In the same week as Public Service Minister Nicola Willis directed department bosses to tighten up on working from home arrangements, it’s a little ironic to see Inland Revenue release a draft consultation on the topics of deductions for expenditure and travel by motor vehicle between home and work and when an employer provided motor vehicle is subject to fringe benefit tax (FBT) for travel between home and work.

These were released alongside some interesting commentary from Inland Revenue that it is currently reviewing FBT, so what is set out in the draft consultations may change, but as Inland Revenue note, it gets a lot of questions on the topic. With regard to this FBT review my understanding is we may see something relatively soon. I think given the outcome of the Inland Revenue’s regulatory stewardship review of FBT and what the Minister of Revenue has said previously, it’s likely this review with look at simplification measures.

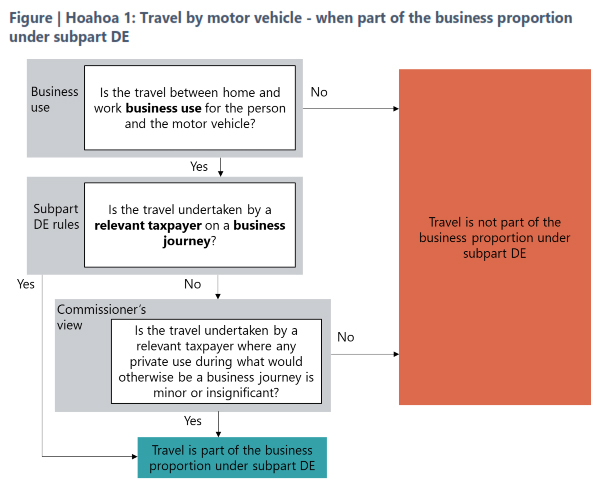

There are actually two consultations which will replace the previous interpretation statement IS3448. The topic is quite involved, because the two draft consultations run to 111 pages of commentary and examples. Fortunately, as is now the common practise, each draft consultation is accompanied by fact sheets, each containing a very useful flow chart to help people work their way through the maze.

The deductibility of motor-vehicle travel between home and work

The first draft interpretation statement deals with the question of deductibility of travel by motor vehicle between home and work which is set out in Subpart DE of the Income Tax Act 2007. What that subpart does is limit deductions for motor vehicle expenditure to the business proportion of the expenditure. It generally applies to self-employed taxpayers and partners in partnerships, but it can also apply in some circumstances to close companies and look through companies.

The basic position is that a journey is deductible if it’s a business journey, but to be a business journey and deductible, the whole journey must be undertaken for the purpose of deriving income. This is actually slightly different from the general deductibility provision for tax, which allow deductions quote to the extent to which they are incurred in deriving gross income. By contrast, this the provisions in Subpart DE are very specific it’s got to be a business journey if it is to be deductible.

Four exceptions

Generally speaking, and it’s probably no surprise here, travel between home and work is viewed as private. But there are four exceptions as a result of case law. Firstly, where the vehicle is necessary for the taxpayer to transport goods and equipment that are essential for their work between their home and workplace and for use both at home and in their workplace.

Now secondly, the taxpayers work is itinerant, which means that the taxpayer works at different locations during the workday and the sequence of where they work and how much time they spend is unpredictable and varies. It’s therefore not practicable for them to carry out their work without the use of a vehicle.

The third case is where a taxpayer is responding to emergency call outs and does so from home. And finally, and this is increasingly relevant, the taxpayer’s home is a workplace or base of operations for the purposes of travel to and from work.

This latter point is where we’ll probably see a lot of discussions and arguments. In order for a home to be treated as a workplace or base of operations the role requires a significant proportion of a person’s work to be spent working at home. I think it’s most likely to apply to owners of businesses who may be working between two places, but senior employees who might be required to make international calls in the evening, they may will be covered.

What’s a business journey?

A business journey is one primarily carried out for business purposes. Case law allows an overall journey to be treated as two journeys if there is a stop in between. It’s possible that one part represents a business journey, and the other part is private.

Furthermore, case law also said that some incidental private use does not mean a journey is prevented from being a business journey. Under the draft Inland Revenue consider that insignificant private use can’t exceed either approximately 5% of the total journey and approximately two kilometres.

The consultation also deals with the issue of what if vehicles are taken home for security purposes or, as is now more common, it’s an electric vehicle taken home to be recharged. Either of those circumstances are not sufficient in themselves to make the relevant journey between home and work a business journey. There have to be other factors at play, such as the exceptions we’ve previously mentioned or that home represents a workplace.

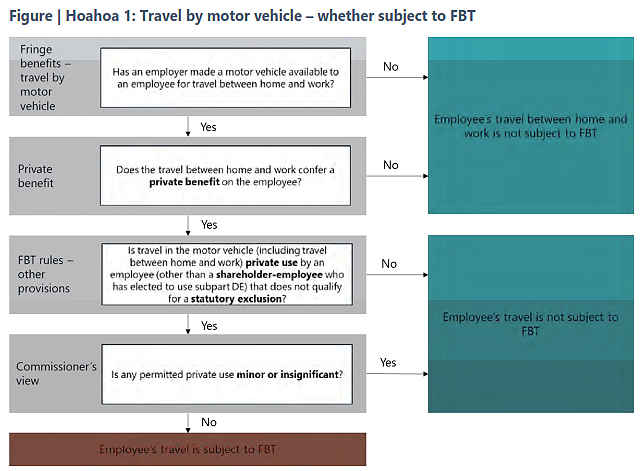

When does a fringe benefit arise?

