Inland Revenue guidance on the new 39% trustee rate

Briefing the Minister

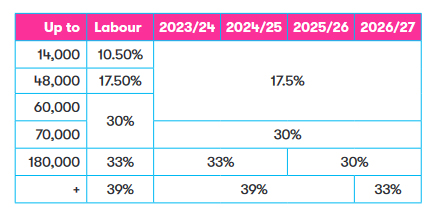

Tax credits or threshold adjustments?

The Finance Minister signed off 2023 rather like a Shortland Street season finale, leaving us all guessing as to the exact extent of the proposed tax cut package and when it might apply. We were told at the Half Year Economic Fiscal Update Mini-Budget on 20th December we could expect more details shortly. But now it’s February and we’re no wiser. It now appears likely we’ll have to wait until the Budget in May for full details.

A 39% trustee tax rate?

On the other hand, the business of government carries on and we will know early next month whether the coalition government will proceed with increasing the trustee tax rate to 39%. That’s when the Finance and Expenditure Committee reports back on the Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill. This is the annual tax bill currently before Parliament which proposed the increase to 39%. It must be passed by 31st March.

The FEC heard oral submissions last week, and I note that (previous podcast guest) John Cantin thinks it’s most likely that the tax rate will go ahead. This is even though such evidence as we’ve seen suggests that a 39% tax rate for trusts probably represents over taxation of many trusts once the wider family context is considered.

I tend to agree with John that the rate increase will go ahead, in part because it is a base protection measure as it aligns the trustee rate with the top individual tax rate. But also, the Government will probably be grateful for some additional revenue to counterbalance the lost revenue from the proposed tax threshold adjustments. That said, I know a number of submissions proposed that some sort of de minimis threshold is introduced, and the rate of 39% will only apply on the excess.

Inland Revenue’s view on tax planning for the new 39% rate

Meantime, and rather helpfully, Inland Revenue released last Friday some high-level guidance about how it might perceive taxpayer transactions and structural changes ahead of a rate change. General Article GA 24/01 proposed increase in the trustee tax rate to 39% has been released in response to requests since the rate was proposed for guidance on how Inland Revenue might perceive some transactions.

GA 24/01 contains several examples of possible transactions and how Inland Revenue would view the transaction. The first example is a company owned by a trust which changes its dividend paying policy. Inland Revenue considers a company is entitled to change its dividend paying policy and while taking into account the funding needs of shareholders and applicable tax rates, it “is unlikely without more (such as artificial or contrived features) to be tax avoidance.”

The example then notes Inland Revenue might have concerns if the company could pay a dividend by crediting shareholder current accounts, but “objectively has no real ability to pay those credit balances if it was to be liquidated.” In other words, the company tries to pay a dividend ahead of the trustee rate increase but doesn’t have the funds to pay the dividends in cash in full.

Another example is of a trustee choosing to wind up a trust. Again, GA 24/01 suggests such a step is “unlikely without more (such as artificial or contrived features) to be tax avoidance.” GA 24/01 also looks at the question of trustees investing in Portfolio Investment Entities instead of other available investment options. The advantage here is that the maximum rate applicable to Portfolio Investment Entities is 28% Again, Inland Revenue concludes such a step is unlikely without artificial or contrived features to be tax avoidance.

That said, Inland Revenue is going to continue to gather information on trusts and something it has said would be of concern to it is where income is allocated to a beneficiary taxed at a lower rate, and then instead of actually being paid out or being fully available to the beneficiary, is resettled back on the trust. In effect, the beneficiary has not benefited from the distribution.

The allocation of income to a beneficiary, where the beneficiary actually doesn’t know of an allocation or has no expectation of receiving the income together with replacing dividend income with loans “in an artificial manner”, are other alternatives which would concern Inland Revenue if there’s no real commercial reality behind the arrangement. And then artificially altering the timing, ie: bringing forward or deferring any taxable deductible payment, particularly it’s linked to existing contractual terms or practise for the date of payment.

These are just a number of scenarios which might play out. And clearly Inland Revenue’s watching. As I said, we really won’t know what the state of play will be until early next month when the FEC reports back, and when it does, we’ll let you know. But as I said, the expectation I have is we should see that tax rate increase.

The Tax Principles Act may be gone but its first draft report lives on

Moving on, one of the first things the coalition government did was repeal the controversial Tax Principles Act. Nevertheless, the draft report that was due to be produced under the Tax Principles Act has been proactively released and it makes for some interesting reading.

The report gives a background as to why it’s being prepared, its reporting obligations, and it explains what are the tax principles that were measured. These were included in the Act – efficiency, horizontal equity, vertical equity, revenue integrity, compliance and administration costs, flexibility and adaptability and certainty and predictability. Incidentally, a lack of certainty and predictability was one of the objections that was made about the Tax Principles Act because didn’t go through the full generic tax policy process.

Inland Revenue was required to assess the principles, against four measurements:

Income distribution and income tax paid;

Distribution of exemptions from tax and of lower rates of taxation;

Perceptions of integrity of the tax system, and

Compliance with the law by taxpayers.

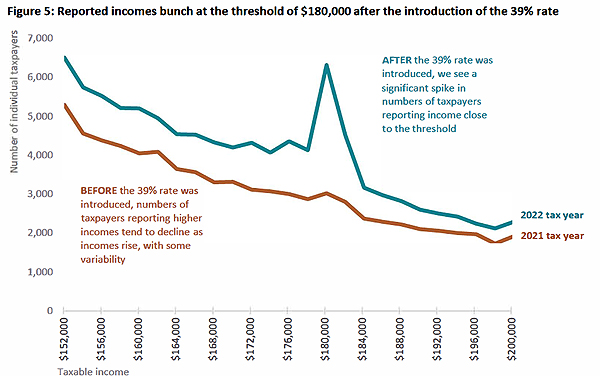

The report has lots of interesting graphs including the taxable income distribution for individuals for the 2022 tax year which shows a wee spike around the $180,000 mark.

I think that’s rather revealing even if there are apparently only 4,000 individuals involved. But still for those taxpayers you may need to have a good explanation of what’s going on.

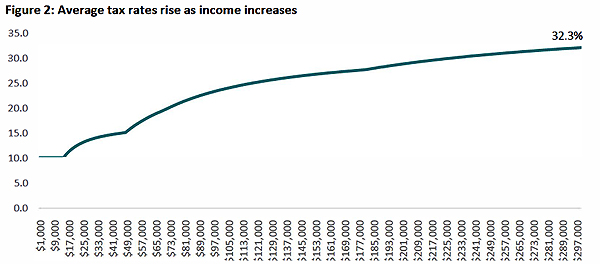

There’s a graph showing how average tax rates rise as income rises. This graph tops out at $300,000, by which point the average tax rate has risen to 32.3% for someone of that income.

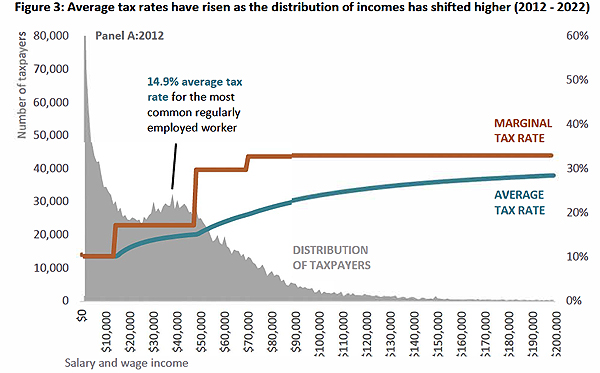

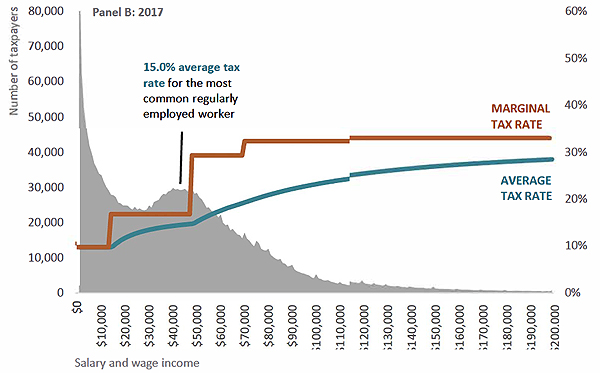

But what I thought was quite interesting were the graphs looking at the average tax rates from 2012 to 2022. In particular the graphs illustrated the effect of inflation combined with the non-adjustment of thresholds. That’s an issue I’ve talked about frequently and threshold adjustments we think will be at the core of the Government’s proposed tax relief package expected to be rolled out later this year.

