Australian Tax Office ruling on residency – time for a clearer statutory definition?

Applying for Australian citizenship? Watch out for the sting in the tail.

Submissions closed Friday on the Tax Principles Reporting Bill. Now for a bill that doesn’t actually increase the tax rates this has been a surprisingly controversial bill, mainly because it’s actually perceived as being highly political in its ambit in introducing reporting on tax principles. The speed with which with which it has been rushed through is also controversial because normally tax legislation is developed through what we call the generic tax policy process (GTPP). The GTPP is very well regarded around the world.

But every so often, for whatever reason, the process is bypassed. Sometimes as during the COVID emergency because things need to be done immediately. It’s a framework through which New Zealand tax policy has operated for the better part of nearly 30 years. And it means changes of tax policy and of the particular tax treatment of certain items are developed over time through consultation.

Controversy around the Tax Principles Reporting Bill

In this case, the Tax Principles Reporting Bill came out of left field. There’s been very little consultation about it. In fact, we’ve only had barely three weeks between its introduction alongside the Budget and today. So that’s part of the controversy around it.

The other question is what it really is setting out to do. I think most objections will centre around this question of why is this here? The idea of setting out some ideas about what tax principles might be is not unreasonable in itself. But criticism of the Bill is focusing on whether it’s very clear about what it’s trying to do. For example, Inland Revenue is required to report on certain effective principles and whether there are inconsistencies in the tax system with these principles. But then, as several tax advisors have asked, what action will be taken at that point. There is also no acknowledgement that tax policy ultimately involves trade-offs between principles and politics. To be frank, tax is politics.

I’ve seen one or two interesting comments about which agency should be reporting under the Bill. Inland Revenue or maybe Treasury? There are a whole heap of things to consider about the Bill. Although it comes into effect on 1st July, if there is a change of government, it will almost certainly be repealed.

It’s an interesting Bill because it’s attempting to clarify the basis on which we design and operate a tax system. But it’s also flawed because I don’t think it’s has actually achieved that. We’ll see plenty of pushback and I’ll be interested to read the submissions on the bill. (Shortly after the podcast was recorded, John Cantin published his submission).

Australian tax residency

Moving on, I frequently deal with issues of tax residency. It’s a core part of what I do because tax residency determines what sources of income will be taxed in Aoteaora-New Zealand. There are also rules set out in double tax agreements, and one pretty basic principle wherever you go in the world is that if you have property situated in the country, that country gets what we call the primary taxing rights to it.

But individual tax residency is a matter of great practical importance. If a person is resident in the country, then that country can tax them on their world-wide income, and that can have quite significant implications.

The Australian Tax Office (ATO) has just updated and released a tax ruling TR 2023/1, on income tax residency tests for individuals. Australia deems a person to be tax resident in Australia if they reside in Australia under what they call the ‘ordinary concepts’ test, and that includes a person whose domicile in Australia, unless they’re satisfied that they have a permanent place of abode outside Australia.

A person is also resident if they have actually been in Australia continuously or intermittently during more than half of the year of income, unless they’re satisfied that they have a usual place of abode outside Australia and they do not intend to take up residency in Australia. There’s also another series of tests, which I’ve not come across, relating whether or not they’re a member of a superannuation scheme or are covered under the Commonwealth Fund.

When you look at these tests you can see there are quite a few value judgements involved. And so there have been calls for the Australian tax residency test to be put on a more statutorily defined basis, most notably by the Australian Board of Taxation. “The Board’s core finding is that the current individual tax residency rules are no longer appropriate and require modernisation and simplification.”

Now it’s of interest here obviously for people going across to Australia, but also because our own residency test is twofold. The primary test, and this is often forgotten, is a person is tax resident in New Zealand if they have a permanent place of abode in New Zealand. You’ll note that phrase, “permanent place of abode” is actually also used in Australia.

Failing that, there’s the days present test where a person is deemed to be resident in New Zealand if they are physically present in New Zealand for more than 183 days in any 12-month period. There’s a subtle difference there between our days present test and many other jurisdictions in that it is based on a rolling 12-month period rather than a tax year. On the other hand, when you get down to defining a permanent place of abode, that involves quite a number of value judgements.

The current residency test is now over 30 years old. As noted above the Australian Board of Taxation suggested that really the Australian test perhaps should be more clearly defined in statutory legislation. And I’m coming around to the view that maybe that’s what we need to do in New Zealand as well. I’ve seen at least one academic article in the past year that’s picked up on this point.

“You can check out any time, but you can never leave”

Now, why we don’t do that is explained in the Inland Revenue Interpretation Statement on residency. Right now the permanent place of abode test does make it easy for someone to be defined as tax resident, but difficult to lose that.

Notably, the Interpretation Statement does not have an example of a time period of how many years must a person be overseas before Inland Revenue would consider that someone has lost their permanent place of abode.

So, this makes residency a very open-ended issue, which is not terribly good in terms of certainty for taxpayers. It’s become more of an issue in the past 30 years since we introduced the permanent place of abode test in 1989 because as we have seen in the last three or four years, the world’s got a lot more mobile with people moving and working around the world.

This issue of being tax resident here, perhaps inadvertently, is actually something that individuals are concerned about. They obviously want to minimise their tax obligations as far as legally possible. On the other hand, governments know that if you set out very specific tests then people will play to the letter of those rules by watching carefully the number of days present in a country.

A British alternative?

The British residency test, the statutory residence test, actually deals with this day count issue pretty well by specifying what it calls “ties”. Depending on how many ties to the UK you have, whether you’ve been tax resident beforehand and how many days you spent in the previous tax years, then the number of days you can spend in a in the UK in a tax year before you become resident drops.

It’s therefore not as simple as you can spend 182 days and then you’re okay. Each year it drops off quite dramatically and basically at its tightest definition you can only spend 16 days in the UK. Obviously, people will still try and manipulate their timing within these limits but the UK test is much more specific and it gives a great deal of clarity.

