Last week I discussed the Green Party’s wealth tax proposals, and commented about how what makes New Zealand an outlier in world tax terms is not so much that we don’t have a capital gains tax, but we also don’t have an estate tax, gift tax, land taxes (other than rates), stamp duties and taxes on wealth or wealth transfers, which exist in many other jurisdictions.

This prompted reader kiwikidsnz to respond as follows

It’s a really interesting comment and thank you for that, because it gets to the heart of the issue around tax and how it changes people’s behaviour. Tax is regarded in economic literature as a deadweight cost. Any tax is therefore distortionary, but we have taxes because they pay for things that people like, such as roads, schools, hospitals, infrastructure and pensions, and a whole heap of other services. Accordingly, a key purpose of taxation is to raise the maximum amount of revenue without producing too many distortions and disincentives.

International Monetary Fund on productivity “a significant challenge”

kiwikidsnz’s comments coincided with a report issued by the International Monetary Fund (the IMF) on New Zealand’s productivity challenge. This paper was prepared following the IMF’s visit here in late February and early March as part of their annual review of the New Zealand economy and it does not make for good reading.

As the paper’s opening paragraph notes:

“Weak productivity growth poses a significant challenge for New Zealand’s long-term prospects. Low productivity growth partly reflects structural factors, including New Zealand’s remote geography and small markets, as well as the relatively large role of the tourism and agricultural sectors. However, it also reflects costs and incentives for investment and innovation, which are in turn shaped by features of the business environment and limited financing options.”

Tax is a part of the business environment and as mentioned above the question arises about the distortionary effect of tax. Now the report, and I recommend reading it, is relatively short, but it’s very thorough. But as I said, it’s pretty grim reading because

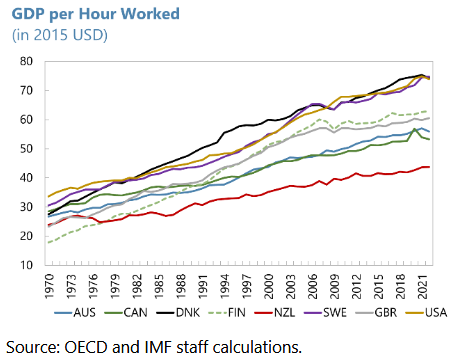

“Over the past five decades, labor productivity growth in New Zealand has lagged that in peer advanced economies, resulting in a widening gap between New Zealand’s GDP per hour worked and that in peers. As a result, by 2022, GDP per hour worked was well below levels in comparable economies.”

A productivity growth challenge across the economy

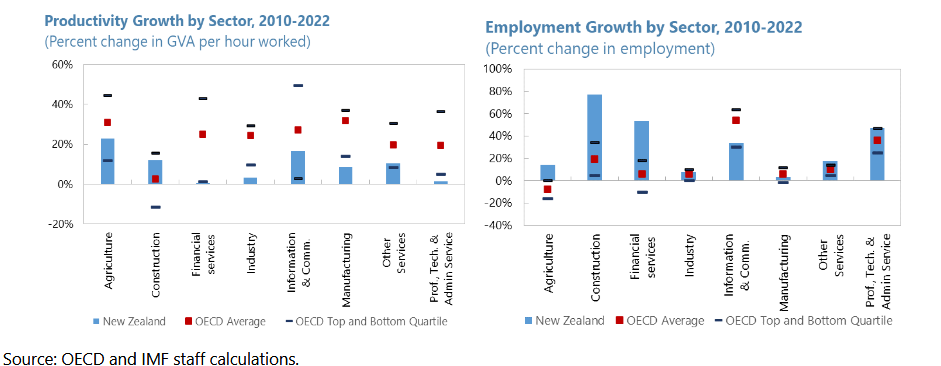

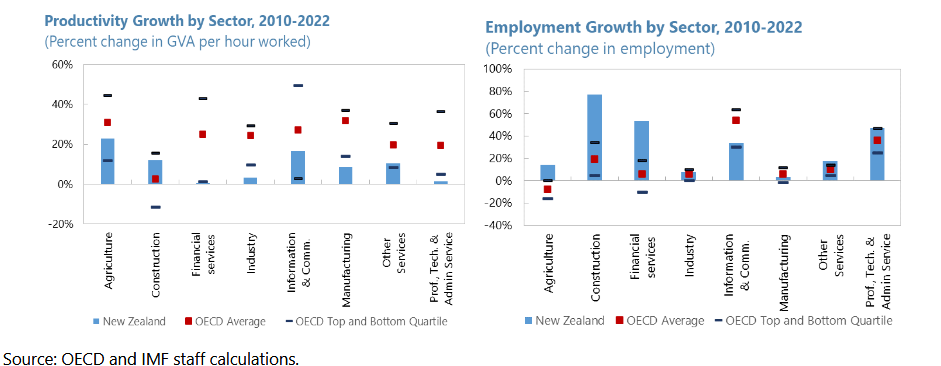

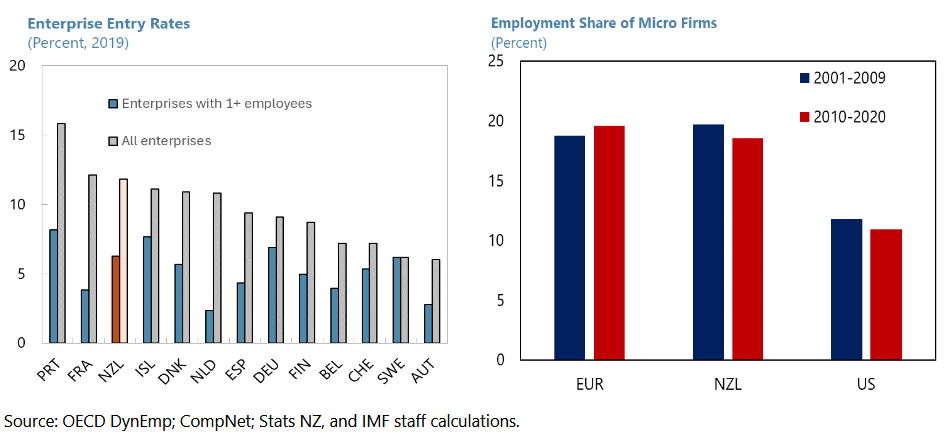

The paper examines this why this has happened and it’s not good reading. A part of the paper that really jumped out at me was paragraph 8 Productivity at the Sector Level. According to the paper labour productivity growth from 2010 to 2022 was below the OECD peer average in agriculture, information and communication (ICT) and some service sectors. In fact

“Productivity growth in New Zealand was in the bottom quartile among OECD peers for financial services, industry, manufacturing and professional and technical service sectors over the same period. The only sector where productivity growth in New Zealand was above the OECD average over this period was the construction sector. New Zealand’s productivity growth challenge thus does not appear to be confined to a few sectors, but to reflect broader issues across the economy.”

Basically, it appears our high immigration has been masking the low GDP per capita growth. ”New Zealand’s workforce has not witnessed the same efficiency gains as workforces in AE [advanced economy] peers (has not been ‘working smarter’), but it has compensated for this with adding more workers at a faster pace.”

Not enough gazelles and too many in the wrong sectors

Another damning part of the report is Section B In Search of New Zealand’s Gazelles. Gazelles are young high growth firms that see 20% growth in sales over at least one three-year period when they are under 10 years, from a base of at least USD100,000. Basically, we don’t have enough:

“Since the Global Financial Crisis, birth rates of gazelles in New Zealand, as a share of all new firms established, have been below the median observed in peer advanced economies. At around 13% gazelle birth rates in New Zealand were below levels observed in Australia, Finland or Sweden, but above levels observed in the Netherlands or Denmark.”

Paragraph 14 of the report I think, gets to where the real problems within our economy have arisen, and where tax may have played a very significant part. It notes young, high growth firms in New Zealand have been concentrated in a few sectors:

“Over 2008 to 2018 new gazelles in New Zealand were primarily concentrated in the financial and real estate sectors. The share of new gazelles in this sector was higher in New Zealand than in most peers, even as the sector saw lower overall productivity growth. At that same time, the share of new gazelles in ICT and professional and technical services, which include hi-tech product, high-productivity sectors dependent on innovation, has been lower in New Zealand than in peers. These trends suggest investment and innovation incentives may be misaligned between sectors in New Zealand. Trends could also be a symptom of the high propensity to save in real estate.”

