more on Inland Revenue’s crackdown on student loan debt

and why we might need to pay more tax

At an event for the Young International Fiscal Association, the Revenue Minister, Simon Watts announced the Government’s Tax and Social Policy Work Programme. These work programmes are a working document updated frequently so that after a change of government they reflect the new government’s priorities in tax policy and social policy areas.

According to the speech made by the Revenue Minister, the work programme under the current government is designed to support rebuilding of the economy and improve fiscal sustainability by simplifying tax, reducing compliance costs and addressing integrity risks.

There are six areas of priorities going forward: economic growth and productivity, modernising the tax system, social policy, the integrity of the tax system, strengthening international connections and other agency work.

Out with the old, in with the new

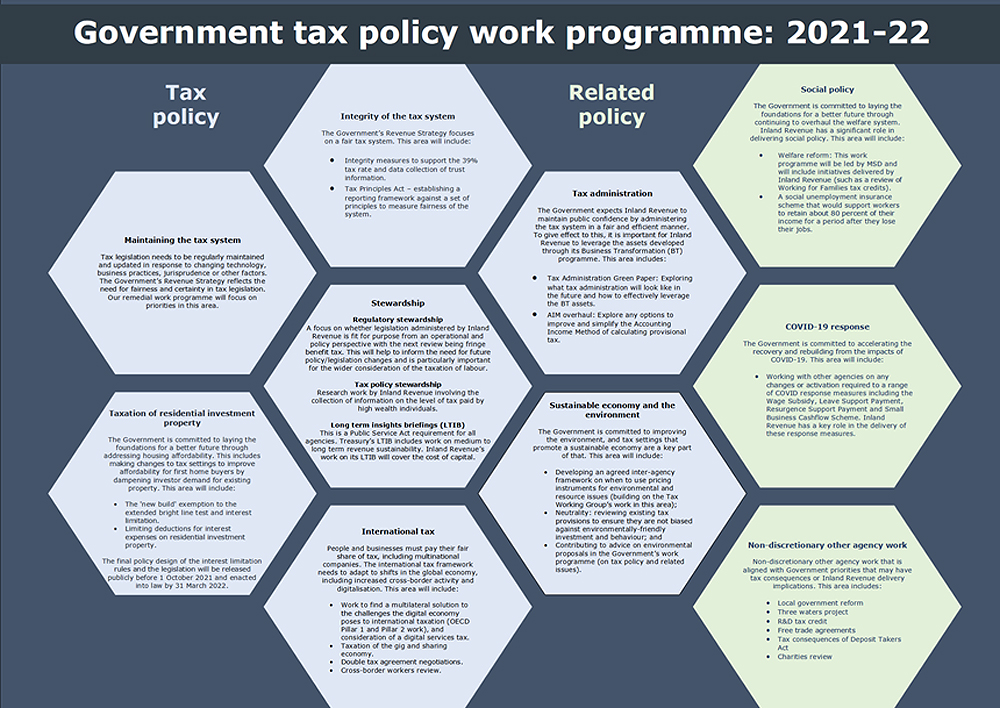

It’s interesting to have a look at what changes have been made since the programme was last officially updated back in 2021-22.

There under the Labour Government, there were 10 work streams of tax policy and related policy matters some of which overlap with the updated programme. Social policy integrity of the tax system, maintaining the tax system were all part of the 2021-2022 work programme and they’ll be part of every work programme going forward.

On the other hand, the COVID-19 response and the taxation of residential investment property were two major areas back in 2021-22 which are no longer there. As is well known the current government when it came in repealed all the work in relation to changes to the taxation of residential investment property.

Tax policy changes already happening

Drilling into the latest workstreams, some of them are already underway such as improvements to employee share schemes, implementation of the Crypto-asset Reporting Framework, simplification of the Approved Issuer Levy reporting including allowing retrospective registration and changes to inward pension transfers. All these are in the current tax bill before the House.

The other interesting things they’ve added in here, which we’ll watch with some interest, are exploring compliance cost reductions, including improving tax compliance with small businesses. Now you recall last week in my review of Inland Revenue’s annual report one of the areas Inland Revenue felt that business transformation hadn’t delivered as much as had been hoped for, was in reducing compliance costs for small businesses.

I totally support what Inland Revenue are doing, but the issue that they’ve run up against is that sometimes it has to accept the trade-off between good tax policy and the risk of tax seepage around the margins. If a policy allows a deduction or other benefit for taxpayers such as SMEs that meet certain criteria, you get certain deductions, Inland Revenue is always concerned about people exploiting that. The question that arises is does the wish to reduce compliance costs outweigh the risk that some of those measures might be abused?

A place where talent wants to live?

An interesting one that caught my eye was their plan to review the Foreign Investment Fund rules. This is something that was mentioned in passing by the Minister of Revenue at the recent New Zealand Law Society Tax Conference. This looks to address the issues raised by the report The place where talent does not want to live in relation to the problems the Foreign Investment Fund regime causes for investors migrating here.

Another interesting one is reviewing the thin capitalisation rules for infrastructure. That’s almost certainly tied up to the desire to have public/private partnerships help build infrastructure in the country. What it would almost certainly mean is that the current thin capitalisation rules (which basically limit interest deductions for international multi-nationals, which have more than 60% debt asset ratio) would almost certainly be relaxed.

In terms of other agency work Inland Revenue is considering, is an improved information sharing agreement with the Ministry of Business and Innovation and Employment, student loans, the question of final year fees free and overseas based borrower settings, the highly topical Treaty of Waitangi settlement, Local Water Done Well and supporting the all-of-Government response to organised crime. (Organised crime often represents tax evasion so it will always fall in the ambit of Inland Revenue).

Changes to the taxation of the Super Fund?

A big work programme, probably in terms of modernising the tax system, would be exempting the New Zealand Superannuation Fund from income tax. This would be quite significant as the New Zealand Superannuation Fund probably contributes $1 billion a year in company income tax. On the other hand, the Government will probably then be able to dial back completely its contributions to the scheme. In other words, the fund would now be expected to be self-funding going forward, which is quite possible now it’s reached a near critical mass of at least $70 billion in value.

The document’s fairly light on detail, just a one pager, but it gives you an insight as to where the priorities are right now. There are no real big surprises and we’ll watch and bring developments as these policies mature and are brought to fruition.

Student loan debt – Inland Revenue ups the ante

Moving on, last week I talked at some length about Inland Revenue’s actions around the collection of student loan debt and it so happened that yesterday Inland Revenue’s Marketing and Communications Group Manager Andrew Stott appeared on RNZ’s 9:00am to Noon with Catherine Ryan. They discussed what Inland Revenue is doing with its extra $116 million of funding over the next four years. This Includes an additional $4 million for recovering overdue student loan debt.

Quite a lot of interesting commentary came out of this interview. One of the first surprises was that many young people going overseas don’t know that their student loan debt, once they leave the country, starts to accrue interest. Therefore, they get behind surprisingly quickly. As is known, only 29% of overseas based borrowers are making repayments at the moment, and the student loan debt is now up to $2.37 billion, $2.2 billion of which is owed by overseas borrowers. A substantial number of whom are based in Australia.

So that’s now obviously a focus both operationally and in the latest work programme. I’m particularly interested to know more about what is planned in the overseas based borrower settings. What does Inland Revenue consider it needs to improve its ability to collect debt under the student loan scheme?

Inland Revenue has been allocated $4 million in funding to get cracking on recovering debt and it’s expected to produce a four to one return this year, which is expected to rise to eight to one next year. It will meet those targets pretty comfortably I’d say. Apparently in the first quarter of its new financial year – 1st July to 30th September this year it’s already collected $60 million in overdue debt up 50% from last year.

A surprising statistic

I guess the big surprise that came out of the interview was when Mr. Stott noticed that most of the debt is owed by people in their 40s or 50s who had never got round to repaying Inland Revenue. These people had been much younger when they went overseas with student loan debt which then accumulated as interest and penalties were added. This does beg the question that if people went overseas in their 20s and we’re now chasing them in their 40s and 50s, what was Inland Revenue doing in between?

As I said in last week’s podcast, relying on late payment and interest charges for enforcement just doesn’t work. We know from research in other areas when a person’s debt blows out (and probably the threshold is as low as $10,000), people will put their head in the sand and not take action because the matter feels too big to manage. Mr Stott mentioned that there’s several debts running into tens of thousands. I have seen one where it’s over $100,000. The average debt owed is about $17,000, but it’s the old overseas debtors, obviously larger debts, that Inland Revenue is going to be targeting.

