And reveals results of increased audit activities.

Is GST really a tariff?

It’s been a busy week in tax. Right at the start of the tax year, Inland Revenue has launched a public consultation on a review of the fringe benefit tax regime which is now 40 years old. The 75 page issues paper titled Fringe benefit tax – options for change reviews the current status of FBT, focusing on issues Inland Revenue has identified. It puts forward a number of proposals aimed at simplification of these rules and a reduction in compliance costs, a long standing issue with major employers. There’s plenty to digest here but there’s a summary of the proposals on pages 6-8 of the paper if you want to get a quick handle on the proposals.

Reimagining FBT

The paper also addresses the separate issue of general compliance with the regime. A particular source of grief amongst compliant taxpayers is the treatment of the ubiquitous twin cab ute and the application of the work related vehicle exemption. Overall, the purpose of the paper is to

“…to review how FBT is assessed now, highlight current issues we are aware of with FBT and then outline some new concepts for how we could think about a reimagined FBT regime that is less complex and more targeted…”

The paper has 12 chapters, beginning with an introductory chapter, with Chapter 2 setting out the aims of the review. Chapter 3 explains how FBT is currently assessed. Chapter 4 picks up the FBT regulatory stewardship review from August 2022 which is really one of the initiators of this project. Chapter 5 then provides some comparisons with international FBT regimes.

Chapter 6 has an interesting discussion about FBT’s connection with remuneration. We tend to forget FBT was mainly introduced to ensure that all types of remuneration were brought into scope. Back in the 1980s, before FBT was introduced and the top personal tax rate was 66% it was common practice to give employees non-cash benefits such as company vehicles. Countering this was a key driver behind the introduction of the FBT rules in 1985.

Chapters 7 and 8 look at FBT and motor vehicles and considers options for change. Chapter 9 considers one of the areas of complexity, the treatment unclassified benefits. Chapter 10 discusses the option of applying FBT on entertainment expenditure, a proposal which will probably surprise a few people. The paper notes that entertainment regime also attracts a great deal of controversy and complaints about the compliance costs involved. Finally, chapter 11 looks at miscellaneous issues before Chapter 12 looks at data filing and integrity.

Why such a tight submission deadline?

There’s a lot to consider in this paper but submissions are due by 5th May, which means between Easter and Anzac Day there’s barely 4 weeks in total to review the paper and make submissions. The Minister of Revenue, Simon Watts, has repeatedly expressed a wish to simplify the FBT rules so he is keen to get this moving. My understanding the reason for the tight timeline is a desire to have the relevant legislation ready to be part of this year’s main tax bill, which will be introduced around late August or early September.

Proposed changes to FBT on motor vehicles

I expect many will focus on the proposals for motor vehicles. An interesting proposal is to increase the weight limit for vehicles subject to FBT from 3,500 kg to 4,500. Given the weight limit for a person with a full individual drivers’ license is 6,000 kg, my view is the FBT limit should tie into that threshold. Another proposal is to exempt vehicles that are used for providing emergency services.

A key change is removing the tax book value based option for calculating the fringe benefit value of a vehicle. Something worth considering is the suggestion for an optional valuation basis based on the fuel source for the vehicle i.e. electric, hybrid or petrol and diesel.

As part of re-connecting FBT with remuneration the paper suggests the FBT value of the motor vehicle could be calculated by reference to external sources such as remuneration consultations or maybe the AA calculations of vehicle running costs. The paper suggests regular revaluations, maybe every four years. One of the reasons why the tax book value option was introduced was that if people are not changing their vehicles regularly, then there’s an issue that the vehicle may be overvalued for FBT purposes. The proposal would address this issue.

However, the Lord giveth, and the Lord taketh. The paper proposes the following new rates for calculating the fringe benefit value of a vehicle based on its cost:

standard rate: 26% annual or 6.5% quarterly

hybrid vehicles: 22.4% annual or 5.6% quarterly, and

electric vehicles: 19.4% annual or 4.8% quarterly.

Availability vs actual use

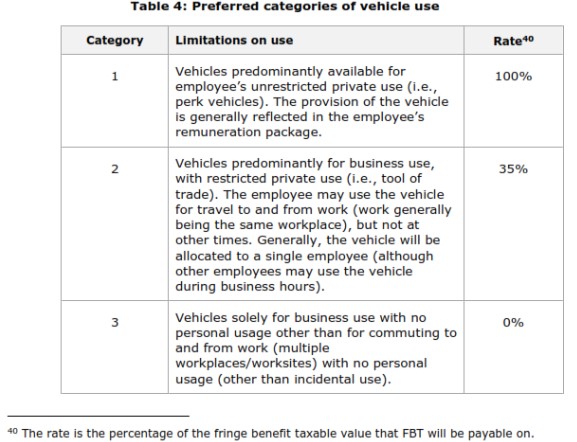

As part of the intention to simplify FBT, the suggestion is to no longer require taxpayers to maintain logbooks to determine the days the vehicle is available for private use. Instead, the focus will shift towards the actual extent of private use the vehicle is available for (for example, is it limited to home to work travel?).

