Tax continues to feature heavily in the Election with the ongoing debate over the validity or otherwise of National’s proposed foreign buyer tax. But away from the election, it has been a busy week in the tax world. By far the most interesting story, partly because of its source, but also how it speaks to the structure of our tax system, is the commentary from Matt Whineray, the outgoing chief executive of the New Zealand Superannuation Fund (NZSF), about the fund’s tax status.

In an interview with the New Zealand Herald’s Markets with Madison, he remarked on the NZSF’s tax status, noting that since the fund began investing in 2003, it had paid nearly $10 billion in tax, including $2.2 billion for the year to June 2022.

This makes it by far and away the largest single taxpayer in the country. He thought this was rather nonsensical and that the fund really should have tax immunity status in line with many other sovereign wealth funds around the world, (including ACC and the Reserve Bank of New Zealand, both quite substantial investment funds). “My wish would be that we didn’t pay tax because I think that would solve a few issues.”

A nonsensical money-go-round?

He questioned the practice of the NZSF returning money to the Crown in tax, and the Crown in return contributes to the fund annually. “If I take my wallet out of this pocket and put it into this pocket, I haven’t got richer.” The problem, in his view, was exacerbated when the Crown stopped contributing to the fund completely, as it did for almost a decade between 2009 and 2017.

It’s interesting to hear such commentary from Matt Whineray, which highlights an anomaly about the NZSF, in that it is a sovereign wealth fund, but it pays tax, which is highly unusual around the world. In fact, I’m not sure there are any other sovereign wealth funds which do pay tax. (It’s an issue Whineray’s predecessor Adrian Orr also raised, ashas Whineray previously).

Now when the NZSF was set up 20 years ago, the rationale behind it paying tax was this would help it make sound investment decisions based on investment principles and not by tax considerations. And in a broader sense, that’s not unreasonable. I always tell my clients, don’t let the tax tail wag the investment dog. Think in the longer-term investment and returns rather than the short, potentially shorter-term tax implications.

A “Fair” Dividend Rate?

Someone else this week commenting on this question of the tax status of savings was financial planner Rachelle Blanch speaking to Susan Edmonds of Stuff.

Rachelle thought it was time for a review of the Foreign Investment Fund (FIF) regime, particularly in relation to how it applies to portfolio investment entities such as KiwiSaver funds. Now, the FIF regime and the Financial Arrangement regime are the two main reasons the NZSF pays so much tax. That’s because both regimes tax unrealised gains and there will be substantial unrealised gains in investment funds.

As the story in Stuff noted, under the FIF regime KiwiSaver funds and the NZSF must use what’s called the fair dividend rate in respect of their overseas shareholdings. This deems 5% of the opening market value of the investments held at the start of the tax year to be taxable income. Now obviously as KiwiSaver funds grow in size, and they diversify out of the New Zealand market as the NZSF has done, then the amount of tax payable as a consequence of the FIF regime will increase. However, unlike individuals or trusts, who can switch methods to mitigate the impact of a drop in values of some of investment funds by adopting what we call the comparative value method, KiwiSaver funds and the NZSF can’t do that.

How much tax is payable under the FIF regime is not at all clear. The NZSF is probably the only entity which can give a pretty accurate gauge on that. But to give you some idea of the total tax that might be payable – the Financial Markets Authority produces an annual report each year on KiwiSaver funds, and it notes that for the year to June 2022, KiwiSaver funds paid over $256 million in tax for that year. Remember in the same period, the NZSF paid over $2.2 billion.

Rachelle Bland has raised a very good question as to whether, in fact, this is an appropriate tax policy response where people have long term savings. She describes it as effectively a capital gains tax. Another way of looking at this, and it’s how I describe it whenever explaining the regime to overseas clients, is that it operates as a quasi-wealth tax.

As I said, there’s no mitigation for significant falls in stock markets. Unlike a capital gains tax regime which taxes on a realisation basis you can decide to realise capital losses and offset them against capital gains. You can’t do that under a FIF regime. Therefore you have this situation where the value of investments are falling but you’re still paying tax on the value of those investments. And that’s been the scenario for quite a few funds over the past 12 to 18 months.

What about a tax exemption then?

It’s not surprising then that quite apart from this anomalous washing – as Matt Whineray referred to the process of cycling funds from the Crown to the NZSF and then back in the form of tax – there’s also calls for some form of tax exemptions for KiwiSaver funds. You see such tax exemptions around the world for other pension schemes. New Zealand is yet again, a bit of an outlier here. The reason such exemptions were taken away in the late 1980s is they are costly. However, in overseas jurisdictions where tax exemptions apply to pension schemes withdrawals are taxed, whereas in our system we apply what we call a tax-tax-exempt approach where the contributions are made out of after-tax income, the schemes are subject to the ordinary taxation rules, but any withdrawals are exempt.

What’s the most effective approach? Well, that’s still a matter for debate. But one thing to keep in mind is that tax does have an impact on the long-term return of funds. Now, whether anyone is going to do anything about this is very questionable. The FIF regime in its current iteration has been in place now since 1st April 2007, and it generally works pretty well. The rules were very controversial when they were first proposed. There was an absolute storm of protest when they were first proposed, with Parliament’s Finance and Expenditure select committee receiving 3,400 submissions against the introduction of what is now the FIF regime, and only two in favour. In the face of this criticism, they were actually reshaped and now everyone has got used to working with the regime.

And this perhaps is the critical point. Governments appreciate the tax paid by the NZSF and KiwiSaver funds. The total tax for the year ended 30th June 2022 from those two sources probably represents just about 2% of the total tax take for that year. Therefore, changing the tax treatment for the NZSF and for KiwiSaver Funds would be an expensive move even if as a trade-off the Government might not then need to make any more contributions to the NZSF.

Wrong sort of investment signals?

Given the short-term pressures at the moment on the Government’s books, I think any move in this area is not going to happen. But I also consider it underlines a scenario where we’re prepared to tax savings under the current tax system, but generally whole asset classes, such as property, the bright line test excepted, are outside the tax net. This treatment sends an investment signal which politicians aren’t prepared to address.

Where does investment get directed? The evidence we have points to it being directed into relatively unproductive residential property investment as opposed to the likes of KiwiSaver funds, which will invest in productive businesses.

The discussion we’re not having

Now, this is a discussion we’re not having at the moment about how the tax system and investment interacts. As I’ve said in previous podcasts when you consider National is proposing removing commercial property depreciation on non-residential property again, (as is Labour for its part) in both cases to fund some form of tax cuts this to me sends the wrong signals. We’re basically directing funds away from investment in our economy into consumption.

But this is not a discussion we’re going to have because although politicians quietly recognise that whatever we the electorate might say about the impact of tax in the back pockets – and we’ll happily all take tax relief, tax cuts, how you phrase them – we also like the services tax provides. So, this dichotomy exists. We’ve got to maintain services as far as possible but not want to pay for them. But as I’ve said repeatedly, I think the under taxation of capital is an unsustainable position long term.

Donations tax credit review announced

Moving on, Inland Revenue just carries on carrying on regardless of whether the Government is out campaigning. It has been busy churning out quite a lot of interesting material. But two particular initiatives happened this week.

Firstly, on Friday, it announced it is going to undertake a review of the rules relating to the donations rebate rule. This review is part of the Regulatory Stewardship programme required of all state agencies in respect of the rules they administer. In this case, a review is going to assess whether the donations tax credit regime is operating effectively, is achieving its policy intent, and how it compares internationally.

Inland Revenue will open up consultation with an aim of undertaking this review and completing a report, setting out its findings as well as any recommendations by mid-2024. Interested parties will be contacted on this. I imagine you can expect the Charities Commission, some more major charities, would be approached. I think the main accounting bodies, together with the New Zealand Law Society will also be approached for comment on the matter.

