The Coalition Government is not proposing to reduce the top rate of income tax from 39% in the near future. It’s therefore probably no coincidence Inland Revenue announced it has started contacting taxpayers it has already identified who appear to be “diverting their income and benefiting from their different tax rate”. Inland Revenue has suggested to tax agents to contact it if they think their clients might be affected and has actually given a specific e-mail address for tax agents to do so.

Prior to when the tax rate was increased to 39% in 2021, Inland Revenue released a Revenue Alert RA 21/01 on diverting personal services income. This Revenue Alert did was to pick up what had happened the previous time we had had a 39% tax rate and the famous, or infamous, depending on your point of view, Penny Hooper decisions. Those cases involved two surgeons who each provided their personal services through a company which was in turn owned by a family trust. Although they were each paid a salary, the salaries were not considered commercially realistic, and the Supreme Court ruled the arrangements represented tax avoidance.

The structures used in Penny Hooper are still commonly used today and with the big rate differential between the company tax rate of 28% and the top personal tax rate of 39% there is obviously a quite a heavy incentive to adopt structures to minimise the impact of tax.

Inland Revenue has been looking at these types of structures for some time. Last year it put out some proposals for “countering” abuse which received a fair bit of pushback when it proposed expanding the ambit of the so-called 80% one supplier rule. The effect of this expansion would have meant that a lot of smaller professional services firms would have been caught with more income subject to the individual personal tax rate.

Inland Revenue backed off on those proposals. However judging by what has been said by the new Minister of Finance Nicola Willis about the state of the Government’s books, combined with the fact that National’s proposed foreign buyer’s tax isn’t happening, means that the funding of National’s proposed tax relief package is rather tight to put it mildly. Against this backdrop I would not be at all surprised to see Inland Revenue reactivate those proposals from last year and push them forward again

I also expect that the increase in the trustee rate tax rate to 39% from 1 April which was included in a bill of the previous government, and which has just been reintroduced, will go through. It would be consistent to do so when considered as a base protection measure to ensure the integrity of the top personal tax rate of 39% is maintained. Whether there will be some form of de minimis exemption we will have to wait and see.

Tax deductibility when letting a room to a flatmate

Moving on, Inland Revenue has also released this week an interesting Question We’ve Been Asked which will be relevant to a number of people. QBWA 23/08 explains when a person can claim deductions for expenditure occurred in deriving rental income when that person rents a room in their home to a flatmate.

The amount of expenditure which will be deductible will be determined by apportioning between the private use portion of living in the house and the income earning proportion. Basically, you can apportion based on the relative proportions of physical space: if 20% of the house is being rented therefore 20% of the associated expenditure would be deductible.

The QWBA also covers off the application of other rules. For example, the interest limitation rules which we have been discussing quite frequently recently, these do not apply if the land is used predominantly for the person’s main home.

Similarly, the residential ring-fencing rule will also not apply if more than 50% of the land is used for most of the income year by the person as their main home. In theory if a homeowner had one flatmate and somehow it turns out there was a rental loss, possibly because of high interest payments, such a loss could offset against the home-owner’s other income.

Finally, the complex mixed-use asset rules shouldn’t apply either, because the house is unlikely to be left vacant for the required period of at least 63 days in a year. Even if the mixed-use asset criteria are satisfied the QWBA thinks the exclusion for long term rental property is likely to apply.

The QWBA also notes that in general the fact the person rents out a room in in their home to a flat mate while living in it should not stop the home being the person’s main home. Overall, this is an interesting QWBA even if only applicable in very specific circumstances. I think given the way interest rates have risen and the large mortgages some people have had to take on to get into the housing market makes it of more relevance appears at first sight.

WorkRide FBT exemption

Another bit of good news this week is the release of a Product Ruling in relation to provision of self-powered or low-powered commuting vehicles to employees of WorkRide’s customers.

Under the WorkRide scheme it enters into agreements with employers under which the employees of WorkRide’s customers agree to a temporary reduction in salary in return for a temporary lease of an electric bike/electric scooter and the opportunity to own the bike/scooter at the end of the lease period.

Under the ruling so long as the limits of the cost of the equipment being provided to an employee are not exceeded then the employer is not liable for Fringe Benefit Tax (FBT) on the value of the bike/scooter provided. The employer can claim the GST charged on the leasing of the equipment to it by WorkRide. The amount of the salary sacrifice agreed between the employer and the participating employee cannot exceed the amount of the service fee charged by WorkRide. The amount of salary sacrifice does represent a taxable supply for GST purposes.

It will be interesting to see how many people take up the exemption which certainly should be attractive to those working in inner city areas.

$1.4 billion of interest deductions claimed for 2021-22 tax year

Finally, this week, coming back to interest deductions, tax guru and former podcast guest John Cantin posted on LinkedIn earlier this week an Inland Revenue response to an OIA request he had made regarding the amount of interest deductions claimed by residential property investors in the 2021-22 tax year together with the amount of rental losses “ring-fenced”.

In summary,140,660 taxpayers claimed interest deductions totalling just over $1.4 billion. 47,490 of these had $663.9 million of rental losses ring fenced after deducting 563.9 million. Therefore 93,170 taxpayers claimed interest deductions totalling $845.6 million, which were allowed in in full. This means about a third of all taxpayers (33.7%) had their interest deduction effectively limited and this amounted to about 40% of the total interest deductions.

We don’t know the exact fiscal effect, that’s dependent on each taxpayer’s marginal tax rate. Assuming an average 20% rate, the cost would be $169 million and on a 33% tax rate $279 million per annum.

These figures are for the first tax year in which the restrictions kicked in, which was 25% non-deductible from 1st October 2021. The first full year of restrictions is for the year ended 31 March 2023. But the data for that year won’t be available until after March next year when the filing period for 2023 tax returns is over. You can still see there’s quite some significant numbers here around the impact of restricting interest deductions and therefore the cost of removing those restrictions.

