The Organisation for Economic Co-operation and Development (OECD) recently released its 2026 Economic Survey of New Zealand. The OECD, like the International Monetary Fund (IMF), carry out regular reviews and this is a fairly detailed report running to over 140 pages, which you would expect, given the OECD has a significant economic database to work with.

The OECD was cautiously optimistic about the state of the NZ economy but noted that GDP growth was slower than in many OECD countries. Ongoing fiscal consolidation was needed, but the Middle East conflict may require more “targeted support”. It recommended ensuring “strong accountability through transparency of the [RBNZ’s] Monetary Policy Committee decision making”. Other recommendations included harnessing digital tools to improve health system performance and for a more affordable, secure and sustainable electricity system (which, in the long term, does not include LNG in the OECD’s view).

Not all recommendations made by the OECD or the IMF are greeted with enthusiasm by the government of the day. The Prime Minister reacted very strongly to warnings about the Government’s LNG proposals, calling the OECD’s report “a load of rubbish”.

Unlocking capital markets to drive growth

It’s Chapter 4 of the survey, which I found most interesting and relevant, as it included a discussion of our tax settings relating to the taxation of savings. This section was written by Dr David Haugh, the head of the New Zealand (and Finland) desk, together with his colleagues Kyongjun Kwak and Carl Magnus Magnusson. Dr Haugh is actually a New Zealander who started his career with the Treasury before joining the OECD. That means he has a good background knowledge of New Zealand and our challenges.

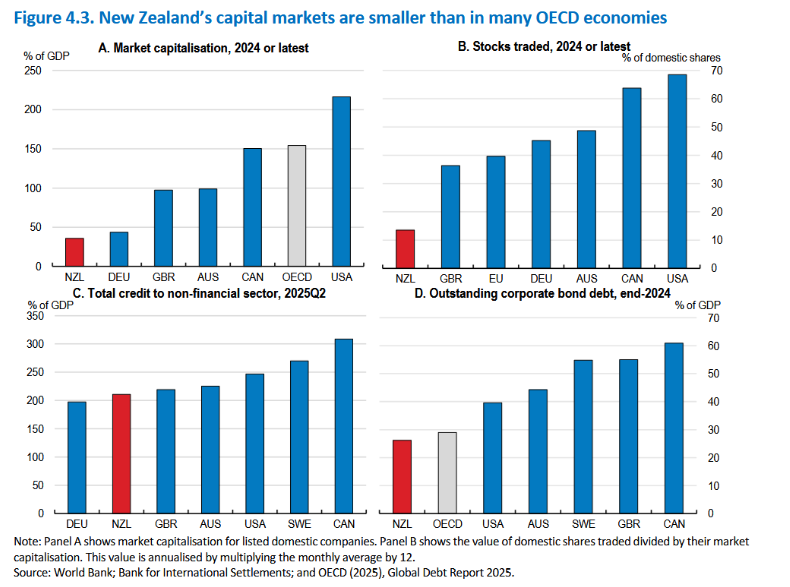

The background summary is that our capital markets remain “shallow by international standards, constraining long-term investment, innovation and productivity growth”. The survey notes that the NZX has seen no major domestic initial public offerings since 2021. That’s apparently part of a worldwide trend, as many firms that might otherwise have gone to market have instead opted for a private or trade sale. A classic example would be Fonterra’s recent sale of its global consumer and associated businesses, Mainland Group, to Lactalis.

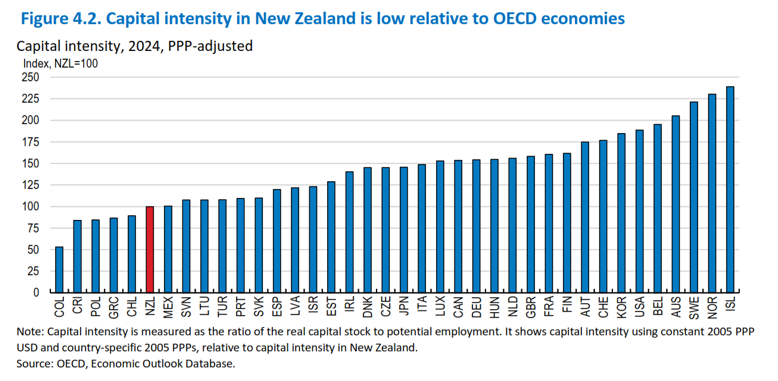

There are some pretty damning graphs illustrating the scale of the problem. Quite apart from smaller-than-average capital markets, ‘capital intensity’ or the ratio of real capital stock to potential employment is low relative to other OECD economies. In 2024, New Zealand’s capital intensity was just about 100%, whereas if you look at Israel, Norway and Australia, they’re all over 200%.

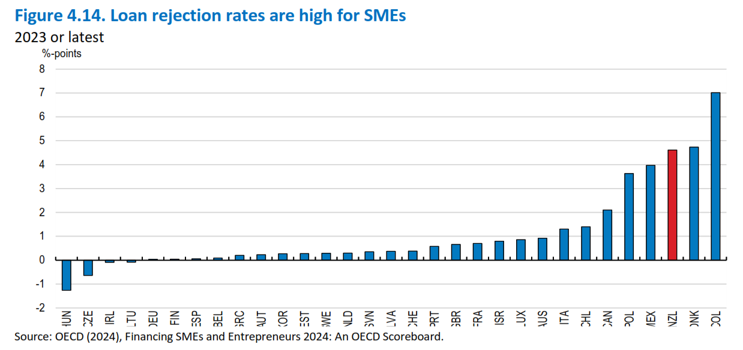

There’s also a sideswipe for the Australian banks, with the OECD saying “costly bank lending dominates, with OECD analysis of lending margins showing they’re about twice the international norm”. With the main banks preferring mortgage lending, SME loan rejection rates are high.

There’s a fairly blunt assessment of why our capital markets are underdeveloped – the decision in 1975 to cancel the Third Labour Government’s compulsory superannuation scheme:

“The decision to abolish the private pension saving schemes in 1975 and replaced it with a publicly funded universal pension at age 60, significantly hampered the development of New Zealand’s capital markets by reducing households’ incentives to accumulate private pensions, depriving capital markets of a key source of long-term domestic funding.” [page 98]

Developing public equity markets – the Swedish example

There’s a very interesting discussion about how Sweden “has developed one of the most dynamic and inclusive equity markets relative to its economic size in Europe and across the OECD.” A key element of this is the Investment Savings Account, or an ISK account. There are over 4 million ISK accounts, with half the adult population having an ISK. These have helped channel household investments into listed equities. Britain’s Individual Savings Account is a slightly similar product. The recommendation is that we consider introducing a non-retirement New Zealand Equity Savings Account.

Raising household savings through changes to KiwiSaver

The report notes our retirement savings are fairly inadequate by world standards. In September 2025, the value of funds under management in KiwiSaver was $141 billion or 32% of GDP. By comparison, in Australia, the assets under management exceeded A$3.6 trillion or 133% of GDP. Furthermore, the average Australian retirement pension plan value is NZ$130,000 or nearly five times greater than the average NZ$28,000 in New Zealand.

The survey notes that withdrawals are allowed to buy a first farm or first house, which, together with increasing withdrawals for hardship (these have doubled from $100 million a month in 2023 to $200 million a month in 2025), slows the accumulation of funds. The OECD questions the purpose of withdrawals for first farms or houses. It suggests that if the policy objective is to support low-income people into house ownership, then a separate instrument would be more effective. The OECD also recommends not creating any further exemptions.

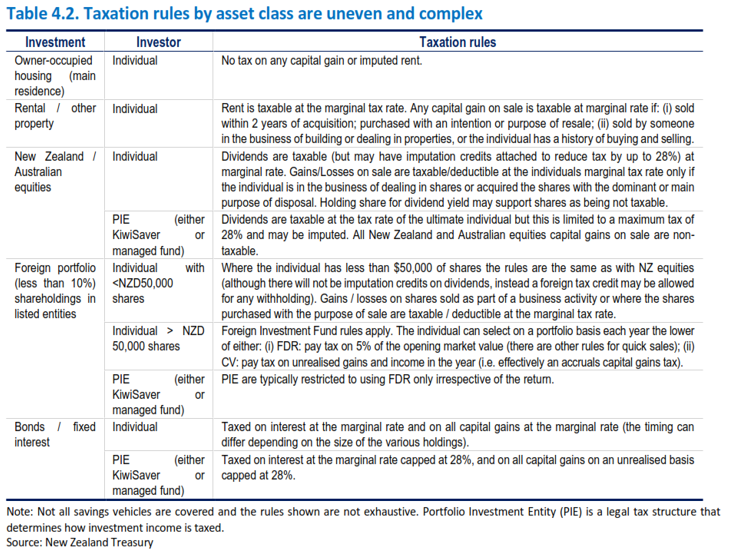

‘New Zealand’s taxation of capital income and savings is complex and uneven’

The survey then discusses the taxation of capital income and savings, which it describes as “complex and uneven, with housing taxed lightly relative to financial assets and especially pensions”. Our corporate income tax at 28% is noted to be amongst the highest in the OECD. Taken together, these settings:

“…distort household and firm investment decisions and suppress the accumulation of private pensions and other long-term financial savings, which is a critical issue not only for capital market developments but also for retirement income adequacy.”

In short, the way our tax system has distorted savings has had long-run consequences. This is something I’ve been saying for a long time and it’s also the view of the International Monetary Fund.