The paper suggests the following categories of vehicle use:

As part of this change, the paper proposes excluding “incidental travel” to ensure that one-off private use of a vehicle can be ignored for FBT purposes. Behind this idea is a “close enough is good enough” approach.

A key proposal is to remove the current work-related vehicle exemption which as the paper says, is a “most misunderstood” exemption. The changes should address the issue of double-cab utes supposedly qualifying for the work related vehicle exemption and avoiding FBT entirely.

Changes to the entertainment regime

The other major proposal of note is integrating the entertainment regime into the FBT regime. Again, the idea behind this is to simplify quite a number of issues that currently exist in relation to the entertainment rules which have never been very popular and compliance is also a problem. As the paper notes many employers are taking a close enough is good enough approach to entertainment expenditure.

The interaction of the entertainment and FBT regimes can be confusing. For example, if an employer takes an employee out to a restaurant that is subject to entertainment rules. However, if the employer gives a voucher for that restaurant to an employee to use whenever they want, then that’s subject to FBT. Another example one would be if an employer pays for employees to participate in a front run, and then then provides a BBQ for staff staff at the finish line. Is the cost of the fun run subject to FBT but the BBQ represents entertainment? Integration of the two regimes is intended to address these issues.

Overall, this is a welcome review and as previously noted pretty timely given it’s now 40 years since FBT was introduced. Just remember you’ve got to get your skates on to submit by the deadline of 5th May.

Inland Revenue ramps up its audit activities with good results

At the start of last week Inland Revenue announced some of the results of its “noticeably increased” compliance activity. For the period from 1st July to 31st December 2024, it opened 3,600 audits 50% up on the same period in 2023. According to Inland Revenue’s Segment Lead for Significant Enterprises, Tony Morris, “Inland Revenue has found $600 million of additional tax that should have been declared.”

Morris went on to add “We’ve had a strong focus on the largest businesses in New Zealand and it’s worth noting that half of that additional tax came from less than 10 audits.” In other words 10 audits yielded $300 million.

Furthermore, Inland Revenue screened over three million returns as part of its annual year-end auto-assessment process. 30,000 of those, or about 1% were selected for review which resulted in a further $859 million of tax revenue. That’s a pretty good bang for buck on the additional funding it got in last year’s Budget.

Inland Revenue has also been focusing on debt and I thought this particular comment was of interest

“We’ve been in touch with 200 business owners and told them we know they have multiple properties – some in a company name, some in trusts, some personally. We believe they should be able to refinance to pay their debts to us and told them so.

“…These 200 people had $14 million of debt between them, but within a month more than $10 million had been paid or put under arrangement.”

Inland Revenue’s data gathering around property transactions is second to none and people would be wise to not underestimate this. It has been identifying transactions in this area for quite some time. A colleague recently told me of an audit that he was involved in where the client was saying, ‘Oh well, a number of property transactions were simply renovations of my main home’. That is until Inland Revenue investigators presented a “ream sized folder” full of property transactions for this taxpayer. From that point, the question wasn’t about rebutting Inland Revenue’s proposition that he was actually a property trader but trying to mitigate the damage. You have been warned.

“This is Baycorp calling on behalf of Inland Revenue”

However, something that does concern me is Inland Revenue’s announcement on 10th April it would be “running a six month pilot program in partnership with Baycorp to improve our debt collection process.”

Inland Revenue warned taxpayers that during this pilot, “you may be collected, may be contacted by representatives from Baycorp. Please be assured that these contacts are legitimate and part of our authorised programme.”

That’s as may be, but I’m not so sure given everyone’s growing concern about scams, not too many people are going to accept calls from Baycorp saying ‘you own Inland Revenue money pay up.’ I therefore doubt the pilot is actually going to be as effective as hoped even if Baycorp show the taxpayer incontrovertible proof that they have a debt due to Inland Revenue.

This is just the latest push by Inland Revenue to improving debt collection. As we noted in our last podcast given the rise in GST debt in particular, it’s basically no surprise that Inland Revenue is putting resources into debt collection. And as I’ve said previously, I expect there will be more funding given to it in next month’s Budget.

Is GST a tariff?

Meanwhile, around the world there has been large scale turmoil in the financial markets as everyone tries to work out what exactly is happening with the tariffs proposed by President Trump’s administration. As part of this he has indicated that value added tax (VAT) is now seen as a tariff. There’s been a huge pushback against this with the basic counterargument being that tariffs are only imposed on imported goods and services, whereas GST/VAT applies regardless of source of the goods or services

If you want more a bit more detailed analysis of why GST/VAT isn’t a tariff, I suggest this interesting post by Dan Neidle of Tax Policy Associates. He considers the issue using the example of beer, which is always handy, and the implications of the policy.