The second interpretation statement and supporting fact sheet considers the question of when a fringe benefit arises when an employer provided motor vehicle is used for travel between home and work. The position is pretty straightforward: if a vehicle has been provided for private use, FBT will apply. In this context private use would include the use of the vehicle for travel between work and home and work. If a employee has a employer provided vehicle and travels to between home and work in that, then fringe benefit will apply.

There are three statutory exclusions from FBT which would cover travel between home would work. These exclusions apply to work related vehicles (a topic the subject of a whole another interpretation statement;

Emergency calls affecting health, life or the operation of essential machinery and services; and

business trips of more than 24 hours.

If any of these exclusions apply the whole day is excluded from the calculation of FBT.

As noted above Inland Revenue is in the course of reviewing FBT, so maybe some of this might change within the next couple of years or so. In the meantime, it’s good to have this draft guidance. Consultation on this is open until 6th November.

Meanwhile progress on the international tax deal continues

Moving on, we’ve talked regularly about the G20/OECD international tax agreements on base erosion and profit sharing. This week, several jurisdictions signed a multilateral treaty which will to help the Pillar Two subject to tax rule. But the other thing that’s important which was concluded in the last few days, was a Model Competent Authority Agreement on the Application of the Simplified and Streamlined Approach to Amount B of Pillar One. This agreement will provide a framework to enable jurisdictions to comply with what’s expected to be the final format of the rule of the Pillar One and Pillar Two agreements.

However, progress has slowed right down since October 2021 when 135 jurisdictions announced that they were accepting the two-pillar solution. With tax, the devil is in the detail and there is a lot of detail and devil to work through.

I think the other thing that should be kept in mind is that the US Presidential and Congressional elections happening in November will determine how much further progress will happen. As previously noted, the likes of Meta and Alphabet are none too keen on what’s proposed here and their lobbyists have the ears of plenty within Congress. We’ll just have to wait and see. But in the meantime, the deal seems to be inching forward.

“The time has arrived for a capital gains tax”

Last week I covered the report from Victoria University of Wellington about comparing tax rates between New Zealanders and taxpayers in nine other jurisdictions. This week things got spicier than I would expect in this sort of debate after the CEO of ANZ Bank Antonia Watson said in the course of her RNZ interview with Guyon Espiner “the time has arrived for a capital gains tax.” This in turn provoked a strong response from both the Prime Minister and the Minister of Finance. I found this a little surprising. I would have thought they’d just let Ms Watson make her comments and move on, but it certainly adds to the headlines.

CGT the most likely option

Following on from Antonia Watson’s remarks, I spoke to RNZ’s The Panel on Wednesday evening about the question of a capital gains tax. Put on the spot I said I could see it happening. To expand on my answer, it seems to me that a CGT is the most likely option if we do expand the tax base, because CGTs are common in other jurisdictions and the concepts are broadly well understood. And as Antonia Watson also noted, wealth taxes on unrealised gains are deeply unpopular with those that would be affected.

The interview with Antonia Watson is well worth listening to. One of the things I found quite interesting was that a couple of times she mentioned the impact of adverse weather effects. This wasn’t anything to do with tax, but she was explaining that our vulnerability to such events was a factor in why we have higher interest rates than Australia.

This circles back to the point that I made last week and again on The Panel, that the discussion around the question of capital gains tax or expanding the taxation of capital base is really around the question of how do we pay for the forthcoming costs of climate change and an ageing population? Are we raising enough tax revenue right now? If not, what are the options on the table?

What does Inland Revenue think?

Inland Revenue currently have their proposed long-term insights briefing for next year out for consultation. Susan Edmunds of RNZ picked up on this in a story on Thursday. The consultation finishes Friday 4th October, and I really do recommend reading and submitting on it.

