What connects Pillar One and Pillar Two with the collapse of Newshub?

New draft Inland Revenue guidance on employee share schemes.

Today (Monday) I was (virtually) at the Accountants and Tax Agents Institute of New Zealand (ATAINZ) annual conference which, like last week’s International Fiscal Association, (IFA) Conference, was opened by the Minister of Revenue, the Honourable Simon Watts. The Minister repeated much of what he had said to the IFA conference about supporting the Generic Tax Policy Process, his wish for simplification in the tax system and improving compliance being a main driver. As the focus at the IFA conference is very much on tax policy his comments were very welcome.

By contrast, at the ATAINZ conference, the focus is slightly different because the audience there was comprised of tax agents, and we’re more focused on operational matters. So, when it came to Question Time, there were quite a number of questions around operational aspects of Inland Revenue. One of the first questions that was asked was what was going to happen with the trustee tax rate, which you may recall is proposed to rise to 39% under a bill presently before the Finance and Expenditure Committee.

Now we’re expecting to hear back from that fairly soon, but during the week the Minister of Finance, Nicola Willis, hinted that some form of carve-out might be happening, in that the 39% trustee tax rate might not apply to all trusts. So naturally, some questions were directed at the Minister seeking clarification on this point.

He wasn’t able to give more guidance, simply saying that we will have to wait until the Finance and Expenditure Committee reports back, which is expected next week. The Minister got told it is a rather frustrating scenario because we’ve got the run up to the end of the tax year on 31st March, and we will be wanting to plan payments for dividends and other distributions in before then. Unfortunately, the issue remains a bit of a grey area for the moment.

More trusts file tax returns in New Zealand than in the United Kingdom

There’s a couple of statistics that highlight the scale of this issue.According to Inland Revenue for the 2022 income year (typically the year ended 31st March 2022), the number of trusts and estates which filed a tax return totalled 237,226. That’s actually a decrease of more than 19,000 from the prior year.

It so happens that I came across statistics from the UK’s HM Revenue and Customs about the number of trust tax returns that are filed there. And according to the equivalent tax year to 5th April 2022, HMRC received 141,500 returns.

Just pause and think about that. In absolute terms, more trust and estate tax returns are filed in New Zealand than in the UK, despite the UK, with its population of some 67,000,000 being almost 13 times greater than here. So actually, on a per capita basis, it would point to the fact, for every trust tax return that’s filed in the UK, there would appear to be close to 21 filed here. The tax rate for trusts is therefore a big issue in relative and absolute terms and that’s why the tax community and trust community are really keen to get this matter resolved as quickly as possible.

What evidence is available points to the fact that for most trusts – once you include the associated families and beneficiaries that are in there – their income would not exceed $180,000, the threshold at which the 39% top tax rate kicks in. But there is a small and significant group, about 11% according to Inland Revenue, that do receive a very large amount of income. So that’s something we’d like to see resolved soon and hope it’s in time for us to get clients advised and ready for the new tax year changes.

Interestingly, on the other comments the minister made to both the IFA and the ATAINZ conferences about Inland Revenues regulatory stewardship review of fringe Benefit Tax which it did in 2022, it’s clear that there is likely to be a focus on this issue from Inland Revenue on greater audit activity. This is something promoted under the Coalition agreement. What extra resources Inland Revenue is going to have and the full direction that it’s going to take going forward are probably only going to become clearer after the Budget on 30th May. Which, as the Minister pointed out, was not that far off in reality.

How the end of Newshub and the OCED international tax deal are connected

The news that Newshub’s operations will end with effect from 30th June was a big shock to the media community. As someone who has occasionally appeared on various Newshub programmes, my sympathies go out to all those affected. And I do hope that some means is found to keep the operation going, although it has to be said, it’s very doubtful at this point. I’ve always found in all my dealings with journalists of whichever organisation, they have always been incredibly professional, and I’ve appreciated that. And so, as I said, this is not a great day for journalism, and has also been pointed out, it’s not actually a great day for democracy as a whole.

Now one of the many excellent sessions at last week’s IFA Conference was an American perspective on Pillar One digital services tax and Pillar Two, the proposed international tax agreements, which have been under negotiation for some time. The taxation of the tech giants such as Facebook and Google is a key part of Pillar One and Pillar Two, and that’s the connection with the collapse of Newshub.

Newshub is no longer financially viable according to its owners, Warner Brothers, because of collapsing advertising revenues. A couple of days after the Newshub announcement, its competitor TVNZ reported an operating loss of $4.6 million for the six months to 31st December 2023. TVNZ noted that its advertising revenue fell from $171.3 million in the six months to December 2022 to $146.8 million in the six months to December 2023, against a background of rising costs.

So where is that advertising going? Well, most of it is going offshore. From what we can pick out from the financial statements of Google and Facebook New Zealand for the year ended 31 December 2022, it would appear that close to $1.1 billion during those years was paid to offshore affiliates in so-called service fees. Now that’s a substantial amount of money, and those transactions are entirely legitimate under the present tax rules. But it has to be said, even if 10% of that $1.1 billion were to stay in New Zealand, it would be a significant boost to the industry. And arguably the difference between Newshub’s operations continuing and being closed.

The offshore advertising and the service fees and the whole issue around the taxation of tech companies, point to the pressure building on the tech companies because New Zealand is not alone on this. Over in Australia Meta, the owner of Facebook, has said it’s no longer going to go through with the deal to pay news companies who were providing content on its websites.

The presentation at the IFA Conference kept coming back to a key point that I’ve always believed, which is tax is inherently political. The French were one of the first drivers of change in this space but obviously the American companies, which would be the most affected, pushed back by putting pressure on the American government to respond. And so even though the Generic Tax Policy Process tries to depoliticise tax policy as much as possible, ultimately governments are elected with certain political objectives, and those will often trump best tax policy, and that’s just a fact of life.