Removing GST from fruit and veg – “a well-known solution to every human problem”

The American writer HL Mencken was the source of the quote “There is always a well-known solution to every human problem – neat, plausible and wrong.” This often comes to mind in relation to the frequent proposal to remove GST from fruit and vegetables. It so happened the Prime Minister was asked about this suggestion on TV1’s Breakfast Show. He responded that it was far more complex than people imagined.

I subsequently appeared on Wednesday’s show to discuss the issues involved in removing GST from fruit and veg. To be fair following Mencken’s dictum about the policy being ‘wrong’ would be a bit harsh. This is an extremely well meant suggestion based on the precept if you wanted to try and help people struggling with the cost of living then removing GST is an option or step and no doubt would provide some assistance.

But as I explained it is complex and definitional issues lead to extreme examples such as the UK Mega-Marshmallows which enabled me to sneak in a reference to The Princess Bride. Furthermore, well-meant though it is, the proposal is not perhaps the right solution for the problem you’re trying to deal with, which is people with low income who are struggling with rising costs. A targeted response is more appropriate.

The Tax Working Group’s view

This was also the analysis of the 2018-19 Tax Working Group which also addressed a key complaint about GST, that it’s seen as regressive for those on low incomes. In response to addressing regressivity by perhaps reducing the rate of GST or introducing a GST exception for food the TWG commented “there are more effective ways to increase progressivity than a reduction in the rate of GST.”

Instead, the Tax Working Group suggested

“…increases in welfare transfers would have a greater impact on low income households. Changes to personal income tax can also have a greater impact on low and middle income earners. GST exceptions are complex, poorly targeted for achieving distributional goals and generate significant compliance costs, and furthermore, it is not clear whether the benefit of specific GST exceptions are passed on to customers.”

I agree with that analysis. It’s also supported by research carried out by Tax Policy Associates on the impact of VAT(GST) changes in the UK, where VAT has been removed from several products again for very well meant reasons. Examples include a reduction in the VAT rate for tampons and other menstrual products and the zero-rating of e-books. In both cases, the analysis carried out by Tax Policy Associates identified little or no benefit going to final consumers. In fact, in the case of e-books, no benefit passed through to consumers, costing the UK £200 million.

A complex and ineffective solution

In sum removing GST from fresh fruit and veg is complex and leads to boundary definitional issues. UK cases such as Mega-Marshmallows or the older Jaffa cake case involving the UK’s zero-rating of food are very, very good examples of the sometimes absurd distinctions that arise. Even although accounting systems are much improved the fact remains there are irreducible minimum compliance costs involved. These will fall most heavily on smaller operators such as dairy owners who already have a fairly heavy compliance burden with GST.

Much as I can see why people would want to suggest zero-rating fresh fruit and vegetables, ultimately, you’d have to consider whether the benefit of such a change is actually going to flow through to those who you want to benefit? Remember, if you do apply an exception, everyone benefits from it. As the Tax Working Group noted wealthier deciles spend more on food and fresh fruit and vegetables so would probably benefit disproportionately.

This isn’t a matter that’s going to go away. My view remains in line with that of the Tax Working Group. Look at what the real issue is, and it’s some families don’t have enough income. The best approach is therefore to give them more income. But we’ve got an election coming up next year and no doubt the proposal together with other well-meaning but inefficient ideas will be put forward.

And on that note, that’s all for this week, we’ll take a short break for Easter and be back for the ANZAC Day weekend. In the meantime I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day and Happy Easter.

Last Sunday, the Climate Change Commission released its draft advice for consultation. The draft advice has already stirred up a great deal of controversy and discussion about the suggested objectives for the country and how they are to be met.

On tax, the Commission’s Necessary Action 3 recommended accelerating light electric vehicle (EV) uptake. As part of this it suggested the Government –

“Evaluate how to use the tax system to incentivise EV uptake and discourage the purchase and continued operation of internal combustion engine vehicles.”

I’ve covered this elsewhere and my suggestion is that Inland Revenue needs to look at greater enforcement of the fringe benefit tax rules, maybe including an exemption for electric vehicles and looking also at the application of FBT to parking.

What else did the Commission discuss on the taxation side? Well, it noted that the climate transition will impact government taxation and spending and that the Government needs to plan for this. It noted that fuel excise duties, the revenue comes from that which is spent on land transport, will change and probably decline. It also noted that reducing oil and gas production will result in less tax revenue and also affect the balance of exports because of the reduction in oil exports.

On the other hand, the emissions trading scheme will generate income from the sale of emissions units. Obviously the amount raised will depend on the volume of units and the market price for years, but at current estimates are that it could equate to about $3.1 billion over the next five years.

Now, what the Commission has suggested is that maybe these funds could be recycled back into climate change projects. And that’s something I would agree with. In my piece on the Commission’s draft report I suggested that increased FBT take should be recycled into funding a vehicle purchase scheme.

