Rachel Reeves, the first ever female Chancellor of the Exchequer delivers a UK Autumn Budget with potentially significant implications for many Kiwis and Britons who have migrated to New Zealand.

Meanwhile Inland Revenue’s crackdown on tax evasion continues.

The UK finance minister is officially called the Chancellor of the Exchequer, a post which is more than 800 years old, and until this year it had never been held by a woman. So, when Rachel Reeves, the Labour Chancellor of the Exchequer delivered her maiden budget speech last Wednesday night, she made history as the first woman Chancellor in British history.

There was quite a lot to consider in this UK Budget, as people were watching to see how the new government would respond to the challenges it inherited. British budgets, unlike ours, coincide with the release of a Finance Bill and tax measures there’s always a lot of tax matters to consider beyond the headline measures.

The headline measures

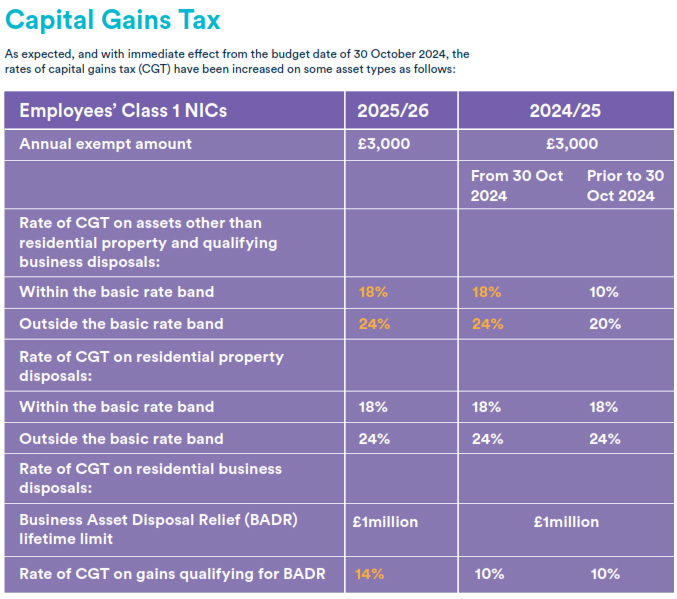

Most notably, there was an increase in Employer National Insurance Contributions (a Social Security tax) by 1.2 percentage points to 15% with immediate effect. There are also immediate tax rises for capital gains tax, but the top rate for capital gains tax still was capped at 24% for both property and non-property assets. Which as some commentators said is still lower than countries with which the UK compares itself. It’s quite interesting to see that comment about 24%, because one of the key points of our discussion around capital gains taxes here is what rate would apply? It’s therefore interesting to have an international comparison.

Beyond the headlines

It’s always interesting to dig around in other countries’ budgets and see what they do in certain areas. For example, the UK doesn’t have an imputation credit system, but there are lower rates of tax applied to dividends, even for those on the highest income. There’s also a savings allowance, which exempts certain amounts of investment income. It’s currently £1,000 for basic rate taxpayers (taxable income up to £37,700) and £500 for the higher rate taxpayers. The UK basic rate of tax is 20% and we have two rates lower than that so this savings allowance is not necessarily a measure we might want to copy here.

Twin cab utes and fringe benefits – an example to follow?

There’s apparently some uncertainty around the fringe benefit taxation treatment of twin cab utes which the Budget clarified. Where they have a payload of one tonne or more such vehicles are not there to be treated as cars for benefit in kind purposes unless they were acquired prior to 6th April 2025.

On Fringe Benefit Tax, the benefit value is calculated as a percentage of the vehicle’s list price when the car was first registered which is similar to our treatment. However, the percentage used is determined by the vehicle’s carbon dioxide emissions, or its range if it’s an electric vehicle. These percentages are set to increase steadily over the next three years as part of the range of tax increases announced. Inland Revenue is presently reviewing FBT and as is well known tax can act as a disincentive. If we want to incentivise a transition to a lower emissions economy, maybe we should be looking at how the UK applies FBT to vehicles.

UK pension tax free lump sum unchanged

There’s always lots of rumours before a Budget which I’ve seen sometimes used as a means to get people to buy new products or make tax driven decisions in fear of change. One of the rumours before this budget was that there were going to be changes to the taxation of pensions and in particular to the 25% tax free lump sum. That hasn’t happened, but remember, our rules are completely different. Just because 25% of the pension can be withdrawn tax free in the UK, that doesn’t mean the same rules apply here.

