Every year, the International Monetary Fund (IMF) undertake an official staff visit or mission to New Zealand as part of regular consultations under Article IV of the IMF Articles of Association. Each IMF mission speak with the Minister of Finance, Treasury officials and other persons – economists, academics and the like about the state of New Zealand’s economy and related issues. At the end of the visit the Mission then issues a short concluding statement of its preliminary findings.

The IMF will then prepare a lengthier report setting out its findings in more detail which we can expect to see in a couple of months time.

“A window of opportunity”

After noting it expects real GDP growth to rise to 1.4% for this year and then to 2.7% in 2026 the Mission noted:

“The macroeconomic environment provides a window of opportunity for New Zealand to consider broad based reforms needed to address medium- and long-term challenges, including to secure fiscal sustainability, boost productivity, address persistent infrastructure and housing supply gaps, and initiate early dialogue on population aging.”

“A comprehensive capital gains tax”

My understanding of the IMF submission is that each Mission has a different focus. This year, I understand the Mission was looking at the question of funding the future cost of New Zealand Superannuation and therefore the tax policies required. This led the Mission to call for some tax policy reforms

“Tax policy can support a more growth-friendly fiscal consolidation, and reforms aimed at improving the tax mix can help increase the efficiency of the income tax system while reducing the cost of capital to incentivize investment and foster productivity growth. Options include a comprehensive capital gains tax, a land value tax, and judicious adjustments to the corporate income tax regime.”

I expect we’ll hear a lot more about this when we see the final report.

“Initiate early dialogue”

It’s not the first time the IMF have suggested a comprehensive capital gains tax, and the Organisation for Economic Cooperation and Development has also frequently made a similar suggestion. Generally speaking, the government of the day just responds, “Yeah, but, nah”. However, the issues prompting the suggestion still don’t go away. In this particular case, the IMF suggests we need to start transitioning into a new system to cope with the rising cost of New Zealand superannuation.

“It is essential to initiate early dialogue among all stakeholders regarding comprehensive reform options that can help mitigate these challenges and other long term spending pressures from healthcare and aged care care needs with a fair burden sharing across generations. This can be further supported by KiwiSaver reforms aimed at achieving greater private savings retirement savings.”

The IMF is echoing comments myself and others have repeatedly made. We have rising costs in relation to aged healthcare and superannuation and we need to start thinking seriously about how we’re going to address those. This is a multi-generational impact. One of the unusual points about New Zealand Superannuation is it is a fully funded universal pay as you go system.

An intergenerational issue

In other words, it’s available to everyone, but it’s funded out of current taxation. I think there’s a widespread perception that some part of your tax pays for your future superannuation. It doesn’t. Tax paid by working people below the age of retirement is used to fund the current superannuation of those who have retired. The funding of superannuation is therefore a major intergenerational issue but one rarely discussed. Hence the IMF’s call to initiate early dialogue. I’ll have more on this when the IMF releases its final report.

In the meantime, whenever the IMF or OECD calls for tax reforms, the Minister of Finance of the day usually responds, sometimes in quite snippy terms. Sir Michael Cullen was wont to do so as did Nicola Willis last year. This year the Finance Minister hasn’t publicly responded to the IMF concluding statement, possibly because her attention was on this week’s Infrastructure Investment Summit in Auckland.

Foreign Investment Fund changes announced

As part of the summit, the Minister of Revenue Simon Watts has announced that there will be changes to the current Foreign Investment Fund, or FIF regime. The Government has very heavily signalled that it would do something in this space, so this is no surprise.

The proposed changes to the FIF rules include the addition of a new method to calculate a person’s taxable FIF income, the revenue account method, in other words taxing capital gains. According to the Minister;

“This will allow new migrants to be taxed on the realisation basis for their FIF interests that are not easily disposable and acquired before they came to New Zealand. For migrants who risk being double taxed due to their continuing citizenship tax obligations, this method can apply to all their FIF interests.”

This last point is of particular interest to United States citizens who face this double taxation issue, and which is turning people away. Furthermore, these changes will apply to migrants who became New Zealand tax residents on or after 1st April 2024.

