Change on the way for GST recordkeeping requirements

A clear-eyed dissent by a Supreme Court justice

Tax revenue exceeds $100 billion for the first time

Over the next few months, GST registered businesses will receive a stream of information from Inland Revenue explaining new recordkeeping requirements for GST purposes, which will take effect from the 1st April next year. These changes relate to what information needs to be shared or retained to support GST input tax claims.

These changes are permissive in nature, and existing invoicing practises and systems which are compliant with the previous GST rules will still remain compliant with the new information rules. The new rules are less prescriptive about the information required to support a GST input tax claim.

The key purposes of these changes are to try and reduce compliance costs for businesses and facilitate the introduction of e-invoicing. The changes will be done by way of requiring the supplier and recipient of a taxable supply to retain a minimum set of information relating to that supply. The current rules, which required formal documents such as tax invoice, credit notes, debit notes etc. to support input and output tax will be repealed.

One of the most noticeable changes will be that there will no longer be a requirement for an invoice to have the words ‘Tax Invoice’ in a prominent place. Tax invoices will now be caught termed ‘taxable supply information’ and the former debit and credit notes which had to be issued when a correction was made, will now be termed ‘supply correction information’, which is better terminology as it actually reflects what’s going on.

There are also changes to the buyer credit created tax invoice regime which are now called ‘buyer created taxable supply information’. And these changes have already come into effect and actually are pretty helpful because you now no longer need to get Inland Revenues permission to operate the buyer created taxable supply information.

There will be a minimum set of information required to be retained in business records under the new rules for a taxable supply. According to Inland Revenue these rules are generally consistent with the requirements of commercial contract law relating to invoicing and recordkeeping. The requirement to hold a tax invoice in order to claim an input tax deduction is now replaced with the requirement to have business records showing that GST has been borne on the supply.

Now key information for both a supplier and a recipient of a supply of goods or services is that of, ‘supply information’. This includes, at a minimum, all the following information:

– the name and registration number of the supplier,

– the date of supply,

– a description of the goods or services, and

– the amount of consideration for the supply.

Helpfully, the low value transaction threshold for taxable supplies has been increased from $50 to $200. And that is part of a drive to simplify recordkeeping requirements for a large number of low value transactions.

There are now three value thresholds for the general meaning of taxable supply information and the information requirements for each of these are mutually exclusive. The thresholds are:

– Supplies exceeding $1,000,

– Supplies between $200 and $1,000,

– and then those for supplies not exceeding $200.

All these changes come into effect from 1st April next year, although, as I mentioned, the changes to the buyer created taxable supply information have already taken effect. As noted, existing systems will still remain compliant. So, there’s no need to dramatically go out and change everything to meet the new requirements. Inland Revenue will continue to release information about the changes over the coming months.

Supreme Court justices display worrying lack of tax knowledge in key decision

Last Friday, the Supreme Court released its decision in the case of Frucor Suntory New Zealand Ltd v Commissioner of Inland Revenue. This case has been watched with some keen interest by tax professionals. It relates to a series of transactions that took place in 2003, as a result of which DHNZ, a predecessor to Frucor Suntory, claimed interest deductions totalling $66 million in respect of an advance made by Deutsche Bank.

Inland Revenue sought to restrict the interest deductions totalling just over $22 million dollars claimed for the 2006 and 2007 income years on the grounds the funding arrangements constituted tax avoidance. Just for good measure, they also levied shortfall penalties totalling $3.8 million for the two years because they considered the tax avoidance was abusive.

The case reached the High Court in 2018, which ruled in favour of Frucor which was something of a surprise at first sight for those not familiar with the facts. Inland Revenue unsurprisingly appealed the decision and in 2020 the Court of Appeal held that the deductions did represent tax avoidance. However, the Court of Appeal did not accept the criteria for shortfall penalties had been met, so both parties were unhappy with their decision and naturally both appealed to the Supreme Court.

Last Friday it ruled by a 4 to 1 majority that the arrangement did represent tax avoidance and the shortfall penalties were correct as the tax position adopted by DHNZ (Frucor) was unacceptable and abusive as DHNZ acted with the dominant purpose of obtaining tax advantages.

Now, in some ways, the Supreme Court’s ruling is unsurprising. New Zealand courts have taken a fairly hard line on what is perceived as tax avoidance for the last 15 years or so. But there’s still a number of points of interest here. Firstly, you will note the length of time involved: the transaction happened in 2003. The assessments, which are the subject of the appeal, were for the 2006 and 2007 tax years. And there’s nothing I’ve seen yet explaining why it took nearly so long to reach the High Court. Under the principle of justice delayed is justice denied it’s concerning to see the amount of time involved.

Then there is the imposition of shortfall penalties, which seems harsh. If you are taking something all the way to the Supreme Court, you know you’re arguing on the margins. Nine judges looked at the matter and five said no shortfall penalties were appropriate. The only four that did think they were appropriate were the ones that mattered most because they were all on the Supreme Court. And you often see this in in court cases, the lower courts rule one way and then the Supreme Court says, nope, it’s the other way, and that’s the end of it.

But most interesting of all is the strong dissent by Justice Glazebrook in the Supreme Court now. Dissenting justice judgements are often very interesting reads, and I suspect Justice Glazebrook’s will be read and examined in quite considerable detail, given what she rebutted completely the principles adopted by the other four justices. Just for the record it’s worth noting that before she became a judge back in 2000, Justice Glazebrook was a tax partner in a law firm. She’s actually one of the co-authors of a book on the financial arrangements regime. In fact, the first edition, published back in 1999, is still had not yet been updated. So she’s got a good background in tax.

But the paragraph, I think is going to raise a few eyebrows is the penultimate one of her judgement.

[247] “The majority say that the dominant purpose of the arrangement in this case was to reduce the tax liabilities of Frucor. This despite the fact that the whole reason for the restructuring was to ensure that Danone Asia did not incur tax liabilities in Singapore, unlike the position before the refinancing where direct debt funding was provided by Danone Finance. Given that, before the refinancing, Frucor was deducting interest payments roughly equivalent to the amounts it claimed deductions for under the current arrangement, it is difficult to see how its purpose could have been to achieve a result it was already receiving (deductibility of interest) and thus difficult to see its dominant purpose as being to reduce its tax liabilities or to achieve an illegitimate tax advantage in New Zealand.”

Now that’s quite some paragraph, I have to say I don’t think I’ve seen for a while a judgement where you’ve got such completely opposite views on between the judges.

You often see differences in interpretation, but here there’s a very marked difference on the core of the case. Justice Glazebrook has questioned how it is tax avoidance in New Zealand when you consider that the real purpose of the restructure was to resolve a tax problem for the offshore parent.