The report notes between 2012 and 2017, the average tax rate for the most common regularly employed worker increased by 0.1 percentage points. Not too bad. But from 2017 to 2022 it increased by 1.2 percentage points. That’s quite a more significant example. Overall, in the period between 2012 and 2017 it rises from 14.9% to 15% and then rose between 2017 and 2022 to 16.2%.

This is the fiscal drag (or bracket creep) I discussed with Susan Edmunds of Stuff. It’s been an issue for quite some time. As wages rise faster, they drag persons on average incomes into a higher tax bracket. It will be interesting to see how the Government addresses it, and I’ll talk about that in a few minutes.

There’s plenty of other material to consider. There’s an interesting stat that the top decile of taxable income earners paid 44% of personal income tax. The report notes that the same group earned 33% of total income and suggests this is a better indicator of progressivity in the tax system than the fact that 44% of tax is paid by the top decile.

The arguments will rage around the progressivity and fairness, David Seymour of the Act Party for one has been talking about this area. Overall, there’s a lot to consider in the report. Interestingly, in the note to Cabinet regarding the repeal of the Tax Principles Act, the new Minister of Revenue Simon Watts suggested that much of this data could be made separately available, perhaps as part of Inland Revenue’s annual report. I hope we do see that, because for some time I’ve felt that the discussion around bracket creep, fiscal drag and thresholds has been sort of sidelined because governments have been not too keen to discuss it in great detail.

Briefing the Minister

Mentioning the new Minister of Revenue Simon Watts, another report released last Friday was the Briefing to the Incoming Minister. I think some of the data that’s been included in this draft report under the Tax Principles Act, would normally go into the Briefing for Incoming Minister.

What I found interesting in the Briefing was Inland Revenue’s discussion around where it’s at and the effect of the completion of the Business Transformation Programme which has allowed it to “deliver significant cost savings”. For example, the Briefing notes the amount of revenue collected for the year ended 30 June 2023 grew by 62.5% compared with the year ended 30 June 2016, the last full year before transformation began. Over the same period, the number of Inland Revenue full-time equivalents reduced by 29%.

There’s been a lot of talk about government cuts for the public sector, but I think the Briefing subtly, or not too subtly, you might say, raises a good question – if an organisation has managed to reduce its headcount by 29% and its funding is not tracked with inflation since 2017, which appears to be the measure for the basis of these public spending cuts, why would you add further cuts?

My view would be, and I think I wouldn’t be alone in thinking this amongst tax practitioners, is that Inland Revenue is under a bit of strain. We know it probably needs to boost its investigations efforts. So why it should be on the chopping block when it’s already done much of what any government would want it to do – more with less. But we’ll see how that plays out.

I thought the amount of commentary in the Briefing around the question of funding this point was quite interesting. It notes that for the year, to June 2024, the department gets about $800 million a year. And at October 31st 2023 its workforce was 4,231. Whereas back in June 2016 it was 5,662. And by the way, the report also notes the department has planned for taking a $13.9 million reduction for the year to June 2025, which was announced by the previous government in August 2023.

According to the Briefing funding would be running around about $700 million going forward, but then adds something the government should probably pay attention to.

“Our primary cost pressures in out years will be remuneration and inflationary cost pressures on technology as a service contracts, accommodation, leases and other operating costs. We are currently developing options for meeting these costs and we’ll report back to you on these matters.”

I know speaking as an employer and along with other colleagues, finding staff is difficult at the moment, so that puts pressure on salaries, obviously. And Inland Revenue is not immune to that because it needs to pay near market rates to attract good quality people, because as the gamekeeper, so to speak, it needs to match the poachers on the other side. Like so much in the year ahead it will be interesting to see how the Minister settles in and what happens with Inland Revenue’s funding.

The shape of things to come – tax credits or threshold adjustments?

And finally, coming back to what lies ahead, as I mentioned at the start, the Half Year Economic Forecast Update left us none the wiser as to the nature of the threshold adjustments, which we think are going to happen. In that gap. David Seymour of ACT has come forward and talked about the ACT policy, which is to simplify the tax rate structure down from the current five rates down to three, with a top rate of 33%. This is moving back to the rate structure which applied from 1989 through to 2008. Basically, until 1 April 2000 (when the 39% rate was introduced) there were two main rates with a tax credit adjustment for low-income earners.

David Seymour talked about tax credits similar to the existing Independent Earner Tax Credit. But as I told RNZ while the concept’s not uncommon, there’s still the issue we discussed earlier. What about adjustments for inflation and keeping the true value of that, otherwise lower rate/ lower income earners will face higher effective marginal tax rates.

There’s also a certain complexity with tax credits. The thing about applying thresholds across the board to everybody, it’s pretty straightforward. Whereas with tax credits, if there’s a claim process that’s involved, not everybody will claim that. It introduces a bit of complexity at the bottom end, which Inland Revenue’s Business Transformation was determined to do the opposite in order to try and make it as easier for most taxpayers to comply.

As mentioned, we have the independent earned tax credit, but it starts cutting out at $44,000 and then drops out at $48,000 once income crosses that threshold. We’ll have to wait to see what happens and in the meantime there will be plenty of debate ahead. We will bring all of those developments to you as usual.

In the meantime, that’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

More details have emerged about the Coalition’s tax plans with a surprising twist that changes to interest deductibility for residential property investors have effectively been backdated to 1st April this year. Like many others when I was discussing this last week, I assumed that the reference to 2023/24 was to the Government’s financial year ending 30 June 2024 and the increase to 60% deductibility would kick in from 1st April 2024. (National’s own workings released during the Election use a 30 June year-end).

But this week the ACT Party clarified the increase in deductibility to 60% is in effect for the current income year, ending on 31st March 2024. So effectively, it’s backdated to the start of the year on 1st April. That caused a wee bit of a stir, because something of this nature hasn’t been done in a while. I can’t recall a new government coming in and announcing a tax measure effectively having a retrospective effect.

The change accelerates the restoration of full interest deductibility. It means that from 1st April 2024, interest deductibility will rise to 80% and then will be fully 100% deductible from 1st April 2025. So, within the next 16 or so months, it will be restored to full deductibility. However, as CTU Chief Economist Craig Renney pointed out this acceleration adds another $900 million over the forecast period to the cost of restoring interest deductibility.

Changes to provisional tax?

One of the practical implications of the change is an interesting debate around what action landlords who are provisional taxpayers should take. Such landlords would have paid the first instalment on 28th August. This would have been done based on either 110% of the residual income tax for the 2022 tax year, or 105% of the residual income tax for the 2023 tax year. In both cases, the interest deductibility proportion was higher, so the change might not have an effect. On the other hand, interest rates were lower in both years, particularly in 2022.

What I think you’ll almost certainly see is taxpayers will be keen to understand the impact of the change and how it will affect their provisional tax. My general view would be to pay on 15th January as normal, but then have a really close look before the final instalment on 7th May next year when you should have a fairly good idea of your likely tax liability for the year.

Still there are options to perhaps consider reducing the next amount of provisional tax. And some will take advantage of that. Of course, the risk comes that you may have to pay use of money interest at 10.93%. Although tax pooling can help with that.

What else is now clear?

The release of the Government’s 100 day, 49 point action plan makes clear the Auckland Regional fuel tax is to be abolished and increases to the fuel excise duty will not go ahead. No surprises there as National campaigned on these initiatives. The Clean Car Discount is set to go by the end of this year.