More detail needed and further changes ahead?

This is a very good move but there’s a bit more detail still required. Does the reference to new residents arriving on or after 1st April 2024 mean those new residents are able to make use of this provision in the current tax year? One of the other key issues is if you do opt to be taxed on the revenue account method, what tax rate would apply? From discussions with Inland Revenue policy officials, they seem to be intending that it should be at the person’s marginal rate. Which for those on the 39% bracket would not be terribly welcome. So that’s a key design point.

The other thing of note is that Mr Watts added the Government will also be looking at how the rules impact New Zealand residents and will have more to say later in 2025. That’s interesting, because for me, the rules are quite a compliance burden in terms of calculations and have huge impact for everyone who has a KiwiSaver with overseas investments.

How to pay for New Zealand Superannuation

As noted above the IMF are looking very closely at the question of the fiscal cost of superannuation and aged healthcare which they suggest mean reforms to the tax system are needed to address those growing costs.

Coincidentally, Assistant Professor Susan St John of Auckland Business School’s Economic Policy Centre Pensions and Intergenerational Equity Hub released a working paper on New Zealand Superannuation as a basic income. This is an interesting proposal, which I know Susan has been working on for some time with the assistance of Treasury modelling.

The idea is that New Zealand Superannuation is changed into a universal basic income and treated as a grant. This allows an effective claw back mechanism to operate through the tax system. The proposal is that this claw back would generate additional revenue to help meet the cost of pensions and aged care.

The paper begins by setting out the background to the issue, the increasing demographic strains that we’re seeing. It notes that Treasury has been raising this issue for some time now, such as in its 2021 Long Term Fiscal Statement, He Tirohanga Mokopuna and speeches last year by Dominic Stephens of Treasury on the fiscal projections and costs.

Demography and migration

One of the interesting points the paper makes is although we face some financial strains ahead, because of our demographics the cost of New Zealand Superannuation will not be as high as what some nations are currently dealing with.

Incidentally, as part of their concluding statement, the IMF made a number of presentations illustrating certain areas they’re examining in more depth. One was the question of demographic pressures of superannuation, and it made the point that migration is not going to be the magic bullet some policymakers seem to think.

What about means testing?

After setting out the background Susan St John discusses the option of using means testing as a means of addressing costs. The paper looks at what happens in Australia and our own experience when New Zealand Superannuation was means tested for a while – right up until Winston Peters and New Zealand First became part of the first MMP Parliament in 1996. One of the conditions of that coalition agreement was the abolition of the New Zealand Superannuation Surcharge.

Australia tests income and assets but it’s highly complex and achieves a fiscal objective of managing the cost. On the other hand, Australia has a much more well developed long running compulsory private saving scheme, which makes what they call the Age Pension (the equivalent of New Zealand Superannuation) more of a backstop. The paper also notes that the private pension savings in Australia are more generously state subsidised than KiwiSaver.

The Australian means testing approach is very comprehensive and frankly a nightmare. The paper notes our surcharge which operated between 1985 and 1998 was highly unpopular, but it did deliver useful savings. In short, surcharges or means testing helps mitigate superannuation costs. But they are unpopular and like the Australian approach complicated to run. Furthermore, they encourage attempts to mitigate their effect.

Making New Zealand Superannuation a universal basic income

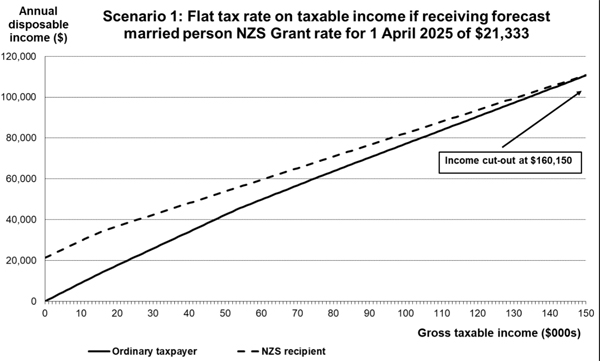

Instead, Susan proposes turning New Zealand Superannuation into a basic income, the New Zealand Superannuation Grant (the NZSG). She also suggests equalising the current different rates which currently apply depending on whether a person is in a relationship or living together, so it becomes a universal basic income for those who’ve reached the superannuation age.

