Budget Day lockup is a mad frenzy of activity as you basically have three and half hours to sift through a massive information dump, determine the key points and write something for release at 2PM when the Budget is officially released.

Surprisingly, in the midst of all the information provided, you don’t get copies of any accompanying legislation, bill commentary and Regulatory Impact Statements that will be also released at 2PM. Therefore, those of us who are in the Budget Lockup are a still little bit blind as to the full details of the Budget initiatives. Because of this I increasingly view the Budget Lockup as an interesting experience, a good opportunity to interact with Treasury officials, because you can actually ask for specific information and an opportunity to perhaps quiz the Minister of Finance on some points.

Budget Day – just a government showpiece?

On the other hand, it is increasingly clear from the run up to Budget Day that the budget itself is very much a set piece for the government of the day to boost specific Budget initiatives and narratives. Any detailed analysis on the day is swamped by all the good or bad news about the state of the economy or who’s getting extra or reduced funding. It’s not really until the week following the Budget that you start to get some detailed analysis of what is in the budget and the potential implications.

Investment Boost – a real boost to productivity or just meh?

On Budget Day the Investment Boost proposal was well received, but as people looked into the detail some concerns have emerged. What the measure does is essentially accelerate the depreciation which would have been claimed on these assets. This is done by way of an immediate 20% deduction with the remaining 80% of the asset expenditure depreciated as normal. My initial reaction was to recall the First Year Allowances I used to deal with when I was working in the UK and which operated in a similar fashion.

The twist is last year the Government removed depreciation on commercial buildings, including factories, to pay for its tax cuts. But this year commercial buildings are included in those groups of assets that are able to qualify for the Investment Boost. This about-face has prompted Andrea Black the former independent advisor to the last Tax Working Group, and a previous a guest on the podcast to write an op-ed in The Post about the Investment Boost initiative. In summary, she argues if we are trying to boost productivity, then Investment Boost is a step in the right direction but is not the productivity game changer that is being promoted.

New Zealand is an outlier, again

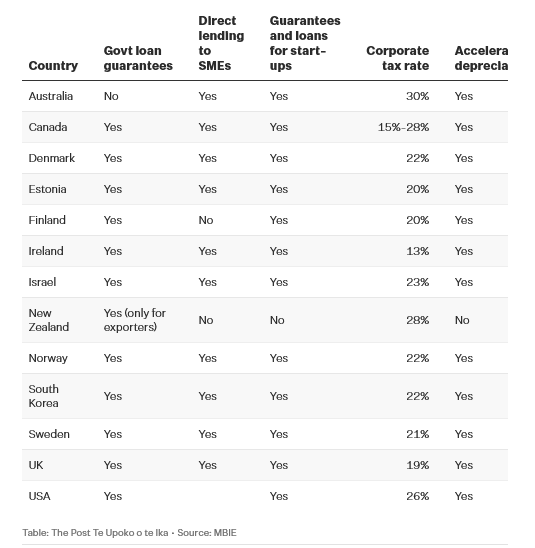

Andrea is critical that the Investment Boost initiative does include commercial property and notes that our labour productivity is poor and that direct assistance in terms of accelerated depreciation – which she strongly supports – doesn’t really exist for many New Zealand manufacturers. She includes a very telling graph put together based on information obtained under the Official Information Act from the Ministry of Business, Innovation and Employment about how other countries subsidise business, including through tax breaks and government loan guarantees.

As can be seen we only grant government loan guarantees for exporters, in contrast to most other countries in the OECD. Similarly, we and Finland are the only countries which do not provide direct government lending support to small and medium enterprises. The United States, for example, has the Small Business Administration, and this initiative was something we looked at when I was on the Small Business Council back in 2018-2019. I thought then, and still do, that the lack of government financial support for our SME sector is something we really need to address.

A step in the right direction but…

As Andrea notes until Investment Boost New Zealand had no accelerated depreciation which meant we were very much out of line with other jurisdictions. So the Investment Boost initiative is a step in the right direction even if it perhaps could have gone further. I have little doubt Investment Boost will have an effect on investment, like Andrea whether it will have the effect the government is hoping for in boosting productivity, I’m not so sure.

I’m particularly concerned wearing my devious tax planner cap that the opportunity now exists for some clever financiers to put some property related deals together to accelerate the building of some commercial properties to obtain the 20% upfront deduction. I saw something similar happen in the UK with the former Business Enterprise Scheme, which was designed to boost startups but quickly saw property backed schemes emerge to claim the generous deductions. Anyway we shall see how this plays out over time.

Investment Boost, Fringe Benefit Tax and skewing the composition of our vehicle fleet

Incidental to this issue Newsroom published an interesting article talking about the impact of proposed changes to the Fringe Benefit Tax (FBT) regime treatment of motor vehicles. The article suggested that the Investment Boost proposal, which applies to vehicles as well, might mean that we might see a shift away from the use of double cab utes.

There’s a number of reasons that they are now so prevalent on our streets and a growing component of the vehicle fleet. One reason is that there was a perception that double cab utes qualify for the work-related vehicles exemption from FBT. The other was that manufacturers were promoting these vehicles with some highly favourable deals.

The increase in the number of double cab utes prompted Angela Hodges, from NZ Tax Desk to comment the combination of those two factors and particularly the perceived exemption has

“skewed the composition of New Zealand’s vehicle fleet over time, with tax settings influencing business-purchasing decisions in ways that probably weren’t intended”.

The Newsroom article suggests that the coming FBT changes together with the Investment Boost initiative may encourage a switch away from double cab utes to alternative vehicles. It will be interesting to see how this develops.

Inland Revenue’s “significant funding boost”– what can we expect?

Moving on and in as big a surprise as the sun will rise tomorrow, Inland Revenue was given additional permanent funding of $35 million per year to invest in tax compliance and collection activities. As the Commissioner of Inland Revenue, Peter Mersi, pointed out, “This is a significant funding boost and is recognition of what we do and the excellent results we’ve had so far this year.”

These results include for the year to 31st March 2025 assessing additional tax of $880 million from audit activity and improved debt collection activities, with just under $3 billion collected in the year to date compared with $2.7 billion for the previous year. There’s also been a doubling in the number of prosecutions and a big increase in the collection of overseas student loan repayments. In my view this is a scheme that really needs a lot of re-thinking about how it’s managed.

