The Organisation for Economic Co-operation and Development (OECD) recently released its 2026 Economic Survey of New Zealand. The OECD, like the International Monetary Fund (IMF), carry out regular reviews and this is a fairly detailed report running to over 140 pages, which you would expect, given the OECD has a significant economic database to work with.

The OECD was cautiously optimistic about the state of the NZ economy but noted that GDP growth was slower than in many OECD countries. Ongoing fiscal consolidation was needed, but the Middle East conflict may require more “targeted support”. It recommended ensuring “strong accountability through transparency of the [RBNZ’s] Monetary Policy Committee decision making”. Other recommendations included harnessing digital tools to improve health system performance and for a more affordable, secure and sustainable electricity system (which, in the long term, does not include LNG in the OECD’s view).

Not all recommendations made by the OECD or the IMF are greeted with enthusiasm by the government of the day. The Prime Minister reacted very strongly to warnings about the Government’s LNG proposals, calling the OECD’s report “a load of rubbish”.

Unlocking capital markets to drive growth

It’s Chapter 4 of the survey, which I found most interesting and relevant, as it included a discussion of our tax settings relating to the taxation of savings. This section was written by Dr David Haugh, the head of the New Zealand (and Finland) desk, together with his colleagues Kyongjun Kwak and Carl Magnus Magnusson. Dr Haugh is actually a New Zealander who started his career with the Treasury before joining the OECD. That means he has a good background knowledge of New Zealand and our challenges.

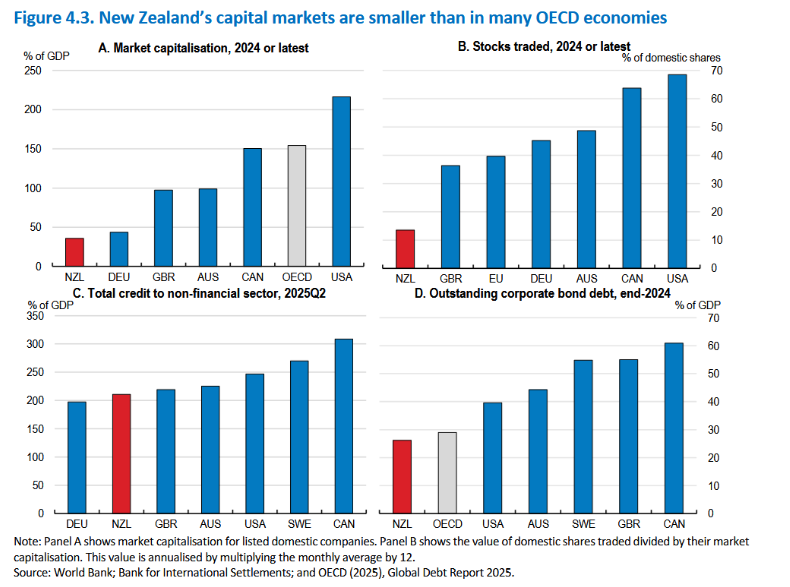

The background summary is that our capital markets remain “shallow by international standards, constraining long-term investment, innovation and productivity growth”. The survey notes that the NZX has seen no major domestic initial public offerings since 2021. That’s apparently part of a worldwide trend, as many firms that might otherwise have gone to market have instead opted for a private or trade sale. A classic example would be Fonterra’s recent sale of its global consumer and associated businesses, Mainland Group, to Lactalis.

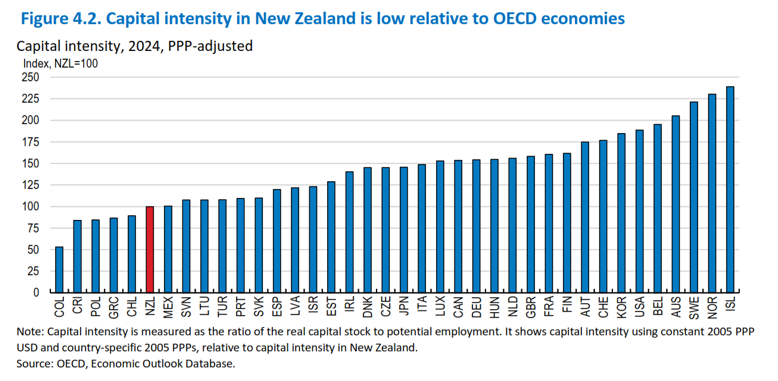

There are some pretty damning graphs illustrating the scale of the problem. Quite apart from smaller-than-average capital markets, ‘capital intensity’ or the ratio of real capital stock to potential employment is low relative to other OECD economies. In 2024, New Zealand’s capital intensity was just about 100%, whereas if you look at Israel, Norway and Australia, they’re all over 200%.

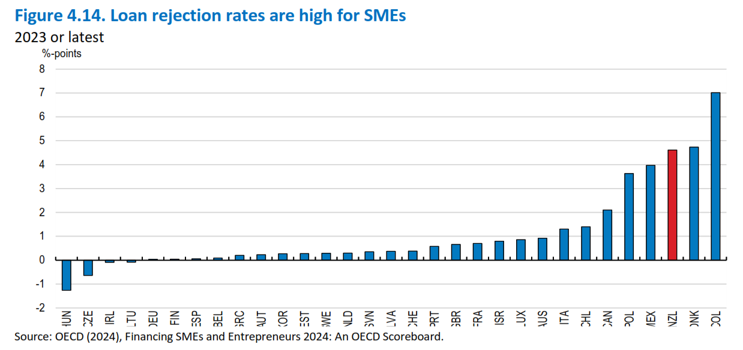

There’s also a sideswipe for the Australian banks, with the OECD saying “costly bank lending dominates, with OECD analysis of lending margins showing they’re about twice the international norm”. With the main banks preferring mortgage lending, SME loan rejection rates are high.

There’s a fairly blunt assessment of why our capital markets are underdeveloped – the decision in 1975 to cancel the Third Labour Government’s compulsory superannuation scheme:

“The decision to abolish the private pension saving schemes in 1975 and replaced it with a publicly funded universal pension at age 60, significantly hampered the development of New Zealand’s capital markets by reducing households’ incentives to accumulate private pensions, depriving capital markets of a key source of long-term domestic funding.” [page 98]

Developing public equity markets – the Swedish example

There’s a very interesting discussion about how Sweden “has developed one of the most dynamic and inclusive equity markets relative to its economic size in Europe and across the OECD.” A key element of this is the Investment Savings Account, or an ISK account. There are over 4 million ISK accounts, with half the adult population having an ISK. These have helped channel household investments into listed equities. Britain’s Individual Savings Account is a slightly similar product. The recommendation is that we consider introducing a non-retirement New Zealand Equity Savings Account.

Raising household savings through changes to KiwiSaver

The report notes our retirement savings are fairly inadequate by world standards. In September 2025, the value of funds under management in KiwiSaver was $141 billion or 32% of GDP. By comparison, in Australia, the assets under management exceeded A$3.6 trillion or 133% of GDP. Furthermore, the average Australian retirement pension plan value is NZ$130,000 or nearly five times greater than the average NZ$28,000 in New Zealand.

The survey notes that withdrawals are allowed to buy a first farm or first house, which, together with increasing withdrawals for hardship (these have doubled from $100 million a month in 2023 to $200 million a month in 2025), slows the accumulation of funds. The OECD questions the purpose of withdrawals for first farms or houses. It suggests that if the policy objective is to support low-income people into house ownership, then a separate instrument would be more effective. The OECD also recommends not creating any further exemptions.

