Inland Revenue regularly releases Technical Decision Summaries (TDS). These are summaries from its Adjudication Unit in relation to dispute cases of interest between Inland Revenue and taxpayers. These give a good indication of Inland Revenue thinking around particular topics and how it might react to a transaction.

TDS 22/21 released last week is particularly interesting. It involves a two-lot subdivision carried out on a property by a taxpayer. He had initially purchased the property when working offshore for the purpose of renovating and extending it to live in with their extended family. Once the property was purchased, the extended family moved into the dwelling and the taxpayer joined them later on his return to New Zealand.

He then started planning to extend the property, but it emerged that there were problems with drainage and asbestos. Instead, it was suggested that the taxpayer should subdivide the property into two lots, constructing a new dwelling on each lot. And that’s what happened, during which time he was working overseas and visiting intermittently. Once one of the new properties was constructed, he occupied it for eight months. Shortly after the subdivision was completed one property was sold and the taxpayer and his extended family continued to live in the other property for a further five years.

Inland Revenue argued that the taxpayer had entered into an undertaking or scheme with the dominant purpose of making a profit under section CB 3 of the Income Tax Act. This provision is outside the normal land tax provisions, which is slightly unusual. Inland Revenue also ran the argument that the property was acquired for the purpose of intentionally disposing of it under CB 6, which is within the land taxing provisions. The question arose whether there was relief available because it was a main home. And finally, Inland Revenue also raised the question whether the sale of the subdivided lot and the property was subject to GST.

It seems part of the issue here may have been Inland Revenue just didn’t believe what they were being told. The Technical Decision Summary reasons for the decision opens with a reminder that the onus of proof is on the taxpayer to prove that an assessment is wrong, why it is wrong and by how much it is wrong.

This case turned out to have a good outcome for the taxpayer, because the Adjudication Unit ruled that the taxpayer did not enter into an undertaking or scheme for the dominant purpose of making a profit. Therefore, the gain wasn’t taxable under section CB 3. The Adjudication Unit ruled the taxpayer acquired the property for the sole purpose and with the sole intention of creating a home for themselves and their extended family. Therefore, the sale of the second lot was not taxable under section CB 6. It followed that as the property had been occupied mainly as residential land prior to subdivision, an exclusion applied. Finally, the taxpayer did not carry out a taxable activity for the purposes of the Goods and Services Tax Act, so no GST applied to the transaction.

The taxpayer won on all points. But there are several interesting points here. First is that Inland Revenue even took the case and the arguments it ran. This transaction appears to have happened before the Bright-line test was introduced, the TDS isn’t clear about the timing. The attempt to apply section CB 3 is unusual.

Secondly it highlights that Inland Revenue is paying attention to just about any property transaction and it’s prepared to use all provisions that are available to it. The case is a reminder to keep good records. I think the taxpayer struggled initially because not enough evidence was available, but they were eventually able to persuade the Adjudication Unit of what had happened.

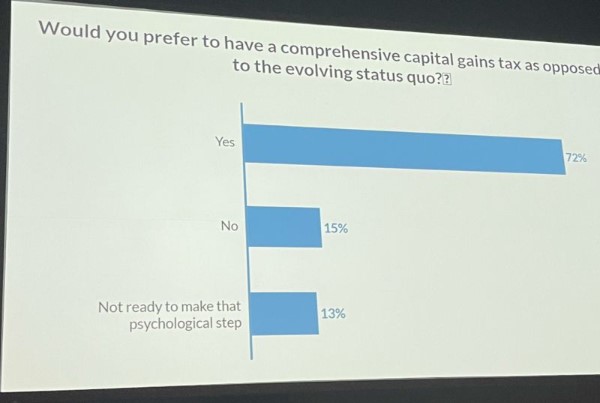

Tax professionals vote for a Capital Gains Tax

Moving on, the Technical Decision Summary does point to an ongoing strain within the tax system around the taxation of capital gains. In many jurisdictions that have capital gains taxes the issue we’ve just been discussing would be not on whether or not the transaction was taxable, which is an all-or-nothing proposition, but what proportion might be taxable.

It’s therefore interesting to see that at the Chartered Accountants of Australia and New Zealand’s National Tax Conference recently, a poll was conducted on the introduction of a capital comprehensive capital gains tax. The question was put would you prefer to have a comprehensive capital gains tax as proposed to the evolving status quo, which is actually a very generous description of the evolving state, still, to be frank.

(Photo by Richard McGill of PwC)

I wasn’t at the conference. I would have voted yes, although plenty of caveats around how we might go about it. It’s also tempting to respond, “Well, that is a lot of self-interest by accountants voting for such a measure.” I know that I’ve seen similar comments pointing out when I raise the issue that of course I would support it because I get extra work out of that. I find it ironic to be accused of acting out of self-interest when the flipside of it equally applies people who don’t want a capital gains tax would also be saying so out of self-interest. Self-interest arguments cut both ways, in my view.

I do happen to think that self-interest is a problem in the tax system around this whole area. It’s very difficult to see how parliamentarians owning substantial capital assets are going to ever going to vote for something which is directly against their own self-interests.