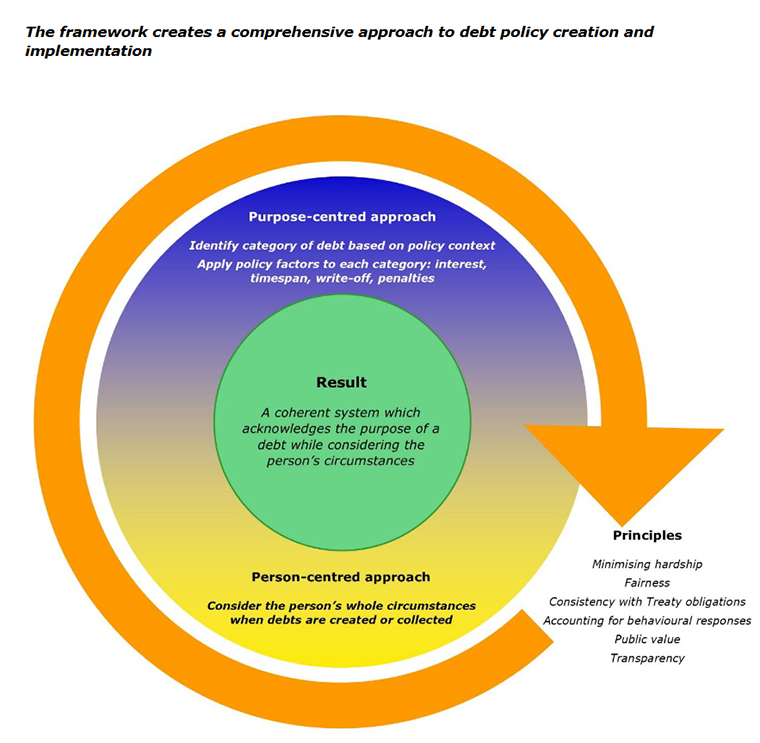

A fairer Government debt policy framework?

The second Inland Revenue initiative and probably something that’s going to have more immediate impact ties into the rather strange case we talked about last week involving the Nelson woman who got herself into a whole heap of trouble with Inland Revenue and decided the best way out of avoiding a $365,000 tax debt was to sell her property worth $845,000 to a UK company. The Official Assignee took a dim view of the idea and obtained a court order striking the sale down.

Leaving aside the oddities involved the case is relevant for the important question of tax debt and other debt that’s owed to the Government. According to the New Zealand Herald story reported last week, as of 30th June 2023 Inland Revenue is owed nearly $5 billion.

Now, both the Tax Working Group and the Welfare Expert Advisory Group took a look at the question of debt owed to the Government as part of their reviews, and they recommended there should be some form of all of government approach to debt. Firstly trying to prevent debt arising with the Government, but also how each relevant government agency responds and manages that issue.

Consequently, a policy framework for debts the Government is owed has now been developed and has been signed off by the Cabinet. Inland Revenue this week released its report and background details on this framework.

There’s quite a bit to consider in here, not just the $5 billion Inland Revenue is owed but the other debts built up, primarily with the Ministry of Social Development and also with the Ministry of Justice.

According to this report, at present 762,460 New Zealand residents collectively owe $4.68 billion of debt to these three agencies – Ministry of Social Development, Inland Revenue and the Ministry of Justice. More than a quarter of these persons owe debt to two or more agencies and 6% that’s over 45,000 people owe a debt to all three. Furthermore, around three quarters of this debt, so that’s well over $3 billion, is owed by low-income individuals, many of whom rely on government benefits as well. 13% or just over 99,000 people owe more than $10,000 to the Government.

More than 85% of those who do owe a debt have owed it for more than a year and about 45% cent, an incredible number, have owed debt for at least four years. Finally, Māori and Pacific people are overrepresented in almost all categories of debt a sadly quite typical issue.

The debt policy framework is trying to ensure is that debt recovery is fair and effective and avoids exacerbating hardship. And above all, it aims to prevent debt occurring in the first place and not exacerbate issues.

There are three main parts to the framework. Firstly, a set of overarching principles for creating and managing debt. Then secondly, a purpose centred approach which classifies debt into different groups according to the policy purpose and discusses how different settings might be appropriate for some purpose and others. And then finally, what’s called term to person centred approach, which takes into consideration the personal circumstances, with focus on consideration of financial hardships, as I said.

These debt issues tend to exacerbate and build on each other leading to a circle of despair. $10,000 of debt doesn’t sound like a lot, but for very low-income people it seems like an insurmountable mountain.

Anyway, this framework has been signed off by the Government after feedback from quite a number of interested agencies. For example, the Citizens Advice Bureau, the Methodist Alliance, the New Zealand Council of Christian Social Services, the Salvation Army, and a whole range of other non-governmental organisations. Hopefully this feedback will build a better framework for the practice of managing this debt.

Good but Inland Revenue also needs to do its part

I welcome this initiative, but I also think that as part of it, Inland Revenue needs to be also considering its approach to debt management, such as the effectiveness of the late penalty regime, and how efficiently it is on top of managing debts, because if the debts get away from people, they just give up. That’s what my experience has shown time and again and it’s also what Inland Revenue has experienced.

I think it’s still a good step forward, particularly, in trying to bring a coordinated approach because there’s nothing more infuriating to someone who might be unlucky enough to find ourselves in a position of debt with two or three agencies, and finding that the approach taken by each of those agencies is different.

The Tax Working Group recommended a single Crown agency to manage current debt should be established to deal with this issue. That does not seem to have been part of these recommendations at the moment, maybe it might be picked up at a later stage. Nevertheless, it’s a step forward in the right direction and we’ll hope that it starts to address these issues of managing the debt fairly and efficiently for people.

The $5 billion PREFU hole no-one is worried about

And finally, this week, back to the Election. We’re still hearing plenty about tax in the election campaign. Politicians are all out on the trail telling us everything that’s going to happen or not happen. This week the formal opening of the government books happened with the release of the Pre-election Economic and Fiscal Update (PREFU). There was plenty of differing interpretation about the state of the government’s finances going forward.

But there was a wonderfully interesting little snippet which Newsroom picked up on, and that was the impact of next year’s Matariki public holiday. Matariki always falls on a Friday, and next year it falls on 28th June, which is the last working day of the fiscal year to 30th June 2024. And because of that, the cash that would come in on that day, which represents about $5 billion of GST and provisional tax won’t actually hit the Government’s coffers until the following Monday, which is 1st July and the start of the following tax year. So, on the face of it, the Government’s going to be $5 billion short of cash for the current year ending 30th June 2024.

As a Treasury spokesperson said, “This public holiday effect is expected to affect the Crown’s tax receipts but not tax revenue, since Inland Revenue will calculate accrued tax revenue as at 30 June 2024 as it normally would at any other year end.”

And for the record, this won’t really affect individuals because we file tax returns to 31st March each year. Furthermore, Inland Revenue won’t penalise people for making a payment on 1st July, the first working day after it was due because Inland Revenue hasn’t switched over to a seven-day banking. So nice quirky little story to end the week.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

It’s been a busy week in the tax world. The Taxation Principles Reporting Bill passed its third reading in Parliament and very shortly will receive the Royal assent. Now this was the bill introduced at the time of the May Budget, the purpose of which was to provide a statutory reporting framework and required the Commissioner of Inland Revenue to provide the Minister of Revenue with an annual report on the operation of the tax system.

This report would outline aspects of the tax system against a set of tax principles such as equity, efficiency and certainty. As commentary provided by Inland Revenue to the Finance Expenditure Committee noted. “These principles are often considered when designing changes to a tax system”.

Tax being political the Government also wants this bill to

…help improve the public’s understanding of the tax system and encourage informed debate about its future. New Zealand has seen several Tax Working Groups and Committees over the last 20 years, with the most recent being the 2019 Tax Working Group These reviews have offered useful insights into the operation of the tax system and suggestions for improvement. These reviews have also highlighted areas of the tax system where information is lacking, which makes a fully informed debate on some aspects of the tax system more difficult.

The bill requires the Commissioner of Inland Revenue to prepare and publish an annual report which considers the tax system measured against the principles included in this bill.

What will happen is Inland Revenue will produce a short form report annually with a full report every three years. The first full report will be produced in 2025 with the shorter version reports produced in the interim years starting later this year. The intention is to align the requirement for this report to be produced the second calendar year of each parliamentary term.