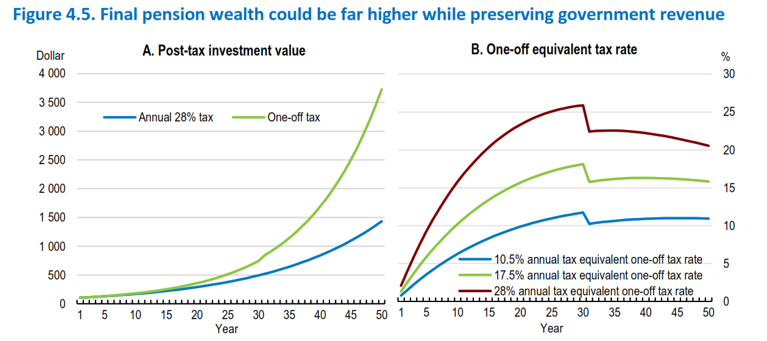

Increasing the accumulation of pension savings by reforming the taxation of savings

The OECD’s view is that the taxation of savings needs reform to allow greater accumulation of pension savings. The survey notes only seven of 38 OECD countries tax the investment income pension and only three, New Zealand, Australia and Türkiye, have a tax-tax exempt system (TTE). The most common system operated in about 17 out of 38 countries is an exempt tax, which is what you see in the UK and America, which allows the accumulation of more funds within the fund that eventually gets taxed as a pension.

The critical disadvantage of our TTE system is that it penalises the accumulation of long-term financial retirement assets, sharply reducing compounding returns relative to the exempt-exempt-tax systems used by many other countries, such as the UK and the United States.

The OECD bluntly concludes:

“The TTE system for financial savings combined with light taxation of housing in New Zealand… makes the overall system one of the most housing-biased tax systems in the OECD. This bias has been capitalised into higher house prices, larger new dwellings, lower ownership rates amongst younger cohorts, and a worsening of New Zealand’s net international asset position, reflecting reduced domestic financial capital available for firms.”

The OECD notes that because pension savings compound over 40 years or so, lowering the tax burden on returns “substantially increases long-run private wealth accumulation”. So, does that mean switching to the common exempt-exempt-tax approach? Not quite. An argument against such tax incentives, and one I share, is that the benefit of such savings is mostly captured by the wealthy who would be saving anyway, and tax incentives don’t lead to significantly increased savings. Another issue with tax incentives is, as Finance Minister Nicola Willis pointed out, they are extremely expensive.

Auto-enrolment and KiwiSaver

According to the OECD, many of these concerns are indirectly addressed by an auto-enrolment system, i.e. everyone would be in KiwiSaver and therefore automatically contributing and saving. UK evidence is that within such auto-enrolment schemes, savings do not fall or rise in response to tax incentives and other private savings are not reduced to offset the diversion into tax-preferred schemes. Furthermore, the strongest benefit of such a change would be for low and middle-income households, who have limited discretionary savings anyway.

Removing or reducing tax on KiwiSaver returns would operate primarily by allowing greater compounding and unchanged contribution patterns, generating substantial increases in total retirement wealth. In other words, directing the incentives there towards the lower-income earner is an approach I fully support.

The survey includes an example illustrating that if this approach is adopted and coupled with a withdrawal tax, the post-tax pension value is twice as large by age 65 compared with the current annual taxation approach.

Overall, there’s plenty of food for thought in this survey. We’ve had a long period of stable policy settings in relation to savings, but we have problems with productivity and access to capital for start-up companies. New Zealand actually has a fairly vibrant tech sector, but as this paper notes, a lot of small tech companies go overseas to get funding because they can’t get it here. I’ve advised on a few such situations, and I’m always surprised the investment capital isn’t readily available here. This OECD survey should therefore provoke plenty of debate amongst politicians and analysts alike, but I fear it will get drowned out by the noise around the coming general election.

The latest National Climate Change Risk Assessment is not a pretty read

More or less simultaneously with the OECD report release, the Climate Change Commission released its National Climate Change Risk Assessment (NCCRA) for 2026. This is the first one that’s been produced since 2020 and is not pretty reading. It identifies the 10 significant risk areas “where focused action would make the biggest difference.” In short, this means increased infrastructure spending, particularly in relation to water infrastructure. The NCCRA warns that without immediate action, water infrastructure could be the “first climate risk to reach an extreme severity level within the next 25 years”.

The regularity of natural disasters has been increasing. According to the NCCRA stat, about 97% of the estimated $33 billion of government expenditure on natural hazards since 2010 was spent on responding to and recovering from disasters, with only 3%, i.e. a billion dollars, spent on risk reduction.

What happens when the insurers withdraw cover?

Whether or not you accept what’s driving climate change, it is happening. The NCCRA notes that 556,000 buildings with a combined replacement value of $235 billion are currently exposed to inland flooding. Insurance premiums are rapidly rising, leading the OECD’s economic survey to note “climate-change-induced rises in insurance premiums make inflation control more difficult”.

Quite apart from rising insurance premiums, my concern is that at some point, the insurers are going to dictate what happens with such properties. If the insurers start withdrawing cover, and that’s now coming into general discussion, people will look to the government to help because if they can’t get insurance on their properties, the banks won’t lend against that. This also ties into what the OECD was saying about the high dependency on property ownership for savings.

The NCCRA notes that if we keep allowing the current pattern to continue, of simply accepting damage will happen and then repairing it afterwards, this will drain funds away from core services such as health and education. Over the past 15 years, we’ve spent on average $2 billion a year, or roughly 0.5% of GDP, on climate mitigation and recovery, and things are only getting worse.

All this comes back to a long-standing argument I’ve been making here on the podcast and elsewhere: that climate change is going to drive changes in our tax system by way of having to increase revenue to fund these changes. There’s been plenty of debate about the long-term fiscal sustainability of New Zealand superannuation, but the impact of climate change is an immediate and growing problem.

This is a long-term issue where you really do hope that all the major parties in Parliament accept the need to address this and move accordingly. But as we’ve seen with the superannuation debate, that’s not likely to happen.

The Australian Budget

Finally, across the ditch, the Australian Budget was handed down on Tuesday, 12th May. There had been a lot of speculation beforehand that there would be changes to ‘negative gearing’ and the taxation of capital gains. This speculation was correct, but the extent of the changes has taken people by surprise.

Negative gearing is what the Australians call the ability to offset losses from residential property investment against other income. With immediate effect, any new investors will now only be able to offset losses from purchases of ‘new builds’. (Rather like our previous interest limitation rules.) Taxpayers with existing rental properties will still be able to offset their losses against other income. In other words, they will not be subject to what we term ‘loss ring fencing’.

The capital gains tax surprise

Presently, Australia grants a 50% discount on the amount of a capital gain for individuals, trusts and partnerships if the asset in question has been owned for more than 12 months.

This 50% discount will no longer apply for any gains realised on or after 1st July 2027. Instead, there will be a cost-based indexation, i.e. based on retail price, which was the rule between 1985 (when Australia introduced capital gains tax) and 1999. There will also be a minimum 30% tax rate on capital gains.

This is a significant change, and it’s expected to result in a rise in payable capital gains tax. Pre-Budget speculation focused on gains from residential property investment, but this change will apply to all asset classes.

A potential silver lining?

Now, the interesting thing if you’re a New Zealand resident and you’ve got a property investment in Australia, this change may be beneficial. At present, New Zealand tax residents are subject to Australian capital gains tax on disposals of Australian-situated property, but because they are not Australian tax residents, they do not get the 50% discount. (Australia is frequently quite sneaky in how it taxes non-residents.)

This change may mean that New Zealand investors subject to Australian capital gains tax on Australian properties may actually be better off. We’ll need to see the details on that, but it’s perhaps a silver lining for everyone.

On that note, that’s it for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and tell you and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

[This is the transcript of the episode recorded on Friday 15th May – it has been edited for brevity and clarity]

One of the unseen revolutions in international tax over the last decade has been the adoption of the automatic exchange of financial account information. Also known as the Common Reporting Standards https://www.ird.govt.nz/crs this was developed by the Organisation of Economic Cooperation and Development, the OECD, in conjunction with G20 countries. It requires the automatic exchange of information on financial accounts – which is bank accounts, other investments held by taxpayers outside their jurisdiction. Financial institutions are required to provide information on such accounts to their respective tax authority which then sends that information to the jurisdiction in which that taxpayer is resident.

This project began in 2017. For the latest year, the tax authorities from 111 jurisdictions have automatically been exchanging information on financial accounts. And as I said, it’s a very broad range of investments, not just bank accounts. It’s all forms of investments. By and large, the public is pretty unaware of what’s happening here even though the numbers are significant.

€130 billion in tax interest and penalties so far

According to the latest peer reviewfrom the OECD, information from over 134 million financial accounts was exchanged automatically in 2023, and that covered total assets of almost €12 trillion. As a result, over €130 billion in tax interest and penalties have been raised by the jurisdictions through various voluntary disclosure programmes and other offshore compliance programmes.

Now the interesting thing here is that as a consequence of the introduction of the CRS, financial investments held in international finance centres or tax havens have decreased by 20% since the introduction of CRS in 2017. That’s a significant change. It means investments are moving into jurisdictions where they will be taxed. Over the long term that’s going to be quite significant for increased tax revenue around the world.

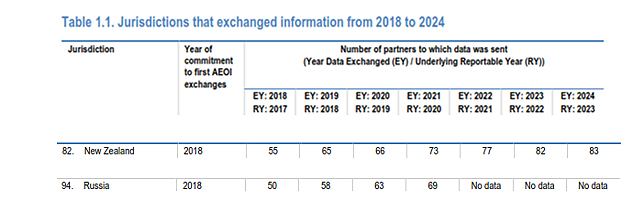

The full OECD report, which also discusses methodologies, runs to 248 pages, but the bulk of what people will be interested in is covered in the first chapter. Table 1.1. gives a summary of how many jurisdictions have been exchanging information, starting in 2018. According to the latest report the time of this report, 118 jurisdictions including New Zealand have started exchanging information.