A digital services tax to help media?

The whole question of the impact on democracy and journalism of Newshub’s closure is beyond this podcast. But the pressure will now mount on the Coalition Government to consider what steps it can do to help the media. On the other hand, the Public Interest Journalism Fund was highly controversial.

Does that mean that there may need to be a change in tax policy to perhaps try and claw back some of the revenues going offshore through, for example, a digital services tax which is controversial and hated by the tech companies? Does the Government press hard for a resolution to Pillar One and Pillar Two? Or does Newshub just get shut down and we have to live with the consequences of that? Whatever, pressure will be building for the Government to take some form of action. Watch this space to see whether any such action results in amended tax policy.

Inland Revenue consultation on employee share schemes

Moving on to more routine matters, Inland Revenue has released several draft consultations on employee share schemes. The taxation of employee share schemes underwent major reforms in 2018. Subsequently, there’s been a number of questions to Inland Revenue about how the law applies in certain scenarios and how it interacts with other regimes such as PAYE and FBT.

Inland Revenue has therefore released six items – five draft interpretation statements and one draft Questions We’ve Been Asked, each focusing on a specific aspect of employee share schemes. This has been done rather than producing one single interpretation statement, so that people can more easily focus on the topic of particular interest to them. Alongside this, Inland Revenue has produced a four-page reading guide briefly summarising what each interpretation statement/QWBA addresses.

This is slightly unusual but it’s an indication of the complexity involved. Employee share schemes are used by a lot of companies and particularly small growth companies in the growth phase where they don’t have cash but want to attract and keep key employees as they expand until the ultimate goal, whether it’s ultimately a share market listing or perhaps a sale to a larger company.

The first interpretation statement is one of the more important ones, as it considers what represents an employee share scheme. The critical issue is when does the share scheme taxing date arise? That’s often a critical issue because one of the things about share schemes which causes difficulties is if there’s a mismatch between when the tax is due, but when cash might be available for the person who’s being taxed to actually pay the tax due. In fact, another of the drafts looks at the questions about an employer’s PAYE, student loan and KiwiSaver obligations where an employer wants to fund the tax cost on an ESS benefit provided in shares.

Another important draft reviews what happens with the ACC, PAYE and KiwiSaver obligations, when the employee share scheme benefit is paid in cash rather than shares. The draft concludes cash-settled ESS benefit is an “extra pay” under the general definition of extra pay and therefore a PAYE income payment, regardless of whether an employer elects to withhold PAYE in respect of the benefit.

Of the other draft consultation items, topics covered include what deductions are allowable for employers in respect of employee share schemes, and what is the treatment of dividends that are paid on shares held by a trustee for an employee share scheme.

Overall, this is very useful guidance and I do like Inland Revenue’s approach of issuing separate interpretation statements rather than consolidating all the items in a single item which would be close to 150 pages. Consultation is open until 26th April.

Thanks Chris

And finally, this week, Chris Cunniffe, CEO of Tax Management New Zealand (TMNZ) for 12 years, has just stepped down from his role. He made a brief presentation at the ATAINZ conference, explaining it coincided with the 44th anniversary of the start of his tax career at Inland Revenue. We’ve worked with Chris and his team at TMNZ for many years, helping our clients save tens of thousands of dollars. Chris has also been a past guest on the podcast. We wish him all the very best for the future.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

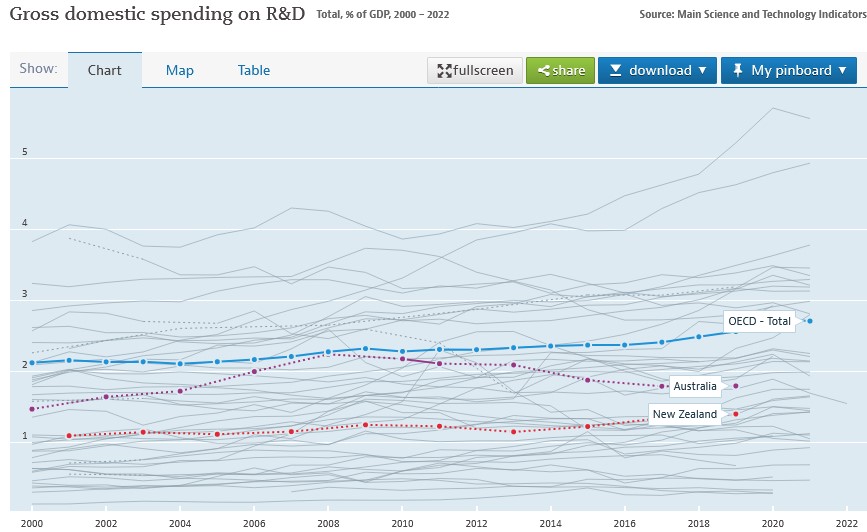

Inland Revenue has released a draft interpretation statement on the research and developments loss tax credits regime. This is a refundable tax credit available to eligible companies when they have a loss which has arisen from their eligible research and development expenditure.

The regime was introduced in 2016 to encourage business innovation and also to address New Zealand’s poor record of R&D expenditure. According to OECD data, in 2019 New Zealand’s spending on R&D was just 1.4% of GDP, well below the OECD average of 2.56% of GDP. Over the past 20 years research and development in spending in New Zealand has been a full percentage point of GDP below the OECD average.

So given that we also have a poor record of productivity, increasing R&D expenditure is seen as critical in improving productivity and ultimately the strength of the economy.

That’s the background behind the introduction of the loss tax credits regime. It’s intended to assist the cash flow of those companies carrying out research and development. Often in the early years, these companies are running at a loss. Hopefully once the R&D matures and bears fruit, they will then have profits resulting from the expenditure.

