggered a tax bill which taxpayers could not pay as the funds were locked up in the transferred funds.

One suggestion that had been made was this scheme pays proposal, where transfers are made into a scheme. The scheme may make a payment on behalf of the transferring taxpayer and that will be done at a flat rate of 28%, a “transfer scheme withholding tax”. There’s been a bit of tinkering with the proposal mainly about reporting requirements. Otherwise, the regime looks all set to go ahead with effect from 1st April 2026.

It’s a measure I feel ambivalent about. I was part of a group which lobbied for this change so it’s good to see it finally in place. On the other hand, as I’ve said previously, I do think that we ought to be thinking harder about why we’re taxed. (I also think taxing people years ahead of when they could access the funds is technically questionable – what if they died before reaching the required age?)

Crypto-Asset Reporting Framework

The other thing of note is that this Bill also introduced the legislation for the Crypto-Asset Reporting Framework. No amendments have been made to that regime. So that will be coming into force with effect from 1st April 2026. From that date New Zealand-based reporting crypto-asset service providers would be required to collect information on the transactions of reportable users that operate through them and report it to Inland Revenue by 30 June 2027. Inland Revenue would exchange this information with other tax authorities (to the extent it related to reportable persons resident in that other jurisdiction) by 30 September 2027.

Taxation and the not-for-profit sector

Moving on Inland Revenue has now released for consultation an Officials Issues Paper Taxation and the not-for-profit sector. This consultation is something that has been telegraphed for some time, there’s what might be termed unease around the exemption for the charitable sector and the merits of some entities apparently making use of the exemption. For example, the involvement of Destiny Church in the recent events at the Te Atatu library prompted calls for its charitable status being withdrawn.

Quite surprisingly, given the scale of the topic, the Issues Paper is a reasonably short paper running to just 24 pages in all. It covers three main topics. Firstly, a review of the issues involved in the charity business income tax exemption including the rationale for providing such an exemption, and then what potential policy design issues would need to be considered if that exemption was to be removed.

The second topic is donor-controlled charities, which is probably where the most controversy is emerging. It considers the integrity issues that arise from the absence of specific rules for donor-controlled charities in New Zealand, and again looks at possible design issues, including how other countries treat such entities.

And finally, the paper considers a number of integrity and simplification issues to protect against tax avoidance.

The charity business income tax exemption

Apparently, there are over 29,000 charities registered under the Charities Act. Many raise funds through business activities ranging from small op-shops to significant commercial enterprises. There’s been long-standing grumbling about how charities which run a business and have an exemption have an unfair advantage. So, it’s interesting to read the background behind this exemption which has been in place since 1940.

Para 2.3 of the Paper sets out the scope of the review:

“Some tax-exempt business activities directly relate to charitable purposes, such as a charity school or charity hospital. Other tax-exempt business activities are unrelated to charitable purposes, such as a dairy farm or food and beverage manufacturer. It is the unrelated business activities that are the focus of this review.”

“…an international outlier”

According to the Paper “The current tax policy settings make New Zealand an international outlier”. According to a 2020 OECD study Taxation and Philanthropy most countries have either restricted the commercial activities that charitable entity can engage in, or they tax charity business income if the business income is unrelated to charitable purpose activities. As the Paper notes

“These countries have typically been concerned with a loss of tax revenue from businesses if a broader tax exemption was applied, unfair competition claims, a desire to separate risk from a charity’s assets, and a desire to encourage charities to direct profits to their specified charitable purpose.”

New Zealand’s exemption is based on the “destination of income approach.” This means that income earned by registered charities is exempt because it would ultimately be destined for a charitable purpose. But, and this is again one of the key concerns that’s emerged over time, this approach allows income to be accumulated tax free for many years within a charity’s registered business subsidiaries before the public receives any benefit.

What competitive advantage?

Paras 2.7 to 2.14 of the paper look at the question of the exemption providing a competitive advantage because they don’t pay tax. This is an allegation I’ve seen repeatedly raised. As the Paper notes not paying tax means

“One element of a firm’s normal cost structure, income tax, is not present in the case of charity run trading operation. It is argued that this “lower” cost could be used by a large-scale entity to undercut its competitors, to improve its market share, or to deter new entrants.”

The Paper does not accept this argument stating:

“Although the exemption does provide a tax advantage, it does not provide a competitive advantage. Any one type of cost can be looked at in isolation.”

The reasoning for this conclusion is:

[2.9] “Because the tax-exempt entity can generally earn tax free returns from all forms of investment, the “after tax” return it expects from a trading activity is correspondingly higher than that of its tax competitors. Therefore, an income tax exempt entity cannot rationally afford to lower its profit margins on a trading activity because alternative forms of investments would then become relatively more attractive.

[2.10] On this basis, the tax exempt entity will charge the same price as its competitors. The tax exemption merely translates to higher profits and hence higher potential distributions to the relevant charitable purpose. Consequently, funding the charitable activity from trading activities is no more distortion than sourcing it from passive investments such as interest on bank deposits or from direct fund raising.”

What about predatory pricing?

