The just concluded UK general election was the first general election held in July since 1945, when coincidentally the Labour Party also won by a landslide ending Sir Winston Churchill’s wartime prime ministership. Before he became Prime Minister again in 1951, Churchill started writing his monumental six volume history of the Second World War, the first volume of which was titled The Gathering Storm.

And if you’ll pardon the somewhat laboured analogy, this is very much what’s happening with Inland Revenue at the moment. There’s a very clear gathering storm approaching as Inland Revenue pulls together and beefs up its investigation resources. We saw signs of this a couple of weeks back with its commentary about targeting smaller liquor outlets. Now last Wednesday, an Inland Revenue media release announced it is “honing in on customers who are actively dealing in crypto assets but not declaring income from them in their tax returns.”

By way of background, back in 2020, Inland Revenue updated its guidance on the tax treatment of crypto assets. Clearly that was part of a plan to follow through and check on who was trading and investing in crypto but not reporting the income. However, first COVID and then the cost-of-living crisis got in in the way of Inland Revenue’s intentions to follow through up its guidance.

Targeting non-compliance

But those immediate crises have passed now, and it appears that Inland Revenue has been busy investigating potential non-compliance because according to the media release late last year, it wrote to “a group of high-risk customers and gave them the chance to fix any non-compliance issues before facing audit.” This is a standard tactic of Inland Revenue. It basically puts it out to taxpayers without being too specific that it is aware of potential non-compliance and “invites”, that is the terminology used, the taxpayers involved to come forward and make a voluntary disclosure. If the taxpayers do so, then the potential to be charged shortfall penalties is likely to be greatly reduced.

Following on from these “invitations”, the next stage if the taxpayers don’t come forward is directly targeted follow up action. This appears to have just happened, as Inland Revenue is saying it has “just sent another round of letters to those Inland Revenue believes are not complying.

According to Inland Revenue it has data which has enabled it to identify “227,000 unique crypto asset uses in New Zealand undertaking around 7 million transactions with a value of about $7.8 billion.” There’s a potentially sizable sum of tax on the line here.

Pay up, or else…

The media release continues with a rather veiled threat

“Cryptoasset values have reached new highs, so now is a good time for people to think seriously about tax on their crypto asset activity. The high value also means customers are well positioned to pay their tax for the 2024 tax year and earlier.”

In other words, Inland Revenue is saying as values have recovered that means taxpayers can’t plead poverty when it comes to paying the tax due on their profits.

The media release goes on to explain something that we’ve said frequently; Inland Revenue has more data available to it than people realise.

“We want customers and tax agents to know that we are stepping up our compliance activity for customers with cryptoassets. Despite popular thinking – people are not invisible on blockchain and we have the tools and analytics capabilities to identify and expose cryptoasset activities.”

So there it is, very clearly stated ‘We know more than you think we know and we are coming for you.’ Part of this, by the way, is that New Zealand and therefore Inland Revenue has signed up to the new Crypto-Asset Reporting Framework (CARF) recently developed by the Organisation for Economic Cooperation and Development. This is yet another example of the growing international cooperation on the exchange of information, a regular topic on this podcast.

Under CARF the first set of reporting is due to apply from the 2026/27 tax year which will lead through to increased tax revenue. In fact, according to the Budget, the expectation is that CARF will deliver $50 million of additional tax revenue in the June 2028 year..

That’s in the future. What’s happening right now is that Inland Revenue has used its existing network of information exchanges and data sharing almost certainly by tax treaty partners such as Australia, the UK and the US, to obtain data about transactions carried out by New Zealand based crypto-asset investors and traders. It’s now going to put the squeeze on those it considers non-compliant.

It’ll be interesting to see what comes out of it and we will watch with interest and bring you news of developments. In the meantime you have been warned and this is of course the latest sign of the gathering storm of Inland Revenue investigations.

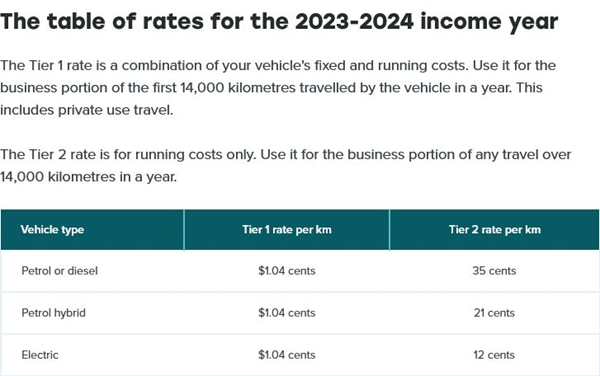

Inland Revenue kilometre rates for 2023-24

Moving on, Inland Revenue has just published its kilometre rates for the 2023-2024 income year. Unsurprisingly, given the recent rise in fuel prices, the so-called tier one rates show an increase in vehicle running costs that are allowable for the year. These rates may be used to calculate the deductible running costs for a vehicle.

Note that the Tier 1 rate of $1.04 for the first 14,000 kilometres applies to all vehicles whether petrol, diesel, hybrid or electric. The Tier 2 rates above the first 14,000 km DO vary between vehicle type.

This is good to know, but I do wonder whether it might be a bit more useful to have this sort of information earlier in the relevant tax year. Inland Revenue obviously wants to be accurate, but a different approach perhaps might be to adopt an interim rate and index that for inflation. Anyway, these are the rates that are now applicable for the 2023-24 tax year if you wish to claim the relevant deduction.

Are we raising enough tax?

And finally, this week, the Tax Policy Charitable Trust held an event on Thursday last night to announce its four finalists for this year’s Tax policy scholarship prize. The first half of the event was a panel discussion on New Zealand’s tax revenue sufficiency. Ably chaired by Geof Nightingale, a member of the last two Tax Working Groups, the four panellists that joined him were Talia Harvey and Matt Wooley, joint winners of the scholarship prize in 2017, Nigel Jemson, the winner in 2020 and Vivian Lei, the winner in 2022. You may recall Vivien, have previously been a guest on the podcast.

Now, this was a fascinating panel discussion conducted under Chatham House rules, focusing on the scale of fiscal challenges for the next few decades and how could we meet those? Does this mean for example, some new taxes might be required such as capital gains tax? What about boosting Inland Revenue’s investigation efforts? And then on the spending side of the equation what do we do about rising health care and superannuation costs? Do we perhaps increase the age for eligibility or (re)introduce some forms of mean testing for New Zealand Superannuation? All these points were raised for discussion.

The panel discussed ‘the tax gap’, the gap between what we think the tax collection should be and what’s not being collected. There’s a lot of work to be done in this space, because we really don’t have a clear handle on the extent of this particular issue. Some work carried out several years ago by Inland Revenue suggested that when you look at the consumption patterns between self-employed persons and employees, there might be as much as a 20% gap. In other words, self-employed people appear to have about 20% higher levels of consumption than employees on ostensibly similar levels of income. This is a topic which actually might be worth a podcast episode in itself.

And the finalists are…

It was then followed by the announcement of the four finalists of this year’s Tax Policy Charitable Trust scholarship prize. Every two years the Tax Policy Charitable Trust invites young professionals (anyone under 35 on 1 January 2024) to submit proposals for review, improving any aspect of New Zealand’s tax system. Entrants submit a 1500 word overview proposal on any part of the tax system from which the judges choose four finalists will be selected to go through for the final main scholarship prize, which is worth $10,000.

Submissions are judged for their creativity, original thinking and sound and reasoned research and analysis. In addition the judges take the following factors into consideration:

Impact on the New Zealand economy, including GDP and business growth.

Social (including distributional equity) and environmental acceptability.

Feasibility of introduction, including political and public acceptability.

Impact on simplicity of tax system.

