Could the US retaliate against a digital services tax?

Last week, in a series of interviews with the press, notably with Newstalk ZB, Finance Minister Nicola Willis dropped several hints about what might be in the forthcoming May 22nd Budget. In particular, she talked about the corporate tax rate, and the possibility of cuts to that as part of promoting the Government’s growth agenda.

Corporate tax rate above OECD average

Speaking with Heather Du Plessis-Allan, Ms Willis commented:

“Well, if you compare New Zealand with the rest of the world, we’re not as competitive as we used to be. Which is to say that our corporate tax level is reasonably high when you compare it to the rest of the developed world.”

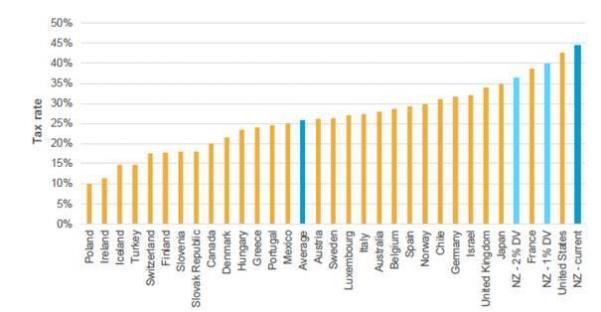

This is a very valid point which comes up frequently in discussions. Our current company tax rate at 28% is well above the OECD average of 24% and has been out of alignment for some time.

New Zealand back in the late 80s under the Fourth Labour Government was actually at the forefront of cutting company tax rates. A particularly interesting action was to align the company tax rate with the top individual and trust rates of 33%. The three basically stayed in line until the election of the Fifth Labour Government and the increase in the top personal tax rate to 39% in 2000.

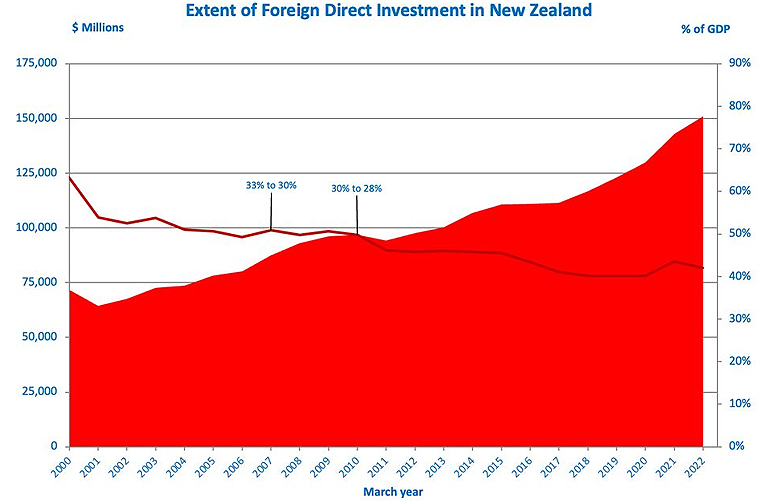

There have been a couple of corporate tax cuts over the past 15 years or so. In 2007, the rate was cut from 33% to 30% and then in 2010, as part of the rebalancing that took place under Bill English with the increase of GST from 12.5%, the corporate tax rate was cut to 28% where it remained since.

As I’ve discussed previously, there has been a long running global trend towards lower corporate tax rates. But that has slowed in recent years, first because of the effect of the Global Financial Crisis and secondly, the fiscal shock to government finances because of the COVID-19 pandemic. As a result, according to the OECD in 2023, corporate tax rates rose generally across the board. Nevertheless, we are out of sync at the headline rate level.

More to investment than the corporate tax rate and will it work?

A lower corporate tax is undoubtedly attractive. However, the tax rate needs to be seen in context with what other incentives are available. Overseas companies and investors are very focused on what else might be on the table. A lower company tax rate would certainly be attractive, so the suggestion has been met with enthusiasm by some. Others are a bit more sceptical. Economist Ed Miller noted that when the effect of the corporate tax cuts in 2007 and 2010 are considered there does not seem to be any significant increase in foreign direct investment as a result.