The Paper also discusses whether a charity has a greater ability to use predatory pricing to gain an advantage. Again, that’s dismissed because “the value of tax losses for taxable businesses mitigates this advantage. Taxable businesses can carry forward losses to offset future profits.” That said, if the taxable company goes bust then it has no use for those losses so maybe that is an actual advantage.

“Second order imperfections”

On the other hand, the Paper acknowledges that there are “various ‘second order’ imperfections in the income tax system that may need to be taken into account.” One is that charitable trading entities do not face compliance costs associated with meeting their tax obligations. This lowers their relative costs of doing business.

Another is the non-refundability of losses for taxable businesses and can result in a disadvantage for such businesses relative to tax exempt business resulting in a higher relative rate of return for non-tax paying entities when there has been a loss in one year.

A third is the costs associated with raising external capital such as negotiating with investors or banks can be significant. These costs often make retained earnings the most cost effective form of financing. Because charities retained earnings are higher, this may give them lower costs for raising capital. On the other hand, charities can’t raise equity capital because private investors cannot receive a return.

How much is ‘significant’?

Interestingly, the Paper describes the fiscal cost of not taxing charity business income unrelated to charitable purposes as “significant and is likely to increase.” But no numbers are given and I’m curious to know exactly what is the cost of this particular concession?

The Paper asks submitters to consider what are the most compelling reasons to tax or not tax charity business income before it analyses the potential implications and design issues involved. A major issue will be distinguishing between related and unrelated business activities which could prove difficult in practice without clear legislation and guidance.

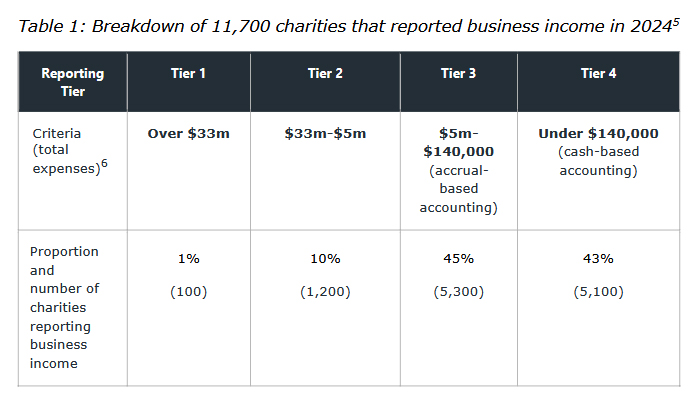

There’s more detail about the trading activities of charities. According to the Paper 11,700 of New Zealand’s 29,000 registered charities reported business income in their published 2024 financial accounts.

These four defined tiers follow the reporting requirements within the Charities Act.

A de minimis exemption?

Based on this initial analysis the Paper suggests a de minimis exemption for charities within Tiers 3 and 4. This would take 10,400 charities out of scope with only 1,300 subject to any policy change. Part of any policy change would involve the treatment of accumulated surpluses and whether there should be minimum distribution requirement.

According to the Paper a donor-controlled charity is any “charity registered under the Charities Act that is controlled by the donor, the donor’s family or their associates.” The current issue that there’s no distinction between donor-controlled charities and any other charitable organisations. The concern is growing that this can enable tax avoidance and raised compliance concerns “because of the control the donor or their associates can exercise over the use of charity funds.”

The Paper gives a few examples of potential abuse such as ‘circular arrangements’ when the donor gifts money to a charity they control, claim a donation tax credit or gift deduction, and the charity immediately invests the money back into the businesses controlled by the donor or their associates.

Also of concern with donor-controlled charities there can be a significant lag between the time of tax concessions for the donor and the charity, and the time of ultimate public benefit. This occurs because funds are accumulated and no or very minimal charitable distributions are made.

Another issue arises when donor-controlled charities purchase assets, or goods and services from the donor or their associates, at prices exceeding what would normally be paid by unrelated parties. These acquisitions are often made on terms that would not normally exist between unrelated parties.

Defining donor-controlled charities

This is the nub of the matter what criteria should be used to define a donor-controlled charity? The funds contributed and level of control a founder has. In Canada for example a charity is considered a private foundation if it is controlled by a majority (more than 50%) of directors, trustees, or like officials that do not deal with each other at arm’s length, or more than 50% of capital is contributed by a person, or a group of persons, not dealing with each other at arm’s length and who are involved with the private foundation.

The Paper suggests that transactions between donor-controlled charities and their associates could be required to be on arm’s length terms or prohibited outright noting in para 3.13:

“This approach was supported by the Tax Working Group in 2019, which found that the rules were private charitable foundations in New Zealand appeared to be unusually loose. The group recommended that the government considering removing tax concessions for private controlled foundations or trusts that do not have arm’s length, governance or distribution policies.”

Apart from citing the Canadian approach the Paper considers the approach to this issue in Australia, the United Kingdom and the United States. It suggests there should be a minimum distribution rule to deal with the question of the time lag between the charity and a donor claiming a benefit and the actual public benefit accruing from the distribution.

Taxing membership fees?

Chapter 4 considers integrity and simplification. This section has already attracted some media comment because it raises the possibility of taxing membership fees which could affect as many as 9,000 not-for-profit organisations.

At issue is the concept of mutuality and member transactions. Generally speaking, most not-for-profit organisations are treated as mutual associations. That includes many clubs, societies, trade associations, professional regulatory bodies.