In addition to that $35 million Inland Revenue also got an additional $29 million per year last year for compliance and debt collection. Furthermore, the Government has also agreed to continue $26.5 million of funding set to end this year. All up Inland Revenue is getting close to $90 million of funding for investigation and debt collection activities.

This should have a significant impact given the rate of return of between seven and eight dollars for each dollar invested, which has been achieved in the past. The total return from increased compliance and collection activities is therefore potentially as high as $700 million per year.

A warning and a reminder

Against this backdrop people should keep two things in mind. Firstly, as I’ve said on many previous occasions, Inland Revenue has vast resources. It receives data from many sources, and it is increasingly efficient at absorbing, analysing and acting on that data. The basic proposition you should operate on is; if you have put anything in writing anywhere, Inland Revenue will have access to that information at some point. In particular, Inland Revenue has become increasingly efficient in tracking property transactions.

The other point is in relation to tax debt. If you are behind, take action and front up to Inland Revenue. It’s much better doing so than hoping you won’t be on their radar. Being proactive will get a better result for you in the long term.

The Digital Services Tax is dead – now what?

Now at last, in the run up to the budget, the Minister of Revenue, Simon Watts, announced that the Government had decided to discharge the Digital Services Tax bill from the legislative programme. This had been introduced in 2023 by the previous Labour Government. It was really intended as a backstop to OECD’s Two-Pillar international tax initiative.

According to Mr. Watts, “we’ve been monitoring international developments and decided not to progress the Digital Services Tax bill at this time. A global solution has always been our preferred option and we have been encouraged by the recent commitment of countries to the OECD work in this area.”

The consequence of the decision is that the forecast revenues from the introduction of the Digital Services Tax will no longer be included in the Crown accounts. This represents a $476 million reduction in tax revenue over a four-year period. The question therefore arises as to what replaces this lost revenue.

Google New Zealand’s billion-dollar service fees are not unique

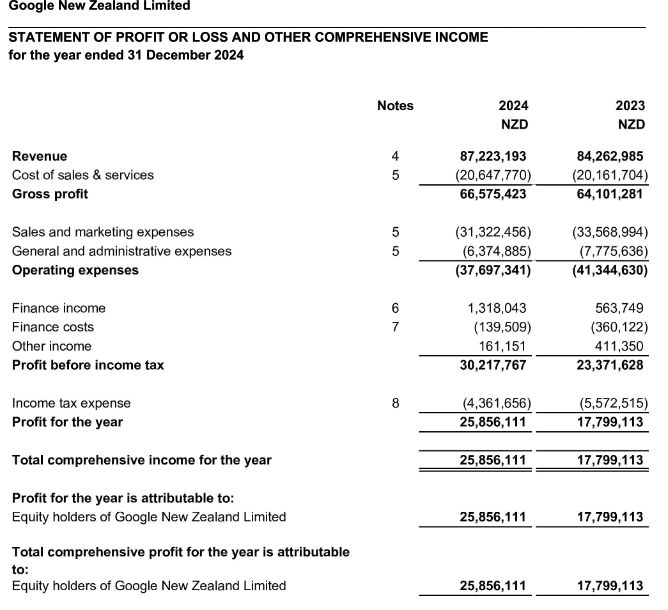

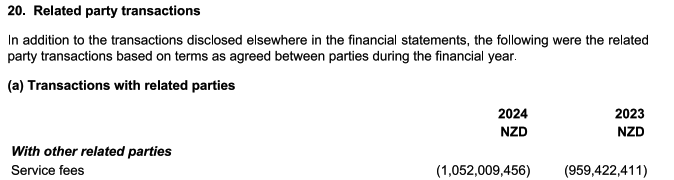

In the same week as the Budget and the announcement about the Digital Services Tax, Google New Zealand released its results for the year ended 31 December 2024.

During the year Google NZ paid $1.05 billion in service fees to related parties, almost $100 million more than in 2023.

A week or so later, Facebook New Zealand announced its December 2024 results and the amount of fees it paid to associated entities was over $150 million, roughly the same as for 2023.

Jonathan Milne of Newsroom wrote an interesting article looking at the question of the payments that were being made by all the tech companies. Taking into consideration the fees paid by Apple, Amazon, Microsoft together with Google and Facebook he estimated the annual amount of service fees being paid to associated entities was close to $4 billion. Assuming all are deductible then at the corporate income tax rate of 28% that represents over $1.1 billion of lost tax revenue.

What about the OECD Two-Pillar deal?

Now, of course, it’s more complicated than this simple calculation. But the withdrawal of the Digital Services Tax should be seen alongside what can only be described as regulatory capture in Washington by the tech giants. That in turn has led to these trade threats made by President Trump against digital services taxes and other attempts to tax the tech giants. This all means that the international Pillar One and Pillar Two proposals in which Minister of Revenue Simon Watts places great faith are practically dead in the water.

The Government therefore has a problem. Having accepted it’s not going get $476 million of revenue from the Digital Services Tax, how does it replace that lost revenue. What about the potential $4 billion of service fees going in affiliate fees, should these be subject to some questions under the transfer pricing rules? What is going to happen in that space? Will some of the roughly additional funding of $90 million discussed earlier be deployed in boosting Inland Revenue’s reviews of the transfer pricing practices of the tech companies? We don’t know, but this is an area other jurisdictions around the world are also grappling with.

In Australia at the moment some of these transfer pricing issues are involved in the PepsiCo case. The case revolves around an embedded royalties issue, basically: do some of the payments made for concentrate include some form of royalty which should be subject to non-resident withholding tax? Typically, non-resident withholding taxes for royalties are between 5% and 10% of the payment. Increased focus here may be a means of recovering some of the lost revenue from the digital services tax.

This issue of the treatment of service fees is in my view probably one of the most interesting challenges in the international tax space right now. All around the world there’s great interest in addressing this issue of transfer pricing. We’re therefore watching to see how Inland Revenue moves and, as always, we will report on developments as and when they arise.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

Could the US retaliate against a digital services tax?

Last week, in a series of interviews with the press, notably with Newstalk ZB, Finance Minister Nicola Willis dropped several hints about what might be in the forthcoming May 22nd Budget. In particular, she talked about the corporate tax rate, and the possibility of cuts to that as part of promoting the Government’s growth agenda.