The last tax working group didn’t see overwhelming evidence to support the theory that lower tax cuts at lower corporate tax rate would attract investment.

Problems and an alternative

There’s a flip side to this though, and it’s tied into the Government’s intention of restoring a surplus. Our corporate tax rate is not only above the OECD average, but our corporate tax take is also high by world standards. According to OECD statistics, 14% of the total tax receipts in New Zealand for 2022 came from company tax, whereas around the OECD the average is 12%.

So, if the Government, in an attempt to boost economic growth, is going to cut the corporate tax rate, it must then look at other alternatives to replace the lost revenue. One of the things it did back in 2010 and which it has already repeated, was to remove depreciation on all buildings. Depreciation for commercial buildings was restored under Labour but then removed again from the start of the current tax year on 1st April 2024.

A counter argument to the Government’s proposal for corporate tax cuts would be that enhanced depreciation allowances, including restoration of commercial building depreciation, which would include factories, might be a more effective approach than across the board tax cut.

How to replace lost tax revenue?

But if the Government is thinking of a corporate tax cut, and that does seem to be the case, what counter measures could they take to ensure that it is not fiscally too draining on the resources? One option might be that the availability of imputation credits may be restricted. For example, it might be that you can elect to have a lower corporate tax rate, but you imputation credits are no longer available to for shareholders.

As an aside, imputation (sometimes called franking) credit regimes were very popular during the 1980s, but gradually fell out of favour over time, mainly because, or in part because the European Court ruled that imputation credits or franking credits have to be available to all shareholders resident in the EU. After the German government lost this case its response was to heavily restrict the use of franking credits.

Change the tax treatment of Portfolio Investment Entities?

Another option might be to review the taxation of portfolio investment entities held by persons with effective marginal tax rates above the 28%. To quickly recap, Portfolio Investment Entities (PIEs) have a tax rate of 28%, equal to the company tax rate, which is also the maximum prescribed investor rate for individuals. So, there is actually a tax saving opportunity for individuals whose other income is taxed above the 28% rate for PIEs.

The Government might look at this, decide that will no longer apply and instead income from PIEs will be taxed at the person’s marginal rate. That could raise sufficient sums to partially offset the effect of a lower corporate tax rate.

The Finance Minister also mentioned reforming the Foreign Investment Fund regime, which is currently being considered by Inland Revenue and made some encouraging sounds about that potentially being an option.

We shall see. No doubt there’s a lot of work going on in Treasury and Inland Revenue looking at these options. All will be revealed in the Budget on 22nd May.

A threat to our Digital Services Tax

As covered in our first podcast of the year, one of President Trump’s initial executive orders withdrew the United States from the OECD Two-Pillar international tax deal. I drew attention to the second paragraph of that Executive Order, which directed the US Treasury to consider taking actions against other jurisdictions for tax actions which are potentially prejudicial to American interests.

Vernon Small, who was an advisor to the former Minister of Revenue, David Parker, now writes a weekly column in the Sunday Star-Times has picked up on this point noting that “Treasury has budgeted to rake in $479 million between January 2026 and June 2029 from a 3% Digital Services Tax (DST) on tech giants like Google and Meta.”

This, according to Small, “is an heroic piece of forecasting given current uncertainties and the provision for delaying collections until 2030 if progress is made on a multilateral approach through the OECD.”

And then the crunch point:

“Trump has bosom buddies in high places in the industry with Elon Musk first amongst them, and Mark Zuckerberg making a play for the new US administration’s affections.

Trump has promised to retaliate against discriminatory or extra-territorial taxes aimed at US interests. So the DST could be a prime target.”

Vernon Small is underlining the potential threat to our revenue base and our sovereign right to tax. If the OECD deal does fall over there are a number of countries including Canada, no longer America’s best friend, it seems, with DSTs ready to go. So there’s a whole potential for a tax war.