It will be interesting to see feedback from other, more experienced legal practitioners and tax specialists who work in this space about this decision. As I said, I find Justice Glazebrooks dissent there quite strong, and I suspect it will generate quite a bit of commentary.

Hiding the effect of fiscal drag

Moving on, the Government published its financial statements for the year ended 30th June 2022 on Wednesday. As you no doubt are aware by now these turned out to be better than expected and have generated quite a bit of chatter around the overall tax burden and the implications for next year’s election.

From a tax perspective, what’s interesting to see is the strong rebound in company income tax. The forecast in the 2021 Budget was that corporate tax would be just over $13 billion. By the time of this year’s budget in May the estimate had risen to $17.25 billion. In fact the total for the year was just under $19.9 billion.

For individuals the tax source deduction payments (PAYE) are up. Two factors are at play here: the well-known one of fiscal drag or bracket creep which means as people’s wages rise, they cross tax thresholds and their tax increases. On top of that, you’ve got the introduction of the new 39% tax rate. Those two combined, according to the commentary to the financial statements, represented about $1 billion of extra tax.

You have to dig very hard to find out what is the effect of bracket creep or fiscal drag, because that’s not being reported in the budget statements. You can draw your own conclusions as to why that is so. But we do know that when it was included in the 2012 Budget the effect was between 0.1 and 0.2% of GDP.

At a rough guess the current effect of fiscal drag would be somewhere around $500 Million a year.

The GST take rose to $43 billion gross with the net GST for the year being $26 billion through. Overall, as I mentioned at the top of the podcast, tax revenue, including indirect taxation, exceeded $100 billion for the first time at just under $107.9 billion.

So, lots of excitable chatter about what that means politically for tax cuts and other changes. Speaking on RNZ’s The Panel yesterday afternoon, (about 12 minutes in) I reiterated what I have said elsewhere that we need to do more about the tax brackets at the bottom end because that’s where the effects of fiscal drag are the hardest. The non-indexation of income tax and Working for Families thresholds means there are people on say $50,000 a year & receiving Working for Families who are on an effective marginal tax rate of 57%.

Roasting the idea of GST exemptions

Obviously what went on over in the UK has also attracted attention. This week the UK Government abandoned its higher rate tax cuts in the face of extreme political pressure from all sides, including Conservative MPs. It’s been very interesting and entertaining to watch a really classic example of the “Order, Counter-order, Disorder” maxim. And I do wonder how Prime Minister Liz Truss and her [Finance Minister] Kwasi Kwarteng are going to survive.

And finally, speaking of the UK, one of the things that comes up in discussions about how do we help with the cost of living is a not unreasonable suggestion on the face of it, to remove GST on certain foods. Now I’m in the GST purist camp here. I don’t believe we should do that. To repeat a point I’ve made several times, if you are trying to help people who have not enough income, give them more income. Any changes to the GST system such as zero-rating food benefits everybody and therefore are also more expensive as a consequence. And that idea of targeted assistance is consistently noted by the Tax Working Group and also the Welfare Expert Advisory Group.

But there’s another reason why you wouldn’t want to do it unless you wanted some inadvertent laughs. And that is the absurdity of the distinction which happens at the point where you are trying to determine whether a particular product is zero rated or standard rated. Now, Britain, with its VAT (value added tax) regime, has produced a number of very entertaining cases on this. I think people may be aware of the Max Jaffa case, which involves the distinction between a biscuit (standard rated) and a cake (zero-rated).

But this week I was alerted to one which is even more spectacularly hilarious, and it involved marshmallows of unusual size, which really sounds like something a line from The Princess Bride. A VAT tribunal case ruled that marshmallows of an unusual size are 0%, but standard sized marshmallows were standard rated at 20%. As one commentator noted, it’s sometimes very difficult to decide whether a VAT case is indistinguishable from satire.

This case involved a £470,000 dispute between Innovative Bites Ltd and H.M. Revenue Customs about the product “Mega marshmallows”. The VAT tribunal ruled that mega marshmallows were zero rated because they have to be roasted before they could be consumed and therefore not a standard rated snack.

On that bombshell, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

A new tax bill causes a massive storm but what happens next?

Also a brief run-through of what other tax measures are in the Taxation (Annual Rates for 2022-23, Platform Economy and Remedial Matters) Bill. (TL:DR – a lot!)

On the face of it this was a provision to address a technical issue which had developed over time where fund managers were applying different treatments to how they determined what proportion of the fees they provided were taxable supplies subject to GST and what portion represented GST exempt financial services.

The proposal determined by Inland Revenue was to standardise the approach and apply GST service and fees. This would have taken effect from the 1st of April 2026. We’re therefore talking about a measure three years in the future, but which would have netted an estimated $225 million a year in GST. That in itself probably wouldn’t have caused many issues except the Regulatory Impact Statement which accompanies the Bill, included modelling by the Financial Markets Authority which on the assumption that the increase in GST would be fully passed on to KiwiSaver fund members, KiwiSaver balances would be reduced by an estimated $103 billion by 2070.

And then the fun kicked off. There clearly was quite a bit of misunderstanding about this measure with some people thinking the Government would be charging GST on KiwiSaver balances. The Government was taken completely by surprise and the furore was such that it decided to abandon the proposal within 24 hours of announcing it, which is some form of record. It certainly made for an entertaining 24 hours in tax. You can hear more about what happened in this week’s edition of the Spinoff’s podcast When the Facts Change where Bernard Hickey and I discuss the background to the proposal and how it fits into the history of tax reform since 1984.

But it should be noted that the particular issue of an inconsistency of approach by fund managers still remains. So, what’s going to happen now? Probably Inland Revenue will have to negotiate with fund managers and come to some form of agreement over what proportion of fees it deems to be acceptable to be treated as taxable supplies. This was what happened back in 2001, but that agreement has long expired. Such an agreement is going to take some time, although maybe negotiations already started. We’ll have to wait and see how that pans out.

Ironically the GST on fund management proposal was a relatively minor part of the Bill, although it would have had the biggest single tax effect. The rest of the Bill, as its name implies, covers a whole range of matters, including the gig economy, more GST issues, cross-border workers, fringe benefit, and the bright-line test to name a few.

Addressing the Platform Economy

A number of reporting and other tax issues have arisen around economic activity facilitated by digital platforms. That is where an app connects buyers and sellers and includes accommodation services such as Airbnb and transportation services, such as the ride sharing apps, Uber and Zoomy and Ola together with other professional services provided through digital platforms.