Corporate tax rate above OECD average

Speaking with Heather Du Plessis-Allan, Ms Willis commented:

“Well, if you compare New Zealand with the rest of the world, we’re not as competitive as we used to be. Which is to say that our corporate tax level is reasonably high when you compare it to the rest of the developed world.”

This is a very valid point which comes up frequently in discussions. Our current company tax rate at 28% is well above the OECD average of 24% and has been out of alignment for some time.

New Zealand back in the late 80s under the Fourth Labour Government was actually at the forefront of cutting company tax rates. A particularly interesting action was to align the company tax rate with the top individual and trust rates of 33%. The three basically stayed in line until the election of the Fifth Labour Government and the increase in the top personal tax rate to 39% in 2000.

There have been a couple of corporate tax cuts over the past 15 years or so. In 2007, the rate was cut from 33% to 30% and then in 2010, as part of the rebalancing that took place under Bill English with the increase of GST from 12.5%, the corporate tax rate was cut to 28% where it remained since.

As I’ve discussed previously, there has been a long running global trend towards lower corporate tax rates. But that has slowed in recent years, first because of the effect of the Global Financial Crisis and secondly, the fiscal shock to government finances because of the COVID-19 pandemic. As a result, according to the OECD in 2023, corporate tax rates rose generally across the board. Nevertheless, we are out of sync at the headline rate level.

More to investment than the corporate tax rate and will it work?

A lower corporate tax is undoubtedly attractive. However, the tax rate needs to be seen in context with what other incentives are available. Overseas companies and investors are very focused on what else might be on the table. A lower company tax rate would certainly be attractive, so the suggestion has been met with enthusiasm by some. Others are a bit more sceptical. Economist Ed Miller noted that when the effect of the corporate tax cuts in 2007 and 2010 are considered there does not seem to be any significant increase in foreign direct investment as a result.

The last tax working group didn’t see overwhelming evidence to support the theory that lower tax cuts at lower corporate tax rate would attract investment.

Problems and an alternative

There’s a flip side to this though, and it’s tied into the Government’s intention of restoring a surplus. Our corporate tax rate is not only above the OECD average, but our corporate tax take is also high by world standards. According to OECD statistics, 14% of the total tax receipts in New Zealand for 2022 came from company tax, whereas around the OECD the average is 12%.

So, if the Government, in an attempt to boost economic growth, is going to cut the corporate tax rate, it must then look at other alternatives to replace the lost revenue. One of the things it did back in 2010 and which it has already repeated, was to remove depreciation on all buildings. Depreciation for commercial buildings was restored under Labour but then removed again from the start of the current tax year on 1st April 2024.

A counter argument to the Government’s proposal for corporate tax cuts would be that enhanced depreciation allowances, including restoration of commercial building depreciation, which would include factories, might be a more effective approach than across the board tax cut.

How to replace lost tax revenue?

But if the Government is thinking of a corporate tax cut, and that does seem to be the case, what counter measures could they take to ensure that it is not fiscally too draining on the resources? One option might be that the availability of imputation credits may be restricted. For example, it might be that you can elect to have a lower corporate tax rate, but you imputation credits are no longer available to for shareholders.

As an aside, imputation (sometimes called franking) credit regimes were very popular during the 1980s, but gradually fell out of favour over time, mainly because, or in part because the European Court ruled that imputation credits or franking credits have to be available to all shareholders resident in the EU. After the German government lost this case its response was to heavily restrict the use of franking credits.

Change the tax treatment of Portfolio Investment Entities?

Another option might be to review the taxation of portfolio investment entities held by persons with effective marginal tax rates above the 28%. To quickly recap, Portfolio Investment Entities (PIEs) have a tax rate of 28%, equal to the company tax rate, which is also the maximum prescribed investor rate for individuals. So, there is actually a tax saving opportunity for individuals whose other income is taxed above the 28% rate for PIEs.

The Government might look at this, decide that will no longer apply and instead income from PIEs will be taxed at the person’s marginal rate. That could raise sufficient sums to partially offset the effect of a lower corporate tax rate.

The Finance Minister also mentioned reforming the Foreign Investment Fund regime, which is currently being considered by Inland Revenue and made some encouraging sounds about that potentially being an option.

We shall see. No doubt there’s a lot of work going on in Treasury and Inland Revenue looking at these options. All will be revealed in the Budget on 22nd May.

A threat to our Digital Services Tax

As covered in our first podcast of the year, one of President Trump’s initial executive orders withdrew the United States from the OECD Two-Pillar international tax deal. I drew attention to the second paragraph of that Executive Order, which directed the US Treasury to consider taking actions against other jurisdictions for tax actions which are potentially prejudicial to American interests.

Vernon Small, who was an advisor to the former Minister of Revenue, David Parker, now writes a weekly column in the Sunday Star-Times has picked up on this point noting that “Treasury has budgeted to rake in $479 million between January 2026 and June 2029 from a 3% Digital Services Tax (DST) on tech giants like Google and Meta.”

This, according to Small, “is an heroic piece of forecasting given current uncertainties and the provision for delaying collections until 2030 if progress is made on a multilateral approach through the OECD.”

And then the crunch point:

“Trump has bosom buddies in high places in the industry with Elon Musk first amongst them, and Mark Zuckerberg making a play for the new US administration’s affections.

Trump has promised to retaliate against discriminatory or extra-territorial taxes aimed at US interests. So the DST could be a prime target.”

Vernon Small is underlining the potential threat to our revenue base and our sovereign right to tax. If the OECD deal does fall over there are a number of countries including Canada, no longer America’s best friend, it seems, with DSTs ready to go. So there’s a whole potential for a tax war.

The Trump threat to tax administration

But equally worryingly, coming out of the United States is something about the question of bureaucratic independence from the executive. This might sound an arcane issue but it’s actually quite important to the independence of tax authorities.

One of the first actions of the Trump administration was to sack 17 Federal Inspectors-general. There’s also a move to put all Federal Government employees on the basis that they serve at the pleasure of the President. This would mean that an employee could be fired without the need for cause as the American terminology puts it.

Project 2025’s Schedule F

The implications of this have been picked up by Francis Fukuyama, the author of the famous The End of History essay written in the wake of the collapse of the Soviet Union and the end of the Cold War.