The Trump threat to tax administration

But equally worryingly, coming out of the United States is something about the question of bureaucratic independence from the executive. This might sound an arcane issue but it’s actually quite important to the independence of tax authorities.

One of the first actions of the Trump administration was to sack 17 Federal Inspectors-general. There’s also a move to put all Federal Government employees on the basis that they serve at the pleasure of the President. This would mean that an employee could be fired without the need for cause as the American terminology puts it.

Project 2025’s Schedule F

The implications of this have been picked up by Francis Fukuyama, the author of the famous The End of History essay written in the wake of the collapse of the Soviet Union and the end of the Cold War.

Writing for the Persuasion Substack under the title Schedule F is Here (and it’s much worse than you thought) Fukuyama wrote:

‘ “For cause” protection means that the official cannot be removed except under specific and severe conditions, like committing a crime or behaving corruptly. And now many individuals have been moved, in effect, to Schedule F because they are said to serve at the pleasure of the President.

Consider what this may mean if Trump hand picks a new Internal Revenue Service chief, that individual can be pressured by the Government to order audits of journalists, CEOs, NGOs and NGO leaders. Removal of Inspectors General will cripple the public’s ability to hold his administration accountable.’

Trump’s decision to move all Federal employees to Schedule F status is a step towards autocracy. What perhaps we all need to keep in mind is that the separation between the Commissioner of Inland Revenue and the Minister of Revenue is actually incredibly important. Yes, at times the Inland Revenue might do something which probably might embarrass the Minister of Revenue, but he cannot directly intervene in Inland Revenue’s operations.

A key part of a well-functioning democracy is that civil servants can act independently from their nominally political superiors. Fukuyama is right to say we should therefore have some concern coming at what’s happening in, in the United States because it does seem to be centralising power very rapidly around the President. The .potential for mischief is therefore enhanced as a result, and don’t think that such a step ultimately doesn’t have tax consequences.

Latest on the changes to the United Kingdom ‘non-dom’ regime

On a more positive note, last year I discussed the changes to the so-called ‘non-dom’ regime in the United Kingdom. This is where persons who are not domiciled in the UK have a special basis of taxation. Basically, they’re not taxed on income and gains which are not remitted to the UK.

This is a significant concession which is ending with effect from 5th April this year when it will be replaced by something which is more akin to our transitional resident’s exemption. This is pretty important for the approximately 300,000 Britons like me who’ve migrated here, plus the significant number of Kiwis who have assets in the UK or family going to the UK but have retained assets here. All of this group are potentially within the scope of these reforms.

There’s been a fair amount of push back on the reforms together with concerns that there will be a flight effect as wealthy, ‘Non-doms’ leave the UK. The UK Labour Government has been under pressure to make some changes to the proposals.

In response, the Chancellor of the Exchequer (Finance Minister) Rachel Reeves announced a concession (ironically at the gathering of the super-wealth at Davos) which will increase what’s called the temporary repatriation concession.

This concession will allow non-doms a three year window to pay a temporary repatriation charge on designated foreign income and capital gains so that they can subsequently be remitted to the UK without any further tax. The temporary repatriation charge will initially be 12% before rising eventually to 15% in the year ended 5th April 2028. For comparison, without the concession remitted income would be taxed at rates up to 45% and remitted capital gains would be subject to capital gains tax at 24%.

There’s a lot of opportunity here for potential tax savings for those who could be affected or will be affected by the proposed change to the non-dom regime. We’re still working through all of the implications but we will be updating our clients and bringing you developments as they arise.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

The aim is to develop a corporate tax database which is going to be available to tax policy researchers and policy makers about corporate tax rates, effective tax rates, tax incentives for research and development and other topics such as withholding taxes. Increasingly, the amount of information includes anonymised and aggregated country by country reporting data, which provides an overview of the global tax and economic activities of thousands of large multinational enterprises operating worldwide. This year’s report covers 8000 such enterprises.