Now the interesting thing to notice is the steady growth in the number of partners to which data has been sent. For example, the tax haven Anguilla in 2017 sent data to four countries but by 2023, it’s up to 67. The Cayman Islands, another key tax have sent data to 83 jurisdictions.

CRS and New Zealand

New Zealand began swapping data in 2018 when it sent information to 55 partners. For the latest year that’s grown to 83. Based on the early data exchanges Inland Revenue began a review programme in late 2019 which was then interrupted by COVID. However, it has now resumed its review programme, and I have one case at the moment which involves the taxpayer making the relevant disclosures after Inland Revenue enquiries based on data received through CRS. They won’t be the only one.

I was rather amused to see that Russia began exchanging data in 2018 when it sent data to 50 jurisdictions. But for the last three years no data is available. Wonder what’s happened there.

By the way the United States is not part of the CRS. That’s because it has something called the Foreign Account Tax Compliance Act, which basically was the model on which the current global CRS was built, and so it reports data separately.

How much data is Inland Revenue sharing?

I’ve tried unsuccessfully to obtain more detailed information on the data exchanges using the Official Information Act (the data exchanges are outside the OIA because of international treaty obligations which is fair enough). Notwithstanding this the impression I have is there are some huge numbers involved.

You have been warned…

What people should be aware of is that there’s a massive amount of data being circulated by tax authorities around the world right now. Many people may be oblivious to what’s going on. The likelihood is if you have an overseas financial account and you haven’t declared it for whatever reason, then it is quite likely that you will soon be asked a few questions about that by Inland Revenue.

Speaking about Inland Revenue, earlier this year they asked for consultation on their proposed long-term insight briefing (LITB). To quickly recap, LITBs are

“…future focused think pieces that government departments produce every three years. They provide information on long term trends, risks and opportunities that could affect New Zealand in the future, and policy options for responding to these matters. Their purpose is to help us collectively think about and plan for the future. They are developed independently of ministers and are not current policy.”

Back in August Inland Revenue proposed that its next long term insight briefing will explore what would be a suitable structure of the tax system for the future, and invited submissions by early October.

Inland Revenue has now published a summary of those submissions. In total, there were 35 submissions from 12 groups and 23 individuals. Most submissions were generally supportive of the topic. The rest, either suggested something completely different or were either ambivalent about it or did not actually specify whether they supported the project or not.

Seven themes in feedback

Inland Revenue’s picked out seven themes that came through from those submissions. Firstly, the fiscal pressures arising from superannuation and healthcare are a key trend and that’s one of the reasons behind Inland Revenue wanting to do a long term insight briefing on this topic. Most agreed with that, but several also added the question of increasing fiscal pressures arising from climate change.

My belief is its climate change that’s going to be the trigger point around changes to the tax system because that’s happening right now. And as damage from the floods grows and costs and insurers look increasingly wary about insurance, people will be looking to the Government for support.

The second theme was keeping flexibility in the tax system. In its submission EY commented

“We agree improvements to system flexibility should be the focus for this LTIB. In particular, working through options for system integrity in the context of tax rate increases is in our view, important.”

The devil is in the detail

A third theme was the analysis needs to consider policy design details and looking at first principles. Chartered Accountants of Australia and New Zealand made the comment that “Sometimes it is the detail that can make things unworkable. The framework should consider the merits of expanded tax bases with different design parameters”.

Another theme – and this is something I think I would endorse – the analysis needs to consider the tax and transfer system interaction. There were a few submissions pushing very strongly on that point.

A fifth theme proposed considering corrective taxes. The Young International Fiscal Association Network suggested that environmental taxes would fit well with Inland Revenue’s proposed topic because of the long term environmental trends.

The impact of technology

Another theme was the question of technological change and how that will affect the sustainability of tax bases. Earlier this year an IMF report on the impact of artificial intelligence suggested changes to tax systems could be needed.

Some submitters emphasised that it was important to consider how the tax system impacts a wider range of social outcomes. These included Doctor Andrew Coleman who was broadly in support of what was in the proposed LTIB. He suggested that they need to look at a wider range of retirement savings reforms, which would be no surprise to anyone who listened to the podcast with Gareth Vaughan and myself earlier this year. Several other submissions suggested how tax system could support productivity.

Finally, there were suggestions about considering progressive consumption taxes, which hasn’t really been looked at in any detail in New Zealand.

How Inland Revenue will proceed

Following this feedback Inland Revenue has said the LTIB will discuss the arguments for lower taxes on savings and the question of the tax treatment of retirement savings as part of a discussion about social security taxes. This is an interesting development because as the consultation noted generally, most jurisdictions have social security taxes which represent somewhere around 25% of total tax revenue. Whereas we don’t have them at all. This was a point Dr Coleman made in the podcast so it’s good to see Inland Revenue will be looking at that.

No to considering financial transaction taxes

As part of managing the whole scope of the LTIB Inland Revenue believes it “could reduce the discussion of some tax bases are less likely to be subject of significant public discussion such as financial transaction taxes.” This makes sense. Financial transaction taxes or Tobin Taxes are something that pop up in discussions about tax reform. I’m ambivalent about whether in fact they will achieve what people make out for them. I think they would add complexity and they would drive all sorts of different behaviour.

They’re not going to do a full review of the interaction of the tax and transfer system. And to be fair to Inland Revenue, I think that would be an entire long-term insight briefing of itself. But their chapter on consumption taxes discussed using transfers to offset GST rate increase somewhat similar to what Andrew Paynter proposed last week. (Just to repeat Andrew’s proposal is his alone and does not reflect any Inland Revenue policy). According to Inland Revenue the tax regimes chapters “will largely focus on how to make our main tax bases more flexible to rate changes, including considering options to support system coherence and integrity.”

Providing an analytical base

In summary Inland Revenue’s intention

“…is to provide an analytical base to provide further consideration of these issues in the future. For example, our focus on tax bases is on understanding the relative costs of taxing different underlying factors and what the overlaps and differences are in those tax bases. Our focus on tax regimes is on exploring how to make our tax based main tax bases more flexible to rate changes without undermining equity or efficiency goals.”

All of this seems perfectly reasonable to me.

From here there will be a future opportunity to provide feedback when Inland Revenue releases a draft of its briefing for public consultation in early 2025. It will then be finalised and given to Parliament in mid-to-late 2025.

Sir Roger Douglas’s radical proposals

Inland Revenue have also published all the submissions, from those who gave permission to do so, adding up to 175 pages of submissions, from individuals and organisations alike. It’s interesting to dip in and see what is being suggested on the topics. Sir Roger Douglas was one of the submitters and as you might expect, the old warrior is still looking for something radical.

Part of his proposal is a tax-free threshold of $62,000. But the trade-off is most of that gets put into retirement and health accounts. With the proposed retirement account, he’s probably reflecting the thinking of Andrew Coleman about the need for the current generation to start saving in earnest because of the various pressures coming towards us. Can’t say I agree fully with Sir Roger’s proposal but full marks for boldness.

Feedback on Andrew Paynter’s proposal

And finally, this week, to pick up a little bit from last week’s podcast with Andrew Paynter and his proposal to increase GST by 2.5% points to 17.5%, but then with a rebate for low- and middle-income earners. The transcript has been very well read and generated a phenomenal number of comments, over 150 at last count, and I thank all the readers and commenters for that.

What about the self-employed?

One commenter asked a question which we didn’t cover off during the podcast; how would Andrew’s proposal apply to the self-employed? The answer is it would use something similar to the provisional tax system. A person’s income would be uplifted from last year and if you’re in the range then you qualify for the proposed payments.

Last week Tax Management New Zealand and the Young International Fiscal Association network ran a joint presentation for the two winners, Andrew and Matthew to come and present their proposals. If you recall, Matthew proposed expanding the withholding tax regime to contractors. Andrew and Matthew both made excellent presentations to a very engaged crowd, and I can see why the judges had a difficult time splitting the pair. So well done again.

Left-to-right Matthew Seddon, Terry Baucher and Andrew Paynter

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This week the ninth edition of the OECD’s Tax Policy Reforms was released. This is an annual publication that provides comparative information on tax reforms across countries and tracks policy developments over time. This edition covers tax reforms in 2023 for the 90 member jurisdictions of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting.

Reversing the trend

It’s a fascinating document which tracks trends of what’s happening around the tax world at both a macro and micro level. The report has three parts: a macroeconomic background, then a tax revenue context, and then part three is the guts of the report with details of tax policy reforms around the world.

There is an enormous amount in here to consider and the executive summary lays out the ‘balancing act’ issues pretty clearly.

“Policymakers are tasked with raising additional domestic resources while simultaneously extending or enhancing tax relief to alleviate the cost-of-living crisis… On the one hand, governments further protected and broadened their domestic tax bases, increased rates, or phased out existing tax relief. On the other hand, reforms also kept or expanded personal income tax relief to households, temporary VAT [GST] reductions, or cuts to environmentally related excise taxes.”

A key observation for 2023 was a trend towards reversing the responses to the COVID-19 pandemic. Instead, as the report notes “2023 has seen a relative decrease in rate cuts and base narrowing measures in in favour of rate increases and base broadening initiatives across most tax types.”

“A notable shift”

This includes “A notable shift occurred in the taxation of business, where the trend in corporate income tax rate cuts seems to have halted with far more jurisdictions implementing rate increases than decreases for the first time since the first edition of the Tax Policy Reforms report in 2015.”

This is a pretty significant change. I think actually when you consider last week’s speech by Dominick Stephens of Treasury, it was setting out the context for why having got over the crisis of responding to the pandemic, countries are realising they’ve got to deal with the demographic issues of ageing populations and funding superannuation.

Climate considerations

Beyond these concerns, there is the immediate impact of climate change and its growing effects. The executive summary picks up on this issue:

“Climate considerations are also increasingly influencing the design and use of tax incentives, with more jurisdictions implementing generous base narrowing measures to promote clean investments and facilitate the transition towards less carbon intensive capital.”