Writing for the Persuasion Substack under the title Schedule F is Here (and it’s much worse than you thought) Fukuyama wrote:

‘ “For cause” protection means that the official cannot be removed except under specific and severe conditions, like committing a crime or behaving corruptly. And now many individuals have been moved, in effect, to Schedule F because they are said to serve at the pleasure of the President.

Consider what this may mean if Trump hand picks a new Internal Revenue Service chief, that individual can be pressured by the Government to order audits of journalists, CEOs, NGOs and NGO leaders. Removal of Inspectors General will cripple the public’s ability to hold his administration accountable.’

Trump’s decision to move all Federal employees to Schedule F status is a step towards autocracy. What perhaps we all need to keep in mind is that the separation between the Commissioner of Inland Revenue and the Minister of Revenue is actually incredibly important. Yes, at times the Inland Revenue might do something which probably might embarrass the Minister of Revenue, but he cannot directly intervene in Inland Revenue’s operations.

A key part of a well-functioning democracy is that civil servants can act independently from their nominally political superiors. Fukuyama is right to say we should therefore have some concern coming at what’s happening in, in the United States because it does seem to be centralising power very rapidly around the President. The .potential for mischief is therefore enhanced as a result, and don’t think that such a step ultimately doesn’t have tax consequences.

Latest on the changes to the United Kingdom ‘non-dom’ regime

On a more positive note, last year I discussed the changes to the so-called ‘non-dom’ regime in the United Kingdom. This is where persons who are not domiciled in the UK have a special basis of taxation. Basically, they’re not taxed on income and gains which are not remitted to the UK.

This is a significant concession which is ending with effect from 5th April this year when it will be replaced by something which is more akin to our transitional resident’s exemption. This is pretty important for the approximately 300,000 Britons like me who’ve migrated here, plus the significant number of Kiwis who have assets in the UK or family going to the UK but have retained assets here. All of this group are potentially within the scope of these reforms.

There’s been a fair amount of push back on the reforms together with concerns that there will be a flight effect as wealthy, ‘Non-doms’ leave the UK. The UK Labour Government has been under pressure to make some changes to the proposals.

In response, the Chancellor of the Exchequer (Finance Minister) Rachel Reeves announced a concession (ironically at the gathering of the super-wealth at Davos) which will increase what’s called the temporary repatriation concession.

This concession will allow non-doms a three year window to pay a temporary repatriation charge on designated foreign income and capital gains so that they can subsequently be remitted to the UK without any further tax. The temporary repatriation charge will initially be 12% before rising eventually to 15% in the year ended 5th April 2028. For comparison, without the concession remitted income would be taxed at rates up to 45% and remitted capital gains would be subject to capital gains tax at 24%.

There’s a lot of opportunity here for potential tax savings for those who could be affected or will be affected by the proposed change to the non-dom regime. We’re still working through all of the implications but we will be updating our clients and bringing you developments as they arise.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

It’s been a busy week in the tax world. The Taxation Principles Reporting Bill passed its third reading in Parliament and very shortly will receive the Royal assent. Now this was the bill introduced at the time of the May Budget, the purpose of which was to provide a statutory reporting framework and required the Commissioner of Inland Revenue to provide the Minister of Revenue with an annual report on the operation of the tax system.

This report would outline aspects of the tax system against a set of tax principles such as equity, efficiency and certainty. As commentary provided by Inland Revenue to the Finance Expenditure Committee noted. “These principles are often considered when designing changes to a tax system”.

Tax being political the Government also wants this bill to

…help improve the public’s understanding of the tax system and encourage informed debate about its future. New Zealand has seen several Tax Working Groups and Committees over the last 20 years, with the most recent being the 2019 Tax Working Group These reviews have offered useful insights into the operation of the tax system and suggestions for improvement. These reviews have also highlighted areas of the tax system where information is lacking, which makes a fully informed debate on some aspects of the tax system more difficult.

The bill requires the Commissioner of Inland Revenue to prepare and publish an annual report which considers the tax system measured against the principles included in this bill.

What will happen is Inland Revenue will produce a short form report annually with a full report every three years. The first full report will be produced in 2025 with the shorter version reports produced in the interim years starting later this year. The intention is to align the requirement for this report to be produced the second calendar year of each parliamentary term.

There’s been some discussion around whether we need this bill and how does it sit within the Generic Tax Policy Process (GTPP)? You could say it’s an extension of the GTPP and of course, it does mean that we can have a look at some of the tax policies that have been put out by the various parties and compare them against the principles set out in this bill. And I’ll be doing that a little later on. The politicians may find this new bill is something of a double edged sword.

A Digital Services Tax just in case…

It so happens a digital services tax bill was introduced on the last sitting day of this parliamentary term which is a bit of a surprise. Digital services taxes (DST) have been talked about for some time but have generally not been brought into effect. They’re obviously not favoured by the targets, the digital giants such as Google and Facebook. But they are a tool that many governments around the world have been considering implementing.

The ongoing OECD Pillar One and Pillar Two negotiations are intended to eliminate the need for these taxes. In fact, it’s a condition of the introduction of the OECD model that any digital services tax in effect would be repealed.

The Government’s actually been looking at a DST for some time. There was a discussion document back in 2019 on the topic. That said, it still was a bit of a surprise to see this bill pop up at this particular time. Arguably, you could see it as a bit of politicking. The key thing is the Government is already committed to not introducing a DST until 1st January 2025 at the earliest. Now Inland Revenue and Treasury have said it will be handy to have the legislation ready just in case the OECD deal falls over. So that’s a reason given for this bill being introduced now.

The DST would target multinational multinationals with global revenue in excess of €750 million per year from digital activities and New Zealand revenue from these activities which exceeds $3.5 million per year. The DST taxes the revenues rather than the profits, because then it doesn’t require trying to establish a connection with a multinational’s physical presence in New Zealand. The rate to be proposed is 3%, pretty standard compared with others around the world.

This bill is a more fallback measure and it’s interesting to see where it stands that they’ve made this move now. But many countries have DSTs, Britain is one, France another and India is probably the biggest exponent of them. And as I said, the Government’s basically saying, ‘We want this in our back pocket in case the OECD Pillar One and Pillar Two deals fall over.’ These are still very much up in the air for discussion, as we’ve mentioned in previous podcasts.