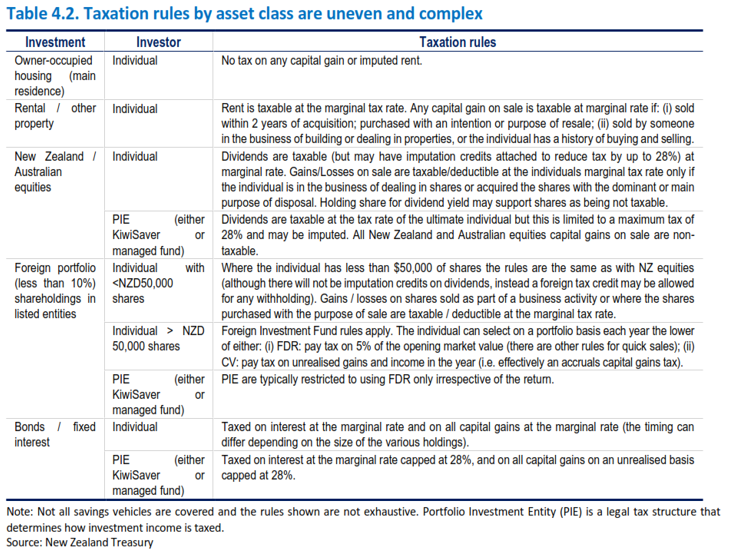

‘New Zealand’s taxation of capital income and savings is complex and uneven’

The survey then discusses the taxation of capital income and savings, which it describes as “complex and uneven, with housing taxed lightly relative to financial assets and especially pensions”. Our corporate income tax at 28% is noted to be amongst the highest in the OECD. Taken together, these settings:

“…distort household and firm investment decisions and suppress the accumulation of private pensions and other long-term financial savings, which is a critical issue not only for capital market developments but also for retirement income adequacy.”

In short, the way our tax system has distorted savings has had long-run consequences. This is something I’ve been saying for a long time and it’s also the view of the International Monetary Fund.

Increasing the accumulation of pension savings by reforming the taxation of savings

The OECD’s view is that the taxation of savings needs reform to allow greater accumulation of pension savings. The survey notes only seven of 38 OECD countries tax the investment income pension and only three, New Zealand, Australia and Türkiye, have a tax-tax exempt system (TTE). The most common system operated in about 17 out of 38 countries is an exempt tax, which is what you see in the UK and America, which allows the accumulation of more funds within the fund that eventually gets taxed as a pension.

The critical disadvantage of our TTE system is that it penalises the accumulation of long-term financial retirement assets, sharply reducing compounding returns relative to the exempt-exempt-tax systems used by many other countries, such as the UK and the United States.

The OECD bluntly concludes:

“The TTE system for financial savings combined with light taxation of housing in New Zealand… makes the overall system one of the most housing-biased tax systems in the OECD. This bias has been capitalised into higher house prices, larger new dwellings, lower ownership rates amongst younger cohorts, and a worsening of New Zealand’s net international asset position, reflecting reduced domestic financial capital available for firms.”

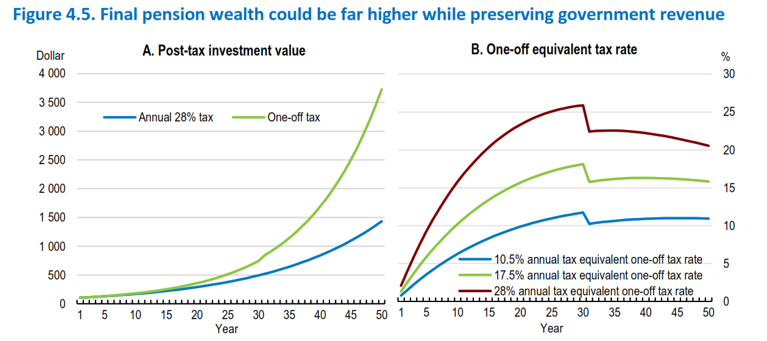

The OECD notes that because pension savings compound over 40 years or so, lowering the tax burden on returns “substantially increases long-run private wealth accumulation”. So, does that mean switching to the common exempt-exempt-tax approach? Not quite. An argument against such tax incentives, and one I share, is that the benefit of such savings is mostly captured by the wealthy who would be saving anyway, and tax incentives don’t lead to significantly increased savings. Another issue with tax incentives is, as Finance Minister Nicola Willis pointed out, they are extremely expensive.

Auto-enrolment and KiwiSaver

According to the OECD, many of these concerns are indirectly addressed by an auto-enrolment system, i.e. everyone would be in KiwiSaver and therefore automatically contributing and saving. UK evidence is that within such auto-enrolment schemes, savings do not fall or rise in response to tax incentives and other private savings are not reduced to offset the diversion into tax-preferred schemes. Furthermore, the strongest benefit of such a change would be for low and middle-income households, who have limited discretionary savings anyway.

Removing or reducing tax on KiwiSaver returns would operate primarily by allowing greater compounding and unchanged contribution patterns, generating substantial increases in total retirement wealth. In other words, directing the incentives there towards the lower-income earner is an approach I fully support.

The survey includes an example illustrating that if this approach is adopted and coupled with a withdrawal tax, the post-tax pension value is twice as large by age 65 compared with the current annual taxation approach.

Overall, there’s plenty of food for thought in this survey. We’ve had a long period of stable policy settings in relation to savings, but we have problems with productivity and access to capital for start-up companies. New Zealand actually has a fairly vibrant tech sector, but as this paper notes, a lot of small tech companies go overseas to get funding because they can’t get it here. I’ve advised on a few such situations, and I’m always surprised the investment capital isn’t readily available here. This OECD survey should therefore provoke plenty of debate amongst politicians and analysts alike, but I fear it will get drowned out by the noise around the coming general election.

The latest National Climate Change Risk Assessment is not a pretty read

More or less simultaneously with the OECD report release, the Climate Change Commission released its National Climate Change Risk Assessment (NCCRA) for 2026. This is the first one that’s been produced since 2020 and is not pretty reading. It identifies the 10 significant risk areas “where focused action would make the biggest difference.” In short, this means increased infrastructure spending, particularly in relation to water infrastructure. The NCCRA warns that without immediate action, water infrastructure could be the “first climate risk to reach an extreme severity level within the next 25 years”.

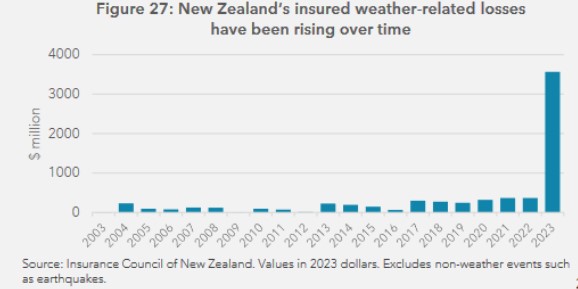

The regularity of natural disasters has been increasing. According to the NCCRA stat, about 97% of the estimated $33 billion of government expenditure on natural hazards since 2010 was spent on responding to and recovering from disasters, with only 3%, i.e. a billion dollars, spent on risk reduction.

What happens when the insurers withdraw cover?

Whether or not you accept what’s driving climate change, it is happening. The NCCRA notes that 556,000 buildings with a combined replacement value of $235 billion are currently exposed to inland flooding. Insurance premiums are rapidly rising, leading the OECD’s economic survey to note “climate-change-induced rises in insurance premiums make inflation control more difficult”.

Quite apart from rising insurance premiums, my concern is that at some point, the insurers are going to dictate what happens with such properties. If the insurers start withdrawing cover, and that’s now coming into general discussion, people will look to the government to help because if they can’t get insurance on their properties, the banks won’t lend against that. This also ties into what the OECD was saying about the high dependency on property ownership for savings.

The NCCRA notes that if we keep allowing the current pattern to continue, of simply accepting damage will happen and then repairing it afterwards, this will drain funds away from core services such as health and education. Over the past 15 years, we’ve spent on average $2 billion a year, or roughly 0.5% of GDP, on climate mitigation and recovery, and things are only getting worse.

All this comes back to a long-standing argument I’ve been making here on the podcast and elsewhere: that climate change is going to drive changes in our tax system by way of having to increase revenue to fund these changes. There’s been plenty of debate about the long-term fiscal sustainability of New Zealand superannuation, but the impact of climate change is an immediate and growing problem.

This is a long-term issue where you really do hope that all the major parties in Parliament accept the need to address this and move accordingly. But as we’ve seen with the superannuation debate, that’s not likely to happen.

The Australian Budget

Finally, across the ditch, the Australian Budget was handed down on Tuesday, 12th May. There had been a lot of speculation beforehand that there would be changes to ‘negative gearing’ and the taxation of capital gains. This speculation was correct, but the extent of the changes has taken people by surprise.

