Canada loses patience and imposes a Digital Services Tax effective 1 January 2024

Inland Revenue appears to be gearing up for a fringe benefit tax initiative.

Late last week, in response to some questions about a review the charitable exemption that religious organisations enjoy, the Prime Minister responded he was “quite open” to the idea, adding “I’ve actually been thinking through the broader dimension of our charitable taxation regimes…We will certainly be looking at things like that this term.”

The hint that a review of the exemption religious organisations and churches enjoy provoked a testy response from Brian Tamaki, among others which was in turn rebuffed by the Finance Minister, Nicola Willis.

But this is a topic which keeps popping up and obviously people have some concerns about how the exemption operates. It was also reviewed in some depth by the last Tax Working Group.

So what’s the exemption worth?

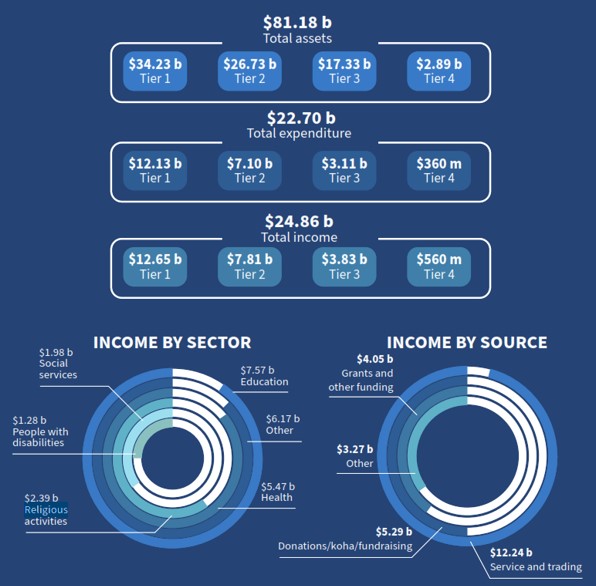

Putting some numbers around the value of the charitable exemption is a little difficult. Every Budget Treasury prepares a paper on the value what are called “Tax Expenditures” that is specific tax exemptions granted under the Income Tax Act. According to the Tax Expenditure statement prepared by Treasury for Budget 2023,

the forecast value for the year ended 31 March 2023 of charitable and other public benefit gifts given by companies was $32 million. In relation to the donations tax credit for charitable or other public benefits (including to religious organisations), value for the same period was estimated to be $315 million. (Which grossed up at 33% is ~$945 million.)

The annual report of Charities Services include a snapshot of the finances for 27,000 charities registered with it. According to the report for the year ended 30th June 2023 the income of the religious activities sector was $2.39 or just under 10% of the total income across all charities.

It’s interesting to consider charities income by source for the same period. $5.29 billion represented donations, koha and fundraising activities. Based on Treasury’s Tax Expenditures statement it appears donations tax credit or charitable donations by companies has been claimed for maybe only a billion dollars of this sum. Interestingly, about half of the total income charitable sector earns during the year comes from services and trading.

Overall Charities Services estimated that the total expenditure by charities was about $22.7 billion. In other words about $2.1 billion of the funds raised were not spent or distributed for whatever reason.

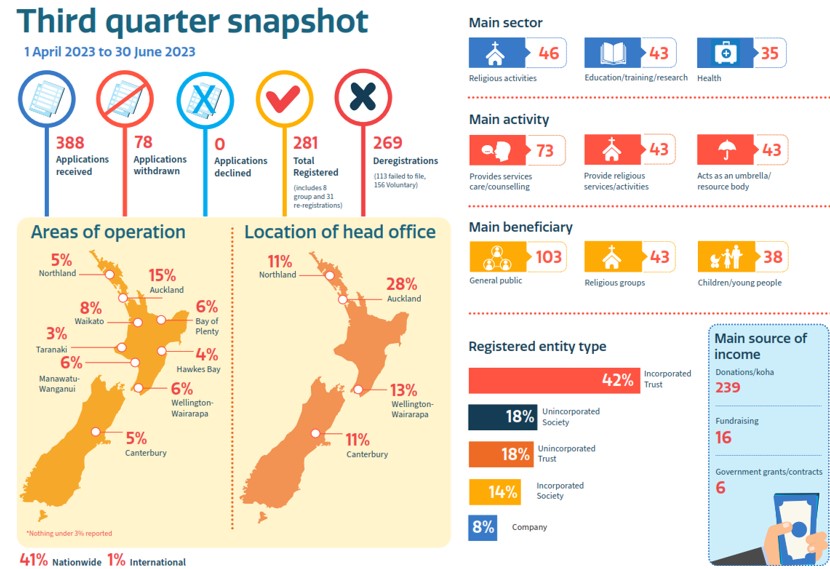

Charities Services also provides a quarterly snapshot of new registrations. The latest available is for the period to 30 June 2023 when it received 388 applications (of which 78 were subsequently withdrawn). Religious activities seem to represent a fairly substantial portion of the new registrations.

What did the Tax Working Group recommend?

The last Tax Working Group took a look at this issue and the best place to consider its views is in Chapter 16 of its interim report which sets out the issues involved.

In its final report the Tax Working Group noted it had “received many submissions regarding the treatment of business income for charities and whether the tax exemption for charitable business income confers an unfair advantage on the trading operations of charities.”

The Tax Working Group responded as follows:

“[39] It considers that the underlying issue is more about the extent to which charities are distributing or applying the surpluses from their activities for the benefit of the charitable purpose. If a charitable business regularly distributes its funds to its head charity or provides services connected with its charitable purposes, it will not accumulate capital faster than a tax paying business.

[40] The question then, is whether the broader policy tax settings for charities are encouraging appropriate levels of distribution. The Group recommends the Government periodically review the charitable sector’s use of what would otherwise be tax revenue to verify that the intended social outcomes are actually being achieved.

I think if the Government is going to review the charitable sector, and religious organisations in particular, the Tax Working Group’s recommendations will be starting point. In April 2019 when the last Government responded to the Tax Working Group’s eight recommendations on charities it noted that Inland Revenue’s Policy Division was already working on five of the recommendations. Two of the remaining three were under consideration for inclusion in Inland Revenue’s policy work programme. The other, in relation to whether New Zealand should apply a distinction between privately controlled foundations and other charitable organisations, would be undertaken by the Department of Internal Affairs, which oversees Charities Services. It’s likely the COVID pandemic disrupted this proposed work programme.

We may get a clue as to the Government’s thinking in next month’s budget, but I think the Government’s focus will be on getting its tax relief package out of the way first so Inland Revenue’s resources will be applied there. The Government and Inland Revenue may then look at this exemption, but I imagine given the fuss and general controversy around such a move, it’s probably relatively low priority. Maybe we’ll see something in the Budget.

Canada loses patience and introduces a digital services tax

There was an interesting development in the Canadian budget, which was released earlier this week. The Canadian Government has decided to push ahead with the introduction of a digital services tax (DST) on large tech companies. Over a five-year period, this was expected to raise ~C$5.9 billion (about NZ$7.3 billion).

Canada had held off for two years to allow for the conclusion of the international negotiations on Pillar 1 and Pillar 2 to conclude, but they’ve dragged on with no clear conclusion in sight. The Canadians have therefore decided to push the button on a DST commenting:

“In view of consecutive delays internationally in implementing the multilateral treaty, Canada cannot afford to wait before taking action….The government is moving ahead with its longstanding plan to enact a Digital Services Tax.”

The tax would begin to apply for the 2024 calendar year, with the first year covering taxable revenues earned since January 1st, 2022. Understandably, this has provoked a pretty vigorous reaction from the United States, where the headquarters of all these tech companies are situated.

What does that mean for us down here? Well, again, we may find out more in the Budget. The Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill which was enacted just before 31st March included legislation for our digital services tax. The Government is therefore in a position that it can watch to see if other countries follow Canada’s lead and then decide whether it should follow suit.

