New tax bill drops.

- Insights on transfer pricing

- Inland Revenue comes knocking

This year’s main tax bill the Taxation Annual Rates for 2024-25 Emergency Response and Remedial Measures Bill was introduced by the Minister of Revenue, Simon Watts into Parliament last week. And as always with such an omnibus tax bill, there was quite a bit in it.

The one thing that wasn’t in there, which I was expecting, was a move by Inland Revenue to restrict the use of portfolio investment entities with a maximum rate of 28%. These are increasingly being used by trusts and individuals subject to the 39% top tax rate. I’ve had a feeling for some time that this might be something that Inland Revenue was looking at, and maybe this bill would see some action on that part. But nothing, so far.

Preparing for emergency events

Instead, there’s a number of key initiatives and a lot of remedial measures. The first key measure relates to developing a generic response to emergency events. This sounds pretty mundane but what’s intended here is to enable Inland Revenue to be quicker in responding to provide tax relief following any emergency events.

What’s proposed is to build in tax relief measures into the legislation, which then can be activated by an Order in Council. This has been something that Inland Revenue has had to do rather a lot recently. As the commentary to the bill notes there have been three national emergencies declared in the last 15 years, where Inland Revenue’s basically had to apply some discretion to provide some measures of tax relief. Those were the February 2011 Christchurch earthquake, the COVID-19 pandemic and then the flooding in the wake of Cyclone Gabrielle last year. Cyclone Gabrielle came hot on the heels of the Auckland Anniversary weekend flood. Then there was also a huge earthquake in Hironori Kaikoura in 2016, which was a local emergency.

This bill proposes to introduce primary legislation which will enable Inland Revenue in the wake of an emergency event to use an Order in Council to activate these measures so it can respond to the emergency event.

I think it’s a good move. The COVID response in particular, showed that there was a need for greater discretion for Inland Revenue in certain areas, and in fact the Finance and Expenditure committee suggested last year that some form of this measure was needed.

It’s a fact of the times that we need such a measure, and incidentally also supports my long-standing view that it’s climate change which is going to hit the balance sheets first, and we need to be responding to that.

Crypto-asset reporting framework

The Bill also introduces the legislation required to implement the Crypto-Asset Reporting Framework (CARF), an OECD initiative, which is planned to take effect from 1st of April 2026. From that date New Zealand-based reporting crypto-asset service providers would be required to collect information on the transactions of reportable users that operate through them. The providers would then need to report any information for the year ended 31st March 2027 to Inland Revenue by 30th of June 2027. And then Inland Revenue would exchange this information with other tax authorities to the extent that it did come across information that a user of a platform in in New Zealand was actually resident elsewhere.

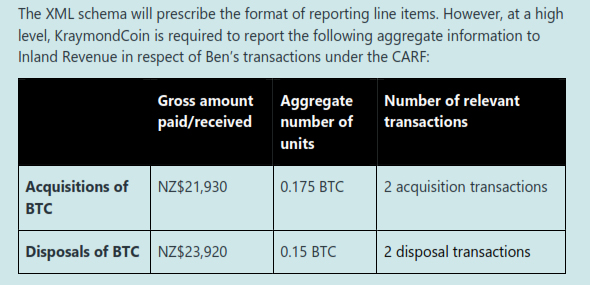

(Example of information reporting required)

As the commentary to the Bill notes, the market for crypto assets has grown enormously and there are now more than 22,000 crypto assets with a total market capitalisation of that is now close to NZ$4 trillion. This is up from barely US$17 billion back in 2017. According to the commentary between 6% and 10% of New Zealanders own some crypto-currency and Inland Revenue analytics show that 80% of crypto-asset activity by New Zealanders is undertaken through offshore exchanges.

There are some interesting notes in the accompanying Regulatory Impact Statement that once this is all up and running, Inland Revenue expects to be gathering about $50 million a year from it. In the meantime, a colleague has told me about a client who was using the Binance platform who has received some queries from Inland Revenue. The CARF initiative once implemented will boost Inland Revenue’s audit activities in this area.

Foreign superannuation scheme transfers – a good fix for a bad policy?

The next couple of measures relating to foreign superannuation scheme transfers and the Approved Issuer Levy are good to see, but also raise some interesting policy questions.

Under our current foreign superannuation scheme rules, if you transfer a foreign superannuation scheme into New Zealand or withdraw funds from the scheme (the money doesn’t necessarily have to reach New Zealand), you trigger a liability.