A $900 million bigger hole

As I mentioned earlier, one of the fallouts of the change in the timing of the restoration of full interest deductibility for residential property is an extra blow out by $900 million dollars. One of the apparent means of meeting that gap is the rollback of smokefree legislation, which was set to be world leading. Ironically, several countries seem to have decided to follow our previous example.

The smokefree changes have caused quite a stir. Bernard Hickey in his daily substack The Kaka said that Treasury had estimated that using a 3% discount, smoke free legislation would cut public health costs by $5.25 billion. But that’s now being kicked down the road.

We’ll know more about progress on other measures to fill this gap when the Half Year Economic Fiscal Update, and the promised Mini-Budget are announced on 13th December.

Time to legalise and tax marijuana? The Colorado example.

But if we are looking at the question of raising taxes, or essentially getting more tax revenue from tobacco excise duty, then I’m going to pick up a point that I’ve had for some time and ask why not legalise and tax marijuana. Now, yes, there was a referendum which voted against that. But referendums are not binding on governments. I also think there are second order benefits of legalisation including putting a hole in organised crime’s finances.

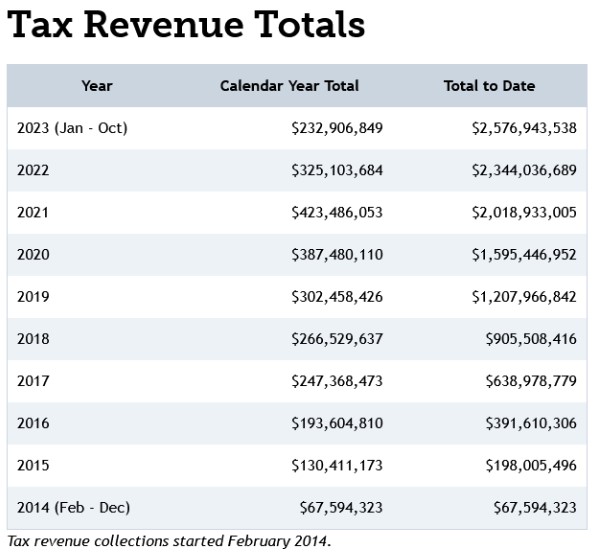

At present 24 states in the United States of America have now legalised or decriminalised marijuana. One of those is Colorado, which has a population of just over five million, more or less identical to Aotearoa New Zealand.

Colorado legalised marijuana in 2014 and have been taxing it since then. The taxes comprise the state sales tax (2.9%) on marijuana sold in stores, the state retail marijuana sales tax (15%) on retail marijuana sold in stores, and the state retail marijuana excise tax (15%) on wholesale sales/transfers of retail marijuana. In addition, Colorado also has fee revenue coming in from licensing and application fees.

Colorado’s Department of Revenue publishes monthly marijuana tax reports, and between February 2014 and October this year it has collected over US$2.5 billion from marijuana taxes. That’s over NZ$4 billion.

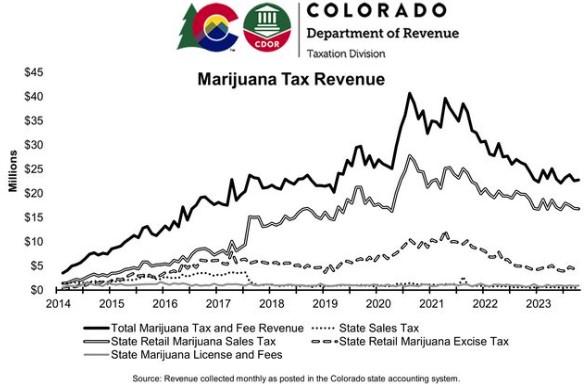

However, whether you are taxing smoking or marijuana, long term, the revenue should decline to nil, because ultimately we want people to not smoke because of the health order benefits. You can see this in Colorado’s marijuana tax revenue which rises quite steadily initially but then since mid-2021, it has started to fall away. This is probably the second order effects of people stopping smoking altogether.

But anyway, on average, the tax take is settling down to about US$300 million a year which is roughly $500 million New Zealand dollars. That’s actually a not insubstantial amount of revenue.

So that’s the Colorado example. I’m not going to say it’s going to happen here under the new Government. But you never know. Henry Kissinger died yesterday, and the relevance of that is that he was the one who coined the phrase “Only Nixon could go to China” which opened the door to a US rapprochement with China.

The phrase means bold leadership could surprise people by doing the unexpected. Bear in mind, back in 2015, John Key and Bill English surprised everyone by introducing the bright-line test. The point by referencing Kissinger and Nixon, two of the nastier people of the 20th Century, is that a bold and welcome change of direction can come from an unexpected source.

Revision of the bright-line test – when?

Speaking of the bright-line test, it isn’t specifically mentioned in the 49-point first 100 days action plan the Government announced on Thursday. I imagine we’ll get the timeline for revision at the Half Year Economic Fiscal Update.

“Overlooked” some income? The clock never stops ticking for Inland Revenue

This week Inland Revenue released five Technical Decision Summaries with a common theme relating to disputes over omitted income and penalties. To recap, Technical Decision Summaries are anonymised summaries of adjudication decisions made by a unit within Inland Revenue’s Tax Counsel Office as part of the formal dispute process between Inland Revenue and taxpayers.

The facts vary slightly in each summary, but all involve some form of income diversion/suppression which was picked up by an Inland Revenue review. For example in TDS 23/18 the taxpayer was the sole director and shareholder of Company B which carried on a retail business. The taxpayer also held 49% of the shares in Company A which operated a retail business. Y, who was married to the taxpayer, was Company A’s sole director and held the remaining 51% of its shares. The Taxpayer was also a settlor, trustee, and beneficiary of a Trust which was involved in property investment. (This is a fairly common structure in my experience.)

The Taxpayer filed income tax returns showing wages from which PAYE had been deducted and shareholder salary from Company B and income from the Trust. But on review by Inland Revenue, it appeared that money from Company B had been deposited into the taxpayer and his wife’s personal accounts partner and then used to pay personal expenses and to fund a property major purchase made by another company. These deposits had not been declared as income.

Inland Revenue proposed taxing this income and included a shortfall penalty for tax evasion. The shortfall penalty for tax evasion is 150% of the tax that’s been evaded, although in this case it will be reduced by 50% because of previous good behaviour.

What is also of note here and the other four Technical Decision Summaries is that the four-year time bar period for many tax returns had passed in respect to some of the years in dispute. (Generally, Inland Revenue can’t increase an assessment if it’s more than four years after the end of the tax year in which the relevant return was filed). The taxpayers tried to rely on the time bar rule but Inland Revenue argued it did not apply because of tax evasion and omission of income.

And that is how it panned out. The Tax Counsel Office’s Adjudication Unit ruled there is assessable income and the time bar provision is not applicable because of tax evasion and/or omission of income. Accordingly, the shortfall penalties also applied.

As I mentioned the other Technical Decisions Summaries involved similar issues and had similar outcomes. In TDS 23/16, there was a further problem for the taxpayer in that they were trying to make a subvention payment, to offset losses. And that was also turned down because of a lack of common shareholding.

There are some good lessons from these summaries, primarily if you don’t declare income, don’t try and rely on the time bar to stop Inland Revenue looking at earlier years. As the summaries make apparent it’s very clear Inland Revenue has the power under sections 108 and 108A of the Tax Administration Act 1994 to assess older years that would normally be time barred. In such circumstances, shortfall penalties for tax evasion will almost always apply.

“A really good idea”

As I mentioned last week one of the things that was surprising about the Coalition’s tax policies is the additional resources for Inland Revenue’s audit and investigation activities. On TVNZ’s Q+A last Sunday Minister of Finance Nicola Willis said that she welcomed the proposal which she thought “was a really good idea.”