As a basic income the NZSG would no longer be taxable. Instead, when a recipient earns additional income, it’s taxed under a progressive tax regime, so the tax system does the work of providing a claw back of the universal grant for high income people. The effect would be that above a certain point a person decides it’s simply not worth their while taking the NZSG.

For example with a flat tax of 40% on all other income, above $160,150 it would not be worthwhile taking the NZSG.

Another alternative would be a two-tiered rate of 17.5% for the first $15,000 of other income, and 43% on each dollar above. In this case the breakeven point becomes $151,885. A third scenario has a two-tiered rate, 20% for the first $20,000 earned and then 45% above that level. Under this scenario, the income cut out point drops to $135,000. Treasury has helped Susan with the modelling for this paper and its methodology is explained in the appendices to the paper.

15-20% savings possible?

Under Susan’s approach up to 5% of all eligible super annuitants will not apply for the NZSG because there’s no gain in it. She estimates savings could be between $2.8 billion and $3.8 billion or between 15% and 20%.

This is an interesting proposal which seems preferable to reintroducing the New Zealand Superannuation Surcharge or adopting the Australian means testing approach. I think it’s worth considering but the key thing is, as the IMF said, this is an issue we really need to start discussing now because these costs are starting to accelerate as baby boomers age.

It also seems fairer than raising the age of eligibility, which is unfair on Māori and Pasifika. There’s already a seven-year life expectancy gap between Māori and non-Māori so raising the age of eligibility for superannuation is politically difficult particularly as the proportion of the Māori population grows because of those changing demographics.

This is a worthwhile proposal which merits serious consideration as part of the ongoing debate.

This is an edited transcript of the podcast episode recorded on 14th March – it has been edited for clarity and length.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

Last week I joined Gareth Vaughan of interest.co.nz for a joint podcast with Andrew Coleman. He’s a New Zealand economist who has worked in academia and for the government, including Reserve Bank, Treasury and the Productivity Commission. In the last few months, he’s written a 13 part series for Interest looking at how we currently fund New Zealand Superannuation and what alternatives we should be considering.

Why we’re talking about more tax – the rising cost of New Zealand Superannuation

As I’ve mentioned previously, part of what’s driving the debate around whether New Zealand should have a capital gains tax is when you consider the government’s long term fiscal position, the conclusion you reach is that something radical will have to happen: either benefits will have to be reduced significantly, or taxes will have to be increased. If we’re increasing taxes, how are we going to go about that? That, by the way, is the subject of Inland Revenue’s long-term insights briefing consultation on which is going on at the moment.

(He Tirohanga Mokopuna 2021, Treasury)

Coleman has written extensively about the issue of funding New Zealand Superannuation and in the podcast he went through the issues behind why he wrote the series and what alternatives he proposes. It was very informative, and I highly recommend listening to the full podcast. Here are a few key takeaways.

New Zealand’s unique approach to funding superannuation

Firstly, the way New Zealand currently funds New Zealand Superannuation is very unique in that it is entirely funded out of current taxation. That means the current cost of New Zealand Superannuation, over $20 billion a year before tax, is being paid out of current taxation. This is unusual by world standards, because most other countries in the OECD adopt some form of Social Security tax to pay for their public superannuation. In Britain they have National Insurance Contributions, in America, they have Social Security. Throughout most of the EU you will see Social Security taxes in place. Apart from us, only Denmark in the OECD has no Social Security taxes. Other countries use social security taxes to pre-fund superannuation; people pay social security taxes which are then drawn down when they reach retirement age. We fund everything out of current taxation.