The big changes

But the main reason I was paying particular attention to this UK budget was because we finally got more detail around the two announcements made in the March Budget – the new foreign and income gains regime and the end of the non-domicile regime and the changes to inheritance tax. These are both measures which have significant impact for New Zealanders, who are either going to the UK or have returned to the UK, but also for UK expats who have migrated here.

New foreign income and gains regime

The foreign income gains (FIGS) regime is very similar to our transitional resident’s exemption in that a new tax resident’s foreign income and capital gains will be tax exempt for the first four UK tax years that they are resident in the UK. It’s not like our 48-month exemption period, it is tied to the UK tax year, which remember runs from 6th April to 5th April. (Perhaps reflecting that some of this stuff does date back 800 years or more, there’s no intention to change that tax year end).

What has also been clarified is that individuals who have previously elected to be taxed on the remittance basis, which meant their non-UK sourced income investment income was not taxable, can now be allowed to take advantage of a so-called temporary repatriation facility. This will last for three years, and they will be able to nominate and remit their non-UK income and gains from years when they were within the remittance basis and take advantage of lower tax rates. Initially 12% for the first two years ending 5th April 2026 and 2027, and then 15% for the year ended 5th April 2028.

As part of the FIGS regime there are also changes to what’s called the Overseas Workday Relief. This will allow UK tax resident employees who perform all or some of their duties outside of the UK to claim tax relief on the remuneration relating to their non-UK duties determined on “a just and reasonable basis”. This is quite a significant one for expats and for companies that have very highly paid and skilled employees and has been greeted with general enthusiasm by by those impacted.

Inheritance Tax

Potentially the biggest change though, is in relation to inheritance tax (IHT). This applies to all assets situated in the UK or all assets situated anywhere, if the person is domiciled within the UK. There’s a nil rate band of £325,000, above which 40% will apply (these rates and thresholds have been frozen until 2030). IHT has a potentially significant impact because under the present rules, someone tax resident outside the UK could still be within the IHT net because they are still deemed to be domiciled in the UK. I’ve had to deal with one or two of these instances.

There’s also a pretty nasty trap for someone like me who might have left the UK a long time ago and adopted a new domicile of choice outside the UK. At present if I ever became tax resident again in the UK, our domicile would immediately revert to the UK. Therefore, working or living for prolonged periods of time in the UK was actually potentially highly tax disadvantageous from an IHT perspective.

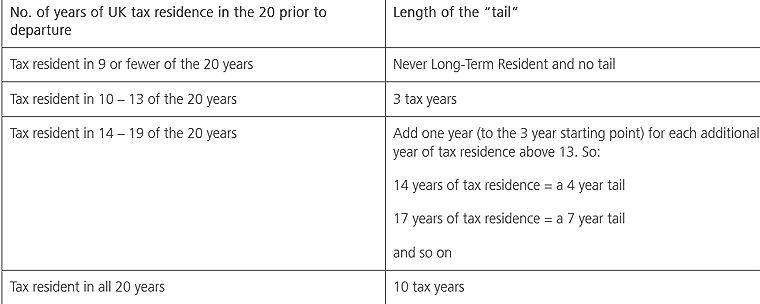

All this will be replaced now by a residence-based regime. The tests for whether non-UK assets are subject to IHT will now be whether the individual has been tax resident in the UK for at least 10 out of the last 20 tax years immediately preceding the tax year in which the chargeable event, most typically death, but can also be a lifetime transfer into a trust, happens.

There’s also a tail on how long a person is in scope if they’ve been non-resident during a period. For example, if someone had been UK tax resident for between 10 and 13 years, they remain in scope for IHT for three years post departure.

(Courtesy Burges Salmon)

Implications for New Zealand residents

What this change means for a lot of British expats resident here is they’ve got to think again about what their IHT obligations could be. By the way, our double tax agreement with the UK does not cover IHT. The UK has the right to charge IHT on assets situated in the UK, that’s not surprising. However, it potentially also has got a long reach if HM Revenue & Customs determine someone resident here is subject to IHT.