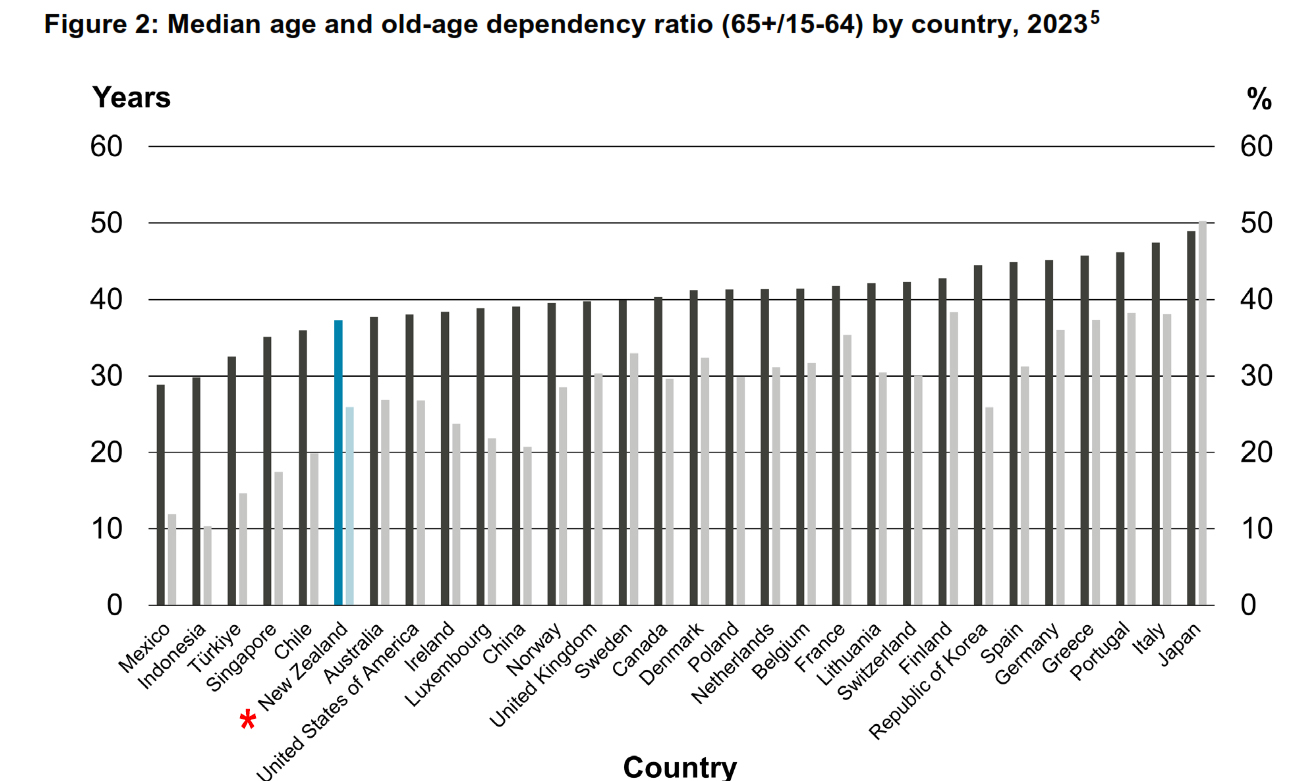

On the question of the forthcoming actual fiscal pressures, Dominick Stephens, the chief economic adviser for the New Zealand Treasury (and former chief economist for Westpac), delivered a speech on Wednesday titled Longevity and the Public Purse, which I’d recommend reading. It includes plenty of graphs illustrating the difficulty that we are facing. Our population is ageing, which is well known and the median old age dependency ratio is rising, although as the speech notes thanks to strong population growth it’s not as bad as other jurisdictions which means we are at the lower end of that range.

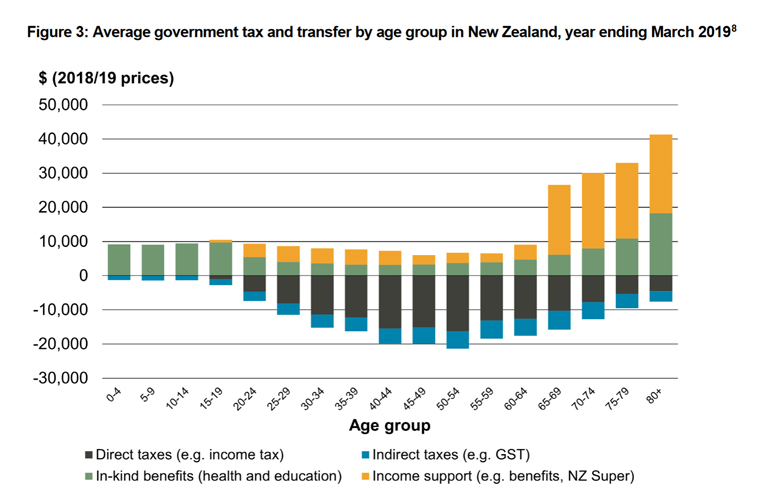

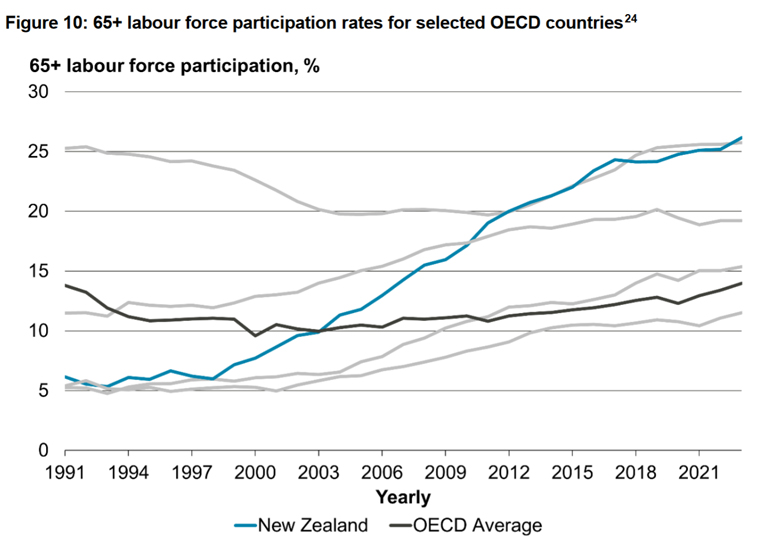

There’s a particularly telling graph about the average government tax and transfer by age group in New Zealand, for the year ended 31 March 2019

As can be seen above for the 65 and over age groups the transfers from Government rise significantly. These are the age groups which is where the debate about sustainability arise, as Dominick Stephens comments:

“Since 2006, the Treasury’s Long-term Fiscal Statements have repeated the message that our fiscal settings are not sustainable over the long run given the impact of population ageing.”

Over the period since 2006 some interesting developments have somewhat ameliorated the potential impact. Interest rates, for example, have been lower than were predicted in 2006, while population growth has been higher.

One of the more extraordinary developments since 2006 is labour force participation for 65 plus age groups has dramatically increased. Consequently, we’ve gone from being amongst the lower labour force participation rates to one of the highest.

All things being considered, there are difficult choices to be made and the question of whether more revenue is necessary is a question which isn’t going to go away.

“There is no silver bullet: none of the policy options we modelled in 2021 was large enough to stabilise debt on its own. This means that governments will need to likely draw on multiple expenditure and revenue changes to close the fiscal gap.

Some savings can be made from a greater preventative focus and reducing inefficiencies but making substantive savings is likely to require some tough choices around entitlements. This would have come with trade-offs, particularly for groups of the population who already face challenges accessing health services.”