National unveils its tax policy

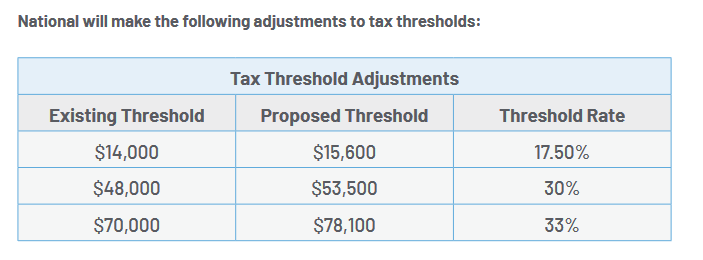

But the big news this week would have been the launch of the National Party’s tax policy on Wednesday, and it landed with quite a thump and contained quite a few surprises. National had already signaled well in advance that it proposes to increase thresholds by 11.5%. As regular listeners to this podcast will know my view is tax threshold increases are long overdue.

What about Working for Families abatement?

National has an identical proposal to that of Labour to increase the Working for Families In-Work Tax Credit by $25 to $97.50 per week starting next April. There’s a commitment that the current $42,700 abatement threshold for Working for Families will rise to $50,000 from 1st April 2026. This is also a Labour Party commitment. But as I said to a number of media outlets, the problem is that the Working for Families abatement threshold already kicks in at very low level and in fact if they had been adjusted for inflation since the last adjustment in July 2018, it would now be $51,800.

Both parties promising to raise the threshold to $50,000 in three years’ time is frankly a little off in my view. It just compounds the problem these families at the lower end of the income scale face with what we call high effective marginal tax rates because of the abatement level of 27 cents per dollar above the $42,700 threshold. This issue isn’t being addressed but instead the can has been kicked down the road.

But on the other hand, there is the proposed FamilyBoost childcare tax credit, which is worth up to $150 per fortnight for couples with childcare costs. This will be no doubt welcome, but the trade-off is the loss of the proposed extension of the Early Childhood Education subsidy that Labour included in its May Budget.

All good but how are you paying it?

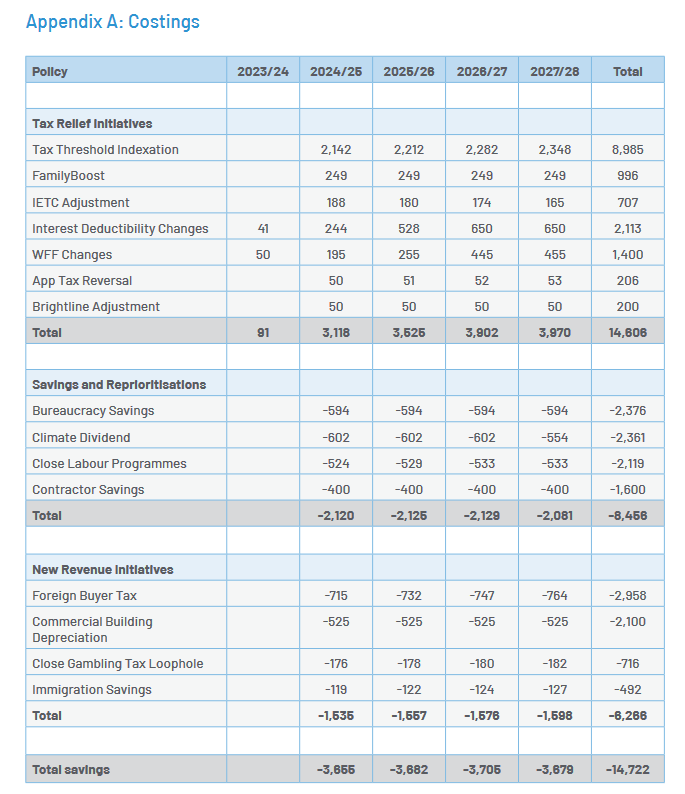

In fact, the controversy around National’s plan has broken out over how it’s going to fund this program and of these proposed tax adjustments. There are several surprises here, the first of which was this proposed foreign buyer tax. Currently no one who does not have permanent residency can buy property. National are proposing to keep that in place for properties worth less than $2 million, but to allow properties worth more than $2 million to be purchased. But that would be subject to a 15% tax, which sounds a bit like a stamp duty. We haven’t had stamp duty, by the way, since 1999.

The controversy is around the numbers involved, which do seem very optimistic. Revenue of $700 million a year would imply sales of at least $6 billion in property. I’ve seen a report in the New Zealand Herald which suggests that actually something like 60 to $65 million is more reasonable. But the proposal also runs up against questions that certain of our double tax treaties and trade agreements have clauses that would not allow such a clause to be a tax to be introduced, notably Singapore and Australia.

But now it’s been pointed out that what we call non-discrimination clauses in double tax agreements may apply to this. In which case these income assumptions of tax revenue would be well short.

There is a proposal to close an online casino gambling tax loophole as its described. This would require offshore operators to pay GST and register and report their earnings for tax purposes. The suggested penalty for non-compliance would be IP geo blocking of services. It subsequently emerged that the Government got $38 million in online GST for the year ended 31st March 2023. This is a result of the so-called “Netflix Tax” which, ironically, was introduced by the National Government in 2016.

National assume the measure will raise $180 million, and I admit I raised my eyebrows when I saw that suggestion. This seemed high to me particularly when I considered that the proposed DST I mentioned earlier is expected to raise about $55 million a year. Online gambling would seem to be a similar type of activity, if not quite identical, so assuming they’re going to raise 2 to 3 times as much as a DST struck me as optimistic.

National Party documents seem to be saying this is essentially a corporate income tax. In which case, it appears this particular tax could also be caught by the anti-discrimination articles in double tax agreements. And that could mean a $140 million shortfall in National’s projections.

Good news for singletons…ironically

On the other hand I do think the proposal to increase the Independent Earner Tax Credit threshold to $70,000 from its current $48,000 is a good initiative. I’ll be honest, I was a bit surprised that Labour didn’t think to do something similar as part of its budget earlier this year. But there is actually a little bit of an irony in that this Independent Earner Tax Credit was actually going to be abolished by National under the last budget it published in May 2017. But that measure never went through because of the change of government later that year.