IHT and trusts

One of the other IHT changes is to the taxation of trusts used to hold assets outside the scope of IHT, so-called excluded property trusts. If I understand it right, starting from 6th April 2025, if a settlor dies and they’re within the scope of IHT, assets settled by them into what was previously an excluded property trust are now within IHT. This is a major change and I’m investigating it further given we make very extensive use of trusts. I’ve been dealing with quite a few clients who have UK connections year and it’s been really revealing to see how complex the taxation of trusts is from the UK perspective. It’s good to see some clarity around the new rules, but as I say, it’s a significant budget in many ways, and there could be quite major consequences for more people based here than they might anticipate.

Meanwhile, Inland Revenue’s crackdown continues

Moving on, Inland Revenue continues its crackdown when it announced on Thursday that it’s making unannounced visits to hundreds of businesses who it believes are not meeting all their tax obligations as employers.

According to Inland Revenue, they receive about 7000 anonymous tip offs each year. It has said “the volume of tip offs has grown over previous years indicating an increased sense of frustration by the community in general, businesses who are not doing the right thing.”

Inland Revenue’s analysis shows that the tax risks overwhelmingly relate to taking cash for personal use without reporting sales and or paying employees in cash.

Based on this Inland Revenue is making unannounced visits to over 300 employers whose practices it will closely examine. I’ve seen this happen with a few clients under investigation. Inland Revenue staff will go to a café or business and just watch to see what’s happening. They may buy something, but they will certainly sit and observe and see who uses the till, how everything is recorded and from there they will draw the relevant conclusions.

The consequences of being investigated

As an example of what happens to taxpayers who have not been compliant, the director of an asbestos removal and labour hire company has been jailed for three years in what the judge called serious offending and the worst of its kind to come before the Christchurch District Court in the last 20 years. The director, Melanie Jill Tatana, also known as Melanie Jill Smith, was jailed for three years for what was described as wilful diversion of funds.

Her company employed around 60 people, and between April 2019 and September 2022 had been required to deduct PAYE on 63 occasions but failed to pay the full amounts totalling $1.6 million. Tatana was therefore charged with 63 counts of aiding and abetting to knowingly take PAYE from workers’ wages and not pay it on to Inland Revenue. Instead, more than $800,000 had been diverted for her personal use.

One of the more encouraging things from my perspective about this case is that this offending has all been pretty recent and Inland Revenue tracked it down within a couple of years. I’ve seen cases where the offending has been four or five years.

I still think 63 occasions of nonpayment is a little generous, but bear in mind that Inland Revenue did take the the foot off the throttle around pushing hard on on companies and businesses because of COVID. That amnesty or less stringent approach is now over and it’s back to business. And Tatana won’t be the first to find out about Inland Revenue’s hardline approach.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Thousands here could be potentially subject to UK Inheritance Tax.

Airbnb and Uber are not happy about a GST law change.

GST for all its complexities, is the best example of the Broad Base Low-Rate tax principle, a single rate of 15% applied broadly. However, one of the ongoing controversies with GST is around its application to food and other basic necessities. New Zealand’s approach is at odds with many other countries, such as Australia or the UK, where food is not subject to GST (or VAT, as the UK calls it).

Frequently we see commentary that it would be a good move to help lower income earners by removing GST on food. This has been suggested as a response to the current cost of living crisis. I am opposed to such moves and many GST specialists are also in the same camp. Firstly, I don’t think this move is effective as proponents believe, and secondly, if the issue being addressed is low income, then it is better, in my view, to give more income to that target group rather than using a tax measure which would benefit more people, including some who we probably think don’t need assistance.

A report released yesterday in the UK regarding the impact of the withdrawal of the so-called tampon tax bears out these concerns of myself and other GST specialists about introducing GST exemptions. In the UK, VAT of 5% used to apply to tampons and other menstrual products until January 2021, when it was abolished. Prior to its abolition, VAT specialists predicted that the full benefit of abolition would not be reflected in lower prices. And a report by Tax Policy Associates bears this fear out. According to the report, at least 80% of the savings from the tax savings was retained by retailers. In fact the report questions whether any of the benefit of the removal of VAT ever passed through to lower prices.

Professor Rita de la Feria the chair of tax law at the University of Leeds was one of those who warned beforehand of this likely outcome. Commenting on the report she noted this was not only predictable but predicted. In her view “we have to stop confusing policy aim with policy instrument and we also need to stop using tax policy instruments to signal we care about the policy aim.”