Up until the early 2000s Inland Revenue’s guidance was that mutual associations were not liable for income tax from transactions with their members, including membership subscriptions and levies. Inland Revenue has withdrawn that advice and has drafted a replacement operational statement which will be released pending what feedback it receives on this Issues Paper.

The impact of Inland Revenue’s revised position would be that trading and other normally taxable transactions with members, including some subscriptions, would be deemed to be taxable income regardless of whether the common law principle of mutuality would apply. The Paper notes that most not-for-profits would not qualify for mutual treatment anyway, because their constitutions will prohibit distribution of surpluses to members including on winding up. This prevents the necessary degree of mutuality required.

Fringe Benefit Tax exemption under review

Finally, the paper touches on the FBT exemption for charities, which has been available since 1985. The paper notes “there are weak efficiency grounds for continuing this exemption” which “lacks coherence”. Inland Revenue is currently reviewing FBT generally and these comments suggest the FBT not-for-profits exemption is likely to go.

Submissions are open on the Issues Paper now, and close on the very unhelpful date it has to be said, of 31st March, when we’re all rather tied up with tax year-end issues. Notwithstanding that I expect there will be plenty of submissions particularly around the potential impact of taxing membership transactions.

Meanwhile in America…

Finally, a quick update on last week’s comments in relation to my concerns about potential leaks coming out of the US Internal Revenue Service (“the IRS”), following the Department of Government Efficiency (DOGE) trawling through the IRS and every other U.S. government agency.

The update I’ve had is that the DOGE people are looking more at IRS internal processes and nothing to do with any data that the IRS has received from Inland Revenue, or any other agency. There are a number of international obligations that the US has still to meet, but no doubt some concerns will have been raised.

But as I said at the time, which I believe is almost certainly the case, IRS officials will be highly professional in making sure that that information shared by other tax authorities is not leaked, accidentally or otherwise, to outside parties.

An interesting choice…

On the other hand, the IRS is getting a new Commissioner. The nominee is William Hollis Long II, or Billy Long, who is a former Republican House of Representatives member from Missouri.

He’s a controversial pick to say the least. He’s not a tax professional, and of particular note is that he was a co-sponsor of a bill in 2015 that would have abolished the IRS and introduced a national sales tax. He is also long-time supporter of a flat income tax for the US system. It’ll be interesting to see how this plays out, and as always, we will bring you developments as they emerge.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

The just concluded UK general election was the first general election held in July since 1945, when coincidentally the Labour Party also won by a landslide ending Sir Winston Churchill’s wartime prime ministership. Before he became Prime Minister again in 1951, Churchill started writing his monumental six volume history of the Second World War, the first volume of which was titled The Gathering Storm.

And if you’ll pardon the somewhat laboured analogy, this is very much what’s happening with Inland Revenue at the moment. There’s a very clear gathering storm approaching as Inland Revenue pulls together and beefs up its investigation resources. We saw signs of this a couple of weeks back with its commentary about targeting smaller liquor outlets. Now last Wednesday, an Inland Revenue media release announced it is “honing in on customers who are actively dealing in crypto assets but not declaring income from them in their tax returns.”

By way of background, back in 2020, Inland Revenue updated its guidance on the tax treatment of crypto assets. Clearly that was part of a plan to follow through and check on who was trading and investing in crypto but not reporting the income. However, first COVID and then the cost-of-living crisis got in in the way of Inland Revenue’s intentions to follow through up its guidance.

Targeting non-compliance

But those immediate crises have passed now, and it appears that Inland Revenue has been busy investigating potential non-compliance because according to the media release late last year, it wrote to “a group of high-risk customers and gave them the chance to fix any non-compliance issues before facing audit.” This is a standard tactic of Inland Revenue. It basically puts it out to taxpayers without being too specific that it is aware of potential non-compliance and “invites”, that is the terminology used, the taxpayers involved to come forward and make a voluntary disclosure. If the taxpayers do so, then the potential to be charged shortfall penalties is likely to be greatly reduced.

Following on from these “invitations”, the next stage if the taxpayers don’t come forward is directly targeted follow up action. This appears to have just happened, as Inland Revenue is saying it has “just sent another round of letters to those Inland Revenue believes are not complying.

According to Inland Revenue it has data which has enabled it to identify “227,000 unique crypto asset uses in New Zealand undertaking around 7 million transactions with a value of about $7.8 billion.” There’s a potentially sizable sum of tax on the line here.

Pay up, or else…

The media release continues with a rather veiled threat

“Cryptoasset values have reached new highs, so now is a good time for people to think seriously about tax on their crypto asset activity. The high value also means customers are well positioned to pay their tax for the 2024 tax year and earlier.”

In other words, Inland Revenue is saying as values have recovered that means taxpayers can’t plead poverty when it comes to paying the tax due on their profits.

The media release goes on to explain something that we’ve said frequently; Inland Revenue has more data available to it than people realise.

“We want customers and tax agents to know that we are stepping up our compliance activity for customers with cryptoassets. Despite popular thinking – people are not invisible on blockchain and we have the tools and analytics capabilities to identify and expose cryptoasset activities.”