Governments could also choose to raise additional revenue, in fact as Dominick remarked “successive increases in taxes over time would be required unless actions were also taken to manage demographic expenditure pressures.”

So tough fiscal choices ahead. I note in the comments on last week’s transcript some noted ‘well, wait a minute, why don’t we try and reduce expenditure?’ That’s certainly a driver for the current Government. But I think what Dominick Stephens and Treasury are saying, addressing the fiscal pressures will be a two-part process. We will need to both reduce costs and raise revenue. So, this debate over capital taxation isn’t going to go away soon and will continue. I expect I’ll be asked plenty more times to comment.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

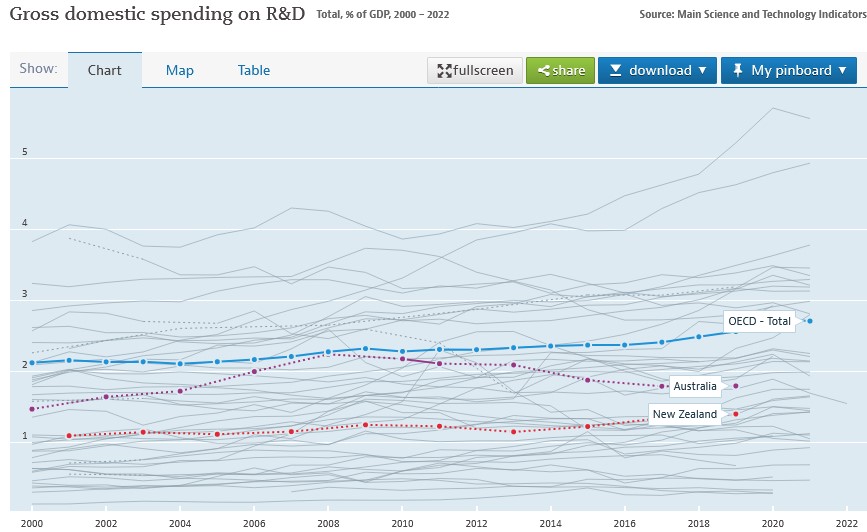

Inland Revenue has released a draft interpretation statement on the research and developments loss tax credits regime. This is a refundable tax credit available to eligible companies when they have a loss which has arisen from their eligible research and development expenditure.

The regime was introduced in 2016 to encourage business innovation and also to address New Zealand’s poor record of R&D expenditure. According to OECD data, in 2019 New Zealand’s spending on R&D was just 1.4% of GDP, well below the OECD average of 2.56% of GDP. Over the past 20 years research and development in spending in New Zealand has been a full percentage point of GDP below the OECD average.

So given that we also have a poor record of productivity, increasing R&D expenditure is seen as critical in improving productivity and ultimately the strength of the economy.

That’s the background behind the introduction of the loss tax credits regime. It’s intended to assist the cash flow of those companies carrying out research and development. Often in the early years, these companies are running at a loss. Hopefully once the R&D matures and bears fruit, they will then have profits resulting from the expenditure.

But funding cash flow in those early years is pretty difficult. So instead of the tax losses to be used against future profits, under the regime, companies can instead receive a payment. Note, only companies can receive this R&D tax loss credit payment. That’s because losses incurred by partnerships, limited partnerships, look-through companies and sole traders can already pass those losses through to the underlying owners anyway, who will often be able to offset them against their other income. Essentially, they are already able to benefit from the ability to cash-up losses. But companies can’t do that, hence the introduction of the regime.

The Inland Revenue draft interpretation statement looks at the background to scheme, summarises the rationale for scheme and how it operates. A couple of key points about the regime: you can drop in and out of it, you can opt to choose a payment in one year but not in another year. Once you have claimed a refund by cashing up your losses, the regime operates rather like an interest free loan. You’re essentially required to repay it and it’s generally treated as being repaid when the company starts paying tax, the R&D having borne fruit.

However, there are other circumstances where the credit may have to be repaid earlier when there is, in the terminology of the regime, a loss recovery event. Now, that typically will happen if there’s a disposal or transfer of the intangible property, core technology, intellectual property, etc., which is done for either less than market value or the amount sold is a non-assessable capital gain.

Another situation, and this is actually one where I’ve been involved, is where the company is no longer tax resident in New Zealand. Some very interesting issues arise in that case. Then there’s the worst-case scenario, where a company goes into liquidation although what exactly can be recovered at that point is a moot point. But that’s still a loss recovery event.

And then finally, and similar to our other rules around the carry forward of losses and imputation credits, a loss recovery may occur if there is a loss of the required shareholder continuity. In the case of the tax loss credit regime, the relevant shareholding percentage is 10%. In other words, there’s no breach if at least 10% of the voting interests of the company are held by the same group of persons throughout the relevant period.

In my view this is a very important regime for improving the future productivity of the country. The scale of the spending is going on is quite interesting to see. We can get an idea of this because the Inland Revenue as part of the budget produces what is called a tax expenditure statement.

Tax expenditure statements are a summary of the cost of a particular tax preferred regime, which, like, for example, this regime, has been introduced for specific policy reasons. The OECD collects data on tax expenditures to get a global picture of what spending is going on in tax preferred regimes.

In the case of the R&D loss tax credit, the estimated value of the expenditure for the year to 30th June 2023 is $362 million, a little bit below 1% of GDP. The estimated expenditure for the year to June 2022 was $473 million. And you can see a steady rise since the regime was introduced in 2016.

Of course, the real importance of this regime is whether it has produced a boost in total R&D spending within the economy. And then ultimately, does that lead to increased productivity. It’ll be interesting to measure these once the data flows through in due course.