As part of this it is talking to anyone who returns to New Zealand who has a debt of at least $1,000. They can now identify such persons thanks to the information sharing that goes on between New Zealand Customs and Inland Revenue.

Inland Revenue also have the ability to detain/prevent someone from leaving until they have a conversation about payment of debt. According to Mr Stott the group being targeted are those who have persistently not engaged with Inland Revenue. They have not responded to Inland Revenue at all. They’ve simply just said now go away, I’m not going to talk to you and ignored them. They will be fined and will find themselves having an extra stay at the airport just prior to departure.

Deducting debts from overseas salaries?

Inland Revenue has the ability to issue deduction notices requiring amounts to be withheld from payments to Inland Revenue debtors. (According to an Official Information Act response I got from Inland Revenue, it issued over 42,000 such notices in the year ended 30th June 2024).

Mr Stott was asked whether it could do the same in Australia? Can Inland Revenue ask the Australian Tax Office (ATO) to issue the equivalent to a deduction notice so that an employee working in Australia has part of their salary deducted to pay student loan debt. The answer is yes it can, but it’s not easily done. It’s termed a “garnishee order” in Australia and requires a court order. Consequently, Inland Revenue hasn’t really used such orders.

It seems to me that is something Inland Revenue really will need to look at closely, because if you’ve got 70% non-compliance and you’ve got an estimated 900,000 student loan debtors in Australia, it would be worthwhile establishing a process to enable garnishee orders to happen more frequently.

It may be that they have to ask the ATO to amend legislation, which would delay everything. But it would appear that they have the tools already, so it will be interesting to see if that’s employed more frequently.

Increased audit activity

The other thing Inland Revenue has ramped up is audit activities. It has apparently already launched 2,000 audits in the first quarter of its new financial year. This is up 50% on the previous year. Incidentally, 10% of those, are targeting the largest companies in the in the country.

As previously mentioned, Inland Revenue have recently targeted bottle stores and the construction industry. The next group of people that they’re going to be talking to now are vape stores, nail salons and hairdressers. Because in all cases they suspect cash income is not being declared, so these businesses will be the subject of unannounced visits.

The focus in Inland Revenue now is on enforcement and debt collection and there are more signs of it. So, I’ll repeat what I’ve said previously. If you have debt with Inland Revenue approach them to discuss it. You will find that if you take proactive action, it will be reasonable in most cases, unless you have a history of non-payment In which case good luck. Taking proactive action is the best approach, because tax debt is something you simply can’t put your head in the sand and hope it goes away. It won’t. Inland Revenue has got many more resources now, and the net is closing.

Why we might need to pay more tax

Finally, earlier in the week, I was one of several commentators Susan Edmunds of RNZ spoke to for a story on why we might need to pay more tax. Her story picked up the recent speech by the Treasury’s chief economic adviser Dominick Stephens which noted that the country appears to be running a fiscal deficit of 2.4% of GDP – that’s about $10 billion – and the pressure that’s building on demographic change, the ageing population, and rising healthcare costs. The article also referenced, Treasury’s 2021 Statement on the long term fiscal position He Tirohanga Mokopuna. I repeated that I think it is a matter of when, not if, the tax take has to rise when you put all these factors together.

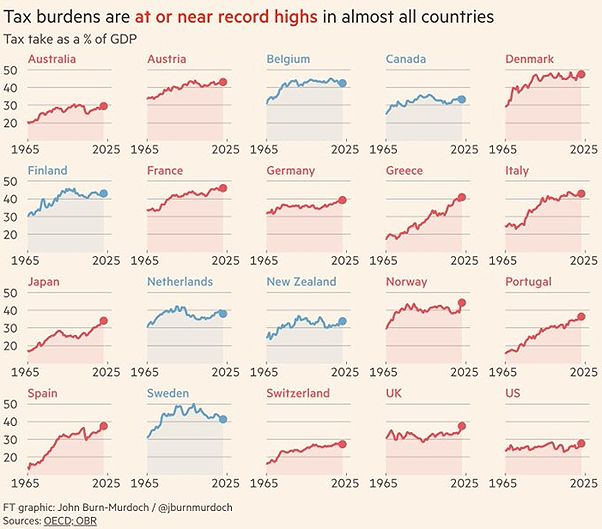

It’s also worth noting that the recent UK budget I covered a couple of weeks back increased taxes. Subsequently, the Financial Times had a very interesting graphic noting that tax burdens as a percentage of GDP for the last 50 years are at all-time highs in 14 of the 20 countries highlighted.

The pressure on tax revenues is a global problem, so we are not alone in trying to deal with these issues.

I think the break point, so to speak, will be the increasing cost of dealing with the damage as a result of extreme weather events. And I note that last week the Helen Clark Foundation released a report on the question of climate change and insurance premiums. My personal view is we need to get moving on this sooner rather than later, because that will help ease the transition.

Other jurisdictions we compare ourselves with, such as Australia and the UK, have a 45% top rate. And of course, in Europe the rates are much higher, still around 50% or so. I remain firmly committed to the broad-based low-rate approach, which means if we do broaden the base, we can hold tax rates down below these levels.

More tax, or less costs?

There was a nice to and fro in the comments on the LinkedIn post I put up with one commenter noting that we also need to reduce costs. Managing our expenses is part of what we have to do here, but if we’re talking about 2.4% of GDP, I think the pressures are too great for such a big gap to be easily closed just by better enforcement and cost management.

University of Auckland Professor in Economics Robert McCullough, thinks that this tax debate will define the next election in terms of “if we’ve got these expectations, how are we going to pay for everything?”

We shall see. And as always, we will bring you developments as they happen.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Rachel Reeves, the first ever female Chancellor of the Exchequer delivers a UK Autumn Budget with potentially significant implications for many Kiwis and Britons who have migrated to New Zealand.

Meanwhile Inland Revenue’s crackdown on tax evasion continues.

The UK finance minister is officially called the Chancellor of the Exchequer, a post which is more than 800 years old, and until this year it had never been held by a woman. So, when Rachel Reeves, the Labour Chancellor of the Exchequer delivered her maiden budget speech last Wednesday night, she made history as the first woman Chancellor in British history.

There was quite a lot to consider in this UK Budget, as people were watching to see how the new government would respond to the challenges it inherited. British budgets, unlike ours, coincide with the release of a Finance Bill and tax measures there’s always a lot of tax matters to consider beyond the headline measures.

The headline measures

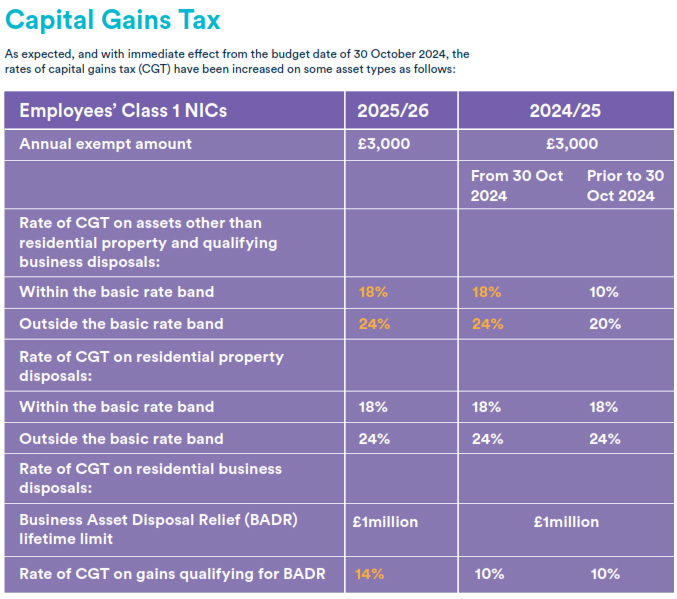

Most notably, there was an increase in Employer National Insurance Contributions (a Social Security tax) by 1.2 percentage points to 15% with immediate effect. There are also immediate tax rises for capital gains tax, but the top rate for capital gains tax still was capped at 24% for both property and non-property assets. Which as some commentators said is still lower than countries with which the UK compares itself. It’s quite interesting to see that comment about 24%, because one of the key points of our discussion around capital gains taxes here is what rate would apply? It’s therefore interesting to have an international comparison.

Beyond the headlines

It’s always interesting to dig around in other countries’ budgets and see what they do in certain areas. For example, the UK doesn’t have an imputation credit system, but there are lower rates of tax applied to dividends, even for those on the highest income. There’s also a savings allowance, which exempts certain amounts of investment income. It’s currently £1,000 for basic rate taxpayers (taxable income up to £37,700) and £500 for the higher rate taxpayers. The UK basic rate of tax is 20% and we have two rates lower than that so this savings allowance is not necessarily a measure we might want to copy here.