So there it is, very clearly stated ‘We know more than you think we know and we are coming for you.’ Part of this, by the way, is that New Zealand and therefore Inland Revenue has signed up to the new Crypto-Asset Reporting Framework (CARF) recently developed by the Organisation for Economic Cooperation and Development. This is yet another example of the growing international cooperation on the exchange of information, a regular topic on this podcast.

Under CARF the first set of reporting is due to apply from the 2026/27 tax year which will lead through to increased tax revenue. In fact, according to the Budget, the expectation is that CARF will deliver $50 million of additional tax revenue in the June 2028 year..

That’s in the future. What’s happening right now is that Inland Revenue has used its existing network of information exchanges and data sharing almost certainly by tax treaty partners such as Australia, the UK and the US, to obtain data about transactions carried out by New Zealand based crypto-asset investors and traders. It’s now going to put the squeeze on those it considers non-compliant.

It’ll be interesting to see what comes out of it and we will watch with interest and bring you news of developments. In the meantime you have been warned and this is of course the latest sign of the gathering storm of Inland Revenue investigations.

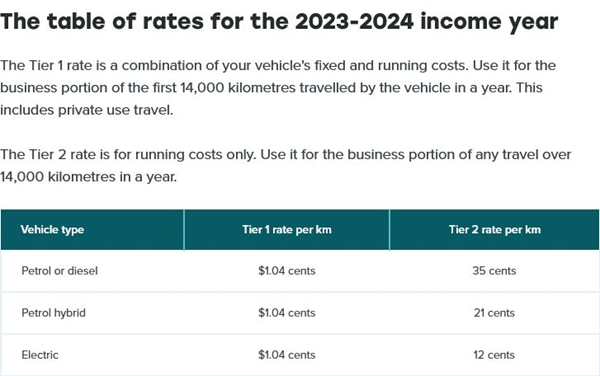

Inland Revenue kilometre rates for 2023-24

Moving on, Inland Revenue has just published its kilometre rates for the 2023-2024 income year. Unsurprisingly, given the recent rise in fuel prices, the so-called tier one rates show an increase in vehicle running costs that are allowable for the year. These rates may be used to calculate the deductible running costs for a vehicle.

Note that the Tier 1 rate of $1.04 for the first 14,000 kilometres applies to all vehicles whether petrol, diesel, hybrid or electric. The Tier 2 rates above the first 14,000 km DO vary between vehicle type.

This is good to know, but I do wonder whether it might be a bit more useful to have this sort of information earlier in the relevant tax year. Inland Revenue obviously wants to be accurate, but a different approach perhaps might be to adopt an interim rate and index that for inflation. Anyway, these are the rates that are now applicable for the 2023-24 tax year if you wish to claim the relevant deduction.

Are we raising enough tax?

And finally, this week, the Tax Policy Charitable Trust held an event on Thursday last night to announce its four finalists for this year’s Tax policy scholarship prize. The first half of the event was a panel discussion on New Zealand’s tax revenue sufficiency. Ably chaired by Geof Nightingale, a member of the last two Tax Working Groups, the four panellists that joined him were Talia Harvey and Matt Wooley, joint winners of the scholarship prize in 2017, Nigel Jemson, the winner in 2020 and Vivian Lei, the winner in 2022. You may recall Vivien, have previously been a guest on the podcast.

L-R Matt Woolley, Geof Nightingale, Vivien Lei, Talia Harvey and Nigel Jemson

Now, this was a fascinating panel discussion conducted under Chatham House rules, focusing on the scale of fiscal challenges for the next few decades and how could we meet those? Does this mean for example, some new taxes might be required such as capital gains tax? What about boosting Inland Revenue’s investigation efforts? And then on the spending side of the equation what do we do about rising health care and superannuation costs? Do we perhaps increase the age for eligibility or (re)introduce some forms of mean testing for New Zealand Superannuation? All these points were raised for discussion.

The panel discussed ‘the tax gap’, the gap between what we think the tax collection should be and what’s not being collected. There’s a lot of work to be done in this space, because we really don’t have a clear handle on the extent of this particular issue. Some work carried out several years ago by Inland Revenue suggested that when you look at the consumption patterns between self-employed persons and employees, there might be as much as a 20% gap. In other words, self-employed people appear to have about 20% higher levels of consumption than employees on ostensibly similar levels of income. This is a topic which actually might be worth a podcast episode in itself.

And the finalists are…

It was then followed by the announcement of the four finalists of this year’s Tax Policy Charitable Trust scholarship prize. Every two years the Tax Policy Charitable Trust invites young professionals (anyone under 35 on 1 January 2024) to submit proposals for review, improving any aspect of New Zealand’s tax system. Entrants submit a 1500 word overview proposal on any part of the tax system from which the judges choose four finalists will be selected to go through for the final main scholarship prize, which is worth $10,000.

Submissions are judged for their creativity, original thinking and sound and reasoned research and analysis. In addition the judges take the following factors into consideration:

Impact on the New Zealand economy, including GDP and business growth.

Social (including distributional equity) and environmental acceptability.

Feasibility of introduction, including political and public acceptability.

Impact on simplicity of tax system.

Ease of administration by taxpayers and Inland Revenue, or other relevant government agencies, and impact on compliance costs.