Ease of administration by taxpayers and Inland Revenue, or other relevant government agencies, and impact on compliance costs.

This year, there were 17 entrants and the four finalists chosen are

Matthew Handford, who proposes an Independent Tax Law Commission aimed at improving the Generic Tax Policy Process, or GTPP. The GTPP is a cornerstone of tax policy and is internationally well regarded, but it’s now 30 years old, so is due a reconsideration. I look forward to hearing more about Matthew’s proposal.

Claudia Siriwardena, who is suggesting a simplified FBT regime for small and medium enterprises. This gets a big tick from me, and I’m very interested in hearing more about this one.

Matthew Seddon, who proposes extending the independent contractor withholding tax regime. Mathew’s suggestion picks up the point just raised about the tax gap and deals with it by improving compliance. Again, another interesting proposal.

Finally, Andrew Paynter who is putting forward a proposal to increase the GST rate from GST but also tackle the regressivity of GST with a rebate for low and middle income earners. I’ve seen some international papers on this particular topic, so I’m very, very interested to hear more about what Andrew’s proposing here.

My intention is to get all four scholarship finalists on the podcast to talk about their ideas before the winner is announced in October, so stay tuned for developments. In the meantime, congratulations to Matthew, Claudia, Matthew and Andrew and to everyone else who entered. No doubt there were some interesting ideas put forward that did make the cut this time, but overall, it’s a great sign of the healthy state of tax policy debate in New Zealand.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

What makes a good tax system and where does New Zealand presently sit?

The current broad-base, low rate approach is under strain. How do we address that? What can we do to keep/ preserve that as far as possible? And more.

Terry Baucher: It is my very great privilege this week to be joined by three of the titans of tax in New Zealand, Rob McLeod, Robin Oliver and Geof Nightingale.

Rob, or more correctly Sir Robert McLeod, KNZM is one of THE gurus of New Zealand tax, has been involved in tax policy at the highest levels since the 1980s. A former chair of EY, he was chair of the 2001 McLeod Tax Review and was also a member of the 2010 Victoria University of Wellington Tax Working Group. He’s currently a consultant, although still very much involved in the tax policy world. He was knighted in 2019 for services to business and Māori. Kia Ora, thank you for joining us.

Robin Oliver, another of the gurus of New Zealand tax, until he retired from Inland Revenue, was Deputy Commissioner of Inland Revenue and head of Tax Policy where he advised the 2001 and 2010 tax working groups. He is now a partner in tax consultancy Oliver Shaw and was a member of the last Tax Working Group. Robin was made a member of the New Zealand Order of Merit in 2009.

Geof Nightingale recently retired from PwC, and when he’s not cycling the length of the South Island, is an independent tax consultant. He was a member of both the 2010 and 2019 tax working groups. Thank you again to all of you for joining us.

What makes a good tax system and where does New Zealand presently sit?

We’ll begin with what was asked at this year’s International Fiscal Association Conference. The three of you spoke on the topic of what makes a good tax system. What does make a good tax system and where does New Zealand presently sit? Rob, would you like to lead off?

Rob Mcleod (RM) Thanks, Terry. Well, I think at its core tax is mainly about raising revenue to finance government programmes. It’s true that tax has peripheral tasks as well, like you know, correcting for market failure. If we think about carbon taxes, the primary purpose of that kind of tax is really to moderate adverse behaviour in the economy, which is not is not really a revenue raising objective. Some would also argue that taxes are there to achieve redistribution goals, transfer income to those that are in need. That too is not so much a revenue raising goal.

“At its core tax is mainly about raising revenue to finance government programmes”

But if you go to the real reason why income tax exists in countries, it’s actually to raise revenue for governments. If governments didn’t need revenue, you wouldn’t have taxes. And chances are you wouldn’t have such a major regime doing these other two things, like corrective taxation, like carbon taxes, or trying to redistribute income without the agenda of raising revenue. I would argue that we wouldn’t have tax systems on the scale that we have them doing those other things. So, I believe that raising revenue is the primary goal of a good tax system and doing it at least cost would be my formulation.

Robin Oliver (RO) I agree with Rob, even more so, that a good tax system is one that works. It raises money for the government. That may seem obvious to people, but you can’t have taxes which fail to raise money. Margaret Thatcher’s poll tax failed to raise money. It was a failure.

“You’ve got to really focus on raising money at least cost”

So it has to raise money at least cost to society and that’s admin costs, compliance costs, but overall economic costs. The cost of disincentivising people from work and savings and so forth. People think that’s “blah blah blah blah” but the estimates in New Zealand and Australia, and used by the Australian Treasury, is that twenty cents in every dollar of tax is lost in economic costs. In other words, not quite, but basically lost output, lost wealth for the country. So, you’ve got to really focus on raising money at least cost.

Rob mentioned redistribution. I think redistribution’s got nothing to do with a good tax system. Government raises money to do good things – health, education, welfare. We’ve lost focus on what tax is about. We’ve got diverted into all sorts of ideas that it could be used for. No, it’s about raising money, at least cost. Every tax proposal should be looked at “Is this the way we could raise some money, effectively, at least the cost to society.”

TB Thanks, Robin. Geof, I think you have a slightly different take on the redistribution issue and I note that the IMF was talking about redistribution in one of its papers recently

Geof Nightingale (GN) Well, Terry, I’d largely, and violently agree with Rob and Robin that the primary function of a good tax system is to raise the revenue that government needs. But it’s how it goes about that where I might differ.

There’s a couple of backgrounds, opening points I’d like to make, and the first is I think it seems, really uncontroversial that our modern democratic states with tax systems and, you know, rule of law-based things. They’ve done more than anything that’s ever been tried to lift living standards. So, broadly, I think they are a good thing that the tax status policy people might call it is a good thing.

“You can only tax by consent”

The second point is, that in those democracies, it’s really important for tax policy people to acknowledge that you can only tax by consent. I mean we impose taxation through the rule of law and through enforcement. But in the end people vote on taxes and people vote governments in and out and tax is often a key election thing. So you can really only tax by consent.

So, whatever the theory may tell you, you have to – I’ve learned over many years now – bring the public with you. That’s the job of the politicians, not the policy people. The policy people have to accept. That general consent point is really important when you start talking about the future of tax in New Zealand.

And then the third thing is there’s no such thing as a perfect tax system and as Robin pointed out, we navigate it, every tax policy choice is a bunch of trade-offs, and we navigate those trade-offs with some well-established principles. You know, equity efficiency, administration etcetera. And those principles can never be applied scientifically. In the end, they come down to, in my view anyway, value judgments at the margin, and that’s where the politics comes into the tax system as it as it should be.

So what is a good tax system? Well as Rob and Robin said, primarily one that raises revenue with the least cost to society. And there are secondary objectives, and those are the distributional impacts. I think those are important for policymakers to take into account. And I think they feedback around into the consent of citizens to be taxed and and the fundamental democratic process actually. and. Most OECD countries, in fact all I think, have progressive tax systems by and large and general voting patterns suggest that that’s the majority view of life across OECD democracies.

The problem with behavioural taxes

Other secondary objectives that Rob and Robin mentioned with behavioural changes, carbon taxes and things and those are very specific instruments of public policy, and they might raise some short term revenues. But they shouldn’t be relied on for long term revenues and it’s almost a different category of taxation to the general tax system because if they work – those behavioural taxes – the revenues will often dry up, will be reallocated into the areas that they’re trying to change.

TB That’s something we’re actually seeing with the tobacco excise duty. It worked and now revenues are falling and now that’s sort of a hole in the finances.

RO But if that works, yeah, it’s the same as environmental taxes. You know you have taxes on degradation of the environment. And if you don’t degrade the environment, you get no money. And it’s perfectly fine. They work, but back to Geof’s point. I totally disagree that redistributions got anything about it. You clearly have to have a democracy; in a democracy you have to have consent. I agree with that. You have to have consent to make the tax system work because of voluntary compliance and all that.

