As is well known, income tax thresholds have not been increased since October 2010. What also gets overlooked is that the GST threshold of $60,000 was last adjusted in April 2009. And this week, Stuff ran a story about Kristen Murray, who has petitioned Parliament to have the GST threshold increased to $75,000.

She argued in her petition that the lower threshold is crippling small businesses. Inland Revenue disagrees but Kristen has gained the support of BusinessNZ, who supports regular indexation of tax thresholds.

A BusinessNZ economist noted that the effect of inflation means that the $60,000 threshold set back in 1 April 2009 should now be roughly about $82,000. Now the driving principle of the GST system is a broad based, low-rate principal approach and a reasonably low threshold is consistent with that approach.

GST came into effect on the 1st of October 1986 and the threshold set then was $24,000.

Looking at the table above it has actually more or less kept pace with inflation based on where it started – until now.

Notwithstanding that, given that it’s now 14 years since it was last adjusted, some form of increase to the threshold is not unreasonable. And the number of businesses a threshold change could affect is quite significant.

According to Inland Revenue data supplied to Parliament’s Finance and Expenditure Committee in 2022 there were 264,457 taxpayers who are GST registered, but with turnover of $60,000 or less. There’s another 27,000 or so with turnover between $60 and $75,000. So, as we said, increasing the GST threshold could take a large number of taxpayers theoretically out of the GST net.

But GST has an interesting effect and it’s also seen officially as a main pillar against tax evasion because of its comprehensive nature. Pretty much everyone finishes up paying GST somewhere along the line, even those within the cash economy. They still finish up paying GST when they’re purchasing supplies, food, petrol and the like. So, there would be a natural reluctance on the part of Inland Revenue to increase that threshold substantially. But to repeat an earlier point after 14 years, it’s not unreasonable.

By the way, Kristen’s suggested $75,000 threshold would actually bring it in line to the Australian threshold, which is A$75,000. I think one of the things they could also borrow from Australia is perhaps allow for quarterly GST returns.

There are therefore risks about the GST threshold being too high and the base being narrowed, but if they kept it too low then businesses may deliberately hold back from growing and crossing the GST registration threshold.

Over in the UK, where the equivalent of GST, value added tax or VAT, registration threshold is £85,000, there is in fact a very noticeable drop-off effect around that threshold.

The reason possibly might be because once you are VAT registered, you’re charging VAT at 20%, so businesses that can’t see themselves growing substantially quickly pass that threshold may be quite reluctant to effectively increase prices by 20%.

Now, I’m not aware of any such evidence here in New Zealand. And I think the issue, which Kristen pointed out, compliance is a bigger issue for micro-businesses. With compliance there comes a point where there is an irreducible minimum. Whether we’re at that point there know I don’t know. As I mentioned earlier, offering opportunities around quarterly reporting would perhaps help. And these days, the advent of software programs such as Xero, MYOB, and Hnry do help micro-businesses manage their tax much more effectively.

But in terms of GST and tax administration, I think the next big step would be to zero rate all supplies between GST registered businesses. That would help put an end to the merry go round which goes on right now where a GST registered business charges another GST registered business GST, collects and pays that GST to Inland Revenue, while the GST registered business, which has just paid GST, then claims it back from Inland Revenue. Overall, there’s no net GST effect. I therefore think moving to zero rate such B2B transactions is a logical step. How far away that is, I don’t know. It doesn’t appear to be on Inland Revenue’s work programme at this point.

At the moment, we’re left with the only other adjustment that might help microbusinesses would be to increase the GST threshold. As I said, my view is something like that should happen soon, but we’ll have to just wait and see.

Airbnb, GST and unintended consequences

Moving on, and still on GST, I came across a case this week where a residential property owner couldn’t let the property so decided to change his approach and started letting it out as an Airbnb. Airbnb letting represents taxable supplies for GST purposes. He was GST registered for another activity and he did include the Airbnb income in his GST returns.

The issue has now popped up that he wants to sell the property. And it looks like unless he is selling to a GST registered person when compulsory zero rating will apply, then he has inadvertently given himself a GST problem. If he sells the property, which remember was originally a residential property to a non-GST registered purchaser, the sale price the price will become GST inclusive, which basically will bite into his margin.

This is a good example of paying attention to what’s going on around your activities and that you should always seek advice when you propose to do something that may have GST implications. Tax is full of unintended consequences and for this particular taxpayer, I’m afraid there probably is a huge unintended consequence of basically surrendering the equivalent of 13% (the GST inclusive portion of the sale price) on a residential property sale. He was already carrying on a GST activity already and Airbnb just represented additional taxable supplies. So, for anyone thinking of switching from residential property letting to Airbnb that’s a trap to watch out for.

The Great Tax Debate – “Think of the consulting fees!”

And finally, on Friday night I was part of the Great Tax Debate organised by the Tax Policy Charitable Trust, where I and several other tax practitioners debated the proposition: A wealth tax is the best solution to wealth inequality.

I was the leader of the affirmative team, and I was ably assisted by Mat McKay of Bell Gully and Sladjana Freakley of EY. Opposing us were Robyn Walker of Deloitte, Simon Coosa of Minter Ellison, Rudd Watts and Jeremy Beckham of KPMG. Professor John Prebble, one of THE gurus of New Zealand tax, chaired the debate. We had a lot of fun on the topic including an interesting Q&A session where someone asked, “Has EY gone woke?” The answer, of course, is no.

In the end thanks mainly to some pretty shameless populism including an appeal to the base instinct of the tax consultants in the audience, “Think of the consulting fees!”, we in the affirmative team sneaked home. Before the debate started everyone was asked to register their position as a yay or nay. And then the net movement from that would determine the winner. And we managed to move the dial several points in our favour. But before the Green Party start jumping up and down celebrating “We told you people wanted a wealth tax”, over 60% were still against a wealth tax.

As I said, it was a lot of fun with plenty of laughs all around. The question about whether EY has gone woke raising one of the bigger laughs. I’d like to thank the organisers, the Tax Policy Charitable Trust, hosts Bell Gully, Professor Prebble, my team-mates, Mat and Sladjana and our opponents, Robyn, Simon and Jeremy together with the 80 plus attendees in the audience for a fun night. We hope to see more of these debates in the future.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Plus big changes to the retirement landscape she helped initiate.

She also explains why she was one of the first of the 97 signatories on the Open Letter on Tax.

During her time as Retirement Commissioner, she also helped develop a national strategy for financial literacy that incorporated practical strategies such as the excellent sorted.org website, multimedia campaigns and education in schools.