The Bill intends to ensure Inland Revenue has better access to information about income earned by sellers using digital platforms based in New Zealand or offshore. These provisions build on proposals developed through consultation by the OECD. Inland Revenue will get greater information and it will also share that information with foreign tax authorities where it relates to non-residents.

The Bill also wants to maintain the sustainability of the GST system. Digital platforms will be required to collect GST on services provided through them in New Zealand. This will be done by extending the rules that currently apply to imported digital services and low value imported goods. These will now apply to accommodation, ride sharing and food and beverage delivery services all currently provided through digital platforms.

There is a proposed flat rate credit scheme intended to reduce the compliance costs for those accommodation hosts and drivers who are not required to register for GST because the value of the services they provide over 12 months is less than $60,000. The GST changes will come into effect from 1st April 2024 and the net impact is expected to be around $37 million per annum.

These changes reflect the growing impact of the digital economy and the moves by tax authorities to ensure they know what’s going on and close potential gaps in loss of revenue may be arising because some of this may be happening under the table. It also reinforces something we see a lot of already and which we’ll see more of, and that is information sharing with other jurisdictions as appropriate.

We’re still working through the impact of COVID-19. And one of the areas where I’ve seen quite a bit of interesting work develop is in relation to cross-border workers. In the wake of the pandemic, we’ve seen a lot of people return to New Zealand from overseas. In many cases these returnees continue to carry on working remotely for their previous employer. This pattern of working remotely has expanded greatly as a result of the pandemic, and I don’t think that’s going to change significantly. But it was also another one of the situations where tax legislation and reporting and withholding tax obligations haven’t kept up with developments.

The Bill therefore has measures to deal with cross-border workers. The PAYE, FBT and employer superannuation contribution tax rules are very strictly applied, but they are incredibly inflexible. They really don’t take into account that employees might be working in New Zealand for non-resident employers and have very different compliance circumstances to those employees of New Zealand resident employers.

The Bill’s proposals acknowledge that such people coming in and working remotely for overseas employers justify taking a different approach to help reduce compliance costs for those cross-border workers. The key amendments are to allow more flexible application of the PAYE rules in specific circumstances. For example, it might allow PAYE to be paid annually. There’s also a repeal of a little used PAYE bond provision.

Alongside those rules are changes to the non-resident contractor rules which relate to the performance of services by non-resident contractors in New Zealand. These are essentially a withholding tax which operates to try and manage the tax risk of people coming in for a short period to perform contract work on a project and then return overseas. Without these non-resident contracting rules, no tax would be deducted. These rules have been in place for a very long time. Apparently, they were first introduced in the wake of the ‘Think Big’ projects of the late seventies and early eighties. They also apply quite extensively to the film industry as well which is where I first encountered them.

The non-resident contractor rules are being tweaked to update them and manage the compliance costs for those subject to them. Again, this reflects a trend that had been developing but has accelerated in the wake of the pandemic. The changes for the PAYE and non-resident contracting rules take effect from 1st April next year.

Notwithstanding what went on with the GST on managed funds issue, there’s quite a bit of other GST matters addressed in the Bill. These include provisions to address issues in the GST apportionment and adjustment rules. These are intended to reduce the compliance costs these rules impose and supposedly better align with current taxpayer practises.

There will be a principal purpose test for goods and services acquired for $10,000 or less GST exclusive. This would enable a registered person to claim a full GST input tax deduction. The other key change is to allow GST registered persons to elect to treat certain assets that have mainly private or exempt use, such as dwellings as if they only had a private or exempt use.

That latter change addresses an issue which has popped up from time to time in is that people may have made claimed GST as part of a home office deduction. If so, then potentially when that property is sold, is it therefore not the case that some portion of the sale will be subject to GST? This was a matter which technically existed, but probably wasn’t being addressed by many taxpayers and advisors.

This issue is generally covered by the GST apportionment and adjustment rules which are very complex and have high compliance costs. Under these rules if you have claimed an input tax deduction based on the estimated use business use of an asset, you are meant to track the business use of the asset. Where the actual use is different from the estimated business use, then you calculate and return an adjustment at the end of the tax year.

This is quite an involved process, and this measure is intended to try and simplify the matter. It’s a sensible change, in my view, which reflects the fact that although GST is a very broad-based tax, you can’t actually really describe it as a simple tax in its operation. There are all these issues around its margins regarding what represents business use, what proportions become taxable and therefore subject to GST, etc. And as we saw in relation to the GST and fund management services, the sums involved can be quite large actually. These proposed changes to try and simplify matters and will take effect from 1st April 2023.

I frequently discuss tax and environmental issues and I’m therefore pleased to see a proposal in the Bill for an exemption from fringe benefit tax (FBT) for certain public transport fares which are subsidised by an employer. This will take effect from 1st April 2023.This is a good example of tax being used as a behavioural change and comes about by looking at the bigger picture of how we address greenhouse gas emissions and what role can tax have in that. The Tax Working Group identified that the FBT treatment of parking is inconsistent and in many cases is not subject to FBT. By contrast, FBT is applied to subsidised public transport.

When you step back and take a wider environmental policy perspective about this, what’s happening is the opposite of what you really would want. The policy should be to tax parking to help reduce emissions and encourage the use of public transport. That’s what this measure is intended to do. It’s a very welcome move which is estimated to cost about $9 million a year. This would also appear to be a good example of how environmentally friendly changes can be achieved at relatively low cost.

Outside of the main policy issues we just discussed, the Bill, as is typical, contains a whole heap of provisions relating to many other issues. For example, there’s a number of changes in relation to the Bright-line test and interest limitation rules introduced last year.

Unsurprisingly, given the complexity of those rules, we are seeing a number of tweaks and clarifications about how they operate. One such example relates to when relief is available under the bright line test, when land is transferred on the death of the owner to the executor of or beneficiaries of the estate. Such a transfer is meant to be exempt, and the Bill has provisions making that clear.

There are some other provisions relating to rollover relief, that is when the bright-line test does not apply to transfers between related parties in certain circumstances. Most of those amendments will take effect the day after the Bill receives Royal Assent, which will probably be in late March next year. But some pleasingly have a retrospective effect back to when the changes to the Bright-line test and the interest limitation rule were announced on 27th March 2021. I fully expect we’ll see more such technical changes in the future, possibly even with some Supplementary Order Papers to this particular tax bill.

Another provision deals with a potential issue with the foreign trust regime and the exemption for foreign trusts whereby income from a non-New Zealand source is not taxable in New Zealand so long as it’s not distributed to a New Zealand resident. In some instances, a trust can make use of that provision but not have to comply with the foreign trust, registration and disclosure rules. The Bill therefore has provisions addressing that issue and some other minor technical matters applying to foreign trusts.