Allied to that, and a matter that makes our tax system unique, is that most other jurisdictions operate what’s called an exempt, exempt tax (EET) approach to private retirement savings. That is a person gets some form of tax deduction for making a contribution to a private superannuation savings scheme. The superannuation schemes are not taxed, but when you withdraw funds on retirement age you pay tax at that point. On the other hand, since 1989 we have adopted the complete opposite approach (TTE). We don’t give a deduction for contributions to superannuation schemes such as Kiwisaver, which are subject to the ordinary rules. However, withdrawals are tax exempt.

Point of order Prime Minister…

Just as an aside, I note that one of the Prime Minister’s comebacks to questions around capital gains tax was that if introduced it would apply to KiwiSaver. (Actually, when the last Tax Working Group proposed a CGT, they didn’t actually seem to think to go there). The PM’s comment glossed over the fact that KiwiSaver funds are subject to tax. If they’ve invested in bonds, these are subject to the foreign financial arrangement regime. If they’ve invested in overseas stocks, those are taxed under the Foreign Investment Fund which because the 5% fair dividend rate automatically applies, is a quasi-wealth tax.

Time for social security taxes?

That point of order aside, Coleman’s key point remains that our treatment of private superannuation schemes and funding of public superannuation is quite unique by world standards. So how are we going to meet the growing cost of superannuation? He suggested that maybe we should look seriously at Social Security taxes.

A Capital Gains Tax won’t be enough

Gareth and I raised the question of alternative taxes, such as a capital gains tax and Coleman made the point that the likely cost of New Zealand Superannuation scheme is going to rise towards somewhere around 8-9% of GDP. Hence the need to be thinking about how to fund that cost. Capital gains taxes don’t generally raise that much, typically, somewhere between one and two percent of GDP. That still leaves a funding gap of between 6-8 percent of GDP. It’s very doubtful a wealth tax, by the way, would make that gap up. In his view, the inexorable conclusion is that Social Security taxes are going to be needed to fill the gap.

How the 1989 changes helped distort the housing market

We also had a very interesting discussion about how the changes in 1989, which by removing the incentives for private savings, drove investment into residential property. He published his research on the matter in 2017, just at the same time that myself and the Honourable Deborah Russell, published Tax and Fairness. Separately we had reached the same conclusion, that the 1989 changes to the savings regime had driven people to start over-investing in housing.

Time for KiwiSaver 2.1

Coleman calls his answer to funding New Zealand Superannuation KiwiSaver 2.1 It would be a compulsory savings regime, but it would be for younger taxpayers, basically those under the age of 40 who were not old enough to vote back in 1997, when a referendum on a question of a compulsory superannuation savings scheme was overwhelmingly rejected.

Coleman’s argument is that younger taxpayers are currently funding what they want and need, such as health, education and transport. But they’re also having to fund the superannuation of older taxpayers, who voted for the current system which benefits them. KiwiSaver 2.1 as a compulsory superannuation savings scheme would be a transition to a fairer system which would include some form of social security tax. The idea would be to be gradually building up savings in a similar way to Australia, which, although it doesn’t have significant social security taxes, does have a compulsory savings scheme. There would be this transitional period, as the older workforce aged out, but all new younger workers would be part of the new KiwiSaver 2.1.

Taxing older, wealthier superannuitants

As part of the transition Coleman sees it requiring more taxes from older persons, which is where our discussion got to talking about capital gains taxes and wealth taxes. He’s not a particularly big fan of wealth taxes. But he sees a capital gains tax having an efficiency aspect to it, which means it should be part of the tax system.

Incidentally, one suggestion I have seen about taxing superannuitants involves applying a separate tax rate to persons receiving New Zealand Superannuation. This would be a way of clawing back payments from those who have other means without going down the route of the deeply unpopular means testing that happened in the early 1990s.

I thoroughly recommend listening to the podcast. Coleman’s analysis highlights the need to keep in context why we’re having this discussion about capital gains and wealth taxes and that’s to do with everyone realising that we have to address the rising cost of funding New Zealand Superannuation and related healthcare costs for the elderly. These issues are not going to go away because the demographics are inexorable, contrary to what politicians might hope as they repeatedly kick the can down the road.

