My guest this week is Claudia Siriwardena one of the four finalists for this year’s Tax Policy Charitable Trusts Scholarship.

We discuss her proposal for a simplified fringe benefit tax regime for small businesses.

My guest this week is Claudia Siriwardena, a tax consultant with Deloitte and another of the four finalists for this year’s Tax Policy Charitable Trust Scholarship competition. The Tax Policy Charitable Trust was established by Tax Management New Zealand and its founder Ian Kuperus to encourage future tax policy leaders and support leading tax policy thinking in Aotearoa.

Claudia is suggesting a simplified fringe benefit tax regime for small businesses. I should make it clear here that everything in Claudia’s proposal and what is in this podcast represents her views and not those of Deloitte. Kia ora Claudia, welcome to the podcast. Thank you for joining us.

Claudia Hi, Terry. Thanks very much for inviting me on.

Terry Fringe benefit tax is a very controversial tax and one where there based on anecdote people seem to be shall we say, pushing the envelope. I think the main controversy around fringe benefit tax is around the charge that’s that payable for the private use of public company vehicles.

That’s by far and away probably the largest single component of FBT’s and the advent of the twin cab ute, with people thinking that it qualifies for a work-related vehicle seems to have magnified the issues here. There was an Inland Revenue Stewardship Review of FBT a couple of years back and that had a lot of interesting stuff.

What caught your eye about FBT into thinking “Oh there’s something here to consider.”?

Claudia Yes, like you say, Terry, it can be a very complex regime. There’s a lot of rules that that go into it and my initial inspiration for this simplified FBT regime came through my personal experience of undertaking tax due diligence. A common topic of discussion throughout tax due diligence is FBT, but particularly the FBT rules regarding motor vehicles provided to employees for private use.

I was thinking about ideas for the tax policy competition so I took that personal experience and I thought there was a real opportunity here to simplify these rules and to increase compliance. And aside from that, I think like you’ve said, there is a commonly held view that the FBT rules are relatively complicated and hard to understand. And that was something that was discussed in that Stewardship Review that you mentioned, and also a 2003 government discussion document. So what my proposal is intended to do is to simplify these rules and make it understandable.

A tax with a lot of non-compliance?

Terry Yes, that Stewardship Review was very interesting, one of the numbers that interested me was that it raised $592 million for the 2019-20 year. But there are only 21,885 filers

When you think there’s several hundred thousand companies around, that does point to a seeming mismatch. I think also, like the old 80/20 rule, the majority of FBT is paid by a few groups. When you look at it like that, you think, gosh, that does point to something of an inconsistency? You can put it like that.

Claudia Yes, totally agree. And I think throughout that sort of report, there’s a lot of comments in there from interviewees around non-compliance, or this perception that there is a lot of non-compliance.

Terry Yes, because that undermines the integrity of the tax system because people feel that they’re complying with the rules, but others aren’t. Then the incentive to keep complying is diminished.

It wasn’t in the Stewardship Review, but I had seen other somewhat offhand comments from Inland Revenue along the lines of “Well, we don’t know if it’s worth our while doing that.” And I always thought that’s not necessarily why you enforce the rules for collection purposes. It’s also about maintaining the integrity of the tax system.

And just to digress slightly, FBT is one of those regimes that was introduced to encourage compliance because with the high income tax rates in the early 80s, people were being provided with vehicles instead. And that was thought to bypass the high tax rates and that was why FBT was introduced in 1985.

How do you propose addressing these issues?

Claudia The cornerstone of my proposal is introducing a default private use percentage for motor vehicles based on 175 days of private use. And the idea of this is essentially if employers apply this default private use percentage, they can use that to calculate the FBT liability. And then what it means is they don’t then have to go and track the actual days of private use. We can sort of cut down time and costs having to actually track all of that, because for a lot of small employers, that is quite a large exercise. So what my proposal does is set a fixed percentage and apply that as the filing position.

And then obviously if people said, well, that’s not good enough for us, we want more accuracy because our use is lesser. They would then have to produce evidence or file on that basis. Inland Revenue would know they’ve moved off the 175 day default basis and then could ask for an explanation.

Terry Just coming back to those 175 days, how did you arrive at that?

Claudia So, the 175 days is calculated by treating Friday to Sunday of regular working weeks, the statutory annual leave entitlement and annual public holidays, as available for private use. Which in another way is essentially saying that Monday to Friday is treated as not being available for private use, and what I’ve done again for simply. What that does is it assumes that the Friday to Sunday of regular working weeks, your annual leave annual public holidays will typically confer a greater private benefit to employees then use on Monday to Thursday.

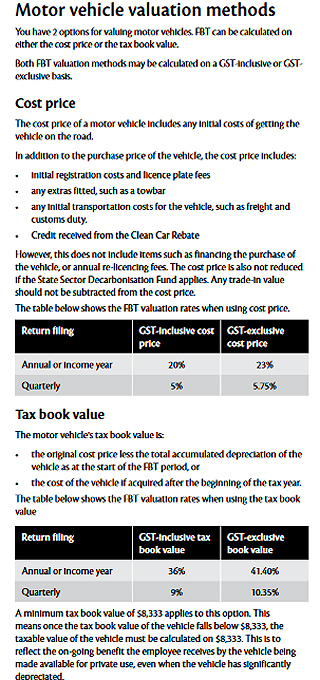

Terry Thanks. But you wouldn’t change the basis of how FBT is calculated. To recap , quickly on a car, it’s 20% of the GST inclusive value of the vehicle when new or when acquired. Alternatively, you can use 36% of the depreciated tax book value.

Claudia No, I don’t propose changing the basis of calculating FBT.

Terry The availability of alternative calculations reinforces your point about the complexity of FBT. If you’re a small business, it’s another compliance headache.

Eligibility thresholds

Terry Your proposal would not be available to all employers as you’re targeting smaller businesses. What are the relevant thresholds?

Claudia I’ve got three main criteria. So firstly, the business has to employ less than 50 full time equivalent employees. The business has got to have an annual turnover of the preceding income year of less than $10 million. And the company also is providing fewer than 10 motor vehicles to employees, which were available for private use.

My thinking in terms of that criteria, is that the small businesses, the compliance costs that they incur, are typically out of proportion to the larger businesses. So, what this is doing is focusing on smaller businesses who can actually get the most benefit from this, and who may not have sort of the processes in place or the scale of resources available to larger enterprises.

You’ve got to find some sort of threshold or middle ground. So, these criteria are where I landed in terms of deciding who falls in and out, because when we are considering revenue integrity and maintaining that. And what I don’t want is my proposal to then decrease revenue integrity by allowing, say, a lot more businesses than desirable into sort of this regime.

Increased Inland Revenue activity & the integrity of the tax system

Terry You see your proposal as encouraging compliance, but you also expect Inland Revenue to increase its activity in this field?

Claudia Yes, when you look at the Stewardship Review together with recent comments from the Minister of Revenue around FBT and you put that together with the increased funding that Inland Revenue have recently received in terms of audit activity, then I don’t really think anything is off the table in terms of looking at FBT. Especially when there is this common view that there is potentially non-compliance either intentionally or because of the complexity.

Terry Yes, this is the thing it is all about. Protecting the integrity of the tax system always matters but I think FBT is an area where I would have said a risk has developed. there. Do we know about how many companies that could be affected in your proposal?

Claudia No, no, I haven’t come across that detail, which then also makes it quite hard to quantify potential impacts. But I think a lot of it this also goes back to the recent Inland Revenue Improvement Performance review which talks a bit about the tax gap. It doesn’t analyse what that FBT tax gap might be, which can make the benefit of this proposal quite hard to quantify.

Terry That’s a very interesting point. One of the things I took away from the Performance Improvement Review was commentary that although Inland Revenue, is a high performing organisation it probably could be doing a lot better for small and micro businesses.

Just to tie up this point about non-compliance is I think twin cab utes have been in the top 10 selling new vehicles in New Zealand for several years now. I must admit when I see a web company advertising on a twin cab ute, I’m thinking “Don’t be trying to tell me you’re a work-related vehicle.” So yes, I’d be wanting to focus resources on that.

The pros and cons of simplifying the tax system

Earlier we talked about how you calculate the FBT and straight away we got into a lot of detail. I guess there’s got to be scope as well for perhaps thinking further about can we how can we make this easier?

But Inland Revenue is reluctant to create options that people might use for simplification, for fear that it might be abused. I would point to the accounting income method as an example of a good idea made over-complicated. It means that the same standard of compliance is imposed on a small company with two or three employees and one or two vehicles as for a District Health Board. What’s your thoughts on that? About maybe simplifying the regime further on the grounds of integrity and maybe compliance?

Claudia I think general simplification of regimes is an interesting question and it definitely is the core of my proposal. I think what can be good with simplified tax regimes is it just makes it understandable; it makes it simple which I think is really important for ensuring taxpayer compliance and maintaining that revenue integrity.

I think, for example, I’m not too sure how many clients respond positively when we start discussing the FBT rules, and we need to review this and that because it’s complicated. On the other hand, a critique could be that you will lose revenue. Often with a simplified regime you sort of can strip back the detail, which is sort of what my default private use percentage is doing. But that potentially introduces is an under reporting or under collection of potential revenue.

But how I’ve sort of approached this, especially in the context of FBT and motor vehicles, is well, when you consider the current non-simplified regime is that actually losing revenue itself because of its complexity, because of people not complying? It’s a tricky one to balance and my proposal is definitely hoping that by simplifying the regime we increase compliance. I think it has its place in certain in certain regimes.