Twin cab utes and fringe benefits – an example to follow?

There’s apparently some uncertainty around the fringe benefit taxation treatment of twin cab utes which the Budget clarified. Where they have a payload of one tonne or more such vehicles are not there to be treated as cars for benefit in kind purposes unless they were acquired prior to 6th April 2025.

On Fringe Benefit Tax, the benefit value is calculated as a percentage of the vehicle’s list price when the car was first registered which is similar to our treatment. However, the percentage used is determined by the vehicle’s carbon dioxide emissions, or its range if it’s an electric vehicle. These percentages are set to increase steadily over the next three years as part of the range of tax increases announced. Inland Revenue is presently reviewing FBT and as is well known tax can act as a disincentive. If we want to incentivise a transition to a lower emissions economy, maybe we should be looking at how the UK applies FBT to vehicles.

UK pension tax free lump sum unchanged

There’s always lots of rumours before a Budget which I’ve seen sometimes used as a means to get people to buy new products or make tax driven decisions in fear of change. One of the rumours before this budget was that there were going to be changes to the taxation of pensions and in particular to the 25% tax free lump sum. That hasn’t happened, but remember, our rules are completely different. Just because 25% of the pension can be withdrawn tax free in the UK, that doesn’t mean the same rules apply here.

The big changes

But the main reason I was paying particular attention to this UK budget was because we finally got more detail around the two announcements made in the March Budget – the new foreign and income gains regime and the end of the non-domicile regime and the changes to inheritance tax. These are both measures which have significant impact for New Zealanders, who are either going to the UK or have returned to the UK, but also for UK expats who have migrated here.

New foreign income and gains regime

The foreign income gains (FIGS) regime is very similar to our transitional resident’s exemption in that a new tax resident’s foreign income and capital gains will be tax exempt for the first four UK tax years that they are resident in the UK. It’s not like our 48-month exemption period, it is tied to the UK tax year, which remember runs from 6th April to 5th April. (Perhaps reflecting that some of this stuff does date back 800 years or more, there’s no intention to change that tax year end).

What has also been clarified is that individuals who have previously elected to be taxed on the remittance basis, which meant their non-UK sourced income investment income was not taxable, can now be allowed to take advantage of a so-called temporary repatriation facility. This will last for three years, and they will be able to nominate and remit their non-UK income and gains from years when they were within the remittance basis and take advantage of lower tax rates. Initially 12% for the first two years ending 5th April 2026 and 2027, and then 15% for the year ended 5th April 2028.

As part of the FIGS regime there are also changes to what’s called the Overseas Workday Relief. This will allow UK tax resident employees who perform all or some of their duties outside of the UK to claim tax relief on the remuneration relating to their non-UK duties determined on “a just and reasonable basis”. This is quite a significant one for expats and for companies that have very highly paid and skilled employees and has been greeted with general enthusiasm by by those impacted.

Inheritance Tax

Potentially the biggest change though, is in relation to inheritance tax (IHT). This applies to all assets situated in the UK or all assets situated anywhere, if the person is domiciled within the UK. There’s a nil rate band of £325,000, above which 40% will apply (these rates and thresholds have been frozen until 2030). IHT has a potentially significant impact because under the present rules, someone tax resident outside the UK could still be within the IHT net because they are still deemed to be domiciled in the UK. I’ve had to deal with one or two of these instances.

There’s also a pretty nasty trap for someone like me who might have left the UK a long time ago and adopted a new domicile of choice outside the UK. At present if I ever became tax resident again in the UK, our domicile would immediately revert to the UK. Therefore, working or living for prolonged periods of time in the UK was actually potentially highly tax disadvantageous from an IHT perspective.

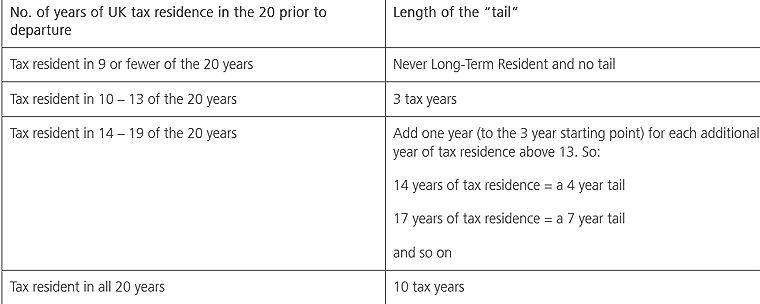

All this will be replaced now by a residence-based regime. The tests for whether non-UK assets are subject to IHT will now be whether the individual has been tax resident in the UK for at least 10 out of the last 20 tax years immediately preceding the tax year in which the chargeable event, most typically death, but can also be a lifetime transfer into a trust, happens.

There’s also a tail on how long a person is in scope if they’ve been non-resident during a period. For example, if someone had been UK tax resident for between 10 and 13 years, they remain in scope for IHT for three years post departure.

(Courtesy Burges Salmon)

Implications for New Zealand residents

What this change means for a lot of British expats resident here is they’ve got to think again about what their IHT obligations could be. By the way, our double tax agreement with the UK does not cover IHT. The UK has the right to charge IHT on assets situated in the UK, that’s not surprising. However, it potentially also has got a long reach if HM Revenue & Customs determine someone resident here is subject to IHT.

IHT and trusts

One of the other IHT changes is to the taxation of trusts used to hold assets outside the scope of IHT, so-called excluded property trusts. If I understand it right, starting from 6th April 2025, if a settlor dies and they’re within the scope of IHT, assets settled by them into what was previously an excluded property trust are now within IHT. This is a major change and I’m investigating it further given we make very extensive use of trusts. I’ve been dealing with quite a few clients who have UK connections year and it’s been really revealing to see how complex the taxation of trusts is from the UK perspective. It’s good to see some clarity around the new rules, but as I say, it’s a significant budget in many ways, and there could be quite major consequences for more people based here than they might anticipate.

Meanwhile, Inland Revenue’s crackdown continues

Moving on, Inland Revenue continues its crackdown when it announced on Thursday that it’s making unannounced visits to hundreds of businesses who it believes are not meeting all their tax obligations as employers.

According to Inland Revenue, they receive about 7000 anonymous tip offs each year. It has said “the volume of tip offs has grown over previous years indicating an increased sense of frustration by the community in general, businesses who are not doing the right thing.”

Inland Revenue’s analysis shows that the tax risks overwhelmingly relate to taking cash for personal use without reporting sales and or paying employees in cash.

Based on this Inland Revenue is making unannounced visits to over 300 employers whose practices it will closely examine. I’ve seen this happen with a few clients under investigation. Inland Revenue staff will go to a café or business and just watch to see what’s happening. They may buy something, but they will certainly sit and observe and see who uses the till, how everything is recorded and from there they will draw the relevant conclusions.

The consequences of being investigated

As an example of what happens to taxpayers who have not been compliant, the director of an asbestos removal and labour hire company has been jailed for three years in what the judge called serious offending and the worst of its kind to come before the Christchurch District Court in the last 20 years. The director, Melanie Jill Tatana, also known as Melanie Jill Smith, was jailed for three years for what was described as wilful diversion of funds.

Her company employed around 60 people, and between April 2019 and September 2022 had been required to deduct PAYE on 63 occasions but failed to pay the full amounts totalling $1.6 million. Tatana was therefore charged with 63 counts of aiding and abetting to knowingly take PAYE from workers’ wages and not pay it on to Inland Revenue. Instead, more than $800,000 had been diverted for her personal use.

One of the more encouraging things from my perspective about this case is that this offending has all been pretty recent and Inland Revenue tracked it down within a couple of years. I’ve seen cases where the offending has been four or five years.

I still think 63 occasions of nonpayment is a little generous, but bear in mind that Inland Revenue did take the the foot off the throttle around pushing hard on on companies and businesses because of COVID. That amnesty or less stringent approach is now over and it’s back to business. And Tatana won’t be the first to find out about Inland Revenue’s hardline approach.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week I joined Gareth Vaughan of interest.co.nz for a joint podcast with Andrew Coleman. He’s a New Zealand economist who has worked in academia and for the government, including Reserve Bank, Treasury and the Productivity Commission. In the last few months, he’s written a 13 part series for Interest looking at how we currently fund New Zealand Superannuation and what alternatives we should be considering.

Why we’re talking about more tax – the rising cost of New Zealand Superannuation

As I’ve mentioned previously, part of what’s driving the debate around whether New Zealand should have a capital gains tax is when you consider the government’s long term fiscal position, the conclusion you reach is that something radical will have to happen: either benefits will have to be reduced significantly, or taxes will have to be increased. If we’re increasing taxes, how are we going to go about that? That, by the way, is the subject of Inland Revenue’s long-term insights briefing consultation on which is going on at the moment.