Incidentally on this I’d be very interested to see what happens going forward for investors buying properties which don’t qualify as new builds. At present such investors aren’t to claim interest deductions and that was a deliberate policy decision by the Labour government. Could the new Coalition Government change that rule to allow interest deductions subject to the interest limitation rules for the relevant period. We shall see, and as always, we will bring that news when and if it happens.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

More details have emerged about the Coalition’s tax plans with a surprising twist that changes to interest deductibility for residential property investors have effectively been backdated to 1st April this year. Like many others when I was discussing this last week, I assumed that the reference to 2023/24 was to the Government’s financial year ending 30 June 2024 and the increase to 60% deductibility would kick in from 1st April 2024. (National’s own workings released during the Election use a 30 June year-end).

But this week the ACT Party clarified the increase in deductibility to 60% is in effect for the current income year, ending on 31st March 2024. So effectively, it’s backdated to the start of the year on 1st April. That caused a wee bit of a stir, because something of this nature hasn’t been done in a while. I can’t recall a new government coming in and announcing a tax measure effectively having a retrospective effect.

The change accelerates the restoration of full interest deductibility. It means that from 1st April 2024, interest deductibility will rise to 80% and then will be fully 100% deductible from 1st April 2025. So, within the next 16 or so months, it will be restored to full deductibility. However, as CTU Chief Economist Craig Renney pointed out this acceleration adds another $900 million over the forecast period to the cost of restoring interest deductibility.

Changes to provisional tax?

One of the practical implications of the change is an interesting debate around what action landlords who are provisional taxpayers should take. Such landlords would have paid the first instalment on 28th August. This would have been done based on either 110% of the residual income tax for the 2022 tax year, or 105% of the residual income tax for the 2023 tax year. In both cases, the interest deductibility proportion was higher, so the change might not have an effect. On the other hand, interest rates were lower in both years, particularly in 2022.

What I think you’ll almost certainly see is taxpayers will be keen to understand the impact of the change and how it will affect their provisional tax. My general view would be to pay on 15th January as normal, but then have a really close look before the final instalment on 7th May next year when you should have a fairly good idea of your likely tax liability for the year.

Still there are options to perhaps consider reducing the next amount of provisional tax. And some will take advantage of that. Of course, the risk comes that you may have to pay use of money interest at 10.93%. Although tax pooling can help with that.

What else is now clear?

The release of the Government’s 100 day, 49 point action plan makes clear the Auckland Regional fuel tax is to be abolished and increases to the fuel excise duty will not go ahead. No surprises there as National campaigned on these initiatives. The Clean Car Discount is set to go by the end of this year.

A $900 million bigger hole

As I mentioned earlier, one of the fallouts of the change in the timing of the restoration of full interest deductibility for residential property is an extra blow out by $900 million dollars. One of the apparent means of meeting that gap is the rollback of smokefree legislation, which was set to be world leading. Ironically, several countries seem to have decided to follow our previous example.

The smokefree changes have caused quite a stir. Bernard Hickey in his daily substack The Kaka said that Treasury had estimated that using a 3% discount, smoke free legislation would cut public health costs by $5.25 billion. But that’s now being kicked down the road.

We’ll know more about progress on other measures to fill this gap when the Half Year Economic Fiscal Update, and the promised Mini-Budget are announced on 13th December.

Time to legalise and tax marijuana? The Colorado example.

But if we are looking at the question of raising taxes, or essentially getting more tax revenue from tobacco excise duty, then I’m going to pick up a point that I’ve had for some time and ask why not legalise and tax marijuana. Now, yes, there was a referendum which voted against that. But referendums are not binding on governments. I also think there are second order benefits of legalisation including putting a hole in organised crime’s finances.

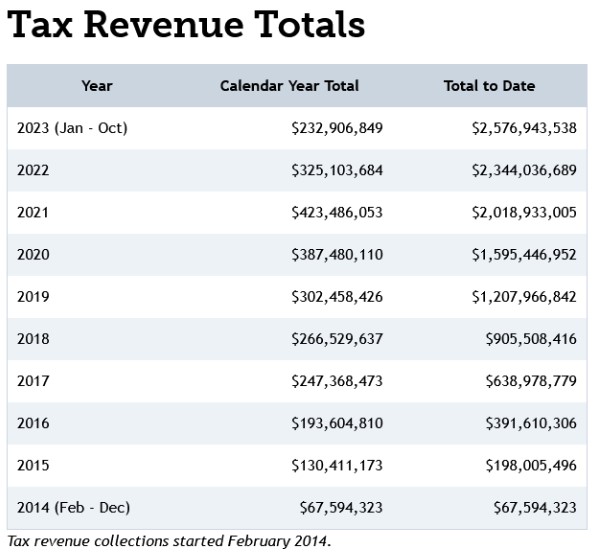

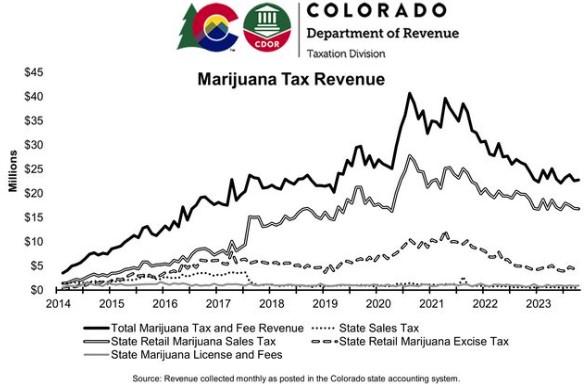

At present 24 states in the United States of America have now legalised or decriminalised marijuana. One of those is Colorado, which has a population of just over five million, more or less identical to Aotearoa New Zealand.

Colorado legalised marijuana in 2014 and have been taxing it since then. The taxes comprise the state sales tax (2.9%) on marijuana sold in stores, the state retail marijuana sales tax (15%) on retail marijuana sold in stores, and the state retail marijuana excise tax (15%) on wholesale sales/transfers of retail marijuana. In addition, Colorado also has fee revenue coming in from licensing and application fees.