So, an interesting regime and good to see Inland Revenue give some guidance on this. It contains a few hooks but it’s well worth looking at if you’re thinking about trying to make use of the scheme. And as I said, we will watch with interest to see how it bears fruit.

Shuffling forward on internationalPillar One and Pillar Two proposals.

Moving on, we’ve talked fairly regularly about the OECD’s global minimum tax deal and Pillar One and Pillar Two. Last week the G20 met in India and the Secretary General of the OECD reported to the meeting that, “A historic milestone was reached at the 15th Plenary Meeting of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (Inclusive Framework) on 11 July 2023, as 138 members of the Inclusive Framework approved an Outcome Statement on the Two-Pillar Solution.”

In summary, what’s happened is that they’ve developed a text to a multilateral convention which will allow jurisdictions to exercise a domestic taxing right over the residual profits of the largest, most profitable multinationals. That’s what they call Amount A of Pillar One, and that will apply to multinationals with revenues in excess of €20 billion and profitability above 10%. What will happen is the scope of that taxing right will be 25% of the profit in excess of 10% of revenues. This €20 billion revenue threshold will gradually be lowered to €10 billion after seven years, conditional on the successful implementation of Amount A.

There’s a proposed framework for the simplified reporting application of arm’s length principle, which is key to transfer pricing and for baseline marketing and distribution activities. That’s what referred to as Amount B of Pillar One.

There’s a Subject to Tax Rule, again with an implementation framework, and this is really for developing countries to update their bilateral tax treaties to tax intra group income. This is where such income is subject to lower tax in another jurisdiction, in other words say one country has a 20% corporation tax rate. But that multinational shifts charges to another part of the multinational group in a jurisdiction where those charges are only taxed at a lower rate. This Subject to Tax Rule gives the first country more taxing rights in that income. Developing countries are very keen on this particular point because they feel that this is where the current tax regime has been almost predatory on their tax base.

There will be a comprehensive action plan developed by the OECD to “Support the swift and coordinated implementation of the Two Pillar Solution, coordinating with regional and international organisations”

On the face of it, all pretty much good news. But it’s interesting to read the views of those people who specialise in this field and there still seems to be quite a bit of uncertainty about whether in fact this whole thing will come to fruit.

In the meantime, for example, you’ve got lobbying going on in the United States. And it appears now that the US has managed to secure a further delay in the implementation of the Pillar Two global minimum tax 15% until 2026, according to a report coming out of the United States.

Pillar Two is the key proposal, because it applies to companies with annual revenues in excess of €750 million. Apparently, the US Treasury Department has managed to negotiate a delay in the implementation of this. It has got people watching all around the world as to what’s going on. It also means that the in the background, digital services taxes, for example, could still be ready to be deployed or introduced by jurisdictions if they feel that Pillar Two isn’t making enough progress and they want to secure their revenues. [Under the agreement just announced countries have agreed to hold off imposing “newly enacted” digital services taxes until after 31st December 2024.]

Overall, it’s a bit of a shuffling: one step forward, maybe half a step sideways and a quarter of a step back. In other words, progress is slow, but it’s still inching the way forward. Ultimately, it comes down to watching what happens in the United States and the lobbying goes on. If there’s a change of President next year all bets will be off at that point, I would say.

Smith, banged to rights, again. But should Companies Office be in the gun?

And finally, this week, the murderer and escapee, Philip John Smith, who’s been in jail since 1995 apart from the brief time he escaped to Brazil has now been sentenced to further two years imprisonment on tax fraud charges.

He was convicted for dishonestly using documents intending to gain pecuniary advantage, firstly, a application under the Small Business Cashflow Scheme and then for filing 17 false GST returns and a false income tax return. in total the attempted fraud was just over $66,000 of which was actually paid $53,593. He’s also been ordered to pay full reparations on that amount.

What he did was between October 2019 and March 2020, he registered five companies with the Companies Office with shareholders and directors, who were friends, associates or third parties unknown to him. He then he set up and activated myIR accounts for each company.

But Inland Revenue was quite quickly onto him, it seems, because it apparently detected the fraud involving the Small Business Cashflow Scheme in June 2020 only a few months after it started operating in April. So good quick work by Inland Revenue.

But the case also raises the point which an associate I bumped into this week mentioned, and that’s the actions (or inaction) of the Companies Office in allowing those five companies to get set up. New Zealand scores highly for ease of business in establishing companies. Many times, whenever I’m talking to overseas people, they are remarkably impressed about how quick it is to set up a company in New Zealand.

The question arises if people setting up companies by going directly through the Companies Office website, is it a little bit too easy? Was an opportunity to pick up Smith’s attempted fraud missed at that point by Companies Office? We don’t know. Accountants and lawyers are subject to the current anti-money laundering legislation, so we need to pay attention to what’s going on with company registrations and we have to obtain proof of ID. But my understanding is this process is a little less rigorous when you go directly through the Companies Office.

So good work by Inland Revenue picking it up quickly and catching Smith, again. But maybe some questions should be asked as to whether he should ever have been able to get that far along the line and that Companies Office should have picked it up sooner.

And finally, congratulations to the Football Ferns for their magnificent win last night at the start of the FIFA Women’s World Cup. I was lucky enough to be at Eden Park, which is why I might sound a little hoarse today! It was fantastic to experience such a great occasion even if the final nine minutes seemed like an hour. Congratulations again to everyone involved. Football definitely was the winner on the night!

That’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The Tax Working Group report and capital gains tax

Inland Revenue’s business transformation

OECD’s international tax proposals

Transcript

This week, our final episode of the year takes a look back at the big tax stories of 2019 and also casts an eye over the tax events of the past decade.