And I think in our case, just as the Australian Board of Taxation considers, it’s not an unreasonable objective to be looking at a statutory definition of residency which addresses the concerns Inland Revenue rightly has about people trying to game the system, but it provides certainty for people.

Becoming an Australian citizen – beware the potential tax trap

Still on Australia, there was good news recently that there’s now a pathway for Australia and New Zealanders who live in Australia to become citizens. This is very important for the huge numbers of New Zealanders over there, well over half a million. There is, however, a potential sting in the tail.

People will be aware that New Zealand has what we call a transitional residents exemption, which applies to new migrants or people who have returned to here and have not been tax resident for ten years. Under this exemption their non-New Zealand sourced investment income for the first 48 months is generally not taxable here.

Australia has a similar test if it applies to what they call temporary residents and it applies to most New Zealanders living in Australia. The sting in the tail is that if you apply for citizenship in Australia, you are no longer a temporary resident. What that means in particular is your New Zealand assets here become subject to Australian tax, including capital gains tax. The impact of Australian capital gains tax on New Zealand assets is often overlooked. It’s an issue I deal with regularly.

So that’s the trade off on Australian citizenship. Overall, it’s a good news and it puts people who have contributed significantly to the Australian economy on a level footing. But there is a wee sting in the tail for some. So, approach with caution.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue has released Interpretation Statement IS 22/04 on claiming depreciation on buildings. Critical to this issue is determining the meaning of a “building” for depreciation purposes and the distinction between residential and non-residential buildings. The Interpretation Statement addresses this issue when it sets out when depreciation may be claimed for non-residential building and also for some fit outs. It confirms that no depreciation is available for residential buildings.

The Interpretation Statement then sets out where you can find the right depreciation rate for buildings when fit outs attached to buildings may be depreciable. How to treat an improvement of a building for depreciation purposes. And then finally, what happens when the building is disposed of or its use changes?

To recap, depreciation for all buildings was reduced to zero, with effect from the 2011-12 income year. Back in 2020 as part of the initial response to the pandemic, the Government reintroduced depreciation for non-residential buildings with effect from the start of the 2020-21 income year. Generally, the depreciation rate is 2% on a diminishing value basis, or 1.5% on a straight-line basis. Some other depreciation rates may be used where the building has a shorter than normal useful economic life. Examples would be barns, portable buildings or hot houses. Additionally, it’s possible to claim a special rate if the building is used in an unusual way.

Now for depreciation purposes “building’ retains its ordinary meaning which means anything that is structural to the building or used for weatherproofing the building. The Interpretation Statement emphasises that whether a building is residential or non-residential is an all or nothing test. If the building is non-residential depreciation is available, otherwise not, there’s no apportionment.

Residential buildings are any places mainly used as a place of residence. This includes garages or sheds included with that building. Places used as residential residences for independent living in retirement villages and rest homes are residential buildings are is short stay accommodation where there’s less than four separate units.

On the other hand, non-residential buildings include buildings used predominantly for commercial and industrial purposes, but not residential buildings. This also includes hotels, motels, inns, boarding houses, serviced apartments and camping grounds. Retirement villages and rest homes where places are not being used for independent living are non-residential buildings as is short stay accommodation where there are four or more separate units.

If improvements are made to a building, you must treat it as a separate item of depreciable property in the first tax year. Then you can either continue to treat it as a separate item of depreciable property or simply add it to the building by increasing the adjusted taxable value of the building.

In some cases, a fit out can be separately depreciated depending on the nature of the building and the nature of the fit out. Where the fit out is considered structural to the building or used to weatherproof the building it must be treated as part of building and not depreciated separately. Fit outs are depreciable in a wholly non-residential building and sometimes in a mixed-use building. But remember, the key point is that depreciation is not available under any circumstances for a residential building. So overall, this is a useful Interpretation Statement and is also, as has become the norm, accompanied by a very handy fact sheet.

The agencies tackling organised crime and its tax evasion

Moving on, last week I discussed a suggestion by ACT Party leader David Seymour to use Inland Revenue against the gangs. I looked at the powers available to Inland Revenue and discussed how practical his proposal was. To summarise, Inland Revenue has extensive powers which would be useful in tackling gangs and organised crime. However, this is a resource intensive approach which probably in Inland Revenue’s view, would divert its attention from other areas it considers equally important.

This prompted some discussion in the comments section and thank you again to all those who contributed. As I said, my view is Inland Revenue probably thinks other agencies, such as the Police, are better suited for this activity. But it will cooperate with those agencies. Its annual reports make clear they pass information to other agencies. So Inland Revenue is probably working on this matter in the background.

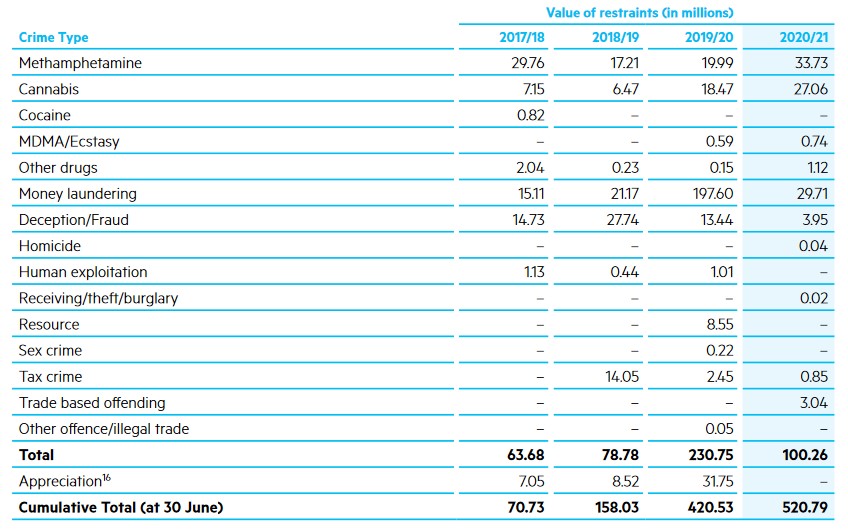

It was interesting just to take a look to see what other agencies were doing in this space and get a gauge of what’s happening. A key tool for the Police is the use of restraining orders to seize assets. According to the Police’s Annual Report for the year ended 30th June 2021 the value of restraints for the year totalled just over $100 million, including nearly $30 million seized from anti-money laundering.