The whole purpose of the digital services tax legislation is to act as a backstop in the event the Two-Pillar solution does not reach a satisfactory conclusion. At the moment negotiations are stalled thanks to vigorous push back by the the companies most affected, such as Alphabet, the owner of Google, Amazon and Meta, owner of Facebook. It’s interesting to see this Canadian move and I wonder if other countries will push ahead with their own DSTs. There are quite a number lot of digital services taxes around the world, with many on hold pending the outcome on the Two-Pillar negotiations.

Taxing Google to help New Zealand media?

Just as an aside, as is well known the media in New Zealand is in desperate financial straits and a question that keeps coming popping up is taxing the digital giants more effectively. That’s because a substantial portion of the advertising revenue that in the past went to New Zealand media companies is now going overseas in the form of (little taxed) various licence payments and fees for services to the the likes of Alphabet and Meta. Watch this space I think things are about to get very interesting.

Inland Revenue gearing up for fringe benefit tax initiatives?

This week, Inland Revenue consolidated the various advice and commentary on fringe benefit tax advice it’s published over the years under a single link. This seems to me to be further signs that Inland Revenue is gearing up to launch a fringe benefit tax initiative. It follows comments by the Minister of Revenue Simon Watts, in several speeches in which he referred to Inland Revenue’s regulatory stewardship review of FBT released in 2022. I got the clear impression that he, and therefore Inland Revenue were keen to look further at this matter and investigate what revenue raising opportunities may arise through a more through stricter enforcement of the FBT rules.

As a very good article by Robyn Walker of Deloitte noted FBT is nearly 40 years old. It’s a very strong behavioural tax. It exists to stop people converting taxable salaries into non-taxable benefits. So, it never really should be an extensive tax raise revenue raiser.

That said, I think there have been issues particularly in relation to the status of twin cab utes and the work-related vehicle exemption as to whether there is sufficient enforcement going on. My expectation therefore is Inland Revenue is gearing up to launch a number of fringe benefit tax reviews and this small step consolidating its previous commentary and advice into a single space is another sign.

Got an idea to improve our tax system? Enter the Tax Policy Charitable Trust scholarship competition

Finally, this week, the Tax Policy Charitable Trust has announced its 2024 scholarship competition. This is designed to support the continuation of leading tax policy research and thinking and to inspire future tax policy leaders. Regular listeners to the podcast will know we’ve had past winners Nigel Jemson and Vivien Lei as guests, and I’m looking forward to meeting the next batch of scholarship recipients.

Entrants may submit proposals for propose significant reform of the New Zealand tax system, analyse the potential unintended consequences from existing laws and changes, and suggest changes to address them. It’s open to young tax professionals aged 35 and under on 1st January 2024 working in New Zealand with an interest in tax policy. The winning entry this year will receive a $10,000 cash prize. The runner up will receive $4000 and two other finalists will each receive $1000 each.

I look forward to seeing what comes out of this and hopefully we will have the winners on our podcast sometime in the future. In the meantime good luck to all those who enter.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue releases three special reports regarding the changes to the platform economy rules, the 39% trustee tax rate and the new 12% offshore gambling duty

Under the banner “Cut your excuses and sort your tax” Inland Revenue last Monday issued what it called a “last chance warning to the construction sector” to do the right thing and get on top of their tax obligations. The release advises that if people do the right thing, then Inland Revenue will help them. If they don’t, Inland Revenue will find them and start follow up action.

Richard Philp, a spokesperson for Inland Revenue, commented;

“Most people and businesses in New Zealand pay tax in full and on time but there is a core group who don’t. … we also know that while some are struggling just to keep up with the everyday grind, others are actively avoiding their tax obligations.”

Tax evading tradies?

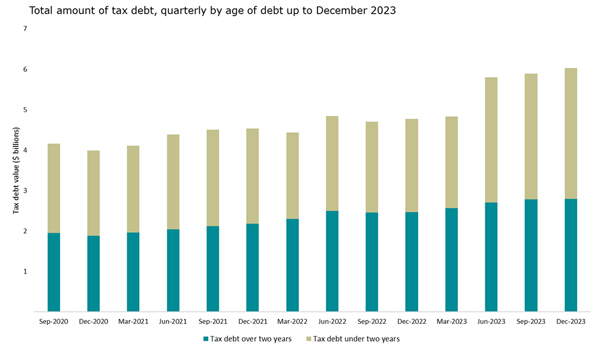

Apparently, tax debt is high in the construction sector and there’s also a fair amount of cash jobs apparently happening in the sector. The Inland Revenue release commented that across all sectors, it gets about nearly 7,000 anonymous tip offs about cash jobs and the like each year noting “Construction is the industry most anonymously reported to Inland Revenue”.

The media release is silent about the extent of the debt within the sector, but we do know from the latest statistics as of 31st December 2023, that tax debt over two years old has increased to from $2.5 billion in December 2022 to $2.8 billion in December 2023.

ADVERTISING

Understandably, with the Government’s books under pressure, Inland Revenue is keen to collect as much of this overdue debt as quickly as possible. This is probably the first of many such campaigns where we will see Inland Revenue taking additional action. And remember, under the Coalition agreement, additional resources have been promised to Inland Revenue for investigation work.

In this particular campaign, Inland Revenue is saying it’s going to issue emails and letters to 40,000 taxpayers in the construction industry who have either outstanding tax debt or tax returns, or both. It then specifies that 2,500 of those will be contacted by text message, asking if they would like to support to get their outstanding tax sorted. There will be a follow up call if the taxpayers they respond that they do want help. Inland Revenue will also be carrying out site visits to key locations across the country.

As I said, this is likely to be the first of several initiatives we’re going to see from Inland Revenue. I would be interested in seeing some specific stats around the proportion of debt and the composition of debt and get an understanding of what sort of businesses are struggling here. It will also be interesting to see how successful this campaign turns out to be.

More on the new GST rules for online marketplaces

Last week I discussed the confusion that seems to have arisen following the introduction of new GST rules from 1st April. These rules affect people who are not GST registered but provide services through such apps as Airbnb, Bookabach and Uber.

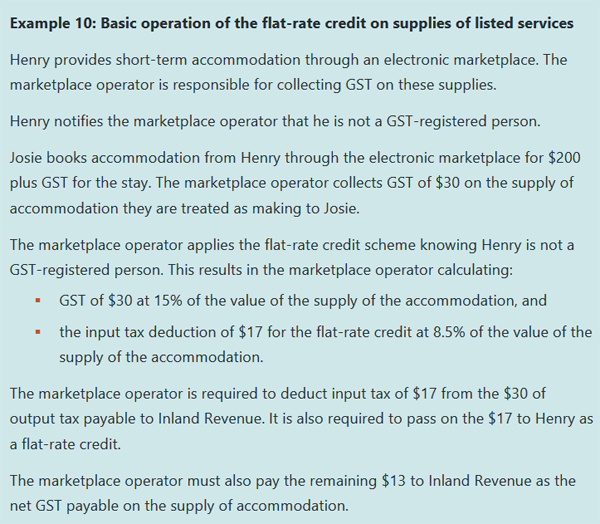

This week, Inland Revenue released three special reports relating to the new legislation and one of these is on accommodation and transportation services supplied through online marketplaces. In fact, this is an updated version of a report previously issued in June last year. The report has been updated to include the changes that took effect as of the start of this month and in particular how the flat-rate credit scheme operates.

Changes to online marketplace operators

Under the new rules, so-called online marketplace operators such as Airbnb, Uber and Bookabach will charge GST on all bookings made through them. However, the person who actually provides the ride or the accommodation may not be GST registered. This is where the flat-rate credit scheme comes into effect as the following example illustrates:

The full report is 68 pages so there’s plenty more to dive into.