Terry That’s very well put. I think sometimes the perfect is the enemy of the good. Everyone should comply, but what is making it difficult for everyone to comply is because for small businesses it’s an enormously expensive compliance burden. With compliance there is an irreducible minimum requirement which I think we’ve reached in many cases. But that’s still a lot for small businesses and, micro businesses in particular.

I think a lot more support could be made available to businesses turning over between $3 and $30 million, and it would pay off in terms of increased compliance.

I come from Britain and the fringe benefit tax regime there, the value of the benefits, is included in an employee’s income at the end of the year and then taxed that way. When I came here and saw how New Zealand taxed fringe benefits I thought the approach here was much sounder in terms of revenue collection.

When you think that with a 39% personal income tax rate FBT is now 63.93% on the value of the benefit unless you get into calculating it in more detail. Have we reached a point that a better alternative for, say, larger companies to apply the fringe benefit to employees and tax it through PAYE rather than the company taking the hit. What’s your thoughts on that?

Claudia Yes, when I was going through my initial process of brainstorming FBT issues and potential proposal ideas, I did consider the case of whether employees should bear different benefit tax costs through PAYE.

I think like you say, times have sort of moved on and they continue to, but based on some initial research that I found, it actually appeared that it was questionable whether making such a change would simplify the FBT regime and reduce compliance costs, which was my key focus.

I mentioned earlier the government discussion document from 2003. It noted that changing who pays the tax is unlikely to result in any material compliance savings for employers and may in fact actually increase compliance costs on employers.

Which for my proposal and just in general, that’s not something that I would want to put forward. So, in this respect, who pays the tax doesn’t necessarily remove the issues that are associated with the FBT rules at present. So yes, noting that it was 2003, that’s probably still my view at the moment, based on that initial research.

Terry I think that’s a good point to leave it there for now, Claudia. What’s next for you in terms of the scholarship?

Claudia I’ve got my final 4000-word submission in a few weeks on the 16th of September. So over the next few weeks, refining my idea, sort of fleshing it out, answering my key points and then down to Wellington last week of October to do a 10 or 11 minute presentation to an audience and answer a few questions.

Terry That sounds quite intimidating.

Claudia Yes, but excited by it. It’ll be good fun.

Terry Well, good luck and thank you so much for coming along. It’s been great to have you on the podcast. It’s a very interesting proposal, full of merit in a space which I think needs initiatives like this.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

How to deal with recipients of paid parental leave with tax underpayments

A bizarre tax avoidance case from the UK involving snails

In line with other government agencies, Inland Revenue is required to produce a long-term insight briefing once every three years. These briefings are intended to

“…help us collectively as a country think about and plan for the future. They do this by identifying and exploring long-term issues that matter for our future wellbeing. Specifically, [briefings] are required to make publicly available:

information about medium- and long-term trends, risks and opportunities that affect or may affect New Zealand society, and

information and impartial analysis, including policy options for responding to the trends, risks and opportunities that have been identified.”

This is Inland Revenue’s second long-term insight briefing, its first one released in 2022 was on tax, foreign investment and productivity and that was a fairly chunky topic. But this time around it’s proposing to take on a bigger topic “what broad structure of the tax system would be suitable for the future.” What it would do is look at this topic by reviewing our tax system through the lenses of what is the tax base and what regimes apply.

As part of the initial stage of consultation for this topic Inland Revenue has released a 50 page briefing document giving a background on the whole process. The briefing summarises the current state of the New Zealand tax system and the options for consideration. Chapter one gives a complete overview of the current system. Chapter two then gives options for a future tax system and looks at international perspective. The final chapter summarises the topic and the approach to be taken by the briefing.

A mini-tax working group review

There are a lot of interesting insights in this paper, because in essence it’s similar to the scoping paper usually prepared by a tax working group at the start of a review before the group gets into detailed analysis of particular aspects of the tax system. The briefing is a therefore a handy high level summary of the current state of the New Zealand tax system.