Poll taxes – efficient but unworkable?

But the purpose of tax is to raise the money in the most cost-effective way. And I give the example of that is the poll tax, Margaret Thatcher’s poll tax. I mean poll taxes are loved by economists because it’s thought of as being efficient. But it doesn’t work. I mean if you want to raise New Zealand’s government revenue by poll tax you’ve got to raise about $30,000 per individual. You’re not going to go out to people in South Auckland, a family household, and demand $100,000 from them please. I mean, they don’t have it. And there’s no point in demanding money, which people just don’t have.

And that’s why even an efficient tax system, inevitably given the level of government expenditure we have, will need to be progressive. Because you know the lower income earners just don’t have money to pay the tax that the government needs. But again, the point is, you’re really trying to raise money to spend on health, education and welfare and you want to do it at least cost. And forget about trying to have a secondary objective of redistributing income, that just leads you into bad taxes. And that’s led us from having a good tax system to one which is now pretty awful or going that way.

TB It’s a hell of a topic that. I mean, there is always a redistributive effect of tax, and the recent Treasury paper on the fiscal incidence of taxation was quite interesting in that regard.

RO Yes, good paper.

What about ring-fencing taxes for certain objectives?

TB The Treasury paper showed health and education benefits going to different deciles. They’re essentially redistributed within the system. So just a quick thought about these behavioural taxes Do you actually see much of a role for ring fencing? Tax takes such as, for example, environmental taxation that we raise these, we’re trying to encourage better behaviour, but the funds don’t go into the general pool but are used to mitigate the impact of climate change. Is there a role for that Rob?

RM Yes, I think I think there is. We call this hypothecation and we’ve had hypothecation in the area of fuel taxes for example, which are put on road users and then reinvested back on to roads at various times. But over time, you know, I think that money was ultimately then sent to the consolidated fund.

RO I mean, money is fungible. And therefore, putting it in one pot versus many pots, you can have an argument about whether that’s effective. I think ultimately if governments ensure there is a correlation between how they apply the funds and the taxes they raise, and hypothecation is a solid principle to get that correlation. But I think that the more recent view of governments has been that they can be relied on to effectively finance it all out of a consolidated pot. So yes, hypothecation is certainly there, and we’ve got examples of it.

Economists hate hypothecated taxes, because it ends up government spending money wastefully and low priority areas, because that’s where the money is. But it does serve a purpose, it provides the right incentives. There’s a case for it you know road user charges, Rob said was a good case in point. And you can make other cases like how do we control the level of health expenditure? Well, you could hypothecate GST to health and if people want to spend more on health, GST goes up and everybody has to pay it, so you can end up with arguments for hypothecated taxes. But the economists really hate them.

GN At the risk bringing distributional effects back onto the table, hypothecated taxes can also be highly regressive, so yes, I’ll just leave that there.

TB Yes, a common hypothecated tax around the world, which we don’t now have but once did, was Social Security. You see that many other jurisdictions had that and we’d had that until the late 60s. I think it was Rob Muldoon who decided stuff this we’ll just get rid of it because it was, as Rob described, was just going into the consolidated fund. But looking way back, it was a quite significant part of tax revenues if you look track the history of tax.

The problem with social security taxes

RO And very important in Europe in particular, and the United States of America. And we are very lucky not to have them. Australia and New Zealand, one of the few OECD type countries not to have Social Security payroll taxes, which are linked with the benefits. The reason for that is it results in peoples’ old age pensions, or whatever you call them – New Zealand super being linked with past earnings.

And that means that the poor are really poor, when they are elderly. And that’s the case in the UK. Everybody gets the same in New Zealand which in my view is absolutely a much better system than using your tax system to provide benefits linked with wages. Which means particularly women who are not always in the workforce, but child rearing, skills get really done over. I think we’ve got a much more equitable system of expenditure on welfare because we don’t have that.

The incidence of tax – who is actually bearing the tax burden?

RM Terry, can I just perhaps take us back to redistribution, I think there’s one important point about redistribution which unfortunately is a bit of a technical point. But it’s one that is overlooked not only by lay persons, you know, people not familiar with technical stuff, but also the tax profession itself. Which is the issue of incidence.

So if you just start with the GST as an example, most New Zealanders wouldn’t accept, and rightly, that the GST is not imposed on them. And yet, if you have a look at who pays the GST, they don’t pay it. The consumers do not send cheques to Inland Revenue. The tax is actually imposed on businesses. As a matter of imposition. When we talk about redistribution, we’re inclined to assume that the tax impact is where the law imposes it, but the key principle that’s demonstrated by the GST example is the market actually takes that tax and spreads it around, arguably like margarine, to all of the stakeholders and sometimes non stakeholders, and the and the contract to be affected.

These are such things as gross ups, if you go and slap a tax on somebody and they’ve got market power, they’ll put the price up of what they’re supplying to others. And in so doing, they’ll pass that tax burden on to others. And this is completely ignored in my view, when people are talking about redistribution, because there’s the assumption that the taxes that are actually imposed by the government, is actually borne by the people who send cheques to Inland Revenue Department, is utterly false. And if you try and unravel that mathematically and work out who actually is bearing the tax, the best you can get to on most of it is estimates including the dead weight loss of the 20% that Robin is talking about, it’s there’s a lot of estimation going on to get to those numbers.

There’s no argument that that economic effect is real, and for me that’s a big undercut of why I don’t buy all the redistribution argument, because it tends to proceed on the assumption that the way the government’s levying the tax will ultimately shape and determine the burden of it.

RO We don’t know a lot about the incidence of tax. But what we do know, it’s almost never born entirely by the person paying it. So, you end up with these studies, like the awful IRD study on high wealth, totally ignoring this fact, just totally ignoring it.

And the classic example of economics in the United States is that you have local body bonds, the interest rate is tax free. It’s a subsidy to like City Councils or what, and the federal government doesn’t tax them.

The high wealth individual – the person on the very high rates – ends up owning all these municipal bonds. They don’t pay any tax. But they’re getting a lower interest rate because they’re bidding up the price of these bonds, which is what’s intended and the local City Council get cheap money. And then along comes a bunch of officials measuring their tax burden and finding it zero. Disastrous. Horrible. Well, in fact, they’re paying it through the lower interest rates on it.

And this happens all the time, all through the tax system. You put taxes up on foreigners, that’s a good idea. Foreigners we don’t like, they’re not voting, and we put big tax on foreigners. They just simply demand a higher rate of return or don’t invest here. We end up with lower productivity, lower wages and the economics is absolutely clear. Put your tax on your non-resident investor, it ends up coming out in lower wages. And that’s exactly Rob’s point. The incidence is always shifting and yet we totally ignore this. The political debate just assumes the world is not what it is.

TB Robin, I think we’re going to see more and more of that. Sorry, Geof, you were about to say something.

GN I totally agree with Robin and Rob on incidence, it’s critical. But it comes back to my opening point that you can only tax through consent, eventually. If incidence is not well understood, policymakers – and it’s very hard and very slippery getting your hands on the concept – but policymakers need to think about it. But if you can’t convey that to voters, then it becomes kind of irrelevant.

I remember Sir Rob’s MacLeod committee and the $1,000,000 tax cap for individuals. I thought was a was a great idea because of that sort of argument that we’d be better off with $1,000,000 than not. But that policy is too easy to attack politically from an equity and a sort of a fairness sense. And that’s what happens in the real world as we all know and that’s why we end up in political arguments around the secondary purposes of the tax system, as opposed to really discussing the primary purpose of the tax system Which is least cost revenue raising for government policy. So, I agree with their incidence comments, but it works both ways, I think.