Colorado’s Department of Revenue publishes monthly marijuana tax reports, and between February 2014 and October this year it has collected over US$2.5 billion from marijuana taxes. That’s over NZ$4 billion.

However, whether you are taxing smoking or marijuana, long term, the revenue should decline to nil, because ultimately we want people to not smoke because of the health order benefits. You can see this in Colorado’s marijuana tax revenue which rises quite steadily initially but then since mid-2021, it has started to fall away. This is probably the second order effects of people stopping smoking altogether.

But anyway, on average, the tax take is settling down to about US$300 million a year which is roughly $500 million New Zealand dollars. That’s actually a not insubstantial amount of revenue.

So that’s the Colorado example. I’m not going to say it’s going to happen here under the new Government. But you never know. Henry Kissinger died yesterday, and the relevance of that is that he was the one who coined the phrase “Only Nixon could go to China” which opened the door to a US rapprochement with China.

The phrase means bold leadership could surprise people by doing the unexpected. Bear in mind, back in 2015, John Key and Bill English surprised everyone by introducing the bright-line test. The point by referencing Kissinger and Nixon, two of the nastier people of the 20th Century, is that a bold and welcome change of direction can come from an unexpected source.

Revision of the bright-line test – when?

Speaking of the bright-line test, it isn’t specifically mentioned in the 49-point first 100 days action plan the Government announced on Thursday. I imagine we’ll get the timeline for revision at the Half Year Economic Fiscal Update.

“Overlooked” some income? The clock never stops ticking for Inland Revenue

This week Inland Revenue released five Technical Decision Summaries with a common theme relating to disputes over omitted income and penalties. To recap, Technical Decision Summaries are anonymised summaries of adjudication decisions made by a unit within Inland Revenue’s Tax Counsel Office as part of the formal dispute process between Inland Revenue and taxpayers.

The facts vary slightly in each summary, but all involve some form of income diversion/suppression which was picked up by an Inland Revenue review. For example in TDS 23/18 the taxpayer was the sole director and shareholder of Company B which carried on a retail business. The taxpayer also held 49% of the shares in Company A which operated a retail business. Y, who was married to the taxpayer, was Company A’s sole director and held the remaining 51% of its shares. The Taxpayer was also a settlor, trustee, and beneficiary of a Trust which was involved in property investment. (This is a fairly common structure in my experience.)

The Taxpayer filed income tax returns showing wages from which PAYE had been deducted and shareholder salary from Company B and income from the Trust. But on review by Inland Revenue, it appeared that money from Company B had been deposited into the taxpayer and his wife’s personal accounts partner and then used to pay personal expenses and to fund a property major purchase made by another company. These deposits had not been declared as income.

Inland Revenue proposed taxing this income and included a shortfall penalty for tax evasion. The shortfall penalty for tax evasion is 150% of the tax that’s been evaded, although in this case it will be reduced by 50% because of previous good behaviour.

What is also of note here and the other four Technical Decision Summaries is that the four-year time bar period for many tax returns had passed in respect to some of the years in dispute. (Generally, Inland Revenue can’t increase an assessment if it’s more than four years after the end of the tax year in which the relevant return was filed). The taxpayers tried to rely on the time bar rule but Inland Revenue argued it did not apply because of tax evasion and omission of income.

And that is how it panned out. The Tax Counsel Office’s Adjudication Unit ruled there is assessable income and the time bar provision is not applicable because of tax evasion and/or omission of income. Accordingly, the shortfall penalties also applied.

As I mentioned the other Technical Decisions Summaries involved similar issues and had similar outcomes. In TDS 23/16, there was a further problem for the taxpayer in that they were trying to make a subvention payment, to offset losses. And that was also turned down because of a lack of common shareholding.

There are some good lessons from these summaries, primarily if you don’t declare income, don’t try and rely on the time bar to stop Inland Revenue looking at earlier years. As the summaries make apparent it’s very clear Inland Revenue has the power under sections 108 and 108A of the Tax Administration Act 1994 to assess older years that would normally be time barred. In such circumstances, shortfall penalties for tax evasion will almost always apply.

“A really good idea”

As I mentioned last week one of the things that was surprising about the Coalition’s tax policies is the additional resources for Inland Revenue’s audit and investigation activities. On TVNZ’s Q+A last Sunday Minister of Finance Nicola Willis said that she welcomed the proposal which she thought “was a really good idea.”

We’ll only know exactly how much extra funding Inland Revenue is going to get in the Budget next May. But for the moment, you can expect Inland Revenue to be cranking up its investigation activity, and you can expect to see a lot more shortfall penalties kicking in.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

When the shape and tax policies of the new Coalition Government were announced one of the first surprises for me was the appointment of Simon Watts, the National MP for North Shore, as Minister of Revenue. I was surprised by this because Andrew Bayly has been National’s Spokesperson for Revenue for the past four years.

During that time, he has built up knowledge and background in this area. And I know that colleagues who have met him believe he understands the issues involved in the portfolio. So, it is a surprise to see Andrew overlooked for this portfolio. Obviously, there are reasons behind that, but it still means that Simon Watts will be picking up a portfolio with little background knowledge on how Inland Revenue has been operating. But no doubt he’ll get up to speed quickly. It will be interesting to see what’s in the Inland Revenue and Treasury Briefings to Incoming Minister. And we’ll report on that when those briefings are released in due course.

No foreign buyer’s tax but plenty of “buffer” still

In terms of the headlines about what what’s happened, it is no surprise to hear that the foreign buyers’ tax proposed by National is off the table. That was obviously a precondition of getting New Zealand First on board. The coalition is “committed to delivering tax relief” with increases to tax thresholds from 1st July 2024.

But beyond that, it’s not clear what’s to happen. National’s agreement with Act confirms “…no ongoing commitment to income tax changes, including threshold adjustments beyond those to be delivered in 2024.” Furthermore, the two parties recognise “that details of [National’s] Fiscal Plan may be subject to amendment in response to significant new information or events.”