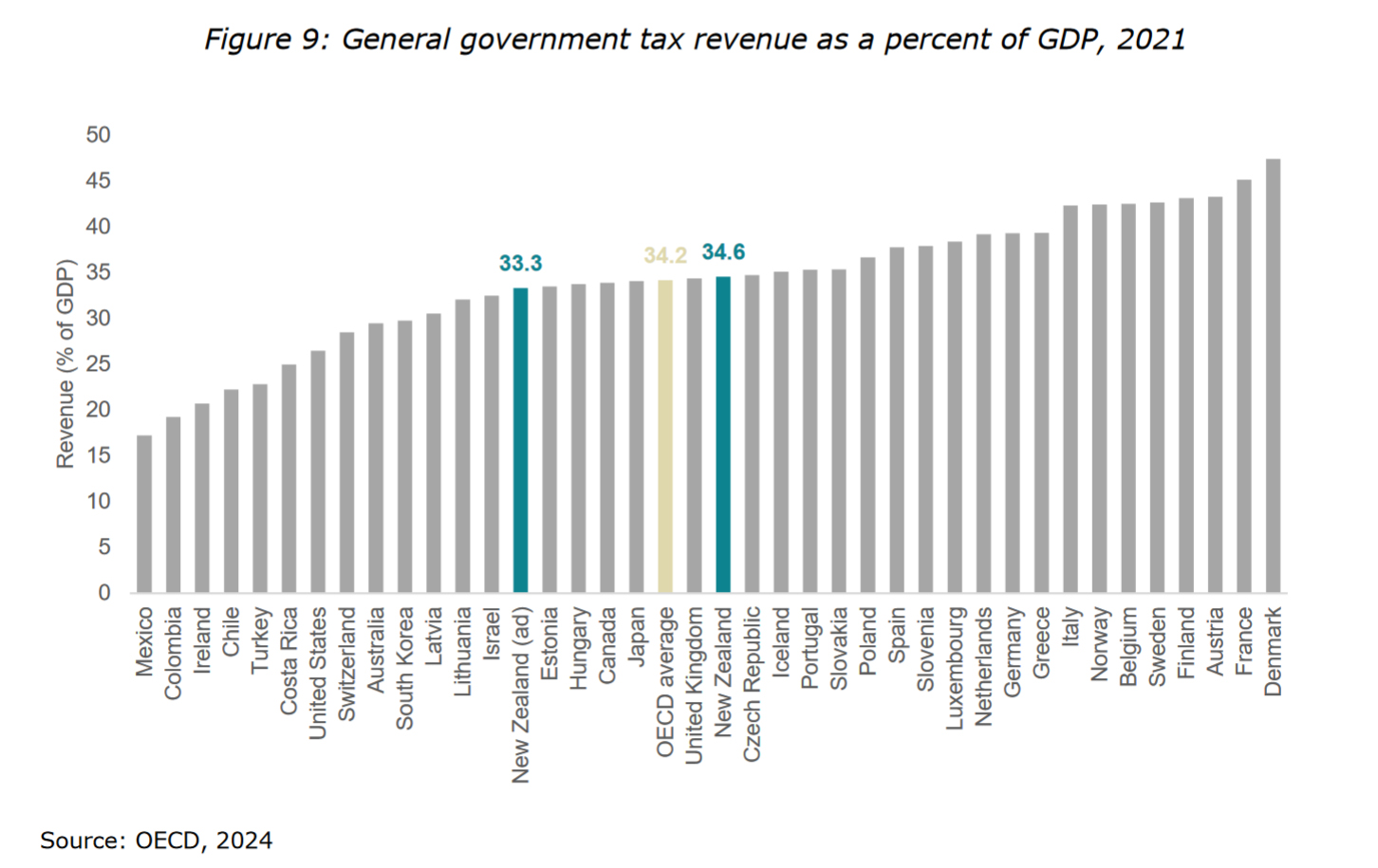

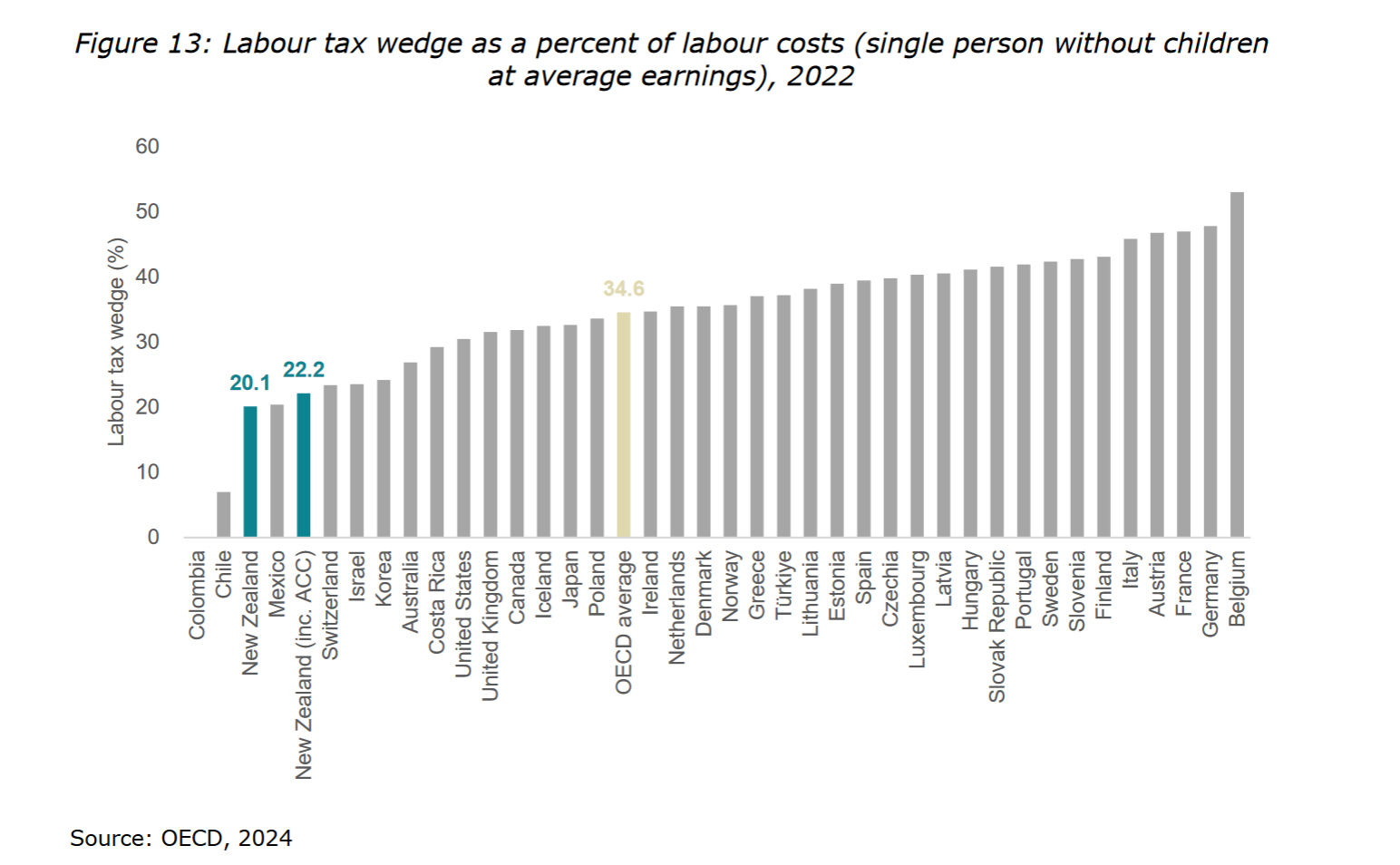

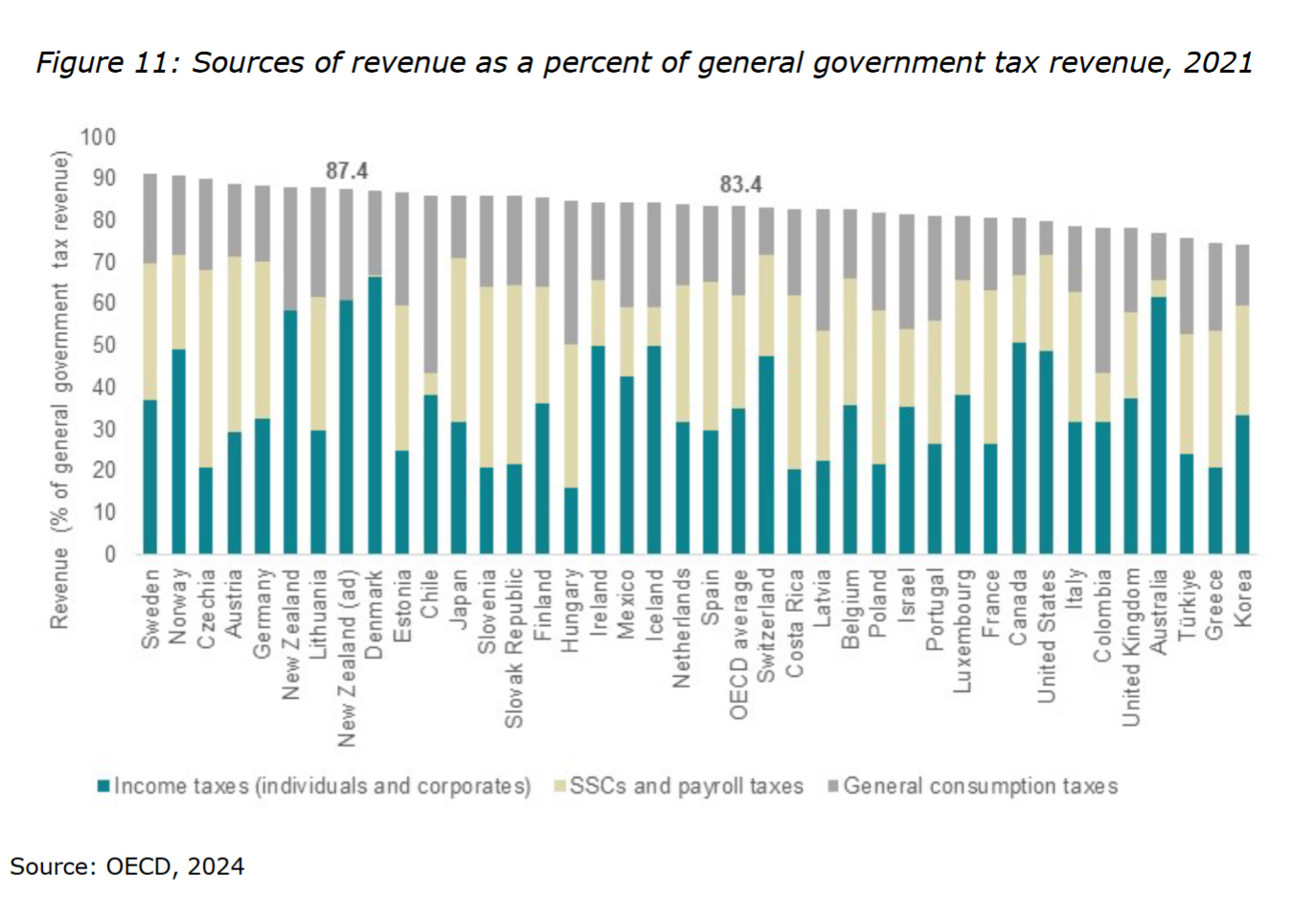

In summary, the level of tax revenue we currently raise relative to the size of our economy is pretty close to the OECD average. It’s in the composition of tax revenue. It’s where it gets interesting. We are almost unique in the OECD in not having any significant specific taxes on labour income such as social security contributions or payroll taxes.

Taxing labour…lightly?

Furthermore, quite a few of other OECD tax systems have what they call a schedular tax system, which means in some cases they tax capital income such as dividend, and in some cases capital gains at lower rates than taxes on labour. As a result, many OECD countries have a higher tax burden on employee labour than New Zealand.

To give an example, the UK has a 20% basic tax rate, but employees also pay National Insurance Contributions above a certain threshold (8% on income between £242 and £967 per week and 2% above £967 per week). Employers pay 13.8% on all earnings over £175 per week. By contrast we have no such taxes which means we have one of the lowest tax wedges in the OECD.

Also, where we stand out is we raise more than the OECD average on general consumptions and that’s because our GST is one of the most comprehensive in the world. We also currently have a higher company income tax rate than the OECD average.

The paper notes some concerns noted about high effective marginal tax rates on inbound investment. I have to say I do wonder whether the small size of our economy and its isolation is more of a factor than tax in attracting inbound investment.

And finally, and this is highly ironic and also relevant if, you just opened your rates bills and the comments from the Prime Minister earlier this week, New Zealand raises more than the OECD average from recurrent property taxes, mainly through local government rates.

Building fiscal pressures

As part of the background the paper explains the various fiscal pressures building up. This is something we’ve talked about before, and we’ve frequently referenced, Treasury’s He Tiro Mokopuna 2021 statement on the long-term fiscal position. The well-known pressures building in in relation of our changing demographics, rising superannuation and health costs are all mentioned again.

So too is climate change, but more in passing, although personally I think that’s the one the impact of which is going to land first for most people as we saw last year in the wake of Cyclone Gabrielle. Suddenly, climate change is not an abstract thing with targets for 2050. It’s here and now. Remember Auckland ratepayers, for example, we got a $400 million bill as a result of buying out properties rendered uninhabitable by the Anniversary Weekend floods and Cyclone Gabrielle.

A suitable tax system for the future

The paper discusses what would you do in terms of meeting these pressures. Do you expand the tax base by adding new taxes or what about increasing tax rates? The paper mentions that there are limitations about raising tax rates which is not always as straightforward as you might think. For example, we raised the rate of GST from 12.5% to 15% in October of 2010 and GST as a result is a very significant tax because our system is so comprehensive.

But GST comes at the price of being very regressive for people on lower incomes. How would you deal with that? And the paper, by the way, references an IMF Working Paper on a progressive VAT/GST which I mentioned recently.

There was also an interesting comment I’d like them to know more about in relation to company tax. The paper notes that we raise a relatively high amount of revenue from company income tax as a proportion of GDP compared with other countries.

It notes this “may be partly attributable to the level of incorporation.” I’d be interested in knowing how much more company incorporation goes on here relative to other OECD countries. I think our imputation tax system is also a factor in why we pay relatively high amounts of tax relative to other jurisdictions.

What the briefing does reinforce is something I think is agreed within the tax community that there’s pretty much little scope for increasing company income tax rates. There’s always a lot of talk about that, but I don’t think there’s much scope for actually doing so.