The feedback from the CAANZ conference was that it’s necessary to keep our tax system comprehensive and robust. And it would actually simplify quite a lot of measures that we see right now. For example, if you had a capital gains tax, you wouldn’t have to work through the bright line test and its various iterations. You could remove the foreign investment fund rules, another set of rules which are complex and not well understood. And you would also probably remove, or certainly reduce the need for measures such as restricting interest deductions. This has been introduced partly as a response to the absence of a capital gains tax.

In my view, there’s a lot of distortions in the tax system because we don’t tax capital gains, and we are seeing more and more of that. At last year’s International Fiscal Association’s annual conference many of the issues we were debating really revolved around the strains on the edges of the tax system produced by not taxing capital gains.

A CGT is not going to be popular with politicians or for those who would be affected. But the rest of the world manages these strains. So, to pretend that we can get by without a CGT and continue the current incoherent approach to taxing capital gains, is a position that just simply isn’t sustainable in the long term.

Updates on global tax coordination

Now, moving on, in international tax news the OECD released its latest corporate tax statistics. There’s a lot to consider here which I’ll discuss next week.

The OECD also released data relating to the latest Mutual Agreement Procedure statistics covering 127 jurisdictions and practically all the mutual assistance cases worldwide. These Mutual Agreement Procedure cases arise when two or more tax jurisdictions want to resolve the tax treatment of a transaction or entity where each jurisdiction thinks they have priority. Transfer pricing issues are often involved.

According to the OECD, approximately 13% more Mutual Agreement Procedure cases were closed in 2021 than in 2020. But fewer new cases started this year, which is a small, unusual trend given the internationalisation of the global economy. But these Mutual Agreement Procedure cases do take some time to resolve, on average, about the 32 months for transfer pricing cases and 21 months for other cases.

But amidst all this, there’s some good news, including an award for Inland Revenue which together with Ireland was awarded the prize for the most effective caseload management. The most improved jurisdiction was Germany, which closed an additional 144 cases with positive outcomes – that is, the matter was fully resolved.

These awards seem a bit of fun, but actually it’s a pretty important matter because with the Base Erosion and Profit Shifting and the hopefully soon introduction of the Two-Pillar international tax agreement, the role of Mutual Agreement Procedures in resolving disputes is going to be important. It’s encouraging to see jurisdictions are making progress and cooperating better

Paying tax and the right to vote

And finally this week, the Make it 16 win in the Supreme Court over the potential voting rights of under 18 caused quite a stir. David Seymour of ACT jumped in with a rather ill thought out comment “We don’t want 120,000 more voters who pay no tax voting for lots more spending.”

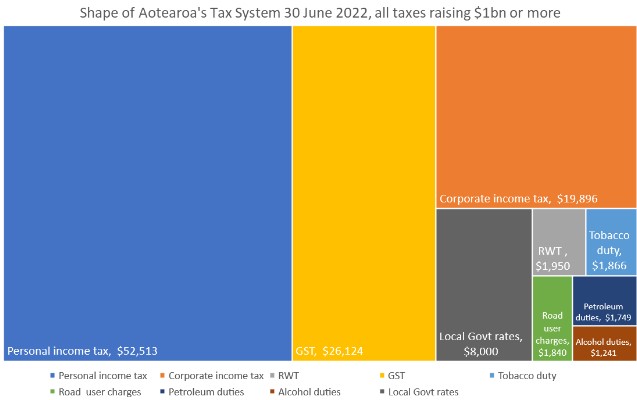

From the first time a child uses their pocket money to buy an ice cream and dairy, they’re paying tax. It’s called GST, which at over $26 billion is a quarter of the Government’s tax revenue. And as I pointed out on Twitter, lots and lots and lots of under-18s pay GST.

(The total of local government rates is an estimate. It appears the true figure is just over $7.3 billion)

The Make It 16 group made an Official Information Act request to Inland Revenue about how much tax 16- and 17-year-olds pay. And according to Inland Revenue over 94,600 16 -and 17-year olds paid a total of $82 million in income tax during the year ended 31 March 2022. That’s not an insubstantial amount of money (and doesn’t take into consideration the GST they also paid).

Given that 16 is the age of consent and 16 year-olds may drive, I don’t see much logic in saying that’s too young to vote. The kids are all right in my book.

Until next time kia pai te wiki, have a great week!

Last week Inland Revenue issued a press release warning real estate agents that this was an area that its analysis “suggests real estate salespeople/agents commonly claim a high level of expenses relative to their income. Inland Revenue believes the issue is widespread and we must act. People are claiming private expenditure, but not keeping logbooks or other business records to support the claim.”

The release goes on to warn that if someone has over-claimed expenses in Inland Revenue’s view, “they will receive a letter from us requesting they prove the expenses claimed.”