Those are wise words and should be kept in mind next time you hear calls for tax changes for ostensibly very sensible reasons. In tax, even with well-meaning policy, there are always unintended consequences and tax is not always the most appropriate mechanism. Sometimes direct action, such as giving payments to those affected, or supplying tampons for free is the best approach.

How UK tax law applies to NZ residents

Staying in the UK, next week the latest Chancellor of the Exchequer, Jeremy Hunt, Grant Robertson’s equivalent, will be presenting the Autumn Statement. He is expected to introduce a number of tax changes and tax increases in an effort to try and restore the UK’s finances. Hunt, incidentally, is the fourth chancellor this year, whereas Grant Robertson is only the fourth New Zealand finance minister this century. So that gives you a measure of just how much upheaval has been going on up there.

I regularly advise New Zealanders and migrants from the UK about UK tax matters. Frequently there are ongoing issues for them and inevitably complexities creep in.

Based on my experience, there are probably thousands of New Zealanders and family trusts who may unwittingly have UK tax obligations. There are also former residents from the UK who are now living here who misunderstand the relationship between the UK and New Zealand tax treatments of investments. So here’s a quick summary of those people who may be affected by UK tax and the differing tax rules between New Zealand and the UK.

Firstly, if you have property in the UK, then UK capital gains tax will apply to any disposals. There are strict timelines about reporting those disposals which are unrealistic in my view, but they still apply. CGT will apply even though the disposal might not be taxable for New Zealand purposes. By the way, the bright line test does apply to overseas property.

If you were renting a property out in the UK then you must report that income both in the UK and in New Zealand. However, for New Zealand purposes, any UK tax paid will be given as a credit against your New Zealand tax payable.

As should be well-known transfers of, or withdrawals from UK pension schemes are subject to New Zealand income tax. I don’t agree with that policy but it’s the law. In addition, if you are receiving a pension from the UK then the UK pension scheme should not be deducting any PAYE. You will need to apply to H.M. Revenue and Customs through Inland Revenue to get any refund of any such tax deducted. By the way, Inland Revenue will not give you a credit for any tax deducted, it wants the tax paid here. That’s the procedure under the double tax treaty and you’ll have to go and get the PAYE back off HMRC, which can be a very frustrating experience, believe me.

But potentially the most significant tax that will apply, which is also the least known, is Inheritance Tax. Inheritance Tax applies firstly to any assets situated in the UK. So, if a New Zealander who worked over in London, bought an investment property there before moving back here, that property is in the UK Inheritance Tax net.

Secondly Inheritance Tax also applies on a global basis to all assets wherever they’re situated if you are “domiciled” or deemed to be domiciled in the UK. Domicile is a complicated concept which I am not going to get into now. But basically, pretty much anyone born in the UK who’s migrated here in the last ten years or so probably still is domiciled for UK tax purposes. If you were a Kiwi and you spent more than 15 years in the UK, you may also be deemed to be domiciled in the UK. If so, Inheritance Tax applies at a rate of 40% on all assets over the first £325,000. (The price of New Zealand property means that this threshold is comfortably exceeded).

In my experience, many migrants and returning Kiwis are completely unaware of the potential impact of Inheritance Tax. For example, UK Inheritance Tax law does not recognise de facto relationships (apparently much to the relief of several politicians a partner in a London law firm once told me). I once dealt with a scenario where the New Zealand resident survivor of an unmarried couple had to pay over £50,000 of Inheritance Tax on her share of a jointly owned New Zealand property after her Scottish partner’s death.

Finally, the UK has a trust register which arrived in the wake of anti-money laundering legislation and its use has been greatly expanded. Any trust which has property in the UK must register. Furthermore, any trust which has a UK source of income such as bank interest must register if it has beneficiaries, including discretionary beneficiaries who are resident in the UK. This is a common scenario I’ve seen. It appears this registration requirement applies even if no distributions have ever been made to the UK situated beneficiaries. There’s some controversy about that particular provision because it appears New Zealand trusts may even have to file UK tax returns even if all the UK income is being distributed to New Zealand beneficiaries.

So that’s a quick summary of some of the UK tax issues which I commonly encounter. I’ll look to update this summary next week if there are any developments from the Chancellor’s Autumn Statement. Now is maybe time to have a look at your position to see if, in fact, you might potentially have a UK tax issue. And also keep in mind that Inland Revenue is currently running an initiative where it is checking on people’s potential tax obligations from their overseas investments.