Negative gearing is what the Australians call the ability to offset losses from residential property investment against other income. With immediate effect, any new investors will now only be able to offset losses from purchases of ‘new builds’. (Rather like our previous interest limitation rules.) Taxpayers with existing rental properties will still be able to offset their losses against other income. In other words, they will not be subject to what we term ‘loss ring fencing’.

The capital gains tax surprise

Presently, Australia grants a 50% discount on the amount of a capital gain for individuals, trusts and partnerships if the asset in question has been owned for more than 12 months.

This 50% discount will no longer apply for any gains realised on or after 1st July 2027. Instead, there will be a cost-based indexation, i.e. based on retail price, which was the rule between 1985 (when Australia introduced capital gains tax) and 1999. There will also be a minimum 30% tax rate on capital gains.

This is a significant change, and it’s expected to result in a rise in payable capital gains tax. Pre-Budget speculation focused on gains from residential property investment, but this change will apply to all asset classes.

A potential silver lining?

Now, the interesting thing if you’re a New Zealand resident and you’ve got a property investment in Australia, this change may be beneficial. At present, New Zealand tax residents are subject to Australian capital gains tax on disposals of Australian-situated property, but because they are not Australian tax residents, they do not get the 50% discount. (Australia is frequently quite sneaky in how it taxes non-residents.)

This change may mean that New Zealand investors subject to Australian capital gains tax on Australian properties may actually be better off. We’ll need to see the details on that, but it’s perhaps a silver lining for everyone.

On that note, that’s it for this week. I’m Terry Baucher and thank you for listening. Please send me your feedback and tell you and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

[This is the transcript of the episode recorded on Friday 15th May – it has been edited for brevity and clarity]

calls for capital gains tax to help solve housing affordability.

Earlier this year, the popular Auckland Cafe chain Little and Friday closed its final store in Ponsonby. That was a great personal disappointment for me as its food was wonderful, although my waistline is probably all the better for its closure.

It has now emerged that at the time of its closure, the owners owed $640,000 in tax and the company has now been put into liquidation owing creditors over $1.4 million.

This obviously puts a different complexion on the closure, and it also prompted an interesting debate amongst my tax agent colleagues, with quite a few pointing out the inconsistencies that they see in Inland Revenue’s debt management. One took particular exception to the news, commenting how he had been grilled over a relatively small adjustment, less than three figures, and yet somehow Little and Friday had been allowed to build up unpaid GST and PAYE totalling $640,000.

Focusing on the wrong target?

Another tax agent noted that he had received a call regarding a client being overdue in making their small business cashflow scheme repayments. The amount outstanding was $18,000, but as the tax agent pointed out, the client also owed several hundred thousand dollars in relation to unpaid GST and income tax. The agent was therefore rather puzzled as to why Inland Revenue seemed to prioritise the small business cashflow scheme arrears. Several other tax agents weighed in with similar points about such inconsistencies.

Now, debt management is a core role for Inland Revenue. That goes without saying. But it is also an issue where there are clearly strains emerging. We’ve talked previously about what’s been going on with the student loan scheme, where substantial amounts of debt are allowed to build up over enormously long periods of time.

My attention has been drawn to a case where the student loan borrower left more than 20 years ago and was eventually contacted by Inland Revenue demanding over $200,000 of accumulated interest and penalties. Like Little and Friday, and other cases noted above, the unanswered question is “How did Inland Revenue manage to let it get to that stage?”

Earlier intervention needed?

When looking at Inland Revenue’s management of its debt portfolio two concerns arise – its approach seems inconsistent and it doesn’t intervene soon enough.

Inland Revenue has enormous tools at its disposal. It can put companies into liquidation and that’s actually what happened with Little and Friday. But it doesn’t want to do that all the time. It will sometimes hesitate before doing anything, for perfectly reasonable circumstances. But there does come a point where it is probably better for all concerned that the Inland Revenue moves sooner and doesn’t allow the debt to build up.

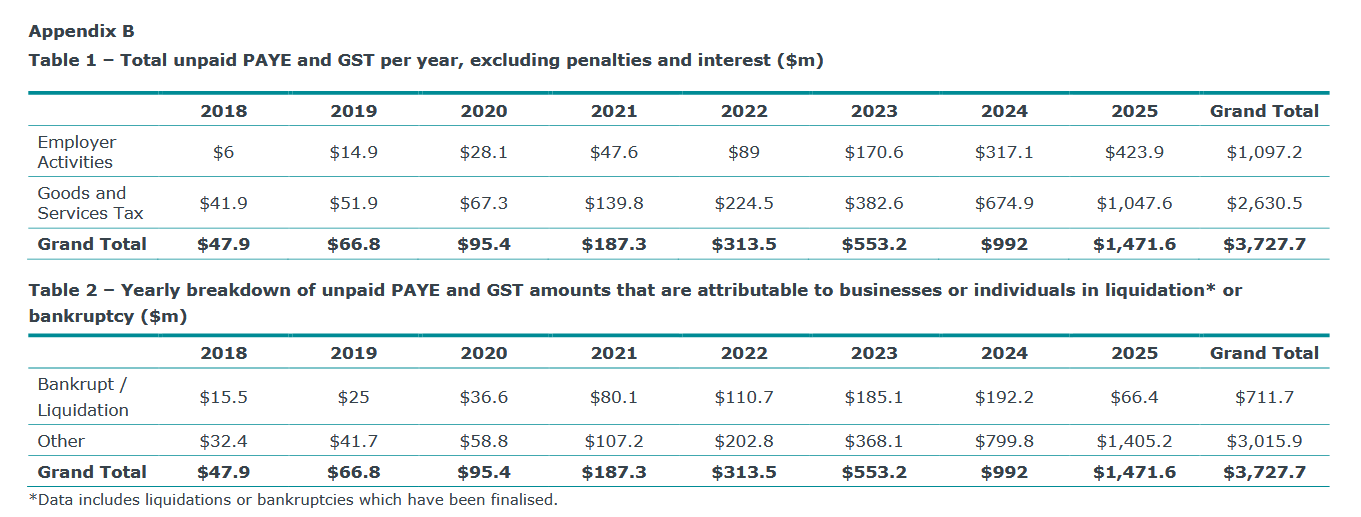

Now Little and Friday is not an unusual circumstance. While preparing for this podcast I came across an Official Information Act request about debt dating from June this year, and the number being reported was frankly horrifying. According to this report, as of 31st of March 2025, the total amount of unpaid PAYE and GST, excluding penalties and interest, stands at $3.727 billion.

As can be seen $711.7 million of that $3.7 billion represents businesses or individuals going into liquidation. The rest is simply outstanding debt which Inland Revenue is hoping to obviously try and recover. But the amount of debt it is writing off is starting to increase, as is the amount of debt that it deems non-collectible. According to this OIA report the non-collectible amount as of 31st of March 2025 is expected to be $1.1 billion dollars.