A counter-productive proposal and more irony

But I think one of the measures that should attract more controversy, is the proposal to remove depreciation for commercial property which includes factories. Now this is something that Labour have also proposed to pay for the proposed removal of GST on fresh and frozen fruit and vegetables.

This is a counterproductive move in my view. The proposal refers to “commercial building” but the depreciation deduction covers all sorts of property such as factories, farming sheds etc. These all depreciate. It was recognised by the last tax working group, that depreciation on commercial and industrial buildings should really be re-introduced, introduced and is actually quite common around the world.

A measure that takes it away seems to be counterproductive particularly if we’re talking about encouraging investment in productive assets. There’s also the added irony that this would be the second time that a National government had removed that depreciation to pay for tax cuts.

Overall there’s an awful lot to pick apart here and the devil is always in the detail. This does seem to point to the revenue forecasts being on the optimistic side, certainly in relation to the foreign buyer online gambling taxes.

Good news for landlords…mostly?

On the other hand, there was also no surprise about the reintroduction of interest deductibility for residential properties. But what is interesting about this move is that’s it’s not simply being fully restored as of a change of government. What’s proposed is for it to be brought back in over a two-year period from 1st April 2024. At present the proportion which would become non-deductible is due to rise to 75%. Instead it will stay at 50% non-deductible and then starting 1 April 2025 the non-deductible proportion will year drop down to 25% before becoming fully deductible with effect from 1st April 2026.

Reducing the bright-line test back down to two years will be welcome for a lot of people. The unintended consequences arising from the extension of the period to first five and then ten years were giving me and plenty of other advisors a lot of work as we try to unpick where the boundary was, and what transactions were caught. So that’s probably quite welcome.

On the other hand, there’s a surprise that nothing has been said about allowing losses from residential property investment (“loss ring-fencing”) to again be offset against other income. This hasn’t been allowed since 2019. It also appears that the proposed increase in the trustee tax rate to 39% will still go ahead. I had heard whispers to that effect, and although there’s been plenty of pushback on the proposed increase it will be interesting to see what eventually emerges.

Now about those Tax Principles…

Having just got a new Tax Principles Reporting Act in place, it is interesting to compare the principles set out in there against these policies. You’d have to say for now, not entirely a big pass. Indexing the thresholds is a reasonable measure, as I said, but that’s a minor point. The tax on foreign homebuyers probably could be said to be questionable in terms of equity. Why should one group of people suddenly get a far higher tax charge than other groups of people in reasonably similar circumstances.

The removal of depreciation for commercial and industrial buildings doesn’t seem to fit with the tax principles. And since we’re talking about things that wouldn’t pass that bill, I’d have to say removing GST on fresh and frozen fruit and vegetables wouldn’t pass muster either.

Sucks to be a student…and an Auckland ratepayer?

But to summarise, tax is politics, so we can expect plenty of politicking. There’s no doubt that the tax relief in terms of the changes in the thresholds will be welcome, but there’s going to be quite a few losers as well. Following the announcement I spoke to a student radio station in Christchurch who were wondering about the impact for students. The answer was not very much and if the proposal to remove the 50% discount on public transport goes ahead, students would be worse off as a consequence.

Auckland ratepayers are also probably worse off with the proposed abolition of the Auckland Regional Fuel tax. Mayor Wayne Brown has already said that could mean a $2 billion funding shortfall. How is that gap going to be funded?

Overall National’s proposals are very much a sort of the Lord giveth and the Lord taketh. And where you sit on that spectrum depends on how well you end up. If you’re a landlord and high-income earner, and you don’t use public transport, you’ll be reasonably okay.

On the other hand, if you’re on lower incomes, perhaps receiving Working for Families income and you do use public transport, you’re going to be worse off. But this is politics, the electorate will decide in six weeks exactly which tax policy is fair.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This was introduced in the wake of the move to level three and then level two lockdowns in the Auckland region. This had been in the works for some time, but then just got pushed through under urgency following what we might call the Valentine’s Day mini outbreak.

Resurgence supports payments may be applied for if there is an increase in the alert levels from Level 1 to Level 2 or higher and the alert level remains higher than Level 1 for seven days or more.

It’s going to be available to all businesses in New Zealand each time it activates. So even though Auckland went into a Level 3 Lockdown and then back down to Level 2, because a lot of tourism is currently dependent on tourists from Auckland, the resurgent supports payments will apply nationally. This is a wise move, which cuts down a lot of administration, but also reflects the fact that Auckland is a prime source of tourism for the very weakened tourist industry.

Businesses are able to apply if they’ve experienced a revenue decrease or a decrease in capital raising ability of at least 30% due to the increase in the alert level. And they need to measure their revenue for that 30% fall over a continuous seven-day period where the first day is on or after the first day of the increased alert level. All seven days must be within the period of the increased alert level. The affected revenue period then needs to be compared against a regular seven-day revenue period that starts and ends in the six weeks prior to the increased alert level.

This scheme is going to be administered by Inland Revenue rather than the Ministry of Social Development as happened with the wage subsidies. Applications should be made through myIR and Inland Revenue is expecting that people receive the resurgence support payment within five working days of their application.

The payment must be used to cover business expenses such as wages and fixed costs. Note that this isn’t a wage subsidy per se, it’s a support payment. And that possibly explains the slightly unusual change from the previous wage subsidy in that this payment is subject to GST now.

Although no income tax deduction will be available for expenditure relating to use of the resurgence support payment, GST registered businesses will be able to claim input tax deductions for any expenditure funded by the resurgence support payment. In other words, if you pay the rent using the resurgence support payment, you won’t get an income tax deduction for it, but you will still be able to claim a GST input tax credit.

The payment consists of a base amount of $1,500 dollars per applicant, plus $400 per full time equivalent employee, up to a cap of 50 full time employees. Although payments are capped at 50 full time employees, businesses with more than 50 full time employees may still apply.

There is a further cap in that the amount an applicant may receive will be the lower of the base amount and four times the amount their revenue has declined, as declared by the applicant as part of the application. And I can see Inland Revenue having a bit of work going on in years for larger scale applications here.

Anyway, the measure is now in place and fortunately everyone within the Auckland region, because they are still in level two, will be able to apply for this because they have been at an Alert Level higher than Level 1 for the required seven-day period. I imagine there will be further tweaks to the scheme as we go forward in the event of further outbreaks.