We’ll only know exactly how much extra funding Inland Revenue is going to get in the Budget next May. But for the moment, you can expect Inland Revenue to be cranking up its investigation activity, and you can expect to see a lot more shortfall penalties kicking in.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This is the first year under the leadership of new Commissioner of Inland Revenue, Peter Mersi, who took over from Naomi Ferguson on 1st July 2022. It’s worth noting that Inland Revenue hasn’t had the easiest of 12 months. It did finalise its Business Transformation programme in the June 22 year, but during that period it was tied up very heavily with this and then the various COVID support programs. Those have wound down in the June 2023 year, but it got landed with the Cost of Living Payments program, which the last Government introduced in its May 2022 budget.

At first sight, the structure of the Annual Report seems similar to that of previous years, but there are several subtle differences in the presentation and layout and in the department’s apparent focus. Overall, the report feels a lot more readable and digestible than in previous years.

One of the first signs of a change of approach is the lack of reference to a mission statement. Instead, there’s a clear emphasis on Inland Revenue’s role and the benefits for everyone that it delivers. As one of the online bookmarks to the Annual Report notes, “the tax and social policy system is a major national asset which underpins the well-being of all New Zealanders.” Under the headline, “We deliver three long term outcomes for Aotearoa New Zealand” page ten of the report summarises these long-term outcomes as Revenue, Social policy payments and Collaboration.

A more collaborative approach

Now, the last point about collaboration is interesting because this is a point picked up in other places in the report. In fact, the reference to collaboration is new. The word was never used in last year’s report, but this year it is a clear theme and I think it’s a welcome development. The report also talks about partnerships noting,

“We work with many other parties to help manage and run the tax and social policy systems such as tax agents, employers, KiwiSaver providers, financial institutions and community groups such as Citizens Advice Bureau.”

The report also references the international cooperation, such as with the OECD and tax agencies in other jurisdictions. And it notes that it exchanges financial account information under the Common Reporting Standards and the automatic exchange of information with almost 100 jurisdictions. As I’ve said in previous podcasts, the depth and extent of the international information sharing exchanges that go on are not well understood by taxpayers. In fact, probably are underestimated by many.

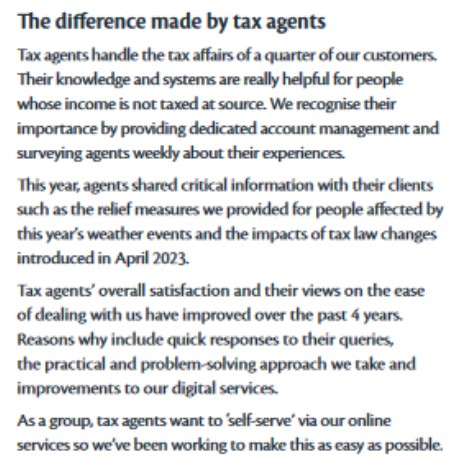

Reviewing last year’s report, I thought Inland Revenue had a bit of a bumpy relationship with tax agents, but I noted Peter Mersi was busy meeting representatives of professional bodies, clearly with the intention of addressing this particular point. And on the ground as tax agents we can see there’s been progress in this field, and we feel that there’s a definite shift in the attitude towards ourselves with greater cooperation.

It’s also made clear in the report that Inland Revenue sees tax agents as a vital part of the tax ecosystem.

This is a very welcome development in my mind and, as I said, mirrors what we’re experiencing on the ground. We certainly would like more support, such as easier phone access and definitely an updated playlist when we are put on hold. There are only so many times in the day I can hear Sierra Leone.

Overview of report

As I said, there’s a fresher feel to this year’s report which looks better organised and more readable for the general reader. If you’re wanting to dip into the report, page 11 sets out a good overview and then pages 14 to 38 summarise its work. There’s plenty of graphics and it’s very readable.

99% of income tax, GST and employment information returns are filed digitally, pretty near identical to the June 2022 results. It currently costs $0.43 to collect every hundred dollars of tax revenue. Back in 2015, that figure was $0.80 per hundred dollars of tax revenue.

Investigations and assurance – a mixed bag

I’m always interested about specific programs Inland Revenue has been running in the compliance space and I think this is a bit more of a mixed bag. According to the report it “identified or assured $973 million in revenue through our interventions.” This covers a number of initiatives. There is reference, for example, to advanced pricing agreements, which are prepared by multinationals in relation to agreements between a New Zealand subsidiary and its offshore affiliates. The idea is to make sure that Inland Revenue is satisfied that the transfer pricing regulations have been met and revenue is not being stripped out of New Zealand. Apparently 92 multinationals have active advance pricing agreements as of 30th June representing tax assured of about $440 million a year.

Real-time reviews

One of the other great things that the Inland Revenue has got as a result of business transformation, is the ability to pretty much live track applications that are being made. This topic is probably worth a podcast on its own to explain its capability. We understand from Inland Revenue presentations that it very carefully watched what was going on when applications for COVID support payments were being made.

With real-time reviews, if Inland Revenue sees something which on the face of it, looks incorrect it can take immediate action to defer payment or put that application under additional scrutiny before it’s paid out. According to Inland Revenue’s report, real time review of returns stopped, “$145 million of incorrect or fraudulent refunds or of or tax deductions at the time of filing”. Real-time reviews mean if a person is filing online and is constantly correcting a return and it appears this is because the person is after a certain result that will be identified by Inland Revenue for review.

International compliance

As I mentioned earlier, Inland Revenue is party to over 100 international information sharing agreements. According to the report Inland Revenue it received more than 600 voluntary disclosures over the last three years, resulting in more than $74 million in omitted overseas income now being assessed. That’s a bit of a surprise in my view and is probably on the low end in my view. We see quite a bit of movement in this area with people coming forward when they realise they haven’t complied with their obligations and we help them make the right declarations and pay the correct amount of tax.

In fairness this was an area, prior to the pandemic where in the wake of the introduction of the Common Reporting Standards on the Automatic Exchange of Information Inland Revenue was gearing up to throw quite a bit of resources at perceived non-compliance. Of course, that all went sideways, but with things sort of settling back down to a new normal, we may see Inland Revenue activity pick up again depending on resourcing.

Scope for more investigation work?

$397 million of the $973 million “assured” in the year stemmed from investigation work. Comparisons are not clear, but it appears well down on previous years. So, this is an area for improvement. By a perhaps slightly unfair comparison, the Australian Tax Office recently announced that it had picked up and collected an additional A$6.4 billion in the year to June 23 as a result of its tax avoidance taskforce.

This was a specific ATO initiative which scrutinised the tax returns and outcomes of the largest 1100 businesses and multinational groups in Australia to verify that they were paying the right amount of tax.

I expect Inland Revenue looked at that program and considered what lessons and opportunities a similar program might present. But it should be said that the Australian economy being bigger it also presents more opportunities for the ATO. The other thing about the Australian economy in transfer pricing terms, is it’s further up the value chain. In other words, more value can be created and captured in Australia, whereas New Zealand is more typically a price taker. Nevertheless, I think there’s room for improvement in the investigation space.

Increase in outstanding tax debt

As of 30th June, the total amount of general tax and Working for Families debt amounted to $5.8 billion. That’s up $600 million from the June 2022 year. At year end more than 524,000 taxpayers had a tax payment that was overdue although 315,000 owed less than $1,000. During the year Inland Revenue wrote off or remitted $754 million of debt compared with $689 million in 2022.

$231 million of the $754 million written off related to penalties and interest for taxpayers affected by COVID 19. In the wake of the pandemic if a taxpayer fell into debt as a result of COVID 19 Inland Revenue adopted a sympathetic view and was prepared to write off interest and penalties on such debt.

The rise in debt is a concern, but it’s a reflection of a number of things going on, not least of which the fact the economy is slowing down. Consequently, there are 44,000 more taxpayers with tax debt than in 2022. As ever, Inland Revenue’s working with those in debt to set up arrangements to pay off the debt. As I’ve said many times previously, if you’re in debt approach Inland Revenue and if you show serious intent to deal with the debt, it is generally willing to enter into an arrangement.