Now, this is a little bit unusual from Inland Revenue because we haven’t heard anything in the grapevine that this was something they were looking at. But it is not entirely surprising because one thing that emerged from hearing the Commissioner of Inland Revenue speak at the excellent Accountants and Tax Agents Institute of New Zealand conference is that Inland Revenue has great faith in its Business Transformation systems. These give it the ability to analyse data and identify areas where it believes income is either being under declared or in this case, taxpayers are, shall we say, being overly generous in their calculation of the deduction available.

Although, as I mentioned, we haven’t previously had an indication Inland Revenue viewed this as an issue, it’s apparent from what they’ve said here, that they’ve done enough preliminary work to identify that expenses being claimed by real estate agents seem high relative to income.

In one way I think this is a positive development in that Inland Revenue by warning people what it can do, can clear out some of the chaff.

On the other hand, there’s a lack of specific detail in this press release which concerns me. It’s “We think there’s an issue, but we haven’t actually specified what particularly is concerning us”. And simply to say that people claim a high level of expenses relative to their income is to assume that that expenses automatically should follow income. It could well be that there is a fair amount of baseline expenditure that people would incur in this business, running around making phone calls, driving to see clients and the like sometimes without actually a great deal of success, as the real estate sector is largely commission only based.

And so one of the things that taxpayers perhaps should consider is the implications of Inland Revenue’s capability to do a great deal of analysis. One thing Inland Revenue could do is to start saying, “Well, here is a standard deduction. You can claim X amount which to we’re going to accept as deductible without the need to keep very detailed records because our indication is that is likely to be the level of expenditure you would incur in your business.”

Now, Inland Revenue will come straight back and say they don’t want to do that because people will abuse that. But on the other hand, you’ve got to wonder the benefit of the current approach when you consider the time and energy put in by people preparing their tax returns and also the effort Inland Revenue then spends investigating what may well turn out to be an entirely legitimate expenditure. Maybe just simplifying matters all around would be more efficient.

It could be yes, there could be some seepage around the edges under a different approach and Inland Revenue doesn’t get as much as it could do if the rules were applied correctly. But applying a so-called standard deductions approach deals with an issue in the tax system, in that compliance is particularly onerous for smaller businesses. The rules are written around the expectation that people have a good understanding of the law and have the systems to manage their accounting and recording income and expenditure. And with the advent of online accounting systems such as Xero and MYOB that’s largely true.

But not everyone wants or needs to spend money on accountants. And I have felt for some time that adopting a different approach to what we call micro businesses, that are businesses with a turnover of say, less than $100,000, dollars would actually benefit everyone. Make it easier to comply and encourage more people to comply.

Anyway, we’ll watch with interest to see how this plays out with Inland Revenue. As I said, I’d like to see some more specific examples of the abuse that they are clearly warning against. But until some cases hit the courts or Inland Revenue releases some more information on the matter, we’ll just have to wait and see. In the meantime, it’s a good warning for anyone involved in business that you have to keep accurate records of your business expenditure.

The IMF wants tax action on overheated housing market

Moving on, the IMF, the International Monetary Fund, has waded into the debate over housing by recommending the Government should introduce a stamp duty or a more comprehensive capital gains tax to help deal with the overheated property market.

This is part of a routine check on the New Zealand economy, what’s called the Article IV discussions. These happen periodically when IMF staff come down here, talk to Treasury and other officials and draw their own conclusions on the state of the New Zealand economy and areas for improvement.

The Government will not welcome the call for a capital gains tax or stamp duties. We haven’t had stamp duties in nearly 30 years now, but they are used a tool used elsewhere. They’ve fallen out of fashion here because they are regarded as economically inefficient taxes, and there are concerns that they increase costs for purchasers. So as a means of helping first home buyers, a stamp duty isn’t necessarily going to be a great approach according to theory.

But for those who’ve read Tax and Fairness, the book I co-wrote with Deborah Russell MP, you’ll know that in chapter four, we talked extensively about how the IMF is not the first organisation to have raised the need for a capital gains tax to deal with housing inflation. The OECD raised the idea way, way back at the start of the century in November 2000 and then again in 2011, and the IMF also made similar suggestions back in February 2016.

I was going to say it’s really quite remarkable how this issue keeps popping up, but actually it’s not because the issues around tax were identified decades ago but have not been addressed. And meantime, the pressure on the Government builds now that the housing market has accelerated again. And this week (Tuesday) the Government will announce some proposed disincentives for property investors to try and reduce demand in the sector together with some form of targeted incentives to encourage savings in other sectors.

Just a little note on this, way back in 2000 the OECD concluded there was substantial overinvesting in housing, maybe one and a half times greater than that of major OECD countries. Now, I imagine that number has actually become considerably worse. So, as I’ve said before, the capital gains tax debate is not going to go away.

And on that debate, this coming Thursday, March 25th, I’ll be on a panel alongside Geof Nightingale of PWC and the Tax Working Group and Paul Dunn of EY together with Craig Elliffe and Julie Cassidy from Auckland University. Our topic is “Taxation: the ticking time bomb of our generation. Four tax questions for 2021”. This is an event run by the New Zealand Centre for Law Business I have no doubt whatsoever we will be talking about the issue of capital taxation.