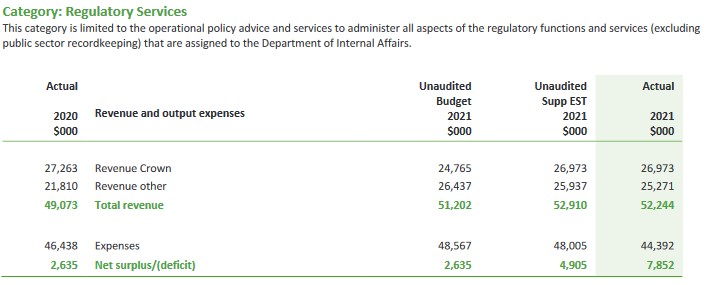

The Department of Internal Affairs also has responsibilities for anti-money laundering, as it’s a key regulator on that. Its Annual Report to June 2021 indicates that perhaps it could do more in this space, as its budget for its regulatory services for the year was set at $52 million, but it only spent $44 million.

And then when you look at the DIA’s performance metrics, such as desk-based reviews of reporting entities, it’s supposed to be targeting between 150 and 350 such reviews annually, but managed only 219 for the year, up from 198 in the previous year. And on-site visits were meant to be somewhere between 70 and 180 but came in at 79. To be fair these were probably disrupted by the impact of COVID 19.

Still, there are other agencies involved in pursuing gangs including Customs who will also be very interested. Inland Revenue will be playing a role, it shares information with these other agencies. So even if it’s not wielding a very big stick publicly, it’s working in the background.

The interaction of tax and abatements on social assistance

Now tax has been in the news a lot recently with the election coming up even though it’s still just over a year away probably. National and the ACT Party have both set out they would proposed some tax cuts. Last Saturday, Max Rashbrooke, a senior associate at the Institute of Governance and Policy Studies, who has written quite a lot on wealth and taxation put out some counter proposals to National and ACT’s proposals.

He suggested that really the focus should be on middle income earners. And he made a suggestion, for example, that we could have a $5,000 income tax free threshold, something we see in other jurisdictions. Britain’s is just over £12,500, Australia’s is A$18,200 and the US has a slightly different thing. It gives you a standard deduction of US$12,000. But anyway, let’s take that comment elsewhere. And Max suggested that something could be done in that space.

But it got me thinking about the question of who does actually pay the highest tax rates in the country. And the answer isn’t those on over $180,000 where the tax rate is 39%, it’s actually more around $50,000 mark if those people are receiving any form of government assistance, such as Working for Families. If they have a student loan as well, then an additional 12% of their salary after tax gets deducted.

The interaction of tax and abatements on social assistance, such as the family tax credit and parental tax credit can mean in some cases, the effective marginal tax rate for some families is more than 100% on every extra dollar they’re earning. This is an issue which the Welfare Expert Advisory Group touched on, but the Tax Working Group wasn’t allowed to address. But it’s a huge problem.

Take, for example, someone earning $50,000, just above the $48,000 threshold where the tax rate goes from 17% to 30%. And that, by the way, is the rate where I think we need to focus our attention on adjustments to thresholds and tax rates. At that level every extra dollar they’re earning is taxed at 30%. If they’ve got a student loan then they pay a further 12%. If they have a young family and are receiving Working for Families tax credits, then these are abated at 27%. Incidentally, the abatement threshold is $42,700. So that means that that person is on a marginal tax rate of 69%. Definitely not nice.

Then there’s a separate credit, the Best Start tax credit which has a separate abatement regime in addition to the Working for Families abatement regime I just explained. So that’s why people could be suffering an effective marginal tax rate of over 100%.

In my view, this is the area where we really need to be thinking about changing the tax system, because to compound matters, governments have been very cynical about not adjusting thresholds for inflation, something I’ve raised repeatedly in the past.

Working for Families thresholds were adjusted for inflation every year until National was elected in 2008. Starting in the 2010 Budget they started freezing thresholds. They also increased the abatement rate which used to be 20% and is now 27%. The current Working for Families abatement threshold is $42,700, which is less than what someone working full time on the minimum wage will earn annually

Looking at student loans the threshold where repayments start in 2009 was $19,084. That is now $21,268 but for a long period of time under the last government it was frozen. National also increased the repayment rate from 10% to 12% in 2013.

So this is an area where governments of both hues have been really quite cynical in my view, and where a lot of serious thought needs to go in about trying to address the inequities that have arisen. The Welfare Expert Advisory Group suggested the abatement rate should be 10% on incomes between $48,000 and $65,000, then increase to 15% before rising to 50% on family incomes over $160,000. (Yes, large families with that level of income could be receiving social assistance in some instances).

There’s a lot of work to be done in this space and inflation adjustments to thresholds is something that should be done anyway. But I think we need to think carefully around the thresholds and how the interaction with social assistance works. At the moment we’re not getting that sort of analysis from either any of the main parties and that’s disappointing, as it’s something that really needs to be addressed.

Why the FER deals with recurrent taxes better

And finally this week, just hot off the press is an OECD report on Housing Taxation in OECD countries. This makes for some interesting reading. Briefly, the report is concerned about how housing wealth is mostly concentrated amongst high income, high-wealth and older households. And in some cases, they believe that a disproportionately large share of owner-occupied housing wealth is held by this group. There’s been unprecedented growth in house prices, not just in New Zealand, but across the whole OECD, making housing market access increasingly difficult for younger generations.