There’s been some discussion around whether we need this bill and how does it sit within the Generic Tax Policy Process (GTPP)? You could say it’s an extension of the GTPP and of course, it does mean that we can have a look at some of the tax policies that have been put out by the various parties and compare them against the principles set out in this bill. And I’ll be doing that a little later on. The politicians may find this new bill is something of a double edged sword.

A Digital Services Tax just in case…

It so happens a digital services tax bill was introduced on the last sitting day of this parliamentary term which is a bit of a surprise. Digital services taxes (DST) have been talked about for some time but have generally not been brought into effect. They’re obviously not favoured by the targets, the digital giants such as Google and Facebook. But they are a tool that many governments around the world have been considering implementing.

The ongoing OECD Pillar One and Pillar Two negotiations are intended to eliminate the need for these taxes. In fact, it’s a condition of the introduction of the OECD model that any digital services tax in effect would be repealed.

The Government’s actually been looking at a DST for some time. There was a discussion document back in 2019 on the topic. That said, it still was a bit of a surprise to see this bill pop up at this particular time. Arguably, you could see it as a bit of politicking. The key thing is the Government is already committed to not introducing a DST until 1st January 2025 at the earliest. Now Inland Revenue and Treasury have said it will be handy to have the legislation ready just in case the OECD deal falls over. So that’s a reason given for this bill being introduced now.

The DST would target multinational multinationals with global revenue in excess of €750 million per year from digital activities and New Zealand revenue from these activities which exceeds $3.5 million per year. The DST taxes the revenues rather than the profits, because then it doesn’t require trying to establish a connection with a multinational’s physical presence in New Zealand. The rate to be proposed is 3%, pretty standard compared with others around the world.

This bill is a more fallback measure and it’s interesting to see where it stands that they’ve made this move now. But many countries have DSTs, Britain is one, France another and India is probably the biggest exponent of them. And as I said, the Government’s basically saying, ‘We want this in our back pocket in case the OECD Pillar One and Pillar Two deals fall over.’ These are still very much up in the air for discussion, as we’ve mentioned in previous podcasts.

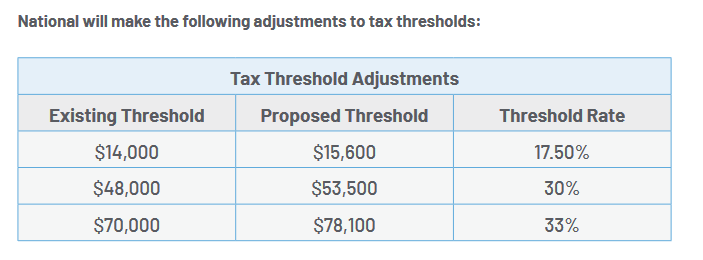

National unveils its tax policy

But the big news this week would have been the launch of the National Party’s tax policy on Wednesday, and it landed with quite a thump and contained quite a few surprises. National had already signaled well in advance that it proposes to increase thresholds by 11.5%. As regular listeners to this podcast will know my view is tax threshold increases are long overdue.

What about Working for Families abatement?

National has an identical proposal to that of Labour to increase the Working for Families In-Work Tax Credit by $25 to $97.50 per week starting next April. There’s a commitment that the current $42,700 abatement threshold for Working for Families will rise to $50,000 from 1st April 2026. This is also a Labour Party commitment. But as I said to a number of media outlets, the problem is that the Working for Families abatement threshold already kicks in at very low level and in fact if they had been adjusted for inflation since the last adjustment in July 2018, it would now be $51,800.

Both parties promising to raise the threshold to $50,000 in three years’ time is frankly a little off in my view. It just compounds the problem these families at the lower end of the income scale face with what we call high effective marginal tax rates because of the abatement level of 27 cents per dollar above the $42,700 threshold. This issue isn’t being addressed but instead the can has been kicked down the road.

But on the other hand, there is the proposed FamilyBoost childcare tax credit, which is worth up to $150 per fortnight for couples with childcare costs. This will be no doubt welcome, but the trade-off is the loss of the proposed extension of the Early Childhood Education subsidy that Labour included in its May Budget.

All good but how are you paying it?

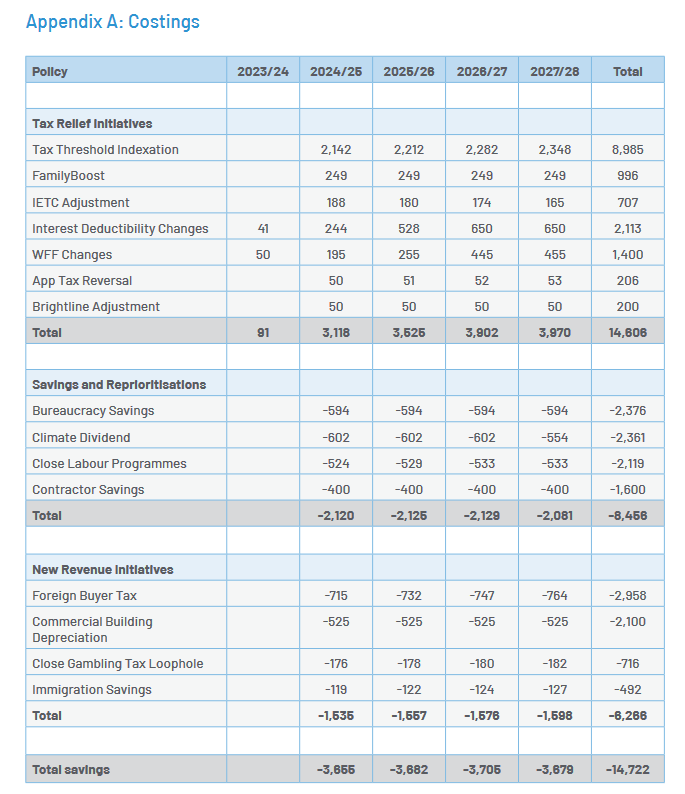

In fact, the controversy around National’s plan has broken out over how it’s going to fund this program and of these proposed tax adjustments. There are several surprises here, the first of which was this proposed foreign buyer tax. Currently no one who does not have permanent residency can buy property. National are proposing to keep that in place for properties worth less than $2 million, but to allow properties worth more than $2 million to be purchased. But that would be subject to a 15% tax, which sounds a bit like a stamp duty. We haven’t had stamp duty, by the way, since 1999.

The controversy is around the numbers involved, which do seem very optimistic. Revenue of $700 million a year would imply sales of at least $6 billion in property. I’ve seen a report in the New Zealand Herald which suggests that actually something like 60 to $65 million is more reasonable. But the proposal also runs up against questions that certain of our double tax treaties and trade agreements have clauses that would not allow such a clause to be a tax to be introduced, notably Singapore and Australia.

But now it’s been pointed out that what we call non-discrimination clauses in double tax agreements may apply to this. In which case these income assumptions of tax revenue would be well short.

There is a proposal to close an online casino gambling tax loophole as its described. This would require offshore operators to pay GST and register and report their earnings for tax purposes. The suggested penalty for non-compliance would be IP geo blocking of services. It subsequently emerged that the Government got $38 million in online GST for the year ended 31st March 2023. This is a result of the so-called “Netflix Tax” which, ironically, was introduced by the National Government in 2016.

National assume the measure will raise $180 million, and I admit I raised my eyebrows when I saw that suggestion. This seemed high to me particularly when I considered that the proposed DST I mentioned earlier is expected to raise about $55 million a year. Online gambling would seem to be a similar type of activity, if not quite identical, so assuming they’re going to raise 2 to 3 times as much as a DST struck me as optimistic.

National Party documents seem to be saying this is essentially a corporate income tax. In which case, it appears this particular tax could also be caught by the anti-discrimination articles in double tax agreements. And that could mean a $140 million shortfall in National’s projections.

Good news for singletons…ironically

On the other hand I do think the proposal to increase the Independent Earner Tax Credit threshold to $70,000 from its current $48,000 is a good initiative. I’ll be honest, I was a bit surprised that Labour didn’t think to do something similar as part of its budget earlier this year. But there is actually a little bit of an irony in that this Independent Earner Tax Credit was actually going to be abolished by National under the last budget it published in May 2017. But that measure never went through because of the change of government later that year.