More recently, Diana was the chief executive of the Wellington Free Ambulance and is presently chair of the Lifetime Retirement Income and several charities. She is also one of the initial 97 signatories of last month’s Open Letter on Tax.

Ki Ora Diana, welcome to the podcast. Thank you for joining us.

Diana Crossan Ki Ora Terry, thank you for having me.

TB Oh, not at all. Enormous privilege and thank you. I’m really fascinated. You’ve got an incredibly distinguished career there. But I’m most fascinated by your time as Retirement Commissioner. Because when I was researching/writing Tax and Fairness and looking at the superannuation savings regime, as it was in 2002, prior to when you took over, it was pretty much ground zero. There was practically little or no incentives to save.

And we know that the numbers of superannuation schemes had basically collapsed from where the numbers that prior to the removal of insane tax incentives in 1988, they had fallen quite dramatically, to I think barely 13% of the workforce was covered about 2002.

So, you come onto the scene, you’re appointed Retirement Commissioner. It must have been quite daunting. What were your thoughts when you volunteered for that?

Diana Crossan You’re right, it was a bit overwhelming initially. And I was the second Retirement Commissioner, the first one was Colin Blair, who was a tax specialist. So, when the government set up the retirement commission, they thought that they were helping the nation. Hopefully they were because we had a superannuation, or a retirement savings system that was very different from the rest of the world, or the OECD world really.

We had New Zealand super, which is of course brilliant, and should be protected and we had private saving. The Retirement Commissioner was supposed to be there to help people understand that they needed to save for their own retirement. That was why it was set up.

And what we discovered – the Retirement Commission was just on to this when I arrived – was that the advertisements and the encouragement and all of the messages they were sending out to people were getting to people who were already looking for it. It was preaching to the converted, really.

And the average age of people they were talking to at that point was about 45 to 50, and the Retirement Commission recognised that that wasn’t going to work. That starting to save at that late stage in your career didn’t work. So that’s how it came about. The recognition that maybe in the 2000s at the beginning of this century, we had to do something very different.

So, they stopped all paper brochures and television interviews and things that focussed on brochures. And the team introduced Sorted https://sorted.org.nz/ and I came in just at that time. And so the focus on financial literacy and on getting to people earlier was the most important thing I picked up when I first arrived.

TB And that’s been a huge transformation there, I take.

Diana Crossan Yes, absolutely. We started off by thinking, how do we do this? You know, this is new. I thought it was very brave of the group just before I arrived. You talked about the national strategy for Financial Literacy.

We were one of the first countries to do that because we recognised that if the government was (and we kept talking to government about other things as well) going to stick with this policy of having a New Zealand super, which was very basic as we know, somewhere between 30 and 40% of New Zealand population live on New Zealand super alone. So first of all, it was that and then it was up to you to say we needed to find ways of talking to people about what to save, how to save, how safe is it. All of the issues in our trustworthy financial services sector, we needed to talk about that. We need to talk about government policy that didn’t get in the way.

So until KiwiSaver came along, we were different from the rest of the world. The countries that we tend to look up to like Australia, Canada, US – well, the US is unusual – the UK and parts of Europe because we didn’t have the middle pillar which is about supported saving by government.

TB Yes, some countries do that by means of very generous tax incentives which were abolished under Roger Douglas in late 1988. So, you were closely involved in the development of KiwiSaver?

Diana Crossan Yes, Michael Cullen approached me to join the team. So, it was an interesting group of people from a variety of government organisations and his statement was “We are going to have a savings scheme. I don’t want this group to come back and say it’s not a good idea because we’re going to have it while I’m in government. What I do want you to do is tell me how to develop that.”

And just before I came into the Retirement Commission role, I had been funded by a businessman and business family in Auckland who asked me to look at how we could help New Zealanders go to university and polytechnic, tertiary education. There were high fees and high interest rates for university students at that time.

So, we had done four years of work about a children’s savings scheme. Therefore, when I was asked to join the KiwiSaver group by Michael Cullen, I was able to take all that work to that. So that included the kick start and included thinking about other ways of doing things.

TB Yes, it’s been enormously successful. Even the FMA Financial Market Authority’s June 2022 report now says that we have $90 billion in KiwiSaver as of 30th June 2022 and over 3.17 million members. And that’s not even 20 years. It’s 15 years max. It’s been transformative.

Diana Crossan It is, however, there are issues with that. As you know, there are a lot of people who don’t know where their money goes or know what kind of fund they’re in. And they might be young and in a fund that’s quite conservative and they could do better to be in the balanced or growth funds, and they don’t understand that.

So that’s what the financial literacy was about. Also, many of them have very low savings in KiwiSaver. And while it will be helpful when they get to retirement, we want people to put more in now so that they have a better retirement when they retire.

TB How do we achieve that? The Tax Working Group in 2018 made a number of recommendations around that. It was suggesting that perhaps we should increase for example, a KiwiSaver member on parental leave would receive a maximum member tax credit even if they didn’t make the full $1042 contributions. And we saw something in the last month’s Budget for that alongside that. But that’s not enough, is it really?

Diana Crossan No. And one of the recommendations I would have made, which was too bold, I think, is that if we want women to have children, and I think we do, and if we want women to have equal opportunity through their career and their retirement, that we do, then maybe we should be thinking about how we help women to keep their KiwiSaver going. We do it with ACC. We keep it going at 80%, so what about keeping KiwiSaver going?

You know, there’s lots of ways of thinking about it, but I think we have to be quite bold in that area because not only are women having time out to have children, but they’re also earning less on average. And so we need to find ways to reduce both of those things. And one would be while you’re on parental leave, your KiwiSaver is put in by the government to even things out. And the other one would be let’s keep pushing for equal pay.

TB Absolutely.

Diana Crossan It makes a difference in retirement.

TB Well, yes, because the thing about retirement is a dollar saved 20 years ago is worth exponentially much more than one saved with ten years to go to retirement. It’s that sort of thing. It’s just volume of savings steadily each year, year in, year out.

Diana Crossan So we’re not good at this, though, because we had a government – I think it closed in 1991 I think – a government savings scheme, a superannuation scheme for its staff. And what was interesting was of course women had unequal pay until the 1960s and some of those women who had unequal pay, when equal pay came in, there was no adjustment in the super.

So they lived out their lives on those savings that were made in relation to the pay at the time. And there was an attempt to tell government that this was completely unfair. Other countries, when they made equal pay rules and legislation, changed the super at the same time so that the women who’d retired by that stage got a better income.