The agreement with New Zealand First refers to letting “Kiwis keep more of what they earn with tax relief of up to $100 per fortnight for an average income per household and a Family Boost childcare tax credit of up to $150 per fortnight.”

At the press conference following the signing of the Coalition agreement the incoming Prime Minister Luxon, said in response to the cancellation of the foreign buyer’s tax that National believes there is a “buffer” available to allow the proposed tax threshold adjustments to happen next July. They actually have a buffer around the finances.

Interestingly, when you go through both coalition documents there is no reference to “budget surplus” in either document. But there is a commitment to restore fiscal responsibility and deliver value for money. So, what does that mean? It could be that the Coalition might be prepared to allow deficits to run longer than was previously said. Otherwise, there’s no mention of how the gap created by the lack of the foreign buyer’s tax will be met. We might get a clearer idea with the mini-Budget which is going to be part of the Half Year Economic Fiscal Update to be released in mid-December.

Accelerated restoration of mortgage interest deductibility

National campaigned on a phased restoration of full mortgage interest deductibility for residential rental properties. That timeline will be accelerated under the agreement with Act. From 1st April 2024, it’s going to be 60%, then 80% from 1st April 2025 and 100% from 1st April 2026.

The agreement with Act includes the repeal of the Clean Car Discount and a commitment to

“Ensure the concepts of Act’s income tax policy considered as a pathway to delivering National’s promised tax relief subject to no earner being worse off than they would be under National’s plan.”

A couple of New Zealand First surprises

There are a couple of interesting initiatives in the New Zealand First agreement neither of which were part of their election policies.

The first is “By or before 2026, assess the impact inflation has had on the average tax rates phased by income earners.” This is an implicit acknowledgment of the impact of not increasing income tax thresholds since 2010. We should actually get a measure of the consequential effect of fiscal drag. I wonder if this initiative would include Working for Families’ abatement level. However, there’s no commitment to take action on the findings.

More funding for Inland Revenue investigation

More importantly, and already incoming Minister of Finance Nicola Willis has included the impact of this in the “buffer”, the Coalition Government will “increase funding for IRD tax audits to urgently expand the IRD tax audit capacity, minimise taxation losses due to insufficient IRD oversight, and to ensure greater integrity and fairness in our tax system.”

How this will be achieved, is going to be very interesting to see. Obviously, it should mean an increase in resources for Inland Revenue. Exactly how much we probably won’t see the full details until the full year’s Budget next May. Still, this is a surprise, including the fact that it has got sign off from Act as well, who are generally committed to lower taxes. (Incidentally, Inland Revenue ought to be safe from Act’s proposal to reduce the public sector headcount by reference to a 2017 baseline, because its staffing level has fallen from 5,519 in June 2017 to 4,130 in June 2023).

Sharing GST with Councils?

The agreement with Act contains a couple of other proposals of varying interest. Firstly, the new Government will not progress the development and delivery of National’s manifesto commitment to a “Taxpayer’s Receipt” for taxpayers. Although minor it’s interesting that Act didn’t want that.

On the other hand, in terms of local government financing, there’s a couple of things here which I think are really interesting and potentially significant. Firstly, they are to consider sharing a portion of GST collected on new residential builds bills with councils. This is part of Act’s commitment to wanting to expand development and housing, that it thinks there should be more revenue sharing going on councils. I agree we should be looking at how councils fund themselves because my view is the current model is unsustainable, particularly for very small councils. A shake up in this area is well overdue and sharing GST receipts is one option going forward.

Road user charging & a congestion charge for Auckland?

The Act agreement calls for work to replace the fuel excise taxes with electronic road user charging for all vehicles starting with electric vehicles, which are currently exempt from road user charges. Does this mean the Auckland regional fuel tax isn’t to be repealed until this new system is in place? The agreements are not clear on this point. [It appears that unless a specific National policy is covered by one or both the agreements it remains National policy. This would appear to include the reduction in the Bright-line test timeframe to two years].

During the election campaign Auckland Mayor Wayne Brown asked if the Auckland regional fuel tax goes how was Auckland going to fund that gap.

The Act agreement has a specific commitment to “Work with Auckland Council to implement time of use road charging to reduce congestion and improve tight travel time reliability.” Again, that’s something that Mayor Wayne Brown has mentioned recently. And maybe it’s tied into that question of a replacement for the regional fuel tax.

A public health levy?

Also of interest in the Act Coalition Agreement is a reference in its immigration policy introducing “a five-year renewable parent category visa, conditional on covering healthcare costs, with consideration for public health care levy.” It’s not clear whether this levy refers to those people coming in under that immigration category or a wider public health care levy. It doesn’t appear to be a commitment in Act’s election promises.

39% trustee rate

The Agreements are silent on whether the outgoing Labour Government’s intention to increase the trustee tax rate to 39% will be implemented. This is part of an existing tax bill which lapsed when the last Parliament rose. This particular bill must be reintroduced because it includes setting the annual income tax rates, which must be passed each year to enable the funding of the government. This initial silence implies that that the increase in the 39% Trustee tax rate is going to remain. We’ll have to wait and see but we’ll probably get more specific information when the Half-Year Economic Fiscal Update is released next month.

(This is an edited transcript of part of the Podcast recorded on Friday 24th November)

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This is the first year under the leadership of new Commissioner of Inland Revenue, Peter Mersi, who took over from Naomi Ferguson on 1st July 2022. It’s worth noting that Inland Revenue hasn’t had the easiest of 12 months. It did finalise its Business Transformation programme in the June 22 year, but during that period it was tied up very heavily with this and then the various COVID support programs. Those have wound down in the June 2023 year, but it got landed with the Cost of Living Payments program, which the last Government introduced in its May 2022 budget.

At first sight, the structure of the Annual Report seems similar to that of previous years, but there are several subtle differences in the presentation and layout and in the department’s apparent focus. Overall, the report feels a lot more readable and digestible than in previous years.