During the year they entered into 163,000 such debt arrangements. That’s up nearly 20% on the 140,000 for the previous year. As of 30th June 2023, there were still 77,000 active arrangements involving tax and student loan debt, which covered about $1.6 billion or just over a quarter of all debt.

Incidentally, on the measurement of tax debt to tax revenue, tax debt is about 5% of tax revenue, which isn’t bad by international comparisons, and certainly is an improvement on the 2013 year when it was nearly 10%.

More legal action

Inland Revenue also started to play harder with defaulters. It threatened legal action or issued notice of legal proceedings against 2850 taxpayers and 35% of those promptly settled in full or set up an arrangement. It’s also issued a thousand statutory demands involving other defaulters. I think we can continue to see expect to see the level of legal action continue to rise during in the current year.

More new hires

The key to any organisation is its people. And after the upheaval of business transformation which saw Inland Revenues workforce fall by 25% between June 2018 and June 2022 this is the first year since June 2015 that there were actually more new hires than exits. Inland Revenue’s total workforce rose by a net 203 persons, or 5.2% to 4,130. Staff turnover was 10.1%, which is a big improvement on last year’s 18.7%.

As for the profile of Inland Revenue, two thirds of its workforce are women. The average age of staff is 45.3, with an average length of service of 13.7 years. Now, the length of service has fallen in recent years, but it’s an improvement on the 11.1 years’ average service in the June 2014 year.

How much does all of this cost?

What’s interesting is that Inland Revenue didn’t spend all the appropriations it received from the Government for the year. The appropriations budgeted for the year was $735 million, but it actually only spent $691 million. That underspend of $44 million was partly due to challenges recruiting staff in the tight labour market and the timing of residual transformation activities. That underspend is going to be transferred to the current year subject to confirmation by ministers.

The operating expenditure on contractors and consultants fell to $42 million from $75 million in the previous year. And apparently the ratio of contractors and consultants operating expenditure to workforce spend was 10.3% this year, compared with 17.6% now.

Last year I noted that the Department had devolved authority to Madison Recruitment Ltd to provide extra staff, which didn’t terribly impress me because I think delegating authority outside the public service is not something a revenue authority should do lightly.

Inland Revenue engaged Madison Recruitment again in June 2022 to provide contingent labour to help with the roll out of the Cost of Living Payment scheme and wrap up of the COVID 19 support work. This engagement finished on 16th December 2022.

Areas for improvement

There are three specific areas where I think there is potential for improvement. Firstly, underspending by $44 million even allowing for a tight labour market is a bit of a concern. And so, I’d want to make sure that the appropriations are fully utilised to build the appropriate capacity.

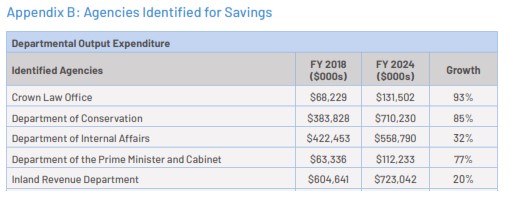

And on this I would just say that during the election campaign, National campaigned on cuts to civil service and Inland Revenue is one of those departments identified for savings. As I’ve noted, Inland Revenue has lost a quarter of its staff since 2018. In fact, if you look at the numbers National used for their policy, you can see that the increase in Inland Revenue’ spend since 2018 was 20%, whereas inflation since June 2018 is 23.4% (based on the Reserve Bank’s inflation calculator).

In other words, Inland Revenue has not been increasing its staff and spend above inflation. The Business Transformation program has delivered quite a lot and the report has some very interesting commentary on this. The estimated cumulative reduction in compliance costs for SMEs is thought to be around $925 million. The cumulative additional Crown revenue was expected to be $1.86 billion for the year and next year it projected a $2.8 billion. Internal Revenue is achieving its goals, but there’s always room for improvement. If the incoming Government’s finances are going to be tight which is what we’ve heard, it seems odd to be proposing reductions for a department which is actually very efficient and which gets a very good return on investment.

Getting better returns on investment

That said two of the areas where added investment measures return between $7 or more per dollar invested would be investigative capacity and debt management. In the area of debt management generally, we appear to be in the downside of the economic cycle so debt is bound to rise and to some extent there’s little Inland Revenue can do about that.

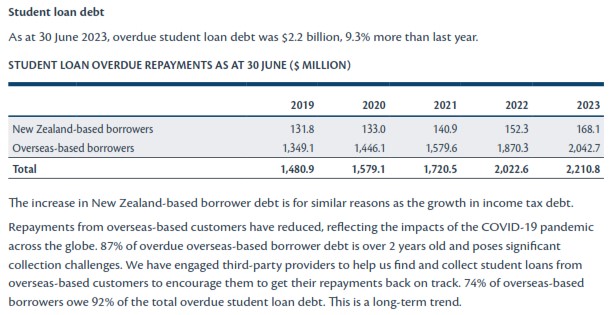

Student Loan debt a major area for concern

But there is an area where I think Inland Revenue really should and could be doing a lot more, and that’s in the student loan debt sector because the numbers are really quite large. The total amount of student loan debt rose by over 10%. And it’s particularly increasing in relation to overseas based borrowers.

Inland Revenue ran a specific campaign in May this year to remind those overseas based borrowers who had missed payments due on 31st March. It contacted nearly 75,000 such borrowers resulting in over 3000 instalment arrangements. But at this stage, the amount of overdue student loan debt now stands at $2.2 billion and over $2 billion of that is overseas based borrowers.

And this is where Inland Revenue does not seem to be as on top of the issue as it should be. I talked previously about the agreement with the Department of Internal Affairs in relation to child support. The same information sharing agreement is used to track down student loan debtors. During the year Inland Revenue received nearly 237,000 contact records from the Department of Internal Affairs. Through cross-checking its records for overseas based student loan defaulters, it managed to get hold of 88 defaulters resulting in 108 payments totalling $16,421. That’s pretty average, to put it mildly.

Time to rethink the Student Loan scheme?

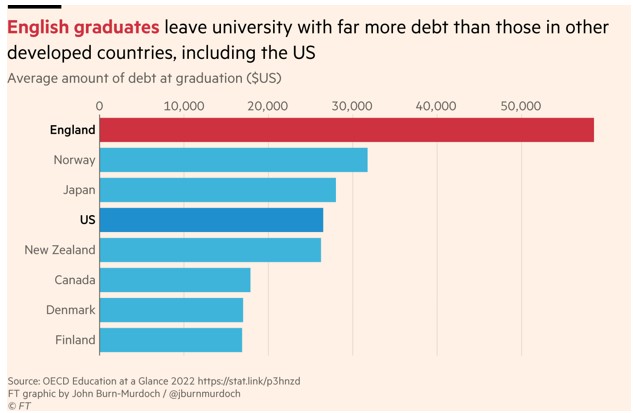

If we are looking at where to put extra resources, then there’s something else we need to think about in this area. Just adopting a big picture approach here maybe we should ask whether in fact the student loan scheme is achieving what we want. I came across a graph in the Financial Times which noted that English graduates leave university with far more debt than those in other developed countries, including the US. English graduates were leaving with debt in excess of USD50,000 (NZ$85,000). New Zealand graduates are just below the US with USD26,232 or NZ$45,550 on graduation.

And we have a large diaspora with over a million Kiwis overseas. We have a large amount of overseas student loan debt, but we also have a skills shortage. I just wonder whether as well as trying to find a better way to manage that debt we should be thinking more about encouraging people who’ve taken on student debt to stay here to meet those skills gaps maybe through debt moratoriums.

I would say overall for Inland Revenue it’s been a good year mostly, a difficult one at times, but it’s done a good job. However, I think the issue of debt management needs to be addressed swiftly and be properly resourced.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

An Australian case highlights the problems around removing GST from food, and as the Government’s financial statements for the year ended 30th June 2023 are released, instead of our tax cuts do we actually need more tax?