TB Yes, that is still a perennial problem, and it shouldn’t be. As you say, equal pay is closing that gap, which is, what, 13% now?

Diana Crossan Yes, about that.

TB Give or take. Still, closing that gap is vitally important. And we all hear plenty of stories about the shortage of workers and experience. So I think, “Well, guys, we need to address those issues and retirement issues.” And looking at the Tax Working Group, what I liked about what it said in relation to proposal tax incentives, was they were focussed on the lower end.

Because to pick up your point earlier on when you became Retirement Commissioner, the people who should be saving knew they should be saving, were saving anyway. It was getting to those people who weren’t as aware as they needed to be about what they could do.

And so helping that group was what I liked about the Tax Working Group’s suggestions. For example, removing the employer superannuation tax charge on employer contributions below the $48,000 threshold at the moment. What do you think about the tax treatment of KiwiSaver and savings?

Diana Crossan I’m not a tax expert as I said earlier I think. It’s not something I have spent a lot of time on. I think my reason for signing up to the letter was much more about getting more tax, rather than tinkering with what we’ve got at the moment.

You might think, paying women when they’re on parental leave is tinkering. But it’s dear to my heart.

TB I don’t think it’s tinkering. I think it’s something we should be doing.

Diana Crossan In terms of why I signed up and why I’m interested in this issue, is I just don’t think we’ve got enough money. And I know it’s as basic as that. We have one of the lowest tax rates, as you know, in the OECD. Why do we do that? Why don’t we tax? We want the same schools, the same health services. We want housing for everybody. We want the same services as they have in France or as they have in Germany or Canada or Australia. But we all pay less tax. That’s just madness to me.

TB As I heard someone put it “We want Scandinavian levels of [‘free’] service, but American levels of tax” and the two are incompatible.

Diana Crossan There is strong evidence that investing in health and education outcomes leads to productivity and economic well-being. There’s strong evidence that if you focus on health and education in a nation that there will be an increase in productivity and an increase in economic well-being. Why don’t we do it?

TB Well, yes, because the way I do see it as an economic issue. Because if we have poor outcomes for lower income groups and Pasifika and Māori etc., that’s an economic anchor on the rest of us. We pay more for our health care.

And I know from my time when I was coaching rugby in South Auckland, players didn’t get the ACC treatment that we wanted them to get to have the injuries looked after because they couldn’t afford the little surcharge. That was only $5/$10. Some people, I think $5/ $10, that’s nothing. When you’re on minimum income, it’s a lot. And so you could see players, you could see from their injuries, that had never been properly treated, that there’s a shortage of funds there. And so longer-term health issues develop from that.

Diana Crossan And you’ll be aware that we’ve had underspend for a long time, so it is catch up time and that’s why I signed this letter. Yes, let’s get out there and say for those who can afford it, and we’re not talking about the stinking rich, we’re talking about people who could pay a little bit more. I mean, if we went to Australia, we’d be paying 45% and we’re paying 39% at the top and mostly 33%.

TB Yes, our tax rates are not high by world standards. To me, the big issue that we have in our tax system when we talk about income tax rates, is that low to middle income earners pay a lot more, the $48,000 threshold which it goes from 17% to 30% has not been lifted since 2010.

And how that’s been allowed to develop – politicians then come along and like snake oil salesman said, ‘Oh, we’re giving you a tax cut’. And I’m thinking, ‘No, you’re just simply restoring a position that shouldn’t have existed in the first place.’

So, there’s enormous pressure there, and then we’re on to the question of wealth. Last week, when I talked about how the Greens tax proposal for a wealth tax caused a lot of conniptions amongst people. So politically I think it’s going to be a hard push. But we have this aversion, it seems, to taxing capital, which I’m not sure where that’s developed. Is that something you’ve seen over time? Has it come up in discussions about broadening the tax base?

Diana Crossan What I’ve seen, Terry, I think there’s two things. One is people get nervous. It’s almost NIMBY, isn’t it? Let’s find a way of doing it in somebody else’s backyard but don’t let me pay more, let others do it somehow.

And I think there’s a lot of ignorance about what capital gains or wealth tax might be and that people are concerned they’re going to pay millions somehow. Yet not paying capital gains seems blatantly unfair. I would say if we could have a poll, I think we’d find more people would be for capital gains tax than those who are against it. And they were hoping that this government, when it had its huge mandate, would have done that. Maybe the ones against it are more vocal. But I think overall the people I meet, the ordinary people, understand that it’s fairer.

TB There’s an awful lot of misinformation that goes on around this now and watching the debate at the time. It was certainly the squeaky wheel squeaking a lot back in 2018/2019, happened to be those that would have been most affected by it.

Naturally someone who sits on substantial unrealised capital gains and property or whatever, of course they’re going to say, ‘Well, this is going to hurt, so I don’t want it’. And I don’t have a problem with people saying that. I know we need to look at the bigger picture.

Diana Crossan If you have enough money to get into the property market and you manage it well, you can make quite a lot of money.

TB On leveraging the gains, when you look at how generous our tax system was until this current Labour government came in, it was extraordinary generous. You could offset your losses against your other income, you’re able to leverage it. And one of the key parts of the return, the capital gain was untaxed, until the changes around Brightline tested all yanked that scenario.

So now we have a de facto capital gains tax applicable to one asset class, a residential property. You know, for me I have great fun explaining to people who want to migrate here from overseas. “Yes, we’ve got about five different tax treatments because we don’t have a general capital gains tax.” Now that keeps me in work, but I can hear the brains whirring away trying to understand the intricacies of the various regimes in place, thinking what is the problem here? Broadening the base means we can lower the tax rates. We may not need a 45% tax rate if we broaden the base.

Diana Crossan I’m not suggesting a 45%. Even if we went to 40%. My understanding is that the tax take brings in $113 billion. And if we had another $20 to 30 billion, we would be able to do the things we need to do in housing and health. And I can also hear people who might be listening saying “We can be more efficient, we waste money”. Well, my understanding is that yes, we can be more efficient, but we can’t make $20 to 30 billion out of efficiencies.

TB Yes, that’s the key issue. What was surprising, the Greens were proposing $10 to $12 billion of tax increase, a 10% tax increase to tackle it. That is a substantial tax increase. But it gives you an idea of the scale of the problem. But no one’s really talking about that. They were focussed on this wealth tax, which was probably the most ambitious part of the proposal and the least likely to actually come into force. Because that would require a lot of political balls to drop in the right place for that to happen.