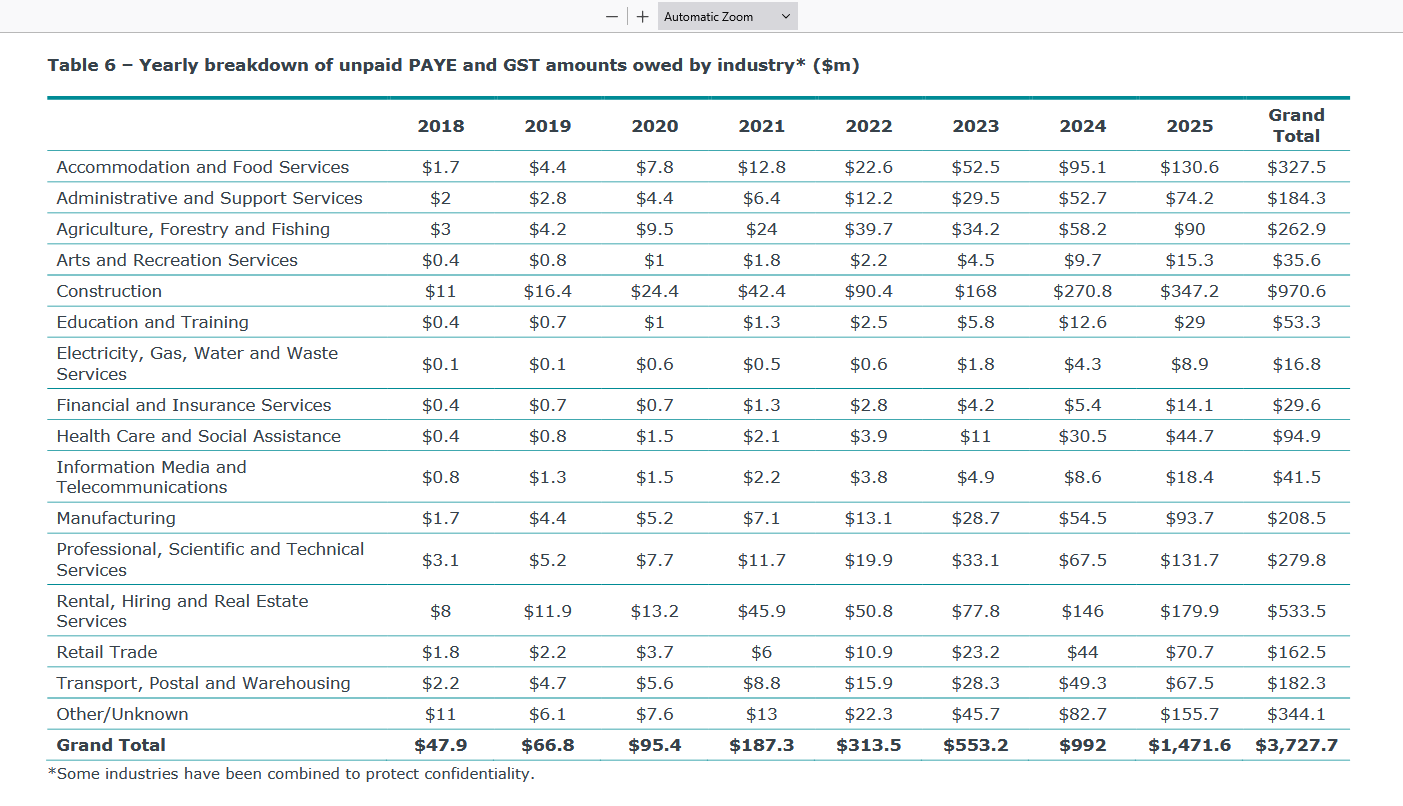

Then there’s a very interesting industry breakdown of how that amount of debt has accumulated.

The sectors hardest hit in that are our construction which has $347.2 million of unpaid debt as of March 2025. accommodation and food services, i.e. cafes like Little and Friday owe $130.6 million, manufacturing $93.7 million and professional, scientific and technical services have also accelerated remarkably $131.7 million. Even rental hiring and real estate services, which you would regard as relatively strong industries, has unpaid GST and PAYE of $179.9 million as of 31st March this year.

Across the whole of the economy, these numbers are piling up and it presents a huge problem for Inland Revenue, and by extension for the Government as to how is it going to manage this issue.

Unfairly targeting student loan defaulters?

A very real threat for people owing student loans who are not meeting their obligations is being arrested at the border. But none owe $600,000 of tax. In theory, someone owing that amount of unpaid GST and PAYE could be freely entering and leaving the country without customs making a move against them.

On the other hand, someone owing $100,000 of student loan debt, which is sizeable, yes, could enter the country and be arrested. I wonder why such an inconsistent approach applies.

To be fair Inland Revenue is working through the overdue debt issue and taking enforcement action. This week it reported how an accountant, Luke Daniel Rivers, also known as Mai Qu was jailed for six years over a $1.7 million COVID-19 fraud. He made false claims over wage subsidies in the small business cash flow scheme.

Now quite correctly Inland Revenue and the Ministry of Social Development have pursued that. But at the same time, we have these other businesses falling over, owing very substantial sums of money, and it appears almost as if the defaulters are able to walk away without consequences, to the frustration of myself and other tax agents.

What about MBIE?

One other thing of note in this area are the potential breaches under the Companies Act 1993. In some cases, you’d have to say there there’s a strong argument that businesses racking up hundreds of thousands of dollars of tax debt are in breach of their Companies Act obligations, which could lead to action by the Ministry of Business, Innovation and Employment.

The economy is under strain and tax debt is rising. Sometimes really bad luck hits a business or person. Small businesses can get hit particularly hard if a key person falls ill. Tax debt may just be down to sheer bad luck, the wrong thing happening at the wrong time.

But overall, Inland Revenue looks to be struggling, for want of a better word, managing the portfolio. Even allowing for maybe getting better resources to manage this, there’s still the question of an inconsistent approach that I and other tax agents have noted. So, there’s a lot of going on in this space.

I expect the Commissioner of Inland Revenue is reporting very frequently to the Minister of Revenue on this issue and any new initiatives to address these concerns. The most important thing would be to get the economy going again and hopefully some of these businesses are able to trade their way out. But we’ll have to wait and see.

Capital gains tax to deal with housing affordability?

Now, in recent weeks, there’s been quite a lot of chatter around Inland Revenue’s long-term insights briefing, which has talked about the need to perhaps expand the tax base. Last week we discussed how CPA Australia called for a capital gains tax.

This week at the Government’s Building Nations 2025 Infrastructure Summit on Wednesday 6 August, Group Chief Economist and Head of Research for ANZ Richard Yetsenga discussed the question of what he described as runaway house prices in Auckland, Australia and New Zealand. He said that we should look seriously at introducing a capital gains tax as a means of addressing house price affordability. In his view, if this issue is not resolved, “I think it’s going to eat us alive. It’s our biggest intergenerational issue.”

Mr Yetsenga was speaking after addresses from the Finance Minister, Nicola Willis, and Transport Minister and Housing Minister Chris Bishop. In response he suggested looking at both the supply and demand issues of the tax system, which in his view, was one of most effective ways available to influence economic activity.

That’s something I would agree with. What we don’t tax is as important as what we do tax. I think the fact that we don’t have a capital gains tax has resulted in major distortions for our economy. This was something which the recent International Monetary Fund report on our poor productivity mentioned. It’s very interesting to see all the constant chatter on the topic of capital gains taxation.

How many people return overseas income?

Finally, Inland Revenue proactively publishes any Official Information Act (OIA) requests that it receives. These often include some very interesting data such as the breakdown of debt I discussed earlier.

The question was rather oddly phrased because the requester asked “Do you know if/believe there high compliance with NZ tax rules for NZers working overseas?” Inland Revenue’s response was basically this is actually not a request for information, it’s more for an opinion so we aren’t answering that.

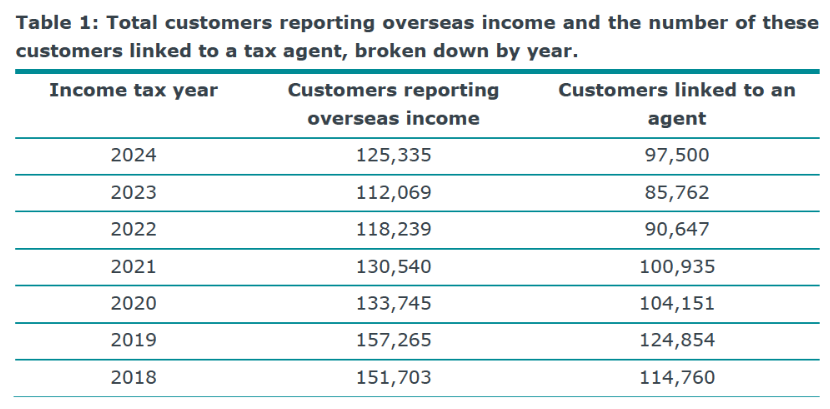

The request then asked for specific data about taxpayers reporting overseas income, and also the split between taxpayers who reported it and those taxpayers with tax agents who report it. Inland Revenue provided the following breakdown for the 2018 to 2024 tax years. (The final due date for filing tax returns for the 2024 tax year is 31st March 2025 so 2024 is the latest year for which complete details are available).