What has been an issue all along, particularly for Britons, is if they transfer their overseas scheme into a Qualifying Recognised Overseas Pension Scheme – or QROPS – they trigger a tax liability but may have no access to the funds, because they’ve not reached the age in which they’re allowed to do so under UK pension law. Any attempt to do so would trigger what’s called an unauthorised payments charge which could be up to 55%.

This was a problem that was identified with the legislation when it was first proposed back in 2013. Thanks in part to COVID, it’s taken this long to come up with a workable solution which is to kick in from 1st April 2026. From that date there will be a “Scheme Pays” option, under which the receiving scheme will calculate the tax due and pay that on behalf of the transferring client. The receiving scheme will do so at a flat rate of 28%, which is the prescribed investor rate. Transferring clients will have the option to fund the tax liability out of their own pockets, presumably because their marginal tax rate is 10.5% or 17.5%.

As I said, it’s a solution to a long standing problem. I am not a fan of the foreign superannuation scheme rules. It seems to me that we are taxing the importation of capital. People are bringing capital into the country and yes, they have benefited from an overseas tax regime. Conceptually, what we do ties in with our tax policy and in particular, the Foreign Investment Fund regime.

A ‘highly problematic’ regime?

But those of you who have been reading Dr Andrew Coleman’s recent articles will know our tax regime in relation to the taxation of savings is quite unique. I think in this area it’s highly problematic. People are bringing overseas savings and currency, into the country and we are essentially taxing them for that. Now looking at the bigger macroeconomic picture, that doesn’t seem to make a lot of sense to me. It’s conceptually correct from our taxation perspective, but it seems nonsense. This has always been my view, and I’ve still not received a satisfactory explanation other than “Well, that just fits in with our tax regime.”

My second point here is with the proposal for schemes to apply the prescribed investor rate at 28%. The Regulatory Impact Statement notes that on average the tax rate transfers is about 29%. Now the reason we tax foreign superannuation scheme transfers is so that people who have overseas pension schemes don’t have an advantage relative to their New Zealand counterparts, who would be in KiwiSaver funds, which as prescribed portfolio investment entities have a maximum prescribed investment rate of 28%.

Over taxation of transfers?

This begs the question as to why these transfers have been taxed at a person’s marginal tax rate which in some cases would be 39%. Surely if we are saying we’re looking to try and prevent a disadvantage, the top rate that should have been applied was 28%. That’s not discussed in the commentary or the Regulatory Impact Statement. But I will raise it in my submission to the Finance and Expenditures Committee and see what develops of it.

I was also interested to see the numbers of people that are affected by this seem to have been dropping off. According to the Regulatory Impact Statement, 2,700 individuals reported a foreign superannuation scheme withdrawal or transfer in the 2022 income year. For 2023 the number was 458 with 113 reporting the amount was mainly sourced from the UK. That’s quite a drop off.

The “Schemes Pay” solution has taken a long time to get here. I’ve been involved as part of the group that’s worked with Inland Revenue on this policy measure, so I’ll give it a qualified pass. But I still think the bigger issue as to why we are taxing these transfers in the first place really should be addressed properly.

Changes to the Approved Issuer Levy – fixing a problem but not addressing the cause?

Another good measure which also resolves a long-standing issue, involves the Approved Issuer Levy regime. Where a person pays interest to a non-resident lender, the payer is required to withhold non-resident withholding tax (NRWT). Alternatively, if the interest payments are being made to non-associated lenders, then you can register to apply to register the loan and instead deduct the 2% Approved Issuer Levy (AIL) and that’s what most people do.

According to the Regulatory Impact Statement about 1200 taxpayers are filing AIL returns paying AIL totalling $153 million for the year ended 30th June 2023. This represents annual interest of approximately $7.7 billion subject to the 2% AIL.

But some people haven’t registered the loan for AIL and the current rules are that they can’t register for AIL until they’ve paid the NRWT. The loan cannot be registered retrospectively. There’s an example in the Regulatory Impact Statement that one borrower had to pay $2 million in NRWT as a result. The proposal is to enable Inland Revenue to allow retrospective registrations.

Paying withholding tax on your mortgage interest

What has also emerged as an issue is that there are a number of individuals with overseas mortgages. They have moved here, but they’ve kept their overseas property and usually rented it. The UK and Australia are the two most common examples I’ve encountered. These persons are paying interest to the UK/Australian located banks on UK/Australian located properties because they have mortgages. These payments are also subject to AIL and NRWT but practically speaking it’s very hard to explain why AIL/NRWT is payable particularly when the payments are being made from an account situated in the UK/Australia.