In terms of suggestions the OECD believes that housing taxes are “of growing importance given the pressure on governments to raise revenues, improve the functioning of housing markets and combat inequality.” The report notes the way housing taxes are designed often reduces their efficiency. Recurrent property taxes, such as rates, are often levied on outdated property values, which significantly reduces their revenue potential. This also reduces how equitable they are because where housing prices have rocketed up, people are underpaying based on current values. And conversely people in places where prices are falling or have been stagnant are paying more relative to those in richer areas.

One of the suggestions the report makes is that the role of recurrent taxes on immovable property should be strengthened, by ensuring that they are levied on regularly updated property values. And this is one of these reasons why Professor Susan St John and I have been promoting the Fair Economic Return approach. One of the strongpoints of our proposal would be strengthening the role of recurrent taxes.

Capping a capital gains tax exemption on the sale of a primary residence

Another proposal would not at all popular. It is to consider capping the capital gains tax exemption on the sale of main houses so that the highest value gains are taxed. This should strengthen progressivity in the system and reduce some of the upward pressures. This is what happens the U.S. There is a US$250,000 exemption on the main home per person, and above that the gains are taxed. There’s no reason why we shouldn’t have a similar type exemption here if we want to introduce a capital gains tax. But as I said, that would be particularly unpopular.

The OECD also believes there should be better targeted incentives for energy efficient housing, because housing, according to this report has a significant carbon footprint, maybe 22% of global final energy consumption and 17% of energy related CO2 emissions.

So, there’s a lot to consider in this report, and we come back to it and consider it in more detail. But again, it sort of comes to this point we’ve talked about repeatedly on the podcast, the question of broadening the tax base and the taxation of capital. These issues aren’t going to go away, particularly when you consider, as I mentioned a few minutes ago, how very high effective marginal tax rates are paid by people on modest incomes who may not have any housing. No doubt we’ll be discussing all these issues sometime again in the future.

Well, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Inland Revenue is currently gearing up to begin processing 31st March 2022 year-end tax returns and personal tax summaries. Starting later this month it will be issuing automatic income tax assessments for most New Zealanders. But in preparation for that it has been giving updates to tax intermediaries on particular matters of interest. And a couple of notifications in the latest release caught my eye.

Firstly, there is form IR833 bright-line residential property sale information return which is required to be completed whenever a transaction which is subject to the bright-line test has taken place during the tax year. What Inland Revenue is saying is the form will pop up in a client’s return if it thinks the client has made a bright-line sale. And it will also pre-populate the information on the form, including the title number, address, date of purchase and date of sale.

This illustrates something we’ve spoken about many times, the level of information that’s available to Inland Revenue. It’s actually very good, in my view, that Inland Revenue is proactively putting in this information and saying, “Well, we know this.” I am aware that a few tax agent colleagues have had some very interesting discussions with clients where this notification has popped up and it’s the first the accountant or tax agent has heard about the matter.

As of last income year, all portfolio investment entity (PIE) income must be included in individual income tax return. Inland Revenue will pre-populate returns with the relevant data but not all returns will contain all the PIE information until after the PIE reconciliation returns and filed on or before 16th May.

In the meantime, Inland Revenue has reminded tax agents about this and advised not to file March 2022 tax returns either through Inland Revenue’s myIR or other tax return software until after that date unless you know for certain that the client is not a KiwiSaver member and does not have any other PIE income. That’s something to keep in mind because I’m sure some tax agents will be under pressure from clients who think that they are due a refund but haven’t factored PIE income into the equation.

What’s also going into tax returns is details of payments received under the Wage Subsidy Scheme, Leave Support Scheme and Short-Term Absence Payments. All these are what are termed reportable income. Consequently, tax returns will be required to be filed by recipients and there is going to be an information request in relation to these as part of the tax returns. Yet again, this is another example of how MSD and Inland Revenue shared the relevant information.

Inland Revenue administers the highly successful Small Business Cashflow Scheme which gave out loans to small businesses at the start of the pandemic. The initial two-year interest free period is now expiring for some businesses so repayments will be required to start shortly.

Talking about COVID-19 support, the numbers involved were quite extraordinary: apparently MSD has so far paid out $19.28 billion in the various subsidies and leave support payments. And Inland Revenue has paid out another $3.95 billion including Resurgence Support Payments and COVID-19 Support Payments.

The Resurgence Support and COVID Support payments were paid to businesses to help them pay business costs and therefore GST output tax is required to be returned on those receipts. Where the funds are used on relevant expenditure GST input tax credits may be claimed.

Inland Revenue has started checking that those who claimed the support payments were entitled to do so and assuming they passed that hurdle, they then applied the expenditure as was intended, i.e. business expenses. And I’m hearing stories from tax agents of very thorough investigations combing through the bank accounts of the businesses and individuals who received these payments. Some have resulted in “Please explain” enquiries coming back where apparently personal expenditure has been identified such as in one case where an EFTPOS payment for McDonald’s was identified.

This is yet another warning for those who applied for COVID support payments they either weren’t entitled to or misapplied the payments that they may find themselves under the gun from Inland Revenue. So far Inland Revenue have decided to proceed with 15 criminal charges and court proceedings are already underway for seven. In addition, as a result of investigations and some self-reviews the repayments made to date to MSD are over $794 million. ,

All of this is a timely reminder that with things calming down a little bit and so coming back to a stability, Inland Revenue is now applying itself back to its core business activities of investigations and reviews. Expect to see more news of these reviews and I think we may see one or two interesting cases emerge.