Diana Crossan I think one of the things about the TOP party and the Green Party is their tax proposals didn’t increase the tax take a lot because they also were dealing with supporting the low income. That was more about making it fairer. I’m all for making it fairer too. But I think, we need more money. I know we need more money.

TB I keep harking on about the climate change costs. 700 properties were rendered unliveable by Cyclone Gabriel. That is probably the thick end of a billion dollars. And that’s just this year. 400 are in Auckland. Another 300 are along the Hastings, Napier, Tairawhiti-Gisborne and Wairoa districts, none of whom by the way have the funds. You can see from their rating base. So, it’s a communal responsibility.

Climate change doesn’t distinguish between postcodes. It’s coming and we’re dealing with it right now. And I think the crunch point will be the insurers. They’re already starting to say, “Well, we’re not going to insure you if you build there. We’re not going to give you that.”

Last week I got a call from someone who was down in Christchurch and they’re still arguing with the insurers over the earthquakes. We don’t want that scenario repeated across the whole of the country in relation to climate change.

Diana Crossan We certainly don’t. And while I’ve focussed on housing, education, child poverty and health – the whole issue of being prepared for what’s coming – we’ve had a taste of it and it’s not going to go away quickly.

We need to work hard for ourselves, but we can’t stop it all, so we’re going to have, I think we all agree, having weather we’ve never had before, and we’re going to have more weather we’ve never had before. And so we need more money. I just keep saying we need more money.

TB And a little a lot goes a long way.

Diana Crossan And people have asked why the signatories of the letter don’t just put their hands in their pockets and pay up and give more to education and health and poverty.

And what I know, of course, is that quite a few people I knew who signed the letter are already doing that. But some of them, of course, rightly said, “I’d be much happier if everybody was doing it and it was fairer across the board so that it wasn’t just philanthropists. We weren’t just relying on charity.”

TB Yes, that was my philosophy as well. And we are actually a generous nation in that. And what’s notable is often it is relatively low-income people are very generous, as a proportion of income given to charities.

Diana Crossan When I was working at Wellington Free Ambulance, it was collecting in the street. It was always very interesting who gave money, and it was people who you would think wouldn’t be able to afford to. But people are generous and that’s good. But I think it’s so much better for housing, health, even ambulance, I believe, should be part of our government funded services. And that’s what we want. And we just need to pay more even if I sound like a broken record, Terry.

TB Well, Dame Diana Crossan, that seems to be a very good place to leave it, broken record or not. I think it’s something we need to be hearing.

Thank you so much for being part of this podcast. It has been fascinating to talk to you and hearing the story of your back involvement with the Retirement Commission and the changing landscape, which has changed considerably for the better. Thanks for your efforts. It’s been a pleasure having you on the podcast. Thank you so much.

Diana Crossan Sure. Thank you for having me.

TB That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

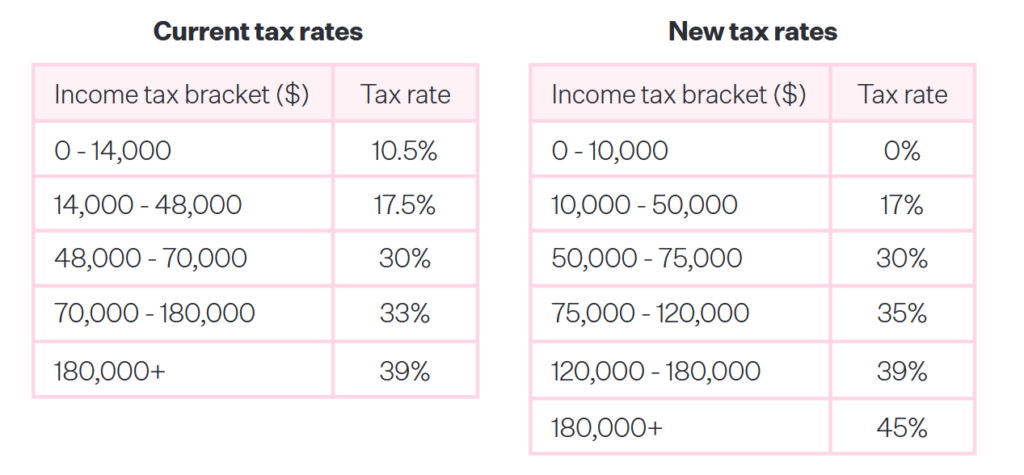

The Greens announced their tax proposals a week ago, last Sunday.

And my reaction was, “These are very bold.” They proposed major tax cuts at the lower end, meaning 95% of taxpayers will be better off under the Greens. Those cuts are paid for by increasing the top tax rate to 45% and increasing the 33% tax rate to 35% as well. These increases are part of the trade-off for the proposed nil rate band of $10,000, which no doubt will be very popular. As is well known, many other jurisdictions have something similar and given the fact that nothing has been done in relation to indexation of thresholds for well-nigh 13years now, it’s unsurprising that the pressure is built up, particularly at the lower end, to change the tax rates.

But most of that got swept away by the Greens controversial wealth tax proposal. In summary, there are two parts to it. Any individual whose net assets, net of mortgages for example, exceed $2 million will be subject to a wealth tax of 2.5% on the excess. For family trusts there is no nil rate band or threshold at all. It’s a flat 1.5% which is a deliberate anti-avoidance mechanism.

Latest Inland Revenue data on trusts

Trusts were used to avoid the impact of estate and gift duties in the past and are used in other jurisdictions to mitigate the impact of wealth and estate duties. So, the Greens have targeted this avoidance. Coincidentally, last Saturday the New Zealand Herald published a piece including details of the trust tax return filings made to Inland Revenue for the year end 31st March 2022 which indicated the value of assets held in trusts. The net assets of the 201,100 trusts which reported, was just over $300 billion. So at 1.5%, theoretically that’s $4.5 billion dollars straight up there.

Incidentally, what that Inland Revenue report doesn’t show is the non-reporting trusts, those are likely to be quite significant. We really don’t know how many trusts there are in New Zealand, the best estimates are somewhere between 500,000 and 600,000. Many of the non-reporting trusts don’t do so because they have no income, but they hold assets such as the family home. So, family homes that have been held in trusts may now be subject to the Greens’ proposal.

Now this kicked off quite a storm, which I watched with a little bemusement because the Greens first of all have to put themselves in a position of such leverage that its coalition partners, almost certainly Labour and Te Pati Māori, agree to the proposal. And then somehow between 14th October, the date of the election, and 1st April next year, the legislation to introduce all of this is drafted and passed through Parliament. So ,it’s a big challenge ahead.