The detailed statistics in the report are mostly from the 2021 calendar year although some 2022 data is included. The report does take into account the statutory tax rates currently in force.

Increased country by country reporting and more reporting generally is part of the 15 actions within BEPS. The report sets out why this is important:

“Action 11 noted the lack of available and high-quality data on corporate taxation is a major limitation to the measurement and monitoring of the scale of BEPS and the impact of the measures agreed to be implemented under the OECD/G20 BEPS Project.”

Corporate tax rates are stabilising

The headline summary is that corporate tax revenues remain important, but statutory corporate tax rates as the report are now showing signs of having stabilised after pretty near two decades of decline. During the period between 2000 and 2024 the average statutory tax rate declined from about 28% in 2000 to 21.7% in 2019. However, between 2019 and through to 2024, it has remained relatively stable at a rate of 21.7% in 2019 and 21.1% in 2024. I think stabilisation is a trend that’s going to continue.

Who knows, though, if the possible re-election of Donald Trump may change this. But I think governments balance sheets worldwide have been weakened considerably by the double whammy of the Global Financial Crisis and then the pandemic. I therefore think the opportunities to actually cut corporate tax rates further are quite limited, but we shall see.

Just to put New Zealand in context, back in 2000, our corporate tax rate was 33%. With effect from 1st April 2008, it was reduced to 30% and then on 1st April 2011 it was reduced to its current level of 28%. Across the ditch Australia has had a 30% corporate tax rate since 2001.

There’s interesting data about the importance of the corporate tax take. On average for the 2021 year, which was also a pandemic affected year, corporate tax revenue represented 16% of all tax revenues. New Zealand is in line with that average, but as a percentage of GDP, the OECD average was 3.3% whereas here it was considerably higher at 5.7%.

The report also considers effective average tax rates (EATRs) and examines the effect of tax incentives such as more generous tax depreciation compared with true economic deprecation. Again, according to the report effective average tax rates have remained relatively stable falling slightly from 20.9% in 2019 to 20.2% in 2023. Median effective average tax rates were 22.8% in 2019 and practically unchanged at 22.7% in 2023. Meanwhile, New Zealand’s effective marginal effective average tax rate is still relatively close to our statutory tax rate of 28%.

But…a narrowing tax base?

Chapter 4 of the report discusses effective and marginal tax rates and has some interesting commentary around declines of effective marginal tax rates (EMTRs). The report notes

“The stability of EATRs combined with declines in EMTRs suggests a narrowing of tax bases in the sample, notably through an increase in the generosity of depreciation provisions. Examining the asset breakdown shows these trends have been driven by increased generosity of depreciation of tangible and intangible assets, as opposed to buildings and inventories.”

I think some of this might be part of the response to the pandemic. New Zealand is noted being alongside Argentina, Japan, Papua New Guinea and Peru as having a higher effective marginal tax rate because we’ve got less generous depreciation rules. (This has become more so with the imminent withdrawal of building depreciation).

Research and development incentives

Chapter 5 looks at tax incentives for research and development, noting that they’ve become more generous over the past 20 years or so. 33 out of 38 OECD jurisdictions offer tax relief from R&D expenditures in 2023, compared with 19 in 2000. New Zealand is one of the new jurisdictions now offering R&D incentives. These are becoming more generous over time.

From a New Zealand perspective, we discuss the importance of R&D in boosting our productivity and we still could do more in that space. I’m inclined to the view I heard recently expressed that it’s better to give a tax incentive for it rather than get involved in the grant process. Because with a grant process, the companies can be restrained in what they have to spend because of the application process. Also, there’s a lot of effort involved with applying grants, less so with an R&D tax incentive, subject to Inland Revenue monitoring.

According to the report the level of direct government funding and tax support for business R&D in 2021 was about .12% of GDP, well below the OECD average of .2 of GDP. So, there’s still room for improvement although that’s something that’s been acknowledged across the board.