The recently announced build to rent exemption from interest limitation is also part of this bill. According to the supporting Regulatory Impact Statement this will cost $2.1 million if applied to existing build to rent assets.

Then inevitably, as in any of these tax bills, there’s a whole heap of other little remedial matters tidying up technical issues that have arisen around student loans, financial arrangements, provisional tax look-through companies, dual resident companies and more.

Ordinarily, this type of tax bill would barely get a mention in the press, so this week’s drama was quite unexpected. Now the dust has settled, it’s worth remembering that the issue around inconsistent treatment of GST on fund management services still remains. Ultimately, the Government backdown is another example of how short-term politics will nearly always trump longer-term policy.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Inland Revenue has begun taking more action on outstanding tax debt. It dialed back how hard it was pushing on overdue tax debt during last year in the wake of Covid-19. But in recent weeks, its activity has stepped up, and those involved with corporate reconstructions are seeing much more activity with Inland Revenue pursuing tax debt.

There are some reports that it’s particularly targeting the housing and construction sector, but that’s not necessarily the case, as I understand it. But the housing and construction industry has a record of nonpayment. Inland Revenue is particularly concerned about those companies or individuals not keeping up to date in relation to their GST and PAYE obligations. Inland Revenue’s longstanding view is that such receipts are held on trust (because they’re being withheld from the payees) and therefore the companies have no right to the payments and need to pass them straight through to Inland Revenue.

An Inland Revenue spokesperson confirmed they were taking more action adding “We give high priority to any business that has failed to pay employee deductions when due.” In the past Inland Revenue sometimes seemed quite extraordinarily slow in taking action with overdue PAYE. But if it’s boosted its efforts in this space that’s all well and good because following Gresham’s law, bad money drives out the good. And those conscientious employees and businesses that follow the rules and make the payments as required are being undercut by more unscrupulous operators.

In that context, what I’ve been told is that Inland Revenue is also upping its efforts in relation to developers who are claiming GST on land purchases, but then failing to declare the GST when they make the subsequent sales of the properties. In some cases, you also have what they call “Phoenix companies” where there’s a pattern of developers establishing companies which then fall over leaving unpaid tax debts. Inland Revenue got itself extra powers to try and deal with those matters. And I would expect that with its enhanced capabilities following completion of the Business Transformation programme, Inland Revenue should be on top of that situation.

As always with tax debt the key thing to do if you run into trouble, is talk to Inland Revenue. It is actually surprising how little tax debt can soon become unmanageable for people. Inland Revenue’s own research suggests that break point is as little as $10,000. This ties in anecdotally what I’ve seen.

The key thing is, if you get in front of Inland Revenue early, tell them that you have hit difficulties and want to arrange an instalment plan, they will be cooperative. Where they won’t be cooperative, and in fact they may look to take action and prosecute, is where someone persistently fails to meet their obligations in relation to paying over PAYE and GST and then tries to evade any responsibility by attempting to liquidate the company. Such scenarios increasingly will lead to prosecutions by Inland Revenue.

People will be surprised at how reasonable Inland Revenue can be. But to do so you have to be front up early, put all your cards on the table and you can then hope to get a reasonable hearing. Sometimes it doesn’t work out, but you would be surprised at how often these issues can be resolved.

And this also takes the stress away from people, employers and business owners who get into tax trouble quite naturally stress about the matter and often put their heads in the sand. It’s remarkable how much of a difference to stress levels it makes once you’ve spoken to Inland Revenue, and you find is this they are prepared to come to some form of arrangement. That’s dependent on a number of factors, the key factor being willing very early on to deal with the issue.

GST for directors’ fees

Moving on and still talking about GST, Inland Revenue has released some draft guidance for consultation on the treatment of GST for directors’ fees and board members’ fees. This covers a number of draft public rulings and is accompanied as well by a very useful fact sheet. I’m liking how Inland Revenue is sending out a lot of these fact sheets alongside the longer papers with detailed consultation, because the fact sheets of what you can put in front of clients as they are a good summary of the issues.

The rulings will cover directors of companies, board members not appointed by the Governor-General and board members appointed by the Governor-General or the Governor-General in Council. Basically, what the rulings say is board members or directors must charge GST on the supply of services where the director or board member is registered or liable to be registered for a taxable activity that they undertake, and the director or board member accepts a directorship or membership of a board in carrying on that tax taxable activity. Remember, liable to be registered means they are carrying out taxable supplies which over a 12-month period would exceed $60,000.

And the director or board member cannot charge GST on the supply of services where they are engaged as the director or board member in their capacity as an employee of their employer or they’re engaged in in that capacity as a partner in a partnership, or they do not accept the office as part of carrying on a taxable activity.

As I said, these draft rulings are accompanied by a fact sheet, which includes a very handy flowchart, these flow charts and fact sheets makes life a lot easier and more understandable for those affected. The proposed rulings are reissues of previous rulings on the matter. They’re fairly uncontroversial as they generally are simply restating the law, updating the statutory references and setting it out in a clearer and more understandable format for the general public.

Tax take up strongly

Now, this week, the Treasury released the government’s financial statements for the 11-month period ended 31st May 2022. And it all looks a lot better than what was being forecast in May’s Budget. Core tax revenue is $2.9 billion ahead of forecast just at just under at $98.9 billion. Now, the main reason it’s ahead of forecast is a higher than expected corporate income tax take which is $1.6 billion ahead of forecast. There’s also more tax from individuals which is $700 million ahead of forecast and PAYE collections are another $600 million ahead of the Budget forecasts.

The corporate income tax take for the 11 months of the year to date is just under $17.9 billion compared with a forecast $16.2 billion. Just for comparison, in the year ended 30th June 2021, the total corporate income tax take was $15.7 billion. So corporate profits look strong, and I think one or two economists might be pointing to whether that might be feeding inflation. But whatever its role is, I’m sure the Government will be grateful for the continued strong growth in the corporate income tax take. By the way, that increased corporate income tax take will also reflect the fact that the New Zealand Superannuation Fund will be paying substantially less tax this year than in 2021 because of the volatility in the financial markets.

Favourable winds for windfall taxes

Elsewhere in the world President Macron in France is under pressure to consider a windfall tax on some parts of the corporate sector where high energy prices have resulted in higher profits. Britain, you may recall, imposed a windfall tax on some oil companies, although it’s come with a potential subsidy which may dilute the impact of that. Windfall taxes have no real history in New Zealand, so are unlikely to happen here. But it is to see how other jurisdictions are reacting to questions of what they perceive as excessive profiteering.