Last week I mentioned the retirement of Geof Nightingale and I also surmised that it wouldn’t be long before we heard from him again. And sure enough, this week he popped up on Mike Hosking breakfast show talking about the various tax policies on offer. After a tongue in cheek confession that this had all given him a bit of a headache, Geof then made the very wise suggestion that perhaps it is time to establish an independent fiscal costings unit so that during an election campaign the claims of the various parties can be scrutinised impartially.

As Geof noted, this is actually something the Labour Party proposed in the run up to the 2014 election. Now, given the claims, counterclaims and accusations this week about exactly how many families would gain the maximum benefit from National’s tax proposals, maybe this is something which should be looked at again. On the other hand, someone else has also suggested perhaps we can refer them for false advertising? Probably a bit too late for that really.

Removing GST on food – a legislative headache in the making?

Moving on, the multi-party debate on Thursday night on TV1 threw up several moments of light relief, including when the leaders were asked to comment on National’s foreign buyer tax policy and Labour’s proposal to remove GST from fresh and frozen fruit and vegetables. None of the leaders thought much of either policy.

This prompted moderator Jack Tame to challenge Winston Peters, noting that New Zealand First’s manifesto proposed the removal of GST from food. (For the record, the Greens and Te Pati Māori both propose to go further than Labour on this point). It turned out, however, that New Zealand First had literally just updated their manifesto, dropping the original proposal and instead proposing it would “secure a select committee inquiry into GST off basic fresh foods. We must examine if this would deliver real benefits for taxpayers before legislating for it.”

Maybe New Zealand First’s change of tack on this topic was prompted by a recent Australian tax case. In this case the court ruled that a series of frozen food products were subject to GST and could not be zero rated (or “GST-free”, in Australia’s somewhat peculiar GST terminology). In brief, what happened was that Simplot was marketing six frozen food products such as a fried rice or pasta product, each of which contained a combination of vegetables and seasonings, as well as grains, pasta and/or egg.

The case turned on around what constitutes a kind of food marketed as a prepared meal. If they were food, as Simplot argued, then no GST applied. However, if they were if they represented a kind of “food marketed as a prepared meal but not including soup as per Australia’s GST legislation“, then it would have been subject to GST.

After an exhaustive analysis, including examining the packaging and advertising, Justice Hespe ruled GST applied. But it appears that she was none too happy with the whole process and the legislation. She remarked in paragraph 141 of her judgement

“The legislative scheme with its arbitrary exemptions is not productive of cohesive outcomes. It has left the Court in the unsatisfactory position of having to determine whether to assign novel food products to a category drafted on the premise of unarticulated preconceptions and notions of a “prepared meal”. It may be doubted whether this is a satisfactory basis on which taxation liabilities ought to be determined.”

Now that’s probably justice speak for “You have got to be kidding that we have to do this every time.” But they represent pretty wise words of warning for future drafters of any New Zealand legislation removing GST from food.

More tax, not less?

As mentioned at the beginning, a key part of the election campaign has been the various tax proposals on offer, and particularly promises of tax relief in the form of tax cuts or threshold adjustments. Each of the parties, with the exception of Labour, have something on this. But in Stuff economist and previous podcast guest Shamubeel Eaqub said of both Labour and National that they were, “pretending somehow we don’t have long term big, long term issues that we need to deal with and time is running out.” He continued, “In terms of reaching surplus they are all saying getting back to surplus is important but how do you do it while giving tax cuts and spending on things we’ve already promised ourselves?”

I echoed his comments in part by saying that I didn’t believe the politicians of the two main parties are “being serious enough about funding what’s ahead.” And I noted that it was the coming challenges in terms of the ageing population and in particular related health care and superannuation costs that had prompted the last Tax Working Group to propose a capital gains tax.

Several other commentators weighed in as well, and I’d recommend reading in particular what I thought was some fairly insightful commentary from Gareth Kiernan, the Chief Forecaster at Infometrics. He noted something that’s been a theme of this podcast for some time, that New Zealanders are already paying significantly more tax due to the issue of bracket creep because income tax thresholds had not been adjusted since 2010. Governments had benefited from inflation moving people into higher tax brackets.

But in his opinion, this policy,

“It reduces discipline on government spending and muddies the tax and welfare decision for voters. It would be more appropriate for tax thresholds to be indexed to incomes or inflation, so that if any government wanted to alter the income tax rates or thresholds, they would need to articulate the reasons for their policy.”

He also went on to note,

“..in the current environment, one might argue that there needs to be more investment in infrastructure, and more funding for healthcare, and therefore taxes need to go up to pay for that. Alternatively, one might argue that there has been considerable expansion in government spending in recent years with few results to show for it, so spending needs to be reined in and taxes can be cut to go alongside that change.”

Now, I posted a link to this story on LinkedIn and it provoked a lively debate. A couple of people came back straight away with the reasonable assertions if we cut out wasteful expenditure and enforce the tax legislation, we would have sufficient income and that we may not necessarily get a better economy or better outcomes for people by increasing tax.

What is the state of the Government’s finances?

Now, the question of how much the Government spends is quite relevant in this particular example, because this week and providing some context, the Government’s financial statements for the year ended 30th June 2023 were released.

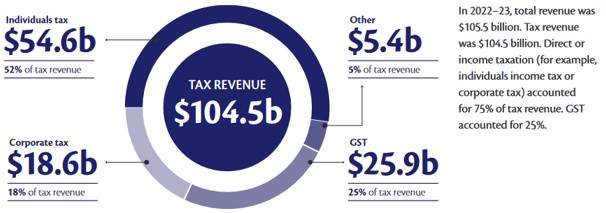

Tax revenue was up +$3.9 billion on June 2022 to a total of $111.7 billion. But that’s actually about $3 billion less than what was projected in the Budget in May. And the main reason for that fall is that corporate tax income at just under $18 billion, is -$2.4 billion below forecast, although higher withholding taxes on interest and dividend income has somewhat compensated for that fall. The GST take was bang on with what was projected at the Budget ($28.13 billion)

Ultimately the Government overall had an operating deficit before gains and losses of $9.4 billion. There’s been a lot of debate about government spending and core Crown expenses as a proportion of GDP were 32.2% of GDP, which is down from 34.5% in the June 2022 year. And the reason for that is the end of the COVID 19 restrictions and support that was given. Net debt is 18% of GDP, which is incredibly low by world standards.

And actually, here’s something we’ve I’ve mentioned before, but perhaps isn’t really known is that we are currently one of the few countries, according to our financials where the Government has positive net worth.

The government has net wealth of about 46% of GDP, whereas some countries such including Australia, which surprises me, are actually negative. Obviously, the big standout here is Norway, thanks to its trillion-dollar sovereign wealth fund.

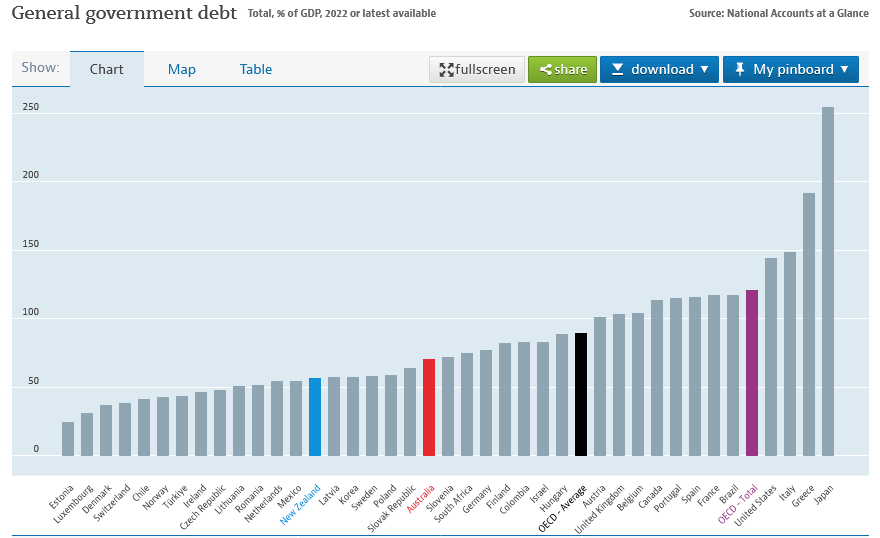

The OCED measures of debt is slightly different, but general government debt is still below the OECD average. But like the commentators who are thinking we should be looking at our spending, I’m of the view we need to be investing in our infrastructure beyond roads.