And on that point, I hope all the listeners and readers down in Dunedin and Otago are safe and well at the moment.

Paying for superannuation

The other thing picked up is that in referencing that point I made a few minutes ago about population ageing. There has been a growing trend amongst countries to increase Social Security contribution taxes. Alongside Australia, and to a lesser extent Denmark, we are unique in that we don’t have social security contributions. However, elsewhere in the OECD social security contributions raise increasingly significant amounts of revenue.

The report begins with a macroeconomic background. It notes that for the OECD as a whole in 2023 government debt rose by about nine percentage points, reaching 113% of GDP. For context, New Zealand’s debt-to-GDP ratio is just over 50%.

As the macroeconomic summary notes after generally decreasing in 2022 Government deficits increased again in 2023 following the energy crisis triggered by the war in Ukraine. Consequently,

“As debts and interest rates increased, interest payments have started to rise as a share of GDP. Even so, in 2023 they mostly remained below the average over 2010 to 2019, except notably for Australia, Hungary, New Zealand, the United Kingdom, and the United States.”

In short, we definitely have issues to deal with in terms of debt management and rising costs.

Responding to growing deficits

The report then notes that responses to growing deficits have been to start at increasing taxes. In general tax revenue terms,

“From 2020 to 2021, the tax-to-GDP ratio rose in 85 economies with available data for 2021, fell in 38, and stayed the same in one. In more than half of these economies, the change in the tax-to-GDP ratio was under one percentage point, whereas 22 economies saw shifts greater than two percentage points in their tax-to-GDP ratio.”

Denmark saw the most significant drop of 5.5 percentage points, with New Zealand’s tax-to-GDP ratio falling by three-quarters of a percentage point, well above the OECD average fall of .147 percentage points. (Norway’s dramatic corporate income tax take increase of 8.775% is the result of “extraordinary profits in the energy sector”.)

Composition of tax base

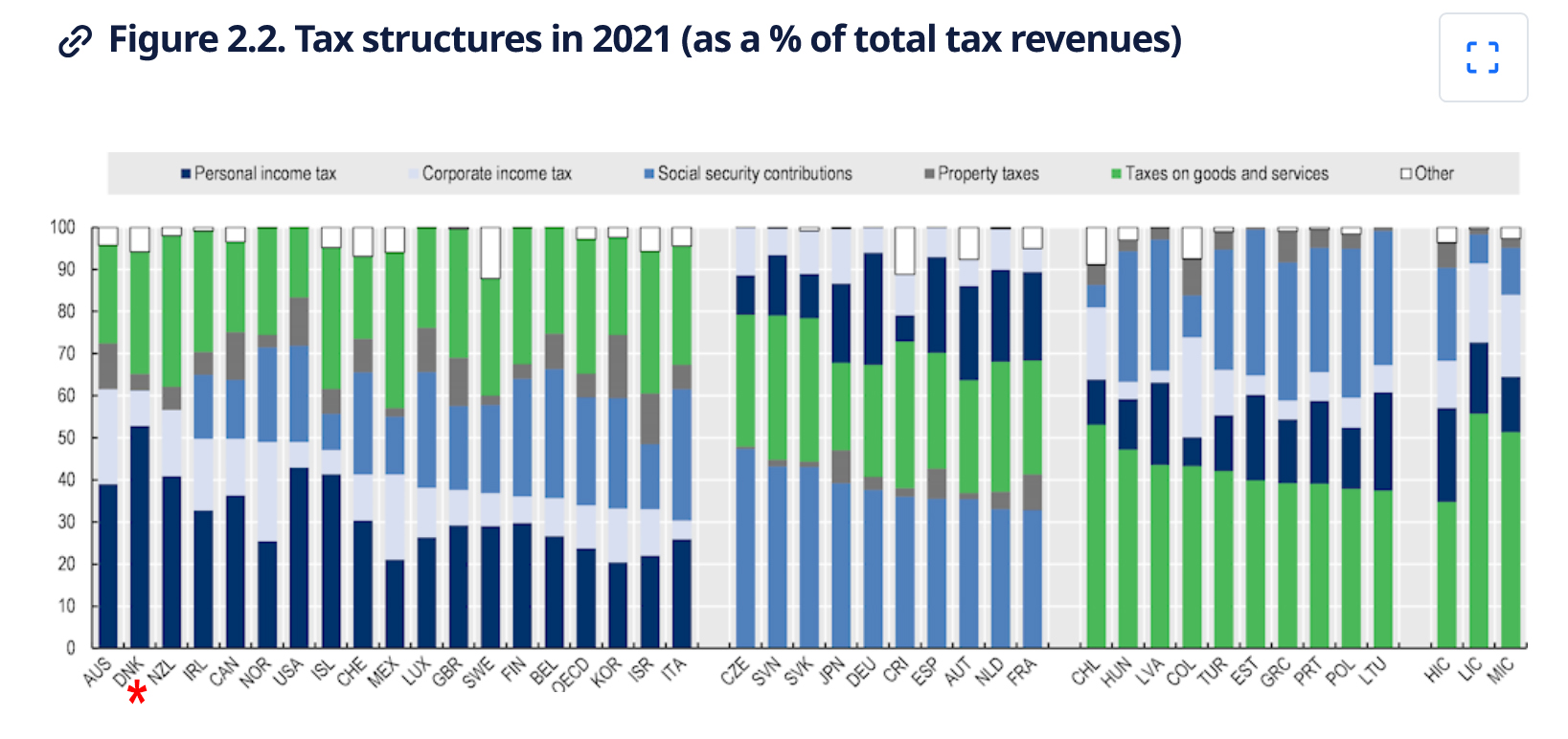

With regards to the composition of tax, 18 OECD countries (including New Zealand) primarily generate their revenues from income taxes, including both corporate and personal taxes. Ten OECD countries relied most heavily on Social Security contributions, and another 10 derived the majority of the revenues from consumption taxes, including VAT, (GST). Notably, taxes on property and payroll taxes contributed less significantly to the overall tax revenue mix in OECD countries during 2021.

Drilling into the detail

Part 3, of the report looks at the detail of the tax policy reforms adopted during 2023. This part has an introduction, then looks at five separate categories of taxes beginning with personal income tax and Social Security contributions, followed by corporate income tax and other corporate taxes, taxes on goods and services, environmentally related taxes and finally taxes on property.

As I mentioned previously, there was “a marked increase in the number of jurisdictions that broadened their Social Security contribution bases and raised rates”. Generally speaking, for high income countries personal income tax and social security contributions represent 49% of total tax revenue. Across the OECD personal income tax represented 24% and social security contributions 26% on average.

Here about 40% of all tax revenue comes from personal income tax. That’s one of the higher proportions around. Around the globe there was a bit of tinkering around personal income tax reforms mainly targeting lower income earners. This is an area where I think we need to focus any future reforms.

We have just (partly) adjusted thresholds for inflation and interestingly, I see that during 2023 quite a few jurisdictions did increase thresholds for inflation. For example, Austria updated its automatic inflation adjustment mechanism to counteract inflation, pushing workers into higher brackets. Meanwhile Australia increased its threshold for its Medicare levy to ensure low income households continue to be exempt, given that inflation has led to higher normal wages.

Corporate income tax rates are on the rise

Substantially more corporate income tax rate increases and decreases were announced or legislated by jurisdictions in 2023. Six jurisdictions increased their corporate tax,four of those did so by at least two percentage points. Türkiye increased all its corporate tax rates by five percentage points.

Whenever there are discussions about reforming our tax system, the issue of reducing our corporate tax rates will come up. With a 28% rate we are at the higher end of the corporate tax rate scale. There is potentially some scope, but as economist Cameron Bagrie has noted any such decrease needs to be part of a broader range of changes.

An example of such a change was the introduction of a general capital gains tax by Malaysia for all companies, limited liability partnerships, cooperatives and trusts from 2024.

Picking out of the details something which I know businesses here would look at with a certain amount of envy is more generous depreciation allowances. The UK, for example, has permanent full expensing for main rate capital assets as it’s called and a 50% first year allowance for special rate assets. Australia has also increased its thresholds for effectively fully expensing items for small businesses. Around the world there’s a whole range of incentives for R&D and environmental initiatives.

We have just limited the limits for residential interest deductions but it’s interesting to see that Italy abolished its allowance for corporate equity provision. Meantime Canada has new restrictions on net interest and financing expenditure claimed by companies and trusts.