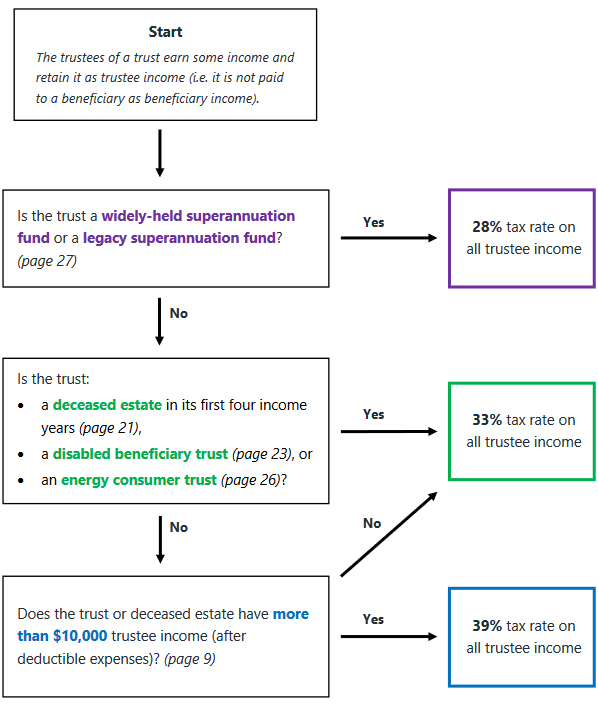

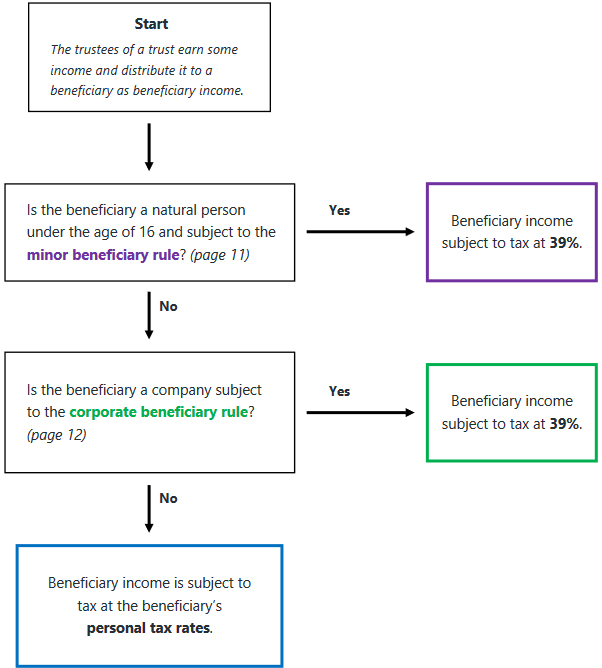

Special report on 39% trustee rate

One of the other reports that was issued is on the application of the trustee rate of 39%. Basically, trustee income is the net income of the trust, which has not been distributed to beneficiaries. The 30-page report explains the basic provisions about “beneficiary income” and “trustee income” together with a couple of useful flow charts.

Trustee income flowchart

Beneficiary income flowchart

The report references the minor beneficiary rule which applies where the beneficiary is a natural person under the age of 16. In such a case only $1,000 of income per year can be distributed to that person as beneficiary income and be taxed at that person’s marginal tax rate, presumably below 39%. Under the new rules, any beneficiary income in excess of $1,000 paid to a minor would be taxed at 39%.

Overall, this is useful guidance. Just remember the $10,000 threshold is all or nothing: if trustee income is $10,000 or less, the trustee tax rate that applies is 33%, but if it’s $10,001 then it’s 39% on everything.

The third report is on the proposed offshore gambling duty, which takes effect from 1st of July and will apply to online gambling provided by offshore operators to New Zealand residents.

The bright-line test and tax evasion – a couple of useful real-life case studies

Finally, this week a couple of interesting Technical Decision Summaries from Inland Revenue. Technical Decision Summaries are anonymised summaries of some interesting cases that Inland Revenue’s Tax Counsel Office has encountered either through tax disputes and investigations or applications for binding rulings.

The first one, TDS 24/06, is an application for a ruling regarding whether the bright-line test or section CB 14 of the Income Tax Act would apply. The facts are complicated but involve three sections of land currently owned by the ruling applicant.

The applicant had initially acquired one section outright before his spouse and another co-owner acquired interests as tenants in common. Over time, the applicants proportion of the ownership changed until at the time his spouse died the property was held 50% as tenants in common with his late spouse. The second section was owned 50% each as tenants in common with his late spouse. After her death her 50% interest had passed to him under her will. The third section was owned by the applicant and his late spouse as joint tenants. Following her death, her interest was automatically transmitted to him.

The ruling applicant was concerned about the treatment of future sales. Would the bright-line test apply or failing that, would section CB 14? This section is a little used provision and applies where there’s been a disposal within 10 years of acquisition and during that time there’s been a 20% more increase in value of the land thanks to a change in zoning, or removal of restrictions.

The Tax Counsel Office concluded neither the bright-line test nor section CB 14 would apply. This is obviously a good result for the taxpayer but it’s actually also a good example, of how you can apply for a ruling to get Inland Revenue’s interpretation on a tax issue. You don’t necessarily have to follow it, but if you don’t, you better have good reasons for not doing so.

Fiddling the books and getting found out

On the other hand, TDS 24/07 involved suppressed cash sales, GST and income tax evasion and shortfall penalties. The taxpayer carried on a restaurant business which was registered for income tax and GST. Inland Revenue’s Customer Compliance Services (CCS) investigated the company and formed the view that there was fraudulent activity going on. There was suppression of cash sales, and the taxpayer was under returning GST and income tax.

CCS reassessed the taxpayer’s GST and income tax returns for the relevant periods and they increased the taxable revenue for suppressed cash sales based on analysis of point of sale data, the taxpayer’s bank statements and industry benchmarking.

Industry benchmarking – an underused tool?

Just on industry benchmarking, I think Inland Revenue ought to be much more public about its data here and warn taxpayers there are benchmarks against which it will measure your business. It has done so in the past, but I think the combination of Business Transformation and then the pandemic interrupted progress in this space.

What people should remember is, Inland Revenue has some of the best data available anywhere about measuring industry benchmarking. I believe it should be making this much more public so that it can serve as an early warning shot for businesses that think they can suppress income. Everyone loses when this happens. Gresham’s law about bad money driving out the good is very applicable here, because businesses which are not tax compliant are undercutting those businesses which are following the rules. This is not a healthy situation as it leads to considerable frustration and anger and if not dealt with, will just simply encourage more of the same behaviour.

Tax evasion? Have a 150% shortfall penalty

In this particular case, the taxpayer’s fraud was identified, and GST and income tax reassessments followed. In addition, Inland Revenue also imposed tax evasion shortfall penalties, which are 150% of the tax involved. These evasion shortfall penalties were reduced by 50% for previous good behaviour, but that’s still represents a penalty of 75% of the tax and GST evaded.

Unsurprisingly, the taxpayer counter-filed a Notice of Proposed Adjustment under the formal dispute process, and the dispute ended up with the Adjudication Unit, which is run by the Tax Counsel Office as part of the formal dispute process. The Adjudication Unit did not accept the taxpayer’s counter arguments, including an attempt to claim an income tax and GST input tax deduction for the cost of fresh produce purchased with cash. The problem was there was no supporting evidence for this claim, so the Adjudication Unit probably found it easy to reject it. The Adjudication Unit ruled not only was the tax due, but the penalties were also correctly imposed.

Get ready for more Inland Revenue action

Circling back to our first story, this TDS illustrates what lies ahead for those in the construction industry who have been suppressing income. As I said, I do think Inland Revenue should make everyone more aware of its benchmarking data which would be a warning for would be tax evaders. It’s pretty clear from the announcement about the construction industry that Inland Revenue is gearing up for many campaigns targeting debt arrears and clamping down on tax evasion in particular industries. As always, we will keep you updated as to developments in those areas as they happen.

On that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

This week our guest is Tracey Lloyd, Service Leader Compliance Strategy and Innovation at Inland Revenue. We discuss how Inland Revenue’s new START system enables it to detect fraud.

TB: My guest this week is Tracey Lloyd, Service Leader, Compliance Strategy and Innovation at Inland Revenue. Kia ora Tracey, thanks for coming along.