This is where I think the issue of our lack of capital gains tax and a general lack of capital taxation comes home to roost. The incentives to invest in businesses have been trumped by the investment and lending practises in real estate. I think it was a particularly telling comment here about how those new gazelles, which are a very important part of productivity growth, are primarily concentrated in the financial and real estate sectors.

Replacing one set of disincentives with another

To pick up the issue that kiwikidsnz raised, economic efficiencies do arise from tax policies. Removing incentives such as 66% tax rates and a whole pile of distortionary tax incentives that are given because a government is trying to promote particular behaviour is a good move. But there’s also the disincentives to divert capital if you do not tax something, and it’s is becoming clearer and clearer to me that this is the biggest single problem with not taxing capital gains comprehensively. Coupled with bank lending practices what has happened is we’ve diverted resources into real estate resulting in lower productivity growth and less efficient use of our limited capital. That’s a policy issue that all parties need to consider.

The Australian counter-example

It’s worth talking about the long run implications of the Rogernomics reforms that happened starting in 1984. In October 1985 Australia was also going through its reform period but taking a more measured approach. One of the things it did was to introduce a comprehensive capital gains tax with effect from October 1985. We actually therefore have 40 years of examples to look at what happened around productivity.

Now productivity growth in Western advanced economies has been an issue, but Australia has seen higher productivity over the past 40 years. It has a capital gains tax. We have had lower capital productivity growth, and we don’t have a capital gains tax. Now, correlation is not causation, but there’s 40 years of examples there to make everyone think very hard that maybe in this case correlation does equal causation.

Interestingly, around the whole question of the 1980s idea of supply side economics and cutting taxes to generate economic growth, generally now seems to have run its course, and it probably was always going to do that. Simply because if you’re starting in the 1980s, individual tax rates were then at 60-70% and even more, in some cases. If you’re cutting rates down to 30-40% that’s a significant move and you’re bound to see something happen. But once rates get down to 30%-40%, the impact of tax cuts is less clear.

Meanwhile, in America, maybe not such a Big Beautiful Bill?

What’s really interesting is at the same time as the IMF report came out over the United States) someone who’s been described as the MAGA movement’s top economic guru, Oren Cass, has come out and been very critical of the latest President Trump backed tax cuts included in the Big Beautiful Bill (yes, it really is called that). Mr. Cass is the chief economist for the right leaning American think tank American Compass. He remains the leading proponent of conservative economic populism amongst allies of President Trump.

In talking about the Big Beautiful Bill and the tax cuts that have been included in that, Oren Cass has basically said that the ideas around the Laffer Curve and supply-side theories which have dominated tax policy thinking for the last 40 years have essentially run their race. After commenting “There’s much less confidence in the 1980s-style supply-side tax cutting” he went on

“The reality is we are not going to solve our economic problems if we do not get serious about the fiscal push and fiscal picture and actively reduce the deficit that’s going to require both reduced spending and raising revenue. If you’re not willing to do that, then I don’t think you can credibly say you’re addressing our economic problems.

…Whereas in the past you would have just said, “Well, this thing pays for itself,” This time there is a recognition that it does not pay for itself, — and we have a fiscal crisis — so we also need to explain how we’re at least partly going to pay for it.”

This is an absolutely astonishing admission to hear from a right wing think tank, and particularly in America, which is the home of the supply-side theory.

The thing to keep in mind about taxes, as I said last week, it’s all about politics. But taxes reflect economies and economies change. kiwikidsnz was right to make the comments that there were inefficiencies in our tax system in the 1980s and they were ripe for reform. But it is not a question of set and forget and that’s it, job done, we never have to change again. The dynamics of tax and economies change all the time. And our thinking around that needs to change and reflect that. As a few people pointed out in response to kiwikidsnz we may not have a capital gains tax but other countries do and they have also inheritance taxes, stamp duties, etc and in most cases those peers are wealthier than us. There is 40 years of evidence to suggest that non taxation of capital isn’t actually the economic Nirvana you might think, and it has distorted our economy, particularly our productivity as the IMF notes.

Dr Rod Carr on markets: “myopic, reckless and selfish”

On a related point there was a really interesting leader opinion piece by Dr Rod Carr in the Sunday Star-Times on 1st June. Dr Carr has had a hugely impressive career. He’s been previously chair of the Reserve Bank of New Zealand, worked at Treasury in the 1980s during the Rogernomics reforms and was the inaugural chair of the Climate Change Commission. In summary he has a vast wealth of knowledge about economic policy development in New Zealand over the past 40 years.

His topic was the role and influence of markets. Looking back, after completing an MBA in Columbia University in the mid-1980s, there was little doubt then that markets could allocate financial capital more efficiently than politicians and technocrats and corporate conglomerates. And he believes markets are still, “ruthlessly efficient at allocating privately scarce resources with a price.”

However, he continues markets are “myopic, reckless and selfish,” and understate future benefits and exclude or understate future costs. This results in

“…underinvestment in long-life infrastructure, the degradation of natural ecosystems and under investment in public health and education markets. Markets are reckless because we have created an asymmetry that sees profit accrue to those with private property, while costs are left to lie with the general public.”

He concluded “Markets should be a tool to enable us, not a mantra to enslave us.”

After 40 years, time to think again?

If you combine what Dr Carr said with the comments of Oren Cass and the IMF report on productivity, we’ve now had 40 years of results to look back at how our tax system has evolved and worked in relation to taxation and capital. In my view the long and the short of it is, it hasn’t gone according to plan. Maybe it’s time to look at the script all over again and rethink how we want to have our capital used if we want to start growing a few more gazelles, lift productivity and our living standards.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā.

It was a busy week in tax with Inland Revenue releasing guidance in relation to a couple of commonly encountered scenarios. The first is QB 24/04When is a subdivision project a taxable activity for GST purposes?

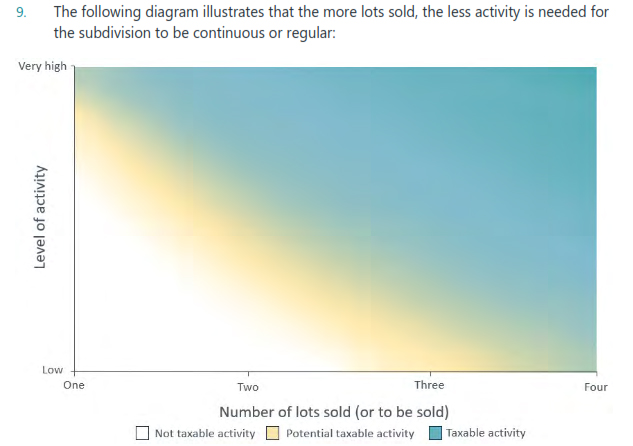

This covers the frequently discussed and very important issue of what is the GST treatment when you are subdividing land into two or more plots? The standard position about GST is that you must register if you’re carrying on a taxable activity and the value of those supplies exceeds the registration threshold of $60,000.

What’s a taxable activity?

Clearly many subdivisions will exceed that $60,000 threshold when they are sold so what represents a taxable activity? In order for a taxable activity to exist it must be carried on continuously or regularly. Therefore, it follows that for a subdivision to be continuous or regular, it usually needs to involve the sale of more than one lot. A subdivision which only involved one sale would usually be regarded as a one-off activity because it does not meet this threshold of continuous or regular.

Notwithstanding that the Inland Revenue guidance points out that some subdivisions which only led to one sale may in fact be continuous and regular. But that would only be if the level of activity involved was very high. Now, like so much of tax, it’s this comes down to the question of the facts of a particular case. Very high in this context might be something like construction and sale of a large office block, or more likely, because more often than not we’re talking about subdivisions of residential land, an apartment block.

The guidance continues the more subdivision plots are divided, the more likely it is to be deemed as being continuous or regular. Following the Newman decision way back in 1995, if a subdivision leads to the sale of four or more lots, that’s typically taken as the benchmark for determining that the continuously or regularly is happening and there is a taxable activity.