Tax deduction notices

Moving on, Inland Revenue makes great use of tax deduction notices as a debt collection tool. These enable it to require a third party to make deductions from payments due to a taxpayer with an outstanding tax liability. The power is contained in section 157 of the Tax Administration Act 1994, or related provisions of the Child Support and Student Loans Acts. I once saw a notice where a supplier to someone with tax debt was told to withhold 100% of any payment that was going to be made to the person in default.

Inland Revenue typically issues thousands of deduction notices each year.

Deduction Notice issued to:

FYE 30 June 2020

FYE 30 June 2021

Total

Bank

5,222

7,388

12,610

Employer

21,333

43,535

64,868

Total

26,555

50,923

77,479

(Figures obtained under the Official Information Act)

I think it’s appropriate Inland Revenue has the power to issue deduction notices. My concern, however, is I’ve seen them issued for under $1,000 of tax debt which in my view is an inappropriate use for what is a fairly small sum of tax debt under $1,000. When a deduction notice is issued to an employer in such circumstances this essentially notifies the employer that the relevant employee is behind on their taxes.

Are these notices breaches of privacy?

In my view, a deduction notice in this situation represents a breach of privacy and employers really do not need to know about relatively small sums of tax debt owed by an employee. Instead, and I will propose this in my submission on the draft, I believe Inland Revenue should make greater use of tailored tax codes to collect the unpaid tax from an employee. The employer still has the responsibility for deducting the tax through PAYE but now all they know is the tax code has changed. They don’t know the reasons why. This preserves the privacy of the person who has been the subject of the tax deduction.

I think this is important. I discussed this issue with a previous Privacy Commissioner, and he was of the view that, yes, it seemed like a breach of privacy. But as he noted, he couldn’t really do much about it because Inland Revenue had the legislative power to issue the notices. Still just because Inland Revenue can doesn’t mean it should, and I think there are opportunities for improving matters. Looking at the UK, it’s common practice for HM Revenue & Customs to use adjusted PAYE codes to collect arrears of tax. Submissions are open until 15th November.

How many anonymous tip-offs does Inland Revenue typically receive each year?

Across the ditch the Australian Tax Office (ATO) revealed this week that in the past five years it has received over 250,000 tip offs about potential tax evasion. According to ATO assistant commissioner Tony Golding “We get on average over 3500 tip-offs a month from people who know or suspect tax evasion or shadow economy behaviour.” The ATO believes there is about A$16 billion in stolen, unpaid tax each year.

By comparison, according to Inland Revenue it receives about 7,000 anonymous tip-offs each year. These are important sources of information even if sometimes the tip-offs are malicious and stem from toxic relationship or business breakdowns or partnership breakdowns. Regardless of this issue Inland Revenue will follow up (the ATO says 90% of tip-offs lead to further investigation.

How many audits is Inland Revenue undertaking?

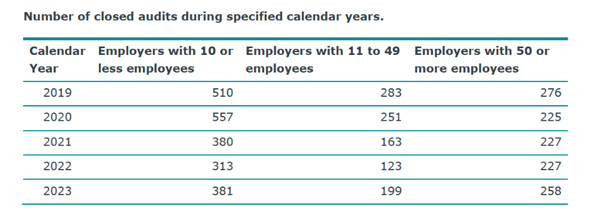

On the issue of audits and my thanks to regular listener and reader, Robyn Walker of Deloitte for reminding me, Inland Revenue publishes Official Information Act responses and there are often some very interesting releases. One of the latest OIAs relates to the number of audit cases carried out on businesses between 2019 and 2023.

It’s interesting to see the impact of Covid and the quite marked drop-off in audits for those employing fewer than 50 employees.