End of year prep

And finally, more on one specific issue which will require action before 31st of March, and that is the question of overdrawn shareholder current accounts.

Now, this happens when a director or a shareholder of a company takes out more in cash from the company during the year. This is traditionally treated as drawings. So, prior to year-end, we take a look to see what we can do. And most times we deal with this issue by either paying a dividend before year-end (a particularly important thing to do this year before tax rates increase on 1st April) or voting a shareholder employee’s salary.

But in some cases, that is not enough. And in those situations, a company is required to charge interest using the FBT prescribed rate of interest. Now this rate is regularly adjusted and generally reflects what’s going on elsewhere in the market. Until 30th June 2020, the rate was 5.26%. It was then reduced to 4.5%, the lowest rate I can recall. This is the rate that should apply from 1st July 2020 right through until 31st March 2021.

But from 1st April the rate increases to 5.77%, something that has slipped under the radar and possibly reflects Inland Revenue unease about the use of current accounts to get around higher tax rates. On the face of it a rate increase in this low interest economy seems anomalous.

But as I said, I think it reflects Inland Revenue concern about the use of an overdrawn current account to get around income being taxed at either 33%, or from 1st of April, 39%. In some other jurisdictions the amount of an overdrawn current account is treated as a dividend. Our rules treat only require charging of interest. So if you’ve got an overdrawn current account of $100,000 in Australia, that’s going to be taxed as income of $100,000. Here we apply the FBT prescribed rate of interest of 4.5% so the taxable income is just $4,500.

So you can see there is some form of incentive to make use of overdrawn current accounts. In fact Inland Revenue has started paying a lot more attention to this issue and this small but quite subtle and unnoticed rate increase in the prescribed rate of interest is probably a clue it is planning to take greater action on the matter.

Well, that’s it for today, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next week Ka kite ano!

A look ahead at the expected big tax themes in the coming year.

The arguments for taxing property, a wealth tax, what might Joe Biden’s presidency mean for international environmental taxation and how will Inland Revenue respond.

Welcome to 2021. So what lies ahead in the tax world this year? Well, firstly, housing will remain an issue and I expect we will see steady calls for radical action on this front, including a demand for a capital gains tax. I actually think it’s gone beyond the point at which a CGT would have an impact.

In terms of tax measures, as I’ve said previously, restricting interest deductions including applying the existing thin capitalisation rules to investment properties might help to even the playing field between investors and first-time buyers, a group to which the Government appears to be paying particular attention.

Susan St. John has called for the Risk-Free Rate of Return (which is similar to the Foreign Investment Fund fair dividend rate rules) to apply to investment property. And her suggestion was recently echoed by Professor Craig Elliffe, who was a member of the Tax Working Group.

The Tax Working Group looked seriously at the question of applying a Risk-Free Rate of Return to investment property. It estimated the revenue from applying a rate of 3.5% would be approximately $1 billion in the first year and was expected to rise to $2 billion per annum within 10 years. The expectation would be that such a move would,

“tax a currently undertaxed asset class more adequately and act as a curb to burgeoning house prices. Westpac economist, Dominick Stephens calculates that a 10 per cent CGT would reduce house prices by nearly 11 per cent. It is unclear what effect the RFRM, but it should stem the increase. But it’s not clear what effect a Risk Free Rate of Return method would have, but it should stem the increase.”

Now, tied to the question of housing is the issue of wealth inequality, and I expect we will continue to see calls for a wealth tax. Over in the UK just before Christmas, their Wealth Tax Commission released a report recommending a one off wealth tax for the UK, which it estimated could raise about £260 billion over five years. What was particularly interesting about this commission is the depth of the research into the topic.

Quite apart from the final report, the Commission produced a series of other working papers on the design and operation of wealth taxes around the world. And these, in the commission’s own words,

“represents the largest repository of evidence on wealth taxes globally. To date, it comprises half a million words across more than 30 papers covering all aspects of wealth, tax design and both in principle and practice.”

Just to put that in context, I estimate the Tax Working Group’s consideration of wealth taxes amounted to perhaps 10,000 words in total. So we are looking at a very significant amount of research.

Now, one other thing to keep in mind about the British Wealth Tax Commission was that it called for a wealth tax, even though the United Kingdom has a capital gains tax and an inheritance tax. Instead, it recommended a thorough review of those existing taxes. The Commission also went for a one-off tax rather than an annual wealth tax, which is the common type of wealth tax currently and what the Greens propose. The Commission saw that there were quite a few practical issues around the operation and an ongoing wealth tax. These issues together with political pressure, has meant that the use of wealth taxes has declined throughout the OECD.

The Tax Working Group also concluded that an annual wealth tax would have enormous practical issues in implementation, which is why it did not recommend it.

But what the Wealth Tax Commission’s research makes clear is just how unique New Zealand’s approach to the taxation of capital is. It’s well known that New Zealand does not have a comprehensive capital gains tax, but that’s not entirely unique within the OECD. Switzerland, for one, does not have a capital gains tax.