“New Zealand is unusual among OECD countries in not having a general tax on income from capital gains”

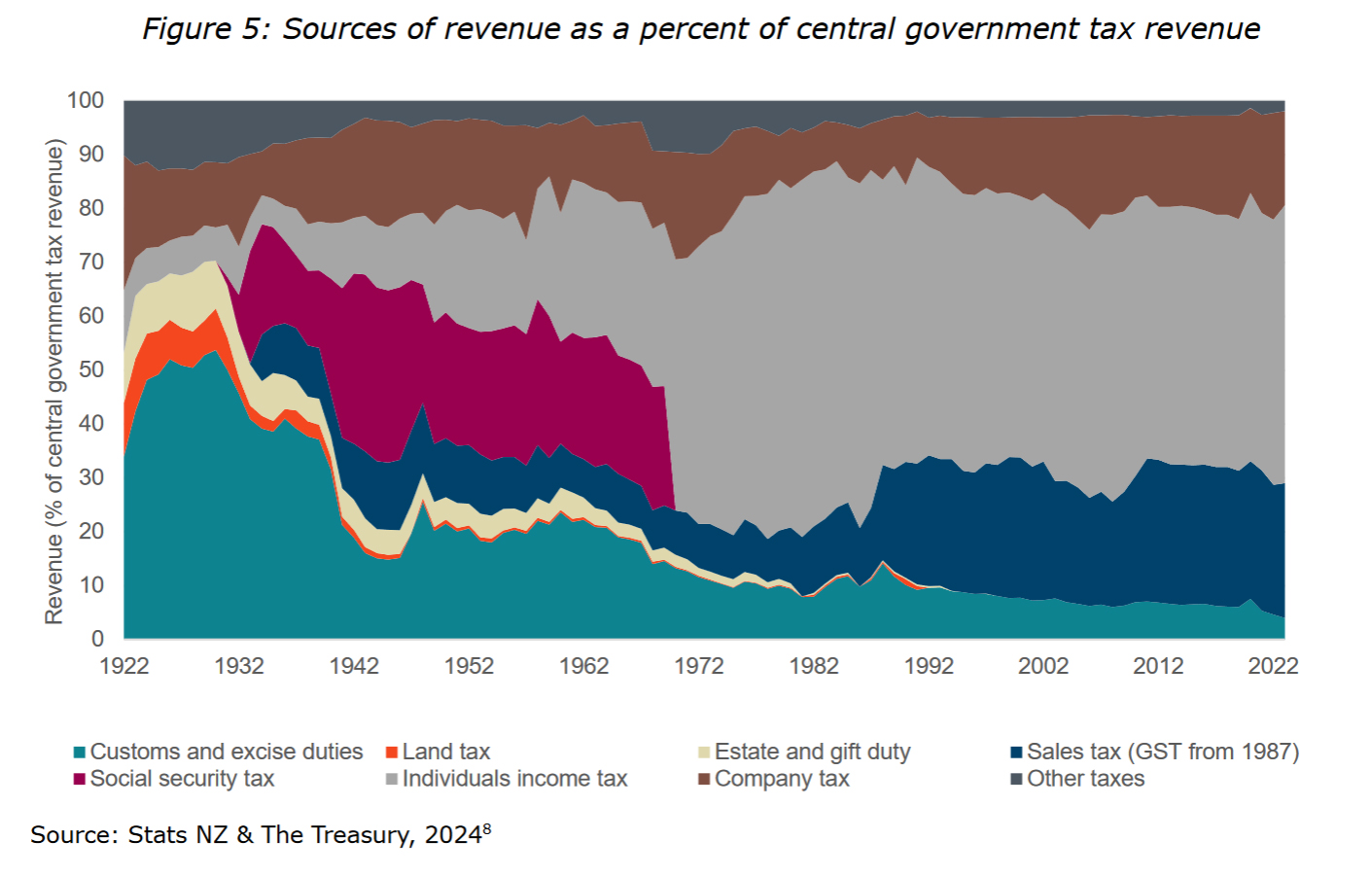

Unsurprisingly the paper considers the question of taxing capital, as part of reviewing the composition of taxes in other countries. There are a lot of interesting graphs and stats are in this section including an excellent section summarising the historical changes in the composition of the tax base over the past century.

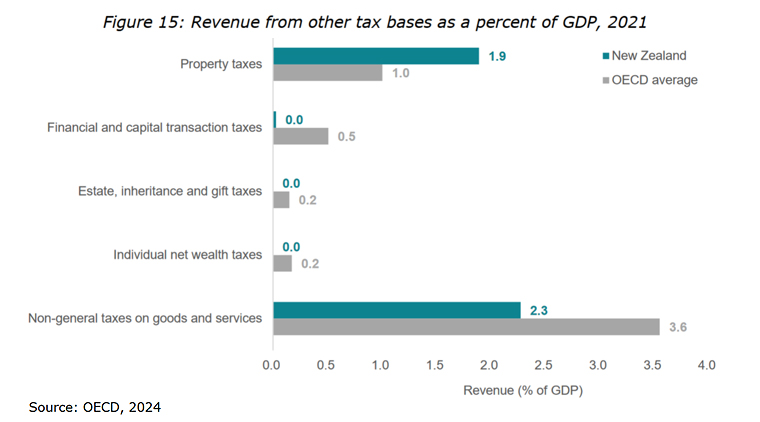

As I mentioned, we raise more revenue as a share of GDP from recurrent property taxes compared to the OECD. In 2021 it amounted to about 1.9% of GDP. B comparison, the average in the OECD is 1%, ranging from 0.1% of GDP in Luxembourg to 3% of GDP in Canada.

On the other hand, we don’t raise anywhere near the same level as other OECD countries from taxes on financial and capital transactions, estates and gifts. I mean, many countries have a combination of estate taxes, gift duties, capital gains, taxes and wealth taxes. According to the OECD data taxes on estates, inheritances and gifts raised an average of 0.1% of GDP in 2021. That seems a surprisingly low number, although it rose to 0.2% in 2022. This take is starting to rise as the Baby Boomers, the richest generation in history are starting to pass on. In the UK Inheritance Tax, which is a combined estate and gift tax, is now over 0.3% of GDP (£7.5 billion) and rising.

What about corrective and windfall taxes?

The paper gives a background on the possible options which might deal with future cost pressures. Its focus is going to be on revenue raising taxes. The final briefing will not examine taxes that are primarily about changing behaviours (so called “corrective taxes” such as excise duty, particularly in relation to tobacco. It will not discuss environmental taxes which are another form of corrective taxes. All taxes change behaviour in different ways and I think considering the behavioural impact of certain types of taxes would be useful

The final briefing will not consider windfall taxes, which have recently popped up in discussion in relation to supermarkets and the banks. Such taxes are one-off in nature and frankly, a reactionary tax to a set of events. If the concern, correctly in my view is about responding to the pressure of ever increasing costs, then windfall taxes are not in that context a sustainable addition to the tax base.

All in all, this is very interesting and pretty digestible reading. Consultation is now open until 4th October, so my suggestion is get reading and start submitting.

A baby and a tax bill…

Moving on, Inland Revenue has mostly completed its year-end auto assessment process for the majority of taxpayers’ income for the March 2024 tax year. Subsequently, it’s emerged that some 13,261 recipients of paid parental leave, about 27% of all such recipients have finished up with a tax bill. This is causing some concern because in some of these cases, these bills are quite substantial, amounting to several thousand dollars in some cases which have to be paid.

Paid parental leave is taxable and subject to PAYE. What seems to have happened is that people haven’t factored in the effect of their other income, for example they may have continued to work reduced hours in their main employment while also receiving paid parental leave. Consequently, because PAYE is designed around one person, one job per year the parental leave has been under taxed. But this only emerges as part of the end of tax year wash up. You can deal with this by using a secondary tax code, but that often goes the other way and leads to over taxation during the year.

Tailored tax codes

An answer to all of this, and also as a means of collecting the tax paid would be a tailored tax code. Tailored tax codes are ideal for an employee with other sources of income which aren’t subject to PAYE such as overseas pensions. What you do is advise Inland Revenue of these other sources of income and ask it to adjust your PAYE tax code taking into effect this other income. It’s then taxed during the year through PAYE. By the way, this also is a good way of bypassing the provisional tax system.

This approach is something I saw a lot of when I worked in Britain. HM Revenue and Customs adjusted tax codes for the equivalent of New Zealand Superannuation and used adjusted tax codes to collect underpayments of tax for prior years. If you underpaid one year, your PAYE code for the following year would be adjusted to collect the underpaid tax. I think this is probably an easier system than expecting lump sum payments.

My view is Inland Revenue could make a lot more use of tailored tax codes and should do so proactively. It has the information to know when someone has started a second job or starts receiving paid parental leave. It can then contact that person and ask they want to have a secondary tax code or a tailored tax code. This may already be happening but people with new babies have plenty going on, so this sort of admin detail just slips off the radar. I think it’s something where Inland Revenue systems ought to be good enough to be able to actively encourage people to make greater use of these codes.

Snail farm in city office sparks tax avoidance probe

Finally, and returning to an earlier topic, rates, there’s a story from the BBC about a quite flagrant tax avoidance scheme in the UK. The story involves a commercial building in Liverpool and what’s happened is this building has been home to a snail farm for more than a year. The firm renting the premises has told Liverpool City Council that because the building is being used for agricultural use that part of the building is exempt from business rates. Otherwise, the rates bill would be about £61,000 for the whole building.

Understandably, Liverpool Council’s not impressed, and neither are other snail farmers. (Apparently snails retail for £14 a kilo). They think the scale of the operation isn’t realistic because according to the owner there are only two snails in each crate which has been done to avoid “cannibalism, group sex and snail orgies”. (Yikes!)

This seems a fairly flagrant tax avoidance case. And it’s caught the eye of Dan Neidle of the UK tax think tank Tax Policy Associates. As he notes you’d think this sort of thing would be struck down quite easily by the courts but not so. There doesn’t appear to be a specific anti-avoidance rule in the relevant legislation, and it appears that there’s quite an industry around so-called “business rates mitigation”. Astonishingly, a recent case involved a Crown organisation Public Health England attempting to bypass rates through one of these schemes. Dan has suggested that the new Chancellor of the Exchequer, (Finance Minister) Rachel Reeves, put in place legislation to strike this sort of activity down.

An opportunity here?