A counter-productive proposal and more irony

But I think one of the measures that should attract more controversy, is the proposal to remove depreciation for commercial property which includes factories. Now this is something that Labour have also proposed to pay for the proposed removal of GST on fresh and frozen fruit and vegetables.

This is a counterproductive move in my view. The proposal refers to “commercial building” but the depreciation deduction covers all sorts of property such as factories, farming sheds etc. These all depreciate. It was recognised by the last tax working group, that depreciation on commercial and industrial buildings should really be re-introduced, introduced and is actually quite common around the world.

A measure that takes it away seems to be counterproductive particularly if we’re talking about encouraging investment in productive assets. There’s also the added irony that this would be the second time that a National government had removed that depreciation to pay for tax cuts.

Overall there’s an awful lot to pick apart here and the devil is always in the detail. This does seem to point to the revenue forecasts being on the optimistic side, certainly in relation to the foreign buyer online gambling taxes.

Good news for landlords…mostly?

On the other hand, there was also no surprise about the reintroduction of interest deductibility for residential properties. But what is interesting about this move is that’s it’s not simply being fully restored as of a change of government. What’s proposed is for it to be brought back in over a two-year period from 1st April 2024. At present the proportion which would become non-deductible is due to rise to 75%. Instead it will stay at 50% non-deductible and then starting 1 April 2025 the non-deductible proportion will year drop down to 25% before becoming fully deductible with effect from 1st April 2026.

Reducing the bright-line test back down to two years will be welcome for a lot of people. The unintended consequences arising from the extension of the period to first five and then ten years were giving me and plenty of other advisors a lot of work as we try to unpick where the boundary was, and what transactions were caught. So that’s probably quite welcome.

On the other hand, there’s a surprise that nothing has been said about allowing losses from residential property investment (“loss ring-fencing”) to again be offset against other income. This hasn’t been allowed since 2019. It also appears that the proposed increase in the trustee tax rate to 39% will still go ahead. I had heard whispers to that effect, and although there’s been plenty of pushback on the proposed increase it will be interesting to see what eventually emerges.

Now about those Tax Principles…

Having just got a new Tax Principles Reporting Act in place, it is interesting to compare the principles set out in there against these policies. You’d have to say for now, not entirely a big pass. Indexing the thresholds is a reasonable measure, as I said, but that’s a minor point. The tax on foreign homebuyers probably could be said to be questionable in terms of equity. Why should one group of people suddenly get a far higher tax charge than other groups of people in reasonably similar circumstances.

The removal of depreciation for commercial and industrial buildings doesn’t seem to fit with the tax principles. And since we’re talking about things that wouldn’t pass that bill, I’d have to say removing GST on fresh and frozen fruit and vegetables wouldn’t pass muster either.

Sucks to be a student…and an Auckland ratepayer?

But to summarise, tax is politics, so we can expect plenty of politicking. There’s no doubt that the tax relief in terms of the changes in the thresholds will be welcome, but there’s going to be quite a few losers as well. Following the announcement I spoke to a student radio station in Christchurch who were wondering about the impact for students. The answer was not very much and if the proposal to remove the 50% discount on public transport goes ahead, students would be worse off as a consequence.

Auckland ratepayers are also probably worse off with the proposed abolition of the Auckland Regional Fuel tax. Mayor Wayne Brown has already said that could mean a $2 billion funding shortfall. How is that gap going to be funded?

Overall National’s proposals are very much a sort of the Lord giveth and the Lord taketh. And where you sit on that spectrum depends on how well you end up. If you’re a landlord and high-income earner, and you don’t use public transport, you’ll be reasonably okay.

On the other hand, if you’re on lower incomes, perhaps receiving Working for Families income and you do use public transport, you’re going to be worse off. But this is politics, the electorate will decide in six weeks exactly which tax policy is fair.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

At last week’s International Fiscal Association’s Trans-Tasman conference, a lot of the discussion among New Zealand advisors outside of the seminar rooms was around the state of tax policy. There is a growing concern that a more active government with interventions and proposals such as the proposed zero rating of GST on fruit and frozen and fresh fruit and vegetables is undermining the Generic Tax Policy Process which has been in place for nearly 30 years.

Like many practitioners, I’ve been involved with the GTPP at various stages. It is well-regarded internationally and has operated since 1994. It is intended to ensure

“better, more effective tax policy development through early consideration of key policy elements and trade-offs of proposals, such as their revenue impact, compliance and administrative costs, and economic and social objectives. Another feature of the process is that it builds external consultation and feedback into the policy development process, providing opportunities for public comment at several stages.”

However, the concern is emerging that against this well-established background more recent measures such as the Tax Principles Bill, or the legislation that enabled Inland Revenue to carry out its high wealth individual research project, have happened outside the GTPP framework. The proposed GST zero rating of fresh and frozen fruit and vegetables could be another example. These developments are unsettling the previously predictable process for working through and discussing tax proposals.

I’m of the view that tax is fundamentally about politics and politicians will always make political calls. The GTPP is intended to minimise the effect of that and give more predictable tax policy outcomes. But you can’t eliminate it entirely and this dichotomy between efficient tax policy process and politics will always be there.

There is also the question raised in an interesting story this week by BusinessDesk (paywalled) in reference to the work of the Corporate Taxpayers Group (CTG) about when consultation ends and lobbying begins. The CTG includes the main corporate taxpayers such as Fonterra and the four big banks. The New Zealand Superannuation Fund, the largest single taxpayer in the country, is also a member.

The CTG meets regularly at the offices of Deloitte (more frequently than I had imagined) as the story outlines, and there is an annual membership fee which is to pay for the secretariat, which will make submissions to Parliament and to Inland Revenue.

But when does this move from consultation to lobbying. Very difficult to say. I don’t see it as lobbying although I do appreciate the risks that might be involved in that. But having been involved in the process and been in meetings with CTG representatives, Inland Revenue officials, I don’t believe that’s the case.

But as I said, I can understand why some might be concerned by this. It comes back to a key part of any democracy, and that’s transparency. But on the whole, as I said, I think New Zealand’s been very well-served by the GTPP. And I know that internationally it’s very well regarded because it has got a stability of process to it.

I think one of the issues that’s causing raising concern is because left wing governments are likely to more interventionist. But I do think this situation is exacerbated at the moment because the strain of the boundary between capital and revenue, and our general under taxation of capital, the lack of a capital gains tax, wealth, tax, death duties, are putting strains on the system. And so, politicians are trying to find shortcuts to try and deal with this issue and the need for more revenue. You can dispute how much is needed. But when I look at the state of roads and hospitals and you see the growing bill for climate change, my view is and it’s also the view of Treasury, as I pointed out a number of times, and its Long Term Insights Briefing He Tirohanga Mokopuna we need more revenue.

A whole lot of hissing

So, there are strains emerging and it’s impacting the GTPP, which makes tax advisers understandably a little unsettled about how well that process will continue. As Louis XIV’s finance minister Jean-Baptiste Colbert said in probably one of the most famous maxims about taxation: “The art of taxation consists in so plucking the goose as to obtain the largest possible amount of feathers with the smallest possible amount of hissing.” That was true in the 17th Century and remains true today. And there is quite a lot of hissing going on at the moment.

The GTPP in operation – consulting on trading stock

Moving on and still on to the topic of consultation and an example of the GDP in operation. Inland Revenue has released a paper for consultation on the treatment of trading stock disposed of below market value.

At present, whenever trading stock is given away, or disposed of for below market value it’s deemed to have been disposed of at market value. The reason for that rule is reasonably solid. It’s to counter potential tax avoidance where the stock is given away or may be used for private consumption by a business owner or sold at a deep discount to associated persons. In some cases, it could apply for a particular industry, exchanges of stock could take place at cost or less. All of those generate benefits in terms of the under taxation of revenue. So that’s why that rule exists.

But there have been instances where businesses have wanted to give away stock and make donations for charitable purposes, and that’s when this rule becomes problematic because they can’t effectively do so. Over time the practice has developed for granting temporary emergency relief in some situations as a work-around.

In 2004 a permanent override was put in place with donations to farming, agricultural and fishing businesses during what is termed an adverse event. And there have been a large number of those weather-related adverse events either for drought or like we’ve experienced this year, flooding.