Chapter 6 looks at BEPS actions and notes that there’s a large number of controlled foreign corporation or control foreign company rules with apparently 53 jurisdictions having it in place in 2024. There’s also growth in the use of interest limitation rules. This is part of a growing trend in tax policy around the world to consider imposing restrictions on the deductibility of interest. Apparently, there are now over 100 interest limitation rules in place up from 67 jurisdictions back in 2019.

The dangers of following Ireland’s example

Chapter 7 has a breakdown of country by country reporting statistics with 52 jurisdictions out of a possible 101 submitting statistics to the OECD. As I mentioned earlier, this report includes the activities of over 8000 multinationals so there’s a lot of detail in here.

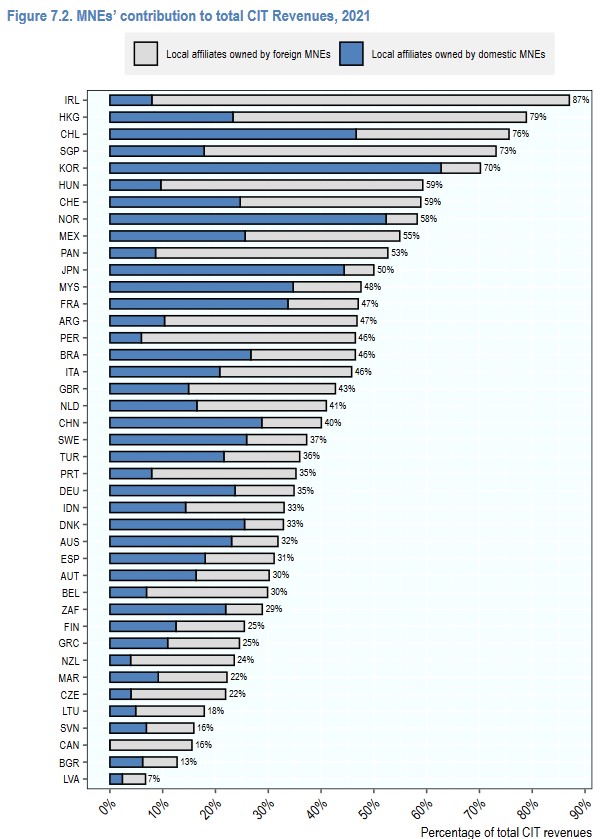

Several commentators including the New Zealand Initiative have recently mentioned Ireland as a potential model to follow. As is well known, Ireland has a very low corporate tax rate. I was therefore very intrigued by figure 7.2 on page 81 of the report, which illustrates the multinational enterprises contribution to local corporate income tax revenues in 2020.

As can be seen, 87% of Ireland’s corporate tax came from multinationals, and the vast majority of those multinationals were local affiliates owned by foreign multinationals. In fact, the Irish Treasury and the European Commission have expressed concern about the sustainability of Ireland’s corporate tax revenue because of the dependency on a few large multinationals.

New Zealand is near the opposite end of the scale with only 24% of corporate tax revenue coming from multinationals, probably three-quarters of which look to be from overseas owned. I think this is an extremely interesting stat which makes me wonder about whether New Zealand is attracting enough investment and whether we should have more multinationals of our own based overseas.

Yes, but is BEPS working?

In summarising key insights on BEPS from the Country by Country Report data the report makes this observation”

“There is evidence of misalignment between the location where profits are reported and the location where economic activities occur. The data show continuing differences in the distribution across jurisdiction groups of employees, tangible assets, and profits.” [page 87]

In other words, the report is basically saying there appears to be some profit shifting going on, but we don’t quite know enough about it. This gets to the heart of the idea behind the BEPS initiative, find out more about what’s happening and then fix it.

As I said the OECD’s corporate database is constantly being expanded so if you’re a bit of a stats guru there’s plenty to dive into and research. Overall, another interesting report highlighting how New Zealand’s corporate tax rate is at the higher end, but noting it also raises a lot of revenue relative to other jurisdictions.

Is that asset depreciable?