RM Can I just jump in on that one and just observe that in the McLeod Review where we did recommend that to be honest, I think it’s politicians that say that say no to those sorts of things than not, as opposed to public sentiment. Muldoon made the famous quote that Joe Blog, the average person on the street, wouldn’t know fiscal deficit if he tripped over one. And I think that’s a long way back and things weren’t as sophisticated then as perhaps they are now.

But if you think about the complexities of tax and you think about the extent to which the public is actually engaged with that complexity, I think that you are apt to over egg that interaction. Because ultimately politicians and officials and people like ourselves, there is a leadership role we play and the public follows that leadership.

I think you can observe that in history. The differences between countries and the qualities of their tax system often reflect the differential qualities of officials, politicians, et cetera, that’s going on in those countries. So, while I agree that in the concept of democracy, there’s a public underbelly in debate and voting terms, there’s one hell of a space for leadership and tax policy. Otherwise, we might as well pack our bags and go home. And I think that that is very influential and that’s why these debates and these principles of incidence and so on are important and need to be approached in the way we’re doing it.

RO We can see that with GST. We’ve got a flat rate, a good GST system, world class.

I remember back in the 80s Sir Robert Muldoon, the proposals was put to him about that. And he said, “You mean we’re going to tax water?” And he chuckled, “No way.” We put GST on doctor’s bills. People overseas think that’s just totally astonishing. Yet there’s broad support for what we have in GST, a non-progressive tax. Bizarrely we legislated to make it regressive, but it does meet those economic principles and it’s got widespread support. I mean, politicians keep on arguing for GST on no food, but those proposals get put up and get rejected every time.

Rob McLeod’s suggested alternative to a capital gains tax

TB Rob in your review, you raised the possibility of the risk-free rate of return method (RFRM) as an alternative to a capital gains tax. And we’ve seen that in the Foreign Investment Fund regime. Are you still keen on the idea?

RM The RFRM, the McLeod Review, came largely out of the debate around taxing housing. And this was in a discussion document, by the way. It wasn’t the final recommendation; it was abandoned because of what Robin said. Michael Cullen’s switchboard was blown up by the complaints of from telephone callers and we knew that was a pretty strong signal that no government was ever going to support it.

So, we pulled the plug. But basically, the problem with taxing assets that produce, that give sort of imputed income like your motor car or your house or your washing machine, there’s no cash flow to really measure the income. It’s economic income, but it’s hard to measure. And so, the beauty of the RFRM is that you calculate it effectively as a wealth tax, which is applying a percentage, I think we had 4%, against the market value of the of the equity in the asset. It’s quite important. That’s one feature of the RFRM is you’ve got to work out what you’re going to do with debt, debt funding of the asset. And we came to the conclusion we’re best to deal with that by narrowing the tax onto the equity, which is the total value of the asset minus debt associated with it. Which brings in problems because people then start to plan with where they load their debt, right?

But it was simplicity. If we could have made the income tax work on that kind of asset that’s a superior way of going, if you can make it work. I think the only reason you go to RFRM in substitution is there’s easier compliance and administration for taxpayers and the Inland Revenue. The F|IF regime I think Terry came out of the international regime As the child of the CV, the mark-to-market option.

I think you’re thinking of the FDR [fair dividend rate] in today’s terms is probably the most relevant analogy. Fixed dividend rate which I think did come from a an RFRM logic, although it’s a bit screwy because FDR, the RFRM tax principle is you should apply it at the riskless rate of return, and not at the risky rate of return, which is the way FDR works. And also, no deductions which FDR doesn’t abide by in its various option formats. So the concept is much the same but quite different in detail.

What’s surprising in the tax world now?

TB Is there anything in the tax world that surprises you right now?

RO I would say the wealth tax coming on the table, totally unworkable. According to the papers the last government almost legislated for a wealth tax in the last budget, ??? funding and massive reductions in income tax rates. And that wealth tax was completely unworkable and would never get off the ground. It was a total nuclear bomb on our tax system. The fact that people are seriously talking about totally impractical things is a serious concern.

We’ve got to be adults here. There is no fairies at the bottom of the garden. There is no pot of gold at the end of the rainbow. Grow up. Taxes have to be pragmatic and have to be workable, and trying to measure everybody’s wealth on a comprehensive basis every year is not.

GN I remain surprised by the continued acceptance by middle New Zealand of what I consider to be really high effective tax rates on labour income through the combination of GST and [tax] rates. And I remain surprised when you look at their voting patterns, their general resistance to extending taxation into capital income to address that, so not raising taxes as a percentage of GDP, but recycling revenue, shifting the instance of where slightly where that tax is paid, and it continues to surprise me. I think that message came through the high net worth survey that came out last year, but it was obfuscated by the complexity and some of the methodology problems and the way that survey was done. That’s what I’m still surprised at.

TB I think there’s a general lack of awareness of what effective marginal tax rates are and how they interact and how high they are at relatively low incomes. The 30% rate, $48,000 is a real problem threshold.

RM I suppose I am a bit surprised that the fundamental features of what’s been great for the New Zealand tax system, reappear as controversies, in the political realm particularly. Like the high tax rate. The problem is that Europe’s got high tax rates and Australia’s got high tax rates. New Zealand trying to wave the flag in favour of the low tax rate component of the BBLR has been a challenge. And I think it’s actually been because our neighbour has high marginal rates. And Europe has been very influential on people like Robertson and so on in my opinion in the sense that they buy into the idea that we can have government spending and taxes at 50% plus of the GDP. I should say that I’m therefore not surprised by it. But I think that’s been the big disappointment, that our rates structure has been allowed to sort of get up, and in a sense it’s part of narrow base, high rate [NBHR] thinking. They don’t realise that with those high rates comes the NBHR concept.

The other thing I just touched on is I kind of worry about the international – the OECD and the EU – devices through which large countries bully other countries. And the treaty networks and the BEPS regime and all that sort of stuff is typically a mask for powerful big countries grabbing money off other countries. And the more that happens, that’s a source of corruption and cancer for me and can ripple down and reach these national tax systems. And we’ve had more of that in the last five years than we’ve ever had before.

RO The OECD stuff is probably more two big elephants fighting, the US versus Europe and we get squashed in the middle.

TB I think that’s why the Global South is pushing back and trying to get the UN involved led by Nigeria and Pakistan which are small economies globally, but giant populations, you’re talking over 400 million people between them. They’re not buying into Pillar two. There seems to be pressure building in that area.

What one proposal from your respective tax working groups would you like to see implemented?

RM That’s a that’s a good question. Sorry to be boring, but I think I came back to the broad-based low rate. For Geof and Robin who know me well, I am a bit of a bore-a-thon drum beater on base principles, and the thing that I’ve seen is the base principle lose a bit of its grip in New Zealand in the last decade. We’ve taken our personal and our trust rate to 39%, which I do not like.

It’s the fiscal stuff that’s that this government is arguing that I don’t accept that it’s necessary for that, but that’s another big debate point about understanding how balance sheet management in government needs to be separated from profit and loss account management. I don’t think that those two aspects of the debate are properly worked through. We should take the longer road and the longer term to fix our debt issues, obviously try and avoid them from happening in the first place. But debt is not necessarily needed to be paid immediately. And not to be factored immediately into tax rate design in my opinion, which is a mistake that we’re currently going through.

GN I’ll be boringly repetitive, but I think the extension of income tax to more realised capital gains on a realisation basis and then using that revenue to recycle, I think that’s got equity efficiency benefits. And I also think it helps in some ways to resolve those high effective marginal tax rates around our productive sector of our economy, labour productivity. So that’s still what I would do if we were able to do one thing.