Housing’s tax-free advantage

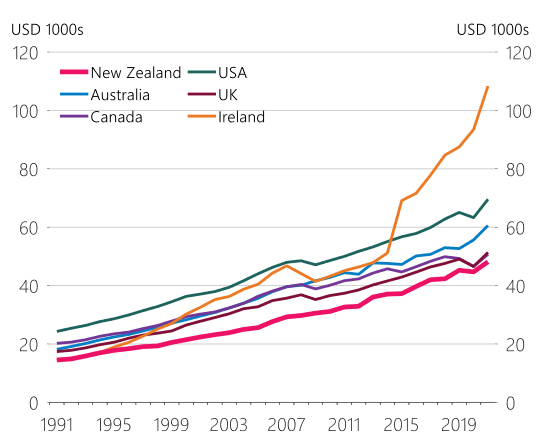

And finally, this week the Reserve Bank of New Zealand issued an Analytical Note on how the New Zealand housing market looks in the international context. What it does is compares facets of the housing market in New Zealand with those in 12 other developed countries[1] over the 30-year period from 1991 to 2021.

And it notes that several other economies, Australia is one, have experienced increasing house prices in recent years, but the rate of increase has been the highest here. Interestingly we have also seen the steepest decline in mortgage rates since the Global Financial Crisis and then almost the strongest increase in population. Apparently, although we’ve been ramping up construction quite dramatically in the past few years, the number of dwellings per inhabitant remains low and below the average for the OECD.

There was some mostly passing commentary in the note about the impact of tax. The paper does touch on the absence of a general capital gains tax commenting:

“Another feature of the New Zealand economy that may support higher housing demand is the absence of a comprehensive capital gains tax. New Zealand is unique in that aspect in the sample of countries we consider, fiscal authorities in other countries tax capital gains from asset sales at or close to the personal income tax rate.”

Being an analytical note, it doesn’t make any recommendations as to whether there should be increased taxes on housing, although the OECD has been for a long time pushing that point. It’s always interesting to consider the role of tax in our housing market and also whether the absence of the fact that housing is treated so generously for tax purposes means that investment is driven into that rather than into more productive sectors.

On that point, there’s a very interesting graph illustrating the surge in Irish GDP per capita over the last ten years or so, it’s really quite marked. The note comments that this surge

“was supported by high-performing multinational companies that relocated their intellectual property assets to Ireland attracted by lower corporate tax rates [12.5%] as well as Brexit-related uncertainty in the United Kingdom.”

Figure 4: per capita GDP in US dollars at current PPP

This Reserve Bank note reinforces my long held view that our favourable tax treatment of housing does divert funds away from productive investment and we need to change that treatment. As previously stated, my preference is for the Fair Economic Return approach Susan St John and I have proposed. .

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week.

In the wake of the Budget, a Cost of Living Payments bill was introduced and has now been enacted. As part of the enactment a supplementary analysis report was released giving background to the proposed $350 payment. And this supplementary analysis has some very interesting commentary.

It appears the Cost of Living Payment was put together very much at the last minute as a response to the adverse effects of inflation on low to middle income households. According to these documents, this report was finalised on May 4th, barely two weeks before the Budget was delivered, which is very late in budget terms.

According to the document, Inland Revenue recommended against being the delivery agency for this Cost of Living Payment. The reason it gave was that it was concerned, that being asked to administer the payment would significantly impact its services to customers – taxpayers in plain English.

“The addition of this payment to their portfolio of services Inland Revenue already delivers will compromise Inland Revenue’s already stretched workforce and affect the taxpayer population, including the families and individuals that the payment would be intended to support them.”

Inland Revenue correctly identified that as soon as the announcement was made, they would get contacted about it which would put strains on their systems. It calculated a maximum of approximately 750 full time equivalent staff would be required to handle the payments to be made in the weeks of 1st August, 1st September and 1st October. Now, to put that in context, Inland Revenue staff as of 30th June 2021 was 4,200 full time equivalents. It would therefore need to use the equivalent of 18% of its staff to handle the delivery of this Cost of Living Payment. Quite clearly this would put strains on its system. The $816 million appropriation for the Cost of Living Payments includes $16 million to Inland Revenue for delivery of the services.

It’s therefore likely that Inland Revenue will need to hire additional staff, presumably contractors, on a short-term basis. And as we’ve discussed previously, the issue of contractors hit the courts with the Employment Court ruling that the contractors were not employed by Inland Revenue although I understand that decision is being appealed.

It also seems the Inland Revenue poured a bit of cold water on how the payments would be structured. According to the report, 55% of the total payments to be made will be to the middle 40% of households, 20% would be made to the bottom 30%, and 25% would go to the top 30%. There would be an estimated 478,000 households with children and 610,000 households without children who would receive a Cost of Living Payment. Although around 60% of all potentially eligible recipients will have annual income below $70,000, 10% would have family income of between $70 and $100,000 and 30% will have family incomes over $100,000.

And this led Inland Revenue to point out that potential equity concerns could arise because using individual income to calculate the eligibility for the payment rather than household income may result in different outcomes for households with the same income level. For example, a single person earning $100,000 won’t receive a payment, but a household with two people working who each have income of $50,000 would both receive the payments.

There’s also some analysis regarding how the eligibility is dependent on a person’s prior year’s income, which means the tax returns for the March 2022 must be filed. The paper notes that by the time Inland Revenue begins making payments on 1st August, it expects to have already raised individual tax assessments for approximately 3.2 million individuals, about 75% of individual taxpayers. But that leaves about 500,000 individuals, who may not initially receive the payment between the August to October payment run period because they haven’t filed their tax return. And this includes people who file through tax agents and have in theory until 31st March 2023 to file last year’s tax return.

This underlines a point I made in last week’s Budget commentary that you can probably expect tax agents to come under more pressure to get tax returns done on time so that those people who think they’re eligible may get a Cost of Living Payment. Overall, it’s some interesting insights into the administration of these systems and the Budget process.

GST pitfalls for the unwary

Now moving on, GST is probably the best example you can find of the broad-base low-rate approach to taxation policy. But even though it’s a highly comprehensive tax, that does not make it a simple tax. In fact, it’s full of pitfalls for the unwary. And I’ve been alerted to one which may affect farmers who are selling up.

Back in 2020, Inland Revenue caused some consternation when it issued Interpretation Statement IS20/05 on the supplies of residences and other real property. The Interpretation Statement reversed a long-established policy since 1996 on the sale of the farmhouse where the farmer might have used part of the property for their taxable activity, for example a home office in the homestead. Previously Inland Revenue’s position was that the sale of a farmhouse would generally be a supply of a private or exempt asset and not subject to GST.