But funding cash flow in those early years is pretty difficult. So instead of the tax losses to be used against future profits, under the regime, companies can instead receive a payment. Note, only companies can receive this R&D tax loss credit payment. That’s because losses incurred by partnerships, limited partnerships, look-through companies and sole traders can already pass those losses through to the underlying owners anyway, who will often be able to offset them against their other income. Essentially, they are already able to benefit from the ability to cash-up losses. But companies can’t do that, hence the introduction of the regime.

The Inland Revenue draft interpretation statement looks at the background to scheme, summarises the rationale for scheme and how it operates. A couple of key points about the regime: you can drop in and out of it, you can opt to choose a payment in one year but not in another year. Once you have claimed a refund by cashing up your losses, the regime operates rather like an interest free loan. You’re essentially required to repay it and it’s generally treated as being repaid when the company starts paying tax, the R&D having borne fruit.

However, there are other circumstances where the credit may have to be repaid earlier when there is, in the terminology of the regime, a loss recovery event. Now, that typically will happen if there’s a disposal or transfer of the intangible property, core technology, intellectual property, etc., which is done for either less than market value or the amount sold is a non-assessable capital gain.

Another situation, and this is actually one where I’ve been involved, is where the company is no longer tax resident in New Zealand. Some very interesting issues arise in that case. Then there’s the worst-case scenario, where a company goes into liquidation although what exactly can be recovered at that point is a moot point. But that’s still a loss recovery event.

And then finally, and similar to our other rules around the carry forward of losses and imputation credits, a loss recovery may occur if there is a loss of the required shareholder continuity. In the case of the tax loss credit regime, the relevant shareholding percentage is 10%. In other words, there’s no breach if at least 10% of the voting interests of the company are held by the same group of persons throughout the relevant period.

In my view this is a very important regime for improving the future productivity of the country. The scale of the spending is going on is quite interesting to see. We can get an idea of this because the Inland Revenue as part of the budget produces what is called a tax expenditure statement.

Tax expenditure statements are a summary of the cost of a particular tax preferred regime, which, like, for example, this regime, has been introduced for specific policy reasons. The OECD collects data on tax expenditures to get a global picture of what spending is going on in tax preferred regimes.

In the case of the R&D loss tax credit, the estimated value of the expenditure for the year to 30th June 2023 is $362 million, a little bit below 1% of GDP. The estimated expenditure for the year to June 2022 was $473 million. And you can see a steady rise since the regime was introduced in 2016.

Of course, the real importance of this regime is whether it has produced a boost in total R&D spending within the economy. And then ultimately, does that lead to increased productivity. It’ll be interesting to measure these once the data flows through in due course.

So, an interesting regime and good to see Inland Revenue give some guidance on this. It contains a few hooks but it’s well worth looking at if you’re thinking about trying to make use of the scheme. And as I said, we will watch with interest to see how it bears fruit.

Shuffling forward on internationalPillar One and Pillar Two proposals.

Moving on, we’ve talked fairly regularly about the OECD’s global minimum tax deal and Pillar One and Pillar Two. Last week the G20 met in India and the Secretary General of the OECD reported to the meeting that, “A historic milestone was reached at the 15th Plenary Meeting of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (Inclusive Framework) on 11 July 2023, as 138 members of the Inclusive Framework approved an Outcome Statement on the Two-Pillar Solution.”

In summary, what’s happened is that they’ve developed a text to a multilateral convention which will allow jurisdictions to exercise a domestic taxing right over the residual profits of the largest, most profitable multinationals. That’s what they call Amount A of Pillar One, and that will apply to multinationals with revenues in excess of €20 billion and profitability above 10%. What will happen is the scope of that taxing right will be 25% of the profit in excess of 10% of revenues. This €20 billion revenue threshold will gradually be lowered to €10 billion after seven years, conditional on the successful implementation of Amount A.

There’s a proposed framework for the simplified reporting application of arm’s length principle, which is key to transfer pricing and for baseline marketing and distribution activities. That’s what referred to as Amount B of Pillar One.

There’s a Subject to Tax Rule, again with an implementation framework, and this is really for developing countries to update their bilateral tax treaties to tax intra group income. This is where such income is subject to lower tax in another jurisdiction, in other words say one country has a 20% corporation tax rate. But that multinational shifts charges to another part of the multinational group in a jurisdiction where those charges are only taxed at a lower rate. This Subject to Tax Rule gives the first country more taxing rights in that income. Developing countries are very keen on this particular point because they feel that this is where the current tax regime has been almost predatory on their tax base.

There will be a comprehensive action plan developed by the OECD to “Support the swift and coordinated implementation of the Two Pillar Solution, coordinating with regional and international organisations”

On the face of it, all pretty much good news. But it’s interesting to read the views of those people who specialise in this field and there still seems to be quite a bit of uncertainty about whether in fact this whole thing will come to fruit.

In the meantime, for example, you’ve got lobbying going on in the United States. And it appears now that the US has managed to secure a further delay in the implementation of the Pillar Two global minimum tax 15% until 2026, according to a report coming out of the United States.

Pillar Two is the key proposal, because it applies to companies with annual revenues in excess of €750 million. Apparently, the US Treasury Department has managed to negotiate a delay in the implementation of this. It has got people watching all around the world as to what’s going on. It also means that the in the background, digital services taxes, for example, could still be ready to be deployed or introduced by jurisdictions if they feel that Pillar Two isn’t making enough progress and they want to secure their revenues. [Under the agreement just announced countries have agreed to hold off imposing “newly enacted” digital services taxes until after 31st December 2024.]

Overall, it’s a bit of a shuffling: one step forward, maybe half a step sideways and a quarter of a step back. In other words, progress is slow, but it’s still inching the way forward. Ultimately, it comes down to watching what happens in the United States and the lobbying goes on. If there’s a change of President next year all bets will be off at that point, I would say.