Between 2010 and 2012, there was a temporary override for 18 months in response to the Canterbury earthquakes. And then again, starting in March 2020, a temporary override was put in place for four years in response to COVID 19.

That override will end on 31st March next year, and the object of this consultation paper, is to propose a more permanent solution rather than using ad hoc solutions whenever we encounter a particular scenario such as COVID or earthquakes.

The consultation paper runs to 29 pages and includes a useful appendix which summarises all the potential summary policy options and how they may play out. Overall, this is a good example of the Generic Tax Policy Process in operation. Consultation on the paper is now open and closes on 6th September.

Managing retreat & how to pay for it.

As just mentioned, temporary emergency relief from the usual stock donation rules has been granted for a number of reasons, including this year, the flooding in January and February and the impact of Cyclone Gabrielle. A constant theme of this podcast is the question of environmental taxation and the need to address the longer-term question of how we going to pay for these climate related events.

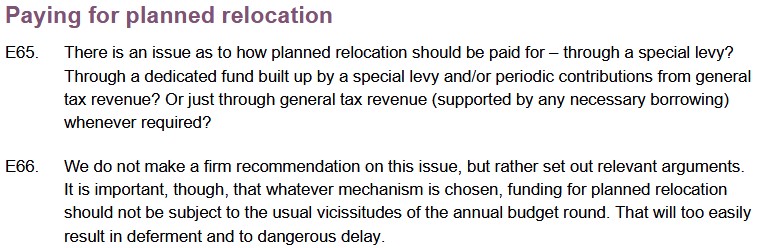

Earlier this week a Government expert working group released its report on the question of what’s termed managed retreat.

The report, which clocks in at 284 pages, is very comprehensive and raises a number of potential scenarios and alternative measures that could be needed. One of which, as the excellent Newsroom story covering the report notes, is conditional powers to basically force people to leave particular areas that are under threat.

Being a tax podcast the question we are most concerned about with environmental and climate change impacts is how we are going to pay for it. The report has two key proposals E65 and E66.

But consider this, we have currently 700 homes which have been rendered uninhabitable following the flooding in January and February. And there’s another 10,000 homes that require flood protection. The Government has said it will split the costs over the uninhabitable homes with local councils affected. But, as far as I can tell, neither the councils nor the Government have really fully funded for these costs of maybe a cool billion or so this year and maybe every year and rising. So, it is an issue that needs to be addressed.

The report has some interesting discussion around what happened in Canterbury in relation to the earthquakes and then the first and I emphasise, first, example of managed retreat, from the Bay of Plenty settlement of Matatā

The report says, however we decide to fund this, the funding should not be subject to the usual vicissitudes of the annual budget round because that would mean it would lead deferment and dangerous delay. When it comes to kicking a football down the road, the politicians, as we know, are better than the Football Ferns at kicking it a long way out of trouble. Or so they think, but the issue still remains. I totally agree, therefore, with the report’s recommendation that there has to be a permanent funding solution.

I maintain that if we are going to do something around the lines of environmental taxation, the funds that are allocated to it should be hypothecated, and certainly not form part of the consolidated fund because we’ll then have politicians tempted to raid those funds. We’ve seen this in the recent Auckland Budget Council, by the way, where reserves built up for environmental purposes were used for other purposes.

In terms of holding politicians to account, I think we need to be asking a lot more questions about them on this matter because this is going to affect us all. We’ve had a miserable winter with extensive flooding and the ground is sodden. What happens when the next big floods come along, who pays for the clean-up?

No longer friends with Russia…

At the International Fiscal Association Trans-Tasman conference last week, we spent a lot of time discussing double tax agreements. It so happens, Russia has decided to suspend its double tax agreements with 38 countries, which it considers are now ‘unfriendly’ in the wake of the invasion of Ukraine. New Zealand is on that list. So that probably means that for someone in Russia trying to claim tax relief from under the double taxation between New Zealand and Russia, they’re out of luck and they’re probably going to be facing higher tax bills as a consequence.

TikTok and GST fraud

And finally, just on the topic du jour this week of GST, there’s an absolutely extraordinary story coming out of Australia about how social media influencers on TikTok encouraged at least 56,000 people to take part in a A$1.6 billion tax fraud scheme. Apparently these TikTok influencers explained how to get fraudulent GST refunds. The scam involved obtaining an Australian Business Number, then filing Business Activity Statements (the equivalent of GST returns) and claiming false GST refunds. In some cases, there were attempts to claim refunds of up to A$100,000.

The Australian Tax Office apparently is still grappling with the sheer size of the scandal. There’s a story in the Australian Financial Review about a Victorian woman who managed to stay out of jail, after repeated attempts to try and get A$115,000 fake GST refunds for a dog grooming business that had been set up more than a decade ago but had been largely dormant until 2020 before she attempted to pull this scam.

Fascinating story which will be interesting to see how it plays out. To me it lends support to the suggestion that we should look seriously at zero rating transactions between GST registered businesses. It should be a means of stopping such attempted frauds. Obviously, if that proposal is taken forward, it should go through the proper Generic Tax Policy Process consultation.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue has released a draft interpretation statement on the research and developments loss tax credits regime. This is a refundable tax credit available to eligible companies when they have a loss which has arisen from their eligible research and development expenditure.

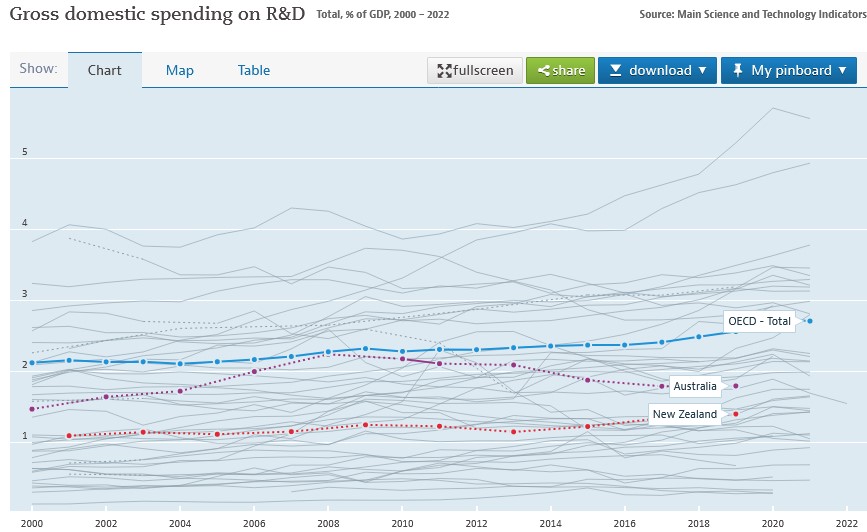

The regime was introduced in 2016 to encourage business innovation and also to address New Zealand’s poor record of R&D expenditure. According to OECD data, in 2019 New Zealand’s spending on R&D was just 1.4% of GDP, well below the OECD average of 2.56% of GDP. Over the past 20 years research and development in spending in New Zealand has been a full percentage point of GDP below the OECD average.

So given that we also have a poor record of productivity, increasing R&D expenditure is seen as critical in improving productivity and ultimately the strength of the economy.

That’s the background behind the introduction of the loss tax credits regime. It’s intended to assist the cash flow of those companies carrying out research and development. Often in the early years, these companies are running at a loss. Hopefully once the R&D matures and bears fruit, they will then have profits resulting from the expenditure.

But funding cash flow in those early years is pretty difficult. So instead of the tax losses to be used against future profits, under the regime, companies can instead receive a payment. Note, only companies can receive this R&D tax loss credit payment. That’s because losses incurred by partnerships, limited partnerships, look-through companies and sole traders can already pass those losses through to the underlying owners anyway, who will often be able to offset them against their other income. Essentially, they are already able to benefit from the ability to cash-up losses. But companies can’t do that, hence the introduction of the regime.

The Inland Revenue draft interpretation statement looks at the background to scheme, summarises the rationale for scheme and how it operates. A couple of key points about the regime: you can drop in and out of it, you can opt to choose a payment in one year but not in another year. Once you have claimed a refund by cashing up your losses, the regime operates rather like an interest free loan. You’re essentially required to repay it and it’s generally treated as being repaid when the company starts paying tax, the R&D having borne fruit.