On the other hand, what happens when there are two or three lots? Then you have to consider the level of the activity relative to the number of lots being sold in order to determine whether or not this activity is continuous or regular. Therefore, you’d look at the level of development work, the time and effort involved, the level of financial investment and the level of repetition. This last point is probably most critical. If you’re repeating the process multiple times, this is more likely to fall into the continuously or regularly category. But as the guidance notes, everything is fact dependent.

On the other hand, the factors that are not so relevant are whether or not the subdivision is commercial. It doesn’t matter whether the subdivision has a “commercial” flavour or you are subdividing your own land to downsize. Anything done without an intention to sell the resulting land is not relevant. For example, if you build a house on a subdivided lot with the intention of living in it, but later change your mind and decide to sell, work done before you change your mind is not relevant.

Overall, this is useful guidance which comes with a helpful accompanying fact sheet. Keep in mind that the GST treatment is not tied to the income tax treatment. Your project might not be a GST taxable activity, but it could well be subject to the bright-line test or any of the other land taxation rules.

Another common issue – loans to shareholders

Moving on, the other topic, on which Inland Revenue has released useful guidance is a draft interpretation statement on the income tax position in relation to overdrawn shareholder loan account balances (sometimes called shareholder current accounts). Now, as anyone who works with small businesses will tell you this is actually a pretty common scenario. Despite this, the income tax position is not always as well understood as it should be.

In my experience, overdrawn shareholder current account balances typically arise in two scenarios. Firstly, where the owner or shareholder is taking out more in drawings than they’re being paid as a shareholder or employee or any other form of payment. This is a fairly common scenario.

The other instance is where the company has realised the substantial capital gain and shareholders extract the cash without waiting to consider the tax implications of doing so. Often in those situations, advisers don’t find out until maybe months afterwards. At that point it can become quite difficult to unwind the tax consequences because the numbers involved are quite substantial.

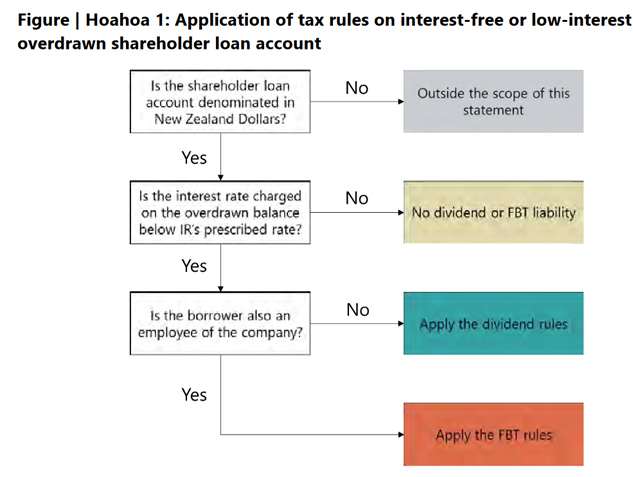

It’s therefore good to have Inland Revenue guidance and this comprehensive interpretation statement runs to 41 pages begins with the summary of the basic rules. A dividend is deemed to arise for a shareholder if they are paying little or low interest on an overdrawn shareholder loan account.

The amount of a dividend on an interest free or low interest loan typically represents the difference between a benchmark interest rate that should be charged and the amount of actual interest rate occurring on the loan. Benchmark for this purpose is Inland Revenue’s prescribed rate of interest, which since 1 October 2023 has been 8.41%.

A dividend can also arise where the loan has been advanced to an associated person of the shareholder. This can lead to some quite involved tracing of shareholdings and related calculations about percentage of shareholdings. This is necessary to determine if there is an association and whether that associated company is part of the same 100% owned group and therefore potentially eligible for the exemption on intra-group dividends. This is another area where I’ve encountered situations where this associated person issue hasn’t been picked up.

Incidentally, it’s worth noting, by the way, that although for New Zealand tax purposes, the amount of the dividend is the amount of interest that should have been charged in Australia and the UK, the amount of the dividend is deemed to be the full amount of the advance made. This might be something we might see Inland Revenue take a look at as it’s something that has occasionally come up in discussions with officials.

Loans to shareholder-employees

Were the shareholder is also an employee of the company, then the low or interest free loan is not treated as a dividend but is instead subject to fringe benefit tax. The amount of the benefit is the difference between the interest paid and the prescribed rate of interest. Something to note here is that the shareholder-employee doesn’t solely mean someone within the provisional tax regime, but it also includes shareholders who are employees and whose salary are subject to PAYE There’s a couple of useful flow charts to help people determine who might be captured by these rules.

The draft interpretation statement also notes that typically interest paid by a shareholder on an overdrawn current account is generally not deductible. This is because usually the drawings are often applied for private or domestic purposes, and so there’s no link to an income earning process. However, in some cases the money might have been withdrawn to invest in a residential property or some other income producing asset, in which case the interest would become deductible, if all the other deductibility criteria can be met.

One other key point to note is what happens if a shareholder is no longer required to repay the overdrawn balance, because the company forgives or remits the debt in some way. In this case the full amount of the loan will be deemed to arise either as a dividend or under the financial arrangements regime. In either case the shareholder will usually be taxed on the amount that’s been remitted.

The interpretation statement also covers scenarios when resident withholding tax might need to be deducted and interest therefore be reported as investment income. This would be somewhat unusual, but the interpretation statement explains when it might happen.

Overall, this is an important and useful document setting out the rules pretty clearly on a topic which as I noted is frequently encountered amongst small businesses but isn’t always as policed or managed as effectively as it should be. It’s also accompanied by a more digestible 8 page fact sheet. Consultation is open until 2nd August.

A blueprint for taxing billionaires?

One of the interesting things going on around the world in the tax policy area now is something of a trend amongst international organisations such as the International Monetary Fund (IMF), the Organisation for Economic Cooperation and Development (OECD) for releasing papers for discussion on the taxation of capital and wealth.

The latest such paper A blueprint for a coordinated minimum effective taxation standard for ultra-high-net-worth individuals was commissioned by the Brazilian G20 presidency earlier this year. The report was written by the French economist, Gabriel Zucman, a protégé of Thomas Piketty. It proposes a framework the approximately 3,000 or so billionaires in the world to pay at least 2% of their wealth in individual income tax or wealth taxes each year.

Zucman’s report notes there been a vast improvement in international tax cooperation since the mid-2010s, particularly with the Common Reporting Standard on the Automatic Exchange of Information which commenced in 2017. He also pointed to the recent agreement hammered out by the OECD for a minimum tax of 15% on large multinationals. (It’s worth noting though that agreement has yet to be fully implemented as progress has slowed recently).

Zucman correctly points to this growing international cooperation and exchange of information as laying the baseline for further international cooperation in the form of what he terms a common minimum standard, ensuring an effective taxation of ultra-high net worth individuals. According to Zucman this “would support domestic policies to bolster tax progressivity by reducing incentives for the wealthiest individuals to engage in tax avoidance and by curtailing the forces of tax competition.” This would target the tax havens where much of this wealth is sheltered.

The paper estimates that a 2% tax on those 3,000 billionaires could realise between US$200 and US$250 billion U.S. dollars in revenue annually. If it was extended to those worth more than $100 million, that could generate another US$100 to US$140 billion per annum. These tax revenues would be collected from “economic actors who are both very wealthy and undertaxed today”. Those affected might not agree with this assessment that they’re presently under taxed.

The paper is realistic enough to note that there are real challenges with the proposals, such as how to value the wealth, ensure effective taxation if some jurisdictions don’t agree to implement it, and of course compliance by taxpayers. It’s a bold proposal which has attracted a lot of attention although I’m sceptical about the potential level of revenue which could be raised. We really don’t have a very detailed understanding of the composition of the wealth and where it is held of the very wealthy. That’s an issue which would need to be addressed. And as I mentioned, there are serious issues around valuations and informed enforcement, which Zucman acknowledges.

Starting a conversation?