Smith, banged to rights, again. But should Companies Office be in the gun?

And finally, this week, the murderer and escapee, Philip John Smith, who’s been in jail since 1995 apart from the brief time he escaped to Brazil has now been sentenced to further two years imprisonment on tax fraud charges.

He was convicted for dishonestly using documents intending to gain pecuniary advantage, firstly, a application under the Small Business Cashflow Scheme and then for filing 17 false GST returns and a false income tax return. in total the attempted fraud was just over $66,000 of which was actually paid $53,593. He’s also been ordered to pay full reparations on that amount.

What he did was between October 2019 and March 2020, he registered five companies with the Companies Office with shareholders and directors, who were friends, associates or third parties unknown to him. He then he set up and activated myIR accounts for each company.

But Inland Revenue was quite quickly onto him, it seems, because it apparently detected the fraud involving the Small Business Cashflow Scheme in June 2020 only a few months after it started operating in April. So good quick work by Inland Revenue.

But the case also raises the point which an associate I bumped into this week mentioned, and that’s the actions (or inaction) of the Companies Office in allowing those five companies to get set up. New Zealand scores highly for ease of business in establishing companies. Many times, whenever I’m talking to overseas people, they are remarkably impressed about how quick it is to set up a company in New Zealand.

The question arises if people setting up companies by going directly through the Companies Office website, is it a little bit too easy? Was an opportunity to pick up Smith’s attempted fraud missed at that point by Companies Office? We don’t know. Accountants and lawyers are subject to the current anti-money laundering legislation, so we need to pay attention to what’s going on with company registrations and we have to obtain proof of ID. But my understanding is this process is a little less rigorous when you go directly through the Companies Office.

So good work by Inland Revenue picking it up quickly and catching Smith, again. But maybe some questions should be asked as to whether he should ever have been able to get that far along the line and that Companies Office should have picked it up sooner.

And finally, congratulations to the Football Ferns for their magnificent win last night at the start of the FIFA Women’s World Cup. I was lucky enough to be at Eden Park, which is why I might sound a little hoarse today! It was fantastic to experience such a great occasion even if the final nine minutes seemed like an hour. Congratulations again to everyone involved. Football definitely was the winner on the night!

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Greens announced their tax proposals a week ago, last Sunday.

And my reaction was, “These are very bold.” They proposed major tax cuts at the lower end, meaning 95% of taxpayers will be better off under the Greens. Those cuts are paid for by increasing the top tax rate to 45% and increasing the 33% tax rate to 35% as well. These increases are part of the trade-off for the proposed nil rate band of $10,000, which no doubt will be very popular. As is well known, many other jurisdictions have something similar and given the fact that nothing has been done in relation to indexation of thresholds for well-nigh 13years now, it’s unsurprising that the pressure is built up, particularly at the lower end, to change the tax rates.

But most of that got swept away by the Greens controversial wealth tax proposal. In summary, there are two parts to it. Any individual whose net assets, net of mortgages for example, exceed $2 million will be subject to a wealth tax of 2.5% on the excess. For family trusts there is no nil rate band or threshold at all. It’s a flat 1.5% which is a deliberate anti-avoidance mechanism.

Latest Inland Revenue data on trusts

Trusts were used to avoid the impact of estate and gift duties in the past and are used in other jurisdictions to mitigate the impact of wealth and estate duties. So, the Greens have targeted this avoidance. Coincidentally, last Saturday the New Zealand Herald published a piece including details of the trust tax return filings made to Inland Revenue for the year end 31st March 2022 which indicated the value of assets held in trusts. The net assets of the 201,100 trusts which reported, was just over $300 billion. So at 1.5%, theoretically that’s $4.5 billion dollars straight up there.

Incidentally, what that Inland Revenue report doesn’t show is the non-reporting trusts, those are likely to be quite significant. We really don’t know how many trusts there are in New Zealand, the best estimates are somewhere between 500,000 and 600,000. Many of the non-reporting trusts don’t do so because they have no income, but they hold assets such as the family home. So, family homes that have been held in trusts may now be subject to the Greens’ proposal.

Now this kicked off quite a storm, which I watched with a little bemusement because the Greens first of all have to put themselves in a position of such leverage that its coalition partners, almost certainly Labour and Te Pati Māori, agree to the proposal. And then somehow between 14th October, the date of the election, and 1st April next year, the legislation to introduce all of this is drafted and passed through Parliament. So ,it’s a big challenge ahead.

But it caused quite a stir, and I fielded several calls from people concerned about what they saw here, trying to get an understanding about it and my views on it. At our Accountants and Tax Agents Institute New Zealand’s regional meeting on Tuesday we had a very lively debate around the question of this wealth tax. Normally, a lot of the time we’re talking about what’s in the legislation and whether Inland Revenue ever answer their phones again. All this I think shows the impact of the proposals, even though in theory they affect only a small group of people, the top 1%.

But there is substantial wealth locked up in property. We know that from digging around the official figures. For example, Auckland Council estimates the rateable value for all property within the Auckland Council region will be over one trillion dollars as of 30th June. Obviously, not all of those would be subject to a wealth tax.

What’s being suggested by other parties?

But I thought it was interesting that people are taking the Green’s proposals very seriously. The income tax shift to 45% on income over $180,000 won’t be terribly popular. But at present, the proposals that they’ve put out for the income tax cuts would affect many more people and benefit many more people, all those earning under $125,000, which is something like just over 4 million people. This has a broader impact than either National or Act’s proposals.

It’s quite interesting now as the election comes ever closer, we can start to see the tax policies of the various parties taking shape. The Greens are raising a substantial amount of tax to deal with poverty. Act is proposing tax cuts and it’s taking the ideologically opposite approach of substantial cuts to spending in order to achieve its top rate of 28%.