However, there are other circumstances where the credit may have to be repaid earlier when there is, in the terminology of the regime, a loss recovery event. Now, that typically will happen if there’s a disposal or transfer of the intangible property, core technology, intellectual property, etc., which is done for either less than market value or the amount sold is a non-assessable capital gain.

Another situation, and this is actually one where I’ve been involved, is where the company is no longer tax resident in New Zealand. Some very interesting issues arise in that case. Then there’s the worst-case scenario, where a company goes into liquidation although what exactly can be recovered at that point is a moot point. But that’s still a loss recovery event.

And then finally, and similar to our other rules around the carry forward of losses and imputation credits, a loss recovery may occur if there is a loss of the required shareholder continuity. In the case of the tax loss credit regime, the relevant shareholding percentage is 10%. In other words, there’s no breach if at least 10% of the voting interests of the company are held by the same group of persons throughout the relevant period.

In my view this is a very important regime for improving the future productivity of the country. The scale of the spending is going on is quite interesting to see. We can get an idea of this because the Inland Revenue as part of the budget produces what is called a tax expenditure statement.

Tax expenditure statements are a summary of the cost of a particular tax preferred regime, which, like, for example, this regime, has been introduced for specific policy reasons. The OECD collects data on tax expenditures to get a global picture of what spending is going on in tax preferred regimes.

In the case of the R&D loss tax credit, the estimated value of the expenditure for the year to 30th June 2023 is $362 million, a little bit below 1% of GDP. The estimated expenditure for the year to June 2022 was $473 million. And you can see a steady rise since the regime was introduced in 2016.

Of course, the real importance of this regime is whether it has produced a boost in total R&D spending within the economy. And then ultimately, does that lead to increased productivity. It’ll be interesting to measure these once the data flows through in due course.

So, an interesting regime and good to see Inland Revenue give some guidance on this. It contains a few hooks but it’s well worth looking at if you’re thinking about trying to make use of the scheme. And as I said, we will watch with interest to see how it bears fruit.

Shuffling forward on internationalPillar One and Pillar Two proposals.

Moving on, we’ve talked fairly regularly about the OECD’s global minimum tax deal and Pillar One and Pillar Two. Last week the G20 met in India and the Secretary General of the OECD reported to the meeting that, “A historic milestone was reached at the 15th Plenary Meeting of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (Inclusive Framework) on 11 July 2023, as 138 members of the Inclusive Framework approved an Outcome Statement on the Two-Pillar Solution.”

In summary, what’s happened is that they’ve developed a text to a multilateral convention which will allow jurisdictions to exercise a domestic taxing right over the residual profits of the largest, most profitable multinationals. That’s what they call Amount A of Pillar One, and that will apply to multinationals with revenues in excess of €20 billion and profitability above 10%. What will happen is the scope of that taxing right will be 25% of the profit in excess of 10% of revenues. This €20 billion revenue threshold will gradually be lowered to €10 billion after seven years, conditional on the successful implementation of Amount A.

There’s a proposed framework for the simplified reporting application of arm’s length principle, which is key to transfer pricing and for baseline marketing and distribution activities. That’s what referred to as Amount B of Pillar One.

There’s a Subject to Tax Rule, again with an implementation framework, and this is really for developing countries to update their bilateral tax treaties to tax intra group income. This is where such income is subject to lower tax in another jurisdiction, in other words say one country has a 20% corporation tax rate. But that multinational shifts charges to another part of the multinational group in a jurisdiction where those charges are only taxed at a lower rate. This Subject to Tax Rule gives the first country more taxing rights in that income. Developing countries are very keen on this particular point because they feel that this is where the current tax regime has been almost predatory on their tax base.

There will be a comprehensive action plan developed by the OECD to “Support the swift and coordinated implementation of the Two Pillar Solution, coordinating with regional and international organisations”

On the face of it, all pretty much good news. But it’s interesting to read the views of those people who specialise in this field and there still seems to be quite a bit of uncertainty about whether in fact this whole thing will come to fruit.

In the meantime, for example, you’ve got lobbying going on in the United States. And it appears now that the US has managed to secure a further delay in the implementation of the Pillar Two global minimum tax 15% until 2026, according to a report coming out of the United States.

Pillar Two is the key proposal, because it applies to companies with annual revenues in excess of €750 million. Apparently, the US Treasury Department has managed to negotiate a delay in the implementation of this. It has got people watching all around the world as to what’s going on. It also means that the in the background, digital services taxes, for example, could still be ready to be deployed or introduced by jurisdictions if they feel that Pillar Two isn’t making enough progress and they want to secure their revenues. [Under the agreement just announced countries have agreed to hold off imposing “newly enacted” digital services taxes until after 31st December 2024.]

Overall, it’s a bit of a shuffling: one step forward, maybe half a step sideways and a quarter of a step back. In other words, progress is slow, but it’s still inching the way forward. Ultimately, it comes down to watching what happens in the United States and the lobbying goes on. If there’s a change of President next year all bets will be off at that point, I would say.

Smith, banged to rights, again. But should Companies Office be in the gun?

And finally, this week, the murderer and escapee, Philip John Smith, who’s been in jail since 1995 apart from the brief time he escaped to Brazil has now been sentenced to further two years imprisonment on tax fraud charges.

He was convicted for dishonestly using documents intending to gain pecuniary advantage, firstly, a application under the Small Business Cashflow Scheme and then for filing 17 false GST returns and a false income tax return. in total the attempted fraud was just over $66,000 of which was actually paid $53,593. He’s also been ordered to pay full reparations on that amount.

What he did was between October 2019 and March 2020, he registered five companies with the Companies Office with shareholders and directors, who were friends, associates or third parties unknown to him. He then he set up and activated myIR accounts for each company.

But Inland Revenue was quite quickly onto him, it seems, because it apparently detected the fraud involving the Small Business Cashflow Scheme in June 2020 only a few months after it started operating in April. So good quick work by Inland Revenue.

But the case also raises the point which an associate I bumped into this week mentioned, and that’s the actions (or inaction) of the Companies Office in allowing those five companies to get set up. New Zealand scores highly for ease of business in establishing companies. Many times, whenever I’m talking to overseas people, they are remarkably impressed about how quick it is to set up a company in New Zealand.

The question arises if people setting up companies by going directly through the Companies Office website, is it a little bit too easy? Was an opportunity to pick up Smith’s attempted fraud missed at that point by Companies Office? We don’t know. Accountants and lawyers are subject to the current anti-money laundering legislation, so we need to pay attention to what’s going on with company registrations and we have to obtain proof of ID. But my understanding is this process is a little less rigorous when you go directly through the Companies Office.

So good work by Inland Revenue picking it up quickly and catching Smith, again. But maybe some questions should be asked as to whether he should ever have been able to get that far along the line and that Companies Office should have picked it up sooner.

And finally, congratulations to the Football Ferns for their magnificent win last night at the start of the FIFA Women’s World Cup. I was lucky enough to be at Eden Park, which is why I might sound a little hoarse today! It was fantastic to experience such a great occasion even if the final nine minutes seemed like an hour. Congratulations again to everyone involved. Football definitely was the winner on the night!