Facebook gives Australia the fingers

Moving on, yesterday across the Ditch, Facebook announced that …

“due to new laws in Australia from today, we will reluctantly restrict publishers and people in Australia from sharing or viewing Australian and international news content on Facebook.”

And with that, it stopped any sharing of Australian news media sites and indirectly, some New Zealand sites could be affected as well.

Now, this stoush has been brewing for some time. The Australian Government is trying to force Google, Facebook and other tech giants to pay more for the media content. Google has played along with this proposal. Microsoft, which runs the Bing search software, is also playing along. But Facebook has pushed back very hard and decided to go very hardball with this move.

Now, barely two years ago, Facebook literally made blood money about live streaming the Christchurch massacre and then wrung its hand about the difficulties of taking down such abominations. But yesterday it basically was able to switch off all of Australia’s major media sites on Facebook just like that. And I’m sure there will be a few pointed comments made about that.

I can’t see how such outrageous behaviour will not draw a strong response. And this is where I think from a tax perspective, things may go. The Australian government has previously been lukewarm about a Digital Services Tax, but Facebook’s actions might prompt a rethink. The Australian Tax Office has done some work on this, and there might be a bill lying around which could be introduced at the drop of a hat in effect saying, “Here, stick this up you”.

If Australia does move forward with a Digital Services Tax, then I think our government will surely follow. Now I’m in the “ get into the Tax Tech Giants hard” basket and have been for some time, particularly since what happened in Christchurch. Yesterday’s actions by Facebook underscore my belief in that approach.

Incidentally, during this whole run up to this stoush erupting, at least one tech commentator suggested that a DST would be a better approach instead of what the Australian government was trying to do. We’ll see how this all plays out and it’s going to be very interesting to watch. Facebook just lifted the stakes considerably.

There are, according to the OECD, about 40 countries either with an active DST or considering introducing one. Maybe Australia is about to become number 41.

KiwiSaver makeup

Now, briefly following up from last week’s podcast, Inland Revenue is to pay approximately $6.6 million to compensate over 640,000 KiwiSaver members whose employer contributions were delayed in getting to the providers. Now, this happened last April, when Inland Revenue moved KiwiSaver to its new Business Transformation START platform. And for some reason there was a delay in passing on employer contributions to people’s KiwiSaver accounts.

This story reports delays of as much as six months or more. So people lost out on investment performance over that time. And during that time, the use of money interest rate paid by Inland Revenue dropped to zero which would have been the usual way of compensating for the delay.

Instead, what’s going to happen is Inland Revenue has been given approval to make ex gratia payments of about $6.6 million in total. This is a slight bit of a disappointment for Inland Revenue because as I said, by and large, the Business Transformation programme, controversial as it is, has worked relatively smoothly and improved processes. It’s certainly not a Novopay scale disaster, but it’s just another sign that sometimes with IT projects things go wrong.

End of year planning

And finally, the 31st March tax year end is fast approaching. So it’s time to start thinking about what steps could be done in advance of that. Now, there’s a couple of things in particular people might pay attention to.

This is an emergency measure introduced a year ago as part of the Government’s initial response to Covid-19. So now’s a good time to see if there’s equipment you want to replace or upgrade and take a full write off.

For assets purchased on or after 17th March, that threshold of $5,000 will be reduced to $1,000 going forward.

Now, the other thing to think about is tied in with the forthcoming increase in the personal tax rate to 39%. And the suggestion would be that companies might want to think about paying dividends out to use imputation credits prior to that date so that the shareholders are taxed at 33% rather than 39%.

Sometimes you might pay a year-end dividend anyway because that’s just part of the regular distribution pattern. But you might also do so because the shareholders might have an overdrawn current account which you want to get into credit.

The thing that complicates matters this year is whether such a move might represent tax avoidance. I don’t believe so. But one thing people must keep in mind is that as part of the increase in the tax rate to 39%, trusts have to provide more information about distributions they’ve made in prior years. So as the commentary on the tax bill said, “this is expected to assist in understanding and monitoring the changes in the use of structures and entities by trustees in response to new 39% rate.”

And that’s what gives me pause for concern about paying large dividends before 31st of March. If there isn’t a regular pattern of large dividends before the increase and then a large dividend isn’t repeated after the rate increase, Inland Revenue may look to argue tax avoidance and effectively tax retained earnings. So approach that one with caution.

I think this is a point where Inland Revenue really needs to come out and be very clear about what is going to happen with dividends paid by companies to trust shareholders, which aren’t then distributed. I think you’ll have a problem if the pattern was previously such dividends were distributed by the trust, maybe less so if that wasn’t the case. Again it’s a question of watching this space. And we’ll bring you developments as and when they happen.

Well that’s it for today, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week Ka kite ano!

The new Minister of Revenue, David Parker, made his first public speech in his role last week at the Chartered Accountants Australia and New Zealand Tax Conference. The speech introduced himself, gave a bit of his background in business and in government. He then outlined the Government’s expectations over what is to happen over the next three years.

And in talking about the Government’s priorities over the short term he mentioned that one of the first items of business for the Cabinet, was making improvements to the Small Business Cashflow Scheme so it continues to provide ongoing support.

Now, the latest is that close to 100,000 businesses have taken out loans with total lending of $1.6 billion. So, it’s been a huge success. I’m a big fan of the scheme which fills a hole we identified on the Small Business Council.

The new measures approved by Cabinet: extending the scheme for three years, increasing the interest free period from one year to two, and broadening how the loans may be applied, such as for capital items are estimated to result in additional lending of about $130 million for small businesses.

What the Minister has also asked for is further advice on changes to the scheme that will allow more businesses to benefit from it, including adjusting the eligibility criteria for the loan

On the tax side of matters the Minister confirmed that the Government will progress the promised new top personal tax rate of 39% on income over $180,000. And that new top personal rate will apply from 1st April 2021. The plan is to have it legislated and in place before the end of this year.

Minister Parker then said “the new 39% rate will need to be supported with integrity measures to address issues like people sheltering income in trusts to avoid the top tax rate. I’m receiving advice from officials on the necessary integrity measures.” So that’s a coded warning that although they haven’t increased the trust tax rate from 33% to 39%, it’s clearly something they may well consider.