RO Oh, I still like Rob’s RFRM on residential rental and get rid of all these bright lines, interest deductions and ring-fencing rules. The other one Geof raised was seriously considered by the Labour government under Michael Cullen, was that you pay a million bucks worth of tax and you’ve done your bit and go away. An anathema now, times have changed. That was acceptable then it seems, but not now.

It was seriously considered by the caucus at the time. The idea is you get someone come and live in New Zealand and pay a million bucks and fund a Children’s Hospital. Doesn’t seem to me to be a bad idea.

RM Like a hypothecated tax, Robin?

RO I wouldn’t mind if it was hypothecated for good healthcare for children. I think that would be good.

TB Well, I think we’ll leave it there. I want to thank my guests this week, Sir Robert McLeod, Robin Oliver and Geof Nightingale. It’s been fantastic talking with you all. Thank you so much for being part of this.

[This is an edited part of the full podcast which readers are encouraged to download and listen to at the link at the top of this page.]

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

IMF and Climate Change Commission suggest changes to the Emissions Trading Scheme are needed.

Like a never-ending Groundhog Day, every International Monetary Fund report on the New Zealand economy suggests tax reforms would promote efficiency. For example,

“There is a sense that the asset allocation in New Zealand households has a bit too much emphasis on housing versus other investments. We think a capital gains tax at the margin would help.”

That was IMF Mission Chief Thomas Helbling in 2017.

“…tax policy reforms are needed to promote investment and productivity and growth increase, increase the progressivity of income tax and mobilise additional revenue in response to long term fiscal challenges. To achieve these objectives, reforms should combine comprehensive capital gains tax, land value tax and changes to corporate income tax.”

And invariably the IMF’s conclusions are usually followed by a fairly dismissive response from the Minister of Finance of the day.

In 2002 it was the late Sir Michael Cullen responded to that year’s report: “The IMF’s credibility is not assisted by the fact that it tends to apply the same policy template regardless of the country’s circumstances”. This year Nicola Willis’s retort was “There are some things that are certain in life, death, taxes and the IMF recommending a capital gains tax.”

Associate Minister of Finance David Seymour also weighed in commenting. “I see the IMF again saying, oh, you need a capital gains tax. Every country has one. The only countries that don’t have one are New Zealand and Switzerland. But I say let’s be more like Switzerland.”

However, I’m not so sure that this was quite the zinger he hoped because as someone mischievously pointed out on Twitter, Switzerland has a wealth tax and a $59 per hour minimum wage in Geneva.

Deputy Prime Minister and former Treasurer Winston Peters was apparently not available for comment.

A de-facto capital gains tax – the bright-line test

Now, amidst all of the commentary about the IMF’s suggestions, one of the things that came up time and again is that in many ways, we do have a de-facto capital gains tax, except we don’t call it that. The bright-line test is an example of the approach that we’ve adopted, which has been ad hoc and responsive based on the government of the day’s policies at the time.

As you may recall the bright-line test was brought in with effect from 1st October 2015 by the National Government and it then applied to disposals within two years. In March 2018 the Labour Government introduced a five-year period and in 2021 it was increased a 10-year period. And so, a quite confusing scenario has developed as to which bright-line test applies because some of the exemptions have changed over time as well, particularly in relation to the main family home.

In one way, therefore, the reduction of the bright-line test back to two years again from 1st July is to be welcomed because it is clarifying and simplifying what has become an incredibly complicated area.

Tax Red Flags: More than just the bright-line test to be considered

The bright-line test and taxation of land has plenty of red flags when together with the excellent Shelley-ann Brinkley and Riaan Geldenhuys and moderator Tammy McLeod, I made a presentation about tax red flags on Tuesday to the Law Association. (Formerly the Auckland District Law Society). My thanks again for the invitation to present and to my excellent co-presenters, we had a very lively session talking around this.

In short when you drill into our current land taxation rules, they are very incoherent. The bright-line test is a backup test. It applies if none of the other land taxing provisions apply. And this is something that tripped up people before the bright-line test was introduced and will continue to do so even now it’s been reduced down to two years.

For many people, the particular issue to watch out for is the question of subdivision. If you own a property and undertake a subdivision within 10 years of acquisition it may still be caught under the existing rules, outside of the bright-line test. And in some cases, you may be caught by the combination of the provisions with the associated persons test which deem transactions to be taxable if at the time you acquired the land you were associated with the builder, dealer, or developer in land.

Sometimes the tax charge can be triggered way past the 10-year timetable since acquisition. That’s particularly the case in relation to a disposal of property where building improvements have been carried out. That particular provision, section CB 11 of the Income Tax Act, deems income to arise if a person disposes of land and

“within 10 years before the disposal”, the person or an associate of the person completed improvements to the land and at the time the improvements were begun, the person or an associated person carried on a business of erecting buildings. Note, the reference to “within 10 years before the disposal.” So, you may have owned that land for considerably longer than 10 years and yet still be subject to the provision.

Just a pro tip for anyone thinking ‘Great, with a two year bright-line test coming in, I can now sign a sale and purchase agreement, make sure settlement takes place after July 1st and it’s not going to be subject to the bright-line test.’ That’s not the case. The sale point for the bright-line test in that case is when the sale and purchase agreement is signed and not when settlement happens. I had at least one client get caught by that very provision because they went for a long settlement thinking that got past the two year period. It didn’t, and it is another case of always seek advice on transactions involving land, because as I’ve just outlined, the provisions are complicated.

Could a capital gains tax be ‘simpler?’

And this was the point we reinforced during our seminar. There is a lot of complexity already in our tax system around the taxation of land and in my view, in some ways a capital gains tax would actually clear away a lot of that uncertainty. It’ll become clearer that, broadly speaking, if you buy something, and you sell it subsequently, any gain will be taxable.

Now, how the gain is calculated and the rate at which it’s taxed are two different things. But often in the debate around the capital gains tax, those two things get conflated to run as an argument against the taxation of capital gains.

In my view, the point still remains that we have a confusing hotchpotch approach to taxing capital gains and at some point, grasping the nettle with a CGT as suggested by the IMF and also the OECD, would ultimately perhaps be a better approach.

Incidentally, doing so would be consistent with the well-established principle we have of the broad-based low-rate approach. There’s nothing to say that by broadening the tax base, we could not hold tax rates at current levels or even lower. Bear in mind that the when the last tax working group recommended the capital gains tax, it was intended to keep to help keep the top tax rate at 33%.

Watch out for trustees on the move across to Australia

One of the other issues that came up in our Tax Red Flag Seminar was the question of trustees, and beneficiaries and settlors moving cross-border, particularly to and from Australia. That is something all three of us are seeing quite a bit of and it is something to watch out for as a key red flag.

The IMF on how to tax wealth

If there is a certain repetitiveness to the IMF’s discourse about taxing capital, it’s part of a global discourse on the topic. Earlier this month the IMF released a How to Tax Wealth note. These how to notes are “intended to offer practical advice from IMF staff members to policy makers on important issues.” And this this was a very interesting read as you might expect.

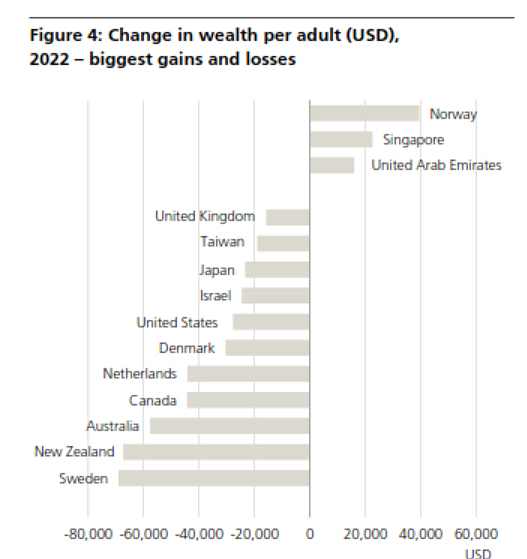

The IMF’s How to Tax Wealth note neatly coincided with the release of the UBS/Credit Suisse, Global Wealth Report for 2023. According to the report, in 2022 New Zealand ranked sixth in the world with an average wealth of US$388,760 per adult. On the basis of median adult wealth per adult, again in U.S. dollars, we ranked 4th behind Belgium, Australia and Hong Kong, with a median wealth of US$193,060.