The Tax Working Group report

The release of the Tax Working Group report and the Government’s decision not to follow through on the group’s recommendation for a general capital gains tax is by far and away the biggest tax story of the year. Although the Prime Minister stated that as long as she remains leader of the Labour Party, she will not be proposing a capital gains tax, the issue still excites and generates quite a degree of controversy. The reaction, for example, to a recent podcast in which I talked about Robin Oliver and Geof Nightingale’s session about why a capital gains tax didn’t happen at the recent Chartered Accountants Australia New Zealand Tax Conference is a good illustration of that.

As I’ve said many times beforehand, the frustrating thing for me about the aftermath of the Tax Working Group is that the debate around a capital gains tax completely drowned out all the other good work the group undertook. Some very interesting matters were raised and discussed. The tax system was found to be in generally good health, but there were issues. Pressures are building around the demographics and the funding of New Zealand Superannuation and rising health care costs for our ageing population.

On the other hand, the Government’s books are pretty solid and there is no immediate requirement to be raising revenue and expanding the tax base to pay for those additional costs. So, a capital gains tax is not something that’s going to be immediately necessary. But what the group did point out was those pressures are not that far off and we need at some stage to consider how the tax base will respond to that.

The other thing I thought was very interesting and I’ve talked about it before, is we started to see some movement on the question of environmental taxation. The TWG said we could do a lot more in this space. But also, and certainly this was Sir Michael Cullen’s recommendation initially, much of any changes that happened in this environmental taxation space should be in terms of recycling the funds through to enable the transition to a lower carbon emission economy. And that is something which is much more immediate and doesn’t require a capital gains tax. We should really be spending more time debating how we will implement these taxes and in which way we will allocate the funds that are raised.

Inland Revenue

The second large story for the year was Inland Revenue’s Business Transformation and in particular its Release Three, which happened in April. This is when it said, right, we are going to do auto-calculations for all taxpayers. And instead of them having to use a tax intermediary, Inland Revenue will automatically calculate the unders and overs for the year and issue appropriate refunds or demands as required.

This is a hugely ambitious project. About 2.9 million automatic assessments were processed resulting in approximately $572 million dollars of refunds being paid to taxpayers. But it threw up quite a lot of controversy. Probably in hindsight Inland Revenue was too ambitious in what they tried to do. They were bedding in the new tax system which for example involved transferring something like nineteen point seven million records into the new START (Simplified Tax and Revenue Technology) system.

Two key points emerged from the switch. Firstly, somehow over a period of time, 1.5 million people had managed to get their prescribed investor rate wrong. So those who had underpaid were expected to pay up. But those who had overpaid on average about 40 dollars each weren’t going to get a refund.

Now, as it transpires, political pressure and the howls of outrage from the public means that work is in progress to correct this issue. Currently the Finance and Expenditure Committee is looking at a measure which will deal with the question of the overpayments not presently being able to be refunded. That’s a good outcome coming from that pressure.

We don’t need no education?

What that issue shows to me though, is something that’s been taken for granted across the system. Not just this year, but for the past decade and probably even longer. And that is a dangerous assumption – that taxpayers know how the system operates and will always act in their own best interests because they are always across what’s happening their prescribed investor rate, their PAYE codes. That’s clearly not true. And it’s something Inland Revenue and tax professionals will have to deal with going forward.

Looking ahead to what’s going to be happening over the next three or four years, I think it’s probably one of Inland Revenue’s greatest priorities to introduce an educational process to ensure people are kept up to date about what happens with their KiwiSaver and PAYE.

The other part of the fallout from Release 3 as it was called, was that Inland Revenue basically did enormous damage to its relationship with tax agents. We as a group were pretty much left out in the cold about how to manage the transition to the new tax system. As a result, our experience in using the phones when interacting with Inland Revenue was uniformly very poor. And the survey I talked about last week with Chris Cunniffe of Tax Management New Zealand shows how dissatisfied tax agents have become with Inland Revenue’s performance.

Now credit to the Commissioner of Inland Revenue Naomi Ferguson, she’s acknowledged this. And we now know that going forward, Inland Revenue will not be making auto calculations for any taxpayer who is linked to a tax agent, and is overhauling its procedures around contacting clients of tax agents directly.

This is very much a sore point. 72% of tax agents had clients approached directly by Inland Revenue. And one of the interesting points about that was a significant proportion of them were approached by Inland Revenue in relation to the Accounting Income Method AIM, which Inland Revenue has been promoting as a simpler means of paying provisional tax.

At present only two thousand or so people have taken up AIM. And the reason is they’ve done that – despite Inland Revenue’s huge push – is that we as tax agents feel that it isn’t right for many of our smaller clients’ businesses – that it requires too much information and is rather inflexible in its approach. So that’s something which is probably going to change. I know Inland Revenue is working on that.

Overall, I think this huge transformation can be regarded as a qualified success. There are issues, as I’ve just said, around how Inland Revenue’s relationship with tax agents deteriorated. At the same time this is a reflection of how open our tax policy process is. We were able to get to Inland Revenue and say, “Hey, this is not working, and you need to do something about it”. And through various sources – including also the Revenue Minister, Stuart Nash, getting his ears bent by many tax agents and accounting bodies – change is happening. And that’s actually how the system should operate. So that’s a sort of reflection of the good and the bad of how our tax system works.

Meanwhile over at the OECD…

The third story, and again, this is another one that’s been running for quite some time with huge implications, are the ongoing international developments that we’re seeing in tax now. There are two parts to this. The first is what we’re seeing right now, the impact of the Automatic Exchange of Information under The Common Reporting Standard. This is where the tax authorities around the world swap information about taxpayers’ offshore financial holdings. There’s a colossal amount of data being swapped, and it really is surprising how unaware people are about just how much data is being swapped by tax agencies. Inland Revenue has now received over the two releases made to date under CRS, one point five million account records of New Zealanders who have overseas financial accounts. It’s presently working its way through that data and starting to ask questions.