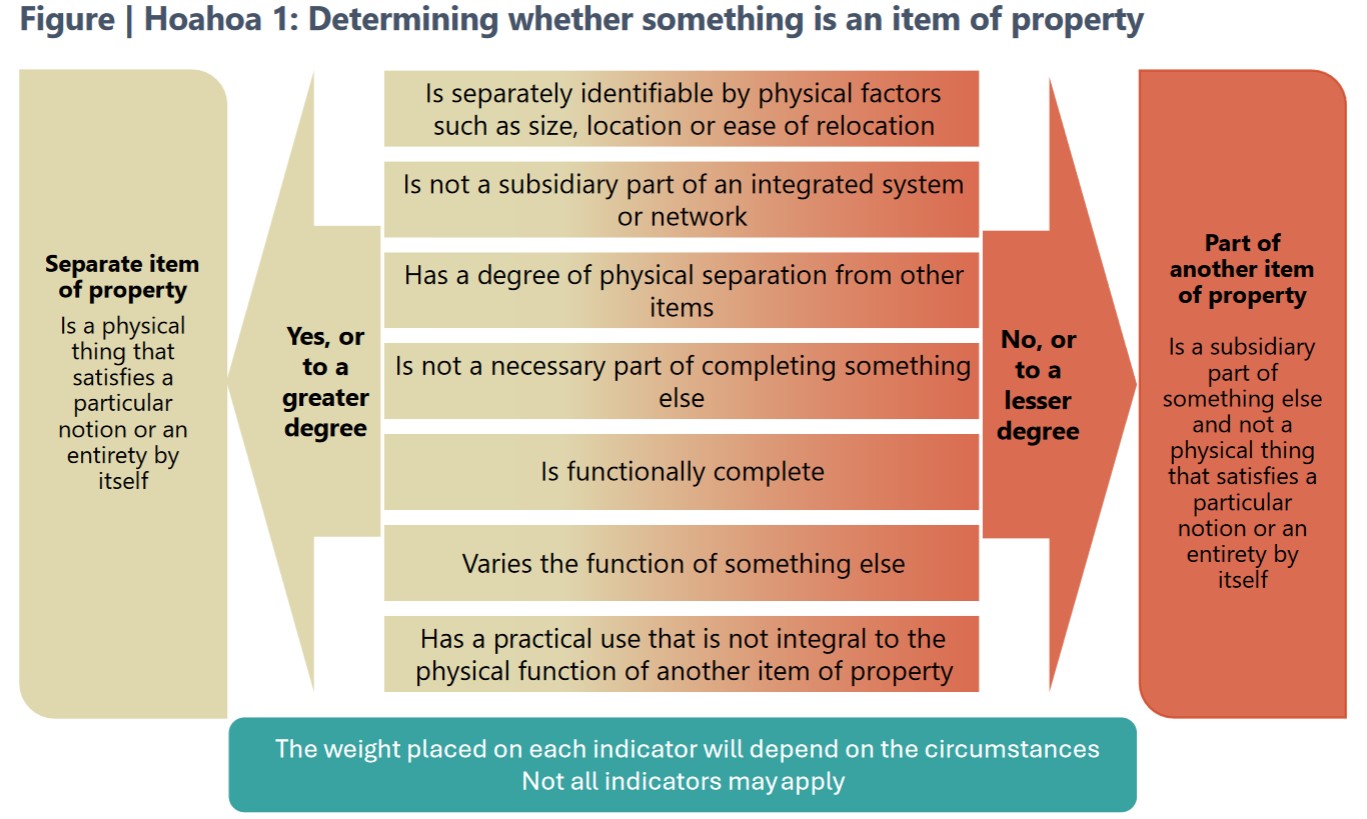

Moving on and picking up on depreciation one of the issues covered by the OECD stats, Inland Revenue has just released a draft interpretation statement for comment on identifying the relative relevant item or property for depreciation purposes. This is quite important because our depreciation regime is extremely detailed with a myriad of available rates across several categories.