(He Tirohanga Mokopuna 2021, Treasury)

Coleman has written extensively about the issue of funding New Zealand Superannuation and in the podcast he went through the issues behind why he wrote the series and what alternatives he proposes. It was very informative, and I highly recommend listening to the full podcast. Here are a few key takeaways.

New Zealand’s unique approach to funding superannuation

Firstly, the way New Zealand currently funds New Zealand Superannuation is very unique in that it is entirely funded out of current taxation. That means the current cost of New Zealand Superannuation, over $20 billion a year before tax, is being paid out of current taxation. This is unusual by world standards, because most other countries in the OECD adopt some form of Social Security tax to pay for their public superannuation. In Britain they have National Insurance Contributions, in America, they have Social Security. Throughout most of the EU you will see Social Security taxes in place. Apart from us, only Denmark in the OECD has no Social Security taxes. Other countries use social security taxes to pre-fund superannuation; people pay social security taxes which are then drawn down when they reach retirement age. We fund everything out of current taxation.

Allied to that, and a matter that makes our tax system unique, is that most other jurisdictions operate what’s called an exempt, exempt tax (EET) approach to private retirement savings. That is a person gets some form of tax deduction for making a contribution to a private superannuation savings scheme. The superannuation schemes are not taxed, but when you withdraw funds on retirement age you pay tax at that point. On the other hand, since 1989 we have adopted the complete opposite approach (TTE). We don’t give a deduction for contributions to superannuation schemes such as Kiwisaver, which are subject to the ordinary rules. However, withdrawals are tax exempt.

Point of order Prime Minister…

Just as an aside, I note that one of the Prime Minister’s comebacks to questions around capital gains tax was that if introduced it would apply to KiwiSaver. (Actually, when the last Tax Working Group proposed a CGT, they didn’t actually seem to think to go there). The PM’s comment glossed over the fact that KiwiSaver funds are subject to tax. If they’ve invested in bonds, these are subject to the foreign financial arrangement regime. If they’ve invested in overseas stocks, those are taxed under the Foreign Investment Fund which because the 5% fair dividend rate automatically applies, is a quasi-wealth tax.

Time for social security taxes?

That point of order aside, Coleman’s key point remains that our treatment of private superannuation schemes and funding of public superannuation is quite unique by world standards. So how are we going to meet the growing cost of superannuation? He suggested that maybe we should look seriously at Social Security taxes.

A Capital Gains Tax won’t be enough

Gareth and I raised the question of alternative taxes, such as a capital gains tax and Coleman made the point that the likely cost of New Zealand Superannuation scheme is going to rise towards somewhere around 8-9% of GDP. Hence the need to be thinking about how to fund that cost. Capital gains taxes don’t generally raise that much, typically, somewhere between one and two percent of GDP. That still leaves a funding gap of between 6-8 percent of GDP. It’s very doubtful a wealth tax, by the way, would make that gap up. In his view, the inexorable conclusion is that Social Security taxes are going to be needed to fill the gap.

How the 1989 changes helped distort the housing market

We also had a very interesting discussion about how the changes in 1989, which by removing the incentives for private savings, drove investment into residential property. He published his research on the matter in 2017, just at the same time that myself and the Honourable Deborah Russell, published Tax and Fairness. Separately we had reached the same conclusion, that the 1989 changes to the savings regime had driven people to start over-investing in housing.

Time for KiwiSaver 2.1

Coleman calls his answer to funding New Zealand Superannuation KiwiSaver 2.1 It would be a compulsory savings regime, but it would be for younger taxpayers, basically those under the age of 40 who were not old enough to vote back in 1997, when a referendum on a question of a compulsory superannuation savings scheme was overwhelmingly rejected.

Coleman’s argument is that younger taxpayers are currently funding what they want and need, such as health, education and transport. But they’re also having to fund the superannuation of older taxpayers, who voted for the current system which benefits them. KiwiSaver 2.1 as a compulsory superannuation savings scheme would be a transition to a fairer system which would include some form of social security tax. The idea would be to be gradually building up savings in a similar way to Australia, which, although it doesn’t have significant social security taxes, does have a compulsory savings scheme. There would be this transitional period, as the older workforce aged out, but all new younger workers would be part of the new KiwiSaver 2.1.

Taxing older, wealthier superannuitants

As part of the transition Coleman sees it requiring more taxes from older persons, which is where our discussion got to talking about capital gains taxes and wealth taxes. He’s not a particularly big fan of wealth taxes. But he sees a capital gains tax having an efficiency aspect to it, which means it should be part of the tax system.

Incidentally, one suggestion I have seen about taxing superannuitants involves applying a separate tax rate to persons receiving New Zealand Superannuation. This would be a way of clawing back payments from those who have other means without going down the route of the deeply unpopular means testing that happened in the early 1990s.

I thoroughly recommend listening to the podcast. Coleman’s analysis highlights the need to keep in context why we’re having this discussion about capital gains and wealth taxes and that’s to do with everyone realising that we have to address the rising cost of funding New Zealand Superannuation and related healthcare costs for the elderly. These issues are not going to go away because the demographics are inexorable, contrary to what politicians might hope as they repeatedly kick the can down the road.

Tax deduction notices

Moving on, Inland Revenue makes great use of tax deduction notices as a debt collection tool. These enable it to require a third party to make deductions from payments due to a taxpayer with an outstanding tax liability. The power is contained in section 157 of the Tax Administration Act 1994, or related provisions of the Child Support and Student Loans Acts. I once saw a notice where a supplier to someone with tax debt was told to withhold 100% of any payment that was going to be made to the person in default.

Inland Revenue typically issues thousands of deduction notices each year.

Deduction Notice issued to:

FYE 30 June 2020

FYE 30 June 2021

Total

Bank

5,222

7,388

12,610

Employer

21,333

43,535

64,868

Total

26,555

50,923

77,479

(Figures obtained under the Official Information Act)

I think it’s appropriate Inland Revenue has the power to issue deduction notices. My concern, however, is I’ve seen them issued for under $1,000 of tax debt which in my view is an inappropriate use for what is a fairly small sum of tax debt under $1,000. When a deduction notice is issued to an employer in such circumstances this essentially notifies the employer that the relevant employee is behind on their taxes.

Are these notices breaches of privacy?

In my view, a deduction notice in this situation represents a breach of privacy and employers really do not need to know about relatively small sums of tax debt owed by an employee. Instead, and I will propose this in my submission on the draft, I believe Inland Revenue should make greater use of tailored tax codes to collect the unpaid tax from an employee. The employer still has the responsibility for deducting the tax through PAYE but now all they know is the tax code has changed. They don’t know the reasons why. This preserves the privacy of the person who has been the subject of the tax deduction.

I think this is important. I discussed this issue with a previous Privacy Commissioner, and he was of the view that, yes, it seemed like a breach of privacy. But as he noted, he couldn’t really do much about it because Inland Revenue had the legislative power to issue the notices. Still just because Inland Revenue can doesn’t mean it should, and I think there are opportunities for improving matters. Looking at the UK, it’s common practice for HM Revenue & Customs to use adjusted PAYE codes to collect arrears of tax. Submissions are open until 15th November.

How many anonymous tip-offs does Inland Revenue typically receive each year?

Across the ditch the Australian Tax Office (ATO) revealed this week that in the past five years it has received over 250,000 tip offs about potential tax evasion. According to ATO assistant commissioner Tony Golding “We get on average over 3500 tip-offs a month from people who know or suspect tax evasion or shadow economy behaviour.” The ATO believes there is about A$16 billion in stolen, unpaid tax each year.

By comparison, according to Inland Revenue it receives about 7,000 anonymous tip-offs each year. These are important sources of information even if sometimes the tip-offs are malicious and stem from toxic relationship or business breakdowns or partnership breakdowns. Regardless of this issue Inland Revenue will follow up (the ATO says 90% of tip-offs lead to further investigation.

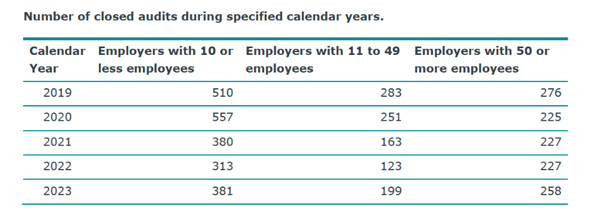

How many audits is Inland Revenue undertaking?