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

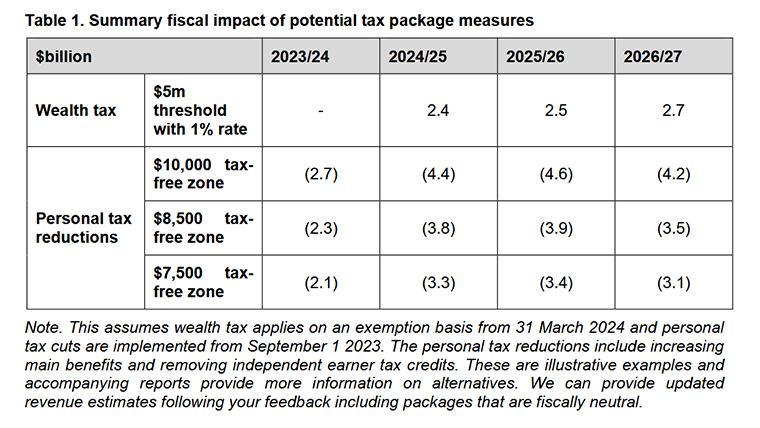

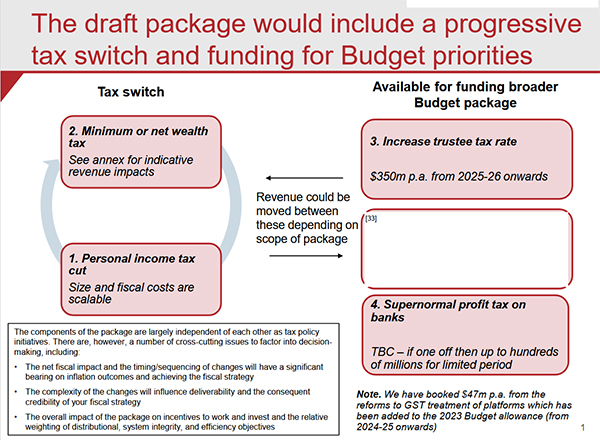

The big news last week was the release of the official advice to Ministers on tax incentives during the lead up to this year’s Budget. And it was quite a bombshell. Amongst the wealth of material provided was the surprising news that a key proposal had been until quite late in the piece a tax switch where in exchange for introducing a tax free threshold of $10,000, the Government would introduce a wealth tax.

Now, the Prime Minister immediately ruled out the wealth tax and also ruled out any capital gains tax if the government gets re-elected. So to a large extent, all this fascinating material is largely redundant. But it still provoked the continuing debate around the pros and cons of a wealth tax. And in fact, it’s really very interesting to go through the material and see how the policy developed and where they were planning to take it.

The final scheme would have applied a 1% tax rate to net wealth above a $5 million threshold under what was termed an “exemption approach”. This was initially thought it could raise between $2.7 and $2.9 billion annually and would have affected some 46,000 individuals. According to officials the wealth in scope at a $5 million threshold would be about $210 billion

A minimum tax?

Now, in the course of development the proposal started with something called a “minimum tax” under which proposal a person with high wealth would pay tax on the greater amount of either their deemed income calculated as a percentage of the net worth or the taxable income they have under existing income tax rules. The deemed income would have been based on the idea of economic income, which would include unrealised gains. If you recall when the Sapere report and the Inland Revenue High Wealth Individual research project were released, there was a great deal of controversy around this measurement because once you measured economic income and unrealised gains, it appeared the wealthy were paying an effective tax rate of 9%.

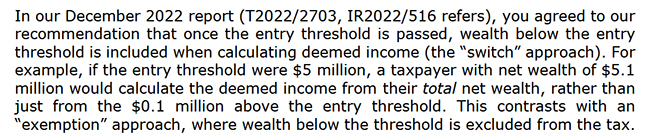

This minimum tax was the initial proposal which then got dropped over time. In the course of discussions, they moved away from what they called a “switch approach”. Under this once a person crossed the threshold, then all the deemed economic income would be subject to the wealth tax rather than just the proportion above the threshold.

And this so-called “exemption” is pretty much what we see in other wealth taxes around the world. It appears in the design of the wealth tax officials took a close look at the Norwegian system. One of the other features I found surprising was that the family home would be excluded. It seems to me that the tax preferred approach to the family home, has led to a large amount of overinvestment in housing.

Wealth taxes – profile of potential taxpayers

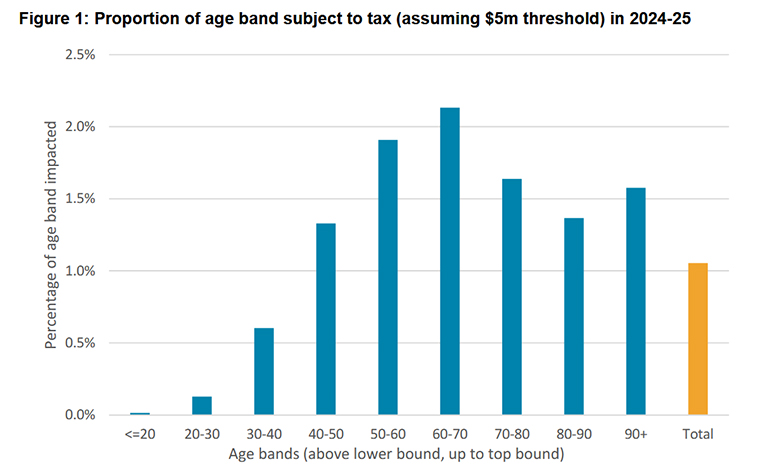

A key report on a wealth tax contained a very interesting discussion, around which group of taxpayers would be most affected. The projection was the age group which would be most affected at the $5 million threshold was that between 60 and 70. An estimated 2.1% of this group population has net worth over $5 million. According to these statistics, 1.5% of the over 90 year old group would be affected.

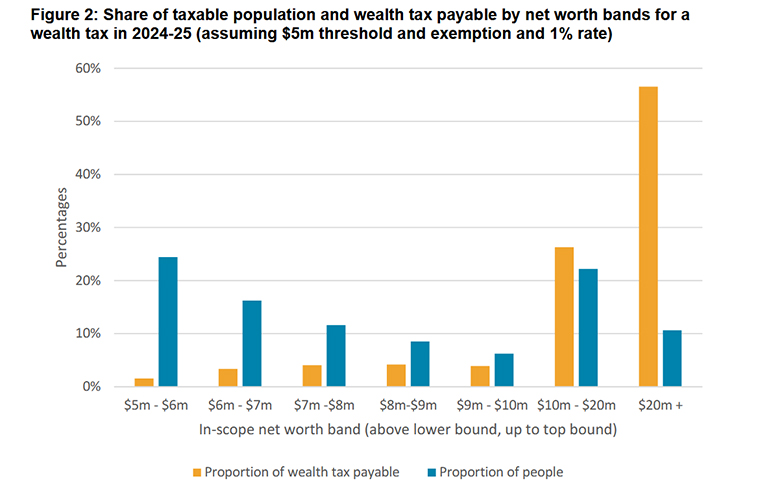

But in fact, as you might expect, more than half of the wealth tax would have been paid by the high net worth individuals with a net worth in excess of $20 million.

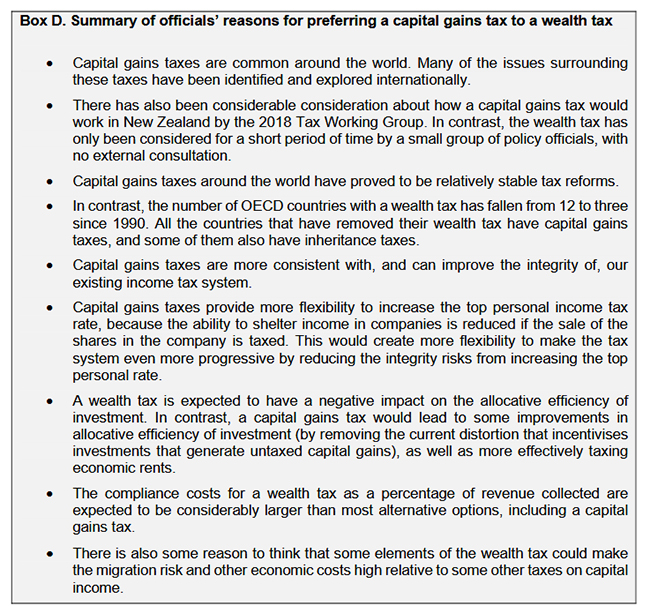

Officials prefer a capital gains tax

But I think the other thing that came out quite clearly from the papers was that the officials were not at all impressed by wealth taxes. They preferred a capital gains tax.

By the way, the officials view probably reflects a reasonably widely held belief if largely unspoken view amongst the tax community, that if we’re going to tax capital then a capital gains tax is probably the way forward.