One of the first signs of a change of approach is the lack of reference to a mission statement. Instead, there’s a clear emphasis on Inland Revenue’s role and the benefits for everyone that it delivers. As one of the online bookmarks to the Annual Report notes, “the tax and social policy system is a major national asset which underpins the well-being of all New Zealanders.” Under the headline, “We deliver three long term outcomes for Aotearoa New Zealand” page ten of the report summarises these long-term outcomes as Revenue, Social policy payments and Collaboration.

A more collaborative approach

Now, the last point about collaboration is interesting because this is a point picked up in other places in the report. In fact, the reference to collaboration is new. The word was never used in last year’s report, but this year it is a clear theme and I think it’s a welcome development. The report also talks about partnerships noting,

“We work with many other parties to help manage and run the tax and social policy systems such as tax agents, employers, KiwiSaver providers, financial institutions and community groups such as Citizens Advice Bureau.”

The report also references the international cooperation, such as with the OECD and tax agencies in other jurisdictions. And it notes that it exchanges financial account information under the Common Reporting Standards and the automatic exchange of information with almost 100 jurisdictions. As I’ve said in previous podcasts, the depth and extent of the international information sharing exchanges that go on are not well understood by taxpayers. In fact, probably are underestimated by many.

Reviewing last year’s report, I thought Inland Revenue had a bit of a bumpy relationship with tax agents, but I noted Peter Mersi was busy meeting representatives of professional bodies, clearly with the intention of addressing this particular point. And on the ground as tax agents we can see there’s been progress in this field, and we feel that there’s a definite shift in the attitude towards ourselves with greater cooperation.

It’s also made clear in the report that Inland Revenue sees tax agents as a vital part of the tax ecosystem.

This is a very welcome development in my mind and, as I said, mirrors what we’re experiencing on the ground. We certainly would like more support, such as easier phone access and definitely an updated playlist when we are put on hold. There are only so many times in the day I can hear Sierra Leone.

Overview of report

As I said, there’s a fresher feel to this year’s report which looks better organised and more readable for the general reader. If you’re wanting to dip into the report, page 11 sets out a good overview and then pages 14 to 38 summarise its work. There’s plenty of graphics and it’s very readable.

99% of income tax, GST and employment information returns are filed digitally, pretty near identical to the June 2022 results. It currently costs $0.43 to collect every hundred dollars of tax revenue. Back in 2015, that figure was $0.80 per hundred dollars of tax revenue.

Investigations and assurance – a mixed bag

I’m always interested about specific programs Inland Revenue has been running in the compliance space and I think this is a bit more of a mixed bag. According to the report it “identified or assured $973 million in revenue through our interventions.” This covers a number of initiatives. There is reference, for example, to advanced pricing agreements, which are prepared by multinationals in relation to agreements between a New Zealand subsidiary and its offshore affiliates. The idea is to make sure that Inland Revenue is satisfied that the transfer pricing regulations have been met and revenue is not being stripped out of New Zealand. Apparently 92 multinationals have active advance pricing agreements as of 30th June representing tax assured of about $440 million a year.

Real-time reviews

One of the other great things that the Inland Revenue has got as a result of business transformation, is the ability to pretty much live track applications that are being made. This topic is probably worth a podcast on its own to explain its capability. We understand from Inland Revenue presentations that it very carefully watched what was going on when applications for COVID support payments were being made.

With real-time reviews, if Inland Revenue sees something which on the face of it, looks incorrect it can take immediate action to defer payment or put that application under additional scrutiny before it’s paid out. According to Inland Revenue’s report, real time review of returns stopped, “$145 million of incorrect or fraudulent refunds or of or tax deductions at the time of filing”. Real-time reviews mean if a person is filing online and is constantly correcting a return and it appears this is because the person is after a certain result that will be identified by Inland Revenue for review.

International compliance

As I mentioned earlier, Inland Revenue is party to over 100 international information sharing agreements. According to the report Inland Revenue it received more than 600 voluntary disclosures over the last three years, resulting in more than $74 million in omitted overseas income now being assessed. That’s a bit of a surprise in my view and is probably on the low end in my view. We see quite a bit of movement in this area with people coming forward when they realise they haven’t complied with their obligations and we help them make the right declarations and pay the correct amount of tax.

In fairness this was an area, prior to the pandemic where in the wake of the introduction of the Common Reporting Standards on the Automatic Exchange of Information Inland Revenue was gearing up to throw quite a bit of resources at perceived non-compliance. Of course, that all went sideways, but with things sort of settling back down to a new normal, we may see Inland Revenue activity pick up again depending on resourcing.

Scope for more investigation work?

$397 million of the $973 million “assured” in the year stemmed from investigation work. Comparisons are not clear, but it appears well down on previous years. So, this is an area for improvement. By a perhaps slightly unfair comparison, the Australian Tax Office recently announced that it had picked up and collected an additional A$6.4 billion in the year to June 23 as a result of its tax avoidance taskforce.

This was a specific ATO initiative which scrutinised the tax returns and outcomes of the largest 1100 businesses and multinational groups in Australia to verify that they were paying the right amount of tax.

I expect Inland Revenue looked at that program and considered what lessons and opportunities a similar program might present. But it should be said that the Australian economy being bigger it also presents more opportunities for the ATO. The other thing about the Australian economy in transfer pricing terms, is it’s further up the value chain. In other words, more value can be created and captured in Australia, whereas New Zealand is more typically a price taker. Nevertheless, I think there’s room for improvement in the investigation space.

Increase in outstanding tax debt

As of 30th June, the total amount of general tax and Working for Families debt amounted to $5.8 billion. That’s up $600 million from the June 2022 year. At year end more than 524,000 taxpayers had a tax payment that was overdue although 315,000 owed less than $1,000. During the year Inland Revenue wrote off or remitted $754 million of debt compared with $689 million in 2022.