So I think one of the things that comes out of the Commission’s draft report is that its recommended changes are going to affect the country and the community greatly, and we need to mitigate for that. And if funds are being raised from environmental taxation, my view is they need to be recycled into the economy to mitigate the impact of change.

That, by the way, was also the view of Sir Michael Cullen when he presented the Tax Working Group’s report, which covered environmental taxation, but its interesting observations on that were completely lost in all the hoo-ha over capital gains tax. As the Commission notes, one of the key objectives going forward is a

“process for factoring distributional impacts into climate policy and designing social, economic and tax policy in a way that minimises or mitigates the negative impacts.”

There’s going to be a very interesting debate on this issue which will continue for quite some time. But we are at a point where we’re going to need to take quick action, I believe, which come with consequences. We need to mitigate those consequences as far as possible.

Late last week, the OECD held its 11th meeting of the OECD/2020 inclusive framework on base erosion and profit shifting (BEPS). This is the international project on reforming international taxation.

The (virtual) meeting included a last address from the outgoing Secretary-General of the OECD, Angel Gurría. He talked about what has happened over his 15-year term as Secretary-General. As he said when he took the helm in 2006 –

“tax avoidance and evasion were running rampant. Urgent action was needed, and the aftermath of the global financial crisis presented the opportunity to crack down on these nefarious practices backed by the newly established G20.”

The Secretary-General then ran through the latest developments noting that 107 billion euros of additional tax revenue has been identified as a result of the initiatives such as the Common Reporting Standard and the Automatic Exchange of Information. There have been over 36,000 exchanges of tax rulings between jurisdictions and over 84 million financial accounts have been identified and exchanged in 2019, with a total value of around 10 trillion euros.

He also made a very important point that in a globalised world, tax cooperation is the only way to protect tax sovereignty. That was true at the start of his term in 2006 and remains the case now. Without such cooperation each country’s domestic tax policies are at risk. The latest state of play is a reflection of this where if an international solution is not found by the middle of the year, over 40 countries, including New Zealand, are considering or will move ahead with a unilateral digital services tax.

The solution to this is the so-called Pillar One and Pillar Two proposals. Now, these are progressing, and an encouraging fact is that the new United States Secretary of the Treasury, Janet Yellen, as part of her confirmation hearings stated the United States is –

“committed to the cooperative multilateral effort to address base erosion and profit shifting through the OECD/G20 process, and to working to resolve the digital taxation disputes in that context.”

So that’s extremely encouraging.

The Secretary-General also picked up the Climate Change Commission’s draft report, that carbon pricing is an issue that needs to be addressed. As Mr Gurría noted across the OECD 70% of energy related CO2 emissions from advanced and emerging economies are entirely untaxed. And so, as he put it, “putting a big fat price on carbon is one of the most effective ways to tackle climate change by creating incentives to reduce emissions.”

He also made an interesting comment about rising inequality, saying that policymakers need to do more in this space. This picks up a general trend I have seen emerging for quite some time, following the double whammy of the global financial crisis and covid pandemic, of a renewed focus on taxing wealth and using taxation to reduce inequality.

Now, the Climate Change Commission’s recommendations and the ongoing OECD BEPS Initiative are just two of the major policy issues on which Inland Revenue will be needing to provide policy advice and ultimately implementation. Although the Treasury provides advice to the Ministers of Finance and Revenue on tax policy, Inland Revenue is the main tax policy adviser to the Government. That’s actually quite unusual by world standards, where more often it is the Treasury Department that drives tax policy advice.

So where is Inland Revenue at in terms of where it thinks tax policy is going? Well, as part of its general processes it prepares a briefing to each incoming Minister of Revenue. And the briefing Inland Revenue provided to the new Minister of Revenue, David Parker has now been released.

Inland Revenue, in conjunction with Treasury, will develop a tax policy work programme, which is then signed off by the Ministers of Finance and Revenue. These programmes will show what the priorities are and the expected policy focus over the next 18 months.

Now, obviously, Covid-19 will have some impact on the programme. The five top policy issues that Inland Revenue have identified as key priorities are rebuilding the economy, issues related to misalignment of the top personal tax rate, the role of environmental taxes and what an environmental tax framework should look like, improving data analytics, and international tax settings.

And the briefing then goes on to set out significant current policy issues, most of which reflect these policy priorities. There is a specific item on taxing the digital economy which notes –

“Ministers will need to make a decision about the suitability of any OECD multilateral solution for New Zealand and whether to progress a unilateral digital services tax.”

But as often is the way it’s what’s not actually said in a document that makes it interesting. Briefings to Incoming Ministers are usually frank in giving an overview of where the department is at, what the main policy issues are as it sees it, and how it proposes that it should deal with the issues. But not everything is revealed.

And there are one or two interesting redactions in here, one of which appears to relate to some form of investigation into taxation of wealth. At a guess this is identifying the wealthy in the group, usually defined as those with more than $50 million dollars in assets, their tax behaviours, how much tax they pay and what are they doing to mitigate tax.