On the issue of audits and my thanks to regular listener and reader, Robyn Walker of Deloitte for reminding me, Inland Revenue publishes Official Information Act responses and there are often some very interesting releases. One of the latest OIAs relates to the number of audit cases carried out on businesses between 2019 and 2023.

It’s interesting to see the impact of Covid and the quite marked drop-off in audits for those employing fewer than 50 employees.

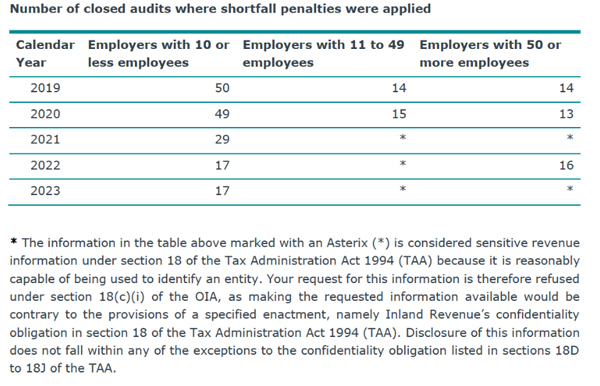

There’s also data on the number of shortfall penalties applied as a result of audit. Now shortfall penalties enable Inland Revenue to impose penalties of up to 150% of the tax involved where tax evasion has happened although the more common range of penalties is 20%. Again, the somewhat sparse data makes for interesting reading.

That’s all for this week. Next week, we’ll be taking a deep dive into Inland Revenue with a look at its annual report.

Until then, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

How to deal with recipients of paid parental leave with tax underpayments

A bizarre tax avoidance case from the UK involving snails

In line with other government agencies, Inland Revenue is required to produce a long-term insight briefing once every three years. These briefings are intended to

“…help us collectively as a country think about and plan for the future. They do this by identifying and exploring long-term issues that matter for our future wellbeing. Specifically, [briefings] are required to make publicly available:

information about medium- and long-term trends, risks and opportunities that affect or may affect New Zealand society, and

information and impartial analysis, including policy options for responding to the trends, risks and opportunities that have been identified.”

This is Inland Revenue’s second long-term insight briefing, its first one released in 2022 was on tax, foreign investment and productivity and that was a fairly chunky topic. But this time around it’s proposing to take on a bigger topic “what broad structure of the tax system would be suitable for the future.” What it would do is look at this topic by reviewing our tax system through the lenses of what is the tax base and what regimes apply.

As part of the initial stage of consultation for this topic Inland Revenue has released a 50 page briefing document giving a background on the whole process. The briefing summarises the current state of the New Zealand tax system and the options for consideration. Chapter one gives a complete overview of the current system. Chapter two then gives options for a future tax system and looks at international perspective. The final chapter summarises the topic and the approach to be taken by the briefing.

A mini-tax working group review

There are a lot of interesting insights in this paper, because in essence it’s similar to the scoping paper usually prepared by a tax working group at the start of a review before the group gets into detailed analysis of particular aspects of the tax system. The briefing is a therefore a handy high level summary of the current state of the New Zealand tax system.