And there’ll be other matters in hand to support the new rate which obviously, we’ll have to wait and see. These potential measures are something I would like the Government and Inland Revenue be very transparent about because the situation that developed the last time the tax rate was at 39% was only finally resolved by the Penny Hooper case. I think this is unsatisfactory because it creates uncertainty about the boundaries of acceptable tax planning.

Parker then went on to talk about improving our tax system and the taxation of multinationals stating

Our preference continues to be an OECD led multilateral solution rather than a proliferation of digital services taxes. However, success at the OECD is not guaranteed and has been blocked for some time. We are seriously considering implementing a DST in the event the OECD project fails to reach agreement within a reasonable timeframe.

And in talking about this, he referenced the fact that local New Zealand companies “deserve a level playing field when doing business. We don’t want to force New Zealand competitors into dodgier tax minimisation strategies to compete”. So the Minister is pointing the finger very firmly at the digital giants and their ability under present rules to order their affairs where they pay little or no tax in New Zealand which, as he put it, “This is a legal fiction that is divorced from modern reality and needs to be fixed”. So I think we can expect to see more action in this regard from the Minister of Revenue and Inland Revenue.

The Minister finished his speech with a line which I’m pretty certain was written by the Honourable Deborah Russell MP, who’s a big Star Trek fan: “Let’s all crack on with it so our people can live long and prosper even in the midst of a global pandemic.” Indeed.

Capital gains

Moving on, one of the matters that wasn’t mentioned by the Minister in his speech directly, but has been boiling over this week has been the question of taxing capital gains and the role of tax in dealing with the housing crisis and house prices.

The Minister of Finance has said that he has already requested Treasury to explore the options about extending the bright-line test. In the exchange of letters between the Minister of Finance and the Reserve Bank Governor, Adrian Orr, the Reserve Bank Governor, pointed out he would be happy to talk about fiscal measures, which would include tax changes.

This, of course, has prompted a lot of speculation about what’s happening. And the ACT party then went straight out and said, is the Government looking to bring in a capital gains tax by stealth?

Of course, the Prime Minister last year ruled out a capital gains tax on her watch. The thing is, though, the bright-line test is already in existence, so it’s hardly it would be a new tax to extend its scope. That happens with taxes all the time. And yes, it would also be bending the position a little bit.

But it’s also worth pointing out that the bright-line test is actually a fallback test. It applies if none of the other taxing provisions apply. And this brings us to a provision which if I was a rather devious Inland Revenue official, I’d be closely looking at applying. And this is Section CB14 of the Income Tax Act.

Now, under Section CB14, where a person sells land within 10 years of acquisition, any gains from that sale that are not taxed under other provisions and this would include the bright-line test will be taxable if at least 20% of the gain results from one or more factors that occurred after the land was acquired. Those factors include a change or a likelihood of change in the operative district plan.

Section CB14 almost certainly applies to properties which are rezoned for higher density or may have been brought into the special housing areas if you remember those. It’s a little applied provision. And in fact, the Tax Working Group recommended that it be repealed but it’s still on the books.

It has a couple of stings in its tail. It applies, as I mentioned, for land sold within 10 years of acquisition. But if you occupied it as a residential home, normally under the Income Tax Act, you will be fine. However, in this particular provision, the sale is not exempt unless the purchaser acquires it for residential purposes. So that means if someone whose house may have gained value because of a zoning change, such as the Auckland Unitary Plan, sells it to a developer or, and this is the tricky part, you actually decide to move on and sell it to a trust or another entity, such as a look through company, for example, to rent out the property, that sale/ transfer will be taxed under this provision. There’s a deduction of 10% of the gain allowed for each year of ownership.

Now, what this provision points out and what the ongoing debate around, what do we do about taxing wealth (you may recall the Deutsche Bank report I mentioned last week), is that our current rules are all over the place. We have very specific rules, such as the Foreign Investment Fund regime, which apply. But then in relation to land transactions, we have a series of rules that apply, mostly for disposals within 10 years, but in other cases indefinitely if there is an intent to purchase for a purpose of disposal.

And so, one of the arguments in favour of a capital gains tax is actually Simplification, believe it or not, because of these overlapping rules. Picking your way through these is a minefield with plenty of traps where I and other accountants get plenty of work when people misunderstood the implications of the bright-line test and other land taxing provisions.

So, I’ve never bought the argument that capital gains taxes are too complex. All taxes have a certain level of detail. But capital gains tax basic principle, you buy something which you sell and you’re taxed on the difference is fundamentally easier for people to grasp than, say, trying to explain the operation of the Foreign Investment Fund rules. But the politics are what they are. So a capital gains tax is probably not going to happen.

But I think we will see Inland Revenue making extensive use of provisions such as CB 14 to pick up transactions that have not previously been taxed. And we know they’re going through all transactions where a transfer has happened within five years, the bright-line period, where there is no obvious answer that it’s been a residential property sale to a new home-owner.

So watch this space there’s going to be plenty of activity from Inland Revenue in that area and the debate will continue to rage. I think the Government will find it has to make a movement on this space. It’s also worth remembering that the bright-line test was introduced in response to housing pressures and was introduced by a National government. So there is, in theory, a possibility of cross party support for a measure. It probably won’t happen, politics being politics.

But as I said, I think the dam is under increasing pressure and will break unless something is done to relieve the pressure of expectations of younger generations who are presently locked out of the housing market.

Backdating GST registration

And finally, a quick reminder from Inland Revenue about GST registrations. Generally speaking, the date of GST registration is the date an application is made. But in exceptional circumstances, those registrations can be backdated.

And Inland Revenue have issued a Standard Practice Statement on the effective date of GST registrations and what you can do about backdating a GST registration.

The key thing is, you got to have the supporting relevant documents, bank statements, tax issues, tax invoices issued and copies of contracts, and you’ll need to explain what was going on with your taxable activity and why your registration wasn’t filed sooner.

The fact Inland Revenue has drawn attention to this issue means that obviously it’s been receiving a few such applications or they’re looking at situations where people probably should have been registered for GST sooner.

Well, that’s it for this week. Next week, I’m going to be joined by Rod Spicer from Accountancy Insurance. We’ll be talking about the role of insurance in handling Inland Revenue audits and what Inland Revenue activity they are now seeing.

Until then, I’m Terry Baucher, and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week, ka kite āno.