But for me, the most interesting thing to me about this whole proposal, it’s the latest. As I said, it’s the latest in the line of papers coming out of the likes of the G20, the OECD, the IMF, the World Bank, all of whom are basically saying that we are not taxing wealth sufficiently and we need to do something about that to address inequality. As Zucman himself puts it in the Foreword of the report

“The goal of this blueprint is to offer a basis for political discussions – to start a conversation not to end it. It is for citizens to decide through democratic deliberation and the vote how taxation should be carried out.”

In other words, he is repeating my old precept that tax is politics.

My personal view is we need to have a broader discussion around the taxation of capital. One of the points to emerge from the current debate going on over replacing the Cook Strait ferries is that the new ferries represented just 21% of the total cost of Project iReX. The other 79% represented the cost of upgrading the supporting infrastructure not just for the larger ferries but also to make it climate change and earthquake resilient for the next 100 years.

Even if we dialled back the futureproofing to, say, 50 years, we’re still talking about significant sums of investment. We’re also still left with the key point of how will we pay for the vast amount of infrastructure that we will need to upgrade to deal with the continuing impact of climate change. In my view our politicians have not yet seriously engaged with us on this issue.

Meanwhile in the UK…

And finally, this week a quick note on the UK election which is next Thursday. The likelihood is that the opposition Labour Party is heading for a massive win. One of their key tax proposals is the abolition of the remittance basis or non-dom tax regime.

But not every voter has understood exactly what that means. As Labour candidate Karl Turner recounted to the Guardian

“We met a guy who said he was going to vote Labour but wouldn’t now because he had just heard that we were taxing condoms,”

“I said, ‘condoms?’ ‘Yeah,’ he said: ‘I just heard on that [pointing to the TV] that you are taxing condoms, and I’m not having it. You’re not getting my vote.’ It was Terence [Turner’s parliamentary assistant] here who worked it out.

“‘We’re taxing non-doms, not condoms,’ I said. ‘Oh,’ he said. ‘Like the prime minister’s wife? Ah.’ He calls out: ‘Margaret: they’re taxing non-doms, not condoms.’”

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

(Loaded to Soundcloud 30 June 2024. Appeared interest.co.nz 1 July 2024).

IMF and Climate Change Commission suggest changes to the Emissions Trading Scheme are needed.

Like a never-ending Groundhog Day, every International Monetary Fund report on the New Zealand economy suggests tax reforms would promote efficiency. For example,

“There is a sense that the asset allocation in New Zealand households has a bit too much emphasis on housing versus other investments. We think a capital gains tax at the margin would help.”

That was IMF Mission Chief Thomas Helbling in 2017.

“…tax policy reforms are needed to promote investment and productivity and growth increase, increase the progressivity of income tax and mobilise additional revenue in response to long term fiscal challenges. To achieve these objectives, reforms should combine comprehensive capital gains tax, land value tax and changes to corporate income tax.”

And invariably the IMF’s conclusions are usually followed by a fairly dismissive response from the Minister of Finance of the day.

In 2002 it was the late Sir Michael Cullen responded to that year’s report: “The IMF’s credibility is not assisted by the fact that it tends to apply the same policy template regardless of the country’s circumstances”. This year Nicola Willis’s retort was “There are some things that are certain in life, death, taxes and the IMF recommending a capital gains tax.”

Associate Minister of Finance David Seymour also weighed in commenting. “I see the IMF again saying, oh, you need a capital gains tax. Every country has one. The only countries that don’t have one are New Zealand and Switzerland. But I say let’s be more like Switzerland.”

However, I’m not so sure that this was quite the zinger he hoped because as someone mischievously pointed out on Twitter, Switzerland has a wealth tax and a $59 per hour minimum wage in Geneva.

Deputy Prime Minister and former Treasurer Winston Peters was apparently not available for comment.

A de-facto capital gains tax – the bright-line test

Now, amidst all of the commentary about the IMF’s suggestions, one of the things that came up time and again is that in many ways, we do have a de-facto capital gains tax, except we don’t call it that. The bright-line test is an example of the approach that we’ve adopted, which has been ad hoc and responsive based on the government of the day’s policies at the time.

As you may recall the bright-line test was brought in with effect from 1st October 2015 by the National Government and it then applied to disposals within two years. In March 2018 the Labour Government introduced a five-year period and in 2021 it was increased a 10-year period. And so, a quite confusing scenario has developed as to which bright-line test applies because some of the exemptions have changed over time as well, particularly in relation to the main family home.

In one way, therefore, the reduction of the bright-line test back to two years again from 1st July is to be welcomed because it is clarifying and simplifying what has become an incredibly complicated area.

Tax Red Flags: More than just the bright-line test to be considered

The bright-line test and taxation of land has plenty of red flags when together with the excellent Shelley-ann Brinkley and Riaan Geldenhuys and moderator Tammy McLeod, I made a presentation about tax red flags on Tuesday to the Law Association. (Formerly the Auckland District Law Society). My thanks again for the invitation to present and to my excellent co-presenters, we had a very lively session talking around this.

In short when you drill into our current land taxation rules, they are very incoherent. The bright-line test is a backup test. It applies if none of the other land taxing provisions apply. And this is something that tripped up people before the bright-line test was introduced and will continue to do so even now it’s been reduced down to two years.

For many people, the particular issue to watch out for is the question of subdivision. If you own a property and undertake a subdivision within 10 years of acquisition it may still be caught under the existing rules, outside of the bright-line test. And in some cases, you may be caught by the combination of the provisions with the associated persons test which deem transactions to be taxable if at the time you acquired the land you were associated with the builder, dealer, or developer in land.

Sometimes the tax charge can be triggered way past the 10-year timetable since acquisition. That’s particularly the case in relation to a disposal of property where building improvements have been carried out. That particular provision, section CB 11 of the Income Tax Act, deems income to arise if a person disposes of land and

“within 10 years before the disposal”, the person or an associate of the person completed improvements to the land and at the time the improvements were begun, the person or an associated person carried on a business of erecting buildings. Note, the reference to “within 10 years before the disposal.” So, you may have owned that land for considerably longer than 10 years and yet still be subject to the provision.

Just a pro tip for anyone thinking ‘Great, with a two year bright-line test coming in, I can now sign a sale and purchase agreement, make sure settlement takes place after July 1st and it’s not going to be subject to the bright-line test.’ That’s not the case. The sale point for the bright-line test in that case is when the sale and purchase agreement is signed and not when settlement happens. I had at least one client get caught by that very provision because they went for a long settlement thinking that got past the two year period. It didn’t, and it is another case of always seek advice on transactions involving land, because as I’ve just outlined, the provisions are complicated.

Could a capital gains tax be ‘simpler?’

And this was the point we reinforced during our seminar. There is a lot of complexity already in our tax system around the taxation of land and in my view, in some ways a capital gains tax would actually clear away a lot of that uncertainty. It’ll become clearer that, broadly speaking, if you buy something, and you sell it subsequently, any gain will be taxable.

Now, how the gain is calculated and the rate at which it’s taxed are two different things. But often in the debate around the capital gains tax, those two things get conflated to run as an argument against the taxation of capital gains.

In my view, the point still remains that we have a confusing hotchpotch approach to taxing capital gains and at some point, grasping the nettle with a CGT as suggested by the IMF and also the OECD, would ultimately perhaps be a better approach.

Incidentally, doing so would be consistent with the well-established principle we have of the broad-based low-rate approach. There’s nothing to say that by broadening the tax base, we could not hold tax rates at current levels or even lower. Bear in mind that the when the last tax working group recommended the capital gains tax, it was intended to keep to help keep the top tax rate at 33%.

Watch out for trustees on the move across to Australia

One of the other issues that came up in our Tax Red Flag Seminar was the question of trustees, and beneficiaries and settlors moving cross-border, particularly to and from Australia. That is something all three of us are seeing quite a bit of and it is something to watch out for as a key red flag.

The IMF on how to tax wealth

If there is a certain repetitiveness to the IMF’s discourse about taxing capital, it’s part of a global discourse on the topic. Earlier this month the IMF released a How to Tax Wealth note. These how to notes are “intended to offer practical advice from IMF staff members to policy makers on important issues.” And this this was a very interesting read as you might expect.