What Parker means

Moving on, last week’s speech by the Minster of Revenue David Parker quite predictably caused a stir and there was plenty of politicking over whether or not the proposal would lead to the introduction of wealth tax at some point and whether the Prime Minister would stand by her comments it wasn’t going to happen, the usual politicking etc. etc.

Subsequently, last Sunday I appeared together with Jenée Tibshraeny of www.interest.co.nz on TVNZ Q&A to discuss the implications of Mr. Parker’s speech. Off-air Jenée made a point echoed by several colleagues commenting on a LinkedIn post that the Tax Principles Act, if enacted, would work both ways. It wasn’t just a tool for saying, “Well, we need to introduce a particular type of tax.” It could equally stop a government introducing changes because it contradicted the agreed principles.

It’s a very valid point and it’s actually one of the sources of disagreement with the introduction of the 39% tax rate, because it affects the integrity of the tax system and the idea of administrative efficiency. Furthermore, it could apply to the measures relating to personal services, income attribution, which also I discussed last week. The argument here is that these rules would breach potential principles of horizontal equity, in that people earning similar amounts, may pay different rates of tax because of variations in the tax treatment.

Under the microscope

Other interesting insights have emerged in the wake of the speech. The Revenue Minister pointed to the lack of information about the high wealth individuals which prompted the research project into high wealth individuals would have caused some controversy. And earlier this week journalist Thomas Coughlan in the New Zealand Herald commented on an interesting briefing note about the project he’d obtained under the Official Information Act.

The briefing note looked into the representativeness of the wealth project population, and whether the high wealth research project population effectively represented the 0.1% of the wealth distribution of the population and the economic sectors they operated.

The note explains that the group that was selected for the project was based on

…environmental scanning undertaken by Inland Revenue over the past 20 plus years. This environmental scanning involved monitoring large transactions or other indications that individuals had significant wealth holdings using both public information and the department’s tax data. …

The briefing notes the selection is non-random and it is not expected to be representative of the population of all high wealth individuals. It is therefore quite possible that there may be high wealth individuals missing from the group “and there is no way to definitively state that the selected group is representative of the top 0.1% of the wealth distribution.”

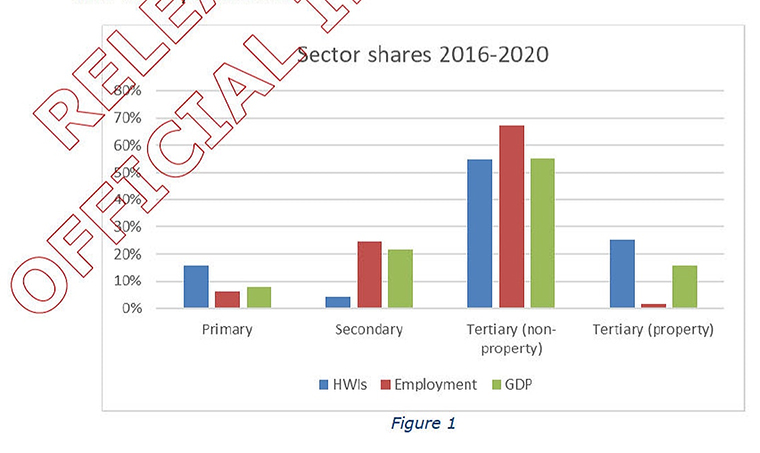

Having included that caveat, the note had some interesting analysis of what they had found so far. And it had a diagram comparing the share of GDP and employment to the main activities of high wealth individuals on the basis that you could reasonably expect the share of the industries represented by the individuals to be broadly similar to the spread of industries and activities in the New Zealand economy.

But it turns out that wasn’t the case. And in particular, relative to employment and GDP shares, the property and primary sectors are disproportionately represented in this project. The number of high wealth individuals in the primary sector is approximately 15%, even though the sector represents less than 10% of GDP. In relation to the property sector the proportion of high wealth individuals is 25%, compared with approximately 15% of GDP.

However, as the briefing note commented, there are clear reasons why there is this discrepancy “…there are certain activities (investment, property ownership) that would be expected to have greater involvement by those accumulate significant wealth….”

Incidentally, the primary sector and particularly the property sector, are sectors where existing tax rules such as the Bright-line test and the associated person rules work already to tax capital transactions. So that’s another reason why Inland Revenue may have better data on this particular group of wealthy individuals than others that work in the service economy.

Anyway, it will be interesting to see what further insights emerge from this high wealth research project. Meantime, no doubt the debate over how that data may be applied and the question of the taxation of capital and wealth will continue to rage, particularly in the run up to next year’s election.

Getting ready for tax filing season

And lastly this week, the final instalment of Provisional tax for those with a 31st March year-end is due on Monday. The key point here is taxpayers whose residual income tax liability for the year is expected to exceed $60,000, should ensure that they pay sufficient provisional tax to cover that total liability for the year. Otherwise, use of money interest, which is increasing to 7.28%, will start accruing together with potential late payment penalties.

As always, if taxpayers are struggling to meet payments in full, then either contact Inland Revenue to let them know and start to arrange an instalment plan. You will find that they are generally cooperative on this. Alternatively, consider making use of tax pooling to mitigate the potential use of money, interest and late payment penalties.

Well, that’s all for this week I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

Ministers of Revenue typically deliver several speeches during the year, mostly to business audiences or at the start of tax conferences.

On Tuesday, however, the Minister of Revenue, David Parker, delivered a speech at Victoria University Wellington entitled Shining a Light on Fairness in the Tax System, which is without doubt one of the most interesting speeches made by any Minister of Revenue in many years.

After some scene setting about the purpose of tax and how the Government has been able to use tax revenues to fund its COVID 19 response, Parker then pivoted to talk about beginning what he called a fact-based discussion. He started by challenging the assumption that our tax system is progressive overall.

“What’s hidden that the effective marginal tax rate for middle income Kiwis is generally higher than it is for their wealthiest citizens. Indeed, some of their wealthier Kiwi compatriots pay very low rates of tax on most of their income.”