“We want to remain tax-free”

Finally, this week and back to GST, Airbnb made a submission to Parliament’s Financial Expenditure Select Committee complaining about the proposal for it to charge GST on all accommodation bookings made through its platform.

In its submission, it warned this would stifle the country’s economic recovery and cost the economy up to $500 million a year.

Now this measure was introduced in the Taxation (Annual Rates for 2022-23, Platform Economy, and Remedial Matters) Bill (No 2). Airbnb along with Uber, also affected by the new proposals, unsurprisingly, think the law changes are unfair. On the other hand, the Hospitality Association was amongst those submitting in favour of the change. Chief executive Julie White said a third of its membership consists of commercial accommodation providers adding “and a consistent frustration of theirs is a lack of level playing field when it comes to services like Airbnb”.

The comments from Uber and Airbnb are unsurprising to me. But what I did find of interest about the bill was there have been quite a considerable number of submissions made 820 so far, and quite a few from individuals who would be affected. To quote one, “this law change will result in fewer bookings to me and significantly impact my retirement plans. This will have the additional impact of higher costs of vacations for New Zealand families who are largely for larger families and cannot afford to stay in a hotel.”

Another submitter thought “This action will have a huge negative impact on a new form of tourism at a very personal, localised level.” I’m personally not sure that the impact will be quite as dramatic as those submitters suggest, but it is interesting to see the reaction to what might be seen as a relatively straightforward GST proposal.

As is often the case, many other submitters took the opportunity to push for other changes, such as several suggesting for the removal of FBT on the provision e-bikes to employees.

There was also criticism of the complexity of the interest,limitation and bright-line test rules. One submitter noted that the commentary to the bill had more than 28 pages devoted to remedial provisions for this legislation, and he concluded correctly, in my view, “it is simply not appropriate to expect most landlords to be able to apply the detail of tax law of this complexity.”

Incidentally, the same submitter suggested that because the interest limitation measures had been introduced partly in response to rising house prices, now house prices were falling logically the interest limitation measures should be repealed. It’s a fair point, and he wasn’t the only one to make it. But somehow I can’t see that happening. To leave off where we came in this is another situation where the policy aim and policy instruments have got confused.

At last week’s International Fiscal Association conference, Revenue Minister David Parker announced that the Government would be proceeding with a new business continuity test to enable tax losses to be carried forward. The general rule is that for tax losses to be carried forward, at least 49% of the shareholding in the company must remain the same between the date the losses arise and when the losses are to be used.

Now, this is regarded as one of the most stringent loss continuity tests in the world, and it has been seen as an impediment for businesses trying to obtain capital in order to innovate and grow their growth.

Companies in their early stages may rack up a lot of losses, but if they want to attract capital and investors shareholding changes may mean a loss of accumulated tax losses. So there’s been pressure for some time to think about easing these restrictions and adding a what we call business continuity test.

The idea is a similar business test will now be able to apply, and even if the 49% threshold might have been breached, the company may continue to carry its losses forward after a change in ownership as long as the underlying business continues. Now, similar tests apply in Britain and in Australia, and the Australian test has been used for the purposes of designing our legislation.

The principle is that losses will be carried forward unless there’s a major change in the nature of the company’s business activities.

In determining this, you’d look at the assets used and other relevant factors, such as business processes, users, suppliers, market supply to and the type of product or services supplied.

There is an expectation that the test will run for the time from the ownership change, which brought about a 49% breach of shareholding continuity, as we call it, until the earliest of the end of the income year in which tax losses are utilised or at the end of the income year, five years after the ownership change. This is subject to one or two exceptions as well as a specific anti avoidance measure to prevent possible manipulation of the rule.

The rule would appear to be retrospectively applicable from the start of the current tax year or 1st April, 2020 for most businesses. But that’s not absolutely specifically spelt out, but is implied by the commentary we’ve received. We’ll know for sure when we see the final legislation in the next week or so.

This is a very positive measure. It’s been one that businesses have been asking for for some time, particularly those in their high growth tech sector, where they rack up a lot of losses during development before switching to substantial profitability. But they’ve been unable to attract or had difficulty attracting investors because of the existing loss continuity rules.

The fiscal cost is actually quite modest. It’s estimated to be about $60 million per annum, which still does beg the question that perhaps this could have been addressed much sooner. It’s certainly been on the wish list for a lot of investors for some time and was a matter we raised on the Small Business Council. It’s a good development and I imagine that it will be taken up with some enthusiasm.