But it caused quite a stir, and I fielded several calls from people concerned about what they saw here, trying to get an understanding about it and my views on it. At our Accountants and Tax Agents Institute New Zealand’s regional meeting on Tuesday we had a very lively debate around the question of this wealth tax. Normally, a lot of the time we’re talking about what’s in the legislation and whether Inland Revenue ever answer their phones again. All this I think shows the impact of the proposals, even though in theory they affect only a small group of people, the top 1%.

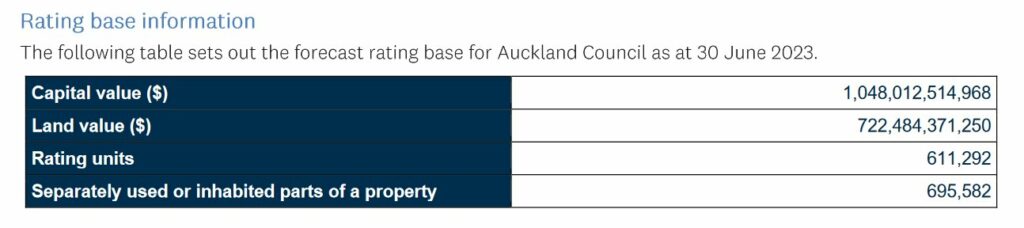

But there is substantial wealth locked up in property. We know that from digging around the official figures. For example, Auckland Council estimates the rateable value for all property within the Auckland Council region will be over one trillion dollars as of 30th June. Obviously, not all of those would be subject to a wealth tax.

What’s being suggested by other parties?

But I thought it was interesting that people are taking the Green’s proposals very seriously. The income tax shift to 45% on income over $180,000 won’t be terribly popular. But at present, the proposals that they’ve put out for the income tax cuts would affect many more people and benefit many more people, all those earning under $125,000, which is something like just over 4 million people. This has a broader impact than either National or Act’s proposals.

It’s quite interesting now as the election comes ever closer, we can start to see the tax policies of the various parties taking shape. The Greens are raising a substantial amount of tax to deal with poverty. Act is proposing tax cuts and it’s taking the ideologically opposite approach of substantial cuts to spending in order to achieve its top rate of 28%.

TOP, The Opportunities Party, are putting out a policy which has a land value tax, and they also propose tax increases at the higher end together a nil rate band and also substantial tax cuts at the lower end.

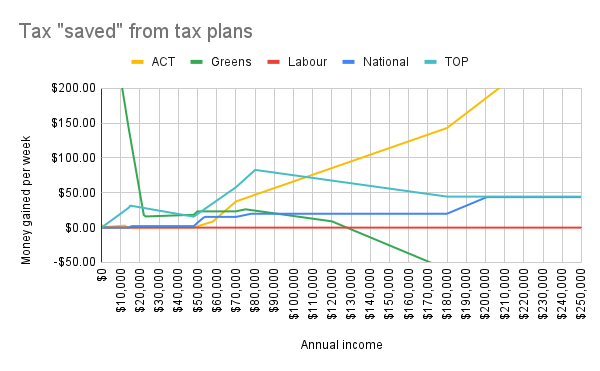

We haven’t yet heard from Labour on what they would do. Over on Twitter @binkenstein put together a graph comparing the various parties’ proposals so far.

So, the debate has ramped up quite a bit. Obviously, the Greens wealth tax is the most controversial part of it, but the other part which really got very little commentary but is equally controversial, was a proposal to raise the income tax rate for companies from 28% to 33%. More than most of the Greens’ proposals, that would probably produce a certain frisson of tension amongst multinationals. They may look and think “Maybe we might not increase our activities in New Zealand” or they may ramp up what they try and do under profit shifting.

Anyway, it all made for a very lively discussion all round. As I told people, wait and see. But it is interesting to see the pressure point for those are likely to be affected around a wealth tax.

What does the IMF think?

With almost impeccable timing, the IMF, the International Monetary Fund, were in town and it suggested that maybe it was time for a capital gains tax.

The Concluding Statement of the 2023 Article IV Mission noted:

Well-designed tax reform could allow for lower corporate and personal income tax rates by broadening the tax base to other more progressive sources, such as comprehensive capital gains and land taxes, while also addressing fiscal drag and improving efficiency.

It’s not the first time the IMF has suggested changing the tax system. They did so in 2021. In fact, there’s a regular pattern of the IMF and/or the OECD coming here looking around saying, “Well, guys, the country is in good shape, generally government policy is pretty sound, but you need to do something about capital gains taxes.” Regardless of whichever party is in power the Government’s reaction is quite funny. They like the bit about everything being under control. But at the mention of capital gains tax, they all throw up their hands in horror. And yet, as we know all around the world, capital gains taxes are a common feature of tax policy.

The Crypto-Asset Reporting Framework, the latest expansion of the Common Reporting Standards

Now, the Greens wealth tax proposal will probably be music to the ears of the French economist Thomas Piketty, who has proposed a global wealth tax, as one of the core points of his monumental work, Capital in the 21st Century. And at the time of publication in 2014, the opportunities for that global wealth tax to ever eventuate were probably just about zero or maybe marginally above zero.

But since then, we’ve had the introduction of the Common Reporting Standards which I think is actually revolutionising the tax world quietly because an enormous amount of information sharing is now happening on. We know from what’s been reported under the Automatic Exchange of Information that there’s something like €11 trillion held in offshore bank accounts. The Americans have got their FATCA, the Foreign Account Tax Compliance Act, and as a result of that, they know that American citizens have got maybe US$4 trillion held offshore.

Now, the latest part of the Common Reporting Standards is extending the framework to crypto-assets and I talked about this last year when the proposals first came out. Those proposals have now been finalised and the Crypto-Asset Reporting Framework is now in place. There have also been some amendments to the Common Reporting Standards. I’m going to cover all these changes in a separate podcast because I think they’re worth looking at in a bit more detail.

The tightening noose of information exchange

But the key trend in international taxation that’s going on, which I think is going to have a long-term impact around the world, and particularly for tax havens, is this growing interconnectedness, the sharing of information that goes on between tax authorities through mechanisms such as the Common Reporting Standards. I asked Inland Revenue about what information they had been supplied under the CRS in relation to the numbers of taxpayers and the amounts held in overseas bank accounts. Inland Revenue turned down my Official Information Act request on the basis that much of this is obviously confidential, but also would be compromising to the principles under which the information is shared.