Under our rating legislation here I think that a similar scheme probably wouldn’t work. Based on what I understand our rating approach seems to be a bit more comprehensive. But one of the things I know about working in tax is that where people perceive there’s an opportunity to, let’s say, push the envelope, they will do so.

And on that note, that’s all for this week. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

Matthew Seddon suggests imposing withholding taxes on organisations that engage independent contractors, including through electronic marketplaces

My guest this week is Matthew Seddon. Matthew is a lawyer at Bell Gully and one of the four finalists for this year’s Tax Policy Charitable Trusts Scholarship competition. He has suggested extending the withholding tax regime to include more independent contractors. Kia Ora Matthew, welcome to the podcast. Thank you for joining us. So how did you get into this and where did your proposal come from?

Matthew Seddon Hi, Terry, thanks for inviting me onto your podcast. It’s great to be here. The Tax Policy Scholarship provides young tax professionals with the ability to set out a proposal for a significant reform in the New Zealand tax system. My proposal is to extend PAYE withholding to independent contractors engaged by persons with an existing PAYE withholding obligation, i.e. employers, and also to those independent contractors engaged through an electronic marketplace.

TB Those electronic marketplaces try and match buyers and service providers. You picked up on something from the Tax Working Group in this space, is that right?

Matthew Seddon Yes, the Tax Working Group in 2018 had identified the rise of self-employed independent contractors as the most likely and most significant challenge facing the integrity and sustainability of the New Zealand tax system. The Tax Working Group’s final report had noted that withholding taxes should be extended as far as practicable in order to ensure greater levels of compliance. Furthermore, the Government’s recent focus on increased compliance activities is another reason which prompted me into this proposal.

TB Yes, because Inland Revenue got $29 million a year. I think they were saying they’re expecting a $700 million return on that. Is that right?

Matthew Seddon Yes, the $29 million I think is over each year and I think $116 million is set across for the four-year period. So their expectation is to raise $702 million over a four-year period from those increased compliance activities. Inland Revenue has also been stating recently that they’re going to focus on taxpayers who have not been complying with their tax obligations. Especially in the hidden economy.

TB Like I was saying the other week, the hibernating bear has woken up and it’s hungry and it’s making moves. Yes, I mean just picking up on that, the Performance Improvement Review recently released on Inland Revenue was quite interesting in its discussion around the tax gap, which the Tax Working Group fenced around a little but didn’t really go into specifics. But this is the area, right on scope of the tax gap, isn’t it?

A billion dollar gap?

Matthew Seddon Indeed, and Terry, just for listeners to understand, the tax gap is the difference between what Inland Revenue should receive in taxes if all taxpayers are fully compliant with their obligations compared to what tax they actually receive. The Tax Working Group had received some research that was commissioned by Inland Revenue on the tax gap for independent contractors, and that research indicated that independent contractors were under reporting their taxable income by about 20% on average. This was resulting in a loss of revenue of $850 million a year.

TB And that’s in 2018 dollars. So now we’re talking potentially over a billion dollars per year.

Matthew Seddon Exactly.

TB Well, if I was Nicola Willis, I’d be very interested in that because that’s a quarter of a percent of GDP. It’s actually a significant number now. So how does your proposal work?

Matthew Seddon So my proposal looks at imposing withholding taxes on organisations which engage significant numbers of independent contractors. For example, a large number of independent contractors operate through electronic marketplaces. A lot of employers engage independent contractors. So it’s by centralising the withholding obligation and imposing it on employers and electronic marketplaces instead of the numerous independent contractors underneath, that provides Inland Revenue with a greater ability to receive those taxes rather than having to chase independent contractors individually.

TB Yes. So I mean we have an extensive withholding tax regime. It’s something that’s I think has always been taken for granted, but we don’t realise actually how very comprehensive it is. But when you look back on it, the sort of sphagnum moss collectors, charges for directors’ fees is a 33% rate I believe. But these withholding tax obligations aren’t updated frequently or as frequently as you might imagine. As the Tax Working Group pointed out, we’ve seen a big growth in this sector. You’re saying we’ve got these existing mechanisms in place and should extend it to this particular group. Is there going to be a de minimis or is it going to be for anyone who’s already got a PAYE obligations or who has employees?

Matthew Seddon That’s right, Terry. So, the starting point is that if you’re an employee, your employer withholds PAYE. If you’re an independent contractor, generally you deal with your own tax obligations. What you’re referencing there about sphagnum moss collectors and directors’ fees are schedular payments and that imposes an obligation to withhold on the payer of those payments. My proposal would be to extend that schedule and the schedular payments regime to include those employers and electronic marketplaces that engage the independent contractors.

Now the reason why I was looking at employers in particular and the reason why I would not have a de minimis, is because employers have the systems and software in place that pay their existing employees and they also make those payments to independent contractors. So the software and systems should only require minor modification and configuration to be able to deal with withholding on payments to those independent contractors. The independent contractors that are engaged by employers and electronic marketplaces. It wouldn’t be all of those independent contractors that are subject to the withholding. It would only be those independent contractors who are principally providing services to the employer or the electronic marketplace such that they are functionally equivalent to employees.

TB Yeah, that’s a really interesting point there because often you find that someone walks out the door on Friday is contracting back on Monday. So this question of functionally acting as an employee – is that going to be a requirement, do you think? Would it perhaps just be extended if a person is providing personal services to a company, would that perhaps be a stronger approach? I think so rather than try to get to a definition that they’re doing the same as if they were an employee because all the employment lawyers listening will be twitching on that one because there is a big case going through the courts at the moment, I believe on that matter.

Matthew Seddon It’s essentially to look at who is providing services to the employer or the electronic marketplace. It’s designed to carve out people who are genuinely supplying goods to an employer or an electronic marketplace. So, you don’t have an overreach of withholding obligations. You could imagine if withholding was made on all payments to independent contractors, it would lead to chaos. There would be withholding on every single payment that’s made by an employer.

Furthermore, proposals to extend withholding to all independent contractors have a significant downside in the fact that you’d be requiring, for example, home owners to withhold tax and pay that to Inland Revenue for a painter that was engaged to paint their house. So this proposal is designed to narrow the focus to the independent contractors who are providing services to employers and electronic marketplaces.

TB That makes perfect sense. It’s a huge area though. But as I said, the scope of this with downsizing that’s been going on through Ministries, for example, this exactly is happening, as I said, some people are probably coming out on Friday as employees and coming back contracting with a different role on the Monday. A flat 20% rate, was that what you are thinking?

Matthew Seddon Yes. The default rate would be 20%. This is in recognition of the fact that independent contractors can claim deductions for income tax purposes. It also aligns with the current voluntary schedular payments regime that already exists.

TB Yes, the voluntary schedular payments regime. So right now, if you were contracting to an employer, you could say take 20% off and the employer or rather the contracting company could do that?

Matthew Seddon Yes, there is a mechanism whereby both parties can agree to undertake a withholding. The one thing I would note about my proposal is that it is simply the default rate of 20%. There is an existing regime for schedular payments which provides that an independent contractor can notify the payer of their name, IRD number and an elected rate no less than 10%. The independent contractor can essentially toggle the rate to reflect their effective tax rates so that they they’re not overpaying tax throughout the year. And they’re not underpaying as well, so that they can get a correct tax outcome by the end of the year.

TB Yes. Our pay-as-you-earn-system is more flexible than it was, but there’s scope for improvement there. I think real time payments are the next step in the evolution of our tax system. Something just popped into my mind. If I recall correctly, if a company is providing hiring, hiring contractors, they have a withholding tax obligation automatically. Is that correct?

Matthew Seddon The labour hire rules in the schedular payments regime, I think it’s a 20% rate.

TB Yes, 20%. And it wouldn’t matter, say a contractor was working individually or through a company. Generally speaking, you can under the schedular payments rules, generally speaking, if you’re working through a company, the payer doesn’t have to withhold tax. What do you think? Would you change that here?

Matthew Seddon I think there’s a company exemption in the schedular payments regime which looks through certain companies. So, I think that could also fit in with this proposal.

TB Because mainly the fact someone’s running through a company doesn’t mean that they’re actually completely up to date with their obligations, as week after week Inland Revenue tells us what’s going on. And the other thing that you touched on in there was about the fact that as contractors, they have the ability to claim deductions. I think this is where the paper prepared for the Tax Working Group was saying basically that it seems given comparable levels of income there is this gap of about 20% and they identified that on the basis that self-employed or contractors appear to have 20% more discretionary spending than their employee counterparts.

How would you counter that? I know as a small business, when you are dealing with small businesses, people are very keen to claim everything they can, and they don’t always tell you what they’ve claimed or they’re not always as straight up or as accurate as we would all like in this space. I’ve wondered whether we should have standard deductions. What’s your view on that? I know in the UK they did that for self-employed individual. Any thoughts on that particular idea?

Matthew Seddon My proposal primarily focuses on the withholding obligation, that is on the income side of the equation, so by being able to report and withhold on these payments, Inland Revenue is going to see exactly what these independent contractors are earning.

I guess to the extent that independent contractors are claiming sizable amounts of deductions relative to their industry peers. It would allow Inland Revenue to go and look and audit those independent contractors. On the deduction side, it’s something that I have thought about. I know in the GST rules for listed services there are flat rate credits for non-GST registered persons. So, there could be a similar flat rate deduction for independent contractors to align themselves across the board.

TB I deal with quite a number of American clients and their tax returns have what they call a standard deduction of $12,000. But you don’t have to claim that, you can go for what they call itemised deductions which presumably you do so on the basis that you’ve got more to claim.