TOP, The Opportunities Party, are putting out a policy which has a land value tax, and they also propose tax increases at the higher end together a nil rate band and also substantial tax cuts at the lower end.

We haven’t yet heard from Labour on what they would do. Over on Twitter @binkenstein put together a graph comparing the various parties’ proposals so far.

So, the debate has ramped up quite a bit. Obviously, the Greens wealth tax is the most controversial part of it, but the other part which really got very little commentary but is equally controversial, was a proposal to raise the income tax rate for companies from 28% to 33%. More than most of the Greens’ proposals, that would probably produce a certain frisson of tension amongst multinationals. They may look and think “Maybe we might not increase our activities in New Zealand” or they may ramp up what they try and do under profit shifting.

Anyway, it all made for a very lively discussion all round. As I told people, wait and see. But it is interesting to see the pressure point for those are likely to be affected around a wealth tax.

What does the IMF think?

With almost impeccable timing, the IMF, the International Monetary Fund, were in town and it suggested that maybe it was time for a capital gains tax.

The Concluding Statement of the 2023 Article IV Mission noted:

Well-designed tax reform could allow for lower corporate and personal income tax rates by broadening the tax base to other more progressive sources, such as comprehensive capital gains and land taxes, while also addressing fiscal drag and improving efficiency.

It’s not the first time the IMF has suggested changing the tax system. They did so in 2021. In fact, there’s a regular pattern of the IMF and/or the OECD coming here looking around saying, “Well, guys, the country is in good shape, generally government policy is pretty sound, but you need to do something about capital gains taxes.” Regardless of whichever party is in power the Government’s reaction is quite funny. They like the bit about everything being under control. But at the mention of capital gains tax, they all throw up their hands in horror. And yet, as we know all around the world, capital gains taxes are a common feature of tax policy.

The Crypto-Asset Reporting Framework, the latest expansion of the Common Reporting Standards

Now, the Greens wealth tax proposal will probably be music to the ears of the French economist Thomas Piketty, who has proposed a global wealth tax, as one of the core points of his monumental work, Capital in the 21st Century. And at the time of publication in 2014, the opportunities for that global wealth tax to ever eventuate were probably just about zero or maybe marginally above zero.

But since then, we’ve had the introduction of the Common Reporting Standards which I think is actually revolutionising the tax world quietly because an enormous amount of information sharing is now happening on. We know from what’s been reported under the Automatic Exchange of Information that there’s something like €11 trillion held in offshore bank accounts. The Americans have got their FATCA, the Foreign Account Tax Compliance Act, and as a result of that, they know that American citizens have got maybe US$4 trillion held offshore.

Now, the latest part of the Common Reporting Standards is extending the framework to crypto-assets and I talked about this last year when the proposals first came out. Those proposals have now been finalised and the Crypto-Asset Reporting Framework is now in place. There have also been some amendments to the Common Reporting Standards. I’m going to cover all these changes in a separate podcast because I think they’re worth looking at in a bit more detail.

The tightening noose of information exchange

But the key trend in international taxation that’s going on, which I think is going to have a long-term impact around the world, and particularly for tax havens, is this growing interconnectedness, the sharing of information that goes on between tax authorities through mechanisms such as the Common Reporting Standards. I asked Inland Revenue about what information they had been supplied under the CRS in relation to the numbers of taxpayers and the amounts held in overseas bank accounts. Inland Revenue turned down my Official Information Act request on the basis that much of this is obviously confidential, but also would be compromising to the principles under which the information is shared.

Now, I’m not entirely sure about that. I think the more openness we have about what is being shared, the better the likelihood of tax enforcement once people cotton on to what’s happening. They will not think “Yeah, well, I’m just going to leave it over in the UK or the US or wherever, and Inland Revenue will never find out.” My view, as I tell my clients, is they always find out and they know much, much more than you can imagine.

And outside of the CRS there appears to be a regular exchange of information about property purchases between the United States Internal Revenue Service and Inland Revenue here. So be advised, the Crypto-Asset Reporting Framework is just the latest in a building block of international information exchange.

The Auckland Budget – what about climate change?

And finally, the Auckland budget got signed off last week. I’ve been in the press disagreeing with the sale of any part of the Auckland airport shares, and I still stand by that. I think it’s a short-term fix for a long-term problem, but that’s now done and we move on.

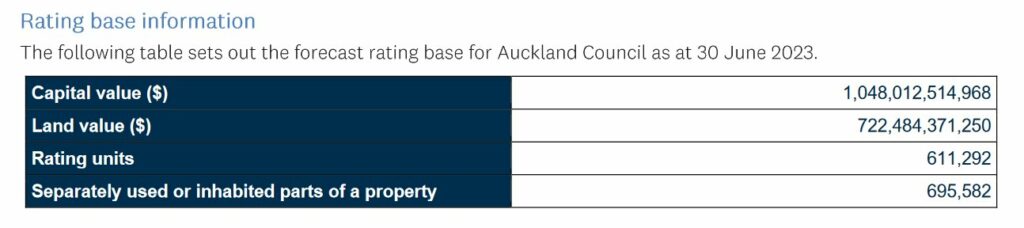

What I did think was quite surprising as you delve into the budget is some of the numbers that come out. As I mentioned earlier, the rating base for Auckland and according to the Auckland Council’s documents is over $1 trillion.

But the thing that really surprises me, which wasn’t addressed in the budget so we’re going to have to address it next year, is the question of climate change. Towards the end of the process, the Government announced that in the wake of Cyclone Gabrielle 700 homes around the country are too risky to rebuild. The Government and councils will offer a buyout option to those property owners.

400 of those are in the Auckland region and apparently it doesn’t also take into account what is going to have to happen out at Muriwai because of the slips and the dangerous cliffs over there. As Deputy Mayor Desley Simpson pointed out, “If you say it’s 400 [Auckland homes] times $1.2 million, give-or-take just like the average house price, you’re talking half a billion dollars.”