$231 million of the $754 million written off related to penalties and interest for taxpayers affected by COVID 19. In the wake of the pandemic if a taxpayer fell into debt as a result of COVID 19 Inland Revenue adopted a sympathetic view and was prepared to write off interest and penalties on such debt.

The rise in debt is a concern, but it’s a reflection of a number of things going on, not least of which the fact the economy is slowing down. Consequently, there are 44,000 more taxpayers with tax debt than in 2022. As ever, Inland Revenue’s working with those in debt to set up arrangements to pay off the debt. As I’ve said many times previously, if you’re in debt approach Inland Revenue and if you show serious intent to deal with the debt, it is generally willing to enter into an arrangement.

During the year they entered into 163,000 such debt arrangements. That’s up nearly 20% on the 140,000 for the previous year. As of 30th June 2023, there were still 77,000 active arrangements involving tax and student loan debt, which covered about $1.6 billion or just over a quarter of all debt.

Incidentally, on the measurement of tax debt to tax revenue, tax debt is about 5% of tax revenue, which isn’t bad by international comparisons, and certainly is an improvement on the 2013 year when it was nearly 10%.

More legal action

Inland Revenue also started to play harder with defaulters. It threatened legal action or issued notice of legal proceedings against 2850 taxpayers and 35% of those promptly settled in full or set up an arrangement. It’s also issued a thousand statutory demands involving other defaulters. I think we can continue to see expect to see the level of legal action continue to rise during in the current year.

More new hires

The key to any organisation is its people. And after the upheaval of business transformation which saw Inland Revenues workforce fall by 25% between June 2018 and June 2022 this is the first year since June 2015 that there were actually more new hires than exits. Inland Revenue’s total workforce rose by a net 203 persons, or 5.2% to 4,130. Staff turnover was 10.1%, which is a big improvement on last year’s 18.7%.

As for the profile of Inland Revenue, two thirds of its workforce are women. The average age of staff is 45.3, with an average length of service of 13.7 years. Now, the length of service has fallen in recent years, but it’s an improvement on the 11.1 years’ average service in the June 2014 year.

How much does all of this cost?

What’s interesting is that Inland Revenue didn’t spend all the appropriations it received from the Government for the year. The appropriations budgeted for the year was $735 million, but it actually only spent $691 million. That underspend of $44 million was partly due to challenges recruiting staff in the tight labour market and the timing of residual transformation activities. That underspend is going to be transferred to the current year subject to confirmation by ministers.

The operating expenditure on contractors and consultants fell to $42 million from $75 million in the previous year. And apparently the ratio of contractors and consultants operating expenditure to workforce spend was 10.3% this year, compared with 17.6% now.

Last year I noted that the Department had devolved authority to Madison Recruitment Ltd to provide extra staff, which didn’t terribly impress me because I think delegating authority outside the public service is not something a revenue authority should do lightly.

Inland Revenue engaged Madison Recruitment again in June 2022 to provide contingent labour to help with the roll out of the Cost of Living Payment scheme and wrap up of the COVID 19 support work. This engagement finished on 16th December 2022.

Areas for improvement

There are three specific areas where I think there is potential for improvement. Firstly, underspending by $44 million even allowing for a tight labour market is a bit of a concern. And so, I’d want to make sure that the appropriations are fully utilised to build the appropriate capacity.

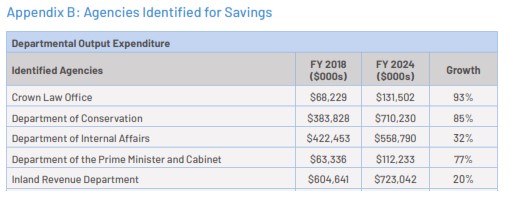

And on this I would just say that during the election campaign, National campaigned on cuts to civil service and Inland Revenue is one of those departments identified for savings. As I’ve noted, Inland Revenue has lost a quarter of its staff since 2018. In fact, if you look at the numbers National used for their policy, you can see that the increase in Inland Revenue’ spend since 2018 was 20%, whereas inflation since June 2018 is 23.4% (based on the Reserve Bank’s inflation calculator).

In other words, Inland Revenue has not been increasing its staff and spend above inflation. The Business Transformation program has delivered quite a lot and the report has some very interesting commentary on this. The estimated cumulative reduction in compliance costs for SMEs is thought to be around $925 million. The cumulative additional Crown revenue was expected to be $1.86 billion for the year and next year it projected a $2.8 billion. Internal Revenue is achieving its goals, but there’s always room for improvement. If the incoming Government’s finances are going to be tight which is what we’ve heard, it seems odd to be proposing reductions for a department which is actually very efficient and which gets a very good return on investment.

Getting better returns on investment

That said two of the areas where added investment measures return between $7 or more per dollar invested would be investigative capacity and debt management. In the area of debt management generally, we appear to be in the downside of the economic cycle so debt is bound to rise and to some extent there’s little Inland Revenue can do about that.

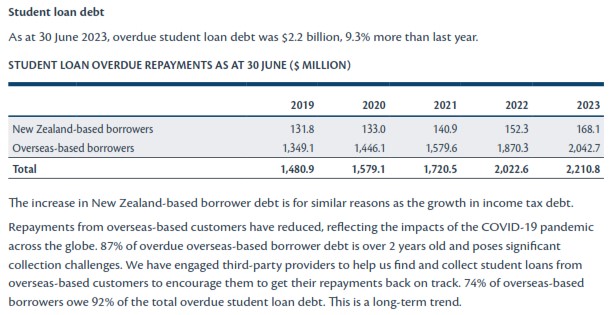

Student Loan debt a major area for concern

But there is an area where I think Inland Revenue really should and could be doing a lot more, and that’s in the student loan debt sector because the numbers are really quite large. The total amount of student loan debt rose by over 10%. And it’s particularly increasing in relation to overseas based borrowers.

Inland Revenue ran a specific campaign in May this year to remind those overseas based borrowers who had missed payments due on 31st March. It contacted nearly 75,000 such borrowers resulting in over 3000 instalment arrangements. But at this stage, the amount of overdue student loan debt now stands at $2.2 billion and over $2 billion of that is overseas based borrowers.