Interestingly, by the way, the tax concessions charities and not for profits get is going to be reviewed to “ensure they operate coherently and fairly and to ensure the integrity of the tax system is protected.” As the Tax Working Group noted, it received a number of submissions complaining about tax preference treatment of charities.

The Briefing also talks about Inland Revenue’s Business Transformation project, described as “complex, high-risk and fiscally significant (costing $1.8 billion)” in the separate briefing provided by the Treasury to the Minister of Revenue.

And there are some more very interesting redactions in here relating to funding of the Inland Revenue including references to other reports which have not been provided and which I have therefore requested under the Official Information Act.

What some of these redactions to an issue that in my view the Minister of Revenue and the Commissioner of Inland Revenue, Naomi Ferguson, need to address, is the poor state of morale.

Inland Revenue’s 2020 Annual Report, released just before Christmas, at the same time as the Briefing to Incoming Minister, puts its staff engagement at a shocking 25%. And it has been bumping around at the 25 to 29% for several years now. And that’s an impact of Business Transformation, which has shaken up the workforce in Inland Revenue quite substantially. In the year to June 2016, the headcount of Inland Revenue was 5,789. As of 30 June 2020, that has fallen to 4,831.

So a substantial amount of change has gone on in the department which doesn’t appear to have been welcomed or met with enthusiasm. It has certainly had a dramatic impact on the Inland Revenue staff engagement and morale. Whatever you might think about Inland Revenue and its activities, poor staff engagement is not good for tax payers at large.

It should be said that remarkably and consistently Inland Revenue staff in their direct interactions with tax agents like myself and the general public continue to be highly professional, well-mannered and and responsive to our needs. But clearly behind the scenes, there is stuff going on that needs to be fixed and that should be a priority for the Minister of Revenue and the Commissioner of Inland Revenue.

There’s also ongoing controversy around exactly what savings are going to be achieved from Business Transformation. The scale of the Business Transformation project means the Cabinet gets regular updates on progress. So next week I’m going to take a closer look at a couple of the documents that have also been released in relation to Business Transformation. These report on how it’s progressing relative to what was expected and what changes and additional funding, if any, may be required.

Well, that’s it for today. I’m Terry Baucher and you can find my podcast on website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients. Until next week, Ka kite āno.

The Commission’s Necessary Action 3 recommended accelerating light electric vehicle (EV) uptake. As part of this it suggested the Government:

Evaluate how to use the tax system to incentivise EV uptake and discourage the purchase and continued operation of ICE [internal combustion engine] vehicles.

As the Commission is no doubt aware taxes can have significant behavioural changes very quickly as the following example of the changes in the United Kingdom’s Landfill Tax illustrates.

Between its introduction in 1996 and 2016 the rate of Landfill Tax was increased from just under £10 a tonne in 1996 to nearly £90 a tonne by 2016. Over that 20-year period the annual amount of waste landfill fell from 50 million tonnes to 10 million tonnes.

So what tax changes could be used to incentivise change?

The available evidence indicates that the present fringe benefit tax (FBT) rules are unintentionally environmentally harmful. A NZ Transport Agency report in 2012examining the impact of company cars found they were heavier with higher engine ratings than cars registered privately. The availability of employer-provided parking encouraged longer commutes from more dispersed, automobile-dependent locations than would otherwise occur. Under present rules employer-provided parking is largely exempt from FBT.

A by-product of the trend for purchasing of twin-cab utes appears to be widespread non-compliance with the existing FBT rules. This is in part because of an incorrect perception that such vehicles automatically qualify for the “work-related vehicle” exemption from FBT. The combination of greater numbers of such vehicles and apparent under-enforcement of the FBT regime[1] exacerbates the trend for indirectly environmentally harmful practices identified by the NZTA in 2012.

Inland Revenue should therefore immediately increase its enforcement of the FBT rules relating to twin-cab utes. These changes should be allied with the adoption of the approach in Ireland and the United Kingdom where FBT is greater on higher emission vehicles. I consider these emission-based FBT rules can be adopted relatively quickly, and it ought to be possible to have these in place by 31st March 2023.

As an interim measure to encourage greater take up of EVs the Government could consider exempting EVs from FBT until the new emission-based FBT rules are in place. In Ireland, EVs with an original market value below €50,000 are presently exempt from FBT. The threshold here could be $50,000.

Additional FBT related measures include increasing the application of FBT on the provision of carparks to employees and not taxing the provision of public transport to employees. This reverses the present treatment and fits better with a policy of decarbonisation without impacting an employer’s ability to provide such benefits.

Taxing the provision of employer-provided carparks could raise significant funds. The 2012 NZTA report estimated the annual value of free parking in Auckland to be $2,725. With at least 24,000 employer owned car parks in the city this amounted to a tax-free benefit of $65 million per annum. FBT is generally charged at 49% of the value of the benefit so the potential FBT payable could be between $75 and $100 million per annum.