Tracey Lloyd: Thank you for asking me.

TB: What’s your role within Inland Revenue? What does Compliance Strategy and Innovation mean?

TL: OK, so I’m the service leader of a relatively new unit in Inland Revenue called Compliance Strategy and Innovation or CSI for short. During Inland Revenue’s Business Transformation, we introduced our brand-new computer solution called START (Simplified Taxation and Revenue Technology). I oversaw the team that was responsible for utilising the analytical tools of that system once Business Transformation was finished. CSI was designed to take over and expand the work that we had been doing. It’s been in existence for about 20 months now and there’s 25 of us, including me.

TB: CSI Inland Revenue sounds very ominous but joking aside you’ve got these new tools that Business Transformation has provided and other Inland Revenue officials have told me that it has greatly enhanced your capabilities. How have you deployed those capabilities? What does CSI do in this case?

TL: We’re basically using intelligence to lead our approach to compliance. We combine insights from our customer segments, what our customers are saying, what our people are seeing, our systems, the tax and social policy products that we administer and analytics. We then connect the dots between all those different challenges to help the leadership teams make decisions about how to prioritise compliance initiatives.

It’s not just proactive compliance activities. It’s such things as sending out query letters, following up overdue debt overdue returns, but also working on educating our customers through tailored communications marketing campaigns and of course audit work.

Basically, we look at problems where our compliance is not good or where customers are confused. And we think how we can help; how can we help our customers and how can we improve compliance with the amazing tools that we now have available?

CSI – connecting the dots and checking COVID payments

TB: Where is an initiative that you’ve been able to deploy some of these tools, which has helped clear up confusion?

TL: Probably one which we should probably touch on is how CSI interacted with the Ministry of Social Development (MSD) and some of the various COVID products that Inland Revenue administered.

MSD had the wage subsidy, and I won’t cover our interactions with them over that. I just want to clarify that if someone was in business and eligible for the wage subsidy which was administered by MSD, then that wage subsidy had to be in their income tax return.

What we found within one week of the 2021 tax returns being able to be filed was that 80% of people who’d received the wage subsidy were not returning it.

TB: 80%? Wow!

TL: Yes, 80% and obviously we can identify that but then every single one of them needs some manual action and a contact for us to ask whether people are happy for us to include it because there was the odd one where the data wasn’t quite right, but only very rarely.

What we did is we worked with MSD who were super helpful, and we were able to upload those Wage Subsidy files and pre-populate that information within 10 days into everyone’s tax returns. That meant that we went from an 80% fail rate of people including it to a 20% fail rate where it was pre-populated, but people were perhaps changing that figure or deleting that figure out of their return before they submitted it.

TB: What happened then if they deleted or amended those numbers?

TL: The return would be stopped for manual review. We would contact the person and ask if there was a reason for the change, maybe they had paid some of it back to MSD. And so we would liaise over that to check that they returned the right amount.

TB: This group of people would be self-employed or shareholder employees because everyone’s else wage subsidies should have gone through PAYE?

TL: Yes, that’s right. If you were an employee, then there was no impact to you.

TB: The other COVID support payments, those were directly Inland Revenue’s responsibility?

TL: They were, so we had Covid Support and Resurgence Support Payments and the Small Business Cashflow Scheme.

CSI in action – detecting COVID fraud early

TB: I see today there’s a report about a Waikato sharemilker who was sentenced to home detention for fraudulently claiming Covid Support Payments and the Small Business Cashflow Scheme. https://www.ird.govt.nz/media-releases/2023/waikato-sharemilker-sentenc… How might you have picked this up?

TL: Well, a lot of the work that we did was at front end based on the application rather than letting the money out the door because it’s very difficult to recover once the money’s gone out.

We are obviously doing that audit activity because we’re starting to see prosecutions following on from those reviews. We will contact people and determine whether they fraudulently applied for it or applied in error.

But what we were able to use START for was to proactively stop those applications in the system based on running them across a whole lot of rules and then stop suspicious ones for manual review.

To give you an example of some of the rules that we ran such as duplicate bank accounts, or if someone had a few entities using the same bank account, that was usually a a trigger for us that there was some sort of identity theft potentially going on. We also had examples where we had no record of that particular customer being in business at all. We stopped applications completed from offshore, as you had to be a New Zealand based business.

TB: You would have identified those offshore applications through the domain and the IP address.

TL: That’s right. All that information was available to us. We also had people putting deceased persons on their employee schedule or the number of employees over lockdown were going up, that generated some questions from us. We found employees that were either children or very, very elderly.

Sometimes the same employee was on a large number of schedules, which also raises a number of questions. Currently one of my team is preparing for a prosecution relating to a Resurgence Support Payment claim.

Just on Resurgence Support Payments, applications used to open at 8:00 AM in the morning and there five or six different iterations over time. One time, something like four out of the first five applications that arrived within a couple of minutes after 8:00 AM were fraudulent. A lot of those claims were from offshore, but our systems were able to stop all of those.

In relation to Covid Support Payments we stopped 9% of all applications for manual review. That’s actually quite low if you think about it. 91% went automatically out the door overnight and people got the money that they desperately needed.

Of the 9% that we did stop, we declined 66% which is a very high percentage. Generally speaking, the ones that we did pay out after stopping for a manual review were people who had recently started in business. So we asked them for some proof of business and that type of stuff and then the application was fine. I know that’s no help to customers who had to wait, but did get the money in the end. But we did decline about 33,032 applications and we stopped $147 million from being erroneously issued to people who weren’t entitled.

With the Small Business Cashflow Scheme loan, we declined 67% of the applications we stopped and this amounted to $550 million.

TB: I mean the Small Business Cashflow Scheme was in many ways bigger than the various Covid support payments, I think it ran to over $1.5 billion. [$2.3 billion per Inland Revenue’s Annual Report for 30 June 2022] So people attempted to borrow $550 million on top of what was already lent?

TL: Yes, that’s correct. It’s testament to the people that we had working on it and the new system that we were able to do it proactively instead of coming along afterwards and saying hey, you shouldn’t have got that money, can you pay it back because that’s very, very difficult.

TB: I mean the wage subsidy is a good example of a high trust environment. It was money out the door because we’re in the midst of the COVID crisis.

TL: That’s right, the wage subsidies were the first COVID product that was paid out.

Lessons from the Australian Tax Office TikTok GST scandal

TB: To give a comparison with another overseas tax agency that didn’t quite get it so right, there’s this ongoing scandal over the Australian Tax Office where these TikTok influencers basically said, “Here’s how to scam the ATO out of GST”. I think it’s over a billion dollars and counting. The ATO has admitted it really isn’t sure how big this scandal is, and that’s quite staggering.

I mean, what do you do about that? Could TikTok influencers do that here?

TL: We’re going to talk about Integrity Manager a little later but we’ve definitely had people send us snips of social media marketing along the lines of “Hey, give me your IRD number and I’ll get you a refund” but nothing quite to the extent of Australia.

We keep a very, very close eye on our own GST to ensure that nothing like that will happen in in New Zealand. We’ve spoken to our senior execs about it and we’re very comfortable that we would be able to react immediately if we saw any of that behaviour. But I mean that the numbers are just staggering over in Australia.

TB: To repeat a point I made earlier, conversations I’ve had with other Revenue officials is that if START hadn’t been available when COVID turned up, it would have been very difficult for Inland Revenue to have run any of these COVID support programmes. They probably would have all had to have been run out of MSD with a higher risk of fraud, perhaps.

TL: Yes. Or even just high trust model with payouts from Inland Revenue with no checking beforehand.

START and auto-assessment

TB: One of the great things that START did was to bring in the year-end auto-assessment routine. https://www.ird.govt.nz/income-tax/income-tax-for-individuals/what-happ… People no longer had to either go through a tax agent or the tax intermediaries and instead the majority of taxpayers who are salary-earners with all their income having tax withheld either through pay as you earn or through resident withholding tax are now on auto assessment.

You just mentioned Integrity Manager this is something that is part of this auto-assessment routing. How does it operate? Because you’re dealing with 2,000,000 taxpayers in six or seven weeks.