And this is where Inland Revenue does not seem to be as on top of the issue as it should be. I talked previously about the agreement with the Department of Internal Affairs in relation to child support. The same information sharing agreement is used to track down student loan debtors. During the year Inland Revenue received nearly 237,000 contact records from the Department of Internal Affairs. Through cross-checking its records for overseas based student loan defaulters, it managed to get hold of 88 defaulters resulting in 108 payments totalling $16,421. That’s pretty average, to put it mildly.

Time to rethink the Student Loan scheme?

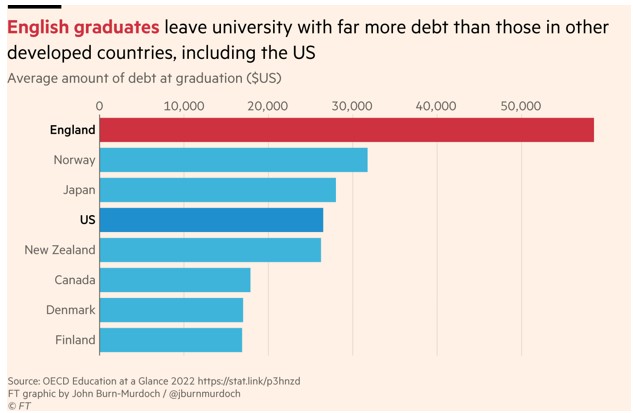

If we are looking at where to put extra resources, then there’s something else we need to think about in this area. Just adopting a big picture approach here maybe we should ask whether in fact the student loan scheme is achieving what we want. I came across a graph in the Financial Times which noted that English graduates leave university with far more debt than those in other developed countries, including the US. English graduates were leaving with debt in excess of USD50,000 (NZ$85,000). New Zealand graduates are just below the US with USD26,232 or NZ$45,550 on graduation.

And we have a large diaspora with over a million Kiwis overseas. We have a large amount of overseas student loan debt, but we also have a skills shortage. I just wonder whether as well as trying to find a better way to manage that debt we should be thinking more about encouraging people who’ve taken on student debt to stay here to meet those skills gaps maybe through debt moratoriums.

I would say overall for Inland Revenue it’s been a good year mostly, a difficult one at times, but it’s done a good job. However, I think the issue of debt management needs to be addressed swiftly and be properly resourced.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week, the OECD/G20 announced a new multilateral convention had been agree in relation to Amount A of Pillar One of the international tax agreement.

Pillar One is the part of the international agreement which allocates the taxing rights to market jurisdictions with respect to the share the profits of the largest and most profitable multinational enterprises which are operating in that jurisdiction’s markets, regardless of whether or not the multinational has a physical presence.

This multilateral convention is also intended to ensure the repeal and prevent the proliferation of digital services taxes and other similar measures. Based on 2021 data, the OECD/G20 estimate that this should result in about US$200 billion of profits being reallocated each year. This should represent an approximate additional corporate income tax of about between US$17 and 32 billion.

Although the convention has been signed, we’re still working forward towards the actual final detail and agreement on the application of Pillar One and for that matter, we’re also working forward on the application of Pillar Two. This multilateral convention, by the way, extends to perhaps 800 pages so you can see the level of detail involved.

Yeah, but are we getting there?

You may think we’ve heard this sort of announcement before, and we have. What’s happening is the framework of how the final international agreements will operate is being put into place very slowly. But, and it’s a big but, are we actually going forward and is an agreement on the cards? And that’s where a fair bit of scepticism is starting to develop amongst those in the international tax community who deal with international tax issues day in, day out. (I have to be honest that most of this stuff involving the multinationals is way above my pay grade).

There was a particularly interesting article this week on the matter by Rasmus Corlin Christensen, a political economist at the Copenhagen Business School.

In short, he is highly sceptical of exactly what progress is being made on this and whether, in fact an agreement is as close to agreement as is being touted by the OECD/G20.

His blog post discusses the history of the Pillar One and Pillar Two process from when it started about ten years ago. He notes the tensions that have arisen around the agreements, like all tax, comes down to politics. As he explains, the initial drive for an agreement came from the French, and the Americans have been pushing back because it’s their multinationals that are most likely to be taxed. Although, as he rather wryly notes, Ireland has a big part to play in this because that’s where quite a bit of the profits from larger multinationals such as Apple, for example, are centred.

It’s a good read explaining the whole topic and but he thinks ultimately what will happen is that various pressures will build on the topic as the political posturing and manoeuvring goes on between the Americans and Europeans. But Christensen also points out that emerging nations, in particular Nigeria, the largest economy in Africa, are starting to push back wanting to see some progress.

The concern is if no agreement is reached then the Americans have already indicated as they did so under President Trump, that they will deploy trade weapons and tariffs. No one wants a trade war and that’s where Christensen thinks that this may force the issue bringing about some form of agreement.

Quite apart from the Europeans and Nigeria he also noted that Canada has broken ranks by going forward with a digital services tax. You may recall that just before Parliament rose for the election, the Labour government introduced a digital services tax. This is a fallback in case the Pillar One and Pillar Two negotiations don’t proceed.

But if you’re reading between the lines here, from what Rasmus Corlin Christensen is saying, it’s quite possible that we’re going to need that. And as he notes,

“But there’s really nothing puzzling about Canada’s move, or the proliferation of digital taxes globally. International corporate tax policy has risen to the top of national and global political agendas, with governments individually and collectively asserting their authority against the forces of globalization – a significant shift from years past.”

And this, by the way, fits in with how I see tax policy internationally developing, the era of low taxation globally and corporate tax in particular is over. Governments’ balance sheets and finances, including our own, are under strain. Everyone is looking under all available rocks as to what funds might be available.

Christensen’s article is well worth a read with a different perspective on international tax away from the sort of “rah rah rah it’s all great” messaging coming out of the OECD/G20. He focuses on the politics, but doesn’t necessarily see that this deal isn’t going to happen, it just may happen in a different way than is presently planned.