The Minister then dived into the question of the lack of data on the distribution of wealth and capital income in New Zealand. He highlighted the fact that according to the Household Economic Survey, the highest net worth ever reported was $20 million.

This was, he said, ridiculous, given that we know there are billionaires in the country. As he pointed out, that meant the National Business Review’s annual rich list is a better set of data than the official statistics. In fact, that’s quite common around the world as statistics on capital wealth are rare and rich lists are often used to help revenue authorities gather data in this area.

So this lack of data, Parker explained, was the rationale behind the powers granted to Inland Revenue for the purposes of conducting research into high wealth individuals. As listeners will know, this is a somewhat controversial project, even though the Minister repeatedly stated that the intent was to gather better data for research and not as had been accused, so Inland Revenue could secretly work on new taxes.

“Until we have a much more accurate picture about how much tax the very wealthy pay relative to their full “economic income”, we can’t really we can’t honestly say that our tax system is fair.” And this led on to the most surprising part of the speech his proposal for a Tax Principles Act.

He referenced four principles of taxation that Adam Smith set out in Wealth of Nations back in 1776. And he noted that the many tax working groups and other reports that New Zealand has had over the past 40 years, such as the McCaw Review in 1982, the MacLeod Review in 2001, the most recent tax working group, and the all the work that went on during the Rogernomics period all basically followed these four principles set out by Adam Smith.

“They all endorse the same principles, based in that most core value of New Zealand – fairness. The main settled principles are:

Horizontal equity, so that those in equivalent economic positions should pay the same amount of tax

Vertical equity, including some degree of overall progressivity in the rate of tax paid

Administrative efficiency, for both taxpayers and Inland Revenue

The minimisation of tax induced distortions to investment and the economy.”

He also noted that recent reviews in the UK and in Australia both adopted similar approaches. Incidentally and perhaps not coincidentally here, Deborah Russell and I adopted the same principles when we wrote Tax and Fairness back in 2017.

And as you know, Deborah is now the Parliamentary Under-Secretary for Revenue and David Parker’s number two. The proposal is that officials should periodically report to ministers on the operation of the tax system using the principles as the basis for the reporting.

The Tax Principles Act would sit alongside existing legislation, such as the Public Finance and Child Poverty Reductions Acts, which also require the Government and officials to report on specific issues. This is quite revolutionary, but in a way sits within the philosophy of open tax policy that New Zealand has adopted through what we call our generic tax policy process.

This open approach to developing tax policy is widely regarded as world leading by other jurisdictions. The proposed Tax Principles Act is not inconsistent with the existing approach. The intention is there will be consultation later this year and following that a bill would be introduced once the principles had been agreed and the reporting requirements had been established.

The resulting bill would be enacted before the end of the current parliamentary term, i.e. just in time for next year’s election. The proposal caused quite a stir and there’s plenty of good reading on it. Bernard Hickey has a very good summary of the matter.

It’s also quite rare certainly to see Ministers of Revenue philosophise in quite a public way. David Parker referenced Thomas Piketty’s seminal work, Capital in the 21st Century. He also acknowledged the very regressive nature of GST. Somewhat controversially he noted that because GST in transactions between GST registered businesses essentially zeros out and is a final tax for those who are not GST registered, it many ways it falls on labour earners.

As he put it, “GST is really paid out of our earnings when we spend it. In economic terms, GST is mainly a tax on labour income. Who pays that cost?”

The Minister noted we have limited data on the overall rate of GST paid by New Zealanders, either by income or wealth decile. So he’s asked Inland Revenue to gather data and to provide feedback on this. I suppose from a political viewpoint this hints that potentially if there are changes to a tax mix at a later date, something may be done in relation to GST as it impacts lower income earners.

All this kicked up quite a stir. When I appeared on Radio New Zealand’s the Panel following the speech, the panellists expressed some shock about the fact that we don’t really have data about how wealthy people are. I think the reason for this, which wasn’t discussed by Minister Parker, is that it’s probably largely the unintended consequences of the abolition of stamp duties, estate and gift duties, and the absence of a general capital gains tax.

In other jurisdictions which have some or all of those taxes, this gives a reference point when a transaction occurs as to what wealth is held and by whom. Incidentally, the disclosure requirements regarding trustsI discussed last week although they are primarily an integrity measure, they also represent, in part, an attempt to gather some data about wealth held in trusts and help fill the gaps in Inland Revenue knowledge.

With National and Act already putting out their tax proposals, it looks like tax will feature quite heavily in next year’s election. So it’s very much a case of let’s watch this space.

Firstly, that sales and share of shares in a company with undistributed retained earnings would trigger a deemed dividend.

And secondly, changes to the personal services income attribution rules, which would mean more income would be attributed to a primary income earner.

Now, neither of these proposals have gone down particularly well and to describe them as controversial would be a bit of an understatement. The personal services attribution rules, in fact, may well have a very much wider effect politically than the Government might want to see.

Brian Fallow, writing in a very good column in last week’s New Zealand Herald, pointed out that the attribution rules, if enacted, would affect very large numbers of small businesses quoting former Inland Revenue Commissioner Robin Oliver “It is likely to catch tradies — a plumber, say, or a landscape contractor — with a van and some equipment and just themselves or one employee doing the work,”

And Oliver raised the question, is this really appropriate? I expect a lot of submissions on this paper, and I urge you to do so because as you can gather from comments made by Oliver, it could have a quite potentially significant impact for the SME sector.

I personally think the proposals go too far. And incidentally, one of the reasons that the proposals have been made comes back to a longstanding topic in this podcast and something that wasn’t directly referenced by Minister Parker in his speech, the absence of a general capital gains tax.