The US changes its tune

Moving on, I’ve recently discussed the issues around the taxation of digital companies, particularly in relation to Facebook’s stoush with the Australian government. The OECD, as I mentioned in previous podcasts, has been working through what it called a new global framework and two options to this Pillar One and Pillar Two.

This week, there was a major development with the US Treasury Secretary, Janet Yellen, (the equivalent of the finance minister), telling G20 officials that Washington was going to drop the Trump administration’s proposal to allow some companies to opt out of the new global digital tax rules. And this was clearly seen as an impediment to getting these rules through. But the fact that these have now been dropped and that the US is no longer advocating for a safe harbour in relation to Pillar One is very important.

The OECD has been working through matters in relation to the development of the new global framework. This week it announced it now believes it’s got the 10 components of Pillar One put together on which it can now start to build a consensus. Drafts of these Pillar One proposals are expected to be released in the next few months. The hope is still to have this all wrapped up sometime this year.

So that’s a very positive development. As I said, in relation to the Facebook and Australia stoush, some form of taxation probably would have been a better approach to the matter than what has been proposed by the Australian government.

UK Budget implications

And finally, on Wednesday night, our time, the UK Budget for 2021 was released. Now, this is of more importance to Kiwis than people might realise because of the global reach of UK capital gains tax and inheritance tax in particular.

To recap, anyone who owns property, commercial or residential in the UK is subject to capital gains tax on a disposal of that property. So this would affect the some 300,000 Britons or people of British descent like myself who live here in New Zealand. But it also affects Kiwis who come back from their OE but have retained a property for whatever reason in the UK.

The other significant UK tax issue, which I’m seeing a lot more of, is Inheritance Tax. And this applies globally to anyone who has a UK domicile (which is a different concept from tax residency) or assets situated in the UK. Inheritance Tax applies at a rate of 40% on the value of an estate greater than £325,000 (what we call the Nil Rate Band).

But the UK budget has frozen the Inheritance Tax nil rate band at £325,000 right through until 2026. The annual capital gains allowance is also going to be frozen for a further five year period.

One of the things that is perhaps not really appreciated is anyone who is deemed to have a UK domicile are taxed for Inheritance Tax purposes on their global assets. And with the fall in the value of sterling to below two dollars to the pound, combined with the incredible rise in the value of New Zealand property, what I’m seeing is that people now have potentially significant Inheritance Tax issues. Property prices in the UK have not accelerated anywhere near to the fashion that has happened here. To give you an example, I came across this week a client with a London property valued in April 2015 at £775 ,000. Its current value is just £765,000 pounds. In other words, over six years it’s gone backwards. Compare that with what’s going on in the New Zealand market.

So there’s an increasing number of New Zealanders and Britons who have potentially Inheritance Tax liabilities. And they also will face capital gains tax if they decide to dispose of those properties. One of the things that’s also increasingly coming into play will be the information sharing under the Common Reporting Standards and The Automatic Exchange of Information. This means the UK HM Revenue & Customs and Inland Revenue here will have a greater understanding of who owns property in which jurisdiction.

So, as I said, this British budget may seem far away, but it’s actually incredibly important to a significantly greater number of people than you might imagine.

There’s also one other thing that’s come into play, which has been a surprise to the tax community and that is the British Government have signalled an increase in the corporation tax rate from its current rate of 19% to 25% for businesses with net profit in excess of £250,000 from 1st of April 2023. That’s a very significant increase. The other thing that the British have also kept in place is what they call a diverted profits tax, of which remains at 6%. This is an anti-avoidance measure aimed at multinationals.

Incidentally if Grant Robertson and Treasury are looking for ideas the UK also has a bank corporation tax surcharge of 8%. This is something which if introduced here would probably be quite popular.

The proposed increase in corporation tax rates is a surprise. But I think this is something that’s gradually become inevitable. In the wake of both the GFC and Covid-19, government budgets are so badly shot that they need to restore them with significant tax increases at some point. Whether any such increases flow through here to the extent of what’s just happened in the UK remains to be seen. But as always, we’ll keep you abreast of developments.

That’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week Ka kite ano!