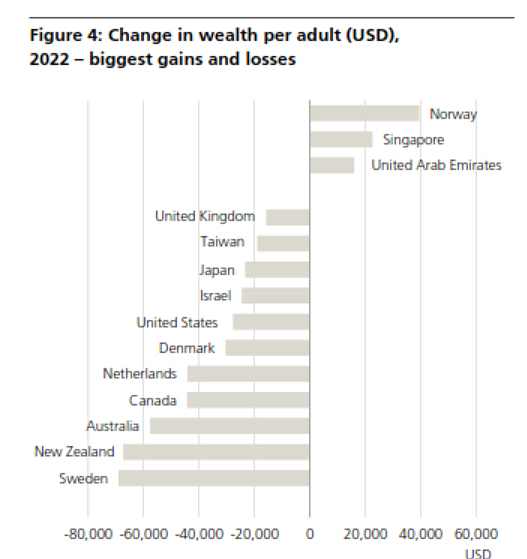

The IMF’s How to Tax Wealth note neatly coincided with the release of the UBS/Credit Suisse, Global Wealth Report for 2023. According to the report, in 2022 New Zealand ranked sixth in the world with an average wealth of US$388,760 per adult. On the basis of median adult wealth per adult, again in U.S. dollars, we ranked 4th behind Belgium, Australia and Hong Kong, with a median wealth of US$193,060.

Incidentally, these rankings were after a very sharp fall from 2021 levels, where New Zealand was only behind Sweden in the biggest loss in wealth per adult.

I am genuinely very surprised to see New Zealand rating so highly for both average wealth and median wealth. On the other hand this Credit Swisse/UBS report is another example of why there’s a great debate going on around the taxation of wealth not just here, but globally.

And this IMF How to Tax Wealth note is instructive in its approach. It starts by making a very obvious point, how much to tax wealth is a distinct question from how to tax wealth. The note argues that:

“returns to capital generally should be taxed for equity and possibly efficiency reasons. and that in many countries, wealth inequality and better tax enforcement strengthen the case for higher effective taxation than in the past.”

Now the IMF doesn’t make any particular proposal about a specific level of tax, the note is basically about ‘here are things you should consider.’ But on the question of wealth taxes, it does come down pretty much against them noting,

“Improving capital income taxes tends to be both more equitable and more efficient compared with replacing them with net wealth taxes. Countries hence should prioritise improving capital income taxation over considering the introduction of wealth taxes”.

Then it talks about – in terms of strengthening capital taxes – addressing loopholes, notably the under taxation of capital gains in many countries. There’s a passing comment, that perhaps you can use a one-off net wealth tax or maybe apply it to very, very high wealth levels.

Time for inheritance tax?

But the Note also concludes “taxing capital transfers through gifts or inheritance provides another opportunity to address wealth inequality.” The IMF comments that the efficiency costs of such taxes are modest, and notes that “inheritance taxes are better aligned with redistribution than estate taxes, since exemptions and rate structures can account for the circumstances of the heirs.”

What really makes the New Zealand tax system unique is not the absence of a capital gains tax because, as David Seymour pointed out, other countries don’t have that, namely Switzerland. It’s the complete absence of taxes on the transfer of wealth, which has been the case now since 1992. That’s what makes New Zealand unique – we have no general capital gains tax together with no estate or gift or wealth taxes.

And this is an area where I think a lot more consideration needs to go into because as the IMF noted, we’ve got fiscal challenges ahead, and where might the revenue be raised from to meet those challenges.

The IMF and Climate Change Commission suggest changes to the ETS

And finally, back to the IMF again. It concluded its mission report by noting that “New Zealand’s ambitious climate goals call for major reforms,” and it referenced the Emissions Trading Scheme, having helped limit net emissions by encouraging robust reductions and removals, particularly from afforestation.

But the IMF then went on to say that “significant reforms” are going to be needed to meet domestic and international targets, and these include reducing the number of available units in the ETS, pricing agricultural emissions and strengthening the incentives for gross emissions reductions within the ETS. The IMF finally note that given the ambition of New Zealand’s first nationally determined contribution under the Paris Agreement, the use of international mitigation i.e.; buying credits from offshore, is likely to be required.

Now the IMF report was a week after the Climate Change Commission, and pretty much said the same thing, and advised the coalition government they should halve the number of ETS units on offer in each of the next six years. The last ETS auction did not go brilliantly. That has a flow on effect in that by reducing the amount of income from emission trading unit sales, it’s going to limit crown revenue for tax cuts.

Vale Rod Oram

It’s interesting to see a confluence of opinion happening here and an appropriate time to remember the late Rod Oram someone who was a very strong environmental journalist. I was fortunate enough to know him all too briefly after we met at a panel discussion. We’d planned on him appearing as a guest on the podcast. Sadly, with his passing that will never happen now, and our thoughts go out to his family and friends.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

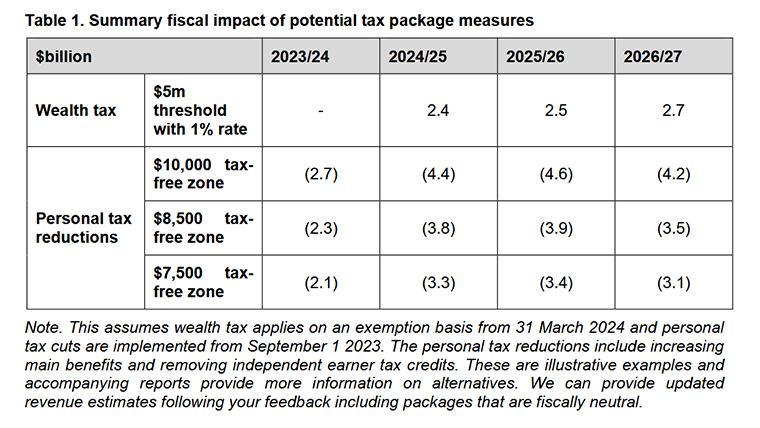

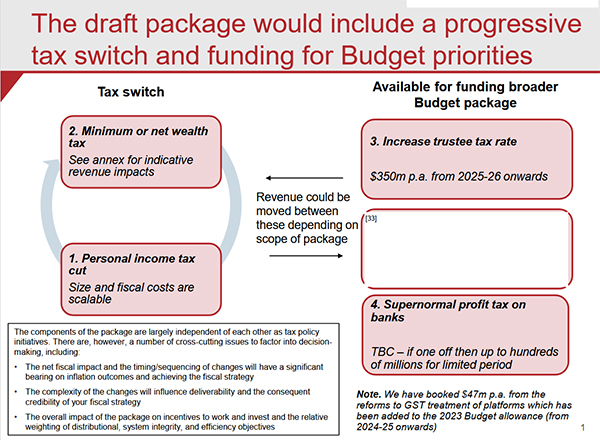

The big news last week was the release of the official advice to Ministers on tax incentives during the lead up to this year’s Budget. And it was quite a bombshell. Amongst the wealth of material provided was the surprising news that a key proposal had been until quite late in the piece a tax switch where in exchange for introducing a tax free threshold of $10,000, the Government would introduce a wealth tax.

Now, the Prime Minister immediately ruled out the wealth tax and also ruled out any capital gains tax if the government gets re-elected. So to a large extent, all this fascinating material is largely redundant. But it still provoked the continuing debate around the pros and cons of a wealth tax. And in fact, it’s really very interesting to go through the material and see how the policy developed and where they were planning to take it.

The final scheme would have applied a 1% tax rate to net wealth above a $5 million threshold under what was termed an “exemption approach”. This was initially thought it could raise between $2.7 and $2.9 billion annually and would have affected some 46,000 individuals. According to officials the wealth in scope at a $5 million threshold would be about $210 billion

A minimum tax?

Now, in the course of development the proposal started with something called a “minimum tax” under which proposal a person with high wealth would pay tax on the greater amount of either their deemed income calculated as a percentage of the net worth or the taxable income they have under existing income tax rules. The deemed income would have been based on the idea of economic income, which would include unrealised gains. If you recall when the Sapere report and the Inland Revenue High Wealth Individual research project were released, there was a great deal of controversy around this measurement because once you measured economic income and unrealised gains, it appeared the wealthy were paying an effective tax rate of 9%.