It just crossed my mind that one of the things coming out of the Performance Improvement Review of Inland Revenue which we discussed a couple of weeks back, they talked about the tax gap, and I think they also talked about making one of its objectives to make the tax system easier and simpler and particularly for small businesses micro businesses. Your proposal basically is in that space, isn’t it? And it does have that benefit.

Matthew Seddon Exactly. It provides greater levels of compliance for those small businesses, those independent contractors. There’s going to be less need for them to engage accountants and third-party providers. There’s going to be less engagement with the provisional tax system. That’s going to be a much simpler experience for those independent contractors. My proposal also recognises that there will be some costs imposed on employers and electronic marketplaces. But by leveraging off the existing PAYE rules and schedular payments rules, it is designed to minimise those compliance costs as much as possible requiring them to just modify and configure their software and systems.

I think it’s important as well to notice that prior to any implementation of this proposal, there should be a sufficient period of time in which engagement can take place between Inland Revenue and these payroll software providers. I know this has recently taken place for the personal tax cut changes which had effect from 31 July.

TB That’s actually quite critical, and wider consultation is always welcomed in this space. Something just came to mind. I mean, obviously what we’re talking about here, this could be a measure that helps to close the tax gap and raise revenue, which is great from Inland Revenue’s perspective and for Treasury, but it’s actually as I see it, and what I find attractive about this is that it’s also a benefit to contractors.

I deal a lot with small businesses here and you know, managing their tax isn’t always easy and everyone is not as diligent about managing their tax as they should be. I’m a big believer in making payments regularly, and in this case, withholding payments seems to me would contribute quite a bit to that. That was something you had that in mind when you were looking at the proposal weren’t you, because that’s one of the judging criteria of the competition.

Matthew Seddon Exactly, minimising compliance costs for taxpayers and also minimising administration costs for Inland Revenue as well.

I think independent contractors, while they might have the benefit of the time value of money by only making provisional tax payments three times a year, as they currently have no withholding may allow them to have less tax obligations in the first place, as it’s all dealt with by their employer or the electronic marketplace and really allows them to focus on doing what they do best, and that’s running their own business.

TB Yeah, I’d endorse that approach. I do recommend to a lot of my clients, they run businesses, they’re shareholder-employees, we don’t often use the shareholder-employee regime and I tell them, go through the pay-as-you-earn system making your payments regularly, so you keep on top of your tax payments. That’s one of the things, as I mentioned a minute or two ago, I like about the more frequently people make their tax payments, they’re going to be more compliant, get up to date and they will have less stress about it. It’s one of the things about managing small businesses. There’s a lot to deal with and there’s not much that you can actually do, there’s an irreducible minimum you’re dealing with at times and withholding payments helps in that space.

Slightly related topic, what about GST? Now it’s not directly in scope, but to me, I think this is the next frontier of tax could be compulsory zero-rating which would be easy for both the employer or the contracting company and the contractor. What’s your thoughts on that?

Matthew Seddon Yeah, that’s right. It’s not directly included in my proposal, but I think when thinking holistically about the tax obligations of these independent contractors and how they can be automated as much as possible. GST is obviously another area to consider. I think zero-rating, there might be some scope for that. It would mean there’s less obligations on the independent contractor and would not be required to return the GST amount and they’d still be able to claim some GST credits.

The alternative I was thinking about was potentially having the carve out for employment apply to these independent contractors who are functionally equivalent to employees. You should ideally end up with a scenario where if you’ve got an employee and an independent contractor sitting across from the table from one another at their employers’ offices, they should be treated as similarly as possible so that there’s horizontal equity between the two.

TB So what’s next for you? 1500 words was your initial proposal. So now you’ve got the 4000 words which means you’re in the money, you’re going to come away with a medal of some sort. As they say, it’s always good to make the medal rounds. So it’s in mid-October sometime. You’ve got to finalise your entry and what’s involved in that?

Matthew Seddon The final oral presentation is in October and our 4000-word submission is due in September. The 4000 words is essentially branching out and expanding on our initial 1500-word proposal. The 1500-word proposal was a teaser to the judges to set out what the concept was and how it met the relevant judging criteria. The 4000 words will expand on this initial idea.

TB It’s not many though, 4000 words, really when you think about it and then obviously your oral presentation, you’ll be in front of several gurus of tax. That would be interesting, I’d say.

Matthew Seddon Indeed, it will be interesting to hear the judge’s comments and questions in person.

TB Well, I’m sure you’re looking forward to it. I am. I think it’s a very interesting proposal. It sounds mundane, but it’s actually quite important. Thank you very much, Matthew Seddon. Thank you for coming along. Good luck for October for this scholarship, we’ll watch with interest.

Matthew Seddon Thanks Terry.

TB And on that note, that’s all for this week. We’d like to thank Matthew Seddon again for joining us and wish him all the best for the scholarship. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

The just concluded UK general election was the first general election held in July since 1945, when coincidentally the Labour Party also won by a landslide ending Sir Winston Churchill’s wartime prime ministership. Before he became Prime Minister again in 1951, Churchill started writing his monumental six volume history of the Second World War, the first volume of which was titled The Gathering Storm.

And if you’ll pardon the somewhat laboured analogy, this is very much what’s happening with Inland Revenue at the moment. There’s a very clear gathering storm approaching as Inland Revenue pulls together and beefs up its investigation resources. We saw signs of this a couple of weeks back with its commentary about targeting smaller liquor outlets. Now last Wednesday, an Inland Revenue media release announced it is “honing in on customers who are actively dealing in crypto assets but not declaring income from them in their tax returns.”

By way of background, back in 2020, Inland Revenue updated its guidance on the tax treatment of crypto assets. Clearly that was part of a plan to follow through and check on who was trading and investing in crypto but not reporting the income. However, first COVID and then the cost-of-living crisis got in in the way of Inland Revenue’s intentions to follow through up its guidance.

Targeting non-compliance

But those immediate crises have passed now, and it appears that Inland Revenue has been busy investigating potential non-compliance because according to the media release late last year, it wrote to “a group of high-risk customers and gave them the chance to fix any non-compliance issues before facing audit.” This is a standard tactic of Inland Revenue. It basically puts it out to taxpayers without being too specific that it is aware of potential non-compliance and “invites”, that is the terminology used, the taxpayers involved to come forward and make a voluntary disclosure. If the taxpayers do so, then the potential to be charged shortfall penalties is likely to be greatly reduced.

Following on from these “invitations”, the next stage if the taxpayers don’t come forward is directly targeted follow up action. This appears to have just happened, as Inland Revenue is saying it has “just sent another round of letters to those Inland Revenue believes are not complying.

According to Inland Revenue it has data which has enabled it to identify “227,000 unique crypto asset uses in New Zealand undertaking around 7 million transactions with a value of about $7.8 billion.” There’s a potentially sizable sum of tax on the line here.

Pay up, or else…

The media release continues with a rather veiled threat

“Cryptoasset values have reached new highs, so now is a good time for people to think seriously about tax on their crypto asset activity. The high value also means customers are well positioned to pay their tax for the 2024 tax year and earlier.”

In other words, Inland Revenue is saying as values have recovered that means taxpayers can’t plead poverty when it comes to paying the tax due on their profits.

The media release goes on to explain something that we’ve said frequently; Inland Revenue has more data available to it than people realise.

“We want customers and tax agents to know that we are stepping up our compliance activity for customers with cryptoassets. Despite popular thinking – people are not invisible on blockchain and we have the tools and analytics capabilities to identify and expose cryptoasset activities.”

So there it is, very clearly stated ‘We know more than you think we know and we are coming for you.’ Part of this, by the way, is that New Zealand and therefore Inland Revenue has signed up to the new Crypto-Asset Reporting Framework (CARF) recently developed by the Organisation for Economic Cooperation and Development. This is yet another example of the growing international cooperation on the exchange of information, a regular topic on this podcast.

Under CARF the first set of reporting is due to apply from the 2026/27 tax year which will lead through to increased tax revenue. In fact, according to the Budget, the expectation is that CARF will deliver $50 million of additional tax revenue in the June 2028 year..

That’s in the future. What’s happening right now is that Inland Revenue has used its existing network of information exchanges and data sharing almost certainly by tax treaty partners such as Australia, the UK and the US, to obtain data about transactions carried out by New Zealand based crypto-asset investors and traders. It’s now going to put the squeeze on those it considers non-compliant.

It’ll be interesting to see what comes out of it and we will watch with interest and bring you news of developments. In the meantime you have been warned and this is of course the latest sign of the gathering storm of Inland Revenue investigations.

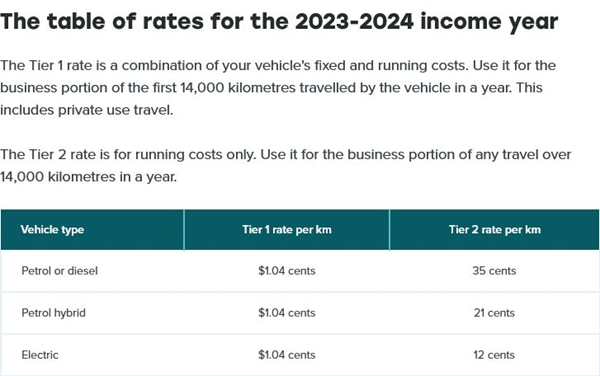

Inland Revenue kilometre rates for 2023-24

Moving on, Inland Revenue has just published its kilometre rates for the 2023-2024 income year. Unsurprisingly, given the recent rise in fuel prices, the so-called tier one rates show an increase in vehicle running costs that are allowable for the year. These rates may be used to calculate the deductible running costs for a vehicle.