But one of the things that puzzles me and it’s always brought up about government spending, it seems, is that somehow $55 million was spent on a proposed cycleway across the Auckland Harbour Bridge, which never eventuated. And then there’s a significant amount of money that’s gone into mental health, but yet doesn’t seem to have found its way to the frontline. So, I definitely agree with the view that there’s questions to be asked about the quality of our spending and how effectively it’s deployed is the quality of our public service able to deliver on what’s required? It may mean the answer is a combination that we do need more funding, but also we may actually need to invest in the capacity of bureaucrats to actually deliver.

The climate change bills arrive for Auckland ratepayers and us all

But the key point I want to come back to about the costs ahead which we’re not hearing enough about from the two main parties, is how are we going to manage the impact of climate change? This week, remember, Auckland Council has just signed off on the process of what’s to happen with a buyout of 700 properties that were red stickered following the January and February floods. That’s going to cost a total of $774 million, $387 million of which is going to come from the government.

Of note here and it’s something quite a few people have raised a red flag about, is that although insured Category 3 property owners will receive 95% of the the pre-flood market value, those who were uninsured will receive 80%. This raises the issue of moral hazard – if that’s what’s going to happen why bother insuring.

This is a big issue that I think we have to discuss: how are we going to fund all of this? Then if we are going to be in a scenario where we have to be buying out property owners, is buying out uninsured people fair for the those who have insured themselves? Is this approach a fair cost both to the people in the affected local government area and those generally in the wider population, because that’s who’s funding these buyouts.

In my view this is going to be a bigger issue because, I want to repeat again, we have so much of our wealth tied up in property, and yet property is the asset class that is most exposed to the effects of climate change. We’ve had Auckland with 700 homes, and over on the East Coast there’s another 400 homes, I believe, where this buy out process is underway.

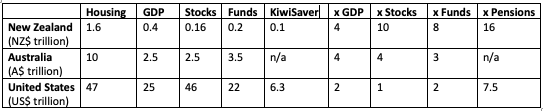

If we are going to be assisting property owners, and I believe we should, is the quid pro quo that the level of taxation on property rises? Bernard Hickey had some interesting stats in his daily Substack The Kākā around how much of our wealth relative to the country’s GDP is committed to housing. A total of $1.6 trillion, or four times our GDP, is committed to housing. But more importantly, although that’s not so out of line with other countries, it dwarfs our other investments

This royally skewed set of incentives is why our housing market is worth NZ$1.6 trillion, which is four times our GDP (NZ$400 billion), 10 times the value of our listed companies (NZX total market value of $160 billion), eight times larger than our total managed funds sector ($200 billion including NZ Super Fund and ACC) and 16 times larger than our only-very-marginally-incentivised household pension funds (Kiwisaver at $100 billion). For comparison, Australia’s housing market is worth the same four times GDP, but is worth four times stocks, three times and funds under management. In the United States, its housing market is worth twice GDP, once the stock market, twice funds under management and 7.5 times its comparable ‘subsidised’ household pensions market, which is known as 401k in America, rather than KiwiSaver.

Bernard believes, and I agree having looked at it when researching Tax and Fairness this overinvestment is a by-product of our tax settings. Therefore, if we change those tax settings around the incentive to invest in property that may change two things. One, we invest in more productive assets. And two, we raise the revenue to help deal with the coming crisis around climate change.

Will the Election change the discussion?

But at the moment it has to be said that funding the cost of climate change is not part of the two major parties’ discussions around tax, but who knows? My view is the debate around tax policy and our tax settings isn’t going to end with the Election next Saturday, it’s going to continue beyond that. In my view these issues around funding climate change will accelerate. If we can come to some form of multi-party accord on this, I think it will be better for us. But tax is politics, so don’t be holding out too much hope for agreement soon.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Last week The Post published a story about Roger and Shaun Nixon, father and son landlords who by The Post’s calculation owned at least 111 residential and lifestyle properties either in person or through a combination of trusts and companies. (In total across various entities and including commercial, industrial and retail properties the pair apparently own over 300 properties across the length of the country from Kaitaia to Invercargill, including properties on Waiheke Island and Omaha, where former Prime minister Sir John Key had a holiday home).

The story was produced as part of The Post’s Mega Landlords series, and I spoke to journalist Ged Cann on the question whether many of the homes in this property empire would ever re-enter the market for sale. As I explained, at the moment there are no tax incentives such as a capital gains tax or an inheritance tax (what we used to call Estate Duties), which could force the break-up of the Nixon’s holdings.

Estate and Gift Duties were first introduced in the 1890s, and were in part designed to provide a relatively good source of revenue for the Government, but they were also a means of breaking down large estates. The Liberal government of the time was concerned about accumulation of excess wealth and the related issue of inequality which drives a lot of discussion in this area. Inequality will exist in any society, no matter what the tax setting settings are. I think it’s a by-product of any modern capitalist society. Some people are extremely able to use their advantages of natural and inherited capital to make fortunes. And by and large, I don’t have a problem with that at all.

The question we should be addressing is how far we are prepared to accept inequality and what strains it puts on our social system. It’s a difficult question to answer. We have seen a rise in inequality since the 1980s and the end of the post-war consensus where higher taxes were seen as means of equalising society. And I spoke to Ged about one of those tax tools used, Estate Duty which disappeared just over 30 years ago.

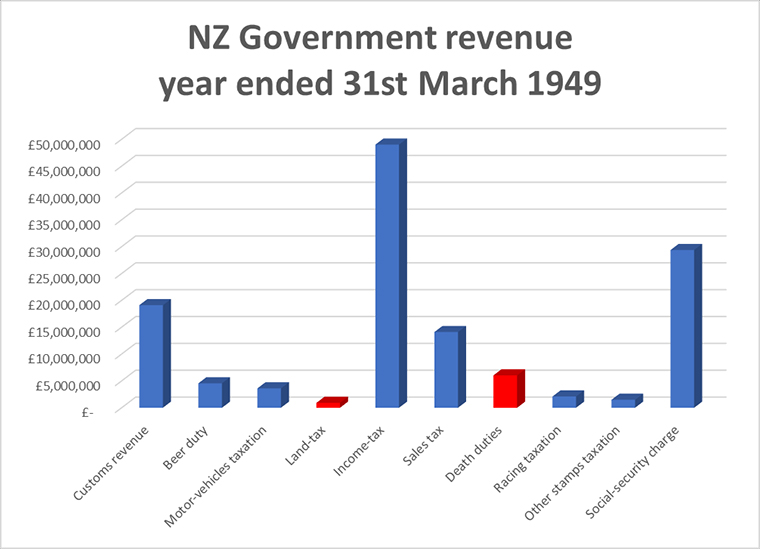

Estate and Gift duties were quite a substantial part of the tax revenue for New Zealand governments for a long period of time after the 1890s, right up until probably the turning point with the election of the First National Government in 1949. For the year ended 31st March 1949 the total amount of land tax, estate and gift duties amounted to just under £7 million of the government’s £130 million revenue. In other words, it was the equivalent of 5.3% of the total tax take for that year. If you were to project that forward, it would be the equivalent of $5.7 billion using the June 2022 numbers. So, these taxes were a very significant proportion of past governments’ revenue.

Whatever happened to Estate Duty?

Starting with the election of the First National Government the exemptions from Estate Duty were widened. This started to undermine the theory we’ve often discussed here and which I strongly support, of a broad based, low-rate approach to taxation. The broader the tax base, the lower the tax rate you can apply. And to a large extent this was the case with estate and gift duties.