This year, there were 17 entrants and the four finalists chosen are

Matthew Handford, who proposes an Independent Tax Law Commission aimed at improving the Generic Tax Policy Process, or GTPP. The GTPP is a cornerstone of tax policy and is internationally well regarded, but it’s now 30 years old, so is due a reconsideration. I look forward to hearing more about Matthew’s proposal.

Claudia Siriwardena, who is suggesting a simplified FBT regime for small and medium enterprises. This gets a big tick from me, and I’m very interested in hearing more about this one.

Matthew Seddon, who proposes extending the independent contractor withholding tax regime. Mathew’s suggestion picks up the point just raised about the tax gap and deals with it by improving compliance. Again, another interesting proposal.

Finally, Andrew Paynter who is putting forward a proposal to increase the GST rate from GST but also tackle the regressivity of GST with a rebate for low and middle income earners. I’ve seen some international papers on this particular topic, so I’m very, very interested to hear more about what Andrew’s proposing here.

My intention is to get all four scholarship finalists on the podcast to talk about their ideas before the winner is announced in October, so stay tuned for developments. In the meantime, congratulations to Matthew, Claudia, Matthew and Andrew and to everyone else who entered. No doubt there were some interesting ideas put forward that did make the cut this time, but overall, it’s a great sign of the healthy state of tax policy debate in New Zealand.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

(Originally loaded to Soundcloud 6 July 2024. On interest.co.nz 8 July 2024).

The just concluded UK general election was the first general election held in July since 1945, when coincidentally the Labour Party also won by a landslide ending Sir Winston Churchill’s wartime prime ministership. Before he became Prime Minister again in 1951, Churchill started writing his monumental six volume history of the Second World War, the first volume of which was titled The Gathering Storm.

And if you’ll pardon the somewhat laboured analogy, this is very much what’s happening with Inland Revenue at the moment. There’s a very clear gathering storm approaching as Inland Revenue pulls together and beefs up its investigation resources. We saw signs of this a couple of weeks back with its commentary about targeting smaller liquor outlets. Now last Wednesday, an Inland Revenue media release announced it is “honing in on customers who are actively dealing in crypto assets but not declaring income from them in their tax returns.”

By way of background, back in 2020, Inland Revenue updated its guidance on the tax treatment of crypto assets. Clearly that was part of a plan to follow through and check on who was trading and investing in crypto but not reporting the income. However, first COVID and then the cost-of-living crisis got in in the way of Inland Revenue’s intentions to follow through up its guidance.

Targeting non-compliance

But those immediate crises have passed now, and it appears that Inland Revenue has been busy investigating potential non-compliance because according to the media release late last year, it wrote to “a group of high-risk customers and gave them the chance to fix any non-compliance issues before facing audit.” This is a standard tactic of Inland Revenue. It basically puts it out to taxpayers without being too specific that it is aware of potential non-compliance and “invites”, that is the terminology used, the taxpayers involved to come forward and make a voluntary disclosure. If the taxpayers do so, then the potential to be charged shortfall penalties is likely to be greatly reduced.

Following on from these “invitations”, the next stage if the taxpayers don’t come forward is directly targeted follow up action. This appears to have just happened, as Inland Revenue is saying it has “just sent another round of letters to those Inland Revenue believes are not complying.

According to Inland Revenue it has data which has enabled it to identify “227,000 unique crypto asset uses in New Zealand undertaking around 7 million transactions with a value of about $7.8 billion.” There’s a potentially sizable sum of tax on the line here.

Pay up, or else…

The media release continues with a rather veiled threat

“Cryptoasset values have reached new highs, so now is a good time for people to think seriously about tax on their crypto asset activity. The high value also means customers are well positioned to pay their tax for the 2024 tax year and earlier.”

In other words, Inland Revenue is saying as values have recovered that means taxpayers can’t plead poverty when it comes to paying the tax due on their profits.

The media release goes on to explain something that we’ve said frequently; Inland Revenue has more data available to it than people realise.

“We want customers and tax agents to know that we are stepping up our compliance activity for customers with cryptoassets. Despite popular thinking – people are not invisible on blockchain and we have the tools and analytics capabilities to identify and expose cryptoasset activities.”

So there it is, very clearly stated ‘We know more than you think we know and we are coming for you.’ Part of this, by the way, is that New Zealand and therefore Inland Revenue has signed up to the new Crypto-Asset Reporting Framework (CARF) recently developed by the Organisation for Economic Cooperation and Development. This is yet another example of the growing international cooperation on the exchange of information, a regular topic on this podcast.

Under CARF the first set of reporting is due to apply from the 2026/27 tax year which will lead through to increased tax revenue. In fact, according to the Budget, the expectation is that CARF will deliver $50 million of additional tax revenue in the June 2028 year..

That’s in the future. What’s happening right now is that Inland Revenue has used its existing network of information exchanges and data sharing almost certainly by tax treaty partners such as Australia, the UK and the US, to obtain data about transactions carried out by New Zealand based crypto-asset investors and traders. It’s now going to put the squeeze on those it considers non-compliant.

It’ll be interesting to see what comes out of it and we will watch with interest and bring you news of developments. In the meantime you have been warned and this is of course the latest sign of the gathering storm of Inland Revenue investigations.