The suggested FBT changes should change behaviour, but as the Commission also pointed out we need to reduce emissions. We have one of the oldest vehicle fleets in the OECD and it is getting older. The average age of light vehicles in Aotearoa New Zealand increased from 11.8 years to 14.4 years between 2000 and 2017.[2] Compounding this issue, the turnover of the vehicle fleet is slow, on average vehicles are scrapped after 19 years (compared with about 14 years in the United Kingdom).

Furthermore, we are one of only three countries in the OECD without fuel efficiency standards. As a result the light vehicles entering Aotearoa New Zealand are more emissions-intensive than in most other developed countries. For example, across the top-selling 17 new light vehicle models, the most efficient variants available here have, on average, 21% higher emissions than their comparable variants in the United Kingdom. They are also less fuel efficient, burning more fuel and therefore generating higher emissions. The Ministry of Transport estimated if cars entering Aotearoa New Zealand were as fuel efficient as those entering the European Union, drivers would pay on average $794 less per year at the pump.

The Commission is concerned about the impact of its proposals on low-income families, who could be asked to bear a disproportionate part of the costs of change. For this reason, I suggest the funds raised from the FBT changes should be first applied to a vehicle exchange programme. This would remove older higher-emitting vehicles (say ten or more years old) by subsidising purchase of newer vehicles (maybe from car rental companies with excess stock).

If it seems counter-intuitive to subsidise “old carbon” technologies there are three short-term benefits to consider: newer cars generally have lower emissions, are more fuel efficient and are safer, indirectly helping reduce the road toll. This scheme also supports the most vulnerable families who cannot rely on public transport and are most likely have older, less fuel-efficient vehicles. Furthermore, funds involved would go further than if applied in directly subsidising the purchase of electric vehicles.

I also suggest the buy-back scheme is targeted at lower-income families and should therefore be means-tested. A starting threshold might be the Working for Families tax credits threshold of $42,700 above which abatement applies. This threshold could be increased if the vehicle is more than, say, 15 years old with accelerated rates applying if the car is more than 19 years old (i.e. older than the life expectancy of the average car in Aotearoa New Zealand).

The Commission has opened the debate on our transition to a greener, low-emissions economy. Tax will have a major role in that as Pascal Saint-Amans, the Director of the OECD’s Centre for Tax Policy and Administration acknowledged last year when he suggested that when responding to the impact of Covid-19.

Governments should seize the opportunity to build a greener, more inclusive and more resilient economy. Rather than simply returning to business as usual, the goal should be to “build back better” and address some of the structural weaknesses that the crisis has laid bare.

A central priority should be to accelerate environmental tax reform. Today, taxes on polluting fuels are nowhere near the levels needed to encourage a shift towards clean energy. Seventy percent of energy-related CO2 emissions from advanced and emerging economies are entirely untaxed and some of the most polluting fuels remain among the least taxed (OECD, 2019). Adjusting taxes, along with state subsidies and investment, will be unavoidable to curb carbon emissions.

Unfortunately, the backlash against the TWG’s proposed capital gains tax meant that its commentary and proposals on environmental taxation were overlooked.

Nevertheless, the TWG’s groundwork in this area now needs to be built on. It’s therefore interesting to note that in its briefing to the new Minister of Revenue David Parker Inland Revenue noted one of its top tax policy priorities was “the role of environmental taxes and what an environmental tax framework should look like.”

Given that David Parker is also the Minister for the Environment I suggest Inland Revenue might be accelerating its work in this field, if the goals suggested by the Climate Change Commission are to be met. Watch this space.

[1] FBT is tied to employment. Over the 10 years to 30th June 2020 the amount of PAYE collected by Inland Revenue rose by almost 66% from $20.5 billion to $34 billion. However, over the same period the amount of FBT paid rose 28% from $462 million to $593 million. This gap suggests some level of under-reporting and enforcement.

[2] By comparison in the United States in 2016 it was 11.6 years for cars and light trucks and 10.1 years for all vehicles in Australia for the same year and 7.4 years for passenger cars in Europe in 2014 (Ministry of Transport data)

The Tax Working Group report and capital gains tax

Inland Revenue’s business transformation

OECD’s international tax proposals

Transcript

This week, our final episode of the year takes a look back at the big tax stories of 2019 and also casts an eye over the tax events of the past decade.

The Tax Working Group report

The release of the Tax Working Group report and the Government’s decision not to follow through on the group’s recommendation for a general capital gains tax is by far and away the biggest tax story of the year. Although the Prime Minister stated that as long as she remains leader of the Labour Party, she will not be proposing a capital gains tax, the issue still excites and generates quite a degree of controversy. The reaction, for example, to a recent podcast in which I talked about Robin Oliver and Geof Nightingale’s session about why a capital gains tax didn’t happen at the recent Chartered Accountants Australia New Zealand Tax Conference is a good illustration of that.