Incidentally, these rankings were after a very sharp fall from 2021 levels, where New Zealand was only behind Sweden in the biggest loss in wealth per adult.

I am genuinely very surprised to see New Zealand rating so highly for both average wealth and median wealth. On the other hand this Credit Swisse/UBS report is another example of why there’s a great debate going on around the taxation of wealth not just here, but globally.

And this IMF How to Tax Wealth note is instructive in its approach. It starts by making a very obvious point, how much to tax wealth is a distinct question from how to tax wealth. The note argues that:

“returns to capital generally should be taxed for equity and possibly efficiency reasons. and that in many countries, wealth inequality and better tax enforcement strengthen the case for higher effective taxation than in the past.”

Now the IMF doesn’t make any particular proposal about a specific level of tax, the note is basically about ‘here are things you should consider.’ But on the question of wealth taxes, it does come down pretty much against them noting,

“Improving capital income taxes tends to be both more equitable and more efficient compared with replacing them with net wealth taxes. Countries hence should prioritise improving capital income taxation over considering the introduction of wealth taxes”.

Then it talks about – in terms of strengthening capital taxes – addressing loopholes, notably the under taxation of capital gains in many countries. There’s a passing comment, that perhaps you can use a one-off net wealth tax or maybe apply it to very, very high wealth levels.

Time for inheritance tax?

But the Note also concludes “taxing capital transfers through gifts or inheritance provides another opportunity to address wealth inequality.” The IMF comments that the efficiency costs of such taxes are modest, and notes that “inheritance taxes are better aligned with redistribution than estate taxes, since exemptions and rate structures can account for the circumstances of the heirs.”

What really makes the New Zealand tax system unique is not the absence of a capital gains tax because, as David Seymour pointed out, other countries don’t have that, namely Switzerland. It’s the complete absence of taxes on the transfer of wealth, which has been the case now since 1992. That’s what makes New Zealand unique – we have no general capital gains tax together with no estate or gift or wealth taxes.

And this is an area where I think a lot more consideration needs to go into because as the IMF noted, we’ve got fiscal challenges ahead, and where might the revenue be raised from to meet those challenges.

The IMF and Climate Change Commission suggest changes to the ETS

And finally, back to the IMF again. It concluded its mission report by noting that “New Zealand’s ambitious climate goals call for major reforms,” and it referenced the Emissions Trading Scheme, having helped limit net emissions by encouraging robust reductions and removals, particularly from afforestation.

But the IMF then went on to say that “significant reforms” are going to be needed to meet domestic and international targets, and these include reducing the number of available units in the ETS, pricing agricultural emissions and strengthening the incentives for gross emissions reductions within the ETS. The IMF finally note that given the ambition of New Zealand’s first nationally determined contribution under the Paris Agreement, the use of international mitigation i.e.; buying credits from offshore, is likely to be required.

Now the IMF report was a week after the Climate Change Commission, and pretty much said the same thing, and advised the coalition government they should halve the number of ETS units on offer in each of the next six years. The last ETS auction did not go brilliantly. That has a flow on effect in that by reducing the amount of income from emission trading unit sales, it’s going to limit crown revenue for tax cuts.

Vale Rod Oram

It’s interesting to see a confluence of opinion happening here and an appropriate time to remember the late Rod Oram someone who was a very strong environmental journalist. I was fortunate enough to know him all too briefly after we met at a panel discussion. We’d planned on him appearing as a guest on the podcast. Sadly, with his passing that will never happen now, and our thoughts go out to his family and friends.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

What connects Pillar One and Pillar Two with the collapse of Newshub?

New draft Inland Revenue guidance on employee share schemes.

Today (Monday) I was (virtually) at the Accountants and Tax Agents Institute of New Zealand (ATAINZ) annual conference which, like last week’s International Fiscal Association, (IFA) Conference, was opened by the Minister of Revenue, the Honourable Simon Watts. The Minister repeated much of what he had said to the IFA conference about supporting the Generic Tax Policy Process, his wish for simplification in the tax system and improving compliance being a main driver. As the focus at the IFA conference is very much on tax policy his comments were very welcome.

By contrast, at the ATAINZ conference, the focus is slightly different because the audience there was comprised of tax agents, and we’re more focused on operational matters. So, when it came to Question Time, there were quite a number of questions around operational aspects of Inland Revenue. One of the first questions that was asked was what was going to happen with the trustee tax rate, which you may recall is proposed to rise to 39% under a bill presently before the Finance and Expenditure Committee.

Now we’re expecting to hear back from that fairly soon, but during the week the Minister of Finance, Nicola Willis, hinted that some form of carve-out might be happening, in that the 39% trustee tax rate might not apply to all trusts. So naturally, some questions were directed at the Minister seeking clarification on this point.

He wasn’t able to give more guidance, simply saying that we will have to wait until the Finance and Expenditure Committee reports back, which is expected next week. The Minister got told it is a rather frustrating scenario because we’ve got the run up to the end of the tax year on 31st March, and we will be wanting to plan payments for dividends and other distributions in before then. Unfortunately, the issue remains a bit of a grey area for the moment.

More trusts file tax returns in New Zealand than in the United Kingdom

There’s a couple of statistics that highlight the scale of this issue.According to Inland Revenue for the 2022 income year (typically the year ended 31st March 2022), the number of trusts and estates which filed a tax return totalled 237,226. That’s actually a decrease of more than 19,000 from the prior year.

It so happens that I came across statistics from the UK’s HM Revenue and Customs about the number of trust tax returns that are filed there. And according to the equivalent tax year to 5th April 2022, HMRC received 141,500 returns.

Just pause and think about that. In absolute terms, more trust and estate tax returns are filed in New Zealand than in the UK, despite the UK, with its population of some 67,000,000 being almost 13 times greater than here. So actually, on a per capita basis, it would point to the fact, for every trust tax return that’s filed in the UK, there would appear to be close to 21 filed here. The tax rate for trusts is therefore a big issue in relative and absolute terms and that’s why the tax community and trust community are really keen to get this matter resolved as quickly as possible.

What evidence is available points to the fact that for most trusts – once you include the associated families and beneficiaries that are in there – their income would not exceed $180,000, the threshold at which the 39% top tax rate kicks in. But there is a small and significant group, about 11% according to Inland Revenue, that do receive a very large amount of income. So that’s something we’d like to see resolved soon and hope it’s in time for us to get clients advised and ready for the new tax year changes.

Interestingly, on the other comments the minister made to both the IFA and the ATAINZ conferences about Inland Revenues regulatory stewardship review of fringe Benefit Tax which it did in 2022, it’s clear that there is likely to be a focus on this issue from Inland Revenue on greater audit activity. This is something promoted under the Coalition agreement. What extra resources Inland Revenue is going to have and the full direction that it’s going to take going forward are probably only going to become clearer after the Budget on 30th May. Which, as the Minister pointed out, was not that far off in reality.

How the end of Newshub and the OCED international tax deal are connected

The news that Newshub’s operations will end with effect from 30th June was a big shock to the media community. As someone who has occasionally appeared on various Newshub programmes, my sympathies go out to all those affected. And I do hope that some means is found to keep the operation going, although it has to be said, it’s very doubtful at this point. I’ve always found in all my dealings with journalists of whichever organisation, they have always been incredibly professional, and I’ve appreciated that. And so, as I said, this is not a great day for journalism, and has also been pointed out, it’s not actually a great day for democracy as a whole.