This draft ties into several other related items of guidance such as residential rental properties depreciation, the question of deductibility of repairs and maintenance – if expenses are not deductible are they depreciable instead? There’s also QB 20/01 – can owners of existing residential parental properties claim deductions for costs incurred to meet healthy home standards? And finally, Interpretation Statement IS 22/04 relating to claiming depreciation on buildings. The imminent withdrawal (again) of building depreciation makes it very important now to maximise depreciation and to identify whether in fact that asset is part of the building or can be claimed separately. This draft is therefore pretty relevant.

The draft runs to 40 pages the last 15 or so pages of which are examples. There’s also a useful 6 page fact sheet accompanying it. Submissions are open until 29th August.

A post-hibernation bear is hungry…

Finally, as we discussed last week, one of the things that came out of Inland Revenue’s recent performance improvement review was for it to be more prominent in promoting what actions it has taken against non-compliant taxpayers. We’re seeing more of that this week when Inland Revenue was announced that an Auckland couple have been sentenced to three years in prison on tax evasion charges. The pair committed 69 tax related offences involving income tax and GST evasion amounting to about $750,000, together with another $80,000 in unaccounted for PAYE. The judge described it as very deliberate offending including deliberate under reporting of business income filing false returns, and even failing to file false returns once under investigation. The couple withheld information from their accountants and concealed the existence of what were described as “highly relevant bank accounts.” So pretty clear case here of tax evasion.

One thing of note that does slightly concern me is this offending occurred over a six year period between 2010 and 2015. That’s quite some time ago and I think Inland Revenue is much more on the case now. Even so you would hope that it doesn’t take 7-8 years or more to bring people to justice on this in the future.

The taxman cometh…

For an idea of how Inland Revenue’s increased activities might play out for your average person, this week’s episode of RNZ’s podcast The Detail discussed how Inland Revenue plans to utilise its additional funding. The episode focuses on the construction industry because of the sector’s long association with the proliferation of the “cashie”. Inland Revenue apparently gets 7,000 anonymous tip offs a year, many of which relate to tradies.

There’s some very interesting commentary from Malcolm Fleming, the New Zealand Certified Builders Association chief executive. He rightly points the finger back at the public for this issue. As he notes, nobody asks their accountant or lawyer ‘Well, how much is it for cash?’ On the other hand, the public seems to be happy to try this tactic with builders and others in the construction industry. On the question of tax evasion and cashies, maybe quite a few people should be looking in the mirror about that rather than pointing the finger elsewhere. It’s a very valid point.

The episode is well worth a listen; it highlights more of what Inland Revenue is currently doing. It’s now doing unannounced site visits to construction sites, for example, which I’m sure would alarm some businesses. But to be fair it also points out most small businesses are run on the straight and narrow. They are perhaps poorly capitalised with overworked owners who are also the main administrator. In many cases the question of tax arrears is more one of poor administration rather than in the case of the couple who were jailed, deliberate malfeasance.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The story begins in January 2010 when the Victoria University of Wellington Tax Working Group (the VUW TWG) released its report. The VUW TWG’s key recommendation was for the personal, trust and company income tax rates to be aligned as far as possible. This would involve a reduction in the top personal income tax rate from 38% to 33%. The VUW TWG also commented on the need for the company income tax rate to remain competitive.

The VUW TWG also recommended broadening the tax base “to address some of the existing biases in the tax system and to improve its efficiency and sustainability.”It then noted that base-broadening would be “required if there are to be reductions in corporate and personal tax rates while maintaining tax revenue levels.” The VUW TWG suggested that one such base-broadening measure could be an increase in the rate of GST from 12.5% to 15%. Another measure could be “Removing tax depreciation on buildings (or certain categories of buildings) if empirical evidence shows that they do not depreciate in value.”

The evidence presented to the VUW TWG indicated commercial and industrial properties did in fact depreciate in value. However, this didn’t appear to be the case for residential properties.