Where New Zealand is unique, is that it does not have comprehensive taxation of capital in any form. Switzerland has a comprehensive wealth tax. In fact, the tax it raises from wealth taxes represents one per cent of GDP, which is the highest of any country with a wealth tax. Wealth tax revenue amounts to 4% of the Swiss tax take so it’s an important part of the Swiss tax system,

Wealth taxes in the OECD do not raise significant amounts of revenue and that’s one of the reasons they’ve been declining in use. The Wealth Tax Commission’s papers are well worth reading. A particularly interesting one is about the political economy of the abolition of wealth taxes in the OECD, which those who want to promote taxation changes would do well to read closely.

I think pressure will continue to mount on the Government on the taxation of wealth because of this ongoing anomalous position where we don’t tax capital on transfers by way of an inheritance tax or even a stamp duty, and not tax increases in value generally will feed into the debate around inequality.

And there’s an interesting point a client made to me on this topic. It’s been a long-standing New Zealand policy to attract high net worth individuals to come to New Zealand. Such immigrants may well qualify for a four-year tax holiday on their non-New Zealand investment income. These people being wealthier tend to have very diverse investment portfolios.

But as the client pointed out to me, it seems wrong that their investments would be taxed on their capital growth under the Foreign Investment Fund regime whereas property investors are not taxed on that growth at all. My client thought that was an anomaly that sooner or later would start to act as a disincentive for high-net-worth migrants to New Zealand. This may lead to growing political pressure to level the playing field, so to speak.

So anyway, the taxation of wealth, whether through a capital gains tax and/or a wealth tax or some other mechanism, is going to remain on the agenda.

A week before the British Wealth Tax Commission issued its report, our Government declared a climate change emergency, joining 32 other nations who have made such a declaration.

Now in my first podcast of last year, I said that the role of environmental taxes as one of the tools in the meeting our emissions targets will become ever more important. And that remains the case.

But we now have a new American president, and one of the first actions of President Biden after his inauguration was an executive order confirming the United States would re-join the 2015 Paris agreement. Now, several people have pointed out this may well act as an indirect trigger for the government to take further action on reducing emissions.

More than a few columns have pointed out that there is a discrepancy between the government’s declared intentions and the actual steps being taken to reduce emissions and meet our commitments under the Paris agreement. One estimate is that New Zealand exceeded its national share of consumption-based emissions by more than a factor of 6.5.

So this year I expect we should start to see some movement on taxing emissions more thoroughly and a place they might well start because the transport sector is the biggest source of emissions is to change the taxation of motor vehicles, maybe by following the UK’s example of applying FBT on the basis of emissions.

The government should also look at eliminating anomalies in the tax system, which effectively penalise low carbon activities such as employers paying FBT on providing free public transport. Another would be as a paper prepared for the NZTA suggested was maybe applying FBT to employer provided parking.

Biden’s inauguration could mean swifter resolution to the issue of international taxation. I think this is one where we will have to wait and see because there will be fierce lobbying in the US by the so-called GAFA – Google, Apple, Facebook and Amazon. I think progress will be made, but it will be slower than people expected.

And finally, the third trend I think we’ll see this year is Inland Revenue coming out from its rather inward-looking attitude in recent years as it completes the final stage of its controversial Business Transformation programme. With the immediate requirement to respond to the COVID pandemic now over, (please people remember to scan) Inland Revenue can get back to its more regular work.

Already before Christmas we started to see a number of new initiatives including one in relation to following up on the information Inland Revenue received under the Common Reporting Standards on the Automatic Exchange of Information.

Another is reviewing all transactions potentially within the bright-line test. You may recall that Inland Revenue fired out emails to tax agents advising “These clients appear to have made transactions within the bright-line test” which caused quite a stir. I expect we’ll see more work going into that space, which coming back to the start of the podcast ties into the taxation of property.

And finally, I think we’ll also see more activity going after the so-called cash economy. I think we’ll see Inland Revenue start following up on cash transactions, such as tradies offering a discount for cash.

So we’re going to have a busy year ahead, as always, and I will bring you the news as it develops. Next week, I’ll take a closer look at Inland Revenue, and its annual report which was released just before Christmas.

In the meantime, that’s it for today. I’m Terry Baucher and you can find my podcast on website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients until next week, Ka kite āno.

This is the last podcast for the year so we will be taking a look back over the main tax stories for 2020. It’s no surprise that the response to COVID-19 will feature very heavily but looking back, the thing that stands out is how rapidly events developed and then the sheer scale of what we were dealing with.

In the podcast on Friday 16th March, I suggested some actions Inland Revenue could take in response to coronavirus following a week in which first Italy then the UK and finally Australia announced special measures throwing around huge sums of money. By the following Friday we had the first COVID-19 support package including the first iteration of the wage and subsidy scheme.

From then on it was a frantic blur until late May with barely a week passing without one new measure after another. Most of those did what they were intended to do: get money into the economy and keep people employed. Some were more successful than others. The Business Finance Guarantee Scheme for example did not work as anticipated with only $176 million lent to 834 businesses by the end of August.