Now one of the many excellent sessions at last week’s IFA Conference was an American perspective on Pillar One digital services tax and Pillar Two, the proposed international tax agreements, which have been under negotiation for some time. The taxation of the tech giants such as Facebook and Google is a key part of Pillar One and Pillar Two, and that’s the connection with the collapse of Newshub.

Newshub is no longer financially viable according to its owners, Warner Brothers, because of collapsing advertising revenues. A couple of days after the Newshub announcement, its competitor TVNZ reported an operating loss of $4.6 million for the six months to 31st December 2023. TVNZ noted that its advertising revenue fell from $171.3 million in the six months to December 2022 to $146.8 million in the six months to December 2023, against a background of rising costs.

So where is that advertising going? Well, most of it is going offshore. From what we can pick out from the financial statements of Google and Facebook New Zealand for the year ended 31 December 2022, it would appear that close to $1.1 billion during those years was paid to offshore affiliates in so-called service fees. Now that’s a substantial amount of money, and those transactions are entirely legitimate under the present tax rules. But it has to be said, even if 10% of that $1.1 billion were to stay in New Zealand, it would be a significant boost to the industry. And arguably the difference between Newshub’s operations continuing and being closed.

The offshore advertising and the service fees and the whole issue around the taxation of tech companies, point to the pressure building on the tech companies because New Zealand is not alone on this. Over in Australia Meta, the owner of Facebook, has said it’s no longer going to go through with the deal to pay news companies who were providing content on its websites.

The presentation at the IFA Conference kept coming back to a key point that I’ve always believed, which is tax is inherently political. The French were one of the first drivers of change in this space but obviously the American companies, which would be the most affected, pushed back by putting pressure on the American government to respond. And so even though the Generic Tax Policy Process tries to depoliticise tax policy as much as possible, ultimately governments are elected with certain political objectives, and those will often trump best tax policy, and that’s just a fact of life.

A digital services tax to help media?

The whole question of the impact on democracy and journalism of Newshub’s closure is beyond this podcast. But the pressure will now mount on the Coalition Government to consider what steps it can do to help the media. On the other hand, the Public Interest Journalism Fund was highly controversial.

Does that mean that there may need to be a change in tax policy to perhaps try and claw back some of the revenues going offshore through, for example, a digital services tax which is controversial and hated by the tech companies? Does the Government press hard for a resolution to Pillar One and Pillar Two? Or does Newshub just get shut down and we have to live with the consequences of that? Whatever, pressure will be building for the Government to take some form of action. Watch this space to see whether any such action results in amended tax policy.

Inland Revenue consultation on employee share schemes

Moving on to more routine matters, Inland Revenue has released several draft consultations on employee share schemes. The taxation of employee share schemes underwent major reforms in 2018. Subsequently, there’s been a number of questions to Inland Revenue about how the law applies in certain scenarios and how it interacts with other regimes such as PAYE and FBT.

Inland Revenue has therefore released six items – five draft interpretation statements and one draft Questions We’ve Been Asked, each focusing on a specific aspect of employee share schemes. This has been done rather than producing one single interpretation statement, so that people can more easily focus on the topic of particular interest to them. Alongside this, Inland Revenue has produced a four-page reading guide briefly summarising what each interpretation statement/QWBA addresses.

This is slightly unusual but it’s an indication of the complexity involved. Employee share schemes are used by a lot of companies and particularly small growth companies in the growth phase where they don’t have cash but want to attract and keep key employees as they expand until the ultimate goal, whether it’s ultimately a share market listing or perhaps a sale to a larger company.

The first interpretation statement is one of the more important ones, as it considers what represents an employee share scheme. The critical issue is when does the share scheme taxing date arise? That’s often a critical issue because one of the things about share schemes which causes difficulties is if there’s a mismatch between when the tax is due, but when cash might be available for the person who’s being taxed to actually pay the tax due. In fact, another of the drafts looks at the questions about an employer’s PAYE, student loan and KiwiSaver obligations where an employer wants to fund the tax cost on an ESS benefit provided in shares.

Another important draft reviews what happens with the ACC, PAYE and KiwiSaver obligations, when the employee share scheme benefit is paid in cash rather than shares. The draft concludes cash-settled ESS benefit is an “extra pay” under the general definition of extra pay and therefore a PAYE income payment, regardless of whether an employer elects to withhold PAYE in respect of the benefit.

Of the other draft consultation items, topics covered include what deductions are allowable for employers in respect of employee share schemes, and what is the treatment of dividends that are paid on shares held by a trustee for an employee share scheme.

Overall, this is very useful guidance and I do like Inland Revenue’s approach of issuing separate interpretation statements rather than consolidating all the items in a single item which would be close to 150 pages. Consultation is open until 26th April.

Thanks Chris

And finally, this week, Chris Cunniffe, CEO of Tax Management New Zealand (TMNZ) for 12 years, has just stepped down from his role. He made a brief presentation at the ATAINZ conference, explaining it coincided with the 44th anniversary of the start of his tax career at Inland Revenue. We’ve worked with Chris and his team at TMNZ for many years, helping our clients save tens of thousands of dollars. Chris has also been a past guest on the podcast. We wish him all the very best for the future.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A suggestion for the new Minister of Revenue about tax simplification; and

What tax tattoo would you have?

The International Fiscal Association (IFA) tax conference is one of the premier tax conferences in the year as it is attended by most of the very senior tax specialists in the country together with senior Inland Revenue officials. Somehow, they also let me in as well.

The primary focus is on tax policy, and the conference is held under Chatham House rules, which means that comments that are made by officials cannot be directly attributed. Notwithstanding this you still get an indication of where officials’ thinking might be heading.

This year’s conference had a particularly interesting agenda covering topics ranging from, the use of trusts, international GST, the treatment of embedded royalties, limited partnerships, to a US perspective on the OECD’s international tax agreement process. It concluded with what was probably the highlight of the whole conference ‘What makes a tax good system?’ which we’ll discuss later.

Introducing Simon Watts

Traditionally the conference is opened by the Minister of Revenue the Honourable Simon Watts. A qualified paramedic, he had once worked at Inland Revenue as an intern before he moved on to later became a tax consultant with one of the Big Four firms. Coincidentally, the Commissioner of Inland Revenue Peter Mersi was also attending his first IFA conference. It was therefore interesting to see how they interacted, and they both explained to the audience how they felt they were progressing.

The Minister began by reiterating his commitment and that of the Government, to the Generic Tax Policy Process, GTPP, the open consultative process that has been a keystone of New Zealand tax policy for almost 30 years. He was aware that the business community and the tax community had become a little concerned that there was not enough certainty in the tax system as projects were being developed. In particular, he referenced the design of a wealth tax that was undertaken by the last Government but never followed through.

He wants to make sure that there is a strong degree of certainty within the tax system, so he supports the GTPP. Notwithstanding that, there will be times such as around the Budget policy process where the GTPP will be sidelined, and consultation will only begin in earnest when the budget measures are announced.

It’s also clear, he’s been getting himself up to speed very quickly. He referenced the long-term insights briefing, the Inland Revenue prepared in 2022 on the impact of tax on foreign investment and productivity. He also referenced the regulatory stewardship review of fringe benefit tax (FBT). Following on the Minister’s remarks and comments made by the Commissioner of Inland Revenue, I think we could expect to see more action following up the FBT stewardship review maybe in terms of greater enforcement but also in terms of simplification of the tax and compliance.

The Coalition Government’s is still under development, but the focus will be on tax simplification and reducing compliance costs. That’s not unexpected, and from what officials are saying, they’re all very heavily invested at the moment in working on those areas and meeting the pressures of the Government’s 100-day programme.