TL: I think our last auto-assessments had 3.2 million individual income tax returns were sent to customers and 88% of those required a customer to do absolutely nothing. I was one of those, I didn’t have to do absolutely anything.

We’ve discussed Decision Support Manager which we used for the COVID products and Integrity Manager is another amazing tool that we now have which stops returns with potential errors and fraud in them.

Every single tax return goes through Integrity Manager before it’s processed. We screened 10 million tax returns in the last year.

TB:Tax returns would not only be individual tax returns, but also GST returns which would be a big group and particularly the Pay As You Earn filings.

TL: The only one that doesn’t have rules through Integrity Manager are the PAYE employer schedules. That’s because we need to make sure that the deductions and entitlements get paid out as soon as possible. You know, Child Support and Student Loan, etcetera. But we will do some back work on that on those.

Basically, we review Non Resident Withholding Tax, Approved Issuer Levy, GST returns and donations. That’s another big group where we also run rules over returns. And so, while we had 10 million tax returns in the past year, over 200,000 were looked at to be manually reviewed because they hit a rule which raised some concern from us.

TB: That’s what 2% of all returns?

TL: Yes, a pretty small group. So, some of the main areas we look at are GST, income tax and donations. They’re our big ones and examples of some of the things that we review are changing pre-populated figures. You know, why are you changing them? Because we have already got that data. Another is making up figures even though we can check that against other data we hold. I think you could describe that as a frequent flyer, shall we say. Every year people just making up figures.

Snapshotting to prevent incorrect tax returns

TB: You gave an example at a recent ATAINZ conference where one person was constantly changing the online return until they got the right number and by that stage they had amended it 50 or 60 times.

TL: We call that Snapshot and it’s another tool in the new START system. It’s the ability for us to view activity in myIR. We also use it just as much internally. For example, every time I’m in the system it’s all recorded and for training purposes. So when we’ve got someone on the phone, I can hear the people sitting behind me saying, “OK, you’re in the wrong part of the return. You need to go to this particular tab to do what you’re trying to do”. We’re able to track where a person is and help them through the system.

But one of the sides things that’s come from that is that we’re actually able to look at what someone’s done while they’ve been filing their return. For example, we can see when people are adjusting figures, to see how big or small the refund is now and then going back and changing the figures. Doing this backwards and forwards and backwards and forwards countless times.

Now if you’re doing that type of behaviour, even either you’re really confused and you need some help from us, or you’re just making up figures. And so, we have the ability to see that and we’re also able to stop such returns.

Some of the other rules we can run identify an IP address which has been used to commit fraud in the past so we can red list that. Identity theft is an ongoing issue for us unfortunately.

Overclaimed donations and other “creative” deductions

TL: Other rules that we have include one for large school donations, which may possibly be private and therefore not allowed. Or large donations compared with total income. It may be totally legit, but let’s just ask a question about it and see how you how you go.

I mean in the past we’ve had people just making up figures and putting them in the return such as made-up employee share scheme figures. We’ve seen interest and resident withholding tax entries that are the same amount – $10,000 and $10,000. What we also see is that when people are making up figures to put in their return, they quite often make them all zeros. Nothing quite like a round number.

Over the last year to June 2023 year Integrity Manager reviews stopped $145 million of incorrect or fraudulent refunds dollars. $56 million of this was voluntarily disclosed by customers. Another $89 million of refunds were stopped after we engaged with the customer and asked them some questions.

With regards to some examples of non-business expenses, these have been a continual source of frustration for us. Under the auto-assessments system there are only four or five things that you can claim for. The one that most people claim for is for loss of income insurance. the main. But we get everything, literally everything coming through there.

One example I’ve got is someone had claimed just over $15,000 of non-business expenses and when we called to ask what it was, he said that he’d paid quite a lot of tax and his father-in-law suggested he claimed some of it back.

TB: Nothing like being honest.

TL: We did sort of point out that the amount of tax you pay is relevant to the amount of income that you and this person had earned a significant amount of income. We had another one where this person was only on salary and wages but had claimed $20,800 of non-business expenses. When we asked what they were, she said her son was at Auckland University and she was still supporting him. She thought she should be allowed to claim his expenses and added up his rent and groceries because he eats quite a lot. She did ask if we could put it in another box if that would help. But we said there was no other box that we could put that in.

But an example of a more deliberate fraud, shall we say we had someone who was receiving Working for Families but had no income at all. And then when we did some deep diving into their searches, we found fifteen other customers were linked to the same bank account. And a majority of those customers were overseas because we can do Customs checks.

TB: Yes, because you share information fairly frequently.

TL: We do very regularly.

TB: In my role we’re often determining when someone became tax-resident. We’ll tell a client go to Immigration and they’ll come back to you with the dates you arrived and left the country. Clients are often incredibly impressed how efficient Immigration is with providing those details. And I’ve been in a meeting where the file of information which had been shared from Customs and Immigration was literally about a foot high and I thought “We’re in a bit of trouble here.” Unsurprisingly, we didn’t win that case.

So, yes, a lot of information sharing regularly goes on. It’s a common theme in the podcast, but I think people do not understand just how much information is shared and how much information you can access.

TL: That was definitely something that we saw with the wage subsidy when we pre-populated returns. And you know people deleted the entry and we asked “Why?” and they actually admitted to us straight off the bat that they weren’t actually eligible for it.

And we’re just like “Well, we’re not sure what you want us to do about that because you did actually receive the money.” They didn’t obviously think that we would talk to MSD and get that information. While the pre-population was a second step, we were always getting that file with the income information.

Running information campaigns and engaging with migrant communities

TB: Inland Revenue sometimes runs campaigns based around this misinformation. Talking about expenses are I recall recently there was a campaign advising real estate agents about what they could claim. https://www.ird.govt.nz/pages/campaigns/realestateagents This arose because it had come to your attention that there seemed to be a lot of expenses being claimed. And I think the result of that campaign was the following tax year the amount of expenses claimed declined, is that right?

TL: That’s right. Integrity Manager was used because obviously we have BIC codes which tell us who’s a real estate agent. Yeah. And we’re able to look at the level of income compared with the level of expenditure. And it doesn’t necessarily always prove that there’s anything wrong, but it does beg a question and the number of very imaginative expenses that people claimed was huge.

And that’s why on our website now it’s very easy to find the real estate agents form which details what expenses you’re able to claim and what you cannot.

I think we also did that in a few different languages as well to hopefully help people understand the rules a little bit better because it can be different in other countries.

TB: Just to talk about other languages in there, there was a little snippet that came out of the report that was released in connection with the repealed Tax Principles Act. One of the comments about trust and Inland Revenue was that it was extremely high amongst migrant communities, and highest amongst Asian migrant communities. That’s credit to Inland Revenue for being able to build a level of trust there.

TL: Oh, thank you. Yes, our community compliance folks spend a lot of time working with our migrant communities and speaking to them in their own languages and going to trade fairs and community halls and so on. Helping people understand because they’re also entitled to social policy, which we need to make sure they get as well.

TB: That’s right. Inland Revenue is not just about taking tax off people. It also redistributes because it’s the key agency for distributing KiwiSaver, Working for Families, which is $2 billion and Child Support.

Inland Revenue and tax agents

TB: How important are tax agents to your role? Because we work with you on campaigns and we’ve seen increased engagement recently.

TL: Absolutely that’s certainly how it feels like to us. I mean, tax agents represent about 1.8 million customers to Inland Revenue. It’s a massive way for us to contact a huge customer group by using tax agents.

Many of the rules we’ve discussed when checking returns we don’t enable for tax agents because we just don’t see the same type of erroneous and fraudulent behaviour that we do with customers who aren’t represented by tax agents. You know, there’s always the odd one, but they’re very rare.

Tax can be really complex and tax agents are a critical part of making sure that people get it right. And as you know, we have regular meetings with Chartered Accountants Australia New Zealand and also with ATAINZ, which is how we met after I did a presentation at an ATAINZ workshop.