1966 and all that: The chequered history of entertainers, sports stars and tax

What have William Shakespeare, The Beatles, The Rolling Stones, U2, Norman Wisdom, Richard Burton, Boris Becker, Lionel Messi, Christian Ronaldo and Bobby Moore all got in common? They are but a few of the many, very many, actors, entertainers and sports stars who have found themselves in trouble (sometimes bigly) with the taxman.

One reason entertainers and sports stars run into money and tax problems so frequently is that they work in an industry where vast sums of money can be generated practically overnight from all around the world. Consequently, musicians and bands probably have some of the most complex tax affairs outside of multinationals. It’s therefore unsurprising many engage in elaborate tax planning and it’s equally unsurprising this sometimes comes unstuck with expensive consequences.

This Top Five looks at actors, musicians and footballers who left a tax legacy as well as an artistic one. Moreover, these tax legacies remain highly relevant today.

1.“Know you of this taxation?” (Henry VIII).

Despite his colossal cultural legacy, we know very little about the real Shakespeare. We do know that between 1597 and 1600 he appears in several rolls for the “lay subsidies” for the St Helen’s Bishopgate parish in London. Lay subsidies were a form of local wealth tax on local householders. The lay subsidy roll contained an estimate of a person’s wealth and the amount assessed.

It appears that in 1598 Shakespeare defaulted on his lay subsidy for the year of 13 shillings and four pence. It’s not known whether this debt was ever paid but since about this time he bought into the Globe Playhouse for £70, he was surely not short of money. This has led to much conjecture about whether Shakespeare was one of the first known tax avoiders of the entertainment industry.

Like so much else about the man, we’ll never know the truth about Shakespeare’s finances. I can’t help but wonder if the quip in Henry VI“The first thing we do, let’s kill all the lawyers” might reference some dud tax advice he received.

2. From Abbey Road to Exile on Main Street.

It appears The Beatles were pioneers in tax planning for musicians. Very early on in their career they were introduced to accountant Harry Pinsker who specialised in the entertainment area. (Pinsker’s first reaction was that “they were just four scruffy boys”).

One of Pinsker’s recommendations was a songwriting company Lenmac through which their earnings would be channelled. He successfully argued the company’s income should be taxed as trading income rather than investment income which would have incurred higher taxes.

Even so, the very high tax rates of the mid-60s (more than 90%) prompted George Harrison to write Taxman.

“One, two, three, four, one, two

Let me tell you how it will be There’s one for you, nineteen for me ‘Cause I’m the taxman, yeah, I’m the taxman”

Pinsker ultimately suggested the formation of Apple Records as a tax effective means of managing the band’s revenue. His efforts did not go unnoticed by the Beatles. During rehearsals of their final album Let it Be, the band started singing Harry Pinsker instead of Hare Krishna.

The Rolling Stones weren’t as well managed as The Beatles and in 1971, facing huge tax bills, they moved to the south of France where they recorded one of their greatest albums: Exile on Main Street.The title was a deliberate reference to their tax exile.

Having also fallen out with Decca Records and their manager Allen Klein, the band took control of their affairs at this time by forming their own record company. They also established a Netherlands company to shelter their income. This started a trend which other bands including U2 would follow.

The Rolling Stones move into tax exile didn’t attract much criticism at the time, perhaps because the rates of tax they then faced were so high. Forty years on attitudes have changed.

U2 were in town recently and their tax practices have drawn increasing criticism. Lead singer Bono has been accused of hypocrisy after he was linked to the Panama Papers.

In 2015 Bono and U2 were criticised for making changes to shift royalties through the Netherlands to take advantage of a special concession. Now it appears this concession is ending.

If U2 still haven’t found the perfect tax structure they were looking for, The Rolling Stones should remind them “You can’t always get what you want.”

3. The slapstick clown with a tax lesson for crypto-asset investors.

The British comic Sir Norman Wisdom rose to fame in the 1950s playing a hapless but good-natured incompetent who somehow through a combination of slapstick humour and good fortune saves the day.

Contrary to his clownish on-screen character, Wisdom was a very shrewd investor, and this ultimately resulted in one of the more notable and still influential tax cases of the 1960s.

In 1961 Wisdom invested in silver ingots as a hedge against a possible devaluation of the British Pound, eventually realising a profit of £48,000 (about £800,000 today). At a time of very high personal tax rates Wisdom claimed the profit was a tax free capital gain (the transaction occurred prior to the introduction of capital gains tax in Britain).