Taxes on goods and services (VAT/GST)

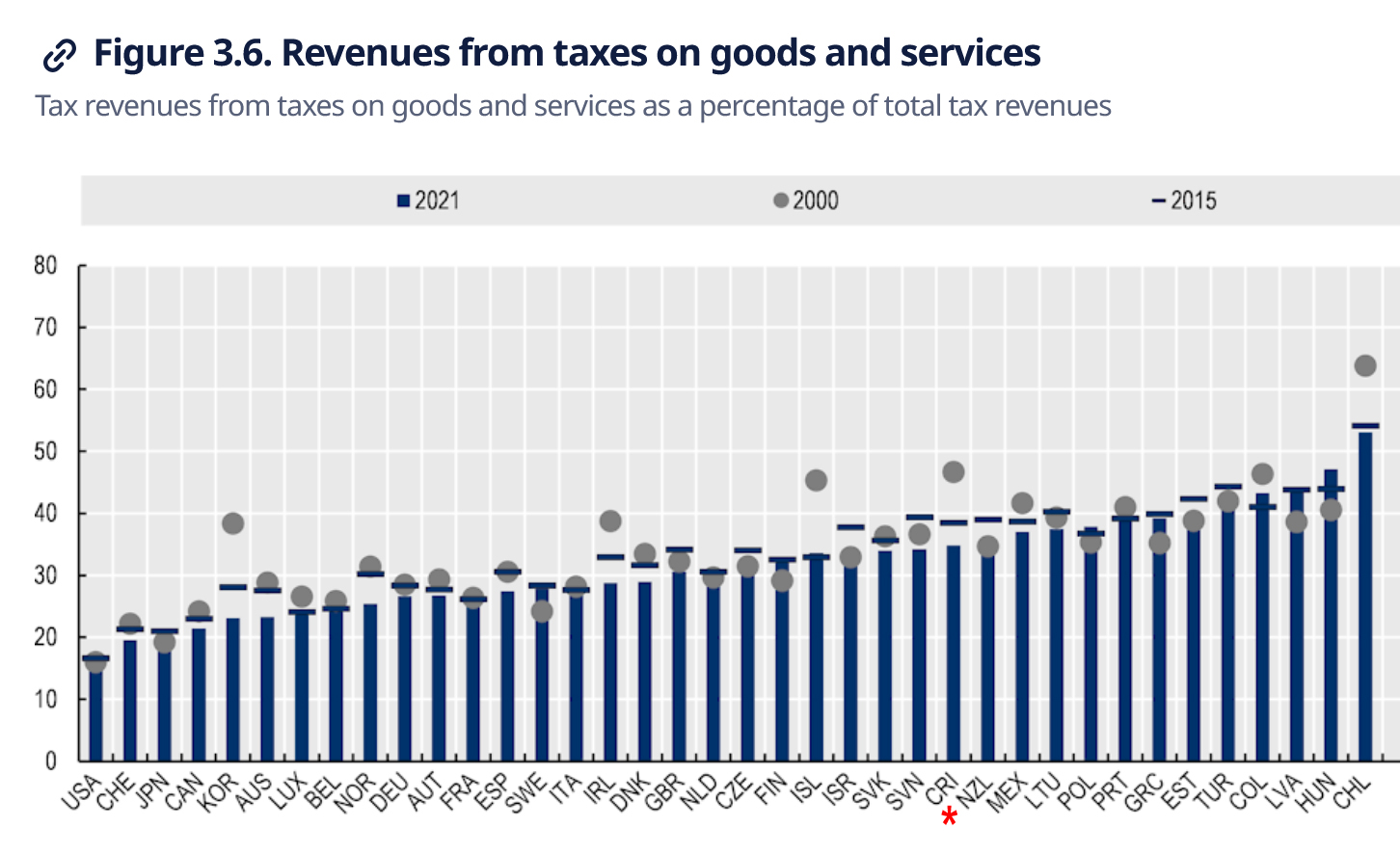

In the VAT/GST space, in terms of revenue from taxes on goods, although we have one of the most comprehensive GST systems in the world, New Zealand was only twelfth in the OECD for the percentage of tax revenue from goods and services as a percentage of total tax revenues. GST raises just over 30% of total tax revenue here, whereas Chile raises over 50%. This is quite interesting given how comprehensive our GST system is. It might mean that there is scope to expand the the rates of GST further. (Six countries including Estonia, Switzerland and Türkiye did so in 2023). But any government doing so should do so as part of a total tax switch package.

We discussed GST registration thresholds a couple of weeks back. During 2023 seven countries increased or planned to increase their VAT registration threshold. I was very interested to discover that Ireland has a split VAT registration threshold treatment: the registration threshold for the sale of goods is €80,000. But for the provision of services, it’s €40,000. I’ve not seen this split before. Meanwhile Brazil is undertaking the introduction of VAT/GST, which is a huge step forward.

A stable tax policy or just less tax activism?

There’s a lot to consider in this report more than can be easily covered here. Overall, it’s incredibly interesting to see what’s going on around the world. Many of the reforms discussed here involve threshold adjustments but there are plenty of new exemptions and incentives introduced. We generally don’t get into this space, that’s possibly a reflection of a very stable tax policy environment, but also perhaps a less activist philosophy by New Zealand governments which hope market incentives will work. Whatever, the approaches it’s interesting to see what’s going on around the world and I recommend having a look at this very interesting report.

ACC crackdown

Moving on, ACC has been in the news when it emerged that it has been chasing thousands of New Zealanders for levies on income they earned while working overseas.

According to the RNZ report, ACC sent 4,300 Levy invoices for the 2023 tax year to New Zealand tax residents who had declared foreign employment or service income in their tax return. The issue is that the person was often overseas at the time the income was earned and in some cases the the person has probably incorrectly reported the income in their return.

It’s an interesting issue and coincidentally, it so happens that I’ve just come across a couple of similar instances. My initial view is there seems to a bit of a mismatch between the relevant income tax legislation and the legislation within the Accident Compensation Act 2001. Watch this space on this one because I’m not sure the matter is entirely as cut and dried as ACC considers.

Inland Revenue responds to social media criticisms

A couple of weeks back, we covered criticism of Inland Revenue for providing the details of hundreds and thousands of taxpayers to social media platforms. It had done so as part of various marketing campaigns targeting people who owed taxes and Student Loan debt in particular.

Inland Revenue has now responded by putting up a dedicated page on its website, referring to customer audience lists.

In its words “social media is just one channel we use to reach customers. It is very effective at reaching people where they are.” As I said in the podcast Inland Revenue’s dilemma is it has to go to where the people are which is on the social media websites. In order to reach out to them it’s going to have to provide certain data. To reassure people the new page explains how it uses custom audience lists and what data is provided.

They do upload a list of identifiers such as name and e-mail addresses, which is then ‘hashed’ within Inland Revenue’s browser before being uploaded to the social media platform. This is where I think the tech specialists have raised concerns that the hash technique is not as secure as Inland Revenue thinks.

Australia – the Lucky Country again

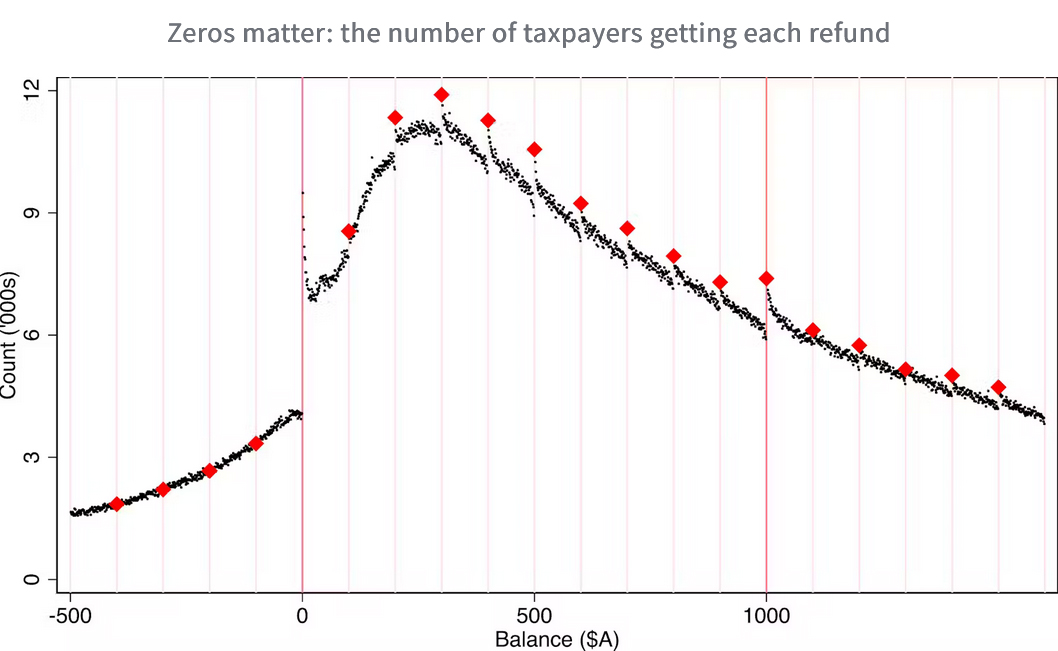

And finally, an interesting story from Australia about tax refunds. A research team at the Australian National University’s Tax and Transfer Policy Institute discovered a “striking” number of returns generating round number refunds (basically any digit ending in zero). The unit examined 27 years of de-identified individual tax files and found far more refunds of exactly $1,000 than of $999 or $995.

The unit concluded these returns are more likely to be driven by efforts to evade and minimise tax and are costly for the Australian Tax Office to audit such as work related expense deductions. Unlike New Zealanders, Australians can claim deductions on their tax returns. Somewhat concerning to me as a professional is that zeros in tax returns prepared by agents were twice as common as those prepared by taxpayers.

What this article is driving at is that some of the complexity of the Australian system results in the system getting gamed. Back in February you may recall Tracey Lloyd, Service Leader, Compliance Strategy and Innovation at Inland Revenue was a guest on the podcast. Based on our discussion and my own observation I would have confidence that Inland Revenue would not get caught out the same way thanks to the Business Transformation programme. As Tracy recounted, Inland Revenue can track live changes and they can see people just trying to square the return off to what they regard as an acceptable number.

Anyway, it’s an interesting story. It shows the differences between our tax system and that of Australia, but it does seem a little rich that not only can you earn more in Australia, but you get bigger refunds.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The aim is to develop a corporate tax database which is going to be available to tax policy researchers and policy makers about corporate tax rates, effective tax rates, tax incentives for research and development and other topics such as withholding taxes. Increasingly, the amount of information includes anonymised and aggregated country by country reporting data, which provides an overview of the global tax and economic activities of thousands of large multinational enterprises operating worldwide. This year’s report covers 8000 such enterprises.

The detailed statistics in the report are mostly from the 2021 calendar year although some 2022 data is included. The report does take into account the statutory tax rates currently in force.