We share about what we’re doing with compliance, and you know how we can help. Quite often when we’re planning to do some sort of compliance campaign, the tax agents will be the first people that we contact to say, “Hey, this is what we’re gearing up to do, we’re just letting you know so that you can think about it in terms of your client base.”

Forthcoming campaigns on the shared economy and overdue Student Loan debt

TB: Speaking of which, any new compliance campaigns on the horizon?

TL: Well, there there’s a few that are sort of in the planning stages. Obviously, you would have heard about payment service providers with the new legislation. We’re getting that data and once we have that, obviously we will definitely kick off some campaigns around that.

We’ll be running a targeted campaign, focusing on raising awareness, educating and so on about ride sharing, food and beverage delivery and short stay accommodation. Trying to raise customers awareness and understanding as it applies from 1st April and some people might get caught out. We’ll soon start our next campaign on auto-assessments around just letting people know that’s coming soon.

The other big one that we’ve got on the go is about student loans. This targeted campaign is mostly focusing on overseas based borrowers who are in default. Only 26% of overseas borrowers are making the required repayments that they should be making on their loans whereas 94% of New Zealand based borrowers do.

The purpose of the campaign is to increase the overall compliance of student loan borrowing customers so that they understand their obligations when they leave New Zealand to perhaps go do their big OE and stuff that they’re still obligated to make repayments.

This particular campaign we’re slicing into nine specific segments to try and make our awareness campaigns a little bit more targeted and hopefully a little bit better at getting through to people. You might see some information on the sharing economy via LinkedIn, but you probably won’t see targeted paid advertising unless you’ve got a student loan debt or you’re doing a Uber side hustle.

TB: Quite a lot to ponder there about what CSI Inland Revenue is up to, but to wrap up what sort of message would you like to send Tracey. Like Liam Neeson in Taken we have the tools and we will find you?

TL: Pretty much. I mean obviously our first step is to make it as easy for people to get it right in the first place and we spend a lot of time reviewing how customers behave in the system so that we can help and maybe change the system to make it more intuitive for people. But you’re right, we’ve got these amazing tools and we’re using and utilising them all the time and we’re learning more and more about them. It’s a great system and it’s good for All New Zealanders.

TB: Computer projects are controversial but START has been an enormous project which was delivered on time and under budget. Just to put some numbers in context. You mentioned earlier about identifying $145 million of fraud. Inland Revenue’s annual operating budget is about $700 million so you pretty much pay for yourself very, very quickly.

On that note, Tracey, thank you so much for joining us. It’s been a pleasure having you on the Podcast.

TL: Thank you for inviting me.

TB: That’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Inland Revenue guidance on the new 39% trustee rate

Briefing the Minister

Tax credits or threshold adjustments?

The Finance Minister signed off 2023 rather like a Shortland Street season finale, leaving us all guessing as to the exact extent of the proposed tax cut package and when it might apply. We were told at the Half Year Economic Fiscal Update Mini-Budget on 20th December we could expect more details shortly. But now it’s February and we’re no wiser. It now appears likely we’ll have to wait until the Budget in May for full details.

A 39% trustee tax rate?

On the other hand, the business of government carries on and we will know early next month whether the coalition government will proceed with increasing the trustee tax rate to 39%. That’s when the Finance and Expenditure Committee reports back on the Taxation (Annual Rates for 2023-24, Multinational Tax, and Remedial Matters) Bill. This is the annual tax bill currently before Parliament which proposed the increase to 39%. It must be passed by 31st March.

The FEC heard oral submissions last week, and I note that (previous podcast guest) John Cantin thinks it’s most likely that the tax rate will go ahead. This is even though such evidence as we’ve seen suggests that a 39% tax rate for trusts probably represents over taxation of many trusts once the wider family context is considered.

I tend to agree with John that the rate increase will go ahead, in part because it is a base protection measure as it aligns the trustee rate with the top individual tax rate. But also, the Government will probably be grateful for some additional revenue to counterbalance the lost revenue from the proposed tax threshold adjustments. That said, I know a number of submissions proposed that some sort of de minimis threshold is introduced, and the rate of 39% will only apply on the excess.

Inland Revenue’s view on tax planning for the new 39% rate

Meantime, and rather helpfully, Inland Revenue released last Friday some high-level guidance about how it might perceive taxpayer transactions and structural changes ahead of a rate change. General Article GA 24/01 proposed increase in the trustee tax rate to 39% has been released in response to requests since the rate was proposed for guidance on how Inland Revenue might perceive some transactions.

GA 24/01 contains several examples of possible transactions and how Inland Revenue would view the transaction. The first example is a company owned by a trust which changes its dividend paying policy. Inland Revenue considers a company is entitled to change its dividend paying policy and while taking into account the funding needs of shareholders and applicable tax rates, it “is unlikely without more (such as artificial or contrived features) to be tax avoidance.”

The example then notes Inland Revenue might have concerns if the company could pay a dividend by crediting shareholder current accounts, but “objectively has no real ability to pay those credit balances if it was to be liquidated.” In other words, the company tries to pay a dividend ahead of the trustee rate increase but doesn’t have the funds to pay the dividends in cash in full.

Another example is of a trustee choosing to wind up a trust. Again, GA 24/01 suggests such a step is “unlikely without more (such as artificial or contrived features) to be tax avoidance.” GA 24/01 also looks at the question of trustees investing in Portfolio Investment Entities instead of other available investment options. The advantage here is that the maximum rate applicable to Portfolio Investment Entities is 28% Again, Inland Revenue concludes such a step is unlikely without artificial or contrived features to be tax avoidance.

That said, Inland Revenue is going to continue to gather information on trusts and something it has said would be of concern to it is where income is allocated to a beneficiary taxed at a lower rate, and then instead of actually being paid out or being fully available to the beneficiary, is resettled back on the trust. In effect, the beneficiary has not benefited from the distribution.

The allocation of income to a beneficiary, where the beneficiary actually doesn’t know of an allocation or has no expectation of receiving the income together with replacing dividend income with loans “in an artificial manner”, are other alternatives which would concern Inland Revenue if there’s no real commercial reality behind the arrangement. And then artificially altering the timing, ie: bringing forward or deferring any taxable deductible payment, particularly it’s linked to existing contractual terms or practise for the date of payment.

These are just a number of scenarios which might play out. And clearly Inland Revenue’s watching. As I said, we really won’t know what the state of play will be until early next month when the FEC reports back, and when it does, we’ll let you know. But as I said, the expectation I have is we should see that tax rate increase.

The Tax Principles Act may be gone but its first draft report lives on

Moving on, one of the first things the coalition government did was repeal the controversial Tax Principles Act. Nevertheless, the draft report that was due to be produced under the Tax Principles Act has been proactively released and it makes for some interesting reading.

The report gives a background as to why it’s being prepared, its reporting obligations, and it explains what are the tax principles that were measured. These were included in the Act – efficiency, horizontal equity, vertical equity, revenue integrity, compliance and administration costs, flexibility and adaptability and certainty and predictability. Incidentally, a lack of certainty and predictability was one of the objections that was made about the Tax Principles Act because didn’t go through the full generic tax policy process.

Inland Revenue was required to assess the principles, against four measurements:

Income distribution and income tax paid;

Distribution of exemptions from tax and of lower rates of taxation;

Perceptions of integrity of the tax system, and

Compliance with the law by taxpayers.

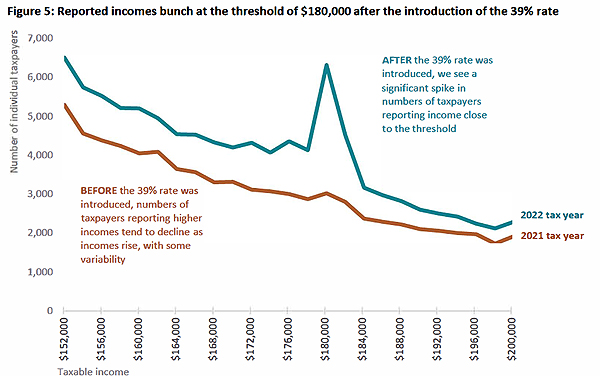

The report has lots of interesting graphs including the taxable income distribution for individuals for the 2022 tax year which shows a wee spike around the $180,000 mark.