Now, I’m not entirely sure about that. I think the more openness we have about what is being shared, the better the likelihood of tax enforcement once people cotton on to what’s happening. They will not think “Yeah, well, I’m just going to leave it over in the UK or the US or wherever, and Inland Revenue will never find out.” My view, as I tell my clients, is they always find out and they know much, much more than you can imagine.

And outside of the CRS there appears to be a regular exchange of information about property purchases between the United States Internal Revenue Service and Inland Revenue here. So be advised, the Crypto-Asset Reporting Framework is just the latest in a building block of international information exchange.

The Auckland Budget – what about climate change?

And finally, the Auckland budget got signed off last week. I’ve been in the press disagreeing with the sale of any part of the Auckland airport shares, and I still stand by that. I think it’s a short-term fix for a long-term problem, but that’s now done and we move on.

What I did think was quite surprising as you delve into the budget is some of the numbers that come out. As I mentioned earlier, the rating base for Auckland and according to the Auckland Council’s documents is over $1 trillion.

But the thing that really surprises me, which wasn’t addressed in the budget so we’re going to have to address it next year, is the question of climate change. Towards the end of the process, the Government announced that in the wake of Cyclone Gabrielle 700 homes around the country are too risky to rebuild. The Government and councils will offer a buyout option to those property owners.

400 of those are in the Auckland region and apparently it doesn’t also take into account what is going to have to happen out at Muriwai because of the slips and the dangerous cliffs over there. As Deputy Mayor Desley Simpson pointed out, “If you say it’s 400 [Auckland homes] times $1.2 million, give-or-take just like the average house price, you’re talking half a billion dollars.”

The question arises how is that split between Auckland ratepayers and the rest of the country? Yet there was nothing in the Auckland budget about this, and that’s just this year’s damage. What happens if we get another Cyclone Gabrielle, next year?

We’ve got an interesting scenario developing where we’re talking about reducing emissions and we’ve got a distant horizon 2030 or whatever farmers and other parties want to extend it to. But in the meantime, we are picking up the bill now for increased damage and we don’t seem to be thinking in terms of how does that affect our taxes and rates? And this is going to be an ongoing issue. So, the question of paying for that, whether it’s a wealth tax, capital gains tax, whatever, is going to become ever more present, in my view.

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

A look ahead at the expected big tax themes in the coming year.

The arguments for taxing property, a wealth tax, what might Joe Biden’s presidency mean for international environmental taxation and how will Inland Revenue respond.

Welcome to 2021. So what lies ahead in the tax world this year? Well, firstly, housing will remain an issue and I expect we will see steady calls for radical action on this front, including a demand for a capital gains tax. I actually think it’s gone beyond the point at which a CGT would have an impact.

In terms of tax measures, as I’ve said previously, restricting interest deductions including applying the existing thin capitalisation rules to investment properties might help to even the playing field between investors and first-time buyers, a group to which the Government appears to be paying particular attention.

Susan St. John has called for the Risk-Free Rate of Return (which is similar to the Foreign Investment Fund fair dividend rate rules) to apply to investment property. And her suggestion was recently echoed by Professor Craig Elliffe, who was a member of the Tax Working Group.

The Tax Working Group looked seriously at the question of applying a Risk-Free Rate of Return to investment property. It estimated the revenue from applying a rate of 3.5% would be approximately $1 billion in the first year and was expected to rise to $2 billion per annum within 10 years. The expectation would be that such a move would,

“tax a currently undertaxed asset class more adequately and act as a curb to burgeoning house prices. Westpac economist, Dominick Stephens calculates that a 10 per cent CGT would reduce house prices by nearly 11 per cent. It is unclear what effect the RFRM, but it should stem the increase. But it’s not clear what effect a Risk Free Rate of Return method would have, but it should stem the increase.”

Now, tied to the question of housing is the issue of wealth inequality, and I expect we will continue to see calls for a wealth tax. Over in the UK just before Christmas, their Wealth Tax Commission released a report recommending a one off wealth tax for the UK, which it estimated could raise about £260 billion over five years. What was particularly interesting about this commission is the depth of the research into the topic.

Quite apart from the final report, the Commission produced a series of other working papers on the design and operation of wealth taxes around the world. And these, in the commission’s own words,

“represents the largest repository of evidence on wealth taxes globally. To date, it comprises half a million words across more than 30 papers covering all aspects of wealth, tax design and both in principle and practice.”

Just to put that in context, I estimate the Tax Working Group’s consideration of wealth taxes amounted to perhaps 10,000 words in total. So we are looking at a very significant amount of research.

Now, one other thing to keep in mind about the British Wealth Tax Commission was that it called for a wealth tax, even though the United Kingdom has a capital gains tax and an inheritance tax. Instead, it recommended a thorough review of those existing taxes. The Commission also went for a one-off tax rather than an annual wealth tax, which is the common type of wealth tax currently and what the Greens propose. The Commission saw that there were quite a few practical issues around the operation and an ongoing wealth tax. These issues together with political pressure, has meant that the use of wealth taxes has declined throughout the OECD.

The Tax Working Group also concluded that an annual wealth tax would have enormous practical issues in implementation, which is why it did not recommend it.

But what the Wealth Tax Commission’s research makes clear is just how unique New Zealand’s approach to the taxation of capital is. It’s well known that New Zealand does not have a comprehensive capital gains tax, but that’s not entirely unique within the OECD. Switzerland, for one, does not have a capital gains tax.

Where New Zealand is unique, is that it does not have comprehensive taxation of capital in any form. Switzerland has a comprehensive wealth tax. In fact, the tax it raises from wealth taxes represents one per cent of GDP, which is the highest of any country with a wealth tax. Wealth tax revenue amounts to 4% of the Swiss tax take so it’s an important part of the Swiss tax system,

Wealth taxes in the OECD do not raise significant amounts of revenue and that’s one of the reasons they’ve been declining in use. The Wealth Tax Commission’s papers are well worth reading. A particularly interesting one is about the political economy of the abolition of wealth taxes in the OECD, which those who want to promote taxation changes would do well to read closely.

I think pressure will continue to mount on the Government on the taxation of wealth because of this ongoing anomalous position where we don’t tax capital on transfers by way of an inheritance tax or even a stamp duty, and not tax increases in value generally will feed into the debate around inequality.

And there’s an interesting point a client made to me on this topic. It’s been a long-standing New Zealand policy to attract high net worth individuals to come to New Zealand. Such immigrants may well qualify for a four-year tax holiday on their non-New Zealand investment income. These people being wealthier tend to have very diverse investment portfolios.