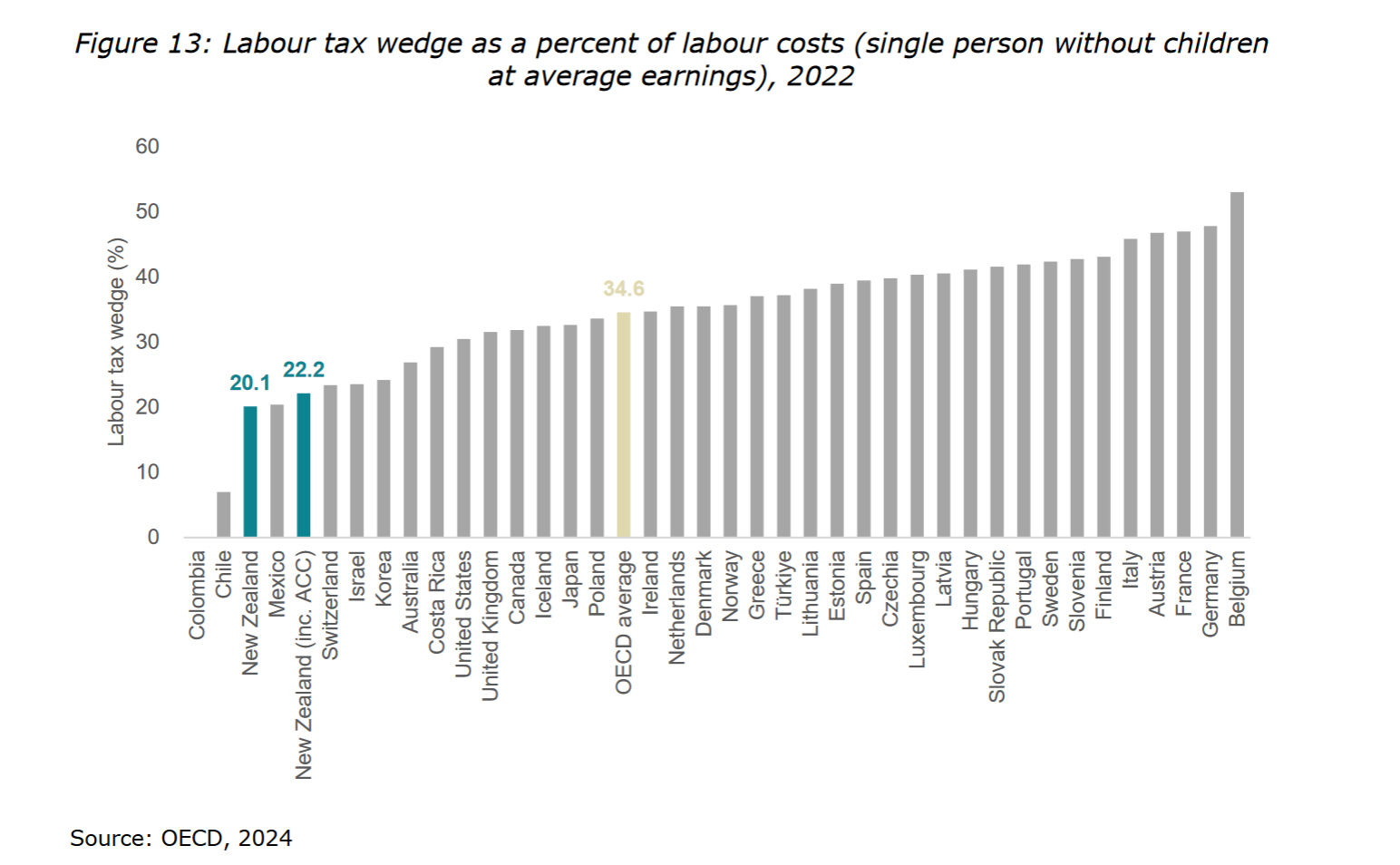

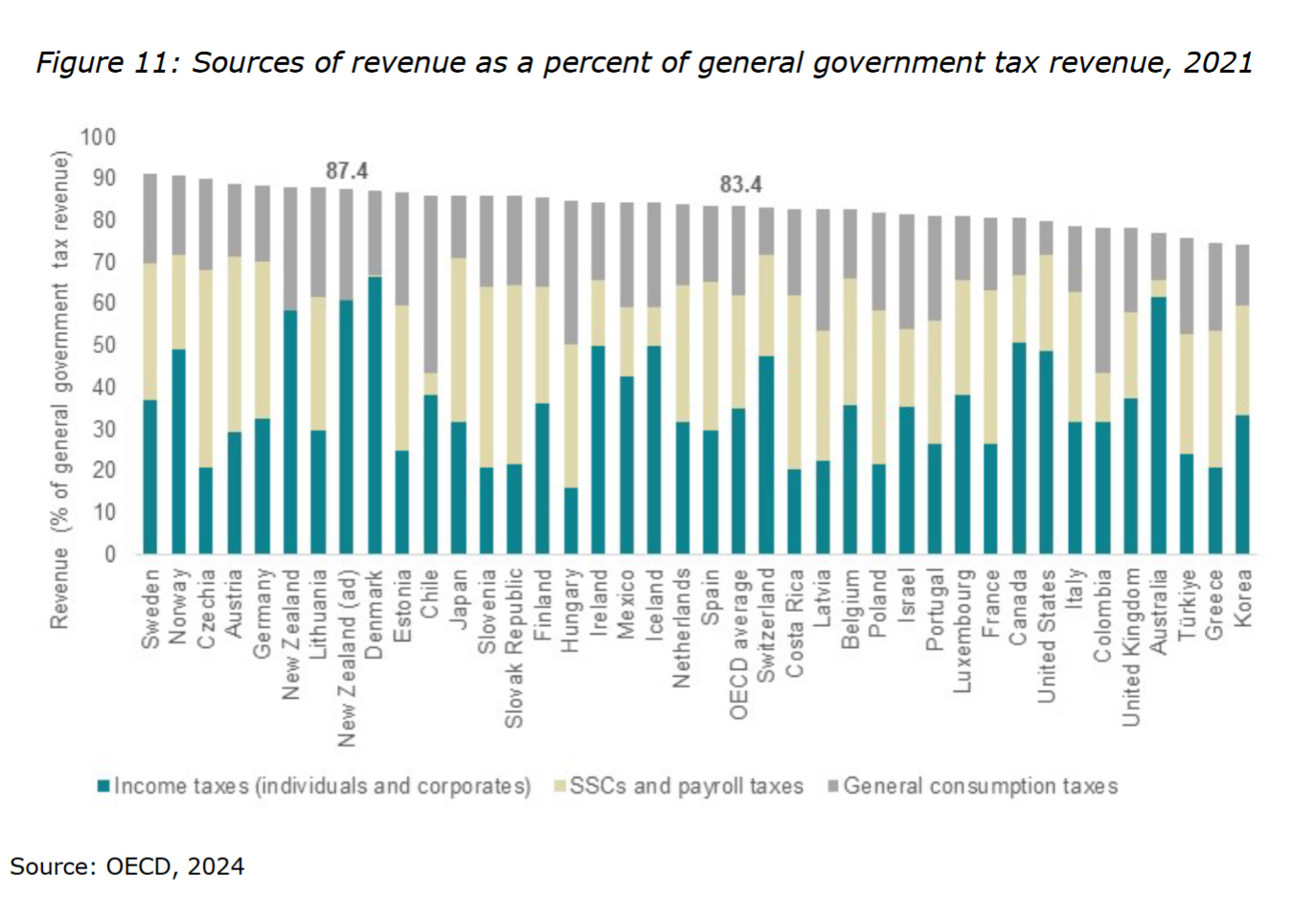

In summary, the level of tax revenue we currently raise relative to the size of our economy is pretty close to the OECD average. It’s in the composition of tax revenue. It’s where it gets interesting. We are almost unique in the OECD in not having any significant specific taxes on labour income such as social security contributions or payroll taxes.

Taxing labour…lightly?

Furthermore, quite a few of other OECD tax systems have what they call a schedular tax system, which means in some cases they tax capital income such as dividend, and in some cases capital gains at lower rates than taxes on labour. As a result, many OECD countries have a higher tax burden on employee labour than New Zealand.

To give an example, the UK has a 20% basic tax rate, but employees also pay National Insurance Contributions above a certain threshold (8% on income between £242 and £967 per week and 2% above £967 per week). Employers pay 13.8% on all earnings over £175 per week. By contrast we have no such taxes which means we have one of the lowest tax wedges in the OECD.

Also, where we stand out is we raise more than the OECD average on general consumptions and that’s because our GST is one of the most comprehensive in the world. We also currently have a higher company income tax rate than the OECD average.

The paper notes some concerns noted about high effective marginal tax rates on inbound investment. I have to say I do wonder whether the small size of our economy and its isolation is more of a factor than tax in attracting inbound investment.

And finally, and this is highly ironic and also relevant if, you just opened your rates bills and the comments from the Prime Minister earlier this week, New Zealand raises more than the OECD average from recurrent property taxes, mainly through local government rates.

Building fiscal pressures

As part of the background the paper explains the various fiscal pressures building up. This is something we’ve talked about before, and we’ve frequently referenced, Treasury’s He Tiro Mokopuna 2021 statement on the long-term fiscal position. The well-known pressures building in in relation of our changing demographics, rising superannuation and health costs are all mentioned again.

So too is climate change, but more in passing, although personally I think that’s the one the impact of which is going to land first for most people as we saw last year in the wake of Cyclone Gabrielle. Suddenly, climate change is not an abstract thing with targets for 2050. It’s here and now. Remember Auckland ratepayers, for example, we got a $400 million bill as a result of buying out properties rendered uninhabitable by the Anniversary Weekend floods and Cyclone Gabrielle.

A suitable tax system for the future

The paper discusses what would you do in terms of meeting these pressures. Do you expand the tax base by adding new taxes or what about increasing tax rates? The paper mentions that there are limitations about raising tax rates which is not always as straightforward as you might think. For example, we raised the rate of GST from 12.5% to 15% in October of 2010 and GST as a result is a very significant tax because our system is so comprehensive.

But GST comes at the price of being very regressive for people on lower incomes. How would you deal with that? And the paper, by the way, references an IMF Working Paper on a progressive VAT/GST which I mentioned recently.

There was also an interesting comment I’d like them to know more about in relation to company tax. The paper notes that we raise a relatively high amount of revenue from company income tax as a proportion of GDP compared with other countries.

It notes this “may be partly attributable to the level of incorporation.” I’d be interested in knowing how much more company incorporation goes on here relative to other OECD countries. I think our imputation tax system is also a factor in why we pay relatively high amounts of tax relative to other jurisdictions.

What the briefing does reinforce is something I think is agreed within the tax community that there’s pretty much little scope for increasing company income tax rates. There’s always a lot of talk about that, but I don’t think there’s much scope for actually doing so.

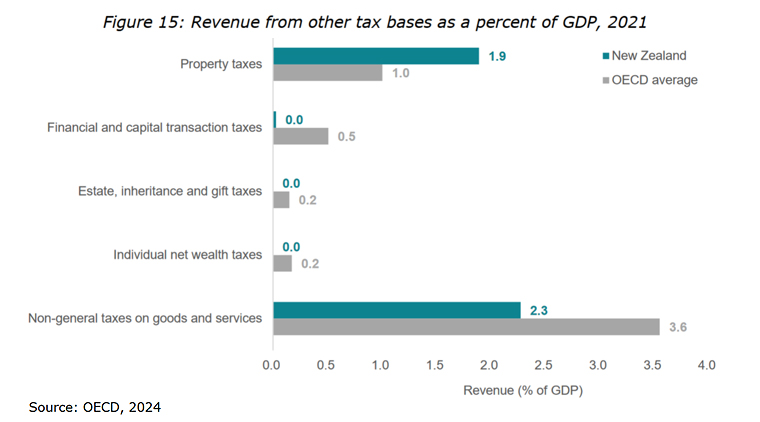

“New Zealand is unusual among OECD countries in not having a general tax on income from capital gains”