As I’ve said many times beforehand, the frustrating thing for me about the aftermath of the Tax Working Group is that the debate around a capital gains tax completely drowned out all the other good work the group undertook. Some very interesting matters were raised and discussed. The tax system was found to be in generally good health, but there were issues. Pressures are building around the demographics and the funding of New Zealand Superannuation and rising health care costs for our ageing population.

On the other hand, the Government’s books are pretty solid and there is no immediate requirement to be raising revenue and expanding the tax base to pay for those additional costs. So, a capital gains tax is not something that’s going to be immediately necessary. But what the group did point out was those pressures are not that far off and we need at some stage to consider how the tax base will respond to that.

The other thing I thought was very interesting and I’ve talked about it before, is we started to see some movement on the question of environmental taxation. The TWG said we could do a lot more in this space. But also, and certainly this was Sir Michael Cullen’s recommendation initially, much of any changes that happened in this environmental taxation space should be in terms of recycling the funds through to enable the transition to a lower carbon emission economy. And that is something which is much more immediate and doesn’t require a capital gains tax. We should really be spending more time debating how we will implement these taxes and in which way we will allocate the funds that are raised.

Inland Revenue

The second large story for the year was Inland Revenue’s Business Transformation and in particular its Release Three, which happened in April. This is when it said, right, we are going to do auto-calculations for all taxpayers. And instead of them having to use a tax intermediary, Inland Revenue will automatically calculate the unders and overs for the year and issue appropriate refunds or demands as required.

This is a hugely ambitious project. About 2.9 million automatic assessments were processed resulting in approximately $572 million dollars of refunds being paid to taxpayers. But it threw up quite a lot of controversy. Probably in hindsight Inland Revenue was too ambitious in what they tried to do. They were bedding in the new tax system which for example involved transferring something like nineteen point seven million records into the new START (Simplified Tax and Revenue Technology) system.

Two key points emerged from the switch. Firstly, somehow over a period of time, 1.5 million people had managed to get their prescribed investor rate wrong. So those who had underpaid were expected to pay up. But those who had overpaid on average about 40 dollars each weren’t going to get a refund.

Now, as it transpires, political pressure and the howls of outrage from the public means that work is in progress to correct this issue. Currently the Finance and Expenditure Committee is looking at a measure which will deal with the question of the overpayments not presently being able to be refunded. That’s a good outcome coming from that pressure.

We don’t need no education?

What that issue shows to me though, is something that’s been taken for granted across the system. Not just this year, but for the past decade and probably even longer. And that is a dangerous assumption – that taxpayers know how the system operates and will always act in their own best interests because they are always across what’s happening their prescribed investor rate, their PAYE codes. That’s clearly not true. And it’s something Inland Revenue and tax professionals will have to deal with going forward.

Looking ahead to what’s going to be happening over the next three or four years, I think it’s probably one of Inland Revenue’s greatest priorities to introduce an educational process to ensure people are kept up to date about what happens with their KiwiSaver and PAYE.

The other part of the fallout from Release 3 as it was called, was that Inland Revenue basically did enormous damage to its relationship with tax agents. We as a group were pretty much left out in the cold about how to manage the transition to the new tax system. As a result, our experience in using the phones when interacting with Inland Revenue was uniformly very poor. And the survey I talked about last week with Chris Cunniffe of Tax Management New Zealand shows how dissatisfied tax agents have become with Inland Revenue’s performance.

Now credit to the Commissioner of Inland Revenue Naomi Ferguson, she’s acknowledged this. And we now know that going forward, Inland Revenue will not be making auto calculations for any taxpayer who is linked to a tax agent, and is overhauling its procedures around contacting clients of tax agents directly.

This is very much a sore point. 72% of tax agents had clients approached directly by Inland Revenue. And one of the interesting points about that was a significant proportion of them were approached by Inland Revenue in relation to the Accounting Income Method AIM, which Inland Revenue has been promoting as a simpler means of paying provisional tax.

At present only two thousand or so people have taken up AIM. And the reason is they’ve done that – despite Inland Revenue’s huge push – is that we as tax agents feel that it isn’t right for many of our smaller clients’ businesses – that it requires too much information and is rather inflexible in its approach. So that’s something which is probably going to change. I know Inland Revenue is working on that.

Overall, I think this huge transformation can be regarded as a qualified success. There are issues, as I’ve just said, around how Inland Revenue’s relationship with tax agents deteriorated. At the same time this is a reflection of how open our tax policy process is. We were able to get to Inland Revenue and say, “Hey, this is not working, and you need to do something about it”. And through various sources – including also the Revenue Minister, Stuart Nash, getting his ears bent by many tax agents and accounting bodies – change is happening. And that’s actually how the system should operate. So that’s a sort of reflection of the good and the bad of how our tax system works.