Accordingly, the initial costings for the 2010 Budget only proposed the removal of depreciation on residential properties. This would raise approximately $340 million in its first year which would help pay for the proposed income tax cuts. Once it was decided to reduce the company tax rate from 30% to 28% (a measure expected to cost $410 million in its first year), the decision was also taken to remove depreciation from all buildings. This raised a further $345 million towards the personal income and company tax cuts.

The National Government duly adopted the VUW TWG’s tax rate alignment proposals, announcing these in its 2010 Budget released on 20th May. With effect from 1 October 2010 personal income tax rates and thresholds would be adjusted and the present top personal rate of 33% introduced. The rate of GST would increase to 15% with effect from the same date and tax depreciation on all buildings would be removed with effect from the start of the 2011-12 income year (1 April 2011 for most taxpayers).

Then the Canterbury Earthquakes happened.

By 1 April 2011 it was quite apparent that owners of commercial and residential investment properties in Canterbury faced significant repair and/or rebuilding costs. Furthermore, all commercial property owners throughout New Zealand would also need to carry out seismic strengthening at a cost initially estimated to be almost $1.4 billion.

Owners of investment properties also had a big tax problem – was the cost of repair and seismic strengthening work tax deductible? Prior to 1 April 2011 if expenditure wasn’t deductible it could at least be depreciated. Repairs were probably deductible but investors rebuilding properties could no longer claim a depreciation deduction unless they could demonstrate the building’s life would be under 50 years. As for seismic strengthening the tax treatment was unclear – were they a repair and therefore deductible or an improvement and non-deductible?

This unsatisfactory state of affairs has continued since then. It caught the attention of the latest Tax Working Group (the Cullen TWG). It noted that the withdrawal of depreciation now meant that by 2015 New Zealand had the highest effective tax rate for foreign investment into both manufacturing plants and office buildings among OECD countries.

The Cullen TWG final report therefore recommended the Government consider restoring depreciation deductions for buildings “if there is an extension of the taxation of capital gains”. Alternatively, the reinstatement could be on a partial basis either for seismic strengthening, multi-unit residential buildings or maybe industrial, commercial and multi-unit residential buildings.

The Cullen TWG estimated the fiscal costs over five years of these various options as between $70 million (seismic strengthening only) and $1.46 billion (industrial, commercial and multi-unit residential buildings).[1] They were, of course, conditional on the availability of additional revenue from the extension of the taxation of capital gains.

As we know, that isn’t happening but fortunately the treatment of seismic strengthening is one of the Cullen TWG’s recommendations which is a high priority for inclusion in Inland Revenue’s tax work policy programme. Frankly, nearly nine years after the Canterbury Earthquakes first hit, this is a well overdue move.

The Cullen TWG interim report in September 2018 also had some commentary on the effects of the reduction of company tax rates in 2010.

“The two most recent reductions in the company rate in New Zealand – in 2008 and 2011 – were not associated with an increase in foreign investment. In fact, the stock of foreign direct investment as a percentage of GDP trended down slightly in the following years. There was also no increase in the level of foreign investment relative to Australia, whose company rate was unchanged during that period.”[2]

In short, New Zealand didn’t get much return in the form of foreign direct investment for its cuts in the company tax rate.

There is perhaps one final irony at play here: holders of investment properties were among the fiercest critics of the Cullen Tax Working Group’s recommended capital gains tax. Did they win that battle at the cost of the loss of the reintroduction of building depreciation? If so, may that win turn out to be a Pyrrhic victory?

The Cullen TWG final report therefore recommended the Government consider restoring depreciation deductions for buildings “if there is an extension of the taxation of capital gains”. Alternatively, the reinstatement could be on a partial basis either for seismic strengthening, multi-unit residential buildings or maybe industrial, commercial and multi-unit residential buildings.

The Cullen TWG final report therefore recommended the Government consider restoring depreciation deductions for buildings “if there is an extension of the taxation of capital gains”. Alternatively, the reinstatement could be on a partial basis either for seismic strengthening, multi-unit residential buildings or maybe industrial, commercial and multi-unit residential buildings.