But what happened was that exemptions for Estate Duties (and Land Tax) began to be expanded. And therefore, as the exemptions expand, the tax base is narrowing and then the tax take starts to fall away. And gradually, over time, the numbers diminished to the point of insignificance. Land tax was abolished in 1990 and Estate Duty reached its end point in 1992. Gift duties, for whatever reason, lingered on until 2011, before they went on the not on reasonable grounds that the barely $2 million revenue collected was far outweighed by the compliance costs.

The question that should come up is whether, in fact, the abolition of Estate and Gift Duties was a wise move on two points, firstly for maintaining a broader tax base. And secondly around this question of inequality, because Estate Duties are something that can hit estates very, very hard particularly where perhaps too much is tied up in illiquid assets, such as property. This is something I’ve seen quite a lot in the UK with the effect of what is now called Inheritance Tax.

To repeat a point I have made before, the absence of Estate and Gift Duties makes our system unusual because we don’t have a capital gains tax. (We’ve also removed stamp duty although by and large, tax theory has that stamp duties are pretty inefficient taxes. Still, they linger on everywhere else). So, we have no taxes which could be part of breaking down large estates. We have to accept whether that’s a good or bad thing.

Following IAG’s move do we need to broaden our tax base to deal with climate change?

My view is that we ought to be thinking about the question of broadening our tax base. And in that context, I’ve been thinking quite a bit on this question of estate and gift duties, because this week there was another reminder of an issue I keep raising – the growing costs of dealing with climate change.

The insurer IAG announced this week it will not offer ongoing insurance for properties in Category 3 of the Government’s Land Categorisation framework for regions affected by the floods earlier this year.

The cost of the property damage this year by those events is currently several billion and climbing. Of course, property owners are the persons that are most closely affected.

One of the doubts I have about National’s proposed foreign buyers tax is about the type of properties foreign buyers are likely to be purchasing. In Auckland, there is a growing number of suburbs where the average price is $2million. But foreign buyers aren’t necessarily wanting to buy a rundown villa in Grey Lynn or Devonport, they’d probably be looking at flashier properties in coastal areas. However, these coastal properties could now be more exposed to climate change which could be a factor in them deciding not to purchase.

Of course property owners, maybe including the Nixons, have already been affected by climate change and if they are struggling to insure their properties, they will be looking to the Government for assistance with this. And so it seems to me we are rapidly reaching a break point because we’re not taxing capital and property in particular. This is going to create a huge issue between those on one hand who have property and want government assistance when their property is flooded out or damaged beyond repair and insurance is limited or not available. On the other hand, there is a group who don’t have property and can’t get onto the ladder, who will, through their taxes end up paying for the former. This dichotomy sets up a whole social strain, which I don’t think we really want.

To repeat, the thing about this story of the megalandlord Nixons is how it illustrates to me this dilemma we have created around the taxation of capital and the preference for property as an asset class.

So why is the New Zealand Super Fund taxed?

There were some very interesting responses to last week’s commentary about the New Zealand Superannuation Fund’s (“the Super Fund”), retiring CEO Matt Whineray’s remarks on the fund’s tax status. (Thank you again to all my readers and listeners for your contributions). The question was asked, ‘Well, why does it pay tax?’ The answer, as I indicated in last week’s podcast, it was designed as such when the Super Fund was being set up prior to when it actually started investing 20 years ago this month.

“There are two main issues surrounding the tax status of the proposed super fund. The first of these is the tax avoidance opportunities that would be created if the fund was tax-exempt. The second is whether poor incentives would be created regarding investment behaviour.

…By making an entity tax exempt, the government effectively gives it an asset that it can trade with taxable entities. Current tax-exempt organisations such as charities have engaged in complicated schemes to take advantage of this kind of opportunity. …

We consider that making the fund tax exempt will create an opportunity for this kind of avoidance activity.”

The driving force of this paper was concern that giving the Super Fund tax exempt status would give it poor incentives. And so, the fund was set up on that basis. (It’s also interesting to note that the paper assumed the Super Fund would be contracting out most of its fund management activity. However, as we know, the Super Fund is now one of the largest fund managers in the country).

Changing the FIF rules

Back when the Super Fund was being established the tax treatment under the foreign investment fund regime was very different. There was what we call a “Grey list” that applied to investments in several countries such as the US, Australia, UK, Germany, Japan and others. Investments here were only taxed on dividends and capital gains would be taxed under the normal rules, similar to those we have now for investing in Australia and New Zealand. The amount of tax payable on these investment would not have been quite significant under those rules.

However, in 2006, proposals were introduced establishing the current Foreign Investment Fund regime which took effect from 1st April 2007. Now, the interesting thing is that I cannot see any commentary or submission to the Finance and Expenditure Committee by the New Zealand Super about the changes, although there’s plenty of commentary from the Corporate Taxpayers Group and others. As I mentioned last week, some 3,400 submissions opposed the changes, and only two were in favour. So of course, the measure went ahead.

From that point the New Zealand Super Fund started to pay a lot more tax. (In the year to June 2008 the fund had a loss of $704 million but had a net tax bill of $164 million because of the changes to the FIF regime). The effect of the FIF regime was described in a submission the New Zealand Super Fund made in 2018 to the last Tax Working Group. It said it would like to be tax exempt because as I noted earlier it’s the only sovereign wealth fund in the world which is taxed. Its tax status also creates some issues when it is investing overseas. In support of tax exempt status, the submission (signed off by then acting CEO Matt Whineray) noted.

“The fund’s tax position can be volatile depending on the performance of the fund and the contributors to that performance. This is often illustrated by our effective tax rate. For example, our effective tax rate was 3% in 2015, 96% in 2016 and 20% in 2017. The main driver of this volatility is how our physical global equities are taxed under the fair dividend rate regime. In simple terms, this means that in any given year, if our return in global equities exceeds 5%, then our tax rate will be lower than 28%. And if our returns are less than 5%, then our tax rate will be higher than 28%.”

Another interconnected issue for the Super Fund is that as so often is the case, I think Governments rather like the tax revenue from the Super Fund. However, as the Fund’s Tax Working Group submission noted if it was tax exempt it would not be forced to sell assets to pay “the Government provisional tax with the Government then turning around to pay the Fund contributions, thereby removing the need for practical work arounds in terms of offsetting provisional tax”.

As I said, way back in 2000 when they were considering the tax status of the New Zealand Super Fund, the FIF regime was very different. And I wonder whether if they had foreseen the impact of the FIF regime that was introduced from 2007, whether they might have rethought the decision to tax the Fund.

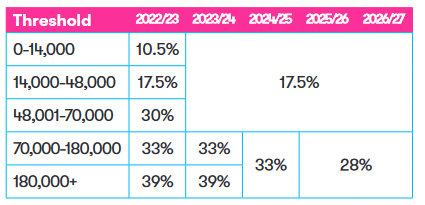

Act is now accepting that cannot happen but instead the top rate from 2026 will be 33%. What it has also said, and this is interesting, is that the top 39% rate will remain until then.

One of the proposals in ACT’s “Alternative Budget” is the Government will stop making contributions to the New Zealand Super Fund. But what won’t change, however, is the tax status of the fund, and it will still be taxed.

Now the ACT numbers are quite detailed, and they note that the expected tax revenue from the New Zealand Super Fund will actually drop by about $100 million over the three years to June 2027 period because of lower Government contributions. (Incidentally, in measuring debt-GDP ratio ACT’s Alternative Budget excludes the $65 billion value of the NZSF which rather unfavourably distorts the ratio).

ACT also proposes winding back the KiwiSaver member’s tax credit (the Government contribution you receive if you make contributions of at least than $1,043 a year), for higher income earners. Instead, it will be capped at 5% of a participant’s taxable income. The maximum subsidy amount will reduce by 3% per dollar of income above $48,000, reducing to zero by around $65,000.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.