Bright-line test and commercial building depreciation changes confirmed

He confirmed that the bright-line test period will revert to two years with effect from 1st July 2024. From that date sales of bright-line property will not be taxed under the bright-line test, if the property has been held for two or more years. (Other tax rules may still apply). He also confirmed that commercial building depreciation will no longer be available from the start of the 2024-25 tax year.

The timing of the withdrawal of commercial building depreciation is possibly going to be controversial. The Minister confirmed it would be from the start of the 2024-25 tax year. For most taxpayers, that is 1st April 2024 so it’s a future impact. However, for what we call early balance, date payers such as those with a 31st December 2023 balance date their new tax year started on 1st January. Therefore, from that date they can longer claim depreciation on commercial buildings.

That I think is slightly controversial in that there’s a retrospective effect to it, obviously, and it may mean some tweaking around provisional tax payments. But the policy has been outlined previously. We’ll see the relevant legislation and more detail in due course maybe around the time of the budget policy process announcement towards the end of March.

(Interestingly, the issue of 39% rate for trustees didn’t actually come up in discussions with either the Minister of Revenue or the Commissioner of Inland Revenue). Apparently, the Finance Minister’s wish for a 6.5% reduction of costs is still on the table although the effect of this may be counter-balanced by the increased funding for audit activities.

The Minister came across as someone wanting to listen. He also holds the Climate Change portfolio, and he sees quite an overlap with Revenue because they’re both seen as financial portfolios. He mentioned that a lot of emphasis is developing in the climate change area around climate finance, which apparently is going to be a focus at this year’s COP 29 Conference, which will be held in Azerbaijan.

I had the impression he’s already across a lot of aspects of the portfolio and from comments from the Commissioner and others, he’s following up on past Inland Revenue asking if “we’ve done this, where are we with it? Let’s move it forward” which is good to hear.

The uses of trusts – trouble ahead?

Trust specialist Vicki Ammundsen regaled the audience with often hilarious tales of some of more extreme situations she’s encountered in her role as a trust lawyer and as a trustee. But amidst all the laughs, a serious point was made time and again: trusts are mostly established and used for non-tax reasons. However, they are not always administered well and in some cases she felt many people had set up trusts for the wrong reasons or completely incorrect reasons and had failed to understand how they would operate.

She also thought there was probably very pretty widespread, if accidental non-compliance with the impact of overseas resident trustees and the treatment of distributions to overseas resident beneficiaries. Her comments echo my own view on what’s happening in the trust space. I would also agree with Vicky that we’re likely to see more and more trusts wound up as people realise that something that was possibly useful 30 years ago is no longer relevant, and in fact the same objectives can now be achieved by holding assets outside trust.

One point she raised, which I found very relevant in relation to some decisions coming out of the Jersey Tax Court which ruled trustees should not be equalising distributions to beneficiaries to account for asymmetric tax treatment. This may arise when one beneficiary may get a distribution which is tax free in their jurisdiction, but another one has to pay tax on a similar distribution, because they live in a different tax jurisdiction. The Jersey Court’s view is that beneficiaries make a choice to live overseas, and other beneficiaries should not be indirectly affected by that. It’s an interesting point to make because issues around distributions to overseas beneficiary is something that’s going to be coming more to the fore in the future. Right now it’s an area I’m receiving more enquiries around.

Embedded royalties and the PepsiCo case, an Australian precedent?

“Embedded royalties” might sound strange, but this Australian decision is potentially very significant. To cut a very long story short, PepsiCo the American soft drinks company signed an exclusive bottling agreement with an Australian company Schweppes Australia Pty Limited. Under the agreement Schweppes Australia would make payments for concentrate which it would then turn into soft drinks such as “Pepsi”, “Mountain Dew” and “Gatorade”.

The Australian Tax Office (the ATO), which has always had a reputation for being pretty aggressive in the transfer pricing space, decided to take a case against PepsiCo on the basis that some part of those payments represented an embedded royalty. That portion was therefore subject to the Australian equivalent of non-resident withholding tax even though the payments by Schweppes Australia were actually made to another Australian company, which was a subsidiary of PepsCo. Last November the equivalent of the High Court ruled in favour of the ATO.

It’s a very interesting case, but the key point which emerged in the session was that the overlap between Australian and New Zealand legislation was strong enough that maybe Inland Revenue here might be tempted to take a similar case. (There was another aspect about Australia’s Diverted Profits Tax that’s not relevant here). The decision has been appealed and it’s thought likely PepsiCo might choose to settle. But it’s interesting to see what happens in Australia because we do tend to watch closely what’s happening with the ATO and transfer pricing.

Tax system oversight – the Australian experience

Speaking of the ATO, one big difference between New Zealand and Australia is that there are more bodies involved in tax oversight of the system in Australia. There’s the Australian Board of Taxation and then there is the Inspector General of Taxation, who also is the Tax Ombudsman for Australia.

The current Inspector General of taxation and Taxation Ombudsman for Australia, Karen Payne, presented on how these two bodies were created and what had been the experience so far. This is a particularly interesting topic for myself because I wrote a paper for the last tax working group on the issues around a tax ombudsman.

She also referenced the American experience with their Taxpayers Advocate Service raising the question whether such an independent office also be an advocate for taxpayers. This could partly resolve the disparity in powers and resources between the tax authority and the ordinary taxpayer. As Karen Payne noted, many of the clients of the partners at the conference are big enough and ugly enough to look after themselves in a dispute. But the general public isn’t, so that’s a question that comes through when considering the role of a taxpayer Ombudsman/advocate.

Karen Payne also referenced the fact that in certain certain circumstances the Australian Commissioner of Taxation has the power to take some remedial actions, in other words say, “We got this wrong and here’s how we wish to remedy it”. She noted that the Australian Commissioner of Taxation has exercised this power that seven times. On the other hand, even though the Commissioner of Inland Revenue here has a similar power, it’s never been exercised. Overall, a very interesting session on what oversight should be in place and the issues involved in setting up that oversight.

International GST, Aotearoa New Zealand leading the way?

On international GST policy, a couple of interesting notes that came out of that one, was that generally speaking in New Zealand has been a world leader in this GST space. We have one of the broadest GSTs in the world which because of much broader reach represents 30% of the total tax revenue. This is above most other countries with GST or Value Added Tax (VAT) system where it generally represents about 20% of the overall tax take.

Around the world, the average VAT/GST rate is 19.2%, whereas ours is lower at 15%. Our GST is a classic example of a very popular topic, the broad based, low rate (BBLR) approach to taxation, where a broader tax makes lower tax rates possible which just about every tax practitioner, including myself, will endorse.

Economics and the environment

We had an economic update from Michael Firth of the New Zealand Superannuation Fund. Several interesting snippets came out of session including that barely 10% of the total funds of the Super Fund are currently invested in New Zealand. Of greater importance when looking ahead to consider the impact of climate change on GDP, the outlook isn’t particularly good. In fact, every forecast seems to make previous ones look over-optimistic even if the best policy response is adopted and we do everything to lower emissions by 2050. The climate change implications around tax policy are how we’re going to fund dealing with the physical effects of climate change.

Alternative tax raising options

Michael Firth’s session led into a very interesting presentation from Young IFA about alternative options for raising revenue. The Young IFA presentation referenced the Treasury Briefing to Incoming Minister, which shows that core expenses are rising and unless changes are made, there’s going to be a growing and unsustainable deficit, the cost of which will be borne by younger generations, hence their particular interest on the topic.

Young IFA deliberately excluded capital gains tax but looked at three areas, windfall profits and a wealth tax. By OECD measurements our environmental taxes are at the the lower end of the scale, but how you define environmental taxes is elastic so once Road User Charges and Fuel Excise Duties are included, we are nearer to the OECD average.