This minimum tax was the initial proposal which then got dropped over time. In the course of discussions, they moved away from what they called a “switch approach”. Under this once a person crossed the threshold, then all the deemed economic income would be subject to the wealth tax rather than just the proportion above the threshold.

And this so-called “exemption” is pretty much what we see in other wealth taxes around the world. It appears in the design of the wealth tax officials took a close look at the Norwegian system. One of the other features I found surprising was that the family home would be excluded. It seems to me that the tax preferred approach to the family home, has led to a large amount of overinvestment in housing.

Wealth taxes – profile of potential taxpayers

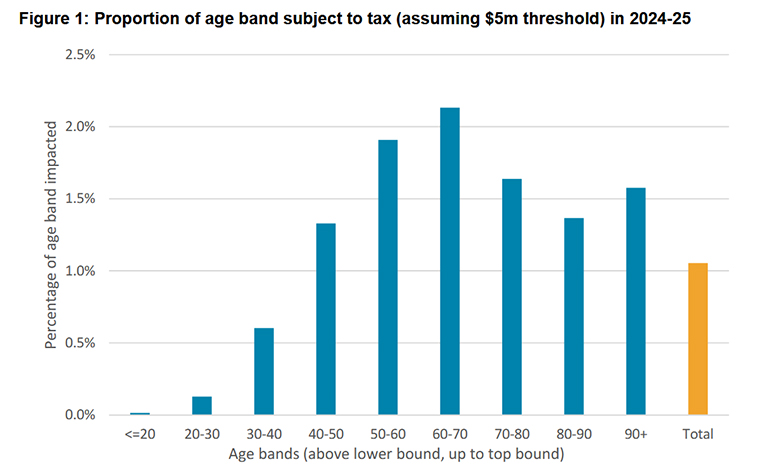

A key report on a wealth tax contained a very interesting discussion, around which group of taxpayers would be most affected. The projection was the age group which would be most affected at the $5 million threshold was that between 60 and 70. An estimated 2.1% of this group population has net worth over $5 million. According to these statistics, 1.5% of the over 90 year old group would be affected.

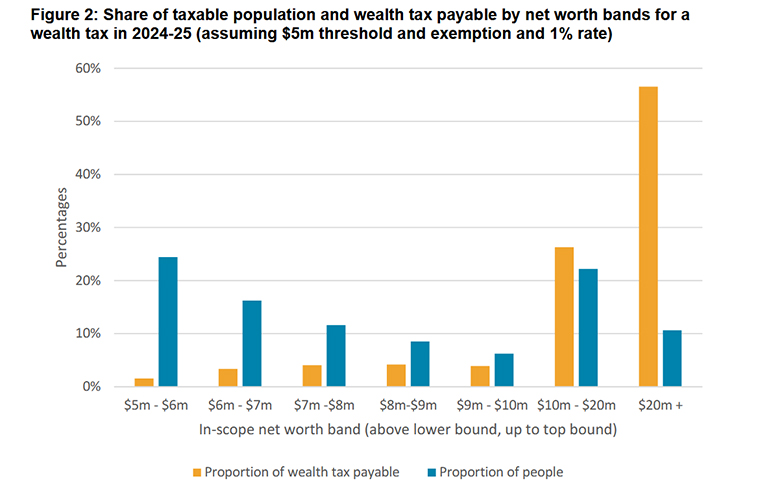

But in fact, as you might expect, more than half of the wealth tax would have been paid by the high net worth individuals with a net worth in excess of $20 million.

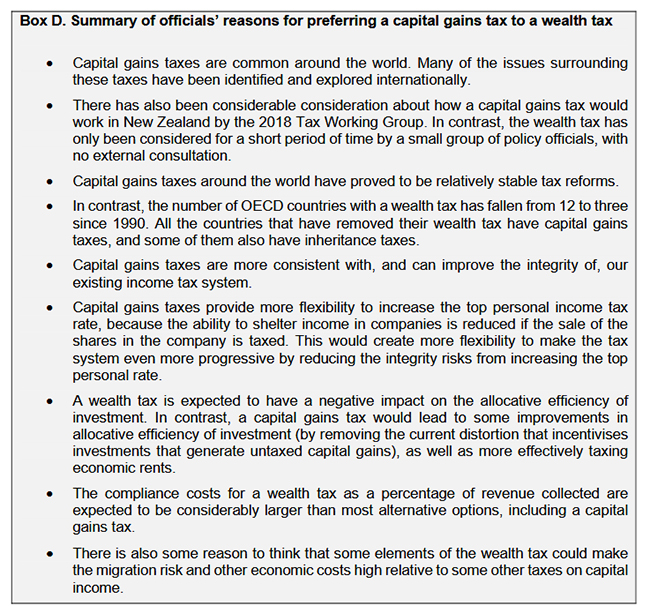

Officials prefer a capital gains tax

But I think the other thing that came out quite clearly from the papers was that the officials were not at all impressed by wealth taxes. They preferred a capital gains tax.

By the way, the officials view probably reflects a reasonably widely held belief if largely unspoken view amongst the tax community, that if we’re going to tax capital then a capital gains tax is probably the way forward.

Anyway politics intervened again and so a capital gains tax has now been ruled out in their prime ministerial lifetimes by two successive Labour prime ministers. However, as I said to Corin Dann on Morning Report the politicians may rule out capital gains taxes but we’ve got a lot of issues with an ageing demographic and the impact of climate change. The strains on the tax system, which have been recognised by Treasury and its Long Term Insights Briefing He Tirohanga Mokopuna in 2021 recognises that. The issues about needing more tax from somewhere haven’t gone away.

Paying for Cyclone Gabrielle

There were also suggestions as a one-off response to the impact of Cyclone Gabriel, for a levy on the banking sector. There was a comment that the four main banks have persistently “elevated levels of profitability relative to the smaller New Zealand banks and overseas and comparators in part due to the relatively low costs of the large New Zealand banks.” A temporary levy on the banks could raise somewhere between $230 and $700 million. As the Greens noted, Margaret Thatcher of all people did actually impose a surcharge on banking excess banking profits when she was Prime Minister.

There was also a suggestion of a one-off flood levy similar to what was introduced in Queensland following their catastrophic floods in 2010-11. A temporary 1% levy applied to all taxpayers would have raised $1.8 billion. But one only applied to income above $100,000 would raise $250 million.

The quid pro quo – a tax-free threshold

The quid pro quo for a wealth tax would have been a $10,000 tax free threshold. Once again Treasury and Inland Revenue weren’t enthusiastic. They suggested more significant increases in the lower thresholds including lifting the threshold at which the rate goes from 10.5 to 17.5% from $14,000 to $25,000, which is actually substantially ahead of where it would have been if had it been indexed to inflation. However, they proposed lifting the next threshold rate increases to 30% to $52,000. This is the threshold which I think is extremely problematical because of the large jump and at its current level of $48,000 is now well below both average and median wages.

There are two things of interest here. Firstly, a recognition that something has to be done. Tax free thresholds are very popular, but they’re not as efficient is the official advice. Secondly the cost of increasing these thresholds would have been over $4 billion annually. This is an acknowledgement that by not indexing thresholds since 2010, governments have given themselves a permanent headache around having to make threshold adjustments that become increasingly expensive.

A mystery policy?

A tax-free threshold is apparently out of the question. But maybe not because amidst all the papers, there’s are parts which have been redacted. These refer to another policy, whether that was capital gains tax, we don’t know. But whatever it was, it’s been redacted and not been released under the Official Information Act.

We’re now within three months of the General Election and Labour is still to release its tax policy. So maybe there’s something in that hidden part which will be revealed.

Secrecy and the Generic Tax Policy Process

There’s been some discussion that because this was all carried out secretly and outside the Generic Tax Policy Process (GTPP) that maybe this might not have resulted in a terribly efficient tax. I’m less concerned about governments deciding they’re going to do something for electoral gain and requesting work be carried out discreetly. But I do agree that if it’s done outside the GTPP, there is a risk that the design could be faulty. We’ve seen that with the bright-line test and the continual tinkering that has to be done. Worth remembering, by the way, that the bright-line test itself was a surprise. There was no previous consultation before it was first introduced in the May 2015 Budget by Bill English.