Inland Revenue proposes any transfer of shares by a controlling shareholder to trigger a dividend where the company has retained earnings. In jurisdictions which have capital gains tax, that transaction is normally picked up as a capital gain. But as we don’t have a capital gains tax Inland Revenue is proposing a workaround which I don’t think is appropriate one.

They are understandable, but I believe go too far and are probably targeting the wrong group of people. Moving on Inland Revenue has a useful draft interpretation statement out considering what is the meaning of building for the purpose of being able to claim depreciation.

This has actually become quite relevant because back in 2011 the depreciation rate on buildings was reduced to zero. But in 2020, in the wake of the pandemic, the depreciation rate for long life non-residential buildings was increased from 0% to 2% if you use a diminishing value basis or 1.5% if you’re using straight line method.

What this draft interpretation statement explains is the critical difference between residential and non-residential buildings. it replaces a previous interpretation statement released in 2010 which has had to be updated following an important tax case in 2019 involving Mercury Energy.

A building owner will be able to claim depreciation for a ‘non-residential building’ and that can in some cases have some residential purposes. Generally, it’s aimed at commercial industrial buildings and certain buildings such as hotels, motels that could provide residential commercial accommodation on a commercial scale. It’s a useful explanation and comments on the draft close on 2nd May.

The projection was that over the ten years to 2020, it would raise about US$8.7 billion US. The US equivalent of Inland Revenue, the Internal Revenue Service, (the IRS) spent US$574 million implementing FATCA. But according to a report just released, all the IRS can show for all that money invested are penalties totalling just US$14 million.

Now, that’s quite extraordinary. And this is important from a New Zealand perspective, because FATCA represents a huge compliance burden for all US citizens who are required to file tax returns, even if they may be tax resident in another jurisdiction.

FATCA was the template for what became the Global Common Reporting Standards on the Automatic Exchange of Information. The rest of the world looked at FATCA and thought, “That’s a good idea. We’d like to have some information about what overseas accounts our taxpayers have”. And so, the CRS, as it’s known, was introduced and has been in force now for about four years.

I would hazard a guess that Inland Revenue probably gathered well in excess of US$14 million as a result of the introduction of CRS. But to come back to a point that David Parker made about politics and tax being inseparable. One of the reasons that the IRS has done so badly is that the Republican controlled Congress won’t give it the money to do its job. And that situation doesn’t look likely to change.

As David Parker said, politics and tax are inseparable. And we’re going to hear plenty more about the two in coming months.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients.

Until next time kia pai te wiki, have a great week!

The Taxation Annual Rates for 2021 to 2022 GST and Remedial Matters Bill was introduced to Parliament on Wednesday. Now this is the annual bill which is required to confirm the tax rates for the current year. And it also contains a number of GST and income tax remedial amendments. It doesn’t, by the way, include anything in relation to the proposed interest limitation rules. Those are going to be introduced separately, probably later this month, by way of a Supplementary Order Paper.

Now, what’s particularly interesting about this bill is that it clarifies the tax treatment of cryptoassets, and it has two proposed amendments which would exclude cryptoassets from GST and the financial arrangements rules.

As the commentary to the bill points out, cryptoassets probably fall within the existing scope of GST rules, although it’s a little unclear. And that means that the supply of a cryptoasset could be subject to 15% GST, or it could be an exempt financial service or a zero-rated supply to a non-resident. And what this means is that GST supply to a non-resident is zero rated, but then subject to GST when applied to residents. And that creates a distortion and a preference to sell to offshore investors. Now, that’s slightly different from the zero rating we do for exports, but it’s not seen as an export service here.

But more importantly – and this is an issue that’s well known – is that there’s a big risk of potential double taxation. That is when an asset is purchased with Bitcoin and then, for example, that Bitcoins converted back into fiat currency.

The commentary gives an example of Lucy purchasing $11,500 of Bitcoin from a domestic Bitcoin exchange. At present, the exchange is required to remit $1,500 dollars of this, being GST, to Inland Revenue on the taxable supply of Bitcoin they’ve made in exchange for New Zealand dollars. When Lucy uses the $11,500 of Bitcoin to purchase a car, GST applies on the sale of the car and therefore the company selling the vehicle must return another $1500 dollars of GST. So that means that GST of $3,000 has effectively been charged in relation to the purchase of a vehicle worth $10,000. If Lucy had used New Zealand dollars instead of Bitcoin, only $1500 of GST would have been paid.

This has been known for some time and what has happened is that the Government has decided they’re going to take cryptoassets out of the GST net. And the proposal is that the definitions of goods and services in the Goods and Services Tax Act will be amended to expressly exclude cryptoassets. Now, this amendment will apply from 1st January 2009, the date of the first cryptoasset, Bitcoin, was launched. By the way, the definition will exclude non fungible tokens, which are going to remain subject to GST if supplied by a registered person.

So this is a very welcome development, clarifying the position that was causing some concern in the cryptoassets world, for the reasons and the example I gave a bit earlier – that there was a probable chance of GST being charged twice in essence, on the same asset. But just remember that GST is still intended to apply for non-fungible tokens as they’re regarded as a good or service that can be supplied.

Now, the other big amendment, which will be welcomed by investors in the cryptoassets world is that cryptoassets will be excluded from the financial arrangements rules. That will be done by amending Section EW5 of the Income Tax Act 2007 to define cryptoassets as an accepted financial arrangement.

Again, however, the issuing of non-fungible tokens are not financial arrangements and they do not meet the definition of a financial arrangements set up in the Section EW 3 of the Income Tax Act. This proposed amendment will also apply from 1st January 2009.

But there is one exception that people need to be aware of, that is cryptoassets will not be treated as an accepted financial arrangement if the owner receives amounts that are determined by reference to the purchase price of cryptoassets, and on the basis that is known by the owner in advance. The purpose of this exclusion is to say that cryptoassets that are economically equivalent to debt arrangements are still taxed under the financial arrangements rules.