Inland Revenue kilometre rates for 2023-24

Moving on, Inland Revenue has just published its kilometre rates for the 2023-2024 income year. Unsurprisingly, given the recent rise in fuel prices, the so-called tier one rates show an increase in vehicle running costs that are allowable for the year. These rates may be used to calculate the deductible running costs for a vehicle.

Note that the Tier 1 rate of $1.04 for the first 14,000 kilometres applies to all vehicles whether petrol, diesel, hybrid or electric. The Tier 2 rates above the first 14,000 km DO vary between vehicle type.

This is good to know, but I do wonder whether it might be a bit more useful to have this sort of information earlier in the relevant tax year. Inland Revenue obviously wants to be accurate, but a different approach perhaps might be to adopt an interim rate and index that for inflation. Anyway, these are the rates that are now applicable for the 2023-24 tax year if you wish to claim the relevant deduction.

Are we raising enough tax?

And finally, this week, the Tax Policy Charitable Trust held an event on Thursday last night to announce its four finalists for this year’s Tax policy scholarship prize. The first half of the event was a panel discussion on New Zealand’s tax revenue sufficiency. Ably chaired by Geof Nightingale, a member of the last two Tax Working Groups, the four panellists that joined him were Talia Harvey and Matt Wooley, joint winners of the scholarship prize in 2017, Nigel Jemson, the winner in 2020 and Vivian Lei, the winner in 2022. You may recall Vivien, have previously been a guest on the podcast.

Now, this was a fascinating panel discussion conducted under Chatham House rules, focusing on the scale of fiscal challenges for the next few decades and how could we meet those? Does this mean for example, some new taxes might be required such as capital gains tax? What about boosting Inland Revenue’s investigation efforts? And then on the spending side of the equation what do we do about rising health care and superannuation costs? Do we perhaps increase the age for eligibility or (re)introduce some forms of mean testing for New Zealand Superannuation? All these points were raised for discussion.

The panel discussed ‘the tax gap’, the gap between what we think the tax collection should be and what’s not being collected. There’s a lot of work to be done in this space, because we really don’t have a clear handle on the extent of this particular issue. Some work carried out several years ago by Inland Revenue suggested that when you look at the consumption patterns between self-employed persons and employees, there might be as much as a 20% gap. In other words, self-employed people appear to have about 20% higher levels of consumption than employees on ostensibly similar levels of income. This is a topic which actually might be worth a podcast episode in itself.

And the finalists are…

It was then followed by the announcement of the four finalists of this year’s Tax Policy Charitable Trust scholarship prize. Every two years the Tax Policy Charitable Trust invites young professionals (anyone under 35 on 1 January 2024) to submit proposals for review, improving any aspect of New Zealand’s tax system. Entrants submit a 1500 word overview proposal on any part of the tax system from which the judges choose four finalists will be selected to go through for the final main scholarship prize, which is worth $10,000.

Submissions are judged for their creativity, original thinking and sound and reasoned research and analysis. In addition the judges take the following factors into consideration:

Impact on the New Zealand economy, including GDP and business growth.

Social (including distributional equity) and environmental acceptability.

Feasibility of introduction, including political and public acceptability.

Impact on simplicity of tax system.

Ease of administration by taxpayers and Inland Revenue, or other relevant government agencies, and impact on compliance costs.

This year, there were 17 entrants and the four finalists chosen are

Matthew Handford, who proposes an Independent Tax Law Commission aimed at improving the Generic Tax Policy Process, or GTPP. The GTPP is a cornerstone of tax policy and is internationally well regarded, but it’s now 30 years old, so is due a reconsideration. I look forward to hearing more about Matthew’s proposal.

Claudia Siriwardena, who is suggesting a simplified FBT regime for small and medium enterprises. This gets a big tick from me, and I’m very interested in hearing more about this one.

Matthew Seddon, who proposes extending the independent contractor withholding tax regime. Mathew’s suggestion picks up the point just raised about the tax gap and deals with it by improving compliance. Again, another interesting proposal.

Finally, Andrew Paynter who is putting forward a proposal to increase the GST rate from GST but also tackle the regressivity of GST with a rebate for low and middle income earners. I’ve seen some international papers on this particular topic, so I’m very, very interested to hear more about what Andrew’s proposing here.

My intention is to get all four scholarship finalists on the podcast to talk about their ideas before the winner is announced in October, so stay tuned for developments. In the meantime, congratulations to Matthew, Claudia, Matthew and Andrew and to everyone else who entered. No doubt there were some interesting ideas put forward that did make the cut this time, but overall, it’s a great sign of the healthy state of tax policy debate in New Zealand.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

In last week’s Sunday Star Times, Miriam Bell looked at the question of how New Zealand’s taxation of property compares with other jurisdictions.

In doing so, she spoke to myself, Robyn Walker of Deloitte, and John Cuthbertson, the tax director for Chartered Accountants Australia and New Zealand. We all gave differing takes on the position.