I think that’s rather revealing even if there are apparently only 4,000 individuals involved. But still for those taxpayers you may need to have a good explanation of what’s going on.

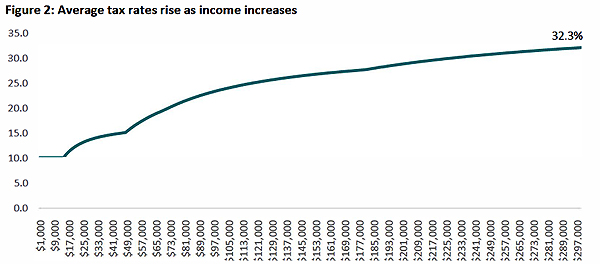

There’s a graph showing how average tax rates rise as income rises. This graph tops out at $300,000, by which point the average tax rate has risen to 32.3% for someone of that income.

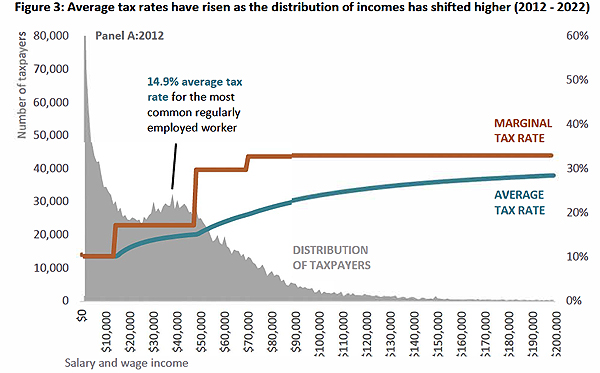

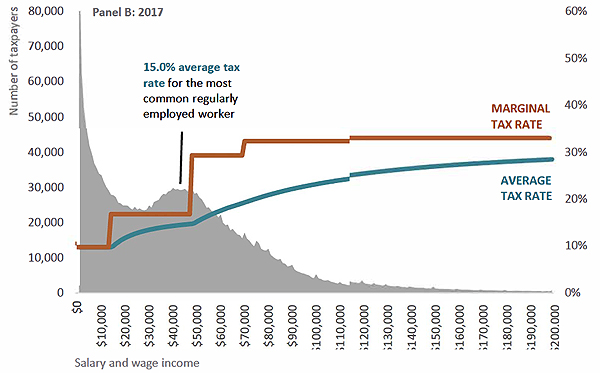

But what I thought was quite interesting were the graphs looking at the average tax rates from 2012 to 2022. In particular the graphs illustrated the effect of inflation combined with the non-adjustment of thresholds. That’s an issue I’ve talked about frequently and threshold adjustments we think will be at the core of the Government’s proposed tax relief package expected to be rolled out later this year.

The report notes between 2012 and 2017, the average tax rate for the most common regularly employed worker increased by 0.1 percentage points. Not too bad. But from 2017 to 2022 it increased by 1.2 percentage points. That’s quite a more significant example. Overall, in the period between 2012 and 2017 it rises from 14.9% to 15% and then rose between 2017 and 2022 to 16.2%.

This is the fiscal drag (or bracket creep) I discussed with Susan Edmunds of Stuff. It’s been an issue for quite some time. As wages rise faster, they drag persons on average incomes into a higher tax bracket. It will be interesting to see how the Government addresses it, and I’ll talk about that in a few minutes.

There’s plenty of other material to consider. There’s an interesting stat that the top decile of taxable income earners paid 44% of personal income tax. The report notes that the same group earned 33% of total income and suggests this is a better indicator of progressivity in the tax system than the fact that 44% of tax is paid by the top decile.

The arguments will rage around the progressivity and fairness, David Seymour of the Act Party for one has been talking about this area. Overall, there’s a lot to consider in the report. Interestingly, in the note to Cabinet regarding the repeal of the Tax Principles Act, the new Minister of Revenue Simon Watts suggested that much of this data could be made separately available, perhaps as part of Inland Revenue’s annual report. I hope we do see that, because for some time I’ve felt that the discussion around bracket creep, fiscal drag and thresholds has been sort of sidelined because governments have been not too keen to discuss it in great detail.

Briefing the Minister

Mentioning the new Minister of Revenue Simon Watts, another report released last Friday was the Briefing to the Incoming Minister. I think some of the data that’s been included in this draft report under the Tax Principles Act, would normally go into the Briefing for Incoming Minister.

What I found interesting in the Briefing was Inland Revenue’s discussion around where it’s at and the effect of the completion of the Business Transformation Programme which has allowed it to “deliver significant cost savings”. For example, the Briefing notes the amount of revenue collected for the year ended 30 June 2023 grew by 62.5% compared with the year ended 30 June 2016, the last full year before transformation began. Over the same period, the number of Inland Revenue full-time equivalents reduced by 29%.

There’s been a lot of talk about government cuts for the public sector, but I think the Briefing subtly, or not too subtly, you might say, raises a good question – if an organisation has managed to reduce its headcount by 29% and its funding is not tracked with inflation since 2017, which appears to be the measure for the basis of these public spending cuts, why would you add further cuts?

My view would be, and I think I wouldn’t be alone in thinking this amongst tax practitioners, is that Inland Revenue is under a bit of strain. We know it probably needs to boost its investigations efforts. So why it should be on the chopping block when it’s already done much of what any government would want it to do – more with less. But we’ll see how that plays out.

I thought the amount of commentary in the Briefing around the question of funding this point was quite interesting. It notes that for the year, to June 2024, the department gets about $800 million a year. And at October 31st 2023 its workforce was 4,231. Whereas back in June 2016 it was 5,662. And by the way, the report also notes the department has planned for taking a $13.9 million reduction for the year to June 2025, which was announced by the previous government in August 2023.

According to the Briefing funding would be running around about $700 million going forward, but then adds something the government should probably pay attention to.

“Our primary cost pressures in out years will be remuneration and inflationary cost pressures on technology as a service contracts, accommodation, leases and other operating costs. We are currently developing options for meeting these costs and we’ll report back to you on these matters.”

I know speaking as an employer and along with other colleagues, finding staff is difficult at the moment, so that puts pressure on salaries, obviously. And Inland Revenue is not immune to that because it needs to pay near market rates to attract good quality people, because as the gamekeeper, so to speak, it needs to match the poachers on the other side. Like so much in the year ahead it will be interesting to see how the Minister settles in and what happens with Inland Revenue’s funding.

The shape of things to come – tax credits or threshold adjustments?

And finally, coming back to what lies ahead, as I mentioned at the start, the Half Year Economic Forecast Update left us none the wiser as to the nature of the threshold adjustments, which we think are going to happen. In that gap. David Seymour of ACT has come forward and talked about the ACT policy, which is to simplify the tax rate structure down from the current five rates down to three, with a top rate of 33%. This is moving back to the rate structure which applied from 1989 through to 2008. Basically, until 1 April 2000 (when the 39% rate was introduced) there were two main rates with a tax credit adjustment for low-income earners.

David Seymour talked about tax credits similar to the existing Independent Earner Tax Credit. But as I told RNZ while the concept’s not uncommon, there’s still the issue we discussed earlier. What about adjustments for inflation and keeping the true value of that, otherwise lower rate/ lower income earners will face higher effective marginal tax rates.

There’s also a certain complexity with tax credits. The thing about applying thresholds across the board to everybody, it’s pretty straightforward. Whereas with tax credits, if there’s a claim process that’s involved, not everybody will claim that. It introduces a bit of complexity at the bottom end, which Inland Revenue’s Business Transformation was determined to do the opposite in order to try and make it as easier for most taxpayers to comply.

As mentioned, we have the independent earned tax credit, but it starts cutting out at $44,000 and then drops out at $48,000 once income crosses that threshold. We’ll have to wait to see what happens and in the meantime there will be plenty of debate ahead. We will bring all of those developments to you as usual.