But as the client pointed out to me, it seems wrong that their investments would be taxed on their capital growth under the Foreign Investment Fund regime whereas property investors are not taxed on that growth at all. My client thought that was an anomaly that sooner or later would start to act as a disincentive for high-net-worth migrants to New Zealand. This may lead to growing political pressure to level the playing field, so to speak.

So anyway, the taxation of wealth, whether through a capital gains tax and/or a wealth tax or some other mechanism, is going to remain on the agenda.

A week before the British Wealth Tax Commission issued its report, our Government declared a climate change emergency, joining 32 other nations who have made such a declaration.

Now in my first podcast of last year, I said that the role of environmental taxes as one of the tools in the meeting our emissions targets will become ever more important. And that remains the case.

But we now have a new American president, and one of the first actions of President Biden after his inauguration was an executive order confirming the United States would re-join the 2015 Paris agreement. Now, several people have pointed out this may well act as an indirect trigger for the government to take further action on reducing emissions.

More than a few columns have pointed out that there is a discrepancy between the government’s declared intentions and the actual steps being taken to reduce emissions and meet our commitments under the Paris agreement. One estimate is that New Zealand exceeded its national share of consumption-based emissions by more than a factor of 6.5.

So this year I expect we should start to see some movement on taxing emissions more thoroughly and a place they might well start because the transport sector is the biggest source of emissions is to change the taxation of motor vehicles, maybe by following the UK’s example of applying FBT on the basis of emissions.

The government should also look at eliminating anomalies in the tax system, which effectively penalise low carbon activities such as employers paying FBT on providing free public transport. Another would be as a paper prepared for the NZTA suggested was maybe applying FBT to employer provided parking.

Biden’s inauguration could mean swifter resolution to the issue of international taxation. I think this is one where we will have to wait and see because there will be fierce lobbying in the US by the so-called GAFA – Google, Apple, Facebook and Amazon. I think progress will be made, but it will be slower than people expected.

And finally, the third trend I think we’ll see this year is Inland Revenue coming out from its rather inward-looking attitude in recent years as it completes the final stage of its controversial Business Transformation programme. With the immediate requirement to respond to the COVID pandemic now over, (please people remember to scan) Inland Revenue can get back to its more regular work.

Already before Christmas we started to see a number of new initiatives including one in relation to following up on the information Inland Revenue received under the Common Reporting Standards on the Automatic Exchange of Information.

Another is reviewing all transactions potentially within the bright-line test. You may recall that Inland Revenue fired out emails to tax agents advising “These clients appear to have made transactions within the bright-line test” which caused quite a stir. I expect we’ll see more work going into that space, which coming back to the start of the podcast ties into the taxation of property.

And finally, I think we’ll also see more activity going after the so-called cash economy. I think we’ll see Inland Revenue start following up on cash transactions, such as tradies offering a discount for cash.

So we’re going to have a busy year ahead, as always, and I will bring you the news as it develops. Next week, I’ll take a closer look at Inland Revenue, and its annual report which was released just before Christmas.

In the meantime, that’s it for today. I’m Terry Baucher and you can find my podcast on website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients until next week, Ka kite āno.

About 11 o’clock on Tuesday morning, myself and what appears to be just about every other tax agent in the country received an email from Inland Revenue with the subject line “Clients meeting the bright-line test”.

The email began: “Our records show the following clients have sold or transferred residential properties that meet the bright-line rule. This means these clients will be required to pay income tax on any profit they have made on the sale of the property.”

The email then set out the clients it believed were caught by the bright-line test rules. That is, they either sold property within two years of it being bought between 1st October 2015, and 28th March 2018 inclusive or within five years of it being bought on or after 29th March 2018.

Now readers and listeners will know that I have previously stated that we are aware that Inland Revenue has been gathering data in relation to the bright-line test. But this is the first time it’s really flexed its muscles and its capability to show exactly what it knows about what’s going on. And an insight into why Inland Revenue did that came the following Wednesday morning, when Stuff published a story under the banner headline “One in four property speculators dodging housing tax”.

Based on Inland Revenue data the story outlined that of 1701 property sales subject to bright-line test in the 2019 income year, 1285 have paid up and complied, but Inland Revenue is looking at the other 416 taxpayers who appear not to have complied with the law. It’s also looking at a further 3,758 sales for that year, where the bright-line test might apply.

This email initiative, as you might imagine, caused quite a bit of a stir amongst the tax agent community, and we know that all accountants from small companies like ourselves to major Big Four firms received these letters for their clients. Although the emails set out the client Inland Revenue believed was caught by the rules, they weren’t any more specific than that.

This upset a few accountants because it means digging around to find out what’s going on here. It also transpires that Inland Revenue may have been a little premature in its information release. Apparently, there is a follow up email coming next week, which will actually set out the address of the property in question so that we can then more accurately work out what’s going on.

But there was a fairly lively debate about the matter on the Facebook page of the Accountants and Tax Agents Institute of New Zealand of which I’m a member. And quite a few interesting snippets emerged about who had received emails and why.

Inland Revenue’s systems appear to have picked up any change in the registration of title. So that would include obviously sales where the title to the property passed to a new owner. But it also appears to have included changes in trustees because contrary to what a common misconception, trusts don’t actually exist in law although they have a separate existence for tax purposes. But in law, the property is held by the trustees. So if you have individual trustees holding property and one retires, there has to be a change of registration on the title. And Inland Revenue systems have picked up a few of these and issued a “Please explain.” Overall, though, the majority of tax agents were reasonably happy that this was the sort of initiative that Inland Revenue should be doing.

I’ve said before that Inland Revenue has access to a lot of data but doesn’t really make people aware of just what it knows. And these bright-line test emails are an example of it using the information it holds and making people aware of their obligations. One or two accountants noted it was interesting to see a sale by that client because they never mentioned it to us. There was one particular case, I recall, where the client went ahead and did something which they thought would be outside of the bright-line test, but in fact the transaction was caught. He was most crestfallen when he eventually spoke to me about the matter and I explained how the rules operated.

So this email initiative is the sort of thing that we can expect to see Inland Revenue doing more of and we can expect it to be fine tuning how it does these information releases. Yes, in some cases, such as those where there’s just merely been a change of trustee, Inland Revenue has jumped the gun. Perhaps a little bit more thought around whether that particular transaction was caught would have saved some headaches and frantic calls between clients and accountants on the matter.