What caught my eye about this data is that the numbers have fallen since the 2019 year. In 2018, 151,703 taxpayers reported overseas income, of which 114,760 were linked to a tax agent. After an increase in the 2019 year the numbers reporting income decline each year until the 2024 year when it rises from 112,069 to 125,335.

I find it quite surprising, given the international mobility of our labour, that fewer people appear to be reporting overseas income when we have a lot more migrants arriving.

I suspect it’s possibly piqued Inland Revenue’s interest, because I’ve had some clients requesting assistance after they have been contacted by Inland Revenue which has received information under the Common Reporting Standards of Automatic Exchange of Information. It will be interesting to see how that number of taxpayers reporting overseas income tracks.

By the way, this OIA also references the Common Reporting Standard, confirming in response to a question it “receives financial account information automatically from the Australian Tax Office under the Common Reporting Standard. This information is matched to taxpayer accounts and risk assessments.”

This ought to be well known and, as noted above, maybe we might see an increase in the numbers reporting overseas income.

Happy Twenty-first!

Now finally this week, according to LinkedIn, Baucher Consulting is 21 years old today. So Happy Birthday to me. It’s been and continues to be an amazing journey and who knows what the future will bring. In the meantime, thank you all for all the messages of support.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

There have been several constant themes throughout this year. A surprising one has been the question of how we tax capital and whether we should have a capital gains tax. Throughout the year there have been a steady stream of stories on the topic. Meanwhile the Labour Party is currently reviewing its tax policy, and whether it’s going to go with a wealth tax or a capital gains tax.

A place where talent does not want to live

Intriguingly, Inland Revenue has added to this mix right at the end of the year with the release of an issues paper on the effect of the Foreign Investment Fund (FIF) rules on immigration.

Earlier this year I discussed a New Zealand Institute of Economic Research report called The place where talent does not want to live, which looked at the impact of the FIF rules on migrants to New Zealand. The NZIER report concluded that the FIF rules were acting as a hindrance to investors, particularly those migrants coming here who have previously invested in offshore startup companies.

The report also discussed an issue I’ve encountered fairly regularly of the impact of the FIF rules for American citizens. Even though they may have been resident in New Zealand for many years, because they are American citizens they still have to file U.S. tax returns. As a result, a mismatch arises for them between the FIF rules, which basically act as a quasi-wealth tax, and the realisation basis of capital gains tax that applies in America.

Inland Revenue policy officials have been aware of this issue for some time. In fact, I spoke to several officials earlier this year about the issues and potential options. The topic was highlighted as an option for review and was included in the Government’s tax and social work policy programme released last month. This report has therefore come out quicker than I expected which is a pleasant surprise.

The problem with the FIF rules

The problem is set out very clearly in paragraph 1.5 of the issues paper.

“Migrants will generally have made their investments without awareness of the FIF rules and may not be organised so that they can fund the tax on deemed rather than actual income. This is particularly a problem for illiquid investments acquired pre migration…. Because the FIF tax is imposed in years before realisation and on deemed rather than actual income, FIF taxes paid may not be creditable against foreign taxes charged on the sale of the investment.“

This highlights a key point about the FIF rules – they’re highly unique by world standards. When I’m discussing them with overseas clients and advisers, to make them more understandable I tend to explain them from the viewpoint that they’re a quasi-wealth tax. As the quote above notes problems also emerge whether the tax paid under the FIF rules can be fully utilised in the United States, for example.

Fixing the problem – taxing the capital gains?

The paper canvasses several options for reform, including one of simply increasing the current $50,000 threshold above which the FIF rules automatically apply. A key proposal is that maybe the investments subject to the FIF rules should be taxed on what is called revenue account. That is only dividends received and any gain in the value of those investments attributed to New Zealand on disposal would be taxed. In other words, an investor would be taxed on dividends and then when the investment was disposed of, a capital gains would be become payable.

Now to buttress this option the paper proposes that there should be an exit tax. In other words, if someone elects to use the revenue account method, but then decides no, actually New Zealand isn’t working out for us for whatever reasons, and they become a non-tax resident, this migration would trigger an exit charge. I’ve seen this in other jurisdictions and current FIF rules do have a provision covering it. This approach should be pretty understandable to investors coming here.

Maybe a deferral basis?

Another alternative is a so-called deferral basis, is where the FIF rules would apply on a realisation basis. This would be achieved in a way similar to how withdrawals on foreign superannuation schemes are currently taxed when the tax charge arises on withdrawal or transfer into a New Zealand based Qualifying Recognised Overseas Pension Scheme.

The taxable amount would be based on a deemed 5% per annum income from the date of their migration, with an interest charge for deferral. Again, this would be buttressed by an exit tax.

What happens overseas?

Picking up on what I was saying at the start about the question of taxation of capital, most other jurisdictions don’t encounter this issue to the same extent as we do because they usually have a capital gains tax regime that applies to comprehensive capital gains. Actually, in paragraphs 2.3 and 2.4 I find there’s some intriguing commentary from Inland Revenue on this issue.

“Because New Zealand does not tax capital gains without the FIF rules, no New Zealand tax would ever be paid on an investment in a foreign company that paid no dividends and was sold for a capital gain.”

This is an interesting insight to the issues caused by non-taxation. In effect without the FIF rules the Government is forsaking potential revenue. I always thought the expansion of the FIF rules in 2006 was really a sidestep around the difficult issue of taxing capital. And of course, despite having kicked the capital gains tax can down the road back in 2006, it’s still there.

Tax driven behaviour, or just a rational investment choice?

The issues paper goes on, quite controversially in my view, to argue that without the FIF rules in New Zealand, residents have a tax driven incentive to invest in foreign companies that enjoy low effective tax rates and do not pay significant dividends. Speaking with 40 years of tax experience, yes taxes do drive investment behaviour.

But this argument sidesteps a huge criticism, which is still valid, of the current FIF rules. When they were introduced in 2006, many of the submissions against them argued that the New Zealand stock market is so small in global terms that investors would be unwise to be fully invested here, and therefore should be spreading their risk by diversification and investing in offshore markets.

That is as valid a criticism of the FIF rules now as it was back in 2006. And of course, memories of the 1987 stock market crash, which was actually quite catastrophic by world standards, still run deep in many areas. We now have this scenario here where the FIF rules were designed because the Government wanted some revenue. It saw tax driven behaviour happening offshore, but it ignored a key fact, the importance of diversification. And if you don’t tax the capital but you want the revenue, where do you go from there?

Backdating the introduction of the changes?

Anyway, the whole paper is a very worthwhile read. It has one further highly interesting suggestion that changes could be back dated to take effect from 1st April 2025 and the start of the next tax year. Such a swift law change doesn’t happen with issues papers. Normally there’s usually another year or so before legislation is introduced and then comes into effect.

This option is actually very encouraging for migrants. I have had a number of inquiries on this issue, and I know of clients who have backed away from New Zealand because of the FIF rules. So, they will be looking at the proposals with great interest.

The paper also canvasses whether it should apply to new migrants or to existing New Zealand tax residents. That’s a good question it should certainly apply to migrants who can reorganise their affairs in anticipation, but I believe it should also apply to U.S. citizens who still have to file U.S. tax returns and are very disadvantaged by the current FIF rules.

Worth noting that although this is largely a tax measure it’s important to the Government because the existing FIF rules are seen (as the NZIER report noted) as a hindrance to attracting high quality migrants. Changing the law is seen as a priority as part of the Government’s general economic programme,

Submissions are open now and continue until 27th of January. I urge everyone interested in this topic to submit. We will be submitting a paper on this ourselves. We will also be contacting clients on this matter as it’s quite a welcome Christmas present.

The year in review

Moving on, its been a very busy year in tax. And I guess the biggest story in many ways was the Budget on 30th May, with the promised increase in tax thresholds finally being enacted with effect from 31st July. That was certainly the most eagerly anticipated one, and according to my data reads, it was the most read transcript over the year.

The tax cuts which weren’t

These tax cuts as they were called (which they’re not because they’re only inflation adjustments) also highlighted a big and continuing problem with our tax system, which the politicians apparently don’t want to address. The threshold adjustments only factored in inflation from 2018. They therefore effectively locked in the inflationary effect of the non-adjustment between 1st October 2010 (the last time the thresholds were adjusted) and the 2018 baseline.