Increased country by country reporting and more reporting generally is part of the 15 actions within BEPS. The report sets out why this is important:

“Action 11 noted the lack of available and high-quality data on corporate taxation is a major limitation to the measurement and monitoring of the scale of BEPS and the impact of the measures agreed to be implemented under the OECD/G20 BEPS Project.”

Corporate tax rates are stabilising

The headline summary is that corporate tax revenues remain important, but statutory corporate tax rates as the report are now showing signs of having stabilised after pretty near two decades of decline. During the period between 2000 and 2024 the average statutory tax rate declined from about 28% in 2000 to 21.7% in 2019. However, between 2019 and through to 2024, it has remained relatively stable at a rate of 21.7% in 2019 and 21.1% in 2024. I think stabilisation is a trend that’s going to continue.

Who knows, though, if the possible re-election of Donald Trump may change this. But I think governments balance sheets worldwide have been weakened considerably by the double whammy of the Global Financial Crisis and then the pandemic. I therefore think the opportunities to actually cut corporate tax rates further are quite limited, but we shall see.

Just to put New Zealand in context, back in 2000, our corporate tax rate was 33%. With effect from 1st April 2008, it was reduced to 30% and then on 1st April 2011 it was reduced to its current level of 28%. Across the ditch Australia has had a 30% corporate tax rate since 2001.

There’s interesting data about the importance of the corporate tax take. On average for the 2021 year, which was also a pandemic affected year, corporate tax revenue represented 16% of all tax revenues. New Zealand is in line with that average, but as a percentage of GDP, the OECD average was 3.3% whereas here it was considerably higher at 5.7%.

The report also considers effective average tax rates (EATRs) and examines the effect of tax incentives such as more generous tax depreciation compared with true economic deprecation. Again, according to the report effective average tax rates have remained relatively stable falling slightly from 20.9% in 2019 to 20.2% in 2023. Median effective average tax rates were 22.8% in 2019 and practically unchanged at 22.7% in 2023. Meanwhile, New Zealand’s effective marginal effective average tax rate is still relatively close to our statutory tax rate of 28%.

But…a narrowing tax base?

Chapter 4 of the report discusses effective and marginal tax rates and has some interesting commentary around declines of effective marginal tax rates (EMTRs). The report notes

“The stability of EATRs combined with declines in EMTRs suggests a narrowing of tax bases in the sample, notably through an increase in the generosity of depreciation provisions. Examining the asset breakdown shows these trends have been driven by increased generosity of depreciation of tangible and intangible assets, as opposed to buildings and inventories.”

I think some of this might be part of the response to the pandemic. New Zealand is noted being alongside Argentina, Japan, Papua New Guinea and Peru as having a higher effective marginal tax rate because we’ve got less generous depreciation rules. (This has become more so with the imminent withdrawal of building depreciation).

Research and development incentives

Chapter 5 looks at tax incentives for research and development, noting that they’ve become more generous over the past 20 years or so. 33 out of 38 OECD jurisdictions offer tax relief from R&D expenditures in 2023, compared with 19 in 2000. New Zealand is one of the new jurisdictions now offering R&D incentives. These are becoming more generous over time.

From a New Zealand perspective, we discuss the importance of R&D in boosting our productivity and we still could do more in that space. I’m inclined to the view I heard recently expressed that it’s better to give a tax incentive for it rather than get involved in the grant process. Because with a grant process, the companies can be restrained in what they have to spend because of the application process. Also, there’s a lot of effort involved with applying grants, less so with an R&D tax incentive, subject to Inland Revenue monitoring.

According to the report the level of direct government funding and tax support for business R&D in 2021 was about .12% of GDP, well below the OECD average of .2 of GDP. So, there’s still room for improvement although that’s something that’s been acknowledged across the board.

Chapter 6 looks at BEPS actions and notes that there’s a large number of controlled foreign corporation or control foreign company rules with apparently 53 jurisdictions having it in place in 2024. There’s also growth in the use of interest limitation rules. This is part of a growing trend in tax policy around the world to consider imposing restrictions on the deductibility of interest. Apparently, there are now over 100 interest limitation rules in place up from 67 jurisdictions back in 2019.

The dangers of following Ireland’s example

Chapter 7 has a breakdown of country by country reporting statistics with 52 jurisdictions out of a possible 101 submitting statistics to the OECD. As I mentioned earlier, this report includes the activities of over 8000 multinationals so there’s a lot of detail in here.

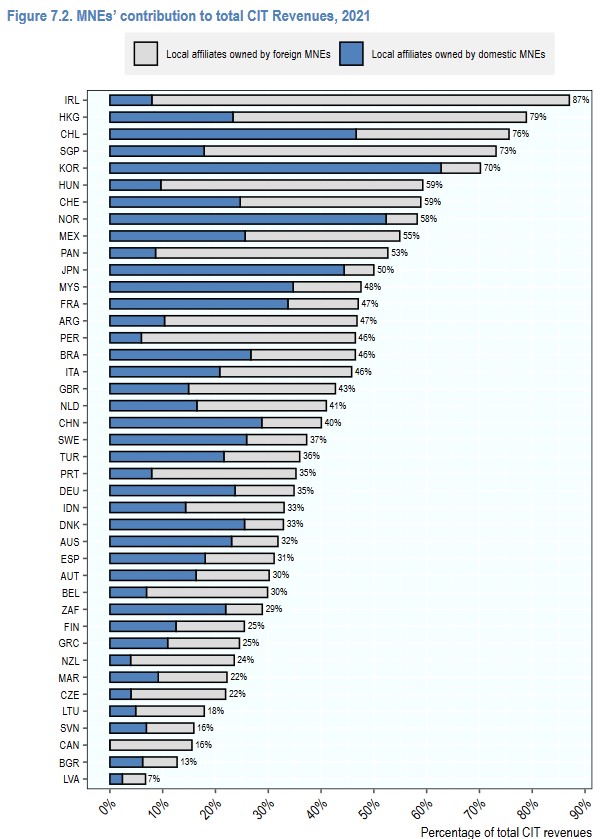

Several commentators including the New Zealand Initiative have recently mentioned Ireland as a potential model to follow. As is well known, Ireland has a very low corporate tax rate. I was therefore very intrigued by figure 7.2 on page 81 of the report, which illustrates the multinational enterprises contribution to local corporate income tax revenues in 2020.

As can be seen, 87% of Ireland’s corporate tax came from multinationals, and the vast majority of those multinationals were local affiliates owned by foreign multinationals. In fact, the Irish Treasury and the European Commission have expressed concern about the sustainability of Ireland’s corporate tax revenue because of the dependency on a few large multinationals.

New Zealand is near the opposite end of the scale with only 24% of corporate tax revenue coming from multinationals, probably three-quarters of which look to be from overseas owned. I think this is an extremely interesting stat which makes me wonder about whether New Zealand is attracting enough investment and whether we should have more multinationals of our own based overseas.

Yes, but is BEPS working?

In summarising key insights on BEPS from the Country by Country Report data the report makes this observation”

“There is evidence of misalignment between the location where profits are reported and the location where economic activities occur. The data show continuing differences in the distribution across jurisdiction groups of employees, tangible assets, and profits.” [page 87]

In other words, the report is basically saying there appears to be some profit shifting going on, but we don’t quite know enough about it. This gets to the heart of the idea behind the BEPS initiative, find out more about what’s happening and then fix it.

As I said the OECD’s corporate database is constantly being expanded so if you’re a bit of a stats guru there’s plenty to dive into and research. Overall, another interesting report highlighting how New Zealand’s corporate tax rate is at the higher end, but noting it also raises a lot of revenue relative to other jurisdictions.

Is that asset depreciable?

Moving on and picking up on depreciation one of the issues covered by the OECD stats, Inland Revenue has just released a draft interpretation statement for comment on identifying the relative relevant item or property for depreciation purposes. This is quite important because our depreciation regime is extremely detailed with a myriad of available rates across several categories.

This draft ties into several other related items of guidance such as residential rental properties depreciation, the question of deductibility of repairs and maintenance – if expenses are not deductible are they depreciable instead? There’s also QB 20/01 – can owners of existing residential parental properties claim deductions for costs incurred to meet healthy home standards? And finally, Interpretation Statement IS 22/04 relating to claiming depreciation on buildings. The imminent withdrawal (again) of building depreciation makes it very important now to maximise depreciation and to identify whether in fact that asset is part of the building or can be claimed separately. This draft is therefore pretty relevant.

The draft runs to 40 pages the last 15 or so pages of which are examples. There’s also a useful 6 page fact sheet accompanying it. Submissions are open until 29th August.

A post-hibernation bear is hungry…

Finally, as we discussed last week, one of the things that came out of Inland Revenue’s recent performance improvement review was for it to be more prominent in promoting what actions it has taken against non-compliant taxpayers. We’re seeing more of that this week when Inland Revenue was announced that an Auckland couple have been sentenced to three years in prison on tax evasion charges. The pair committed 69 tax related offences involving income tax and GST evasion amounting to about $750,000, together with another $80,000 in unaccounted for PAYE. The judge described it as very deliberate offending including deliberate under reporting of business income filing false returns, and even failing to file false returns once under investigation. The couple withheld information from their accountants and concealed the existence of what were described as “highly relevant bank accounts.” So pretty clear case here of tax evasion.

One thing of note that does slightly concern me is this offending occurred over a six year period between 2010 and 2015. That’s quite some time ago and I think Inland Revenue is much more on the case now. Even so you would hope that it doesn’t take 7-8 years or more to bring people to justice on this in the future.

The taxman cometh…

For an idea of how Inland Revenue’s increased activities might play out for your average person, this week’s episode of RNZ’s podcast The Detail discussed how Inland Revenue plans to utilise its additional funding. The episode focuses on the construction industry because of the sector’s long association with the proliferation of the “cashie”. Inland Revenue apparently gets 7,000 anonymous tip offs a year, many of which relate to tradies.