Meanwhile over at the OECD…

The third story, and again, this is another one that’s been running for quite some time with huge implications, are the ongoing international developments that we’re seeing in tax now. There are two parts to this. The first is what we’re seeing right now, the impact of the Automatic Exchange of Information under The Common Reporting Standard. This is where the tax authorities around the world swap information about taxpayers’ offshore financial holdings. There’s a colossal amount of data being swapped, and it really is surprising how unaware people are about just how much data is being swapped by tax agencies. Inland Revenue has now received over the two releases made to date under CRS, one point five million account records of New Zealanders who have overseas financial accounts. It’s presently working its way through that data and starting to ask questions.

Separate from that are the developments by the OECD in international tax and how we actually calculate a multinational’s income and allocate it to various jurisdictions. The previous permanent establishment regime built around a bricks and mortar approach no longer operates in the digital economy and through initiatives such as BEPS – Base Erosion and Profit Shifting -the OECD has been working on a replacement.

And this latest development is called the Global Anti-Base Erosion Proposal or “GloBE”. And this is proposing nothing less than a minimum tax rate for multinationals. This is a huge initiative and the OECD is hoping agreement can be reached among the 135 jurisdictions involved by the end of 2020.

How the GFC changed international tax

And that leads on to what has been happening over the past decade. Back in 2010, the OECD was starting to look at the implications for tax jurisdictions of international tax planning in the wake of the global financial crisis, which in 2008 had pretty much smashed to bits the budget balances of most jurisdictions around the world.

All around the world, countries tax take took a huge hit in the wake of the GFC. And countries then started looking very closely at where all the money was going and the scale of tax avoidance, and in some cases outright tax evasion, became ever more apparent. And so, this is the most important tax story over the past decade because it is transforming the way international tax operates.

You can run but you can’t hide…

And the implications for our tax base have been twofold. One, as a result of the global financial crisis and the initiatives that the OECD started, we now have Automatic Exchange of Information and the Common Reporting Standard and as I mentioned a minute ago, vast amounts of information sharing. We are also seeing moves to determine how multinationals will be taxed and that will not only affect how we tax multinationals, but also how our multinationals are taxed. Fonterra is the one that’s most often mentioned in this regard.

But it was the Americans that kicked this all off in 2010 with the Foreign Account Tax Compliance Act. What FATCA did was it required other jurisdictions to report to the US Internal Revenue Service – the IRS – details of American citizens who held bank accounts in their jurisdictions.

FATCA was the blueprint for what we have now CRS and Automatic Exchange of Information.

American exceptionalism

But there was one other thing that the Americans also did which is still playing out. The Americans are not part of the CRS initiative. In effect they said, “Well, we’ve got FATCA. we don’t need to be part of this.”

And American unilateralism is a continuing issue for the global tax base, because in the wake of the OECD proposal for the Global Anti-Base Erosion Proposal, the American Treasury Secretary just last week said, “Well, actually, we might not join that. Instead, we’ll just rather keep going with our old international tax rules”. The suspicion is that’s because the digital giants are putting pressure on the Treasury Secretary and the American government. So, a decade ago, America took unilateral action to introduce FATCA, which then led to the CRS. And now a decade on, it is throwing a large amount of grit into attempts to reform the taxation of multinationals.

A tax groundhog day

Here in New Zealand, back in 2010, Peter Dunne was the Revenue Minister, the Canadian Robert Russell was Commissioner Inland Revenue. The top income tax rate was 38% and the threshold at which it kicked in had just been increased to $70,000. GST was then 12.5% and the registration threshold had also just recently increased to $60,000.

Now those thresholds haven’t been increased since then. I think one of our faults in our system is we do not review the tax thresholds regularly enough and it causes distortions. And then suddenly politicians are making grandiose claims about massive tax cuts, which are nothing more than inflation led adjustments.

But in a real case of Groundhog Day, back in January 2010, the Victoria University of Wellington Tax Working Group, issued its report. The group (which included recent podcast guest and member of the latest Tax Working Group Geof Nightingale) shied away from recommending a capital gains tax. But it was in favour of increasing the amount of taxation from property, particularly in the form of a low rate land tax. And it also wanted to see more taxation of residential rental properties, suggesting they could be taxed in a similar manner to the fair dividend rate and foreign investment fund regime. So, there you have it, ten years ago, we were also talking about capital gains and the taxation of investment property.

The other thing that was raised by the Bob Buckle led group in 2010 was a recommendation for “a comprehensive review of welfare policy and how it interacts with the tax system with an objective being to reduce high effective marginal tax rates”. Both the Welfare Expert Advisory Group, which reported earlier this year, and the TWG commented on this situation. And I suspect that in another 10 years we will still be talking about this issue. It doesn’t go away, even if governments are unwilling to deal with some of the political consequences of action.

Well, that’s it for the Week in Tax for this year. I’d like to thank all our listeners and my guests throughout the year. I’d also like to thank David Chaston and Gareth Vaughan at www.interest.co.nz for publishing these transcripts.

We’ll be back next decade on Friday, the 17th of January. Until next time. Meri Kirihimete me te Hape Nū Ia. Merry Christmas and a Happy New Year. Thank you.