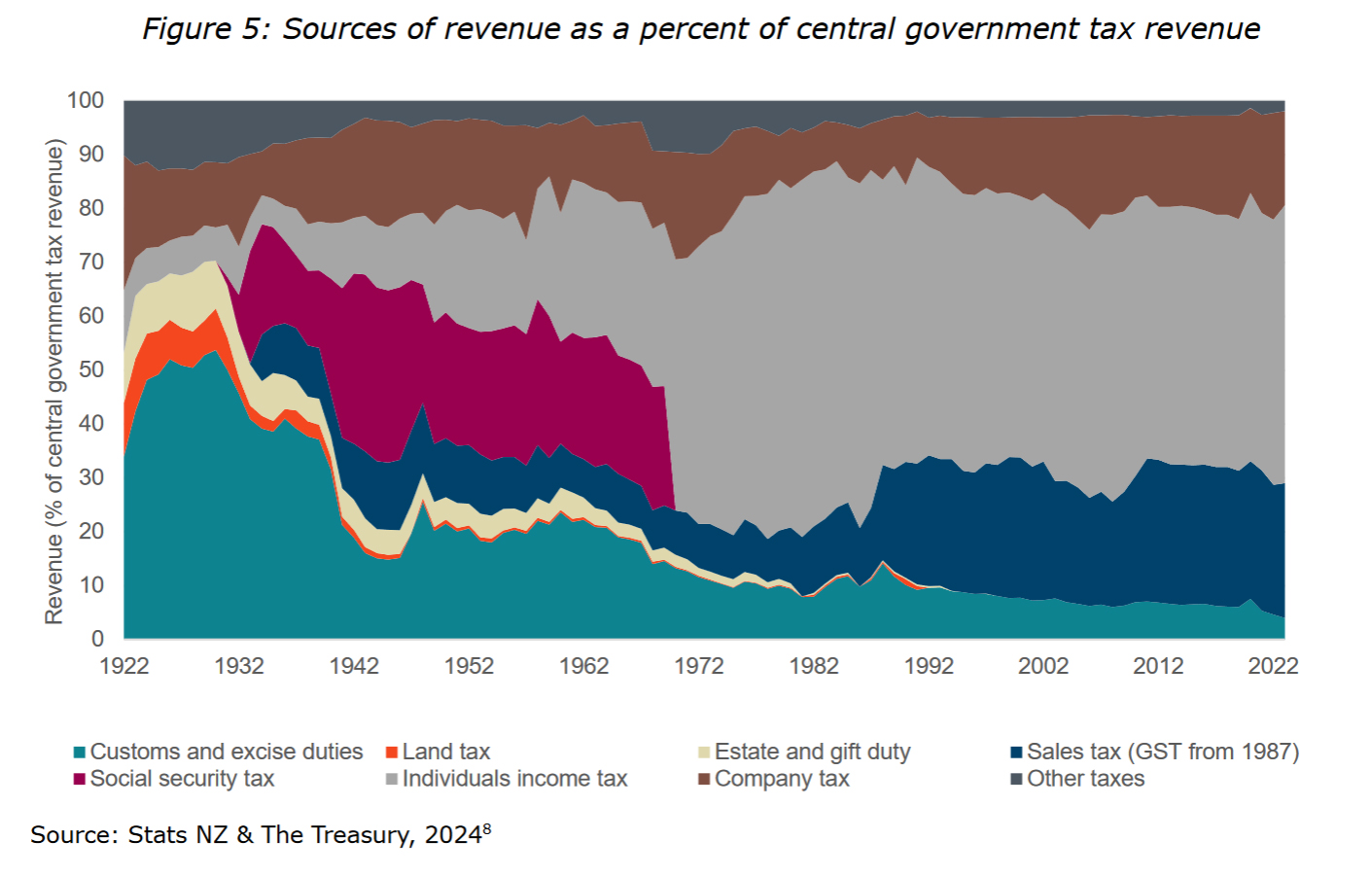

Unsurprisingly the paper considers the question of taxing capital, as part of reviewing the composition of taxes in other countries. There are a lot of interesting graphs and stats are in this section including an excellent section summarising the historical changes in the composition of the tax base over the past century.

As I mentioned, we raise more revenue as a share of GDP from recurrent property taxes compared to the OECD. In 2021 it amounted to about 1.9% of GDP. B comparison, the average in the OECD is 1%, ranging from 0.1% of GDP in Luxembourg to 3% of GDP in Canada.

On the other hand, we don’t raise anywhere near the same level as other OECD countries from taxes on financial and capital transactions, estates and gifts. I mean, many countries have a combination of estate taxes, gift duties, capital gains, taxes and wealth taxes. According to the OECD data taxes on estates, inheritances and gifts raised an average of 0.1% of GDP in 2021. That seems a surprisingly low number, although it rose to 0.2% in 2022. This take is starting to rise as the Baby Boomers, the richest generation in history are starting to pass on. In the UK Inheritance Tax, which is a combined estate and gift tax, is now over 0.3% of GDP (£7.5 billion) and rising.

What about corrective and windfall taxes?

The paper gives a background on the possible options which might deal with future cost pressures. Its focus is going to be on revenue raising taxes. The final briefing will not examine taxes that are primarily about changing behaviours (so called “corrective taxes” such as excise duty, particularly in relation to tobacco. It will not discuss environmental taxes which are another form of corrective taxes. All taxes change behaviour in different ways and I think considering the behavioural impact of certain types of taxes would be useful

The final briefing will not consider windfall taxes, which have recently popped up in discussion in relation to supermarkets and the banks. Such taxes are one-off in nature and frankly, a reactionary tax to a set of events. If the concern, correctly in my view is about responding to the pressure of ever increasing costs, then windfall taxes are not in that context a sustainable addition to the tax base.

All in all, this is very interesting and pretty digestible reading. Consultation is now open until 4th October, so my suggestion is get reading and start submitting.

A baby and a tax bill…

Moving on, Inland Revenue has mostly completed its year-end auto assessment process for the majority of taxpayers’ income for the March 2024 tax year. Subsequently, it’s emerged that some 13,261 recipients of paid parental leave, about 27% of all such recipients have finished up with a tax bill. This is causing some concern because in some of these cases, these bills are quite substantial, amounting to several thousand dollars in some cases which have to be paid.

Paid parental leave is taxable and subject to PAYE. What seems to have happened is that people haven’t factored in the effect of their other income, for example they may have continued to work reduced hours in their main employment while also receiving paid parental leave. Consequently, because PAYE is designed around one person, one job per year the parental leave has been under taxed. But this only emerges as part of the end of tax year wash up. You can deal with this by using a secondary tax code, but that often goes the other way and leads to over taxation during the year.

Tailored tax codes

An answer to all of this, and also as a means of collecting the tax paid would be a tailored tax code. Tailored tax codes are ideal for an employee with other sources of income which aren’t subject to PAYE such as overseas pensions. What you do is advise Inland Revenue of these other sources of income and ask it to adjust your PAYE tax code taking into effect this other income. It’s then taxed during the year through PAYE. By the way, this also is a good way of bypassing the provisional tax system.

This approach is something I saw a lot of when I worked in Britain. HM Revenue and Customs adjusted tax codes for the equivalent of New Zealand Superannuation and used adjusted tax codes to collect underpayments of tax for prior years. If you underpaid one year, your PAYE code for the following year would be adjusted to collect the underpaid tax. I think this is probably an easier system than expecting lump sum payments.

My view is Inland Revenue could make a lot more use of tailored tax codes and should do so proactively. It has the information to know when someone has started a second job or starts receiving paid parental leave. It can then contact that person and ask they want to have a secondary tax code or a tailored tax code. This may already be happening but people with new babies have plenty going on, so this sort of admin detail just slips off the radar. I think it’s something where Inland Revenue systems ought to be good enough to be able to actively encourage people to make greater use of these codes.

Snail farm in city office sparks tax avoidance probe

Finally, and returning to an earlier topic, rates, there’s a story from the BBC about a quite flagrant tax avoidance scheme in the UK. The story involves a commercial building in Liverpool and what’s happened is this building has been home to a snail farm for more than a year. The firm renting the premises has told Liverpool City Council that because the building is being used for agricultural use that part of the building is exempt from business rates. Otherwise, the rates bill would be about £61,000 for the whole building.

Understandably, Liverpool Council’s not impressed, and neither are other snail farmers. (Apparently snails retail for £14 a kilo). They think the scale of the operation isn’t realistic because according to the owner there are only two snails in each crate which has been done to avoid “cannibalism, group sex and snail orgies”. (Yikes!)

This seems a fairly flagrant tax avoidance case. And it’s caught the eye of Dan Neidle of the UK tax think tank Tax Policy Associates. As he notes you’d think this sort of thing would be struck down quite easily by the courts but not so. There doesn’t appear to be a specific anti-avoidance rule in the relevant legislation, and it appears that there’s quite an industry around so-called “business rates mitigation”. Astonishingly, a recent case involved a Crown organisation Public Health England attempting to bypass rates through one of these schemes. Dan has suggested that the new Chancellor of the Exchequer, (Finance Minister) Rachel Reeves, put in place legislation to strike this sort of activity down.

An opportunity here?

Under our rating legislation here I think that a similar scheme probably wouldn’t work. Based on what I understand our rating approach seems to be a bit more comprehensive. But one of the things I know about working in tax is that where people perceive there’s an opportunity to, let’s say, push the envelope, they will do so.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

And issues draft guidance on the taxation of share investments and tax

The Olympics, a cautionary tale involving Snoop Dogg

Earlier this year in June, we talked about Inland Revenue’s releasing insights from its first round of a hidden economy campaign focused on smaller liquor outlets around the country. It noted that in this first stage, compliance staff had made 220 unannounced visits nationwide, looking for signs of issues such as income suppression, unreported sales and non-registered staffs. And it noted that although most of the businesses had their tax affairs in order, unfortunately some hadn’t.

That was described as a deliberate light touch campaign. And Inland Revenue said at the end of that release that more unannounced visits to businesses will be made as it steps up its compliance work

Well, last week we saw the second stage of that, where it announced that from 14th of August it will be sending letters to taxpayers in the liquor industry selected for a possible visit. This time Inland Revenue community compliance teams will be visiting liquor store businesses, including independent and franchise liquor retailers, across most locations. But this does not include bars or hospitality venues. I’d surmise they’ve got a separate plan for that group of taxpayers.

These teams will be looking at income suppression, record keeping practises – including when using cash – and employer obligations. All it’s said is that they will be issuing letters as of 14th of August, which meant they started going out last week. So, if you’ve been selected for one of these visits, I suggest you review your practises to see what areas could possibly be at risk. And certainly talk to your accountant or tax agent if you have one.