And the commentary has an example of such a treatment. An investor invests in Bitcoin on a platform and Bitcoin is locked in for a set period and the investor is paid a guaranteed fixed return for the period that his Bitcoin remains locked into this particular platform. The commentary makes clear that the return on the growth will be taxable, so the additional 5% return will be subject to the financial arrangements rules. I think there might be some more questions dealing around that.

And the commentary also makes clear that the general rules still apply to cryptoassets. That if they’re acquired with the purpose of disposal, they’ll be taxable. Likewise, if you’re trading cryptoassets or you use cryptoassets for a profit-making scheme. But as I said, all the proposals will be welcomed by the investors in the cryptoassets world.

Now, the bill also has proposed amendments in relation to the bright-line test. Firstly, any income derived on the sale of a property which has been used as a main home will not be reduced where the person has used the main home exclusion twice in a two-year period or has engaged in a regular pattern of acquiring and disposal disposing of residential land.

The bill also has an amendment to ensure that a main home that takes longer than 12 months to construct will not be subject to the bright-line test. And this is in relation to residential land acquired on or after 27 March 2021. There’s also an amendment to clarify the application of the 12-month buffer and makes clear that a person may still qualify for the main home exclusion if they have multiple periods each of 12 months where the property is not used as a main home. So, again, that’s welcome because there was some confusion around how these rules might apply.

Business subsidies for wide public health impacts

Now, moving on, the Government’s Wage Subsidies bill has passed $1.2 billion dollars so far. And apparently this subsidy is supporting over 838,000 employees, 117,000 self-employed people and 242,000 businesses.

The highest number of supported workers are in the construction industry, followed then by food and hospitality.

Now, it’s also been made clear that although most of the country has stepped down to Level Two – the wage subsidy is not normally available below Level Three – a claim is still possible if part of the country is still in Levels Three and Four. Because Auckland has remained at Level Four, that means that businesses outside Auckland may still apply for the wage subsidy. However, they have to show the 40% drop in revenue required to meet the wage subsidy requirements is attributable to the effect of the continuation of Alert Levels Three and Four.

So that’s a wee caveat in there that people just need to be mindful of. I know that there’s lobbying going on in relation to the hospitality industry, where the impact of Level Two restrictions limit numbers in bars and restaurants to 50 or fewer. Those lobbying want the ability to still apply for a wage subsidy because they’re affected by that Level Two condition, not necessarily because of the ongoing Level Four lockdown in Auckland.

More taxes to pay for an ageing demographic?

And finally this week, government departments have been asked to prepare a series of long term insights briefings under the Public Service Act 2020. Now these are designed to make available to the general public information about medium- and long-term trends, risks, opportunities that may affect New Zealand.

Treasury has also got a requirement to produce a statement regularly on the long-term fiscal position – what’s known as Long Term Fiscal Statement, and what it’s decided to do is combine the two and it’s released a draft paper for consultation, which makes fascinating reading.

One of the things it says, is that looking at the impact of Covid, it thinks net debt will now peak at 48% of GDP in 2023. And in the Treasury’s view, there is currently no need to reduce debt levels. And it believes that deficits will shrink as the temporary support measures will end. And it also notes that debt level remains low relative to its peers such as the UK, Australia, America. The interest rate composition of debt is much more favourable than when net debt peaked at 55% of GDP in 1992.

And just as an aside, this is a global issue. The UK just this week has announced proposals which effectively increase taxes to pay for the impact of Covid and they’re quite significant increases. And I don’t think that the UK will be the last jurisdiction to be doing so.

But longer term, Treasury is noting that 26% of the population is expected to be 65 years old or more by 2060, compared with 16% in 2020. So that’s going to increase the cost of New Zealand superannuation and also expect healthcare costs to continue to grow because of an ageing population. And that ageing population will change demographics. For example, one of the things that’s happening is that the Pasifika/Māori people are generally significantly younger than other New Zealanders.

For example, by 2038, Māori are projected to account for 20% of the total population, but only 10%of the 65 plus population.

And this leads Treasury to conclude:

“Our projections indicate that the gap between expenditure and revenue will grow significantly as a result of demographic change and historical trends in the absence of any offsetting action by the Government.”

One of the offsetting actions it suggests, is to raise the age of retirement from 65. It suggests let’s have a look at what would be the impact of raising it to 67.

It also looks at what opportunities exist to raise revenue from either existing tax basis or new tax bases beyond personal income tax. And the paper sets out a number of options around raising revenue. And one is ten years of fiscal drag, which incidentally we’ve just done, which is where the tax thresholds and rates are not changed. And wage growth naturally raises the tax take as people’s income crosses income tax thresholds.

Some interesting stats here about the impact of raising GST. For example, in relation to personal income tax – if you raise income tax rates by one percentage point, so that the current top rate of 39% goes to 40%, the 33% rate to 34% and so on, that would raise 0.6% of GDP.

To get the same effect from GST you’d need GST to rise from 15% to 16.5%. And for company income tax, you’d need to raise it from 28% to 34%. So as the paper points out that would not be welcome.

The Treasury paper also points out the Government could extend the taxation of capital gains and maybe think about a land tax as well. However, as the Tax Working Group pointed out there’s a few issues around a land tax. But the paper notes, by the way, that other countries are looking at the taxing of wealth, either by a net wealth tax or maybe taxes on inheritance.

And finally, the paper notes that New Zealand raises less from environmental taxes than other OECD countries. It’s equivalent to 1.3% of GDP, and that’s lower than the OECD average, which is roughly 2% of GDP. But it points out that environmental taxes are often behavioural taxes. In other words, they change behaviours but therefore may not be a sustainable additional source of revenue.

Anyway, there’s a lot of interesting data to consider in this paper. No doubt it will cause some controversy.

Well, that’s it for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.taxor wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and colleagues. Until next time Kia Kaha! Stay strong.