In the meantime, that’s all for now. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The United Nations Conference on Climate Change, COP 28, has just wrapped up in Dubai. The current Minister of Revenue, Simon Watts, is also the Minister of Climate Change so he attended the conference on behalf of the Government. There has been a lot of debate about how far COP28 has moved change forward although an agreement was finally reached on beginning a phase out of fossil fuels.

Now, coincidentally, or maybe not, as COP 28 was ongoing, the Climate Commission released its final advice to inform the Government’s plan to meet Aotearoa New Zealand’s greenhouse gas reduction goal for 2026–2030.

Briefly, the report says that the Government needs to take active steps to encourage change by removing barriers and supporting investment that cuts climate pollution. The Commission’s analysis is the country has made progress, but it is not on track to meet its climate goals for the end of this decade. In the Commission’s view, that means that we will be missing out on benefits like new jobs, a more resilient economy and healthier communities.

In all there are 27 recommendations which are focused on areas where the Commission sees there are critical gaps in action or where efforts need to be strengthened or accelerated. A couple of these are encouraging households and business to switch to electric vehicles and making it easier for more people to choose public or active transport. Key thing here which I think everybody would agree with, is sorting out the roles of the Emissions Trading Scheme and forests in achieving these objectives.

The paper, all 193 pages of it, does refer to tax being one of the tools to be used. For example,

“To support the transition to a low emissions economy, incentives need to be designed to overcome near-term capital constraints to businesses shifting their existing assets and processes to low emissions alternatives. To support this, the Government could explore amending components of the tax system (for example, adjusting depreciation schedules and rates for eligible projects).”

Overall, the Commission has no specific tax suggestions beyond such general suggestions.

Replacing the Ute Tax – a UK suggestion

As it happens, this week the Government repealed what it called the Ute tax and with it the current clean car discount scheme, which seems at odds with the report of the Climate Commission. In the Government’s Coalition Agreements, there was a proposal from ACT for “Work to replace fuel excise taxes with electronic road user charging for all vehicles, starting with electric vehicles.”

Now that also seems at first sight to be contrary to the Climate Commission’s recommendations for reducing emissions. But this week I came across a major report on the UK economy called “Ending stagnation. A new economic strategy for Britain”. This has been produced by The Economy 2030 Inquiry.

The TL:DR (too long: didn’t read) of this 293-page report is that Britain is in a far bigger mess than we might appreciate, and Brexit has done nothing to improve its position. The report has a whole heap of recommendations, including, inevitably, suggestions around changing the tax system which is what attracted my initial interest. I’m always interested to see what’s going on around the world and what goes on in Britain affects quite a large number of people here, either expat Brits or Kiwis who have family in the UK. I have several cases on the go at the moment involving UK New Zealand tax matters.

The report suggests one of the major challenges the UK economy faces is a transition to Net Zero. Which is also a challenge we face. As part of this the report makes the following suggestion:

“Our tax system also needs to keep pace with net zero transition. To ensure the burden of motoring taxes does not fall on poorer households yet to switch to electric vehicles, a 6 pence per mile charge (equivalent to fuel duty), should be introduced for [electric vehicles].”

Viewed in this context and stepping back from the emotions around the repeal of the Clean Car Discount, ACT’s proposal makes sense. Encouraging people to take up EVs is what we want to do long term. But that doesn’t mean those people should have a free pass indefinitely. EVs will soon be subject to road user charges which would be similar to this UK proposal. Therefore charging EVs some form of charge is not unreasonable.

My philosophy around environmental taxes is that the revenue from any such fund raising measures should not go into the general pool of taxation, but instead be ring fenced and applied for environmental measures. In this case my belief is those funds could be used to assist people to swap out older cars into newer cars. Those newer cars may still use fossil fuels, but they will be more fuel efficient, and that’s a worthwhile goal because it does reduce the motoring burden and emissions.

Time for a land tax and “mild increases” in tax revenues?

Incidentally the Economy2030 inquiry report specifically references our post 1984 economic transformation and how we dealt with the change involved in major economic reforms. Given Britain is pretty much in a huge hole and needs to change dramatically, the report looks at how we managed our transition post 1984. As part of that, a separate paper was prepared for the Inquiry by the former Reserve Bank of New Zealand Chair Arthur Grimes.

Incidentally, and in what’s becoming something of a trend for the new Government, Mr. Grimes’ paper makes suggestions contrary to the Government’s actions and intentions. Specifically, around tax breaks for owner-occupied rental housing, his report notes the current policies “increase wealth inequity.” He also believes a “mild increase in tax revenues will eventually be needed”. His suggestion is for “broadening the range of taxes to include a land tax, the most efficient and (vertically) equitable tax available to the Government, should be considered.” I can hear Raf Manji and the members of TOP cheering at this.

Anyway, there’s a lot to read in Arthur Grimes’ paper. I think it’s a good summary of what we went through and how our experience is relevant for other economies.

The deductibility of staff retention payments

Inland Revenue released an interesting Technical Decision Summary about payments made to retain key staff as part of a sale of a company. What happened was the company was being readied for sale and as part of this process the company entered into retention agreements with key staff. These were variations to their current employment agreements which entitled the key staff to bonus payments calculated by reference to their salaries.

And the idea was to incentivise these key employees to remain with the company to enable the ongoing smooth running of the company during the sale process. The payments were made prior to completion of the sale and were conditional on the employees remaining continuously employed by the company on the relevant payment dates.

The company in this case considered a portion of the retention payments were capital and therefore non-deductible because they were part of a capital transaction being the sale of the business. The case finished up before the Tax Counsel Office and its Adjudication Unit which decided that in fact the retention payments could be deductible in full as the capital limitation did not apply.

This is a very fact specific case which is often the case with Technical Decision Summaries. However, they do give insights into how Inland Revenue might approach a particular case. Bear in mind each is very heavily contingent on the facts. Nevertheless this is an interesting one which turned out to be a good result for the taxpayer.

HM Revenue & Customs One – ChatGPT Nil

On the other hand, it did not go well for one Mrs Harber over in the UK who in her appeal against various HM Revenue and Customs (HMRC) assessments used ChatGPT as part of her research.

She then presented these “cases” in evidence.

Unfortunately for Mrs Harber none of these cases were real, ChatGPT in its enthusiasm had just simply dreamed them up, and Mrs. Harber hadn’t realised this.

In fact, she asked the tribunal how it could be confident that the cases relied on by HMRC were genuine. The tribunal pointed out that HMRC had provided the full copy of each of those judgments and not merely simply a summary as she had done, and the judgments were also available on publicly accessible websites. Mrs. Harber had not been aware of those websites.

She obviously lost the case, but the Tribunal generally took her approach as more of misunderstanding her obligations so did not penalise over heavily in terms of costs, awards. But it is an interesting commentary on the perils of making use of ChatGPT and the need to have discernment.

WorkRide FBT exemption update

Last week I discussed the WorkRide Product Ruling Inland Revenue had issued which would give an FBT exemption to employers providing E scooters, E bikes and the like. I originally stated there’s a cost limit of $4,000.

Subsequently a couple of people contacted me and asked if that limit was correct. It’s not. I was actually referencing a submission I’d made to the Finance and Expenditure Committee proposing a FBT exemption. In fact, the limit will be set by regulation, but that limit has not yet been passed nearly nine months after the relevant legislation was passed. It’s expected by the way the limit will be higher than the $4,000 sum I mentioned. My apologies for the confusion.

What’s the character of the year?

Finally, what is the character of this year? It turns out that in Japan it is a tradition to decide the character (kanji) of the year in mid-December. Over in England, Professor Rita de la Feria the chair of tax law at the University of Leeds, heard from a student that the kanji for 2023 has just been announced and it is 税, or “tax”.

On that bombshell, that’s all for this week. Next week in our final podcast for 2023 we’ll be reporting on the Half Year Economic and Fiscal Update and the accompanying Mini-Budget.

Until then, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.