The question arises how is that split between Auckland ratepayers and the rest of the country? Yet there was nothing in the Auckland budget about this, and that’s just this year’s damage. What happens if we get another Cyclone Gabrielle, next year?

We’ve got an interesting scenario developing where we’re talking about reducing emissions and we’ve got a distant horizon 2030 or whatever farmers and other parties want to extend it to. But in the meantime, we are picking up the bill now for increased damage and we don’t seem to be thinking in terms of how does that affect our taxes and rates? And this is going to be an ongoing issue. So, the question of paying for that, whether it’s a wealth tax, capital gains tax, whatever, is going to become ever more present, in my view.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Green Party quotes Margaret Thatcher with approval

The Australian Tax Office’s latest corporate tax transparency report

The latest from the OECD on the carbon pricing of greenhouse gas emissions

Last week, the Green Party released a discussion document on what it’s called an excess profits tax. This is part of its “commitment to a progressive and fair taxation system.” What it is saying is that an excess profits tax or windfall tax is required to level the playing field so that, “big businesses are not able to profit to excess when so many people are struggling”.

The proposal comes on the back of data showing that in the 2021 financial year, corporate profits reached $103 billion, up $24.5 billion on the previous year. And you’ll recall that the corporate tax take for the year to June 2022 was almost $20 billion. The Green Party are saying we’ve got several matters going on at the moment. It believes there are excess profits being earned at a time of hardship. There’s also a need to address the impact of the unprecedented transfer of wealth that happened in response to the COVID 19 pandemic.

The discussion document points out that windfall taxes are common in other countries. It notes that the EU is implementing an excess profit tax in the energy sector. Spain has an excess profit tax on the energy sector and banks. Interestingly, the paper then uses the example of Britain under Margaret Thatcher in 1981, when the Conservative government introduced a windfall tax on banks. This was raised the equivalent of about £3 billion in today’s money and represented about a fifth of the profits banks were pocketing at the time.

That obviously attracted quite a lot of controversy back in 1981. The 1981 British budget is one of the most controversial I can recall in my time. But Thatcher was unrepentant about what she did. In her memoirs The Downing Street Years, she responded

“Naturally, the banks strongly opposed this, but the fact remained that they had made their large profits as a result of our policy of high interest rates rather than because of increased efficiency or better service to the customer.”

So, I guess we live in strange times when the Green Party is quoting Margaret Thatcher with approval, but that is a fair point. And bear in mind ANZ reported a net profit of $2 billion for the first time.

So, windfall taxes are not uncommon elsewhere in the world. They are uncommon under the New Zealand tax framework and haven’t really been used for a very long time. They were used during both world wars but apparently, they weren’t entirely successful.

It’s good to get this discussion going because sometimes I feel that the tax debate in New Zealand is very narrowly circumscribed. We’re living in unusual times so is a windfall tax something that could be done? Even if it was, in my view it would have to be a one-off, such taxes shouldn’t be part of the regular tax take. Incidentally, this is a point I’ve seen discussed elsewhere notably in Ireland following the release of a report about its tax system.

The Green’s proposal suggests a windfall tax could have some retrospective effect. This would be highly unpopular and rightly so, for companies, because it would mean there’s no certainty around their planning. Companies might budget for a 28% tax rate but then suddenly find that in fact it’s been increased to 33%. So businesses would find that hard to deal with, but if they knew there was a possibility it would be interesting to see how pricing might play out.

Overall it’s good to see this discussion going on and no doubt it’ll attract a lot of controversy and you can make your own submission on the idea to the Greens. Next year is an election year so who knows what’s going to happen afterwards? But as I said, windfall taxes are used elsewhere in the world. And if they were good enough for Margaret Thatcher, well, who knows?

Aussie ‘transparency’

Moving on, over in Australia, the Australian Tax Office, (the ATO) has just published its eighth annual report on corporate tax transparency. What this does is look at the amount of tax paid by large corporates for the year to June 2021. According to the report, the over A$68 billion paid during that year by large corporates is the highest since reporting started. It’s up A$11 billion or 19.8% on the previous, COVID-19 affected year. Apparently, rising commodity prices were a key driver for the increase in corporate tax.

The report notes that Australia has some of the highest levels of tax compliance of large businesses in the world, with 93% of tax paid voluntarily. This rises to 96% after the ATO has asked a few questions.

The ATO has been running what it calls the Tax Avoidance Taskforce for some time. According to the report since 2016, the ATO has raised tax liabilities of $29 billion and Tax Avoidance Taskforce funding being responsible for $17.2 billion of that amount. (It’s worth remembering “raised liabilities” doesn’t necessarily mean that they’ve been collected). In last week’s Australian Budget there’s an extra $200 million per annum to help expand the focus of the Tax Avoidance Taskforce. This brings the total funding for the Tax Avoidance Taskforce to A$1.1 billion over the next four years.

Now, this report covered 2,468 corporate entities, more than half of which were foreign owned with income of A$100 Million or more. 529 or about 20% were Australian owned private companies with an income of $200 million or more, which is an indication of the size and scale of the Australian economy. Interestingly, there’s a note that the percentage of entities which pay no income tax was 32%.

It’s interesting to see what other jurisdictions do with their tax data. I feel Inland Revenue should do a lot more in this space with the data it receives, but it’s very reluctant to do so at this point. It’s currently not part of its brief, but such a report and other statistics gives us a better understanding of the scale of the economy and what’s happening in it. I would like to see Inland Revenue produce something similar.

Energy, taxation and carbon pricing

Finally, this week, overnight the OECD released its latest report on pricing greenhouse gas emissions. This looks at how carbon prices, energy prices and subsidies have evolved between 2018 and 2021. This is part of a database the OECD is developing to track what’s happening on energy, taxation and carbon pricing.