This AIL proposal will deal with some of the problems around retrospective registration. But the question has not been asked as to whether in fact individuals in those circumstances that I’ve just described should in fact be within the scope of the regime, because that’s not why the AIL scheme was introduced.

It’s intended to help lower the cost of capital for New Zealand borrowers. As mentioned above in my view taxing foreign superannuation schemes seems to be taxing the importation of capital. This is contradictory to the purpose of the AIL regime. Both those positions can’t be correct in my view if we want to make it easier to access capital. In my view we should be changing the approach in relation to foreign superannuation schemes.

Rant aside, allowing retrospective AIL registration is actually a welcome move. The bigger question still remains as to whether in fact individuals with overseas mortgages should be within the regime. As the Regulatory Impact Statement notes, we don’t really know what’s the impact for individuals. It’s pretty near minuscule overall and there’s probably more non-compliance than the Regulatory Impact Statements acknowledge.

A hefty dose of remedials…

Another policy measure is to increase the exempt employee share scheme threshold. The maximum value of market shares that can be offered will be increased from $5,000 to $7,500 with effect from 1 April 2024. Finally, there are a large number of remedial measures relating to GST, trustee tax rate changes, partnerships, land tax rules, international tax and sundries. These often pop up in tax bills, just tidying up inconsistencies in legislation.

Submissions are now open and close on 18th October.