The Small Business Cashflow Scheme on the other hand was a huge success in getting money out to small businesses very quickly. Currently over $1.6 billion has been lent to close to 100,000 businesses and the Government is now working on making the scheme permanent.

Some of the tax measures that have been announced – such as increasing the provisional tax threshold to $5,000 or increasing the low value asset write off temporarily to $5,000 – are measures that probably would have happened sometime soon, possibly even this year it being an election year. What COVID-19 did was make the Government bring forward those measures and put them into effect much sooner than otherwise might have happened.

It’s also worth pointing out just how well the Ministry of Social Development and Inland Revenue handled the distribution of funds under the various wage subsidies. The Small Business Cashflow Scheme meant that the billions of dollars got very quickly to where it was needed and both organisations deserve credit for making that happen. However, it undoubtedly put Inland Revenue under considerable strain and we’ll talk about that a little later on.

The immediate legacy of the response to COVID-19 is of course the Government’s books being shot to bits. Interestingly the latest figures show the tax take has not fallen significantly and the deficit is more down to expenses increasing sharply such as the wage subsidies.

The impression is that the economy has come through the crisis in better shape than was anticipated way back in March.

For all that, the Government faces deficits for the foreseeable future so we had the somewhat unusual situation of it running an election campaign with a promise to increase the income tax rate to 39% for income over $180,000. The increase in the income tax rate to 39% is expected to yield about $550 million a year but I suspect we may find it yields more than that because the economy has been in better shape than expected so far.

Aside from the Opposition, Labour’s proposal also got criticised from various sectors saying that the response was inadequate given the scale of the problem. There was also criticism, and this is going to be a continuing theme, that the income tax increase primarily on labour and earnings was not really where tax changes were needed.

Notwithstanding those issues, there are a number of complicated flow-on effects from increasing the top income tax rate to 39% – such as resident withholding tax and fringe benefit tax. Then of course there are the significantly increased powers for Inland Revenue in respect to requesting information from trustees.

This is something which is going to give trustees and beneficiaries pause for thought before they get involved in aggressive tax planning. The Government has made it clear that if it sees such activity it will increase the trust tax rate to 39%, something which Inland Revenue recommended should be done.

So the immediate impact of COVID-19 and the Government’s response has been the major tax story of the year.

The second big tax story has been the ongoing capital taxation debate which is something I suspected might happen. Writing at the start of the year I suggested that although the Government had said in April last year it would not introduce a capital gains tax, that would not mean the end of the story.

And so it proved.

Throughout the year, particularly in the wake of COVID-19 and an unexpected housing price boom, there has been a string of stories looking at the question of taxing capital either in the form of a wealth tax as proposed by the Greens or more recently an extended bright line test.

In one recent article I suggested if the bright-line test is to be extended, a ten year timeline would be consistent with the other land taxing provisions in the Income Tax Act. (Unsurprisingly how that ten year timeline is measured can differ between the various provisions).

What Geof Nightingale from the Tax Working Group pointed out in the same article , was that it would be fairer to have a comprehensive capital gains tax at a rate of 33% rather than the muddled approach to capital taxation we have presently and the previously mentioned complexities of increasing the top rate to 39%.

So, I think we’re still going to see more on the debate around capital gains tax and taxing capital. This is in part because of the housing price boom but also because many of the journalists covering the story are relatively young. Despite having good jobs they’re struggling to get together deposits to purchase houses. Effectively, they have been priced out of the market and understandably they’re not happy about that.

But they are in a position to make quite some noise about it, so the Government will find this story isn’t going to go away. So, throughout 2021 and beyond there will be a steady stream of stories about what are we going to do about house prices and what role will tax have to play.

The final tax story of the year is the role of Inland Revenue; how it managed its response to COVID-19 and then going forward, how well is its Business Transformation programme really going?

As I mentioned previously Inland Revenue’s immediate response to COVID-19 deserves praise. It took action to help clients running into difficulties with payments of tax, including a number of measures which effectively wrote off interest on overdue tax where the taxpayer had been adversely affected by COVID-19. It administered the Small Business Cashflow Scheme very efficiently and it worked very closely with the Ministry of Social Development on the wage subsidy schemes. At its peak Inland Revenue was handling over 15,000 requests for verification from MSD each day in relation to the wage subsidy scheme.

At a tax conference during the year, I asked Inland Revenue representatives there whether they would have been able to manage all the additional demands that came on them because of COVID-19 without Business Transformation, and their response was that it had given them the additional capacity and flexibility to manage the demands put on them. In particular the upgrade of the computer systems meant they could actually physically cope with what was coming at them

So far so good, but as listeners will know, in recent weeks I’ve raised questions around what exactly has been going on with Inland Revenue in relation to its audit and investigation performance in view of the fact that hours spent on investigation had fallen by two thirds over the past five years from over 680,000 annually to just over 240,000. That led to an interesting response from Inland Revenue Deputy Commissioner Sharon Thompson on the matter.