This report covers 71 countries (including New Zealand) which together account for approximately 80% of global greenhouse gas emissions and energy use. There’s a summary report by country as well. Overall, more than 40% of greenhouse gas emissions in 2021 were covered by carbon prices and that’s up from 32% in 2018. And the average carbon price from emissions trading system schemes and carbon taxes more than doubled to reach €4 per tonne of CO2 equivalent.

And obviously the report goes into what’s happening across the across the globe. There’s been a rise in the amount of greenhouse gas emissions now covered, and that is as a result of the introduction or extension of explicit carbon pricing mechanisms notably in Canada, China and Germany.

What’s termed carbon net prices are rising further in 2021 as have permit prices under emission trading schemes. There’s steady changes in carbon taxes, with new carbon taxes introduced, together with increases in carbon tax rates or the phasing out of carbon tax exemptions.

As for New Zealand, 44.1% of all greenhouse gas emissions are now subject to a positive ‘Net Effective Carbon Rate’ which has not changed since 2018. The report also notes that fuel excise taxes, which are described as an implicit form of carbon pricing cover 23.8% of emissions. Again, that’s unchanged since 2018. So, looking at this, we appear to be stalling a bit on this and I do wonder whether next year’s report might show that because of the cut in fuel excise duty, we’ve gone backwards. However, other countries have also been cutting fuel taxes because of the high inflation in the wake of the war in Ukraine.

Although the level of coverage of greenhouse gases covered by carbon pricing hasn’t changed since 2018, the average carbon price has risen. For example, fuel excise taxes in 2021 amount to €19.73 per tonne of CO2 equivalent. That’s up by +9.4% relative to 2018, which is probably below inflation, though. However, once adjusted for inflation the average Net Effective Carbon Rate on greenhouse gas emissions has increased by +39% since 2018

There’s a lot to consider in this report, more than I’ve had a chance to go through right now. But again, it reflects a constant theme of this podcast about the increasing role of environmental taxation and the scope for opportunities in this space.

What we do with those funds is the other side of the equation. It’s one thing to say we need more taxation. What isn’t always debates is what we do with those taxes. I’ll repeat my longstanding view that funds coming out of environmental taxation in the form of new taxes or the existing emission trading scheme should be used to mitigate the impact of climate change.

There was a report earlier this week identifying 44 communities in great risk of environment impact from climate change which are unprepared for the flood risk. No doubt they will be looking for assistance. In the meantime, Nick Smith, Nelson’s new mayor (and former Environment Minister) has requested government assistance with dealing with the impact of the recent flooding. No doubt there will be plenty more to come on this topic.

The OECD proposes a crypto-asset reporting framework

New levy proposal for farmers’ greenhouse gas emissions;

TOP’s bright idea about tax rate

Last week, the OECD launched its Crypto-Asset Reporting Framework (CARF). This is a response to a G20 request that the OECD develop a framework for the automatic exchange of information between countries on crypto-assets. In other words, it is going to be a development of the existing Common Reporting Standards on the Automatic Exchange of Information or CRS. The CARF was presented to G20 Finance Ministers and Central Bank Governors for discussion at their meeting this week in Washington D.C.

The proposed rules cover four areas:

the scope of crypto-assets to be covered,

the entities and individuals subject to data collection and reporting requirements,

the transactions subject to reporting as well as the information to be reported in respect of such transactions and

the due diligence procedures to identify crypto-asset users and controlling persons and to determine the relevant tax jurisdictions for reporting and exchange purposes.

CARF is intended to complement the CRS and mean that crypto-assets will be subject to automatic exchange of information reporting. Now the reason that that has come up is unsurprising really. Individuals holding wallets which are not affiliated with any current financial institution or service provider, and are therefore then able to transfer crypto-assets across jurisdictions. As the OECD report notes:

“this presents the risk that relevant crypto-assets are used for illicit activities or to evade tax obligations. Overall, the characteristics of the crypto asset sector have reduced tax administrations visibility on tax relevant activities carried out within the sector, increasing the difficulty of verifying whether associated tax liabilities are appropriately reported and assessed”

This is a very long way of saying there’s probably a lot of tax evasion going on in the crypto-assets sector.

CARF is therefore an obvious response. It is also part of the huge ongoing trends in the modern tax world of the acceleration in reporting and exchange of information between jurisdictions. This is a very, very significant development in the tax world that happened in the wake of the Global Financial Crisis and has largely gone unreported in the wider press although it appears to be generally accepted by the public. When you align this alongside what’s happening with the Pillar One and Pillar Two proposals, then the days of tax havens where money can be parked outside the tax net of major jurisdictions, are numbered.

So what crypto assets are covered? Well, the definition is pretty broad, it targets assets “that can be held and transferred in a decentralised manner and without the intervention of traditional financial intermediaries”, i.e. banks and other financial institutions. This includes stablecoins, derivatives issued in the form of crypto-assets and certain nonfungible tokens.

There are three categories excluded from what’s termed “Relevant Crypto-Assets”:

crypto assets, where have it’s been determined they cannot be used for payment or investment purposes,

Central Bank Digital Currencies which represent a claim in Fiat Currency on an issuing Central Bank or monetary authority, which function similar to money held in a traditional bank account,

Specified Electronic Money Products that represent a single Fiat Currency and are redeemable at any time in the same Fiat Currency. (Not sure I’ve encountered any of these myself, to be honest).

Reporting entities are any intermediary or service provider which is facilitating exchanges between relevant crypto-assets or between relevant crypto-assets and fiat currencies. Generally, they will be subject to the reporting requirements of the jurisdictions in which they are either tax resident or have a regular place of business or branch through which they carry out reportable transactions.

Keep in mind, CARF ties in with the CRS which is already hugely comprehensive and covers most of the main tax jurisdictions and tax havens. The ability for crypto asset service providers to slip out from underneath the CARF reporting requirements is going to be quite limited.