On the other hand, in order to help pay for these adjustments which will reduce government revenue, the threshold on Working for Families which has been at $42,700 since 1st July 2018, was not increased. This means that families with income above that threshold have their Working for Families credits abated at 27.5%. Consequently, they face some of the highest effective marginal tax rates in the country.

And as I have repeatedly said in past podcasts, our politicians are very much less than transparent about the impact of what’s called fiscal drag. That is, as wages increase with inflation, they pull taxpayers up into higher tax brackets. We have a particularly big problem around the now $53,500 threshold where the tax rate jumps from 17.5% to 30%, the biggest single jump in the whole tax scale.

To bang a drum already beat repeatedly, this hinders a discussion around what is happening with our tax system? How much revenue have we really raised because politicians have been happy to use fiscal drag to quietly increase the tax take.

But the main effect is that the burden of tax falls on low to middle income earners who face significantly higher marginal tax rates because of the effect of abatements on people receiving social support, such as Working for Families.

So overall, those tax threshold adjustments were welcome. They were overdue, but they were one step forward and two steps sideways and half a step back because there’s no comprehensive commitment to ensuring that we have regular threshold adjustments.

If America can do it, why not here?

Just as an aside, in America all thresholds are automatically index-linked. Countries vary on their treatment of inflation and thresholds. And in low inflation periods, you can get away with not needing to do it every year, but you can’t leave such adjustments for 14 years without finally having to do something.

A year of anniversaries

2024 was quite a big year for me personally. I started working in tax 40 years ago in Britain and it so happened that the British budget on 30th October had several announcements which have huge significance not just for UK migrants who have moved here but also for many Kiwis. So, I find myself, somewhat ironically, still doing a lot of work on the impact of British taxation.

It’s also been 20 years since I started Baucher Consulting and as I said in the podcast much has changed, and yet in some ways little has changed. One constant which hasn’t really changed is the behavioural impact of tax- this week’s discussion of the FIF regime is the latest example. I’d like to thank everyone who’s supported me over the these past 20 years.

Our fantastic guests

Looking at some other highlights of the year in terms of the podcast, we had a lot of great guests this year and my thanks again to all of them. My particular favourite episode was the Titans of Tax with Sir Rob McLeod, Robin Oliver and Geof Nightingale. Many thanks to Sir Rob, Robin and Geof for giving up their time. It was a fantastic discussion and very, very enjoyable. It was extremely well received all around. It was fascinating to just sit back and listen and to three experts who’ve been very heavily involved in the last three major tax working groups.

My thanks also to all my other guests this year, including the four finalists for this year’s Tax Policy Charitable Trusts Scholarship. Again, thank you so much for your input. Very interesting to talk to you, and the future of tax policy is in good hands.

Inland Revenue goes full throttle on compliance work

One of the big themes for the year, and less of a surprise, was Inland Revenue’s ramping up its enforcement approach. One of our guests very early in the year (and thanks again) was Tracy Lloyd, service leader of Compliance Strategy and Innovation at Inland Revenue. Tracy’s podcast was a really interesting one looking at what tools Inland Revenue is using and how it’s ramping up its investigative activities.

We’ve seen Inland Revenue’s more aggressive approach constantly through throughout the year. It has made announcements about cracking down on the construction sector, looking at liquor stores. Pretty much every week there’s a media release that another tax fraudster has been jailed or received substantial fines or home detention. In addition Inland Revenue is making use of information received through the Common Reporting Standards on the Automatic Exchange of Information.

These things will continue to come through. Inland Revenue got $116 million over four years to beef up its investigation activities and to improve its tax collection. As part of this we’re seeing a crackdown on student loan debt, which is a much more problematical issue mainly because the biggest portion of debt is held by persons overseas. It’s therefore not so easy to collect.

Inland Revenue’s activities will continue to ramp up but I think it may start to find there’s increasing push back as it clamps down. I think it’s previously been slow in responding, and during the COVID pandemic that was understandable. But right now, the faster it responds to debt issues developing, the better for all of us. Zombie businesses which linger on are no good to anyone.

The surprising continuing debate over capital gains

But the other big thing this year has been a surprising one. It’s the question of the shape of the tax system and persistent media stories about whether we should have a wealth tax or capital gains tax. This is a topic I don’t see going away. I see the pressure mounting on it because as, the Government’s main agency, Treasury, is pointing out we have ongoing demographic pressures in relation to superannuation and funding health.

And as I keep pointing out, we also have the question of climate change. We have insurers withdrawing cover and I think that means the Government will be expected to step in. And that means sharing the burden, which means ultimately some form of tax increases. All this means the composition of the tax base will continue to be a matter of debate.

Of course, we have options like capital gains tax, wealth taxes, or as Dr. Andrew Coleman suggested (another one of the fascinating podcasts this year) maybe we should rethink our issue of Social Security taxes, where again we’re a unique jurisdiction in that we don’t have them. We used to have such taxes way back from the early 1930s through until late 60s, before they were finally abolished,

So overall lots to discuss this year. I’d like to thank all my guests again, and all the listeners, readers and all those who chip in and comment away. Your comments are read and always welcome. And on that note, everyone have a very happy festive season. We’ll be back with what’s new in the tax world in January 2025.

Various Treasury Briefings to Incoming Ministers have been released in the past week including that for the incoming Finance Minister. The slide pack discussing the Economic and Fiscal Context has attracted some attention because it discussed the option of introducing more taxes on capital.

Prepared on 24th November, the Briefing sets out

“Treasury’s view on New Zealand’s economic and fiscal context, including some of the key policy issues you will likely grapple with. It’s intended to provide context for subsequent, more detailed conversations between you and the Treasury.”

The summary section has a really fascinating slide not just about this podcast’s focus, tax and the fiscal outlook for the country, but about the Treasury’s snapshot of the present state of the New Zealand economy and the challenges ahead. And the summary gets straight to the point, “a substantial fiscal consolidation is required to bring revenue and expenses back into balance and support fiscal sustainability.”

The Briefing discusses the state of the economy and how a clear economic and fiscal strategy will create a strong base for growth. Although fairly routine in some ways it’s very well worth a read.

Fiscal pressures are building…

But what has caught people’s eyes are references in the Briefing to the fiscal pressures that are building. Now I’ve talked about this previously, and in particular He Tirohanga Mokopuna the statement on the long-term fiscal position from 2021. Incidentally, the 2016 precursor of that 2021 statement heavily influenced the last Tax Working group in its decision to propose a capital gains tax.

As the Briefing notes fiscal pressures are building. Gross New Zealand Superannuation costs have increased from 4.6% of GDP in 2011/12 to 5% of GDP in 2022/2023 and are forecast to rise to 5.4% in 2026/27. Then there’s the issue of weather-related events such as Cyclone Gabrielle which are increasing in intensity. The Briefing includes this really chilling quote

“In addition, New Zealand is exposed to a very high level of risk from its natural environment. Lloyds, the insurance marketplace, assesses New Zealand as having the second highest risk of annual losses in the world, behind Bangladesh and ahead of Japan.”

There’s also this interesting graph which shows the extent to which insurance claims have been increasing in recent years.

The Briefing references 2021’s He Tirohanga Mokopuna I just mentioned noting it

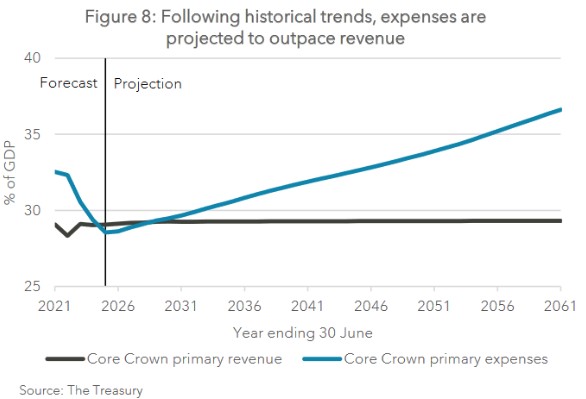

“…illustrated that at historic rates and policy settings, New Zealand’s core Crown expenditure will significantly outpace revenue over coming decades (Figure 8). The most significant spending pressures come from a combination of healthcare and NZ Superannuation.”