That exchange caught the eye of Auckland barrister and ex Inland Revenue investigator Riaan Geldenhuys. What he pointed out was that Inland Revenue was actually under some strain in delivering Business Transformation even before COVID-19 hit.

Riaan noted that in the Minister of Revenue’s regular reports to Cabinet on the progress of Business Transformation in July 2019 then Minister of Revenue Stuart Nash had noted that there were strains emerging because of the unprecedented response to Inland Revenue’s rollout of automatic assessments for all people on PAYE.

Now as you might expect, COVID-19 has exacerbated those strains and in his July briefing to Cabinet this year the Minister of Revenue noted that because Inland Revenue had had to divert staff from audit and collection to maintain services “no new audit or debt collection cases will be opened and existing disputes will be managed as judiciously as possible.” The report then went on to note that “Inland Revenue’s ability to support customers is currently stretched to capacity.”

Now of course an unexpected event like COVID-19 will have some flow-on effects, but what has also emerged from these reports to the Cabinet is that the projected administrative savings that Inland Revenue promised the Government as part of the business plan for the Business Transformation programme have been completely wiped out.

The projection was that Inland Revenue would realise administrative savings for the period ending 30th June 2024 amounting to a total of $495 million. According to the latest report provided to Cabinet in July, none of those administrative savings are now expected to be realised[1] so that’s a $495 million dollar hit to Inland Revenue’s bottom line and effectively the Government’s by extension.

Earlier this year an academic article in the New Zealand Journal of Taxation Law and Policy[2] was critical of Inland Revenue’s Business Transformation programme. The author thought that Inland Revenue had prioritised staff reductions rather than strengthening its ability to improve collection of taxes, particularly in the area of the cash economy.

On top of these issues of cost overruns and poor audit performance, there’s a growing problem of strains in the relationship between Inland Revenue and tax agents. Tax agents are increasingly exasperated by Inland Revenue’s actions in directly contacting clients about various tax issues ostensibly in the name of better communication. More often than not these calls result in confusion and duplicated costs which are often not recoverable.

So, this combination of cost overruns, lower audit and investigation work and a strained relationship with a very significant group of stakeholders, is something which is going to need careful monitoring by the new Minister of Revenue David Parker. We will be watching with interest.

Well, that’s it for this year. Thank you to all my guests and to all my listeners and readers. I really appreciate your feedback and your patience in sticking with me throughout a tumultuous 2020. I suspect it will be well into 2021 before things settle back into what we might call normal.

Until then I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next year have a safe and enjoyable Christmas. Ka kite āno.

[1] “The re-planning of organisation design changes may have implications for Inland Revenue’s ability to realise the administrative savings. The savings have already been removed from outyear baseline funding so the challenge for Inland Revenue is to manage within a reduced funding level. These savings are part of the funding available for transformation. It is too early yet for Inland Revenue to say what the implications will be.” (Para 59)

GST is frequently touted as a simple tax, and I think that’s partly because there’s only one rate and it applies across the board on almost all goods and services consumed in New Zealand. But like any taxes, it has a number of hooks in it which frequently trip people up.

Some of these hooks shouldn’t be tripping people up because they’ve been known about for some period of time. But surprisingly, I still come across this particular issue time and again. And it’s really quite concerning that it still does happen.

The issue will almost invariably involve land. It’s where someone has purchased land from an individual and then decides that it’s perfect for a development activity or whatever, and then sells that across to a company or sometimes a trust which is registered for GST which then claims an input tax credit.

This is where things go off the rails. The issue is that the supply from the individual/another company who initially purchased the property to another party which is “associated” with it means that for GST purposes, the GST input tax claim that can be made is limited to the amount of GST paid by the first person.

Now, this provision, section 3A of the GST Act, has been in place since October 2000. It applies to transactions between “associated persons” which given the wide definition in the associated persons rules is very likely applicable when there are common shareholders/trustees/settlors.

What section 3A is designed to do is to stop someone buying a property then on selling it at an inflated price to an associated GST registered entity, which then picks up an increased input tax credit. And the rule basically says that the GST input tax is limited to the amount paid by the original purchaser. And since that purchaser often purchases it off a non-GST registered person, that amount is nil.

And I see this quite a bit. I’m surprised some lawyers and accountants haven’t really got across a measure which is now 20 years old.

The latest example I’m trying to describe is that the individual purchased the property, and then after advice from a lawyer – that for asset protection and business purposes – it would probably be better that the land be sold to a company to carry out the proposed development. That itself is not unreasonable advice. Problem was the lawyer overlooked the impact of GST and the client who is new to New Zealand didn’t get tax advice at the right time, which is another common mistake.

The company actually did get an input tax credit and refund of $450,000. You might well ask why did the Inland Revenue let a GST input tax claim of that amount go through? Fair question but it’s a complicated story.

Anyway, Inland Revenue then took a further look at it and then said, “Oh, no, you’re not entitled to that refund”. So now the client has to find $450,000 dollars and pay it back. They’re not best pleased which is understandable. And I think that is something that should provoke some fairly sharp questions between the client and their lawyer. But it is a common issue I keep seeing.