However, in IS 20/05, Inland Revenue reversed that position and now said that the sale of the dwelling would have been useful for families who would now be subject to GST. The example the Interpretation Statement gave was if a GST registered farmer was claiming an automatic 20% deduction for farmhouse expenses, an Inland Revenue would expect that the property was therefore being used 20% of the time in the taxable activity and consequently sale of the farmhouse would be a supply in the course or furtherance of a taxable activity and therefore subject to GST.

This change has caused some consternation although some relief was given in the recently enacted Taxation Annual Rates for 2021-2022, GST, and Remedial Matters Act. This included a provision which allowed a deduction for the private use portion of a sale. Coming back to that 20% example I mentioned a moment ago, if 20% of the homestead was used for farming business and 80% for private purposes, there would be an adjustment for the output tax of 80% of the private portion. But that would still mean that 20% of the current value of the farmhouse at the time of sale would be subject to GST, which would be an increased tax burden for many farmers and undoubtedly a surprise for some.

Apparently Inland Revenue is now indicating that it may reconsider its position in its Interpretation Statement, which is a classic example of the military maxim “Order, counter-order, disorder”. But until that point is clarified, farmers who are selling their farm should be aware of this potential liability and seek advice on that transaction.

How the OECD influences our tax policy

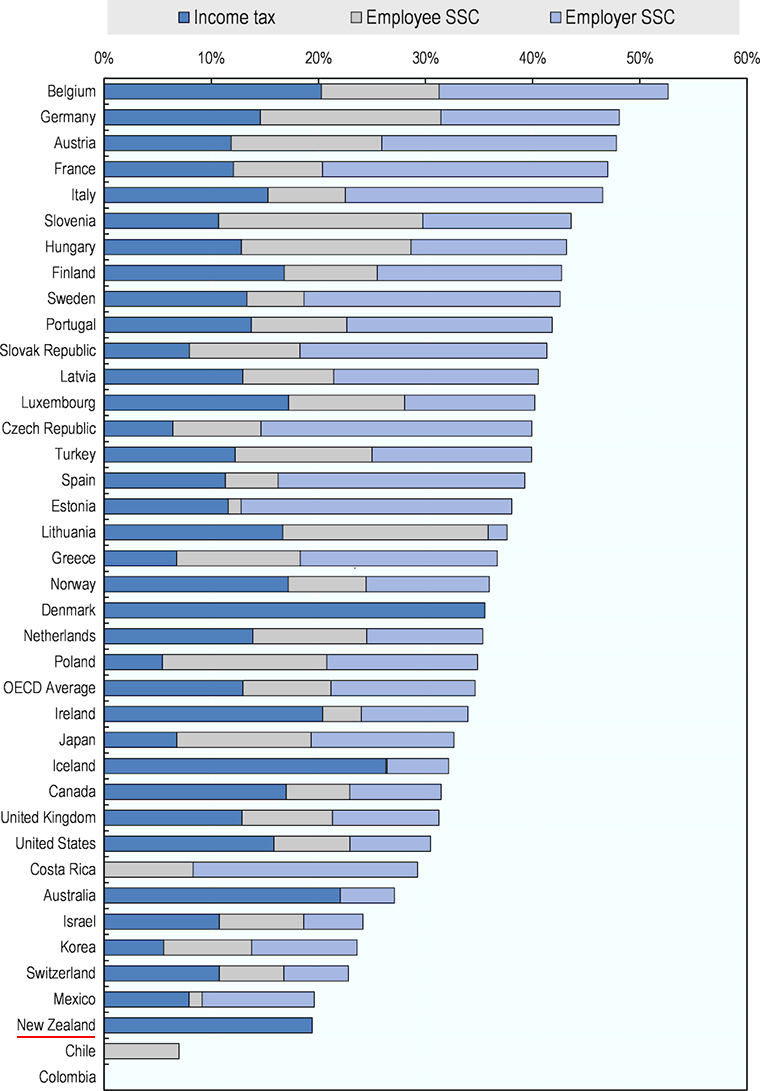

And finally this week, a couple of updates from the OECD. Firstly, it released its annual report on the taxation of wages. This includes its tax wedge analysis, which looks at the difference between labour costs to the employer and the corresponding net take home pay for the employee. Basically, the tax wedge is the sum of the personal tax income tax payable by the employee plus any employee and employer social security contributions plus any payroll taxes less any benefits received by an employee. (I think ACC is included for these purposes).

As can be seen New Zealand, scores very highly with a tax wedge of 19.4%, which is the third lowest in the OECD. The average in the OECD is 34.6%.

What this tax wedge measure also points to is the significance of Social Security and payroll taxes in other jurisdictions. One of the criticisms of the Government’s proposed social insurance scheme is it would be the first real Social Security tax that New Zealand has. It seems from early feedback this is one reason employers are pretty reluctant about the scheme. But even if the scheme was introduced, we’d still be down the lower end of the tax wedge.

Now the second OECD report was titled Tax Cooperation for the 21st Century. This was prepared by the OECD for the G7 finance ministers and central bank governors when they met recently in Germany. It’s particularly interesting because it picks up on what’s been happening with the adoption of the Two Pillar solution for international taxation we’ve talked about recently.

The OECD was asked to prepare was a report that would focus on the further strengthening of international tax co-operation and what recommendations it has in this field. This is looking beyond the implementation of the Two Pillar solution which makes it very significant, in my view, about the future administration of international tax.

For example, a key recommendation is tax administration should be seen as a common mission by tax authorities rather than a potentially adversarial exercise. The development of international cooperation is one of the biggest themes in international taxation in the 21st Century and is also probably one of the least understood. And I will repeat what I’ve said beforehand, most people are oblivious to the amount of information that is being shared by tax authorities at all levels. China, incidentally, has just signed up to the mutual agreement and protocols on that. So every major jurisdiction in the world is cooperating or looking to cooperate on international tax at some level. This is why this paper is important because it starts to map out and where that international co-operation might be going.

The report focuses initially on corporate tax saying there needs to be a reliable framework for cross-border investment. As just noted, tax administration should be seen as a common mission. There should be a collaborative approach with early and binding resolution.

The impact of going digital is emphasised and that it needs to speed up to improve engagement with taxpayers. There are also recommendations beyond corporate tax about moving to real time data availability for taxpayers and tax administrations to make efficient use of evolving technologies while maintaining data privacy and confidentiality.