I like tax surprises in budgets, and I believe they’re part of normal politics. As I’ve said before, tax IS politics. But I do think that if you look entirely at tax through a political lens, then you start to get this narrow view developing right now where everyone says the politics of raising taxes are too hard, but the economic question of, how are we going to pay for the coming challenges just gets sidelined.

To repeat myself, we have serious issues to address coming up. And my view is if you want to maintain the broad based, low rate approach to fund these challenges, you’re going to have to do something around capital taxation. And the sooner you do it, the better.

Inland Revenue dropping the ball on investigations?

Moving on, one of the officials’ key objections to a wealth tax was the cost of compliance. Inland Revenue would clearly need to increase its capabilities. In its advice on its Initiative Work Programme it commented “the Government’s current tax and social policy work programme will use up most of our specialist design and delivery capacity over the next three years.”

Now the question of Inland Revenue’s operational capabilities came up at the start of last week when it was raised by National’s revenue spokesperson Andrew Bayly.

Following some written questions to the Minister of Revenue, he had determined that the number of investigations conducted by Inland Revenue dropped from an average of 77 a month between February 2017 and October 2020 to only 17 a month between October 2020 and June 2022. Furthermore, the time Inland Revenue spent on hidden economy investigations has also dropped substantially, from 3094 hours in November 2020 to just 805 hours in May this year.

Mr Bayly thinks Inland Revenue is dropping the ball here. Now, he’s tried that for obvious political reasons to Inland Revenue’s work on the High Wealth Individual research project, but that was separately funded. (Incidentally, early drafts of the report were made available to Cabinet as part of the pre-budget preliminaries).

There is an ongoing operational issue, in my view, about Inland Revenue’s investigations activity. And actually, it has acknowledged it has not been doing as much work in the investigations and debt recovery field. Page 36 of its Annual Report for the year ended 30 June 2022 notes:

“We did less work than would be typical in areas such as debt collection, investigations, disputes, litigation and liquidation activity.”

Now, part of this is down to the response to COVID. There were great demands made of Inland Revenue to which it responded superbly. But note the number of investigation hours back in November 2020, which is in the heart of the pandemic, was 3,094 but now it’s down to only 805 hours when we’re supposedly post pandemic, or rather a different stage of response to it. Inland Revenue saying that the fall off in investigations is because it has had to deal with COVID and this year’s weather-related events is not a satisfactory explanation in my view.

And when you start digging into Inland Revenue’s appropriation statements which are published as part of its annual report, you can see the amount spent on investigations for the past five years has fallen quite considerably in absolute terms, let alone when adjusted for the impact of inflation.

Reduced investigation funding

In the year to June 2018, the investigations appropriation was just over $140 million. But for the year to June 2022, it was just over $113 million. That’s a significant drop of nearly 20% in absolute terms.

Inland Revenue investigations appropriation per annual reports.

30 June 2022 $113.235 million

30 June 2021 $124.325 million

30 June 2020 $109.720 million

30 June 2019 $134.706 million

30 June 2018 $140.164 million

So, what this points to is the claims being made by Mr Bayly about Inland Revenue taking its eye off the investigations ball does appear to be backed up by the evidence of where it’s been spending its money. One of the explanations for this appears to be tied into its massive Business Transformation project. Inland Revenue, once it got started on this, seems to have pretty much solely focused on getting it across the line.

Where did the investigations staff go?

Part of Business Transformation included substantial reductions in its headcount, which went from 5789 in June 2016 to 3923 in June 2022. Now, that’s nearly a third of the workforce gone. We also know that although there was a substantial number of staff (nearly 800 apparently) whose sole purpose was simply re-inputting data so it could be used, a large number of very experienced investigation and operational staff were also let go. I know that because I’ve been speaking to a few of them.

Therefore, other tax advisers and agents and I are wondering whether Inland Revenue now has a diminished Investigation capability. There’s also another matter which Andrew Bayly also picked up on, the fact that Inland Revenue has decided to adopt a completely new metric for measuring its investigation performance. That makes you wonder why it’s done that. We won’t know what they’re measuring and how effectively, as the year just ended on 30th June is the baseline for this new metric.

But it’s important in a system that relies on voluntary compliance, there is the expectation by all of those taxpayers who comply that Inland Revenue is making sure that those who are not playing by the rules will be found and investigated. The concern is if Inland Revenue’s capacity to do that is diminished and it’s not fulfilling that role, then the overall perception of the integrity of the tax system is undermined. And that’s not good long term because naturally people will start thinking “That person is getting away with it, so we can too”.

I hope this is something the new Commissioner of Inland Revenue Peter Mersi is paying a lot of attention to. It will be very interesting to see what the department says when its latest annual report is published in October.

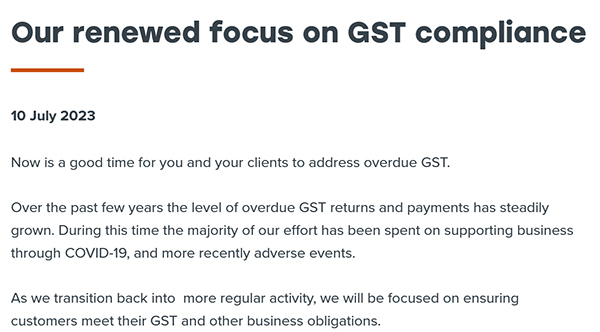

Inland Revenue renews its focus on GST

And finally, this week and, coincidentally or not, a couple of days after the story about Inland Revenue’s lack of investigation focus, it posted a warning for tax agents about “Its renewed focus on GST compliance”

Now, you can easily interpret this as an implicit acknowledgement of Andrew Bayly’s criticisms, but it is in fact another sign which we’ve seen steadily emerging that Inland Revenue is now repositioning itself back into what you might call its regular routine.

As usual, we’ll keep an eye on what that means and bring you developments as they emerge.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Submissions close next Friday on the Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill. This is the tax bill introduced alongside the Budget. The bill, as is typical, sets the annual rates for the current year ending 31st March 2024, but also has key provisions relating to the establishment of the legislative basis for the implementation of the Pillar Two international tax proposals at a later date. Separately, there are key provisions for increasing the trustee tax rate from 33% to 39%, with effect from 1st April next year.

The main part of the bill involves preparing the groundwork for the OECD’s Pillar Two multinational tax proposals. These are part of the Global Base Erosion and Profit Shifting (BEPS) initiative which is intended to introduce a global minimum corporate tax rate of 15%. Now, I generally have no involvement with clients that would be affected by these proposals which are targeted at the large multinationals. Most of the clients I deal with on international affairs are much, much smaller scale operations.

But there will be plenty of expert commentary and submissions on this particular bill because it will affect significantly large multinationals, those with international presence and gross turnover exceeding €750 million annually in any two of the preceding four years. It’s a fairly select group. There may be some tweaks as a result of submissions being made, but I would expect this to go through largely unchanged. But it will be interesting to see what submissions are made around this.

Increasing the trustee tax rate – maybe not quite such an obvious move

Of much more direct interest to many more clients and probably also much more controversial is the proposal to raise the trustee tax rate from 33% to 39%.

Now, conceptually aligning the trustee tax rate with the top personal income tax rate makes sense. We see that in other jurisdictions. Practically speaking, however, given the incredibly diverse and prolific nature of trusts in New Zealand, this would seem to be a much more practically difficult issue to implement it.

In discussions with other advisors, a couple of points have emerged. There seems to be a general consensus that some form of de minimis threshold is appropriate to take account of the fact that there are so many more trusts and they have operated on a policy of not generally distributing income because the 33% tax rate probably aligned with most of the income tax rates applicable to most of the beneficiaries. The 39% tax rate only kicks in above $180,000 income and that’s a much smaller group.

The argument which has been raised is that the measure, although conceptually correct, is actually in response to a small group. And therefore, it has a rather indiscriminate effect on people whose aggregate income including that of a trust, would not cross the $180,000 threshold. The suggestion has been made that we should have some form of de minimis threshold. I’ve seen suggestions raising between $15 and $50,000.