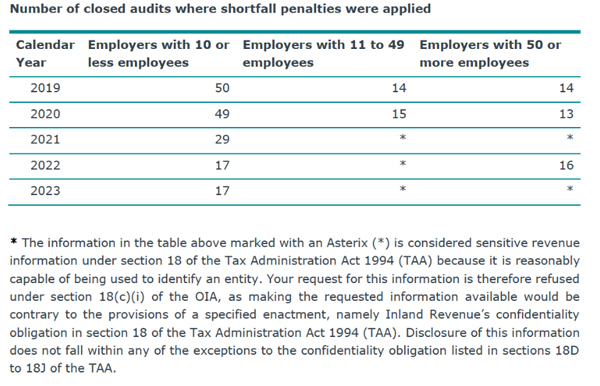

There’s also data on the number of shortfall penalties applied as a result of audit. Now shortfall penalties enable Inland Revenue to impose penalties of up to 150% of the tax involved where tax evasion has happened although the more common range of penalties is 20%. Again, the somewhat sparse data makes for interesting reading.

That’s all for this week. Next week, we’ll be taking a deep dive into Inland Revenue with a look at its annual report.

Until then, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

There’s inevitably been a certain Groundhog Day effect to the current Lockdown now we’re into our fifth week. It dominates the discourse and that hasn’t really changed in the tax world. The Government has now announced that there will be a third round of the Wage Subsidy and applications for that opened at 9:00 a.m. Friday and will remain open until 11. 59 p.m. on Thursday, 30th September.

As of September 12th, there have been 427,388 applications approved for the first two rounds of the wage subsidies, which has supported over 982,000 employees and 274,000 businesses. The total amount paid out to that date is just under $1.8 billion.

To quickly recap the tax implications of the subsidy for an employer, the receipt by an eligible business is excluded income to the extent that the subsidy is passed on to the employee. The employer is not entitled to an income tax deduction for wages paid out of the wage subsidy and the amount of wages paid in excess of the wage subsidy, that is amounts funded by the employer, are deductible as normal. No GST applies to the payment.

Now, Inland Revenue just reminded people that any amount of the subsidy that is not passed on to an employee is required to be repaid to the Ministry of Social Development (MSD)because that’s part of the criteria and declarations made at the time of application. If the wage subsidy isn’t returned to MSD, then Inland Revenue may consider the amount not returned as taxable income, which needs to be included in the income tax return for the year in which it was received.

Now, the interesting development this week is that the Government has now said that a second payment under the Resurgence Support Payments scheme will be available and, applications for that opened Friday. Now, in order to qualify, organisations must experience at least a 30% decline over seven days for the period commencing 8th September as a result of being at Level Two or higher.

Remember, the Wage Subsidy is only available at Levels Three and Four, but the Resurgence Support Payment (RSP)is available at Levels Two, Three and Four.

Now, the income tax treatment of this is that the RSP is not subject to income tax and accordingly, income expenditure funded by payments under the RSP scheme are not deductible. GST registered businesses will return GST on payments received under the RSP and will be able to claim input tax deductions for expenditure funded by payments under the RSP such as rent, for example. The intention is any RSP received is used to cover business expenses such as wages and fixed costs.

As of 12th September, about $500 million dollars has been paid. And the Government has indicated that there could be another two payments after the for which applications opened today. These will be three weeks apart, so long as the conditions that continue to trigger the Resurgence Support Payment scheme continue to apply, i.e. the country is in an Alert Level Two or higher.

Now, there’s an ongoing debate, quite rightly so, about the level of support, whether it’s targeted or appropriated enough, but it’s useful to see Inland Revenue is keeping people up to date as to what their obligations are. Whether the level of support is the right level or appropriately directed, well, that’s another matter.

And just quickly, a reminder that there are some other schemes available. There is the Leave Support and the Short-Term Absence Payments Schemes. Businesses may still be eligible for the Small Business Cashflow (Loan) Scheme. And there’s also Business Debt Hibernation. We talked about these when we first went into Lockdown. All those four schemes, by the way, are available at Alert Level One or higher.

A very large taxpayer

Moving on, the New Zealand Superannuation Fund, which was an initiative by the late Sir Michael Cullen, has just posted its strongest ever annual return of 29.63% for the June 2021 financial year. This means that the fund has now grown to $59.8 billion dollars, an increase of $15 billion over the 12 months.