The issue of data privacy and confidentiality is a developing area where taxpayers are starting to push back against tax authorities because they are concerned, rightly, whether everything is secure as it should be. Furthermore, some are, understandably, not too happy about information sharing.

Finally there’s a recommendation that advanced economies should commit to supporting developing economies so that they can fully benefit from the policy changes. This means building capacity which is going to be needed, especially for the implementation of the Two Pillar solution. Overall, this is a relatively brief but fascinating paper with potentially significant implications.

And just incidentally, on the international Two Pillar solution, the Secretary General of the OECD has now indicated that he expects that implementation will be delayed by a year until 2024. That doesn’t surprise me, given the scale of the project, because there’s a lot of legislation that needs to be put in place by the middle of next year at the latest. Inland Revenue have only just started consultation on the matter.

Still, the Two Pillar project has moved on quicker than some cynics might have expected. But as I’ve said previously, politics is likely to get in the way, particularly the upcoming US Congressional midterm elections. Anyway, as always, we shall bring you the news as it develops.

Well, that’s all for this week I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Last week I mentioned that Inland Revenue had released a discussion document, Dividend Integrity and Personal Services Income Attribution, which set out its proposals for measures to limit the ability of individuals to avoid the 39% or 33% personal income tax rate through use of a company structure. This is what we call integrity measures designed to support the integrity of the tax system. In this case, the proposals are to support the objective of the increase in the top tax rate to 39% and to counter attempts to avoid that rate by diverting income through to entities taxed at a lower rate.

Now this paper is pretty detailed and runs to 54 pages. There’s a lot in here which will get tax agents and consultants sitting upright and reading the fine print as in some cases they will be affected directly. It’s actually the first of potentially three tranches in this area. Tranches two and three will consider the question of trust, integrity and company income retention issues, and finally integrity issues with the taxation of portfolio investment income. And the reason for the last one is that portfolio investment entity income is taxed at the maximum prescribed investor rate of 28%, which is undoubtedly attractive to taxpayers with income which is now taxed at the maximum tax rate of 39%.

The Inland Revenue discussion document has three proposals. Firstly, that any sale of shares in the company by the controlling shareholder be treated as giving rise to a dividend for that shareholder to the extent the company and its subsidiaries has retained earnings.

Secondly, companies should be required on a prospective basis, i.e. from a future date, to maintain a record of their available subscribed capital and net capital gains. These can then be more easily and accurately calculated at the time of any share cancellation or liquidation. That’s a relatively uncontroversial proposal.

And thirdly, the so-called “80% one buyer test” for the personal services attribution rule be removed. This one will probably cause a bit of a stir.

The document begins by explaining these measures are required to support the 39% tax rate. There’s a lot of very interesting detail in this discussion, for example it notes that with the top tax rate of 39%, the gap between this and the company tax rate of 28% at 11 percentage points is actually smaller than the gap in most OECD countries.

But then, as the document says, “However, New Zealand is particularly vulnerable to a gap between the company tax rate and the top personal tax rate because of the absence of a general tax on capital gains.”

And so to repeat a long running theme of these podcasts, this lack of coverage of the capital gains has unintended consequences throughout the tax system. And this question of dealing with this arbitrage opportunity between differing tax rates is, in essence, a by-product of that.

As Inland Revenue notes, one answer would be to align the company, personal and trust tax rates. This was the case until 1999, when the rate was 33% for companies, individuals and for trusts. But this ended on 1 April 2000 when the individual top rate went up to 39%. And since then, the company income tax rate has fallen to 28%.

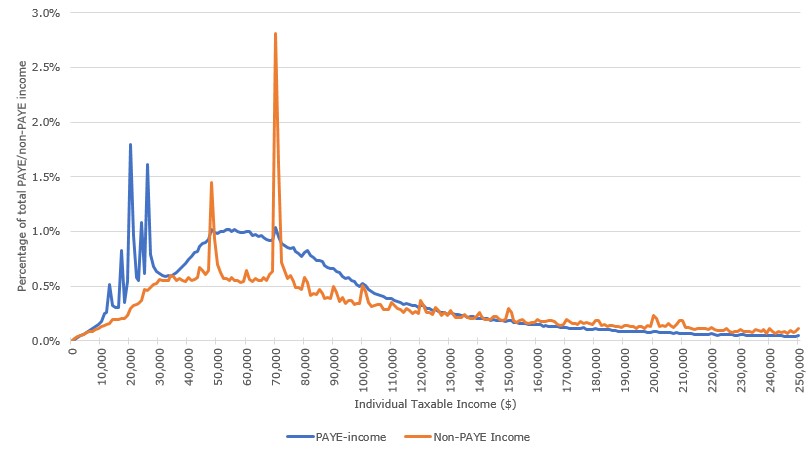

So this is a matter which needs to be addressed. There’s a really interesting graph illustrating the distribution of taxable income and noting there’s a huge spike at around $70,000, where the tax rate rises to 33%.

Taxable income distribution: PAYE and non-PAYE income (year ended 31 March 2020)

There’s also some interesting data around what high wealth individuals pay in tax. For the 2018 income year, Inland Revenue calculated the 350 richest individuals in New Zealand paid $26 million in tax. Meanwhile the 8,468 companies and 1,867 trusts they controlled, paid a further $639 million and $102 million in tax respectively, indicating a significant amount of income earned through lower rate entities.

It appears to Inland Revenue that tax is being deferred through retention of dividends in companies.

The opportunity in New Zealand is that a sale of the shares under current legislation would bypass the potential liability on distribution. The shareholder is basically able to convert what would be income if it was distributed to him or her, to a capital gain. And clearly, the Government wants to put an end to that, but can’t because it doesn’t have a capital gains tax. The discussion document therefore proposes that any sale of shares in the company will be deemed to give rise to a dividend. This will trigger a tax liability for the shareholder.

The paper goes into detail around this particular issue, and I think this is going to be quite controversial. Because although I could see a measure where a controlling shareholder sells shares to a related party such as, for example, someone holding shares personally sells them to a trust or to a holding company, which they control. You could see straight away that Inland Revenue could counter this by arguing it’s tax avoidance.

But the matter gets more complicated where third parties are involved. And this is where I think the rules are going to cause some consternation because it proposes transactions involving third parties would also be subject to this rule. That, I think is where most pushback will come in on this position. Without getting into a lot of detail on this there could be genuine commercial transactions resulting in some might say is a de facto capital gains tax.

The proposal is not all bad. If a dividend is triggered, then the company will receive a credit to what is called its available subscribed capital, ie, its share capital, which can later be distributed essentially tax free.