According to the OECD statistics, we are near the bottom end of the range as a percentage of GDP. Including local government rates, New Zealand’s taxes on property for 2020 was approximately 1.9% of GDP and the total tax take for the year of 32.18% of GDP. By comparison, Australia’s taxes on property was 2.718% of GDP (2019 numbers), the UK was 3.855% and Canada 4.15% of GDP (both 2020 numbers).

As you can see, Canada and the UK are significantly above New Zealand. One of the reasons for this, as Robyn and John pointed out, is that they have a range of stamp duties that may apply. But also, as we all pointed out, all three jurisdictions, Australia, Canada and the UK, also have capital gains tax and in the case of the UK, inheritance tax may also apply on some properties on transfer.

The article provoked a fairly lively debate, as you would expect. The range of views across the board is that, yes, it looks like we’re under taxed. But the bright-line test is in place which is problematic in that although it looks like a capital gains tax, it doesn’t apply comprehensively, unlike in the other three jurisdictions.

Robyn Walker then made a very good point following through that the design of the bright-line test is basically all or nothing. If you hold property for more than 10 years, you’re outside the test, which means that you’re likely not to be taxed on it. So you get this wide variance in the tax effect of sales or property, which you don’t see to the same extent in other jurisdictions.

Robyn subsequently did a nice little post on LinkedIn, in which she looked at what would be the tax consequences in Australia, Canada, the UK, and New Zealand for the sale of a property which realised a $100,000 gain. Because we treat it as income, we’ll tax the full gain at the relevant marginal rate and for the purpose of the example that was 33%. Canada and Australia will tax only half the gain at the relevant marginal rate, although non-residents in Australia will be taxed on the full gain. And although the UK will tax the full gain the top rate applicable is 28%.

The end result was that if the bright-line test applied, then the tax payable in New Zealand would be highest relative to the other three jurisdictions. But if the bright-line test didn’t apply, then it was the lowest. In fact, it would be nil. And this reinforces Robyn’s point that it is a poorly designed test which can be very unfair in its application. You hold a property for nine years and 363 days, you’re taxed. Hold it for 10 years and one day you’re probably not.

The point I stressed in the article is that we want to look at broadening the range of taxation, and it’s fair if we do so because we start to get round these arbitrary distinctions. As I’ve previously said, my preferred methodology for expanding the taxation of capital is that promoted by Associate Professor Susan St John and myself the fair economic return, not a transactional based capital gains tax.

Anyway, this debate will continue to run and run. Miriam Bell’s article provoked a fierce reaction on Stuff, unsurprisingly, and there’s been an interesting debate around Robyn’s LinkedIn article. I urge you to take a look at that.

I think we really do need to address the issue of taxing property particularly when you consider what the Infrastructure Commission said earlier this week about property owners benefiting to the extent of house prices being 69% higher than they would have been without actions being taken to restrict the supply of housing. Housing and the taxation of property is a touchpoint now and will be in next year’s election. We’re going to see plenty more of this debate

Taxes on crypto assets are coming

Moving on to another controversial asset class – crypto assets. Now the value of crypto assets has just simply exploded in the last 10 years. Because of the explosion of the value, it has forced its way onto the tax agenda and tax authorities all around the world are looking to see how this new asset class fits in with their existing rules. New Zealand is no different from other jurisdictions which are all struggling with this. The recent tax bill that was passed last week, by the way, had provisions relating to the application of GST on crypto-assets.

A couple of weeks back, the OECD released a public consultation document proposing a new tax transparency framework for crypto assets. What it has identified is that crypto assets can be transferred and held without going through the normal financial intermediaries, such as banks, and fund managers. And from a tax perspective, there’s no central administrator having what the OECD calls full visibility on either the transactions carried out or on the location of crypto asset holdings.

It also appears that malware attacks and ransomware attacks, payments are increasingly demanded in crypto-assets, which are largely untraceable. So that’s obviously a matter of concern to not just tax authorities.

The OECD paper also points out that some new paid payment products. Such as digital money products and central bank digital currencies, which also provide electronically storage and payment functions similar to money held in traditional bank accounts.

But at the moment, none of these are covered by the Common Reporting Standard on the Automatic Exchange of Information. A reminder the Common Reporting Standard is an agreement between almost 100 jurisdictions where they agree to swap information on financial accounts held in their country by citizens or tax residents of another jurisdiction. It’s been a huge step forward in tackling adn improving tax transparency and tackling tax evasion.

And what the OECD is proposing is, it wants to develop a new global tax transparency framework, which will involve the same reporting for transactions related to crypto assets as for financial assets covered by the Common Reporting Standard. And it’s calling this the Crypto Asset Reporting Framework, or CARF. The paper proposes that the following types of transactions involving crypto assets will be reportable under the CARF:

exchanges between crypto assets and fiat currencies;

exchanges between one or more forms of crypto assets;

reportable retail payment transactions; and

transfers of crypto assets.

This would bring about a very significant change in the crypto asset world as a result. It will basically be bringing the whole crypto asset world in line with other reportable transactions under the existing Common Reporting Standard framework. I doubt that will be very popular with investors in the crypto world, but it certainly will be for tax authorities and other authorities, such as financial regulators and police, as they deal with the implications of the arrival of this asset class. Consultation is now open on the document through until 29th April.