And during that period, the Government made contributions totalling $2.1 billion to the fund. Now the super fund is a sovereign wealth fund, but almost uniquely, as far as I can tell, amongst sovereign wealth funds, it’s taxed. For the year just ended, it paid $2.3 billion dollars on its $15 billion. And that’s because the rules around the Foreign Investment Fund and the Financial Arrangements regimes apply to the super fund. It therefore will pay a fair amount of tax, obviously, when its investment return is nearly 30%.

Making it fairer, go further

Now, of course, the Super Fund was established to help fund the future cost of New Zealand Superannuation. You may recall last week we discussed the Treasury’s draft long term fiscal outlook and in relation to the growing cost of superannuation, Treasury put forward a couple of options to consider, which were increasing the age of superannuation entitlement from 65 to 67 or actually cutting back the amount of people’s entitlements.

New Zealand Superannuation is universal, which is one of its great strengths. Radio New Zealand has received Inland Revenue figures which show that in the March 2010 income year, there were 2,209 people who were on incomes of more than $200,000 a year who were receiving super.

By the year ended 31 March 2020 that number had more than tripled to 7,860. And as Baby Boomers and the population ages, more people who on the face of it don’t need Super will be receiving it because of its universality.

The Retirement Commissioner, Jane Wrightson, was asked about this and she said it’s not a problem, because one of the great things about New Zealand Superannuation is that it is universally applied. But she did say it is a reasonable policy question, the normal answer to this has been means testing which was applied briefly in the mid-90s and applies in Australia. However, this was roundly rejected by New Zealanders in the past.

So, two questions emerge. One, how are we going to fund superannuation going forward? And secondly, is it right that it is universal and people who on the face of it have sufficient to fund their retirement are still receiving it? Mind you, you could say 7,800 people in the context of the hundreds of thousands receiving New Zealand Superannuation isn’t actually that much, but that number will grow.

Now, a suggestion to address this particular issue of potential over generosity for higher income earners has been put forward by my colleague, Associate Professor Susan St John of the University of Auckland Retirement Policy and Research Centre. She has released a briefing paper updating an idea she’d first proposed back in 2019. It basically treats the pension as a basic income and then taxes pensioners’ other income at a higher rate.

And the idea is that there will be a threshold at which it becomes uneconomic to take super, thus saving funds.

The proposals is, instead of having super inside the tax system, take it outside, treat it as a basic income, and then tax people receiving other income at a higher rate. And then that would mean, as I said, once their other earnings reached a certain point they would be better off to not claim superannuation.

The issue, as has been pointed out all around by various people, is that the number of pensioners between now and 2060, is expected to double. And Treasury’s forecast is that the cost of superannuation, which is already our most generous welfare payments, is going to grow at one and a half times faster than the economy over that period. Therefore, its cost, relative to the economy, is going to increase.

Susan St John’s proposal is that by taxing people who are earning higher incomes means that the payment is then focused on those who really need it. That is, those on lower incomes and that amount is likely to grow as well. And her modelling suggests the break-even point with a flat tax rate of 39% is when the other income exceeds $139,000 a year which is still pretty generous, I guess.

You can tinker with the tax rate, but it’s an interesting idea. What it builds on is two things.

Firstly, New Zealand Superannuation is a type of universal basic income, which there’s always been a lot of discussion around. Secondly, it then uses the tax system to introduce a bit of equity and disincentivise excessive take up, but not too much, to be honest, because you can earn up to $130,000 in other income. This relative generosity shouldn’t really disincentivise work which is obviously one of the big problems about means testing, the disincentives it creates.

So it’s an interesting. Treasury I think seems quite interested in it, or appears to have had some discussions on the topic and we may hear more about it.

Well, that’s it for this week. Next week, we may be discussing the interest limitation rules in more detail. We’ve been waiting for those for some time. And given that they come into effect from 1st October, it’s going to be quite a crash course to get people up to speed by that time.

But anyway, that’s it for today. I’m Terry Baucher. And you can find this podcast on my website, www.baucher.tax or wherever you get your podcasts. Thank you for listening and please give me your feedback and tell your friends and clients. In the meantime, kia pai te rā, have a great day!