In making its proposals, the paper looks at what happens in Australia, the Netherlands and Japan and draws on some ideas from there. It’s interesting to see Inland Revenue looking at overseas examples. All three of those jurisdictions, to my knowledge, have capital gains tax as well, but they still have these integrity measures.

But the key point is this question that any sale, will trigger a dividend. There’s no de-minimis proposed. This could disadvantage a company trying to expand by bringing in new shareholders. It might have to use cash reserves it wants to keep to pay the withholding tax on the deemed dividend. The potentially adverse tax consequences for its shareholders might hinder that expansion. I expect there will be a fair degree of pushback as a lot of thought will go into responding to this proposal. It will be interesting to see exactly what comes back.

Cleaning up tracking accounts

Less controversial and something probably overdue, is the proposal for what they call tracking accounts to cover the question of a company’s available subscribed capital, and the available capital distribution amounts realised from capital gains. Both of these may be distributed tax free either on liquidation or in a share cancellation in the case of available subscribed capital. But the requirement for companies to track this is rather limited, and these are very complicated transactions.

As the paper points out, the definition of ‘available subscribed capital’ runs to 40 subsections and 2820 words. So, there’s a lot of detail to work through, and if companies haven’t kept up their records on this, then confusion may arise if, say, 10 years down the track they’re looking to either liquidate or make a share cancellation.

I don’t see this proposal causing much controversy. I think Inland Revenue’s proposals here are fair and probably something that should have been done a long time ago. They will apply on a prospective basis, as I mentioned earlier on.

Personal services income attribution – a 50% rule?

And then finally, the third part deals with personal services income attribution. And what this part does is picking up the principles from the Penny and Hooper decision. This was the tax case involving two orthopaedic surgeons, which ruled on the tax avoidance issues arising from the last time the tax rate was increased to 39%.

The discussion document is basically trying to codify that decision. The intention is to put an end to people attempting to use what you might call interposed entities, lower rate entities, to avoid paying tax personally. The particular issue it’s driving at is when an individual, referred to as a working person, performs personal services and is associated with an entity, a company usually, that provides those personal services to a third person, the buyer.

Inland Revenue is now looking at a fundamental redesign of this personal service attribution rule, which was designed to capture employment like situations. It was really designed where contractors might be providing services to basically one customer (the ‘80% one buyer rule’) and in effect, they were employees. However, they could potentially avoid tax obligations by making use of an interposed entity with a lower tax rate.

Inland Revenue thinks that 80% rule is too narrow. The proposal is to broaden its application and by doing so it can at the same time deal with the issue that arose with the Penny and Hooper case.

Under current legislation, Bill is an accountant who is the sole employee and shareholder of his company A-plus Accounting Limited. The company pays tax at 28% on income from accounting services provided to clients and pays Bill a salary of $70,000, just below the 33% threshold. Any residual profits are either retained in the company or made available to Bill as loans.

The proposal is to remove that 80% one buyer rule and so that now Bill’s net income for the year, if it exceeds $70,000 will all be attributed to him where 80% of the services sold by that company are provided by Bill. Sole practitioners and smaller accounting firms and tax agents will find themselves in the gun. In fact, the discussion document suggests maybe this threshold of 80% should be lowered to 50%.

Now, you might think that the bigger issue is not the 33% threshold at $70,000, but the $180,000 threshold, so why do we want such a low threshold for this rule to apply? The discussion document points to the evidence that shows that there is income deferral going on. It appears to be at the $70,000 threshold (see the graph above) and wants to put an end to that.

So that’s a more detailed look at what is a very important paper. It’s likely to generate quite a lot of controversy and feedback from accountants and other tax specialists. It’s also another part in the long running tale of the implications of not having a capital gains tax. But certainly, this one will run and run. Submissions are now open and will run through until 29th April. I expect all the major accounting bodies and firms will be responding.

Using tax to mitigate cost of living impacts

Moving on briefly, there’s been a lot to talk about what tax changes could be done to help the increased cost of living. And Daniel Dunkley ran through some of the proposals.

One idea that pops up regularly is the question of removing GST from food. My view, which I expressed to Daniel and is also probably that of most tax specialists, is that this would undermine the integrity of GST, because we don’t have any exemptions on that.

I also don’t think it would achieve the objective that is hoped for. There is, regardless of what people might say, an administrative cost to splitting out tax rates, having zero rate for food and standard rate for other household goods in your shopping trolley. And that differential, that cost involved, will be passed on to customers.

So the full effect of the GST decrease will never flow through to customers. To be perfectly frank; supermarkets and operators will play the margins around this. I suggest you have a look at what’s happened with the fuel excise cut. It was 25 cents, but in every case did the pump price fall by 25 cents? And how could you tell because prices move around so much?

As I said to Daniel, and has been a longstanding view of mine, if the issue is getting money to people who have not enough money, give them more money. The Welfare Expert Advisory Group was staunch when it said that there was a desperate need to raise benefits. We also saw how the temporary JobSeeker rate was increased when COVID first hit. So, this issue of increasing benefits hasn’t gone away.

The best position would not be to tinker with the tax system. You could perhaps look at tax thresholds, definitely, but they still would not be as effective as giving people an extra $30-40 or more cash in hand.

End of year preparations

And finally, the end of the tax year is fast approaching, so there’s plenty of tax issues that you might want to get done before 31st March. A key one to think about is if you’re going to enter the look through company regime, you need to get the election in before the start of the tax year. In some situations you might have more of a bit of a grace period for dropping out of the regime, as part of the Government’s response to the Omicron variant. But it you are electing to join the regime, I suggest you file the election on or before 31st March.

Coming back to companies and shareholders another important issue is the current accounts of the shareholders. You should check to see if any shareholder has an overdrawn current account (that is more drawings than earnings). If so, then either see about paying a dividend or a salary to clear that negative balance, although of course, you’re up against the issue of the higher tax rate I discussed earlier. If that’s not possible, charge interest at the prescribed fringe benefit tax rate of 4.5%.

Companies may have made loan advances to other companies, look at those carefully because you may need to charge interest there to avoid what we call a deemed dividend.

Another very important matter is if there are any bad debts. If so, then consider writing them off before 31st March in order to claim a deduction. And then if you’re thinking about bringing forward expenditure to claim deductions such on depreciation, then do so.

Companies should check their imputation credit accounts balances and make sure these are positive. There are mechanisms through tax pooling to manage this problem if you miss a negative balance.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax tax or wherever you get your podcasts. Thank you for listening, and please send me your feedback and tell your friends and clients. Until next time, ka pai te wiki, have a great week.