Core Crown expenditure was at a multi-decade high in response to the COVID pandemic, but is now outstripping the rise in revenue, even though core Crown tax revenue has been rising as a percentage of GDP since 2012/13. Treasury forecasts tax revenue will increase to 30% of GDP by 2026/27 on an unchanged policy. However, after stripping out one-off expenditures Treasury calculates the government is currently running a structural operating balance before gains and losses deficit of around 2% of GDP, which is roughly $8 billion.

But the Briefing notes the problem with tightening expenditure at this time in response to this structural deficit is the demographic change now occurring. This increases the fiscal pressure to deal with an ageing population, including increasing superannuation costs and demand for health services.

A heavy reliance on personal tax

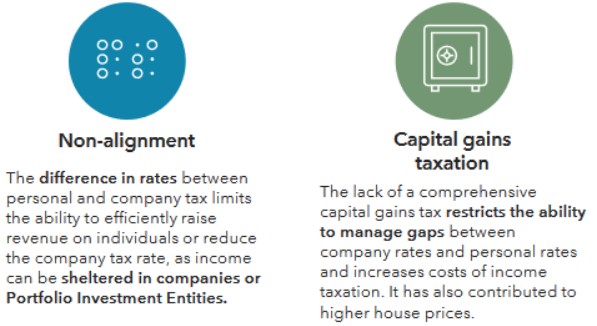

Treasury notes one option would be to increase revenue at which point a government will need to consider a capital gains tax. Because as the Briefing comments “New Zealand relies more heavily on personal tax compared with most OECD countries”. The reason for this is that many other OECD countries have significant Social Security taxes, and they’re used to pay for the likes of New Zealand Superannuation. We don’t have that. We have a very clean system, but because we don’t have Social Security, we rely more on income tax and GST.

Constraints on the tax system – including the lack of a capital gains tax

On the state of the tax system Treasury’s Briefing comments

“However, there are constraints on our personal tax system which are creating increasing pressures and constraining our options for reform. These constraints arise due to the difference between our personal and company tax rates, and the lack of taxes on capital and capital gains. These limit options to raise revenue alter the mix of taxes or make changes that would meet distributional and economic objectives.”

The comment that the lack of capital gains taxation “has also contributed to higher house prices” will be disputed by some, but it’s interesting to see Treasury come out and say it.

Overall Treasury sums up that “At a high-level there are several options to support a return to surplus while delivering priorities” including:

“Increasing revenue through structural reforms of the tax system policy changes to increase revenue or letting fiscal drag continue to increase revenue raised through personal income tax.”

We’ve talked about fiscal drag ad nauseam and last week I referenced the draft report produced under the Tax Principles Act which showed how fiscal drag increases average tax rates over time. We think the Government is still committed to increasing the current income tax thresholds, whether they will index them regularly for inflation is another matter.

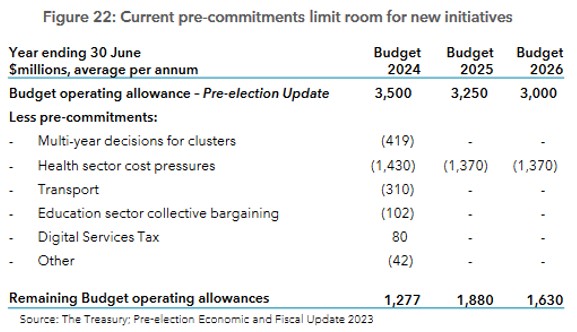

As always, these briefings contain a wealth of little detail. They’re fascinating, really, one little detail that hasn’t picked up by many was on page 19. This was discussing the Budget 2024 operating allowance, which was set at $3.5 billion. The Briefing discusses the existing pre-commitments and included in those pre-commits is revenue of $80 million from a Digital Services Tax.

This seems a little bit optimistic because I understood the DST wasn’t actually being introduced although it possibly reflects the effect of the expected changes in the international tax base. Either way it’s a little detail I was a bit surprised to see. However, $80 million in the context of $3.5 billion operating allowance and over $130 billion annual Government expenditure it’s a drop in the ocean. Still, it’s interesting to see it there.

Inland Revenue consultation on charities’ business income exemption

Mentioning tax working groups, I remember asking the late Sir Michael Cullen the chair of the last Tax Working Group whether there was anything that surprised him. He replied that it was the extent of the charitable sector what was going on there. This is something I see fairly frequently in comments on these transcripts, it seems to be a bit of a sore point that certain charities have a business income exemption (By the way, thank you to everyone who comments, I do read them even if I don’t always respond).

Inland Revenue have just released a 46-page consultation document on to what extent is business income a charitable entity derives exempt from tax. As has become the habit and it’s very welcome, it’s accompanied by a useful little five-page fact sheet on the matter.

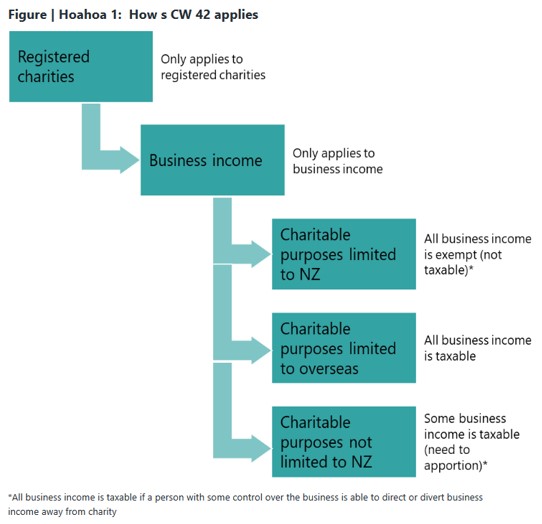

The main business income exemption is in section CW 42 of the Income Tax Act 2007. There’s a related section CW 41 treating non-business income as exempt for charities.

But this particular draft interpretation statement is consulting on what constitutes business income and to the extent to which it will be exempt. How the exemption applies is set out in a very handy flow chart produced in the in the fact sheet.

OK.

In summary, if the charity’s charitable purposes are limited to New Zealand, then all its business income is exempt. But if the charitable purposes are limited to overseas, then all business income is taxable. If it so happens that the charitable purposes aren’t limited to New Zealand, so charitable services are provided both in New Zealand and overseas, then there’s a need to apportion.

The interpretation statement runs through with some good examples what meets the criteria to be business income. It also considers how a charity would about apportioning between business and non-business income and services in and outside New Zealand. Much of this is relatively routine and it’s been standard practice for some time.

I think the thing that concerned the last tax working group, and which prompted the late Sir Michael Cullen’s comment is that there isn’t necessarily a follow through on whether a charity which may meet all these criteria is actually applying its spending to the community. A charity may have an exemption; therefore, they’re not paying income tax. Excellent. But are they applying funds for charitable purposes? If so that’s all well and good. That’s what we want to see. But what if that’s not happening? This is when issues arise about charitable exemptions when the funds are being accumulated and not distributed. That’s a whole topic for another time.

CSI Inland Revenue?

And finally, a little story just came out this week regarding Gordon Kenneth Morris, a Waikato sharemilker, who fraudulently claimed COVID support money which he then spent on online gambling. After he was caught, he was sentenced to nine months home detention.

What happened was he submitted fraudulent applications for the Small Business Cashflow Scheme and also for Resurgence Support Payments. He received a total of $27,200 from the Small Business Cashflow Scheme. But his application for $8,800 in Resurgence Support Payments was declined.

When Inland Revenue investigated it found Morris had also filed false GST and income tax returns and in the period between 1st April 2018 and 20th October 2020, he and his wife had spent over $336,000 on online casinos.

It’s a bit of a tragic case, but it’s also a good introduction for my guest next week, Tracy Lloyd from Inland Revenue, who is Service Leader Compliance Strategy and Innovation. We will be discussing how Inland Revenue detects fraudsters such as Mr Morris.

That’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Thousands here could be potentially subject to UK Inheritance Tax.