But when you consider the heat in the housing market and concerns everywhere amongst those locked out of the housing market and the desire for the government to raise revenue to fill the hole blown in its balance sheet by the Covid-19, it’s not surprising Inland Revenue will be taking this initiative. It reminds people, “Hey, these are the rules. We think you’re caught. If not, please explain”. So, in summary, I think we’ll see more of these initiatives further down the track

By the way, as a PR exercise, it does no harm. Firstly, it tells the new minister that it’s on top of things and secondly, reminds those who think that Inland Revenue is big and dumb, that in fact, it has got access to a lot of information. And to borrow a line from Liam Neeson, it will find you and will, if not kill you, certainly tax you.

Well, on Tuesday, Sharon Thompson, Deputy Commissioner for Community Compliance Services, published a piece responding to our podcast.

And in particular, she addressed our suggestion the transformation hasn’t been successful because cost savings haven’t been reinvested into audit and investigation work. This was, “a narrow view of how Inland Revenue ensures tax revenue in New Zealand is as close as possible to what is required under our laws”. And our view that Inland Revenue’s current approach was incorrect is not supported by international research.

I think the phrase is “Shots fired!”, but it’s certainly intriguing to hear the Deputy Commissioner’s response. One of the points she made in responding to the specific questions we raised about the level of spending on investigations and debt management, was “Our new system has dramatically increased and improved the data we have access to. And we can watch, often in real time, as taxpayers file returns. So, if they’re getting it wrong, accidentally or deliberately, we can see and intervene, reducing the need for post-return audit and investigation.”

That is something I’ve heard from other Inland Revenue staff. If you file a tax return through the Inland Revenue portal, the system tracks the keystrokes. And in one example given to me last year by an Inland Revenue officer, if there is a suspiciously large number of adjustments being made to get the just right amount, they will look into it.

Sharon goes on to comment that every return that can generate a refund is checked automatically and amended returns are checked and screened. For example, between 1st July 2019 and 30th June 2020, Inland Revenue identified approximately 23,000 returns across all tax types which had errors or it believed were fraudulent with a value of just under $200 million. Now, that’s a good initiative and Andrea and I would not dispute that was a good result and also a good use of Inland Revenue resources.

However, Sharon’s article did not address the concerns that I’ve expressed previously and alluded to in the podcast with Andrea about Inland Revenue’s relationship with tax agents. Tax agents are vital to the operation of the tax system. But many other tax agents and I have reservations about how the new Business Transformation programme has integrated tax agents into its system.

The initiative I talked about a few minutes ago is something we would welcome, and we should expect to see that. Tax agents are actually Inland Revenue eyes and ears and so we do a lot of the pre-screening that Inland Revenue would otherwise have to do without us.

But we don’t always get access to Inland Revenue as easily as we should. The phone line for tax agents was abruptly turned off and then reinstated, but with limited hours, for example. So although Inland Revenue may feel that Andrea and I were unfair in some of our criticism, but equally, some of the criticism we raised still needs to be addressed.

The role of tax agents is one where tax agents have a great deal of concerns about what Inland Revenue expects and whether, in fact, it wants to work with tax agents going forward. My belief is Inland Revenue does, but it’s not communicating that very clearly to us at the moment.

I still feel that the dramatic fall in investigation hours of almost two thirds over the last five years is a matter for concern. But we will be able to see how Inland Revenue has worked through the Business Transformation process and see more of the numbers when its annual report is published shortly. It’s been delayed, apparently in part down to the Covid-19 outbreak.

Tax on wealth vs tax on work

And finally, the debate around taxation and housing and wealth taxes continues to rage all week. On Tuesday, Westpac published its Economic Overview for November, in which it made the point that future governments will be forced to either reduce spending or increase taxes because of the fiscal pressures that are starting to build over superannuation and health care.

“The required adjustments to our fiscal position can’t be delayed forever. Sooner or later, some form of consolidation will be necessary, though the precise form this takes will depend on which party is leading the government at the time. Our pick is that a future government will introduce some form of tax on assets such as a land tax, capital gains tax or a wealth tax. Societal concern about increasing wealth and inequality is only going to intensify, eventually creating a large constituency for such a tax. And tax experts agree that broadening the tax base would enhance economic efficiency.”

Later that afternoon, I spoke to Wallace Chapman on Radio New Zealand’s The Panel about this report and the ins and outs of a wealth tax. And in addressing the housing crisis, I made the suggestion that maybe a 10% stamp duty might be imposed on all investors or some measure like that.

Now, last week, I mentioned a Deutsche Bank report which suggested a working from home tax which unsurprisingly got pooh poohed. But the full report is actually quite interesting and actually has one of the more dramatic report openings to any bank report I’ve seen in a long time:

“To save capitalism, we must help the young. Democratic capitalism is under threat as increasing numbers of young people view the system as rigged against them. The pandemic has only exacerbated their economic disadvantage.”

Now, that’s quite an opening for any report, let alone something from a bank, but the report goes on to talk further about some tax changes and these proposals mirror what was suggested by Westpac. Deutsche Bank suggests that, for example, there is a need to have a tax on a primary residence, which if you think about the hoo-ha we had with the idea of a proposed capital gains tax taxing everything except the primary residence last year, you can imagine just how big a fight would happen if we said actually, “We’re taxing the main home as well.”

The Report also suggested that there may need to be additional taxes on financial assets such as stocks, bonds, due to their gains from loose monetary policy. As maybe people are well aware, stock markets have actually boomed quite substantially this year. New Zealand’s stock market has been hitting record highs recently. The Deutsche Bank report, notes that in the 30 years to 2019, the S&P 500, that’s the main index in the United States, gained over 800%, two thirds more than the return seen in three decades previously. The report suggests taxing such income on a basis similar to our foreign investment fund regime, and or remove exemptions and discounts and capital gains. Picking up my Stamp Duty proposal, the report suggests such duties are paid by the vendor and not, as is common, the purchaser.

Now, the point that the Report makes is the reason why it wants to increase the tax on capital is so as to avoid much higher income taxes, which are often cited as an argument against hard work. This is one of the criticisms of Labour’s proposed tax rate increase to 39%. It is very narrow and hits income earners, whereas there’s a growing consensus that it’s the taxation of capital which needs to be broadened.

So this debate is going on all around the world. When banks like Westpac here and Deutsche Bank in Germany are making comments about broadening the scope of capital taxation you know a fundamental shift is happening in taxation thinking. How that will play out, we’ll have to wait and see, and I’ll bring you developments as we go.

Well, that’s it for this week. Thank you for listening. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your regular podcasts. Please continue to send me your feedback and tell your friends and clients. Until next week, ka kite āno.