In response to this proposal Inland Revenue officials have asked “What’s to stop people setting up a number of trusts to maximise the advantage of the differing thresholds?” Well, two things. One, first of all, practically the cost involved of establishing these trusts, you would typically not get much change out $2-3,000 plus GST. But more importantly, you then have ongoing costs involved because following the Trusts Act 2019 coming into force in early 2021, trustees are much more conscious of their obligations including providing information to beneficiaries.

But more importantly, if someone established ten trusts like that and then divided up assets and income producing assets so as to maximise any potential threshold that would run square head on into Inland Revenue’s existing anti-avoidance provisions. Therefore, in practical terms, I think Inland Revenue’s arguments about the risk aren’t really a starter. There is also the question that there are there are increasing compliance costs involved with running trusts now as I just mentioned.

There’s also something Inland Revenue tends to glide around in my view and that’s its very, very narrow view of Section 6A of the Tax Administration Act. This states Inland Revenue’s duty is to collect the highest amount of revenue that is practicable over time, bearing in mind the costs of compliance. Keeping that in mind some form of de minimis seems a not reasonable approach. Otherwise, trustees may feel that they are obliged to do a load of distributions to beneficiaries just to minimise the tax payable.

I have actually encountered scenarios where trusts were established which could have done that and minimise the tax payable but didn’t do so for a variety of reasons. So it could be that inadvertently Inland Revenue may trigger the trustees to actually distribute income at lower tax rates than they were doing previously. I’m certainly watching to see how the Select Committee responds to this point.

Deceased estates potentially unfairly penalised?

The second point about the 39% tax rate increase is how it will apply to estates of deceased persons. The proposal is the 39% rate will apply to a deceased estate after 12 months have passed since the person died. Now, my immediate reaction to that proposal when I read it was that period was way too short, and that has been confirmed in subsequent discussions with other tax practitioners and lawyers. In fact, right now I’m involved with the tax affairs of an estate where more than three years has passed since the death of the deceased person.

The majority view of the lawyers I’ve spoken to on the matter is the minimum period should be at least 24 months and probably somewhere between 36 and 48 months would be much more realistic. I would be interested to see what happens here; particularly about just how many law firms do make submissions on this. I’ve made the law firms I work with aware of the issue and recommend they do submit. Select committees sometimes hear a lot from the same people, but they are always particularly interested in hearing from people who don’t normally submit but are doing so in this case on the practical basis “Our experience is this would be not a good move” or “We would support it”, whatever.

Anyway, submissions on this bill close next Friday. If you have concerns about any of these measures I’ve discussed, make a submission to the Finance and Expenditure Select Committee using this link.

The IMF holds forth on cryptocurrencies

Now moving on, this week the International Monetary Fund, the IMF, released a working paper on the taxation of crypto currencies. https://www.imf.org/en/Publications/WP/Issues/2023/06/30/Taxing-Cryptoc… This is an absolutely fascinating paper, it’s actually one of the most interesting papers on the taxation of cryptocurrencies than I have seen since crypto assets moved into the mainstream over the last five years.

In short, the IMF’s view is that tax systems need updating to handle the challenges posed by crypto assets, particularly in relation to their anonymity and their decentralised nature. And these, in the IMF’s view, make it hard to establish and maintain effective third-party reporting systems such as we use here in the banks or the international OECD’s Common Reporting Standards on the Automatic Exchange of Information.

It’s a very readable paper which starts by pointing out that after basically starting from zero in 2008, the market value of crypto assets peaked in November 2021 at about USD3 trillion USD (nearly NZD5 trillion). Although estimates vary because the surveys are self-selected, maybe perhaps 20% of the adult population in the U.S. and 10% of the adults in the U.K. hold or have held crypto assets. And the number of global users could be as many as 400 million people. On the other hand, although USD3 trillion sounds like a lot, it’s only about 3% of the global value of equities.

But the paper notes the potential for disruption, which is one of the founding ethos of Bitcoin and the crypto asset world, is quite significant. There are all sorts of questions around the tax impact of all these colossal capital gains suddenly arising and then the potential impact of losses, now that USD 3 trillion valuation is down to around $1 trillion. What’s going to happen with those $2 trillion of losses? Are they being claimed?

The paper really is very, very interesting in covering a whole number of topics. And basically it sums up the problem as being tax systems were not designed for a world in which assets could be traded and transactions completed in anything other than national currencies. It has some interesting comments about the effect of crypto billionaires. Apparently 19 were on the Forbes list, the richest list in America in April 2022. In an interesting aside the paper comments about “a loosely defined sense that much wealth channelled into crypto escapes proper taxation appears to have become part of the wider mood of dissatisfaction around the taxation of the rich.”

Blockchain efficiencies for tax administrations?

Yes, there are certainly crypto billionaires, but a lot of ordinary people probably piled into crypto because they saw an opportunity to realise substantial gains. How they declare those is of course where this paper is focussed on. It also notes that much is made of blockchain technology and it the working paper notes that the information blockchains contain on the history of transactions is actually remarkably transparent which

“might ultimately prove valuable for tax administration; and the use of smart contracts (self-executing programs) within blockchains, for example, might in principle help secure chains of VAT compliance and enforce withholding.”

What this paper picks up on is concerns I haven’t seen too much discussion of around the VAT (value added tax) or GST consequences of transactions using crypto. The paper’s section on externalities picks up on an issue which has is often raised in relation to crypto, and that’s the carbon effect of mining. It notes that the associated carbon emissions are cause for considerable concern including an estimate that in 2021 Bitcoin and Ethereum mining used more electricity than either Bangladesh or Belgium and were responsible for generating 0.28% of global greenhouse gas emissions. It suggests there maybe should be a charge on mining in relation to that effect.

Overall, the paper does not propose solutions. It is a working paper which is really raising all the issues. Now, it notes which I’ve mentioned recently, that the OECD has introduced its Crypto-Asset Reporting Framework, which is to extend the Common Reporting Standards reporting to the crypto world. But in the IMF’s view, “implementation remains some way in the future and in any case will not in itself resolve the issues challenges proposal posed by decentralised trading.”

Overall, a very comprehensive and readable paper which brings a big picture thinking to the issues the taxation of crypto crypto presents. I highly recommend reading it.

Government tax revenue behind forecast

And finally this week, the Government released its financial statements for the 11 months to 31st May. Of note immediately was that total tax revenue of $102.8 billion was $2 billion below forecast. Now $1.87 billion of that shortfall related to lower corporate income tax. GST was also $104 million below forecast and also another note that the economy is slowing down.

On the other hand, the rise in interest rates means that the amount of resident withholding tax collected on interest is $242 million ahead of forecast. Incidentally, the withholding taxes on dividends are also $12 million higher than forecast. That latter point may be in reference to what we discussed at the opening of the podcast, with the trustee tax rate rising to 39%, some more dividends are being paid ahead of that rate taking effect.

Government core expenses at $145.6 billion were actually $120 million below forecast. Interest costs were just under $6.6 billion, $134 million higher than the Budget estimate. Overall, the government debt rose by $5.1 billion to $73.3 billion, but net that’s the equivalent of 18.9% of GDP. The Government is still in the black. Overall, based on 2021 numbers, its net worth of $170.4 billion, which is roughly 44% of GDP, keeps it as one of the few OECD countries with a positive net worth.

There’ll be plenty of talk about budget deficits, etc. going forward in the election campaign. And we’ll be paying attention to what the parties say on tax. But it’s probably just worthwhile keeping it in context that the Government’s balance sheet is reasonably solid. You wouldn’t want it to be running away rapidly, but when you look at what’s going on in the United States where they basically cobbled together ad lib budgets to just paper over the cracks until the next crisis emerges, we are in a reasonably strong position.

How that balance sheet is maintained and used to brace ourselves for the impact of climate change is a major challenge. I think we now have a major issue in terms of having to basically fund adaptation by having to fund moving people out of at-risk areas. Cyclone Gabrielle rendered 700 homes unliveable. That could add up to maybe a billion dollars. Although a billion dollars in the context of $145 billion government spending is well under 1%, a billion dollars year in, year out is money that is not going into other areas that people want for health, education, etc. So anyway, the Government’s books are in reasonably good shape, but there are strains ahead.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.