Wisdom won in the High Court but in 1968 the Court of Appeal in Wisdom v Chamberlain (Inspector of Taxes) determined that the transaction was in the nature of trade and therefore taxable. Wisdom paid the tax due and outraged by the high taxes then went into tax exile in the Isle of Man where he lived until his death in 2010.

His case is often cited when considering whether a transaction is of a revenue or capital nature. In 2017 Inland Revenue cited it in a “Question We’ve Been Asked” on whether the proceeds of the sale of gold bullion would be income. (The short answer is almost certainly).

Inland Revenue also consider some crypto-assets to have similar characteristics to bullion. It is therefore probably only a matter of time before some crypto-asset investors will need to acquaint themselves with Wisdom v Chamberlain and Norman Wisdom’s unwilling tax legacy.

4. Gone for a Burton.

Richard Burton was probably too busy being one of the great actor hell-raisers of the 1960s to be paying attention to the price of silver bullion. Yet, he too has left a tax legacy, one of particular relevance to many of the thousands of Britons currently living in New Zealand.

Burton became a tax exile in the late 1950s after taxes had reduced his earnings of £82,000 for 1957 to £6,000. (Allegedly he subsequently remarked “I believe that everyone should paythem [taxes] — except actors.”) Burton moved to Switzerland where he lived until his death in 1984.

Burton was buried in Switzerland, apparently in a red suit together with a copy of Dylan Thomas’ poems. However, many years earlier when he was married to Elizabeth Taylor, Burton had acquired two burial plots for himself and Taylor in the Welsh village where he had been born. And this proved extremely costly for Burton’s estate.

Inland Revenue argued successfully that the presence of the burial plots together with his Welsh themed funeral meant that Burton had never lost his UK tax domicile. Accordingly, his estate worth just over £4 million had to pay a total of £2.4 million in Inheritance Tax.

In my view Inheritance Tax represents the greatest tax risk to anyone either born in the UK or who owns assets situated there. The lesson from Richard Burton’s death is that Inheritance Tax could still apply many years after a person has left the UK.

5. England, One; HM Inspector of Taxes, Nil.

November 22 was the anniversary of when England won the Rugby World Cup in 2003. In the wake of England’s unexpected defeat by South Africa I saw a perhaps rather too gleeful tweet asking if 2003 was destined to become English rugby’s equivalent of England’s sole football World Cup win in 1966.

Anyway, back in 1966 the English Football Association rewarded its world cup winning squad with £1,000 each. (About £15,000 in current terms or only 30% of the English Premier League’s current AVERAGE weekly wage of £50,000). Enter the Inland Revenue stage right in the form of HM Inspector of Taxes Mr Griffiths. He considered the amounts paid to England’s captain Bobby Moore and cup-final hat-trick hero Geoff Hurst were taxable as they formed part of their remuneration.

The case finally reached the High Court in 1972 where Mr Justice Brightman ruled the £1,000 payments were non-taxable as they had the “quality of a testimonial or accolade rather than the quality of remuneration for services rendered”. A convincing one-nil win then.

Other footballers haven’t fared so well against the taxman: Lionel Messi and Christian Ronaldo are unquestionably two of the greatest players of this generation, but their tax planning has not matched their sublime footballing skills. In 2017 Messi had a 21-month jail sentence for tax fraud commuted to a fine. This was in addition to a voluntary €5m “corrective payment” he and his father had made in August 2013. Earlier this year Ronaldo was fined €18.8 million for tax evasion and given a suspended 23-month jail sentence.

5B. Beware the Ides of…November?

Finally, 22nd November, was also my father’s birthday. It’s actually a pretty momentous, if not infamous, day in history. Most notably in 1963 when President John F Kennedy was assassinated (with both Aldous Huxley and C.S. Lewis also dying on the same day the obituary writers had a very busy day). Charles de Gaulle was born on this day in 1890 and Angela Merkel became German Chancellor in 2005.

There’s a tax connection in convicted tax evader and serial tax exile Boris Becker who was born on this day in 1967 and the obligatory Kiwi connection is the death in 1982 of the pioneering aviator Jean Batten.

Lastly, Margaret Thatcher resigned on this day in 1990 (as a result of, you shouldn’t be surprised to hear, a Conservative Party split over Europe). This was not only a pretty funny 60th birthday present for Dad but also something of a rich irony as he was a staunch Thatcher supporter. Miss you Dad.