This isn’t surprising, Inland Revenue foreshadowed this in June. Remember they got an extra $116. million over four years in the budget to ramp up their compliance activity. This is merely the tip of the iceberg.

Inland Revenue’s harder line

What I and other tax agents are also noticing elsewhere, is that Inland Revenue has certainly adopted, let’s say, a harder edge in its approach. We’re now getting requests for information in situations where previously that didn’t happen, and I’ve heard one or two somewhat unsettling stories of borderline bullying of taxpayers.

I’m all in favour of ramping up compliance, but it’s always worth remembering that any tax system, even one as remarkably compliant as ours is, does depend on the goodwill of the taxed to enable its smooth operation. And I would just hope that Inland Revenue would keep that in mind. Because sometimes dropping a heavy hammer on those who’ve made innocent mistakes doesn’t actually achieve very much for the wider perceptions of the integrity of the tax system.

But that said, there’s nothing really surprising in this Inland Revenue campaign. And I expect I’ll be talking more about new investigation initiatives in other areas over the coming months.

Taxing share investments – what are the rules?

Moving on, an area where we spend quite a lot of work advising clients on is the question of share investments, particularly in relation to offshore shares. Although the Foreign Investment Fund regime in its current iteration, has been in place for a very long time, nearly 17 years in fact, it’s probably not as well-known as Inland Revenue perhaps might expect.

I think what I sometimes see in this space is that people coming from other jurisdictions which have a capital gains tax regime, pretty much assume it’s much the same approach here. So, it’s helpful that Inland Revenue last week released some draft guidance on the taxation of share investments for consultation.

The draft guidance runs to 43 pages including some detailed appendices and as always, there are a couple of helpful fact sheets attached. One explains when the FIF rules apply, and the other one summarises the general treatment of share investments.

The draft Interpretation Statement covers what happens when an investor is investing in shares, what liability do they have for dividends, share sales and how these rules interact with the Foreign Investment Fund rules.

Interestingly the guidance refers to share lending arrangements and foreign currency accounts.

“the statement focuses on investments who use online investment plan platforms, although the principles in this statement apply more widely to other share forms of share investments by individuals such as through brokers”.

This tells me that Inland Revenue have been collecting data through the Common Reporting Standards (CRS) on the Automatic Exchange of Information. Just before COVID arrived Inland Revenue had begun marrying up the data that they started receiving in 2018 and 2019 under CRS. Based on this it had started to ask questions of taxpayers, who they knew through the CRS information, had some form of offshore investment, but did not appear to have included that in their tax return.

So, I suspect this is another development in what I just talked about a few minutes ago – Inland Revenue ramping up its compliance activities.

Which set of rules?

Now, as the guidance and the fact sheets explain, there are two treatments at play here. The Foreign Investment Fund regime generally applies to all shares outside Australasia. And not to get into too much detail about that, just always be careful that some listed stocks in Australia do actually represent FIF interests. Shares outside the FIF regime such as those listed either on the New Zealand Stock Exchange or on the Australian Stock Exchange are subject to the “ordinary rules”.

The guidance explains when the ordinary rules will apply and when the Foreign Investment Fund rules will apply. And one of the things that it picks up on is what is the tax treatment where a taxpayer has realised gains from the disposal of shares? The general rule under section CB4 of the Income Tax Act 2007 is that those amounts from selling shares are taxable, where the shares were acquired for the “dominant purpose of disposal or were part of a share dealing business or profit-making scheme.”

Determining the dominant purpose

Now deciding what an investor’s “dominant purpose” is done at the time the shares are acquired. The investor’s stated purpose is tested against a combination of objective factors. And it’s often the case, that an investor may have one purpose or more than one purpose, or not even really any clear purpose when buying shares.

The onus is on the investor to prove that their dominant purpose for buying shares was to dispose of them, or conversely, not dispose of them. The guidance notes an investor only has to prove that disposal was not their dominant purpose. They do not have to prove an alternative dominant purpose.

Generally speaking, share sales will not be taxable if an investor can show that the shares were bought with the dominant purpose of receiving dividend income, receiving voting interests, or other rights provided by shares or a long-term investment growth in assets or portfolio diversification. Other than situations “Where at the time of acquisition this is planned to be achieved through sale.”

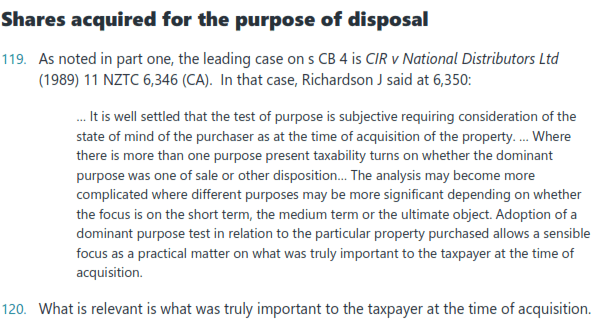

The appendix here has some interesting commentary from case law, most notably is the Court of Appeal decision CIR v National Distributors. Inland Revenue had lost in the High Court but appealed, and their appeal was upheld two to one in the Court of Appeal, with Justice Richardson giving the main judgement.

The taxpayer National Distributors had made eight purchases and sales of shares over a two-year period. The shares were held between eight months and three years with an average of 19 months before sale. The dividend yields were inconsistent and ranged from less than 3% to over 11% year, depending on the shares. Overall, the dividend yield was 6.5% per year compared with 25%-year from gains on sales.

Richardson noted that share purchases fell into two categories. Some were purchased for family reasons, but the second group were held to have been acquired, on the facts, for the purpose of sale. The taxpayer did not in the court’s view establish that there was no dominant purpose of sale.

In summary another useful interpretation statement and fact sheets. It’s good to see Inland Revenue putting some general guides and clarifying the point around when someone is subject to the Foreign Investment Fund regime, and when the ordinary rules will apply.

Tax and the Olympics

And finally, this week congratulations again to our Olympians for their fantastic achievements. I greatly enjoyed the Olympics as I’m sure everyone did. Not just because of the great performances by so many New Zealand athletes, but also just the sheer spectacle of watching the best in their sport.

One of the more entertaining parts of the Olympics was that the American TV channel NBC sent across rapper and record producer Snoop Dogg to provide commentary on the Olympics. Some of what he got up to was quite hilarious, check out him dressed up for a dressage event for example.

All good fun but the sharp-eyed Andy Bubb, Special Counsel, Tax Disputes at the Australian law firm Clayton Utz has pointed out that Snoop Dogg has possibly ended up with a fairly hefty French tax liability.

Apparently, he was paid USD 500,000 a day for his work, and what Andy Bubb has noted, is that under Article 17 of the double tax agreement between France and America, France has the right to tax the earnings of an entertainer or sportsperson where the activities are carried out in France. Now you can’t divert the income to an entity under the tax treaty because that’s overruled as well. As France’s top marginal tax rate is 45% the multimillion dollar question arises did Snoop Dogg’s advisors deal with all the ramifications of his entertaining and well-paid gig at the Olympics?

Never mind Snoop Dogg, what about Hamish?

Now, being a nerd, I took a look at the double tax agreement between New Zealand and France and yes, a similar clause is in there for artists and athletes. Accordingly, if you are competing in France and you are paid, you will be taxed. And this might actually be of relevance for Hamish Kerr because as I understand it, the track and field gold medallists each got US$50,000. France might be looking to take a cut of that.

But there is an exception in Article 17 of the treaty where any payment made to an artist, or an athlete will only be taxed in the jurisdiction where that athlete is resident – New Zealand – if those activities (carried out in France at the Olympics) are supported substantially by public funds from New Zealand.

I’m guessing most of our Olympians are heavily supported by public funding which should mean that any payments that our athletes receive for winning medals, or in relation to their activities in Paris, are only taxable in New Zealand thanks to this exemption under the double tax agreement. It would be interesting to see what comes with this. (It’s also worth noting that although the International Olympic Committee earns billions from the Olympics, the majority of the athletes receive nothing for their efforts).

I thought it was an entertaining wee story, but it also highlights a common issue and something that people perhaps don’t appreciate. That artists and entertainers have some of the most complex tax planning issues of any individual, certainly outside the hyper wealthy and multinationals. That’s because when they trade, carry out gigs in various jurisdictions, they are potentially triggering tax liabilities in every country in which they perform. But in this particular case, although Snoop Dogg may have a tax problem, I’m hopeful that no such problem will be encountered by Hamish Kerr for his winnings.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.