Good news on the Foreign Investment Fund front?

Still on the subject of international tax, Inland Revenue released an interesting Technical Decision Summary in relation to the ability to change foreign investment fund (FIF) calculation methods. This is a private ruling where the applicant has interests in a number of foreign trusts, unit trusts and companies subject to the FIF rules and the attributable FIF method. The taxpayer hadn’t filed a tax return at this point and they wanted to apply for a ruling as to whether in fact they could change methodologies under the FIF rules.

In certain situations, taxpayers can change their FIF calculation methodology between the fair dividend rate and the comparative value. However, in other circumstances and other entities a taxpayer must apply the fair dividend rate. This is an interesting ruling because it gives clarity around this issue and that and on the basis of these facts, and everything is always be very fact specific, you can change methodologies.

The big caveat I would add here is that a critical fact may well be that they hadn’t actually filed returns because there’s been a bit of controversy about Inland Revenue saying that if a return has been filed adopting one methodology, then you can’t adopt a subsequent change in methodologies in most circumstances. And I just wonder whether that was a factor in this ruling. It’s not a formal Inland Revenue ruling, so it may well be converted to one subsequently. But still, it’s interesting to see some guidance on an area where there’s a bit of controversy developing.

Is a Financial Transactions Tax really worthwhile?

Early in the week, I spoke about how the New Zealand Loyal party had campaigned on a financial transactions tax (FTT) as a replacement for income tax and GST. The last Tax Working Group had looked at the question of a financial transaction tax and come down against it. Generally speaking, no one is overly sold on the idea, but it is something that frequently pops up in discussions or when I’m in public forums. It’s sometimes called a Tobin Tax after the economist who dreamed up.

The idea behind a FTT is the fact that there are vast sums of money flushed through financial systems and on the basis of the good old principle of broad base, low rate, a very small charge on this could raise significant sums of money.

It so happened in reading on the topic, I came across a new working paper by Gunther Capelle-Blancard of the University of Paris’ Centre for Economic Studies of the Sorbonne. The paper takes a fresh look at the whole question of financial transactions tax and particularly looks at what happened with Sweden’s tax which failed badly, and that of France which introduced one in 2012. The French financial transactions tax hasn’t gone as well as expected, but even so, it’s still raising close to €2 billion after nearly ten years of implementation.

The French and Swedish experience

Two main objections to a FTT are firstly, it will encourage displacement, people will take their activity and trade elsewhere outside that jurisdiction. Secondly, people will reduce the volume of transactions to mitigate potential charges. According to the paper there certainly appears to have been a reduction in the volume of transactions happening.

But the displacement activity, which was a big problem for the Swedish financial transaction tax, so much so it was abandoned, doesn’t appear to be the same issue for the French because it’s better designed on that. The key difference being that under the French system it is the nationality of the company that issues the shares, which is subject to the to the financial transaction tax and not that of the counterparties or intermediaries carrying out the transaction. In Sweden, it seems what happened was the activity which would have been done by Swedish stockbrokers, was instead performed outside the country and therefore no financial transaction tax applied.

What about Stamp Duty?

But the other thing that I thought was very interesting and I hadn’t actually considered it beforehand was that Capelle-Blancard has also looked at the example of Stamp Duty on financial transactions. This still applies in the UK at a rate of 0.5% on all share transactions. When you take a broader view, stamp duty is a financial transactions tax. It doesn’t apply as broadly as those proponents of a FTT would want, but it still applies. In the case of the UK stamp duty on share transactions has applied since 1694 and raised £4.37 billion for the year ended 31st March 2022. We repealed stamp duty in 1995 if I recall correctly.

This is an interesting paper, well written and quite understandable, which takes a different perspective on a topic which has been pooh poohed on reasonably strong grounds. But a FTT may actually not be as impractical as has been mooted. What I would say is even if it’s more practical to implement than people have said there is no way that it would ever replace income tax and GST, as the New Zealand Loyal party promoted and many people think it can do, because you would have to impose quite a high charge on transactions. And you would then very definitely see a large displacement/reduction in activity.

The paper notes some absolutely eye watering numbers about the growth in the level of financial transactions “Since the 1970s, global GDP has multiplied by 15 times, market capitalisation by 50, and the amount of stock market transactions by 500.” In France, for example, the total amount of transactions in the Paris Stock Exchange has grown from €3.5 billion in 1970 to over €2,000 billion today.

These absolutely eye watering numbers are why people think a FTT could raise a lot of money. The paper estimates a FTT could raise perhaps as much as between €156 and €260 billion annually, based on a nominal rate of 0.3 or 0.5 per cent. I think people will still look at the idea with some scepticism, but in fact as the paper notes, and I didn’t realise, FTTs are more widely spread than many might realise.

The Election’s over, now what?

Finally, the Election is over, and we’re now waiting to see the exact composition of the Government and what involvement Winston Peters and New Zealand First may have. What does that mean for tax? Well, we will have to wait and see. The expectation is there will be some form of tax threshold adjustments coming up starting from 1st April next year and obviously rollback of the rules around interest limitation for residential property landlords.

But I would just point everyone to the example of the New Zealand First National Coalition Agreement in 1996. National went into that election having already implemented a set of tax cuts which took effect from by sheer coincidence of course, on 1st July 1996, just before the election. There was another round of tax cuts to follow shortly afterwards. But under the agreement that was eventually hammered out, which made Winston Peters, Treasurer/Finance Minister, the second round of tax cuts was delayed for a year.

I’m therefore just wondering whether Winston and New Zealand First might just have a look at the books and say, “Ah, maybe not this time”. And of course, you’ve also got Act on the other side saying, “We want to see some movement on this pretty quickly.” So ,the new Government and the expected Prime Minister, Mr. Luxon, have got some negotiations ahead, which might turn out to be trickier around this issue than we’d all first imagined.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.