Separate from that are the developments by the OECD in international tax and how we actually calculate a multinational’s income and allocate it to various jurisdictions. The previous permanent establishment regime built around a bricks and mortar approach no longer operates in the digital economy and through initiatives such as BEPS – Base Erosion and Profit Shifting -the OECD has been working on a replacement.

And this latest development is called the Global Anti-Base Erosion Proposal or “GloBE”. And this is proposing nothing less than a minimum tax rate for multinationals. This is a huge initiative and the OECD is hoping agreement can be reached among the 135 jurisdictions involved by the end of 2020.

How the GFC changed international tax

And that leads on to what has been happening over the past decade. Back in 2010, the OECD was starting to look at the implications for tax jurisdictions of international tax planning in the wake of the global financial crisis, which in 2008 had pretty much smashed to bits the budget balances of most jurisdictions around the world.

All around the world, countries tax take took a huge hit in the wake of the GFC. And countries then started looking very closely at where all the money was going and the scale of tax avoidance, and in some cases outright tax evasion, became ever more apparent. And so, this is the most important tax story over the past decade because it is transforming the way international tax operates.

You can run but you can’t hide…

And the implications for our tax base have been twofold. One, as a result of the global financial crisis and the initiatives that the OECD started, we now have Automatic Exchange of Information and the Common Reporting Standard and as I mentioned a minute ago, vast amounts of information sharing. We are also seeing moves to determine how multinationals will be taxed and that will not only affect how we tax multinationals, but also how our multinationals are taxed. Fonterra is the one that’s most often mentioned in this regard.

But it was the Americans that kicked this all off in 2010 with the Foreign Account Tax Compliance Act. What FATCA did was it required other jurisdictions to report to the US Internal Revenue Service – the IRS – details of American citizens who held bank accounts in their jurisdictions.

FATCA was the blueprint for what we have now CRS and Automatic Exchange of Information.

American exceptionalism

But there was one other thing that the Americans also did which is still playing out. The Americans are not part of the CRS initiative. In effect they said, “Well, we’ve got FATCA. we don’t need to be part of this.”

And American unilateralism is a continuing issue for the global tax base, because in the wake of the OECD proposal for the Global Anti-Base Erosion Proposal, the American Treasury Secretary just last week said, “Well, actually, we might not join that. Instead, we’ll just rather keep going with our old international tax rules”. The suspicion is that’s because the digital giants are putting pressure on the Treasury Secretary and the American government. So, a decade ago, America took unilateral action to introduce FATCA, which then led to the CRS. And now a decade on, it is throwing a large amount of grit into attempts to reform the taxation of multinationals.

A tax groundhog day

Here in New Zealand, back in 2010, Peter Dunne was the Revenue Minister, the Canadian Robert Russell was Commissioner Inland Revenue. The top income tax rate was 38% and the threshold at which it kicked in had just been increased to $70,000. GST was then 12.5% and the registration threshold had also just recently increased to $60,000.

Now those thresholds haven’t been increased since then. I think one of our faults in our system is we do not review the tax thresholds regularly enough and it causes distortions. And then suddenly politicians are making grandiose claims about massive tax cuts, which are nothing more than inflation led adjustments.

But in a real case of Groundhog Day, back in January 2010, the Victoria University of Wellington Tax Working Group, issued its report. The group (which included recent podcast guest and member of the latest Tax Working Group Geof Nightingale) shied away from recommending a capital gains tax. But it was in favour of increasing the amount of taxation from property, particularly in the form of a low rate land tax. And it also wanted to see more taxation of residential rental properties, suggesting they could be taxed in a similar manner to the fair dividend rate and foreign investment fund regime. So, there you have it, ten years ago, we were also talking about capital gains and the taxation of investment property.

The other thing that was raised by the Bob Buckle led group in 2010 was a recommendation for “a comprehensive review of welfare policy and how it interacts with the tax system with an objective being to reduce high effective marginal tax rates”. Both the Welfare Expert Advisory Group, which reported earlier this year, and the TWG commented on this situation. And I suspect that in another 10 years we will still be talking about this issue. It doesn’t go away, even if governments are unwilling to deal with some of the political consequences of action.

Well, that’s it for the Week in Tax for this year. I’d like to thank all our listeners and my guests throughout the year. I’d also like to thank David Chaston and Gareth Vaughan at www.interest.co.nz for publishing these transcripts.

We’ll be back next decade on Friday, the 17th of January. Until next time. Meri Kirihimete me te Hape Nū Ia. Merry Christmas and a Happy New Year. Thank you.

Property developers and a still too common GST mistake

EU proposes sharing credit card data to counter tax fraud

OECD proposes minimum global tax rate as part of BEPS initiative

Transcript

This week, a common and often very expensive GST mistake. The European Union ramps up its anti-fraud fight with a massive data sharing initiative, and the OECD suggests a global minimum tax.

Property developers provide a rich source of work for tax advisers and for Inland Revenue. That is because of the importance of property to the economy as a whole, but also in that they are often remarkably careless about the tax consequences of a transaction. This is probably a character flaw in that a developer sees an opportunity and knows they need to move quickly to maximise the opportunity. They therefore often go charging into a project without having someone on hand sweeping up the bits and pieces to make sure that all the i’s are dotted, and t’s are crossed.

In my experience, a key distinction between developers who fail and those who are successful is often the successful ones make sure that they have a team around them that does look after all the bits and pieces and the necessary legal frame, legal and tax frameworks to ensure the projects go ahead.