There’s some very interesting commentary from Malcolm Fleming, the New Zealand Certified Builders Association chief executive. He rightly points the finger back at the public for this issue. As he notes, nobody asks their accountant or lawyer ‘Well, how much is it for cash?’ On the other hand, the public seems to be happy to try this tactic with builders and others in the construction industry. On the question of tax evasion and cashies, maybe quite a few people should be looking in the mirror about that rather than pointing the finger elsewhere. It’s a very valid point.

The episode is well worth a listen; it highlights more of what Inland Revenue is currently doing. It’s now doing unannounced site visits to construction sites, for example, which I’m sure would alarm some businesses. But to be fair it also points out most small businesses are run on the straight and narrow. They are perhaps poorly capitalised with overworked owners who are also the main administrator. In many cases the question of tax arrears is more one of poor administration rather than in the case of the couple who were jailed, deliberate malfeasance.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A quiet week in the tax world – but is this the calm before the storm of this year’s Budget?

The latest OECD report on taxing wages shows the tax wedge rising in most countries including New Zealand.

It’s been a quiet week in the tax world, which, to be honest, is quite welcome. But there’s also a growing sense of a calm before the storm, that being the Coalition government’s first Budget on 30th May, I’ll offer up some speculation as to what I think will be in the budget closer to the time, but one thing we do know will be expected to happen, is adjustments to the flat tax thresholds, which as listeners will well be aware of, have not actually been adjusted since October 2010.

It so happened last week the Organisation for Economic Cooperation and Development (the OECD) released Taxing Wages 2024, its annual Taxing Wages report. This is a fascinating document which looks across the composition of wages and provides details of taxes paid on wages. This year, it’s also focusing on fiscal incentives for second earners in the OECD and how tax policy might contribute to gender outcome gaps and labour out market outcomes. It’s a big report which runs to 679 pages and is only available online.

Taxes are increasing thanks to inflation

One of the things that comes out of the Executive Summary was that in the words of the report tax systems in the OECD are not fully adjusting to inflation. Consequently,

“The average tax wedge for all eight household types covered in this report increased in the majority of countries between 2022. And 2023 driven in most cases by higher income tax. For the second consecutive year, more post tax incomes at the average wage level declined across the majority of all OECD countries now.”

The tax wedge is described as the difference between the labour costs to an employer and the corresponding net take home pay of the employee. It represents the sum of the total personal income tax and Social Security contributions paid by employees and employers. Less any cash benefits that the employee might receive.

New Zealand has consistently scored well in this measure because we don’t have Social Security taxes and we’ll talk a little bit more about that later. But notwithstanding that, the average take home wage for New Zealand employees has been declining over the past few years.

The report has an appendix showing the evolution of effective tax rates on labour since 2000 with a number of separate measurements based on single persons, single parents, or married couple with two children. It looks at what the tax wedge for each group is based on 67% of average wage, 100% of average wage and 167% of the average wage.

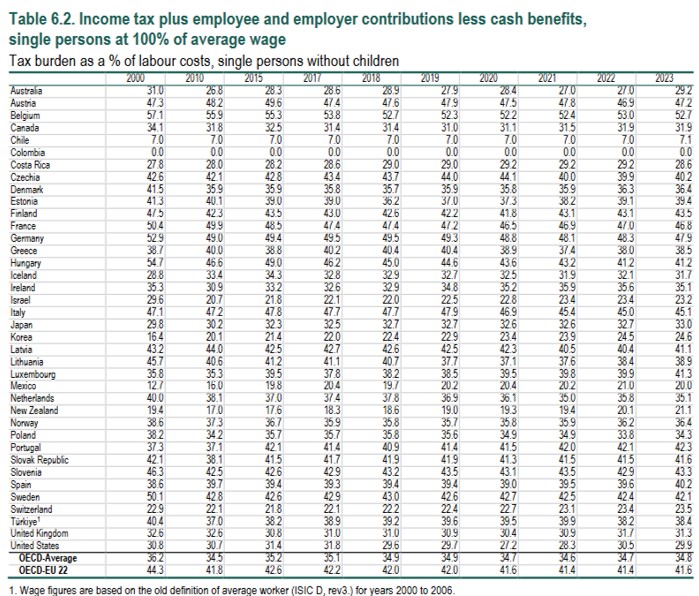

Now, whatever measure you take, you can see that the tax burden for New Zealand employees has been rising steadily since 2010, but you can see it start to accelerate in the last three to four years. So, for a single person at 167% of the average wage, their tax burden has gone from 23.9% in 2017 to 25.8% in 2024. Now you might think 2 percentage points isn’t much, but it becomes more noticeable as it accumulates over time. For a single person at 100% of the average wage the tax burden has gone from 18.3% to 21.1% over the same period.

This OECD report reinforces what we’ve been saying for some time that tax adjustments to the thresholds are long overdue. Now those who listened in to last week’s podcast with Sir Rob, Rob McLeod, Robin Oliver and Geof Nightingale will have noted pretty much everyone was of the view that the threshold where the 30% tax rate kicks in, that’s $48,000 was a major problem in our tax system. Geof was particularly insistent on this point. This OECD data reinforces that point. So, it will be interesting to see what moves are made in that space in the Budget at the end of the month.

Social security taxes – time for a rethink?

Moving on, thanks to everyone who’s commented or given feedback here and across the various social media platforms about last week’s podcast. It’s always great to have some engagement. I do read all the comments even if I don’t always respond.

There were some particularly interesting comments from Dr Andrew Coleman of the University of Otago about Social Security taxes and the absence of them in New Zealand. As he noted, New Zealand is an outlier in world terms in this respect.

Now, as I mentioned in the podcast, Social Security contributions were once quite a significant factor of the New Zealand tax system from the 1930s until the 1960s. But what happened over time was that the contributions weren’t hypothecated and applied only to Social Security payments, but in fact just became treated as part of taxation generally until in April 1964, the Social Security Fund was merged into the Consolidated Fund

Ultimately, the then Finance Minister Robert Muldoon decided in 1968 that separate Social Security contributions were no longer required and merged everything formally into income tax. Since then period, income tax has used to pay for Social Security such as welfare and superannuation.

That’s more than 50 years ago, but as Doctor Coleman pointed out many other countries have Social Security taxes. So, is that something we should consider in more detail? Well, I hope to explore that point in a separate podcast.

Sir Rob McLeod, Robin Oliver and Geof Nightingale on expanding the tax base

[In this part of the podcast I asked Sir Rob, Robin and Geof about the strains New Zealand’s Broad Base Low-Rate approach is experiencing and if a government wanted to raise how would it do so- through a wealth tax, capital gains tax, stamp duties or estate duties, whatever].

Sir Rob Mcleod (RM) Well, if I can kick off, I’m a huge fan of Broad Base Low-Rate (BBLR). I think it’s got a very simple thrust. It’s as much about pragmatism as it is about technical. I think we need to be careful in my experience with the debate and understanding that a Broad Base Low-Rate system is not one characterised by a myriad of taxes. Some people interpret a myriad of taxes as achieving breadth and therefore fitting with Broad Base Low-Rate. No, my definition of Broad Base Low-Rate is a few taxes with a broad reach. That’s where you get the simplicity. And the income tax and the GST covers most of GDP in the nation.

What does it not touch is the question to ask. You can talk about wealth tax and CGT, capital gains tax, but they’re actually part of the income tax. There’s an overlap between wealth tax, capital gains tax and the income tax. I don’t believe that that gap justifies the kind of emphasis that’s being given to wealth tax and CGT.

Sure, we’ve got some capital gains not taxed, most of them actually are taxed already in the system. The comprehensive capital gains tax I think in that sense is a bit of a misnomer because we do not have comprehensive taxation in the New Zealand system. And if you go and then put wealth taxes on, whether it be land or wealth in general, you are actually doubling up on the income tax. You’ve got an element of double tax in doing that and that takes us back to the starting point, that Broad Base Low-Rate is about identifying the gaps. And there’s bugger all gaps actually left by a broadly designed GST and income tax such as New Zealand has.

And when we go into the debates on specifics around the margins of that base, there are good reasons for arguing about why we shouldn’t have them. So that’s why I think BBLR is there. If you want to get more out of what we’ve got than the broad base of income tax and GST, you’ve got to justify it and you’ve got to start with what percentage of the GDP should be taxed in the first place. With balanced budgets, government spending equals taxation. With a balanced budget, which is kind of where the world wants to be these days.

So, I think recognise that the tax rate for the nation is government spending divided by GDP. And there’s a hell of a lot of benefit from there. So, if you want a tax cut, you’ve got to cut the government spending. It’s the only way to do it. Those various elements I think are very interconnected in the debate around Broad Base Low-Rates.

Geof Nightingale (GN) I think your question was where would you go to for another 1% of GDP? And I would agree with Rob that it feels to me that 30% of GDP or Government expenditure to GDP at roughly 30% has (that’s our long-run average, it spikes up and down for pandemics and earthquakes and recessions and things) that’s a constraint that I would be quite personally happy for our economy to operate against.

The question is then how you raise that revenue. And I totally support Broad Base Low-Rate. I think it’s effective in practise and 30 years of experience. I think the missing bit still there is our income tax is not as Broad Based as it should be, and I think we do need to extend it into further realised capital gains. So, whether you do that as a separate comprehensive capital gains tax like other countries, or you just change the definition of income, that’s a design feature.

Philosophically, it’s the same thing. It’s just how you get there. Taxing more income through realised capital gains, and then I would recycle that revenue into tax cuts, reductions, initially in the lower marginal rates because that’s where our problems come with high effective marginal tax rates in conjunction with welfare, which leads to productivity and incentives to work and all of that. So I would extend the taxation of capital, recycle the revenue and like Rob aim for 30% government expenditure over GDP.