Airbnb and Uber are not happy about a GST law change.

GST for all its complexities, is the best example of the Broad Base Low-Rate tax principle, a single rate of 15% applied broadly. However, one of the ongoing controversies with GST is around its application to food and other basic necessities. New Zealand’s approach is at odds with many other countries, such as Australia or the UK, where food is not subject to GST (or VAT, as the UK calls it).

Frequently we see commentary that it would be a good move to help lower income earners by removing GST on food. This has been suggested as a response to the current cost of living crisis. I am opposed to such moves and many GST specialists are also in the same camp. Firstly, I don’t think this move is effective as proponents believe, and secondly, if the issue being addressed is low income, then it is better, in my view, to give more income to that target group rather than using a tax measure which would benefit more people, including some who we probably think don’t need assistance.

A report released yesterday in the UK regarding the impact of the withdrawal of the so-called tampon tax bears out these concerns of myself and other GST specialists about introducing GST exemptions. In the UK, VAT of 5% used to apply to tampons and other menstrual products until January 2021, when it was abolished. Prior to its abolition, VAT specialists predicted that the full benefit of abolition would not be reflected in lower prices. And a report by Tax Policy Associates bears this fear out. According to the report, at least 80% of the savings from the tax savings was retained by retailers. In fact the report questions whether any of the benefit of the removal of VAT ever passed through to lower prices.

Professor Rita de la Feria the chair of tax law at the University of Leeds was one of those who warned beforehand of this likely outcome. Commenting on the report she noted this was not only predictable but predicted. In her view “we have to stop confusing policy aim with policy instrument and we also need to stop using tax policy instruments to signal we care about the policy aim.”

Those are wise words and should be kept in mind next time you hear calls for tax changes for ostensibly very sensible reasons. In tax, even with well-meaning policy, there are always unintended consequences and tax is not always the most appropriate mechanism. Sometimes direct action, such as giving payments to those affected, or supplying tampons for free is the best approach.

How UK tax law applies to NZ residents

Staying in the UK, next week the latest Chancellor of the Exchequer, Jeremy Hunt, Grant Robertson’s equivalent, will be presenting the Autumn Statement. He is expected to introduce a number of tax changes and tax increases in an effort to try and restore the UK’s finances. Hunt, incidentally, is the fourth chancellor this year, whereas Grant Robertson is only the fourth New Zealand finance minister this century. So that gives you a measure of just how much upheaval has been going on up there.

I regularly advise New Zealanders and migrants from the UK about UK tax matters. Frequently there are ongoing issues for them and inevitably complexities creep in.

Based on my experience, there are probably thousands of New Zealanders and family trusts who may unwittingly have UK tax obligations. There are also former residents from the UK who are now living here who misunderstand the relationship between the UK and New Zealand tax treatments of investments. So here’s a quick summary of those people who may be affected by UK tax and the differing tax rules between New Zealand and the UK.

Firstly, if you have property in the UK, then UK capital gains tax will apply to any disposals. There are strict timelines about reporting those disposals which are unrealistic in my view, but they still apply. CGT will apply even though the disposal might not be taxable for New Zealand purposes. By the way, the bright line test does apply to overseas property.

If you were renting a property out in the UK then you must report that income both in the UK and in New Zealand. However, for New Zealand purposes, any UK tax paid will be given as a credit against your New Zealand tax payable.

As should be well-known transfers of, or withdrawals from UK pension schemes are subject to New Zealand income tax. I don’t agree with that policy but it’s the law. In addition, if you are receiving a pension from the UK then the UK pension scheme should not be deducting any PAYE. You will need to apply to H.M. Revenue and Customs through Inland Revenue to get any refund of any such tax deducted. By the way, Inland Revenue will not give you a credit for any tax deducted, it wants the tax paid here. That’s the procedure under the double tax treaty and you’ll have to go and get the PAYE back off HMRC, which can be a very frustrating experience, believe me.

But potentially the most significant tax that will apply, which is also the least known, is Inheritance Tax. Inheritance Tax applies firstly to any assets situated in the UK. So, if a New Zealander who worked over in London, bought an investment property there before moving back here, that property is in the UK Inheritance Tax net.

Secondly Inheritance Tax also applies on a global basis to all assets wherever they’re situated if you are “domiciled” or deemed to be domiciled in the UK. Domicile is a complicated concept which I am not going to get into now. But basically, pretty much anyone born in the UK who’s migrated here in the last ten years or so probably still is domiciled for UK tax purposes. If you were a Kiwi and you spent more than 15 years in the UK, you may also be deemed to be domiciled in the UK. If so, Inheritance Tax applies at a rate of 40% on all assets over the first £325,000. (The price of New Zealand property means that this threshold is comfortably exceeded).

In my experience, many migrants and returning Kiwis are completely unaware of the potential impact of Inheritance Tax. For example, UK Inheritance Tax law does not recognise de facto relationships (apparently much to the relief of several politicians a partner in a London law firm once told me). I once dealt with a scenario where the New Zealand resident survivor of an unmarried couple had to pay over £50,000 of Inheritance Tax on her share of a jointly owned New Zealand property after her Scottish partner’s death.

Finally, the UK has a trust register which arrived in the wake of anti-money laundering legislation and its use has been greatly expanded. Any trust which has property in the UK must register. Furthermore, any trust which has a UK source of income such as bank interest must register if it has beneficiaries, including discretionary beneficiaries who are resident in the UK. This is a common scenario I’ve seen. It appears this registration requirement applies even if no distributions have ever been made to the UK situated beneficiaries. There’s some controversy about that particular provision because it appears New Zealand trusts may even have to file UK tax returns even if all the UK income is being distributed to New Zealand beneficiaries.

So that’s a quick summary of some of the UK tax issues which I commonly encounter. I’ll look to update this summary next week if there are any developments from the Chancellor’s Autumn Statement. Now is maybe time to have a look at your position to see if, in fact, you might potentially have a UK tax issue. And also keep in mind that Inland Revenue is currently running an initiative where it is checking on people’s potential tax obligations from their overseas investments.

“We want to remain tax-free”

Finally, this week and back to GST, Airbnb made a submission to Parliament’s Financial Expenditure Select Committee complaining about the proposal for it to charge GST on all accommodation bookings made through its platform.

In its submission, it warned this would stifle the country’s economic recovery and cost the economy up to $500 million a year.

Now this measure was introduced in the Taxation (Annual Rates for 2022-23, Platform Economy, and Remedial Matters) Bill (No 2). Airbnb along with Uber, also affected by the new proposals, unsurprisingly, think the law changes are unfair. On the other hand, the Hospitality Association was amongst those submitting in favour of the change. Chief executive Julie White said a third of its membership consists of commercial accommodation providers adding “and a consistent frustration of theirs is a lack of level playing field when it comes to services like Airbnb”.

The comments from Uber and Airbnb are unsurprising to me. But what I did find of interest about the bill was there have been quite a considerable number of submissions made 820 so far, and quite a few from individuals who would be affected. To quote one, “this law change will result in fewer bookings to me and significantly impact my retirement plans. This will have the additional impact of higher costs of vacations for New Zealand families who are largely for larger families and cannot afford to stay in a hotel.”

Another submitter thought “This action will have a huge negative impact on a new form of tourism at a very personal, localised level.” I’m personally not sure that the impact will be quite as dramatic as those submitters suggest, but it is interesting to see the reaction to what might be seen as a relatively straightforward GST proposal.

As is often the case, many other submitters took the opportunity to push for other changes, such as several suggesting for the removal of FBT on the provision e-bikes to employees.

There was also criticism of the complexity of the interest,limitation and bright-line test rules. One submitter noted that the commentary to the bill had more than 28 pages devoted to remedial provisions for this legislation, and he concluded correctly, in my view, “it is simply not appropriate to expect most landlords to be able to apply the detail of tax law of this complexity.”

Incidentally, the same submitter suggested that because the interest limitation measures had been introduced partly in response to rising house prices, now house prices were falling logically the interest limitation measures should be repealed. It’s a fair point, and he wasn’t the only one to make it. But somehow I can’t see that happening. To leave off where we came in this is another situation where the policy aim and policy instruments have got confused.