How this often manifests itself is that a developer might come across a residential property which is ripe for development and will make a bid for the property and purchase it. This is where the very common tax problem may emerge if the developers aren’t careful. If the developer purchases the property in the wrong entity, either personally or in a company or a trust which is actually used for development purposes.

At some point down the track, the developer’s lawyer or the accountant might say that property shouldn’t be in that entity and we need to get it into the proper development company. The developer often responds “Well, just deal with it. Get it into the appropriate entity”. And what will happen more frequently than it should happen is that a second transfer is made from the developer or the wrong entity to the correct entity.

And then the new entity goes and claims a GST input tax credit. For example, a residential property worth say $575,000 residential property was bought and was then transferred at a later date to the correct development company, which tries to claim an input tax credit of $75,000. Inland Revenue will turn it down.

The reason why it would turn it down is a provision in the GST Act, section 3A(3)(a). Now this provision has been in place since October 2000 and it is quite astonishing that 19 years on this issue keeps arising. Why?

What this provision exists to do is to stop people buying a property when no GST was paid. For example, a residential property bought from someone who’s not GST registered, holding it and then selling it at an inflated price to a GST registered entity, which then claims the input tax credit. This was something that was going on and was eventually put a stop to by the introduction of this provision in October 2000.

And the way it works is simply to say that if the transaction involves a sale between associated parties, the amount of the GST that can be claimed by the recipient party, the developing company in this case, is limited to the amount of GST paid by the original purchaser. So, if the purchaser buys from a non-GST registered person a residential property and then on sells it to a GST registered person no GST input tax can be claimed on the purchase because no GST was paid by the original purchaser of the property.

Now this is, as I said, a very common mistake I keep encountering. It’s a reminder to all people involved in the property industry to be careful when buying property to make sure that you have the correct entity settle on the transaction with all the necessary paperwork in place. Too often developers are keen to get something done and then buy in the wrong entity just to get the deal done. And unwinding that transaction is either impossible or proves very expensive. So that’s a word to the wise. But I still find it astonishing that this is an issue I’ve been dealing with repeatedly for 19 years.

A credit card trap

Moving on it’s been a busy week in the international tax world. I’ve spoken in past podcasts about the international efforts to address tax evasion and fraud. And this week, the European Union announced an initiative to counter e-commerce VAT(GST) fraud, which is estimated to be about costing 5 billion euros a year in the European Union.

From January 2024, credit card and direct debit providers will be obliged to provide member state tax authorities with data about certain payment details from cross-border sales. The anti-fraud Eurofisc Network will then analyse this data for potential fraud. This is another part of the massive information sharing programmes which are now common to international tax such as FATCA and the Common Reporting Standards on Automatic Exchange of Information.

Inland Revenue has been operating something similar to this for some time. The most notorious example I encountered was a family here had still kept a credit card issued by a UK bank. The mother wanted to come out and visit them and have a holiday in New Zealand. So, what she did was she put money into the credit card in the UK and they then used it for the only time to hire a camper van.

Inland Revenue found the transaction and knew that this was a credit card transaction that was made by a New Zealand tax resident. It issued a “Please explain” letter. And that turned out to be a very costly matter because in fact the son had made a pension transfer which got picked up and tax paid.

What’s notable is that Inland Revenue’s older computer system was able to track and find that credit card transaction. But following Business Transformation what will Inland Revenue’s computers be capable of tracking? It will be interesting to see. But the warning is that if you use a credit card issued by an overseas bank in New Zealand, Inland Revenue will come asking questions.

Tackling tax aribtrage

And finally, another very significant development in overseas tax. This is part of the ongoing work of the OECD/G20 Base Erosion and Profit Shifting initiative (BEPS). The OECD secretariat last Friday issued a discussion document on what’s termed the Global Anti Base Erosion proposal under Pillar Two.

I spoke on a previous podcast about the Pillar One initiative. The references to pillars, by the way, is because these proposals represent significant changes to the international tax architecture, hence the reference to pillars.

“seeks to comprehensively address the remaining BEPS challenges by ensuring that the profits internationally operating businesses are subject to a minimum rate of tax. A minimum tax rate on all income reduces the incentive for taxpayers to engage in profit shifting and establishes a floor for tax competition amongst jurisdictions.”

The press release goes on to note that

“global action is needed to stop a harmful race to the bottom on corporate taxes, which risks shifting the burden of taxes onto less mobile bases and actually may pose a particular risk for developing countries with small economies.”

And this has been something that’s been brewing for a long time now. The way that international multinationals have been using tax competition, encouraging countries to cut their tax rates and also looking to minimise their tax bills through shifting profits into low tax jurisdictions. The OECD proposals are a huge step forward and there’s a lot more to consider.

Things are now happening very rapidly in this space. The timeline for submissions on this particular Pillar 2 proposal is Monday 2nd December. There will be a public consultation meeting the following Monday 9th December in France. And the G20 is saying it wants a solution on the whole matter delivered by the end of 2020. So, stay tuned for what is a remarkably fast changing environment.

Well, that’s it for The Week in Tax. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Please send me your feedback and tell your friends and clients. And until next time have a great week. Ka kite āno.

The Week in Tax – back to normal after the Government’s decision on TWG report?

International tax pressure is building to create a Digital Services Tax because OECD’s BEPS initiative is growing consensus.

Why you shouldn’t be spending any refund from Inland Revenue that turns up unexpectedly. Unexplained credit balances sometimes are paid to prevent interest payments to Inland Revenue and these are getting refunded!

Expect the report from Welfare Expert Advisory Group soon. They consider the interaction between tax and social assistance.