TB Robin, you were part of the tax working group, you were one of the three dissenters in 2019. I that still your opinion?

Robin Oliver (RO) As Rob said and Geof echoed, it’s not a black and white issue. Do you tax capital gains or not? I mean, Michael Cullen kept on trying to make the point, talking about taxing capital income, not capital gains. Everybody ignored it, but he had a point that we do tax capital gains in certain cases and it’s all part of our income tax system and GST anyway. Are there holes in the system where you can efficiently raise more money at low cost? And the big hole, the gap in our system, it came out in the tax working group and all other reports is land.

We are a growing economy, growing population, land rises/increases systematically in value and that produces a lot of income and overall, we don’t tax it. You look at all the data, you know, higher wealth people, predominantly own land. Not all, but predominantly. So OK, should we be taxing land in one form or another? And I’ve got sympathy for that, but you’re going down to the workability. No government will ever tax home ownership. If it does, it will cease to be a government pretty quickly and someone sensible will come in and abolish that tax. So that’s a big hole in any land base. And then you’ve got issues about iwi and their relationship with land. You’ve got farmers.

We used to have a land tax. We had a comprehensive tax in the 1890s and we ended up with a tax just on Queen St commercial property. Everybody else got exemptions over time. I have some sympathy for taxing the increase in the value of land or land in some form which is not taxed now, but the housing, the home ownership stuff. You know, David Caygill, he proposed taxing homeowners. And he got told to back off.

I was working with him on capital gains tax proposal and we officials recommended including home ownership. And we were gobsmacked, totally bewildered when he accepted our recommendation. We expected him not to. And he went off to lose that next election, but probably not for that reason.

Workability matters. Home ownership is off the table. Our problem as a country is we take our savings, we invest it in land, we borrow from Australia, we invest in more land, bid up the price of land. We end up with the same amount of land as we began with – because that doesn’t increase – and heavily in debt to Australian banks. Solving that problem is not easy.

The problem with overinvestment in housing

TB Yes, it’s a behavioural impact. I had this conversation with an American client yesterday, who because of the fact they have to file U.S. tax returns, they’re subject to capital gains tax. But the FIF regime, he looked at that, and said, well, I can’t invest in stocks so I’m going to look at residential investment property here. That’s really a case of an unintended consequence of a tax.

On the family home, I fully grasp all of that, but is there an argument for saying that there is a limit? Because we build some of the biggest houses in the world. New Zealand houses – new houses, were until quite recently – are the third largest in the OECD. They were nearly getting on for close to 200 square metres.

RO We like our houses.

TB So could you say above two and a half million dollars or $5 million, the gain above that – some pro rata, we’re getting into technical details, but there is this thing that you’ve just espoused it perfectly, Robin. That at present we’re encouraged to invest in land and more land and borrow. So, there’s a loss of productivity, that 20% dead weight. There’s got to be a lot of lost productivity because capital is diverted into land rather than elsewhere.

RO The current group did look at something like that, although it was outside our terms of reference. We were not allowed to even consider the home or the land underneath the home or the sky above the. In terms of reference that we did look at that. The trouble is, a $2,000,000 house is not all that much in Auckland, as Michael Cullen kept on putting out, it was a hell of a lot in Whakatane.

TB There are 77,000 homes in Auckland worth more than $2,000,000, according to an OIA I got.

RO Probably one in Whakatane.

GN There’s a technical solution. If you were going to put all realised capital gains into the tax pot, you give every New Zealander a lifetime exemption, regardless of asset class or description, and that might be $5,000,000 or more, less but and that then shouldn’t distort behaviour. It’s arguably equitable and from a compliance and administration perspective, it would take probably 95% of us out of the of the loop.

RO And with that 95% of revenue.

GN Yes, well, maybe not because the assets are weighted towards the top. But anyway, the argument against that was always administrative. It’s very difficult to administer. But with current digitisation and things, I’m not sure those administration and compliance arguments – the integration of the land registers and share registers and things – as strong as it used to be. So, there are theoretical solutions there, but they’re hard to get to the public.

RO The idea of taxing the person with over $5 million has got a lot of appeal, but it’s not realistic. I always give the example of the idea you can freely tax all these very high wealth individual/ medium wealth individual people. Well, some of those are your medical specialists, your surgeon, your oncologist. And they can go to Australia.

You whack this $5,000,000 tax on their income over a lifetime and off they go to Sydney. So you’re sitting here in New Zealand, you’ve got cancer or something like that, and we’ve got a more equal society, but we have no treatment for cancer. Off to a hospice you go.

GN That might be the case with a wealth tax, but with an income tax I’m not convinced, Robin. I mean, Rob might be able to comment with direct experience of working in Australia. But labour and consumption taxes in Australia on high earners, medical professionals, they’re pretty tough compared to New Zealand. (TB 45% top rate plus 2% Medicare).I would have thought, but I don’t know what your experience is Rob.

RM it’s not just Australia, we’re becoming more global, aren’t we? So almost every country is a neighbour of one sort or another these days. The other thing is these people are incentivised to find these loopholes. And having lived, having operated and worked in Australia for six years, they’ve seen wealthy people find loopholes there too. So that that won’t go away.

TB It’s our job to find them, to be frank.

RM Yes.

RO The government legislates for them. You get tax free superannuation in Australia, or 15%. We’ve got to get away from this idea we can tax our wealth. Our problem is, as we’re next to Australia, is Australia becoming wealthier than we are. It’s attracting our nurses, our doctors, our policemen, our police persons and what have you through higher wages. We’ve got to increase our wage level and our productivity, and we don’t do that by sitting around and inventing new taxes.

TB But do we change the incidence of tax, so that capital gets diverted into more productive areas?

RO I give you the example of houses. I agree with that.

GN Our effective marginal tax rates, in those doctors, nurses and policemen, if you go across to Australia and look at those, yes, the incomes are definitely higher 30 or 40%. But I think there’s a tax dynamic in there as well for those people. Because we’re sweating our labour incomes, particularly in those low ends.

Robin has often said this, the worst tax rate we’ve got in New Zealand is the 30% rate at $48,000. Which is huge, it kicks in below the median income. So, I think there’s a tax dynamic in those migrations of doctors, nurses and police as well.

What about inheritance taxes?

TB The $48,000 threshold is a shocker. A final point on this housing. I think you’re right, politically a capital gains that incorporates the family home is impossible. You’re not even a one term government with that. But does that perhaps point to the need – and this is where the IMF come in – is that maybe that’s picked up through an inheritance tax at a separate point. Inheritance taxes, estate duty used to be quite significant. It was 5% of government revenue way back when in 1949, and they were one of the first taxes we introduced here. But they’ve declined over time around the world, but now there seems to be particularly with this, the wealthiest generation in history – and I think all of us are members of the Boomers – are starting to pass away, and there’s a huge transfer of wealth about to happen. And governments are looking at that.

RM Can I bring the conversation back to where I was about what percentage of GDP should tax be.

Because we are straight into, in essence, the tapestry of taxes. And what lurks underneath the motive for that conversation is really redistribution. Because a lot of the motive in the conversation that we’re having is about getting feathers off particular geese, and about certain thresholds and the rest of it.

The starting point ultimately is what does the country need by way of revenue as a percentage of GDP now? Now, if you’re arguing that actually New Zealand’s got a big problem of injustice or inequity because the rich are basically getting away with it, is a bit of a different to back from where we came from and earlier on in our conversation. Geof, to be fair, has identified redistribution as a goal. So he’s been consistent in that regard.

But I think this demonstrates why it’s so important to first of all ask yourself what you’re trying to do with your tax system, and if it is about revenue and getting a particular percentage of the GDP, then I think that these debates about estate duty and wealth tax and land tax are red herrings.

The 1% of GDP, for example, Geof, that you’ve mentioned in the question we’re asked to consider through a new tax, does not undermine my general principle of the broad reach and impact of GST and income tax. In fact, you guys (Robin and Geof) were both on the Cullen Review and you actually, in the report that came out, compared a 1% increase in GST with the capital gains tax and it kind of blew it away. That demonstrates my point that the Broad Base reach of GST and income tax can do everything that you’re trying to get out of these, peripheral and miscellaneous taxes. The only thing that’s left standing as to why you want to do it, is redistribution.

RO I’m OK with that, obviously. But getting on to death duties, estate duties, they have an interesting history. Other countries have them. People have different ideas about bequests and motivation. You know, how important it is to give money to the children. You’ve got Warren Buffett, who honestly gave each of his children 10 million and that’s it. Well, 10 million seems like a nice little nest egg, but in Warren Buffett’s terms, that’s just rounding. Bugger all in bequest terms, Other people will die for it. Literally, they will fight. It is enormously powerful. They will do anything to avoid death duties.

When we used to have them, that was the area of massive tax planning. It was the beginning of it all – avoiding death duties was a massive industry. And you think it’d be easy to do. Well, you’ve got to have gift duties as well, otherwise people just give it away to the kids. And you end up with Inland Revenue, as it used to do, roaring around, stamping every gift that’s made in the country, every Christmas and what have you, and determining they’re not subject to gift duty.

Massive amounts of bureaucracy involved. They are not easy taxes and I’ll just finish with the history of the end of death duties in New Zealand.

It started off with Australia. Death duties were limited to the state governments. When Queensland got rid of its death duties Victoria and New South Wales and the rest of Australia followed suit. We followed thereafter. Because anybody was going to go to the country which didn’t have it.

Death duties have got some appeal to people, I understand the issues. It’s very appealing when people don’t have any bequest, motive to actually tax a windfall gain. The only reason they are working, building their business is for the children and grandchildren. These people will react massively to its reintroduction.

[This is an edited part of the full podcast which readers are encouraged to download and listen to at the link at the top of this page.]

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.