Insights from ten years of Inland Revenue’s transfer pricing questionnaires

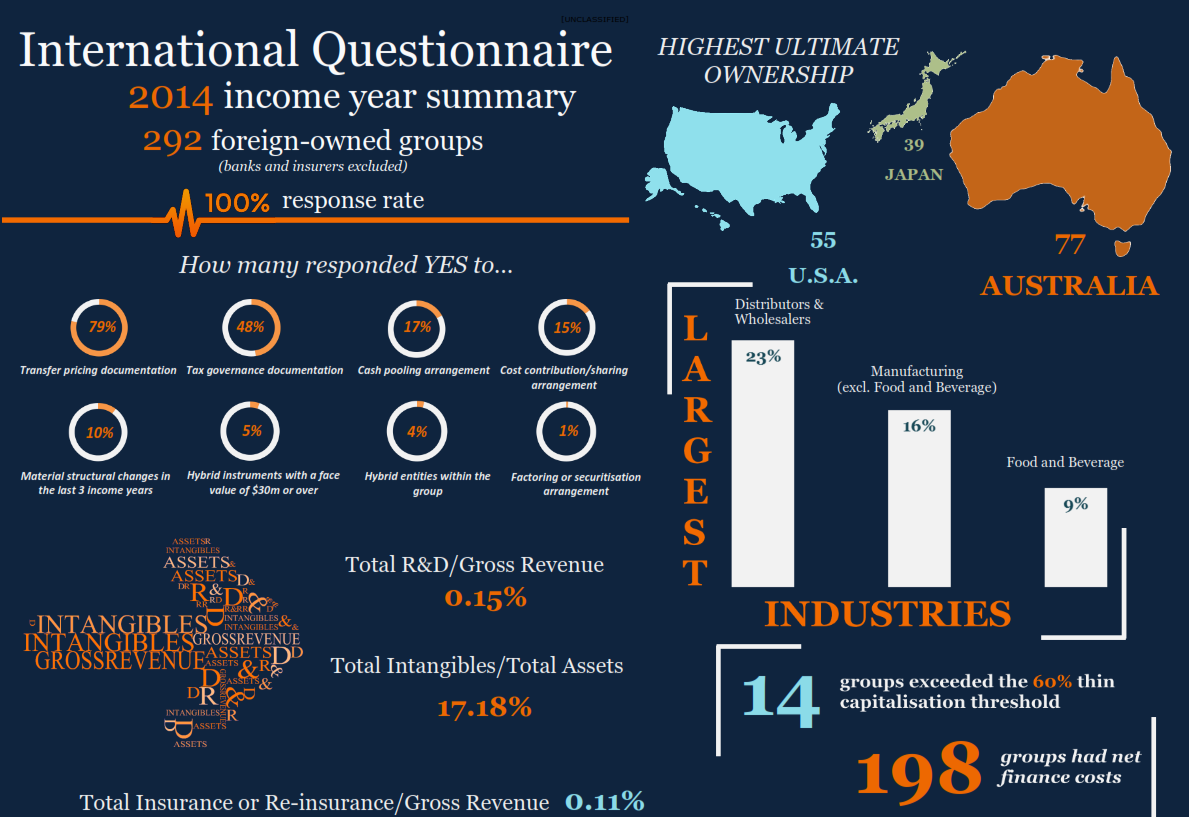

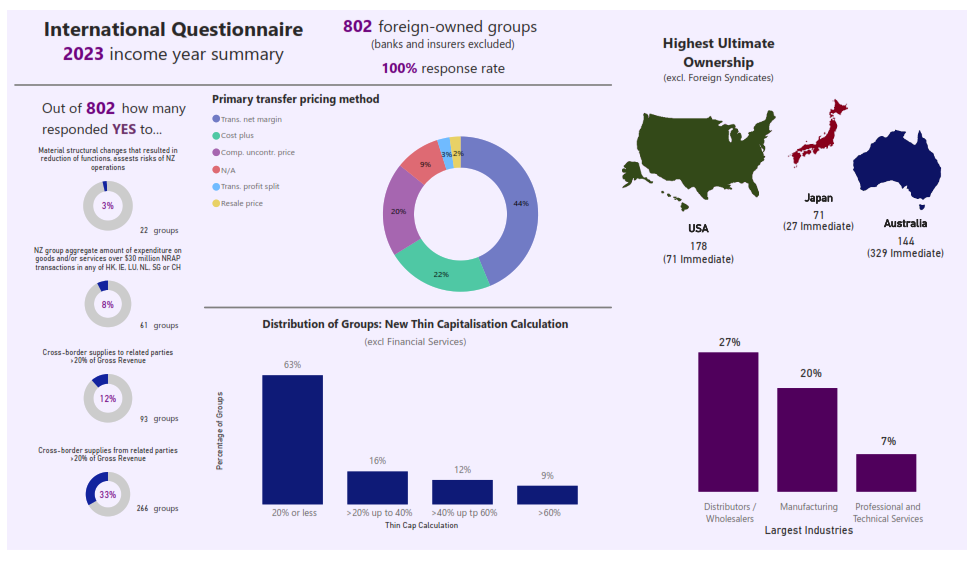

Every year Inland Revenue issues an international questionnaire designed to collect key information about financing debt and transfer pricing issues in regard to foreign owned businesses in New Zealand. The data request for 2023 was sent out in February 2024 and responses were required by 15th April 2024. These questionnaires generally target foreign owned groups with turnover exceeding NZ$30 million.

What’s happened is Inland Revenue’s now published a summary of the answers it received covering the10 years from 2014 to 2023 inclusive. There are some interesting little details in here. In both 2014 and 2023 years, the three countries with the highest ultimate ownership were Australia, Japan and the United States. In 2014 there were 292 foreign owned groups (excluding banks and insurers), 77 had ultimate ownership in Australia, 55 in the USA and 39 in Japan.

Flip forward to 2023 and there are now 802 groups. The top three were still the same, but the order has changed. In that now the United States with 178 groups is the country with the highest ultimate ownership Australia has 144 and Japan 71.

There’s also questions about how many groups are subject to our thin capitalisation rules which kick in where the debt to asset ratio exceeds 60%. In 2023, nine percent of the groups – that’s about 75 – would be subject to some form of interest restriction.

Back in 2014, that was much smaller. Only 14 of the 198 groups that had net finance costs were subject to thin capitalisation. That’s quite interesting because it shows that more debt has been taken on board by foreign owned groups over the ten year period.

I’m always interested to see data like this from Inland Revenue as it gives us insights into the shape of our economy.

“Who’s that knocking on the door?”

And finally, this week a reminder that Inland Revenue has upped the ante in terms of debt collection and just general enforcement across the board. I mentioned earlier on about the taxpayer who had received an inquiry in relation to their Binance account. This week RNZ ran a story about instances where Inland Revenue have actually been out door-knocking and making physical visits to people who owe them debt. It’s something we haven’t seen for about five years. Inland Revenue seemed to have dropped off using this practise prior to COVID and obviously COVID then had a huge operational impact.

Inland Revenue re-engaging in this process is to be honest welcome. You do get the sense that certain taxpayers just push the envelope and think they’ll get away with it. So, it probably was a big shock for them that Inland Revenue can actually turn up on their doorstep and say “Hey, we’d like to talk to you about your debt.” As I’ve said before we’re going to see more of this increased enforcement.

Coincidentally, but I haven’t time to cover it this week, Inland Revenue also released drafts for consultation, updating its operational statements in relation to the use of its (very) extensive search powers. That’s probably something maybe I’ll get a chance to cover later, but for now, that’s all for this week.

I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.