Note that the Tier 1 rate of $1.04 for the first 14,000 kilometres applies to all vehicles whether petrol, diesel, hybrid or electric. The Tier 2 rates above the first 14,000 km DO vary between vehicle type.

This is good to know, but I do wonder whether it might be a bit more useful to have this sort of information earlier in the relevant tax year. Inland Revenue obviously wants to be accurate, but a different approach perhaps might be to adopt an interim rate and index that for inflation. Anyway, these are the rates that are now applicable for the 2023-24 tax year if you wish to claim the relevant deduction.

Are we raising enough tax?

And finally, this week, the Tax Policy Charitable Trust held an event on Thursday last night to announce its four finalists for this year’s Tax policy scholarship prize. The first half of the event was a panel discussion on New Zealand’s tax revenue sufficiency. Ably chaired by Geof Nightingale, a member of the last two Tax Working Groups, the four panellists that joined him were Talia Harvey and Matt Wooley, joint winners of the scholarship prize in 2017, Nigel Jemson, the winner in 2020 and Vivian Lei, the winner in 2022. You may recall Vivien, have previously been a guest on the podcast.

L-R Matt Woolley, Geof Nightingale, Vivien Lei, Talia Harvey and Nigel Jemson

Now, this was a fascinating panel discussion conducted under Chatham House rules, focusing on the scale of fiscal challenges for the next few decades and how could we meet those? Does this mean for example, some new taxes might be required such as capital gains tax? What about boosting Inland Revenue’s investigation efforts? And then on the spending side of the equation what do we do about rising health care and superannuation costs? Do we perhaps increase the age for eligibility or (re)introduce some forms of mean testing for New Zealand Superannuation? All these points were raised for discussion.

The panel discussed ‘the tax gap’, the gap between what we think the tax collection should be and what’s not being collected. There’s a lot of work to be done in this space, because we really don’t have a clear handle on the extent of this particular issue. Some work carried out several years ago by Inland Revenue suggested that when you look at the consumption patterns between self-employed persons and employees, there might be as much as a 20% gap. In other words, self-employed people appear to have about 20% higher levels of consumption than employees on ostensibly similar levels of income. This is a topic which actually might be worth a podcast episode in itself.

And the finalists are…

It was then followed by the announcement of the four finalists of this year’s Tax Policy Charitable Trust scholarship prize. Every two years the Tax Policy Charitable Trust invites young professionals (anyone under 35 on 1 January 2024) to submit proposals for review, improving any aspect of New Zealand’s tax system. Entrants submit a 1500 word overview proposal on any part of the tax system from which the judges choose four finalists will be selected to go through for the final main scholarship prize, which is worth $10,000.

Submissions are judged for their creativity, original thinking and sound and reasoned research and analysis. In addition the judges take the following factors into consideration:

Impact on the New Zealand economy, including GDP and business growth.

Social (including distributional equity) and environmental acceptability.

Feasibility of introduction, including political and public acceptability.

Impact on simplicity of tax system.

Ease of administration by taxpayers and Inland Revenue, or other relevant government agencies, and impact on compliance costs.

This year, there were 17 entrants and the four finalists chosen are

Matthew Handford, who proposes an Independent Tax Law Commission aimed at improving the Generic Tax Policy Process, or GTPP. The GTPP is a cornerstone of tax policy and is internationally well regarded, but it’s now 30 years old, so is due a reconsideration. I look forward to hearing more about Matthew’s proposal.

Claudia Siriwardena, who is suggesting a simplified FBT regime for small and medium enterprises. This gets a big tick from me, and I’m very interested in hearing more about this one.

Matthew Seddon, who proposes extending the independent contractor withholding tax regime. Mathew’s suggestion picks up the point just raised about the tax gap and deals with it by improving compliance. Again, another interesting proposal.

Finally, Andrew Paynter who is putting forward a proposal to increase the GST rate from GST but also tackle the regressivity of GST with a rebate for low and middle income earners. I’ve seen some international papers on this particular topic, so I’m very, very interested to hear more about what Andrew’s proposing here.

My intention is to get all four scholarship finalists on the podcast to talk about their ideas before the winner is announced in October, so stay tuned for developments. In the meantime, congratulations to Matthew, Claudia, Matthew and Andrew and to everyone else who entered. No doubt there were some interesting ideas put forward that did make the cut this time, but overall, it’s a great sign of the healthy state of tax policy debate in New Zealand.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

(Originally loaded to Soundcloud 6 July 2024. On interest.co.nz 8 July 2024).

The aim is to develop a corporate tax database which is going to be available to tax policy researchers and policy makers about corporate tax rates, effective tax rates, tax incentives for research and development and other topics such as withholding taxes. Increasingly, the amount of information includes anonymised and aggregated country by country reporting data, which provides an overview of the global tax and economic activities of thousands of large multinational enterprises operating worldwide. This year’s report covers 8000 such enterprises.

The detailed statistics in the report are mostly from the 2021 calendar year although some 2022 data is included. The report does take into account the statutory tax rates currently in force.

Increased country by country reporting and more reporting generally is part of the 15 actions within BEPS. The report sets out why this is important:

“Action 11 noted the lack of available and high-quality data on corporate taxation is a major limitation to the measurement and monitoring of the scale of BEPS and the impact of the measures agreed to be implemented under the OECD/G20 BEPS Project.”

Corporate tax rates are stabilising

The headline summary is that corporate tax revenues remain important, but statutory corporate tax rates as the report are now showing signs of having stabilised after pretty near two decades of decline. During the period between 2000 and 2024 the average statutory tax rate declined from about 28% in 2000 to 21.7% in 2019. However, between 2019 and through to 2024, it has remained relatively stable at a rate of 21.7% in 2019 and 21.1% in 2024. I think stabilisation is a trend that’s going to continue.

Who knows, though, if the possible re-election of Donald Trump may change this. But I think governments balance sheets worldwide have been weakened considerably by the double whammy of the Global Financial Crisis and then the pandemic. I therefore think the opportunities to actually cut corporate tax rates further are quite limited, but we shall see.

Just to put New Zealand in context, back in 2000, our corporate tax rate was 33%. With effect from 1st April 2008, it was reduced to 30% and then on 1st April 2011 it was reduced to its current level of 28%. Across the ditch Australia has had a 30% corporate tax rate since 2001.

There’s interesting data about the importance of the corporate tax take. On average for the 2021 year, which was also a pandemic affected year, corporate tax revenue represented 16% of all tax revenues. New Zealand is in line with that average, but as a percentage of GDP, the OECD average was 3.3% whereas here it was considerably higher at 5.7%.

The report also considers effective average tax rates (EATRs) and examines the effect of tax incentives such as more generous tax depreciation compared with true economic deprecation. Again, according to the report effective average tax rates have remained relatively stable falling slightly from 20.9% in 2019 to 20.2% in 2023. Median effective average tax rates were 22.8% in 2019 and practically unchanged at 22.7% in 2023. Meanwhile, New Zealand’s effective marginal effective average tax rate is still relatively close to our statutory tax rate of 28%.

But…a narrowing tax base?

Chapter 4 of the report discusses effective and marginal tax rates and has some interesting commentary around declines of effective marginal tax rates (EMTRs). The report notes

“The stability of EATRs combined with declines in EMTRs suggests a narrowing of tax bases in the sample, notably through an increase in the generosity of depreciation provisions. Examining the asset breakdown shows these trends have been driven by increased generosity of depreciation of tangible and intangible assets, as opposed to buildings and inventories.”

I think some of this might be part of the response to the pandemic. New Zealand is noted being alongside Argentina, Japan, Papua New Guinea and Peru as having a higher effective marginal tax rate because we’ve got less generous depreciation rules. (This has become more so with the imminent withdrawal of building depreciation).

Research and development incentives

Chapter 5 looks at tax incentives for research and development, noting that they’ve become more generous over the past 20 years or so. 33 out of 38 OECD jurisdictions offer tax relief from R&D expenditures in 2023, compared with 19 in 2000. New Zealand is one of the new jurisdictions now offering R&D incentives. These are becoming more generous over time.

From a New Zealand perspective, we discuss the importance of R&D in boosting our productivity and we still could do more in that space. I’m inclined to the view I heard recently expressed that it’s better to give a tax incentive for it rather than get involved in the grant process. Because with a grant process, the companies can be restrained in what they have to spend because of the application process. Also, there’s a lot of effort involved with applying grants, less so with an R&D tax incentive, subject to Inland Revenue monitoring.

According to the report the level of direct government funding and tax support for business R&D in 2021 was about .12% of GDP, well below the OECD average of .2 of GDP. So, there’s still room for improvement although that’s something that’s been acknowledged across the board.

Chapter 6 looks at BEPS actions and notes that there’s a large number of controlled foreign corporation or control foreign company rules with apparently 53 jurisdictions having it in place in 2024. There’s also growth in the use of interest limitation rules. This is part of a growing trend in tax policy around the world to consider imposing restrictions on the deductibility of interest. Apparently, there are now over 100 interest limitation rules in place up from 67 jurisdictions back in 2019.

The dangers of following Ireland’s example

Chapter 7 has a breakdown of country by country reporting statistics with 52 jurisdictions out of a possible 101 submitting statistics to the OECD. As I mentioned earlier, this report includes the activities of over 8000 multinationals so there’s a lot of detail in here.