Same old problem returns

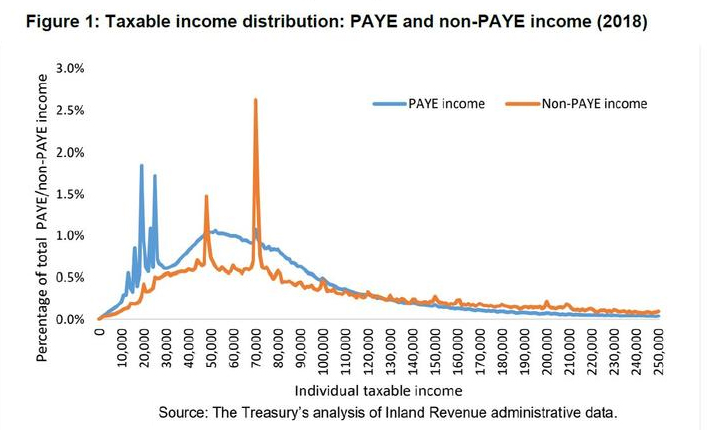

And finally, this week, a couple of weeks ago I discussed the new Inland Revenue consultation paper on countering attempted top tax rate avoidance. It so happens that yesterday RNZ had a story on the paper and Inland Revenue’s concerns that “structures may be being used to reduce incomes below $180,000.”

Inland Revenue has provisionally estimated that income from these high earners will be down $2.88 billion, or about 14% from the year prior. This is on the basis that the average self-employed person – who has the most control over their income – might declare 13% less income than they did the year before, to drop from $191,000 to $166,000 (and by happy coincidence below the $180,000 threshold). The number of PAYE earners is expected to reduce, and also declare lower incomes, from an average of $228,000 to $217,000.

If that is happening then I would expect Inland Revenue to react aggressively. On the other hand, Inland Revenue has known for some time that self-employed income spikes around the $48,000 mark (the threshold when the tax rate increases from 17.5% to 30% and $70,000 dollars when the threshold tax rate increases to 33%). I’m not yet aware of increased Inland Revenue investigation activity into such apparent income manipulation. It seems to me that although Inland Revenue has concerns about manipulation involving the new 39% tax rate, what appears to be happening around the $48,000 and $70,000 thresholds seems very blatant.

The RNZ report included a chart from Inland Revenue of the taxable income distribution for the 2018 income year which illustrated these spikes occurring at the $48,000 and $70,000 thresholds.

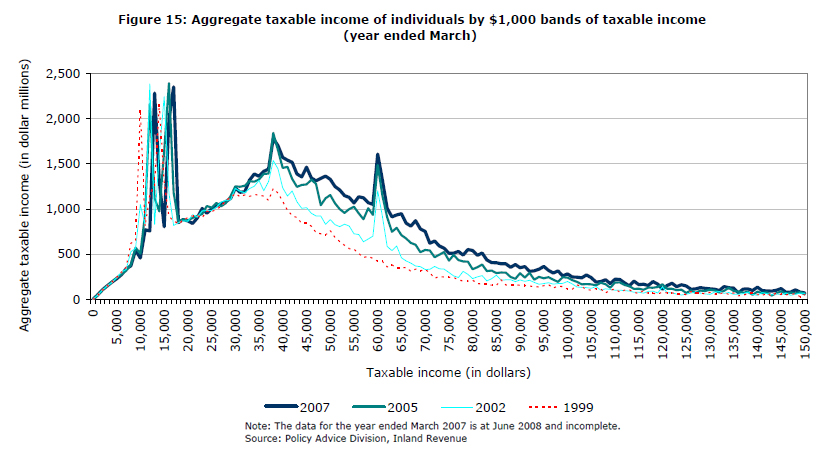

The graph mirrors one produced in 2008 (when the top tax rate was 39%). You can see exactly the same pattern of income spikes around $38,000, the threshold at which the tax rate increased from 19.5% to 33% and then at $60,000 when the tax rate rose from 33% to 39%.

In other words this is a very longstanding problem and the question arises why that issue has been allowed to continue? Does Inland Revenue have the resources to address it? They most certainly will say they do, and they would also probably say that they have had a lot to deal with managing the COVID-19 response over the last two together with finalising the Business Transformation project. Either way you should expect action on this from Inland Revenue.

Incidentally on the question of high tax rates, another news report covered the effect of increases for working for families tax credits. It pointed out that the effective marginal tax rate for recipients of working for families can in some cases be 57%. This is the combination of 30% tax rate on incomes over $48,000 and the 27 cents in the dollar abatement, which applies above a threshold of $42,700.

So before people start complaining about 39% being a very high tax rate, think about what’s going on with working for families, accommodation supplement and other social welfare payments. It’s quite conceivable that someone on $60,000 per annum, receiving working for families with a student loan could have a marginal tax rate on every dollar earned of 69%. This represents 30% income tax, 27 cents on the dollar abatement on their working for families and 12% student loan repayments.

By the way, the $42,700 threshold when the working for families’ abatement kicks in is now, by my calculations, less than the annual income of someone working 40 hours a week on the current minimum wage would earn. It’s another case of where governments have allowed inflation to quietly increase the tax take with worse consequences for people at the lower end of the scale. Yet another issue we’ve talked about repeatedly.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.