Three types of transactions are going to be reportable:

exchanges between Relevant Crypto-Assets and fiat currencies,

exchanges between one or more forms of Relevant Crypto-Assets, and

transfers of Relevant Crypto-Assets.

CARF has been developed to sit alongside CRS and in fact at the same time the OECD carried out its first comprehensive review of the CRS regime. It’s proposing some amendments to bring new financial assets, products and intermediates within the scope of CRS. The changes are also being made to try and avoid duplicate reporting with that which is expected to happen under CARF.

The entire CARF framework runs to over 100 pages. It should be signed off subject to any further work requested by the Central Bank Governors and Finance Ministers at their meeting this week. There will no doubt be some further tweaking, so it’s not yet all set to go. No doubt there will also be some lobbying for changes in the regime.

CARF is, as I said earlier, part of a growing trend for international cooperation on the sharing of information. When implemented it basically will probably mark an end, or certainly a restriction, on the use of crypto assets for tax evasion and other nefarious purposes.

Making farms pay

On Tuesday, the Government released its proposals for how to price agricultural emissions.

These are in response to the recommendations earlier this year from He Weka Eke Noa, the Primary Sector Climate Action Partnership, for a farm level pricing system. The Climate Change Commission, He Pou a Rangi, also provided separate advice on agricultural emissions.

The Government’s proposals try and integrate what He Weka Eke Noa and He Pou a Rangi have suggested. The intention is to price agricultural emissions at the farm level. But it comes with a big stick – if the sector cannot reach agreement by 1st January 2025, then agricultural emissions will be be priced under the Emissions Trading Scheme.

The key part of the proposal is a farm level split gas levy to price agricultural gas emissions. It will apply to farmers and growers who are GST registered and meet certain livestock and fertiliser use thresholds. There would be separate levy prices set for long lived gases and biogenic methane and these will be set up after advice from the He Pou a Rangi and in consultation with the agricultural sector and iwi and Māori.

The long-lived gases (basically carbon) price will be set annually and then linked to the New Zealand Emissions Trading Scheme unit price. There’s a separate biogenic methane levy which will be adjusted based on progress towards domestic methane targets. One of the feedback matters the Government is seeking is whether that methane levy price should be reviewed annually or every three years.

With regards to the revenue raised, the Government proposes it that the revenue is used to fund incentives and sequestration payments, with any remaining revenue to fund the administration of the pricing scheme and a joint government and Māori revenue recycling strategy. There’s a proposal for incentive payments for a range of on-farm emissions reduction technologies and practises. I fully endorse this policy of using funding from an environmental tax to help the transition.

But if you’ve been watching this, you’ll know it has taken a long time to get here. It’s almost 20 years since the infamous ‘Fart tax’ was first proposed and Shane Ardern MP drove a tractor up the steps of Parliament. So progress has been very slow on this, which I personally find very frustrating.

Here in the city, we need to be working on reducing our transport emissions. Rather ironically, on the same day of the Government announcement, Ruapehu Alpine Lifts went into voluntary administration. The ski field operation has clearly been affected not just by one very bad year and the effect of Covid. This is something that’s been building for some time.

We’ve also had the recent floods and damage reports coming out of Nelson where the insurance claims so far total $50 million. So change is happening all around us and my view is we are going to have to adjust to it and try and do something to reduce emissions as part of the global effort. We can’t rely on everyone else to do it for us.

TOP tackles tax bands

Finally, this week, there’s been a lot of talk about tax cuts ahead of next year’s General Election, particularly in the wake of the massive u-turn by the UK government over a proposed higher rate tax cut which has now resulted in the sacking of the Chancellor of the Exchequer (Finance Minister) Kwasi Kwarteng.

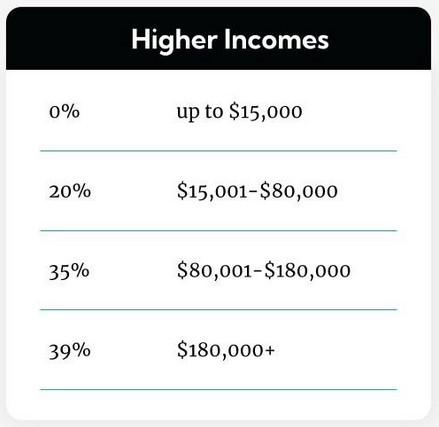

Amidst all of that chaos The Opportunities Party released its two-phase tax policy, phase one of which contains substantial tax cuts. But what caught my eye about TOP’s suggestion is their proposal to introduce a tax-free threshold of $15,000, together with adjusted tax thresholds.

Now tax-free thresholds are expensive, but they are seen around the world. Australia has one for the first A$18,200. The UK tax free personal allowance is £12,570 and America has a flat $12,000 exemption.

But what I thought is interesting about TOP’s proposal is they have looked at the question I’ve talked at length about what happens for low- and middle-income earners when their income crosses the current $48,000 threshold and the rate jumps from 17% to 30%. Under our current tax structure 12.5 percentage point jump is the highest such rate – the next jump at $70,000 is only from 30% to 33%.

So, I’ve been thinking for some time that we really ought to be looking at these thresholds and rate bands and maybe combining three into two, which is what TOP propose.

Now, TOP have got to either win an electorate or get across the 5% threshold before they’ll be in any position to propose their policy. (The second part of their policy would fund those tax cuts by a land value tax, which, of course, is longstanding TOP policy). We’ll have to wait and see until after next year’s election.

But if you want to hear more about what type of tax changes could happen and their implications then this week on RNZ’s The Detail podcast, Jenée Tibshraeny of the Herald and I spoke to Sharon Brettkelly about tax cuts here and in the UK, how our tax system works and what could be done if we’re helping people at the lower income level.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!