So, the golden advice here is get advice from your accountant and other advisors before you make the acquisition or get into the project. If you don’t, because you’re trying to save on professional fees, you might well find that trying to save two or three thousand dollars in advice has, like this particular client, just cost you $450,000. Get advice on any GST related transaction because GST has a lot more hooks to it than people realise.

I have a couple of other GST cases going on at the moment where people who said they were GST registered turned out to be not registered, or vice-versa and that has got lawyers at ten paces throwing writs at each other over whose client picks up the GST warranty.

NZ residents must report global tax income

Moving on, another common error I come across is people misunderstanding their income tax obligations where they have assets in more than one jurisdiction. I frequently encounter a position where a New Zealand tax resident also has property or other income source in the United Kingdom, Australia, wherever, and has been complying with that jurisdiction’s requirements to file a tax return.

This often happens involving assets in the UK. A person might have to file UK a tax return because they’ve got a rental property over there. But although they’ve complied with their UK obligations, they overlook the fact that as tax residents of New Zealand, their income is reportable taxable on a global basis. So they should be reporting the UK income here as well.

And that’s the bit that often gets forgotten about. Most people seem to be aware there’s a rule against double tax. And they seem to think that by filing a tax return in the country in which the property is situated, they have met their obligations and it’s only taxable in the country in which it’s situated. It’s not, it’s taxable worldwide.

Inland Revenue issued in July a very good Interpretation Statement 20/06 which sets out all the rules overseas rental properties. But I daresay this particular case won’t be the last time I’ll come encounter a situation where someone has reported income overseas, but not in New Zealand.

And it’s a good insight into always try and catch up regularly with your clients and take the opportunity to ask questions, because more often than not, if you don’t ask, you don’t find out. And then something happens after which everyone is going “Oops!” and no one is terribly happy about how that plays out.

Labour’s tax policies

And finally, last week, Labour announced their proposed income tax policy, increasing the top income tax rate to 39% for income in excess of $180,000. This has not been terribly well received, partly and very obviously from those who are likely to be affected. They’re not going to be happy about that. And that’s understandable. Who likes paying more tax? Let’s be frank about it.

But also, more importantly, leaving aside partisan issues such as Labour activists saying it’s too timid, the interesting issue to me is how other people have come out and said it really doesn’t do anything to address the issues of inequality and distortions in the tax system. It’s also been dismissed as just a drop in the ocean in terms of addressing deficits.

There’ve been two such articles in the past week that raised these issues. The first was from Jonathan Barratt a senior lecturer in taxation at Te Herenga Waka — Victoria University of Wellington. And he basically said that both Labour and National are really not doing anything to address questions of inequality. The tax base is too narrow, it benefits the wealthy and punishes the poor. And his key point was that neither major party seems to want to do anything about it.

I do have a view that the “Four legs good, two legs bad approach” to discussing taxation over the last 30 odd years hasn’t helped any constructive conversation in this matter. Also, property has become such an important asset for so many people where sometimes the untaxed growth in the value of the asset exceeds a person’s annual earnings, it’s therefore understandable people are reluctant to have that precious nest egg taxed.

Also coming out and having some fairly harsh, but fair, commentary on Labour’s tax policy was Geof Nightingale, of PWC, who’s been a previous guest of the podcast, but more importantly was a member of the last two tax working groups.

And he begins his article by calling it “Brief and predictable, but disappointing”. And he goes on to point out the 39% rate turns us back to the tax settings at the end of the 20th century when we last increased the top tax rate to 39% rate. The policy “makes the existing equity and efficiency distortions in our tax system worse and will have no significant impact on income or wealth inequality”.

Now, Geof was one of those who backed the introduction of comprehensive capital gains tax. What he’s pointed out here is that the increase in the tax rate to 39% is a progressive move but only in relation to employment and personal services income. It’s quite possible if you’ve got investment income, which is in a portfolio investment entity it’s taxed at 28% and it’s held in a trust it’s going be taxed at 33%.

I really do struggle to understand why Labour is not looking closely at the trust tax rate. It was known to be an issue the last time the top tax rate was 39%. But I suspect they may well come back to that if they get re-elected. There are anti avoidance measures in place, as Geof has said. But the whole point is that the zero percent rate on capital gains still applies and investment returns and capital gains because of the amount of money sloshing through the system now are likely to increase.

So, as he said, one solution is of course, a capital gains tax, which in his view and mine spreads the tax burden more equitably across the economy. And it could also allow lower personal tax rates. What’s often forgotten in the wake of what happened at the end of the Tax Working Group, was that lower tax rates were part of the whole package including capital gains tax. National of course will not do anything in that space. It’s saying it’s sticking to opposing capital gains tax and ruling out tax increases.

So Geof’s article was really quite swingeing in its criticism and fair enough in that regard. He concludes

“Here we are then, a government that wants a second term faced with a major fiscal crisis but backed into the dead end of a 20th century tax policy. Predictable but disappointing.”

Well, that’s it for this week. I’m Terry Baucher. And you can find his podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients. Hei konei ra!