Anyway politics intervened again and so a capital gains tax has now been ruled out in their prime ministerial lifetimes by two successive Labour prime ministers. However, as I said to Corin Dann on Morning Report the politicians may rule out capital gains taxes but we’ve got a lot of issues with an ageing demographic and the impact of climate change. The strains on the tax system, which have been recognised by Treasury and its Long Term Insights Briefing He Tirohanga Mokopuna in 2021 recognises that. The issues about needing more tax from somewhere haven’t gone away.

Paying for Cyclone Gabrielle

There were also suggestions as a one-off response to the impact of Cyclone Gabriel, for a levy on the banking sector. There was a comment that the four main banks have persistently “elevated levels of profitability relative to the smaller New Zealand banks and overseas and comparators in part due to the relatively low costs of the large New Zealand banks.” A temporary levy on the banks could raise somewhere between $230 and $700 million. As the Greens noted, Margaret Thatcher of all people did actually impose a surcharge on banking excess banking profits when she was Prime Minister.

There was also a suggestion of a one-off flood levy similar to what was introduced in Queensland following their catastrophic floods in 2010-11. A temporary 1% levy applied to all taxpayers would have raised $1.8 billion. But one only applied to income above $100,000 would raise $250 million.

The quid pro quo – a tax-free threshold

The quid pro quo for a wealth tax would have been a $10,000 tax free threshold. Once again Treasury and Inland Revenue weren’t enthusiastic. They suggested more significant increases in the lower thresholds including lifting the threshold at which the rate goes from 10.5 to 17.5% from $14,000 to $25,000, which is actually substantially ahead of where it would have been if had it been indexed to inflation. However, they proposed lifting the next threshold rate increases to 30% to $52,000. This is the threshold which I think is extremely problematical because of the large jump and at its current level of $48,000 is now well below both average and median wages.

There are two things of interest here. Firstly, a recognition that something has to be done. Tax free thresholds are very popular, but they’re not as efficient is the official advice. Secondly the cost of increasing these thresholds would have been over $4 billion annually. This is an acknowledgement that by not indexing thresholds since 2010, governments have given themselves a permanent headache around having to make threshold adjustments that become increasingly expensive.

A mystery policy?

A tax-free threshold is apparently out of the question. But maybe not because amidst all the papers, there’s are parts which have been redacted. These refer to another policy, whether that was capital gains tax, we don’t know. But whatever it was, it’s been redacted and not been released under the Official Information Act.

We’re now within three months of the General Election and Labour is still to release its tax policy. So maybe there’s something in that hidden part which will be revealed.

Secrecy and the Generic Tax Policy Process

There’s been some discussion that because this was all carried out secretly and outside the Generic Tax Policy Process (GTPP) that maybe this might not have resulted in a terribly efficient tax. I’m less concerned about governments deciding they’re going to do something for electoral gain and requesting work be carried out discreetly. But I do agree that if it’s done outside the GTPP, there is a risk that the design could be faulty. We’ve seen that with the bright-line test and the continual tinkering that has to be done. Worth remembering, by the way, that the bright-line test itself was a surprise. There was no previous consultation before it was first introduced in the May 2015 Budget by Bill English.

I like tax surprises in budgets, and I believe they’re part of normal politics. As I’ve said before, tax IS politics. But I do think that if you look entirely at tax through a political lens, then you start to get this narrow view developing right now where everyone says the politics of raising taxes are too hard, but the economic question of, how are we going to pay for the coming challenges just gets sidelined.

To repeat myself, we have serious issues to address coming up. And my view is if you want to maintain the broad based, low rate approach to fund these challenges, you’re going to have to do something around capital taxation. And the sooner you do it, the better.

Inland Revenue dropping the ball on investigations?

Moving on, one of the officials’ key objections to a wealth tax was the cost of compliance. Inland Revenue would clearly need to increase its capabilities. In its advice on its Initiative Work Programme it commented “the Government’s current tax and social policy work programme will use up most of our specialist design and delivery capacity over the next three years.”

Now the question of Inland Revenue’s operational capabilities came up at the start of last week when it was raised by National’s revenue spokesperson Andrew Bayly.

Following some written questions to the Minister of Revenue, he had determined that the number of investigations conducted by Inland Revenue dropped from an average of 77 a month between February 2017 and October 2020 to only 17 a month between October 2020 and June 2022. Furthermore, the time Inland Revenue spent on hidden economy investigations has also dropped substantially, from 3094 hours in November 2020 to just 805 hours in May this year.

Mr Bayly thinks Inland Revenue is dropping the ball here. Now, he’s tried that for obvious political reasons to Inland Revenue’s work on the High Wealth Individual research project, but that was separately funded. (Incidentally, early drafts of the report were made available to Cabinet as part of the pre-budget preliminaries).

There is an ongoing operational issue, in my view, about Inland Revenue’s investigations activity. And actually, it has acknowledged it has not been doing as much work in the investigations and debt recovery field. Page 36 of its Annual Report for the year ended 30 June 2022 notes:

“We did less work than would be typical in areas such as debt collection, investigations, disputes, litigation and liquidation activity.”

Now, part of this is down to the response to COVID. There were great demands made of Inland Revenue to which it responded superbly. But note the number of investigation hours back in November 2020, which is in the heart of the pandemic, was 3,094 but now it’s down to only 805 hours when we’re supposedly post pandemic, or rather a different stage of response to it. Inland Revenue saying that the fall off in investigations is because it has had to deal with COVID and this year’s weather-related events is not a satisfactory explanation in my view.

And when you start digging into Inland Revenue’s appropriation statements which are published as part of its annual report, you can see the amount spent on investigations for the past five years has fallen quite considerably in absolute terms, let alone when adjusted for the impact of inflation.

Reduced investigation funding

In the year to June 2018, the investigations appropriation was just over $140 million. But for the year to June 2022, it was just over $113 million. That’s a significant drop of nearly 20% in absolute terms.

Inland Revenue investigations appropriation per annual reports.

30 June 2022 $113.235 million

30 June 2021 $124.325 million

30 June 2020 $109.720 million

30 June 2019 $134.706 million

30 June 2018 $140.164 million

So, what this points to is the claims being made by Mr Bayly about Inland Revenue taking its eye off the investigations ball does appear to be backed up by the evidence of where it’s been spending its money. One of the explanations for this appears to be tied into its massive Business Transformation project. Inland Revenue, once it got started on this, seems to have pretty much solely focused on getting it across the line.

Where did the investigations staff go?

Part of Business Transformation included substantial reductions in its headcount, which went from 5789 in June 2016 to 3923 in June 2022. Now, that’s nearly a third of the workforce gone. We also know that although there was a substantial number of staff (nearly 800 apparently) whose sole purpose was simply re-inputting data so it could be used, a large number of very experienced investigation and operational staff were also let go. I know that because I’ve been speaking to a few of them.

Therefore, other tax advisers and agents and I are wondering whether Inland Revenue now has a diminished Investigation capability. There’s also another matter which Andrew Bayly also picked up on, the fact that Inland Revenue has decided to adopt a completely new metric for measuring its investigation performance. That makes you wonder why it’s done that. We won’t know what they’re measuring and how effectively, as the year just ended on 30th June is the baseline for this new metric.

But it’s important in a system that relies on voluntary compliance, there is the expectation by all of those taxpayers who comply that Inland Revenue is making sure that those who are not playing by the rules will be found and investigated. The concern is if Inland Revenue’s capacity to do that is diminished and it’s not fulfilling that role, then the overall perception of the integrity of the tax system is undermined. And that’s not good long term because naturally people will start thinking “That person is getting away with it, so we can too”.

I hope this is something the new Commissioner of Inland Revenue Peter Mersi is paying a lot of attention to. It will be very interesting to see what the department says when its latest annual report is published in October.

Inland Revenue renews its focus on GST

And finally, this week and, coincidentally or not, a couple of days after the story about Inland Revenue’s lack of investigation focus, it posted a warning for tax agents about “Its renewed focus on GST compliance”

Now, you can easily interpret this as an implicit acknowledgement of Andrew Bayly’s criticisms, but it is in fact another sign which we’ve seen steadily emerging that Inland Revenue is now repositioning itself back into what you might call its regular routine.

As usual, we’ll keep an eye on what that means and bring you developments as they emerge.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.