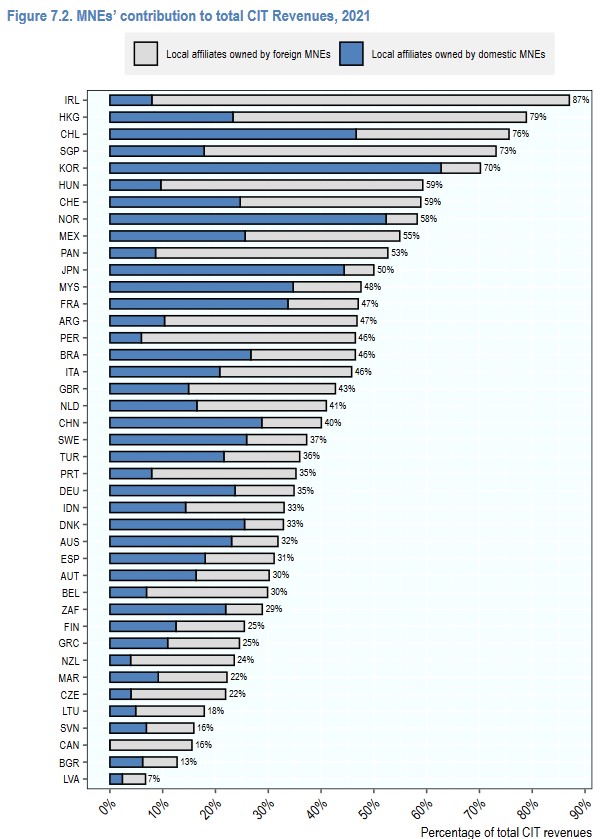

Several commentators including the New Zealand Initiative have recently mentioned Ireland as a potential model to follow. As is well known, Ireland has a very low corporate tax rate. I was therefore very intrigued by figure 7.2 on page 81 of the report, which illustrates the multinational enterprises contribution to local corporate income tax revenues in 2020.

As can be seen, 87% of Ireland’s corporate tax came from multinationals, and the vast majority of those multinationals were local affiliates owned by foreign multinationals. In fact, the Irish Treasury and the European Commission have expressed concern about the sustainability of Ireland’s corporate tax revenue because of the dependency on a few large multinationals.

New Zealand is near the opposite end of the scale with only 24% of corporate tax revenue coming from multinationals, probably three-quarters of which look to be from overseas owned. I think this is an extremely interesting stat which makes me wonder about whether New Zealand is attracting enough investment and whether we should have more multinationals of our own based overseas.

Yes, but is BEPS working?

In summarising key insights on BEPS from the Country by Country Report data the report makes this observation”

“There is evidence of misalignment between the location where profits are reported and the location where economic activities occur. The data show continuing differences in the distribution across jurisdiction groups of employees, tangible assets, and profits.” [page 87]

In other words, the report is basically saying there appears to be some profit shifting going on, but we don’t quite know enough about it. This gets to the heart of the idea behind the BEPS initiative, find out more about what’s happening and then fix it.

As I said the OECD’s corporate database is constantly being expanded so if you’re a bit of a stats guru there’s plenty to dive into and research. Overall, another interesting report highlighting how New Zealand’s corporate tax rate is at the higher end, but noting it also raises a lot of revenue relative to other jurisdictions.

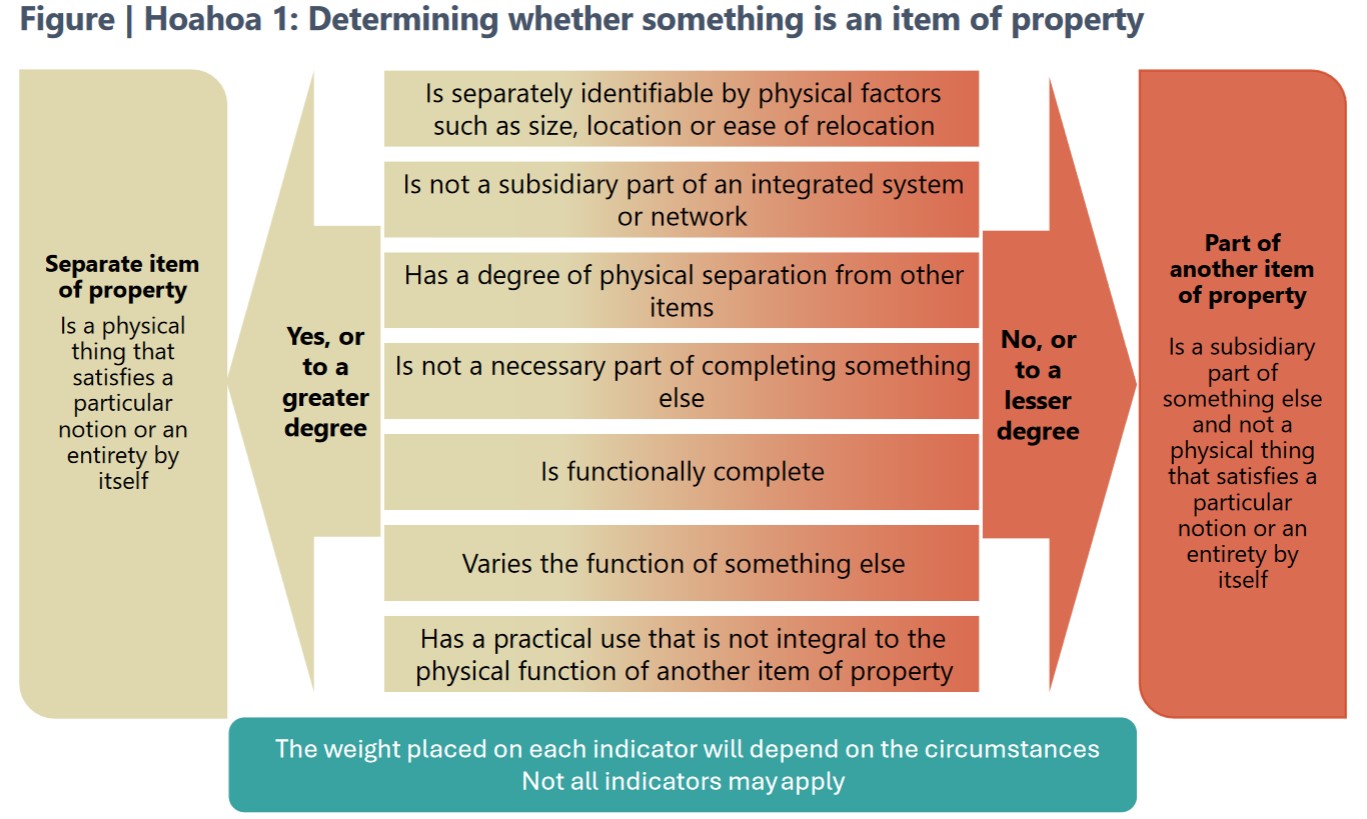

Is that asset depreciable?

Moving on and picking up on depreciation one of the issues covered by the OECD stats, Inland Revenue has just released a draft interpretation statement for comment on identifying the relative relevant item or property for depreciation purposes. This is quite important because our depreciation regime is extremely detailed with a myriad of available rates across several categories.

This draft ties into several other related items of guidance such as residential rental properties depreciation, the question of deductibility of repairs and maintenance – if expenses are not deductible are they depreciable instead? There’s also QB 20/01 – can owners of existing residential parental properties claim deductions for costs incurred to meet healthy home standards? And finally, Interpretation Statement IS 22/04 relating to claiming depreciation on buildings. The imminent withdrawal (again) of building depreciation makes it very important now to maximise depreciation and to identify whether in fact that asset is part of the building or can be claimed separately. This draft is therefore pretty relevant.

The draft runs to 40 pages the last 15 or so pages of which are examples. There’s also a useful 6 page fact sheet accompanying it. Submissions are open until 29th August.

A post-hibernation bear is hungry…

Finally, as we discussed last week, one of the things that came out of Inland Revenue’s recent performance improvement review was for it to be more prominent in promoting what actions it has taken against non-compliant taxpayers. We’re seeing more of that this week when Inland Revenue was announced that an Auckland couple have been sentenced to three years in prison on tax evasion charges. The pair committed 69 tax related offences involving income tax and GST evasion amounting to about $750,000, together with another $80,000 in unaccounted for PAYE. The judge described it as very deliberate offending including deliberate under reporting of business income filing false returns, and even failing to file false returns once under investigation. The couple withheld information from their accountants and concealed the existence of what were described as “highly relevant bank accounts.” So pretty clear case here of tax evasion.

One thing of note that does slightly concern me is this offending occurred over a six year period between 2010 and 2015. That’s quite some time ago and I think Inland Revenue is much more on the case now. Even so you would hope that it doesn’t take 7-8 years or more to bring people to justice on this in the future.

The taxman cometh…

For an idea of how Inland Revenue’s increased activities might play out for your average person, this week’s episode of RNZ’s podcast The Detail discussed how Inland Revenue plans to utilise its additional funding. The episode focuses on the construction industry because of the sector’s long association with the proliferation of the “cashie”. Inland Revenue apparently gets 7,000 anonymous tip offs a year, many of which relate to tradies.

There’s some very interesting commentary from Malcolm Fleming, the New Zealand Certified Builders Association chief executive. He rightly points the finger back at the public for this issue. As he notes, nobody asks their accountant or lawyer ‘Well, how much is it for cash?’ On the other hand, the public seems to be happy to try this tactic with builders and others in the construction industry. On the question of tax evasion and cashies, maybe quite a few people should be looking in the mirror about that rather than pointing the finger elsewhere. It’s a very valid point.

The episode is well worth a listen; it highlights more of what Inland Revenue is currently doing. It’s now doing unannounced site visits to construction sites, for example, which I’m sure would alarm some businesses. But to be fair it also points out most small businesses are run on the straight and narrow. They are perhaps poorly capitalised with overworked owners who are also the main administrator. In many cases the question of tax arrears is more one of poor administration rather than in the case of the couple who were jailed, deliberate malfeasance.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.